ubai esidential maret eport ubai esidential maret eport · dubai house price timeline sales price...

TRANSCRIPT

© Property Monitor 2018 | propertymonitor.ae 32

Dubai Residential Market Report Dubai Residential Market Report

The UAE’s only real estate data source offered by accredited property professionals

Property Monitor is the UAE’s only real estate intelligence platform offered by RICS accredited property professionals, Cavendish Maxwell. It gives us great pleasure to be working alongside Cityscape as their official data partner for the 17th edition of Cityscape Global.

Our data and intelligence service is aimed at increasing transparency in the UAE marketplace. Agencies, developers, banks and consultancies can access real-time data, across multiple data points, and expert intelligence in order to make more informed decisions, based on actual transactions, valuations and trends.

Property Monitor offers users the ability to search up-to-date residential sales and leasing transactions, off-plan sales, commercial transactions, valuation data as well as our professional opinion on achievable prices, across all major areas of Dubai and Abu Dhabi.

CONTENTSFOREWORD

House Price Timeline

Price Performance

Rent Performance

Q4 2018 - Q1 2019 Upcoming Supply

Residential Sales Overview

Property Monitor Residential Survey

Methodology

4

6

8

10

12

13

14

2

© Property Monitor 2018 | propertymonitor.ae 54

Dubai Residential Market Report Dubai Residential Market Report

The UAE’s only real estate data source offered by accredited property professionals

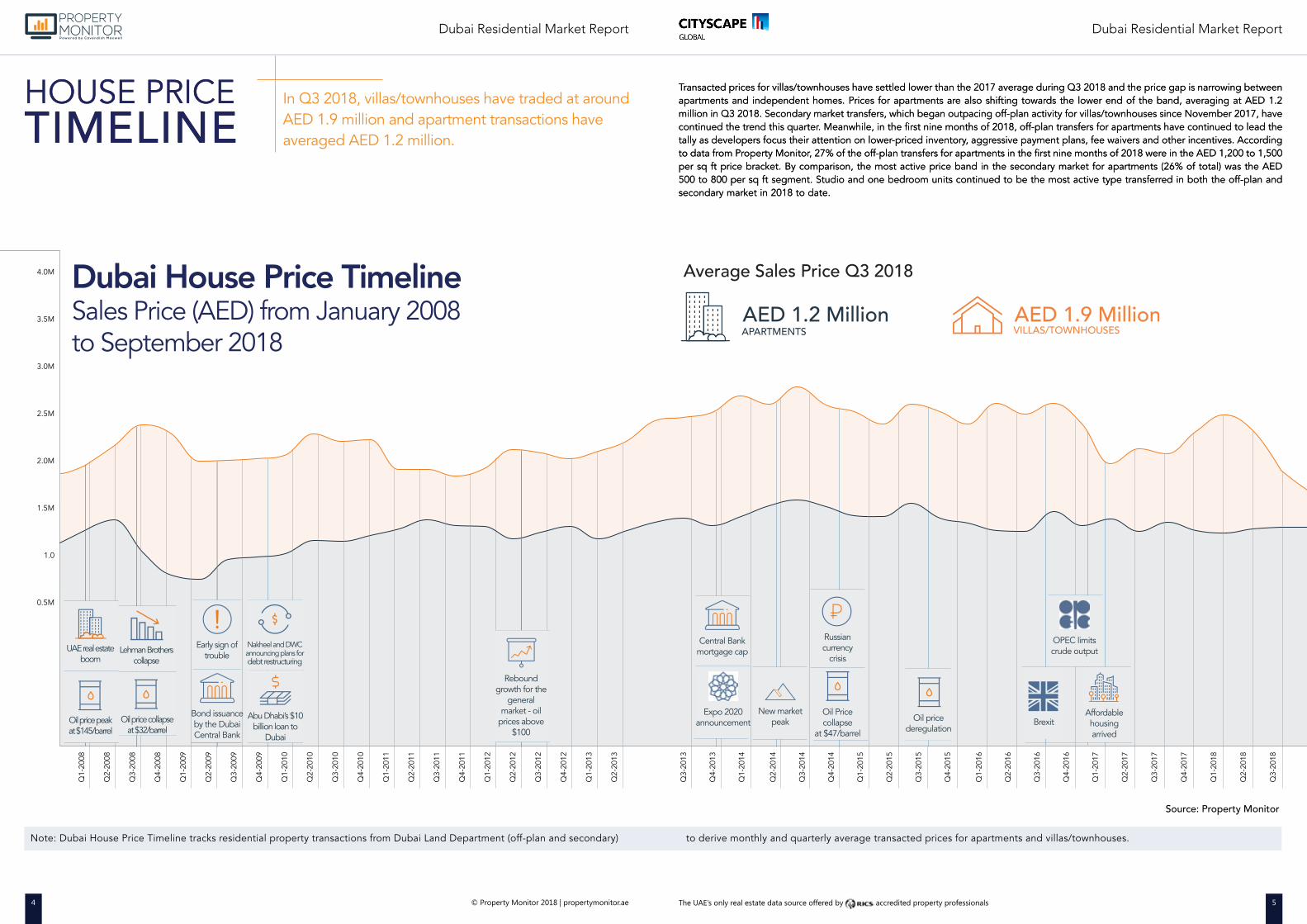

In Q3 2018, villas/townhouses have traded at around AED 1.9 million and apartment transactions have averaged AED 1.2 million.

Dubai House Price TimelineSales Price (AED) from January 2008to September 2018

VILLAS/TOWNHOUSESAED 1.9 Million

Average Sales Price Q3 2018

APARTMENTSAED 1.2 Million

Transacted prices for villas/townhouses have settled lower than the 2017 average during Q3 2018 and the price gap is narrowing between apartments and independent homes. Prices for apartments are also shifting towards the lower end of the band, averaging at AED 1.2 million in Q3 2018. Secondary market transfers, which began outpacing off-plan activity for villas/townhouses since November 2017, have continued the trend this quarter. Meanwhile, in the first nine months of 2018, off-plan transfers for apartments have continued to lead the tally as developers focus their attention on lower-priced inventory, aggressive payment plans, fee waivers and other incentives. According to data from Property Monitor, 27% of the off-plan transfers for apartments in the first nine months of 2018 were in the AED 1,200 to 1,500 per sq ft price bracket. By comparison, the most active price band in the secondary market for apartments (26% of total) was the AED 500 to 800 per sq ft segment. Studio and one bedroom units continued to be the most active type transferred in both the off-plan and secondary market in 2018 to date.

Source: Property Monitor

HOUSE PRICETIMELINE

Transacted prices for villas/townhouses have settled lower than the 2017 average during Q3 2018 and the price gap is narrowing between apartments and independent homes. Prices for apartments are also shifting towards the lower end of the band, averaging at AED 1.2 million in Q3 2018. Secondary market transfers, which began outpacing off-plan activity for villas/townhouses since November 2017, have continued the trend this quarter. Meanwhile, in the first nine months of 2018, off-plan transfers for apartments have continued to lead the tally as developers focus their attention on lower-priced inventory, aggressive payment plans, fee waivers and other incentives. According to data from Property Monitor, 27% of the off-plan transfers for apartments in the first nine months of 2018 were in the AED 1,200 to 1,500 per sq ft price bracket. By comparison, the most active price band in the secondary market for apartments (26% of total) was the AED 500 to 800 per sq ft segment. Studio and one bedroom units continued to be the most active type transferred in both the off-plan and secondary market in 2018 to date.

HOUSE PRICETIMELINE

Note: Dubai House Price Timeline tracks residential property transactions from Dubai Land Department (off-plan and secondary) to derive monthly and quarterly average transacted prices for apartments and villas/townhouses.

Q1-

2008

Q2-

2008

Q3-

2008

Q4-

2008

Q1-

2009

Q2-

2009

Q3-

2009

Q4-

2009

Q1-

2010

Q2-

2010

Q3-

2010

Q4-

2010

Q1-

2011

Q2-

2011

Q3-

2011

Q4-

2011

Q1-

2012

Q2-

2012

Q3-

2012

Q4-

2012

Q1-

2013

Q2-

2013

Q3-

2013

Q4-

2013

Q1-

2014

Q2-

2014

Q3-

2014

Q4-

2014

Q1-

2015

Q2-

2015

Q3-

2015

Q4-

2015

Q1-

2016

Q2-

2016

Q3-

2016

Q4-

2016

Q1-

2017

Q2-

2017

Q3-

2017

Q4-

2017

Q1-

2018

Q2-

2018

Q3-

2018

Oil Price collapse

at $47/barrel

Oil pricederegulation

New market peak

Russian currency

crisis

OPEC limitscrude output

BrexitAffordablehousingarrived

Central Bankmortgage cap

Expo 2020announcement

Rebound growth for the

generalmarket - oil

prices above $100

Nakheel and DWCannouncing plans fordebt restructuring

Abu Dhabi’s $10 billion loan to

Dubai

Early sign oftrouble

Bond issuanceby the DubaiCentral Bank

Lehman Brotherscollapse

Oil price collapseat $32/barrel

UAE real estate boom

Oil price peakat $145/barrel

4.0M

3.5M

3.0M

2.5M

2.0M

1.5M

1.0

0.5M

© Property Monitor 2018 | propertymonitor.ae 76

Dubai Residential Market Report Dubai Residential Market Report

The UAE’s only real estate data source offered by accredited property professionals

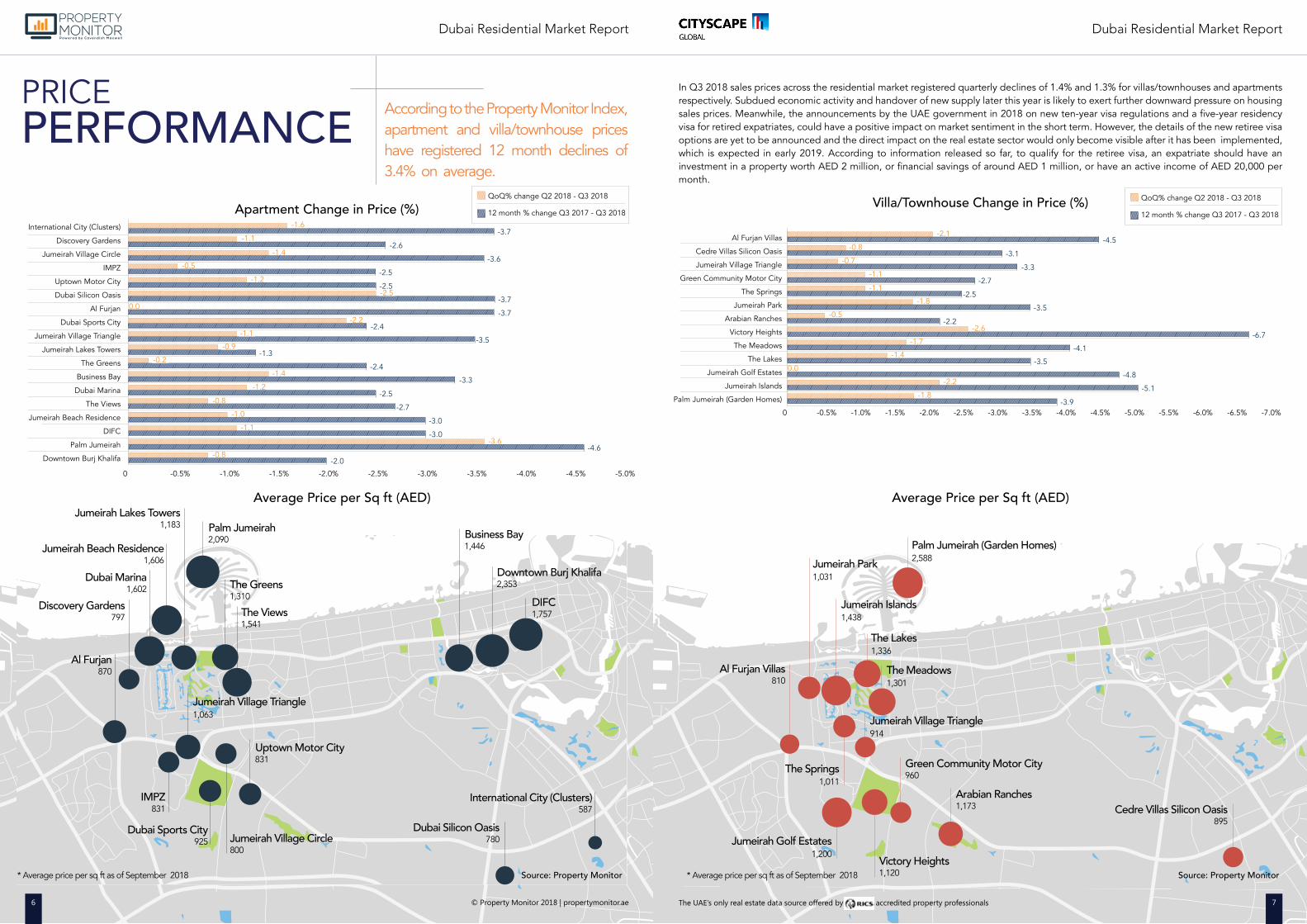

PRICEPERFORMANCE According to the Property Monitor Index,

apartment and villa/townhouse prices have registered 12 month declines of 3.4% on average.

Palm Jumeirah

The Views

Jumeirah Village Circle

Uptown Motor City

The GreensDIFC

International City (Clusters)

Dubai Silicon OasisDubai Sports City

IMPZ

Jumeirah Village Triangle

Al Furjan

Discovery Gardens

Dubai Marina

Jumeirah Beach Residence

Jumeirah Lakes Towers

Downtown Burj Khalifa

Business Bay2,090

1,541

800

831

1,310

1,757

587

780925

831

1,063

870

797

1,602

1,606

1,183

2,353

1,446

International City (Clusters)

Discovery Gardens

Jumeirah Village Circle

IMPZ

Uptown Motor City

Dubai Silicon Oasis

Al Furjan

Dubai Sports City

Jumeirah Village Triangle

Jumeirah Lakes Towers

The Greens

Business Bay

Dubai Marina

The Views

Jumeirah Beach Residence

DIFC

Palm Jumeirah

Downtown Burj Khalifa

0 -0.5% -1.0% -1.5% -2.0% -2.5% -3.0% -3.5% -4.0% -4.5% -5.0%

-1.6

-1.1

-3.6

-3.7

-2.6

-3.0

-3.6

-1.3

-2.5

-4.6

-2.0

-2.5

-2.7

-3.5

-3.7

-3.0

-1.1

-1.1

-0.9

-0.2

-2.5

-2.5

Apartment Change in Price (%)

Average Price per Sq ft (AED)

Source: Property Monitor

-3.7

-1.4

* Average price per sq ft as of September 2018

-2.4

QoQ% change Q2 2018 - Q3 2018

12 month % change Q3 2017 - Q3 2018

6

-3.3

-2.4

-2.1

-0.7

-0.8-4.5

-3.1

-3.3

-3.5

-2.5

-4.8

-3.9

-3.5

-1.7

-2.6

-1.4

0.0

-1.8

-1.8

Average Price per Sq ft (AED)

-1.1

-2.2

-6.7

In Q3 2018 sales prices across the residential market registered quarterly declines of 1.4% and 1.3% for villas/townhouses and apartments respectively. Subdued economic activity and handover of new supply later this year is likely to exert further downward pressure on housing sales prices. Meanwhile, the announcements by the UAE government in 2018 on new ten-year visa regulations and a five-year residency visa for retired expatriates, could have a positive impact on market sentiment in the short term. However, the details of the new retiree visa options are yet to be announced and the direct impact on the real estate sector would only become visible after it has been implemented, which is expected in early 2019. According to information released so far, to qualify for the retiree visa, an expatriate should have an investment in a property worth AED 2 million, or financial savings of around AED 1 million, or have an active income of AED 20,000 per month.

Green Community Motor City

Arabian Ranches

Victory Heights

Cedre Villas Silicon Oasis

Jumeirah Village Triangle

The Springs

Jumeirah Golf Estates

The Meadows

The Lakes

Jumeirah Park

Jumeirah Islands

Palm Jumeirah (Garden Homes)

Al Furjan Villas

960

1,173

1,120

895

914

1,011

1,200

1,301

1,336

1,031

1,438

2,588

810

-2.2

Villa/Townhouse Change in Price (%)

* Average price per sq ft as of September 2018 Source: Property Monitor

Al Furjan Villas

Cedre Villas Silicon Oasis

Jumeirah Village Triangle

Green Community Motor City

The Springs

Jumeirah Park

Arabian Ranches

Victory Heights

The Meadows

The Lakes

Jumeirah Golf Estates

Jumeirah Islands

Palm Jumeirah (Garden Homes)

-1.1

-0.5

-2.7

0 -0.5% -1.0% -1.5% -2.0% -2.5% -3.0% -3.5% -4.0% -4.5% -5.0% -5.5% -6.0% -6.5% -7.0%

7

-4.1

-5.1

QoQ% change Q2 2018 - Q3 2018

12 month % change Q3 2017 - Q3 2018

-0.8

-1.0

-0.8

-2.2

0.0

-1.2

-0.5

-1.4

-1.2

The UAE’s only real estate data source offered by accredited property professionals© Property Monitor 2018 | propertymonitor.ae

© Property Monitor 2018 | propertymonitor.ae 98

Dubai Residential Market Report Dubai Residential Market Report

The UAE’s only real estate data source offered by accredited property professionals

The SpringsJumeirahPark

Dubai MarinaThe Lakes

Al Furjan Villas

Jumeirah Golf Estates

Jumeirah Beach ResidenceThe Greens

The Views

Discovery Gardens

AED 129,906

AED 127,036

AED 96,627

AED 105,000

AED 70,615

AED 71,750

Villa/TownhouseApartment

AED 37,000

AED 53,000

AED 120,627

AED 90,100

AED 64,860

-5.1

AED 115,000

AED 70,000

AED 58,558

-7.7

AED 392,600

AED 189,000

AED 272,650

AED 177,320

AED 146,500

-4.0

-7.9

The MeadowsAED 267,720

AED 210,000

AED 175,560

-5.3

AED 58,640

AED 78,355

AED 99,255

Jumeirah Lakes Towers -6.3

AED 309,000

AED 250,000

AED 244,530

-6.4

AED 171,080

AED 153,240

-5.8

AED 179,200

AED 215,000

AED 230,000

-5.9

JumeirahIslands

AED 260,000

AED 348,800

-4.6Studio Rent 3 BR Rent

1 BR Rent 4 BR Rent

2 BR Rent 5 BR Rent

12 month % change 12 month % change

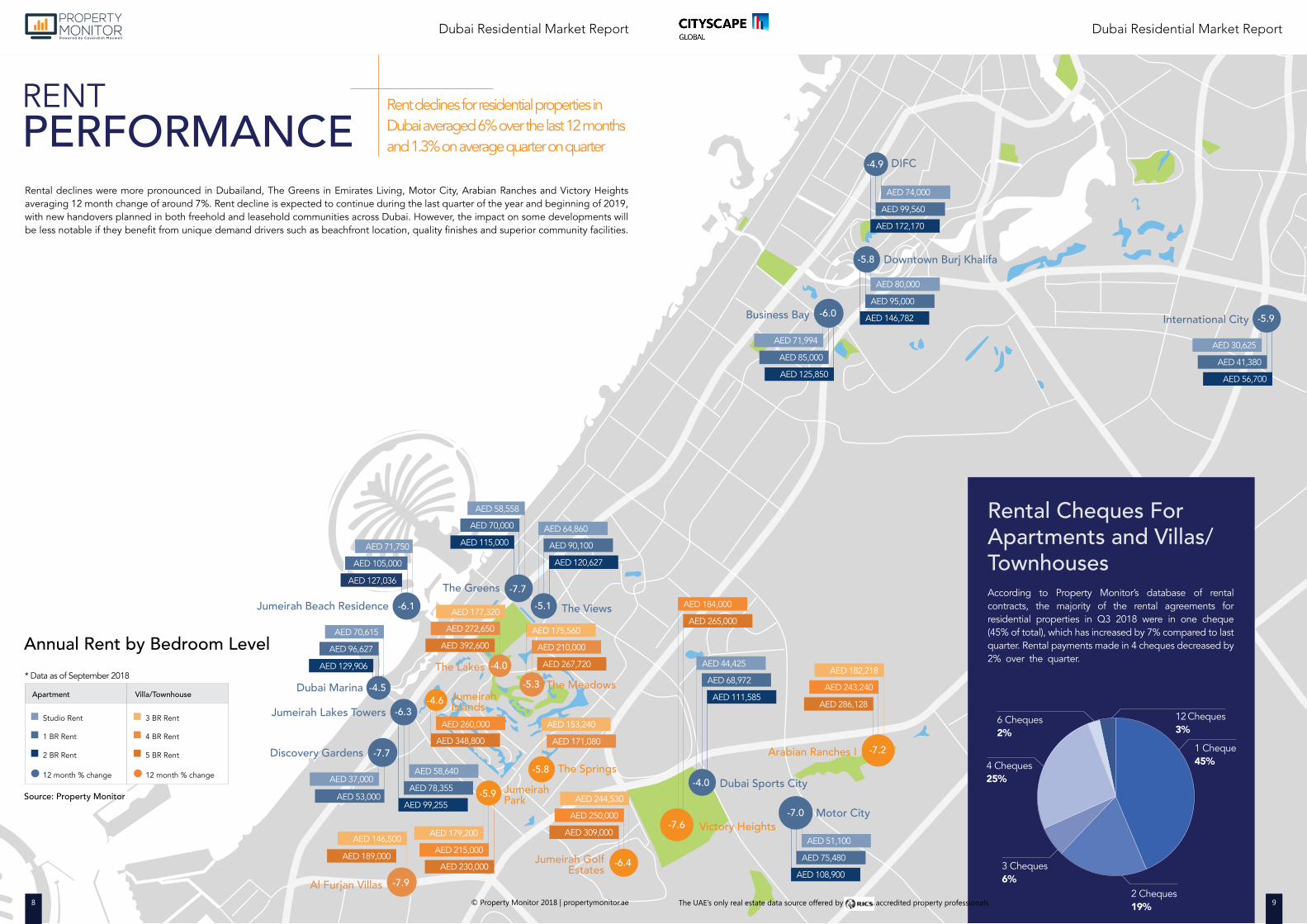

Rental declines were more pronounced in Dubailand, The Greens in Emirates Living, Motor City, Arabian Ranches and Victory Heights averaging 12 month change of around 7%. Rent decline is expected to continue during the last quarter of the year and beginning of 2019, with new handovers planned in both freehold and leasehold communities across Dubai. However, the impact on some developments will be less notable if they benefit from unique demand drivers such as beachfront location, quality finishes and superior community facilities.

* Data as of September 2018

Source: Property Monitor

8

Annual Rent by Bedroom Level

AED 74,000

AED 99,560

AED 172,170

Victory Heights

Arabian Ranches I

International CityBusiness Bay

Dubai Sports City

Downtown Burj Khalifa

Motor City

DIFC-4.9

AED 30,625

AED 111,585

AED 265,000

AED 71,994

AED 41,380

AED 68,972

AED 184,000

AED 85,000

AED 56,700

AED 44,425

AED 125,850

AED 80,000

AED 95,000

AED 146,782

AED 51,100

AED 75,480

AED 108,900

-5.8

-7.0

-5.9

-7.6

-4.0

-6.0

AED 286,128

AED 243,240

AED 182,218

-7.2

9

According to Property Monitor’s database of rental contracts, the majority of the rental agreements for residential properties in Q3 2018 were in one cheque (45% of total), which has increased by 7% compared to last quarter. Rental payments made in 4 cheques decreased by 2% over the quarter.

Rental Cheques For Apartments and Villas/Townhouses

1 Cheque45%

2 Cheques19%

3 Cheques6%

4 Cheques25%

6 Cheques2%

12 Cheques3%

The UAE’s only real estate data source offered by accredited property professionals© Property Monitor 2018 | propertymonitor.ae

RENTPERFORMANCE

Rent declines for residential properties inDubai averaged 6% over the last 12 monthsand 1.3% on average quarter on quarter

-7.7

-4.5

-6.1

© Property Monitor 2018 | propertymonitor.ae 1110

Dubai Residential Market Report Dubai Residential Market Report

The UAE’s only real estate data source offered by accredited property professionals

Q4 2018 - Q1 2019UPCOMING SUPPLY

VILLAS/TOWNHOUSES23%

APARTMENTS77%

Approximately 6,000 residential units have been handed over across Dubai in Q3 2018.

The majority of the handovers during the third quarter of 2018 were in Jumeirah Village Circle, Downtown Burj Khalifa, Town Square, and Dubai South with more than 300 units being handed over in each location. More than 72% of the handed over units were apartments. For the remainder of the year the majority of the upcoming supply is concentrated in Business Bay, Jumeirah Village Circle, Dubai Sports City, Dubai Silicon Oasis and Town Square.

© Property Monitor 2018 | propertymonitor.ae10

PROPERTY MONITOR

SUPPLY TRACKERSupply scheduled to be completed by end of Q1 2019

0 - 200 200 - 400 400 - 600 600 - 1,000

1,000 - 1,500 1,500 - 2,000 2,000+Jumeirah

Golf Estates

JumeirahVillageCircle

Dubai Investments Park

Dubai South

Al Furjan

Barsha Heights

Dubai Marina

Palm Jumeirah

Source: Property Monitor

11

Mohammed bin Rashid City

Akoya Oxygen

Dubai SiliconOasis

International City

Al Jaddaf

Al Qusais Oud Al Muteena

Meydan City

Arabian Ranches II

TownSquare

Living Legends

Dubai Sports CityIMPZ

Business Bay

DowntownBurj Khalifa

The UAE’s only real estate data source offered by accredited property professionals

© Property Monitor 2018 | propertymonitor.ae 1312

Dubai Residential Market Report Dubai Residential Market Report

The UAE’s only real estate data source offered by accredited property professionals

100

90

80

70

60

50

40

30

20

10

0

No.

of T

rans

fers

RESIDENTIAL SALESOVERVIEW

Wad

i Al S

afa

Dub

ai S

outh

Moh

amm

ed B

in

Rash

id C

ity

100

90

80

70

60

50

40

30

20

10

0

No.

of T

rans

fers

Emira

tes

Livi

ng

Vill

a N

ova

Ako

yaO

xyge

n

Al F

urja

n

Tow

n Sq

uare

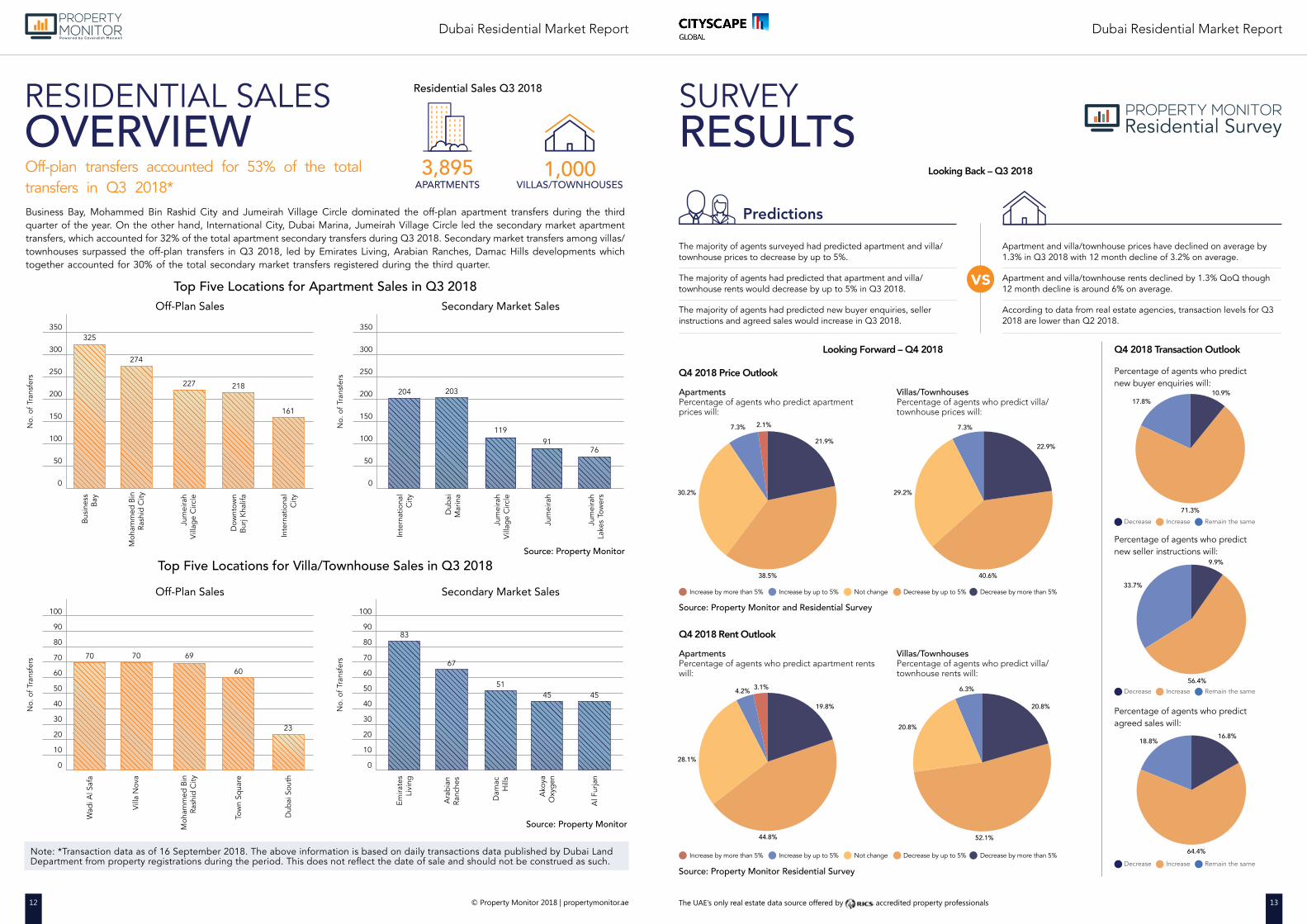

Business Bay, Mohammed Bin Rashid City and Jumeirah Village Circle dominated the off-plan apartment transfers during the third quarter of the year. On the other hand, International City, Dubai Marina, Jumeirah Village Circle led the secondary market apartment transfers, which accounted for 32% of the total apartment secondary transfers during Q3 2018. Secondary market transfers among villas/townhouses surpassed the off-plan transfers in Q3 2018, led by Emirates Living, Arabian Ranches, Damac Hills developments which together accounted for 30% of the total secondary market transfers registered during the third quarter.

VILLAS/TOWNHOUSES1,000

Off-Plan Sales

Secondary Market Sales

Secondary Market Sales

APARTMENTS3,895

Top Five Locations for Apartment Sales in Q3 2018

Residential Sales Q3 2018

Top Five Locations for Villa/Townhouse Sales in Q3 2018Source: Property Monitor

Source: Property Monitor

No.

of T

rans

fers

Off-Plan Sales

350

300

250

200

150

100

50

0

Bus

ines

sB

ay

Dow

ntow

nB

urj K

halif

a

Jum

eira

hV

illag

e C

ircle

325

274

227 218

161

70 70 69

60

23

83

67

5145 45

No.

of T

rans

fers

Inte

rnat

iona

lC

ity

350

300

250

200

150

100

50

0

Jum

eira

hV

illag

e C

ircle

Jum

eira

h

Jum

eira

hLa

kes

Tow

ers

204 203

11991

76D

ubai

M

arin

a

Off-plan transfers accounted for 53% of the total transfers in Q3 2018*

Ara

bian

Ranc

hes

Dam

acH

ills

Note: *Transaction data as of 16 September 2018. The above information is based on daily transactions data published by Dubai Land Department from property registrations during the period. This does not reflect the date of sale and should not be construed as such.

SURVEYRESULTS

vsThe majority of agents surveyed had predicted apartment and villa/townhouse prices to decrease by up to 5%.

Apartment and villa/townhouse prices have declined on average by1.3% in Q3 2018 with 12 month decline of 3.2% on average.

The majority of agents had predicted that apartment and villa/townhouse rents would decrease by up to 5% in Q3 2018.

Apartment and villa/townhouse rents declined by 1.3% QoQ though12 month decline is around 6% on average.

The majority of agents had predicted new buyer enquiries, seller instructions and agreed sales would increase in Q3 2018.

According to data from real estate agencies, transaction levels for Q32018 are lower than Q2 2018.

Predictions

Q4 2018 Price Outlook

Looking Forward – Q4 2018

Looking Back – Q3 2018

Q4 2018 Rent Outlook

ApartmentsPercentage of agents who predict apartment prices will:

ApartmentsPercentage of agents who predict apartment rents will:

Villas/TownhousesPercentage of agents who predict villa/townhouse prices will:

Villas/TownhousesPercentage of agents who predict villa/townhouse rents will:

Increase by more than 5% Increase by up to 5% Not change Decrease by up to 5% Decrease by more than 5%

Increase by more than 5% Increase by up to 5% Not change Decrease by up to 5% Decrease by more than 5%

Source: Property Monitor and Residential Survey

Source: Property Monitor Residential Survey

21.9%

30.2%

2.1%

38.5%

7.3%

3.1%

28.1%

44.8%

19.8%

4.2%

22.9%

29.2%

40.6%

7.3%

20.8%

20.8%

52.1%

6.3%

Q4 2018 Transaction Outlook

Percentage of agents who predict new buyer enquiries will:

Percentage of agents who predict new seller instructions will:

Percentage of agents who predict agreed sales will:

Decrease Increase Remain the same

Decrease Increase Remain the same

Decrease Increase Remain the same

17.8%10.9%

33.7%

56.4%

9.9%

16.8%

64.4%

18.8%

71.3%

Moh

amm

ed B

in

Rash

id C

ity

Inte

rnat

iona

lC

ity

© Property Monitor 2018 | propertymonitor.ae 1514

Dubai Residential Market Report Dubai Residential Market Report

The UAE’s only real estate data source offered by accredited property professionals

METHODOLOGYSale prices and rents are derived from Property Monitor (www.propertymonitor.ae), a real estate intelligence platform established by Cavendish Maxwell in 2014. Property Monitor provides real-time, market-wide transactional data and trends. Working with governments, agencies, banks, developers and corporate investors, it provides deeper insight into real estate advisory, investment, and lending activities. The average sales price per sq ft is based on the Property Monitor Index which incorporates signed contracts, registered transactions, valuations and listings verified by Cavendish Maxwell’s market leading valuation department.

Property Monitor Residential Survey is a quarterly study of agent opinion designed to identify residential market sentiment. This research highlights how new enquiries, leasing activity and transactions, among other metrics, change from quarter to quarter with agent predictions compared to actual real market performance.

Supply projections for residential projects are based on the Property Monitor Supply Tracker which tracks supply in real time, regular tracking of construction projects, new launches and delays. This is achieved through site inspections as well as regular feedback from developers, contractors, Cavendish Maxwell’s building consultancy team and related government entities.

Disclaimer:The information and analysis contained in this report has been obtained from a variety of sources generally regarded to be reliable and assumptions which are considered reasonable, and which were current at the time of undertaking market research, but no representation is made as to their accuracy or completeness. We reserve the right to vary our methodology and to edit or discontinue the indices at any time, for regulatory or other reasons.

The report and analysis does not purport to represent a formal valuation of any property interest and must not be construed as such. Such analysis including forward looking statements are opinions and estimates only and are based on a wide range of variables which may not be capable of being determined with accuracy. Variation in any one of these variables can have a material impact on the analysis and we draw your attention to this. Property Monitor does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this report.

OUR PRODUCTS

PEOPLE

Jay Grant MSc IRRV (Hons) MRICSFounder and Chairman

Nigel Armstrong FMAATChief Executive Officer

Moe AbeidatChief Technology OfficerProperty Monitor

Sofia Underabi MRICS AAPIPartnerHead of Residential Valuation

Manika Dhama BA (Hons), MBAAssociate PartnerStrategic Consulting and Research

Andrew Love MA (Hons) MRICSPartnerHead of Investment and Commercial Agency

MarketData

PropertyMonitor Index

MarketStatistics

HeatMaps

Project andSupply Tracker

Service Feeindex

Agent Tools and Custom Reports

Bank Portfolio Review

Area Risk Matrix

ValuationTracker

Automated Valuation Model

(AVM)

Application Programming Interface (API)

Dubai

2205 Marina PlazaDubai MarinaP.O. Box 118624DubaiUnited Arab Emirates

T: +971 4 453 9525 E: [email protected]

Abu Dhabi

605 West Tower, Abu Dhabi MallTourist Club AreaP.O. Box 126609Abu DhabiUnited Arab Emirates

T: +971 2 448 4677E: [email protected]

Partners

Find us on

Muscat

Villa 836, Way 3012Al SaroojP.O. Box 3438MuscatSultanate of Oman

T: +968 99 445 917E: [email protected]

propertymonitor.ae

Property-Monitor