tolling: the changing landscape of … the changing landscape of transportation finance texas...

TRANSCRIPT

J U N E 2 0 0 6

T O L L I N G : T H E C H A N G I N G L A N D S C A P E O FT R A N S P O R T A T I O N F I N A N C E

Texas Transportation Conference

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

The current landscape of transportation funding

While demands for transportation funding persist, funding sources increasingly lag

18% of major roads nationwide are in poor or mediocre condition1

In 2003, urban areas with 3+ million people experienced 32 hoursof delay & $524 per capita in congestion costs2

The purchasing power of motor fuel revenues is decreasing

American Society of Civil Engineers Report Card 2005

Key sectors 2001 grade

2005 grade Comment

Roads D+ D Poor road conditions cost motorists $54 billion annually Americans spend 3.5 billion hours pa stuck in traffic ($63.2 billion) Total spending of $59.4 billion pa is well below the $94 billion required

Transit C- D+ Transit use increased 21& from 1993 – 2002 The FTA estimates $20.6 billion annually to improve to “good” condition In 2002, total capital outlays were $12.3 billion

1 US DOT Bureau of Transportation Statistics, National Transportation Statistics 2005, June 2005, TABLE 1-26: Condition of U.S. Roadways by Functional System.

2 Texas Transportation Institute, The 2005 Annual Urban Mobility Report (College Station, TX: 2005)

1

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

Inflation, improved vehicle efficiency and rising construction costs have weakened the purchasing power of federal gas tax revenues, despite increased rates

Nominal vs. Real Value of the Federal Gas TaxNominal vs. Real Value of the Federal Gas Tax

Source: ARTBA

0

2

4

6

8

10

12

14

16

18

20

'70 '75 '80 '85 '90 '95 '00

Nominal Value of the Federal Gas Tax

Real Value of the Federal Gas Tax

cent

s

The nominal rate has increased 4.5 times between 1970 and 2000. It was worth just over 3.1 cents per gallon in real terms in 2000

The gas tax has not been increased by more than .1 cent since 1993

2

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

As vehicle miles traveled increases 2.8% annually, road miles only expand .14% annually, on average…

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

'81 '86 '91 '96 '01

Annual Change in Vehicle Distance Traveled

Annual Change in Public Road Length

Growth of Vehicle Miles Traveled vs. Growth of Public Road Lengths NationallyGrowth of Vehicle Miles Traveled vs. Growth of Public Road Lengths Nationally

Source: FHWA Highway Statistics

3

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

…Traffic congestion increasingly plagues the nation’s roadways

0

5

10

15

20

25

1983 1990 1995 2001

Travel TimeTravel Time Trip LengthTrip Length

0

2

4

6

8

10

12

14

1983 1990 1995 2001

(minutes) (miles)

1 Source: FHWA

Average Commute SpeedsAverage Commute Speeds

0

5

10

15

20

25

30

35

40

45

Not MSA Less than 250,000 250,000-499,000 500,000-999,999 1-2.99 Million 3 Million +

1983 1990 1995 2001

After showing modest improvement in the 1990s, average commute speeds have begun to worsen

(mph)

4

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

However, toll roads can provide potential relief for increased transportation needs that lack the necessary funding

Traditional and innovative funding sources haven’t filled the gap

Conversion from indirect user fees to direct user fees

Recent US Federal legislation has supported innovative financing initiatives

There are more than 5,100 miles (8,200 km) of toll infrastructure in the United States

Approximately 3,000 miles (4,800 km) are rural and 2,100 miles (3,400 km) are urban

Vast majority of this infrastructure is operated solely by public authorities

Public private partnerships have been limited in the United States to date

However, reluctance to increase transportation funding has led to an increased interest in public private partnerships

1 US DOT Bureau of Transportation Statistics, National Transportation Statistics 2005, June 2005, TABLE 1-26: Condition of U.S. Roadways by Functional System.2 Texas Transportation Institute, The 2005 Annual Urban Mobility Report (College Station, TX: 2005)

5

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

US Toll Road Timeline

1800 1900 Future2000

1790’s – One of the first US toll roads in Lancaster, PA

Turn of 20th Century - Most toll roads taken over by state highway departments

1940 - The Pennsylvania Turnpike opens starting a resurgence of tolls

1990’s – California permits private concessions and the SR91 express lanes are built

2004 – Chicago Skyway sold to private investors

Source: Caltrans

1956 – National Interstate Highway System Act

1800’s – More than 2,500 private toll road companies operate more than 30,000 miles of toll raods in the US

1907 – Long Island Motor Parkway (private) opens as first toll road for motorcars

2000’s – Trans Texas Corridor Announced. TTC I-35 awarded. Return of private capital.

6

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

Despite having a long history, US toll roads remain underleveraged

Annual US Transportation Spending Sources

Source: The Brookings Institution, 2003

7

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

Toll Roads will play a vital role in expanding the transportation infrastructure in congested areas

Based on a list of currently proposed projects, we estimate more than $50 billion of additional capital will be added to the national transportation

system through new toll road construction in the next few years

= location of a major toll road

= toll road opened or under construction since 1990

= anticipated toll road project

8

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

Toll roads offer several political and economic advantages

Electronic Tolling

Increased traffic efficiency with more advanced ETC technologies

Toll increases are viewed more favorable by the public than increased taxes

Availability of User Fees

Less political costs than tax increases

As shown in table below, a relatively untapped resource

Type of Revenue 1995 1999 ChangePercent Change

($ in millions)

State Borrowing $4,316 $ 8,298 $3,982 92Other Local Taxes Includes Sales Taxes $ 4,487 $ 7,079 $ 2,592 58

Other State Taxes $ 6,565 $ 8,560 $ 1,995 30

Local General Funds $ 12,326 $ 15,857 $ 3,531 29

Local Property Taxes $ 5,220 $ 6,384 $ 1,164 22

State User Fees $36,200 $42,730 $6,530 18Source: Surface Transportation Policy Project, 2002

9

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

In addition to new & proposed toll road construction, sales & leases of current toll roads potentially provide additional capital with which to fund future projects

$1.83 billion

$3.85 billion

Toll road privatizations also provide significant resources that may help alleviate government funding shortfalls

10

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

Private capital can add additional value to toll facilities and provide value to transportation agencies

Aggressive use of capital to maximize value of road or the most road that may be built given a projected stream of tolls

Private capital structure using both debt and equity

Equity demands a higher rate of return, but may in fact be much more flexible during ramp up states

Use of debt in a way that optimizes its use and assumes key risks

May allow for upfront payments to sponsoring government, even in a new construction project

Can be used to extract significant value from existing roads

We estimate a total infrastructure purchasing power (from Private Sources) to be in excess of $200 billion

11

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

Why invest in infrastructure?

Rapid Shift to Funded Pension Systems

Incentives for Private Sector Participation

Long-Term Stable Investment Returns

Infrastructure Assets are Attractive to Investors

Highly Predictable Distribution

Stream

Diversification Capital Appreciation Tax Benefits

Unique

Class

Broad AppealInvestment

12

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

“Striking the Right Balance”

Objective of Public Sector Entity Objective of Private Partner

MaximizeNet Income

Maximize Traffic Flow & Economic

Development

Good Public Policy Profitability

Enhance user mobilityPromote economic developmentMaximize financial resources

Maximize return on investmentGenerate stable equity returnsBuild projects/ improvements that make financial sense

13

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

What are the alternatives and monetization options?

Status Quo -Leverage Assets with

Additional Debt

Asset Transfer to Public Authority

Initial Public Offeringof Equity

Public-Private Concessions:

- 35 years- 50 years- 75 years- 99 years

Direct Asset Sale

Private Investment/Public Regulation

Full Public Ownership & Control Limited Public Ownership

14

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

Potential Transportation Investors: Who may want to invest…

Australasia Europe / UKNorth America

Pass

ive

/ Fi

nanc

ial

Act

ive

/ A

sset

Man

ager

s

Access Economics

Macquarie Infrastructure Group

Developing Market

The list of well credentialed, well capitalized buyers is expanding rapidly

15

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

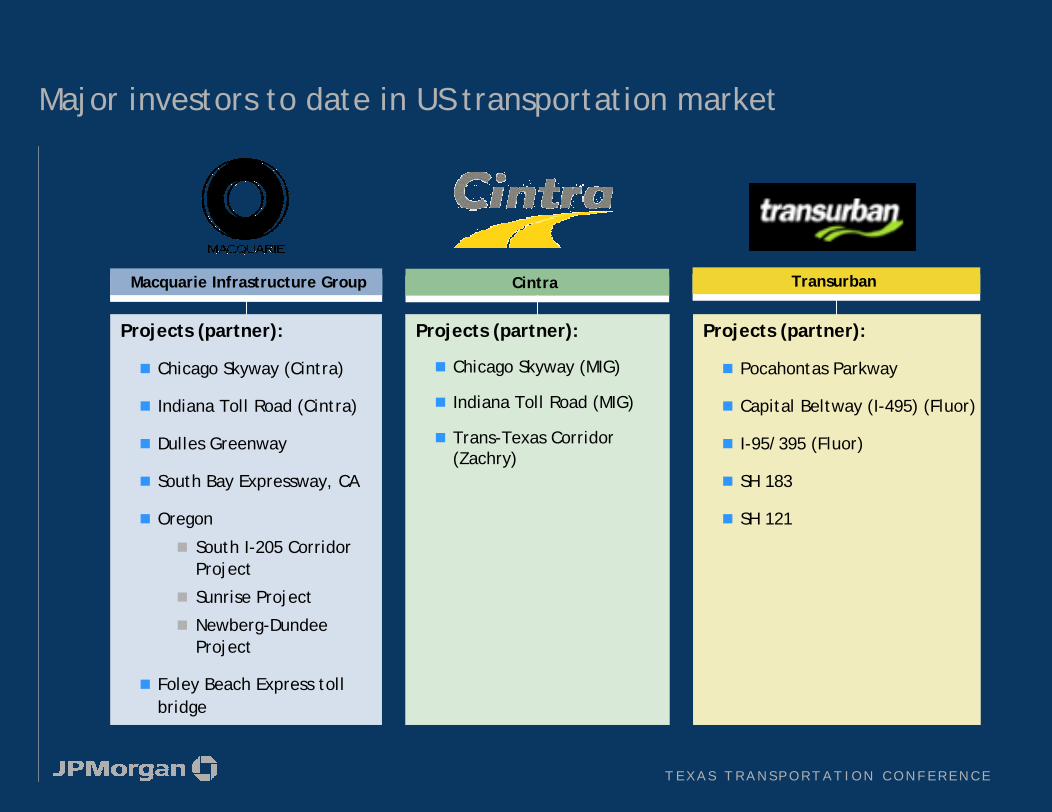

Major investors to date in US transportation market

Projects (partner):

Pocahontas Parkway

Capital Beltway (I-495) (Fluor)

I-95/395 (Fluor)

SH 183

SH 121

TransurbanTransurbanMacquarie Infrastructure GroupMacquarie Infrastructure Group CintraCintra

Projects (partner):

Chicago Skyway (Cintra)

Indiana Toll Road (Cintra)

Dulles Greenway

South Bay Expressway, CA

Oregon

South I-205 Corridor Project

Sunrise Project

Newberg-Dundee Project

Foley Beach Express toll bridge

Projects (partner):

Chicago Skyway (MIG)

Indiana Toll Road (MIG)

Trans-Texas Corridor (Zachry)

16

T E X A S T R A N S P O R T A T I O N C O N F E R E N C E

Conclusions

Toll roads and private capital are not new, but will be very influential going forward

The changing transportation environment renders toll facilities increasingly attractive

Lack of federal funding

No increases to gas taxes at federal or state levels

New federal programs that encourage and enable use of private capital and tolling

Significant amounts of private capital available

17