turkey: quarterly banking & financial stability monitor · turkey quarterly banking &...

TRANSCRIPT

Turkey: Quarterly Banking &

Financial Stability Monitor

March 2018 Deniz Ergun

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

Key messages

1. Since 3Q 2017, credit growth converged to its

historical average and stabilized at these levels as a

result of the expected normalization

2. The increase in FX deposits and the acceleration in

TL loans urged banks to find additional TL funding

causing a further increase in interest rates

3. The banking sector preserves its strong liquidity

position against possible shocks with high Liquidty

Coverage Ratios

4. The asset quality of the banking sector remains

strong. With the push of the credit channel and the

pick up in economic activity, the decreasing amount

of additions to NPLs and write-offs as well as the

restructuring processes contributed to the

preservation of asset quality

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

Global

Improved Bank Lending

Conditions in EMs

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

4 Source: IIF, Garanti Research

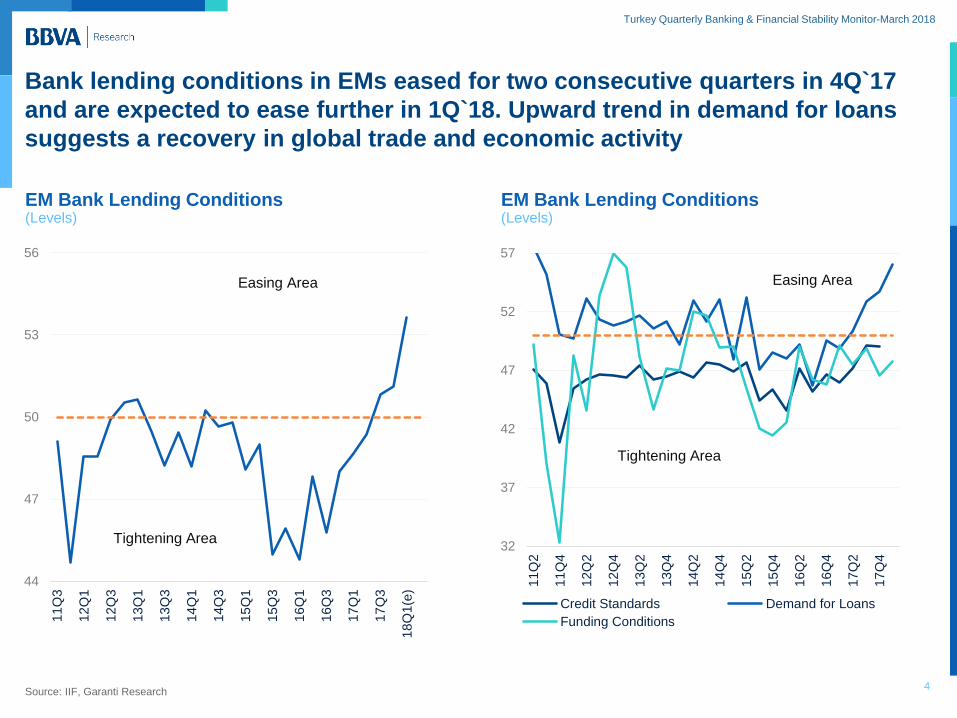

EM Bank Lending Conditions (Levels)

Bank lending conditions in EMs eased for two consecutive quarters in 4Q`17

and are expected to ease further in 1Q`18. Upward trend in demand for loans

suggests a recovery in global trade and economic activity

44

47

50

53

56

11

Q3

12

Q1

12

Q3

13

Q1

13

Q3

14

Q1

14

Q3

15

Q1

15

Q3

16

Q1

16

Q3

17

Q1

17

Q3

18

Q1(e

)

Easing Area

Tightening Area 32

37

42

47

52

57

11

Q2

11

Q4

12

Q2

12

Q4

13

Q2

13

Q4

14

Q2

14

Q4

15

Q2

15

Q4

16

Q2

16

Q4

17

Q2

17

Q4

Credit Standards Demand for Loans

Funding Conditions

Easing Area

Tightening Area

EM Bank Lending Conditions (Levels)

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

5 Source: IIF, Garanti Research

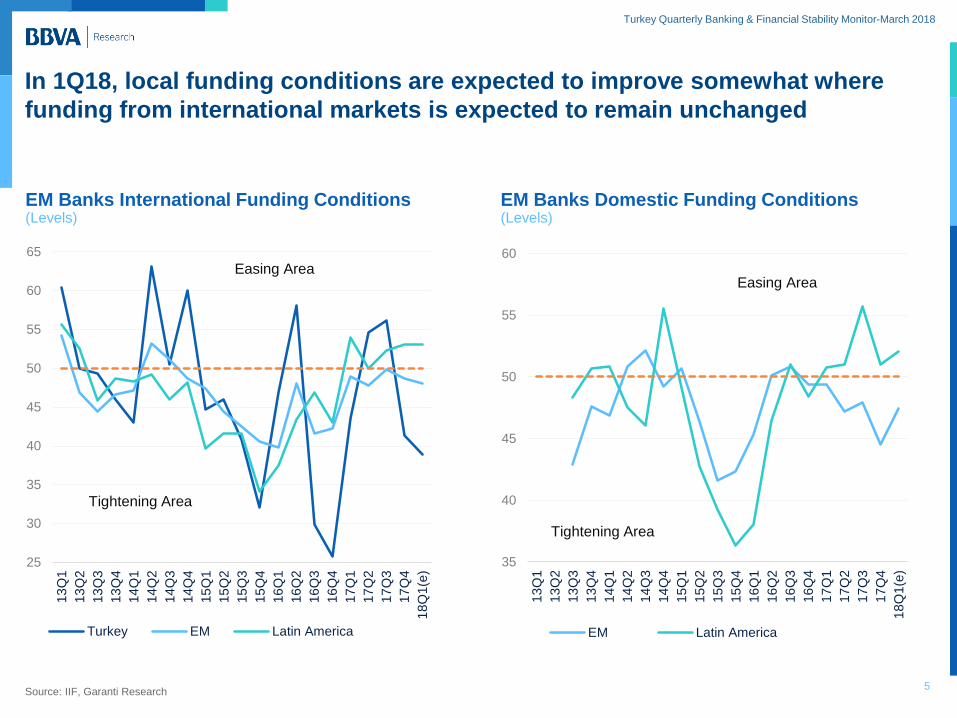

EM Banks International Funding Conditions (Levels)

In 1Q18, local funding conditions are expected to improve somewhat where

funding from international markets is expected to remain unchanged

EM Banks Domestic Funding Conditions (Levels)

25

30

35

40

45

50

55

60

65

13

Q1

13

Q2

13

Q3

13

Q4

14

Q1

14

Q2

14

Q3

14

Q4

15

Q1

15

Q2

15

Q3

15

Q4

16

Q1

16

Q2

16

Q3

16

Q4

17

Q1

17

Q2

17

Q3

17

Q4

18

Q1(e

)

Turkey EM Latin America

Easing Area

Tightening Area

35

40

45

50

55

60

13

Q1

13

Q2

13

Q3

13

Q4

14

Q1

14

Q2

14

Q3

14

Q4

15

Q1

15

Q2

15

Q3

15

Q4

16

Q1

16

Q2

16

Q3

16

Q4

17

Q1

17

Q2

17

Q3

17

Q4

18

Q1(e

)

EM Latin America

Easing Area

Tightening Area

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

6 Source: IIF, Garanti Research

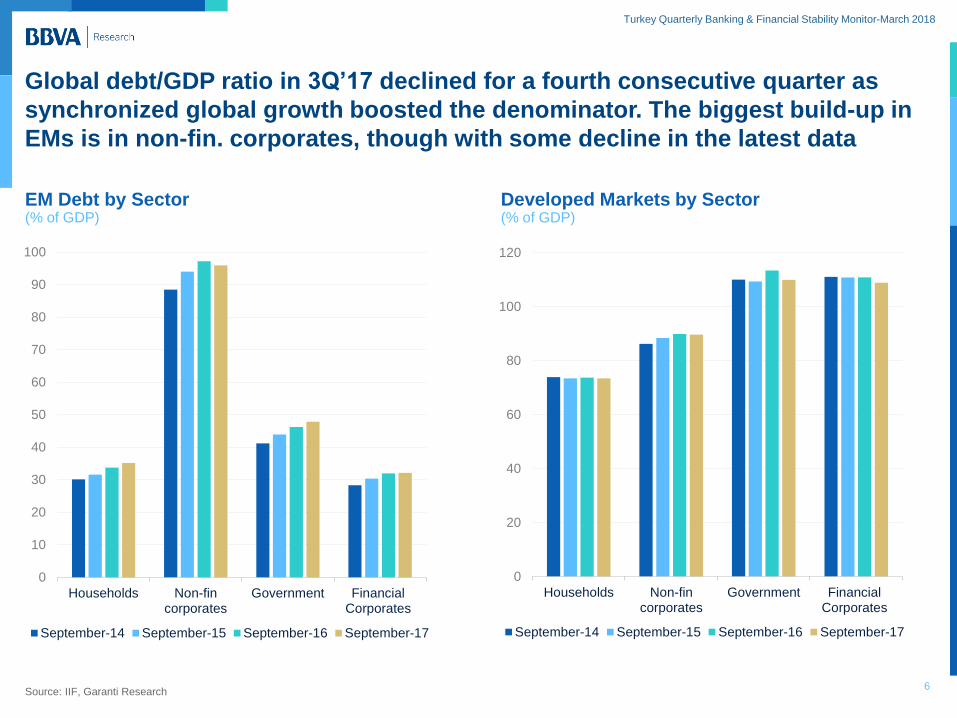

EM Debt by Sector (% of GDP)

Global debt/GDP ratio in 3Q’17 declined for a fourth consecutive quarter as

synchronized global growth boosted the denominator. The biggest build-up in

EMs is in non-fin. corporates, though with some decline in the latest data

Developed Markets by Sector (% of GDP)

0

10

20

30

40

50

60

70

80

90

100

Households Non-fincorporates

Government FinancialCorporates

September-14 September-15 September-16 September-17

0

20

40

60

80

100

120

Households Non-fincorporates

Government FinancialCorporates

September-14 September-15 September-16 September-17

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

7 Source: BIS, Garanti Research

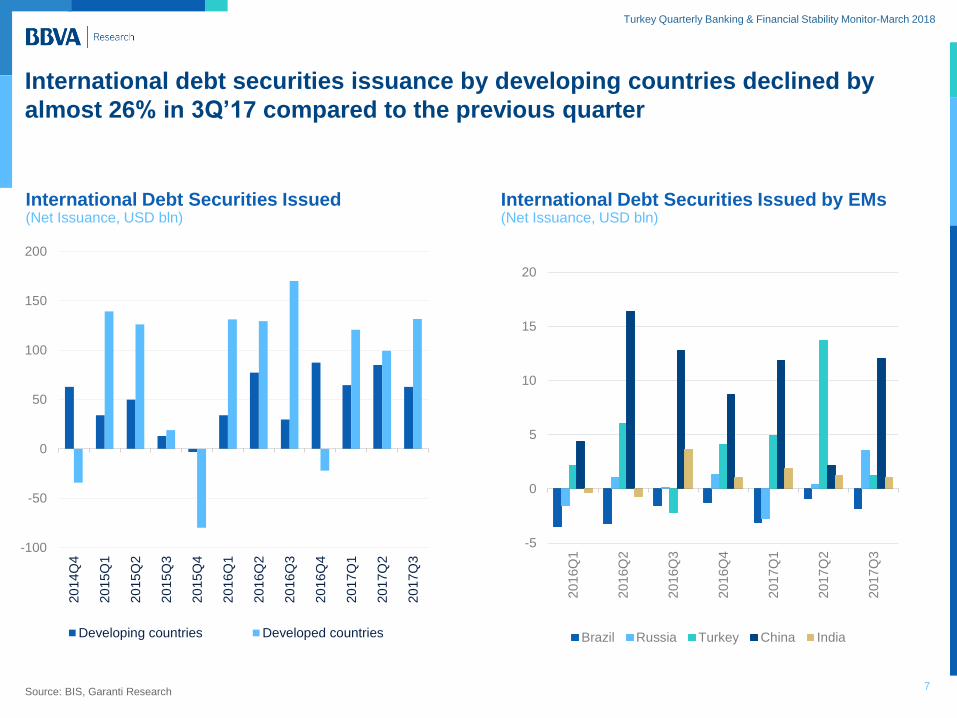

International Debt Securities Issued (Net Issuance, USD bln)

International debt securities issuance by developing countries declined by

almost 26% in 3Q’17 compared to the previous quarter

International Debt Securities Issued by EMs (Net Issuance, USD bln)

-100

-50

0

50

100

150

200

20

14Q

4

20

15Q

1

20

15Q

2

20

15Q

3

20

15Q

4

20

16Q

1

20

16Q

2

20

16Q

3

20

16Q

4

20

17Q

1

20

17Q

2

20

17Q

3

Developing countries Developed countries

-5

0

5

10

15

20

20

16Q

1

20

16Q

2

20

16Q

3

20

16Q

4

20

17Q

1

20

17Q

2

20

17Q

3

Brazil Russia Turkey China India

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

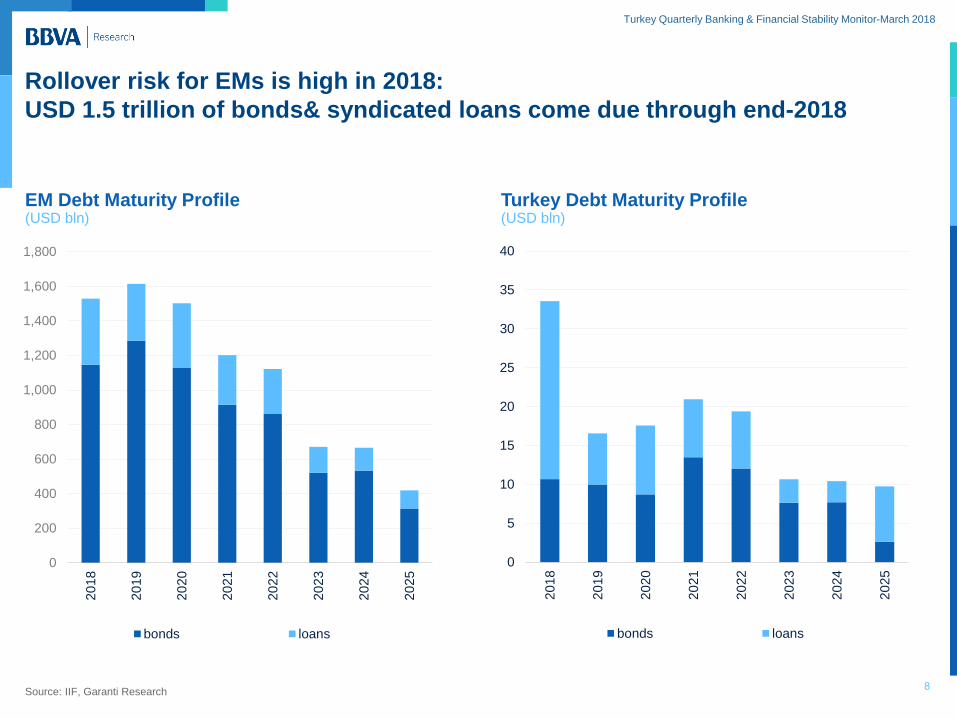

8 Source: IIF, Garanti Research

EM Debt Maturity Profile (USD bln)

Rollover risk for EMs is high in 2018:

USD 1.5 trillion of bonds& syndicated loans come due through end-2018

Turkey Debt Maturity Profile (USD bln)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

bonds loans

0

5

10

15

20

25

30

35

40

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

bonds loans

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

9 Source: BIS, Garanti Research

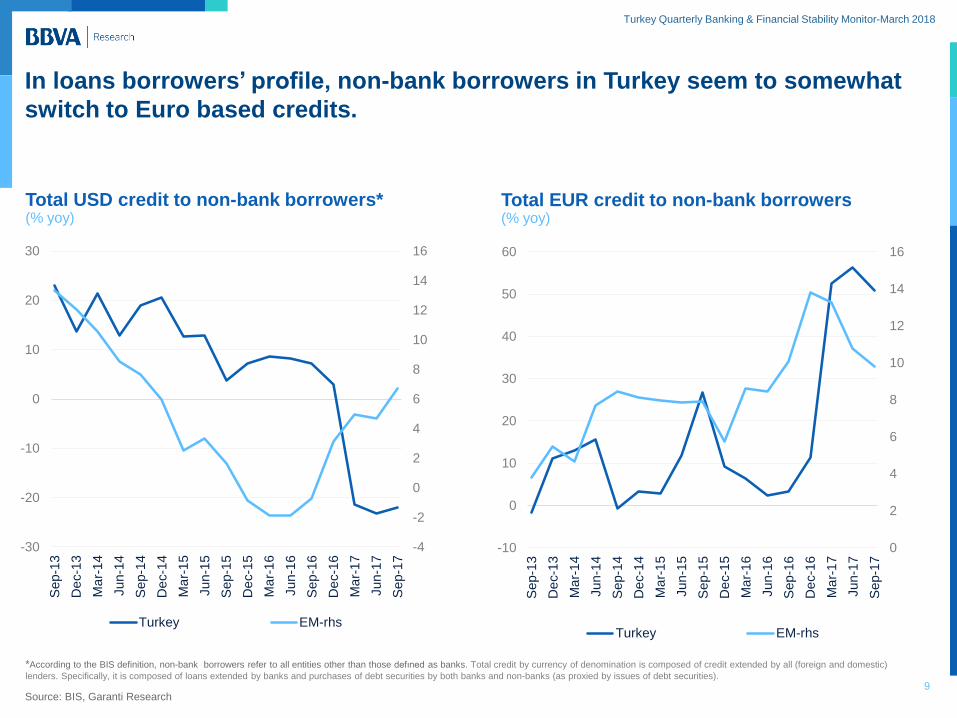

Total USD credit to non-bank borrowers* (% yoy)

In loans borrowers’ profile, non-bank borrowers in Turkey seem to somewhat

switch to Euro based credits.

Total EUR credit to non-bank borrowers (% yoy)

-4

-2

0

2

4

6

8

10

12

14

16

-30

-20

-10

0

10

20

30

Sep-1

3

De

c-1

3

Ma

r-1

4

Jun-1

4

Sep-1

4

De

c-1

4

Ma

r-1

5

Jun-1

5

Sep-1

5

De

c-1

5

Ma

r-1

6

Jun-1

6

Sep-1

6

De

c-1

6

Ma

r-1

7

Jun-1

7

Sep-1

7

Turkey EM-rhs

0

2

4

6

8

10

12

14

16

-10

0

10

20

30

40

50

60

Sep-1

3

De

c-1

3

Ma

r-1

4

Jun-1

4

Sep-1

4

De

c-1

4

Ma

r-1

5

Jun-1

5

Sep-1

5

De

c-1

5

Ma

r-1

6

Jun-1

6

Sep-1

6

De

c-1

6

Ma

r-1

7

Jun-1

7

Sep-1

7

Turkey EM-rhs

*According to the BIS definition, non-bank borrowers refer to all entities other than those defıned as banks. Total credit by currency of denomination is composed of credit extended by all (foreign and domestic)

lenders. Specifically, it is composed of loans extended by banks and purchases of debt securities by both banks and non-banks (as proxied by issues of debt securities).

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

Turkey:

Monetary Policy

and Interest

Rates

Tight Monetary

Policy Stance,

Contained Monetary

Transmission

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

11

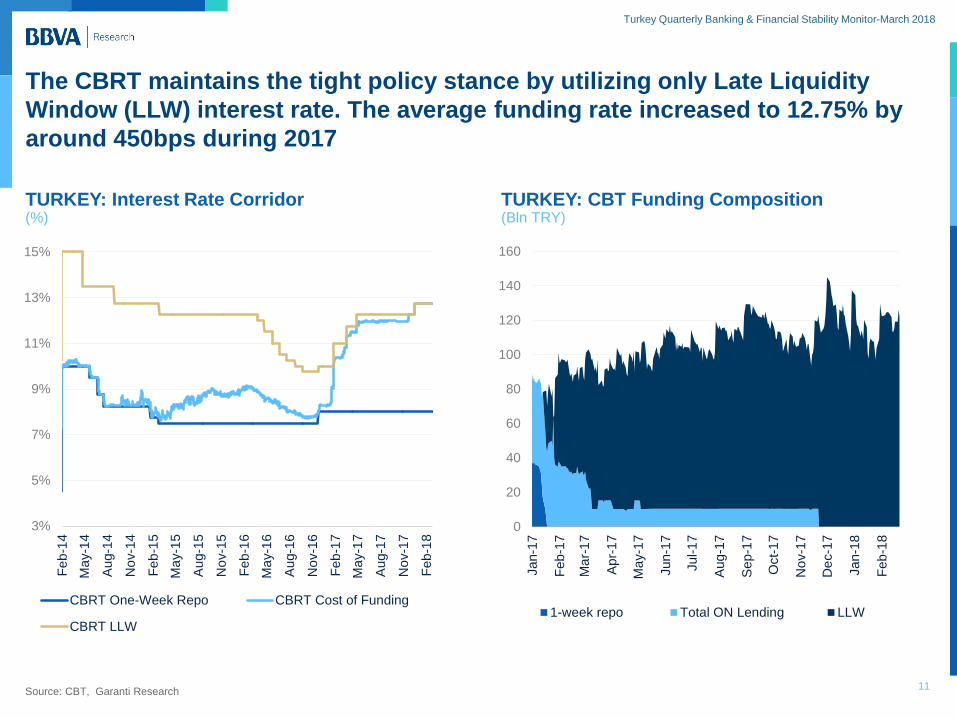

The CBRT maintains the tight policy stance by utilizing only Late Liquidity

Window (LLW) interest rate. The average funding rate increased to 12.75% by

around 450bps during 2017

TURKEY: Interest Rate Corridor (%)

Source: CBT, Garanti Research

TURKEY: CBT Funding Composition (Bln TRY)

3%

5%

7%

9%

11%

13%

15%

Feb

-14

Ma

y-1

4

Aug-1

4

No

v-1

4

Feb

-15

Ma

y-1

5

Aug-1

5

No

v-1

5

Feb

-16

Ma

y-1

6

Aug-1

6

No

v-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

Hu

nd

red

s

CBRT One-Week Repo CBRT Cost of Funding

CBRT LLW

0

20

40

60

80

100

120

140

160

Jan-1

7

Feb

-17

Ma

r-1

7

Apr-

17

Ma

y-1

7

Jun-1

7

Jul-1

7

Aug-1

7

Sep-1

7

Oct-

17

No

v-1

7

De

c-1

7

Jan-1

8

Feb

-18

1-week repo Total ON Lending LLW

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

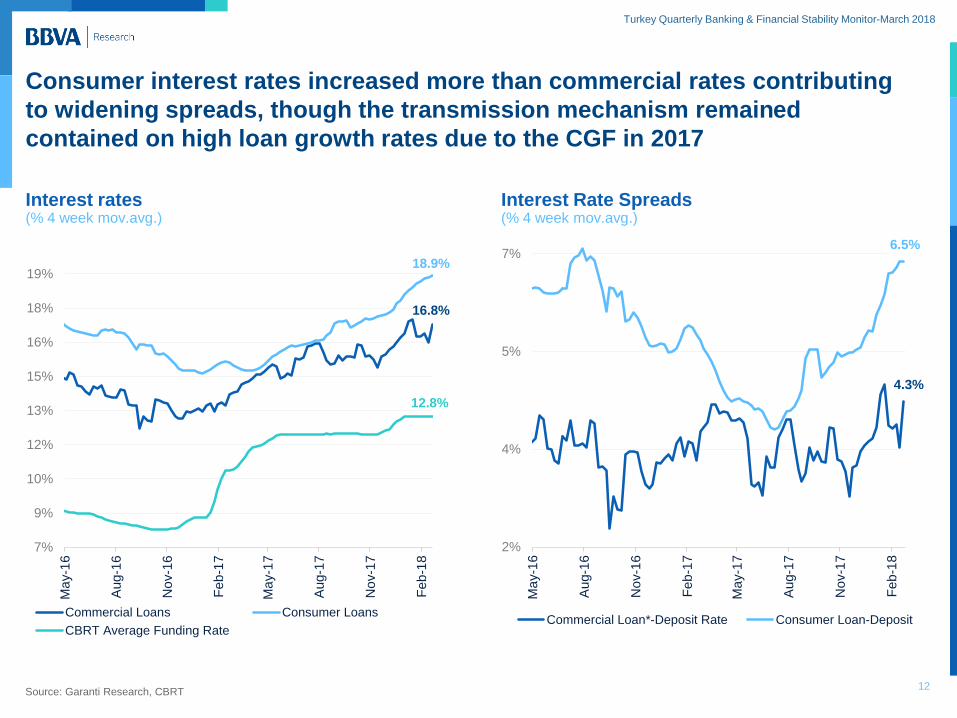

Consumer interest rates increased more than commercial rates contributing

to widening spreads, though the transmission mechanism remained

contained on high loan growth rates due to the CGF in 2017

12 Source: Garanti Research, CBRT

Interest rates (% 4 week mov.avg.)

Interest Rate Spreads (% 4 week mov.avg.)

4.3%

6.5%

2%

4%

5%

7%

Ma

y-1

6

Aug-1

6

No

v-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

Commercial Loan*-Deposit Rate Consumer Loan-Deposit

16.8%

18.9%

12.8%

7%

9%

10%

12%

13%

15%

16%

18%

19%

Ma

y-1

6

Aug-1

6

No

v-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

Commercial Loans Consumer Loans

CBRT Average Funding Rate

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

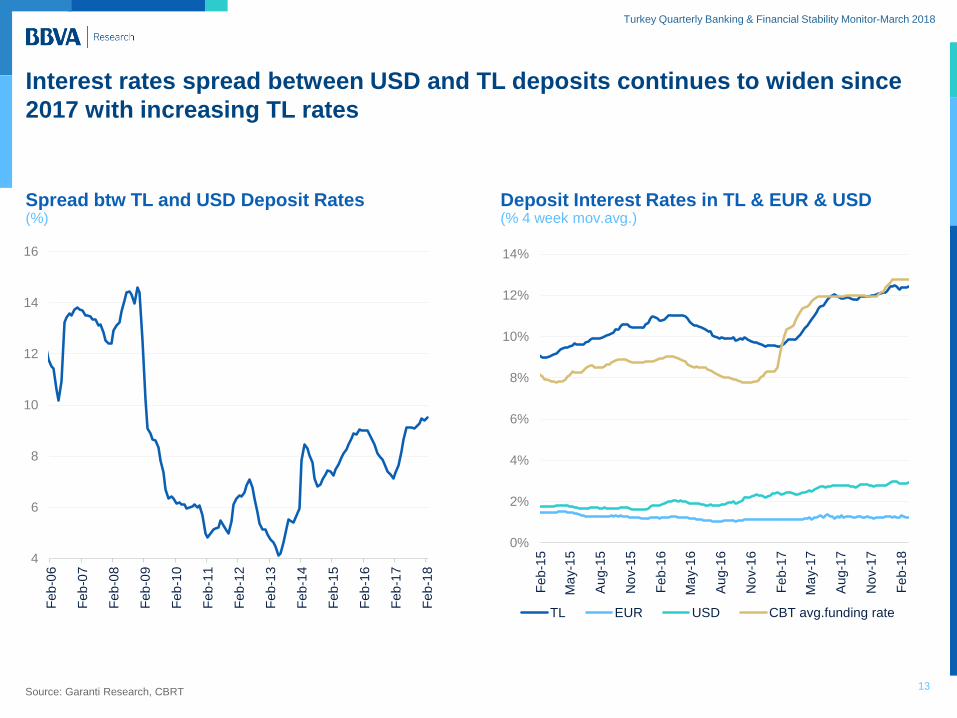

Interest rates spread between USD and TL deposits continues to widen since

2017 with increasing TL rates

13

Spread btw TL and USD Deposit Rates (%)

Deposit Interest Rates in TL & EUR & USD (% 4 week mov.avg.)

4

6

8

10

12

14

16

Feb

-06

Feb

-07

Feb

-08

Feb

-09

Feb

-10

Feb

-11

Feb

-12

Feb

-13

Feb

-14

Feb

-15

Feb

-16

Feb

-17

Feb

-18

0%

2%

4%

6%

8%

10%

12%

14%

Feb

-15

Ma

y-1

5

Aug-1

5

No

v-1

5

Feb

-16

Ma

y-1

6

Aug-1

6

No

v-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

TL EUR USD CBT avg.funding rate

Source: Garanti Research, CBRT

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

Turkish Banking

Sector: Credit

Developments

Normalization in Credits

Decline in NPLs

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

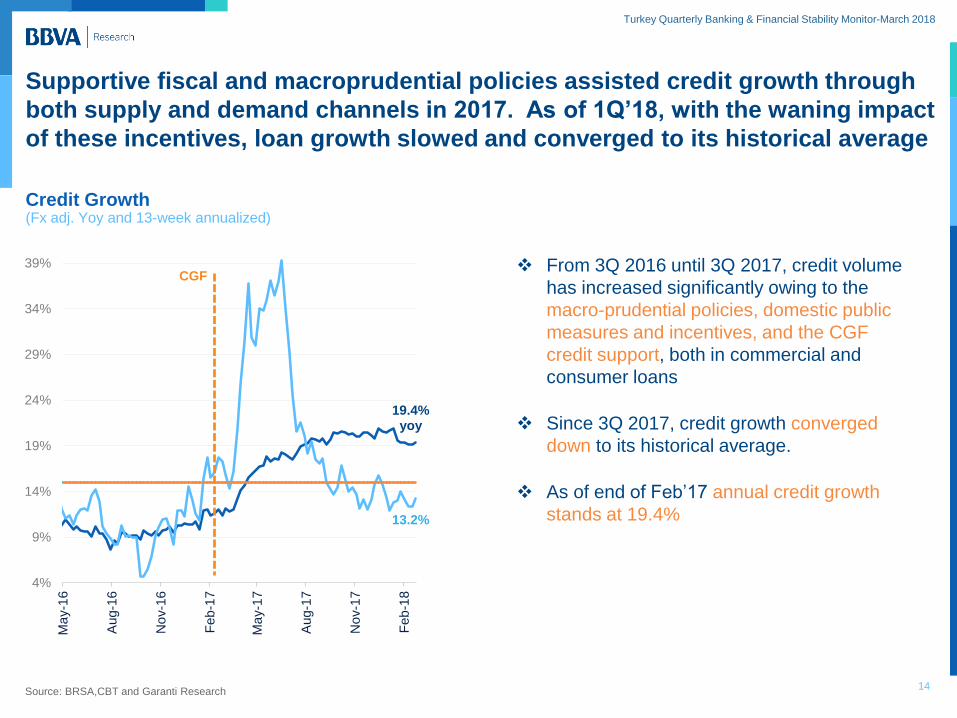

Supportive fiscal and macroprudential policies assisted credit growth through

both supply and demand channels in 2017. As of 1Q’18, with the waning impact

of these incentives, loan growth slowed and converged to its historical average

Credit Growth (Fx adj. Yoy and 13-week annualized)

Source: BRSA,CBT and Garanti Research

19.4% yoy

13.2%

4%

9%

14%

19%

24%

29%

34%

39%

Ma

y-1

6

Aug-1

6

No

v-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

CGF

14

From 3Q 2016 until 3Q 2017, credit volume

has increased significantly owing to the

macro-prudential policies, domestic public

measures and incentives, and the CGF

credit support, both in commercial and

consumer loans

Since 3Q 2017, credit growth converged

down to its historical average.

As of end of Feb’17 annual credit growth

stands at 19.4%

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

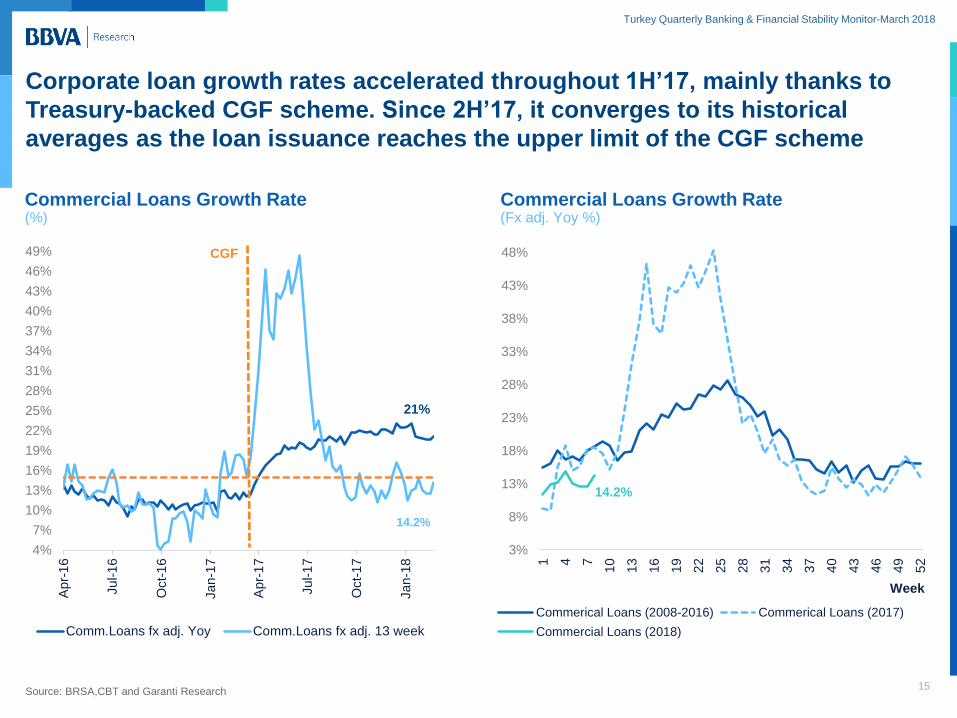

Corporate loan growth rates accelerated throughout 1H’17, mainly thanks to

Treasury-backed CGF scheme. Since 2H’17, it converges to its historical

averages as the loan issuance reaches the upper limit of the CGF scheme

Commercial Loans Growth Rate (%)

Source: BRSA,CBT and Garanti Research

Commercial Loans Growth Rate (Fx adj. Yoy %)

21%

14.2%

4%

7%

10%

13%

16%

19%

22%

25%

28%

31%

34%

37%

40%

43%

46%

49%

Apr-

16

Jul-1

6

Oct-

16

Jan-1

7

Apr-

17

Jul-1

7

Oct-

17

Jan-1

8

CGF

Comm.Loans fx adj. Yoy Comm.Loans fx adj. 13 week

14.2%

3%

8%

13%

18%

23%

28%

33%

38%

43%

48%

1 4 7

10

13

16

19

22

25

28

31

34

37

40

43

46

49

52

Week

Commerical Loans (2008-2016) Commerical Loans (2017)

Commercial Loans (2018)

15

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

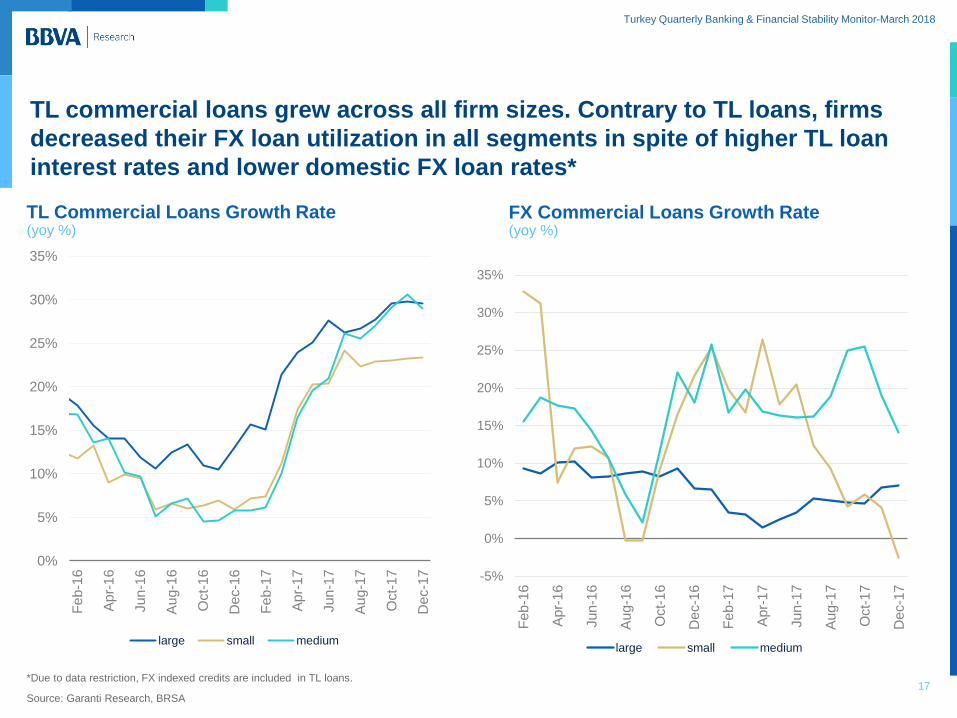

TL commercial loans grew across all firm sizes. Contrary to TL loans, firms

decreased their FX loan utilization in all segments in spite of higher TL loan

interest rates and lower domestic FX loan rates*

17

0%

5%

10%

15%

20%

25%

30%

35%

Fe

b-1

6

Apr-

16

Jun

-16

Au

g-1

6

Oct-

16

De

c-1

6

Fe

b-1

7

Ap

r-1

7

Jun

-17

Aug-1

7

Oct-

17

De

c-1

7

large small medium

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Fe

b-1

6

Ap

r-1

6

Jun

-16

Au

g-1

6

Oct-

16

De

c-1

6

Fe

b-1

7

Ap

r-1

7

Jun

-17

Au

g-1

7

Oct-

17

De

c-1

7

large small medium

Source: Garanti Research, BRSA

*Due to data restriction, FX indexed credits are included in TL loans.

TL Commercial Loans Growth Rate (yoy %)

FX Commercial Loans Growth Rate (yoy %)

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

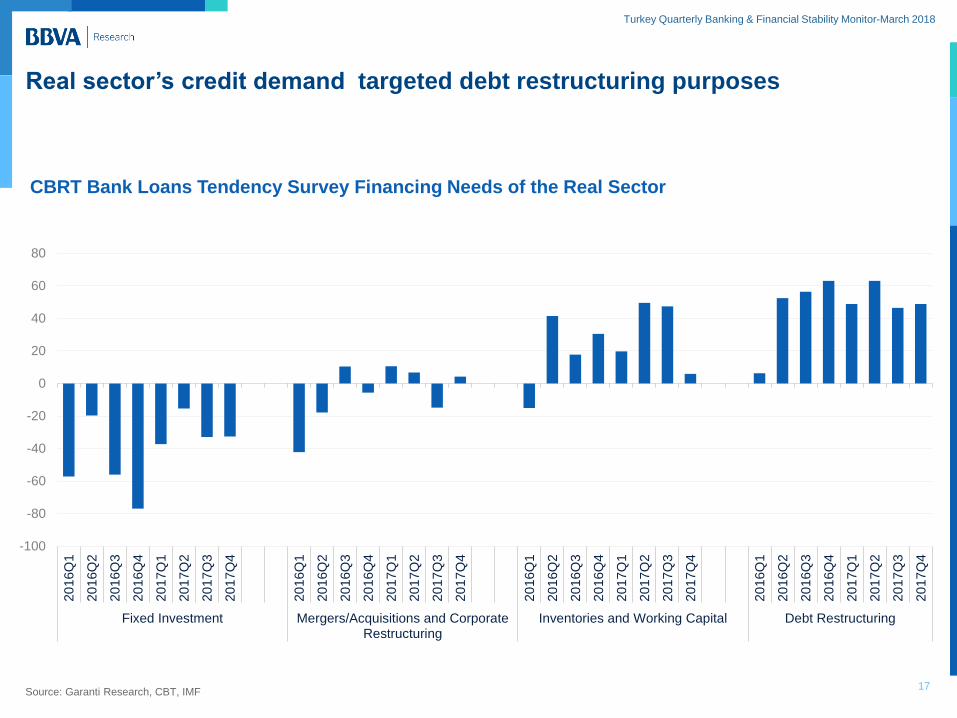

Real sector’s credit demand targeted debt restructuring purposes

Source: Garanti Research, CBT, IMF

-100

-80

-60

-40

-20

0

20

40

60

80

20

16Q

1

20

16Q

2

20

16Q

3

20

16Q

4

20

17Q

1

20

17Q

2

20

17Q

3

20

17Q

4

20

16Q

1

20

16Q

2

20

16Q

3

20

16Q

4

20

17Q

1

20

17Q

2

20

17Q

3

20

17Q

4

20

16Q

1

20

16Q

2

20

16Q

3

20

16Q

4

20

17Q

1

20

17Q

2

20

17Q

3

20

17Q

4

20

16Q

1

20

16Q

2

20

16Q

3

20

16Q

4

20

17Q

1

20

17Q

2

20

17Q

3

20

17Q

4

Fixed Investment Mergers/Acquisitions and CorporateRestructuring

Inventories and Working Capital Debt Restructuring

17

CBRT Bank Loans Tendency Survey Financing Needs of the Real Sector

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

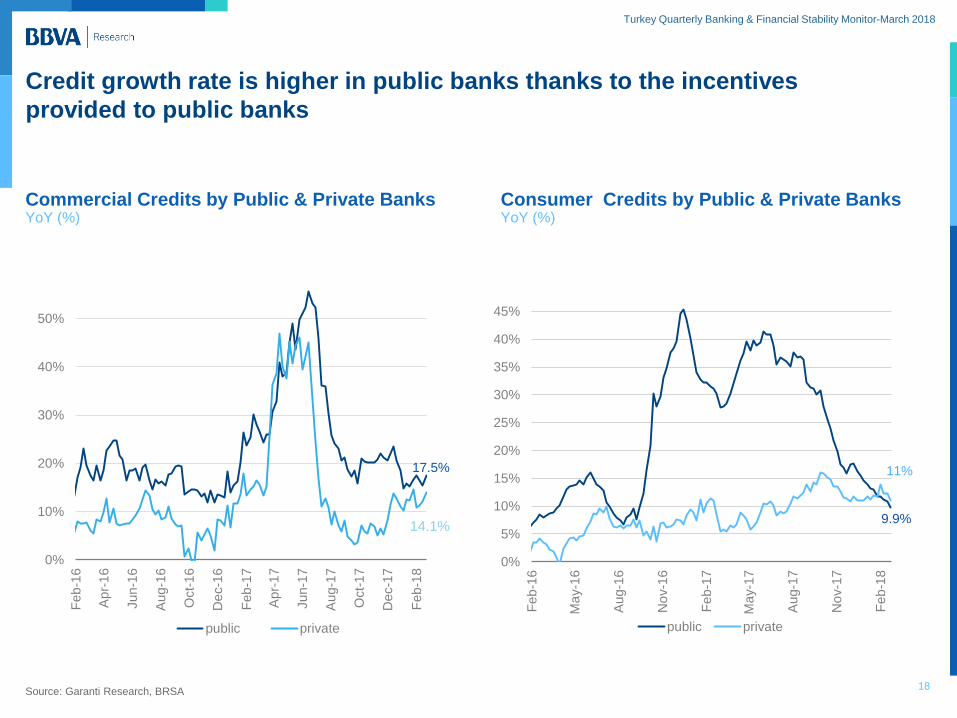

Credit growth rate is higher in public banks thanks to the incentives

provided to public banks

Commercial Credits by Public & Private Banks YoY (%)

Source: Garanti Research, BRSA

Consumer Credits by Public & Private Banks YoY (%)

18

17.5%

14.1%

0%

10%

20%

30%

40%

50%

Feb

-16

Apr-

16

Jun-1

6

Aug-1

6

Oct-

16

De

c-1

6

Feb

-17

Apr-

17

Jun-1

7

Aug-1

7

Oct-

17

De

c-1

7

Feb

-18

public private

11%

9.9%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Feb

-16

Ma

y-1

6

Aug-1

6

No

v-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

public private

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

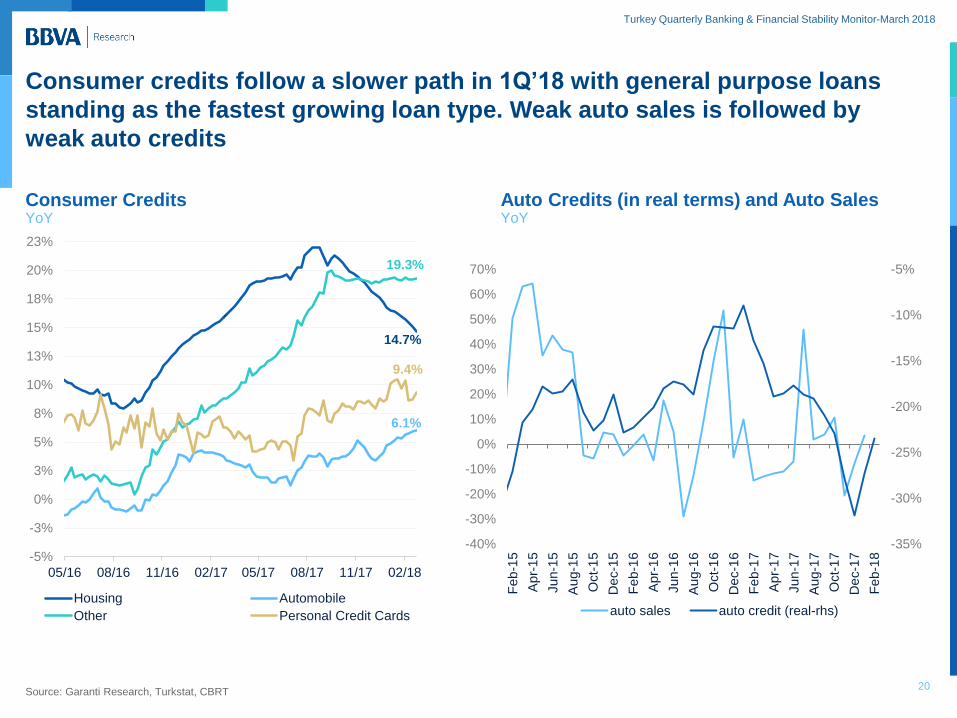

Consumer credits follow a slower path in 1Q’18 with general purpose loans

standing as the fastest growing loan type. Weak auto sales is followed by

weak auto credits

20 Source: Garanti Research, Turkstat, CBRT

Consumer Credits YoY

Auto Credits (in real terms) and Auto Sales YoY

6.1%

14.7%

19.3%

9.4%

-5%

-3%

0%

3%

5%

8%

10%

13%

15%

18%

20%

23%

05/16 08/16 11/16 02/17 05/17 08/17 11/17 02/18

Housing Automobile

Other Personal Credit Cards

Series5

-35%

-30%

-25%

-20%

-15%

-10%

-5%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

Feb

-15

Apr-

15

Jun-1

5

Aug-1

5

Oct-

15

De

c-1

5

Feb

-16

Apr-

16

Jun-1

6

Aug-1

6

Oct-

16

De

c-1

6

Feb

-17

Apr-

17

Jun-1

7

Aug-1

7

Oct-

17

De

c-1

7

Feb

-18

auto sales auto credit (real-rhs)

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

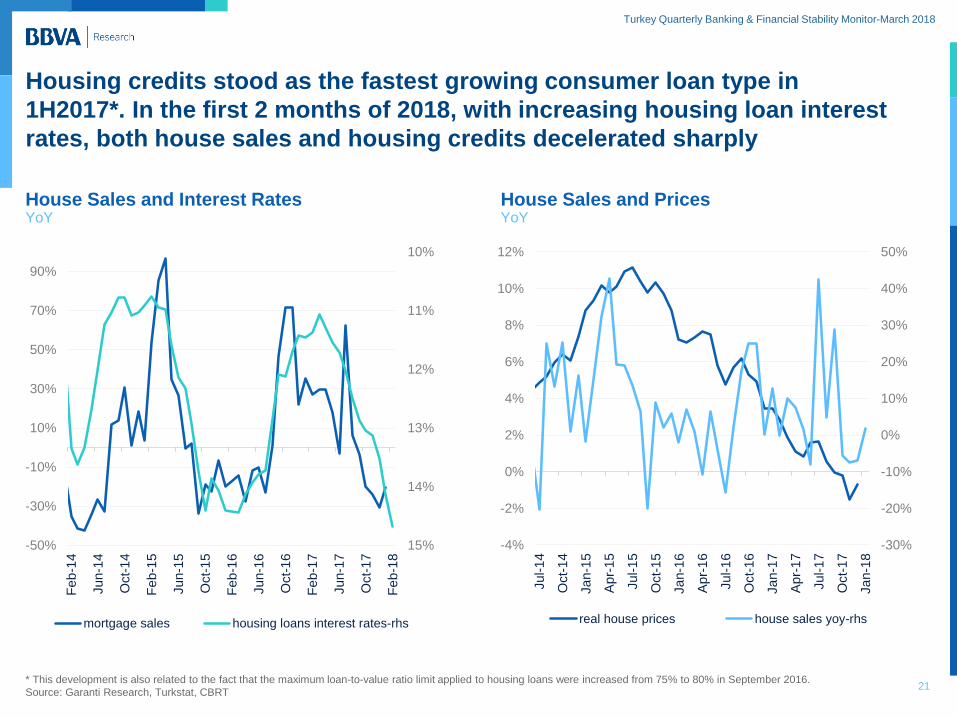

Housing credits stood as the fastest growing consumer loan type in

1H2017*. In the first 2 months of 2018, with increasing housing loan interest

rates, both house sales and housing credits decelerated sharply

21 * This development is also related to the fact that the maximum loan-to-value ratio limit applied to housing loans were increased from 75% to 80% in September 2016.

Source: Garanti Research, Turkstat, CBRT

House Sales and Interest Rates YoY

House Sales and Prices YoY

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

Jul-1

4

Oct-

14

Jan-1

5

Apr-

15

Jul-1

5

Oct-

15

Jan-1

6

Apr-

16

Jul-1

6

Oct-

16

Jan-1

7

Apr-

17

Jul-1

7

Oct-

17

Jan-1

8

real house prices house sales yoy-rhs

10%

11%

12%

13%

14%

15%-50%

-30%

-10%

10%

30%

50%

70%

90%

Feb

-14

Jun-1

4

Oct-

14

Feb

-15

Jun-1

5

Oct-

15

Feb

-16

Jun-1

6

Oct-

16

Feb

-17

Jun-1

7

Oct-

17

Feb

-18

mortgage sales housing loans interest rates-rhs

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

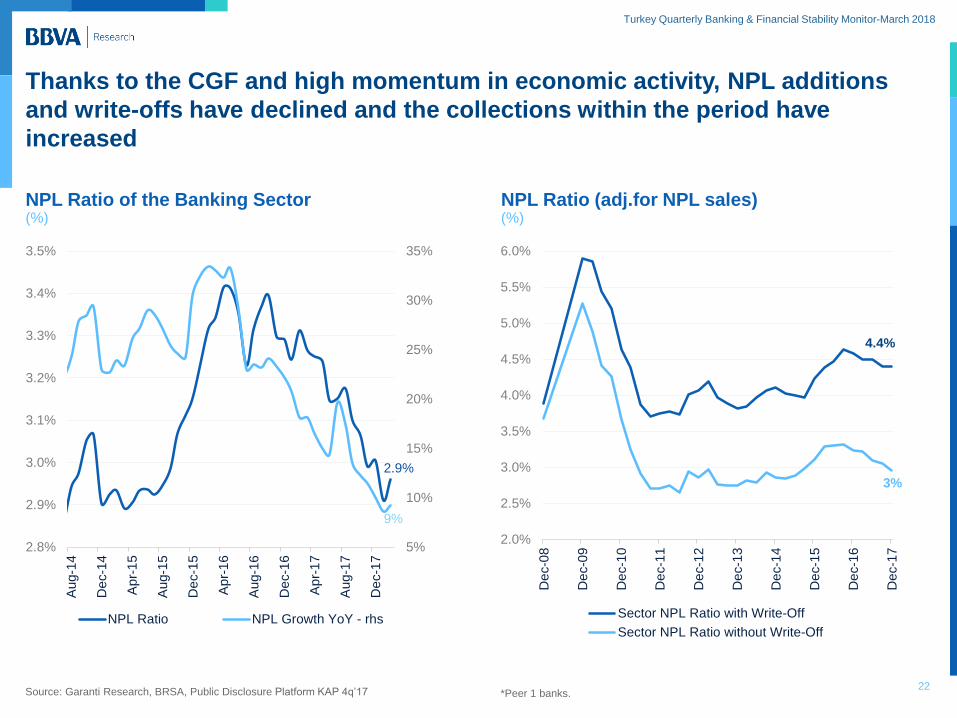

Thanks to the CGF and high momentum in economic activity, NPL additions

and write-offs have declined and the collections within the period have

increased

22 Source: Garanti Research, BRSA, Public Disclosure Platform KAP 4q’17

NPL Ratio of the Banking Sector (%)

NPL Ratio (adj.for NPL sales) (%)

Core

*Peer 1 banks. inflation jumped by 100bps in the last 2 months due to recent

appreciation of euro and second

4.4%

3%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

De

c-0

8

De

c-0

9

De

c-1

0

De

c-1

1

De

c-1

2

De

c-1

3

De

c-1

4

De

c-1

5

De

c-1

6

De

c-1

7

Sector NPL Ratio with Write-Off

Sector NPL Ratio without Write-Off

2.9%

9%

5%

10%

15%

20%

25%

30%

35%

2.8%

2.9%

3.0%

3.1%

3.2%

3.3%

3.4%

3.5%

Aug-1

4

De

c-1

4

Apr-

15

Aug-1

5

De

c-1

5

Apr-

16

Aug-1

6

De

c-1

6

Apr-

17

Aug-1

7

De

c-1

7

NPL Ratio NPL Growth YoY - rhs

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

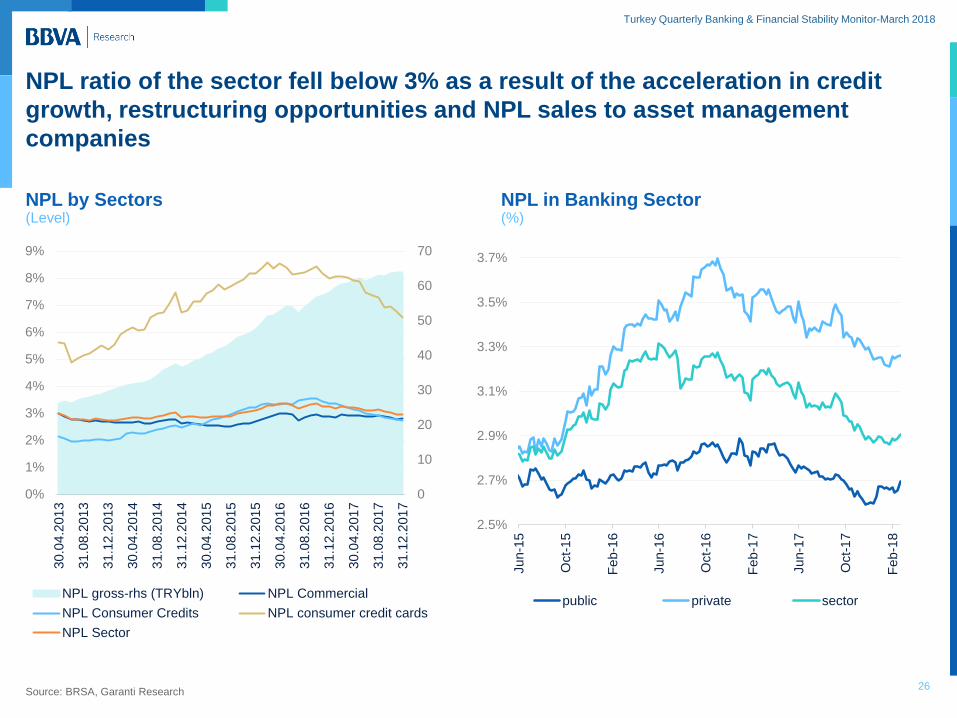

26

NPL ratio of the sector fell below 3% as a result of the acceleration in credit

growth, restructuring opportunities and NPL sales to asset management

companies

Source: BRSA, Garanti Research

0

10

20

30

40

50

60

70

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

30

.04

.201

3

31

.08

.201

3

31

.12

.201

3

30

.04

.201

4

31

.08

.201

4

31

.12

.201

4

30

.04

.201

5

31

.08

.201

5

31

.12

.201

5

30

.04

.201

6

31

.08

.201

6

31

.12

.201

6

30

.04

.201

7

31

.08

.201

7

31

.12

.201

7

NPL gross-rhs (TRYbln) NPL Commercial

NPL Consumer Credits NPL consumer credit cards

NPL Sector

2.5%

2.7%

2.9%

3.1%

3.3%

3.5%

3.7%

Jun-1

5

Oct-

15

Fe

b-1

6

Jun-1

6

Oct-

16

Feb

-17

Jun-1

7

Oct-

17

Feb

-18

public private sector

NPL by Sectors (Level)

NPL in Banking Sector (%)

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

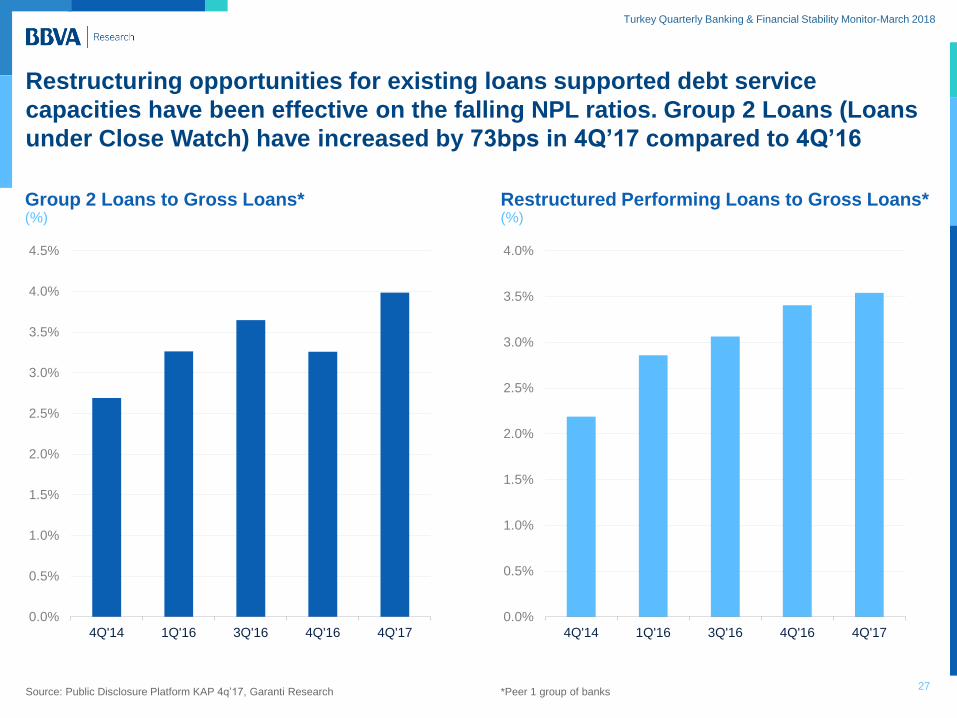

Group 2 Loans to Gross Loans* (%)

27

Restructuring opportunities for existing loans supported debt service

capacities have been effective on the falling NPL ratios. Group 2 Loans (Loans

under Close Watch) have increased by 73bps in 4Q’17 compared to 4Q’16

Restructured Performing Loans to Gross Loans* (%)

Source: Public Disclosure Platform KAP 4q’17, Garanti Research

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4Q'14 1Q'16 3Q'16 4Q'16 4Q'17

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

4Q'14 1Q'16 3Q'16 4Q'16 4Q'17

*Peer 1 group of banks

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

Turkish Banking

Sector: Liquidity

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

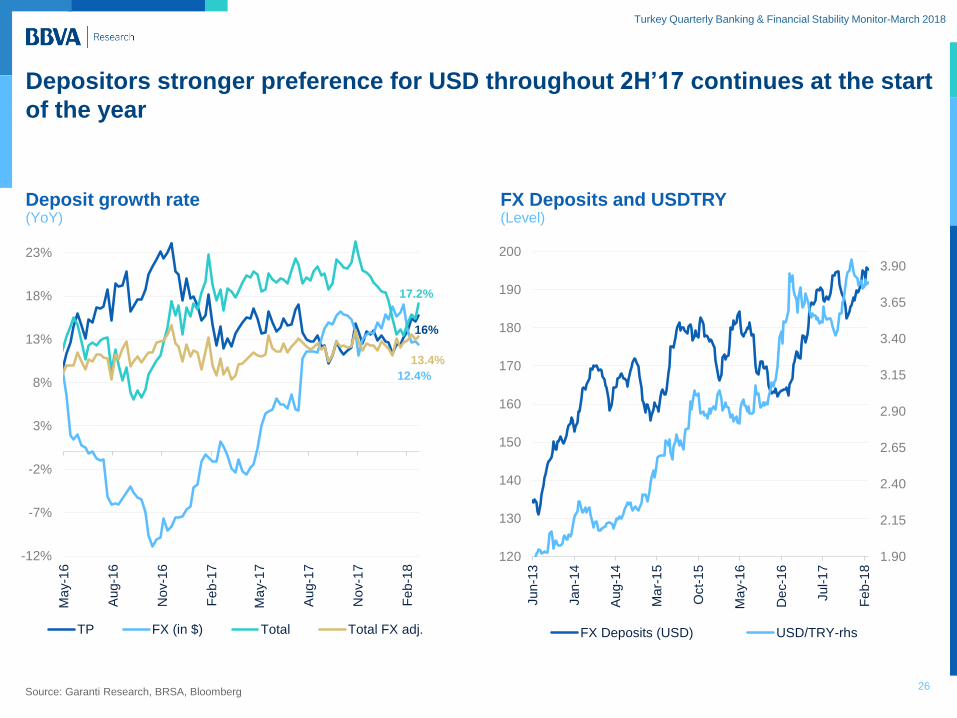

Depositors stronger preference for USD throughout 2H’17 continues at the start

of the year

26 Source: Garanti Research, BRSA, Bloomberg

Deposit growth rate (YoY)

FX Deposits and USDTRY (Level)

17.2%

16%

12.4%

13.4%

-12%

-7%

-2%

3%

8%

13%

18%

23%

Ma

y-1

6

Aug-1

6

No

v-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

TP FX (in $) Total Total FX adj.

1.90

2.15

2.40

2.65

2.90

3.15

3.40

3.65

3.90

120

130

140

150

160

170

180

190

200

Jun-1

3

Jan-1

4

Aug-1

4

Ma

r-1

5

Oct-

15

Ma

y-1

6

De

c-1

6

Jul-1

7

Fe

b-1

8

FX Deposits (USD) USD/TRY-rhs

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

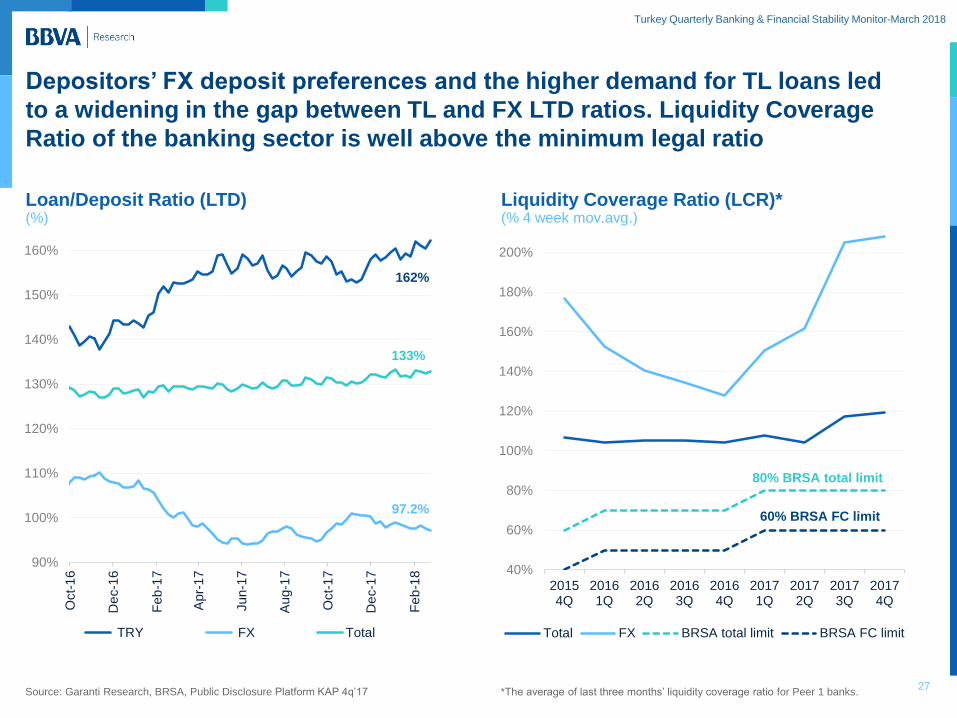

Depositors’ FX deposit preferences and the higher demand for TL loans led

to a widening in the gap between TL and FX LTD ratios. Liquidity Coverage

Ratio of the banking sector is well above the minimum legal ratio

27 Source: Garanti Research, BRSA, Public Disclosure Platform KAP 4q’17

Loan/Deposit Ratio (LTD) (%)

Liquidity Coverage Ratio (LCR)* (% 4 week mov.avg.)

*The average of last three months’ liquidity coverage ratio for Peer 1 banks.on jumped by

100bps in the last 2 months due to recent appreciation of euro and second

40%

60%

80%

100%

120%

140%

160%

180%

200%

20154Q

20161Q

20162Q

20163Q

20164Q

20171Q

20172Q

20173Q

20174Q

Total FX BRSA total limit BRSA FC limit

80% BRSA total limit

60% BRSA FC limit

162%

97.2%

133%

90%

100%

110%

120%

130%

140%

150%

160%

Oct-

16

De

c-1

6

Feb

-17

Apr-

17

Jun-1

7

Aug-1

7

Oct-

17

De

c-1

7

Feb

-18

TRY FX Total

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

Turkish Banking

Sector: Asset

Quality

Sizable Increase in Profit

Asset Quality Improved

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

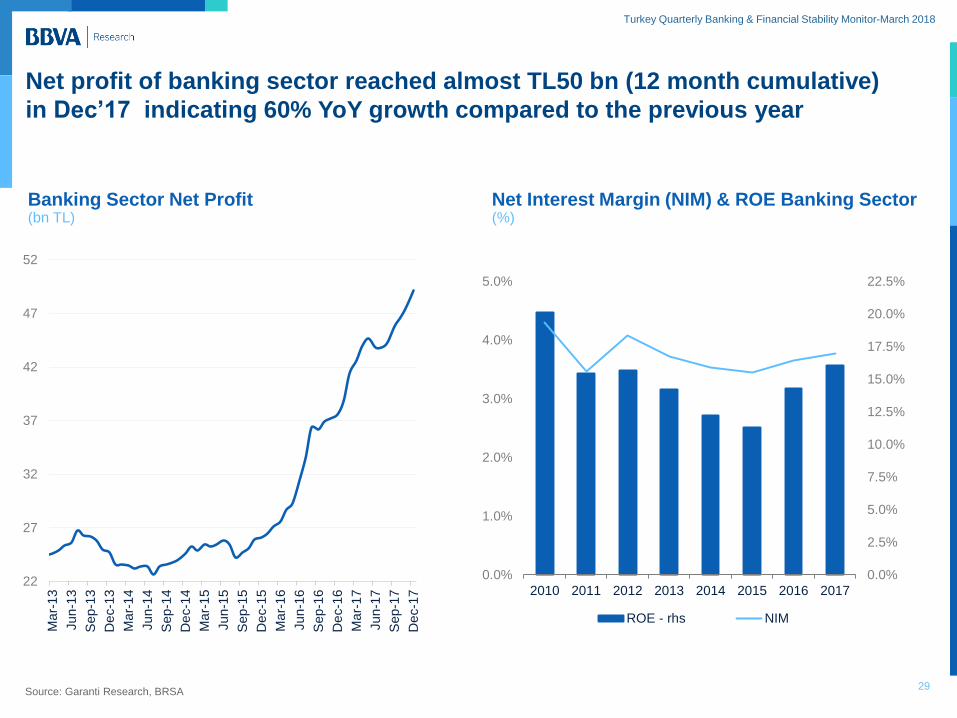

Net profit of banking sector reached almost TL50 bn (12 month cumulative)

in Dec’17 indicating 60% YoY growth compared to the previous year

29 Source: Garanti Research, BRSA

Banking Sector Net Profit (bn TL)

Net Interest Margin (NIM) & ROE Banking Sector (%)

22

27

32

37

42

47

52

Ma

r-1

3

Jun-1

3

Sep-1

3

De

c-1

3

Ma

r-1

4

Jun-1

4

Sep-1

4

De

c-1

4

Ma

r-1

5

Jun-1

5

Sep-1

5

De

c-1

5

Ma

r-1

6

Jun-1

6

Sep-1

6

De

c-1

6

Ma

r-1

7

Jun-1

7

Sep-1

7

De

c-1

7

0.0%

2.5%

5.0%

7.5%

10.0%

12.5%

15.0%

17.5%

20.0%

22.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2010 2011 2012 2013 2014 2015 2016 2017

ROE - rhs NIM

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

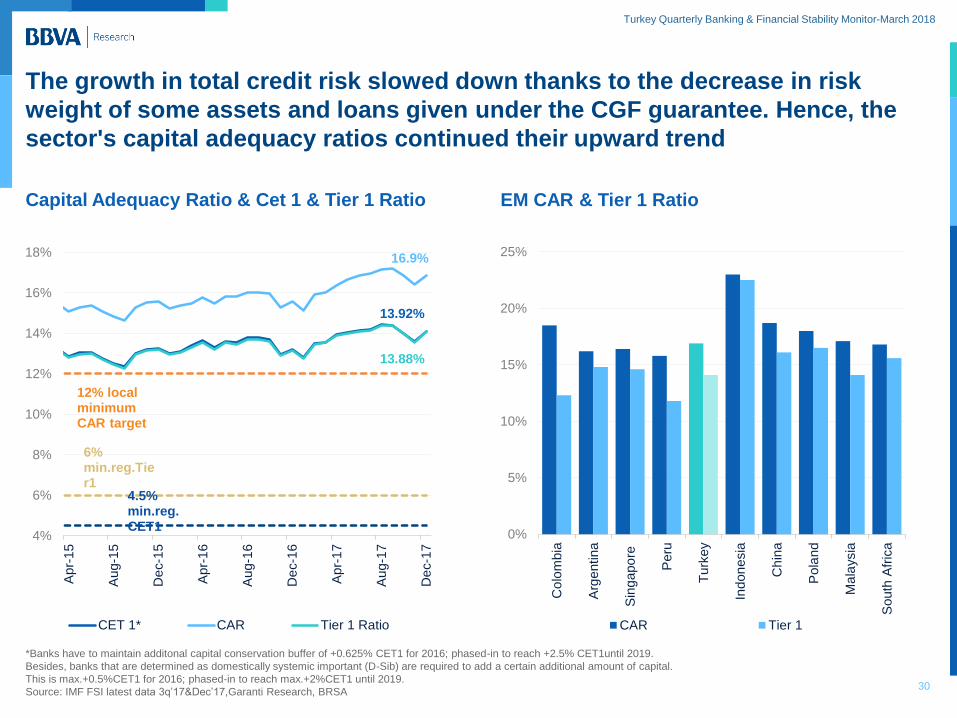

The growth in total credit risk slowed down thanks to the decrease in risk

weight of some assets and loans given under the CGF guarantee. Hence, the

sector's capital adequacy ratios continued their upward trend

30

*Banks have to maintain additonal capital conservation buffer of +0.625% CET1 for 2016; phased-in to reach +2.5% CET1until 2019.

Besides, banks that are determined as domestically systemic important (D-Sib) are required to add a certain additional amount of capital.

This is max.+0.5%CET1 for 2016; phased-in to reach max.+2%CET1 until 2019.

Source: IMF FSI latest data 3q’17&Dec’17,Garanti Research, BRSA

Capital Adequacy Ratio & Cet 1 & Tier 1 Ratio EM CAR & Tier 1 Ratio

16.9%

12% local minimum CAR target

4.5% min.reg. CET1

13.92%

13.88%

6% min.reg.Tier1

4%

6%

8%

10%

12%

14%

16%

18%

Apr-

15

Aug-1

5

De

c-1

5

Apr-

16

Aug-1

6

De

c-1

6

Apr-

17

Aug-1

7

De

c-1

7

CET 1* CAR Tier 1 Ratio

0%

5%

10%

15%

20%

25%

Co

lom

bia

Arg

entina

Sin

gapo

re

Peru

Turk

ey

Indon

esia

Ch

ina

Pola

nd

Ma

laysia

South

Afr

ica

CAR Tier 1

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

External Debt

Indicators

Roll-over Ratios Stand above

100%,

New Regulation on Corporates’

FX loans

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

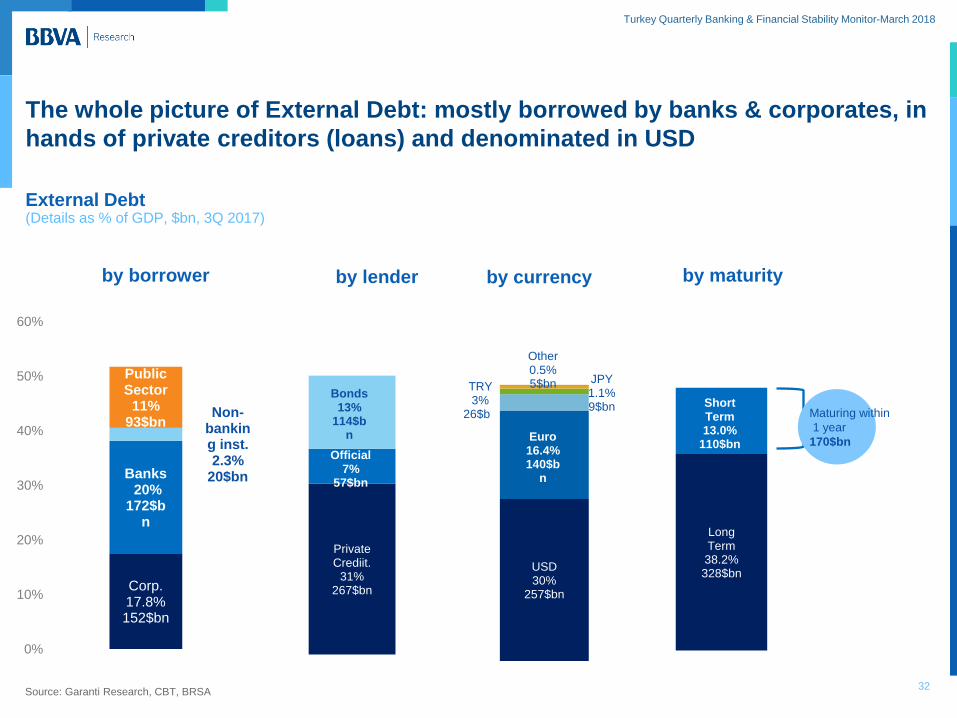

The whole picture of External Debt: mostly borrowed by banks & corporates, in

hands of private creditors (loans) and denominated in USD

32 Source: Garanti Research, CBT, BRSA

External Debt (Details as % of GDP, $bn, 3Q 2017)

Corp. 17.8% 152$bn

Banks 20%

172$bn

Non-banking inst. 2.3%

20$bn

Public Sector

11% 93$bn

0%

10%

20%

30%

40%

50%

60%

by borrower by lender by currency by maturity

Private Crediit.

31% 267$bn

Official 7%

57$bn

Bonds 13%

114$bn

USD 30%

257$bn

Euro 16.4% 140$b

n

TRY 3%

26$bn

JPY 1.1% 9$bn

Other 0.5% 5$bn

Long Term 38.2% 328$bn

Short Term 13.0%

110$bn

Maturing within

1 year

170$bn

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

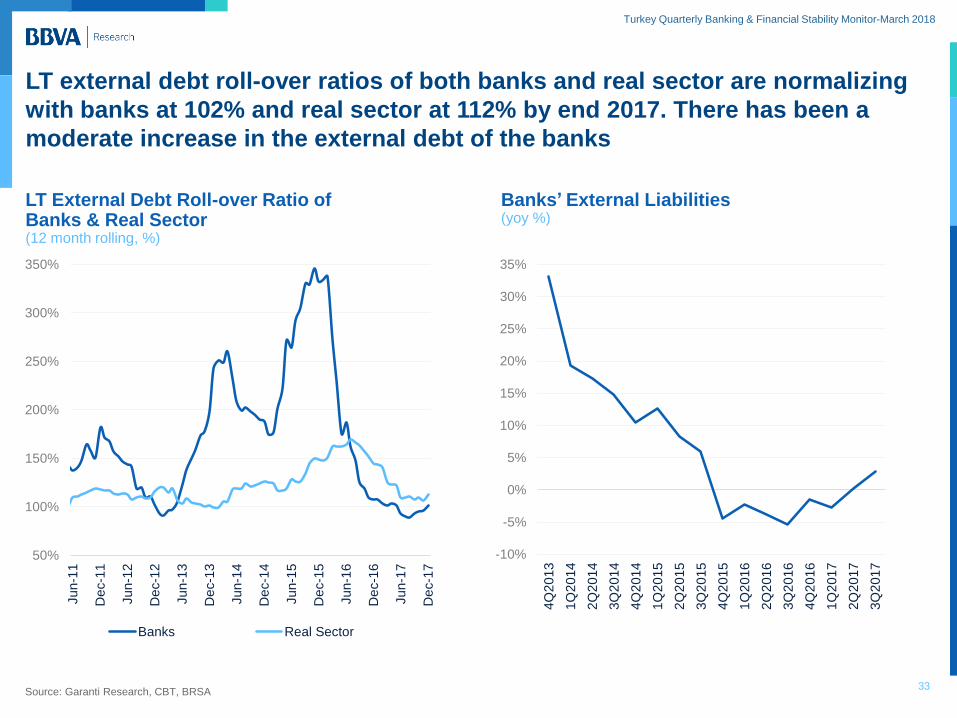

LT external debt roll-over ratios of both banks and real sector are normalizing

with banks at 102% and real sector at 112% by end 2017. There has been a

moderate increase in the external debt of the banks

33 Source: Garanti Research, CBT, BRSA

LT External Debt Roll-over Ratio of Banks & Real Sector (12 month rolling, %)

Banks’ External Liabilities (yoy %)

50%

100%

150%

200%

250%

300%

350%

Jun-1

1

De

c-1

1

Jun-1

2

De

c-1

2

Jun-1

3

De

c-1

3

Jun-1

4

De

c-1

4

Jun-1

5

De

c-1

5

Jun-1

6

De

c-1

6

Jun-1

7

De

c-1

7

Banks Real Sector

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

4Q

2013

1Q

2014

2Q

2014

3Q

2014

4Q

2014

1Q

2015

2Q

2015

3Q

2015

4Q

2015

1Q

2016

2Q

2016

3Q

2016

4Q

2016

1Q

2017

2Q

2017

3Q

2017

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

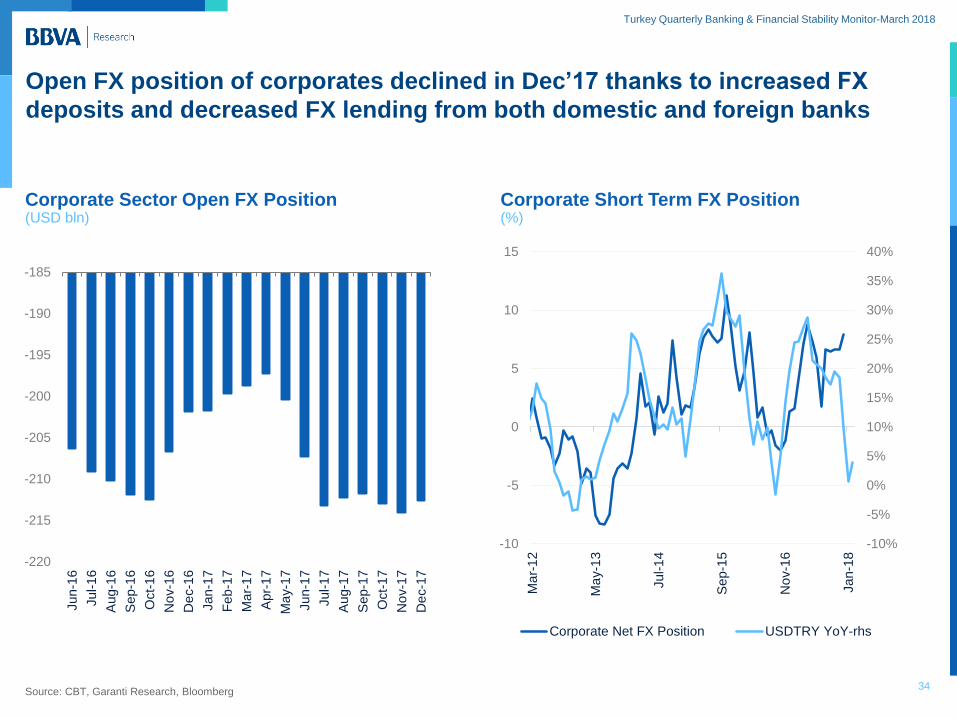

Open FX position of corporates declined in Dec’17 thanks to increased FX

deposits and decreased FX lending from both domestic and foreign banks

34 Source: CBT, Garanti Research, Bloomberg

Corporate Sector Open FX Position (USD bln)

Corporate Short Term FX Position (%)

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

-10

-5

0

5

10

15

Ma

r-1

2

Ma

y-1

3

Jul-1

4

Sep-1

5

No

v-1

6

Jan-1

8

Corporate Net FX Position USDTRY YoY-rhs

-220

-215

-210

-205

-200

-195

-190

-185

Jun-1

6

Jul-1

6

Aug-1

6

Sep-1

6

Oct-

16

No

v-1

6

De

c-1

6

Jan-1

7

Feb

-17

Ma

r-1

7

Apr-

17

Ma

y-1

7

Jun-1

7

Jul-1

7

Aug-1

7

Sep-1

7

Oct-

17

No

v-1

7

De

c-1

7

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

Companies with FX debt

exposure under $15mn

Companies with FX debt

exposure above $15mn

New regulation: a further step to limit risks on financial stability with some

limits for FX borrowing of the corporates

No Mismatch (FX Revenues): foreign exchange income of

the previous three years will be the total available limit

Mismatch (No FX Revenues): cannot roll-over, redeem the

debt at the maturity of the liability

No restriction even if the company has no FX revenues;

the Government now works in some hedging options

Exceptions Public institutions, banks, leasing companies, factoring and

financing companies, lenders under investment incentive,

investors in machinery, public-private partnership firms

32

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

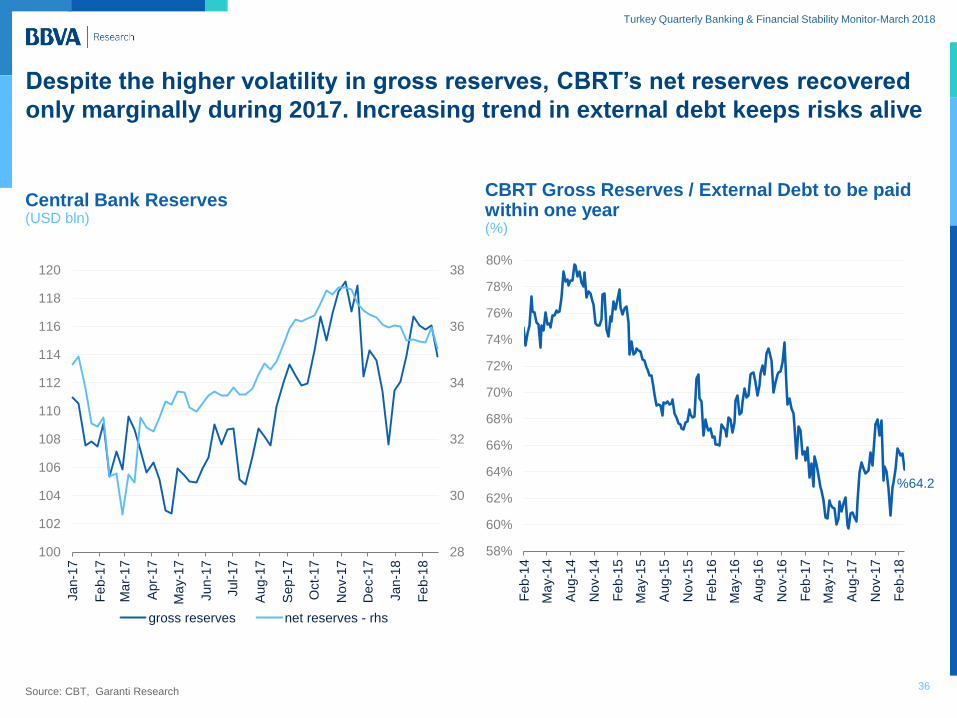

36

Despite the higher volatility in gross reserves, CBRT’s net reserves recovered

only marginally during 2017. Increasing trend in external debt keeps risks alive

Central Bank Reserves (USD bln)

Source: CBT, Garanti Research

CBRT Gross Reserves / External Debt to be paid within one year (%)

28

30

32

34

36

38

100

102

104

106

108

110

112

114

116

118

120

Jan-1

7

Feb

-17

Ma

r-1

7

Apr-

17

Ma

y-1

7

Jun-1

7

Jul-1

7

Aug-1

7

Sep-1

7

Oct-

17

No

v-1

7

De

c-1

7

Jan-1

8

Feb

-18

gross reserves net reserves - rhs

%64.2

58%

60%

62%

64%

66%

68%

70%

72%

74%

76%

78%

80%

Feb

-14

Ma

y-1

4

Aug-1

4

No

v-1

4

Feb

-15

Ma

y-1

5

Aug-1

5

No

v-1

5

Feb

-16

Ma

y-1

6

Aug-1

6

No

v-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

Turkey Quarterly Banking & Financial Stability Monitor-March 2018

This document has been prepared by BBVA Research Department, it is provided for information purposes only and expresses data, opinions or

estimations regarding the date of issue of the report, prepared by BBVA or obtained from or based on sources we consider to be reliable, and have

not been independently verified by BBVA. Therefore, BBVA offers no warranty, either express or implicit, regarding its accuracy, integrity or

correctness.

Estimations this document may contain have been undertaken according to generally accepted methodologies and should be considered as

forecasts or projections. Results obtained in the past, either positive or negative, are no guarantee of future performance.

This document and its contents are subject to changes without prior notice depending on variables such as the economic context or market

fluctuations. BBVA is not responsible for updating these contents or for giving notice of such changes.

BBVA accepts no liability for any loss, direct or indirect, that may result from the use of this document or its contents.

This document and its contents do not constitute an offer, invitation or solicitation to purchase, divest or enter into any interest in financial assets or

instruments. Neither shall this document nor its contents form the basis of any contract, commitment or decision of any kind.

In regard to investment in financial assets related to economic variables this document may cover, readers should be aware that under no

circumstances should they base their investment decisions in the information contained in this document. Those persons or entities offering

investment products to these potential investors are legally required to provide the information needed for them to take an appropriate investment

decision.

The content of this document is protected by intellectual property laws. It is forbidden its reproduction, transformation, distribution, public

communication, making available, extraction, reuse, forwarding or use of any nature by any means or process, except in cases where it is legally

permitted or expressly authorized by BBVA.

DISCLAIMER

34

Turkey: Quarterly Banking &

Financial Stability Monitor

March 2018

Deniz Ergun