uganda microfinance industry assessment · uganda microfinance industry assessment august 2008...

TRANSCRIPT

August 2008

UG

AN

DA

MIC

RO

FINA

NC

E IND

US

TRY

AS

SES

SM

ENT A

ug

ust 2008

AMFIU House Plot 679, Wamala Rd, Najjanankumbi, Off Entebbe Rd

P. O. Box 26056 Kampala - UgandaTel: +256 (0) 414 259176, Fax: +256 (0) 414 254420

Email: [email protected]: www.amfiu.org.ug

ASSOCIATION OF MICROFINANCEINSTITUTIONS OF UGANDA

AMFIU JIREH GROUP

Tel: +256 312 273126, : +256 712 965 315

E-mail: [email protected]

UGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENT

1

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

AUGUST 2008

UGANDA MICROFINANCE INDUSTRY ASSESSMENT UGANDA MICROFINANCE INDUSTRY ASSESSMENT

2

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

FOREWARD

Microfinance in Uganda has taken big strides since 1996 when stakeholders formally came together and since then it has been recognized internationally for its contribution to the economic and social development of the economically active poor in Uganda. However, due to the nascent level of the industry, there is limited and scattered information on what is taking place in the microfinance industry in Uganda.

This Microfinance Industry Assessment study tries to compile information on various issues on the microfinance industry and gives an over-view of the general financial sector in Uganda, development and trends in the microfinance industry and issues on regulation of the sector. It provides a wealth of information and knowledge on what microfinance in Uganda is all about, how it fits into the overall financial sector and the role of various stakeholders in the industry.

As a national Network for Ugandan microfinance practitioners and stakeholders, the Association of Microfinance Institutions of Uganda (AMFIU), has been involved in all the different stages of development of the MF industry. Currently, the network has over 100 members that positively impact on the lives of the poor people in Uganda.

Last but not least, I would like to acknowledge the efforts of the AMFIU secretariat team, particularly the Research and Advocacy Officer Jacqueline Mbabazi Arinanye, and the Operations Manager, Solomon Kagaba for working tirelessly to put together this book. Special thanks go to Friends Consults, who were contracted to conduct the study and Kristen Cortiglia from the SEEP Network, whose input enriched the findings of this study.

Hope you enjoy your reading,

David T. Baguma EXECUTIVE DIRECTOR,

UGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENT

3

LIST OF ACRONYMS

ADC Austrian Development CooperationADF African Development FundAFCAP Africa Capacity Building Program AfDB African Development BankAMFIA Association of Microfinance Institutions of AnkoleAMFIU Association of Microfinance Institutions in UgandaASPS Agricultural Sector Program SupportATM Automated Teller MachineBB Bonna Bagagawale (Local Phrase for “Prosperity for All”)BCF Business Culture FundBoU Bank of UgandaCBU Capacity Building UnitCFIs Community based Financial InstitutionsCGAP Consultative Group to help the PoorCIs Credit InstitutionsCMA Capital Markets Authority CMF Commercial Microfinance LtdCRS Catholic Relief ServicesDANIDA Danish International Development AgencyDCA Development Credit AuthorityDFCU Development Finance Company of UgandaDFID Department for International DevelopmentEU European UnionFIA Financial Institutions ActFINCA Foundation for International Community AssistanceFIS Financial Institutions StatuteFSD Financial Sector Development FSDU Financial Sector Deepening Project UgandaFSS Financial Self SufficiencyGDP Gross Domestic ProductGoU Government of UgandaGTZ German Technical CooperationIFAD International Fund for Agricultural DevelopmentMCAP Matching Grant Facility for Capacity BuildingMCC Microfinance Competence CentreMDI Micro Deposit taking InstitutionMED Net Micro Enterprise Development NetworkMF MicrofinanceMFF Microfinance ForumMFI Microfinance InstitutionMoFPED Ministry of Finance, Planning and Economic DevelopmentMOP Microfinance Outreach PlanMSCL Microfinance Support Centre LtdMTCS Medium Term Competitiveness Strategy

UGANDA MICROFINANCE INDUSTRY ASSESSMENT UGANDA MICROFINANCE INDUSTRY ASSESSMENT

4

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

MTTI Ministry of Tourism, Trade and IndustryNGO Non Governmental OrganizationNORAD Norwegian Agency for Development Cooperation NSSF National Social Security FundPAP Poverty Alleviation ProgramPEAP Poverty Eradication Action PlanPMA Plan for Modernization of AgriculturePMT Performance Monitoring ToolPMS Performance Monitoring SystemPRESTO Private Enterprise Support Training and Organizational DevelopmentPRESTO/CMF PRESTO Centre for MicrofinancePRIDE Promotion of Rural Initiatives for Development EnterprisePSDG Private Sector Donor GroupRFS Rural Financial ServicesRMSP Rural Microfinance Support CentreROSCAs Rotating Savings and Credit AssociationsRural SPEED Rural Savings Promotion and Enhancement of Enterprise DevelopmentSACCO Savings and Credit CooperativeSEEP Network Small Enterprise Education and Promotion NetworkSIDAs Sub-County Development AssociationsSMEs Small and Medium EnterprisesSPEED Support for Private Enterprise Expansion and DevelopmentSUFFICE Support to Feasible Financial Institutions and Capacity building EffortsTA Technical AssistanceTERUDET Teso Rural Development Trust LtdTSC Transformation Steering CommitteeUA Unit of AccountUBOS Uganda Bureau of StatisticsUCA Uganda Cooperative AllianceUCB Uganda Commercial BankUCPA Uganda Consumer Protection UnitUCSCU Uganda Cooperative Savings and Credit UnionUFT Uganda Finance TrustUGAFODE Uganda Agency for Development LtdUML Uganda Microfinance LimitedUNDP United Nations Development ProgramUSAID United States Agency for International DevelopmentUSE Uganda Stock ExchangeUSh Ugandan ShillingYES Youth Enterprise Scheme

UGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENT

5

TABLE OF CONTENTS

FOREWORD .........................................................................................2 LIST OF ACRONYMS .........................................................................3 EXECUTIVE SUMMARY....................................................................61.0 INTRODUCTION .................................................................................81.1 General Background ..................................................................................................... 81.2 Rationale for the Report ................................................................................................ 81.3 Work Methodology and Tasks Accomplished .............................................................. 8

2.0 COUNTRY OVERVIEW ......................................................................92.1 General Economic Policy Framework .......................................................................... 92.2 Population and Demographics .................................................................................... 102.3 Macroeconomic Situation ........................................................................................... 12

3.0 THE FINANCIAL SECTOR ..............................................................143.1 Overview ..................................................................................................................... 143.2 History and Development ........................................................................................... 153.3 Principal Categories of Suppliers of Financial Services ............................................. 183.4 Access to Financial Services ....................................................................................... 223.5 Barriers to Access for the Poor and Low Income Segments of the Population .......... 253.6 Recent Developments ................................................................................................. 253.7 The Role of Government ............................................................................................ 263.8 The role of Bank of Uganda (BOU) ........................................................................... 273.9 The Role of Donors ..................................................................................................... 27

4.0 MICROFINANCE INDUSTRY DEVELOPMENT .........................304.1 Historical Context and Development of the MF Industry .......................................... 304.2 Brief History and Industry Growth Triggers ............................................................... 344.3 Emergence and Growth of MFIs................................................................................. 344.4 Commercialization and Integration ............................................................................ 374.5 The Start and Role of the Microfinance Forum .......................................................... 384.6 Evolution of Government’s Role ................................................................................ 394.7 The Birth and Growth of AMFIU ............................................................................... 424.8 The Role of Other Meso Level Organizations ............................................................ 444.9 Retail Level Suppliers of Microfinance Services ....................................................... 46

5.0 REGULATION OF FINANCIAL SERVICES ..................................475.1 Financial Institutions Act 2004 ................................................................................... 475.2 The MDI Act 2003 ...................................................................................................... 485.4 The Proposed Regulatory Framework for Tier 4 ........................................................ 515.5 The Impact and Effect of Regulation .......................................................................... 53

6.0 FUNDING SOURCES .........................................................................556.1 Funding Sources for the Period (1995-2000) ............................................................. 566.2 Funding Sources Between (2000-2003) ..................................................................... 576.3 Funding Sources (2004 and Beyond) .......................................................................... 59

7.0 IMPACT AND SOCIAL PERFORMANCE OF MICROFINANCE ACTIVITIES .......................................................668.0 OPPORTUNITIES AND CHALLENGES ........................................679.0 CONCLUSION ....................................................................................70 APPENDICES ......................................................................................71

UGANDA MICROFINANCE INDUSTRY ASSESSMENT UGANDA MICROFINANCE INDUSTRY ASSESSMENT

6

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

EXECUTIVE SUMMARY

An overview of the overall national economic performance, financial sector dynamics and the regulatory environment provide a vital context for understanding the state and performance of the microfinance industry. That is why this report, intended to present the history and current status of microfinance in Uganda, starts by examining the key aspects of the national economy before looking at the financial sector and then focusing on the microfinance industry in more detail.

Under the PEAP, which has defined Uganda’s economic planning and management framework since 1997, the country has registered significant improvements on the economic and social fronts in the past 20 years. Among these have been average annual real GDP growth of 6%, containment of single digit annual inflation (save for the recent two years when it has gone to 10 % and 12% respectively due to global increases in food and oil prices), a reduction of HIV/ AIDS prevalence from 18% to 6%, a reduction of absolute income poverty from 64% to 31% of the population and an increase in literacy rates from about 50% to 70%. Agriculture, which provides employment and livelihood to 57% of Uganda’s 28.2 million people, is still the mainstay for many although its relative importance is declining as the manufacturing and service sectors continue to grow.

The financial sector, like many others, has recovered from the economic decadence that resulted from a 15-year turmoil (1971 to 1986). By the end of 2007, the BoU regulated financial institutions consisted of 16 commercial banks, 4 credit institutions, 4 MDIs, 2 leasing firms, 19 insurance companies 84 forex bureaus and the NSSF. The sector is expanding as is typified by the increase in commercial bank branches from 133 in 2004 to 290 in 2007. The combined number of outlets of commercial banks, credit institutions and MDIs was 417 by December 2007. All this not withstanding, rural outreach still remains a challenge. Finscope, a detailed side study carried out in 2007, concluded that only 38% of Ugandans have access to financial services: 21% accessing formal and 17% informal financial services. Barriers mainly relate to difficulty in accessing service points, illiteracy, extreme poverty (causing self exclusion), high costs, unsuitability of some product features and lack of financial awareness.

Within about 20 years, Uganda’s microfinance industry has grown from an insignificant sideline to a key sub sector in the economy. Clientele has during this time increased from below 300,000 to over 3.5 million. Adaptation of international sound practices and stakeholder cohesion have mutually reinforced each other to accelerate industry growth. This has been championed by AMFIU and other industry stakeholders. Microfinance retailers in Uganda currently range from commercial banks

However, due to the dynamic nature of the microfinance industry in Uganda and the general financial sector, changes occurred between August 2008 (the study period) and December 2008. The changes include;

Commercial Banks increased from 17 to 20 banks as new players entered the sectors and others graduated through the tiers. Eco bank entered the sector as a new player while Uganda Microfinance Ltd (UML) was taken over by Equity Bank and therefore moved from tier 3 (MDI) to tier 1 as a Commercial Bank. Commercial Microfinance, which was a Credit Institution in tier 2 also joined tier 1 as it was also taken over by Global Trust bank.The number of MDIs reduced from four to three as UML graduated to tier 1FAULU (U) Ltd, which was a tier 4 microfinance institution graduated to tier 2 as a Credit Institution.

UGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENT

7

to Tier 2 credit institutions, MDIs, SACCOs, NGOs and private companies. While the challenge of modest outreach, limited product variety and high pricing/ costs remain, the microfinance industry continues to facilitate access to financial services for the low income people in a significant way.

The MDI Act, the first law enacted specifically for microfinance, is now facing a critical test as MDIs aspire to upgrade to commercial banks and the mature Tier 4 institutions display profound reluctance to apply for an MDI license – mainly due to the perception that while MDIs are not much riskier but MDIs are over regulated and unduly restricted from some gainful businesses streams. The outcomes of these aspects will in a few years inform microfinance regulation internationally.

Government, recognizing microfinance as a suitable engine of growth through provision of financial services to the poor, has in the past come up with different initiatives which have had varying degrees of failure. Government’s most supportive involvement in the industry was perhaps between 2002 and 2005 when government declared its withdrawal from direct provision of microfinance, committed itself to creating an enabling environment for private-sector delivered microfinance to grow, and continued championing the Microfinance Forum. The success of the latest Government MF initiative, the redesigned RFSP (based on one government aided SACCO per sub county), still remains to be seen as the program is only just rolling out. Which ever way this will turn out, it may to some extent negatively affect MFI operations but the industry is sufficiently mature and dynamic to withstand any undesirable side effects.

Funding for microfinance capacity building and loan capital has been vital in industry growth. In a very notable sense, microfinance successes and industry growth can be ascribed to donors just as it can to AMFIU and other stakeholders. Well focused donor programs like USAID-PRESTO, Microsave, EU-SUFFICE, USAID-SPEED, GTZ-Sida FSD Program, USAID- Rural SPEED, FSDU-DFID and others have all contributed to industry growth through training, entrenchment of sound practices, provision of wholesale loans, systems development and institutional technical assistance. Both capacity building and loan capital funds were initially provided by donors and as the industry grew and the MFIs matured, less of the grants for loans funds was available. Presently, hardly any donor provides loan funds for MFIs although a number of them still support capacity building. MFIs now largely get their loan capital from the money market.

Among the positive impacts of microfinance have been positive influence of government policy, improvements in household income, family access to better healthcare and insurance, promotion of social cohesion in the communities, contribution to improved literacy, access to financial services for the economically active poor and promotion of gender equity through women empowerment. Among the challenges are low rural outreach, high product costing, low financial literacy among the poor, limited product range, modest management information systems, inadequate supply of technical skills, imprudent behaviour by non-regulated Tier 4 institutions and Government’s recent moves towards directed credit delivery through SACCOs in sub counties.

In conclusion the Ugandan microfinance industry, which is now well integrated into the financial sector, has gone through all stages of maturity and is now robust and resilient. Any investments in the sector would be best productive if they are aimed at offering technical assistance and other capacity building in the mentioned areas1 where there are challenges.

1 Of this report

UGANDA MICROFINANCE INDUSTRY ASSESSMENT UGANDA MICROFINANCE INDUSTRY ASSESSMENT

8

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

INTRODUCTION1.0

General Background1.1

This Industry Assessment Report presents the status and dynamics of Uganda’s microfinance industry. Starting with the broader demographic and macroeconomic context, the report proceeds to present the relevant issues in the wider financial sector before narrowing down to the situation and status of the microfinance industry. It is structured so as to be useful for persons encountering Uganda’s microfinance industry for the first time, those who would like to compare it with others as well as those who just want to update their information on the industry. Topical issues like the historical perspective of industry development, regulation, government initiatives, funding and how it has evolved over time, microfinance impact, and opportunities and challenges are covered.

Rationale for the Report1.2

The study was requested by Association of Microfinance Institutions in Uganda (AMFIU) to provide useful information on the outlook of Uganda’s micro finance industry. The study looked at Uganda’s microfinance sector in the context of the broader financial sector and national economy, and from both the historical perspective and current situation. This report should be of use to AMFIU, its members, partners as well as other persons interested in working with or studying the country’s microfinance sector.2

Work Methodology and Tasks Accomplished1.3

This assignment was meant to mainly compile secondary information from various sources, complement them with any necessary interviews, analyze them and produce an industry assessment report. Consultants accordingly assembled the relevant documents, papers and reports, reviewed and collated them, analyzed all the information and produced this report.

Among the main tasks accomplished are:

Review of various papers, reports and documents on the state and trends of Uganda’s economy and demography. This mainly focused on the key social, macro-economic and demographic indicators3

Review the facts and figures relating to the wider financial sector emphasising key issues that are relevant to the development of an inclusive financial sector. Review and analysis of the current and proposed regulations, focusing on their impact on the availability of financial services, safety of public deposits and overall stability of the financial sector Panoramic review and analysis of the microfinance (MF) sector development in

2 As an example, AMFIU has entered a funding arrangement with two development partners –Citi Foundation and Small Enterprise and Education Promotion (SEEP), and this report could be of use to this institutional relationship. 3 Mainly for the past five years, though in some case dating back to the 1980s

UGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENT

9

Uganda including its history, development trends, retail and meso-level actors and the evolution of financial and non financial products/services.A quick inventory of the currently available funding sources in the industry

Review of prior industry assessments relating to the impact of microfinance activities in the countryFrom analysis of all the above and the consultant’s deep and wide knowledge of the industry, identification of opportunities for and challenges in the MF industry were made.

It was not necessary to carry out interviews specifically for this report since the consultants had recently carried out two studies on different aspects of industry development and asked all the questions that would have been necessary for this report. Furthermore, a lot of other data, information and reports were available with AMFIU, Bank of Uganda and FRIENDS Consult that was relevant for the assignment and needed analysis in the light of it. Accordingly, the consultants concentrated more on studying existing data, information, reviewing relevant reports and other documents to broaden and enrich the report.

COUNTRY OVERVIEW2.0

General Economic Policy Framework2.1

Uganda has registered remarkable economic growth in the last 20 years, having emerged from many years of civil wars and strife that had destroyed the country’s economic, social and physical infrastructure. Uganda’s economy (measured by Gross Domestic Product-GDP) grew by an annual average by 6.5% between 1990 and 2006. This has followed a combination of a fairly successful economic recovery programme, growth focused economic planning/ management, review of laws and regulations to attract more investments, liberalization of the economy, Government’s attempts at providing an enabling environment for enhanced economic / business activities and, in the last ten years, a national economic planning framework focused on poverty reduction. The current national planning framework is the Poverty Eradication Action Plan (PEAP). Since its formulation in 1997 and subsequent revisions in 2001 and 2003, the PEAP has guided and influenced formulation of all government policy. As the overall framework, PEAP is built on five pillars:

Sound economic management1.

Enhancing production, competitiveness and incomes2.

Security, conflict-resolution and disaster management3.

Good Governance4.

Human development5.

UGANDA MICROFINANCE INDUSTRY ASSESSMENT UGANDA MICROFINANCE INDUSTRY ASSESSMENT

10

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

PEAP has two grand implementation strategies to realize the first two of the above five pillars:

Plan for Modernization of Agriculture (PMA), developed as a holistic action strategy to facilitate the expansion of the rural economy through increased agricultural productivity, value addition and market access.

Medium Term Competitiveness Strategy for the Private Sector (MTCS) developed to target the areas of business environment and facilitation needed for the private sector to become increasingly competitive and function as an ‘engine of growth’

PEAP together with and the above two implementation strategies drive the national economic agenda.

Population and Demographics 2.2

National population and its growth rateWith a population of over 28.2 million people in 20074 and a population growth rate of 3.3% per annum5, Uganda has one of the fastest population growth rates in the world, and second highest in Sub-Saharan Africa. The literacy level was recorded at 70% and average life expectancy at 49.7 years in 2006. Life expectancy has since slightly improved to just above 50.

HIV/ AIDS prevalenceDemography of many African countries is today closely linked to the prevalence or rate of HIV/ AIDS infection. Uganda’s HIV/AIDS prevalence rate is presently about 6% having declined from 6.4% in 20056 and from 18% between 1990 and 2002. Uganda is regarded as a leader in the fight against HIV/AIDS. However, the prevalence rate in the past five years has stagnated around 6% and the epidemic remains a leading cause of death within the most productive age (15-49)7.

Poverty incidenceDuring the 1990s, income poverty (percentage of people living on below one US$ per day) fell dramatically from over 60% in the 1980s to below 34% in 2000. Between 2000 and 2003, however, income poverty rose, with the proportion of people below the poverty line rising from 34% in 2000 to 38.4% in 2003. This then fell to an all time low of 31.3% as by the end of 20068, at which level it still stands. Uganda remains one of the poorest countries in the world despite the impressive decline in poverty indicators and attaining a per capita income of around $335 per annum (just above the international poverty line break-even) during

4 MoFPED, Back ground to the Budget (2007/08), Uganda Bureau of Statistics5 2005/06 Uganda Population and Housing Census Report Mid-Term Report6 MoFPED, Uganda Poverty status report, 20057 MoFPED, “PEAP Revision 2004”8 MoFPED, Back ground to the Budget 2007/2008

UGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENT

11

2005/2006 fiscal year9 which improved to $353 and $400 in the subsequent two years. Most of the population has crossed the international poverty line but still lives quite close to it. The reduction of absolute poverty, however, is significant for the microfinance industry in that it expands the MF market as more people get out of absolute poverty into the category of economically active poor.

Poverty is mainly prevalent in the rural areas and much more so in the northern part of the country. It is estimated that the number of people living below the international poverty line in northern Uganda increased from 3.3 million in 2002 (61% of the Northern Uganda population) to 3.9 million in 2004 (71% of the population in Northern Uganda). This has been attributed to prolonged drought, cattle rustling and the civil war that has ravaged this part of the country for over 20years10. The income poverty has again reduced to 61% as at 2005/0611.

9 MoFPED, Back ground to the Budget 2007/200810 MoFPED, Uganda Poverty status report, 200511 Background to the Budget

UGANDA MICROFINANCE INDUSTRY ASSESSMENT UGANDA MICROFINANCE INDUSTRY ASSESSMENT

12

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

TABLE 1: KEY POPULATION AND DEMOGRAPHIC INDICATORS

Indicator Period1991 2002 2006 2007

Total population (figure in millions) 16.7 24.4 27.3 28.2Population growth rates (%) 2.5 3.3 3.3 n/a1

% of population living in rural areas 89 88 87 87% of population living in Urban areas 11 12 13 13Literacy rates (%) 54 68 70 n/a

Income poverty (%)21999/ 2000 02/ 03 2004/05 2006/0733.8 38.4 31.3

Sources: 2002 Uganda Population and Housing Census – Main Report, Uganda Bureau of Statistics, BoU, MoFPED, Background to the Budget 2007/08, UNDP (2006), Uganda Poverty status report, 2005.

FIGURE 1: UGANDA POVERTY TRENDS (1992 – 2006)12

55.751.2 50.2 49.1

44.4

33.638.4

31.3

0

10

20

30

40

50

60

1992

1993

/4

1994

/519

96

1997

/8

1999

/2000

2002

/03

2005

/06

Period

Shar

e of

Pop

ulat

ion

(%)

Sources: 2002 Uganda Population and Housing Census – Main Report, Uganda Bureau of Statistics, BoU, MoFPED, Background to the Budget 2007/08, UNDP (2006), Uganda Poverty status report, 2005

Macroeconomic Situation2.3

Agriculture still forms the main source of livelihood and provide more than 57% of total employment to the labor force in 2006. Self-employment within this sector remains the most common source of income, while non-agricultural enterprises employed in micro and small businesses provide about 15% of incomes. The agricultural sector’s contribution to GDP in 2006/07 was 31.9%, declining from 33.3% in the previous fiscal year, and lagging behind dropping further to 22.6% in 2007/08; lagging behind the services sector (52.8%). It is noteworthy that the proportional contribution of agriculture to both employment and GDP is steadily declining, while that of industry is rising modestly and for services, is rising

12 Source: Background to the budget and PEAP 2004

UGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENT

13

quite vividly. The relative decline in the importance of agriculture is not due to its reduced productivity (overall, agricultural production is growing in absolute terms). It is because of the relatively higher growth in the industrial and services sectors. The service sector which is the fastest growing in the economy since 2003/04 (averaging over 8% per year), consists of telecommunications, power, construction, transport, financial services, insurance, education, hospitality (hotels, restaurants, tourism) international and intra-national trade and professional services.

The country’s annual underlying inflation in 2007/ 2008 was recorded at 11.8.% compared to 7.7% for the fiscal year (2006/07). The monthly headline inflation for June 2008 was 12%, the highest in over a decade. The reasons for the rise mainly relate to high international oil and food prices, which affect the domestic economy directly. The foreign exchange rate was USh 1,860 per US dollar in June 2006. By March 2007, the shilling had appreciated by 5.9% to UShs. 1,751 per US dollar, attributed to inflows from the export sector, NGOs and donor inflows. Overall, the exchange now stabilized at between USh 1,640 and 1,720 from Dec 2007 to April 2008, but it has now appreciated further to USh 1,620 per US$. Overall, both the intrinsic and parity value (compared to other currencies) of the Uganda Shilling has been fairly stable. Stable inflation has been good for the growth of the financial sector, including microfinance.

TABLE 2: KEY MACROECONOMIC INDICATORS

Indicator Period04/05 05/06 06/07 07/08

Per Capita GDP (US $) 335 353 400 490

GDP growth per annum (%) 6.2 5.1 6.5 8.9

Sector contribution to GDP (%)AgricultureIndustryServices

35.120.044.3

33.320.945.8

31.921.047.1

22.624.652.8

Underlying annual inflation rates (%) 4.7 5.4 7.7 11.8

Exchange rates (USh per US$) 1,738 1,825 1,7513 1,684

Weighted Interest rates (%) per annum on; Savings Deposits- Demand Deposits- Time Deposits- Lending-

1.921.187.8519.37

2.021.149.1218.19

2.231.1610.4418.83

Not Available

Employment (%):Formal- Government employment - Self employment in agriculture- Self employed outside agriculture- Private employment - Not working -

5.170.812.07.14.9

4.857.725.26.75.6

Not available

Not available

Source: Uganda Population and Housing Census – Main Report, Uganda Bureau of Statistics, BoU, MoFPED, Background to the Budget 2007/08, UNDP (2006), Uganda Poverty status report, 2005.

UGANDA MICROFINANCE INDUSTRY ASSESSMENT UGANDA MICROFINANCE INDUSTRY ASSESSMENT

14

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

Growth and developments in the other sectors of the economy have affected microfinance: Growth in the manufacturing sector, for example, means more people take to retailing locally manufactured goods,, more people are involved in the cultivation of raw materials and other inputs, more people join the low income working group, all of who are suitable clients of MFIs. Growth in the services sectors like communication, construction and education have a similar effect of expanding the market for microfinance, as does the growth of the SME sector.

THE FINANCIAL SECTOR3.0

Overview3.1

Snapshot of the key players3.1.1

TABLE 3: KEY PLAYERS IN THE FINANCIAL SECTOR

Player Role

Ministry of Finance, Planning and Economic Development (MoFPED)4

Management of Government’s Treasury, policy level oversight of the financial sector, promotion of inclusive provision of financial services

Bank of Uganda (BoU) Regulation of the financial sector to ensure orderly and safe growth as well as stability of the financial system

Commercial Banks Normal banking services

Credit institutions Loans and in some cases savings accountsDevelopment Banks Large loans and other types of start-up capital, mainly for

corporate business concerns

MDIs Deposit and loan facilities, mainly for low income people

Tier 4 MFIs and SACCOs Loans for low income people (in the case of SACCOs, savings facilities as well)

MF Wholesale lenders Lending to MFIs

Forex Bureaus Buying and selling foreign currencies

Insurance companies Normal insurance services to the population

National Social Security Fund

Management of social security contributions by workers and their employers

Uganda Securities Exchange (USE)

IPOs, trading in shares, bonds and other securities

Capital Markets Authority (CMA)

Regulation of the Uganda Securities Exchange and overall capital markets within the country

Money lenders Individuals and firms that lend money, usually at very high interest rates

Source: Consultants’ own analysis of the financial sector

UGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENT

15

Overview of the Banking and Microfinance Sector3.1.2

The banking and microfinance sections of the financial sector are composed of commercial banks, credit institutions, micro-deposit taking institutions (MDIs), and more than 1,200 Tier 4 MFIs including savings and credit cooperatives (SACCOs) which offer a variety of financial products and services in both the rural and urban areas. The analysis in this section focuses on these sets of institutions because they are the principal suppliers of financial products and services that impact directly on the microfinance industry in Uganda.

The principal players here can be grouped into three broad categories:

Formal financial institutions: Banks, Credit Institutions, and Microfinance Deposit-i) taking Institutions (MDIs). These are supervised by Bank of Uganda under the Financial Institutions Act 200413 and the MDI Act 2003. Semi- formal financial institutions with some form of legal status but are not supervised ii) by BoU. These include SACCOs registered under the Cooperative Societies Statute 1991, MFIs registered under the Companies Act and microfinance NGOs registered under the non-governmental organizations (NGO) Statute.Informal setups: All other member-based associations, including village savings and iii) loans associations (VSLAs), accumulated savings and credit associations (ASCA) and rotating savings and credit associations (ROSCAs).

This categorization is necessary in assessing the extent of access to formal financial services by the poor and low-income segments of the population in Uganda, and in evaluating how the regulatory and operating environment under the different grouping impact on the building of an inclusive financial sector.

History and Development 3.2

The history and development of the financial sector in Uganda has, in many ways, been shaped by the political history of the country. Different governments since independence have implemented political decisions, macroeconomic policies and strategies that have either strengthened or weakened the financial sector in some way.

The years 1962 to 1986The years immediately after independence were years of relative economic stability and the financial sector grew fairly fast. Government started the first indigenous bank -Uganda Commercial Bank (UCB) to widen access to financial services to Ugandans. At the time, the cooperative movement was strong and many SACCOs provided financial services in rural areas. Later on, Cooperative Bank (which eventually collapsed due to poor management in 1998).was also formed. The years between 1971 and 1986 were times of unrest and turmoil, during which the financial sector and the economy as a whole did not develop to any significant extent

13 Which replaced the Financial Institutions Statute 1991

UGANDA MICROFINANCE INDUSTRY ASSESSMENT UGANDA MICROFINANCE INDUSTRY ASSESSMENT

16

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

The years 1986 to 2000The period between 1986 and 2000 was one of recovery and reconstruction in all sectors of the economy. The country was recovering from the effects of several wars that ousted the previous regimes. The period saw fair growth of the private sector, including the opening of a number of locally-owned commercial banks, credit institutions, and building societies. At this time, only 4 major international banks (Barclays Bank of Uganda Ltd, Standard Chartered Bank Uganda Ltd, Grindlays/ Stanbic Bank Uganda Ltd and Bank of Baroda (U) Ltd) held more than 70% of the total assets of the banking sector among them.

Although Bank of Uganda had the mandate to regulate and supervise the banking sector, the banking law set relatively low entry requirements for indigenous institutions with respect to capitalization, reporting, management of liquid assets, and governance competences, thus making it easy for new entrants. This led to a sudden upsurge in the number of banking and credit institutions, which resulted into some institutional failures, chief among them four banks.14

UCB’s losses in nearly all the rural branches, which caused them to be closed down, were a demonstration of how difficult it was (and still is) to offer commercially viable financial services to rural areas. Private institutions that are committed to offering financial services to the rural areas have argued that differences ought to be considered by regulators when setting infrastructure licensing requirements for the rural areas in order to encourage institutions to set up branches in the rural areas. The loss making UCB was eventually bought by Stanbic Bank Uganda Ltd in 2002, reorganized and Stanbic Bank Uganda Ltd is today the market leader among banks in all aspects.

Following the 1998 banks failures, BoU placed a moratorium on licensing new banks for about three years, based on the argument that the economy was over-banked, and new entrants could further weaken the small banks unless they provide new products. The closure of Co-op Bank had a devastating impact on the sector because of the size of its depth of outreach at that time. Many clients lost their money and with that, confidence in the banking sector. One of the lessons learnt from the Co-op Bank failure is that prudent management of depositors’ funds is important for the stability of both the institutions handling deposits and the formal financial sector in general. Safety of depositors’ funds and financial sector stability therefore became a crucial aspect of subsequent laws and regulations for the financial sector. Accordingly, BoU introduced risk-based regulation and supervision, which it now uses.

The years 2001 to 2008The financial sector in Uganda underwent major changes since 2000. Among the measures undertaken to strengthen the financial sector were:

In 2002, BoU ordered the restructuring of Post Bank including the reduction from 90

to 20 service points, due to its capital inadequacy, modest systems endowment and other resources in relation to the level of operation.

14 Greenland Bank, International Credit Bank, Cooperative Bank and Trust Bank

UGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENT

17

The Financial Institutions Act 2004 was enacted in 2004, replacing the Banking Act

and focusing on safety and soundness of all banks/ credit institutions as well as the systemic soundness of the whole financial sector. The new Act has stronger prudential aspects such as: increased core capital requirement, stricter liquidity and solvency ratios, higher capital adequacy ratio, a requirement for the directors and top managers of banks and credit institutions to pass a tightly-defined “fit and proper” evaluation, elimination of ownership concentration, imposition of tighter limits on insider lending, imposing limits on credit level and concentration, limits on investment portfolios, and increased reporting frequency/ details.

The enactment of the Microfinance Deposit-taking Institutions Act 2003, as a measure

to bring under BoU supervision all non-member-based microfinance institutions which wanted to legally collect and intermediate savings. Four (4) MDIs were subsequently licensed between 2004 and 2006. This means that microfinance, which was originally largely informal and unregulated, became integrated in the formal, regulated financial system.

3.3 Current / More Recent Situation

By end of December 2007, institutions registered and supervised by Bank of Uganda included: 16 commercial banks, 4 credit Institutions, 4 micro deposit-taking institutions (MDIs), 84 forex bureaus, 2 leasing firms, 19 insurance companies and the National Social Security Fund. As at December 2007, there were 290 branches of commercial banks in Uganda. In 2004, by comparison, there were only 133.The fairly rapid expansion in commercial bank outreach reflects both the competitive forces within the financial sector and new opportunities arising from growth of the economy. The table below gives a complete picture (as at Dec 2007) of the branch network of regulated financial institutions that offer credit and deposit services to Ugandans:

TABLE 4: BRANCHES/ OUTLETS OF REGULATED FINANCIAL INSTITUTIONS

INSTITUTIONAL TYPE NO. OF INSTITUTIONS

NO. OF BRANCHES

Commercial banks 16 290

Credit institutions 4 39

MDIs 4 88

TOTAL 24 417Source: Bank of Uganda website

UGANDA MICROFINANCE INDUSTRY ASSESSMENT UGANDA MICROFINANCE INDUSTRY ASSESSMENT

18

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

From all the foregoing, it can be inferred that access to quality financial services is improving in Uganda. The challenge, however, is that regulated institutions rarely cover remote rural areas.

According to the Report of Census of Financial Institutions in Uganda of 2006,15 there were 1,271 institutional outlets (headquarters and branches) from 813 financial institutions of all types covering most districts of Uganda. Of these, 13% were by banks, 3% were by Credit Institutions, 8% were by MDIs, and 67% were by other financial institutions and associations not supervised by BoU, including SACCOs, private company MFIs, NGOs and Sub-County Development Associations (SIDAs).

According to the FinScope Uganda Study Report of 2007, 62% of Uganda’s population has no access to financial services. The balance of 38% that have access, 20% is by the non-BoU regulated institutions, whose branch network is to a great extent in rural areas. The non-BoU regulated institutions, therefore, make up the backbone of the rural financial sector, which means that the rural financial sector is largely undeveloped, fragmented and not integrated into the formal financial sector, but with comparative advantages to provide financial inter-mediation in rural areas. The big question is whether they can be effectively monitored and supervised under a regulatory framework that preserves those unique characteristics that give them advantages in the rural areas. This question is still the subject of debate among stakeholders of the microfinance industry.

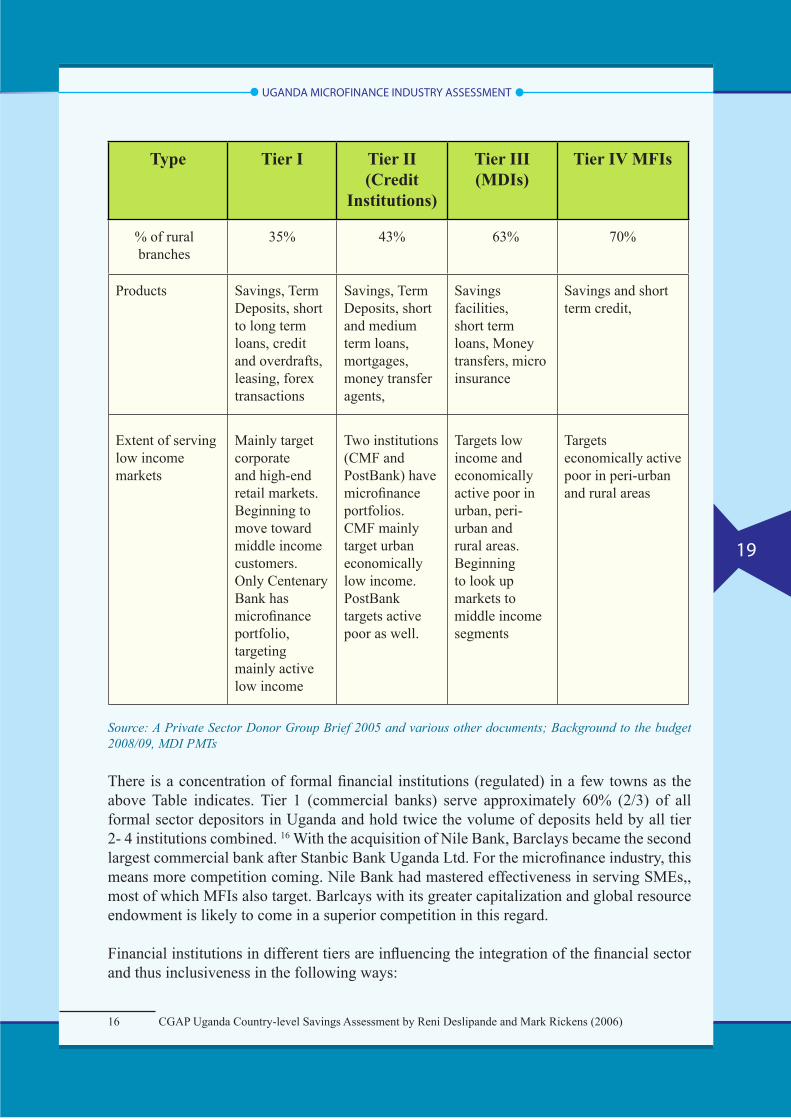

Principal Categories of Suppliers of Financial Services 3.3 TABLE 5: FINANCIAL INSTITUTIONS OUTREACH AS AT 31 DEC 2007

Type Tier I Tier II (Credit

Institutions)

Tier III (MDIs)

Tier IV MFIs

Regulatory instrument

Financial Institutions Act 2004 MDI Act 2003 Co-operative Societies Statute

1991 for SACCOs

Number 16 4 4 >1,000

Number of Towns served

55 18 44 towns (11 with no Tier 1

or 2)

33 towns (9 with no Tier 1,2 and 3)

Number of Branches5

290 39 88 926

15 Census of Tier 4 Financial institutions in Uganda – MoFPED and FSDU, 2006

UGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENT

19

Type Tier I Tier II (Credit

Institutions)

Tier III (MDIs)

Tier IV MFIs

% of rural branches

35% 43% 63% 70%

Products Savings, Term Deposits, short to long term loans, credit and overdrafts, leasing, forex transactions

Savings, Term Deposits, short and medium term loans, mortgages, money transfer agents,

Savings facilities, short term loans, Money transfers, micro insurance

Savings and short term credit,

Extent of serving low income markets

Mainly target corporate and high-end retail markets. Beginning to move toward middle income customers. Only Centenary Bank has microfinance portfolio, targeting mainly active low income

Two institutions (CMF and PostBank) have microfinance portfolios. CMF mainly target urban economically low income. PostBank targets active poor as well.

Targets low income and economically active poor in urban, peri-urban and rural areas. Beginning to look up markets to middle income segments

Targets economically active poor in peri-urban and rural areas

Source: A Private Sector Donor Group Brief 2005 and various other documents; Background to the budget 2008/09, MDI PMTs

There is a concentration of formal financial institutions (regulated) in a few towns as the above Table indicates. Tier 1 (commercial banks) serve approximately 60% (2/3) of all formal sector depositors in Uganda and hold twice the volume of deposits held by all tier 2- 4 institutions combined. 16 With the acquisition of Nile Bank, Barclays became the second largest commercial bank after Stanbic Bank Uganda Ltd. For the microfinance industry, this means more competition coming. Nile Bank had mastered effectiveness in serving SMEs,, most of which MFIs also target. Barlcays with its greater capitalization and global resource endowment is likely to come in a superior competition in this regard.

Financial institutions in different tiers are influencing the integration of the financial sector and thus inclusiveness in the following ways:

16 CGAP Uganda Country-level Savings Assessment by Reni Deslipande and Mark Rickens (2006)

UGANDA MICROFINANCE INDUSTRY ASSESSMENT UGANDA MICROFINANCE INDUSTRY ASSESSMENT

20

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

Tier 1 (Commercial banks):Wholesale lending to MDIs and other MFIs

Downscaling into the traditionally microfinance clientele zone

One Bank, Centenary Bank, has over 80% 17 of its business (clients) in the microfinance portfolioOpening more upcountry branches, thus being able to serve more low income people both directly and by offering loan and deposit facilities for the local MFIs/ SACCOs that serve themTwo banks, Stanbic and Centenary Bank, have strategies aimed to penetrate low- income and rural markets; approximately 93% of deposit accounts in these two banks have average balances of Shs 1 million or below, indicating that they now probably reaching a greater number of clients from the lower economic profile. For Centenary Bank, the motivation for this strategy comes from its social mission derived from its affiliation to the Catholic Church. For Stanbic Bank Uganda Ltd, the extensive country-wide branch network attracts good accounts from government, aid agencies, international organizations and corporate businesses. Linkage banking relationships with SACCOs and other Tier 4 institutions

Although the experiences of Centenary Bank and Stanbic Bank Uganda Ltd (kinds of incentives) cannot be replicated, they may offer valuable lessons for purposes of expanding rural outreach.18

Tier 2 (Credit institutions)Some do wholesale lending to MDIs(examples are DFCU Ltd that lent to UML, UFT and FINCA), to MFIs and to SACCOsOne, Commercial Microfinance Ltd, has microfinance as its sole business

Post Bank, offers savings facilities to middle and low income people and now also lends to micro and small enterprises, salary earners, and wholesales loans to MFIs and SACCOsAll MDIs and some other MFIs cooperate with banks (as agents of banks) and Tier 2 institutions in money transfer services through Western Union and Moneygram, as agents.Linkage banking relationships with SACCOs and other Tier 4 institutions

Tier 3 (MDIs) Loans and deposit facilities to SACCOs and other community based MFIs. According to a 2007 Regulatory Impact Assessment of the MDI Act, low income people have benefited tremendously on the savings facilities offered by MDIs although on the loans side, MDIs have sought more of the less poor borrowers to balance their portfolio

17 Centenary bank annual report 200718 CGAP Uganda Country-level Savings Assessment by Reni Deslipande and Mark Rickens (2006)

UGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENT

21

Now opening more branches; since licensing, for instance, Uganda Microfinance Limited (UML), one of the MDIs, has opened 8 branches and it plans to open 5 more shortly. This way, the MDIs serve both more rural Tier 4 MFIs and more rural/ poor peopleOne MDI, UML, being taken over by the largest retail bank in Kenya, Equity Bank, whose main business is micro, small and medium enterprises (SME) financial services MDIs continue to collaborate with the rest of the industry in promoting sound practices, lobbying and advocacy

Tier 4 (All financial institutions and associations not regulated by BoU) The larger and more progressive Tier 4 institutions have put up effective and engaging competition with MDIs and even commercial bank branchesMoving upscale to diversify the income notches of their clients

Improving their operations and service points to attract more clients

Opening up more remote rural branches to service people who were previously unserved The Tier 4 institutions, especially the SACCOs, are often very suitable in rural areas because of their simple organizational structures that are cost effective, and their ability to respond to clients’ needs because of their being member-based and member-governed.A negative contribution of this tier has been the frequent failure of institutions, leaving their clients/ members with no suitable financial services. The census of tier 4 MFIs in 2005 by MoFPED and FSDU had identified only 628 active SACCOs compared to a total of 1,274 registered with the Department of Cooperatives under the Ministry of Trade, Tourism and Industry (MTTI). The study on the unaccounted for SACCOs and MFIs19 to find out the story behind the 646 variance, established that a good number of the “missing” institutions were registered but never operated, or were once operational but had collapsed, without being deleted from MTTI registry.

The MoFPED has issued a draft regulatory framework for SACCOs in Uganda intended to regulate SACCOs. The new law will recognize the member-based orientation of SACCOs, and also create further opportunity for integration of rural finance into the formal financial system, thus enabling members of SACCOs to get access to formal financial sector institutions and services. It remains to be seen what effect this will have on promoting inclusive financial sector and deepening/ widening outreach.

19 by FRIENDS Consult, commissioned by FSDU

UGANDA MICROFINANCE INDUSTRY ASSESSMENT UGANDA MICROFINANCE INDUSTRY ASSESSMENT

22

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

Access to Financial Services3.4

The most comprehensive and elaborate study so far on access to financial services in Uganda was the Finscope Study20,completed in 2007. Using the “mutually exclusive principle”21, the report among other aspects indicates that:

Only 38% 22 of Uganda’s population access financial services of any sort: 18% access formal financial services, 3% access financial services from semiformal institutions, 17% from informal sources while 62% are un-served by any form of financial services23. The breakdown is as follows;

16% are served by formal banks- 2% are served by MDIs- 2% by SACCOs- 1% by MFIs- 17% by informal financial groups- 62% are financially unserved-

More rural people (65%) than urban people (58%) are un-served

71% of Ugandans save, a majority of them not in cash (buying livestock, land or other valuables)Of those who borrow, most (54%) do so from friends, relatives, greater than the number that borrows from informal, semi-formal and formal institutions all combined. In urban areas, the ratio of the financially served to the un-served is close (48:52) while in rural areas, it is skewed in favour of the un-served (35:65)

FIGURE 2: ACCESS TO FINANCIAL SERVICES BY UGANDANS

Source: FinScope Study 2007

20 Initiated and coordinated by the Financial Sector Deepening Project Uganda (FSDU)-a program of the Department for International Development (DFID) 21 According to the FinScope study: “Mutual exclusivity” = if an individual uses more than one type of financial institution, that individual is graded in the more formal institution in the access strand. For example, if an individual uses both a bank and a SACCO, then that individual is a bank user and not counted in the SACCO strand. 22 FINSCOPE Uganda 2007 23 FINSCOPE Uganda 2007

VSLA1%

ASCAs5%

ROSCA/Welfare funds,savings club

11%

MDIs2%

SACCOs2%

MFIs1%

Commercial Banks16%

Financially unserved

62%

UGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENT

23

In terms of rural/urban distribution, people living in rural areas are more likely to be without financial services than those in urban areas (65% and 52% respectively)24.There are significant regional variations in the populations’ access to financial services.

TABLE 6: FINANCIAL ACCESS BY LOCATION AND REGION

Rural UrbanCentra l Kampala

Central Other Eastern Northern Western

Financially Served (%) 35 48 49 28 33 34 50

Un-served (%) 65 52 51 72 67 66 50

Source: FinScope Uganda Study, 2007

There is notable usage of financial institutions (FIs) and groups by those who access them. A significant proportion of those using formal FIs also use semi-formal and informal financial groups.Ugandans accessing formal financial institutions are most likely to be educated to secondary school level or above (74%), over 25 years of age (85%) and in business (43%).

Non usage of formal and semi-formal FIs is mainly attributed by the respondents to not having enough money to save or open/ maintain an account.

Access to financial services in Uganda is still tilted in favour of men (gender) and urban areas (location).

The Table below highlights how the 38% of the population that is financially served is distributed between urban and rural areas, and between male and female.

TABLE 7: FINANCIAL ACCESS STRAND BY LOCATION AND GENDER

Total all respondents Total Rural Urban Male Female

% % % % %Unserved 62 65 52 58 66Banks 16 12 28 21 11Informal groups –minus ASCAs 11 12 6 11 10ASCAs 5 5 6 4 6MDIs 2 2 3 1 2SACCOs 2 2 2 3 2MFIs 1 1 1 1 1VSLAs 1 1 1 1 1Credit Institutions 0 0 1 0 0

Source: FinScope Uganda Study 2007

24 FinScope Study 2007

UGANDA MICROFINANCE INDUSTRY ASSESSMENT UGANDA MICROFINANCE INDUSTRY ASSESSMENT

24

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

The table indicates that formal banks mainly serve male clients compared to female, while other categories of institutions are fairly balanced on the gender access strand.

Considering that the bulk of the population is in the rural areas, strategies by financial institutions to increase financial access should focus on developing appropriate products for the rural population. Development of agricultural financial products is one area that has received little attention and yet has unmet demand. Slowly, some MDIs and SMEs focused banks are starting to develop suitable agricultural/ agribusiness focused financial products.

It is important to note from these findings that the majority of Ugandans who access financial services use informal institutions, re-emphasizing the need to put in place a law for regulating informal and semi informal financial institutions as soon as possible. Another important finding is that at least 22% of Ugandans that borrow from formal financial institutions borrow from more than one institution (multiple borrowing). This underscores the growing need to have a national credit reference system to reduce on the risks associated with multiple borrowing. This is more critical for and 4 institutions which will not be served by the recently established Credit Reference Bureau.

The highest proportion of “unserved” comes from Eastern and Northern Regions. These two areas have in the last 20 years suffered from insurgency and dry periods that have affected economic activities and progress. In addition the state of infrastructure in terms of communication, roads and utilities is relatively less developed compared to other regions. These are basic requirements for institutions to set up financial outlets. Their absence or relative scarcity in many ways explains the lower levels of business activity and access to financial services in these areas. The special efforts by Government to increase financial access in such areas (such as promoting a SACCO at each sub-county) are quite justified, provided business principles are followed, and regulation is streamlined. With time, formal institutions that are unable to set up branches in such remote places could explore linkage relationships with Tier 4/ member-based institutions that are or will be established there.

To improve access to financial services, government and its development partners in the industry now need to focus their support on initiatives that promote outreach to remote and rural people. Such initiatives could include:

Development of products that are more suitable to small scale rural agriculture, most prevalent in rural areas

Development and refinement of product/ service delivery methodologies that would enable MFIs to serve rural clients sustainably at affordable service costs

Incentives like initial year loss compensation, partial coverage of initial year overheads and funding of branch establishment in rural areas.

Establishment of pro-poor wholesale lending to MFIs (Government is already implementing this with SACCOs)

UGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENT

25

Barriers to Access for the Poor and Low Income Segments of the Population3.5

The major barriers to access to financial services for the poor Ugandans include the following:25

Limited branch network by the formal and regulated institutions

Unsuitable products for the segment (the poor/ low income people, especially in rural areas where farming/ agriculture is predominant)

Inaccessibility and lack of basic infrastructure in some rural and remote rural areas of the country

The high cost of delivering financial services to the poor/ low income rural people, which makes services expensive for clients and less attractive to financial institutions

Sustainability considerations for the institutions in rural and remote rural areas where there is no critical mass to sustain delivery of services limits options for branch networks by formal institutions

Lack of regular income (on the part of the poor rural populations) to save in order to open and maintain a bank account

Discomfort (on the part of poor, modestly literate people) about perceived sophistication of banks and inability to speak ‘their language’

High transaction costs to users – transport to bank, service fees, time it takes to draw money from the formal institution.

In addition to direct interventions like those that reduce the cost of microfinance to clients, addressing the problem of access will also need continued and intensified sensitization/ education on basic business/ entrepreneurial skills and financial literacy (AMFIU is making efforts at addressing the latter).

Recent Developments3.6

Uganda’s financial sector has developed more dynamically and speedily in the last decade than in the previous years. Among the developments are:

The acquisition of Uganda Commercial Bank by Stanbic Bank Uganda Ltd and turn-i. around of the business, which took retail banking in Uganda to a higher levelPurchase of Nile Bank, a leading local bank, by Barclays Bank of Uganda Ltd, ii. making Barclays, which had previously been a high street bank, the third largest in branch network and second largest bank in asset endowmentLicensing and regulation of four leading MFIs into MDIs and their prudential iii. regulation by the central bankDevelopment and adaptation of new products, especially asset leasing and mortgage iv. loan finance, by nearly all the banks

25 Put together from different document reviews, including the FinScope Uganda Study, 2007

UGANDA MICROFINANCE INDUSTRY ASSESSMENT UGANDA MICROFINANCE INDUSTRY ASSESSMENT

26

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

Increasing competition as new banks from other countries enter the market, MDIs get v. more into head-on competition with commercial banks and mature Tier 4 institutions compete with both categoriesReplacement of the history/ forensic based supervision with the more dynamic and vi. preventive risk-based supervision by the central bankIncreasing competition and cooperation between/ among different tiers of financial vii. institutionsSpeedy branching out of banks, MDIs and mature tier 4 MFIsviii. Promotion and strengthening of rural based financial institutions by donor programs, ix. with support of the governmentFailures of several SACCOs and other Tier 4 MFIs that were not commercially viable x. or sustainability focused, and notable growth of the progressive onesEnlightenment of low income/ rural people on their rights and responsibilities as xi. consumers of financial services through consumer education.

Despite many positive developments in the industry, in some remote rural areas where commercially-oriented institutions are not keen to establish, socially- oriented initiatives such as ROSCAs are for sometime likely to remain the main providers of financial services.26 There needs to be a mechanism for identifying such informal set ups and helping them to work better.

The acquisitions, while making the institutions larger and in some cases more competitive, will most likely move a number of MDIs and other mature MFIs further away from offering microfinance to the very poor. Both UML and CMF, for example, have been acquired by banks and will soon become commercial banks. While they will no doubt want to maintain their focus on low income clients, the acquiring banks have to balance between poverty focus and profitability, perhaps more in favour of the latter.

Competition is driving banks to establish branches in most of the districts and MDIs and other MFIs to move deeper into less urban locations. This all shows that competition can drive geographical outreach, although this happens at a pace slower that politicians and other leader would in most cases like to see. A vital role for Government and donors is to help MFIs branch out faster into more rural areas that they would have done on their own.

The Role of Government3.7

Government remains committed to supporting the growth and outreach of inclusive financial services, although this has meant a de-emphasis of the purely market based outreach. Among governments roles in this regard are:

Provision of regulatory framework in which the private sector providers of micro-a) financial services can thrive, in which the industry as a whole can develop and which ensures appropriate protection of public deposits

26 The Microfinance Banker – vol. 6 Issue No.4 2006 (pages 7-15)

UGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENT

27

Active promotion of a “rural financial infrastructure” through Government of b) selected SACCOs at the sub county level

In the past, supporting role of overall institutional capacity building in the c) microfinance industry.

Government has put up different initiatives at different times, all of which have had different degrees of failure (or success). These are elaborated in section 4.6 of this report.

The role of Bank of Uganda (BoU)3.8

BoU has had to embrace the role of regulating and supervising MDIs in addition to its traditional role of supervising commercial banks and credit institutions. In both regulatory roles, BoU uses the risk based, preventive approach which is rigorous, very engaging to the regulated institutions and ensures greater safety of the institutions and their customers’ deposits.

After the negative impact of the 1990s bank failures, the Regulation Guidelines issued by BoU as a basis of supervision of MDIs and banks/ credit institutions are now risk based and preventive. While the new regulatory regime has had excellent success in safeguarding public deposits and ensuring the safety and soundness of the financial system, it has as a side effect tended to limit expansion and outreach by the regulated institutions.

While mobilizing of savings from the public by unlicensed, non-SACCO MFIs is prohibited, BoU does not have the capacity to closely supervise this segment of the sector. BoU’s vigilance has, however, remarkably reduced incidences of deposit taking by non-licensed institutions. Never-the-less, isolated incidences of such still happen and when they do and things go wrong, public confidence in the microfinance sector suffers.

The BoU has the responsibility to maintain a sound financial sector, but it is obvious that some of the necessary measures to achieve this may not necessarily lead to development of increased outreach and depth in the financial sector.

The Role of Donors3.9

During the early and growth/ consolidation years of microfinance industry in Uganda (1995 – 2000), the donors played an important role in the area of capacity building for MFIs, with the USAID funded PRESTO Project at the fore front in the area of developing and training MFIs in basic “best practices” and business approaches, while GTZ was assisting BoU to build capacity in financial systems development including regulatory matters. In the years immediately prior to the passing of the MDI Act (2000 – 2003), the donors supported transformation activities by paying for technical assistance and training, improvement/ overhaul of MIS, branch infrastructure improvements, and by extending grants and subsidized loans, as well as guaranteeing bank loans for funding loan capital of the MFIs. Non-transforming MFIs continued to receive subsidized training and technical assistance (TA) but to a lesser extent than the transformation candidates.

UGANDA MICROFINANCE INDUSTRY ASSESSMENT UGANDA MICROFINANCE INDUSTRY ASSESSMENT

28

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

Donors were instrumental in the setting up of a Microfinance Outreach Plan Coordination Unit (MOP)27 at the government level, and have supported the development and strengthening of AMFIU to carry out its functions. The MF donors as a group also developed their own coordination and principles for funding MF initiatives. This has helped them to be more focused on the industry’s areas of need and to avoid duplication. A number of donors like FSDU and Rural SPEED have funded initiatives in consumer education, either jointly with or to complement AMFIU’s efforts in this regard.

In summary, cooperation among microfinance stakeholders, in which donors were active participants, led to the creation of several highly effective mechanisms for collaboration. Some of the positive developments from this collaboration are listed in the CGAP 2004 Review:

The Private Sector Donors’ Group (PSDG) for donors was formed to coordinate donor support to the industry,

The microfinance forum (MFF) for all stakeholders including high-level government representatives, and its subcommittees for technical consultations on key issues, such as capacity building, financing of MFIs, consumer affairs, regulations, and lobbying,

The industry association AMFIU.

The development and adoption of “Donor Principles for Support to Uganda’s Microfinance Sector” in 2001,

The passage of the MDI Act in 2003, and the development and adoption of a common donor reporting tool (PMT) for Ugandan MFIs in 2003.

Development of the “Donor Code of Best Practices” for microfinance, which happened in part because of the level of organization and interaction in the industry. Although the code was meant to guide only the donors active in the Uganda MF industry, it has now been adopted in many parts of the world as guiding principles for MF donors.

Although the donors were not the only or lead players in the above, they played key roles like financing and providing technical expertise to aid them. Donors have continued, albeit on a reduced scale, to support building capacity for the BoU to supervise and regulate the sector and to retail institutions to enable MDIs and MFIs to sustainably deliver more affordable and appropriate products for the poor. Overall, donor programs have impacted significantly, both negatively and positively, on microfinance in Uganda. Positive results have mainly been registered in areas of human resource/ skill development, adaptation of sound practices, streamlining institutional sustainability of systems/ procedures while negative results (in few of the cases) were registered where donors had conditions that forced MFIs to take less market or operational decisions that were not commercially sound.

27 Now changed to the RFSP Implementation Unit

UGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENT

29

There is still a role for donors to support the industry, particularly in the following areas:

Further development of linkage banking initiatives between MDIs and other MFIs i) and SACCOs in order to join the advantages of local ownership and governance, with the advantages of centralized professional management.28

Establishment of a national identification system that would in turn support a credit ii) reference system, to help reduce the risks being created by multiple borrowings by clients (especially for Tier 4 financial institutions).

Market surveys, especially in the areas of product development and adaptability for iii) middle and low- income segments

Stepping up of consumer education programmes in order to improve the effectiveness iv) of financial markets29.

Promotion of further rural outreach and financial v)

More capacity building for the MFIs, especially in the areas of systems and staff vi) development.

These are areas that can particularly lead to an increase in client- responsive financial services and thereby create increased demand for financial services. Increasing access to financial services to the poor and the poorest probably also requires the substantial growth of financial services for middle-income Ugandans, to achieve a “critical mass” of financially-viable institutions of efficient scale, before outreach can be extended to the poor and poorest in the rural areas.30

28 FSDU 2005: Linkage Banking, DFID FSD Project Uganda 29 Uganda Microfinance Sector Effectiveness Review – CGAP 200430 The Microfinance Banker – vol. 6 Issue No.4 2006 (pages 7-15)

UGANDA MICROFINANCE INDUSTRY ASSESSMENT UGANDA MICROFINANCE INDUSTRY ASSESSMENT

30

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

MICROFINANCE INDUSTRY DEVELOPMENT 4.0

Historical Context and Development of the MF Industry4.1

TABLE 7: SNAPSHOT OF THE VITAL MILESTONES AND KEY-PLAYERS

Period Event(s) Key Players/ Movers

1984 Start of Uganda Women’s Finance and Credit Trust (UWFCT)7 by a group of progressive women, to offer microfinance to low income poor women [Now Uganda Finance Trust-MDI].

A group of influential Ugandan women led by;

Mrs. Ida Wanendeya, 1. Mrs. Mary Maitum(RIP),2. Mrs. Mary Mulumba 3. Mrs. Mary Okwakol4. Mrs. Treza Mbiire5.

1987-1992 Start and implementation of the Rural Farmers’ Scheme by the then Uganda Commercial Bank (UCB)8. The scheme failed because whereas it financed increased productivity, market access was a severe challenge for the farmers.

1. Government of Uganda2. Uganda Commercial Bank

1991-1992 Planning for and start of PRIDE Africa, a microfinance retailing project financed by the Norwegian government (and managed by PRIDE Africa Management Services) as development aid to the government of Uganda. This was institutionalized and is now PRIDE Microfinance (MDI), one of the leading MFIs in the country.

1. Government of Uganda2. Government of Norway) through NORAD)3. PRIDE Africa Management Services Ltd.

1992 Start of FINCA as an NGO, promoted by FINCA International, to offer small loans to low income women entrepreneurs. It grew over the years and FINCA Uganda (MDI) became the first MDI to be licensed by Bank of Uganda in 2004.

FINCA International

Early & 1990s

Emergence of small microfinance programs and institutions, mainly promoted by large international NGOs with a socio-welfare agenda.

International welfare NGOs like World Vision, Feed The Children, Food for the Hungry and Freedom From Hunger.

1994 to 1997

Planning for and implementation of the failed Entandikwa (start-up capital) scheme, retailed through local government structures

Government of Uganda

UGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENTUGANDA MICROFINANCE INDUSTRY ASSESSMENT

31

Period Event(s) Key Players/ Movers

1996-2000 Start and operationalization of the Poverty Alleviation Project (for MF capacity building and loan wholesaling.

1. Government of Uganda2. African Development Bank

Start and implementation of the USAID-PRESTO9 Project which has to date made the most important mark in MF capacity building, entrenching of MF Sound Practices, paradigm shifting from viewing MF as a social/ welfare activity to viewing and practicing it as a business with a focus on sustainability, MF loan capitalization and sound-practice based technical assistance.

1. USAID Uganda (designer and funder)2. Price WaterhouseCoopers (Project manager of PRESTO’s Center for Microfinance)3. Anne Ritchie (Director of the Center for Microfinance, PRESTO)

Start and operationalization of MicroSave Africa, very focused that promoted savings product research/ improvement, market oriented product development and delivery and vital research into key industry issues.

1. DFID (Financier)2. UNDP (Financier)3. Graham Wright (then the Director, MicroSave)

Start of the Microfinance Forum, an informal but well attended and very influential monthly meeting of all MF stakeholders

1. PRESTO2. MicroSave Africa3. PAP4. MoFPED10

5. MFIs – all categories6. Donors7.Bank of Uganda8. Other MF stakeholders

Drafting of the financial sector policy by BoU and approval by Cabinet

Bank of Uganda

Drafting of the MF Regulation Bill by BoU Bank of Uganda

On the basis of the draft bill, several debates, disagreements, lobby events, cross-transfer of information between the industry and BoU, cross-fertilization of learning between government, BoU and the industry. This resulted in drastic, positive changes in the Bill into what eventually became the MDI Act.

1. Bank of Uganda2. PRESTO3.PAP4.MFIs5. Anne Ritchie (PRESTO)6. Henry Bagazonzya (PAP)7. Andrew Obara (PRESTO)8.Anthony Opio, BoU9. Keith Muhankanizi (MOFPED)10. David Baguma (FTC-CBP)11) Eva Mukasa (then CEO-UWFT)12 Suleiman Namara(ED, AMFIU)

UGANDA MICROFINANCE INDUSTRY ASSESSMENT UGANDA MICROFINANCE INDUSTRY ASSESSMENT

32

UGANDA MICROFINANCE INDUSTRY ASSESSMENT

Period Event(s) Key Players/ Movers

2001-2004 Design of USAID-SPEED Project, to help mature MFIs graduate and transform

USAID Uganda

Harnessing and leading MF industry stakeholders in the shaping of the MDI Bill; other lobby, advocacy and information dissemination activities during the period

AMFIU

Operationalization of SPEED’s Microfinance Component, choice of institutions, appraisal and rationalization of focused, targeted technical assistance

1. Joanna Ledgerwood (MF Advisor, SPEED)2. Andrew Obara (Senior MF Specialist, SPEED)3. Olive Kabatalya (MF Specialist, SPEED)

Design of the Microfinance Outreach Plan11 (Government strategy for market responsive outreach with microfinance)