transcom q2 2015 results presentation

TRANSCRIPT

16 July 2015

Outstanding

Customer

Experience

Transcom

Second quarter 2015 results presentation Johan Eriksson, President & CEO

Ulrik Englund, CFO

2

• Good progress against all our financial targets

- Revenue growth

- EBIT margin

- Net debt/EBITDA

• Profitability improvements in all regions

• Management changes

Key highlights Q2 2015

At a glance

1

4

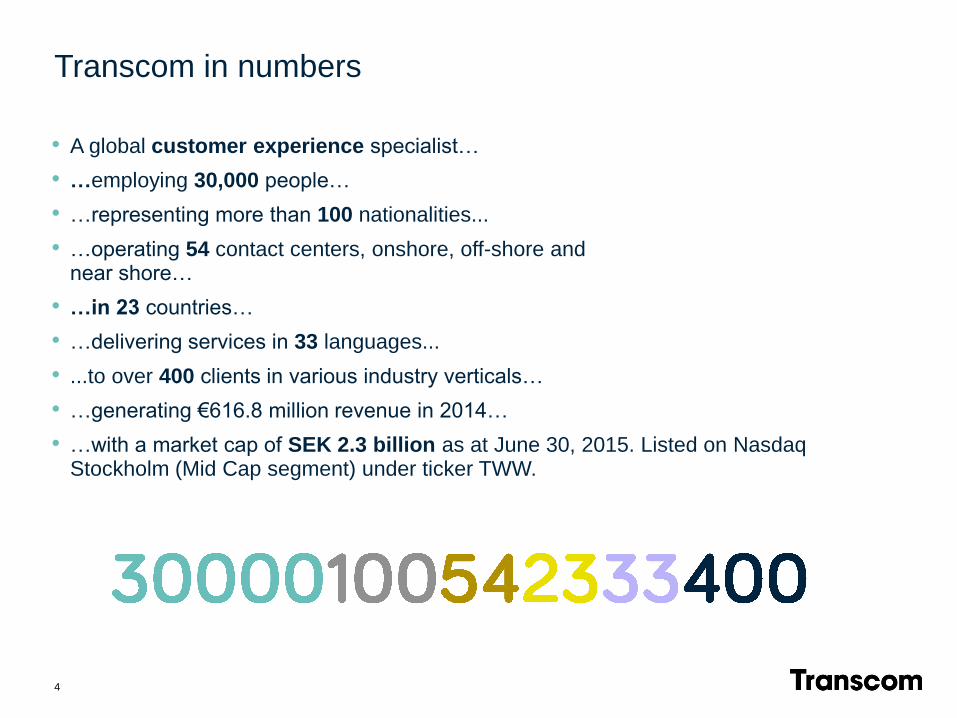

• A global customer experience specialist…

• …employing 30,000 people…

• …representing more than 100 nationalities...

• …operating 54 contact centers, onshore, off-shore and near shore…

• …in 23 countries…

• …delivering services in 33 languages...

• ...to over 400 clients in various industry verticals…

• …generating €616.8 million revenue in 2014…

• …with a market cap of SEK 2.3 billion as at June 30, 2015. Listed on Nasdaq Stockholm (Mid Cap segment) under ticker TWW.

Transcom in numbers

Steady improvement towards our mid-term EBIT margin target of at least 5 percent

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

Q2 2013 Q2 2014 Q2 2015

5

12-month rolling EBIT* margin development

* Excluding items affecting comparability

Mid-term target

• Targeted sales efforts

- Growth with existing

clients in new

geographies

- Broadening client base

• Efficiency improvements

driven by standardization

• Continuous focus on

underperforming areas

Our performance in Q2 2015

2

Q2 2014 Q2 2015

7

Like-for-like revenue, Q2 2015 vs. Q2 2014

€m 157.0

153.1 • Like-for-like revenue in Q2 2014

adjusted for currency effects (€+5.4m)

and CMS divestments (€-4.3m)

• The €3.9m like-for-like revenue

increase was mainly driven by higher

business volumes in Central & South

Europe and Iberia & Latam regions

• We continue focusing our efforts on

revenue growth, targeting at least 5%

organic growth

On a like-for-like basis, revenue in Q2 2015 increased by 2.6%

8

EBIT Q2 2014 One-off items Q2 2014

Cost savings programs

Volume & efficiency

Other EBIT Q2 2015

1.4

+2.4

+0.8 +0.5 -0.3

EBIT (mEUR)

Q2 2014 vs. Q2 2015 4.7

EBIT margin in Q2 2015 improved to 3.0% from 0.9% (2.5% in Q2 2014 excluding items affecting comparability)

• EBIT in Q2 2014 includes a €1.1m cost for the re-domiciliation and a €1.3m

capital loss from the divestment of CMS units

• Excluding the effects mentioned above, the EBIT margin improved by 0.5

percentage points

• Profitability improvements in all regions

0.9%

3.0%

9

• North Europe: Improvements in Sweden and

the Netherlands

• Central & South Europe: Increased volumes in

Germany, Poland and Tunisia

• Iberia & Latam: Improved profitability in Chile,

Peru and Portugal. Continued focus on

improving efficiency in Latin America.

• North America & Asia Pacific: Increased

efficiency and cost reductions.

All regions contributed to the EBIT margin improvement

2015

Apr-Jun

2014

Apr-Jun

EBIT margin

North Europe

Central & South Europe

Iberia & Latam

North America & AP

CRM

CMS*

Total

4.1%

3.4%

0.2%

3.8%

3.0%

n/a*

3.0%

4.0%

1.8%

-1.4%

1.5%

1.8%

-30.3%

0.9%**

* Divested since Q2 2014

** 2.5% excluding items affecting comparability in Q2 2014

Trend vs.

Q2 2014

Q2 2015 vs. Q2 2014

Average seat utilization

ratio

Average Efficiency ratio

(billable over worked hours

Monthly staff attrition

88% vs. 87%

n/a – flat

n/a – flat

10

KPIs vs. previous year

Key drivers to reach mid-term profitability targets

86.3 91.1

94.6 94.4 90.1

85.7

67.0 62.8

56.7 51.2

59.3 56.7

49.7

36.2

55.3 54.3

38.4

24.6 27.1

10.1

0.00

0.50

1.00

1.50

2.00

2.50

3.00

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

Q113 Q213 Q313 Q413 Q114 Q214 Q314 Q414 Q115 Q215

Gross debt (€ m) Net debt (€ m) Net debt/EBITDA

• Gross debt decreased by €5.5m compared to the Q115 level

• Net Debt decreased by €17.0m compared to the Q115 level

• Net Debt/EBITDA ratio: 0.3 (0.9 in Q115)

Debt & leveraging

11

3

Going forward – Transcom’s strategic direction

13

Transcom’s brand promise

Outstanding Customer

Experience, driving

revenue and brand

loyalty

”

Attractive market growth

14

• 5-6% annual growth in customer

management BPO in the next five years

• Fastest growth in emerging APAC and

Latam…

• …but the bulk of the industry increase will

be generated in mature markets, in

particular the United States

15

Respond to voice calls from

customers as efficiently as

possible, at the lowest possible

cost

The industry is transforming

Yesterday Today

• Deliver excellent customer experience

• New channels and technology

platforms

• Offer more knowledge due to diversity

of products and greater customer

demands

• Generating a much higher degree of

revenue and brand loyalty to clients

• Feedback of customer intelligence to

clients

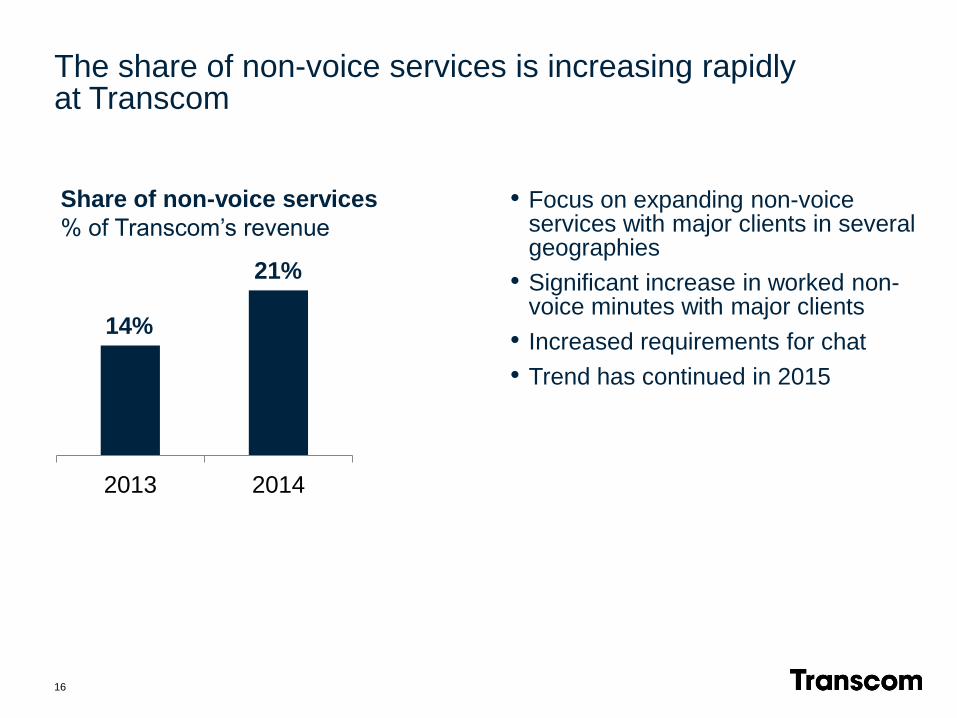

2013 2014

Share of non-voice services

% of Transcom’s revenue

16

The share of non-voice services is increasing rapidly at Transcom

• Focus on expanding non-voice services with major clients in several geographies

• Significant increase in worked non-voice minutes with major clients

• Increased requirements for chat

• Trend has continued in 2015

14%

21%

Transcom’s strategic priorities

17

18

www.transcom.com blog.transcom.com

Stay up-to-date on Transcom

Thank you! Questions?