trends in fish and seafood in europe

TRANSCRIPT

TRENDS IN FISH AND SEAFOOD IN EUROPE

SEAFOOD EXPO GLOBAL – 20/04/2015

WIEBKE SCHOON, ANALYST, EUROMONITOR INTERNATIONAL

© Euromonitor International

2

• Global provider of Strategic Market

Intelligence

• 12 Regional offices - 800+ analysts in 80

countries

• Cross-country comparable data and analysis

• Consumer focused industries, countries and

consumers

• 5 - 10 year forecasts with matching trend

analysis

• All retail channels covered

• Subscription services, reports and consulting

About Euromonitor InternationalEUROMONITOR INTERNATIONAL London

Singapore

Shanghai

Dubai

Vilnius

Cape Town

Santiago

Tokyo

Sydney

Chicago

Bangalore

Sao Paulo

© Euromonitor International

4

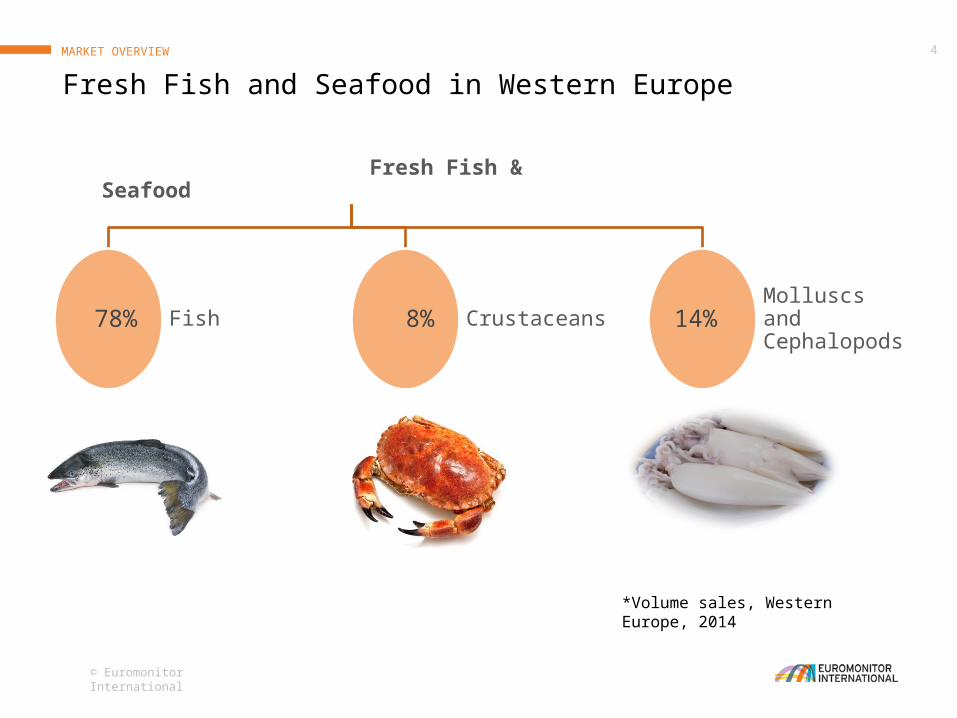

Fresh Fish and Seafood in Western EuropeMARKET OVERVIEW

Fresh Fish & Seafood

78%

Fish 8% Crustaceans 14% Molluscs and Cephalopods

*Volume sales, Western Europe, 2014

© Euromonitor International

5

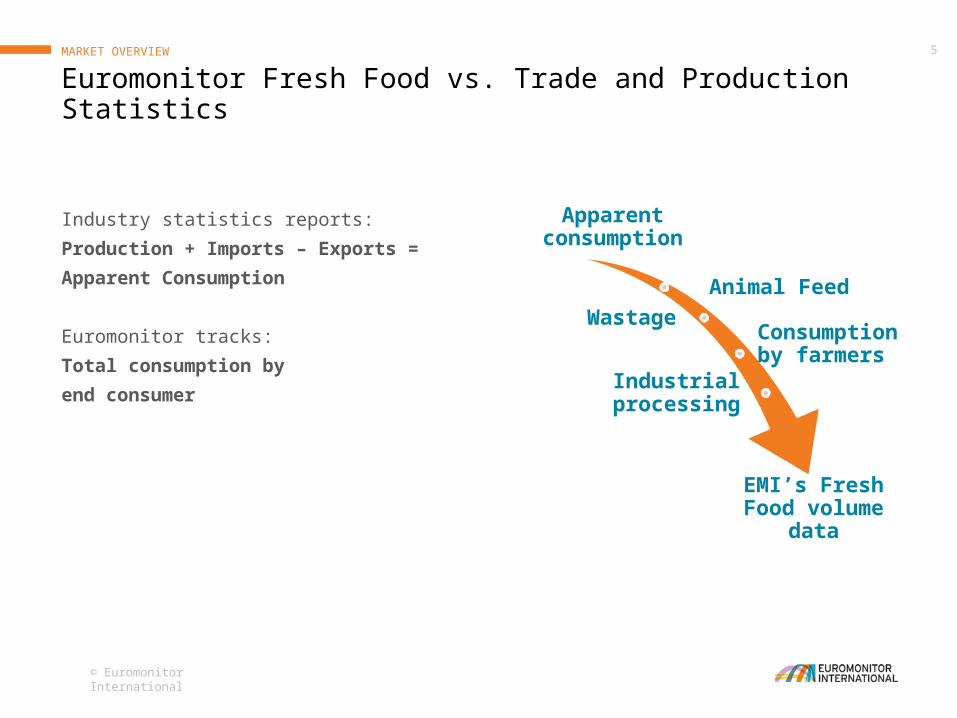

Industry statistics reports:

Production + Imports – Exports =

Apparent Consumption

Euromonitor tracks:

Total consumption by

end consumer

Apparent consumption

Animal FeedWastage

Consumption by farmers

Industrial processing

EMI’s Fresh Food volume

data

Euromonitor Fresh Food vs. Trade and Production StatisticsMARKET OVERVIEW

© Euromonitor International

6

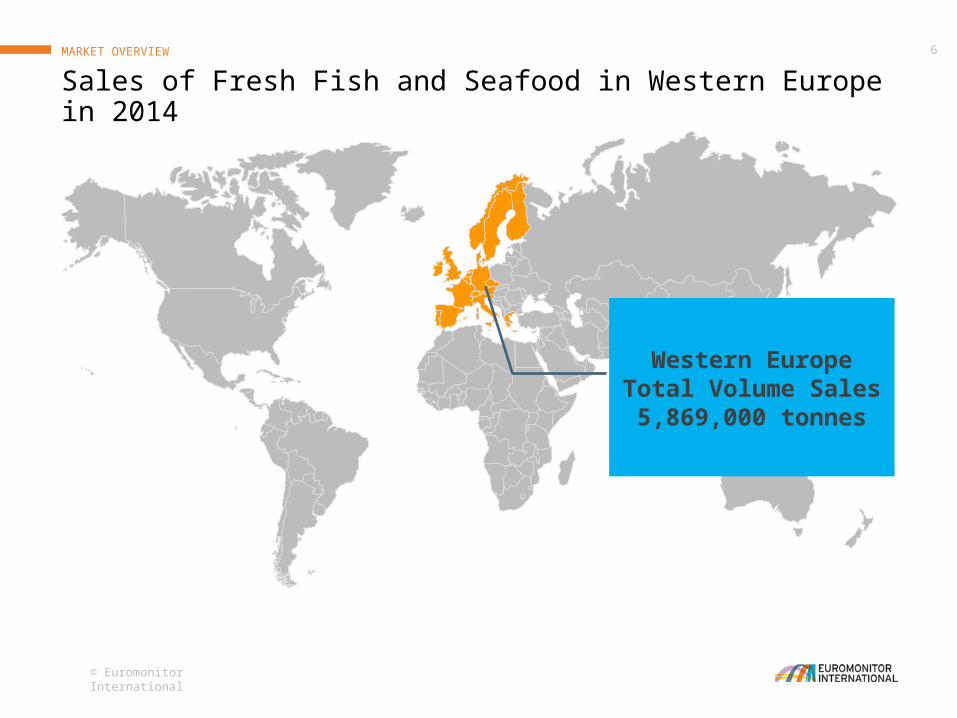

Sales of Fresh Fish and Seafood in Western Europe in 2014MARKET OVERVIEW

Western EuropeTotal Volume Sales5,869,000 tonnes

© Euromonitor International

7

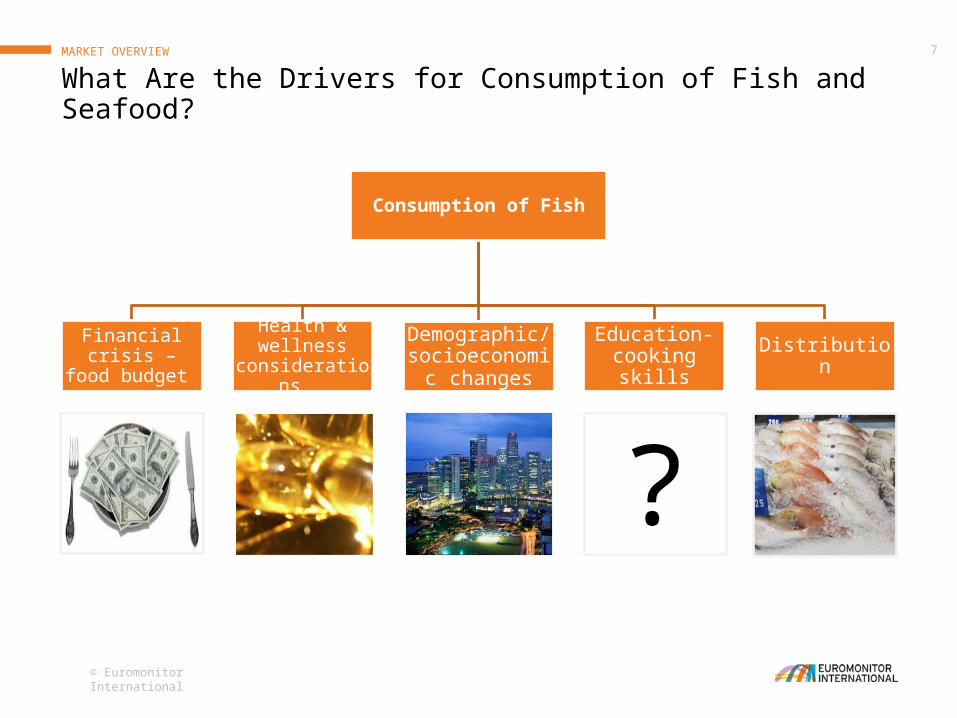

What Are the Drivers for Consumption of Fish and Seafood?MARKET OVERVIEW

Consumption of Fish

Financial crisis – food

budget

Health & wellness

considerations

Demographic/ socioeconomic

changes

Education- cooking skills Distribution

?

© Euromonitor International

8

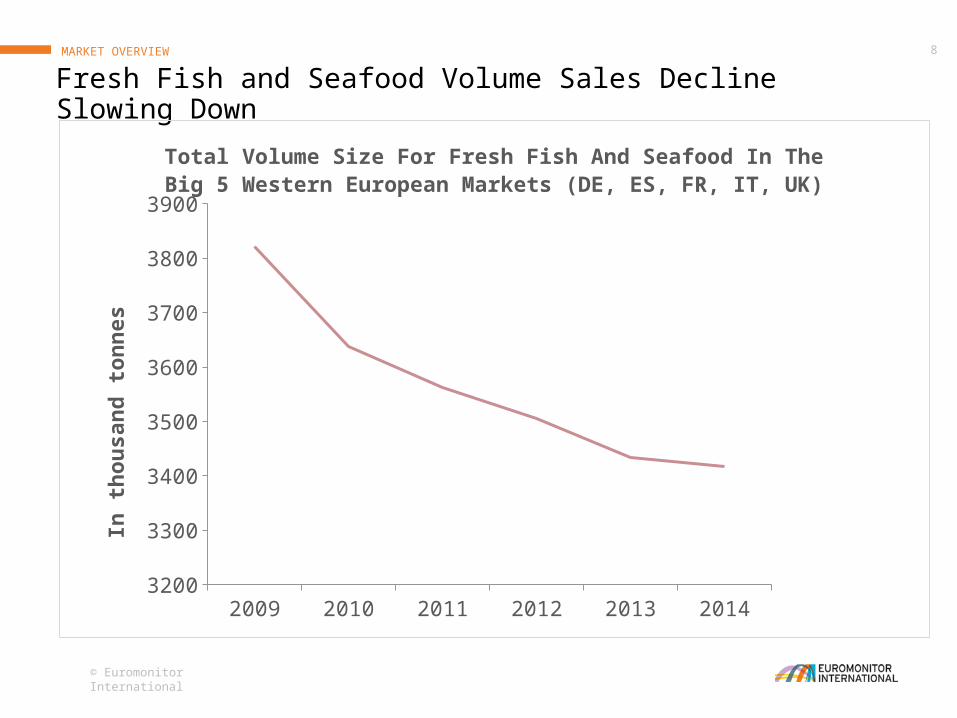

Fresh Fish and Seafood Volume Sales Decline Slowing DownMARKET OVERVIEW

2009 2010 2011 2012 2013 20143200

3300

3400

3500

3600

3700

3800

3900

Total Volume Size For Fresh Fish And Seafood In The Big 5 Western European Markets (DE, ES, FR, IT, UK)

In t

hou

san

d t

on

nes

© Euromonitor International

9MARKET OVERVIEW

Fresh Fish and Seafood Consumption Remains Low

Spain United Kingdom

Italy Germany France0

5

10

15

20

25

30

35 32.2

10.69.2 9.4

6.0

26.4

11.38.4 7.8

4.9

Per Capita Consumption in Kg per Person for the Big 5 Markets (DE, ES, FR, IT, UK)

20092014

Per

cap

ita c

on

su

mp

tion

in

kg

© Euromonitor International

10

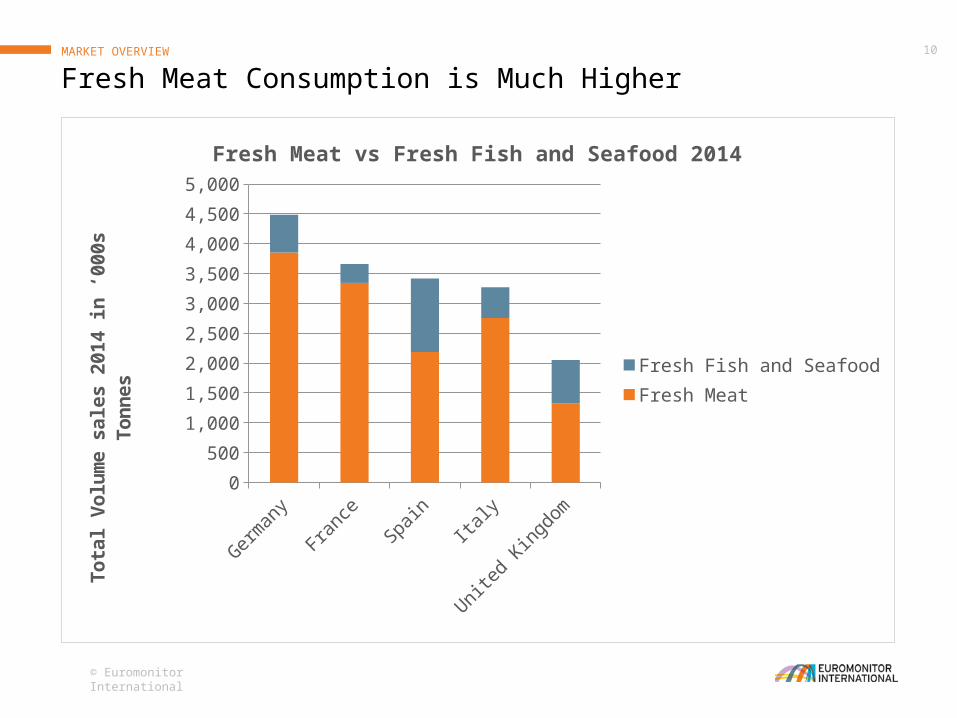

Fresh Meat Consumption is Much HigherMARKET OVERVIEW

Germ

any

Franc

e

Spain

Ital

y

Uni

ted

Kingd

om

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Fresh Meat vs Fresh Fish and Seafood 2014

Fresh Fish and SeafoodFresh Meat

Tota

l V

olu

me s

ale

s 2014 i

n ‘

000s

Ton

nes

© Euromonitor International

11

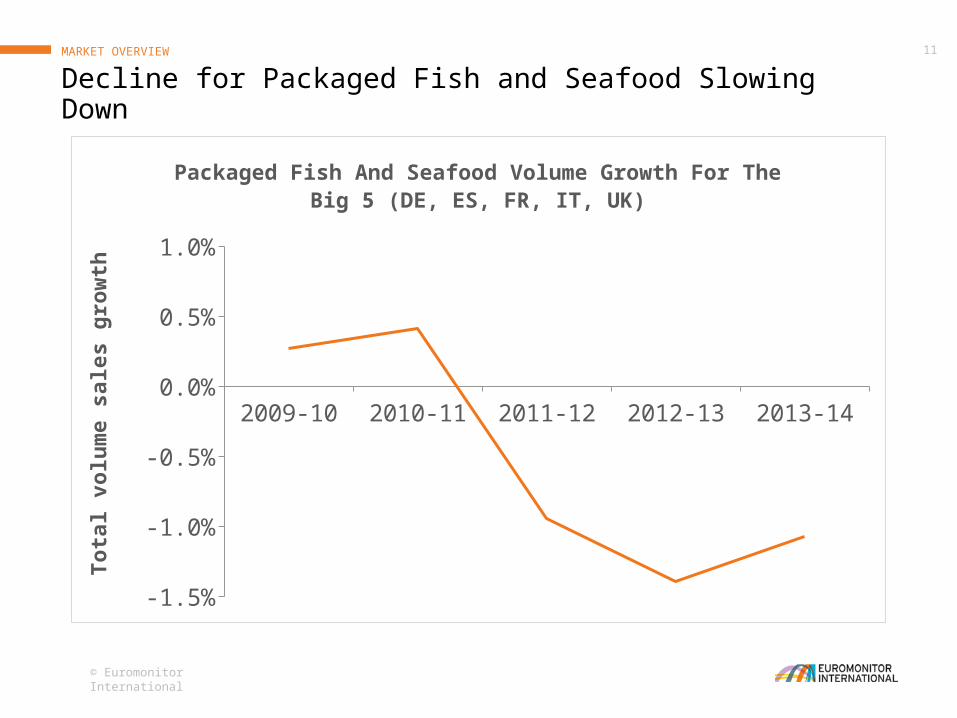

Decline for Packaged Fish and Seafood Slowing DownMARKET OVERVIEW

2009-10 2010-11 2011-12 2012-13 2013-14

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

Packaged Fish And Seafood Volume Growth For The Big 5 (DE, ES, FR, IT, UK)

Tota

l vo

lum

e s

ale

s g

row

th

© Euromonitor International

12

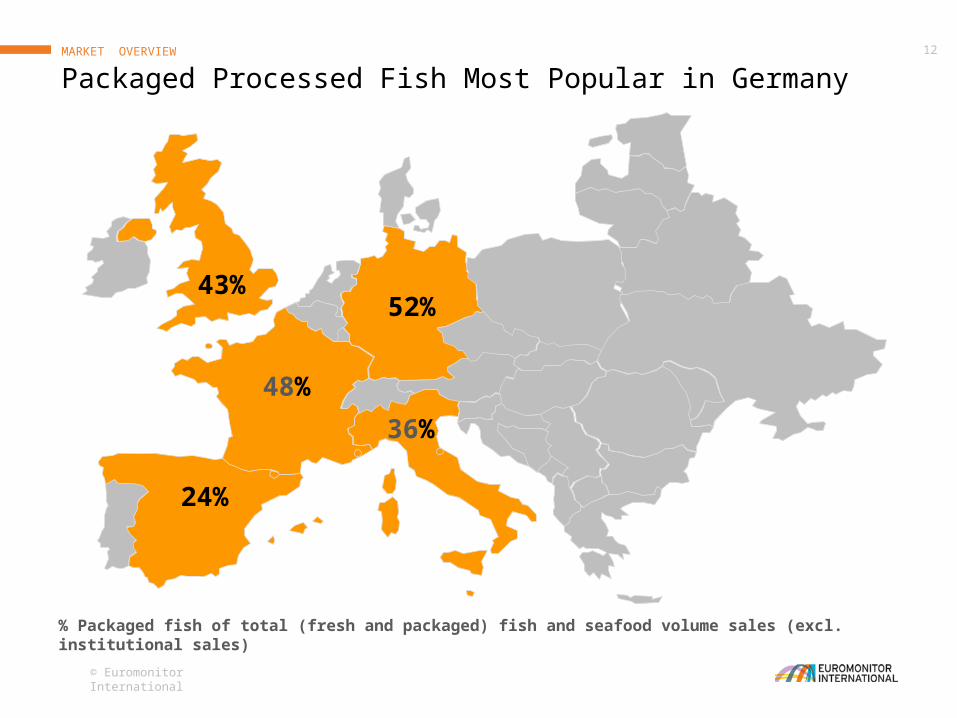

Packaged Processed Fish Most Popular in GermanyMARKET OVERVIEW

52%43%

24%

48%

36%

% Packaged fish of total (fresh and packaged) fish and seafood volume sales (excl. institutional sales)

© Euromonitor International

13

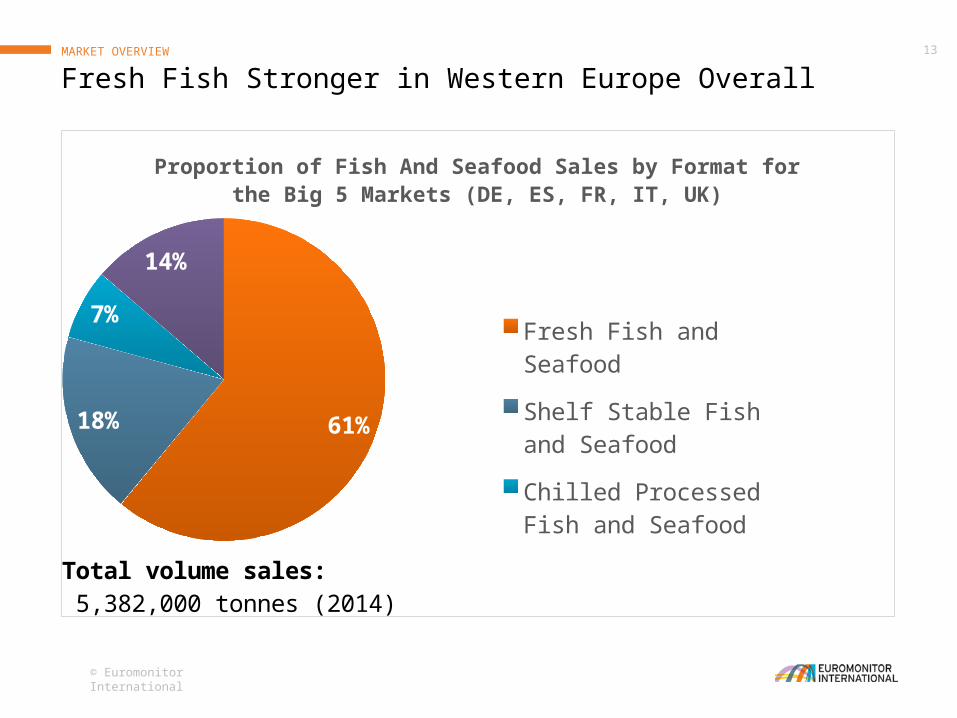

Fresh Fish Stronger in Western Europe OverallMARKET OVERVIEW

61%18%

7%

14%

Proportion of Fish And Seafood Sales by Format for the Big 5 Markets (DE, ES, FR, IT, UK)

Fresh Fish and SeafoodShelf Stable Fish and SeafoodChilled Processed Fish and SeafoodFrozen Processsed Fish and Seafood

Total volume sales: 5,382,000 tonnes (2014)

MARKET OVERVIEW

TRENDS IN FISH AND SEAFOOD

FUTURE OUTLOOK

Bild durch Klicken auf Symbol hinzufügen

© Euromonitor International

15TRENDS & DEVELOPMENTS

Ethical Labels Going Strong

Tuna Tuna Private Label

Fish Fingers

MSC Line Caught

Dolphin Safe Friend of the Sea

© Euromonitor International

16

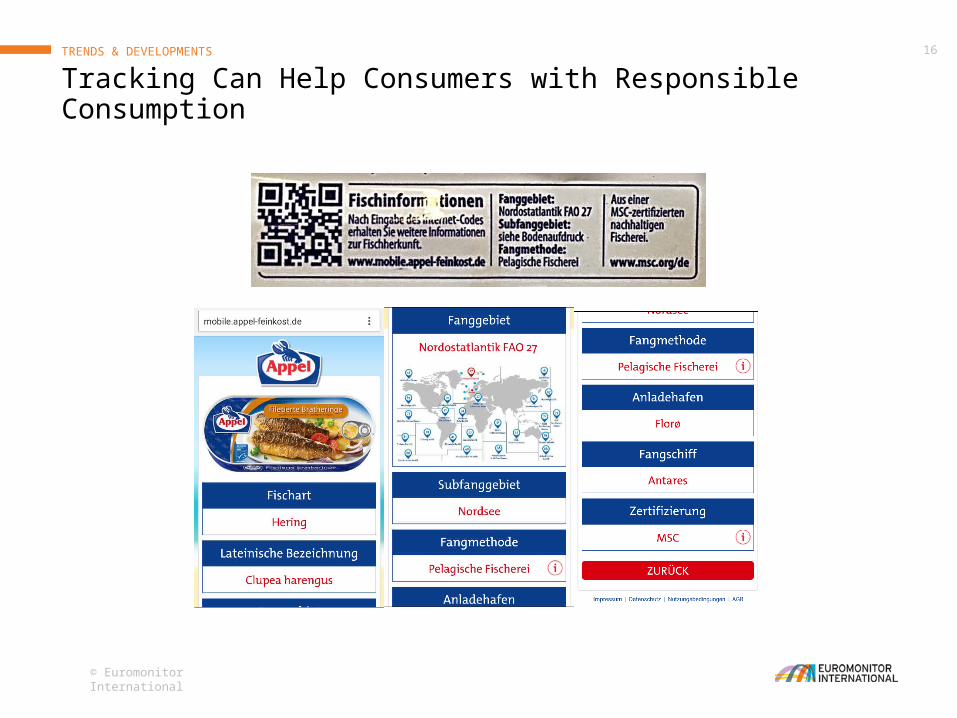

Tracking Can Help Consumers with Responsible ConsumptionTRENDS & DEVELOPMENTS

© Euromonitor International

17

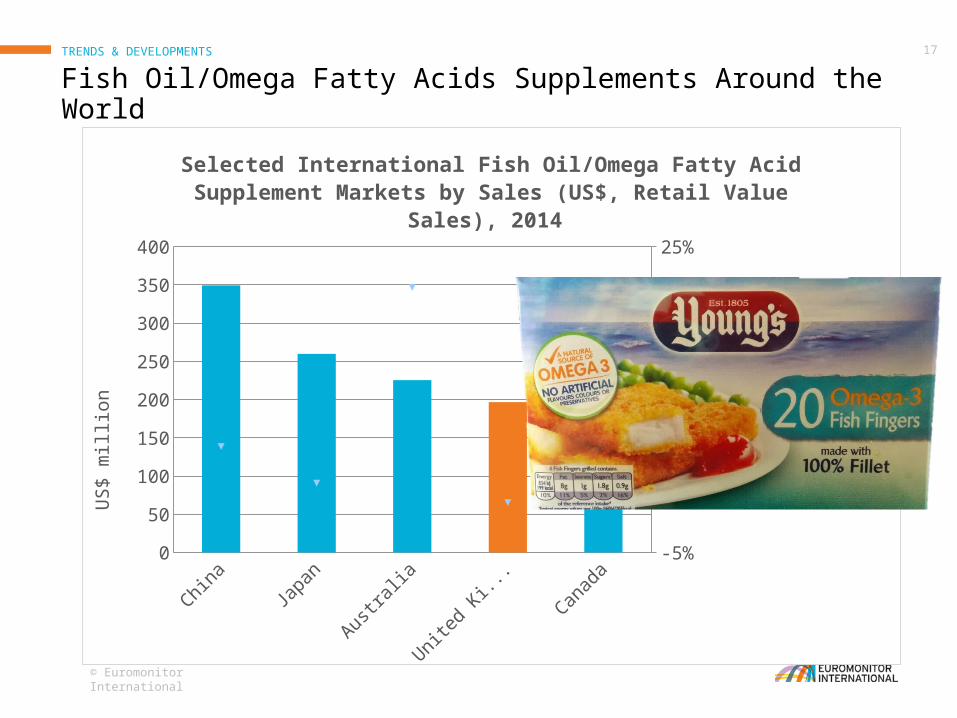

China Japan Australia United Kingdom

Canada0

50

100

150

200

250

300

350

400

-5%

0%

5%

10%

15%

20%

25%

Selected International Fish Oil/Omega Fatty Acid Supplement Markets by Sales (US$, Retail Value Sales), 2014

2014 - Retail value sales

2009-2014 % CAGR

US

$ m

illio

n

% C

AG

R

Fish Oil/Omega Fatty Acids Supplements Around the WorldTRENDS & DEVELOPMENTS

© Euromonitor International

18

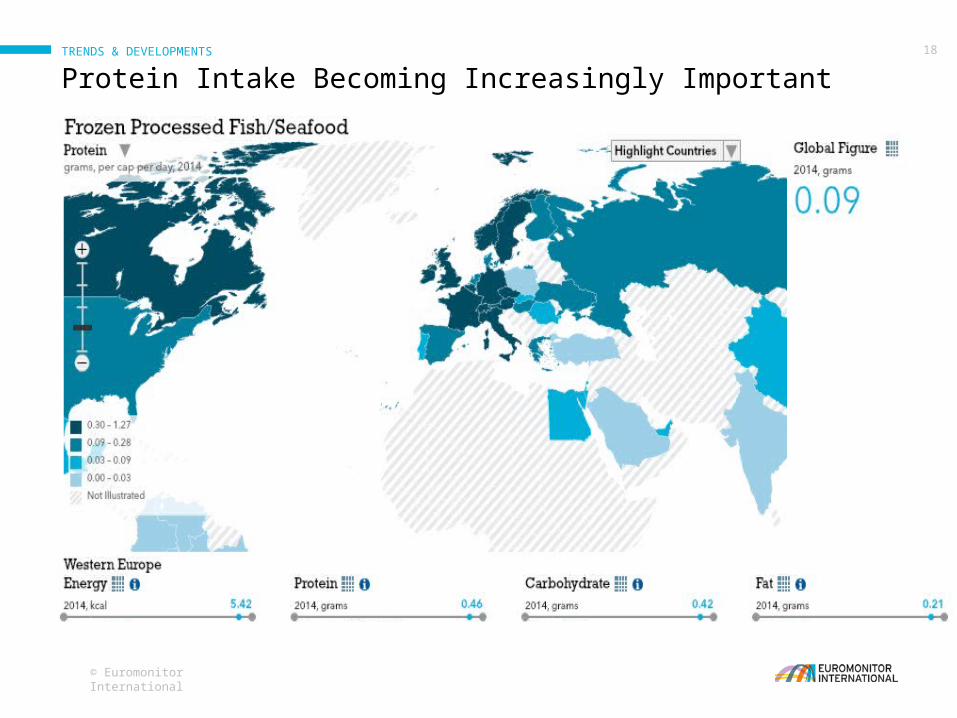

Protein Intake Becoming Increasingly ImportantTRENDS & DEVELOPMENTS

© Euromonitor International

19

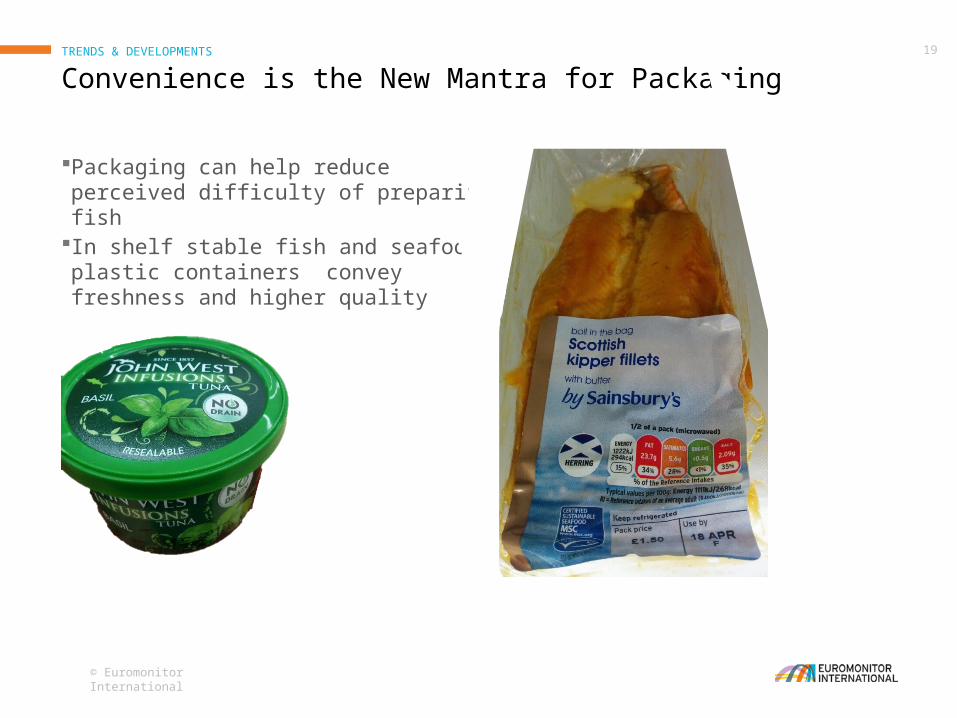

Convenience is the New Mantra for PackagingTRENDS & DEVELOPMENTS

Packaging can help reduce perceived difficulty of preparing fish

In shelf stable fish and seafood, plastic containers convey freshness and higher quality

© Euromonitor International

20

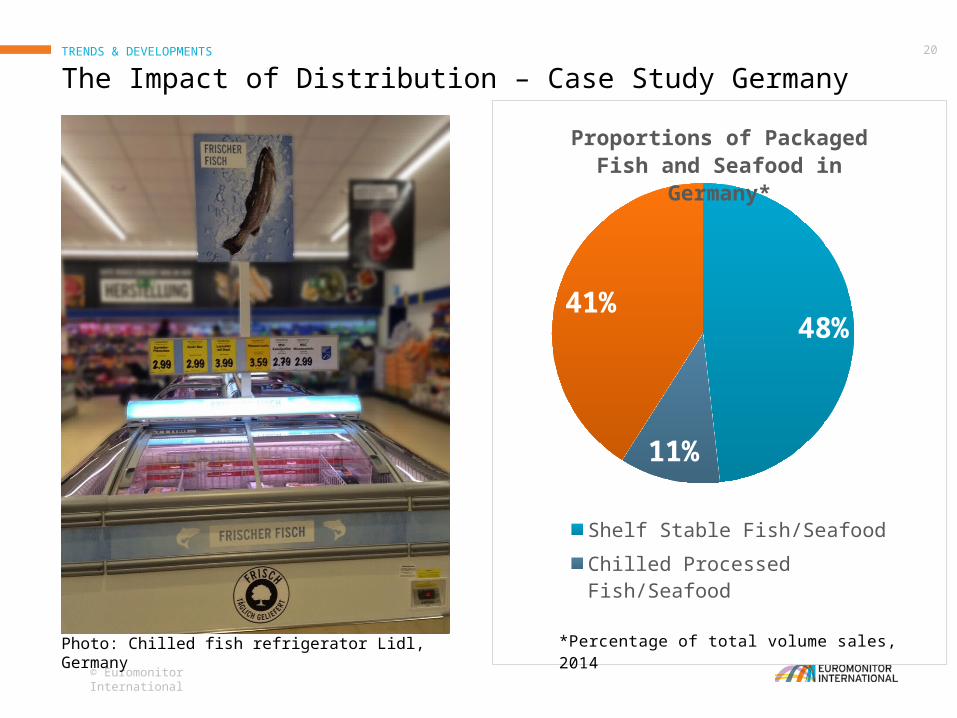

The Impact of Distribution – Case Study GermanyTRENDS & DEVELOPMENTS

Photo: Chilled fish refrigerator Lidl, Germany

48%

11%

41%

Proportions of Packaged Fish and Seafood in Germany*

Shelf Stable Fish/Seafood

Chilled Processed Fish/Seafood

Frozen Processed Fish/Seafood

*Percentage of total volume sales, 2014

MARKET OVERVIEW

TRENDS & DEVELOPMENTS

FUTURE OUTLOOK

Bild durch Klicken auf Symbol hinzufügen

© Euromonitor International

22

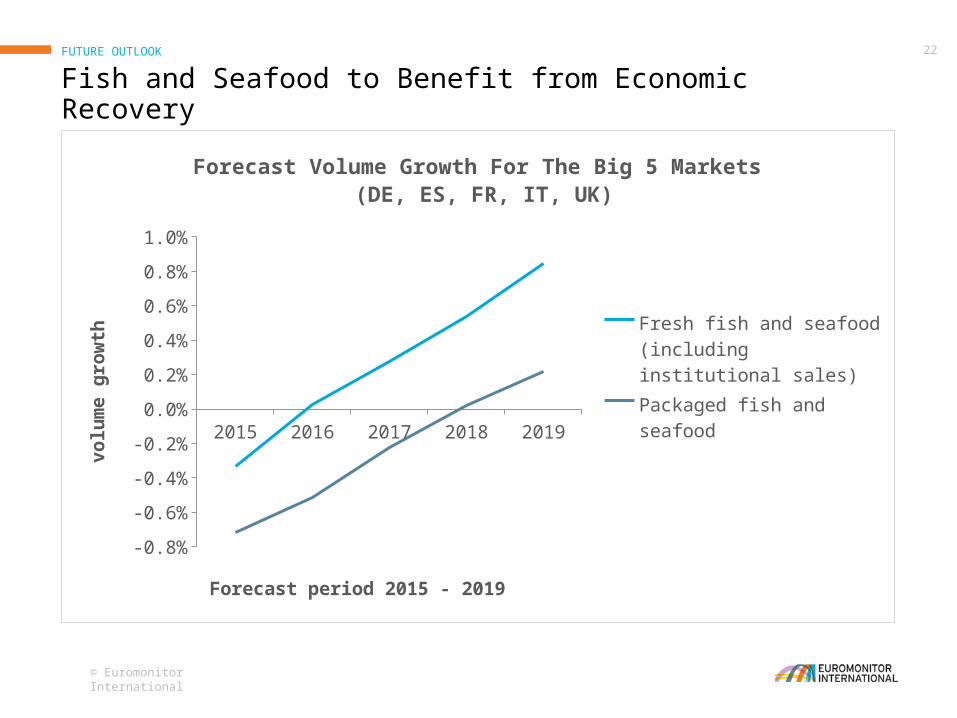

Fish and Seafood to Benefit from Economic RecoveryFUTURE OUTLOOK

2015 2016 2017 2018 2019

-0.8%

-0.6%

-0.4%

-0.2%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

Forecast Volume Growth For The Big 5 Markets (DE, ES, FR, IT, UK)

Fresh fish and seafood (including institutional sales)Packaged fish and seafood

Forecast period 2015 - 2019

vo

lum

e g

row

th

© Euromonitor International

23

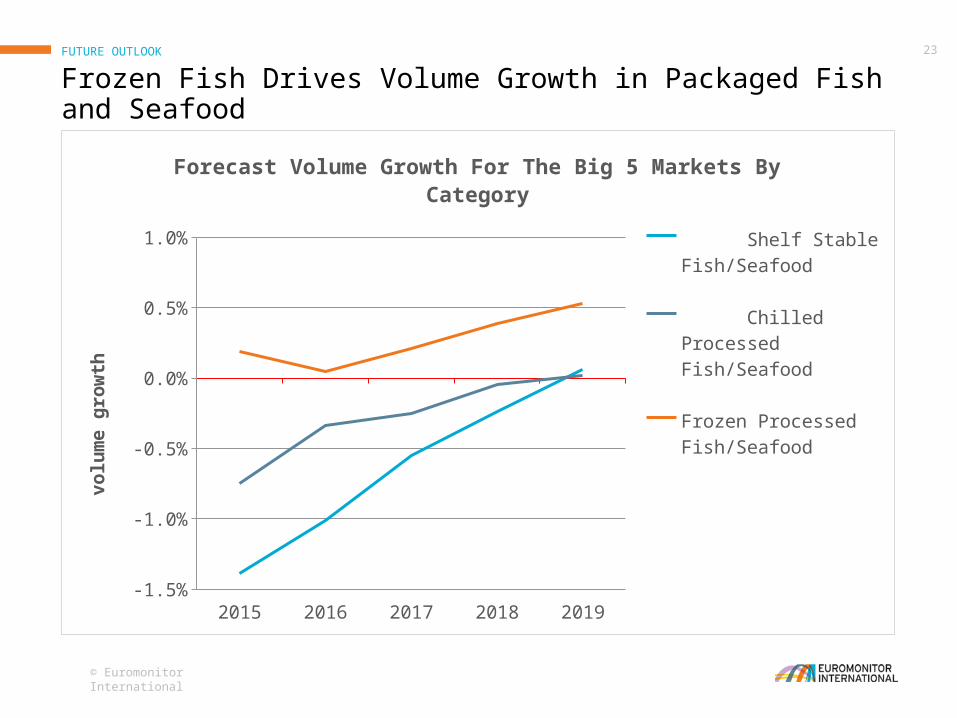

Frozen Fish Drives Volume Growth in Packaged Fish and SeafoodFUTURE OUTLOOK

2015 2016 2017 2018 2019-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

Forecast Volume Growth For The Big 5 Markets By Category

Shelf Stable Fish/Seafood

Chilled Pro-cessed Fish/Seafood

Frozen Processed Fish/Seafood

vo

lum

e g

row

th

© Euromonitor International

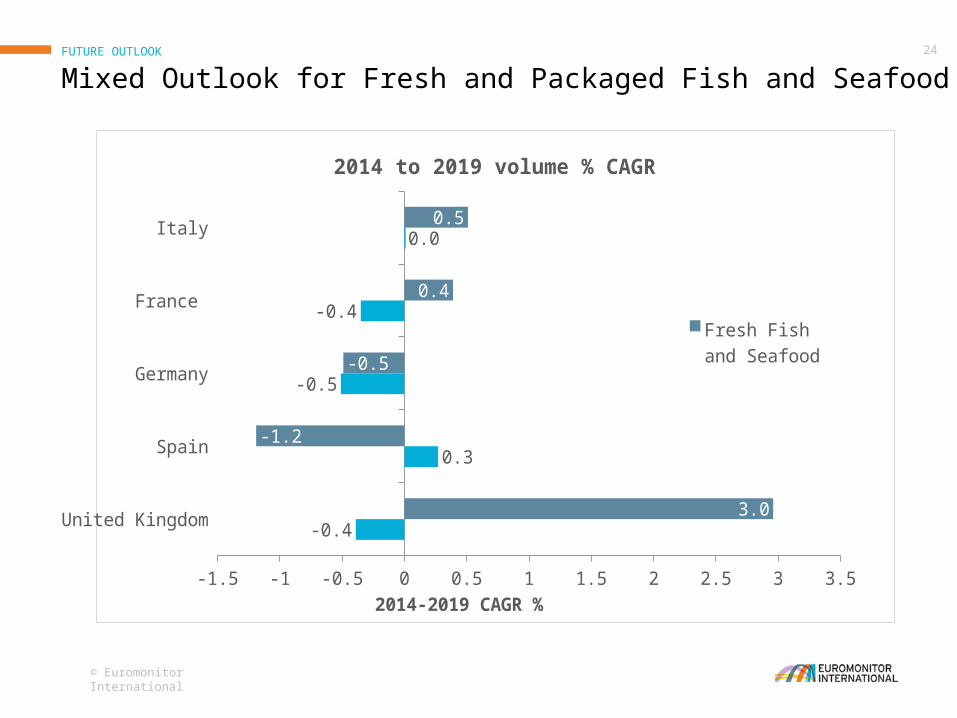

24

Mixed Outlook for Fresh and Packaged Fish and Seafood FUTURE OUTLOOK

United Kingdom

Spain

Germany

France

Italy

-1.5 -1 -0.5 0 0.5 1 1.5 2 2.5 3 3.5

-0.4

0.3

-0.5

-0.4

0.0

3.0

-1.2

-0.5

0.4

0.5

2014 to 2019 volume % CAGR

Fresh Fish and Seafood

2014-2019 CAGR %

© Euromonitor International

25

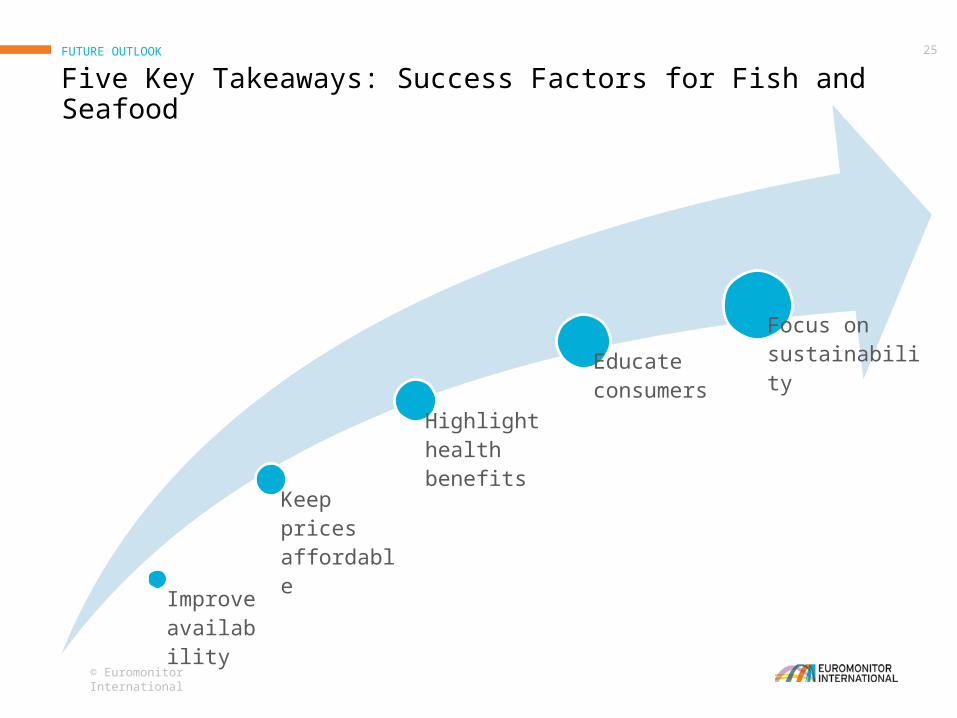

Five Key Takeaways: Success Factors for Fish and SeafoodFUTURE OUTLOOK

Improve availability

Keep prices affordable

Highlight health benefits

Educate consumers

Focus on sustainability

© Euromonitor International

26

THANK YOU FOR LISTENINGWiebke Schoon| Research Analyst Food and Nutrition