transfer pricing developments and comparative cases 32942568/1

Post on 20-Dec-2015

217 views

TRANSCRIPT

TRANSFER PRICING DEVELOPMENTS AND COMPARATIVE CASES

32942568/1

Panel

• Danny Beeton – Freshfields Bruckhaus Deringer

• Mark Carnduff - HMRC• Owen Crassweller - Deloitte• Jonathan Schwarz – Temple Tax Chambers

32942568/2

Agenda

• The challenge of comparability• Contentious choice of methods• Business restructuring and non-recogntion of

transactions• Use of hindsight• Collaborative resolution

32942568/3

Transfer pricing – the challenge of comparability

IFA technical meeting: transfer pricing developmentsDanny Beeton, Freshfields Bruckhaus Deringer3 November 2011

Themes

The requirement for greater comparability (e.g. 2010 TPG, HMRC messages, DSG), leading to…

The increased preference for CUPs to be referred to (e.g. 2010 TPG, SNF)

The need to start from the standalone position of the taxpayer (e.g. AOy, GECC), but adjusted for…

The special relationship between related parties (e.g. GECC, Diligentia, Alberta Printed Circuits - but when and how)?

Revised comparability guidance in the 2010 Transfer Pricing Guidelines

OECD Transfer Pricing Guidelines para. 3.47:

“to be comparable means that none of the differences (if any) between the situations being compared could materially affect the condition being examined in the methodology or that reasonably accurate adjustments can be made to eliminate the effect of any such differences. “

Expanded discussion of problems in using the Transactional Net Margin Method (TNMM - para’s 2.56 to 2.107)

OECD Transfer Pricing Guidelines para 3.33:

“Use of commercial databases should not encourage quantity over quality.”

The new OECD “typical process” for a comparability analysis

1. Determination of years to be covered

2. Broad-based analysis of the taxpayer’s circumstances

3. Functional analysis

4. Review of potential internal comparable uncontrolled transactions

5. Review of potential external comparable uncontrolled transactions

6. Choice of method

7. Application of method

8. Comparability adjustments

9. Determination of arm’s length range

An interpretation of HMRC’s position

Removing the top and bottom 25% of a range of observations does not make the remaining ones any more comparable

HMRC is not obliged to accept that only one end of a transaction should be considered (“the tested party”)

HMRC may feel that the comparability differences are so great that a meaningful comparison cannot be made with another transaction or transactions proposed by the taxpayer

HMRC then form a view on the split of profit between the parties

In extreme cases HMRC may impute a different kind of transaction altogether, or no transaction at all

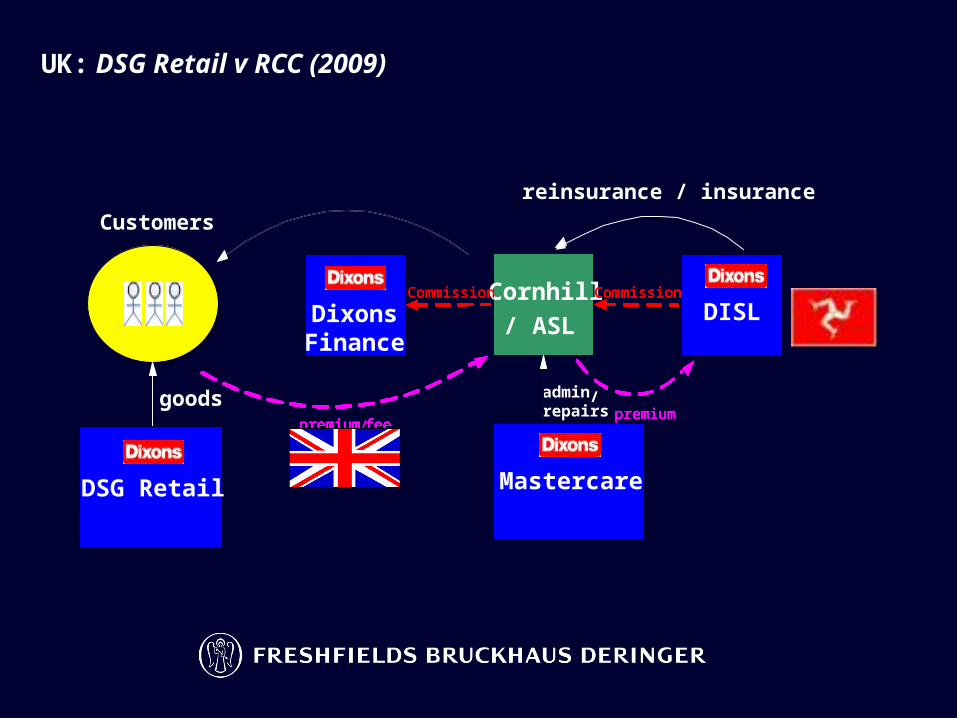

UK: DSG Retail v RCC (2009)

premium fee

DSG Retail

DixonsFinance

Cornhill/ASL

DISL

Mastercare

Customers

warranty

goods(agent) /admin

repairs

reinsurance / insurance

Commission Commission

/premium feepremium

DSG Retail

DixonsFinance

Cornhill

/ ASLDISL

Mastercare

/

Commission Commission

/premium feepremium

premium feepremium feepremium feepremium feepremium feepremium feepremium feepremiumpremium

Commission

premium

Commission Commission

premium

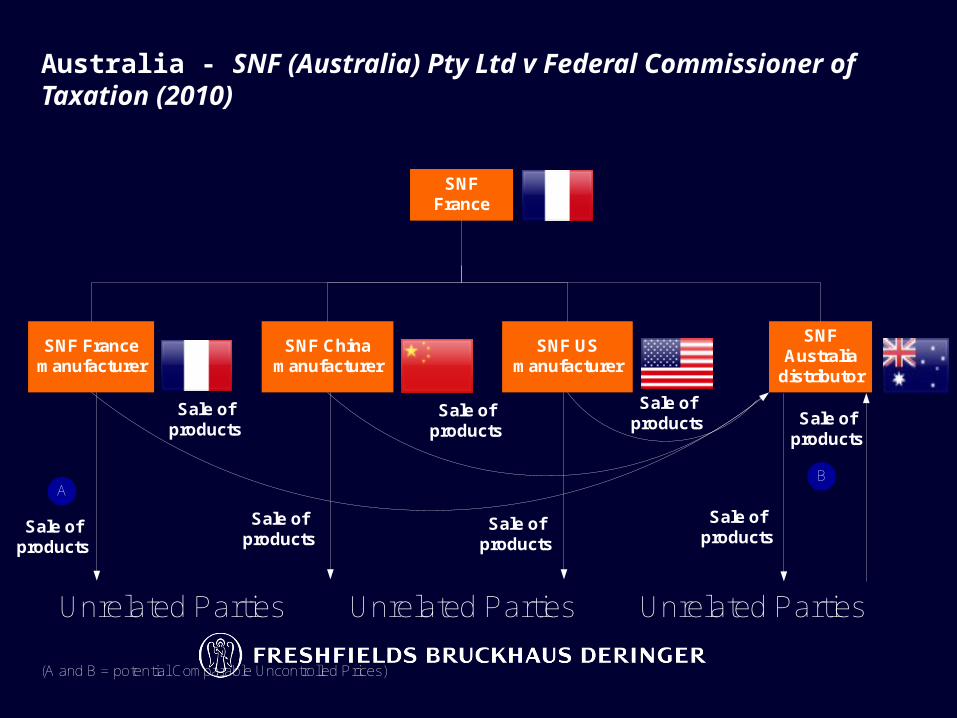

Australia - SNF (Australia) Pty Ltd v Federal Commissioner of Taxation (2010)

SNF France

SNF Francemanufacturer

SNF Chinamanufacturer

SNF USmanufacturer

SNF Australia

distributor

Unrelated Parties Unrelated Parties Unrelated Parties

Sale ofproducts

Sale ofproducts

Sale ofproducts

Sale ofproducts

Sale ofproducts

Sale ofproducts

Sale ofproducts

Sale ofproducts

AB

(A and B = potential Comparable Uncontrolled Prices)

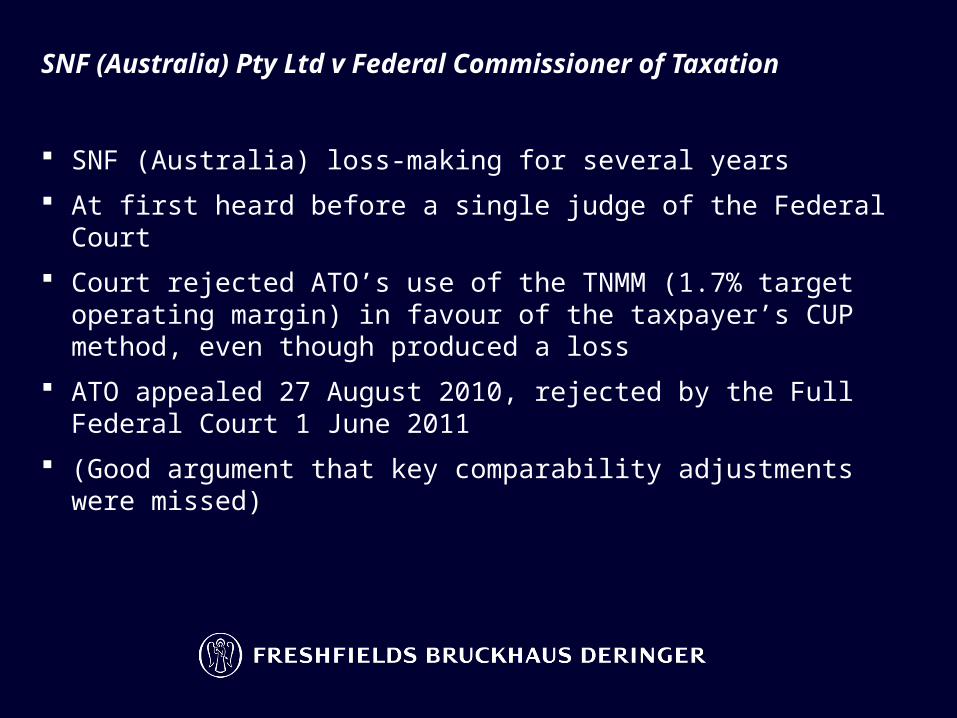

SNF (Australia) Pty Ltd v Federal Commissioner of Taxation

SNF (Australia) loss-making for several years

At first heard before a single judge of the Federal Court

Court rejected ATO’s use of the TNMM (1.7% target operating margin) in favour of the taxpayer’s CUP method, even though produced a loss

ATO appealed 27 August 2010, rejected by the Full Federal Court 1 June 2011

(Good argument that key comparability adjustments were missed)

A Oy: Ruling of the Finnish Supreme Administrative Court published on 3 November 2010, Case KHO 2010-73

New subordinated loans at 12.53% and 16.50%

Bank BAB

Sweden A Oy

Finland Bank

Other third party

lenders

Other A Group

subsidiaries

A Group

New secured and unsecured loans at 3.92% to 7.45%

New loans also at 9.5%

Old secured loans at 3.135% and 3.25%New loan at

9.5%

New shareholder loans at 17%

A Oy (continued)

(9.5% = average of new rates paid to third parties and shareholder)

BAB did not make a profit

A Oy was assessed for tax as if it had paid interest at 3.25%

A Oy appealed to Adjustment Board which reassessed tax as if interest at 7.04% had been paid (= average of interest rates paid by BAB to third parties, excluding shareholder loans)

Helsinki Administrative Court agreed

Taxpayer argued that the shareholder loans should be taken into account because at arm’s length interest rates - subordinated to 16.5% third party loans, so the arm’s length interest rate must be at least 17% as charged

State argued that A Oy’s interest rate should depend on its standalone creditworthiness and not be the same as the other subsidiaries, and on a standalone basis it would not need the third party and shareholder top-up

Supreme Administrative Court agreed, referred to the old bank loans and A Oy’s available collateral and enforced the original tax assessment based on a 3.25% interest rate

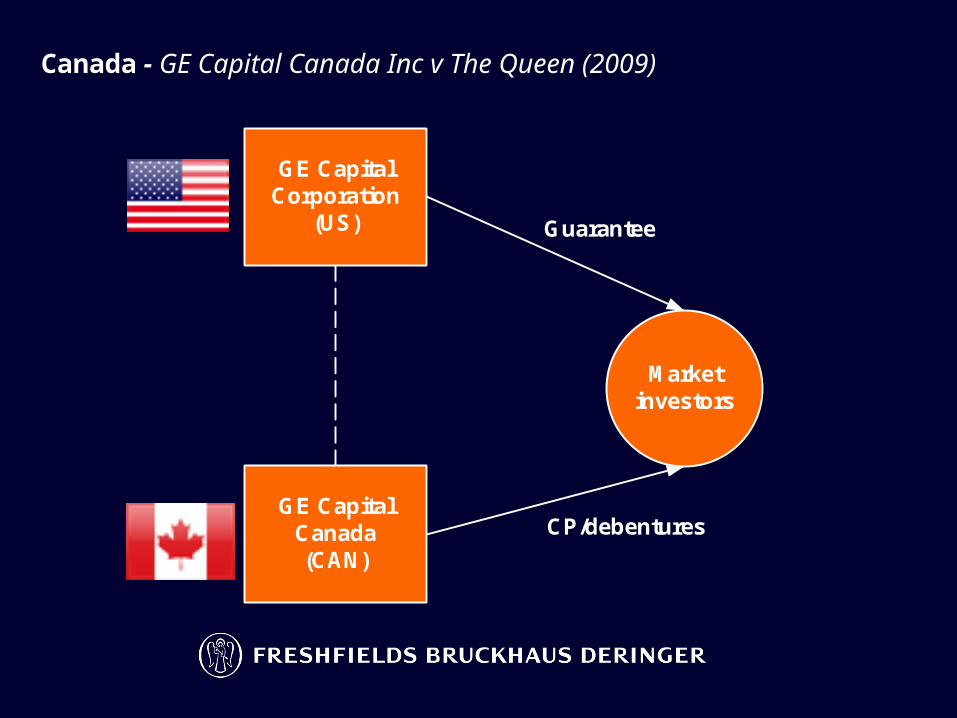

Canada - GE Capital Canada Inc v The Queen (2009)

GE Capital Corporation

(US)

GE Capital Canada(CAN)

Market investors

Guarantee

CP/debentures

GE Capital Canada Inc v The Queen

Canadian Revenue asserted US parent guarantee worthless as Canadian Sub benefited from implicit support anyway

Tax Court Canada (2009) held for GECC that guarantee fee is appropriate:

GECUS shareholding relevant for comparability but does not obviate need for guarantee

Implicit support is not a guarantee (but is a relevant fact – justifying 3 ratings notches in this instance)

Unwarranted to conclude that GECC’s credit rating would be the same as GECUS’s rating if no explicit guarantee

But separateness of entities respected: Sub did not acquire Parent’s AAA rating

Compare paragraph 7.13 OECD TPG

Federal Court of Appeal dismissed the Crown’s appeal in December 2010

Diligentia AB, case no. 2483-2485-09Ruling June 2010, Swedish Supreme Administrative Court

Independent lenders

Interest @ 4.25%

Interest@ 9.5%

Newunsecured

loan

Loans

Diligentia(SWE)

Parent

Repaid

Diligentia AB2010, Swedish Supreme Administrative Court

Consideration of whether unsecured loan from parent to sub analogous to a secured loan because of control relationship

Held: control affected credit risk and thus interest rate

Procedural issue blocked SAC’s consideration of a rate <6.5%, being the rate accepted on earlier appeal; 6.5% rate therefore confirmed

Alberta Printed Circuits Ltd v. The Queen 2011, Tax Court of Canada

APCI Inc received same payment as APCL

Taxpayer’s expert witness relied on the internal CUP without adjustments

CRA’s expert witness said unreliable, used the TNMM to benchmark APCI Inc (too profitable)

Judge accepted the internal CUP but said two business strategy adjustments should be made: being able to offer customers set-up services

lets APCL sell more profitable manufacturing services, so would transact with APCI Inc for no margin or even a loss (offsetting transaction)

and the shareholders of APCL would receive two thirds of the profits of an “overpaid” APCI Inc

but the Judge did not quantify the adjustments to confirm that the transfer price was arm’s length

Ramber Electronics Ltd

(Canada)

Alberta Print Circuits Ltd(Canada)

APCI Inc.(Barbados) · Provision of set-up

services

Customers of APCL

WB and GB DM

· Agreement to share the profits of APCI Inc 2/3 : 1/3

· Provision of set-up services

· Manufacturing of prototypes

© Freshfields Bruckhaus Deringer LLP 2011

This material is for general information only and is not intended to provide legal advice.

LON17860395

TRANSFER PRICING METHODS

Jonathan SchwarzTemple Tax Chamberswww.taxbarristers.com

32942568/20

A Brief History of TP Methods

• 1979 Guidelines– Traditional methods only

• 1995 Guidelines– Traditional transaction methods preferable to other

methods.– Transactional profit methods -last resort for exceptional

situations where no or insufficient data to rely on traditional methods

• Since 1995 Guidelines transactional profit methods used i practice far more than would be expected from their last resort status.

32942568/21

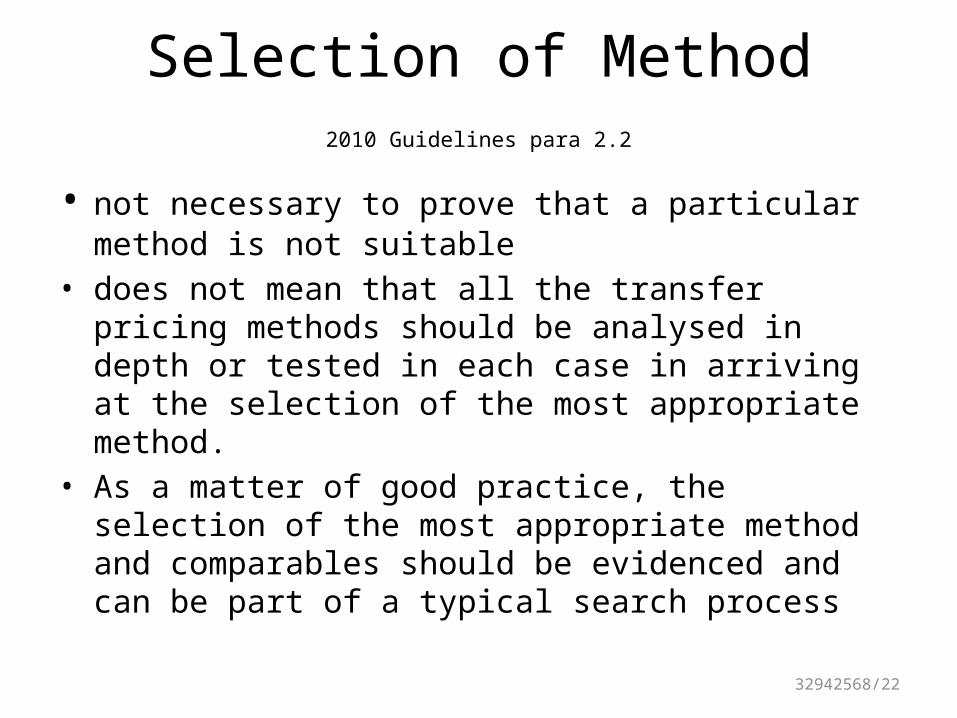

Selection of Method2010 Guidelines para 2.2

• not necessary to prove that a particular method is not suitable

• does not mean that all the transfer pricing methods should be analysed in depth or tested in each case in arriving at the selection of the most appropriate method.

• As a matter of good practice, the selection of the most appropriate method and comparables should be evidenced and can be part of a typical search process

32942568/22

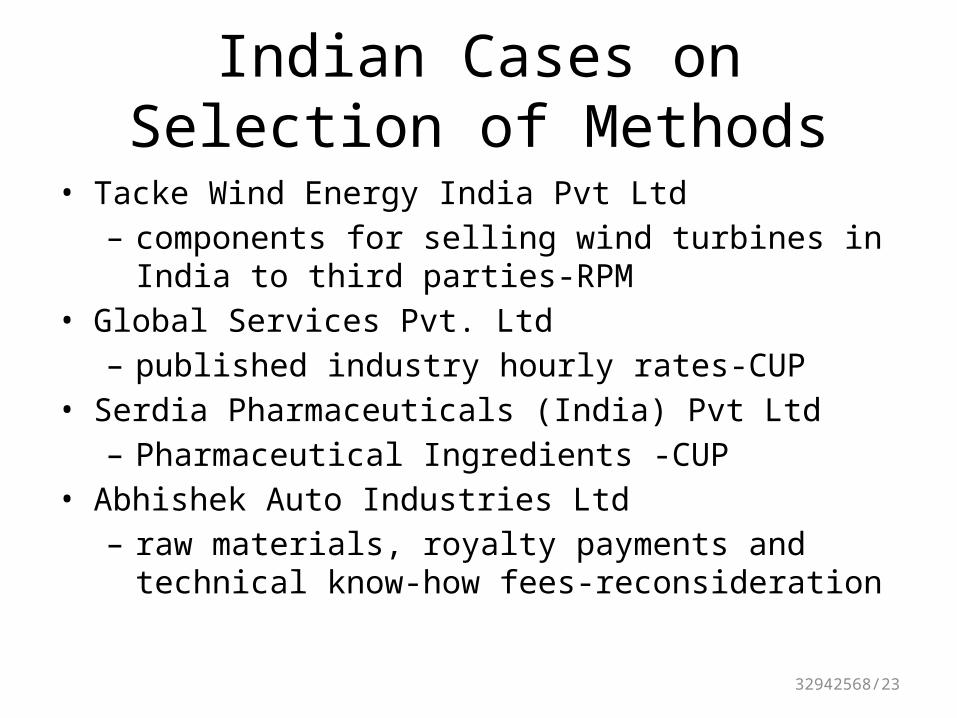

Indian Cases on Selection of Methods

• Tacke Wind Energy India Pvt Ltd – components for selling wind turbines in India to third

parties-RPM• Global Services Pvt. Ltd

– published industry hourly rates-CUP• Serdia Pharmaceuticals (India) Pvt Ltd

– Pharmaceutical Ingredients -CUP• Abhishek Auto Industries Ltd

– raw materials, royalty payments and technical know-how fees-reconsideration

32942568/23

SNF (Australia) Pty Ltd v. FCT[2010] FCA 635

• Imported products for manufacturing and selling chemicals in Australia– Taxpayer- CUP– Commissioner - TNMM

• Held:– TNMM does not provide a proper basis for

determining the arm's length consideration– Therefore does not address the issue as required

by Australian TP provisions.

32942568/24

SNF (Australia) Pty Ltd v. FCT[2010] FCA 635

• Full Bench:Only in the absence of useful evidence of an uncontrolled transaction will it be necessary to use another method. For example, because no comparable transaction exists or because there are differences in the transactions that cannot be taken into account. The other methods are also useful in that they can be used as a check on each other.

32942568/25

DSG Retail Ltd & Ors v HMRC

• Guidelines give a secondary role to other methods where traditional transactions methods cannot be reliably applied alone or exceptionally cannot be applied at all.

• One such other method is ...in particular the profit split method.

• Guidelines make the point that it is unusual to find profit as a condition "made or imposed" in the relevant transactions.

• This is an exceptional case because so long as the loss ratio is under 80%, the underwriting profit for Cornhill and DISL is set

32942568/26

BUSINESS RESTRUCTURING AND NON-RECOGNITION OF TRANSACTIONS

Owen CrasswellerDeloitte LLP

32942568/27

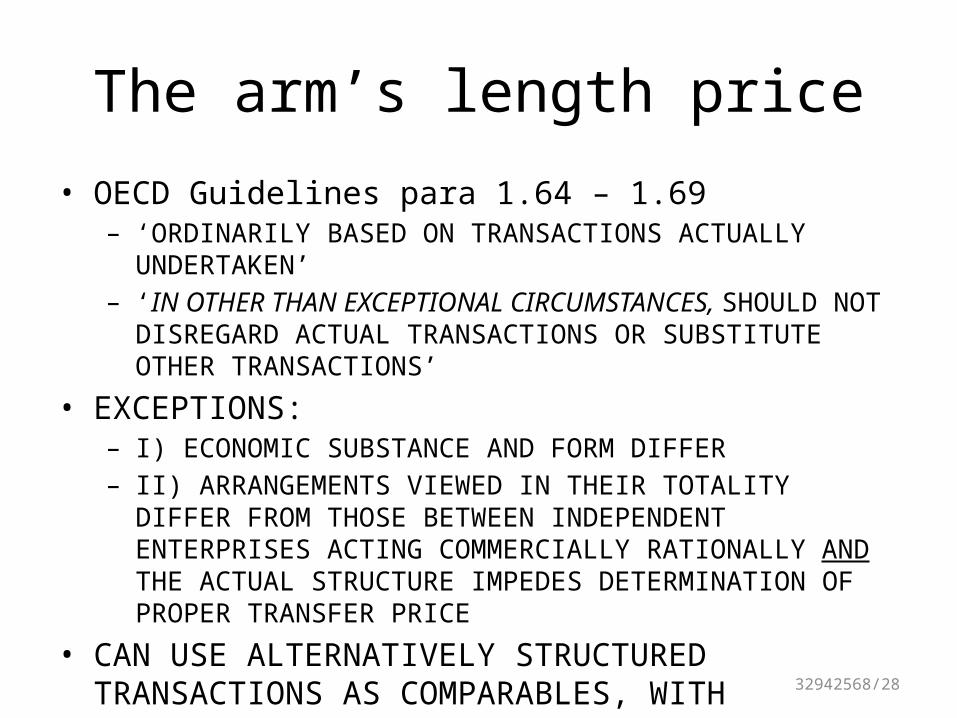

The arm’s length price

• OECD Guidelines para 1.64 – 1.69– ‘ORDINARILY BASED ON TRANSACTIONS ACTUALLY UNDERTAKEN’– ‘IN OTHER THAN EXCEPTIONAL CIRCUMSTANCES, SHOULD NOT

DISREGARD ACTUAL TRANSACTIONS OR SUBSTITUTE OTHER TRANSACTIONS’

• EXCEPTIONS:– I) ECONOMIC SUBSTANCE AND FORM DIFFER– II) ARRANGEMENTS VIEWED IN THEIR TOTALITY DIFFER FROM THOSE

BETWEEN INDEPENDENT ENTERPRISES ACTING COMMERCIALLY RATIONALLY AND THE ACTUAL STRUCTURE IMPEDES DETERMINATION OF PROPER TRANSFER PRICE

• CAN USE ALTERNATIVELY STRUCTURED TRANSACTIONS AS COMPARABLES, WITH APPROPRIATE ADJUSTMENTS

32942568/28

The arm’s length transaction

• Australia – ‘commercial realism’• Germany – ‘prudent business man’• France – ‘abnormal act of management’• UK - ‘could vs would’ / CFC Con Doc re

transfers of intangibles• OECD Guidelines – Chapter IX

32942568/29

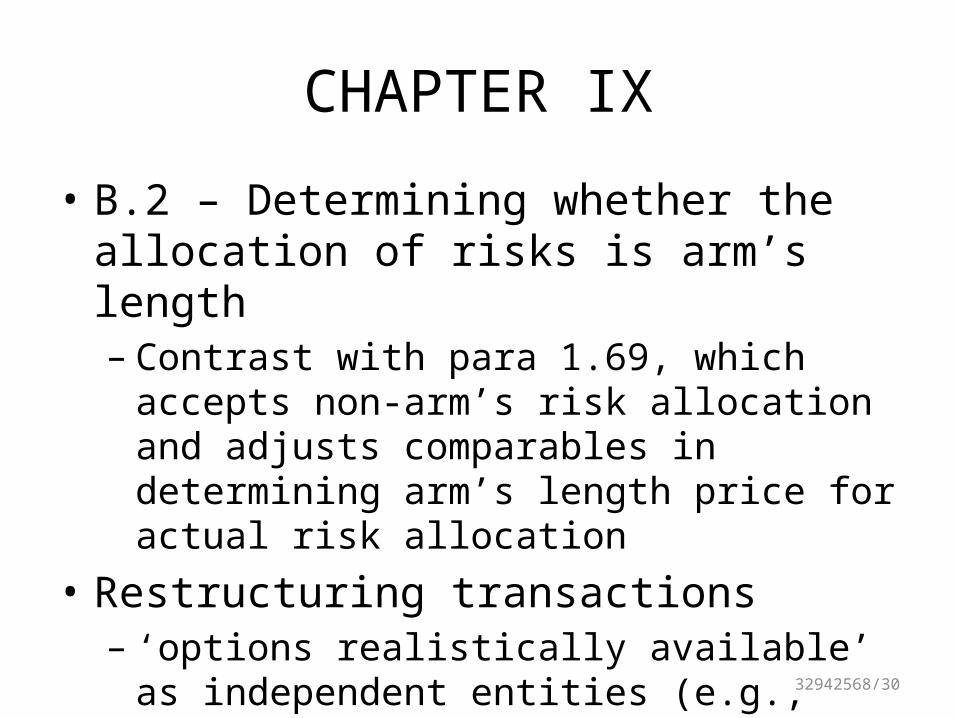

CHAPTER IX

• B.2 – Determining whether the allocation of risks is arm’s length– Contrast with para 1.69, which accepts non-arm’s

risk allocation and adjusts comparables in determining arm’s length price for actual risk allocation

• Restructuring transactions– ‘options realistically available’ as independent

entities (e.g., para 9.84 – group level motives irrelevant)

32942568/30

Chapter IX Part IV

• ‘exceptional’ in para 1.37 - .69 = ‘rare’ or ‘unusal’• Existence of comparable arrangements is binding• No requirement to behave in arm’s length manner• Standard is ‘commercial rationality in light of

realistically available options’• Ability to price actual arrangements prevents non-

recognition (but not risk reallocation!)

32942568/31

HINDSIGHTCOLLABORATIVE RESOLUTION

Mark CarnduffHMRC

32942568/32

Hindsight

‘TPG 3.68 In principle, information relating to the conditions of CUTs carried out during the same period of time as the controlled transaction is expected to be the most reliable information to use in a comparability analysis, because it reflects how independent parties have behaved in an economic environment that is the same as the economic environment of the taxpayers transaction.’

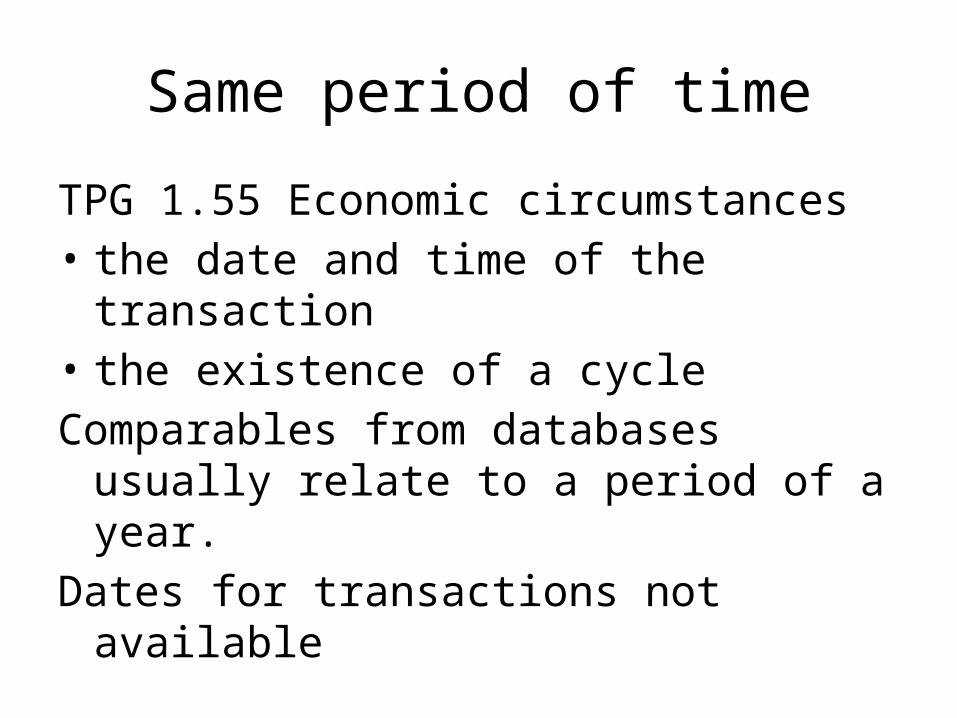

Same period of time

TPG 1.55 Economic circumstances• the date and time of the transaction• the existence of a cycleComparables from databases usually relate to a

period of a year.Dates for transactions not available

Timing

• It may be impossible to know an arm’s length price when transacting

• Will sufficient data be available before the return is completed?

• Fluctuations in prices during the year• What about penalties?• Is it more of an issue for TP compliance in

other fiscs?

Collaborative Resolution

• HMRC will seek to handle disputes non-confrontationally and by working collaboratively with the customer wherever possible.

• In the majority of cases, this is likely to be the most effective and efficient approach.

• A collaborative approach requires all parties to be open, transparent, and focused on resolving the dispute.