transportation labour market outlook … labour market outlook for the asia pacific gateway corridor...

TRANSCRIPT

—

TRANSPORTATION LABOUR MARKET OUTLOOK FOR THE ASIA PACIFIC GATEWAY CORRIDOR 2016–2025—ASIA PACIFIC GATEWAY CORRIDOR

—

The Asia Pacific Gateway Skills Table wishes to acknowledge the funding support from the Government of Canada’s Sectoral Initiatives Program.

—

La Table sur les compétences de la Porte d'entrée de l'Asie-Pacifique reçoit le soutien financier du Programme d’ initiatives sectorielles du gouvernement du Canada.

The opinions and interpretations in this publication are those of the author and do not necessarily reflect those of the Government of Canada.

—

Les opinions et les interprétations figurant dans la présente publication sont celles de l’auteur et ne représentent pas nécessairement celles du gouvernement du Canada.

—

www.apgst.ca

CONTENT

APPENDIX

Chapter1 EXECUTIVESUMMARY 6

LabourDemand 7

LabourSupply 8

HiringDifficultyIndex 8

Chapter2 HIGHLIGHTS 9

AirSector 10

LogisticsSector 13

RailSector 16

TruckingSector 19

Chapter3 KEYFACTS2016–2025 22

HiringDifficultyIndex 22

LabourDemand 23Expansion 24

LabourSupply 25Replacement 26

BaseSupply 27

NewSupply 28

NewEntrants 29

Immigration 30

Mobility 31

Chapter4 IMPACTOFTHEECONOMICSCENARIOS 32 Chapter5 CONCLUSIONS 34

AppendixA DescriptionofMetricsandGlossaryofTerms 38

AppendixB EconomicIndicatorsandMajorProjects includedintheEconomicScenarios 43

AppendixC DataTablesbySectorandEconomicScenario: TheAsiaPacificGatewayCorridor 52

APGC–AllSectors 52

Air 55

Logistics 58

Rail 61

Trucking 64 AppendixE TheAsiaPacificGatewayCorridorOccupations 67

4 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

The Asia Pacific Gateway Skills Table (APGST) and its partners developed this report to provide comprehensive and up-to-date information on employment needs over a 5- and 10-year forecast period, with a focus on key occupations in the Asia Pacific Gateway Corridor (APGC). Reports are also available covering sector outlooks and occupational snapshots for 34 occupations considered essential to the APGC. The snapshots contain detailed supply and demand information, highlights, and data tables. Reports can be found at lmionline.ca.

This forecast provides valuable information that can be used to facilitate labour market planning for decision makers and employers, and can help workers make informed choices about their careers and futures. Forecasts are developed with a leading-edge economic modeling system using data from a variety of reliable sources, and are validated by key stakeholders. The statements and assessments of labour market conditions in this report are based on forecasts; they are “expected” conditions and outcomes relative to the economic conditions used to create the information.

The APGST generates the information in these reports from a labour market forecast based on three economic scenarios: the High Investment Scenario, Moderate Investment Scenario, and Low Investment Scenario. Definitions of these scenarios and a full description of labour market metrics used in the analysis can be found in Appendix A. The analysis that follows, unless otherwise indicated, is based on a Moderate Investment Scenario, which takes into account projects that are planned and likely to proceed. Provincial information is included for British Columbia, Alberta, Saskatchewan and Manitoba in Appendix B. The data tables for the APGC, by sector and economic scenario, are provided in Appendix C.

Related reports that may be of interest are:JJ British Columbia Regional Outlook 2016–2025JJ Alberta Regional Outlook 2016–2025JJ Saskatchewan Regional Outlook 2016–2025JJ Manitoba Regional Outlook 2016–2025JJ Air Sector Outlook 2016–2025JJ Logistics Sector Outlook 2016–2025JJ Rail Sector Outlook 2016–2025JJ Trucking Sector Outlook 2016–2025

These and other documents can be found at lmionline.ca.

ABOUTTHISREPORT

LabourMarketInformationisdataaboutthesupplyofanddemandforlabourinkeyoccupations,sectors,andregionsoftheeconomy.

5 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

of jobs are generated by Expansion in the first 5 years of the forecast. See pages 24–26 for more information on Replacement vs. Expansion.

of workers move into the 34 APGC Occupations from other occupations in the labour force. See page 31 for more information on Labour Force Mobility.

of new workers are immigrants to Canada. See page 30 for more information on Immigration.

BYTHENUMBERS

Air Logistics Rail Trucking APGC Total

Average Jobs1 181,514 190,145 186,892 270,475 557,162

New Positions 13,250 13,673 14,409 19,332 40,037

Net New Workers 11,772 12,413 13,063 17,196 36,109

Growth (%) 7.6% 7.5% 8.1% 7.4% 7.5%

Replacement 49,060 45,440 53,097 68,568 139,056

Replacement Rate for Today’s Workforce

27.3% 24.1% 28.7% 25.3% 25.0%

Job Openings 61,020 59,917 67,296 84,870 177,374

Total New Supply 60,556 58,955 66,628 84,900 176,239

New Supply by Type

Labour Force Mobility

29,112 29,200 27,585 52,904 98,841

International Mobility

9,991 5,958 11,355 12,388 23,880

Mobility 2,801 7,029 5,475 6,824 17,402

New Entrants 18,652 16,768 22,213 12,784 36,116

1 Occupations are not unique to a sector; some are found in all four. As a result, the sum of the sectors will be higher than the total for the APGC.

24 20 14

6

Chapter 1

Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Executive Summary

British Columbia’s geographic location provides a natural advantage as the gateway between North America and Asia. Each of the provinces in the Corridor has vastly different labour, recruitment, and retention challenges. The location of BC’s ports means the sailing time to markets in Asia is two days less than it is from other ports in the Western hemisphere. This adds intensity to British Columbia’s potential liquefied natural gas (LNG) industry and its rich natural resource base; together with the impact of changing oil projects in Alberta, and changes in metals mining in Saskatchewan and Manitoba, there is substantial variability in the economy across the four provinces. If the developments in the Moderate or High Economic Scenarios come to pass in the next decade, then competition for labour will increase dramatically in what is already a very tight labour market for skilled and experienced occu-pations. If the conditions in the Low Scenario dominate the decade, then the challenge across the provinces will be the replacement of experienced workers, who will retire in large numbers.

The support and maintenance of the APGC and its labour force is considered central to supporting expansion in the Canadian economy; a robust and flexible transportation sector will be required to truly capture the area’s full potential. A skilled, mobile labour force will also be essential. The APGC Labour Market Information (LMI) Project provides the foundation for insight into the labour conditions for APG businesses. By doing so, it supports the strong function of this central element of Canada’s economy.

The APGC is forecast to continue to grow during the 10 years of the forecast as trade activity between North America and Asia continues to be a key economic driver for the APGC economy. This growth will intensify the need for an available, well-trained workforce. The forecast shows that employers will face some challenges in hiring the workers they need in the 34 occupations starting in 2017, and the situation will remain challenging through the balance of the forecast period. This trend is similar across the four sectors, which include Air, Logistics, Rail, and Trucking.

See the Sector Outlook reports for in-depth information for each of the sectors.

EXECUTIVESUMMARY

TheAsiaPacificGatewayCorridor(APGC)isanintegratedsupplychain,thatincludesairports,seaports,railways,roadways,andbordercrossings,connectingCanadaandtheNorthAmericanmarkettoAsiaandtheworld.

7

Chapter 1

Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Figure 1 Components of New Supply, APGC, 2016 and 2025

80%

60%

40%

20%

0

-20%

-40%

Perc

ent o

f Tot

al N

ew S

uppl

y

NewEntrants

Mobility Labour ForceMobility

Intl.Mobility

2016 2025

LABOURDEMANDOver the next 10 years, 177,375 jobs will need to be filled, with 22% generated by Expansion and 78% by Replacement (see page 26). The number of Job Openings will peak in 2018 and decline slowly but steadily thereafter, with a slight rebound in 2025.

By sector, Job Opening numbers are approximately:JJ 61,120 in AirJJ 59,915 in LogisticsJJ 67,295 in RailJJ 84,870 in Trucking

The number of positions increases by 7.5%, for a total of 40,035 new positions over the forecast period.

LABOURSUPPLYThe forecast shows New Supply is not keeping pace with Job Openings, especially in Alberta. However, in Manitoba, supply and demand growth are balanced. The composition of New Supply will shift over the 10 years, with increasing reliance on Immigration (Figure 1).

For the New Supply of workers across the four sectors of the APGC:JJ 25% of the workers in the 34 occupations today will retire and

leave the APGC labour market by the end of the forecast period.JJ More than 56% of the New Supply will come from New Entrants.JJ Just under 15% of new workers will come from other countries.JJ 10% of new workers will move to the APGC from other provinces.JJ Approximately 20% will move into the 34 occupations from other

occupations or by returning to the labour force.

Investment Scenario Comparison The forecast shows that both supply and demand for all 34 occupations in all four sectors in the APGC are influenced by the economic scenarios. In the APGC, the High Investment Scenario will generate about 34,085 more Job Openings (47%) than the Low in the first 5 years of the fore-cast. In the final 5 years, between 2021 and 2025, the Low Investment Scenario outperforms the High by 9,265 Job Openings, for a net effect that has the High Investment Scenario generating about 24,820 more Job Openings (16%).

All four sectors show the same pattern. The Logistics and Trucking Sectors show the largest impact from the economic scenarios in both the first 5 years and the full 10 years. Trucking has the largest (49%, or 16,115 Job Openings) 5-year impact among the four sectors, and Rail the smallest (36%, or 10,510 Job Openings) 10-year impact. The analysis in this report is based on the Moderate Investment Scenario (the expected scenario), which takes into account projects that are planned and likely to proceed (see Appendix B).

Executive Summary

8

Chapter 1

Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Executive Summary

HIRINGDIFFICULTYINDEXThe Hiring Difficulty Index assesses the overall challenges for employers who are trying to hire in the labour market. It aggregates five metrics and combines them to provide a single measure that reflects the different interactions between the labour market components. For example, the metrics can show the ratio of workers to Job Openings (the Market Tightness) as “Tight”, with International Reliance and Supply Lag Low and Mobility positive (i.e., workers are moving in), while the Loss of Experience is Moderate and the reliance on New Entrants is Extreme. This implies quite different labour market conditions than a situation where the Market Tightness is “Tightening” (i.e., less difficult), but International Reliance is High, supply is growing much more slowly than Job Openings, and a high portion of current workers are leaving to work in other provinces. For more information on labour market metrics, see Appendix A.

The labour market for the 34 occupations included in the APGC forecast will provide some challenges for employers to find the workers they need for most years of the forecast (see Table 1). The forecast anticipates 2016 as the year with the most flexibility.

Table 1 Hiring Difficulty Index for the APGC and the Sectors

Sector 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Airsome

challengesdifficult some challenges

Logisticseasy

marketsome challenges

Raileasy

marketsome challenges

Truckingeasy

marketsome challenges

APGC Totaleasy

marketsome challenges

Oversupplied Market 0–8

Easy Market 9–15

Difficult 23–29

Extremely Difficult 30+

Some Challenges 16–22

9 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Chapter 2 Highlights

By 2024, Asia–Pacific container traffic providing goods to consumers across Canada and arriving at British Columbia’s deep water ports is expected to increase by more than 70%. Exports of goods (grain, potash, metals and minerals) from all four APGC provinces, driven by demand from our Asian trading partners, is also expected to grow (by 60% or more). To compete successfully for this growing trade and capitalize on Canada’s natural geographic advantage, APGC partners—federal and provincial governments, their agencies, ports, railways, and airport authorities— have set ambitious growth targets for British Columbia’s ports and airports. Major public–private investments have increased capacity and will eliminate congestion and streamline operations. Projects to expand and enhance port, rail, road, and airport infrastructure currently planned or underway total well over $20 billion.

This study indicates that there could be 40,035 more jobs by 2025 than there are today in the 34 APGC occupations assessed across the four provinces in the APGC. It also shows that 177,375 jobs will need to be filled over the 10 years of the forecast: 22% generated by Expansion and 78% by Replacement in those same occupations. This is about 9% of the estimated 2,052,720 Job Openings forecast for all occupations in the four provinces of the APGC.

This section provides labour market highlights for the following four key sectors in the APGC:

HIGHLIGHTS

TheAPGCisforecasttocontinuetogrowinthe10yearsoftheforecastastradeactivitybetweenNorthAmericaandAsiaaccelerates.ToachievethisgrowthandcapturethevalueoftheinfrastructureandcapacityinvestmentsbeingmadeintheCorridor,avibrant,well-trained,resilientworkforcemustbeavailabletoemployers.Demographics,economicchanges,andaccesstotrainingopportunitiesallaffecttheavailabilityoflabour.

Air Logistics Rail Trucking

10 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

AIRSECTOR

Chapter 2 Highlights — Air Sector

By the Numbers

Job Openings to be filled 61,020 34% of APGC total

Replacement Job Openings 49,060 80% of Job Openings

Job Openings created by Expansion

11,958 15% of Job Openings in first 5 years

Workers who will retire and leave the labour force

49,060 29% of today’s workers

New workers – New Entrants to the industry

29,112 48% of the New Supply

New workers – from other countries

9,991 16% of the New Supply

New workers – from other provinces

2,801 5% of the New Supply

New workers – from other parts of the labour force

18,652 31% of the New Supply

Average time left in the industry 16 – 26 years until retirement (between the ages of 60–70)

Air cargo comprises mostly perishables and low-weight, high-value consumer goods. While the volume by weight of air cargo is substantially smaller than in any other mode, the value in dollars is equivalent to that moved by rail. Developing and expanding various aspects of the air cargo business is a strategic focus inside the APGC.

The APGC LMI Project Air Sector includes 15 occupations. For details on individual occupations, please refer to the Occupational Snapshots.

Airtransportusingcargoaircraftisavitalcomponentofmanyinternationallogisticsnetworks.

11 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Chapter 2 Highlights — Air Sector

Table 2 Air Sector Occupations and Job Openings

NOC Occupation Title Job Openings

0016 Senior Managers – Construction, Transportation, Production and Utilities

24,060

0714 Facility Operation and Maintenance Managers

27,380

0731 Managers in Transportation 15,518

1525 Dispatchers 10,291

1526 Transportation Route and Crew Schedulers

1,485

2131 Civil Engineers 24,220

2241 Electrical and Electronics Engineering Technologists and Technicians

11,655

2243 Industrial Instrument Technicians and Mechanics

2,951

2261 Non-Destructive Testers and Inspection Technicians

3,128

2262 Engineering Inspectors and Regulatory Officers

1,896

2263 Inspectors in Public and Environmental Health and Occupational Health and Safety

13,415

2271 Air Pilots, Flight Engineers and Flying Instructors

4,654

7231 Machinists and Machining and Tooling Inspectors

9,932

7311 Construction Millwrights and Industrial Mechanics

20,993

7315 Aircraft Mechanics and Aircraft Inspectors

5,153

The forecast for 2016–2025 shows 2017 as the most challenging year that employers will face. In most of the forecast, employers will have some challenges in hiring the workers they need in the 15 occupations. This trend is similar across the four provinces, with Manitoba showing difficult conditions more often than the others.

Job Openings are more likely to be created by Replacement (80%) than by Expansion. More than 1 in 4 workers will retire and leave the sector, a little higher than in the APGC as a whole. More than 2 in 5 Senior Managers – Construction, Transportation, Production and Utilities will have retired and left the Labour Force by 2025, as will more than a third of Managers in Transportation.

Almost half of all new workers in the Air Sector will be New Entrants. Virtually all new Industrial Instrument Technicians and Mechanics will be New Entrants, which means employers will need to invest in more on-the-job training to enable newly trained workers to contribute to overall productivity. Aircraft Mechanics and Aircraft Inspectors and Air Pilots, Flight Engineers and Flying Instructors show a significant loss of workers to other provinces. Almost a third of new workers in the 15 occupations of the APGC Air Sector are from other parts of the labour force, but there is a wide variance, with 90% of Managers in Transportation coming from this source while Air Pilots, Flight Engineers and Flying Instructors lose the equivalent of more than a third of New Supply to other occupations. Just over 15% of the New Supply of workers will come from other countries. For Air Pilots, Flight Engineers and Flying Instructors, more than 50% of new workers are from other countries.

36% of the workers in the APGC Air Sector live in BC, 47% in Alberta, 8% in Saskatchewan, and 9% in Manitoba.

12 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Chapter 2 Highlights — Air Sector

APGST Labour Market Metrics for the Air Sector The following table shows the six APGST labour market metrics. When considered together, these indicators provide a quick reference “scorecard” on the conditions of the labour market. For more information on labour market metrics, see Appendix A or the Occupational Snapshots, available at lmionline.ca.

Table 3 APGST Labour Market Metrics for the Air Sector in the APGC

Metric 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Hiring Difficulty Index

some challenges

difficult some challenges

Market Tightness

3

Mobility fewer jobs

low leaving

moving in

Supply Lag low medium high medium low

International Reliance

high medium low medium

Loss of Experience

high medium high

In the first 5 years of the forecast, the High Investment Scenario will generate 9,915 (40%) more Job Openings than the Low. In the second half, the Low Investment Scenario will generate 4,775 more Job Openings, for a net effect that has the High Investment Scenario generating 5,140 (9%) more Job Openings than the Low.

13 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Chapter 2 Highlights — Logistics Sector

LOGISTICSSECTOR

By the Numbers

Job Openings to be filled 59,917 34% of APGC total

Replacement Job Openings 45,440 76% of Job Openings

Job Openings created by Expansion

14,482 18% of Job Openings in first 5 years

Workers who will retire and leave the labour force

45,440 26% of today’s workers

New workers – New Entrants to the industry

29,200 50% of the New Supply

New workers – from other countries

5,958 10% of the New Supply

New workers – from other provinces

7,029 12% of the New Supply

New workers – from other parts of the labour force

16,768 28% of the New Supply

Average time left in industry 18 – 28 years until retirement (between the ages of 60–70)

When used with reference to business, the term logistics often occurs in conjunction with the terms supply chain or supply chain management. Supply chain and logistics refers to the science of ensuring that the move - ments to and from each segment of the chain are carried out as efficiently and economically as possible. In the APGC, logistics deals with the movement of goods from source to destination using air, marine, rail, and trucking resources.

The APGC LMI Project Logistics Sector includes 12 occupations. For details on individual occupations, please refer to the Occupational Snapshots.

Logisticsreferstotheformalprocessesbywhichbusinessesensurethatsuppliesareprocuredfromtherightsources,transportedtowheretheyareneeded,andarriveattherighttime.

14 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Chapter 2 Highlights — Logistics Sector

The forecast for 2016–2025 shows 2016 and 2017 as the least challenging years that employers will face. Throughout most of the forecast, employers will have some challenges hiring the workers they need in the twelve occupations. This trend is similar across the four provinces, with Manitoba showing difficult conditions more often than the others.

Job Openings are more likely to be created by Replacement (76%) than Expansion; however, in the first 5 years, close to 1 in 3 Job Openings are generated by Expansion. Just under 1 in 4 workers will retire and leave the sector, about the same as in the APGC as a whole. Close to 1 in 3 Supervisors, Supply Chain, Tracking and Scheduling Co-ordination Occupations and Managers in Transportation will have retired and left the labour force by 2025.

Half of all new workers in the industry will be New Entrants and 4 in 5 for Customs, Ship and Other Brokers, and Production Logistics Co-ordinators and Shippers and Receivers; employers will need to invest in more on-the-job training to enable newly trained workers to contribute to overall productivity. All of the occupations gain some of their New Supply from other provinces, with Purchasing Agents and Officers gaining almost half of their New Supply from other provinces. More than 1 in 4 new workers in the APGC are from other parts of the labour force, with half of the New Supply in Saskatchewan coming from this source along with 9 in 10 Managers in Transportation, Supervisors, Supply Chain, Tracking and Scheduling Co-ordination Occupations and Retail and Wholesale Buyers. About 1 in 10 new workers come from other countries; however, in Saskatchewan, the 12 occupations in the Logistics Sector lose the equivalent of 15% of the New Supply to workers leaving Canada. Across the APGC, 1 in 3 Inspectors in Public and Environmental Health and Occupational Health and Safety will come from other countries.

38% of the workers in the APGC Logistics Sector live in BC, 44% in Alberta, 8% in Saskatchewan and 10% in Manitoba.

Table 4 Logistics Sector Occupations and Job Openings

NOC Occupation Title Job Openings

0113 Purchasing Managers 5,563

0731 Managers in Transportation 15,518

1215 Supervisors, Supply Chain, Tracking and Scheduling Co-ordination Occupations

15,487

1225 Purchasing Agents and Officers 19,174

1315 Customs, Ship and Other Brokers 1,041

1521 Shippers and Receivers 31,850

1523 Production Logistics Co-ordinators 5,580

1524 Purchasing and Inventory Control Workers

8,845

2262 Engineering Inspectors and Regulatory Officers

1,896

2263 Inspectors in Public and Environ - mental Health and Occupational Health and Safety

13,415

6222 Retail and Wholesale Buyers 8,974

7452 Material Handlers 52,099

15 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

APGST Labour Market Metrics for the Logistics Sector In the first 5 years of the forecast, the High Investment Scenario will generate 12,305 more Job Openings than the Low. In the second half of the forecast, the Low Investment Scenario will generate 2,135 more Job Openings than the High, for a net effect that has the High Investment Scenario generating 10,170 more Job Openings (19%) than the Low.

Table 5 APGST Labour Market Metrics for the Logistics Sector in the APGC

Metric 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Hiring Difficulty Index

easy market some challenges

Market Tightness

3

Mobility moving in

Supply Lag low medium high medium low

International Reliance

none medium

Loss of Experience

high medium high

Chapter 2 Highlights — Logistics Sector

16 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Highlights — Rail SectorChapter 2

RAILSECTOR

By the Numbers

Job Openings to be filled 67,296 38% of APGC total

Replacement Job Openings 53,097 79% of Job Openings

Job Openings created by Expansion

14,199 18% of Job Openings in first 5 years

Workers who will retire and leave the labour force

53,095 30% of today’s workers

New workers – New Entrants to the industry

27,585 41% of the New Supply

New workers – from other countries

11,355 17% of the New Supply

New workers – from other provinces

5,475 8% of the New Supply

New workers – from other parts of the labour force

22,213 33% of the New Supply

Average time left in the industry 16 –26 years until retirement (between the ages of 60–70)

TheRailSectormanagestheoperationsofrailwaysandrailwayyardstomovelargequantitiesofbulkandotherformsofcargoacrossthecountry.

A freight train is a group of freight cars hauled by one or more locomotives on a railway, ultimately transporting cargo between two points as part of the logistics chain. Trains can be as long as four kilometres or more, operated by a crew of two. Trains may haul bulk material, intermodal containers, general freight, or specialized freight in purpose-designed cars. When considered in terms of tonne-kilometres hauled per unit of consumed energy, rail transport is more efficient than other means of transportation. Additional economies are often realized with bulk commodities (e.g., coal), especially when hauled over long distances. With bulk shipments, distances as short as 30 kilometres are sufficient to make rail transport economically viable.

The APGC LMI Project Rail Sector incudes 19 occupations. For details on individual occupations, please refer to the Occupational Snapshots.

The forecast for 2016–2025 shows 2016 as the least challenging year that employers will face. For most of the forecast period, employers will have some challenges in hiring the workers they need in the 19 occupations. This trend is similar across the four provinces, with Saskatchewan and Manitoba showing difficult conditions more often than the others.

Job Openings are more likely to be created by Replacement (79%) than Expansion; however, in the first 5 years, close to 1 in 4 Job Openings are generated by Expansion. Just under 1 in 4 workers will retire and leave the sector, about the same as in the APGC as a whole. Close to 2 in 5 Railway and Yard Locomotive Engineers and Railway Carmen/women will have retired and left the labour force by 2025.

17 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Highlights — Rail SectorChapter 2

Table 6 Rail Sector Occupations and Job Openings

NOC Occupation Title Job Openings

0016 Senior Managers – Construction, Transportation, Production and Utilities

24,060

0714 Facility Operation and Maintenance Managers

27,380

0731 Managers in Transportation 15,518

1525 Dispatchers 10,291

1526 Transportation Route and Crew Schedulers

1,485

2131 Civil Engineers 24,220

2231 Civil Engineering Technologists and Technicians

8,033

2241 Electrical and Electronics Engineering Technologists and Technicians

11,655

2243 Industrial Instrument Technicians and Mechanics

2,951

2261 Non-Destructive Testers and Inspection Technicians

3,128

2262 Engineering Inspectors and Regulatory Officers

1,896

2263 Inspectors in Public and Environmental Health and Occupational Health and Safety

13,415

7242 Industrial Electricians 9,004

7304 Supervisors, Railway Transport Operations

1,569

7311 Construction Millwrights and Industrial Mechanics

20,993

7314 Railway Carmen/women 2,743

7361 Railway and Yard Locomotive Engineers

5,462

7362 Railway Conductors and Brakemen/women

6,994

7531 Railway Track Maintenance Workers

4,838

Just over 40% of all new workers in the industry will be New Entrants. Virtually all Industrial Instrument Technicians and Mechanics are New Entrants, which means employers will need to invest in on-the-job training to enable newly trained workers to contribute to overall productivity. All of the occupations gain some of their New Supply from other provinces; Railway Conductors and Brakemen/women gain almost a third of their New Supply from other provinces. 1 in 3 new workers in the APGC are from other parts of the labour force, with close to two thirds of New Supply in Saskatchewan coming from this source along with 9 in 10 Managers in Transportation, Facility Operation and Maintenance Managers and Super visors, Railway Transport Operations. Just over 15% of new workers come from other countries; in BC, it is closer to 25%. Across the APGC, close to 1 in 3 Railway Track Maintenance Workers, Non-Destructive Testers and Inspection T echnicians and Civil Engineers will come from other countries.

35% of the workers in the APGC Rail Sector live in BC, 47% in Alberta, 9% in Saskatchewan, and 9% in Manitoba.

18 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Chapter 2 Highlights — Rail Sector

Table 7 APGST Labour Market Metrics for the Rail Sector in the APGC

Metric 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Hiring Difficulty Index

easy market

some challenges

Market Tightness

3

Mobility moving in

Supply Lag low medium high medium low

International Reliance

none medium

Loss of Experience

high medium high

APGST Labour Market Metrics for the Rail Sector In the first 5 years of the forecast, the High Investment Scenario will generate 10,510 more Job Openings (36%) than the Low. In the second half of the forecast, the Low Investment Scenario generates 4,415 more Job Openings than the High, for a net effect that has the High Investment Scenario generating 6,095 more Job Openings (10%) than the Low.

19 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Chapter 2 Highlights — Trucking Sector

TRUCKINGSECTOR

By the Numbers

Job Openings to be filled 84,870 48% of APGC total

Replacement Job Openings 68,568 81% of Job Openings

Job Openings created by Expansion

16,309 8% of Job Openings in first 5 years

Workers who will retire and leave the labour force

68,570 28% of today’s workers

New workers – New Entrants to the industry

52,904 62% of the New Supply

New workers – from other countries

12,388 15% of the New Supply

New workers – from other provinces

6,824 8% of the New Supply

New workers – from other parts of the labour force

12,784 15% of the New Supply

Average time left in the industry 17 – 27 years until retirement (between the ages of 60-70)

Table 8 Trucking Sector Occupations and Job Openings

NOC Occupation Title Job Openings

0016 Senior Managers – Construction, Transportation, Production and Utilities

24,060

0731 Managers in Transportation 15,518

1525 Dispatchers 10,291

1526 Transportation Route and Crew Schedulers

1,485

2241 Electrical and Electronics Engineering Technologists and Technicians

11,655

2243 Industrial Instrument Technicians and Mechanics

2,951

2262 Engineering Inspectors and Regulatory Officers

1,896

2263 Inspectors in Public and Environmental Health and Occupational Health and Safety

13,415

7242 Industrial Electricians 9,004

7305 Supervisors, Motor Transport and Other Ground Transit Operators

4,914

7321 Automotive Service Technicians, Truck and Bus Mechanics and Mechanical Repairers

41,598

7511 Transport Truck Drivers 111,712

Truckingfirmsprovideanessentialservicebytransportingfinishedgoodsandrawmaterialsoverland,typicallytoandfrommanufacturingplants,retailfacilities,anddistributioncentres.Itisestimatedthattruckingofgoodsiscost-competitivetorailfordistancesupto800kilometres.

The APGC LMI Project Trucking Sector incudes 12 occupations. For details on individual occupations, please refer to the Occupational Snapshots.

20 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Chapter 2 Highlights — Trucking Sector

The forecast for 2016–2025 shows 2016 as the least challenging year that employers will face. For most of the forecast period, employers will have some challenges in hiring the workers they need in all 12 occupations. This trend is similar across the four provinces, with Saskatchewan showing more ease in the later years and Manitoba showing difficult conditions more often than the others.

Job Openings are more likely to be created by Replacement (81%) than Expansion; however, in the first 5 years, close to 1 in 5 Job Openings are generated by Expansion. Just over 1 in 4 workers will retire and leave the sector, a little higher than in the APGC as a whole. Close to 1 in 3 Managers in Transportation and Supervisors, Motor Transport and Other Ground Transit Operators will have retired and left the labour force by 2025.

Almost 2 in 3 new workers in the industry will be New Entrants, virtually all Industrial Instrument Technicians and Mechanics are New Entrants, which means employers will need to invest in more on-the-job training to enable newly trained workers to contribute to overall productivity. For the APGC as a whole, just under 1 in 10 new workers will come from other provinces; all of the occupations gain some of their New Supply from other provinces. About 15% of new workers in the APGC are from other parts of the labour force, with 9 in 10 Managers in Transportation and Supervisors, Motor Transport and Other Ground Transit Operators. Another 15% of new workers come from other countries, higher in Saskatchewan and Manitoba at close to 1 in 5. Across the APGC, 1 in 3 Automotive Service Technicians, Truck and Bus Mechanics and Mechanical Repairers, Electrical and Electronics Engineering Technologists and Technicians and Inspectors in Public and Environmental Health and Occupational Health and Safety will come from other countries.

35% of the workers in the APGC Trucking Sector live in BC, 44% in Alberta, 10% in Saskatchewan and 11% in Manitoba.

21 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

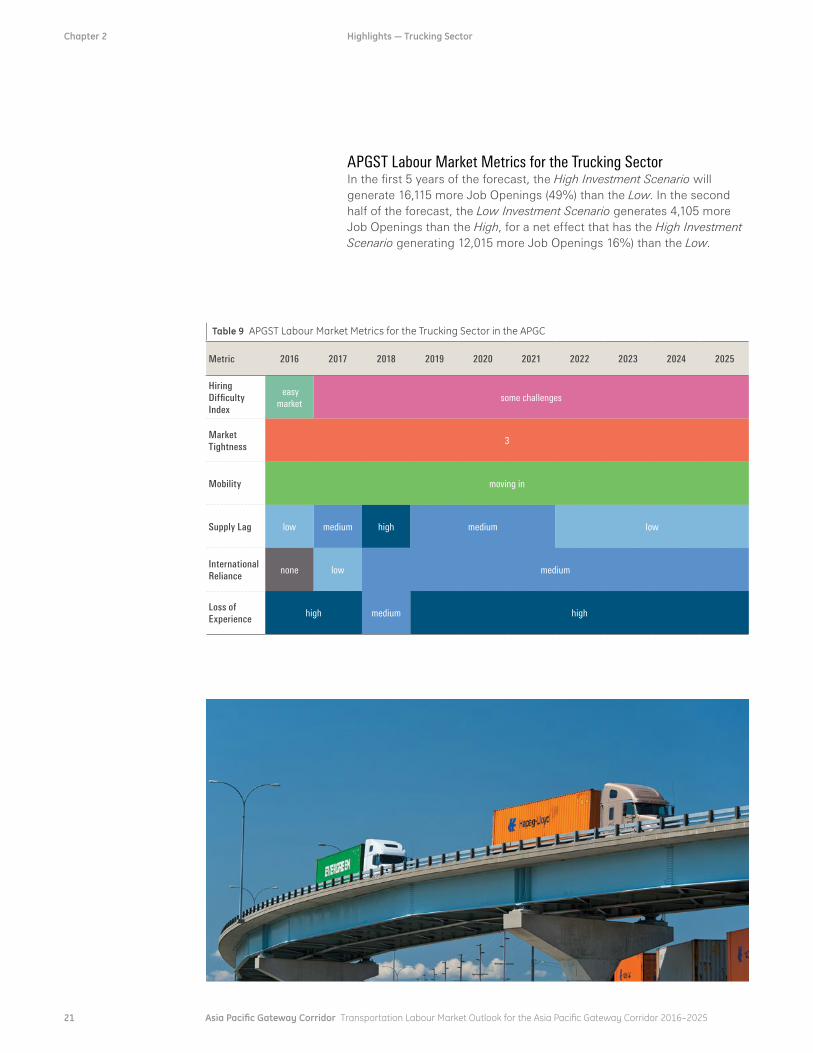

Chapter 2 Highlights — Trucking Sector

Table 9 APGST Labour Market Metrics for the Trucking Sector in the APGC

Metric 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Hiring Difficulty Index

easy market

some challenges

Market Tightness

3

Mobility moving in

Supply Lag low medium high medium low

International Reliance

none low medium

Loss of Experience

high medium high

APGST Labour Market Metrics for the Trucking Sector In the first 5 years of the forecast, the High Investment Scenario will generate 16,115 more Job Openings (49%) than the Low. In the second half of the forecast, the Low Investment Scenario generates 4,105 more Job Openings than the High, for a net effect that has the High Investment Scenario generating 12,015 more Job Openings 16%) than the Low.

22 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

The APGC is forecast to grow in the 10 years of the forecast as trade activity between North America and Asia expands. This growth will increase the need for an available, well-trained workforce. The forecast shows that employers will face some challenges in hiring the workers they need in the 34 occupations starting in 2017 and throughout the balance of the forecast period. This trend is similar across the four sectors. See the Sector Outlook reports for more information.

Chapter 3 Key Facts 2016–2025

KEYFACTS2016–2025

ThisforecastprovidesimportantinformationaboutsupplyanddemandfortheAPGC,withafocusonfoursectorsinthefourprovincesthatmakeuptheAPGC.

Table 10 Hiring Difficulty Index for All Sectors in the APGC

Sector 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Airsome

challengesdifficult

some challenges

Logistics easy

marketsome

challenges

Rail easy

marketsome

challenges

Trucking easy

marketsome

challenges

APGC Total easy

marketsome

challenges

HIRINGDIFFICULTYINDEXThe Hiring Difficulty Index assesses the overall challenges for employers trying to hire in the labour market. It uses five metrics, combining them to provide a single measure that reflects the impacts and interactions between the labour market components. For a complete description of each metric, see Appendix A.

23 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

LABOURDEMAND

Chapter 3 Key Facts 2016–2025

Approximately 177,375 Job Openings, from both growth and retirements combined, are expected to be created across the APGC sectors between 2016 and 2025 (see Table 11).

By sector, Job Openings number approximately:JJ 61,020 in AirJJ 59,915 in LogisticsJJ 67,296 in RailJJ 84,870 in Trucking

The number of positions increases by 7.5%, with a total of 40,035 new positions over the forecast period.

By sector, new positions number approximately:JJ 13,250 (7.6%) in AirJJ 13,675 (7.5%) in LogisticsJJ 14,410 (8.1%) in RailJJ 19,330 (7.4%) in Trucking

Labour Demand is created by the business environment, economic circumstances, and decisions affecting employers’ operations. It reflects the number of jobs available to be filled in an occupation.

Figure 2 Job Openings by Sector, Moderate Scenario

25,000

20,000

15,000

10,000

5,000

02016 2017 2018 2019 2020 2021 2022 2023 2024 2025

APGC Total Air Logistics Rail Trucking

Table 11 Demand and Job Openings in the APGC

Sector Average Annual Number

of Jobs

Total Job Openings,

2016–2025

Jobs Created by Expansion,

2016–2020

Jobs Created by Expansion,

2021–2025

Expansion as a % of

Job Openings

Air 181,515 61,020 6,505 5,455 20%

Logistics 190,145 59,915 8,970 5,510 24%

Rail 186,890 67,295 8,335 5,850 21%

Trucking 270,475 84,870 6,930 9,375 19%

APGC Total 557,160 177,375 20,900 17,420 22%

Growth of Positions in the APGC

7.5%

24 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Expansion Demand is defined as the number of Job Openings in an occupation created by economic or business growth.

Expansion In the APGC, Expansion accounts for approximately 22% of Job Openings over the entire forecast period, with Replacement accounting for the remainder. While 2016 shows declines in all sectors except for Logistics, in the first 5 years, 24% of Job Openings are created by Expansion due to the number of large-scale projects forecast for that period. By sector, Expansion Demand varies greatly, with the lowest impact being in Air and Rail (Figure 3).

Chapter 3 Key Facts 2016–2025

Figure 3 Expansion Demand by Sector

3,000

2,000

1,000

0

-1,000

-2,000

-3,000

-4,000

2016 2025

Jobs

Air Rail Trucking APGC TotalLogistics

Table 12 Expansion Demand by Sector

Sector Expansion Rate, 2016–2020 Expansion Rate, 2016–2025

Air 21% 20%

Logistics 29% 24%

Rail 24% 21%

Trucking 17% 19%

APGC Total 23% 22%

Expansion Demand is higher between 2016 and 2020 in every sector except for Trucking, which shows a slightly higher impact in the second half of the forecast, with the highest averages in Logistics and Rail (Table 12). For more information about Job Openings by occupation, see the Occupational Snapshots at lmionline.ca.

25 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Labour Supply is created by the number of workers who have the skills and/or certifications to be qualified to work in each occupation in each year, including those who are newly trained, have moved from other provinces or countries, or have moved from other occupations.

Chapter 3 Key Facts 2016–2025

LABOURSUPPLYLabour Supply in the APGC is expected to grow by about 36,110 workers over the 10 years of the forecast. With the growth in New Supply not keeping pace with Job Openings, the forecast shows a consistent gap between the growth in supply and the growth in Job Openings in all provinces except Manitoba.

By sector, labour supply is expected to increase by approximately:JJ 11,770 in AirJJ 12,415 in LogisticsJJ 13,065 in RailJJ 17,195 in Trucking

The Supply Lag Measure assesses the extent to which New Supply is keeping pace with Job Openings. It allows for an assessment of the extent to which conditions are tightening or loosening in the labour market (Table 13).

Table 13 Supply Lag Measure for All Sectors in the APGC

Sector 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Air low medium high medium low

Logistics low medium high medium low

Rail low medium high medium low

Trucking low medium high medium low

APGC Total low medium high medium low

Growth in the labour supply

Average age of workers in the APGC

6.3%43YEARS

Count Too Small Job Openings or New Supply

is less than 6

No New Supply New Supply is 0 or negative

Medium New Supply is 93–97%

of Job Openings

High New Supply is 93% or

less of Job Openings

Low New Supply is 97% or more

of Job Openings

26 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Replacement Demand is defined as the number of Job Openings created by workers who leave each occupation, and the labour market as a whole, due to retirement or death each year.

ReplacementReplacement continues to be the primary driver of Job Openings, although its impact has declined from previous forecasts as more workers remain in the workforce after the age of 65, and the impact of the baby boom generation moving out of the workforce lessens. In the APGC, Replacement will generate 139,055 Job Openings over 10 years (Table 14).

Close to 13,905 experienced workers will leave the workforce across the APGC each year.

By sector, this means an annual loss of approximately:JJ 4,905 in AirJJ 4,545 in LogisticsJJ 5,310 in RailJJ 6,855 in Trucking

Chapter 3 Key Facts 2016–2025

Table 14 Impact of Replacement on Job Openings

Sector Replacement Job Openings, 2016–2020

Replacement Job Openings, 2021–2025

Replacement Job Openings %

Air 23,810 25,250 80%

Logistics 21,795 23,645 76%

Rail 26,030 27,065 79%

Trucking 33,835 34,730 81%

APGC Total 68,050 71,005 78%

Table 15 Loss of Experience Measure for All Sectors in the APGC

Sector 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Air high medium high

Logistics high medium high

Rail high medium high

Trucking high medium high

APGC Total high medium high

Loss of Experience assesses the rate at which experienced workers are retiring in relation to the number of Job Openings. The rate of loss is High for most of the forecast in all four sectors (Table 15).

Low 35% of Job Openings

represented by Replacement

Medium 35–70% of Job Openings

represented by Replacement

High More than 70% of Job

Openings represented

by Replacement

27 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Base Supply is calculated as the total supply less the average number of unemployed workers, less Replacement from each year of the forecast. Base Supply calculations demonstrate the changes in each year of the forecast period to the cohort of workers as compared with the first year of the forecast.

Chapter 3 Key Facts 2016–2025

Base Supply In the APGC, Base Supply is expected to decline by 24% over the fore - cast period. There is some variance between sectors (Table 16), but with this decline, employers in all sectors will need to explore alternative recruiting methods to replace their most experienced workers.

Table 16 Changes to Base Labour Supply for the APGC, All Sectors, 2016–2025

Sector Base Supply 2016

Decline 2016–2020

% Decline 2016–2025

%

Air 180,535 -23,810 -13% -49,060 -27%

Logistics 189,375 -21,795 -12% -45,440 -24%

Rail 185,430 -26,030 -14% -53,095 -29%

Trucking 271,960 -33,835 -12% -68,565 -25%

APGC Total 557,510 -68,050 -12% -139,055 -25%

Base Supply is a measure of the decline in the number of workers who are active in an occupation at the beginning of the forecast and sub- sequently leave due to Replacement over the forecast period.

28 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

New Supply is defined as the number of workers who are new to the occupations from Immigration, other provinces or regions, or other occupations, or who are New Entrants—newly trained and new to the workforce.

New Supply The forecast shows New Supply largely keeping pace with Job Openings for the entire forecast period. 3 of the 4 sectors will have greater challenges finding workers in the first 5 years, especially the Air and Logistics sectors. In the Trucking Sector, the growth in supply keeps pace with Job Openings throughout the forecast period.

The composition of New Supply will shift over the forecast, with increasing reliance on Immigration and New Entrants (see Figure 4).

Chapter 3 Key Facts 2016–2025

Table 17 Labour Supply Characteristics

Sector Average Number of Qualified Workers

New Entrants

International Mobility

Mobility Labour Force Mobility

Air 191,225 18,650 9,990 2,800 29,110

Logistics 201,310 16,770 5,960 7,030 29,200

Rail 197,330 22,215 11,355 5,475 27,585

Trucking 289,160 12,785 12,390 6,825 52,905

APGC Total 593,325 36,100 23,880 17,400 98,840

Figure 4 Components of New Supply, APGC Total, 2016–2025

Labour Force Mobility20%

Mobility10%

International Mobility 14%

New Entrants56%

29 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Chapter 3 Key Facts 2016–2025

New Entrants For the New Supply of workers across all sectors in the APGC, 56% are New Entrants—newly trained and new to the workforce. With many workers being new to the workforce, employers in some sectors will benefit from good training programs to help integrate these New Entrants.

By sector, New Entrants make up:JJ 48% in AirJJ 50% in LogisticsJJ 41% in RailJJ 62% in Trucking

The number of New Entrants takes into consideration previous participation in the labour force: If a new graduate has never worked before, they would be counted as 1.0 New Entrant, and if a new graduate worked 25% of the year prior to graduating, they would be counted as 0.75 of a New Entrant. The number of New Entrants may not match administrative data for graduates, as graduates do not always end up in the labour force.

New Entrants refer to the number of graduates from school or training programs who are filling Job Openings.

30 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Immigration refers to workers coming to Canada from other countries. It includes foreign workers as well as immigrants to Canada.

ImmigrationImmigration is expected to add 14% to the total New Supply of APGC workers.

With some workers expected to come from other countries in all of the sectors, employers may need to explore different methods of recruitment when adding to their workforce.

By sector, the amount of workers coming from other countries is:JJ 16% in AirJJ 10% in LogisticsJJ 17% in RailJJ 15% in Trucking

The International Reliance Measure assesses the extent to which the New Supply of workers is dependent on Immigration. Employers do not have control over Immigration, so this measure provides insight into how New Supply expectations could be affected by changes to Immigration policy (Table 18).

Chapter 3 Key Facts 2016–2025

Table 18 International Reliance Measure for All Sectors in the APGC

Sector 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Air high medium low medium

Logistics none medium

Rail none medium

Trucking none low medium

APGC Total none medium

No New Supply New Supply is 0 or negative

None International workers are not

part of New Supply

Extreme 50% or more of New Supply

represented by Immigration

Low Less than 10% of New Supply

represented by Immigration

Medium 10% to 25% of New Supply

represented by Immigration

High 25% to 50% of New Supply

represented by Immigration

31 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

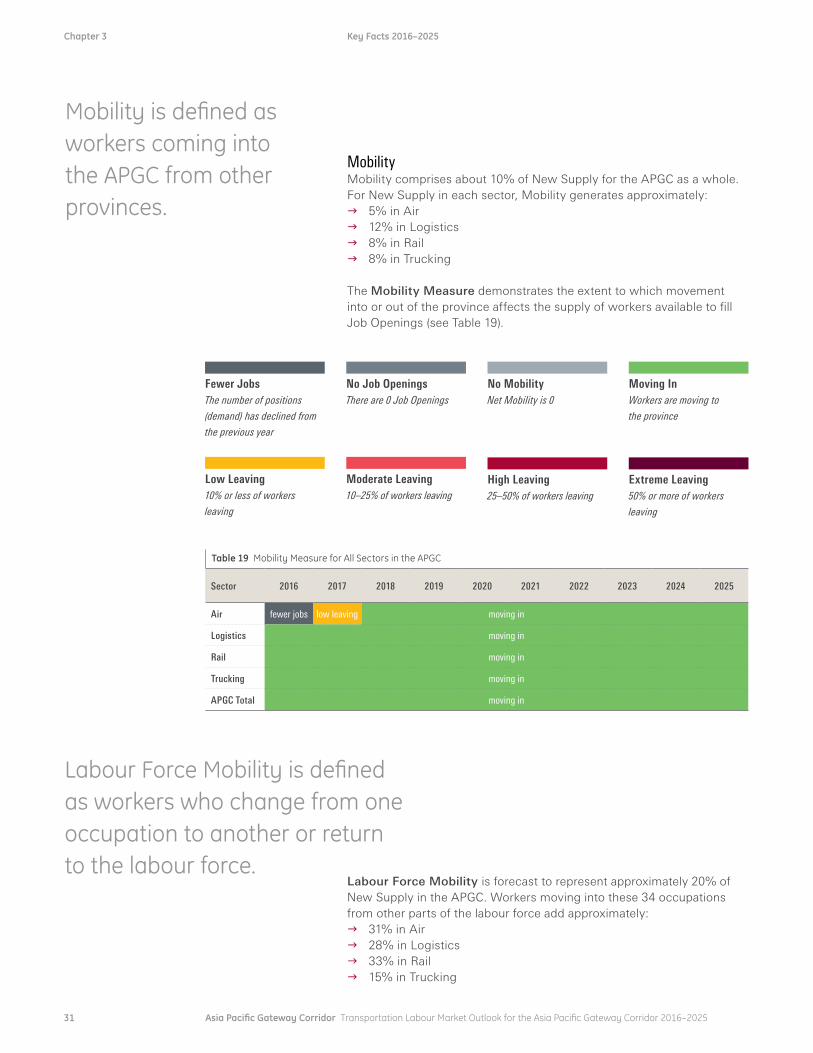

Chapter 3 Key Facts 2016–2025

MobilityMobility comprises about 10% of New Supply for the APGC as a whole. For New Supply in each sector, Mobility generates approximately:JJ 5% in AirJJ 12% in LogisticsJJ 8% in RailJJ 8% in Trucking

The Mobility Measure demonstrates the extent to which movement into or out of the province affects the supply of workers available to fill Job Openings (see Table 19).

Mobility is defined as workers coming into the APGC from other provinces.

Labour Force Mobility is defined as workers who change from one occupation to another or return to the labour force.

Table 19 Mobility Measure for All Sectors in the APGC

Sector 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Air fewer jobs low leaving moving in

Logistics moving in

Rail moving in

Trucking moving in

APGC Total moving in

Labour Force Mobility is forecast to represent approximately 20% of New Supply in the APGC. Workers moving into these 34 occupations from other parts of the labour force add approximately:JJ 31% in AirJJ 28% in LogisticsJJ 33% in RailJJ 15% in Trucking

Fewer Jobs The number of positions

(demand) has declined from

the previous year

No Job Openings There are 0 Job Openings

No Mobility Net Mobility is 0

Moving In Workers are moving to

the province

Low Leaving 10% or less of workers

leaving

Moderate Leaving 10–25% of workers leaving

Extreme Leaving 50% or more of workers

leaving

High Leaving 25–50% of workers leaving

32 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

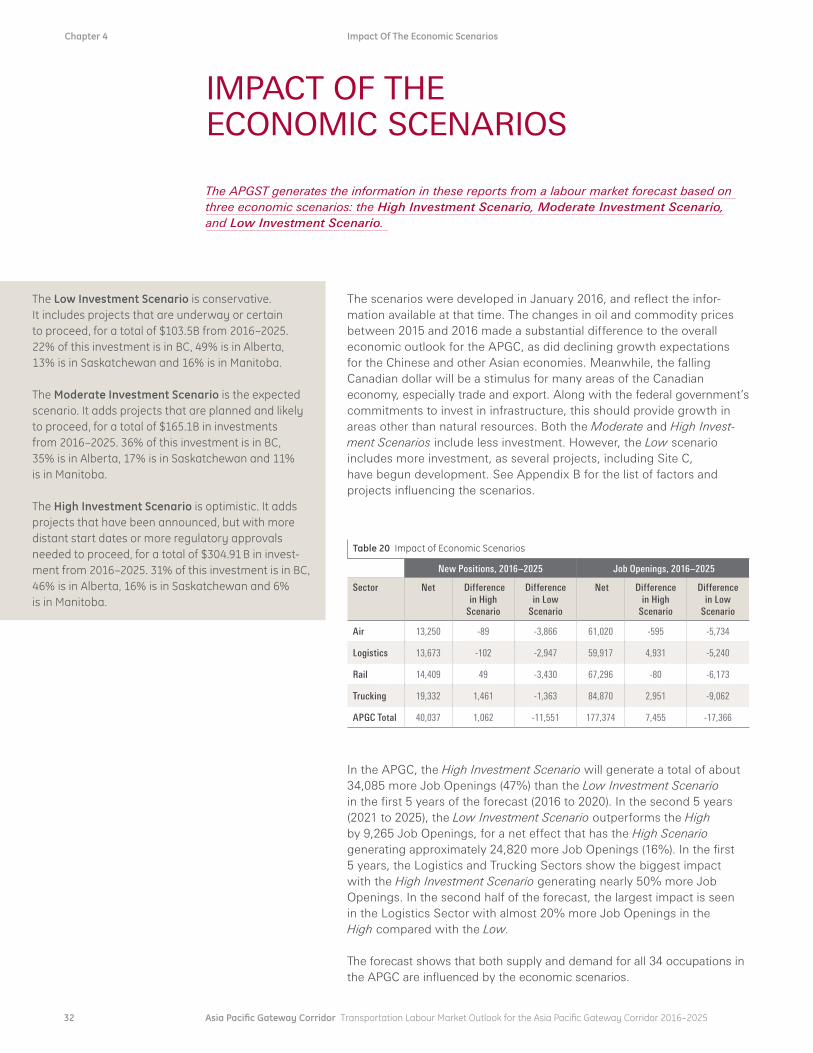

The scenarios were developed in January 2016, and reflect the infor-mation available at that time. The changes in oil and commodity prices between 2015 and 2016 made a substantial difference to the overall economic outlook for the APGC, as did declining growth expectations for the Chinese and other Asian economies. Meanwhile, the falling Canadian dollar will be a stimulus for many areas of the Canadian economy, especially trade and export. Along with the federal government’s commitments to invest in infrastructure, this should provide growth in areas other than natural resources. Both the Moderate and High Invest-ment Scenarios include less investment. However, the Low scenario includes more investment, as several projects, including Site C, have begun development. See Appendix B for the list of factors and projects influencing the scenarios.

Chapter 4 Impact Of The Economic Scenarios

IMPACTOFTHEECONOMICSCENARIOS

The Low Investment Scenario is conservative. It includes projects that are underway or certain to proceed, for a total of $103.5B from 2016–2025. 22% of this investment is in BC, 49% is in Alberta, 13% is in Saskatchewan and 16% is in Manitoba.

The Moderate Investment Scenario is the expected scenario. It adds projects that are planned and likely to proceed, for a total of $165.1B in investments from 2016–2025. 36% of this investment is in BC, 35% is in Alberta, 17% is in Saskatchewan and 11% is in Manitoba.

The High Investment Scenario is optimistic. It adds projects that have been announced, but with more distant start dates or more regulatory approvals needed to proceed, for a total of $304.91 B in invest-ment from 2016–2025. 31% of this investment is in BC, 46% is in Alberta, 16% is in Saskatchewan and 6% is in Manitoba.

TheAPGSTgeneratestheinformationinthesereportsfromalabourmarketforecastbasedonthreeeconomicscenarios:theHigh Investment Scenario,Moderate Investment Scenario,andLow Investment Scenario.

Table 20 Impact of Economic Scenarios

New Positions, 2016–2025 Job Openings, 2016–2025

Sector Net Difference in High

Scenario

Difference in Low

Scenario

Net Difference in High

Scenario

Difference in Low

Scenario

Air 13,250 -89 -3,866 61,020 -595 -5,734

Logistics 13,673 -102 -2,947 59,917 4,931 -5,240

Rail 14,409 49 -3,430 67,296 -80 -6,173

Trucking 19,332 1,461 -1,363 84,870 2,951 -9,062

APGC Total 40,037 1,062 -11,551 177,374 7,455 -17,366

In the APGC, the High Investment Scenario will generate a total of about 34,085 more Job Openings (47%) than the Low Investment Scenario in the first 5 years of the forecast (2016 to 2020). In the second 5 years (2021 to 2025), the Low Investment Scenario outperforms the High by 9,265 Job Openings, for a net effect that has the High Scenario generating approximately 24,820 more Job Openings (16%). In the first 5 years, the Logistics and Trucking Sectors show the biggest impact with the High Investment Scenario generating nearly 50% more Job Openings. In the second half of the forecast, the largest impact is seen in the Logistics Sector with almost 20% more Job Openings in the High compared with the Low.

The forecast shows that both supply and demand for all 34 occupations in the APGC are influenced by the economic scenarios.

33 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Figure 6 Labour Force Supply for BC, All Occupations

630,000

620,000

610,000

600,000

590,000

580,000

570,000

560,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Labo

ur S

uppl

y

High Moderate Low

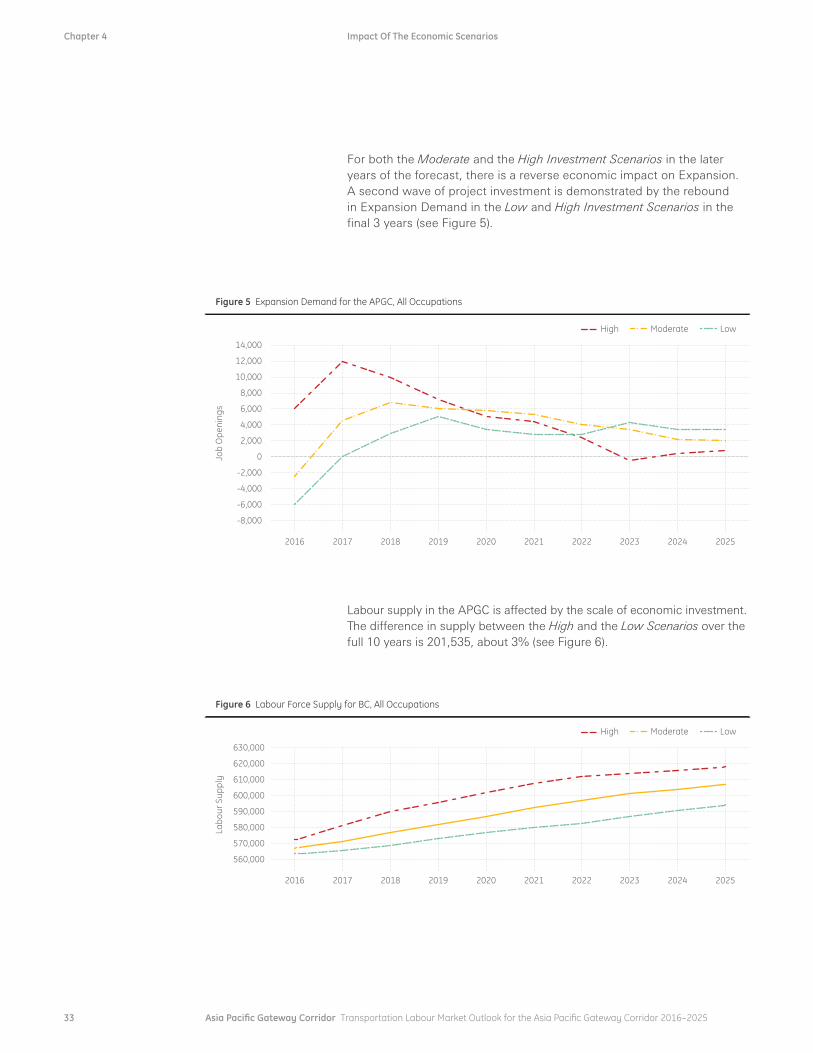

For both the Moderate and the High Investment Scenarios in the later years of the forecast, there is a reverse economic impact on Expansion. A second wave of project investment is demonstrated by the rebound in Expansion Demand in the Low and High Investment Scenarios in the final 3 years (see Figure 5).

Chapter 4 Impact Of The Economic Scenarios

Figure 5 Expansion Demand for the APGC, All Occupations

14,000

12,000

10,000

8,000

6,000

4,000

2,000

0

-2,000

-4,000

-6,000

-8,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Job

Ope

ning

s

High Moderate Low

Labour supply in the APGC is affected by the scale of economic investment. The difference in supply between the High and the Low Scenarios over the full 10 years is 201,535, about 3% (see Figure 6).

34 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

THEAPGCEmployers will face some challenges from 2017 onward, mostly driven by high rates of retirement (Replacement) over the whole forecast period, and in the middle years with supply growth not keeping pace with Job Openings. The loss of workers to other provinces in both Saskatchewan and Manitoba also contributes to the challenges that employers will face in hiring workers in the 34 occupations in the APGC between 2016 and 2025.

New Supply, which keeps pace with Job Openings, except in the middle years of the forecast, is driven mostly by New Entrants and by workers moving into these 34 occupations from other occupations or other parts of the labour force. Over the forecast period, reliance on New Entrants increases as does reliance on international workers, while workers from other provinces and other occupations become a smaller part of the New Supply.

The Moderate Investment Scenario shows growth in the APGC over the first five years, with slow but steady declines in the second half of the forecast. This could be moderated or reversed if there is more investment made in large-scale projects in the APGC in the second half of the forecast. In contrast, the Low Investment Scenario shows slower but steady growth throughout the 10 years of the forecast, while the High Investment Scenario shows sharp growth in the first half and contracts somewhat in the last years of the forecast.

Employers can reduce impacts of the forecasted labour market conditions by building programs and strategies to ensure the attraction of an adequate labour supply and retention of the mature workforce to slow the rate of retirement.

Chapter 5 Conclusions

CONCLUSIONS

35 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Chapter 5 Conclusions

AIRThe 15 occupations in the APGC Air Sector have slightly more difficult conditions than the APGC as a whole, with a loss of workers to other occupations in the first two years and greater reliance on international workers to meet the need for new workers. These occupations rely more on workers from provinces and they also show the smallest impact of the three scenarios, with less than a 10% difference in Job Openings between the High and Low Investment Scenarios.

LOGISTICSThe 12 occupations in the APGC Logistics Sector have slightly less difficult conditions than the APGC as a whole, with a lower rate of retirement and less reliance on international workers to meet the need for new workers. These occupations rely less on New Entrants and more on workers from other occupations and they also show the largest impact of the three scenarios, with a 19% difference in Job Openings between the High and Low Investment Scenarios.

RAILThe 19 occupations in the APGC Rail Sector have about the same conditions as the APGC as a whole. These occupations have a higher rate of retirement and reliance on international workers to meet the need for new workers. These occupations rely much less on New Entrants and more on workers from other occupations and they also show a lower impact of the three scenarios than the APGC as a whole with a 10% difference in Job Openings between the High and Low Investment Scenarios.

TRUCKINGThe 12 occupations in the APGC Trucking Sector have about the same conditions as the APGC as a whole. These occupations have a higher rate of retirement and lower reliance on international workers to meet the need for new workers. They rely much more on New Entrants and much less on workers from other occupations. The 12 Trucking Sector occupations show about the same impact of the three scenarios as the APGC as a whole with a 16% difference in Job Openings between the High and Low Investment Scenarios. This sector has the largest impact in the first five years with 49% more Job Openings in the High Investment Scenario.

APPENDIX

AppendixA DescriptionofMetricsandGlossaryofTerms 38

AppendixB EconomicIndicatorsandMajorProjectsincluded intheEconomicScenarios 43

AppendixC DataTablesbySectorandEconomicScenario: TheAsiaPacificGatewayCorridor 52

AppendixD TheAsiaPacificGatewayCorridorOccupations 67

38 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Appendix A Description of Metrics and Glossary of Terms

APPENDIXA DESCRIPTIONOFMETRICSANDGLOSSARYOFTERMS

Assesses the overall challenges for employers who are trying to hire in the labour market. It aggregates five metrics and combines them to provide a single measure that reflects the different interactions between the labour market components. For example, the metrics can show the ratio of workers to Job Openings (the Market Tightness) as “Tight”, with International Reliance and Supply Lag Low and Mobility positive (i.e., workers are moving in), while the Loss of Experience is Moderate and the reliance on New Entrants is Extreme. This implies quite different labour market conditions than a situation where the Market Tightness is “Tightening” (i.e., less difficult) but International Reliance is High, supply is growing much more slowly than Job Openings, and a high portion of current workers are leaving to work in other provinces.

Oversupplied Market 0–8

No New Supply New Supply is 0 or negative

Easy Market 9–15

None International workers are not part of New Supply

Low Less than 10% of New Supply represented by Immigration

Difficult 23–29

Medium 10% to 25% of New Supply represented by Immigration

Extreme 50% or more of New Supply represented by Immigration

Extremely Difficult 30+

High 25% to 50% of New Supply represented by Immigration

Hiring Difficulty Index

International Reliance Measure

Assesses the extent to which the New Supply of workers is dependent on workers from other countries. Given that the levers that control Immigration are not in the control of employers, this measure provides insight into the potential for New Supply expectations to be influenced by changes in Immigration policy.

Some Challenges 16–22

39 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Appendix A Description of Metrics and Glossary of Terms

1 2

4

3

Fewer Jobs The number of positions (demand) has declined from the previous year

Low 35% of Job Openings represented by Replacement

Excess Supply More than 60% higher than normal unemployment

No Job Openings There are 0 Job Openings

No Mobility Net Mobility is 0

Moving In Workers are moving to the province

Medium 35–70% of Job Openings represented by Replacement

Balanced Supply and demand Between 30–60% higher than normal unemployment

Low Leaving 10% or less of workers leaving

Moderate Leaving 10–25% of workers leaving

Extreme Leaving 50% or more of workers leaving

High Leaving 25–50% of workers leaving

High More than 70% of Job Openings represented by Replacement

Excess Demand, Limited Supply Below normal unemployment

Nearing a Tight Labour Market Between 0–30% higher than normal unemployment

Mobility Measure

Loss of Experience

Market Tightness

Demonstrates the extent to which movement into or out of the province affects the supply of workers available to fill Job Openings.

Assesses the rate at which experienced workers are retiring in relation to the number of Job Openings.

Assesses the “tightness” of the labour market; i.e., the degree of difficulty an employer may experience in trying to hire into the occupation.

40 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Appendix A Description of Metrics and Glossary of Terms

A measure of the decline in the number of workers who are active in an occupation at the beginning of the forecast and subsequently leave due to Replacement over the forecast period. Base Supply is calculated as the total supply less the average number of unemployed workers, less Replacement from each year of the forecast. Base Supply calculations demonstrate the changes in each year of the forecast period to the cohort of workers as compared with the first year of the forecast.

Low Investment Scenario Conservative scenario. It includes projects that are underway or certain to proceed, for a total of $103.5B from 2016 – 2025. 22% of this investment is in BC, 49% is in Alberta, 13% is in Saskatchewan and 16% is in Manitoba.

Moderate Investment Scenario Expected scenario. It adds projects that are planned and likely to proceed, for a total of $165.1B in invest-ments from 2016 – 2025. 36% of this investment is in BC, 35% is in Alberta, 17% is in Saskatchewan and 11% is in Manitoba.

High Investment Scenario Optimistic scenario. It adds projects that have been announced, but with more distant start dates or more regulatory approvals needed to proceed, for a total of $304.91B in investment from 2016 – 2025. 31% of this investment is in BC, 46% is in Alberta, 16% is in Saskatchewan and 6% is in Manitoba.

Base Supply

Economic Scenarios

Assesses the extent to which New Supply is keeping pace with Job Openings. It allows for an assessment of the extent to which conditions are tightening or loosening in the labour market.

Count Too Small Job Openings or New Supply is less than 6

No New Supply New Supply is 0 or negative

Medium New Supply is 93–97% of Job Openings

High New Supply is 93% or less of Job Openings

Supply Lag Measure

Low New Supply is 97% or more of Job Openings

41 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Appendix A Description of Metrics and Glossary of Terms

Expansion is defined here as the number of job openings in an occupation created by economic or business growth.

International Mobility refers to the NET number of workers that coming to Canada from other countries. It includes temporary foreign workers as well as immigrants to Canada. When more workers leave for other countries than come to Canada this can be a negative number.

Job openings is defined here as the need for new workers in an occupation created by expansion and/or replacement demand.

Labour Demand is defined here as the number of jobs available for workers who have the skills and/or required certifications to be considered qualified to work in each occupation in each year.

Labour Force Mobility refers to workers who are in the workforce and change from one occupation to another. An example of this is a worker who was a Heavy Duty Equipment operator and changes employment to become a Truck Driver, or who returns to the workforce after a short period away, such as after a disability leave.

The number of workers who have the skills and/or certifications to be qualified to work in each occupation each year, including those who are newly trained, have moved from other provinces or countries, or have moved from other occupations.

Mobility refers to the net number of workers coming into the APGC from other provinces. Net means the difference between those who leave the APGC to work in other provinces and those who come to the APGC from other provinces.

New Entrants are generally between the ages of 15 and 30. The number of new entrants is not the same as the number of graduates from school/training such as that measured by educational institution administrative data. New entrants refer to the number of graduates from school/training that fill the job openings. This number would not likely be the same as the administrative data for graduates since graduates do not always end up in the labour force. The number of New Entrants also considers previous participation in the labour force—if a new graduate has never worked before graduation they would be counted as 1.0 New Entrant. If a new graduate has worked 25% time before graduation, they would be counted as .075% of a New Entrant.

Expansion or Expansion Demand

International Mobility

Job Openings

Labour Demand

Labour Force Mobility

Labour Supply

Mobility

New Entrants

42 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Appendix A Description of Metrics and Glossary of Terms

New Supply or Net New Workers is the number of workers who are new to the occupations from four sources: immigration, other provinces or regions, other occupations, or those who are newly trained and new to the workforce. This creates growth in labour supply.

Replacement is defined here as the number of job openings in an occupation created by attrition—that is, the number of workers who leave each occupation, and the labour market as a whole, due to retirement or death each year.

Labour Supply is defined here as the number of workers who have the skills and/or required certifications to be considered qualified to work in each occupation in each year.

New Supply or Net New Workers

Replacement or Replacement Demand

Supply

43 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Economic Indicators and Major Projects included in the Economic ScenariosAppendix B

APPENDIXB ECONOMICINDICATORSANDMAJORPROJECTSINCLUDEDINTHEECONOMICSCENARIOS

The APGST LMI program uses Three Economic Scenarios:

Low InvestmentJJ Most ConservativeJJ Intended to be a

floor optionJJ Most project certaintyJJ Closest to Provincial

forecasts

Moderate InvestmentJJ Considered Most likelyJJ Intended to be the

most realistic optionJJ Project certainly decreasedJJ Closest to major eco-

nomic indicator forecasts

High InvestmentJJ Considered optimisticJJ Intended to be a ceiling,

but possible optionJJ Project certainty is lowestJJ Reflects a large amount of

economic stimulation

Economic Indicators by Scenario

Scenario Moderate1,2 Low High

Region Indicator 2016 2017–21 2021+ 2016 2017–21 2021+ 2016 2017–21 2021+

British ColumbiaGDP 2.4 2.2 2.1 2.2 1.3 1.6 5.1 3.4 1.8

Unemployment Rate 5.8 5.7 5.2 6.0 6.6 6.4 5.1 4.4 4.8

AlbertaGDP -1.3 1.2 1.7 -1.6 0.8 1.3 -0.4 1.7 2.0

Unemployment Rate 7.3 6.4 5.2 7.6 6.9 5.9 6.8 5.7 4.8

SaskatchewanGDP 1.0 1.1 0.7 0.0 0.7 0.4 2.0 2.3 1.0

Unemployment Rate 5.4 5.2 5.2 5.8 5.9 5.6 5.0 4.3 5.0

ManitobaGDP 2.6 1.7 1.8 2.2 1.4 1.7 2.9 2.0 2.0

Unemployment Rate 5.1 5.2 5.1 5.3 5.6 5.6 5.0 4.8 4.6

Country3 Indicator 2016 2017–21 2021+ 2016 2017–21 2021+ 2016 2017–21 2021+

ChinaGDP 6.2 5.9 6.0 5.0 4.9 5.0 6.7 6.8 7.0

Unemployment Rate 4.1 4.1 4.1 4.1 4.2 4.2 4.1 4.0 4.0

IndiaGDP 7.5 7.6 7.8 7.5 5.9 6.5 7.5 9.4 9.6

Unemployment Rate – – – – – – – – –

JapanGDP 1.0 0.7 0.7 1.0 0.6 0.5 1.0 1.1 1.0

Unemployment Rate 3.7 3.8 3.7 3.7 3.8 3.8 3.7 3.7 3.7

KoreaGDP 3.3 3.6 3.7 3.3 2.8 2.9 3.3 5.4 5.5

Unemployment Rate 3.6 3.4 3.3 3.6 3.4 3.4 3.6 3.3 3.2

United StatesGDP 2.6 2.5 2.2 2.4 2.0 1.7 2.8 2.9 2.7

Unemployment Rate 5.5 5.0 4.8 5.5 5.1 4.9 5.5 4.9 4.8

1 Canadian Data Source: APGC Forecast Model

2 International Data Source: World Bank

3 The Country data is generated as high, low and moderate, which may not align with the impact of expected commodity prices, they are included to assess the impact of economic differences in key trading partners.

Commodity Price Forecasts by Scenario

Scenario Moderate Low High

Commodity 2016 2017–21 2021+ 2016 2017–21 2021+ 2016 2017–21 2021+

Coal, Australia $/mt $63 $63 $63 $63 $50 $51 $63 $64 $65

WTI Oil (US$) $/bbl $33 $47 $72 $32 $46 $66 $34 $49 $77

Natural gas LNG, Japan $/mmbtu $10 $11 $12 $10 $8 $8 $10 $14 $15

Henry Hub Natural Gas (US$) $/mmbtu $2.6 $3.7 $5.2 $2.6 $3.6 $5 $2.7 $3.8 $5.6

Wheat, US, HRW $/mt $265 $253 $233 $265 $201 $197 $265 $390 $383

Timber Index, 2010=100 $96 $97 $101 $96 $84 $85 $96 $115 $120

Copper $/mt $6,152 $6,175 $6,190 $6,152 $5,800 $5,900 $6,152 $6,500 $7,000

Nickel $/mt $15,144 $14,943 $14,656 $15,144 $11,623 $11,569 $15,144 $16,000 $17,500

Gold $/toz $1,174 $1,092 $963 $1,174 $879 $855 $1,174 $1,307 $1,459

44 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Appendix B Economic Indicators and Major Projects included in the Economic Scenarios

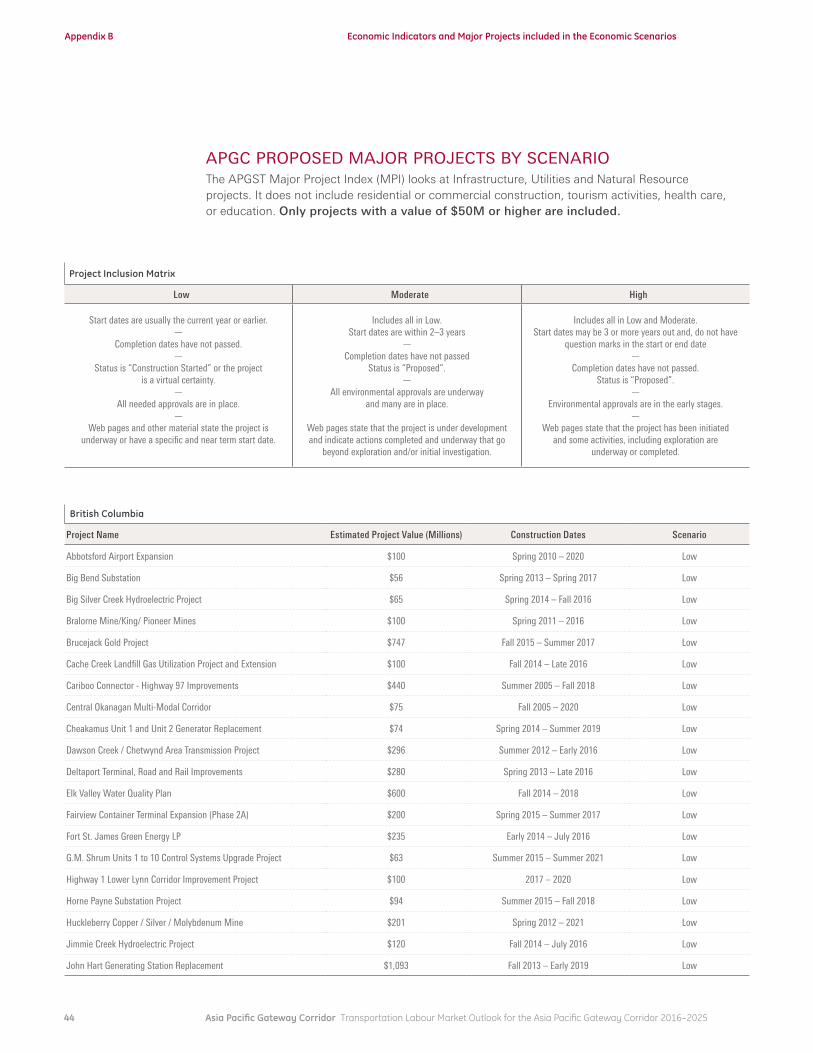

Project Inclusion Matrix

Low Moderate High

Start dates are usually the current year or earlier.—

Completion dates have not passed. —

Status is “Construction Started” or the project is a virtual certainty.

—All needed approvals are in place.

—Web pages and other material state the project is

underway or have a specific and near term start date.

Includes all in Low.Start dates are within 2–3 years

—Completion dates have not passed

Status is “Proposed”.—

All environmental approvals are underway and many are in place.

Web pages state that the project is under development and indicate actions completed and underway that go

beyond exploration and/or initial investigation.

Includes all in Low and Moderate.Start dates may be 3 or more years out and, do not have

question marks in the start or end date—

Completion dates have not passed.Status is “Proposed”.

—Environmental approvals are in the early stages.

—Web pages state that the project has been initiated

and some activities, including exploration are underway or completed.

British Columbia

Project Name Estimated Project Value (Millions) Construction Dates Scenario

Abbotsford Airport Expansion $100 Spring 2010 – 2020 Low

Big Bend Substation $56 Spring 2013 – Spring 2017 Low

Big Silver Creek Hydroelectric Project $65 Spring 2014 – Fall 2016 Low

Bralorne Mine/King/ Pioneer Mines $100 Spring 2011 – 2016 Low

Brucejack Gold Project $747 Fall 2015 – Summer 2017 Low

Cache Creek Landfill Gas Utilization Project and Extension $100 Fall 2014 – Late 2016 Low

Cariboo Connector - Highway 97 Improvements $440 Summer 2005 – Fall 2018 Low

Central Okanagan Multi-Modal Corridor $75 Fall 2005 – 2020 Low

Cheakamus Unit 1 and Unit 2 Generator Replacement $74 Spring 2014 – Summer 2019 Low

Dawson Creek / Chetwynd Area Transmission Project $296 Summer 2012 – Early 2016 Low

Deltaport Terminal, Road and Rail Improvements $280 Spring 2013 – Late 2016 Low

Elk Valley Water Quality Plan $600 Fall 2014 – 2018 Low

Fairview Container Terminal Expansion (Phase 2A) $200 Spring 2015 – Summer 2017 Low

Fort St. James Green Energy LP $235 Early 2014 – July 2016 Low

G.M. Shrum Units 1 to 10 Control Systems Upgrade Project $63 Summer 2015 – Summer 2021 Low

Highway 1 Lower Lynn Corridor Improvement Project $100 2017 – 2020 Low

Horne Payne Substation Project $94 Summer 2015 – Fall 2018 Low

Huckleberry Copper / Silver / Molybdenum Mine $201 Spring 2012 – 2021 Low

Jimmie Creek Hydroelectric Project $120 Fall 2014 – July 2016 Low

John Hart Generating Station Replacement $1,093 Fall 2013 – Early 2019 Low

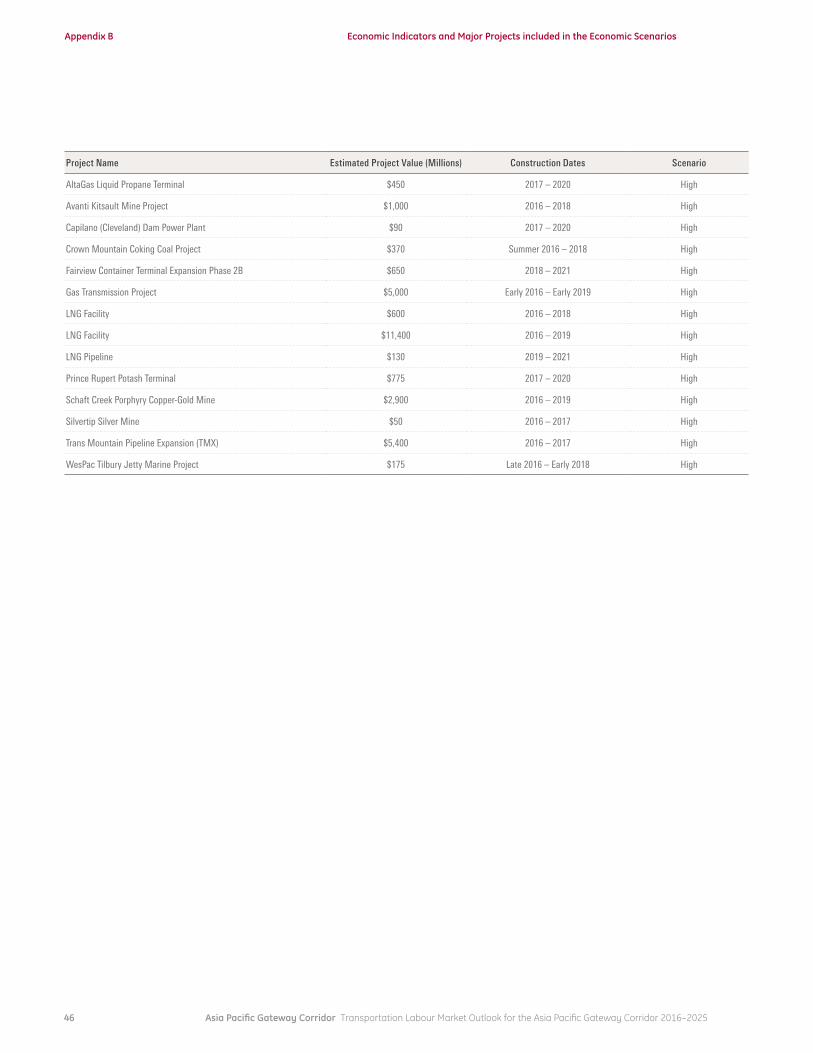

APGCPROPOSEDMAJORPROJECTSBYSCENARIOThe APGST Major Project Index (MPI) looks at Infrastructure, Utilities and Natural Resource projects. It does not include residential or commercial construction, tourism activities, health care, or education. Only projects with a value of $50M or higher are included.

45 Asia Pacific Gateway Corridor Transportation Labour Market Outlook for the Asia Pacific Gateway Corridor 2016–2025

Appendix B Economic Indicators and Major Projects included in the Economic Scenarios

Project Name Estimated Project Value (Millions) Construction Dates Scenario

Johnson Street Bridge Replacement $94 May 2013 – Spring 2017 Low

Kelowna International Airport Expansion $150 Feb 2008 – 2025 Low