today’s trends, tomorrow’s - wpuiwpui.wisc.edu/wp-uploads/2016/06/david-boyd.pdf · today’s...

TRANSCRIPT

Today’s Trends, Tomorrow’s

Energy Needs

Wisconsin Public Utility Institute

David Boyd

VP, Government & Regulatory Affairs

May 20, 2016

Executive Summary

2

• A snapshot of today’s generation portfolio

• The system is changing quickly, for many reasons

• How do we plan for uncertainty and associated

risks?

• What might generation look like in the future?

• What else will we need to consider to deliver

electricity in the future?

MISO is an independent, non-profit organization in 15

U.S. States and one Canadian Province

MISO by-the-numbers

High Voltage Transmission 65,853 miles

Installed Generation 177,388 MW

Installed Generation 1,594 Units

Peak System Demand 127,125 MW

: MISO North

: MISO Central

: MISO South

3

MissionDrive value creation through efficient

reliability / market operations, planning

and innovation

4

Average Market Capacity by Resource Type

13%

42%37%

8%

Coal

Nuclear

Renewables

Natural Gas

5

Hourly Fuel Mix Snapshot

This chart represents the percentage of total megawatts supplied by the listed resources in the MISO footprint. The

category listed as “Other” is the combination of Hydro, Pumped Storage Hydro, Diesel, Demand Response

Resources, External Asynchronous Resources and a varied assortment of solid waste, garbage and wood pulp

burners. Charts like this are updated every five minutes.

6

Environmental / Regulatory

• Mercury & Air Toxics Standards (MATS)

• Air-quality standards for ozone, SO2, etc.

• Potential greenhouse gas regulations

Economics

• Low-cost natural gas

• Economic recovery

• Demand growth shift

• Infrastructure investment

State & Federal Policy

• Renewable portfolio standards

• Energy efficiency/demand-side management programs

• Tax credits

• FERC orders addressing demand response participation in wholesale energy markets

Evolving Technologies

Electric Industry

While EPA’s Clean Power Plan (or other carbon rules) may affect the electric

industry in the future, many other forces are already having major impacts

• Wind power • Energy storage • Load-modifying resources

• Solar energy • Distributed generation

7CO2 Modeling in MISO Planning Studies (5/11/2016)

8

MISO’s analysis is now shifting beyond the CPP alone to the

broader impacts of the evolving resource portfolio

Feb 2016

SCOTUS votes to

stay EPA’s CPP

Sep 2015 - Feb 2016

Near-term

Analysis

(Understanding

CPP compliance

pathways)

Jul 2016 - Nov 2018

Long-term analysis

(Developing

transmission overlay)Jan 2016 - Jun 2016

Mid-term

Analysis

(Prep. for transmission

overlay development)

Aug 2015

EPA releases

final CPP

& proposed

Federal Plan

CPP Rule Timeline (through 2018)

MISO’s Timeline for analyzing fleet transitions (through 2018)

MISO’s goal in this on-going analysis is to enable the reliable, efficient implementation of policy decisions made by our member-states and asset-owners.

In light of the stay, the CPP rule

timeline is currently unclear.

The final rule study evaluates CPP compliance pathways

and will inform the transmission planning process

MISO’s near-term analysis does not attempt to recommend compliance pathways,

optimize the resource mix, identify optimal electric transmission expansion, or

identify optimal gas pipeline expansion.

9CO2 Modeling in MISO Planning Studies (5/11/2016)

10

Mid-term analysis indicates that the CPP would drive coal

retirements with wind and gas replacement

CO2 Modeling in MISO Planning Studies (5/11/2016)

11

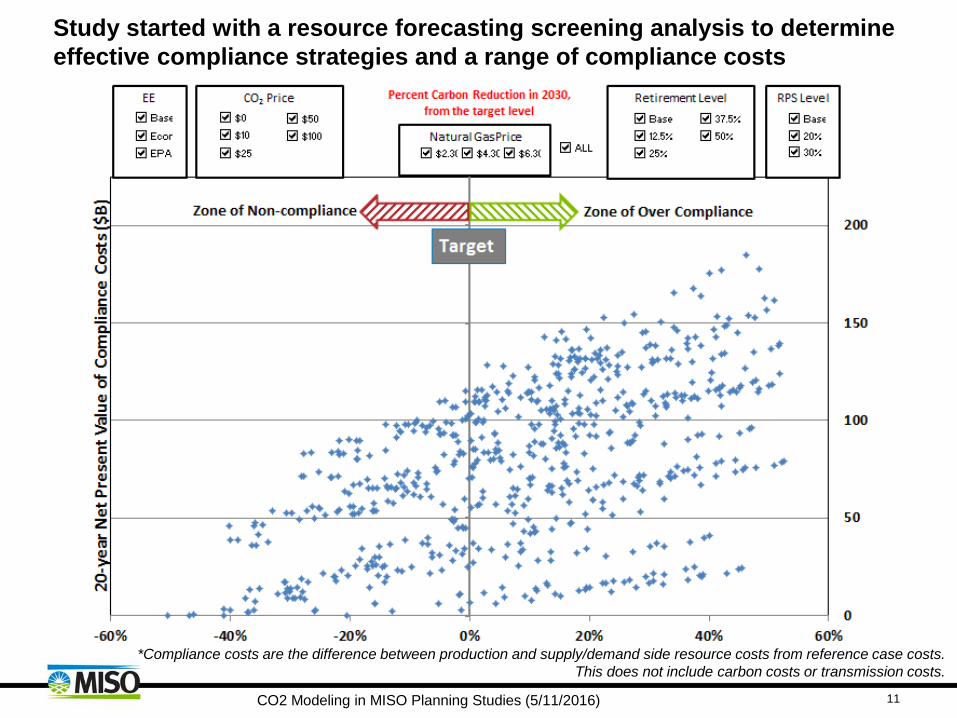

Study started with a resource forecasting screening analysis to determine

effective compliance strategies and a range of compliance costs

*Compliance costs are the difference between production and supply/demand side resource costs from reference case costs.

This does not include carbon costs or transmission costs.

CO2 Modeling in MISO Planning Studies (5/11/2016)

12

Regional compliance is less costly than

state-by-state compliance

Key observations of MISO’s analysis of the CPP rule

The MISO region sees a mass-based compliance advantage unless a regional heavy penetration of renewables and energy efficiency is achieved

New capital investment will be needed to achieve reliable, cost-effective compliance

1. REGIONAL

2. MASS-BASED COMPLIANCE

3. NEW INVESTMENT

The resource portfolio in the MISO region is evolving, with gas-

fired generation growing…

Historicals per MISO Data Services group. Gas prices per SNL

2016 YTD March

6%

11%

8% 7%

12%

16%

17%

23%

27%

0%

5%

10%

15%

20%

25%

30%

2011 2012 2013 2014 2015 2016 (YTD)

MISO North/Central

MISO Total (including MISO South)

Gas Share (%) of MISO Electric Generation (MWH)

How much further can gas grow in MISO?

$4.00 $2.76 $3.73 $4.37 $2.63Henry Hub $/MMBtu $1.99

• 2015 significantly eclipsed prior gas utilization…and the trend continues in 2016 (YTD)

― Though MISO South historically has high gas reliance, gas increased appreciably from 46% in 2014 to

55% in 2015 and 58% in 2016 YTD

1 - Forecast figure based on MISO MTEP16 assumptions and models for “Regional Clean Power Plan” scenario (assumes 26 GW coal retirement, 14 GW new gas-fired combined

cycle, carbon cost $32/ton in 2025, solar and wind include an economic maturity curve to reflect declining costs over time). The gas price forecast applicable to year 2025 has

been updated to reflect recent outlooks with Henry Hub gas prices assumed at ~$4.45/MMBtu.

6%

11%

8% 7%

12%

40%

0%

10%

20%

30%

40%

50%

2011 2012 2013 2014 2015 2025

Gas Share (%) of Electric Generation (MISO North/Central)

A changing generation mix will propel gas utilization even higher

in the coal-heavy Midwest portion of MISO’s footprint

Shift driven by increased gas-fired

capacity and increased capacity factors

Historical Actuals

Regional CPP Planning Scenario Forecast1

………………………..

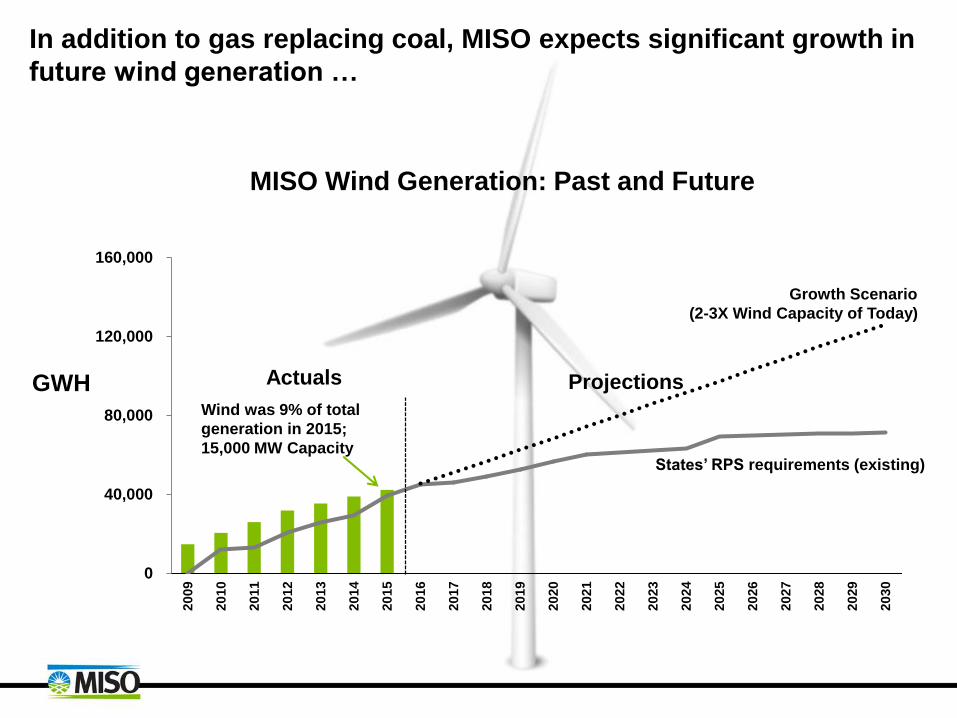

In addition to gas replacing coal, MISO expects significant growth in

future wind generation …

0

40,000

80,000

120,000

160,000

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

Actuals Projections

Wind was 9% of total

generation in 2015;

15,000 MW Capacity

GWH

MISO Wind Generation: Past and Future

Growth Scenario

(2-3X Wind Capacity of Today)

States’ RPS requirements (existing)

…providing additional opportunities for gas as a complement to

intermittent resources

70,000

75,000

80,000

85,000

90,000

95,000

0

5,000

10,000

15,000

20,000

25,000

1 2 3 4 5 6 7 8 9 101112131415161718192021222324

Load

MWWind

MW

February 12, 2015

Winter Hourly Wind Profile

• Wind production can fall off

just as load is rapidly

increasing in early winter

mornings

• In the future, MISO expects

the challenges of

intermittent renewables will

be amplified, requiring more

flexible gas-fired generation

Hour of Day

Solar penetration and ramping

17

Proposed MTEP17 Futures

18

Existing Fleet

Policy Regulations

Accelerated Alternative

Technologies

CO2 Modeling in MISO Planning Studies (5/11/2016)

MTEP17 Futures Key Assumptions

Future Existing Fleet Policy Regulations

Accelerated

Alternative

Technologies

Gross Demand & Energy

Growth Rates

Low

(High for LRZ 9 industrial)

Demand: 0.3%

Energy: 0.4%

Mid

Demand: 0.8%

Energy: 0.7%

High

(Low for LRZ 9 industrial)

Demand: 1.2%

Energy: 1.0%

Natural Gas Price Forecast Low Mid High

Max DR/EE/DG

Tech. Potential4

DR: 8 GW

EE: 9.6 GW

DG: 2.3 GW

DR: 9 GW

EE: 10.8 GW

DG: 2.8 GW

DR: 12.1 GW

EE: 25.6 GW

DG: 6.4 GW

RetirementsCoal: 9 GW1

Gas/Oil: 17 GW1

Total by 2031: 26 GW

Coal: 16 GW2

Gas/Oil: 17 GW1

Total by 2031: 33 GW

Coal: 24 GW2

Gas/Oil: 17 GW1

Total by 2031: 41 GW

Renewables Mandates + GoalsMandates + Goals

+ maturity cost curve

Mandates + Goals

+ maturity cost curve

MISO System CO2

Reduction TargetN/A All units target 25%3 All units target 35%3

Renewable Tax Credit Continues until 2022 Continues until 2022 Continues until 2022

19

1. Based on age-related retirement assumptions – total by year 2031

2. Coal retirements resulting from economics of carbon regulation derived from the CPP Mid-Term Analysis – total by year 2031

3. CO2 reduction on aggregate MISO fleet (measured by total of all units’ output) by 2030 from 2005 levels

4. Technical Potential represents the maximum feasible potential under each scenario. Only economically viable programs will be implemented in the

MTEP17 models (each program will be compared against supply-side alternatives)

CO2 Modeling in MISO Planning Studies (5/11/2016)

20

Focus is minimizing the total cost of energy

to consumers

Minimum Total Cost:

Energy, Capacity and

Transmission

High Generation Cost

Low Transmission Cost

Goal

High Transmission Cost

Low Generation Cost

Total

Cost

($)

Generation Costs

Transmission Expansion

H

L

L

H

CO2 Modeling in MISO Planning Studies (5/11/2016)

CO2 Modeling in MISO Planning Studies (5/11/2016) 21

Since 2011, actual and queued wind siting has been

consistent with RGOS Zone assumptions

CO2 Modeling in MISO Planning Studies (5/11/2016) 22

Other Issues

• Where will generation be sited?

– Renewables

– Coal to gas?

– New gas

– Interconnection

• Reliability---what does the word mean in the future?

• Dispatch and operations altered?

• Ramping events?

• Balancing costs?

• Fuel issues?

• Newer new technologies?