tidewater presentation november 2015 final · 2 forward looking information advisory in the...

TRANSCRIPT

November 2015

2

Forward Looking Information

Advisory

In the interests of providing Tidewater Midstream and Infrastructure Ltd. (“Tidewater” or the “Corporation”) shareholders and potential investors with information regarding Tidewater, including management’s assessment of future plans and operations relating to the Corporation, this document contains certain statements and information that are forward-looking statements or information within the meaning of applicable securities legislation, and which are collectively referred to herein as “forward-looking statements”. Forward-looking statements in this document include, but are not limited to statements and tables (collectively “statements”) with respect to: the strategic acquisition and concurrent equity financing; subsequent acquisitions and strategies for acquisitions, capital projects and expenditures; strategic initiatives; anticipated producer activity and industry trends; and anticipated performance. Readers are cautioned not to place undue reliance on forward-looking statements, as there can be no assurance that the plans, intentions or expectations upon which they are based will occur. By their nature, forward-looking statements involve numerous assumptions, as well as known and unknown risks and uncertainties, both general and specific, that contribute to the possibility that the predictions, forecasts, projections and other forward-looking statements will not occur and which may cause Tidewater’s actual performance and financial results in future periods to differ materially from any estimates or projections of future performance or results expressed or implied by the forward-looking statements. These assumptions, risks and uncertainties include, among other things: receipt of third party, regulatory and governmental approvals and consents in respect of the strategic acquisition and concurrent equity financing; completion of the strategic acquisition and concurrent equity financing; Tidewater’s ability to successfully implement strategic initiatives and whether such initiatives yield the expected benefits; future operating results; fluctuations in the supply and demand for natural gas, NGLs, and iso-octane; assumptions regarding commodity prices; activities of producers, competitors and others; the weather; assumptions around construction schedules and costs, including the availability and cost of materials and service providers; fluctuations in currency and interest rates; credit risks; marketing margins; potential disruption or unexpected technical difficulties in developing new facilities or projects; unexpected cost increases or technical difficulties in constructing or modifying processing facilities; Tidewater’s ability to generate sufficient cash flow from operations to meet its current and future obligations; its ability to access external sources of debt and equity capital; changes in laws or regulations or the interpretations of such laws or regulations; political and economic conditions; and other risks and uncertainties described from time to time in the reports and filings made with securities regulatory authorities by Tidewater.

Readers are cautioned that the foregoing list of important factors is not exhaustive. The forward-looking statements contained in this document are made as of the date of this document or the dates specifically referenced herein. For additional information please refer to Tidewater’s public filings available on SEDAR at www.sedar.com. All forward-looking statements contained in thisdocument are expressly qualified by this cautionary statement.

Any financial outlook or future-oriented financial information, as defined by applicable securities legislation, has been approved by management of Tidewater as of May 17, 2015. Such financial outlook or future-oriented financial information is provided for the purpose of providing information about management's current expectations and goals relating to the future of Tidewater. Readersare cautioned that reliance on such information may not be appropriate for other purposes.

Non-GAAP Financial Measures: This presentation refers to “EBITDA” and “cash available for distribution” (CAFD), which do not have any standardized meaning prescribed by generally accepted accounting principles in Canada (“GAAP”). We define EBITDA as means earnings before interest, taxes, depreciation and amortization. We define “cash available for distribution” (CAFD) as the amount of cash generated from operations, before changes in working capital and after deducting sustaining capital expenditures, scheduledprincipal repayments of debt and distributions to non-controlling interests.

2

3

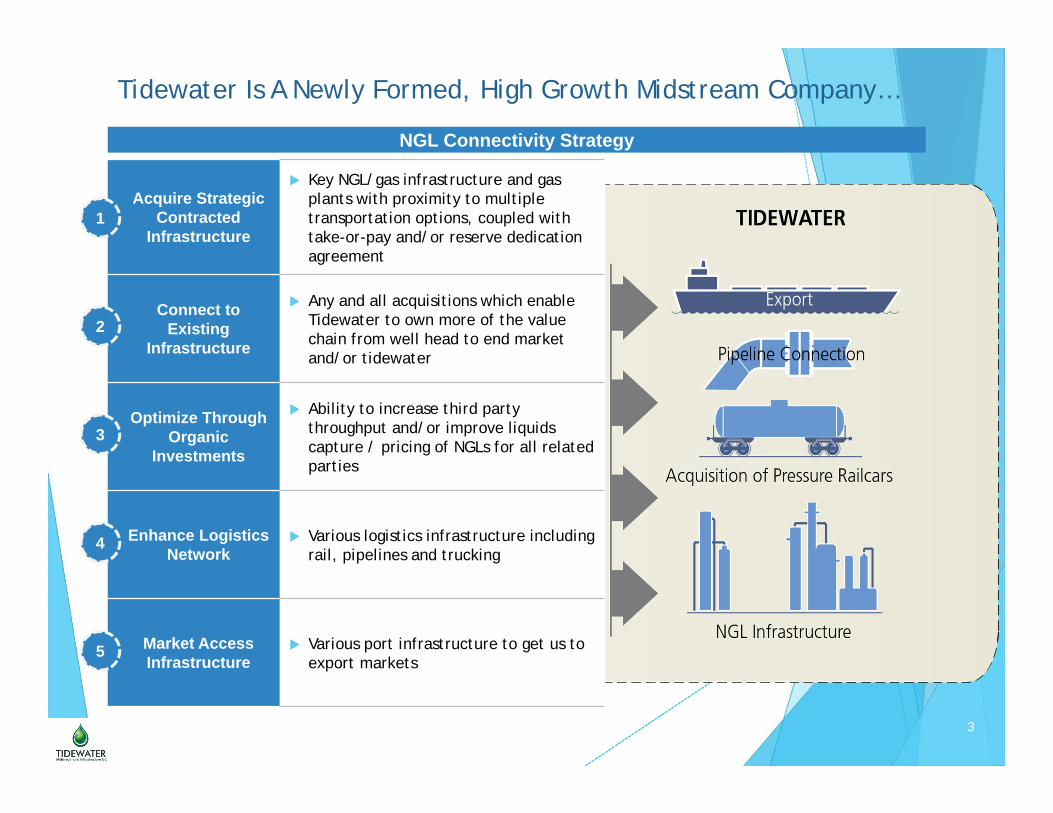

Tidewater Is A Newly Formed, High Growth Midstream Company…

NGL Connectivity Strategy

Acquire Strategic Contracted

Infrastructure

Key NGL/gas infrastructure and gas plants with proximity to multiple transportation options, coupled with take-or-pay and/or reserve dedication agreement

Connect to Existing

Infrastructure

Any and all acquisitions which enable Tidewater to own more of the value chain from well head to end market and/or tidewater

Optimize Through Organic

Investments

Ability to increase third party throughput and/or improve liquids capture / pricing of NGLs for all related parties

Enhance Logistics Network

Various logistics infrastructure including rail, pipelines and trucking

Market Access Infrastructure

Various port infrastructure to get us to export markets

1

2

3

4

5

4

No debt utilized until most current acquisition, maintaining a low-risk and highly flexible capital structure

Protection obtained from vendors, contracts, competitive positioning to ensure go forward cash flow

Taking advantage of ongoing pipeline of acquisition and organic growth opportunities to increase per share value via creativity of management team

Currently trading at an overly large discount to the comparables given more conservative capital structure and more easily achieved relative growth rates

Ongoing review of new opportunities to further enhance the NGL Connectivity Strategy, with ability to finance via available free cash flow, undrawn credit and access to capital markets

... That Currently Provides a Low-Risk Attractive Investment Opportunity

Very Conservative Capital Structure

Underlying Stable Cash Flow Producing Infrastructure Assets

Growing EBITDA, CFPS and Share Value

Relatively Undervalued versus

Comparable Companies

Poised for Continued Low-Risk Growth

Attractive Investment Opportunity

1

2

3

4

5

Pro forma 0.5x net debt / EBITDA and payout ratio of 25%

Asset vendors committed to forward 12 month cash flow minimums including reserve dedications and processing agreements ranging from 2 to 10 years

Since the April 2015 IPO EBITDA increased from zero to pro forma 2016E H2 run-rate of ~$401 million, 2016E H2 run-rate CFPS to ~$0.221 and share value from $1.00 per share to $1.43 per share

Tidewater has leverage of 0.5x EBITDA vs. comparable average of 4.5x, payout ratio of 25% vs. average of 69%, and a TEV/EBITDA multiple of 7.3x vs. average of 12.8x

New opportunities being brought regularly to Tidewater’s creative and experienced management teamExecuted on five acquisitions in six months

1 2016E H2 run-rate EBITDA and CFPS includes organic improvements of existing facilities.

5

Commitment to the NGL Value Chain And Execution of Business Plan Tidewater will aggressively grow its NGL business through both organic

opportunities as well as acquisitions

Closed initial public offering April 2015

Closed significant equity offering to capitalize Tidewater June 2015

Closed acquisition of initial deep cut gas plant within liquids

rich fairway July 2015

Extend largest take or pay contract and work to diversify

customer base September 2015

Announced acquisition of 2nd gas plant and new core area in

one of the most active liquids rich regions in Western Canada October 2015

Announced acquisition of 3rd operated gas plant (100% WI) in additional to propane retail acquisition and 5 year supply deal with vendor of gas plant. $70 million credit facility finalized.

November 2015

In Progress Install truck racks at BRC to obtain better pricing for producers NGLs T+1 months

In Progress NGL Export Terminal T+12 months

In Progress Expand NGL infrastructure, related network and new

downstream markets for NGLs. Continue to offer producers improved pricing for their NGLs and related netbacks

Ongoing

6

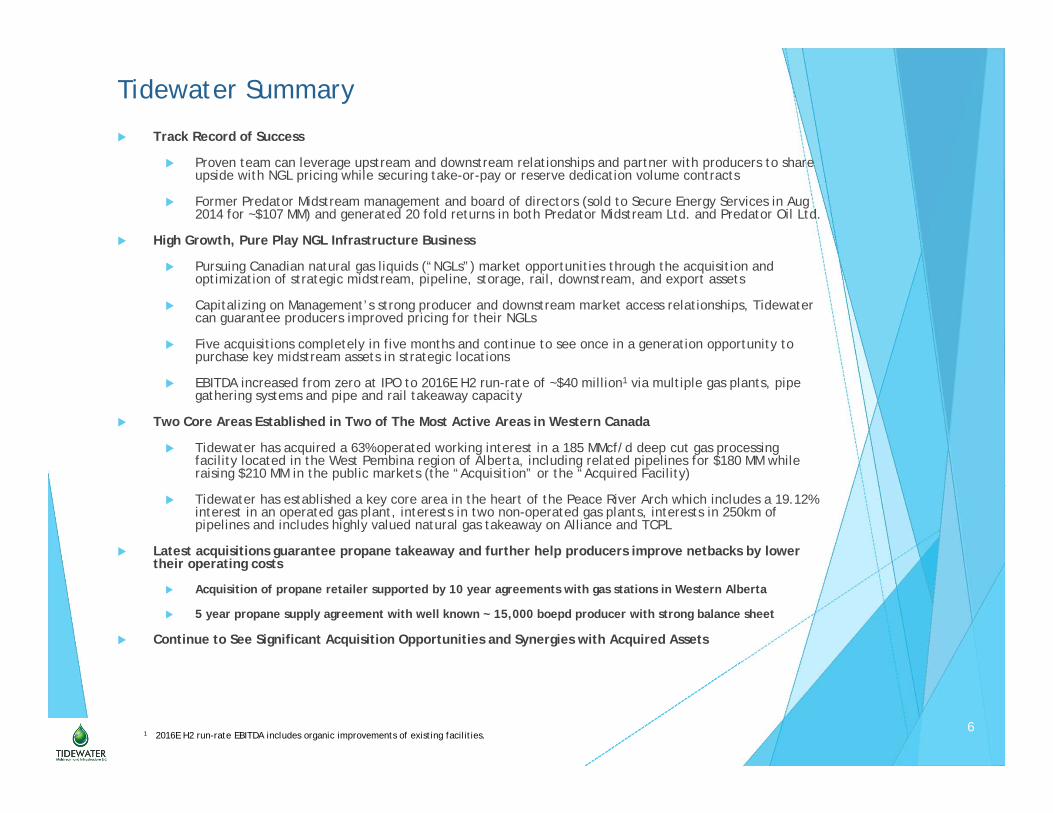

Track Record of Success

Proven team can leverage upstream and downstream relationships and partner with producers to share upside with NGL pricing while securing take-or-pay or reserve dedication volume contracts

Former Predator Midstream management and board of directors (sold to Secure Energy Services in Aug 2014 for ~$107 MM) and generated 20 fold returns in both Predator Midstream Ltd. and Predator Oil Ltd.

High Growth, Pure Play NGL Infrastructure Business

Pursuing Canadian natural gas liquids (“NGLs”) market opportunities through the acquisition and optimization of strategic midstream, pipeline, storage, rail, downstream, and export assets

Capitalizing on Management’s strong producer and downstream market access relationships, Tidewater can guarantee producers improved pricing for their NGLs

Five acquisitions completely in five months and continue to see once in a generation opportunity to purchase key midstream assets in strategic locations

EBITDA increased from zero at IPO to 2016E H2 run-rate of ~$40 million1 via multiple gas plants, pipe gathering systems and pipe and rail takeaway capacity

Two Core Areas Established in Two of The Most Active Areas in Western Canada

Tidewater has acquired a 63% operated working interest in a 185 MMcf/d deep cut gas processing facility located in the West Pembina region of Alberta, including related pipelines for $180 MM while raising $210 MM in the public markets (the “Acquisition” or the “Acquired Facility)

Tidewater has established a key core area in the heart of the Peace River Arch which includes a 19.12% interest in an operated gas plant, interests in two non-operated gas plants, interests in 250km of pipelines and includes highly valued natural gas takeaway on Alliance and TCPL

Latest acquisitions guarantee propane takeaway and further help producers improve netbacks by lower their operating costs

Acquisition of propane retailer supported by 10 year agreements with gas stations in Western Alberta

5 year propane supply agreement with well known ~ 15,000 boepd producer with strong balance sheet

Continue to See Significant Acquisition Opportunities and Synergies with Acquired Assets

Tidewater Summary

1 2016E H2 run-rate EBITDA includes organic improvements of existing facilities.

7

Board & Management Has A Strong Track Record

Energetic and motivated team, which has previously achieved 20 fold returns in prior companies; most recently, Predator Midstream Ltd. (crude-by-rail) and Predator Oil Ltd. (upstream oil)1

7

Team Member Position Background

Joel MacLeod, CA Chairman, President & CEO Founding CEO of Predator Oil Ltd., Founding CEO and majority shareholder of Predator Midstream Ltd., Former CFO SkyWest Energy Corp., PrimeWest Energy Trust/TAQA

Toby McKennaDirector, VP, BusinessDevelopment & Commercial

VP Business Development Predator Oil Ltd., VP Natural Gas Trading Castelton Commodities Canada, Co-Founder Louis Dreyfus Energy Canada

Joel Vorra, CA CFO Former Controller Predator Midstream Ltd., former CFO Predator Oil Ltd., Collins Barrow Calgary LLP

Jarvis Williams VP, Logisticsand Midstream Operations

Former VP Logistics and Midstream Operations of Predator Midstream Ltd., VP Predator Oil Ltd., Skywest Energy Corp/Marquee Energy, Primewest Energy Trust/TAQA

Jeff Ketch VP, Field Operations Former VP Operations Predator Midstream Ltd., VP Operations Predator Oil Ltd., Equal Energy Ltd., 20+ years field operations

Greg MacDonald, P. Eng

VP, Engineering Former VP Engineering Predator Midstream Ltd., President & COO Predator Oil Ltd., Molopo Energy, Compton Petroleum

Don Garner, P.Eng

Advisor to the Board Current Chairman Predator Oil Ltd., former Chairman Predator Midstream Ltd., Former

President & CEO PrimeWest Energy Trust who sold to TAQA for $5 billion in cash, former President & COO Northstar Energy

Doug Fraser, CA Director

Former CFO of Abu Dhabi National Energy Company PJSC (“TAQA”), where he oversaw oil and gas and infrastructure assets with a value of greater than $30 billion. Prior to TAQA, Mr. Fraser was the CFO of PrimeWest Energy Trust at the time of its acquisition by TAQA for approximately $5 billion in cash. Also, formerly CFO of Husky Energy Inc. and held senior roles at Petro-Canada and Imperial Oil Limited

Trevor Wong-Chor, LLB

Director Partner DLA Piper (Canada) LLP, current Corporate Secretary Predator Oil Ltd., former Corporate Secretary Predator Midstream Ltd.

Steve Holyoake, P.Eng

Director VP Drilling & Completions Tangle Creek Energy, current Board Member Predator Oil

Ltd., former Board Member Predator Midstream Ltd., former VP Operations SkyWest Energy Corp and former Manager, Drilling & Completions at Berens Energy Ltd.

1 Past successes are not necessarily indicative of future performance.

88

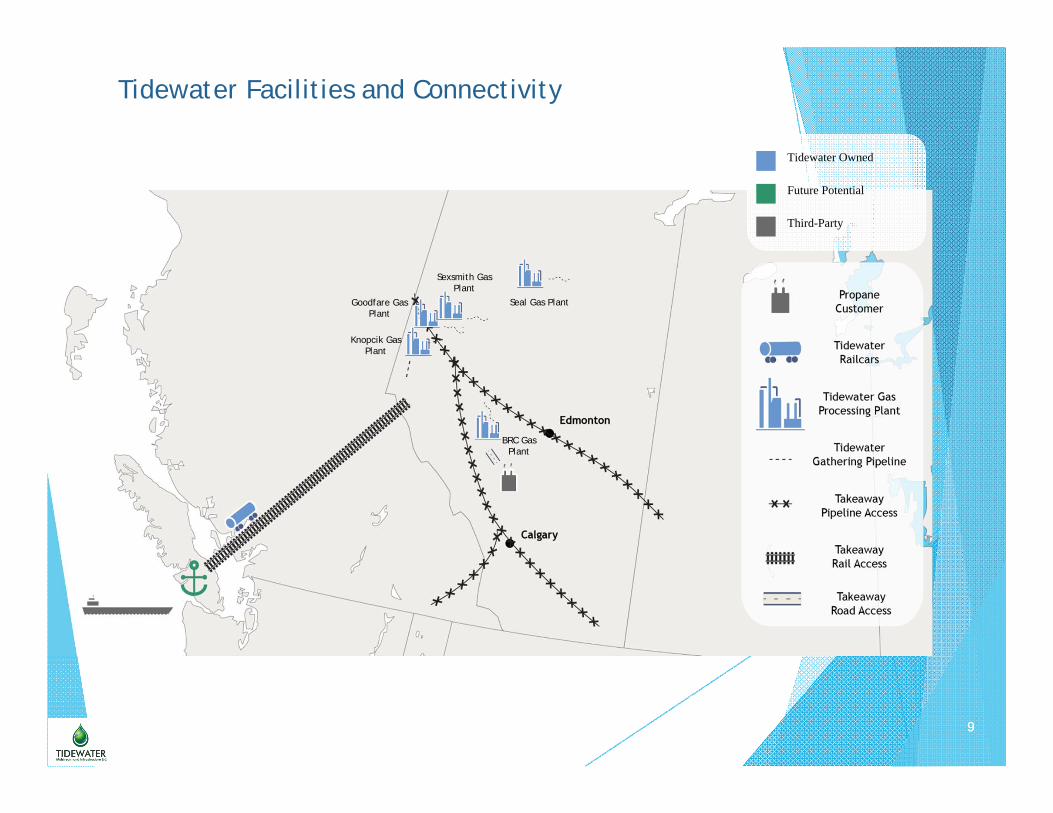

Adding Value Through All Parts of the Value Chain

Tidewater Owned

Future Potential

Third-Party

99

Tidewater Facilities and Connectivity

Tidewater Owned

Future Potential

Third-Party

Seal Gas Plant

Sexsmith Gas Plant

Goodfare Gas Plant

Knopcik Gas Plant

BRC Gas Plant

10

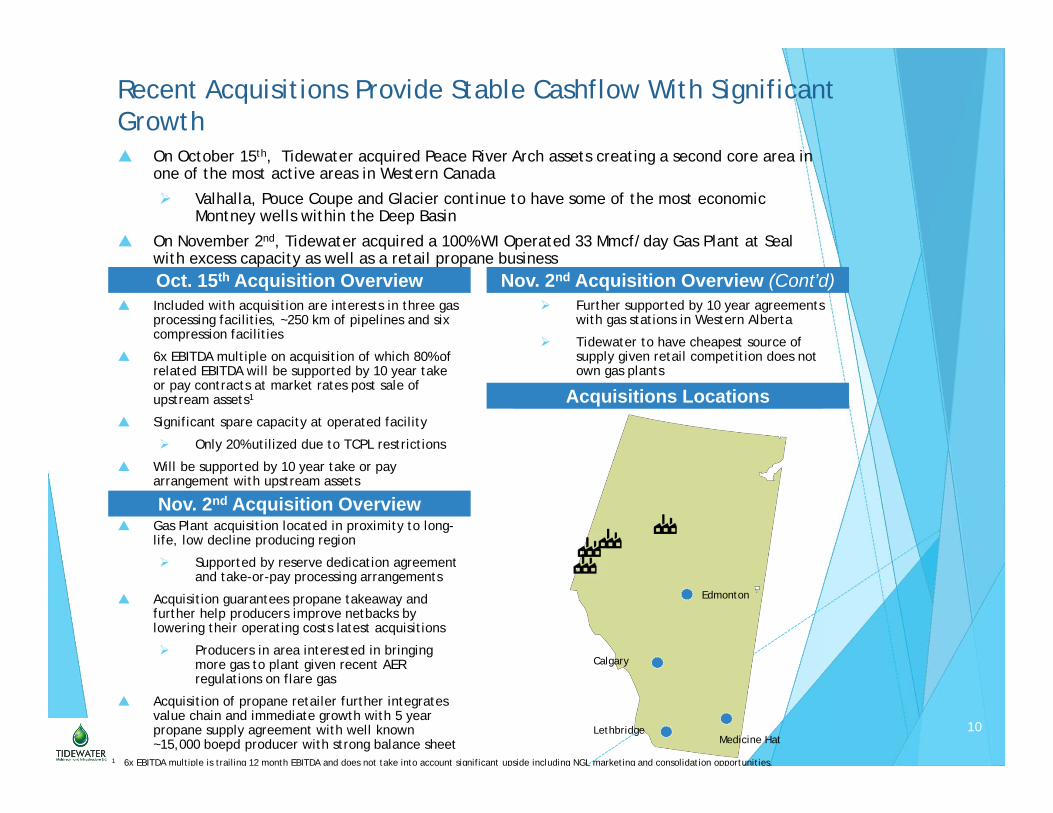

On October 15th, Tidewater acquired Peace River Arch assets creating a second core area in one of the most active areas in Western Canada

Valhalla, Pouce Coupe and Glacier continue to have some of the most economic Montney wells within the Deep Basin

On November 2nd, Tidewater acquired a 100% WI Operated 33 Mmcf/day Gas Plant at Seal with excess capacity as well as a retail propane business

Recent Acquisitions Provide Stable Cashflow With Significant Growth

Oct. 15th Acquisition Overview Included with acquisition are interests in three gas

processing facilities, ~250 km of pipelines and six compression facilities

6x EBITDA multiple on acquisition of which 80% of related EBITDA will be supported by 10 year take or pay contracts at market rates post sale of upstream assets1

Significant spare capacity at operated facility

Only 20% utilized due to TCPL restrictions

Will be supported by 10 year take or pay arrangement with upstream assets

Gas Plant acquisition located in proximity to long-life, low decline producing region

Supported by reserve dedication agreement and take-or-pay processing arrangements

Acquisition guarantees propane takeaway and further help producers improve netbacks by lowering their operating costs latest acquisitions

Producers in area interested in bringing more gas to plant given recent AER regulations on flare gas

Acquisition of propane retailer further integrates value chain and immediate growth with 5 year propane supply agreement with well known ~15,000 boepd producer with strong balance sheet

Acquisitions Locations

Edmonton

Calgary

Medicine HatLethbridge

1 6x EBITDA multiple is trailing 12 month EBITDA and does not take into account significant upside including NGL marketing and consolidation opportunities.

Nov. 2nd Acquisition Overview

Nov. 2nd Acquisition Overview (Cont’d) Further supported by 10 year agreements

with gas stations in Western Alberta

Tidewater to have cheapest source of supply given retail competition does not own gas plants

11

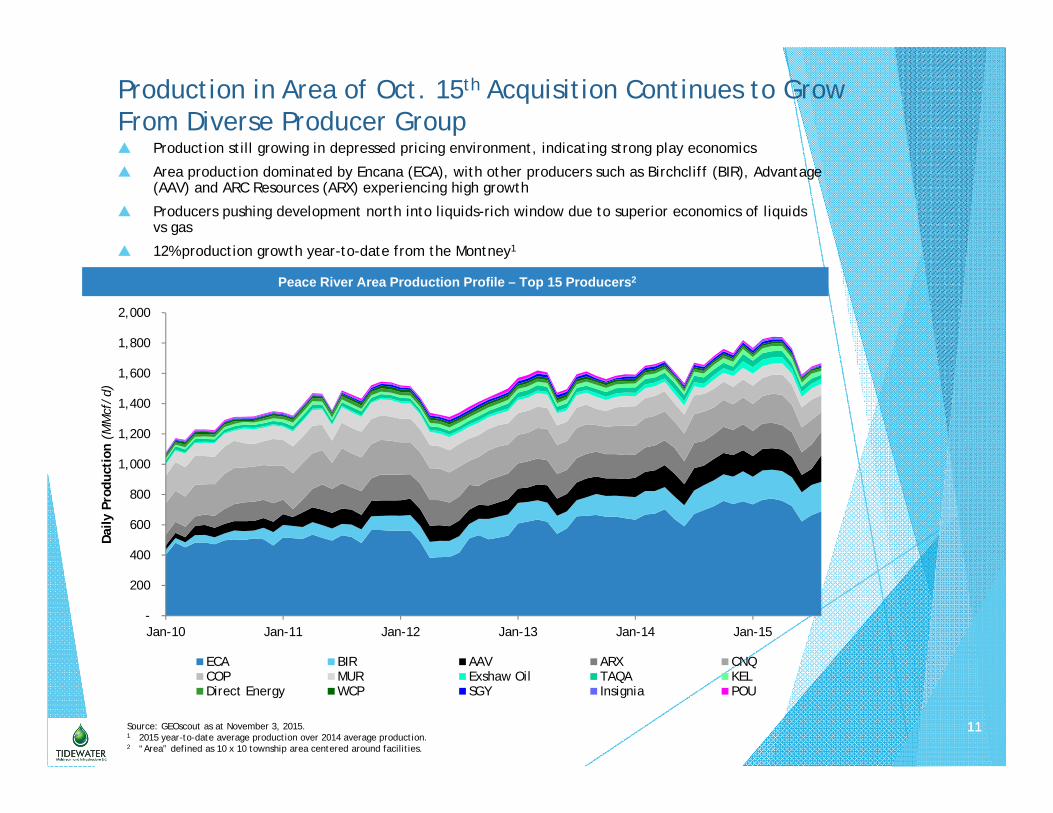

Production in Area of Oct. 15th Acquisition Continues to Grow From Diverse Producer Group

11

Peace River Area Production Profile – Top 15 Producers2

Production still growing in depressed pricing environment, indicating strong play economics

Area production dominated by Encana (ECA), with other producers such as Birchcliff (BIR), Advantage (AAV) and ARC Resources (ARX) experiencing high growth

Producers pushing development north into liquids-rich window due to superior economics of liquids vs gas

12% production growth year-to-date from the Montney1

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Dai

ly P

rodu

ctio

n (M

Mcf

/d)

ECA BIR AAV ARX CNQCOP MUR Exshaw Oil TAQA KELDirect Energy WCP SGY Insignia POU

Source: GEOscout as at November 3, 2015.1 2015 year-to-date average production over 2014 average production.2 “Area” defined as 10 x 10 township area centered around facilities.

12

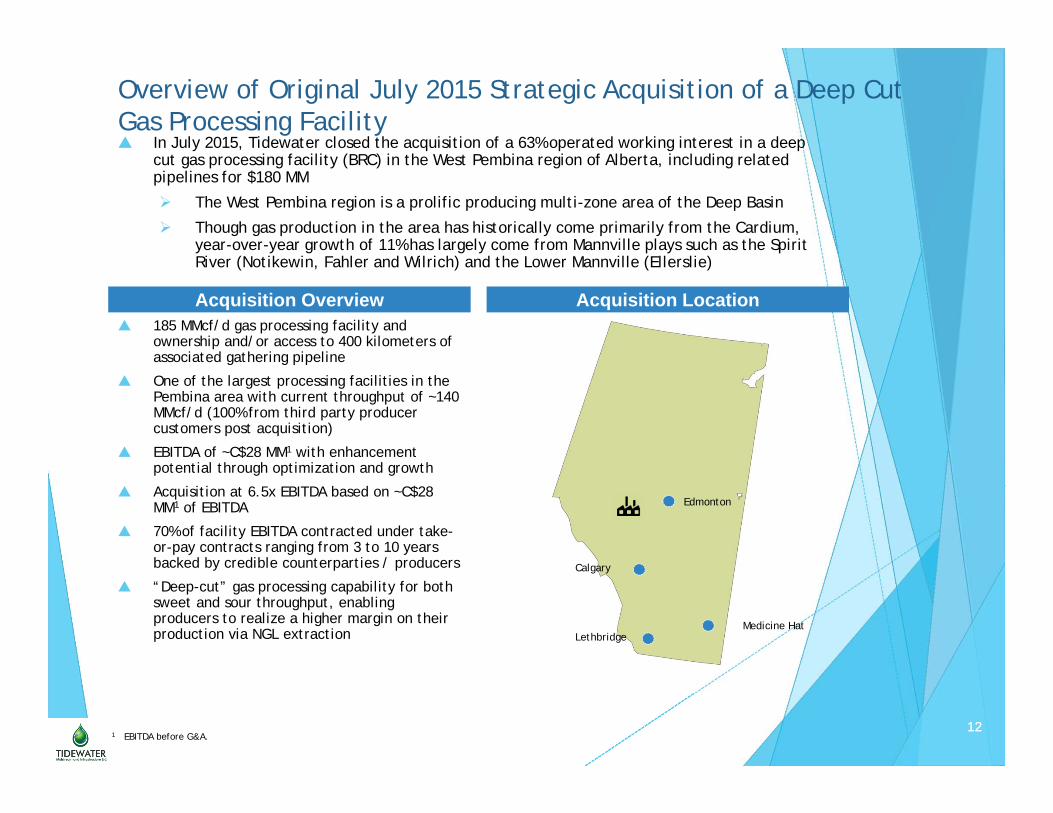

Overview of Original July 2015 Strategic Acquisition of a Deep Cut Gas Processing Facility In July 2015, Tidewater closed the acquisition of a 63% operated working interest in a deep

cut gas processing facility (BRC) in the West Pembina region of Alberta, including related pipelines for $180 MM

The West Pembina region is a prolific producing multi-zone area of the Deep Basin

Though gas production in the area has historically come primarily from the Cardium, year-over-year growth of 11% has largely come from Mannville plays such as the Spirit River (Notikewin, Fahler and Wilrich) and the Lower Mannville (Ellerslie)

12

Acquisition Overview 185 MMcf/d gas processing facility and

ownership and/or access to 400 kilometers of associated gathering pipeline

One of the largest processing facilities in the Pembina area with current throughput of ~140 MMcf/d (100% from third party producer customers post acquisition)

EBITDA of ~C$28 MM1 with enhancement potential through optimization and growth

Acquisition at 6.5x EBITDA based on ~C$28 MM1 of EBITDA

70% of facility EBITDA contracted under take-or-pay contracts ranging from 3 to 10 years backed by credible counterparties / producers

“Deep-cut” gas processing capability for both sweet and sour throughput, enabling producers to realize a higher margin on their production via NGL extraction

Acquisition Location

Edmonton

Calgary

Medicine HatLethbridge

1 EBITDA before G&A.

13

Production in Area of Original Acquisition Continues to Grow From Diverse Producer Group

13

West Pembina Area Production Profile – Top 15 Producers1

Liquids rich gas production by large producers driving strong demand for deep cut facilities

15+ producers have active production in the area

No single producer dominance

Bellatrix leads area production growth

-

200

400

600

800

1,000

1,200

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Dai

ly P

rodu

ctio

n (M

Mcf

/d)

COP BXE TAQA Direct Energy PWTTOU VET APA Sinopec WestbrickHSE BTE Velvet LTS PMT

Source: GEOscout as at November 3, 2015.1 “Area” defined as 10 x 10 township area centered around facilities.

14

Tidewater Is A High Growth Midstream Company

Tidewater adding significantly to shareholder value on a per share basis

EBITDA increased from zero to $25 MM after the first acquisition; 23% EBITDA growth since

Cash flow per share increased from zero to $0.14/share after the first acquisition; 21% CFPS growth since

Share price has increased 43% since IPO

…And maintaining a low risk capital structure with minimal debt

Current Capitalization EBITDA Growth ($MM)1,2

Current Capitalization (ProForma)

Mkt. Cap: $251 MM

Net Debt: $20 MM

TEV: $271 MM

Cash Flow per Share Growth ($/sh)2

1 EBITDA is net of incremental G&A. West Pembina acquisition includes $3 MM of G&A; G&A expected to increase to $4 MM pro forma acquisitions and NGL marketing operations.2 2016E H2 run-rate EBITDA and CFPS.

-

$25 $26 $28

$31

~$40

IPO (April 8,2015)

Pro Forma WestPembina

Acquisition (Jul.22, 2015)

Pro FormaPipeline

Acquisition (Sep.2, 2015)

Pro Forma PeaceRiver Area Gas

Plant Acquisition(Oct. 15, 2015)

Pro Forma GasPlant & PropaneAcquisition (Nov.

2, 2015)

OrganicImprovement at

ExistingFacilities and

Commencementof NGL

MarketingOperations in H2

2016

-

$0.14 $0.15 $0.16

$0.17

~$0.23

IPO (April 8,2015)

Pro Forma WestPembina

Acquisition (Jul.22, 2015)

Pro FormaPipeline

Acquisition (Sep.2, 2015)

Pro Forma PeaceRiver Area Gas

Plant Acquisition(Oct. 15, 2015)

Pro Forma GasPlant & PropaneAcquisition (Nov.

2, 2015)

OrganicImprovement at

ExistingFacilities and

Commencementof NGL

MarketingOperations in H2

2016

2

15

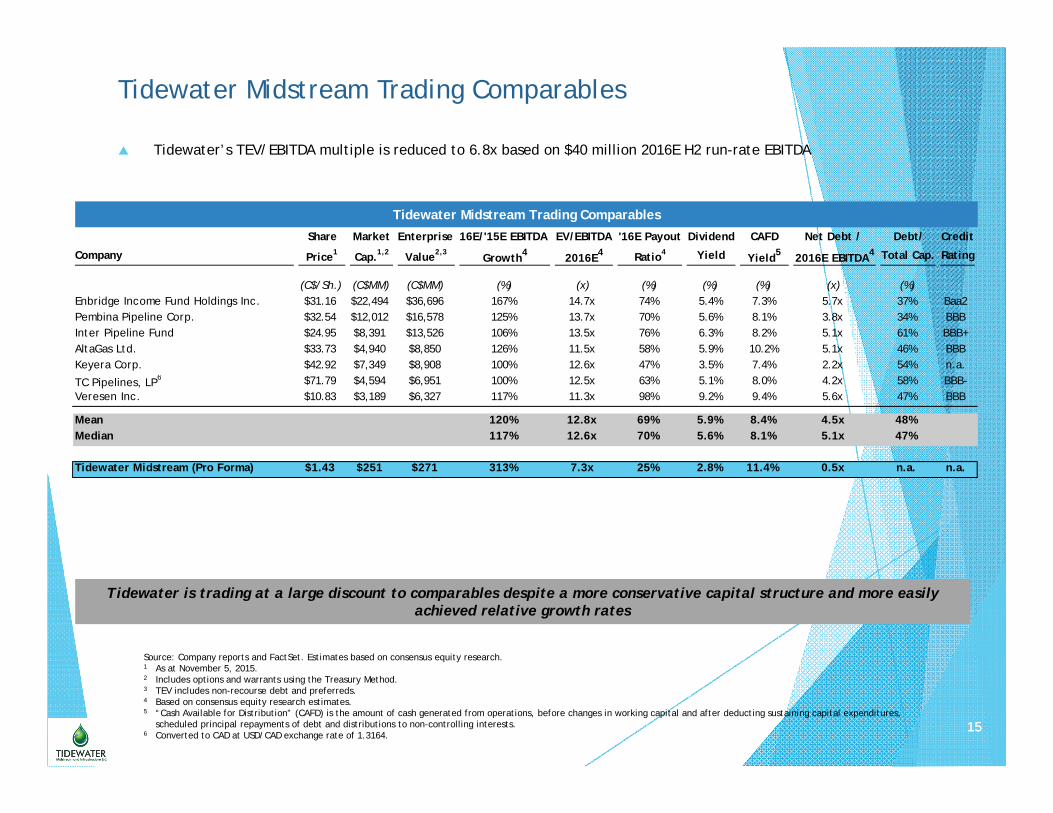

Tidewater Midstream Trading Comparables

15

Tidewater Midstream Trading Comparables

Source: Company reports and FactSet. Estimates based on consensus equity research.1 As at November 5, 2015.2 Includes options and warrants using the Treasury Method.3 TEV includes non-recourse debt and preferreds.4 Based on consensus equity research estimates.5 “Cash Available for Distribution” (CAFD) is the amount of cash generated from operations, before changes in working capital and after deducting sustaining capital expenditures,

scheduled principal repayments of debt and distributions to non-controlling interests.6 Converted to CAD at USD/CAD exchange rate of 1.3164.

Share Market Enterprise 16E/'15E EBITDA EV/EBITDA '16E Payout Dividend CAFD Net Debt / Debt/ Credit

Company Price1 Cap.1,2 Value2,3Growth4 2016E4 Ratio4 Yield Yield5 2016E EBITDA4 Total Cap. Rating

(C$/Sh.) (C$MM) (C$MM) (%) (x) (%) (%) (%) (x) (%)Enbridge Income Fund Holdings Inc. $31.16 $22,494 $36,696 167% 14.7x 74% 5.4% 7.3% 5.7x 37% Baa2Pembina Pipeline Corp. $32.54 $12,012 $16,578 125% 13.7x 70% 5.6% 8.1% 3.8x 34% BBBInter Pipeline Fund $24.95 $8,391 $13,526 106% 13.5x 76% 6.3% 8.2% 5.1x 61% BBB+AltaGas Ltd. $33.73 $4,940 $8,850 126% 11.5x 58% 5.9% 10.2% 5.1x 46% BBBKeyera Corp. $42.92 $7,349 $8,908 100% 12.6x 47% 3.5% 7.4% 2.2x 54% n.a.

TC Pipelines, LP6 $71.79 $4,594 $6,951 100% 12.5x 63% 5.1% 8.0% 4.2x 58% BBB-Veresen Inc. $10.83 $3,189 $6,327 117% 11.3x 98% 9.2% 9.4% 5.6x 47% BBB

Mean 120% 12.8x 69% 5.9% 8.4% 4.5x 48%Median 117% 12.6x 70% 5.6% 8.1% 5.1x 47%

Tidewater Midstream (Pro Forma) $1.43 $251 $271 313% 7.3x 25% 2.8% 11.4% 0.5x n.a. n.a.

Tidewater is trading at a large discount to comparables despite a more conservative capital structure and more easily achieved relative growth rates

Tidewater’s TEV/EBITDA multiple is reduced to 6.8x based on $40 million 2016E H2 run-rate EBITDA

16

Stock Symbol TSXV: TWM

Common Shares Outstanding 175.9 million

Options and RSU‘s 3.8 million

Insider Ownership (Fully Diluted) ~5.3%

Market Capitalization(1) $251 million

Current Net Debt $20 million

Enterprise Value $271 million

Annual Dividend $0.04/sh.

Current Yield(1) ~3%

Tidewater Corporate Profile

1 As at November 5, 2015.

17

Rights of Action for Damages or RescissionThe following statutory rights of action for damages or rescission will only apply to a purchaser of securities of Tidewater in the event that this corporate presentation is deemed to be an offering memorandum pursuant to applicable securities legislation in certain provinces of Canada. These remedies, or notice with respect thereto, must be exercised, or delivered, as the case may be, by the purchaser within the time limits prescribed by the applicable provisions of the provincial securities legislation. Purchasers should refer to the applicable securities legislation for the complete text of these rights or consult with a legal adviser. Where used in this section, “Misrepresentation” means an untrue statement of a material fact or an omission to state a material fact that is required to be stated or that is necessary to make a statement not misleading in light of the circumstances in which it was made.

Ontario

Securities legislation in Ontario provides that purchasers of securities are entitled to rights of action for rescission or damages where an offering memorandum and any amendment to it contains a Misrepresentation. In accordance with Section 130.1 of the Securities Act (Ontario) (the “Ontario Act”), in the event that an offering memorandum or any amendment thereto contains a Misrepresentation, a purchaser who purchases securities offered by such offering memorandum during the period of distribution has, without regard to whether the purchaser relied upon the Misrepresentation, a right of action against the issuer for damages, or, while still the owner of the such securities purchased by that purchaser, for rescission, in which case, if the purchaser elects to exercise the right of rescission, the purchaser will have no right of action for damages against the issuer, provided that: (a) the issuer will not be liable if it proves that the purchaser purchased the securities with knowledge of the Misrepresentation; (b) in the case of an action for damages, the issuer will not be liable for all or any portion of the damages that it proves do not represent the depreciation in value of the securities as a result of the Misrepresentation relied upon; and (c) in no case will the amount recoverable in any action exceed the price at which the securities were sold to the purchaser.

A purchaser resident in Ontario should refer to the provisions of the Ontario Act and its regulations for particulars of the rights and defences discussed above and consult with a lawyer. The rights discussed above are in addition to and without derogation from any other right or remedy which a purchaser might have at law.

No action shall be commenced to enforce these statutory rights more than: (a) in an action for rescission, 180 days from the date of the transaction that gave rise to the cause of action; or (b) in an action for damages, the earlier of: (i) 180 days after the plaintiff first had knowledge of the facts giving rise to the cause of action; or (ii) three years after the date of the transaction that gave rise to the cause of action.

Saskatchewan

A purchaser resident in the Province of Saskatchewan is given certain rights of action under The Securities Act, 1988 (Saskatchewan) (the “Saskatchewan Act”) if this corporate presentation or any amendment to this corporate presentation contains a Misrepresentation. These rights include, but are not limited to:

1. Section 80.1 – on receipt of an amended offering memorandum delivered in accordance with Subsection 80.1(3) of the Saskatchewan Act, the right to withdraw from an agreement to purchase securities by delivering a notice to the person who or company that is selling the securities indicating an intention not to be bound by the purchase agreement, such notice to be delivered within two business days after receipt of the amended offering memorandum.

2. Subsections 138(1) and 138(2) – a right of action for rescission or for damages against the issuer, its directors and every person selling the securities on behalf of the issuer where the offering memorandum and any amendment to the offering memorandum contains a Misrepresentation.

3. Subsection 138.1(3) – a right of action for damages against the issuer, its directors and every person selling the securities on behalf of the issuer for a Misrepresentation in advertising and sales literature.

4. Subsection 138.2(1) – a right of action for damages against an individual who makes a verbal Misrepresentation made before orcontemporaneously with the purchase of the securities.

5. Subsection 141(1) – a right to void the purchase agreement and recover the purchase price if the securities are sold by a vendor who is trading in contravention of the Saskatchewan Act or the regulations to the Saskatchewan Act.

6. Subsection 141(2) – a right of action for rescission or for damages if the offering memorandum or any amendment to the offering memorandum is not delivered to the purchaser as required by subsection 80.1 of the Saskatchewan Act.

17

18

Rights of Action for Damages or RescissionSuch rights of rescission and damages are subject to certain limitations including the following: (a) if the purchaser elects to exercise its right of rescission against the issuer, it shall have no right of action for damages against that party; (b) in an action for damages, a defendant will not be liable for all or any portion of the damages that the defendant proves do not represent the depreciation in value of the securities resulting from the Misrepresentation relied on; (c) no person or company, other than the issuer, will be liable for any part of the offering memorandum or any amendment to it purporting to be made on the person’s or company’s own authority as an expert or purporting to be a copy of or an extract from the person’s or company’s own report, opinion or statement as an expert, unless the person or company failed to conduct a reasonable investigation sufficient to provide reasonable grounds for a belief that there had been no Misrepresentation or believed there had been a Misrepresentation; (d) in no case shall the amount recoverable exceed the price at which the securities were offered; and no person or company is liable in an action for rescission or damages if that person or company proves that the purchaser purchased the securities with knowledge of the Misrepresentation.

A purchaser resident in Saskatchewan should refer to the provisions of the Saskatchewan Act and its regulations for particulars of the rights and defences discussed above and consult with a lawyer. The rights discussed above are in addition to and without derogation from any other right or remedy which a purchaser might have at law.

Pursuant to the Saskatchewan Act, the rights discussed above must be exercised within certain time periods. These time periods are: (a) an action for rescission must be started within 180 days after the date of the transaction that gave rise to the action; (b) an action for damages must be started by the earlier of (i) one year after the purchaser first had knowledge of the facts giving rise to the action; or (ii) six years after the date of the transaction that gave rise to the action.

Manitoba

Section 141.1 of the Securities Act (Manitoba) (the “Manitoba Act”) provides that where an offering memorandum contains a Misrepresentation, a purchaser who purchases a security offered by the offering memorandum is deemed to have relied upon that Misrepresentation, if it was a Misrepresentation at the time of purchase, and has a right of action for rescission against the issuer or has a right of action for damages against: (a) the issuer; (b) every director of the issuer at the date of the offering memorandum; and (c) every person who or company that signed the offering memorandum. If the purchaser elects to exercise its right of rescission against the issuer, the Purchaser shall have no right of action for damages against a person or company referred to above.

If a Misrepresentation is contained in a record that is incorporated by reference in, or that is deemed to be incorporated into, an offering memorandum, the Misrepresentation is deemed to be contained in the offering memorandum.

When a Misrepresentation is contained in an offering memorandum, no person or company is liable: (a) if the person or company proves that the purchaser had knowledge of the Misrepresentation; (b) other than with respect to the issuer, if the person or company proves: (i) that the offering memorandum was sent to the purchaser without the person's or company's knowledge or consent, and (ii) that, after becoming aware that it was sent, the person or company promptly gave reasonable notice to the issuer that it was sent without the person's or company's knowledge and consent; (c) other than with respect to the issuer, if the person or company proves that, after becoming aware of the Misrepresentation, the person or company withdrew the person's or company's consent to the offering memorandum and gave reasonable notice to the issuer of the withdrawal and the reason for it; (d) other than with respect to the issuer, if, with respect to any part of the offering memorandum purporting to be made on the authority of an expert or to be a copy of, or an extract from, an expert's report, opinion or statement, the person or company proves that the person or company did not have any reasonable grounds to believe and did not believe that: (i) there had been a Misrepresentation; or (ii) the relevant part of the offering memorandum: (A) did not fairly represent the expert's report, opinion or statement, or (B) was not a fair copy of, or an extract from, the expert's report, opinion or statement; or (e) other than with respect to the issuer, with respect to any part of the offering memorandum not purporting to be made on an expert's authority and not purporting to be a copy of, or an extract from, an expert's report, opinion or statement, unless the person or company: (i) did not conduct an investigation sufficient to provide reasonable grounds for a belief that there had been no Misrepresentation; or (ii) believed there had been a Misrepresentation.

Such rights of rescission and damages are subject to certain limitations including the following: (a) in an action for damages, a defendant is not liable for all or any part of the damages that it proves do not represent the depreciation in value of the securities as a result of the Misrepresentation; and (b) the amount recoverable shall not exceed the price at which the securities were offered under the offering memorandum.

No action may be commenced to enforce a right: (a) in the case of an action for rescission, more than180 days after the day of the transaction that gave rise to the cause of action; or (b) in any other case, more than the earlier of (i) 180 days after the day that the plaintiff first had knowledge of the facts giving rise to the cause of action, or (ii) two years after the day of the transaction that gave rise to the cause of action.

A purchaser resident in Manitoba should refer to the provisions of the Manitoba Act and its regulations for particulars of the rights and defences discussed above and consult with a lawyer. The rights discussed above are in addition to and without derogation from any other right or remedy which a purchaser might have at law.

18

19

Notice to InvestorsAll purchasers of securities will be required to execute a subscription agreement, which will contain representations, warranties, covenants and acknowledgments of the purchasers required by the relevant regulatory authorities, Tidewater and any agents or underwriters under the offering of securities to establish the availability of such exemptions and to ensure compliance with applicable securities legislation. This corporate presentation is qualified in its entirety by reference to such subscription agreement and any other agreements entered into in relation to the offering, including, without limitation, any agency agreement, underwriting not agreement or subscription receipt agreement. This corporate presentation is provided for informational purposes only as of the date hereof, may not be complete, and may not contain certain material information about the Corporation, including important disclosures relating to the final terms of he proposed investment, risk factors associated with an investment in the Corporation, and fees and expenses. The securities are being offered subject to various conditions, including (a) withdrawal, cancellation or modification of the offering of securities without notice, (b) the right of Tidewater to reject any subscription in whole or in part, (c) the approval of certain matters by legal counsel, and (d) the terms and conditions set out in any agency agreement, underwriting agreement, subscription receipt agreement or any other agreement pertaining to the offering, as the case may be. In making an investment decision, prospective investors must rely on their own due diligence examination of Tidewater and the terms of the offering, including the merits and risks involved. Prospective investors should not construe the contents of this corporate presentation as legal, tax, investment or accounting advice by Tidewater or any of its directors, officers, shareholders, employees, advisors or agents, including, without limitation, any agents or underwriters for the offering. This corporate presentation does not take into account the particular investment objectives or financial circumstances of any specific party who may receive it. Each party who reviews this corporate presentation must make its own independent assessment of Tidewater after making such investigations and each prospective investor is strongly urged to consult with its own advisors with respect to legal, tax, regulatory, financial and accounting matters, including the merits and the risks involved of any investment in Tidewater. In particular, any estimates or projections or opinions contained herein necessarily involve significant elements of subjective judgment, analysis and assumption and each recipient should satisfy itself in relation to such matters. Investment is suitable only for sophisticated investors and requires the financial ability and willingness to accept the potentially high risks and lack of liquidity that are characteristic of an investment in a newly listed company.

Certain information contained in this corporate presentation has been prepared by or derived from third-party sources. This corporate presentation has not been independently verified and the information contained within may be subject to updating, revision, verification and further amendment. While the information contained herein has been prepared in good faith, except as otherwise provided for herein, neither Tidewater, its directors, officers, shareholders, agents, employees, advisors or agents, including, without limitation, any agents or underwriters for the offering, give, has given or has authority to give, any representations or warranties (express or implied) as to, or in relation to, the accuracy, reliability or completeness of the information in this corporate presentation, or any revision thereof, or of any other written or oral information made or to be made available to any interested party or its advisers and liability therefore is expressly disclaimed.

Except as may be required by applicable law, in furnishing this corporate presentation, neither Tidewater nor any agent or underwriter for the offering undertakes or agrees to any obligation to provide the recipient with access to any additional information or to update this corporate presentation or to correct any inaccuracies in, or omissions from, this corporate presentation which may become apparent. This corporate presentation and its contents are confidential and is made available strictly for the purposes referred to above. In no circumstances will Tidewater or any agents or underwriters under the offering be responsible for any costs, losses or expenses incurred by investors in connection with any appraisal or investigation of Tidewater.

19