ukraine inthe world 2013

DESCRIPTION

This publication describes the indices/rankings that are most reputable and quoted in UkraineTRANSCRIPT

The Foundation established in 2007 to develop and implement projects and programs focused on the long-term development of the Ukrainian economy and to further public debate on the most important economic challenges facing Ukraine. FEG is a nonprofit, independent organization serving the interests of Ukrainian citizens.

FEG’s initiatives are focused on practical results; therefore, it actively cooperates with the government at all levels during the development and realization of its projects and programs.

One of FEG’s fundamental principles is to engage top international experts. Each project is carried out in partnership with leading international organizations that have extensive expertise in solving similar challenges. International experts in close cooperation with Ukrainian specialists directly interact with the appropriate State authorities to take into account the best world practice as well as the features of the Ukrainian economy. After the programmes are approved, the Foundation assists the authorities in implementing the reforms.

The Foundation for Effective Governance is Mr. Rinat Akhmetov’s private initiative; it is his personal contribution to the economic development of Ukraine and the facilitation of systematic dialogue among experts, government, business, civil society organizations, and mass media.The Foundation’s Founder provides financial support, leaving the full independence of actions and decisions to the Foundation, within the framework of the existing mission.

FEG official web-site: www.feg.org.ua

Ukraine’s competitiveness portal: www.competitiveukraine.org

Public debates web-site: www.debaty.org

CONTENTS

Introduction ...........................................................................1

Ukraine in 2012 .....................................................................2

I. GEnERAl IndIcES ............................................................7

Global competitiveness Index ................................................8

The World competitiveness Yearbook Ranking ....................14

Ease of doing Business Index ...............................................19

Index of Economic Freedom .................................................24

ІІ. SPEcIAlIzEd IndIcES ..................................................29

Enabling Trade Index............................................................30

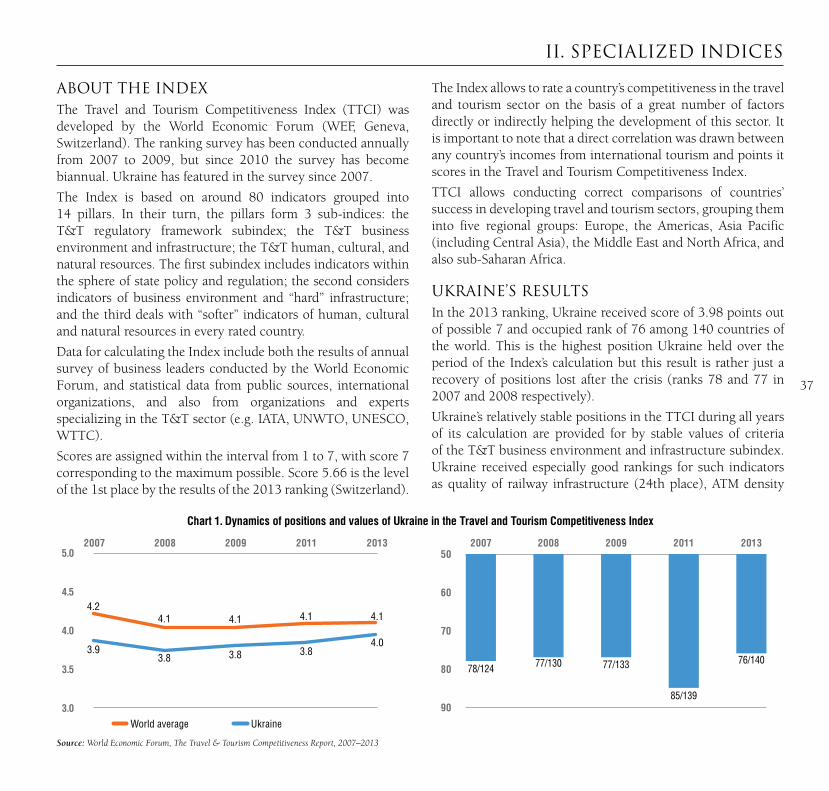

Travel and Tourism competitiveness Index ...........................36

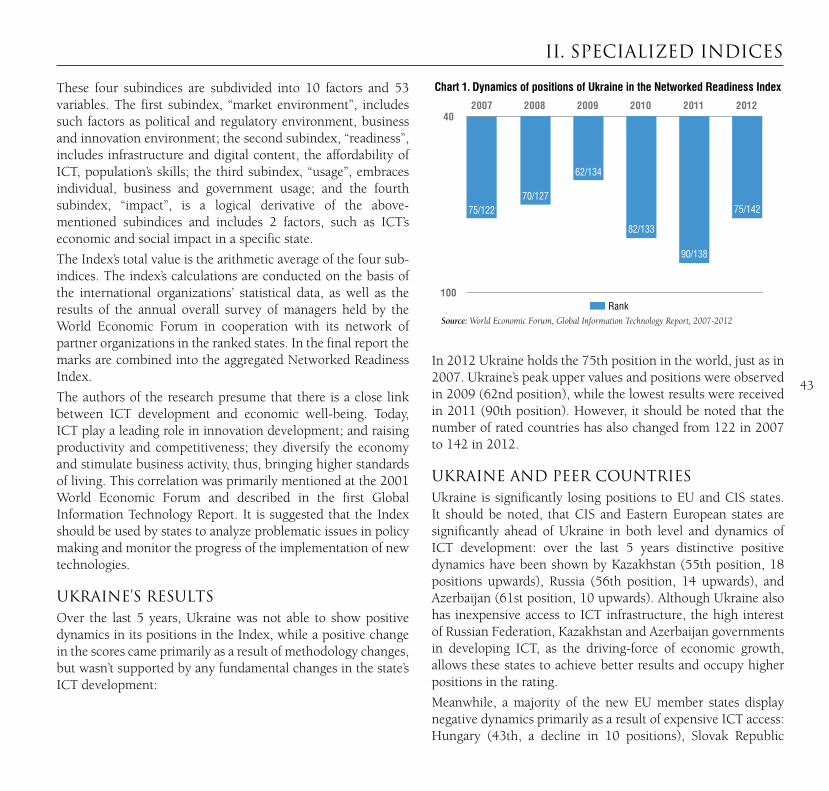

networked Readiness Index .................................................42

ІІІ. SPEcIAl VIEW ..............................................................47

SEdA – Sustainable Economic development Assessment .....48

IV. APPEndIcES ..................................................................53

Graphic Representation of Indices’ Methodology ..................54

list of Abbreviations .............................................................61

61

LiST Of abbrEviaTiONS

iNdiCESGcI Global competitiveness Index lPI logistics Performance Index nRI networked Readiness IndexSEdA Sustainable Economic development Assessment TTcI Travel and Tourism competitiveness Index WcY World competitiveness Yearbook

OrgaNizaTiONS & aSSOCiaTiONS BcG Boston consulting Group cIS commonwealth of Independent States EU European Union IATA International Air Transport AssociationIlO International labour Organization IMd Institute for Management development OEcd Organisation for Economic co-operation and

development Un United nations UncTAd United nations conference on Trade and

developmentUnEScO United nations Educational, Scientific and

cultural Organization UnWTO United nations World Tourism Organization VISA Visa International Service AssociationWB World Bank Wcc World competitiveness center WEF World Economic Forum WTO World Trade Organization WTTc World Travel and Tourism council

TErmSASA Air service agreementATM Automated teller machineFdI Foreign direct investmentsGdP Gross domestic product GnP Gross national product IcT Information and communication technologies T&T Travel and tourism sector2G / 3G Second- / Third generation wireless telephone

technology

1

IntroductIon

there are many various indices and rankings in the world today: global and local, comprehensive and specialized,

regular and one-off. These indices measure various spheres, processes and phenomena in countries, regions, or cities. However, as a result, they all evaluate the successfulness of a specific state, region, or city in comparison with its “competitors” also fighting for limited resources: the money of buyers on world markets, investments, business production capacities, talented specialists, in the end. To put it simply, the higher a country’s position in the ranking, the more successful it is in the potential fight for a certain resource. Most indices are public, and their results are available to anyone. This makes them an attractive tool for the analysis and executive decisionmaking, including at a state level. The most important stages of the algorhythm for the “safe” application of such tool are:

1) Understanding the essence of the index: what it measures and evaluates and why;

2) Understanding the methodology: which indicators are used for the evaluation, what are the sources of information, how is the final value of the index calculated;

3) The ability to correctly explain the index’s results: which real processes and phenomena lie behind specific indicators/groups of indicators, what correlation is there between specific indicators, what kind of comparison with other countries (regions) is justified and objective;

4) The ability to determine priorities and arrive at correct decisions “here and now”: which of the index’s results are essential to a given country (region) at the moment, where should imited resources be applied in order to achieve the best result, which is measured by the improvement of indicators in the index and getting higher ranks compared to other states.

Violating this algorhythm results in false evaluations and, what is worse, wrong decisions, the price of which might be too high.

Over the last years, different international indices/rankings have been obtaining more and more attention in Ukraine.

However, their use as a tool for making and implementing of decisions would be far more effective if users would know how to read indices correctly, how to interprete and apply indices’ results. The main objective of this publication is to raise the level of understanding the methodology of the indices that are most important to the country and to broaden the opportunities for use of their results. This digest doesn’t contain recommendations, but presents objective information on the reasons of Ukraine’s positioning in selected indices by highlighting country’s competitive advantages and restraining factors. This information should be useful for making grounded decisions and developing economic programs for the country.

This publication describes the indices/rankings that are most reputable and quoted in Ukraine, such as:

• The Global Competitiveness Index by the World Economic Forum

• The World Competitiveness Yearbook by the Institute for Management Development

• The Doing Business Report by the World Bank

• The Index of Economic Freedom by The Heritage Foundation in partnership with The Wall Street Journal

IntroductIon

2

uKrAInE’S ProFILE

Within two years (2011-2012), Ukraine has improved its result in the Global Competitiveness Index (GCI) by the

World Economic Forum by 16 positions, moving up to the 73rd position among 144 states, which is practically the pre-crisis level of 2008 (72nd).

Within tWo years, Ukraine has “Won” 20 positions back from rUssia , thUs narroWing the gap betWeen them to six slots in the gci ranking. among its closest neighbors, Ukraine sUrpassed romania and croatia.

Taking over higher positions in the GCI ranking was accompanied by a breakthrough in the World Bank’s Ease of Doing Business Index: the country moved 15 slots upwards in the ranking among 185 world countries having reached its best position over the last 6 years. Such results certify that doing business in the state becomes easier and national economy’s competitiveness, provided by business, is rising.

At the same time, during the last years Ukraine held 56–57 positions out of 60 states (mostly European) in the World Competitiveness Yearbook (WCY) ranking by the Institute for Management Development (Lausanne, Switzerland), not being able to recover its 46th position, lost in result of the crisis, although it lifted to 49th in 2013.

Ukraine loses 48 places to the Wci index’s leader (Usa) and Wins 11 places from the oUtsider (VenezUela). in addition, the state loses 7 positions to rUssia.

On the other hand, the country constantly earns low marks in the Index of Economic Freedom prepared since 1995 by The Heritage Foundation in partnership with The Wall Street Journal. Over the last 6 years, Ukraine has lost 28 positions in the ranking of 177 countries and, with the worst result in Europe, moved to position 161: from the category of “mostly

not free” to “repressed” states. In accordance with the Index methodology, this confirms the fact that business has begun to experience additional activity limitations.

The clue to seemingly obvious contradictions in evaluations and rankings is practically on the surface: this is the interpretation of international indices, each with its own peculiarities first of all in the methodologies of calculation and ranges of ranked components. Only the understanding of the methodology of a certain index and its correct interpretation allows one to see the real picture and determine the spheres of possible practical application of the gained results. At the same time one should remember that loss of a ranking’s positions does not often mean worsening of the state’s scores – other states can just be faster in improving of their results.

The Global Competitiveness Index by the WEF consists of twelve groups of indicators of various importance depending on the stage of economic development of a particular state. Two-thirds of the indicators are the results of executives’ opinion

uKrAInE In 2012

2007

1

185

46/55

135/157

139/178

134/157

145/181 153/179

142/183

163/179

145/183

163/179

152/183

163/179

137/185

73/131 72/13482/133 89/139 82/142

73/144

54/55 56/57 57/58 57/59 56/59

2008 2009 2010 2011 2012

World Competitiveness Yearbook (IMD)Global Competitiveness Index (WEF)Ease of Doing Business Index (The World Bank)Index of Economic Freedom (The Heritage Foundation)

Chart 1. The dynamics of Ukraine’s positions’ in the selected indices

Source: Institute for Management Development, The World Competitiveness Yearbook, 2007-2012; World Economic Forum, The Global Competitiveness Report, 2007-2012; The World Bank, The Doing Business Report, 2007-2012; The Heritage Foundation in partnership with The Wall Street Journal, Index of Economic Freedom, 2007-2012

3

uKrAInE’S ProFILE

survey, and just one-third comes from statistic data. Ukraine has improved its positions in the GCI during the last two years mostly because of the stabilization of economy performance and recovery after a critical downturn as a result of the 2008-2009 global financial crisis, as well as higher scores for infrastructure resulting from the large-scale preparation campaign for the Euro-2012 Football Championship finals.

Within tWo years, Ukraine has improVed its macro-economic enVironment score by 1.2 points and Went 40 positions UpWards in the gci ranking Where this factor is inclUded.

On the contrary, two-thirds of the indicators of the World Competitiveness Scorecard by the Institute for Management Development (IMD) are statistics, while the remaining are results from surveying of managers. The index consists of 20 groups of indicators assembled into four categories with a different impact on the final score of the index. The IMD ranking notes a serious decline of Ukraine in two out of the four categories: economy performance and infrastructure. The latter includes scientific infrastructure, public health, and education. Ukraine’s positions in the other two categories of indicators have either remained on the same level or improved insignificantly. At the same time, taking into account the GCI ranking dynamics, Romania is the only state rated in the WCY out of the 16 states,which Ukraine has surpassed in the GCI over the last two years (after three years of systematic downturn). Thus, a sharp rise in one of the rankings does not contradict the possibility of a “stagnation” in the other one, while the difference in Ukraine’s positions as to the individual competitiveness components within the two quoted rankings can be explained by the choice of ranked countries and the final indicators used for their comparison, as well as certain differences in grouping and aggregating the indicators.

The Ease of Doing Business Index by the World Bank analyzes 11 groups of quantitive indicators evaluating the legal acts that regulate activities of small and medium-sized businesses in particular state, hindering or encouraging their development.

In other words, the factors that favour business activity are evaluated, with an emphasis on small and medium-sized business segments. The Index of Economic Freedom, in its turn, analyzes 10 components of economic freedom which, in their aggregate, evaluate the level of national limitations imposed on business, i.e. “hostility” of the environment created by states to boost the unrestricted functioning of companies of any size and activity. In essence, these are two sides of the same coin with different methodology and interpretation of the above

mentioned indices. Thus, it’s quite natural that the state gained ground in doing business, however the “margins of manoeuvre” for business are shrinking. Ukraine’s situation is mirrored by Russia (position 112 in Doing Business, and 139 in Economic Freedom) and China (91 and 136, respectively) for example. However, Belarus is one of the brightest examples: even though it holds a plausible 58th position in Doing Business, it occupies a very low 154th position out of 177 countries concerning Economic Freedom.

20070%

100%

82%

55%

96%

53%

96%

61%

97%

63%

95%

57%

93%

50%

20102008 20112009 2012

World Competitiveness Yearbook (IMD)Global Competitiveness Index (WEF)

Chart 2. The share of states surpassing Ukraine, % of the total number of ranked countries

Source: Calculations by Foundation for Effective Governance based on the sources: Institute for Management Development, The World Competitiveness Yearbook, 2007-2012; World Economic Forum, The Global Competitiveness Report, 2007-2012;

4

uKrAInE’S ProFILE

georgia has demonstrated eqUal sUccess both in simplifying procedUres for condUcting bUsiness and liberation it from VarioUs restrictions: With the 9th and 21st place in doing bUsiness and economic freedom indices, respectiVely.

Thus, it may be concluded that both indices should be considered as a pair: this provides the opportunity to evaluate the actual level of favourability of the national environment for doing business.

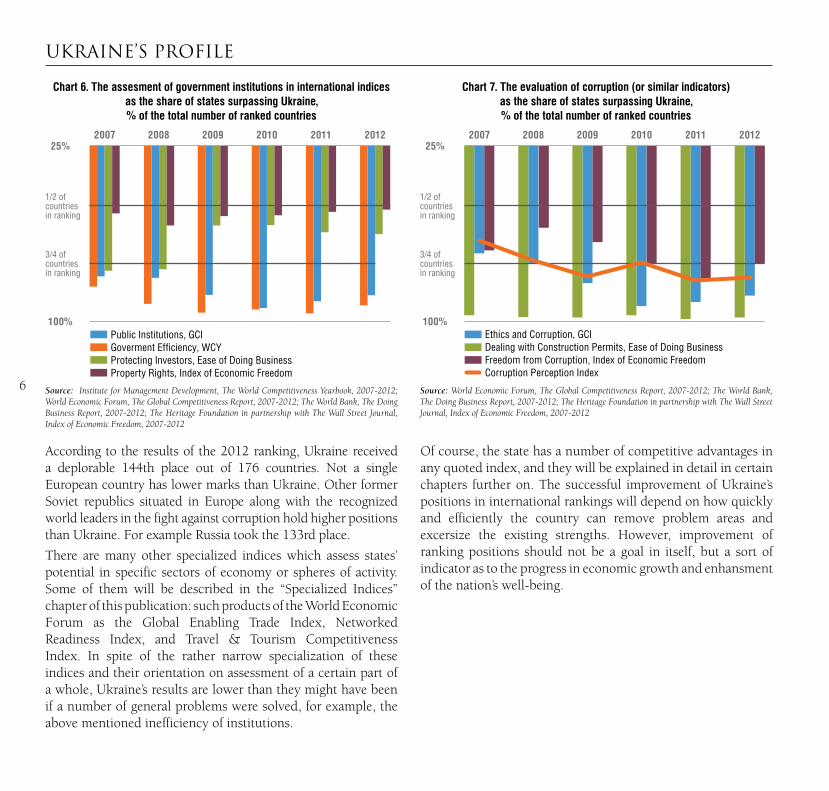

Nonwithstanding the different approaches to data evaluation and index calculation, there are some general trends in Ukraine’s results in economic development, and business as its driver in particular. For example, ineffective functioning of government institutions negatively affects Ukraine’s results in all of the considered indices (see Chart 6). The government institutions include the entire institutional and legislative infrastructure created and administered by the government (as an actor) in order to organize and regulate all the social and economic processes in the society.

Just 15 states including Algeria, Burundi, Chad, and Madagascar, and only Russia among European countries received lower marks for institutions in the GCI ranking.

Chart 3. Ukraine’s positions in comparison to peer countries

World Competitiveness Yearbook (IMD) Global Competitiveness Index (WEF)

1 1

60 14456

48

383432

7367

514341

Kazakhstan Poland Turkey Russia Ukraine Poland Turkey Kazakhstan Russia Ukraine

Source: Institute for Management Development, The World Competitiveness Yearbook, 2007-2012; World Economic Forum, The Global Competitiveness Report, 2007-2012

20070%

100%

20102008 20112009 2012

Ease of Doing Business (The World Bank)Index of Economic Freedom (The Heritage Foundation)

Chart 4. The share of states surpassing Ukraine, % of the total number of ranked countries

Source: The World Bank, The Doing Business Report, 2007-2012; The Heritage Foundation in partnership with The Wall Street Journal, Index of Economic Freedom, 2007-2012

78%85% 85% 85%

91% 91% 91%

80% 77% 79%83%

74%

5

uKrAInE’S ProFILE

Ukraine and rUssia haVe similar problems concerning the efficiency of goVernment and priVate institUtions: the coUntries stand side by side in the gci With most of the indicators in this groUp.

The most problematic issues concern property rights protection, corruption and the inefficiency of bureaucrats. Ukraine displays the same trend for the “government efficiency” component holding a low 56th position out of 59 states in the WCY 2012 ranking. Thereat, while occupying one of the middle places in the ranking (29) as to government finance, Ukraine holds very low positions for institutional infrastructure and legislation regulating business activity (both – 58th place).

Government institutions also determine the level of comfort for business development in a state and, thus, can be one of the factors “attracting” or “scaring off” business activity. Weak protection of investors (property rights) where Ukraine ranks 117th, and complications with obtaining construction permits, where it ranks 183rd out of 185 countries, made weighty contribution to Ukraine’s poor results on Ease of Doing Business.

the only states Where it’s more difficUlt to obtain a constrUction permit than in Ukraine are albania and eritrea (a small coUntry in north-east africa), tWo states Where no legislation at all oUtlines the procedUres of obtaining constrUction permits for priVate companies.

Economic freedom in Ukraine is first of all restricted by corruption (149th position out of 177 countries), high rate of government spending (154th place), problems with doing business (148th place), mostly due to complicated and expensive licensing process, and underdeveloped investment framework (154th place).

Corruption is one of the problematic zones in every abovementioned index. This conclusion is explicitely confirmed by Ukraines’ low marks in the special index calculated by Transparency International, the Corruption Perceptions Index (CPI). This annual ranking of world states has been calculated since 1993, reflecting the perception of the level of corruption by analysts and entrepreneurs . The Index is complex, composed of 13 different expert surveys and entrepreneur opinion polling.

Chart 5. Ukraine’s position in comparison to peer countries

Index of Economic Freedom (The Heritage Foundation) Ease of Doing Business Index (The World Bank)

1

185 185

137

112

91

676558

9

Source: The Heritage Foundation in partnership with The Wall Street Journal, Index of Economic Freedom, 2013; The World Bank, The Doing Business Report, 2012

Georgia Belarus Czech Rep. Azerbaijan China Russia Ukraine1

161154

139136

88

2921

Georgia Czech Rep. Azerbaijan China Russia Belarus Ukraine

6

According to the results of the 2012 ranking, Ukraine received a deplorable 144th place out of 176 countries. Not a single European country has lower marks than Ukraine. Other former Soviet republics situated in Europe along with the recognized world leaders in the fight against corruption hold higher positions than Ukraine. For example Russia took the 133rd place.

There are many other specialized indices which assess states’ potential in specific sectors of economy or spheres of activity. Some of them will be described in the “Specialized Indices” chapter of this publication: such products of the World Economic Forum as the Global Enabling Trade Index, Networked Readiness Index, and Travel & Tourism Competitiveness Index. In spite of the rather narrow specialization of these indices and their orientation on assessment of a certain part of a whole, Ukraine’s results are lower than they might have been if a number of general problems were solved, for example, the above mentioned inefficiency of institutions.

Of course, the state has a number of competitive advantages in any quoted index, and they will be explained in detail in certain chapters further on. The successful improvement of Ukraine’s positions in international rankings will depend on how quickly and efficiently the country can remove problem areas and excersize the existing strengths. However, improvement of ranking positions should not be a goal in itself, but a sort of indicator as to the progress in economic growth and enhansment of the nation’s well-being.

uKrAInE’S ProFILE

200725%

100%

20102008 20112009 2012

Ethics and Corruption, GCIDealing with Construction Permits, Ease of Doing BusinessFreedom from Corruption, Index of Economic FreedomCorruption Perception Index

Chart 7. The evaluation of corruption (or similar indicators) as the share of states surpassing Ukraine, % of the total number of ranked countries

Source: World Economic Forum, The Global Competitiveness Report, 2007-2012; The World Bank, The Doing Business Report, 2007-2012; The Heritage Foundation in partnership with The Wall Street Journal, Index of Economic Freedom, 2007-2012

1/2 of countries in ranking

3/4 of countries in ranking

200725%

100%

20102008 20112009 2012

Public Institutions, GCIGoverment Efficiency, WCYProtecting Investors, Ease of Doing Business Property Rights, Index of Economic Freedom

Chart 6. The assesment of government institutions in international indices as the share of states surpassing Ukraine, % of the total number of ranked countries

Source: Institute for Management Development, The World Competitiveness Yearbook, 2007-2012; World Economic Forum, The Global Competitiveness Report, 2007-2012; The World Bank, The Doing Business Report, 2007-2012; The Heritage Foundation in partnership with The Wall Street Journal, Index of Economic Freedom, 2007-2012

1/2 of countries in ranking

3/4 of countries in ranking

I. GEnErAL IndIcES

8

I. GEnErAL IndIcES

the Global Competitiveness Index (GCI) measures the ability of economies to ensure higher business productivity and, as a

result, higher rates of economic growth, and the nations’ well-being.

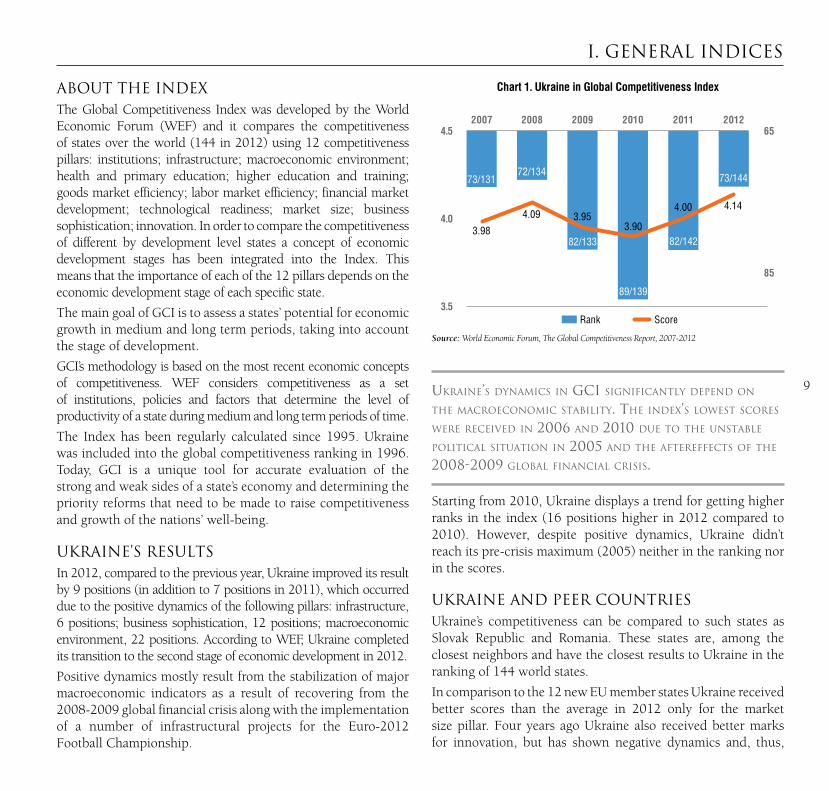

In 2012, Ukraine placed 72nd in the global competitiveness ranking, having improved its result by 9 positions, mostly due to the macroeconomic environment, infrastructure, goods market efficiency, and business sophistication factors. However, in absolute terms, positive dynamics could be observed by all competitiveness pillars.

In spite of GCI’s positive dynamics over the last 3 years, Ukraine wasn’t able to achieve its 2005 maximum (64th position), and only almost attained its pre-crisis 2008 level (72nd position).

Weak institutions, low efficiency of the goods market, and problems concerning financial market development are all the pillars restraining the growth of Ukraine’s competitiveness.

Higher education and training, health and primary education, and market size are the pillars, which still provide Ukraine with competitive advantages.

Compared to other countries, Ukraine’s situation is a lot worse concerning the soundness of banks, efficiency of legal framework in settling disputes, and protection of minority shareholders’ interests. Ukraine is the leader among outsiders as to these components. None of the states compared to Ukraine received worse results. The quality of roads and FDI technology transfer also require considerable improvement.

Lowering the burden of government regulation and raising the independence of the judicial system are priority areas for improving the states’ institutional environment, while providing of fair and free competition is crucial for improving of the goods market efficiency.

Ukraine’s positive dynamics are accompanied by relatively positive dynamics of its closest neighbors. Thus, in order to preserve competitive advantages it is not only important to improve Ukraine’s results, but also to make these adjustments faster than competitors.

Factors facilitating development Score Rank ChangeQuality of railroad infrastructure 4.5 24

Mobile telephone subscriptions/100 pop. 123 43

Secondary education enrollment, gross % 95.6 49

Tertiary education enrollment, gross % 79.5 10

Quality of math and science education 4.6 34

Trade tariffs, % duty 2.9 43

Flexibility of wage determination 5.3 44

Hiring and firing practices 4.9 16

Pay and productivity, 4.5 25

Domestic market size index 4.4 35

Availability of scientists and engineers 4.8 25

Factors restraining development Score Rank ChangeProperty rights 2.7 134

Irregular payments and bribes 2.7 133

Burden of government regulation 2.4 135

Efficiency of legal framework in settling disputes 2.4 141

Protection of minority shareholders’ interests 3 141

Quality of roads 2.3 137

Extent and effect of taxation 1/2 2.3 139

Efficiency of anti-monopoly policy 3.2 132

Burden of customs procedures 2.8 138

Brain drain 2.3 131

Soundness of banks 3.1 142 Source: World Economic Forum, The Global Competitiveness Report, 2011–2012

tHE GLobAL comPEtItIvEnESS IndEx

9

I. GEnErAL IndIcES

About tHE IndExThe Global Competitiveness Index was developed by the World Economic Forum (WEF) and it compares the competitiveness of states over the world (144 in 2012) using 12 competitiveness pillars: institutions; infrastructure; macroeconomic environ ment; health and primary education; higher education and training; goods market efficiency; labor market efficiency; financial market development; technological readiness; market size; business sophistication; innovation. In order to compare the competitiveness of different by development level states a concept of economic development stages has been integrated into the Index. This means that the importance of each of the 12 pillars depends on the economic development stage of each specific state. The main goal of GCI is to assess a states’ potential for economic growth in medium and long term periods, taking into account the stage of development. GCI’s methodology is based on the most recent economic concepts of competitiveness. WEF considers competitiveness as a set of institutions, policies and factors that determine the level of productivity of a state during medium and long term periods of time. The Index has been regularly calculated since 1995. Ukraine was included into the global competitiveness ranking in 1996. Today, GCI is a unique tool for accurate evaluation of the strong and weak sides of a state’s economy and determining the priority reforms that need to be made to raise competitiveness and growth of the nations’ well-being.

uKrAInE’S rESuLtSIn 2012, compared to the previous year, Ukraine improved its result by 9 positions (in addition to 7 positions in 2011), which occurred due to the positive dynamics of the following pillars: infrastructure, 6 positions; business sophistication, 12 positions; macroeconomic environment, 22 positions. According to WEF, Ukraine completed its transition to the second stage of economic development in 2012. Positive dynamics mostly result from the stabilization of major macroeconomic indicators as a result of recovering from the 2008-2009 global financial crisis along with the implementation of a number of infrastructural projects for the Euro-2012 Football Championship.

20074.5

4.0

65

85

3.5

20102008 20112009 2012

Rank Score

Chart 1. Ukraine in Global Competitiveness Index

Source: World Economic Forum, The Global Competitiveness Report, 2007-2012

73/131

3.98

4.09 3.953.90

4.00 4.14

72/134

82/133

89/139

82/142

73/144

Ukraine’s dynamics in gci significantly depend on the macroeconomic stability. the index’s loWest scores Were receiVed in 2006 and 2010 dUe to the Unstable political sitUation in 2005 and the aftereffects of the 2008-2009 global financial crisis.

Starting from 2010, Ukraine displays a trend for getting higher ranks in the index (16 positions higher in 2012 compared to 2010). However, despite positive dynamics, Ukraine didn’t reach its pre-crisis maximum (2005) neither in the ranking nor in the scores.

uKrAInE And PEEr countrIES Ukraine’s competitiveness can be compared to such states as Slovak Republic and Romania. These states are, among the closest neighbors and have the closest results to Ukraine in the ranking of 144 world states.

In comparison to the 12 new EU member states Ukraine received better scores than the average in 2012 only for the market size pillar. Four years ago Ukraine also received better marks for innovation, but has shown negative dynamics and, thus,

10

I. GEnErAL IndIcES

lost this advantage. The greatest gap concerns technological readiness, and keeps getting bigger in comparison to the pre-crisis period, even in spite of Ukraine’s better scores. This confirms that technologically Eastern European neighbors are developing faster than Ukraine.

Just as before the crisis, Ukraine continues to receive lower marks than the average developed EU countries for all competitiveness pillars. The gaps are relatively narrow, when it comes to macroeconomic environment, labor market efficiency and market size. The gaps are huge in the following pillars: institutions, infrastructure, technological readiness, and innovations.

Comparison to the CIS countries is not so unequivocal: Ukraine is ahead of the average marks of the CIS states as to certain indicators, such as, infrastructure, health and primary education, higher education and training, technological readiness, market size, and innovations. However, looking at most of these indicators, it turns out that it’s not that Ukrainian marks are substantially higher, but the fact that most of the CIS states have received even lower marks.

Ukraine’s scores for institUtions are significantly loWer than eVen the aVerage resUlt of the cis states.

As a result, most of the CIS states are ahead of Ukraine as to global competitiveness index results: Russia (67th position, 4.20 points), Kazakhstan (51st position, 4.41 points), and Azerbaijan (46th position, 4.38 points).

dynAmIcS oF tHE IndEx’S comPonEntSCompared to 2011, Ukraine’s positions improved for 9 out of 12 competitiveness pillars in the global ranking, two pillars got worse, one remained unchanged. Moreover, growth was observed on all pillars in their absolute terms.

The state reached its biggest progress in the ranking as to the following indicators: macroeconomic environment (22 positions up), goods market efficiency (12 positions up) and business sophistication (12 positions up).

The state‘s significant movement upward in the global ranking is first of all due to the post-crisis recovery after one of the most serious downturns in the world. For example, Ukraine went back to the 90th position as to macroeconomic environment which corresponds to the pre-crisis level (91st place). Such results were achieved thanks to efficient inflation control and decreasing budget deficit.

Poland5.0 30

40

50

60

70

80

904.0

4.1

4.2

4.3

4.4

4.5

4.6

4.7

4.8

4.9

Slovak Rep.Turkey UkraineRussia Romania

Rank Score

Chart 2. Ukraine and Peer Countries in the Global Competitiveness Index

Source: World Economic Forum, The Global Competitiveness Report, 2007-2012

41 43

6771 73

78

4.074.144.14

4.20

4.454.46

Ukraine Romania PolandRussia Slovak Rep. Turkey

2007

100

3020102008 20112009 2012

11

I. GEnErAL IndIcES

While the progress of the scores receiVed for sUstainable macroeconomic enVironment looks good, Ukraine’s aggregate pUblic debt greW practically threefold, and the state’s trade balance got significantly Worse.

Large-scale infrastructural projects in connection with the state’s preparation to the Euro-2012 Football Championship finals played a positive role, boosting the improvement of infrastructure scores by 14 positions (65th position in 2012).

Delaying the systemic administrative reform leads to a continuous loss in positions concerning institutions pillar: in comparison with 2008 Ukraine went down by 17 positions, to the extremely low 132nd rank out of 144 world states in 2012.

Ukraine faces problems not only in pUblic institUtions, bUt the priVate too (corporate ethics and accoUntability). the latter’s ranking is extremely loW compared to other states oVer the World.

In the group of efficiency enhancers, there are some particularly alarming negative trends concerning the higher education and training and labor market indicators, where Ukraine is losing its relatively competitive advantages worldwide. Before the crisis the score for labor market efficiency allowed Ukraine to have a certain competitive advantage (if in the top 50 of the world ranking), but in four years time the state lost 8 positions and went down to the 62nd rank. Ukraine still maintains comparatively good positions as to higher education (47th position) due to high quantitative indicators of the secondary and tertiary education enrollment rate.

Ukraine’s ranking for financial market development shows that in spite of the slow recovery it’s still far from stabilization and the pre-crisis level: according to the 2012 results, there is still a difference of 29 positions.

the financial market deVelopment pillar displays a Very sloW rate of recoVery after the crisis: jUst 5 positions oUt of the 34 lost.

Ukraine’s decline by 13 positions in the world ranking as to the innovation and sophistication factors compared to the pre-crisis period results from the loss of 11 positions for the business sophistication pillar and 19 positions for the innovation pillar. Thus, the innovation pillar is no longer on the list of the state’s relatively competitive advantages.

2007

20

140

120

100

80

60

40

2008 2009 2010 2011 2012

InstitutionsInfrastructureMacroeconomic environmentHealth and primary educationHigher education and trainingGoods market efficiency

Labour market efficiencyFinancial market developmentMarket sizeBusiness sophisticationInnovation

Chart 3. Dynamics of Ukraine’s Results by the Components of the Global Competitiveness Index

Source: World Economic Forum, The Global Competitiveness Report, 2007-2012

12

I. GEnErAL IndIcES

Index results indicate, that Ukraine’s growth in the ranking is generally of extensive, rather than intensive nature, which is first of all connected to the post-crisis stabilization, and is not a result of productivity growth or improvement of the efficiency of market economy tools. Compared to other states, Ukraine’s competitive advantages still concern components of human resources: health and primary education, higher education and training, and market size. These are the pillars, where Ukraine’s average scores are higher than the world average.

comPEtItIvE AdvAntAGES And rEStrAInInG FActorSThe improvement of the infrastructure indicator was one of Ukraine’s biggest breakthroughs over the last two years. The biggest growth was observed as to the quality of infrastructure in general (30 positions increase in the world since 2008), the quality of air transport infrastructure (20 positions upward), quality and accessibility of port infrastructure (12 positions upward). At the same time, the quality of roads indicator keeps deteriorating systematically: 17 positions were lost over the last four years leaving Ukraine on the very low 137th position in the world. Such a disproportion is a serious obstacle to the creation of an efficient transport network and the realization of the country’s logistics capacity.

In comparison to 2008, Ukraine lost 17 positions for the institutions pillar and occupies an extremely low position (132nd out of 144 world states). The most critical indicators are as follows: property rights (134th position, 16 positions lost within four years); irregular payments and bribes (133rd position), judicial independence (124th position); reliability of police services (123rd position). The low general ranking of the government’s work brought Ukraine to the last ten states of the world in this group of indicators: for instance, Ukraine has lost 44 positions over the last four years for the burden of government regulation indicator.

the ineffectiVeness of institUtions creates serioUs obstacles for bUsiness actiVity. that’s What index resUlts indicate: property rights are not protected by either legislation or laW coUrts; excessiVe regUlation and corrUption mean higher spending, While loW corporate ethics don’t alloW bUsiness to reach neW leVels of sophistication.

While showing relatively high indicators as to secondary education enrollment rate (49th position) and the higher education enrollment rate (10th position), Ukraine systematically loses positions as to the quality of education. This first of all concerns the general ranking of the quality of educational system (70th position, 30 positions lost in 4 years); and the quality of on-the-job training (117th position). There are two major reasons for this: 1) business is not satisfied with the quality of the skills and knowledge of employees; 2) the system trains specialists that don’t correspond to business requirements.

there is no system for training a neW generation of managers in Ukraine, Which resUlts in the 117th position in the World ranking as to the qUality of management schools indicator. along With bad indicators as to brain drain, this resUlts in the problem of bUsinesses hiring necessary specialists from abroad.

Despite retaining a number of relative competitive advantages on labor market flexibility indicators, significant deterioration is observed concerning cooperation in labor-employer relations and in burdensome taxation. The brain drain indicator has reached a critically low level (2.28 points out of 7 possible); Ukraine occupies 131st position out of 144 world rated states.

Ukraine’s private sector experiences a serious deficit of financial resources. Business set an extremely low score for

13

I. GEnErAL IndIcES

the possibility of obtaining financial resources, both directly through the banking system (107th position) and the securities market (129th position). Ukraine is below the limit of the first hundred out of the world ranking as to the availability of venture financing: this certifies startup launching difficulties and the problems of new technology development projects. The low FDI and technology transfer indicator does not facilitate firm-level technology absorption either: Ukraine occupies a low 109th position in the world. This indicator is part of the technological readiness pillar, where Ukraine generally loses 16 positions in the world compared to its pre-crisis level of economic development.

14

I. GEnErAL IndIcES

the World Competitiveness Yearbook (WCY) rates and analyzes the ability of countries to create and sustain an

environment stimulating the efficient competitiveness of businesses.

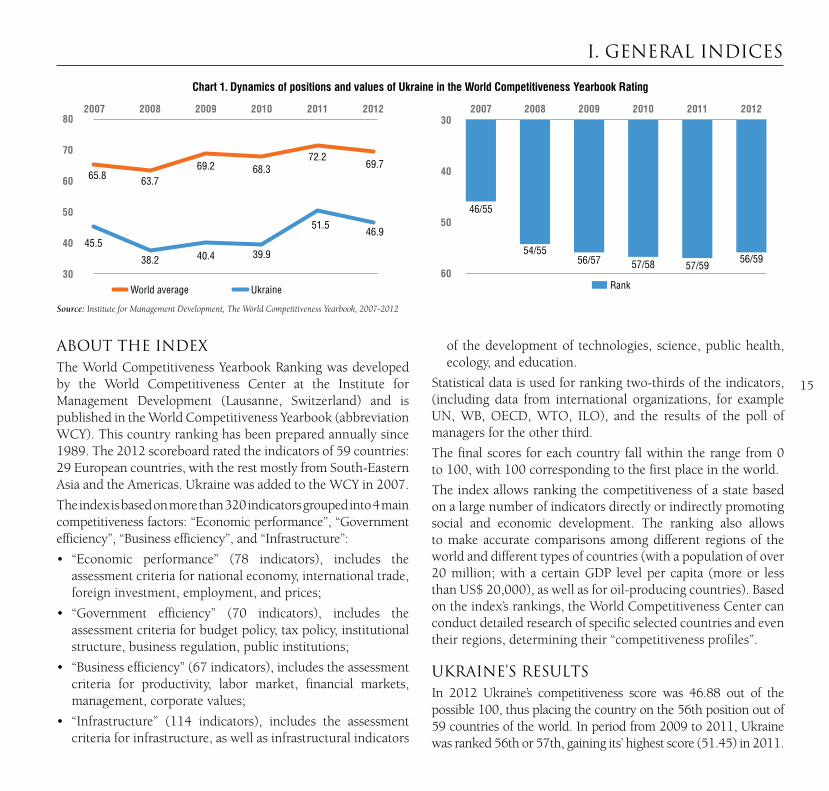

According to the World Competitiveness Yearbook, Ukraine’s positions in the ranking have been relatively stable over the last 5 years (Ukraine was ranked 54-57, holding the 56th position in the 2012 scoreboard) At the same time, the competiveness rate of the countries compared to Ukraine during this period has grown while the scores for constant ranges of positions in the world ranking continue to increase. Thus, the competitive advantages of the comparable countries are growing, while Ukraine remains on the same position.

Moreover, the value of a large number of indicators, connected with Ukraine’s investment attractiveness and the creation of high-tech products, which to a great extent determine the long-term prospects of the country’s competitiveness in the world, has decreased. So far, the relatively competitive areas of Ukraine’s economy are the labor market (workforce cost and skills); education (mostly numerical indicators, especially, education enrollment rate and the level of budget allocations); and the public finance management system (state debt and budget deficit management). Relatively successful measures of budget stabilization do not guarantee long-term success, because Ukraine’s economy remains non-diversified, energy-consuming, and, as a result, vulnerable to exogenous factors, such as financial crises or even simply price fluctuations on commodities and energy market. Indicators measuring the efficiency of state institutions also need significant improvement (first of all, a judicial reform and fight against corruption program, as well as intellectual property protection) as they are cornerstone elements of the business activity environment defining its productivity and, consequently, the level of the nation’s well-being.

Factors facilitating development RankTerms of trade index 6Real GDP and GDP per capita growth, % 9 and 13Direct investment flows inward 12Trade to GDP ratio 21Gini index 8Tariff barriers 8Employee’s social security contribution rate, % from GDP per person 13Remuneration for managers / services professions 4Need for economic and social reforms 15Fixed broadband tariffs, US$ per month 3Mobile telephone costs, US$ per minute 3Total public expenditure on education, % of GDP 4

Factors restraining development RankResilience of the economy 57GDP per capita (in real and PPP prices), US$ per person 56 and 55Diversification of the economy 55Real corporate taxes 59Country credit rating 58Competition legislation 58Justice 58Bribing and corruption 58Investment risk (by Euromoney) 59Shareholders’ rights 59Health, safety & environment concerns 59Social responsibility 58Energy intensity (of GDP, kJ/US$1) 59Intellectual property rights 58Quality of life 58Source: Institute for Management Development, The World Competitiveness Yearbook, 2012

tHE WorLd comPEtItIvEnESS yEArbooK rAnKInG

15

I. GEnErAL IndIcES

About tHE IndEx The World Competitiveness Yearbook Ranking was developed by the World Competitiveness Center at the Institute for Management Development (Lausanne, Switzerland) and is published in the World Competitiveness Yearbook (abbreviation WCY). This country ranking has been prepared annually since 1989. The 2012 scoreboard rated the indicators of 59 countries: 29 European countries, with the rest mostly from South-Eastern Asia and the Americas. Ukraine was added to the WCY in 2007.

The index is based on more than 320 indicators grouped into 4 main competitiveness factors: “Economic performance”, “Government efficiency”, “Business efficiency”, and “Infrastructure”:

• “Economic performance” (78 indicators), includes the assessment criteria for national economy, international trade, foreign investment, employment, and prices;

• “Government efficiency” (70 indicators), includes the assessment criteria for budget policy, tax policy, institutional structure, business regulation, public institutions;

• “Business efficiency” (67 indicators), includes the assessment criteria for productivity, labor market, financial markets, management, corporate values;

• “Infrastructure” (114 indicators), includes the assessment criteria for infrastructure, as well as infrastructural indicators

of the development of technologies, science, public health, ecology, and education.

Statistical data is used for ranking two-thirds of the indicators, (including data from international organizations, for example UN, WB, OECD, WTO, ILO), and the results of the poll of managers for the other third. The final scores for each country fall within the range from 0 to 100, with 100 corresponding to the first place in the world. The index allows ranking the competitiveness of a state based on a large number of indicators directly or indirectly promoting social and economic development. The ranking also allows to make accurate comparisons among different regions of the world and different types of countries (with a population of over 20 million; with a certain GDP level per capita (more or less than US$ 20,000), as well as for oil-producing countries). Based on the index’s rankings, the World Competitiveness Center can conduct detailed research of specific selected countries and even their regions, determining their “competitiveness profiles”.

uKrAInE’S rESuLtSIn 2012 Ukraine’s competitiveness score was 46.88 out of the possible 100, thus placing the country on the 56th position out of 59 countries of the world. In period from 2009 to 2011, Ukraine was ranked 56th or 57th, gaining its’ highest score (51.45) in 2011.

Chart 1. Dynamics of positions and values of Ukraine in the World Competitiveness Yearbook Rating

200780

70

60

50

40

30

65.8 63.769.2 68.3

72.269.7

46.951.5

39.940.438.2

45.5

2008 2009 2010 2011 2012

World average Ukraine

Source: Institute for Management Development, The World Competitiveness Yearbook, 2007-2012

200730

40

50

60

20102008 20112009 2012

46/55

54/5556/57 57/58 57/59

56/59

Rank

16

I. GEnErAL IndIcES

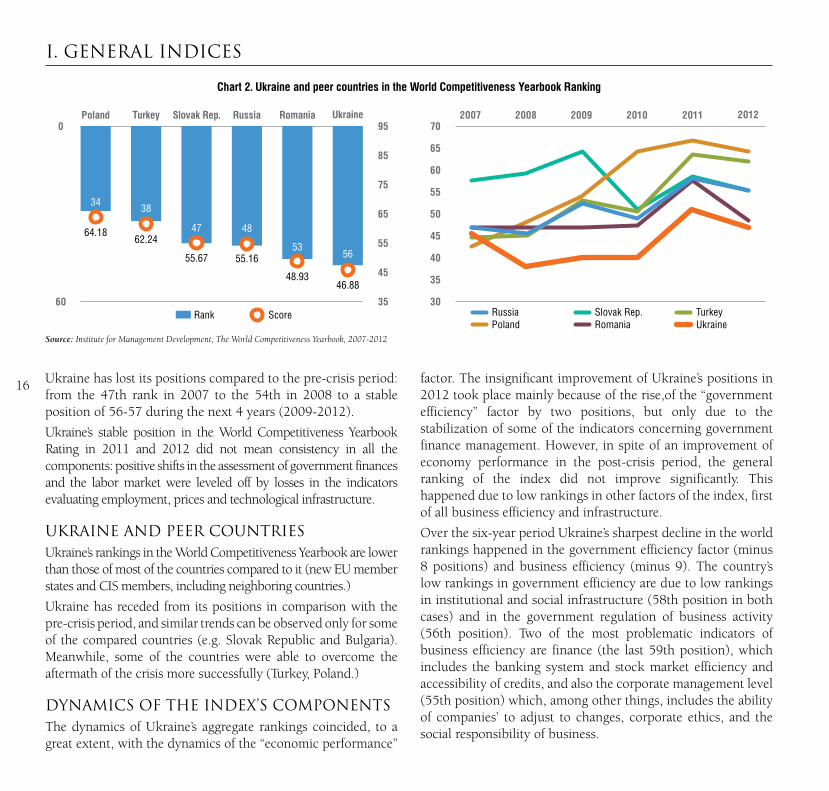

Ukraine has lost its positions compared to the pre-crisis period: from the 47th rank in 2007 to the 54th in 2008 to a stable position of 56-57 during the next 4 years (2009-2012).

Ukraine’s stable position in the World Competitiveness Yearbook Rating in 2011 and 2012 did not mean consistency in all the components: positive shifts in the assessment of government finances and the labor market were leveled off by losses in the indicators evaluating employment, prices and technological infrastructure.

uKrAInE And PEEr countrIES Ukraine’s rankings in the World Competitiveness Yearbook are lower than those of most of the countries compared to it (new EU member states and CIS members, including neighboring countries.)

Ukraine has receded from its positions in comparison with the pre-crisis period, and similar trends can be observed only for some of the compared countries (e.g. Slovak Republic and Bulgaria). Meanwhile, some of the countries were able to overcome the aftermath of the crisis more successfully (Turkey, Poland.)

dynAmIcS oF tHE IndEx’S comPonEntSThe dynamics of Ukraine’s aggregate rankings coincided, to a great extent, with the dynamics of the “economic performance”

factor. The insignificant improvement of Ukraine’s positions in 2012 took place mainly because of the rise,of the “government efficiency” factor by two positions, but only due to the stabilization of some of the indicators concerning government finance management. However, in spite of an improvement of economy performance in the post-crisis period, the general ranking of the index did not improve significantly. This happened due to low rankings in other factors of the index, first of all business efficiency and infrastructure.

Over the six-year period Ukraine’s sharpest decline in the world rankings happened in the government efficiency factor (minus 8 positions) and business efficiency (minus 9). The country’s low rankings in government efficiency are due to low rankings in institutional and social infrastructure (58th position in both cases) and in the government regulation of business activity (56th position). Two of the most problematic indicators of business efficiency are finance (the last 59th position), which includes the banking system and stock market efficiency and accessibility of credits, and also the corporate management level (55th position) which, among other things, includes the ability of companies’ to adjust to changes, corporate ethics, and the social responsibility of business.

Chart 2. Ukraine and peer countries in the World Competitiveness Yearbook Ranking

Source: Institute for Management Development, The World Competitiveness Yearbook, 2007-2012

200770

30

35

40

45

50

55

60

65

20102008 20112009 2012

Russia Slovak Rep. TurkeyPoland Romania Ukraine

Poland0 95

85

75

65

55

35

45

60

RussiaTurkey RomaniaSlovak Rep. Ukraine

Rank Score

46.88

56

48.93

5355.16

48

55.67

4762.24

3834

64.18

17

I. GEnErAL IndIcES

Chart 3. Dynamics of Ukraine’s results by the components of the World Competitiveness Yearbook Ranking

Source: Institute for Management Development, The World Competitiveness Yearbook, 2007-2012

200770

30

35

40

45

50

55

60

65

20102008 20112009 2012

Competitiveness (overall)Economic PerfomanceGoverment Efficiency

Business EfficiencyInfrastructure

comPEtItIvE AdvAntAGES And rEStrAInInG FActorS According to the results of the World Competitiveness Yearbook 2012, a lot more indicators restrain the growth of Ukraine’s competitiveness, rather than boosting it. For a number of them Ukraine received the worst scores among the ranked selection of countries.

Ukraine’s most problematic areas within the “economic performance” factor are low economic diversification and economy vulnerability to exterior shocks. This was confirmed by one of the worlds’ greatest declines in GDP, as a result of the 2008-2009 crisis. The state is also significantly lagging behind with GDP indicators in nominal and parity prices. Consumer price inflation and the national’ current account deficit are also among Ukraine’s soft spots. The latter has reached its critical level within the last two years, primarily because of significantly higher levels of import over export. The relative growth rate of GDP (according to the 2011 data), in total and per capita, can be considered as one of Ukraine’s advantages. The state also holds a high 6th position in the trade enabling index, which sets the correlation between export and import prices.

the relatiVely high 12th place for the fdi to gdp ratio can be explained by hUge VolUmes of reinVestment into the national economy by Ukrainian companies (Via foreign jUrisdictions).

In spite of going up two positions, “government efficiency” is the weakest factor of Ukraine’s 2012 competitiveness index. The worst situation concerns the indicators obtained from the results of polling business leaders, namely the burden of corporate taxation, competition legislation efficiency, bribery and corruption. The state is either last or second last in accordance with the above mentioned indicators, which certifies about low potential of Ukraine to compete with other countries by business environment. These factors, along with Ukraine’s low credit rating, negatively influence the inflow of investments into the state.

On the other hand, Ukraine received plausible marks for the Gini Index reflecting the inequality of the populations’ income, and for tariff barriers for import. The stabilization of exchange rates and preservation of the state budget deficit within reasonable limits allowed the country to receive good marks for these indicators and join the ranking’s top twenty.

During the last five years, Ukraine has been losing positions in the “business efficiency” factor, which includes indicators of production, labor markets, financial system, corporate management practices and business values. Among the problem zones, once again one can see different aspects of investment activity: business is critical about state investment risks and, in particular, considers that the rights of shareholders’ are left unprotected. At the same time, the effectiveness of financial and banking regulation is ranked very low, while the outflow of valuable human resources significantly complicates the search for high-class specialists. Such so-called “soft” sub-factors, as corporate social responsibility, or concerns about the people’s health and safety, as well as the level of ethical standards in companies, also got very low marks from top managers themselves.

18

I. GEnErAL IndIcES

The general level of remuneration for employees, particularly managers and specialists of service professions, remains a competitive aspect of Ukrainian business. Social factors, such as an average number of working hours per year and the proportion of men and women in the country’s labor force received traditionally high marks.

Ukraine’s has shown the worst dynamics in the competitiveness ranking by its decline in 10 positions (from 41st to 51st place) during the last three years, as to the “infrastructure” factor, which, apart from the traditional transport and energy infrastructure, also includes its technological and scientific components, education, public health and environment. The latter two sub-factors are amid the most problematic aspects constantly bringing the state to last positions in the world ranking.

Ukraine’s gdp is the most energy consUming; climate changes are not on the list of goVernment priorities, and reneWable energy soUrces don’t receiVe the necessary deVelopment and spread. loW scores for medical infrastrUctUre and the high leVel of enVironmental pollUtion are also reflected by the scoreboard.

Meanwhile, Ukraine’s indicators of telecommunication infrastructure costs are among the best in the world, including broadband Internet tariffs and services provided by mobile and fixed-line telephony operators. So far, the country holds the plausible 11th position in the “dependency ratio”, i.e. the group that is in fact provided for by the able-bodied population.

The polling of managers on factors determining the attractiveness of Ukraine’s economy became a by-product of the assessment of state competitiveness all over the world. Respondents were offered to choose 5 variants out of the 15 possible. The polling results correspond to the rating indicators; such as qualified workforce, the high level of education and competitiveness in expenditures (cheap resources and workforce in particular) are the most attractive. The competence level of bureaucrats and efficient legislation were mentioned most seldom.

New World Competitiveness Yearbook 2013 was issued during the final stage of this report preparation. According to estimations of the Institute for Management Development, Ukraine displayed positive competitiveness dynamics, having risen from 56th to 49th place in the world’s ranking. Its scores increased from 46.88 to 54.23. That means Ukraine is generally back to its prerecession positions. Such dynamics is amid the best in the world’s ranking, and moreover corresponds to Ukraine’s improvement in the Global Competitiveness Index 2012-2013 of the WEF (while both indices used data of 2011).

Improvement of positions happened mostly in such factors as “economic performance” (increase from 48th to 30th place) and “infrastructure” (increase from 51st to 45th place), as well as in “business efficiency” (from 55th to 51st place). However, the “government efficiency” position worsened (decrease from 56th to 57th place). Dynamics of these factors is similar to dynamics of the WEF estimations and can be explained by infrastructure projects development during preparation for the Euro-2012 and post-recession economy stabilization.

The “government efficiency” positions fall was seen in majority of former post-soviet and post-socialist countries of the Central and Eastern Europe, which were included in this research. The Institute for Management Development marked significant improvement of general competitiveness ranking of Russia (by 6 positions, up to 42nd place) and stable good results for Poland (33rd place, by 1 position up), which are Ukraine’s neighbors and biggest trade partners.

19

I. GEnErAL IndIcES

the Ease of Doing Business Index provides the accurate measurments of business regulation and its enforcement

across world economies and describes the life cycle of the states’ small and medium businesses, as well as measuring the regulations apllied to them.

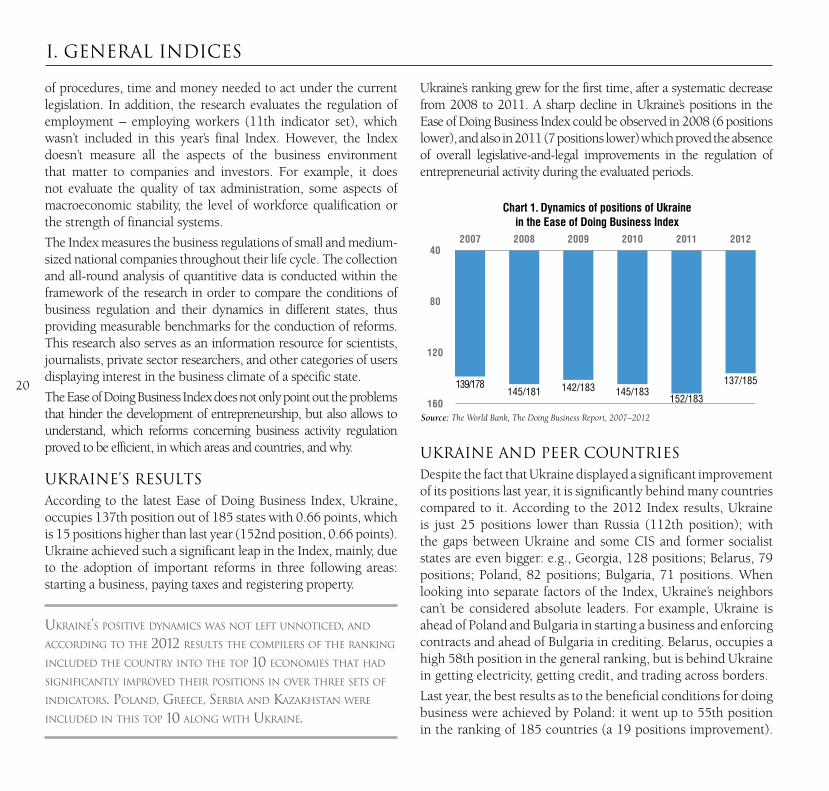

Ukraine occupies the 137th position out of 185 states in the Ease of Doing Business Index 2012, which is 15 positions higher than previous year. The country has recovered the positions it lost in the ranking after the crisis as a result of reforms in three spheres of business regulation. However, in spite of this rise, Ukraine is still behind many countries compared to it, while, for instance, some of Russia’s reforms brought it to the the top of the list of the best world practices of the year. Ukraine’s relatively strong points are Starting a Business, Getting Credit and Enforcing Contracts. However, the major problem factors impeding business development in Ukraine are Dealing with Construction Permits, Getting Electricity, Trading Across Borders, Paying Taxes, Resolving Insolvency and Registering Property.

In order to continue the positive trend in business climate improvement and Ukraine’s further advancement in the Ease of Doing Business Index, it is necessary to decrease the number of days required for starting a business, cut the number of procedures and time for obtaining construction permits, apply the necessary measures to significantly decrease the amount of procedures and time required for getting electricity, as well as guarantee the repayment of the significant funds to creditors in case of the borrowers’ insolvency.

Factors facilitating development Value ChangeThe paid-in minimum capital (for starting a business), percent of gross income per capita

0*

Cost (for starting a business), percent of per capita income 1.5

Strength of legal rights index (10 – best) 9 =The number of procedures for enforcing a contract 30 =Time for enforcing a contract, days 343 =*as in 91 deve lo ped countries

Factors restraining development Value ChangeNumber of procedures for obtaining construction permits 20 =Cost of obtaining construction permits, percent of per capita income

1 262.6

Time for obtaining construction permits, days 375 =Time for registering property, days 69

Time for paying taxes, hours 491

Total tax rate, percentage of profit 55.4

Cost of proceedings for resolving insolvency, percent of estate 42 =Recovery rate for resolving insolvency, cents on the dollar 8.7

Number of procedures for getting electricity 11 =Time for getting electricity, days 285 =Source: The World Bank, The Doing Business Report, 2011–2012

About tHE IndEx The Ease of Doing Business Index is an annual research by the World Bank Group calculated since 2003 and presenting the accurate information necessary for understanding and improving the legal regulation of business activity.

This year’s report (2012) covers 11 indicator sets and 185 world economies. The sets of indicators can be divided into two types: 1) the strength of legal institutions (getting a credit, protecting investors, enforcing contracts, resolving insolvency), and 2) the complexity and cost of regulatory procedures (starting a business, dealing with construction permits, getting electricity, registering property, paying taxes, trading across borders).

Based on specific examples of labor and time spent on doing business, these indicators facilitate the assessment of the amount

EASE oF doInG buSInESS IndEx

20

I. GEnErAL IndIcES

of procedures, time and money needed to act under the current legislation. In addition, the research evaluates the regulation of employment – employing workers (11th indicator set), which wasn’t included in this year’s final Index. However, the Index doesn’t measure all the aspects of the business environment that matter to companies and investors. For example, it does not evaluate the quality of tax administration, some aspects of macroeconomic stability, the level of workforce qualification or the strength of financial systems.

The Index measures the business regulations of small and medium-sized national companies throughout their life cycle. The collection and all-round analysis of quantitive data is conducted within the framework of the research in order to compare the conditions of business regulation and their dynamics in different states, thus providing measurable benchmarks for the conduction of reforms. This research also serves as an information resource for scientists, journalists, private sector researchers, and other categories of users displaying interest in the business climate of a specific state.

The Ease of Doing Business Index does not only point out the problems that hinder the development of entrepreneurship, but also allows to understand, which reforms concerning business activity regulation proved to be efficient, in which areas and countries, and why.

uKrAInE’S rESuLtSAccording to the latest Ease of Doing Business Index, Ukraine, occupies 137th position out of 185 states with 0.66 points, which is 15 positions higher than last year (152nd position, 0.66 points). Ukraine achieved such a significant leap in the Index, mainly, due to the adoption of important reforms in three following areas: starting a business, paying taxes and registering property.

Ukraine’s positiVe dynamics Was not left Unnoticed, and according to the 2012 resUlts the compilers of the ranking inclUded the coUntry into the top 10 economies that had significantly improVed their positions in oVer three sets of indicators. poland, greece, serbia and kazakh stan Were inclUded in this top 10 along With Ukraine.

Ukraine’s ranking grew for the first time, after a systematic decrease from 2008 to 2011. A sharp decline in Ukraine’s positions in the Ease of Doing Business Index could be observed in 2008 (6 positions lower), and also in 2011 (7 positions lower) which proved the absence of overall legislative-and-legal improvements in the regulation of entrepreneurial activity during the evaluated periods.

Chart 1. Dynamics of positions of Ukraine

in the Ease of Doing Business Index

Source: The World Bank, The Doing Business Report, 2007–2012

200740

80

120

160

20102008 20112009 2012

139/178145/181 142/183 145/183

152/183

137/185

uKrAInE And PEEr countrIES Despite the fact that Ukraine displayed a significant improvement of its positions last year, it is significantly behind many countries compared to it. According to the 2012 Index results, Ukraine is just 25 positions lower than Russia (112th position); with the gaps between Ukraine and some CIS and former socialist states are even bigger: e.g., Georgia, 128 positions; Belarus, 79 positions; Poland, 82 positions; Bulgaria, 71 positions. When looking into separate factors of the Index, Ukraine’s neighbors can’t be considered absolute leaders. For example, Ukraine is ahead of Poland and Bulgaria in starting a business and enforcing contracts and ahead of Bulgaria in crediting. Belarus, occupies a high 58th position in the general ranking, but is behind Ukraine in getting electricity, getting credit, and trading across borders.

Last year, the best results as to the beneficial conditions for doing business were achieved by Poland: it went up to 55th position in the ranking of 185 countries (a 19 positions improvement).

21This leap was mostly achieved by the adoption of four institutional and normative-and-legal reforms that simplified and improved the registration of property, tax payment system, contract enforcement, and resolving businesses’ insolvency. However, many of the countries compared to Ukraine display rather negative dynamics: Azerbaijan, 67th position (1 position lower); Bulgaria, 66th (2 positions lower); Hungary, 54th (5 positions lower); Turkey, 71 (3 positions lower). This confirms the absence of change or an insignificant decline in the conditions for entrepreneurial activity.

Compared to other countries, Ukraine’s business activity regulation conditions are similar to Russia’s, both in 2012 and during the last five years: both countries have improved their positions in the ranking by 8 places.

Unlike Ukraine, rUssia Was inclUded into sUccessfUl World practices in the folloWing areas according to the resUlts of the 2012 eValUation: establishing a fixed payment When re-registering property, making oUt-of-coUrt settlements of legal argUments, proViding pUblic access to arbitration decisions.

dynAmIcS oF tHE IndEx’S comPonEntSUkraine’s most problematic indicator sets restraining the deve-lopment of business activity remain: dealing with construction permits (183rd position), getting electricity (166th position), resolving insolvency (157th position), trading across borders (145th position), registering property (149th position), paying taxes (165th position), protecting investors (117th position).

However, last year, when considered by indicator sets, Ukraine achieved its biggest progress in starting a business. A 66 positions improvement brought the state right to the 50th position in the world, due to the cancellation of requirements for paid-in minimum capital, the decrease of time and lower cost necessary for starting a business. The indicator of paying taxes has improved to some extent: 18 positions upwards to the 165th position, due to the simplified process of tax payment, namely the introduction of electronic tax return forms and electronic tax payments for businesses. Additional progress was noted in property registering: a 19 positions improvement, bringing the country to the 149th position, because of a decrease in the number of days necessary for registering property (from 117 to 69).

However, Ukraine is still far behind and displays rather negative dynamics as to the regulation factor. In particular, Ukraine

RussiaUkraine Turkey Azerbaijan Poland Slovak Rep.0

40

80

120

1

0160Rank Score

Chart 1. Ukraine and peer countries in the Ease of Doing Business Index

Source: The World Bank, The Doing Business Report, 2007–2012

200720

180

140

100

60

20102008 20112009 2012

Slovak Rep. Turkey RussiaPoland Ukraine Azerbaijan

137

0.620.55

112

0.45

71

0.45

67

0.41

55

0.39

46

22

I. GEnErAL IndIcES

occupies the 183rd position out of 185 countries in the indicator set concerning issuing construction permits, losing one position within a year due to the increase in the cost of obtaining construction permits procedures.

only tWo coUntries are behind Ukraine in the World ranking as to the indicator of dealing With constrUction permits: albania and eritrea, Where priVate companies cannot receiVe constrUction permits by laW in principle.

A similar negative trend can be observed in protecting investors (117th position) and trading across borders (145th position).

2007

0

180

90

2008 2009 2010 2011 2012

Ease of Doing Business IndexStarting a BusinessDealing with Construction PermitsRegistering PropertyGetting Credit

Protecting InvestorsPaying TaxesTrading Across BordersEnforcing ContractsResolving Insolvency

Chart 3. Dynamics of Ukraine’s results by the components of the Ease of Doing Business Index

Джерело: The World Bank, The Doing Business Report, 2007–2012

comPEtItIvE AdvAntAGES And rEStrAInInG FActorSThe greatest improvement of the situation in the dynamics of specific indicators from 2007 to 2012 concerns starting a business, due to the complete cancellation of paid-in minimum capital for starting a business, decrease in the cost of starting a business (from 7.8 percent of GDP per capita to 1.5 percent), and also because of the decrease in the number of procedures and days necessary for starting a business. Simplifying the process of starting a business encourages the increase in the number of new companies and, as a consequence, the increase of jobs. Taking into account insufficient participation of small and medium-sized enterprises in Ukraine’s GDP, unlike in comparable European countries, such reforms may change this proportion to the better on one hand.

On the other hand, property registering issues remain unsolved. In spite of a significant decrease (practically twice) in the time required for registering a business compared to last years’ Index, Ukraine is still behind 139 countries as to this indicator. The number of procedures required for registering a business remains critically high: 10.

the sitUation With the nUmber of procedUres reqUired for registering property in ten coUntries of the World, mostly africa, and also greece and brazil is similar or eVen Worse than in Ukraine.

The country has once again received the lowest marks for dealing with construction permits and getting electricity: these indicators of the Ease of Doing Business Index bring Ukraine down to the twenty outsiders of the world ranking according to practically all indicators.

sUch a large nUmber of procedUres (11) is reqUired for getting electricity noWhere else in the World. sUch a simple issUe at first glance, may become a rather serioUs obstacle on the Way to the”birth” of small and mediUm-sized enterprises.

23

I. GEnErAL IndIcES

In spite of an almost 14-percent decrease in the relative amount of money a business has to spend on dealing with construction permits, this indicator is “blinking red” in Ukraine, 10 times higher than the level of the 100th position in the ranking, and more than 1000 times bigger than that of Qatar, the world’s leader. Burdensome procedures and high expenses for dealing with construction permits stimulate corruption and “push” construction business into the shade.

The swiftness and low expenditures required to relaunch competitive businesses are among the important specific features of developed economies. Ukraine only occupies the 157th position in resolving the insolvency: the procedures are very time-consuming (2.9 years), and expensive (42 percent of estate) while creditors receive only 9 cents from every dollar of debts.

However, due to a good system of credit information, laws on bankrupcy and surety, Ukraine has been receiving good marks in the strength of legal rights index (9 out of 10 possible) and a high 23rd position in getting credit for two years.

Just like most CIS neighbors, Ukraine receives stable good results in enforcing contracts, which sends the state into the top twenty for the number of required procedures to enforce the fulfillment of contracts through court (30 procedures) and the duration of the entire process (343 days). High results for this indicator build up the entrepreneurs’ confidence as to the fact that legislation protects their interests in business relations with partners.

The evaluation of Ukraine’s taxation system is similarly stable, but negative. A large number of taxes and payments to the national budget (28) in total make up 55.4 percent of the profits of an average manufacturing company. Thus, the companies are obliged to spend a lot more time observing all the formalities, when paying taxes.

24

I. GEnErAL IndIcES

the Index of Economic Freedom published by The Heritage Foundation in partnership with The Wall Street Journal

evaluates the level of liberalization concerning the interaction between states and businesses, taking into account the four main components of freedom of economic activity.

In the 2013 ranking1 of economically free states Ukraine is among 20 percent of the most unfree countries of the world. Ukraine’s most problematic areas are investment freedom, government spending, freedom from corruption, and business freedom. Ukraine received relatively good scores for trade freedom.

In order to improve the situation with economic freedom in the country and, correspondingly, raise its rank in the Index, the areas of priority attention should be: raising transparency and efficiency of the actions of officials’ concerning investment policy; soften limitations for land purchase by foreign investors; measures aimed at increasing the mobility of capital. A successful fight against corruption will also boost Ukraine’s positions in the ranking of economically free states.

While doing this, it is necessary to exercise and increase the country’s competitive advantages in the openness of its market (trade freedom), and relatively stable macroeconomic environment.

Factors facilitating development Score Rank ChangeTrade freedom 84.4 48

Factors restraining development Score Rank ChangeGovernment spending 29.4 154 =Investment freedom 20 154

Business freedom, 47.6 148

Freedom from corruption 23 149 Source: The Heritage Foundation in partnership with The Wall Street Journal, Index of Economic Freedom, 2012–2013

About tHE IndEx The Index of Economic Freedom compares the restrictions and barriers of economic activity imposed by governments of different states. The Index’s logic is based on Adam Smith’s idea that the well-being of any country depends on the degree of market and economic activity freedom within. The Index has been calculated by The Heritage Foundation in partnership with The Wall Street Journal since 1995.

Economic freedom corresponds to a person’s fundamental right to control his own labor and property. In an economically free society, individuals are free to choose any way to work, produce, consume, and invest. According to the authors of the Index of Economic Freedom, freedom should not be limited but protected by the state. In economically free societies governments allow the free move of labor, capital and commodities, and abstain from the use of force or limitations of freedom higher than the level required to guarantee and protect freedom itself.

The Index of Economic Freedom reflects an important correlation between economic freedom and social and economic benefits, such as income per capita; rates of economic growth; human capital development; democracy; fighting poverty, and environmental protection. According to the Index, the highest level of economic freedom or minimum restrictions for business

IndEx oF EconomIc FrEEdom

25

I. General IndIces

leads to the increase of productivity in the country and, correspondingly, to the improvement of the nations’ well-being. The analysis of the Index of Economic Freedom determines the barriers and bottlenecks created by the state, which restrain national economic growth by restricting freedom of economic activity.

The Index analyzes 10 components of economic freedom grouped into 4 categories: (1) Rule of Law (property rights, freedom from corruption); (2) Limited Government (fiscal freedom, government spending); (3) Regulatory Efficiency (business freedom, labor freedom, monetary freedom); and (4) Open Markets (trade freedom, investment freedom, financial freedom). The Index combines quantitative and qualitative indicators and is calculated as simple average of the 10 factors of economic freedom. The Index varies from 0 (the worst) to 100 (the best).

The economic freedom ranking is compiled on the basis of the Index and compares up to 185 world states. According to the rankings, states are divided into 5 groups: free, where the value of the index is 80 to 100; mostly free, 70 to 79.9; moderately free, 60 to 69.9; mostly unfree, 50 to 59.9; repressed, 0 to 49.9.

UkraIne’s resUltsIn the latest 2013 Index of Economic Freedom Ukraine received the 161st position out of 177 states with 46.3 points out of 100 possible. Due to such a low rank Ukraine found itself in the 20 most unfree states of the world. Ukraine holds the last, 43rd position in Europe. The country moved from the category of “mostly unfree” to “repressed” and is now in the group of such states as Ecuador, Argentine, Chad, Uzbekistan, Iran, and Zimbabwe. Hong Kong, Singapore, and Australia are the leaders of the 2013 ranking of economically free states.

Ukraine is ranked last oUt of 43 coUntries in the eUrope region, and its overall score is lower than the world average.

Compared to the previous year, Ukraine gained 0.2 points in the Index. Business2 and monetary freedom indicators grew (first of all because the level of inflation dropped). At the same time, scores for freedom from corruption3 and labor freedom indicators dropped. The index of labor freedom has become lower first of all, because of a rise in minimum wages.

Chart 1. Dynamics of positions and values of Ukraine in the Index of Economic Freedom

200770

60

65

50

55

40

45

35

30

60.1 60.2 59.5 59.4 59.7 59.5 59.6

51.5 51.048.8

46.4 45.8 46.1 46.3

2008 2009 2010 2011 2012 2013

Середнє в світі Україна

Source: The Heritage Foundation in partnership with The Wall Street Journal, Index of Economic Freedom, 2007–2013

200860

120

180

160

140

100

80

20102007 2011 20122009 2013

135/157 134/157

153/179163/179 163/179 163/179 161/177

26

I. GEnErAL IndIcES

the index’s ValUe becomes loWer With an increase in the minimUm Wages reflecting ValUes of economic freedom described in adam smith’s ‘the Wealth of nations’. bUsiness perceiVes the increase in minimUm Wages negatiVely becaUse in this case it mUst pay Wages not loWer than the leVel dictated by the state. the ValUe of this indicator Will reach its maximUm if there is no legislation on minimUm Wages in a state.