treasury risk management - citibank · average r$2.35 for ambev’s 2015 dollar cogs hedge in...

TRANSCRIPT

Treasury Risk

Management

Macro Trends and the

Implications for Corporations

Andre Secron

Head of Foreign Exchange Corporate Sales

and Structuring

Latin America

+1 (212) 723-1351

Treasury and Trade Solutions

1. Market Trend—The Strong US$ Cycle

2. The Implications of the Strong US$ for Corporations

3. Considerations for Hedging Policies

4. Key Takeaways

1. Market Trend—The Strong US$ Cycle

2. The Implications of the Strong US$ for Corporations

3. Considerations for Hedging Policies

4. Key Takeaways

70

90

110

130

150

1973 1978 1983 1988 1993 1998 2003 2008 2013 2018

History Suggests Continued Dollar Appreciation in Current Cycle

Since the inception of floating currencies, peak-to-trough cycles in the US$ have lasted between 6–9 years. With potentially 3–6 years remaining in current cycle, US$ may

strengthen by a further 10–30%. And while cycles may revert eventually, the long-run may encapsulate significant volatility impacting current performance.

US$ Since 1973

US Traded Weighted Real Major Currencies Dollar Index

6–7 years

60% (7.5% ann.)

7–8 years

(40)% (5)% ann.)

6–7 years

60% (7.5% ann.) ~9 years

(33)% (4)% ann.)

Current Cycle

Potentially 3–6 years

Remaining Potential 10–30%

US Corporations Benefited

Greatly from the Previous

9 year Cycle of US$ Weakness

Source: Bloomberg.

4

US$ Appreciation Projected Across the Board

Source: Bloomberg, Citi GEOS.

Note: Projections based on Citi FX forecasts. Market data as of 1/19/2015.

DM Currencies EM Currencies Commodity Currencies

10.9%

-0.6%

3.3%

-0.6%

2.6%

-6.6%

3.9%

0.4%

16.1%

13.7%

7.4%

11.6%

8.8% 8%

10% 10%

7.1% 7.1%

Current 3.22 634 15.1 2590 1.08 121 1.49 0.77 1.26 1Y Forecast 3.57 655 15.5 2690 0.93 130 1.37 0.7 1.35

Long Term 3.2 630 14.1 2600 0.95 135 1.38 0.7 1.35

MXN

5

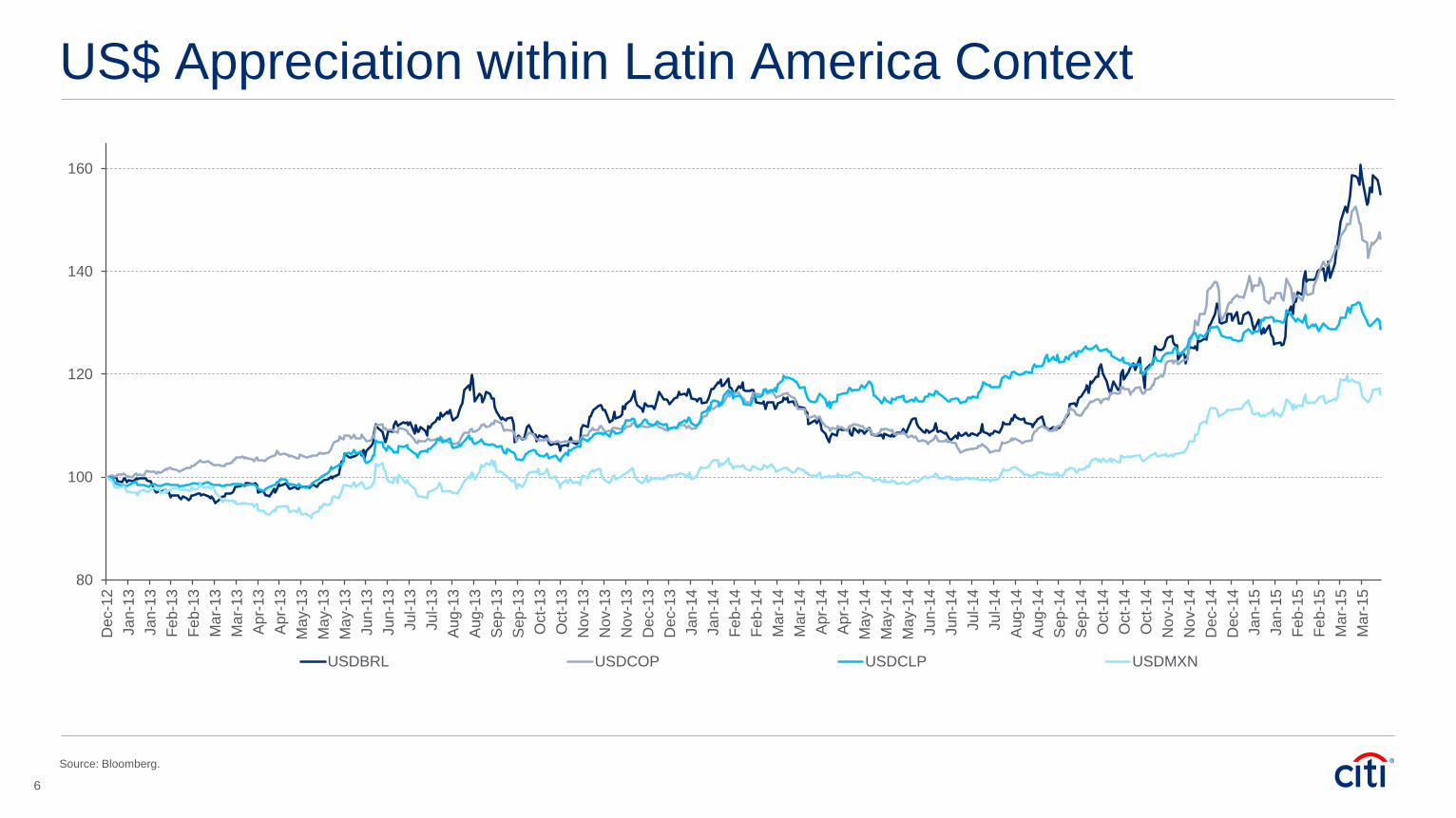

US$ Appreciation within Latin America Context

Source: Bloomberg.

80

100

120

140

160

Dec-1

2

Ja

n-1

3

Ja

n-1

3

Feb-1

3

Feb-1

3

Ma

r-13

Ma

r-13

Apr-

13

Apr-

13

Ma

y-1

3

Ma

y-1

3

Ma

y-1

3

Ju

n-1

3

Ju

n-1

3

Ju

l-1

3

Ju

l-1

3

Aug

-13

Aug

-13

Sep

-13

Sep

-13

Oct-

13

Oct-

13

Nov-1

3

Nov-1

3

Nov-1

3

Dec-1

3

Dec-1

3

Ja

n-1

4

Ja

n-1

4

Feb-1

4

Feb-1

4

Ma

r-14

Ma

r-14

Apr-

14

Apr-

14

Ma

y-1

4

Ma

y-1

4

Ma

y-1

4

Ju

n-1

4

Ju

n-1

4

Ju

l-1

4

Ju

l-1

4

Aug

-14

Aug

-14

Sep

-14

Sep

-14

Oct-

14

Oct-

14

Oct-

14

Nov-1

4

Nov-1

4

Dec-1

4

Dec-1

4

Ja

n-1

5

Ja

n-1

5

Feb-1

5

Feb-1

5

Ma

r-15

Ma

r-15

USDBRL USDCOP USDCLP USDMXN

6

US$—The Multi-Year Bull Trend: Why?

Stronger Expected US

Economic Growth

Declining unemployment rate (under 6%)

Strengthening activity in industrials and

service sectors

Improving personal consumption

expenditures

3% forecasted GDP growth in 2015–2016

Divergence in Central

Bank Action

Sustained US economic recovery

supporting US Fed tightening

Persistent sluggish growth in Eurozone and

Japan supporting further easing

Unexpected central bank actions (i.e.

removal of EURCHF floor) drive volatility

Lower Oil Prices

Oil producing countries experiencing

declining revenues, increasing budget

deficits, and adverse exchange rate impact

Slowdown in Expected

EM Growth

China’s slower transition towards a

domestic consumption driven economy

Broader EM headwinds due to current

account deficits

GDP growth slowing to low 7% in China

Expectation of Sluggish Growth

in Eurozone and Japan

Persistent low/negative inflation despite

unprecedented easing

Weak labor markets with

structural challenges

Stronger

US$

7

1. Market Trend—The Strong US$ Cycle

2. The Implications of the Strong US$ for Corporations

3. Considerations for Hedging Policies

4. Key Takeaways

Strong Dollar Already Affecting Corporates

Our largest exposure remains the euro. […] we’ve hedged

roughly 50% of our 2015 euro exposure […] Considering

these impacts, FX will be a sales headwind for 2015 [ … ],

which works out to about $0.10 per share.

Dollar’s rise against the ringgit was partly to blame for

lower quarterly revenues. About 70% of the company’s

debt is in U.S. dollars, and its bond yields spiked as the

ringgit fell nearly 9% in the past six months.

3M estimates that year-on-year currency effects, including

hedging impacts, decreased net income attributable to 3M

by approximately $10 million for the three months ended

September 30, 2014.

The net income and EPS include a charge of EUR 180

million from negative FX revaluation in the third quarter

due to the strong strengthening of the dollar. […] we

increased the pace of hedging activity due to the favorable

dollar environment.

Source: Bloomberg.

9

Stronger US$ Impacts Multiple Corporate Dimensions A stronger US$ impacts corporates across the financial statements, potentially pressuring margins, overseas valuations, and the

ability to compete in the future. Prudent risk management can help to mitigate these concerns.

Timing mismatch between contract and payment in a foreign currency

Competitor pricing

Lower channel costs

Mismatches between sales in one currency and costs in another currency

Market volatility as well as uncertainty in revenues

Foreign-based subsidiaries may create earnings volatility

Can impact earnings per share (EPS), credit ratings and cost of capital

Potential covenant breaches

Interest cost can be minimized

Match currency exposure of cash flows (CF) and net assets

Protecting shareholder’s investments in foreign subsidiary

Expected repatriation of overseas cash

Increasing global footprint

Potential cross-border acquisitions

Internal investment: Predicable cash flow = more investment

Sufficient liquidity

Operational

Financial

Economic/Strategic

Transactional

Cash Flow

Operating Earnings

Debt/Liabilities

Assets

Business Growth

Competition

Capital

Income

Statement

Balance Sheet

10

Who are Most Impacted?

Multinational Corporates

US multinationals with significant

sales abroad will see their foreign

cash flows erode

Non-US multinationals with US

revenue exposures will benefit from

stronger US$

Non-US multinationals that fund in

US$ will see negative impact on their

balance sheet as US$ strengthens

US$-Funded EM Corporates

EM multinationals with large US

revenue exposures will benefit from

stronger US$

EM multinationals that fund in US$

will see negative impact on their

balance sheet as US$ strengthens

Global Commodity Producers

While revenues of foreign oil

producers will decrease due to falling

oil prices, a stronger US$ will

mitigate the negative impact

US producers will benefit from

lower foreign production costs as

US$ strengthens

Careful analysis is key to

understanding how FX/commodity

correlation impacts corporate top and

bottom lines

11

1. Market Trend—The Strong US$ Cycle

2. The Implications of the Strong US$ for Corporations

3. Considerations for Hedging Policies

4. Key Takeaways

Traditional Hedging Programs Static Hedging Program

Hedges for the entire year implemented at one single point

in time

Rolling Hedging Program

Hedges are implemented throughout the year as new forecasts

become available

Provides predictability of the value of future transactions over a

defined period of time

Layered Hedging Program

Similar to a rolling program in that hedges are implemented

throughout the year

However, in an effort to create smoothing the hedge ratio is

built-up over time

Static Hedging Program

Rolling Hedging Program

Layered Hedging Program

13

A Customized Solution to Protect Against US$ Strength

Front-loading the hedging schedule to increase value at risk (VaR) reduction

Adding options to the mix of hedge instruments to maintain the flexibility lost from front-loading. This is particularly important as the

strengthening in the US$ is unlikely to be in a straight line over time

Standard Layered Hedging

Dynamic Layered Hedging

Extending hedge duration

14

Portfolio Diversification Portfolio diversification can be a powerful tool to stabilize the performance of a hedging portfolio. In particular, the strategy is highly

effective in periods of increased market volatility.

CitiFX ran a backtest analysis of the hypothetical performance of four different hedging strategies and an unhedged portfolio

The simulation assumes a quarterly rolling hedging strategy. Follows ahead the results of the combined portfolios

Hedging

Period

FX Spot at

Beginning

FX Spot at

End Forward Strategy A Strategy B Strategy C Portfolio1 Portfolio 2

1Q13 13.68 12.61 13.92 13.64 13.50 13.92 13.16 13.42

2Q13 12.96 12.27 13.21 12.95 12.82 13.21 12.64 12.81

3Q13 12.61 12.62 12.84 12.59 12.46 12.62 12.58 12.57

4Q13 12.27 12.99 12.46 12.39 12.99 12.55 12.88 12.73

1Q14 12.62 13.51 12.83 12.68 12.44 12.90 13.09 12.88

2Q14 12.99 13.11 13.17 12.90 12.77 13.11 13.02 12.97

3Q14 13.51 12.96 13.69 13.42 13.28 13.69 13.22 13.34

15

Portfolio Diversification (Cont’d)

12.00

12.50

13.00

13.50

14.00

1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 2Q 2014 3Q 2014

FX Spot at End Forward Portfolio1 Porfolio 2

FX Spot at End Forward Strategy A Strategy B Strategy C

Portfolio 1 50% 0% 0% 25% 25%

Portfolio 2 25% 0% 25% 25% 25%

16

1. Market Trend—The Strong US$ Cycle

2. The Implications of the Strong US$ for Corporations

3. Considerations for Hedging Policies

4. Key Takeaways

Key Takeaways—Risks, Implications and Solutions

Risks

Implications

Solutions

Widening growth prospects between US and rest of world, and sustained divergence in central bank policies will

drive US$ stronger in current cycle. Meanwhile, corporates have become more global with a higher percentage

of revenues coming from overseas

Exposure to FX risk is a predominant driver of earnings volatility, while changing volatility and correlation

dynamics today may negatively impact corporate earnings

The turn of US$ cycle from weakness to strength requires corporates today to review and adjust their risk

management strategies

Holistic assessment of a corporate’s market risk exposures that takes into consideration correlation and volatility

dynamics are critical to effective risk management

Effective risk management can potentially boost valuation and improve growth prospects. Corporates should

adjust hedging strategies and capital deployment policies in today’s strong US$ cycle

Stronger US$ may affect corporates in multiple dimensions, with implications on cash flows, balance sheets, and

business strategies

The implications vary for different types of global corporates, depending on their market risks exposures

Many corporates have reported negative impacts from US$ strength in recent quarters with potential for more

downside risk in coming quarters

18

Key Takeaways—Tangible Results

“…dollar COGS hedge is the most “attractive” in several years. A second factor is, following Citi’s recently revised f/x estimate, the value of

Ambev’s dollar COGS hedge for 2015 has increased significantly. This is true both for its own earnings growth potential as well as relative

to its beverage peers (brewers and bottlers alike) who either can’t hedge their dollar-linked COGS against a weaker f/x or hedge less

effectively. We incorporate Citi’s average 2015 real/dollar f/x estimate of R$2.83 (from Jan/26), 13% weaker than the estimate in October

(before the elections), implying a 20% depreciation YoY. More importantly, this average market rate is well above our assumption of an

average R$2.35 for Ambev’s 2015 dollar COGS hedge in Brazil, which we believe no other beverage peer has. R$2.35 implies a 7%

weaker hedge than 2014 (when it was 15% higher YoY), suggesting less pressure compared to prior years. The benefit of the hedge is

partly offset by less favorable commodities hedge this year versus last year.”

Alexander Robats, Head of Citi's Latin American Consumer Staples Equity Research team. In the Food/Beverage/HPC sectors –

January 28th, 2015

“Based on a less onerous beverage tax (see note), more than expected Brazil margin expansion, recent sharp currency

depreciation (increasing the value of its dollar COGS hedge), and an undemanding valuation, we argue Ambev’s de-rating is over

and upgrade to Buy.”

19

Citi believes that sustainability is good business practice. We work closely with our clients, peer financial institutions, NGOs and other partners to finance solutions to climate change, develop industry standards, reduce our own

environmental footprint, and engage with stakeholders to advance shared learning and solutions. Highlights of Citi’s unique role in promoting sustainability include: (a) releasing in 2007 a Climate Change Position Statement, the

first US financial institution to do so; (b) targeting $50 billion over 10 years to address global climate change: includes significant increases in investment and financing of renewable energy, clean technology, and other carbon-

emission reduction activities; (c) committing to an absolute reduction in GHG emissions of all Citi owned and leased properties around the world by 10% by 2011; (d) purchasing more than 234,000 MWh of carbon neutral power for

our operations over the last three years; (e) establishing in 2008 the Carbon Principles; a framework for banks and their U.S. power clients to evaluate and address carbon risks in the financing of electric power projects; (f)

producing equity research related to climate issues that helps to inform investors on risks and opportunities associated with the issue; and (g) engaging with a broad range of stakeholders on the issue of climate change to help

advance understanding and solutions.

Citi works with its clients in greenhouse gas intensive industries to evaluate emerging risks from climate change and, where appropriate, to mitigate those risks.

efficiency, renewable energy and mitigation

© 2015 Citibank, N.A. All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

IRS Circular 230 Disclosure: Citigroup Inc. and its affiliates do not provide tax or legal advice. Any discussion of tax matters in these materials (i) is not intended or written to be used, and cannot be used or

relied upon, by you for the purpose of avoiding any tax penalties and (ii) may have been written in connection with the "promotion or marketing" of any transaction contemplated hereby ("Transaction").

Accordingly, you should seek advice based on your particular circumstances from an independent tax advisor.

In any instance where distribution of this communication is subject to the rules of the US Commodity Futures Trading Commission (“CFTC”), this communication constitutes an invitation to consider entering

into a derivatives transaction under U.S. CFTC Regulations §§ 1.71 and 23.605, where applicable, but is not a binding offer to buy/sell any financial instrument.

Any terms set forth herein are intended for discussion purposes only and are subject to the final terms as set forth in separate definitive written agreements. This presentation is not a commitment to lend, syndicate a

financing, underwrite or purchase securities, or commit capital nor does it obligate us to enter into such a commitment, nor are we acting as a fiduciary to you. By accepting this presentation, subject to applicable law or

regulation, you agree to keep confidential the information contained herein and the existence of and proposed terms for any Transaction.

Prior to entering into any Transaction, you should determine, without reliance upon us or our affiliates, the economic risks and merits (and independently determine that you are able to assume these risks) as well as the legal,

tax and accounting characterizations and consequences of any such Transaction. In this regard, by accepting this presentation, you acknowledge that (a) we are not in the business of providing (and you are not relying on us

for) legal, tax or accounting advice, (b) there may be legal, tax or accounting risks associated with any Transaction, (c) you should receive (and rely on) separate and qualified legal, tax and accounting advice and (d) you

should apprise senior management in your organization as to such legal, tax and accounting advice (and any risks associated with any Transaction) and our disclaimer as to these matters. By acceptance of these materials,

you and we hereby agree that from the commencement of discussions with respect to any Transaction, and notwithstanding any other provision in this presentation, we hereby confirm that no participant in any Transaction

shall be limited from disclosing the U.S. tax treatment or U.S. tax structure of such Transaction.

We are required to obtain, verify and record certain information that identifies each entity that enters into a formal business relationship with us. We will ask for your complete name, street address, and taxpayer ID number.

We may also request corporate formation documents, or other forms of identification, to verify information provided.

Any prices or levels contained herein are preliminary and indicative only and do not represent bids or offers. These indications are provided solely for your information and consideration, are subject to change at any time

without notice and are not intended as a solicitation with respect to the purchase or sale of any instrument. The information contained in this presentation may include results of analyses from a quantitative model which

represent potential future events that may or may not be realized, and is not a complete analysis of every material fact representing any product. Any estimates included herein constitute our judgment as of the date hereof

and are subject to change without any notice. We and/or our affiliates may make a market in these instruments for our customers and for our own account. Accordingly, we may have a position in any such instrument at

any time.

Although this material may contain publicly available information about Citi corporate bond research, fixed income strategy or economic and market analysis, Citi policy (i) prohibits employees from offering, directly or indirectly,

a favorable or negative research opinion or offering to change an opinion as consideration or inducement for the receipt of business or for compensation; and (ii) prohibits analysts from being compensated for specific

recommendations or views contained in research reports. So as to reduce the potential for conflicts of interest, as well as to reduce any appearance of conflicts of interest, Citi has enacted policies and procedures designed to

limit communications between its investment banking and research personnel to specifically prescribed circumstances.