top issues for churches and ministries operating ... powerpoint webinar slid… · top issues for...

TRANSCRIPT

Top Issues for Churches and Ministries Operating Internationally Webinar

March 30, 2017 – ECFA.org

© ECFA 2017. All rights reserved.

Email questions to [email protected]

Today’s Presenters

Ted BatsonTax CounselCapinCrouse

John Van DrunenExecutive Vice President and General CounselECFA

Note: This webinar is general educational information and is not tax, legal or other professional advice. Advice on specific matters should come from a CPA, Attorney, or other professional advisors.

Email questions to [email protected] 3

Key Issues in Today’s Webinar

1. Cultivate an environment of biblically-based accountability

2. Approve and Maintain records regarding transfers to others

3. Monitor the use of funds and document outcomes of the use of funds

4. Understand and follow legal compliance requirements

5. Provide appropriate and accurate reporting on the work conducted

Email questions to [email protected] 4

The importance of accountability and oversight

With him we are sending the brother who is famous among all the churches for his preaching of the gospel. And not only that, but he has been appointed by the churches to travel with us as we carry out this act of grace that is being ministered by us, for the glory of the Lord himself and to show our good will. We take this course so that no one should blame us about this generous gift that is being administered by us, for we aim at what is honorable not only in the Lord’s sight but also in the sight of man.

2 Corinthians 8:18-21 ESV

Email questions to [email protected] 5

Why accountability and oversight are good

• At times our nature is to resist accountability and oversight, but we should welcome this as it is important to the integrity of our mission and ourselves.

• Peer accountability groups forming in other countries provide accountability.

• Givers are encouraged in generosity when they have a high level of trust in their church and organizations they support.

• Fostering accountability is not only good stewardship, it also speaks volumes to those with whom we interact.

Email questions to [email protected] 6

Churches vs. Nonprofits

• Analysis is generally going to be similar in terms of what is required in international oversight (with the exception of the IRS Form 990).

• Churches tend to use several different models when supporting missions which creates some unique aspects that may require coordinating accountability with other churches or partner organizations. Churches and the Support of Missions Article.

• A word about the term “grant” – IRS uses this term broadly to mean transfer, disbursement, contribution, noncash assistance, stipends, scholarships, and so on.

Email questions to [email protected] 7

Understanding the technical requirements

• The U.S. exempt organization must

• retain control and discretion as to the use of funds;

• maintain records establishing that the funds are used for section 501(c)(3) purposes; and

• limit distributions to specific projects that are in furtherance of its own exempt purposes.

(Rev. Rul. 68-489)

Email questions to [email protected] 8

Understanding the technical requirements

• A section 501(c)(3) organization may make grants to individuals, provided

• the distributions are made on a true charitable basis and

• in furtherance of its exempt purposes.

(Rev. Rul. 56-304)

Email questions to [email protected] 9

Keeping adequate records

• The organization should keep adequate records and case histories to show:

• The name and address of the recipients;• The amount distributed to each;• The purpose for which the aid was given;• The manner in which the recipient was selected; and • The relationship, if any, between the recipient and

• Members, officers, or trustees of the organization;• A grantor or substantial contributor to the organization or a member of the

family of either; and• A corporation controlled by a grantor or substantial contributor.

(Rev. Rul. 56-304)

Email questions to [email protected] 10

Understanding the technical requirements

• We can also draw inspiration from the private foundation expenditure responsibility regulations at Treas. Reg. §53.4945-5(b)(1), which require the exertion of all reasonable efforts and establishment of adequate procedures:

• To see that the grant is spent solely for the purpose for which it was made,

• To obtain full and complete reports from the grantee on how the funds are spent, and

• To make full and detailed reports with respect to such expenditures to the Commissioner (only relevant for grantors that are private foundations).

Email questions to [email protected] 11

Expenditure responsibility

• Expenditure responsibility requires three elements:1. A pre-grant inquiry sufficiently complete to give a reasonable

person assurance that the grantee will use the grant for the proper purposes

2. Written grant agreement• Specific content required

3. Post-grant reporting that describes• The use of the funds (including salaries, travel, and supplies)• Compliance with the terms of the grant, and • The progress made by the grantee toward achieving the

purposes for which the grant was made.

Email questions to [email protected] 12

Pre-grant inquiries

• Pre-Grant Inquiry should consider:• The identity, prior history and experience (if any), of the grantee

organization and its managers; and • Any knowledge or other information (from prior experience or

otherwise) concerning the management, activities, and practices of the grantee organization.

• The scope of the inquiry will vary based on the size and purpose of the grant, the period over which it is to be paid, and the grantor’s prior experience with the grantee.

• The pre-grant inquiry may be waived if there is a prior history of compliance

Email questions to [email protected] 13

Agreements

• The written agreement should• Specify the purpose of the grant,• Commit to repay any funds not used for the purposes of the grant,• Commit to submit full and complete reports annually describing how

funds are spent and the progress made in accomplishing the purposes of the grant,

• Commit to maintain records of receipts and expenditures and to make its books and records available to the grantor at reasonable times, and

• Commit not to use any of the funds—• To carry on propaganda, or otherwise attempt to influence legislation• To influence the outcome of any specific public election, or to carry on, directly

or indirectly, any voter registration drive• To make any downstream grant that is not for a charitable purpose

Email questions to [email protected] 14

Bottom Line

• Assess to whom funds will be given.• For intra-organization transfers, strategic plans and field/project

budgets will generally provide this information.• For transfers external to your organization, document who you will be

working with and the competency of the organization and the ability of its management to achieve the mission.

• If there is a lack of competency, what compensating controls can you implement?

Email questions to [email protected] 15

Bottom Line (continued)

• Assess (continued)• For external transfers, enter into written agreements that detail what

is to be accomplished and require accountability.• Unused funds should be returned

• Require post-grant reporting of results• For internal transfers, this may take the form of field or project

reports.• For external transfers, you may need to devise a standard reporting

methodology and work with the recipient to create systems to capture necessary information.

• In addition, ECFA has published Guidelines for Grant-Making that provides a template that implements these practices.

Email questions to [email protected] 16

Screening and vetting

• Post 9/11 the Patriot Act imposed significant requirements on organizations operating internationally—including nonprofit organizations.

• The Treasury Department’s Office of Foreign Asset Control (OFAC) is the principal agency that enforces these rules.

Email questions to [email protected] 17

Screening and vetting

• Office of Foreign Asset Control• Charitable Organization Resource Center• Published U.S. Department of the Treasury Anti-Terrorist Financing

Guidelines: Voluntary Best Practices for U.S.-Based Charities• Includes robust recommended practices around

• Governance, Financial Accountability, Programmatic Verification, and Anti-Terrorist Financing

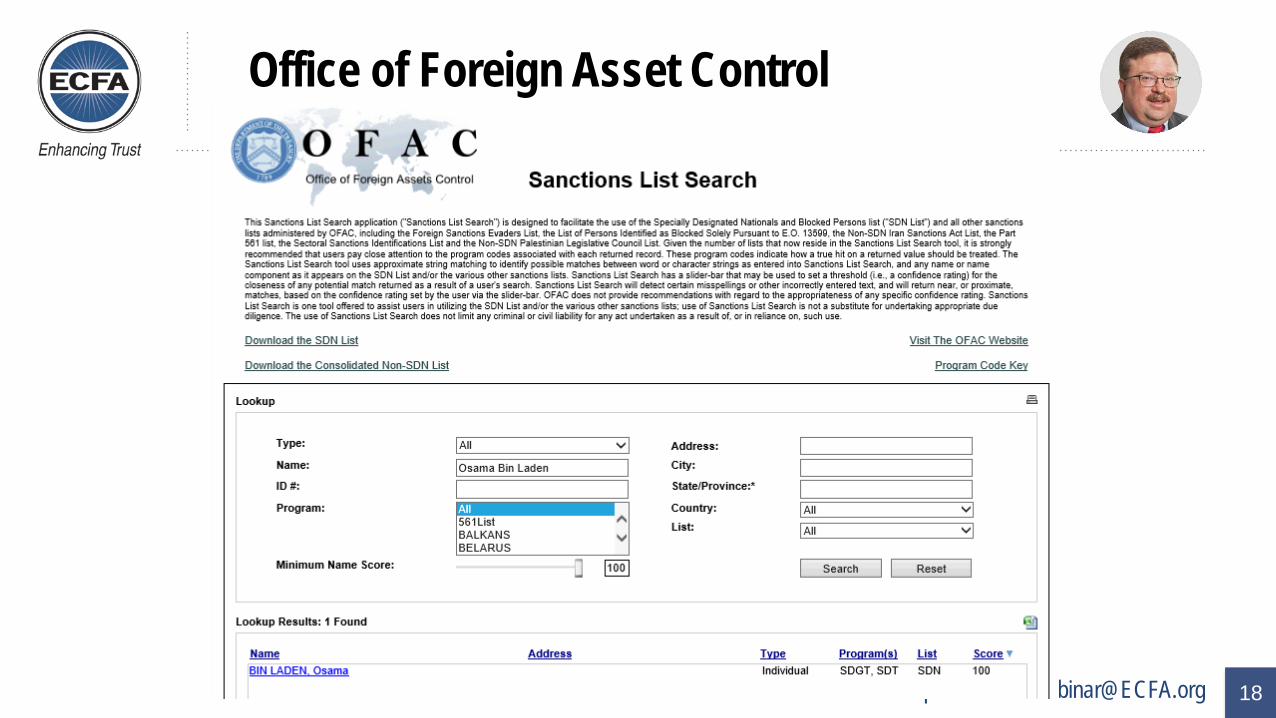

• Maintains OFAC List of Specially Designated Nationals and Blocked Persons• Can be accessed electronically at https://sanctionssearch.ofac.treas.gov/

Email questions to [email protected] 19

Office of Foreign Asset Control (continued)

• Approves a risk-based approach that permits tailoring vetting procedures to an assessment of the risk of a transfer• Has published a risk-matrix tool to use in assessing risk

Email questions to [email protected] 20

Screening and vetting

• A number of commercial tools are available for providing vetting services.

• These can be expensive and will generally require substantial activity to be cost-effective.

• Automation can produce “false positives”.• Examples include:

• Bridger Insight® by LexisNexis• AML Partners• AML 360• There are many others

Email questions to [email protected] 21

Understanding FBAR

• The FinCen 114 Report or FBAR is a required filing for • a U.S. person • having a financial interest in or signature authority over foreign

financial accounts • where the aggregate value of the foreign accounts exceeds

$10,000 at any time during the calendar year• Replaces Form TD F 90-22.1

• A U.S. person includes an individual, a partnership, a limited liability company, or a corporation—including a nonprofit corporation or a church.

Email questions to [email protected] 22

Understanding FBAR

• A U.S. person has a financial interest in a foreign financial account if:– the United States person is the owner of record or holder of legal

title; or– the owner of record or holder of legal title is one of the following:

• An agent, nominee, attorney, or a person acting in some other capacity on behalf of the United States person with respect to the account; or

• An entity which the U.S. person either owns more than 50% of the value or controls more than 50% of the voting power (loose paraphrase, see instructions)

Email questions to [email protected] 23

Understanding FBAR

• The form is due on April 15 of each year (beginning with 2016 reports filed in 2017).

– There is an automatic 6-month extension with no requirement to file an extension form.

• The form may only be filed electronically.

– Go to http://bsaefiling.fincen.treas.gov/main.html to file.

– A third-party, such as an accountant or attorney may prepare and file the form.

Email questions to [email protected] 24

Transporting cash and financial instruments

• Ask first: Is this absolutely necessary?

• Are we placing people at an elevated security risk?

• Are there appropriate internal controls to protect both the organization and the individuals involved?

• Understand potential legal ramifications and reporting requirements.

Email questions to [email protected] 25

FIN CEN 105

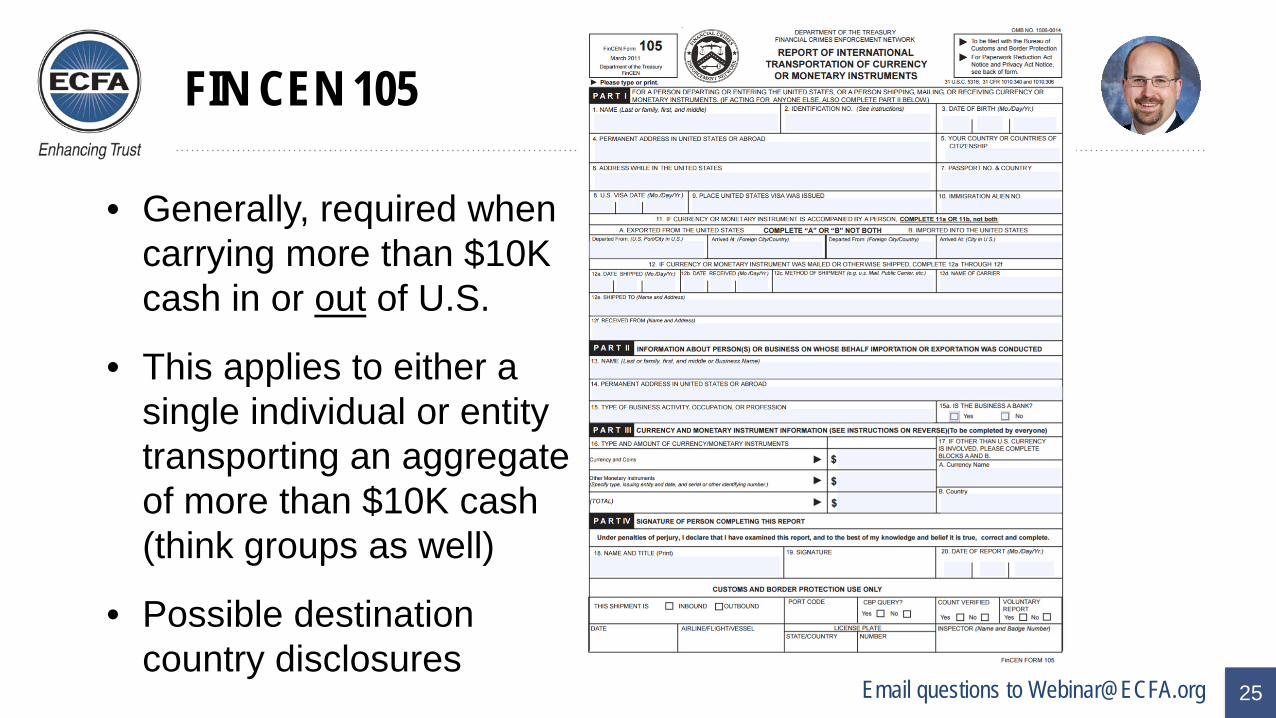

• Generally, required when carrying more than $10K cash in or out of U.S.

• This applies to either a single individual or entity transporting an aggregate of more than $10K cash (think groups as well)

• Possible destination country disclosures

Email questions to [email protected] 26

Form 990 Reporting and International Activity

• Are you required to file the Form 990?

• Understand some of the key questions and what might need to be collected for Form 990 reporting.

• Balance providing adequate disclosure with the need for sensitivity of some data relating to international operations. (Important to understand the history in Schedule F.)

Email questions to [email protected] 27

990 Key questions

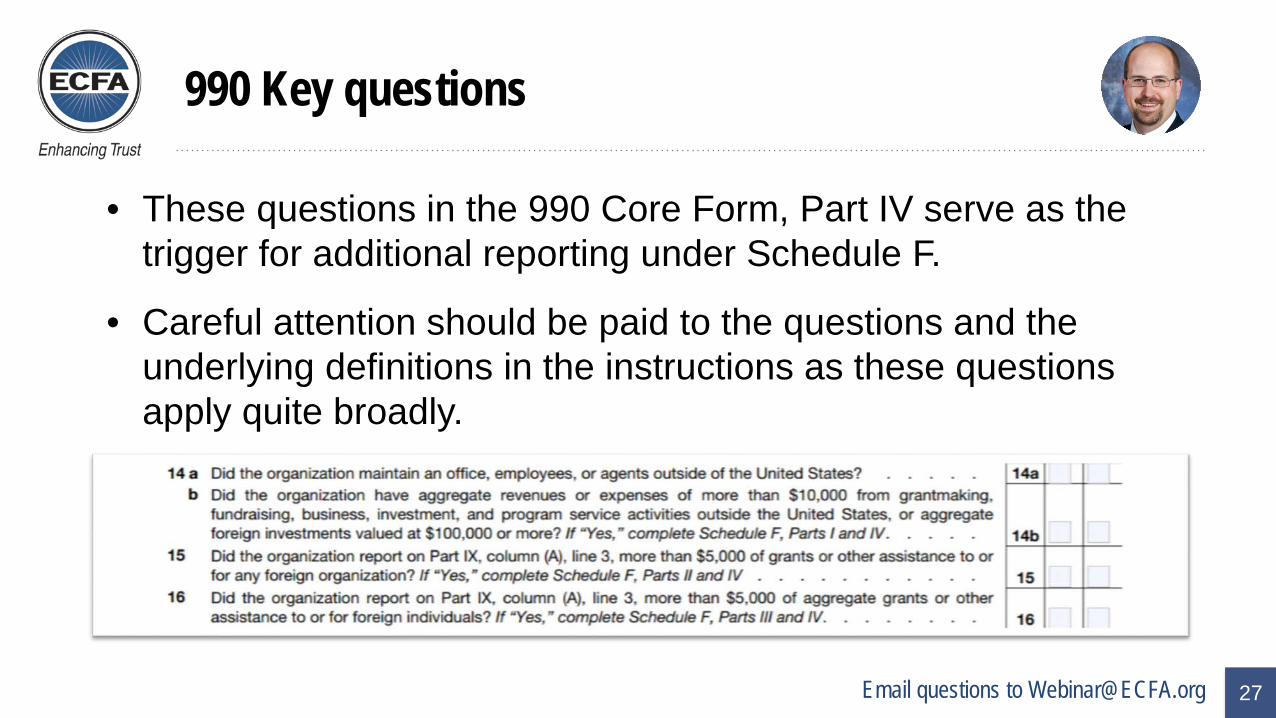

• These questions in the 990 Core Form, Part IV serve as the trigger for additional reporting under Schedule F.

• Careful attention should be paid to the questions and the underlying definitions in the instructions as these questions apply quite broadly.

Email questions to [email protected] 28

Properly categorizing expenses

• Funds sent to international recipients generally should be reported in line 3 instead of line 24.

Email questions to [email protected] 29

Understanding Schedule F of the Form 990

• Checking Yes or No to maintaining records

• Classifying activities by region

Email questions to [email protected] 30

Understanding Schedule F of the Form 990

• Listing assistance to organizations & individuals

• Note the greyed out boxes

Email questions to [email protected] 31

Understanding Schedule F of the Form 990

• Review any filing requirements with your tax or legal advisors.

• 990 is simply asking all filers to answer yes or no to highlight these questions.

Email questions to [email protected] 32

Understanding Schedule F of the Form 990

• This is where organizations should report a high level overview of approving and monitoring the use of funds under Part I.

• Additional Sch. F explanations

Email questions to [email protected]

Email questions to [email protected]

Email questions to [email protected]

Date Topic Speakers

April 13 5 Ways to Take the Mystery Out of Managing Missions Contributions

Dan BusbyMichael MartinJohn Van Drunen

April 20 8 Highlights from The Generosity Project Survey

Susie LippsDirk Rinker

May 25 What to Look for in Charitable Gift Tax Reform

Michael BattsDavid Wills

Register today at ECFA.org/Events

Email questions to [email protected]

Speaker Contact Information

Ted BatsonCapin Crouse LLP972 Emerson Parkway Ste. AGreenwood, IN 46143(o) 317-885-2620 x1150(c) [email protected]

John Van DrunenECFA440 W. Jubal Early Drive Ste. 100Winchester, VA 22601(o) [email protected]

Bonus Content:Other International Related

Issues of Importance

Email questions to [email protected]

Understanding FACTA

• The Foreign Account Tax Compliance Act (FATCA) – requires that foreign financial Institutions (FFI) and certain other non-

financial foreign entities report on the foreign assets held by their U.S. account holders

– failure to report results in the FFI being subject to withholding on withholdable payments

• Certain U.S. taxpayers holding financial assets outside the United States must report those assets to the IRS on Form 8938, Statement of Specified Foreign Financial Assets – The dollar threshold for reporting varies based on marital status (for

individuals) and whether living inside or outside the U.S.– Penalties apply for failure to file

Email questions to [email protected]

Boycotting States

• The U.S. tax code prohibits persons or companies from participating in boycotts that are not sanctioned by the U.S government.

• The primary target today is the Arab League’s boycott of Israel.

• The U.S. Treasury publishes a list of boycotting countries including

o Bahrain; Iraq; Saudi Arabia; United Arab Emirates; Republic of Yemen; Oman; Qatar; Kuwait; Lebanon; Libya; Syria

Email questions to [email protected]

Boycotting States

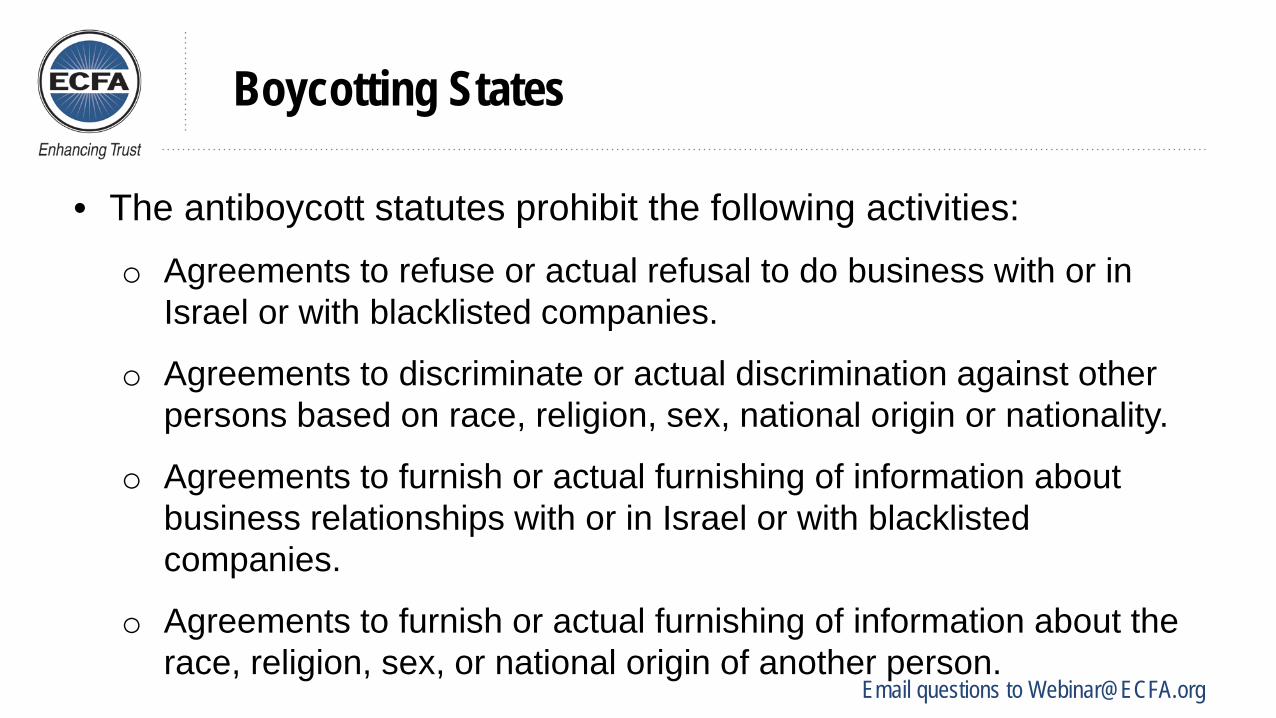

• The antiboycott statutes prohibit the following activities:o Agreements to refuse or actual refusal to do business with or in

Israel or with blacklisted companies.

o Agreements to discriminate or actual discrimination against other persons based on race, religion, sex, national origin or nationality.

o Agreements to furnish or actual furnishing of information about business relationships with or in Israel or with blacklisted companies.

o Agreements to furnish or actual furnishing of information about the race, religion, sex, or national origin of another person.

Email questions to [email protected]

Boycotting States

• The IRS requires the filing of Form 5713 to report operations in or related to boycotting states and the receipt of boycott requests and boycott agreements made.

• For more information see the Commerce Department’s Office of Antiboycott Compliance at https://www.bis.doc.gov/index.php/enforcement/oac#boycottlaws.

Email questions to [email protected]

• Employing or placing workers in foreign countries may impose certain tax liabilities on either the workers and/or your organization.

• A U.S. citizen working in a foreign country is not necessarily exempt from these responsibilities.

• There can be certain formation or authorization requirements to consider when operating in foreign countries.

Importance of understanding foreign compliance requirements

Email questions to [email protected]

Tax Totalization Agreements

• Many countries have systems similar to the U.S. social security system.

• There can be challenges when a resident of Country A works in Country B and both countries have mandatory social security programs.

• Some countries have attempted to streamline this complexity with Totalization Agreements.

• It is important to be mindful of assignment time periods.• Further information: IRS Totalization Agreements

Email questions to [email protected]

• This is a growing trend within the missions community.

• There are appropriate ways of structuring BAM for IRS tax compliance purposes, but this can require very careful attention to avoid issues such as private benefit or inurement.

• Further information: ECFA BAM Legal Issues Webinar

Business as Mission

Email questions to [email protected]

• We have heard from some members that they are struggling to maintain banking relationships due to their high volume of international activity.

• Bank compliance departments may be very cautious given the heightened regulatory environment.

• It is recommended to maintain ongoing conversations with your bank leadership so they understand the nature of your activities and the due diligence you are exercising in disbursing funds.

Banking Relationships