trade finance products - coastline...

TRANSCRIPT

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 1

TRADE FINANCE PRODUCTS

Thriving international trade is a sign of a healthy global economy. Exports and imports

combined drive a huge amount of growth and development in the world, but especially in

emerging or developing economies.

The most common Trade Finance Products used in International Trade are Documentary

Collections, Documentary Credits and Guarantees or Standby Letters of Credit and Trade

Loans.

Trade Finance Products provided by a bank involve two key elements, risk coverage and

provision of finance, or simply put, money to support trade activities.

In this section we will look in greater detail at each product, identifying the benefits and

risks to both the exporter and the importer and the product cycle from application to

payment.

Trade Finance Products> Documentary Collections >

This section outlines how Documentary Collections are used to facilitate international

trade transactions.

This will be achieved by becoming familiar with:

A simple definition of Documentary Collections

The parties involved

The applicable international rules for bank Documentary Collections

The workflow for a Documentary Collections or ‘how it works’?

The benefits

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 2

Here is a simple but complete definition of a Documentary Collection as used in the context of international trade and

finance.

There are basically two ways in which collections may be used to collect payment from an importer in another country.

These two means are known as Export Documentary Collections and Export Clean Collections.

When using documentary collections the commercial and transport documents sent for collection may also be

accompanied by financial documents such as a Bill of Exchange or a Promissory Note.

Documentary Collection

Documentary collections are a service provided by a bank whereby the bank will use its

correspondent bank relationships as a network to collect the proceeds of export shipments

using the documentary collection product operating under internationally accepted rules

known as the URC 522.

Export Documentary Collection

In the case of Export Documentary Collections a bank will remit export documents which

result from the sales contract between the seller and the buyer to a nominated

correspondent bank in the importer's country.

Instructions will be provided to the bank to release the documents to the buyer (importer)

either against ‘sight payment’ or against acceptance of a Bill of Exchange (Draft). Upon

release of the documents to the importer, the importer can take delivery of the goods.

Export Clean Collection

In the case of Export Clean Collections the bank will only remit a financial document (Bill of

Exchange/Promissory Note) to a nominated correspondent bank in the importer's country.

Instructions will be provided to the collecting bank to present the financial document to

the buyer (importer) for payment at ‘sight’ or at some specified future date or ‘term’. As

the commercial documents are not involved in a clean collection, the clean collection

cannot provide any constructive control over the goods, it merely facilitates collection of

payment.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 3

Bill of Exchange

A Bill of Exchange is drawn up by the seller and can be defined as ‘An unconditional order

in writing drawn by the drawer requesting another party to pay on demand or on a future

determinable date a sum certain in money to, or to the order of, the drawer’

A Promissory Note

A Promissory Note is similar to a Bill of Exchange except that the promissory note is drawn

by the buyer and can be defined as ‘An unconditional promise to pay a sum certain in

money on demand or on a future determinable date to, or to the order of, another party’.

Documentary Collections follow a particular cycle or workflow with various roles filled by the parties involved:

The primary parties involved in a documentary collection are:

the Principal

the Remitting Bank

the Collecting Bank

sometimes a Presenting Bank and the Drawee

Like other international trade finance instruments used to facilitate international trade Documentary Collections also

operate subject to international rules developed by the ICC Banking Commission.

The Principal

The Principal is the party that initiates the collection and is often referred to as the

Exporter, Seller or Drawer.

The Remitting Bank

The Remitting Bank is the exporter's bank which remits the collection document to

the collecting bank in the importer's country.

The Collecting Bank

The Collecting Bank is often referred to as the correspondent bank or agent of the

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 4

remitting bank and its role is to endeavour to collect the proceeds of the collection

and remit the collected funds.

A Presenting Bank

The Presenting Bank is often the same bank as the collecting bank or it can be the

bank of the drawee or importer but in any event in the context of collections it is

acting under the collection instruction received from the Remitting Bank.

The Drawee

The Drawee is the importer, otherwise known as the Buyer.

ICC Banking Commission

The ICC Banking Commission is the largest commission of the International Chamber

of Commerce (ICC), the World Business Organization. The ICC Banking Commission has

more than 600 members in more than 100 countries.

The ICC Banking Commission is the rule making body for trade finance instruments

such as Documentary Credits (UCP), Demand Guarantees (URDG), Standby Letters of

Credit (ISP) and Documentary Collections (URC).

The rules, known as the Uniform Rules for Collections (URC) first came into force on 1 January 1968 and have been updated and modified with the most recent update being the Uniform Rules for Collections, 1995 Revision, ICC Publication No. 522, or URC 522 for short.

URC 522

The URC 522 rules provide a set of clear standardised procedures and regulations for all

parties involved in a collection,

the exporter or drawer;

the remitting bank;

the collecting bank;

the presenting bank; and

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 5

the importer or drawee.

The purpose of the URC 522 is to provide a standardised set of international rules for

collections, both clean and documentary, and to establish strict workable guidelines for all

parties that are involved in any stage of a collection operation.

The rules state that any collection can be subject to the URC 522 and that all parties to the

collection must adhere to the URC 522 unless it has been expressly agreed otherwise, and

unless the rules run contrary to the provision of a national, state or local law and/or regulation

which supersede the URC 522.

The Collection Order

When the remitting bank acting of behalf of the exporter sends a documentary collection to a collecting bank it will use a

standardized documentary collection instruction order which will state that the collection is to be handled subject to the

URC 522 rules. Every collection order will contain the following information:

The name of the Collecting Bank.

The number and type of documents included for collection.

Whether the collection is ‘Sight’ or ‘Term’.

The methods by which to remit proceeds.

Procedure in the case of dishonor or non payment.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 6

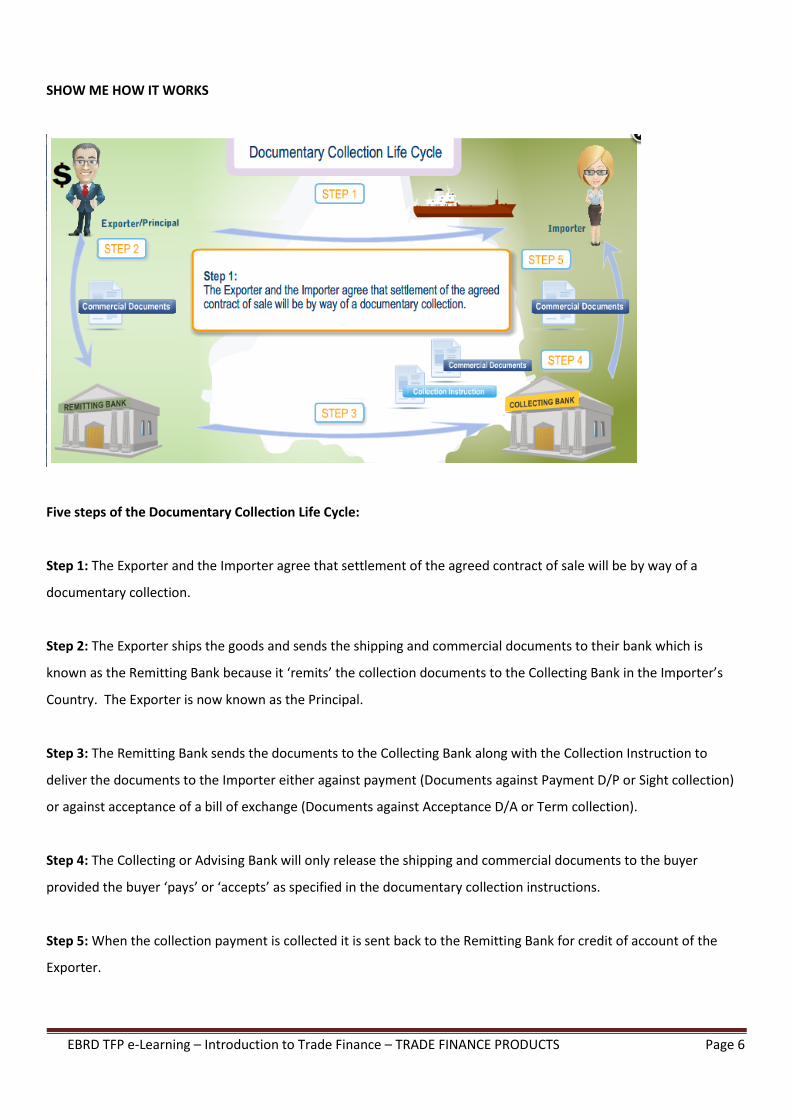

SHOW ME HOW IT WORKS

Five steps of the Documentary Collection Life Cycle:

Step 1: The Exporter and the Importer agree that settlement of the agreed contract of sale will be by way of a

documentary collection.

Step 2: The Exporter ships the goods and sends the shipping and commercial documents to their bank which is

known as the Remitting Bank because it ‘remits’ the collection documents to the Collecting Bank in the Importer’s

Country. The Exporter is now known as the Principal.

Step 3: The Remitting Bank sends the documents to the Collecting Bank along with the Collection Instruction to

deliver the documents to the Importer either against payment (Documents against Payment D/P or Sight collection)

or against acceptance of a bill of exchange (Documents against Acceptance D/A or Term collection).

Step 4: The Collecting or Advising Bank will only release the shipping and commercial documents to the buyer

provided the buyer ‘pays’ or ‘accepts’ as specified in the documentary collection instructions.

Step 5: When the collection payment is collected it is sent back to the Remitting Bank for credit of account of the

Exporter.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 7

There are 2 primary ways in which collection of payment and transfer of documents can take place:

Documents against Payment (D/P), also called a Sight Collection

and

Documents against Acceptance (D/A), also called a Term Collection

Another method for the operation of documentary collection is "D/A + Bank Aval".

Documents against Payment (D/P)

With ‘D/P’ or a Sight Collection, the collecting bank receives the Bill from the remitting

bank and presents it on to the importer, if necessary using the service of another bank

(the presenting bank). The payment instrument is accompanied by the commercial

documents as specified in the collection order.

On sight of this bill, the drawee (importer) is requested to pay the amount due in

exchange for release of the documents. When payment is effected the importer

receives the documents to collect the goods. The proceeds are sent by the collecting

bank to the remitting bank and then paid to the seller.

Documents against Acceptance (D/A)

Documents against Acceptance, or term collections, also known as usance collections

are used when payment is to be made on a future date and they provide the drawee

or buyer with time to pay (period of credit).

The buyer on whom the Bill is drawn is known as the drawee. The drawee is expected

to ACCEPT the term bill, which is an undertaking by the drawee to pay the amount

due at a specified future date (maturity date).

If the Bill is accepted then the documents are released to the drawee/importer to

collect the goods.

D/A + ‘Bank Aval’

In this case the collection order will specify that the Bill of Exchange must be accepted

by the drawee and also guaranteed or "avalised" by the importer's bank prior to

release of the documents.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 8

Documentary Collections - The Benefits for the Exporter

By using documentary collections I have a local bank in the importer's

country working to collect the proceeds of the collection.

Documentary collections are simpler for me to operate and not as

expensive as documentary credits. Of course they do not provide the

same level of security.

I have the protection of international rules setting out the obligations of

the parties involved.

I can obtain trade finance if my bank will discount an accepted draft or

bill of exchange that is for payment at a future date.

I have the security of guaranteed payment when the collection order is

avalised or guaranteed by a bank.

Documentary collections may enable the collecting bank to retain control

over the goods until either "payment" or "acceptance".

Documentary Collections - The Benefits for the Importer

I can avoid making payment in advance before the goods are shipped.

Documentary collections are simpler for me to operate and not as expensive

as documentary credits.

I have the protection of international rules setting out the obligations of the

parties involved.

Under a term or usance documentary collection I do not have to pay until

the maturity date. This reduces the amount of local financing that I need.

I am happy that my exporter trusts me to deliver under a documentary

collection.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 9

Trade Finance Products> Documentary Credits >

This section outlines how a Documentary Credit is used to settle international trade

transactions.

We will look at:

A simple definition of a Documentary Credit

The parties involved

The workflow for a documentary credit or ‘how it works’?

The methods of honour or settlement of a documentary credit

The benefits for the parties involved

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 10

A documentary credit is an undertaking by a bank that payment will be made when the seller presents documents

specified in the documentary credit. The documents should provide evidence that the seller has performed under

the international contract of sale.

A documentary credit is also referred to as a letter of credit or LC.

A documentary credit can be payable at sight (on presentation of documents) or at a future date. Documentary

credits operate globally under a very important set of international banking rules developed by the ICC known as

‘The Uniform Customs and Practice for Documentary Credits, 2007 Revision, ICC Publication no. 600 (“UCP”)’.

Documentary Credit

A documentary letter of credit is an undertaking by a bank, on behalf of an importer

(buyer), to pay a certain amount of money to an exporter (seller) within a specified

period of time, provided that the exporter presents documents specified in the letter

of credit, which comply with the terms and conditions set out in the letter of credit.

Future Date

Payment at a Future Date is (usually shown as 'X days from shipment date').

Where payment is at a future date the payment instrument is known as an

acceptance, deferred payment or usance letter of credit.

The International Chamber of Commerce

The International Chamber of Commerce (ICC) developed the ‘Uniform Customs and

Practice for Documentary Credits’ to provide importers and exporters with a set of

common rules to govern the operation of documentary credits.

When a documentary credit is issued that expressly states the

application of UCP 600 rules, the rules are binding on all parties.

Application of UCP 600 Rules:

The Uniform Customs and Practice for Documentary Credits,

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 11

2007 Revision, ICC Publication no. 600 (“UCP”) are rules that

apply to any documentary credit (“credit”) (including, to the

extent to which they may be applicable, any standby letter of

credit) when the text of the credit expressly indicates that it is

subject to these rules. They are binding on all parties thereto

unless expressly modified or excluded by the credit.

The effective date of the latest version UCP 600 rules was 1 July

2007.

The parties involved in a documentary credit transaction are:

the buyer or importer known as the Applicant,

the importer’s bank known as the Issuing Bank, and

the exporter known as the Beneficiary.

The banks that interact with the exporter (usually in the exporter’s country) are:

the Advising Bank,

the Confirming Bank and

the Nominated Bank

The Applicant

The buyer or importer is known as the Applicant because this party applies to its bank to issue a documentary credit to facilitate the shipment of the goods.

The Issuing Bank

The Issuing Bank issues the letter of credit on the instructions of the applicant. The

issuing bank takes a credit risk decision on the importer before agreeing to open the

letter of credit and must take adequate collateral and get approval for a credit line as

once issued the letter of credit is an irrevocable financial commitment of the bank.

The Beneficiary

The Beneficiary is the party in whose favour the documentary credit is issued and who

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 12

will benefit by means of obtaining payment for complying documents presented

under the documentary credit.

The Advising Bank

The Advising Bank is the bank, usually in the exporter's country, which verifies the

apparent authenticity of the letter of credit received from the issuing bank and which

subsequently forwards or advises it to the exporter.

The Confirming Bank

The Confirming Bank is the bank, usually located in the exporter's country which if

requested and if it agrees provides an additional independent undertaking to pay the

exporter, provided that a complying presentation of documents is made by or on

behalf of the exporter.

It is very often the case that the Advising Bank and the Confirming Bank are the same

bank.

The Nominated Bank

The Nominated Bank is the bank, again usually located in the exporter's country, with

which the documentary credit is available for drawing. In simple terms the

nominated bank can be said to be the bank authorised, within the letter of credit, to

make settlement to the exporter and to whom documents are normally presented.

It is very often the case that the Advising Bank and the Confirming Bank and the Nominated are one and the same bank.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 13

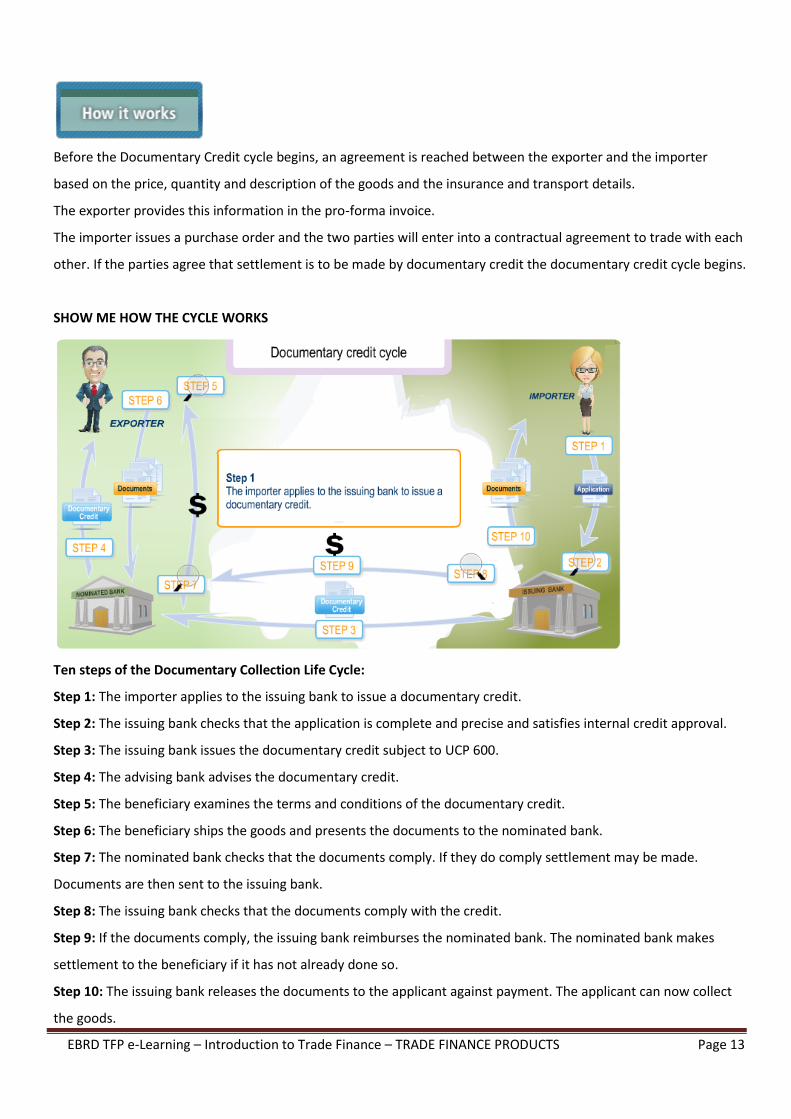

Before the Documentary Credit cycle begins, an agreement is reached between the exporter and the importer

based on the price, quantity and description of the goods and the insurance and transport details.

The exporter provides this information in the pro-forma invoice.

The importer issues a purchase order and the two parties will enter into a contractual agreement to trade with each

other. If the parties agree that settlement is to be made by documentary credit the documentary credit cycle begins.

SHOW ME HOW THE CYCLE WORKS

Ten steps of the Documentary Collection Life Cycle:

Step 1: The importer applies to the issuing bank to issue a documentary credit.

Step 2: The issuing bank checks that the application is complete and precise and satisfies internal credit approval.

Step 3: The issuing bank issues the documentary credit subject to UCP 600.

Step 4: The advising bank advises the documentary credit.

Step 5: The beneficiary examines the terms and conditions of the documentary credit.

Step 6: The beneficiary ships the goods and presents the documents to the nominated bank.

Step 7: The nominated bank checks that the documents comply. If they do comply settlement may be made.

Documents are then sent to the issuing bank.

Step 8: The issuing bank checks that the documents comply with the credit.

Step 9: If the documents comply, the issuing bank reimburses the nominated bank. The nominated bank makes

settlement to the beneficiary if it has not already done so.

Step 10: The issuing bank releases the documents to the applicant against payment. The applicant can now collect

the goods.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 14

When an exporter ships the goods and presents the documents required under the letter of credit the method of

settlement will depend on how the credit was made available.

The documentary credit must state where it is available and how it is made available for drawing or settlement to

the beneficiary exporter.

Where and how a documentary credit may be made available to the exporter beneficiary is covered by UCP 600

Article 6.

In simple terms we can say that a documentary credit can be made available by:

sight payment

deferred payment

acceptance or

negotiation

Where a documentary credit is made available to an exporter:

A credit must state the bank with which it is available or whether it is available with

any bank.

A credit available with a nominated bank is also available with the issuing bank.

How a documentary credit is made available to an exporter:

A credit must state whether it is available by sight payment, deferred payment,

acceptance or negotiation.

UCP 600 Article 6:

a) A credit must state the bank with which it is available or whether it is available with

any bank. A credit available with a nominated bank is also available with the issuing

bank.

b) A credit must state whether it is available by sight payment, deferred payment,

acceptance or negotiation.

c) A credit must not be issued available by a draft drawn on the applicant.

d)

i. A credit must state an expiry date for presentation. An expiry date stated for honour or

negotiation will be deemed to be an expiry date for presentation.

ii. The place of the bank with which the credit is available is the place for presentation.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 15

The place for presentation under a credit available with any bank is that of any bank. A

place for presentation other than that of the issuing bank is in addition to the place of

the issuing bank.

e) Except as provided in sub-article 29 (a), a presentation by or on behalf of the

beneficiary must be made on or before the expiry date.

Sight Payment

The letter of credit may provide for immediate payment of the sum due. This is known

as ‘available by sight payment’. The paying bank will either be the issuing bank, the

confirming bank, or another nominated bank in the exporter’s country. The exporter

will present the required documents to the bank. If the documents are in order,

payment is authorised to be made at sight.

Deferred Payment:

In this case the issuing bank/confirming bank will simply incur a deferred payment

undertaking for payment on a future date.

It is possible for the exporter to request the bank to discount or provide finance under

the deferred payment documentary credit. If the bank provides finance this is known

as the bank making a prepayment or purchasing before the actual maturity date for

payment.

Acceptance:

This method of settlement involves the acceptance of a bill of exchange drawn by the

exporter on the bank where the credit is available.

These credits are known as acceptance, term or usance credits and payment is due at

the maturity of the bill of exchange. However, if the exporter requires cash

immediately, he can request the accepting bank or another bank to discount the

accepted bill of exchange.

Negotiation:

If the issuing bank authorises a nominated bank in the exporter’s country to negotiate,

then the nominated bank may advance its own money to the exporter or beneficiary

of the letter of credit in advance of the maturity date, by purchasing the documents

and/or drafts that have been presented in compliance with the terms and conditions

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 16

of the credit.

The negotiating bank will charge a negotiation fee which basically represents interest

on the advance of funds from the date of advance to the date that the negotiating

bank receives final settlement by the issuing bank.

Documentary Credits - The Benefits for the Exporter

I have an independent bank undertaking before I ship my goods.

I can agree the specified documentary conditions in advance that suit my needs.

With a confirmed documentary credit when I can comply with the terms and

conditions then even the country risk can be removed.

Documentary credits enable me to offer extended credit to my import

customers and this increases my business volumes.

I can on occasion obtain pre-shipment finance when I can show my bank I have

been advised a documentary credit from a reputable bank.

In emerging markets where interest rates are higher than in my country the

documentary credit helps me offer better contract terms to my customers.

Documentary credits are irrevocable so once in place the undertaking to pay

cannot be cancelled or amended unless I agree.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 17

Documentary Credits - The Benefits for the Importer

I can avoid having to pay in advance for goods ordered.

I can agree terms and conditions in the credit which will require documents

that will evidence that the supplier has performed under the contract.

By providing a documentary credit to the exporters it is possible to get

extended payment terms.

With extended payment terms I can sell the imported goods with the profit

margin before the payment is due to be made.

Documentary credits in most instances cost a lot less then borrowing in

local currency to import goods.

My local bank can be more amenable to issue a letter of credit than to give

me an import loan as they can on occasion take the goods as collateral.

Banks also like to finance imports by documentary credit as they are certain

as to the purpose of the documentary credit finance facility.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 18

Trade Finance Products> Guarantees/Standby Letters of Credit >

In this section I will outline how Bank Guarantees and Standby Letters of Credit are used to secure and facilitate

international trade transactions.

This will be achieved by becoming familiar with:

A simple definition of a Bank Guarantee

The use of Direct and Indirect Guarantees

The applicable international rules for bank guarantees

The workflow for a Bank Guarantee or ‘how it works’?

The fundamentals of Standby Letters of Credit and the applicable rules.

The benefits

Here is a simple but complete definition of a bank guarantee which in the context of international trade is often

referred to as a demand guarantee.

Guarantees can be issued by parties other than banks but in the context of international trade most guarantees are

issued by banks. For instance Guarantees can be issued by Insurance Companies, Corporate bodies or other financial

institutions.

In the context of securing international trade and finance transactions guarantees are issued by banks and are

typically payable on demand.

In common with Documentary Credits guarantees are used to secure a payment obligation relating to an underlying

contract but in the context of guarantees this is referred to an underlying relationship.

Bank Guarantee

A bank guarantee is an irrevocable undertaking issued by a bank on behalf of an

instructing party, usually the Applicant, to another party that the bank will pay a sum

of money against a written demand for payment or against submission of a document

(or documents) stipulated in the guarantee document itself.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 19

Demand Guarantee

When a bank issues a demand guarantee that bank has an obligation to pay on

demand without contestation provided that bank receives a demand that is a

complying demand under the demand guarantee

Underlying Relationship

The parties to the underlying contract or agreement are understood to be the parties

to the underlying relationship. The party with the obligation under the underlying

relationship, which is secured by the Guarantee, is known as the ‘Applicant’ whereas

the party in whose favour the guarantee is issued is known as the ‘Beneficiary’.

Historically bank demand guarantees tended to be issued

subject to the local law of a particular country but in the

evolution of modern international guarantee practice there has

been a dramatic increase in the use the international rules of

the ICC.

In day to day international guarantee practice the international

rules for demand guarantees are known as the URDG.

The benefits of using standardised international rules which

have been agreed by the international trade banking community

is that the rules supplement the local law and clearly establishes

the payment must be made on presentation by the beneficiary

of a complying demand and furthermore defines what is the

nature of a demand guarantee issued subject to the URDG.

Simply put, the bank must pay on demand against a complying

demand which under the URDG rules must meet the

requirements of a complying presentation.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 20

There are two general categories of demand guarantees used to secure international trade and finance – these

are Direct Guarantees and Indirect Guarantees.

Both categories are used in international trade transactions but with transactions between parties located in

different countries the use of Indirect Guarantees is more common.

In common with Documentary Credits, guarantees whether they are Direct Guarantees or Indirect Guarantees are

used to secure a payment obligation relating to an underlying contract or agreement.

In the context of bank demand guarantees this relationship is typically referred to an underlying relationship.

Direct Guarantees

Direct Guarantees are used when the beneficiary of the guarantee is willing to accept

the guarantee issued directly by the foreign bank in favour of the beneficiary.

Indirect Guarantees

Indirect Guarantees are when the beneficiary of the guarantee will typically only

accept a guarantee issued by a local bank in the country of the beneficiary.

Underlying Relationship

The parties to the underlying contract or agreement are understood to be the parties

to the underlying relationship.

The party with the obligation under the underlying relationship, which is secured by

the Guarantee, is known as the ‘Applicant’ whereas the party in whose favour the

guarantee is issued is known as the ‘Beneficiary’.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 21

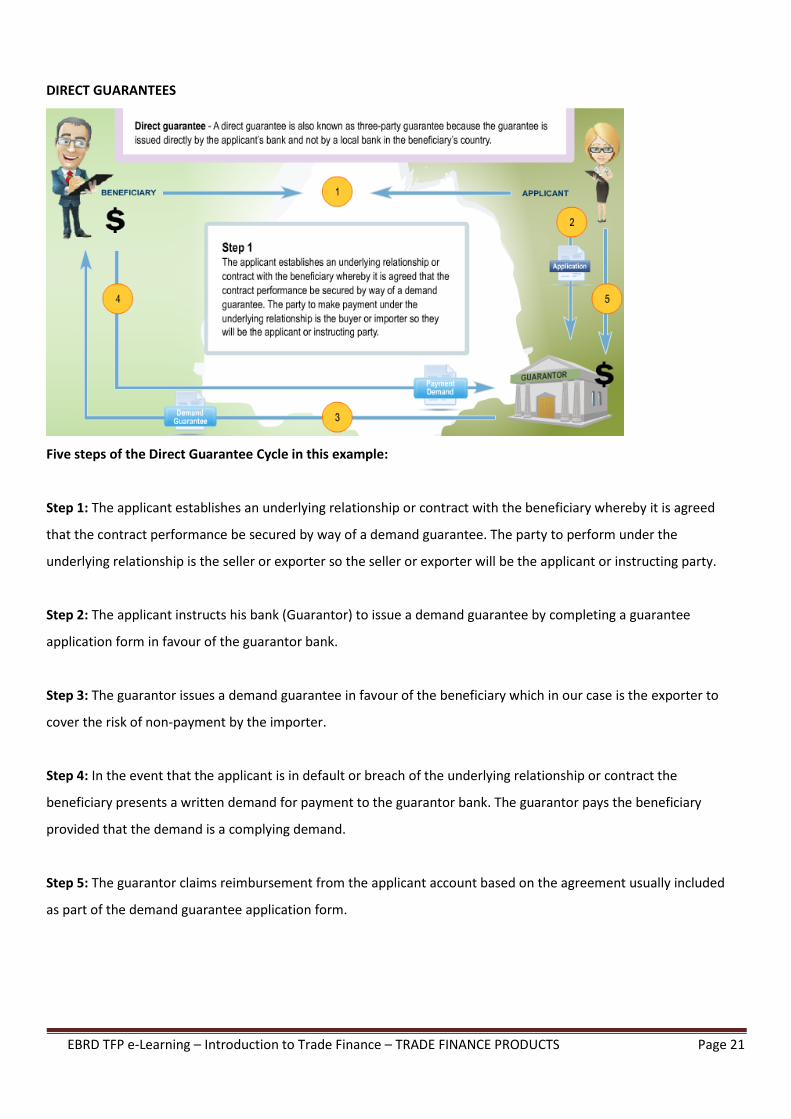

DIRECT GUARANTEES

Five steps of the Direct Guarantee Cycle in this example:

Step 1: The applicant establishes an underlying relationship or contract with the beneficiary whereby it is agreed

that the contract performance be secured by way of a demand guarantee. The party to perform under the

underlying relationship is the seller or exporter so the seller or exporter will be the applicant or instructing party.

Step 2: The applicant instructs his bank (Guarantor) to issue a demand guarantee by completing a guarantee

application form in favour of the guarantor bank.

Step 3: The guarantor issues a demand guarantee in favour of the beneficiary which in our case is the exporter to

cover the risk of non-payment by the importer.

Step 4: In the event that the applicant is in default or breach of the underlying relationship or contract the

beneficiary presents a written demand for payment to the guarantor bank. The guarantor pays the beneficiary

provided that the demand is a complying demand.

Step 5: The guarantor claims reimbursement from the applicant account based on the agreement usually included

as part of the demand guarantee application form.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 22

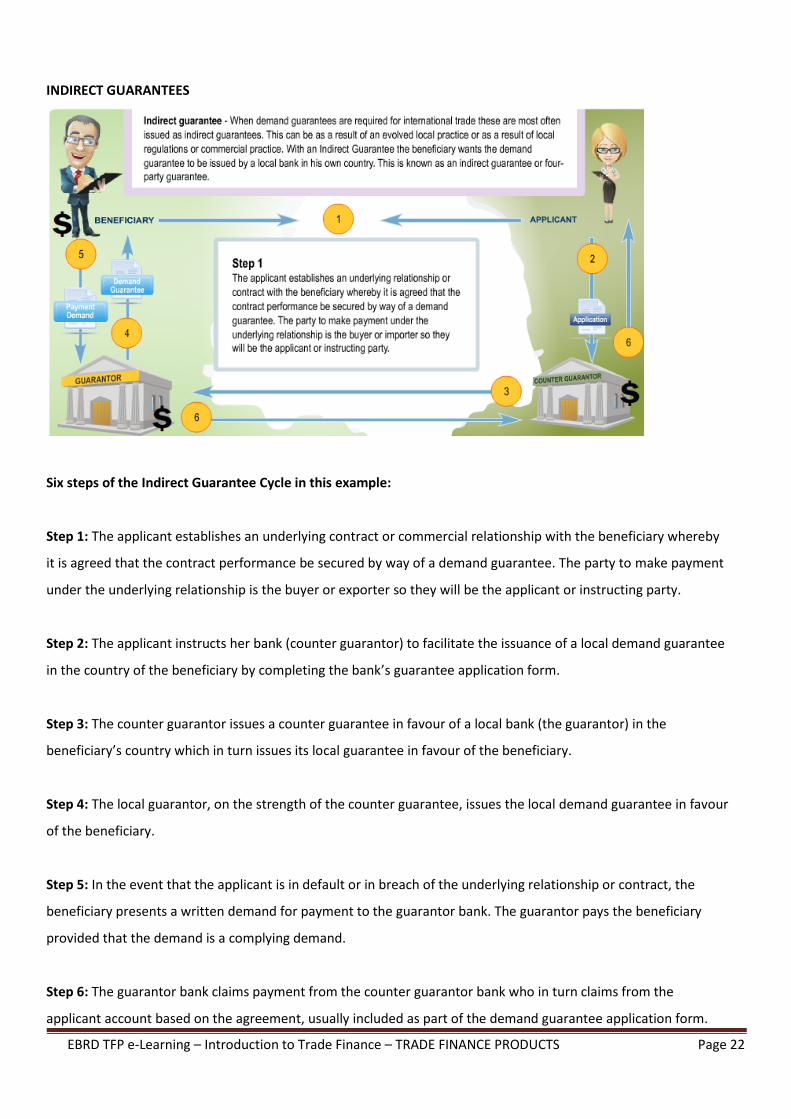

INDIRECT GUARANTEES

Six steps of the Indirect Guarantee Cycle in this example:

Step 1: The applicant establishes an underlying contract or commercial relationship with the beneficiary whereby

it is agreed that the contract performance be secured by way of a demand guarantee. The party to make payment

under the underlying relationship is the buyer or exporter so they will be the applicant or instructing party.

Step 2: The applicant instructs her bank (counter guarantor) to facilitate the issuance of a local demand guarantee

in the country of the beneficiary by completing the bank’s guarantee application form.

Step 3: The counter guarantor issues a counter guarantee in favour of a local bank (the guarantor) in the

beneficiary’s country which in turn issues its local guarantee in favour of the beneficiary.

Step 4: The local guarantor, on the strength of the counter guarantee, issues the local demand guarantee in favour

of the beneficiary.

Step 5: In the event that the applicant is in default or in breach of the underlying relationship or contract, the

beneficiary presents a written demand for payment to the guarantor bank. The guarantor pays the beneficiary

provided that the demand is a complying demand.

Step 6: The guarantor bank claims payment from the counter guarantor bank who in turn claims from the

applicant account based on the agreement, usually included as part of the demand guarantee application form.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 23

Depending on the contractual relationship between the parties involved there are various forms of demand

guarantees that fulfil important functions in supporting :

Delivery of Goods between Exporters and Importers

Completion of major construction, infrastructure or development contracts between contracting parties.

Here are some common various forms of demand guarantees that are used to support secure international trade

and contracts.

Payment Guarantee:

The payment guarantee provides security for a contractual payment obligation, such as in connection with a

contract of sale, a construction contract, loan or any other financial commitment.

A payment guarantee can be issued for the full amount of the contract or, where part of the amount has been paid

in advance, for the remaining amount due under an underlying relationship.

Tender Guarantee (Bid Bond):

The tender guarantee covers the risk that the company submitting the tender under the underlying relationship:

- Withdraws its offer prior to the actual awarding of the tender;

- Fails to sign the contract, if awarded the tender under the underlying relationship

- Fails to submit the required performance guarantee, if required.

These guarantees are normally issued for a specified percentage (usually 1%-5%) of the contract value

Performance Guarantee:

A performance guarantee is issued for a specified percentage (usually 10%-15%) of the contract sum under the

underlying relationship. The performance guarantee may be issued as a single guarantee to cover all phases of the

contract or issued to cover distinct segments of the contract. The performance guarantee will provide that the

beneficiary may make an on demand claim in the event of non or delayed performance by the applicant in respect

of the underlying relationship or contract.

Warranty Guarantee:

The purpose of the warranty guarantee is to cover the applicant’s obligations after it has delivered the goods or

completed its work during the contractual warranty period. In the event that there is a breach of warranty or, for

example, machinery breaks down, the beneficiary may demand payment under the warranty guarantee.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 24

Advance Payment Guarantee:

The contractor (applicant) may receive a pre-payment (the advance payment amount) on the contract value. The

aim of this pre-payment is usually to purchase raw material or hire machinery related to the contract.

This demand guarantee is used to secure the beneficiary’s right to recover the advance payment received by the

applicant in the event of the applicant’s failure to perform the contractual obligations relating to the advance

payment. The amount in such guarantee is usually agreed between the contracting parties.

The use of Standby Letters of credit to support and secure international trade and finance is growing rapidly.

At a basic level the Standby Letter of Credit has many features similar to a demand guarantee.

Standby Letters of Credit are most often used as a ‘Standby Security’ which stand-by in the event that the buyer of

a contractor fails to perform under an underlying contract or agreement – or fails to pay an amount of money due.

In common with Documentary Credits and Demand Guarantees, Standby Letters of Credit

are issued subject to international rules of the ICC.

A Standby Letter of Credit can be issued subject the UCP 600 rules or another set of rules

developed specifically for use with Standby Letters of Credits. These specific rules are

known as the ISP or ‘International Standby Practices’ and the version currently in effect is

ISP98. A Standby Letter of Credit can be issued subject to the UCP 600 rules, or the ISP98

rules.

The ICC

The International Chamber of Commerce (ICC) developed the ‘Uniform Customs and

Practice for Documentary Credits’ to provide importers and exporters with a set of

common rules to govern the operation of documentary credits.

The ISP98 Rules

International Standby Practices (ICC Publication No. 590, 1998 Edition) are rules

developed and designed specifically for use with Standby Letters of Credit.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 25

Guarantees/Standby Letters of Credit - The Benefits for the Exporter

With one bank demand guarantee or a Standby Letter of Credit in my favour I can

cover the risk of non payment for many exports to my regular import customers.

As an exporter I can tender or bid for large contracts when my bank will support my

tender with a tender guarantee.

The independent nature of a demand guarantee provides a lot of security for the

parties involved as it is independent of the underlying contract or relationship.

I can offer greater amount of credit and extended credit to my customers when their

payment obligations are supported by a bank guarantee.

There is significant comfort for my business when there is a bank guarantee or standby

letter of credit standing by in the event of a default.

By getting my bank to issue an advance payment guarantee in favour of my customers I

often receive an advance payment on the contract amount which is much more cost

effective than borrowing in local currency.

Guarantees/Standby Letters of Credit - The Benefits for the Importer

My customers provide me with greater credit and extended credit when I can get my

bank to issue guarantees in their favour.

Some of my suppliers provide me with performance and warranty guarantees which

cover the risk of non performance of the seller or poor quality of goods supplied.

I can comfortably and securely provide an advance payment to the supplier when I

receive an advance payment guarantee as if the supplier does not perform I can claim

the return of the advance payment on demand.

Guarantees generally cost a lot less than borrowing in local currency.

With one bank guarantee issued by my bank in favour of my regular suppliers I can do

many repeat transactions.

Guarantees are issued subject to international rules and while this is very good for me

it is also good for my supplier as we know the specific obligations of the banks

involved.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 26

Trade Finance Products> Trade Loans >

This section outlines how Trade Finance Loans ‘Trade Loans’ are used to finance international trade transactions.

This will be achieved by becoming familiar with:

A simple definition of Trade Loans

Examples of where trade finance loans are suitable for export and import business

The workflow for a Trade Loan or ‘how it works’?

Bank-to-Bank Trade Loans

The benefits

The term Trade Finance includes the traditional trade finance instruments covered in this section such as

Documentary Credits, Documentary Collections, Guarantees and Standby Letters of Credit but it also includes

Trade Finance Loans.

Trade Finance Loans are loans granted for the specific purpose of financing international trade transactions,

commonly known as cross border trade finance. These trade related loans are directly linked to the asset

conversion cycle or ‘trade cycle’ of the underlying goods being traded between the seller and the buyer.

Trade Finance Loans are typically denominated in the currency of the underlying transaction and can mean

reduced levels of Foreign Exchange Risk and also reductions in costs of financing.

Documentary Credits

A documentary letter of credit is an undertaking by a bank, on behalf of an importer

(buyer), to pay a certain amount of money to an exporter (seller) within a specified

period of time, provided that the exporter presents documents specified in the letter

of credit, which comply with the terms and conditions set out in the letter of credit.

Documentary Collections

Documentary collections are a service provided by a bank whereby the bank will use

its correspondent bank relationships as a network to collect the proceeds of export

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 27

shipments using the documentary collection product operating under internationally

accepted rules known as the URC 522.

Guarantees

A bank guarantee is an irrevocable undertaking issued by a bank on behalf of an

instructing party to another party that the bank will pay a sum of money against a

written demand for payment or against submission of a document (or documents)

stipulated in the guarantee document itself.

Standby Letters of Credit

A Standby Letter of Credit is a guarantee of payment issued by a bank on behalf of a

client that is used as "standby payment of last resort" should the client fail to fulfill a

contractual commitment with a third party.

Cross Border Trade Finance

This means that the finance provided is used for export, import or distribution trade

contracts where goods or services actually cross the border of at least one of the

countries involved.

Asset Conversion Cycle

The Asset Conversion Cycle represents the number of days it takes a company to

purchase raw materials, convert them into finished goods, sell the finished product to

a customer and receive payment from the customer/account debtor for the product,

goods or services.

Exchange Rate Risk

The Exchange Rate Risk is that one currency either depreciates or increases in value

with another currency over a period of time.

For example, if the currency expected for settlement of goods exported depreciates

this is an exchange rate risk that can result in an exchange rate loss as the currency

amount received will convert into a smaller amount of local currency.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 28

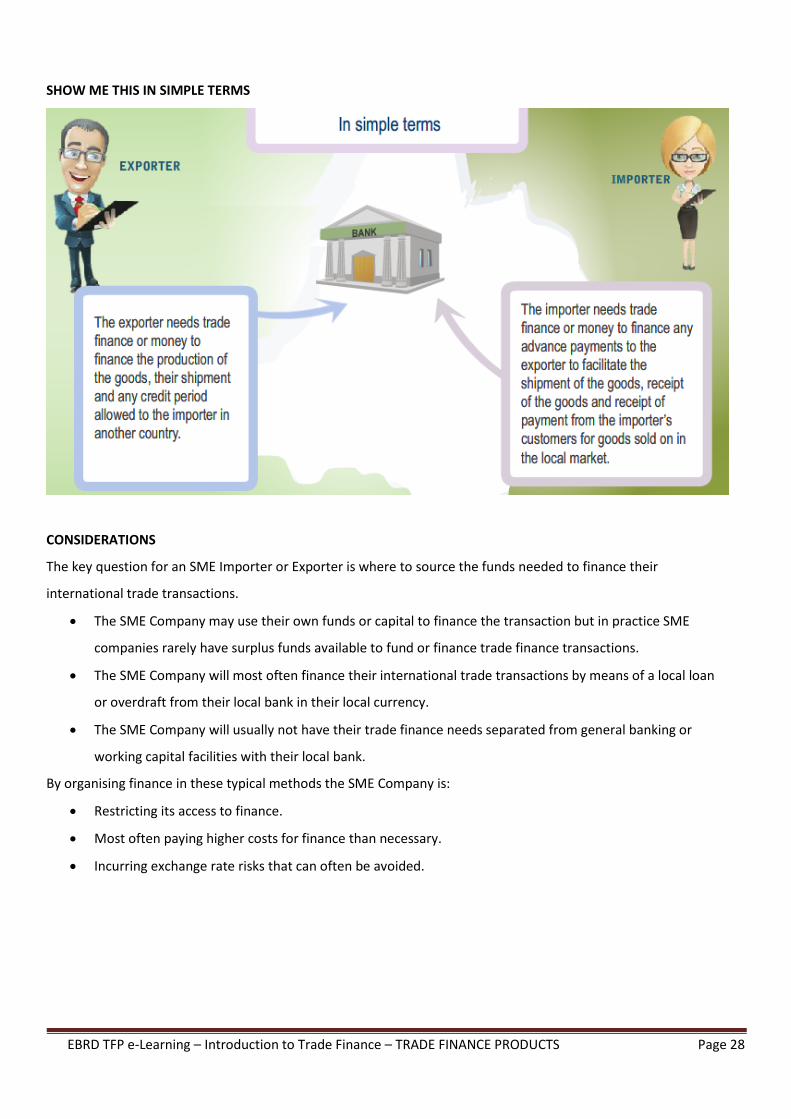

SHOW ME THIS IN SIMPLE TERMS

CONSIDERATIONS

The key question for an SME Importer or Exporter is where to source the funds needed to finance their

international trade transactions.

The SME Company may use their own funds or capital to finance the transaction but in practice SME

companies rarely have surplus funds available to fund or finance trade finance transactions.

The SME Company will most often finance their international trade transactions by means of a local loan

or overdraft from their local bank in their local currency.

The SME Company will usually not have their trade finance needs separated from general banking or

working capital facilities with their local bank.

By organising finance in these typical methods the SME Company is:

Restricting its access to finance.

Most often paying higher costs for finance than necessary.

Incurring exchange rate risks that can often be avoided.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 29

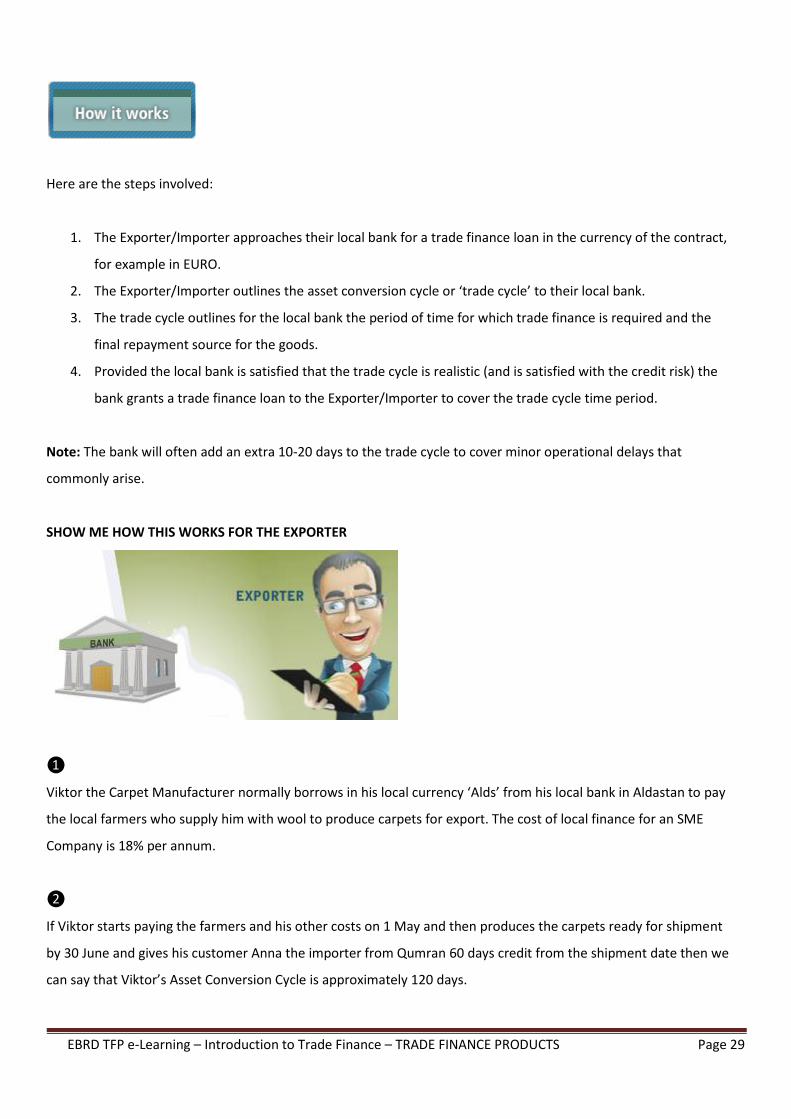

Here are the steps involved:

1. The Exporter/Importer approaches their local bank for a trade finance loan in the currency of the contract,

for example in EURO.

2. The Exporter/Importer outlines the asset conversion cycle or ‘trade cycle’ to their local bank.

3. The trade cycle outlines for the local bank the period of time for which trade finance is required and the

final repayment source for the goods.

4. Provided the local bank is satisfied that the trade cycle is realistic (and is satisfied with the credit risk) the

bank grants a trade finance loan to the Exporter/Importer to cover the trade cycle time period.

Note: The bank will often add an extra 10-20 days to the trade cycle to cover minor operational delays that

commonly arise.

SHOW ME HOW THIS WORKS FOR THE EXPORTER

❶

Viktor the Carpet Manufacturer normally borrows in his local currency ‘Alds’ from his local bank in Aldastan to pay

the local farmers who supply him with wool to produce carpets for export. The cost of local finance for an SME

Company is 18% per annum.

❷

If Viktor starts paying the farmers and his other costs on 1 May and then produces the carpets ready for shipment

by 30 June and gives his customer Anna the importer from Qumran 60 days credit from the shipment date then we

can say that Viktor’s Asset Conversion Cycle is approximately 120 days.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 30

❸

Viktor will incur an interest cost of 18% on the local currency for approximately 120 days or longer if there is a

delay receiving payment from Anna.

As Viktor has borrowed the money in local currency ‘Alds’ but exports to Anna in EURO he also carries an exchange

rate risk as the currency he is paying out is different from the currency he will receive in payment.

If the EURO depreciates before Anna’s payment into local currency ‘ALDS’ then Viktor will receive less local

currency than he expected. This will result in a local currency loss.

If on the other hand, the EURO appreciates then Viktor will receive more ‘ALDS’ than expected i.e. a local currency

gain.

Viktor needs to avoid foreign exchange risk and should know in advance:

• The date and currency of the anticipated payment

• The profit he can expect upon receipt of payment

Features

Viktor is borrowing in EURO so when the goods are exported and sold he will be paid in EURO so there is

no foreign exchange risk.

As Viktor is borrowing in EURO he may pay interest at 6% which is far cheaper than paying interest on his

local currency at 18%.

By clearly defining the asset conversion cycle Viktor is able to increase his access to finance by way of the

trade finance loan or ‘trade loan’.

Summary

By using a trade finance loan Viktor has:

Avoided the Foreign Exchange Risk

Obtained financing at a reduced cost

Gained access to financing that may not normally be available from his local bank for international trade

activities.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 31

SHOW ME HOW THIS WORKS FOR THE IMPORTER

❶

Anna, the Importer from Qumran, banks with her local bank and normally borrows in local currency ‘Qams’ at the

high local interest rate of 20% per annum. Anna needs to borrow money from her local bank to pay Viktor for the

supply of goods she wishes to import.

❷

If Anna pays Viktor on 2 April for the goods ordered and if the goods arrive at her import warehouse on 10 July and

it takes between 40-60 days to sell the goods locally market then we can say that Anna’s Asset Conversion Cycle is

approximately 160 days.

Consequences

Anna will incur interest costs of 20% on the amount of money borrowed from her local bank in the local currency

for approximately 160 days or longer if there is any delay in the delivery and sale of the goods in the local market.

As this transaction is clearly an international trade transaction then it makes sense to finance it with a trade

finance loan or ‘trade loan’ denominated in the currency of the international contract which is EURO.

Summary

By using a trade finance loan Anna has:

• Obtained financing cheaper than borrowing in her local currency

• Gained access to financing that may not normally be available from her local bank for international trade

activities.

However, in this instance there was a foreign exchange risk which should be taken into consideration.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 32

BANK TO BANK TRADE FINANCE LOANS

In the context of international trade banking, trade finance is generally considered to be lower risk than

conventional lending or working capital finance.

As a result international banks:

are often able to provide short term bank-to-bank trade finance loans on favourable terms to local banks

provided the loans are used to fund trade finance activities of customers of the local bank.

where the international bank will provide a trade finance loan or funding to a local bank and that local

bank will then on lend the funds to its customers for the purpose of financing international trade

transactions of their customers.

International banks providing bank-to-bank loans will also be concerned with the credit risk, the bank risk and the

country risk. The funding bank also needs to understand the underlying trade transaction and the applicable asset

conversion cycle in advance of providing funds for on-lending to the local customer.

It would also be common practice for international funding banks to occasionally check that the funds provided by

way of trade finance loan are actually being used to finance international trade activity which as we have seen has

a lower risk profile than conventional or working capital lending.

The Credit Risk (Counterparty Risk)

This is the risk of non-payment by the purchaser of goods or services. The risk of non-

payment is possibly greater in international trade than in domestic trade because the

exporter may not be able to accurately assess the creditworthiness of a customer

located in another country.

Bank Risk

Sometimes an exporter will insist that the importer’s bank guarantees the payment

for goods being shipped. Bank risk is the risk that the bank fails to honour such a

payment obligation. Such a payment obligation could be by way of a bank guarantee,

a documentary credit or a Standby LC.

Country Risk

Country risk arises when a foreign buyer is prevented from making payment due to:

exchange control regulations

other government restrictions

political uncertainty

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 33

or in extreme situations, such as the breakout of war

Asset Conversion Cycle

The Asset Conversion Cycle represents the number of days it takes a company to

purchase raw materials, convert them into finished goods, sell the finished product to

a customer and to receive payment from the customer/account debtor for the

product, goods or services.

EBRD TFP e-Learning – Introduction to Trade Finance – TRADE FINANCE PRODUCTS Page 34

Trade Loans - The Benefits for the Exporter

I can obtain greater levels of finance when I can demonstrate that the trade loan is

to finance my international trade activity.

The trade finance loan can be denominated in the currency of the international

contract of sale which can mean that I can achieve a reduction in the cost of

financing.

Provided the currency of the trade finance loan matches the currency in which I sell

my goods then foreign exchange risks can be avoided.

By understanding the asset conversion cycle and explaining it to my bank I can

obtain financing that will fluctuate in accordance with my trading operations and

match my financing needs.

The documentation for trade finance loans is not complicated so it is much easier to

provide for my bank.

Trade Loans - The Benefits for the Importer

By using trade finance loans I can obtain better terms from my suppliers as by paying

them in advance or early they will often give me a discount on the cost of the goods.

Trade finance loans can be packaged to match my asset conversion or ‘trade cycle’

which gives me greater flexibility in managing my trade finance needs.

By obtaining a trade finance loan in the international currency of my supplier I can

often get my financing at a much cheaper cost than financing in local currency.

Once my bank understands that the repayment source for the trade finance loan is

from the sale of the underlying goods for which there is demand I can achieve

greater levels of trade financing which will help me expand my business.

The documentation to be provided to the bank to organise trade finance loans is

comparatively simple and pretty much standardised.