top ten trends and disruptors in digital beauty

TRANSCRIPT

TOP TEN TRENDS AND DISRUPTORS IN DIGITAL BEAUTY

Make Up in ParisJune 10, 2016

The knowledge bank for the Fung GroupConsultancy for clients within and outside of the Fung GroupFocuses on emerging retail and tech trendsEstablished in 2014. London office established in 2015Based in New York, London and Hong Kong20+ analysts specializing in retail and technologyPublishes thematic and global market research on topics such as the Internet of Things, digital payments, omnichannel retail, luxury and fashion trends and disruptive technologies.

ABOUT FUNG GLOBAL RETAIL & TECHNOLOGY

FUNGTHINKTANK

RETAILTECH

MICRO MACRO

RETAIL REAL

ESTATE

THEMATIC RESEARCH

VR

AI

IOT

DIGITALDIGITALDIGITALDIGITAL

HONG KONG NEW YORK LONDON

3

Fung Global Retail & Technology publishes research, freely available on www.fbicgroup.com, and soon on www.fgrt.com We advise retailers, real estate developers and tech companies on projects situated at the intersection of retail, tech and/or fashion.Our team offers a robust knowledge bank and significant experience in the retail, fashion and tech fields.

A UNIQUE COMBINATION OF RETAIL, FASHION AND TECH

OUR EXPERTISE

FASHION TECHRETAIL

10 DISRUPTORS, THREE THEMES

1. Online: • Primarily about research. 2. Stores: • Experience is all.3. E-Commerce opportunities: • Subscription, luxury and grocery.

THEME 1: ONLINE

• Online is disproportionately about research and browsing.

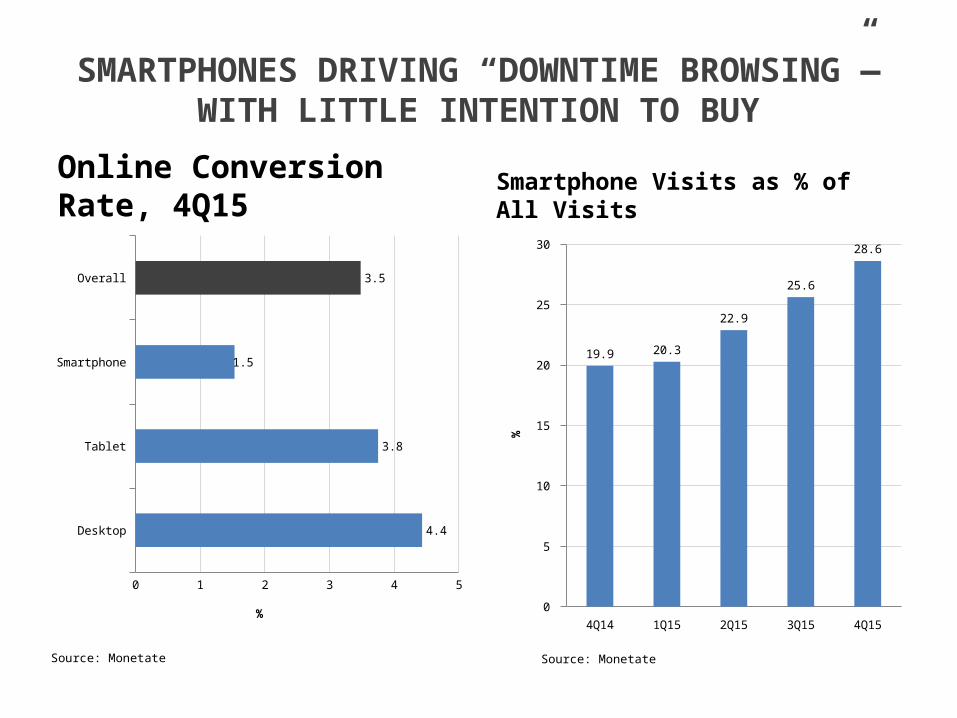

• Smartphones have made it more than ever about browsing: lower conversion rates, because of “downtime browsing” with little or no intention to buy.

SMARTPHONES DRIVING “DOWNTIME BROWSING”—WITH LITTLE INTENTION TO BUY

Online Conversion Rate, 4Q15 Smartphone Visits as % of All Visits

Desktop

Tablet

Smartphone

Overall

0 1 2 3 4 5

4.4

3.8

1.5

3.5

%4Q14 1Q15 2Q15 3Q15 4Q15

0

5

10

15

20

25

30

19.9 20.3

22.9

25.6

28.6

%

Source: Monetate Source: Monetate

Demand for an information-rich experience fulfilled by apps

offering “scientific” advice and social media offering human

recommendations.

INFORMATION-RICH ONLINE EXPERIENCE

1. The App as a Beauty Tool: Facial Mapping

• Virtual makeovers and try-ons• Factual, scientific, algorithm-driven advice• ModiFace, a Toronto-based company with a background in building 2-D

and 3-D facial simulations, offers multiple apps• Sephora Pocket Contour: facial contour analysis • L’Oréal Makeup Genius: magic mirror-type experience

1

INFORMATION-RICH ONLINE EXPERIENCE

1. The App as a Beauty Tool: Color Matching Goes High-Tech

• Sephora + Pantone = Color IQ• IMAN Cosmetics determines a user’s

“color signature” after taking a headshot • ShadeScout matches the Pantone shade

of colors from photos

1

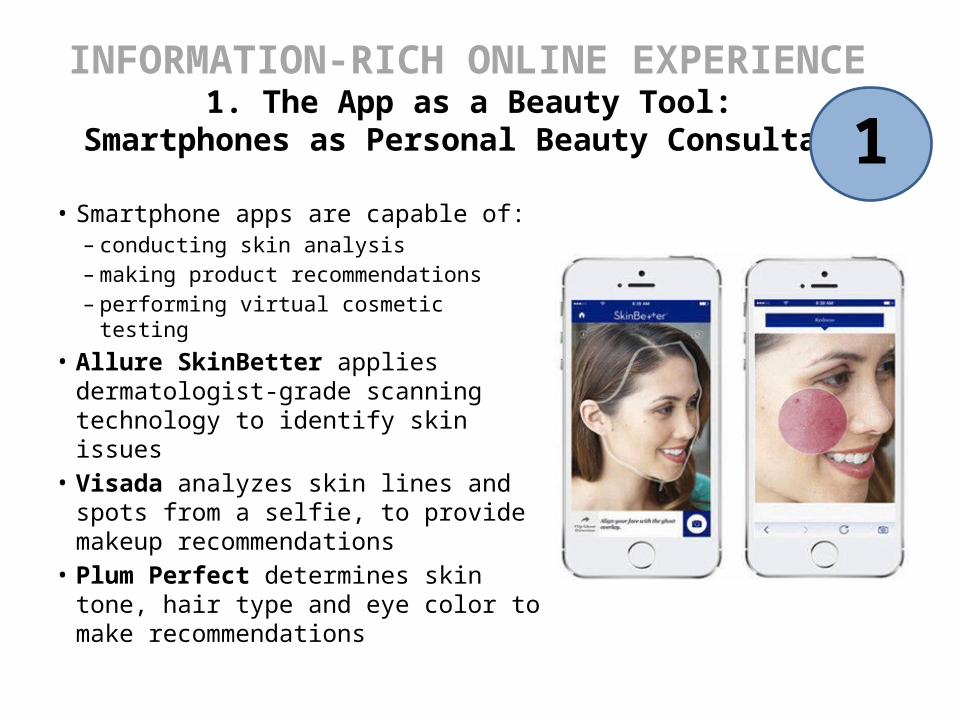

INFORMATION-RICH ONLINE EXPERIENCE 1. The App as a Beauty Tool:

Smartphones as Personal Beauty Consultants

• Smartphone apps are capable of:– conducting skin analysis– making product recommendations– performing virtual cosmetic testing

• Allure SkinBetter applies dermatologist-grade scanning technology to identify skin issues

• Visada analyzes skin lines and spots from a selfie, to provide makeup recommendations

• Plum Perfect determines skin tone, hair type and eye color to make recommendations

1

INFORMATION-RICH ONLINE EXPERIENCE

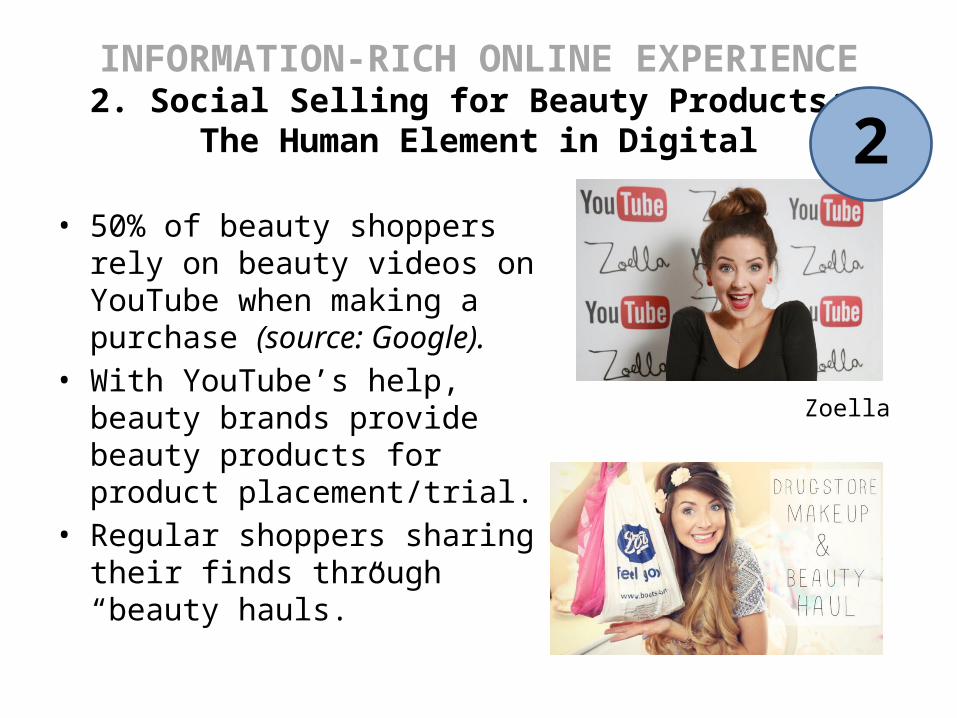

2. Social Selling for Beauty Products: The Human Element in Digital

• 50% of beauty shoppers rely on beauty videos on YouTube when making a purchase (source: Google).

• With YouTube’s help, beauty brands provide beauty products for product placement/trial.

• Regular shoppers sharing their finds through “beauty hauls.”

Zoella

2

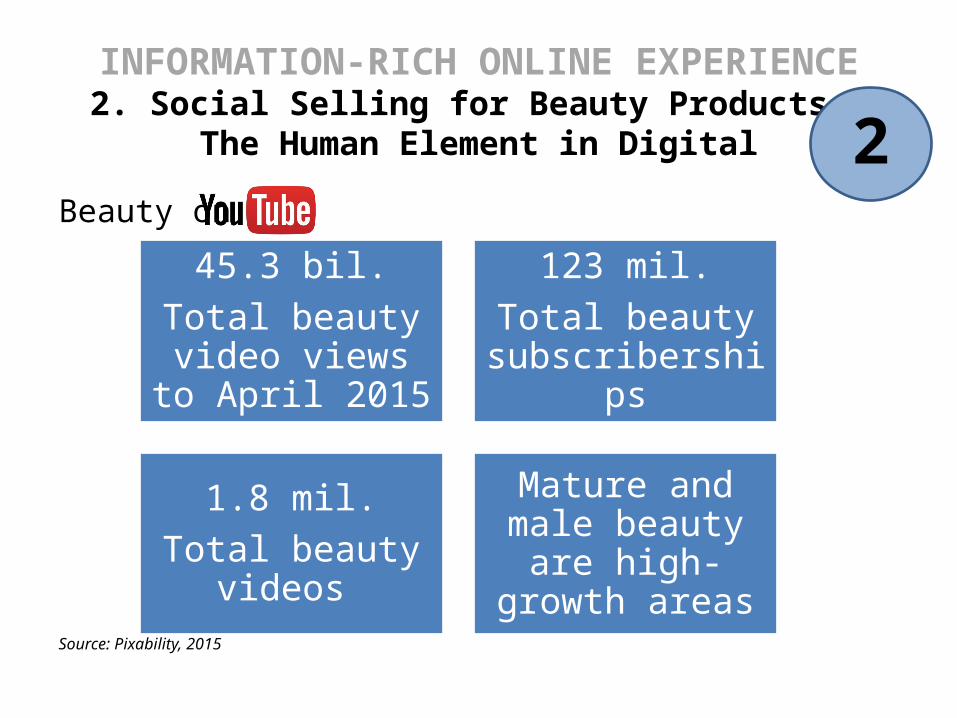

INFORMATION-RICH ONLINE EXPERIENCE

2. Social Selling for Beauty Products: The Human Element in Digital

Beauty on

Source: Pixability, 2015

2

45.3 bil.Total beauty video views to April 2015

123 mil.Total beauty

subscriberships

1.8 mil.Total beauty videos

Mature and male beauty are high-

growth areas

INFORMATION-RICH ONLINE EXPERIENCE

2. Social Selling for Beauty Products: The Human Element in Digital

Beauty brands on YouTube:• 215 beauty brands present on YouTube.• 2.1 billion brand-owned beauty video views…out of 45.3 billion total beauty video

views.• So brand-owned videos have <5% share of beauty video views.• Top-viewed branded beauty channels range from Chanel to Dove to Dior to

Sephora: massmarket and luxury.• 2016: L’Oreal launches “authentic” unbranded content-sharing site, Fab Beauty. • 2016: L’Oreal and YouTube launching an online vlogging school.

Source: Pixability/Company reports

2

THEME 2: STORES• In-store retail is more than ever about experience.• Particularly essential for beauty categories, where

tangibility can be essential. • But shoppers want experience on their terms: some

16% of US consumers decide to shop where sales associates will leave them alone until sought out for help (Mintel, 2015).

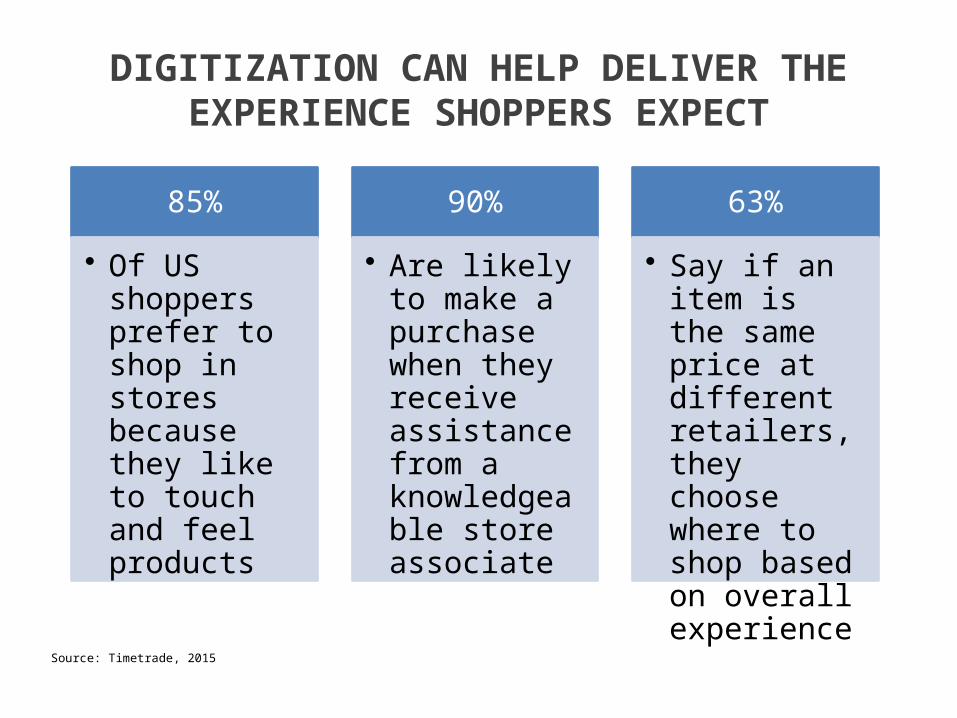

85%

• Of US shoppers prefer to shop in stores because they like to touch and feel products

90%

• Are likely to make a purchase when they receive assistance from a knowledgeable store associate

63%

• Say if an item is the same price at different retailers, they choose where to shop based on overall experience

DIGITIZATION CAN HELP DELIVER THE EXPERIENCE SHOPPERS EXPECT

Source: Timetrade, 2015

In-store tech can play a role in enhancing the experience,

offering service, and bringing the information consumers are

used to getting online, into stores.

EXPERIENCE IS EVERYTHING3. Digital Stores

• Sephora Flash ultra-connected boutiques. First is at 66, Rue de Rivoli in Paris.• An edited selection of products, alongside a digital catalog of more than 14,000

products from 150 brands.• Perfume testers with an NFC (Near Field Communication) tag provide shoppers with a

multitude of information on the fragrance by simply placing the tester on the connected screen.

• NFC-reactive screens can bring some of the information consumers are used to getting online into the store.

3

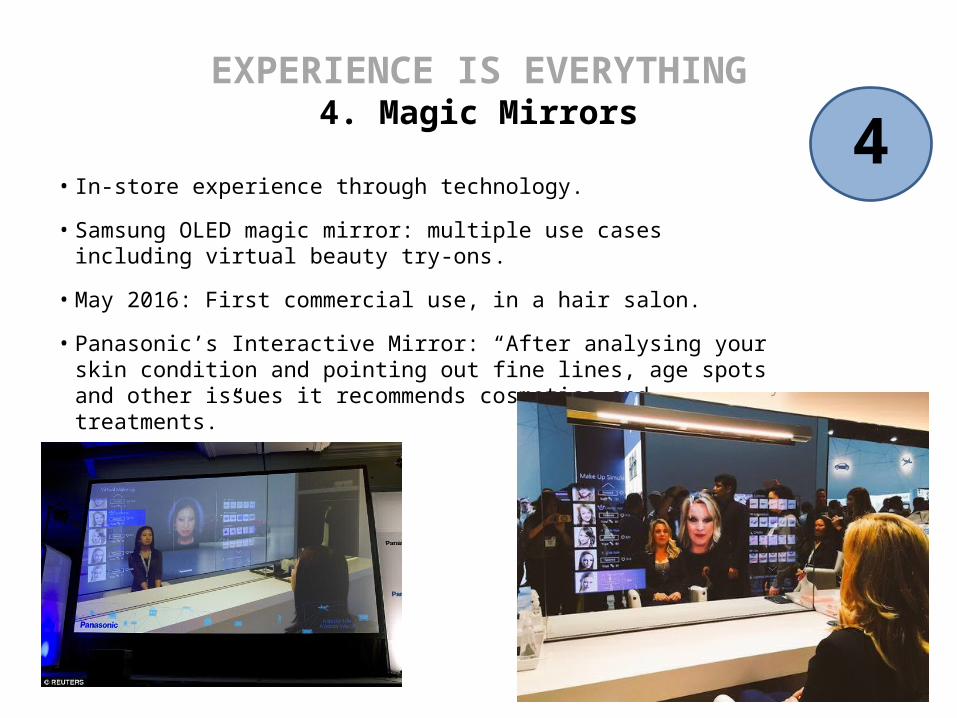

EXPERIENCE IS EVERYTHING4. Magic Mirrors

• In-store experience through technology.

• Samsung OLED magic mirror: multiple use cases including virtual beauty try-ons.

• May 2016: First commercial use, in a hair salon.

• Panasonic’s Interactive Mirror: “After analysing your skin condition and pointing out fine lines, age spots and other issues it recommends cosmetics and treatments.”

4

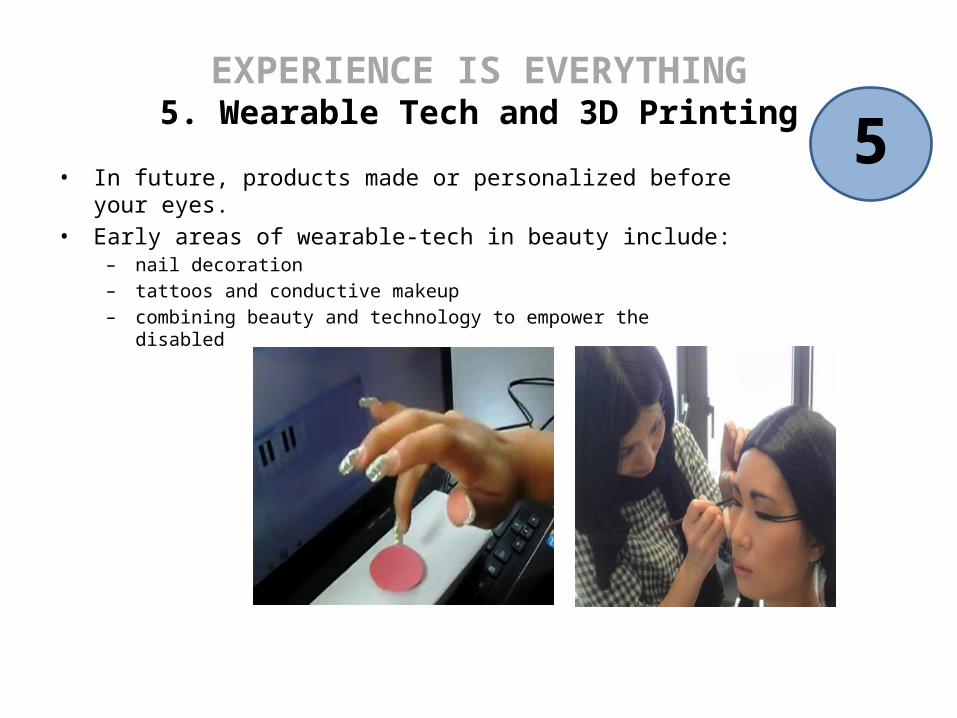

EXPERIENCE IS EVERYTHING5. Wearable Tech and 3D Printing

• In future, products made or personalized before your eyes.• Early areas of wearable-tech in beauty include:

– nail decoration– tattoos and conductive makeup – combining beauty and technology to empower the disabled

5

EXPERIENCE IS EVERYTHING5. Wearable Tech and 3D Printing

• Open-source desktop 3D printer with a sub-$200 price tag that can print makeup such as lipstick, lip gloss, eye shadow, blush, nail polish and brow powder

5

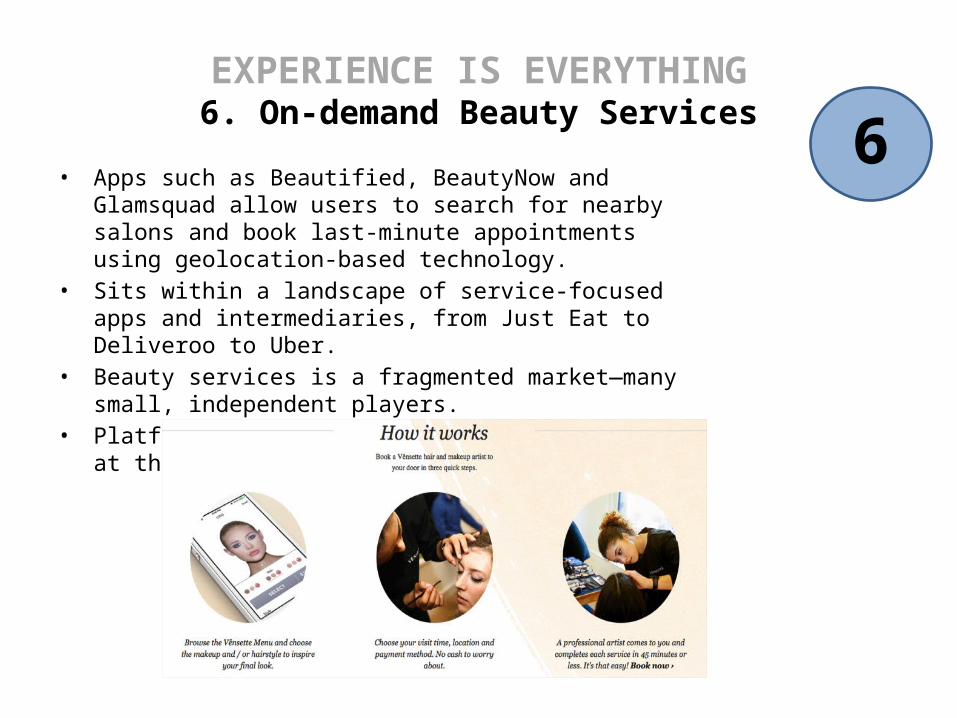

EXPERIENCE IS EVERYTHING6. On-demand Beauty Services

• Apps such as Beautified, BeautyNow and Glamsquad allow users to search for nearby salons and book last-minute appointments using geolocation-based technology.

• Sits within a landscape of service-focused apps and intermediaries, from Just Eat to Deliveroo to Uber.

• Beauty services is a fragmented market—many small, independent players.

• Platforms such as this consolidate the sector at the front end.

6

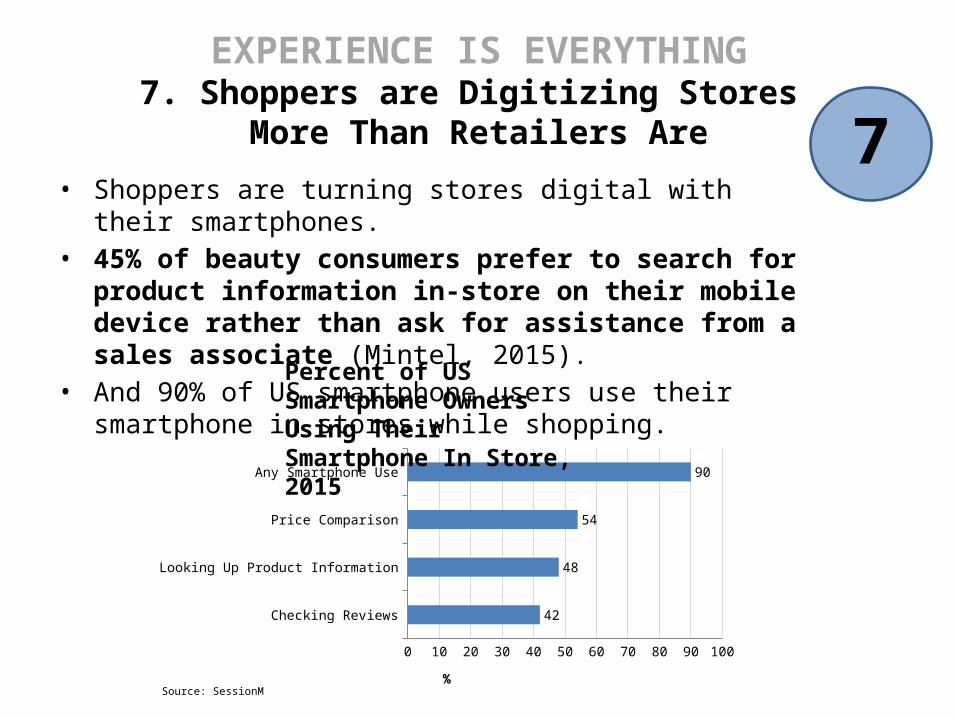

EXPERIENCE IS EVERYTHING7. Shoppers are Digitizing Stores

More Than Retailers Are• Shoppers are turning stores digital with their smartphones.• 45% of beauty consumers prefer to search for product

information in-store on their mobile device rather than ask for assistance from a sales associate (Mintel, 2015).

• And 90% of US smartphone users use their smartphone in stores while shopping.

7

Checking Reviews

Looking Up Product Information

Price Comparison

Any Smartphone Use

0 10 20 30 40 50 60 70 80 90 100

42

48

54

90

%

Percent of US Smartphone Owners Using Their Smartphone In Store, 2015

Source: SessionM

THEME 3: E-COMMERCE OPPORTUNITIES

• Growth and opportunities in three distinct segments.

o Subscription—for habitual purchases and trialing.

o Luxury—a strong channel in a struggling market.

o Grocery—set for strong growth.

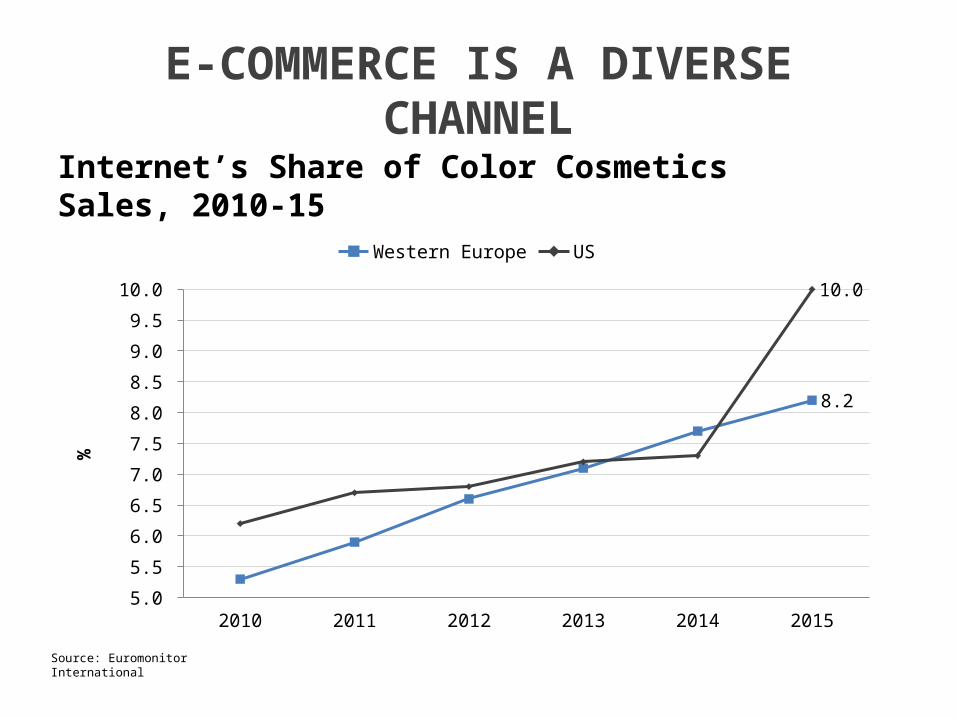

E-COMMERCE IS A DIVERSE CHANNEL

Internet’s Share of Color Cosmetics Sales, 2010-15

2010 2011 2012 2013 2014 20155.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

8.2

10.0

Western Europe US

%

Source: Euromonitor International

“Beauty online” is more nuanced than being a

homogeneous channel.

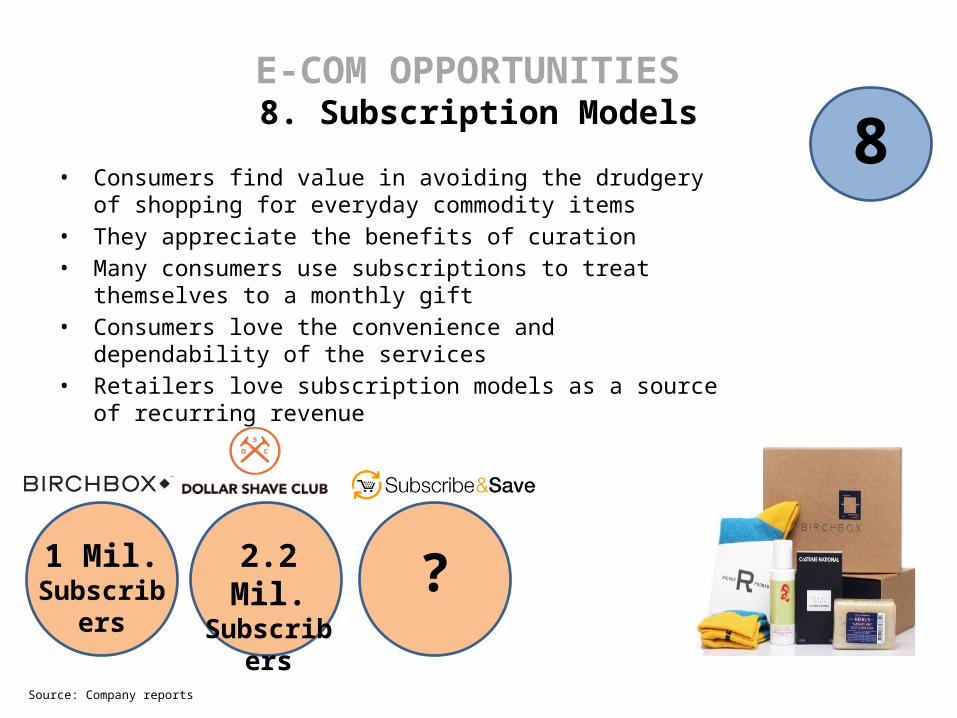

E-COM OPPORTUNITIES 8. Subscription Models

• Consumers find value in avoiding the drudgery of shopping for everyday commodity items

• They appreciate the benefits of curation • Many consumers use subscriptions to treat themselves to a monthly

gift• Consumers love the convenience and dependability of the services• Retailers love subscription models as a source of recurring revenue

8

1 Mil. Subscribers

2.2 Mil. Subscribers ?

Source: Company reports

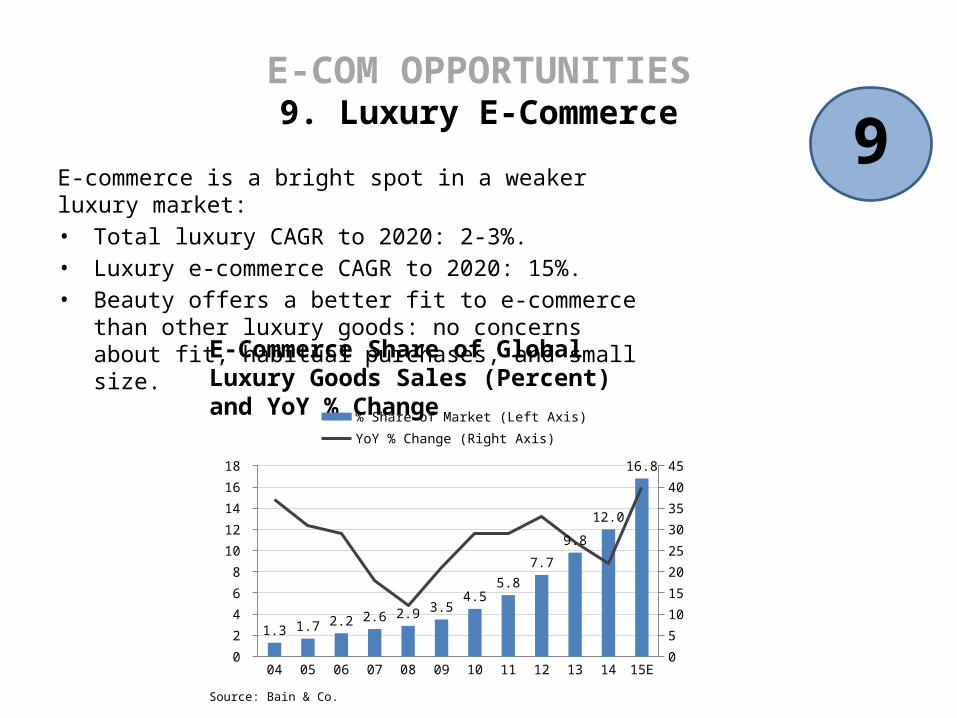

E-COM OPPORTUNITIES9. Luxury E-Commerce

E-commerce is a bright spot in a weaker luxury market: • Total luxury CAGR to 2020: 2-3%.• Luxury e-commerce CAGR to 2020: 15%.• Beauty offers a better fit to e-commerce than other luxury

goods: no concerns about fit, habitual purchases, and small size.

9

E-Commerce Share of Global Luxury Goods Sales (Percent) and YoY % Change

Source: Bain & Co.

04 05 06 07 08 09 10 11 12 13 14 15E0

2

4

6

8

10

12

14

16

18

0

5

10

15

20

25

30

35

40

45

1.3 1.7 2.2 2.6 2.9 3.54.5

5.8

7.7

9.8

12.0

16.8

% Share of Market (Left Axis) YoY % Change (Right Axis)

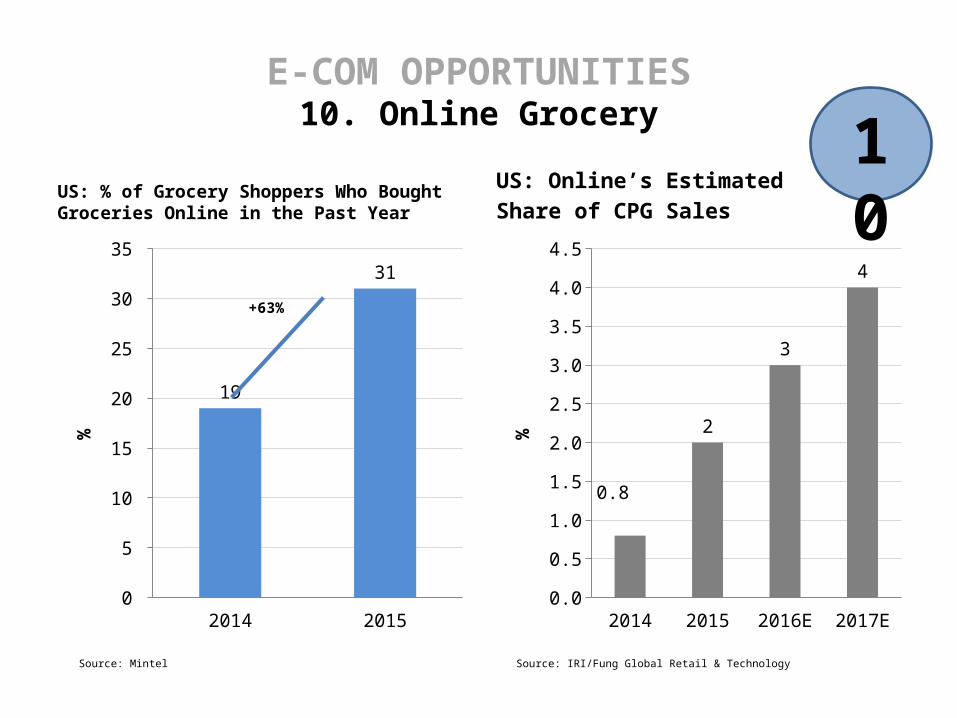

US: % of Grocery Shoppers Who Bought Groceries Online in the Past Year

US: Online’s Estimated Share of CPG Sales

2014 20150

5

10

15

20

25

30

35

19

31

%

+63%

2014 2015 2016E 2017E0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

0.8

2

3

4

%

Source: IRI/Fung Global Retail & TechnologySource: Mintel

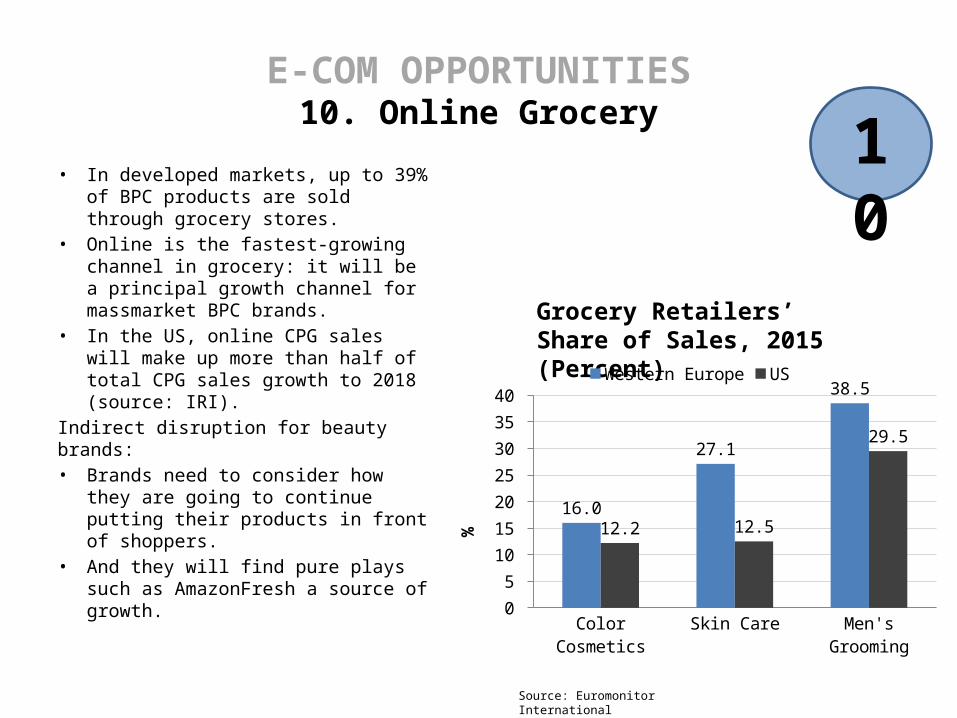

E-COM OPPORTUNITIES10. Online Grocery 10

E-COM OPPORTUNITIES10. Online Grocery

• In developed markets, up to 39% of BPC products are sold through grocery stores.

• Online is the fastest-growing channel in grocery: it will be a principal growth channel for massmarket BPC brands.

• In the US, online CPG sales will make up more than half of total CPG sales growth to 2018 (source: IRI).

Indirect disruption for beauty brands:• Brands need to consider how they

are going to continue putting their products in front of shoppers.

• And they will find pure plays such as AmazonFresh a source of growth.

10

Grocery Retailers’ Share of Sales, 2015 (Percent)

Color Cosmetics Skin Care Men's Grooming0

5

10

15

20

25

30

35

40

16.0

27.1

38.5

12.2 12.5

29.5

Western Europe US

%

Source: Euromonitor International

10 DISRUPTORS, THREE TAKEAWAYS

1. Information-rich online and app tools to help customers research and decide.2. Experience-rich stores, leveraging technology to bring information into the store.3. E-commerce is a diverse channel with discrete opportunities.

Find our research at www.fbicgroup.com And soon at www.fgrt.com