towards a private–public synergy in financing climate change mitigation projects

TRANSCRIPT

Energy Policy 29 (2001) 1363–1378

Towards a private–public synergy in financing climatechange mitigation projects

ZhongXiang Zhanga,b,*, Aki Maruyamac

aFaculty of Law and Faculty of Economics, University of Groningen, P.O. Box 716, 9700 AS Groningen, The NetherlandsbCentre for Environment and Development, Chinese Academy of Social Sciences and China Centre for Regional Economic Research,

Peking University, Beijing, Chinac Institute for Global Environmental Strategies, 1560-39 Kamiyamaguchi, Hayama, Kanagawa 240-0198, Japan

Received 28 December 2000

Abstract

Funding for greenhouse gas mitigation projects in developing countries is crucial for addressing the global climate changeproblem. By examining current climate change-related financial mechanisms and their limitations, this paper indicates that theirroles are limited in affecting developing countries’ future emissions, and argues for the necessity of stronger private sector

engagement in financing mitigation projects. In this regard, the clean development mechanism (CDM), one of the flexibilitymechanisms incorporated into the Kyoto Protocol, could offer great potential in helping mobilize foreign direct investment towardsclimate mitigation, by providing commercial incentives for the private sector to invest in mitigation projects and internalizing

externalities associated with mitigation projects. However, due to additional risks and barriers involved in CDM projects, we believethat appropriate public–private linkage would be necessary in order to bring the CDM into full play. To this end, we suggest thatpublic funds could be used to complement private investment via the CDM, thus enhancing market functions of such an investment.Moreover, in so doing, we think that it would be necessary to examine a host of factors, such as risk sharing, private sector

investment behaviour, types of technologies to be transferred, and co-ordination with the commonly practiced trade and investmentrules. r 2001 Elsevier Science Ltd. All rights reserved.

Keywords: Clean development mechanism; Climate change; Foreign direct investment; Kyoto Protocol; Official development assistance

1. Introduction

In recent years, there has been growing concern aboutchanges in the global climate resulting from increasedatmospheric concentrations of the so-called greenhousegases (GHG) and the resulting socioeconomic impacts.Given the global characteristics of climate change, thispromotes the necessity of taking international co-operative efforts to reduce global GHG emissions.Given that GHG emissions in the Asian developingcountries are already high and are expected to growrapidly in line with their industrialization and urbaniza-tion, these countries will, in particular, require signifi-cant financial assistance from developed countries in

order to reduce their future GHG emissions. To date,assistance for climate change mitigation has beencoming mainly from public financing. Despite someefforts, little progress has been made in investments inthe so-called climate-friendly projects that generallyentail higher risks and initial costs than conventionalprojects. Under these circumstances, the introduction ofthe clean development mechanism (CDM) is expected tofacilitate private sector investments in GHG-reducing,climate-friendlier projects in developing countries. Nodoubt, the CDM as an innovative market mechanismwill provide the private sector’s investment incentives,thereby addressing externalities related to GHG reduc-tions. However, due to additional risks and barriersinvolved in CDM projects, appropriate public–privatelinkage would be necessary in order to bring the CDMinto full play. To this end, public funds could be used tocomplement private investment via the CDM byremoving barriers, reducing implementation costs and

*Corresponding author. Tel.: +31-50-363-6881; fax: +31-50-363-

7101.

E-mail addresses: [email protected] (Z. Zhang),

[email protected] (A. Maruyama).

0301-4215/01/$ - see front matter r 2001 Elsevier Science Ltd. All rights reserved.

PII: S 0 3 0 1 - 4 2 1 5 ( 0 1 ) 0 0 0 3 8 - 6

reducing long-term technology costs associated with theCDM projects, thus enhancing market functions of suchan investment.Against this background, this paper examines relevant

issues from a financial point of view, in order toconstruct wider, more efficient financial mechanismoptions for climate change mitigation projects. In sodoing, special attention is paid to the Asian region.Sections 2 and 3 first provide an overview of currentclimate change-related financial mechanisms and theirlimitations, arguing for the stronger private sectorinvolvement in climate mitigation. Sections 4 and 5then analyse the potential and barriers of the CDM as afinancial mechanism to facilitate private sector invest-ments in climate mitigation. Finally, Sections 6 and 7consider the complementary roles of public funds andprivate investments via the CDM, and point out some ofthe issues that need further consideration.

2. Current climate change-related financial mechanisms

Funding for GHG mitigation projects in developingcountries is crucial for addressing the global climatechange problem. It is important to recognise thatindustrialised countries are responsible for the majorityof both historical and current greenhouse gas emissionsand, thus, must demonstrate once and for all that theyare really taking the lead in reducing their emissions. Onthe other hand, in the light of expected rapid growth ofGHG emissions in developing countries, co-operationby developing countries is also essential. From theindustrialised countries’ perspective, the lack of devel-oping countries’ involvement in combating climatechange aggravates their short-term concerns aboutinternational competitiveness. Non-participation ofdeveloping countries also increases emissions leakagethat could arise in the short term, as emissions controlslower world fossil fuel prices, and in the long term, asindustries relocate to developing countries to avoidemissions controls at home. In addition, it raises thespectre of developing countries becoming ‘‘locked in’’ tomore fossil fuel intensive economy and eliminates theAnnex I countries’ opportunity to obtain low-costabatement options.To date, several steps have been taken to assist

developing countries in financing GHG mitigationrelated activities. Article 4 of the United NationsFramework Convention on Climate Change(UNFCCC) adopted in 1992 specifies some of thefunding needs of developing countries, and for thatpurpose, the Global Environment Facility (GEF) wasidentified as a financial mechanism of the Conventionon an interim basis. At the first Conference of theParties to the UNFCCC, the implementation of the pilotphase of activities implemented jointly (AIJ) up to the

year 2000 was endorsed in order to achieve emissionsreductions in a more cost-effective manner. Althoughthere is no crediting allowed from the AIJ, it is a co-operative mechanism between Annex I (developed) andnon-Annex I (developing) countries through whichdeveloped countries carry out mitigation projects indeveloping countries based on the approval of eachinvolved party. AIJ projects utilise funds additional tothe official development assistance (ODA) and contribu-tions to the GEF, aiming to mobilise resources from theprivate sector. Furthermore, the Kyoto Protocoladopted at the third Conference of the Parties to theUNFCCC in 1997 incorporates emissions trading, jointimplementation (JI) and the CDM to help Annex Icountries to meet their legally binding Kyoto emissionstargets at a lower overall cost. While many Annex Icountries have put and continue to put pressure ondeveloping countries to take on emissions limitationcommitments, the CDM so far is the only mechanismwith an authentic global reach. It aims to contribute tothe sustainable development of developing countrieswhile assisting Annex I countries in meeting theiremissions targets. Although the rules governing theCDM are unclear at this point, what has been agreed onis that CDM projects can generate the so-called certifiedemission reductions (CERs) from 2000 on, makingavailable a stock of CERs for Annex I countries to fulfilpart of their national GHG emission reduction require-ments for the first commitment period (2008–2012).With its main source of finance being expected tocome from the private sector, the CDM will havesignificant implications for future options for financialmechanisms aiming at GHG mitigation in developingcountries.In what follows, we will examine the status and size of

current climate change-related financial mechanisms,with special attention being paid to the Asian region.

2.1. Existing financial mechanisms

2.1.1. Global Environment FacilityWhile international agencies have vast experience of

development aid, none of them have previously ad-dressed the issues of funding projects aimed to secure aglobal benefit. Hence, the GEF1 was set up as a pilotUS$ 1.3 billion trust fund in 1991 to support developing

1The GEF is managed by 3 implementing agencies: United Nations

Development Programme (UNDP), United Nations Environment

Programme (UNEP) and the World Bank. Each implementing agency

contributes its particular expertise to GEF operations: the UNDP is

primarily responsible for implementing technical assistance and

capacity building programmes; the UNEP takes the lead in advancing

environmental management at regional and global levels within GEF-

financed activities and in catalysing scientific and technical analysis;

and the World Bank helps to develop and implement investment

projects and seeks to mobilize resources from the private sector.

Z. Zhang, A. Maruyama / Energy Policy 29 (2001) 1363–13781364

countries for projects and activities that protect theglobal environment and to promote sustainable devel-opment. It was restructured and replenished with overUS$ 2 billion from 34 countries in 1994 to support its 4focal areas: climate change, biodiversity, internationalwaters and conservation of the ozone layer. Anadditional US$ 2.75 billion was pledged in March1998, and its member countries now number 165. GEF’sfinancial assistance is to cover the difference (orincrement) between the costs of a project undertakenwith global environmental considerations and the costsof an alternative project that the country would haveimplemented under the normal circumstances. Duringthe period 1991–1998, the GEF has funded more than500 projects in 120 countries, with the total funding ofmore than US$ 2 billion. Co-finance for GEF projectsfrom other sources, public as well as private, exceedsUS$ 5 billion. Of these investments, the GEF hasallocated US$ 753 million to climate change-relatedprojects, accounting for 38% of the total number ofprojects, matched by more than US$ 4.3 billion in co-financing (GEF, 1999a). There are currently 4 Opera-tional Programmes2 in the climate change portfolio:removal of barriers3 to energy efficiency and energyconservation (OP#5); promoting the adoption of renew-able energy by removing barriers and reducing imple-

mentation costs (OP#6); reducing the long-term costs oflow GHG emitting energy technologies (OP#7); andpromoting environmentally sustainable transport(OP#11). The breakdown of finance allocation byprogramme is shown in Table 1, with Asia and thePacific accounting for 47% of the total funding. With itslimited resources, the GEF cannot significantly affectGHG emissions in the short term; rather, the GEFpromotes the development and use of technologies thatare critical for addressing the climate change problem inthe long term (Martinot, 2000).

2.1.2. Activities implemented jointlyThe first Conference of the Parties to the UNFCCC in

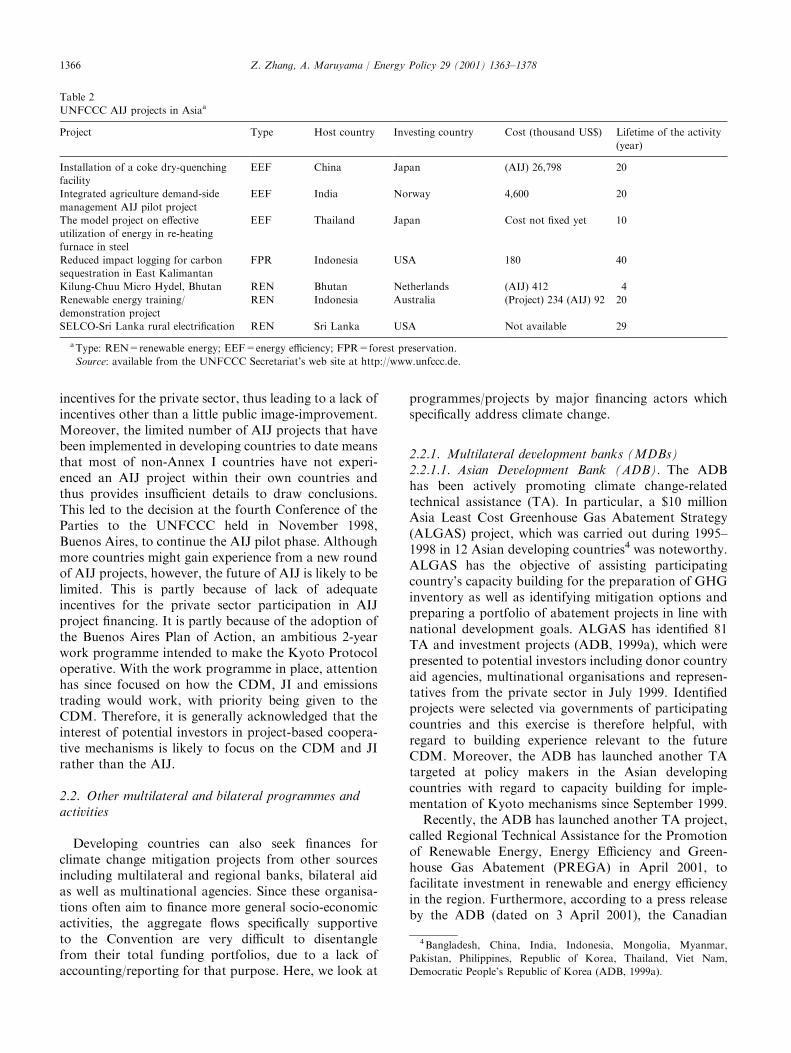

Berlin in April 1995 endorsed the AIJ as a pilotprogramme. During the AIJ pilot phase, emissionreductions achieved are not allowed to be credited tocurrent national commitments of investor countries.Currently, approximately 160 AIJ projects have beenestablished worldwide mainly in energy-related (energyefficiency improvement, fuel-switching, and renewableenergy), forest conservation and afforestation fields. Thecountries with economies in transition host most ofthese projects. As of July 1999, 7 projects wereimplemented in the Asian countries and reported tothe UNFCCC Secretariat. As shown in Table 2, thecosts of these projects vary significantly, depending onthe types and scale of a project. Because much of costinformation is either unclear or unavailable, it is thusvery difficult to derive the aggregated investment in allAIJ projects.The AIJ pilot phase aims at introducing private funds

and technologies. However, it is difficult to say that ithas played a significant role in leveraging private sectorfinance. This is because of factors such as the absence ofcredits as yet for emissions reductions, and the lackof international consensus on providing appropriate

Table 1

GEF financing in the climate change area and its flow to Asia and the Pacific, 1991–1998 (in million US$)a

Total 1991 1992 1993 1994 1995 1996 1997 1998 Total

OP#5 0.00 29.40 15.90 0.00 6.40 55.08 38.19 42.91 187.07

OP#6 40.30 49.00 14.60 0.00 6.90 62.80 46.48 60.23 280.31

OP#7 0.00 0.00 8.12 0.00 0.00 53.50 40.84 0.33 102.79

Enabling 0.00 16.00 6.90 0.00 19.49 5.43 8.85 11.67 68.34

Short-term 19.80 45.00 7.20 0.00 6.26 4.70 10.21 21.39 114.56

Total 60.10 139.40 51.91 0.00 39.05 181.51 144.58 136.53 753.08

Asia/Pacific

OP#5 0.00 16.50 0.00 0.00 1.00 32.80 22.00 17.16 89.46

OP#6 30.00 49.00 0.00 0.00 0.00 43.20 8.83 37.12 168.15

OP#7 0.00 0.00 0.00 0.00 0.00 49.75 0.00 0.00 49.75

Enabling 0.00 11.50 1.50 0.00 0.47 3.39 0.59 0.88 18.34

Short-term 10.00 10.00 0.00 0.00 6.26 0.00 0.00 9.19 29.19

Total 40.00 87.00 1.50 0.00 1.47 129.15 31.42 64.36 354.90

a Information on OP#11 is unavailable here because it became operational since 1999.

Source: Vaish (1999).

2Operational programmes, which consist of the majority of GEF

financial assistance, are conceptual and planning framework for

implementation of a set of projects. In addition, the GEF has other

financial assistance categories: enabling activities; short-term response

measures; project development facility; small grants programme (for

grants up to US$ 50,000); and medium-sized projects requiring no

more than US$ 1 million in GEF financing.3The barriers here refer to incremental expenditure for win–win

finance flows. These include regulatory barriers and biases, lack of

information, insufficient management capability, inability to analyse

non-traditional projects, higher perceived technology risk of the

alternative, high transaction costs, and high initial costs (GEF, 1996).

Z. Zhang, A. Maruyama / Energy Policy 29 (2001) 1363–1378 1365

incentives for the private sector, thus leading to a lack ofincentives other than a little public image-improvement.Moreover, the limited number of AIJ projects that havebeen implemented in developing countries to date meansthat most of non-Annex I countries have not experi-enced an AIJ project within their own countries andthus provides insufficient details to draw conclusions.This led to the decision at the fourth Conference of theParties to the UNFCCC held in November 1998,Buenos Aires, to continue the AIJ pilot phase. Althoughmore countries might gain experience from a new roundof AIJ projects, however, the future of AIJ is likely to belimited. This is partly because of lack of adequateincentives for the private sector participation in AIJproject financing. It is partly because of the adoption ofthe Buenos Aires Plan of Action, an ambitious 2-yearwork programme intended to make the Kyoto Protocoloperative. With the work programme in place, attentionhas since focused on how the CDM, JI and emissionstrading would work, with priority being given to theCDM. Therefore, it is generally acknowledged that theinterest of potential investors in project-based coopera-tive mechanisms is likely to focus on the CDM and JIrather than the AIJ.

2.2. Other multilateral and bilateral programmes andactivities

Developing countries can also seek finances forclimate change mitigation projects from other sourcesincluding multilateral and regional banks, bilateral aidas well as multinational agencies. Since these organisa-tions often aim to finance more general socio-economicactivities, the aggregate flows specifically supportiveto the Convention are very difficult to disentanglefrom their total funding portfolios, due to a lack ofaccounting/reporting for that purpose. Here, we look at

programmes/projects by major financing actors whichspecifically address climate change.

2.2.1. Multilateral development banks (MDBs)2.2.1.1. Asian Development Bank (ADB). The ADBhas been actively promoting climate change-relatedtechnical assistance (TA). In particular, a $10 millionAsia Least Cost Greenhouse Gas Abatement Strategy(ALGAS) project, which was carried out during 1995–1998 in 12 Asian developing countries4 was noteworthy.ALGAS has the objective of assisting participatingcountry’s capacity building for the preparation of GHGinventory as well as identifying mitigation options andpreparing a portfolio of abatement projects in line withnational development goals. ALGAS has identified 81TA and investment projects (ADB, 1999a), which werepresented to potential investors including donor countryaid agencies, multinational organisations and represen-tatives from the private sector in July 1999. Identifiedprojects were selected via governments of participatingcountries and this exercise is therefore helpful, withregard to building experience relevant to the futureCDM. Moreover, the ADB has launched another TAtargeted at policy makers in the Asian developingcountries with regard to capacity building for imple-mentation of Kyoto mechanisms since September 1999.Recently, the ADB has launched another TA project,

called Regional Technical Assistance for the Promotionof Renewable Energy, Energy Efficiency and Green-house Gas Abatement (PREGA) in April 2001, tofacilitate investment in renewable and energy efficiencyin the region. Furthermore, according to a press releaseby the ADB (dated on 3 April 2001), the Canadian

Table 2

UNFCCC AIJ projects in Asiaa

Project Type Host country Investing country Cost (thousand US$) Lifetime of the activity

(year)

Installation of a coke dry-quenching

facility

EEF China Japan (AIJ) 26,798 20

Integrated agriculture demand-side

management AIJ pilot project

EEF India Norway 4,600 20

The model project on effective

utilization of energy in re-heating

furnace in steel

EEF Thailand Japan Cost not fixed yet 10

Reduced impact logging for carbon

sequestration in East Kalimantan

FPR Indonesia USA 180 40

Kilung-Chuu Micro Hydel, Bhutan REN Bhutan Netherlands (AIJ) 412 4

Renewable energy training/

demonstration project

REN Indonesia Australia (Project) 234 (AIJ) 92 20

SELCO-Sri Lanka rural electrification REN Sri Lanka USA Not available 29

aType: REN=renewable energy; EEF=energy efficiency; FPR=forest preservation.

Source: available from the UNFCCC Secretariat’s web site at http://www.unfccc.de.

4Bangladesh, China, India, Indonesia, Mongolia, Myanmar,

Pakistan, Philippines, Republic of Korea, Thailand, Viet Nam,

Democratic People’s Republic of Korea (ADB, 1999a).

Z. Zhang, A. Maruyama / Energy Policy 29 (2001) 1363–13781366

Government has agreed to establish a fund on climatechange to reduce the growth of greenhouse gasemissions in the Asia and Pacific region. The CanadianCooperation Fund will have an initial Can$ 5 million(US$ 3.2 equivalent) and will be administered by theAsian Development Bank (ADB). This will be the firstCanadian trust fund at a multilateral development bankfrom which grants will be provided on an united basis.The fund will assist projects with potential access totreaty mechanisms, including the Global EnvironmentFacility and Clean Development Mechanism. It will alsosupport activities relating to carbon sequestration andadaptation to climate change. Grants from the fund willbe used for project preparation, training and advisoryservices, institutional support or other technical assis-tance services. Although all the ADB’s developingmembers are eligible for the fund, priority will be givento the People’s Republic of China and India to reducegreenhouse gas emissions; Indonesia for carbon seques-tration; and to the Pacific Islands for operations toadapt to climate change. The fund reflects Canada’s aimto contribute towards poverty reduction in the regionthrough policy dialogue and collaborative programmingwith the ADB supporting in managing climate change.

2.2.1.2. World Bank. The World Bank Group is alsopromoting a variety of climate change-related activities.Among them, the most important activities includeserving as one of the 3 implementing agencies of theGEF, involvement of some AIJ projects, and theestablishment of Prototype Carbon Fund (PCF) whichwill be closely related to the future CDM and jointimplementation.AIJ projects at the World Bank are carried out in

conjunction with other Bank Group investment projectswhich meet AIJ criteria of the UNFCCC. The conces-sional funding (the amounts available from a singledonor in the range of US$ 2–5 million) comes fromdonors who are interested in contributing to thedevelopment of AIJ. The Bank aims at identifying adiverse portfolio, providing finance and technologicalassistance and facilitating relevant research. Currently,there are 8 such AIJ projects (most of which receivefinancial contributions from the Norwegian govern-ment), with only one project (in India) being imple-mented in Asia.The PCF was endorsed by the Bank’s Executive

Directors on 20 July 1999 and launched on 18 January2000 as a pioneering model to catalyse a carbon marketin project-based emission reductions. It is a trust fundwith contributions from governments and private sectorparticipants.5 The PCF will invest in 15–20 GHG

mitigation projects in developing countries or incountries with economies in transition during the next3 years, with the primary focus on renewable energyprojects that would not be profitable without revenuesfrom emission reductions sold to the PCF, and will thendistribute its return to investors in the form of emissionsreduction certificates as per their pro rata investment inthe Fund. The size of the PCF is capped at US$ 150million. It is designed to be capable of being adjusted tooperate within the UNFCCC regulatory framework as itdevelops.

2.2.2. Bilateral aid programmesIn addition to AIJ projects, the OECD countries, such

as Germany, Japan, the UK, the US6 and Australia,have carried out projects which contribute to climatechange mitigation in the Asian developing countriesthrough respective bilateral aid programmes. The scopesand objectives of these programmes as well as theirbudgets vary greatly, ranging from a research project toa concessional financing and to building relativedemonstration facilities. In particular, Japan’s coopera-tion in this region is prominent in terms of financialassistance.First of all, main financial assistance in this area

by the Japanese government is through special‘‘environmental ODA’’. Such an assistance, which wasannounced in September 1997, applies specially lowerinterest rate (special environmental rate7) for loans to acategory of environmental projects designed to improvethe global environment including those for climatechange mitigation (e.g., forestry, energy conservation,new energy sources and public transportation) andanti-pollution measures. Special environmental projectsin fiscal year (FY) 1998 numbered 27, and the loanamount associated with these projects totals Yen277.3 billion on an agreement basis (record high),with all loans but one going to the Asian countries(in total Yen 272.2 billion) (OECF, 1999). Besides,although not a programme specifically aimed at addres-sing climate change in a strict sense, the Green AidPlanFa technical and financial assistance to pollutionand energy-related problem targeted at 6 Asiancountries8 provided by the NEDO/MITIFhas acomponent contributing to climate change mitigation.Under the Green Aid Plan, the MITI allocated above

5The required contributions for public sector and private sector

participants are US$ 10 million and US$5 million, respectively (World

Bank, 1999b).

6For instance, the US Country Studies Program has provided

technical and financial assistance to GHG inventory preparation and

vulnerability assessment of 56 developing and economies in transition

countries since 1992.7As of August 1999, the interest rate is 0.75% with 40 years of grace

period (which is the same terms used by the World Bank’s

International Development Association, the most preferential condi-

tions in the world; for middle-income countries the applied rate is

1.8% with 25 years of grace period).8China, India, Indonesia, Malaysia, Philippines, and Thailand.

Z. Zhang, A. Maruyama / Energy Policy 29 (2001) 1363–1378 1367

US$ 280 million between 1993 and 1997 for projectsaiming at the diffusion of energy conservation technol-ogies (Evance, 1999a). Furthermore, the MITI and theEnvironment Agency of Japan have been providing theJapanese entities with financial assistance for feasibilitystudies of potential JI and CDM projects to identifypotential projects and accumulate know-how andexpertises.

2.2.3. Activities by other regional/internationalorganisationsIn addition to the above efforts, several regional/

international organisations offer TA related to climatechange mitigation. They include capacity building,research and technical assistance activities by theUNEP, and the Asia–Pacific Climate Change Seminarfor policy makers organised jointly by the UnitedNations Economic and Social Commission for Asiaand the Pacific and the Environment Agency ofJapan. Being non-financial entities, the main activitiesof these organisations in the climate change arenaare not, in principle, related to investment but informa-tion dissemination and capacity building, the budgetand scope of which for this purpose vary from year toyear.

3. The limitations of conventional public finance

3.1. Problems with current options

Current financial mechanisms for climate changemitigation projects have several problems. For example,problems associated with GEF funding include: thelimited funding sources available for achieving theultimate objective of the Convention and for transfer-ring the necessary environmentally sound technologiesto developing countries; a typically lengthy process ofproject identification and approval for funding; con-sultant-driven project identification that risks leading toprojects which do not take regional or country needsinto consideration (Porther et al., 1998; TERI, 1998;ECON, 1997).Moreover, unequal geographical distributions of

project implementation and non-existence of financialassistance mechanisms for adaptation for countries/regions particularly vulnerable to climate change are thetwo major issues that require special consideration.Difficulties involved in taking concrete and efficient co-operative measures at national, regional and interna-tional levels because of uncertainty with the outcomes ofthe future international negotiations are a majorobstacle to strengthening the supporting efforts. Asmentioned earlier, multilateral development banks aswell as bilateral aid agencies carry out some activitiesrelated to climate change mitigation. However, it is

difficult for them to strengthen their efforts or prescribeparticular policies at this point when rules andmodalities of the Kyoto mechanisms are yet to bedecided. Thus, early formation of international con-sensus is essential for strengthening necessary support-ing measures.

3.2. Necessity of private investment

Generally speaking, investments in climate-friendlierprojects are difficult, due to the higher initial costs, risksand externality of GHG reductions. Thus, theUNFCCC looked to the GEF to fill the cost gap(incremental cost) in order to leverage private funds.However, as reviewed in a GEF overall performancestudy, there has been comparatively little mobilisationof capital from private financial institutions (GEF,1998). The private sector’s involvement has been limitedto providing procured equipment and services oradvisory capacity. The GEF attributes the causes ofthis obvious obstacle to such factors as the privatesector’s low awareness of the GEF, a lengthy approvalprocess, private sector’s fear for the disclosure ofvaluable business information, and vague tangiblebenefits resulting from a partnership with the GEF(GEF, 1999b).However, the limited involvement of the private

sector at this moment does not prevent huge privateflows from going to climate-relevant conventionalprojects in developing countries in the future, providedthat favourable investment conditions are created.Given the fact that the role of financial assistance (fromthe GEF or ODA) for mitigation projects is limited inaffecting future GHG emissions, it has been recognisedthat the mobilisation of private sector investment is thekey to achieve global GHG emissions reductions,particularly in developing countries.

3.2.1. Size and the importance of the foreign directinvestment (FDI)A five consecutive year fall in the ODA ended with

rise to US$ 51.5 billion in 1998, while the net privateflows to developing countries fell drastically to approxi-mately US$ 200 billion,9 due to loss of confidence inemerging markets triggered by the recent financial crisisthat led to the withdrawal of short-term bank flows andportfolio investments (DAC, 1999; World Bank, 1999a).Still, private flows to developing countries are runningat 3–5 times the size of the ODA. The FDI has beenmore resilient than other forms of private capital flowsin the face of the financial crisis, because it is motivatedlargely by the investors’ long-term prospects for making

9According to the DAC statistics, the net private flows from OECD

countries in 1998 were US$181 billion, of which the FDI amounted to

US$110 billion.

Z. Zhang, A. Maruyama / Energy Policy 29 (2001) 1363–13781368

profits in production activities that they directly control.By contrast, foreign bank lending and portfolio invest-ment are not invested in activities controlled by banks orportfolio investors, which are often motivated by short-term profit considerations. These differences are high-lighted, for instance, by their investment patterns in theAsian countries stricken by financial turmoil in 1997.FDI flows in 1997 to the five most affected countriesremained positive in all cases and declined only slightlyfor the group, whereas bank lending and portfolioequity investment flows declined sharply and eventurned negative in 1997 (Mallampally and Sauvant,1999).Developing countries are becoming increasingly

attractive destinations for investment, accounting fortwo-thirds of the increase in global FDI flows from thelate 1980s to the 1990s. The FDI is likely to remain thedominant source of long-term finance for developingcountries in the foreseeable future (World Bank, 1999a).The majority of the US$ 96 billion net long-term flow tothe East Asian region in 1998 was dominated by theFDI of US$ 61 billion, while official flows were US$ 19billion (IMF credit not included) (World Bank, 1999a).Not only can the FDI add to investible resources andcapital formation, but, perhaps more importantly, it isalso a means of transferring advanced technologies tolocal industry, and introducing institutional frameworksof the market economy, such as industrial organisations,contractual concepts, transaction know-how, financialsystems, and labour markets, as well as of accessinginternational marketing networks. In this respect, theFDI is potentially a strong vehicle to activate developingeconomies (Ohono, 1996). Furthermore, even when theODA or other public funds are available for mitigationprojects, project replication and sustainability oftendepend on creating conditions for similar investments bythe private sector (GEF, 1999b). In this respect, green-ing the FDI in climate relevant sectors, such as energysector, is essential for climate change mitigation.

3.2.2. Private sector investment in the electricity sectorElectricity generation, a primary cause of climate

change, is one of the leading infrastructure sectors in

attracting private investment. According to Izaguire(1998), the private sector took on the management,operation, rehabilitation or construction risk of 534projects, with total investments of US$131 billionbetween 1990 and 1997. Of these, the East Asian andthe Pacific countries won 165 contracts, representing atotal investment of about US$50 billion (see Table 3).Independent power producer (IPP) projects account fornearly 60% of all new private generation capacityfinanced in the developing world, and the East Asiancountries show a pronounced trend towards introducingprivate participation in this form.Among the contracts brought to fruition during 1990–

1997, large green field IPPs (exceeding 100MW)comprised 137 projects worth US$ 65 billion, of whichthe IPPs mobilised US$ 51 billion in private funds(Babber and Schuster, 1998). On the other hand, loansto the energy sector (electricity generation and gasprojects) provided by MDBs or bilateral credit agenciesactive in the Asian region (namely, the ADB, theWorld Bank, and the Japan Bank for InternationalCooperationFthe latter created from a merger of theOverseas Economic Co-operation Fund (OECF) andExport–Import Bank of Japan (JEXIM)) totalledapproximately US$ 6 billion in 1998 (see Fig. 1).Although these financial institutions provide loans onconcessional terms, the basic principle of evaluating the

Table 3

Private electricity projects in developing countries by region, 1990–

1997a

Region Projects Total investment

with private

participation

(million US$)

East Asia and the Pacific 165 49,741

Europe and Central Asia 112 10,436

Latin America and the Caribbean 169 45,311

Middle East and North Africa 10 6,721

South Asia 57 16,799

Sub-Saharan Africa 21 2,040

Total 534 131,048

aSource: Izaguirre (1998).

Fig. 1. Loans to energy sector in 1998. Note: measured in million US$ at the exchange rate 1 US$=Yen 130.89. Sources: ADB (1999b); OECF

(1999); World Bank (1999c); Dengen Chiiki Shinko Center (1999).

Z. Zhang, A. Maruyama / Energy Policy 29 (2001) 1363–1378 1369

project economics based on loan repayment is the sameas that of commercial banks. Without relevant environ-mental regulation in place, and with subsidized energyprices, promoting climate-friendlier investments that arenot internalised in economic appraisals of the projects iseven more difficult in developing countries than indeveloped countries. Thus, the cost gap for considera-tion of GHG emissions reductions has been addressedby using public funds with more preferential terms, suchas GEF funds or Japan’s special ‘‘environmental ODA’’.However, as the sizes of these funds show clearly, theimpact of this type of support has been limited inleveraging private investments.From the preceding discussion, it thus follows that

current financial flows for mitigation projects in the Asiandeveloping countries are a tiny part of relatively smallofficial flows. The trend toward privatisation of state-owned electric utilities means that decisions about thecarbon intensity of power plants will be made on the basisof economic criteria. Given that the private sectorinvestments in climate-related areas will shape the futureof developing countries’ economic growth and environ-ment, such as those in the energy sector, our task is to findways to direct private flows to investments that contributeto both economic growth and climate change mitigation.

3.3. Barriers to climate-friendly investments in developingcountries

What risks and barriers are associated with climatechange mitigation projects in developing countries, inaddition to those of conventional projects? Table 4

shows risks and barriers from the point of view offinanciers/investors, according to project type (i.e., thoseassociated with conventional projects (left column),climate change mitigation projects (middle column),and CDM projects (right column)). As shown inTable 4, projects in the area of climate changemitigation have additional barriers/risks on top of thoseassociated with conventional projects in developingcountries. These include risks related to technologies(performance risks of unconventional technology itself),management (risks associated with the use of unfamiliartechnologies) as well as country risks related to domesticregulatory and economic aspects (regulation on invest-ment and import of climate-friendly technologies, anduncertainty over energy pricing and subsidy schemes).Furthermore, there are risks of non-conventional alter-native project itself, such as uncertain rates of return,incapability of analysing non-conventional projects,higher initial investment cost, or small project size andimplicit transaction costs (GEF, 1996; EIC, 1999;APEC, 1998).In order to attract more private investments in

climate-friendlier projects, it is important to create atransparent and stable market where investors haverealistic expectations of future returns. To this end,developing country governments should strive forreduction of investment risks and introduction of policymeasures to promote mitigation technology transfer. Inparallel, new financial mechanisms and measures toaddress incentives and risks of private investors will benecessary. In this connection, the CDM could offer greatpotential in directing the FDI to climate-friendlier

Table 4

Risks associated with mitigation/CDM projects in project financea

Conventional projects Mitigation projects CDM projects

Project performance (completion, operational) Increased risks due to Ratification of the Kyoto Protocol

Technology Non-conventional project Rules and design of the CDM design

Sponsor Non-conventional technology

Insecurity of energy source

Amount of CERs (baseline, leakage, eligibility)

Management Cost-effectiveness (high transaction cost,

adaptation fee)

Force majeure (natural disasters, etc.) Uncertainties associated with the market

(price, behaviour)

Market (quantity, price) Delivery of CERs

Country Institutional arrangement for CDM

Regulatory (underdeveloped regulatory

system in assets and finance)

Unfavourable regulation on investment

and import of climate friendly technologies

Political (war, nationalisation) Energy pricing/low conventional energy price

Economic (foreign exchange, currency

transfer, local financing, creditworthiness of

local partner

and clients)

Social and institutional High initial costs

Uncertain (usually low) rate of return

Small project size and implicit transaction costs

aSources: adapted from Ohara (1996); APEC (1998); GEF (1996); Mundy (1999); Maruyama (1999).

Z. Zhang, A. Maruyama / Energy Policy 29 (2001) 1363–13781370

investments by providing market-based incentives andinternalising externalities associated with mitigationprojects.

4. The potential of the CDM

4.1. Significance of the CDM as an innovative financialmechanism

The flexibility mechanisms incorporated into theKyoto Protocol provide the prospect of GHG emissionreductions (surplus to the compliance needs) beingtreated as a commodity with monetary value. Likeenvironmental taxes, the Kyoto mechanisms are inno-vative financial tools which internalise externalities.They could send price signals to the market andfacilitate energy-related cost savings and cost recoveryof climate-friendly investments, thereby reducing someof the barriers associated with financing of mitigationprojects. Although the details of CDM are as yetunclear, by carrying out mitigation projects in develop-ing countries the mechanism has the potential to helpdeveloped countries to meet their national emissionsreduction targets cost effectively, while contributing tosustainable development in developing countries.Although the ultimate responsibility for fulfilling thenational reductions commitments rests with eachgovernment, the Kyoto mechanisms open the door forparticipation by private entities.Therefore, provided that appropriate domestic mea-

sures provide the private sector incentives for invest-ments (such as, the introduction of domestic emissionstrading systems, early reductions rewarding schemes,voluntary reduction agreements, regulations, or taxbreaks, etc.), the CDM could offer cost-effectiveabatement options and new business opportunities. Inaddition, the sale of the credits generated from theCDM projects (namely, the CERs) offers the prospect ofrecovering the high investment cost associated withclimate-friendly investments, thereby reducing some ofthe barriers associated with financing mitigation pro-jects. Besides, there could potentially be a variety offlexible-financing tools, ranging from conventional FDIor project finance to mutual funds similar to the PCFadvanced by the World Bank. Furthermore, the CDMwould allow each country to take region- and country-specific institutional elements into consideration, de-pending on their project-screening ability. In otherwords, given proper identification of potential CDMprojects by developing country governments, CDMflows could provide a substantial source of income,which can bring co-benefits, addressing not only GHGmitigation, but also other social development goals,such as local and regional environmental problems,

rural development, poverty alleviation, and employmentgeneration, etc.

4.2. Potential size of the CDM market

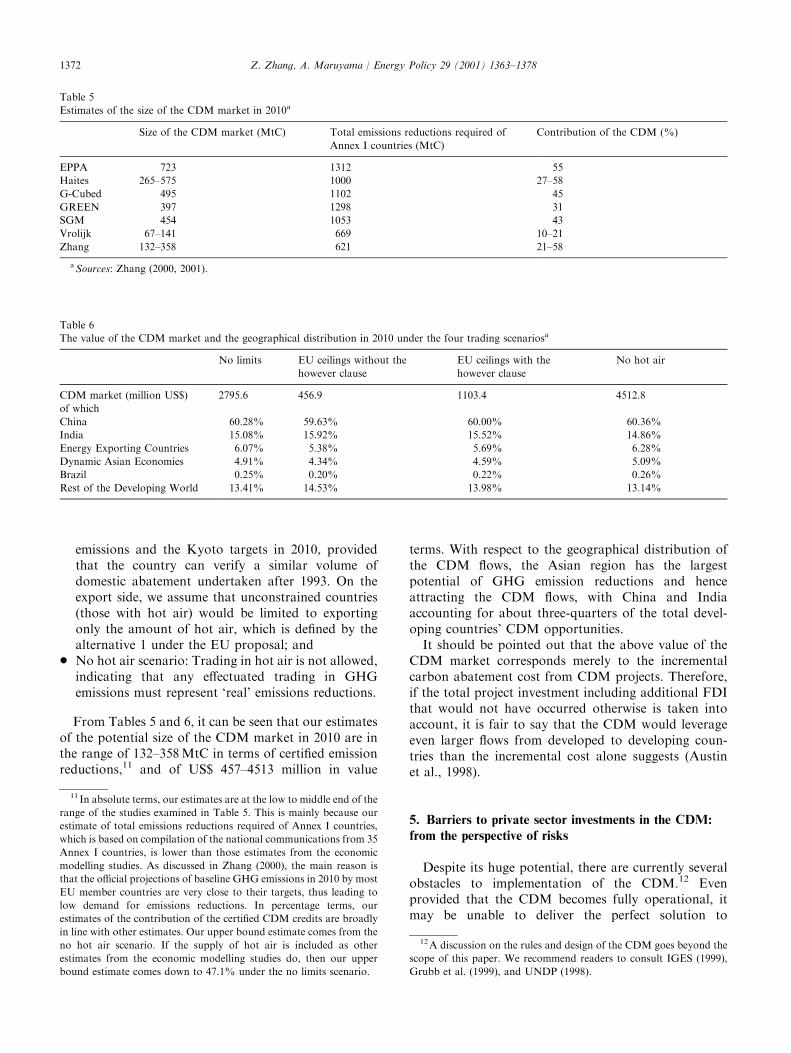

Estimates of the potential of CDM market (see Table5) are very sensitive to the rules governing the CDM andother flexibility mechanisms. Assuming the contribu-tions from domestic abatement actions and hot air anddividing the remaining demand between emissionstrading and JI among Annex I countries and theCDM within non-Annex I countries in proportion tothe estimated potential of supply, Haites (1998) esti-mates that the size of the CDM market in 2010 rangesfrom 265 million tons of carbon (MtC) under the 50%reduction from business as usual (BAU) emissionsscenario to 575MtC under the no limits scenario. Thesize of the market estimated by the four economicmodelling studies examined ranges from 397MtC withthe OECD GREEN model (Van der Mensbrugghe,1998) to 723MtC with the EPPA model (Ellerman andDecaux, 1998). Austin et al. (1998) argue that suchestimates derived from these global modelling exercisestend to overestimate CDM flows because, in practice,political limitations and transaction costs will probablykeep CDM activities at the lower end of such estimates.Based on the national communications from 35

Annex I countries and using the global model basedon the marginal abatement costs of 12 regions, Zhang(2000, 2001) have estimated the contributions of threeflexibility mechanisms to meet the total emissionsreductions required of Annex I countries under fouralternative trading scenarios

* No limits scenario: No caps are imposed on the use ofall three flexibility mechanisms so that one Annex Icountry can trade as much as it wished until itbecomes more costly for the country to trade than toabate domestically;

* The EU ceilings without the however clause scenario:At the June 1999 Sessions of the Subsidiary Bodies ofthe UNFCCC, the European Union (EU) has putforward a proposal for concrete ceilings on the use offlexibility mechanisms (European Union, 1999).10

The EU proposal calls for the limits on bothimporting countries and exporting countries. Thisscenario follows the EU proposal without consider-ing the however clause;

* The EU ceilings with the however clause scenario:For an importing country, the above EU ceilings arerelaxed to the extent that the maximum acquisitionsfrom all three flexibility mechanisms are allowed upto 50% of the difference between projected baseline

10See Zhang (2001) for a detailed discussion on the EU proposal for

concrete ceilings.

Z. Zhang, A. Maruyama / Energy Policy 29 (2001) 1363–1378 1371

emissions and the Kyoto targets in 2010, providedthat the country can verify a similar volume ofdomestic abatement undertaken after 1993. On theexport side, we assume that unconstrained countries(those with hot air) would be limited to exportingonly the amount of hot air, which is defined by thealternative 1 under the EU proposal; and

* No hot air scenario: Trading in hot air is not allowed,indicating that any effectuated trading in GHGemissions must represent ‘real’ emissions reductions.

From Tables 5 and 6, it can be seen that our estimatesof the potential size of the CDM market in 2010 are inthe range of 132–358MtC in terms of certified emissionreductions,11 and of US$ 457–4513 million in value

terms. With respect to the geographical distribution ofthe CDM flows, the Asian region has the largestpotential of GHG emission reductions and henceattracting the CDM flows, with China and Indiaaccounting for about three-quarters of the total devel-oping countries’ CDM opportunities.It should be pointed out that the above value of the

CDM market corresponds merely to the incrementalcarbon abatement cost from CDM projects. Therefore,if the total project investment including additional FDIthat would not have occurred otherwise is taken intoaccount, it is fair to say that the CDM would leverageeven larger flows from developed to developing coun-tries than the incremental cost alone suggests (Austinet al., 1998).

5. Barriers to private sector investments in the CDM:

from the perspective of risks

Despite its huge potential, there are currently severalobstacles to implementation of the CDM.12 Evenprovided that the CDM becomes fully operational, itmay be unable to deliver the perfect solution to

Table 5

Estimates of the size of the CDM market in 2010a

Size of the CDM market (MtC) Total emissions reductions required of

Annex I countries (MtC)

Contribution of the CDM (%)

EPPA 723 1312 55

Haites 265–575 1000 27–58

G-Cubed 495 1102 45

GREEN 397 1298 31

SGM 454 1053 43

Vrolijk 67–141 669 10–21

Zhang 132–358 621 21–58

aSources: Zhang (2000, 2001).

Table 6

The value of the CDM market and the geographical distribution in 2010 under the four trading scenariosa

No limits EU ceilings without the

however clause

EU ceilings with the

however clause

No hot air

CDM market (million US$)

of which

2795.6 456.9 1103.4 4512.8

China 60.28% 59.63% 60.00% 60.36%

India 15.08% 15.92% 15.52% 14.86%

Energy Exporting Countries 6.07% 5.38% 5.69% 6.28%

Dynamic Asian Economies 4.91% 4.34% 4.59% 5.09%

Brazil 0.25% 0.20% 0.22% 0.26%

Rest of the Developing World 13.41% 14.53% 13.98% 13.14%

11In absolute terms, our estimates are at the low to middle end of the

range of the studies examined in Table 5. This is mainly because our

estimate of total emissions reductions required of Annex I countries,

which is based on compilation of the national communications from 35

Annex I countries, is lower than those estimates from the economic

modelling studies. As discussed in Zhang (2000), the main reason is

that the official projections of baseline GHG emissions in 2010 by most

EU member countries are very close to their targets, thus leading to

low demand for emissions reductions. In percentage terms, our

estimates of the contribution of the certified CDM credits are broadly

in line with other estimates. Our upper bound estimate comes from the

no hot air scenario. If the supply of hot air is included as other

estimates from the economic modelling studies do, then our upper

bound estimate comes down to 47.1% under the no limits scenario.

12A discussion on the rules and design of the CDM goes beyond the

scope of this paper. We recommend readers to consult IGES (1999),

Grubb et al. (1999), and UNDP (1998).

Z. Zhang, A. Maruyama / Energy Policy 29 (2001) 1363–13781372

financing mitigation projects. Although the CDM couldhelp to leverage relevant FDI towards climate-friendlierinvestments, the CERs to be generated from the CDMmay be just one of the elements in a project negotiation.To illustrate this point, Table 4 summarises various riskfactors from the financiers/investors’ point of view.As discussed in Section 3.2.2, climate-friendlier

mitigation projects have financing barriers in terms ofrisks and costs. In addition to those barriers, CDMprojects have their own risks and barriers. These include(see right column of Table 4): possible disadvantagesover other Kyoto mechanisms arising from the design ofthe CDM that could affect cost-effectiveness and theamount of CERs to be generated, uncertainty over theratification of the Kyoto Protocol; and uncertaintyassociated with the CDM market in terms of priceand behaviour. There are also risks associated withthe delivery of CERs. Institutional arrangements for theCDM by different host governments could be anotherconcern. Thus, CERs could remain just one of thekey factors in a project negotiation. Therefore, inensuring project-level viability of risk management,considerable attention needs to be paid to developingappropriate public–private sector linkages to mobiliseadditional private sector’s financial sources (Mundy,1999).

6. Public–private synergy in financing climate mitigation

projectsFtowards construction of efficient financialmechanism options

From the preceding discussion, it thus follows thatinvestments in climate mitigation projects should makethe best use of private flows to the extent possible,complementing them with public funds. In this regard,utilisation of the CDM, complemented by publicfinance, could be an ideal model to facilitate privatesector investments in mitigation projects. In this regard,at least the following, interrelated issues need to beaddressed in considering a better framework for overallfinancial mechanism options.

6.1. Financial additionality and the use of public funds

Article 12 of the Kyoto Protocol does not stipulatethe so-called ‘financial additionality’Fi.e., the financialresources of the CDM as additional to existing ODAand GEF funds, although it does refer to additionalityof emissions reductions (meaning that resulting emis-sions reductions must be additional to those that wouldhave occurred in the absence of the CDM projects).13

Whether projects are financially additional could be

important because financial additionality,14 togetherwith environmental additionality, might determinewhether projects are eligible for the CERs under theCDM. Closely related to this, a controversy exists overthe use of the ODA, due to the fact that the ‘financialadditionality’ was a condition attached to the AIJ, anddeveloping countries’ concern about a possible shift ofcurrent ODA funds towards climate change mitigation,which is not a high priority on their current develop-ment agenda. The ODA is differentiated from otherpublic funding on concessional terms according to the‘grant element’ as defined by the Development Assis-tance Committee of the OECD. Without explicitdefinition of the term, it is unclear whether the so-called‘financial additionality’ refers only to the ODA andGEF funds, or to the use of public funds in general toensure that CDM funding comes entirely from privateinvestments.As discussed earlier, the use of public funds could be

essential for mitigating country risks associated withconventional projects in developing countries, let aloneCDM projects. As far as CDM projects that requirelarge investments are concerned, they are likely toinvolve some public sector financing that includes theODA for project development, project financing,country risk insurance or other purposes. Moreover,expected high transaction costs associated with CDMprojectsFi.e., those related to project identification,host government approval, project validation, baselinecalculation, monitoring and verification etc.Fcouldoutweigh benefits from CERs particularly from small-scale renewable energy projects. With its more prefer-ential terms of concessionality, the ODA could broadenthe scope of possible CDM projects, improving eco-nomic viability and addressing externalities moreflexibly. Without appropriate private–public partner-ships to ensure project level risk management, there is adanger of significant flows going into conventionalprojects. Therefore, at least financial additionalityshould be interpreted in such a way to allow thecomplementary use of public finance including theODA. On the other hand, acquiring the CERs fromthe use of the ODA to complement private finance in aCDM project is another issue, requiring furtherconsideration. In this regard, the EU takes the stancethat the ODA should not necessarily be excluded fromCDM projects, but should not be used to acquire theCERs. The EU suggests that the part of the CERsequivalent to the portion of ODA funding in theprojects could be used to reinvest in the same projectsor in any case used for other development purposes (EC,

13See Baumert (1999) for a variety of interpretations of financial

additionality.

14The debate about additionality is further complicated by another

derived concept of ‘investment addtionality’ which supposedly means

that only those projects which are uneconomic in the absence of CERs

are eligible for the CDM.

Z. Zhang, A. Maruyama / Energy Policy 29 (2001) 1363–1378 1373

1999). This principle seems appropriate in light of thespirit of the ODA that aims at helping the developmentof developing countries. However, it cannot be deniedthat countries like Japan, whose ODA activitieshistorically show a strong presence in the field of socialinfrastructures including energy and environment, couldface difficulties because of the budgetary constraints.This suggests that further careful discussions on the useof public funds including ODA would be necessary inorder to reflect real investment practices, while main-taining environmental integrity.

6.2. Public–private complementary roles in project riskmitigation

Risk mitigation measures for conventional projects inthe setting of project finance include contractualagreements, financial design of the project, and insur-ance and guarantees provided both by the private andpublic financial institutions (see left column of Table 7).In considering possible future supporting measures toaddress risks specific to investments in mitigationprojects or those of the CDM, it would be effective toexamine and categorise various types of risks. We

distinguish those best covered by multilateral/regionalbanks by reinforcing existing risk coverage measures,those best addressed by development of new financialproducts developed by the private financial institutions,or those to be covered by government guarantees orbilateral export credits. Table 7 summarises possible riskcoverage measures for mitigation/CDM projects.

6.3. Private–public complementary roles: otherconsiderations

In considering the use of public fund to complementprivate investment in mitigation project, attention needsto be paid to using public funds to address the issuesthat private investment could not address via the CDM.These issues include the transfer of technology, thecreation of an enabling investment environment, theregional balance of future CDM project, and technicalinnovation.

6.3.1. Technology transfer entailing high transaction costIn order to introduce private funds and technologies,

domestic policy measures to provide the private sectorincentives and financial mechanisms for technology

Table 7

Risk mitigation measures for mitigation/CDM projects

Conventional projects Mitigation projects CDM projects

Contract GEF grant Cost recovery through CER

Completion ODA Reduction of transaction costs through CDM

design

Turnkey rump-sum EPC Other bilateral/multilateral programmes Withholding offsets as buffer and insurance to

address CERs delivery risk

Price CDM

Capacity payment and energy payment GEF non-grant financinga Price hedge (forward sale, portfolio)

Long-term purchase Contingent grants/performance grants Reinforcement of risk coverage measures by

MDBs

Take or pay/take and pay contract Contingent or concessional loan Mutual Fund

Performance and operational Partial risk or credit guarantees Reinsurance

Warranties, etc. Reserve fund, etc.

Financial design

Cash flow control, reserve fund, deferred

payment, offshore escrow account, cash

deficiency support, floor price escalation, etc.

Insurance

Property, business Interruption, liability, etc.

Country risk mitigation

Co-financing, guarantees, insurance by export

credit agencies, governmental institutions,

MDBs(e.g., WB, MIGA, IFC, ADB)

Host government guarantees

Domestic policy and measures to reduce barriers/risks in developing countries

aGEF non-grant financing is a new scheme currently being examined at GEF (EIC, 1999).

Sources: adapted from Ohara (1996); APEC (1998); GEF (1996); Mundy (1999), Maruyama (1999).

Z. Zhang, A. Maruyama / Energy Policy 29 (2001) 1363–13781374

transfer should match the kind of technologies to betransferred and corporate investment behaviour. Forexample, Forsyth (1999) categorises technologytransfers into vertical (point-to-point relocation oftechnology by foreign investors) or horizontal (sharingtechnology with local producers) according to owner-ship of a technology, and further classifies by presenceor absence of competition between domestic andinternational producers (see Table 8). He argues thatthe state of art technologies that fall into Category2 are likely to attract most investment and their transfermay be accelerated if the CDM is used to encouragethis type of investment, even though the ownership ofthe technology remains in the foreign investor’s hands.15

On the other hand, the technology transfer currentlydiscussed in the climate change negotiations, whichrepresents horizontal transfer of Category 4, is unlikelyto attract much investment, because of extra costsrequired in sharing technologies and setting upjoint ventures and transfer of intellectual propertyrights. In this category, therefore, public funds mightfind the best scope for value-added. Public fundsincluding financial assistance by the GEF or the ODAcould be used to cover the high transaction costsassociated with this type of technology transfer. Theycan also be used to diffuse the state of the arttechnologies already transferred (vertically) by theCDM to local industry.In current practice, there seem to be broadly two ways

of providing grants to support technology transfer: oneis providing funds to construct demonstration facilities;the other is to cover the license feeFthough the latter isa very rare case (there is an example in the GEF OP#5:China industrial boiler project where it covered licensefee to obtain energy efficient industry boilers fromdeveloped countries). However, companies usuallyprefer demonstration facilities as a reference case to

enter into a new market, thus putting them at anadvantageous position in international competitivebidding (Evance, 1999b). Therefore, technology trans-fers that require setting up a joint venture, license forsharing technologies or a process of training would bedifficult and costly for private companies, withoutfinancial support from public sources. Thus, it isnecessary to take the types of technologies to betransferred and investment behaviour into account inexamining financial mechanisms and policies to provideincentives for the private sector.

6.3.2. Creation of an enabling environment for privatesector investmentsCreating an enabling environment for private sector

investments is also an area where public funds showclear advantage over private flows. Efforts in this areamay include helping to establish regulatory and institu-tional capacity of developing countries to regulate,identify, assess, validate and implement CDM projectsas well as to foster education and relevant informationdissemination. Funding feasibility studies for the identi-fication of potential CDM projects, similar to theapproach taken by the Japanese government, ormaintenance of a project’s surrounding environment,would be another effective means to facilitate privatesector investments (Maruyama, 1999).

6.3.3. Regional balanceBy the time (30 June 1998) of the UNFCCC’s second

synthesis report on the AIJ, 95 projects were listed asAIJ projects (UNFCCC, 1998). These projects arelocated in 24 host countries, with Africa hosting onlyone certified AIJ project. AIJ experiences (Dixon, 1999)suggest the possibility of an inequitable distribution offuture CDM projects. This would be a serious problemfor regions such as Africa that are already facingdifficulties in attracting private flows, by virtue of thefact that they are less industrially developed and havefewer emissions reductions potential. Projects in regionswith poor infrastructure for private investment areaccompanied by higher risks, and are difficult to attractprivate partners for GHG reduction business opportu-nities. Thus, it is important for such regions to put in

Table 8

Different investment niches for technology transfera

Expertise and economic base in technology

exist locally

Expertise and economic base in technology

do not exist locally

Vertical technology transfer (ownership

remains with investor)

1: associated with high competition and low

profit margins

2: most attractive to new foreign investor

Horizontal technology transfer (ownership

is shared with local producers)

3: least attractive to new foreign investor 4: associated with high transaction costs and

potential loss of competitiveness

aSource: Forsyth (1999).

15 In this case, although host countries could not share technologies,

encouraging this type of investment is still in the interest of host

countries because it generates benefits, such as employment opportu-

nities, job training and accumulation of knowledge. However there is a

need for domestic/international measures so that the CDM could not

damage competing industries in developing countries by rewarding the

growth in market shares (Forsyth,1999).

Z. Zhang, A. Maruyama / Energy Policy 29 (2001) 1363–1378 1375

place as soon as possible national mechanisms toidentify, monitor, verify, and certify investments inemissions reductions. In order to foster their participa-tion in the CDM, it is also helpful that CDM projects inthe least developed countries (LDCs) should be exemptfrom the share of proceeds for adaptation, and thatsmaller LDCs could bundle together their smallerprojects to attract finance. Moreover, public fundscould be used to cope with regional imbalances, forinstance, by creating a fund dedicated to implementa-tion of GHG reduction projects in a particular region.

6.3.4. Technological innovationAnother area where public finance has a comparative

advantage is support for RaD of GHG reductiontechnologies in developed countries and implementationof demonstration projects. Support in this area wouldnot only promote innovation of GHG reductiontechnologies needed to make more stringent futureemissions targets affordable, but also contribute indir-ectly to future technology transfer of these technologiesvia the CDM.

7. Conclusion

It has been recognised that the role of currentfinancial mechanism options for climate mitigationprojects in developing countries is limited in addressingrisks and externalities of required climate-friendlytechnology transfers to developing countries and affect-ing these countries’ future GHG emissions. Given thehuge potential of climate-related private flows todeveloping countries, this promotes the necessity ofshifting the focus of current climate-related financialmechanisms from technology transfer and financingfrom the public sector to mobilising resources from theprivate sector in order to achieve the UNFCCC’sultimate objective of stabilising GHG concentrationsin the atmosphere at a level that would preventdangerous anthropogenic interference with the climatesystem.In this regard, the CDM as an innovative financial

mechanism would offer great potential in helping directFDI in relevant sectors towards climate mitigation, byproviding commercial incentives for the private sector toinvest in climate mitigation projects and therebyfacilitating internalisation of externality of climate-friendlier investment. However, due to additional risksand barriers involved in CDM projects, appropriatepublic–private linkage would be necessary in order tobring the CDM into full play. To this end, public fundscould be used to complement private investment via theCDM by establishing regulatory and institutionalcapacity of host developing countries, removing barriersto CDM investors, reducing implementation costs and

reducing long-term technology costs associated with theCDM projects, thus enhancing market functions of suchan investment. In so doing, relevant parties shouldexamine a host of factors, such as private sectorinvestment behaviour, risk sharing, types of technolo-gies to be transferred to developing countries, and otherareas where the private sector is difficult to address.Past experience shows that the involvement of public

funds is often confronted with the dangers of bureau-cracy and abuse of power in a lengthy process of projectidentification and approval for funding. Whether thelimited public funds for addressing the climate changeproblem can avoid the dangers needs to be tested.Besides, careful consideration should be given to suchissues as the relationship between the public financialsupporting measures and the OECD investment rules16

and the rules of the World Trade Organisation. From along-term perspective, climate concerns could be in-corporated as one of the important factors in formulat-ing industrialised countries’ aid strategies. At the sametime, it is perhaps more important for developingcountry governments to strive for eliminating invest-ment risks and introducing policy measures aimed topromote climate-friendlier technology transfer andenergy sector reforms.Finally, it should be pointed out that, at the time of

this paper going to the press, the ratification of theKyoto Protocol faces considerable uncertainty, duelargely to the recent political development in the UnitedStates where Bush administration in April 2001expressed that it will not support the Kyoto Protocol.Although the analysis of the complex political situationsis beyond the scope of the paper, some experts arguethat as long as the climate change problem is real,CDM-like mechanisms for technology/funds transfer todeveloping countries could be realised, even without theKyoto Protocol, for instance, under the UNFCCC itself,or through other channels. The Dutch government’srecent announcement on the closure of the first five JIcontracts under the ERUPT scheme17 can be regardedas an example of such a view. Currently, there are also

16 In particular, the Helsinki package agreed by the OECD countries

in 1991 which bans the use of aid and tied export credit together in

financing projects in developing countries, with the exception of

commercially non-viable projects.17On 17 April 2001, the Dutch Minister of Economic Affairs, Mrs.

Jorritsma, signed the first contracts relating to joint implementation.

With these contracts, the Netherlands buys reductions in emissions of

greenhouse gases realised by investing in Central and Eastern Europe.

The purchases involve a sum of NLG 79 million (EUR 35.3 million),

including the procurement of more than 4 million tons of reductions in

CO2 emissions in 5 years. These reductions will take place at the

following sites: a 60 Megawatt wind-power park in Poland; a hydro-

power plant in Romania; a series of biomass-fuelled boilers in the

Czech Republic; and two urban heating projects in Romania (see The

Hague-based Senter International’s press release on 17 April 2001,

‘‘Jorritsma buys Kyoto reductions in Central and Eastern Europe’’).

Z. Zhang, A. Maruyama / Energy Policy 29 (2001) 1363–13781376

active discussions on the possible ratification scenariowithout the US. In this regard, the resumed sixthConference of the Parties to the UNFCCC in July 2001is considered to be of a paramount importance forseeking to put the CDM in operation as well as for theKyoto process itself.

Acknowledgements

This paper was presented at the International Work-shop on Enhancing GHG Mitigation through Interna-tional Cooperative Mechanisms in Asia, Kanagawa,Japan, 26–27 January 2000. The authors would like tothank participants in the above workshop and ananonymous referee for useful discussions and commentson an earlier version of the paper. The views expressedhere are those of the authors, and do not necessarilyreflect the positions of the organisation with which theauthors are affiliated.

References

ADB, 1999a. Asia least greenhouse gas abatement strategy summary

report. Asian Development Bank, Manila.

ADB, 1999b. Asian Development Bank Annual Report 1998. Asian

Development Bank, Manila.

APEC, 1998. Asia–Pacific Economic Co-operation Guidebook for

Financing New and Renewable Energy Projects. Prepared by

Sustainable Energy Solutions, APEC Energy Working Group,

Asia–Pacific Economic Co-operation (APEC). New Energy and

Industrial Technology Development Organization (NEDO), To-

kyo.

Austin, D., Faeth, P., da Motta, R.S., Young, C.E.F., Ferraz, C.,

Zou, J., Li, J., Pathak, M., Srivastava, L., 1998. Opportunities for

financing sustainable development via the CDM: a discussion

draft. Paper presented at a Side-Event of the Fourth Conference of

the Parties to the UNFCCC, Buenos Aires, November 7.

Babber, S., Schuster, J., 1998. Power project finance: experience in

developing countries. Resource Mobilization and Cofinancing

Discussion Paper 119, The World Bank, Washington, DC.

Baumert, K., 1999. Understanding additionality. In: Goldemberg, J.,

Reid, W. (Eds.), Promoting Development while Slowing Green-

house Gas Emissions Growth. United Nations Development

Programme, New York, pp. 135–145.

DAC, 1999. Financial flows to developing countries in 1998. News

release, Development Assistance Committee (DAC), OECD, Paris.

Dengen Chiiki Shinko Center, 1999. Heisei jyunendo ni okeru chikyu

kankyo e no taio to denryoku ni kansuru chosakenkyu hokokusho

(report of research on the response to global environmental

problems and electricity in fiscal year 1998). Center for Develop-

ment of Power Supply Regions, Tokyo.

Dixon, R.K. (Ed.), 1999. The UN Framework Convention on Climate

Change Activities Implemented Jointly Pilot: Experiences and

Lessons Learned. Kluwer Academic Publishers, Dordrecht/Bos-

ton/London.

EC, 1999. Preparing for implementation of the Kyoto Protocol.

Commission communication to the Council and the Parliament,

COM(1999)230, European Commission (EC), Brussels.

ECON, 1997. Domestic climate regimes and incentives for private

sector involvement in JI. ECON-Report 15/97, Oslo.

EIC, 1999. Non-grant mechanism for GEF climate change

projects. Econergy International Corporation (EIC), Washington,

DC.

Ellerman, A.D., Decaux, A., 1998. Analysis of post-Kyoto CO2

emissions trading using marginal abatement curves. MIT Joint

Program on the Science and Policy of Global Change, Report No.

40, Massachusetts Institute of Technology.

European Union, 1999. Community strategy on climate change:

Council conclusions. No. 8346/99, Brussels.

Evance, P., 1999a. Japan’s green aid plan: the limits of state-led

technology transfer. Asian Survey 39 (6), 825–844.

Evance, P., 1999b. Cleaner coal combustion in China: role of

international aid and export credits for energy development and

environmental protection 1988–1997. Centre for International

Studies, Massachusetts Institute of Technology.

Forsyth, T., 1999. International Investment and Climate Change:

Energy Technology for Developing Countries. Earthscan, London.

GEF, 1996. Operational strategy of the GEF. Global Environment

Facility, Washington, DC.

GEF, 1998. Operational report on GEF programs. Global Environ-

ment Facility, Washington, DC.

GEF, 1999a. Introduction to the GEF. Global Environment Facility,

Washington, DC.

GEF, 1999b. Engaging the private sector in GEF activities. GEF/C.13/

Inf.5, Global Environment Facility, Washington, DC.

Grubb, M., Vrolijk, C., Brack, D., 1999. The Kyoto Protocol: A Guide

and Assessment. Earthscan, London.

Haites, E., 1998. Estimate of the potential market for cooperative

mechanisms 2010. Margaree Consultants Inc., Toronto.

IGES, 1999. Issues and options in the design of the clean development

mechanism. Institute for Global Environmental Strategies (IGES),

Kanagawa, Japan.

Izaguire, A., 1998. Private participation in the electricity sector: recent

trends. Viewpoint Note No.154, Finance, Private Sector and

Infrastructure Network, The World Bank, Washington, DC.

Mallampally, P., Sauvant, K.P., 1999. Foreign direct investment

in developing countries. Finance and Development 36 (1),

34–37.

Martinot, E., 2000. GEF climate change projects in Asia. Global

Environment Facility, Washington, DC.

Maruyama, A., 1999. Potential and constraints of private sector

participation in the clean development mechanism. Paper presented

at the UNESCAP Regional Seminar on Promotion of Energy

Efficiency in Industry and Financing of Related Public and Private

Investments, Bangkok, 30 November–2 December.

Mundy, J., 1999. Managing the risk in Kyoto projects. Environmental

Finance 1 (2), 23–26.

OECF, 1999. OECF annual report fy 1998. Overseas Economic

Cooperation Fund (OECF), Tokyo.

Ohara, K., 1996. Project finance. Kinyu Zaisei Jijyo Kenkyukai,

Tokyo.

Ohono, K., 1996. Shijyouiko-senryaku (strategies for market transi-

tion). Yuhikaku, Japan.

Porther, G., Clemencon, R., Ofosu-Amaah, W., Philips, M., 1998.

Study of GEF’s overall performance. Global Environment Facility,

Washington, DC.

TERI, 1998. Climate change post-Kyoto perspectives from the South.

Tata Energy Research Institute (TERI), New Delhi.

UNDP, 1998. Issuesa Options: The Clean Development Mechanism.

United Nations Development Programme (UNDP), New York.

UNFCCC, 1998. Review of the implementation of commitments and

of other provisions of the Convention. activities implemented

jointly: review of progress under the pilot phase (Decision 5/CP.1).

Second Synthesis Report on Activities Implemented Jointly,

United Nations Framework Convention on Climate Change

(UNFCCC), FCCC/CP/1998/2, Bonn.

Z. Zhang, A. Maruyama / Energy Policy 29 (2001) 1363–1378 1377

Vaish, A., 1999. Support by Global Environment Facility

in addressing climate change. Paper presented at the 9th

Asia–Pacific Climate Change Seminar, Hikone, Shiga, Japan,

13 June.

Van der Mensbrugghe, D., 1998. A (preliminary) analysis of the Kyoto

Protocol: using the OECD GREEN model. Paper presented at the

OECD Workshop on the Economic Modelling of Climate Change,

Paris, September 17–18.

World Bank, 1999a. Global Development Finance 1999: Analysis and

Summary. Washington, DC.

World Bank, 1999b. Information document on the prototype carbon

fund. Washington, DC.

World Bank, 1999c. The World Bank Annual Report 1999.

Washington, DC.

Zhang, Z., 2000. Estimating the size of the potential market for the

Kyoto flexibility mechanisms. Weltwirtschaftliches ArchivFRe-

view of World Economics 136 (3), 491–521.

Zhang, Z., 2001. An assessment of the EU proposal for ceilings on the

use of Kyoto flexibility mechanisms. Ecological Economics

37 (1), 53–69

Z. Zhang, A. Maruyama / Energy Policy 29 (2001) 1363–13781378