the water report 2017 - sqs.com · 25 feature anglian water’s innovation shop ... may seem like a...

TRANSCRIPT

JULY/AUGUST 2017

w

Ofwat's PR19 team on price control design, business plans, customer outcomes, cost e�ciency and �nanceability.

INSIDE WICS' SRC21 DECISIONS|ROSS ON FUTURE REGULATION|CEO STEVE ROBERTSON ON HIS FIRST YEAR AT THAMES WATER

COMPETITIONWATCH❙ Large customers are engaged and switching...but the market lacks wow factor. ❙ Emerging issues three months on from go-live.❙ Pennon Water Services' boss Richard Stanbrook on simplicity and service. ❙ Southern seeks retail partners on water efficiency.

WATER REPORTTHE

POLICY|REGULATION|COMPETITION

In full �ow...

OTHER SECTORS: ENERGY FROM WASTE | HANDLING & LOGISTICS | MACHINERY & EQUIPMENT | RECYCLERS & REPROCESSORS | DATA, TECH & SERVICES

REGISTER FOR FREE ENTRY AT rwmexhibition.com

Discover the future of the energy and water markets in the new Supply & Demand Zone at the RWM event.

Giving you the knowledge to maximise your energy and water resources.

Register today to get expert insight in two dedicated theatres, to discover the latest solutions for facilities and energy management and to benefit from exclusive networking tools and features designed to reduce costs and increase efficiency.

12-14 SEPTEMBER 2017 | NEC BIRMINGHAM

FORMERLY KNOWN AS:

SS002097 RWM WATER REPORT (S&D) PRINT A4 AD AW.indd 1 08/06/2017 13:55

THE WATER REPORT July/August 2017 3

COMPETITIONWATCHWATER

REPORTTHE

EDITORÕSCOMMENTEDITORÕSCOMMENT

CHALLENGE AND COLLABORATIONInevitably this month, all eyes are on PR19 (our coverage is on p8-15). The headline summary is that it is looking pretty tough for companies. There are few surprises in the methodology as the key aspects have been well consulted on. But taking the package as a whole, it poses a real challenge for the industry. A few examples: the opportunity to earn outperformance rewards does not make up for lower base returns; e�ciency baselines incorporate an element of frontier shift; and average performance is likely to incur ODI penalties.

Clearly Ofwat is doing its utmost to tip the scales more in favour of the customer, both �nancially and in terms of ‘fairness’. On the latter, witness in particular new debt indexation, tax cost pass through, and the move to CPIH.

Receiving less widespread attention is WICS’ latest work on its next price control for Scottish Water, SRC21 (see p16-18). It is fasci-nating to compare and contrast the two regulators’ approaches. Sure, the situations are not identical but nonetheless both regula-tors want the same thing: sustainable, resilient water and wastewa-ter services for the long term at the best possible price for custom-ers, delivered by innovative and e�cient companies. But they are going about it in di�erent ways.

PR19 is characterised by challenge: a tough regulator indicating its intention to hold prices down while demanding step changes in performance, with complex incentive mechanisms to oil the wheels. SRC21 is characterised by collaboration: a trusting regulator openly accepting upward price pressure on the back of rising investment which it sees as needed to do the right thing by future as well as cur-rent customers.

Ofwat and WICS have taken di�erent stances on other matters too. Whereas PR19 promotes more markets SRC21 dismisses them. On customer involvement, Ofwat has emphasised that customers must be welcomed as participants in the delivery of water servic-es, and has reinvigorated the Customer Challenge Group role but retained its �nal say on company business plans. WICS meanwhile has given the green light to the Customer Forum again to negoti-ate direct with Scottish Water. Assuming Ofwat stays on its current trajectory under whoever succeeds Cathryn Ross as chief executive in 2018, it will be fascinating to see whether challenge or collaboration delivers the best results.

Editor: Karma Loveday e:[email protected] t:07880 550945Art Editor: Numa Randell e:[email protected] t:07754269168Managing editor: Trevor Loveday e:[email protected] t:07949 579641Subscriptions: [email protected] Website: www.thewaterreport.co.ukAddress: The Water Report, 68 Church Street, Brighton BN1 1RLPublisher: Kew Place Limited

4 INTERVIEW Every challenge is an opportunity for Thames Water CEO Steve Robertson.

8 REPORT PR19: Overview and business plan assessment.

10 REPORT PR19: Multiple controls and new markets.

12 REPORT PR19: Customers and outcomes.

14 REPORT PR19: Cost e�ciency and �nance.

16 REPORT WICS’ initial SRC21 Decision Papers on the capital programme and prices.

19 REPORT Ofwat CEO Cathryn Ross on the future of independent regulation.

20 SQS urges revenue assurance action.

22 REPORT Unlocking the value of customer data.

24 NEWS REVIEW Wessex buys Flipper; EA reports on industry.

25 FEATURE Anglian Water’s Innovation Shop Window.

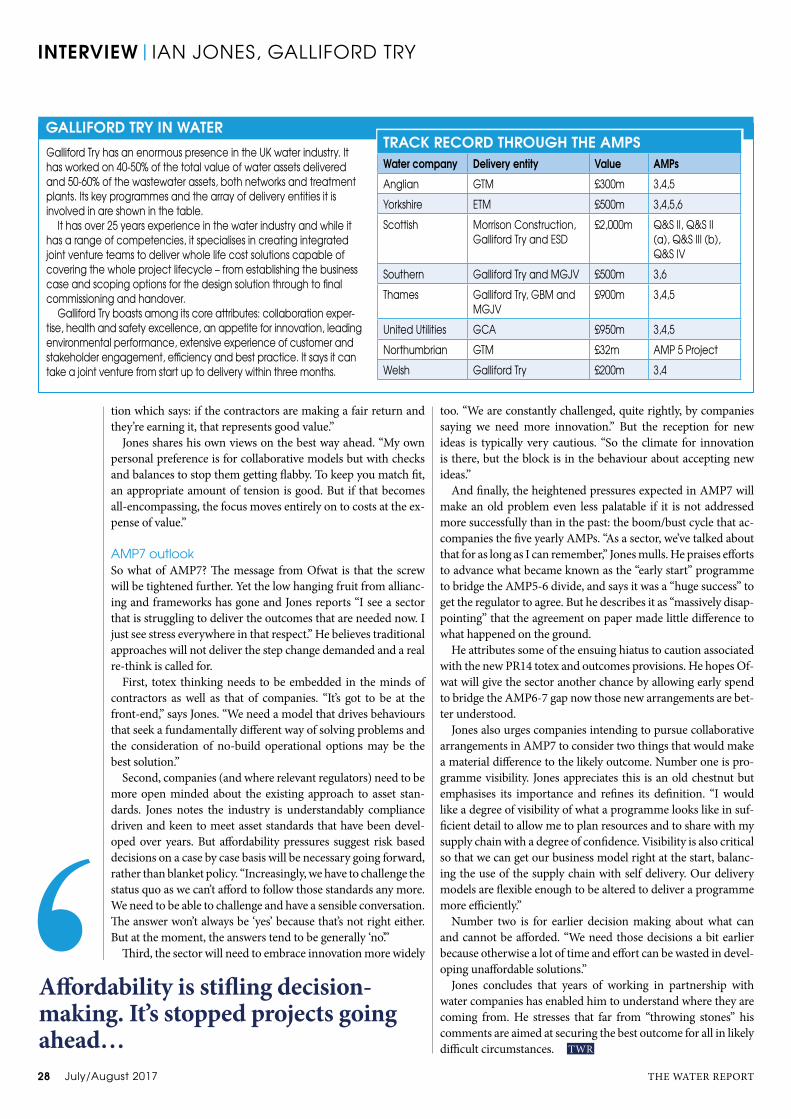

26 INTERVIEW Galliford Try’s water MD Ian Jones.

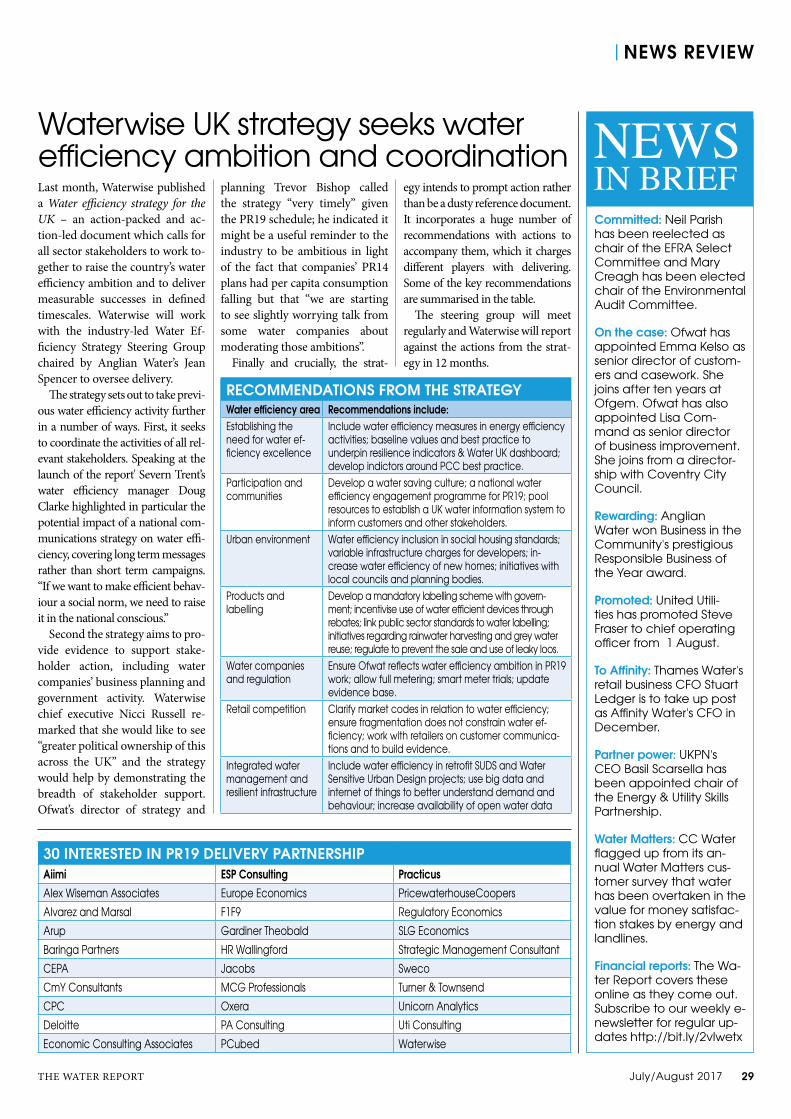

29 NEWS REVIEW Waterwise’s UK water e�ciency strategy.

30 NEWS REVIEW Alternative routes to abstraction reform.

31 REPORT Large customers engaged but deals lack wow factor.

34 REPORT The market, three months on.

36 INTERVIEW Richard Stanbrook says Pennon Water Services is in pursuit of scale.

38 REPORT Southern Water looks to partner with retailers on water e�ciency.

|CONTENTS

Karma Loveday, editor,The Water Report

Feedback, comments and suggestions very welcome.

Contact me on [email protected]

or 07880 550945.

July/August 2017 THE WATER REPORT4

INTERVIEW|STEVE ROBERTSON, THAMES WATER

It is coming up to a year since Steve Robertson became chief executive of �ames Water. To the casual observer, the job may seem like a poisoned chalice; a number of incidents have put �ames in the spotlight for all the wrong reasons

since Robertson started in September 2016. But he says the re-ality is much more balanced. “�ere are a lot of strengths in this business and we’ve got some really good historical perfor-mance but we need to remember that in our region we have a lot of growth, we have got the implications of climate change, and we’ve got some legacy performance issues, especially in the service area, that need addressing.”

On the strengths side, he praises the company’s sta�, many of whom have given years of dedicated service. He says the struc-ture of the organisation is �t for purpose and he likes what he sees the company doing on customer engagement – from the 60,000 water saving home visits completed, to schools work and how plans are shaping up for PR19. “I think we are quite close to being state of the art in that,” he observes.

Robertson highlights two areas in particular as falling short. First, the customer experience. While many indicators including complaints, SIM score and debt recovery are showing improve-ments, “if you look at how �ames Water has played in the cus-tomer services league tables …you can’t be happy if you are the CEO of the business with where we sit.” And second, infrastruc-ture. Network failings have attracted much of the recent bad press. Eight major trunk main bursts in London have brought the dual horrors of �ooding and supply outages. Meanwhile the

company missed its 2016/17 annual leakage target for the �rst time in ten years. Robertson knows he has his work cut out ad-dressing these issues and needs to make sure “we fully exploit all the options and opportunities of having the totex regime”.

Rising to the challengeWhile they are a priority, responding to the regulatory ‘requests’ recently made of �ames by Ofwat chairman Jonson Cox do not feature as a headline challenge, for the simple reason that the company has no di�culty meeting them. �e company notes that even the seemingly intrusive direction to review the compo-sition of the �ames board to ensure its independence and trust-worthiness is already required following recent Ofwat reforms of corporate governance. So on the face of it, Cox’s ‘de-mands’ seem relatively modest – though �ames points out that nevertheless they will re-quire considerable work to make sure that customers expectations are met in full. Under Robertson, �ames has already voluntarily moved to improve customer communications (see below), and to make its �nancial arrangements and investor returns clearer – for instance it has recently published Our taxes explained and Our �nances explained, two book-lets setting these aspects out in plain English.

Meanwhile, tying management rewards to performance for cus-tomers as well as investors is al-ready in place and very much in keeping with the general direc-tion of regulatory travel for PR19

EVERY CHALLENGE IS AN OPPORTUNITYSteve Robertson is facing Thames Water’s adversities head on and is determined to learn as much as he can from them to inform future strategy and delivery.

THE WATER REPORT July/August 2017 5

STEVE ROBERTSON, THAMES WATER|INTERVIEW

(see p12-13). And �ames’ Customer Challenge Group has al-ready requested joining up operational and �nancial reporting. Robertson responds: “I’m going to do it and actually I’m think-ing about what more can we do in that space. �at would be a minimal level from me. I want to think more imaginatively about how we engage with customers about our performance.”

Even the board composition request doesn’t jar. Robertson: “I think the point of Jonson’s comments is to say ‘look, you’ve got new investors coming in; you’ve got a chairman at the end of his tenure with the new chairman to be appointed; pay attention to the people who are coming in’. And from my point of view that’s �ne.” He points out that a number of new appointments have been made in the past few months anyway including indepen-dent non executive director Nick Land as well as new investor representatives a�er Borealis Infrastructure and Wren House ac-quired Macquarie’s 26.3% stake in the business on 31 May 2017.

He o�ers that the new recruits are “smart and have a long term view of the

business” which is not out of kil-ter with Cox’s priorities. “And

as time goes on, the board will evolve as well and over the next couple of years, there’ll be some members of the board who will reach the natural end of their tenure.” He adds that of course it will be “up to Jonson to take a view” on whether the new chairman and recomposed board de-liver his objectives, “but I

think we are in the process of doing exactly that”.

More generally, Robert-son is sanguine about

Ofwat’s – somewhat unusual – pub-

lic pleas. Cox’s comments were framed around the publication of �ames’ �nancial results and operating performance summary (see box, p7). While the leakage target miss was company spe-ci�c, �ames is far from alone in the industry on some of the other aspects in the line of �re – investor returns, gearing, man-agement rewards and balancing customer/�nancial interests. Yet Robertson does not object to being singled out: “We are who we are, we operate where we operate, we are the largest integrated water company, so I’m afraid you have to accept that when things happen, it’s going to be high pro�le. And if you think about the accumulation of the events that have happened – the big bursts before Christmas; we had a incident on Christmas Day at Hamp-ton; we have had lots stu� around the performance around leak-age etc etc – and when you mix all that together then by de�ni-tion you can expect public scrutiny.”

Nor is Robertson perturbed by this public scrutiny. “One of the things about running an infrastructure business is don’t do it, especially a business like �ames Water, if you’re going to get wobbly and angsty about the public scrutiny. I don’t start adopt-ing the ‘Oh it’s not fair…’ line. I have zero angst about the public nature. I only care about the substance and the outcomes.”

AmbitionSo what substance and outcomes might we expect to see? Rob-ertson is ambitious. “�ese moments represent an opportunity and a litmus test for us. When some bad stu� happens, you either use it as an opportunity to engage and as point of motivation to reset agendas etc or you pull the blinds down, shut o� your phone, hide under the desk and hope it goes away.” Clearly opt-ing for the former, he continues: “�e question is, what are we actually going to do di�erently, and how quick and how radical will we be? We can all agree about the direction; the question is how much do we embrace, how fast do we embrace and how far do we go? As you probably get the impression from me… I think we need to challenge ourselves…and the things that I was talking about earlier as areas of weakness that we need to ad-dress, are exactly those things that Jonson pointed out.”

Some changes have already been made, notably in the senior management team. Along with Robertson himself, the company has a new CFO and a new customer services director, as well as some

key internal promotions. Robertson notes he is delighted that some of these top roles have gone to women.

He is also keen to progress work that started be-fore he joined. A good example is implementing the new billing platform. “�at’s started and of course these are notoriously tricky programmes and we need to make sure that we land that; it’s a big focus,” he explains. Similarly he reports �ames has successfully implemented a new digital platform and needs to work now on “how we actually utilise it in terms of the website and for customer interaction; we need to make sure that we fully exploit that.”

It is a similar story on the delivery side of the business. Robertson’s predecessor Martin Baggs put three innovative and collectively incentivised delivery alliances in place: the eight2O alliance, the infrastructure alliance and the transformation and technology al-

July/August 2017 THE WATER REPORT6

liance. �e focus now will be on re�nement. “I don’t think that fundamentally we will be throwing everything up in the air,” Robertson asserts. “I think that getting a good set of partners working together is great and very bene�cial for us. But equally it would be wrong for us to say we can just sit back. Good things don’t happen just because you put a bunch of ingredients in and give it a bit of a shake then sit back. Good things happen through continually learning. And we are in a process of learning; these constructs are very ambitious and are quite di�erent. And what we need to do is to treat them like that.”

Customer centricityRobertson also intends to take the good work �ames has done on customer engagement to the next level, which will include developing the theme of customer participation. “One of the things I want to change is the way that we – philosophically – are addressing our customer base. In a sense they [customers] are very deep stakeholders inside this business…�at’s an area where we’ve been really focusing down and we’ve been making progress on so that when we build our business plans we have demonstrably intelligent well-informed customer input. And for our customers to input sensibly we have to be transparent and share, not just go ‘well what do you think’?”.

And that raises the issue of what the CEO describes as “a set of Russian dolls” in relation to company/customer relationships – that no aspect can really be looked at in isolation; rather one thing leads to another and all parts of the package are linked. So good customer engagement hinges on well informed customers

which hinges on transparency. Robertson: “It’s very important for us to engage externally and it’s very important to make sure that we are being exemplary in terms of our transparency with all our stakeholders especially our customers. One of the things that I think we could do better… is we can step back and say ‘if you look hard enough you can �nd out everything you need to �nd out about the business’, or we can be more proactive in making sure that it is really easy to understand stu� about the business.”

Aside from more transparent formal reporting, Robertson sees a strong role for social media here too. In his short time at at the company, improving �ames’ social media engagement has been a priority and the company’s Customer Challenge Group has already noted the success. He comments: “We didn’t have 24-hour social media coverage; and we tended to be very outward focused rather than interactive. Again I think we’re beginning to �nd our tone of voice; I don’t think we’re there yet again and I think that’s an area we can focus on. And also associated with that, use of digital channels full stop in terms of operating with our customers, I think there’s quite a lot we can do to develop in that space.”

Well informed customers that give insightful feedback will support the development of a truly customer centric business,

Robertson continues. “�at customer centricity needs to be in all the decision-making – whether it’s the [business] plan or how we handle an event or incident. It’s something that we need to focus on and it needs to be an area of continuous improvement and learning.”

Leakage and burstsRobertson is of course also prioritising addressing the infra-structure issues that have blighted his �rst year. An independent report into the trunk main bursts concluded there were no sys-temic failures to address, but that the company should prioritise higher risk �xes and improve its network monitoring capability. It is now investing £97m extra in this up to 2020 and is strate-gically considering how to deal with this asset class. Robertson notes: “It’s always tricky because you need to make the decision: when is it right to stop �xing it and start replacing it?”

�e leakage target miss was signi�cant. Robertson explains in part it was due to the bar being far higher this AMP; in part due to the Infrastructure Alliance taking longer to get up and running than envisaged. What with catching up with the leak �x backlog and trying to keep up with this year’s targets, he “doubts very much” whether �ames will hit its interim AMP6 targets, though he feels “pretty con�dent” it will be back on track by 2020.

But again he intends to extract a positive from a negative and will take the opportunity to learn lessons – and not only about the mobilisation period for a complicated structure like the In-frastructure Alliance. “I think there’s more to it than that. We need to think quite hard about what it is telling us about the con-dition of our network, the distribution of the leaks and how we handle customer side leakage more e�ectively – 30% of leakage is customer side and I think that we’ve got some good policies – we actually will go and �x it for free. But I think one of the learning areas for us is how to engage with our customers over customer side leakage better.” He adds: “We shouldn’t be too simplistic about this…When you have the aspiration to make another big step change in performance, you really need to be thinking very hard about exactly what you need to do to make it happen. And if it isn’t happening, really get underneath the underlying reasons why that is and then take corrective action.”

Similarly, Robertson sees lessons to learn from other targets it missed last year. �e company incurred £18.4 million in ODI penalties, partially o�set by £3.2 million rewards. He is very sup-portive of the ODI policy. He is not particularly ru�ed by the economic impact on the business (the penalties are small in rela-tive terms). “But I’m angsty about the fact that we didn’t hit some of the targets that we should’ve hit. A lot of them were relatively minor misses, but a miss is a miss. And while I know leakage was the big headline, you also need to apply the same thinking to some of the other areas as well.”

Looking at all the infrastructure issues in the round, Robert-son doesn’t �nd fault with �ames’ risk management capabili-ties: “I think we’re actually pretty good at risk management to be honest.” But he sees scope to be able to better predict the state of the network, including through innovative and technological means. “If we think about the internet of things and big data ana-lytics and automation and think about how that whole world can be applied to our business, I think there’s more we can do around that.” On the wastewater side, he points out “massive strides”

We can all agree about the direction; the question is how much do we em-brace, how fast do we embrace and how far do we go?

INTERVIEW|STEVE ROBERTSON, THAMES WATER

THE WATER REPORT July/August 2017 7

have been taken already both on the plant side and on modelling and monitoring the network – “but still you can’t sit back”. It is worth noting that the £20m pollution �ne �ames was hit with in the year was for historic spills and that the company has been at pains to explain its practices are now fundamentally di�erent.

Finally, not to lose sight of the bigger picture, Robertson and his team are planning a deep strategic review. “You can’t let these things happen and not ask some fundamental questions around that. �at’s the bigger challenge: making sure that we’ve got the right strategy across the whole of the business.”

Water resources, NHH and PR19Finally, we catch up on a few other important and topical issues. Firstly, his views on the water resources position; a long running subject for �ames. As CEO of the company that serves Lon-don – densely populated and hugely important nationally and internationally – security of supply is never far from Robert-son’s mind. He confesses: “When I came into the industry and I looked at the relative position of the southern part of the coun-try versus other parts of the country in terms of their resilience from a storage perspective, I was pretty shocked.” He has come to understand how we got to the current position, but argues: “People who aren’t in the water industry don’t understand that. �ey really don’t. And I didn’t. It’s like: why would you have 100 days resilience in the southern part of the country and 500 or 600 in other parts? Why would you do that? You just wouldn’t.”

He appreciates the need to “use the full toolkit” on resources, which includes demand management, improving leakage, catch-ment management and greater re-use of e�uent as well as supply enhancement. On the latter, he questions: “Do we need to have a disaster? Do we need to have a major event? Do we need to have something very bad happen before we are galvanised into mak-ing the right decision. Or are we smart enough to get aligned around a fact-based view of what needs to be done and actually get on with it?”

For his part, Robertson intends to keep his foot on the gas both operationally and in terms of stakeholder engagement. He points out too that environmental and ecological impacts need to be “taken seriously as well as part of this equation”. Is he opti-mistic about supply side progress in his tenure? “Right now I am sort of equivocal. I think that probably we are in a better place now than we have ever been for the past 20 years…but until it’s done, it’s not done.”

On non household retail, Robertson like everyone else in the industry is relieved the market has had a smooth start and seems genuinely pleased with how the transfer of �ames’ business customers to Castle Water has gone. But his experience in other markets, particularly as a wholesaler serving some 400 retailers, tells him we are only in the foothills of the challenge. He men-tions in particular sharpening up the wholesale/retail interface as one example. “On the one hand, we’ve got a bunch of retailers who have got to di�erentiate and on the other hand, we need to have as much standardisation in the wholesale supply chain as possible otherwise life becomes very, very di�cult if you want to work across multiple wholesalers. Working out those competing tensions in a way that ends up with a better set of products and a better sets of experiences for our business customers is some-thing we’ll have to work really, really hard at.”

And �nally, PR19. We met to do this interview on 10 July,

the day before Ofwat released its dra� price review methodol-ogy (see p8-15). He explained that his approach will be to try to match up the methodology with what he knows to be company reality.

“�e message I’m driving inside the business, and actually what is demanded by our board, is we need to take a long-term view in the business and take up a strategy that supports that.” His �rst task on reading the methodology will be to consider �ames’ activities on Ofwat’s four themes (a�ordability, resil-ience, customer service and innovation) and his second to work out how best to align �ames’ desire for long term optimisation with the regulator’s priorities: “How will this [methodology] play into that [corporate strategy] and how can we work with this methodology to absolutely make sure that it’s consistent with that approach?”

On �nanceability, does he anticipate �ames will need to re-spond directly to Ofwat’s well trailed support for signi�cantly lower base returns? “We’ll see what the detail is. But the over-all �nancial construct of the business will not get turned upside down by anything that comes out…�e idea that says one day we will wake up and go ‘Ah, you know, it would be quite nice if we were just leveraged to 70%, that would be really cool’. It’s not going to happen. You can set the direction but you have to put it in context of reality and of what we’ve got to do.” TWR

Financial highlights❙ £605 million underlying operating pro�t (2015/16: £742.2 million). ❙ £71.1 million pro�t before tax (2015/16: £511.2 million), due to fair value loss on �nancial instruments, increased costs and lower property sales. ❙ Capital expenditure of £1.1 billion on network and infrastructure, with around £12 billion invested in last 12 years. ❙ £100 million in dividends paid to external shareholders (2015/16: £nil).

Operational highlights❙ 2016/17 leakage reduction target missed by 47 million litres per day, which represents 1.8% of our average daily production. First miss for ten years. ❙ £18.4 million in ODI penalties (£8.6m on leakage plus smaller sums for supply interruptions of more than12h, security of supply index, sewer �ooding and discharge compliance), partially oªset by rewards of £3.2 million for improving on supply interruptions of less than four hours (£3.1m) and reducing the number of properties aªected by odour.❙ Transformed approach to preventing pollutions following oªences at six sites in the Thames Valley between 2012 and 2014, resulting in a £19.75 million �ne in 2017. “We’ve been more proactive in our wastewater network maintenance, changed our management structure in the aªected region and invested heavily in our infrastructure and control systems leading to a 42% reduction in incidents since 2013.” ❙ 99.96% drinking water quality compliance.❙ 267GWh of energy from sewage produced, best performance to date.❙ Largest water e�ciency programme in the industry. Measures including the installation of 146,000 smart water meters and 60,000 Smarter Home Visits pro-duced an annual saving of 22.2Ml/d, ahead of target.

Customer service highlights❙ 94.5% of complaints resolved �rst time, up from 90.9% in 2015/16. ❙ At £374 a year, customers continue to bene�t from the third lowest average combined water and wastewater bill in England and Wales. ❙ £14.6 million reduction in bad debt expense caused by customer non-pay-ment. ❙ SIM score moved from 76.7 to 77.3 points out of 100.

PERFORMANCE SUMMARY 2016/17

STEVE ROBERTSON, THAMES WATER|INTERVIEW

July/August 2017 THE WATER REPORT8

REPORT|PR19 DRAFT METHODOLOGY

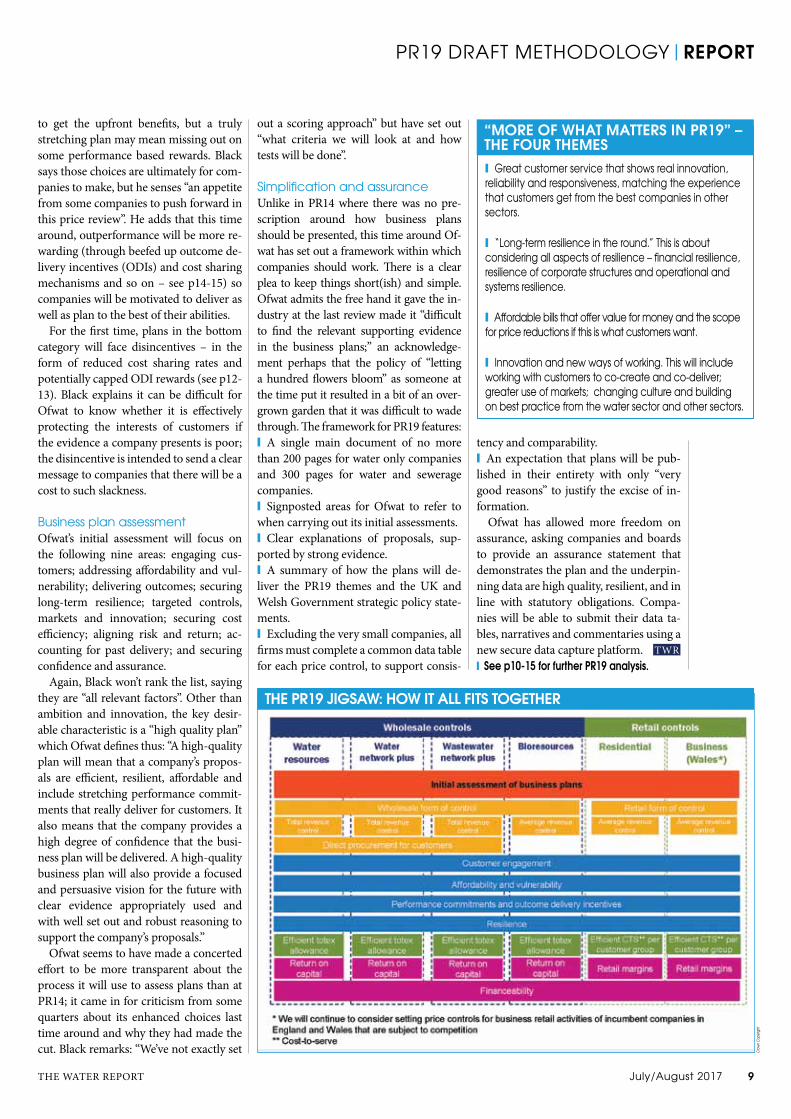

Ofwat’s four themes for its PR19 dra� methodology published on 11 July – cus-tomer service, long term

resilience, a�ordability and innovation (see box) – came as no surprise. �e reg-ulator’s top team had been trailing them for some weeks in speeches and, just ahead of the launch, on Twitter. But the document itself really hammers home the message that these are the priority is-sues: the themes are woven through the paper and head up each chapter.

But how should a water company look-ing at these headline messages set about hitting the optimum mix, given that trade o�s will almost certainly be needed? Se-nior director of Water 2020 David Black won’t be drawn to rank the four themes. “�ey’re all important,” he says. “�ere’s no prede�ned idea about where the bal-ance sits.” He elaborates that the four themes are “all about the customer, now and in the long term” and says he sees “lots of opportunity” from lower �nancing costs and greater e�ciency to deliver for customers in the round. Nor does Black seem to buy the argument that a�ordabil-ity and resilience in particular are pulling

in di�erent directions.”A�ordability for all is important, so average bills are impor-tant,” he says. “And it is important to ad-dress resilience. But resilience is not just about the spend – there are a range of op-tions to mitigate the e�ect on bills.”

Exceptional to abysmal So companies will need to plough through the detail and make judgements, �rmly in consultation with their customers, about how best to deliver great customer ser-vice and long term resilience within the envelope of an a�ordable-for-all bill. �e fourth theme, innovation, could at least in part be the key to the other three and will clearly be highly prized by Ofwat when it assesses business plans.

Four business plan grades have been earmarked for PR19, up from the two –enhanced and standard – used at PR14: ❙ Exceptional status will be awarded to plans that are high-quality with signi�cant ambition and innovation for customers.❙ Fast track status will be given to plans that are high-quality and do not require material intervention to protect customer interests, but which are not ambitious and innovative enough to attain exceptional status.

PR19: FROM ENHANCED TO EXCEPTIONALBusiness plan innovation and ambition will set the best apart from the rest while disincentives will be applied at the bottom.

❙ Slow track status will be given to plans where material interventions are required in some areas to protect the interests of customers.❙ Signi�cant scrutiny status will be given to plans which fall well short of the re-quired quality and where major interven-tions are required to protect the interests of customers.

Ofwat reserves the right not to use all categories but wants to have them avail-able. Black says he “really hopes some plans will make the exceptional category”; meanwhile there is “no reason why any-one should end up in signi�cant scru-tiny” but the regulator wants to have the category there – perhaps as a deterrent as much as anything.

Clearly it will be ambition and innova-tion that will separate the elite from the next best. Black points out this is a break with PR14. �en it was all about the qual-ity of the plan. �is time around, a high quality plan alone will get you to fast track status but to be exceptional “you must go above and beyond and really shi� the frontier forward”. �ere seems to be con-siderable �exibility around which areas Ofwat will reward frontier-shi� in. Black provides some examples: “It might be the frontier on cost, or on outcomes, or on re-silience.” Ofwat believes innovation and e�cient risk management will be key to delivering any such ambition. And that both innovation and ambition will hinge on understanding customers’ needs better and operating more e�ciently – which point towards companies collaborating more with customers, other stakeholders and in some circumstances each other.

Plans in the top two tiers will receive early dra� determinations in March/April 2019 instead of July 2019, with ex-ceptional plans also bene�ting from a �-nancial reward (0.2% of RORE) and the reputational kudos of being elite. Will these rewards be su�cient to incentiv-ise companies to really push themselves? Bear in mind that PR14 enhancement can be viewed as a double-edged sword: great

THE TIMELINE FOR PR19 11 JULY 2017

PR19 draft methodolgy consultaton published

JULY-AUGUST 2017

Continued engagement

through consultation

period

30 AUGUST 2017

PR19 draft methodolgy consultaton

closes

3 SEPTEMBER 2018

Companies submit

business plans to Ofwat

MID DECEMBER

2017 Final PR19

methodolgy published

JANUARY 2019 Initial

assessment of business plans

published

MARCH-APRIL 2019 Draft

determinations (exceptional

and fast track plans)

APRIL 2019 Companies

submit revisions to

buiness plans (signi�cant

scrutiny and slow track)

JULY 2019 Draft

determinations (slow

track and signi�cant scrutiny)

DECEMBER 2019 Final

determinations published

REPORT|PR19 DRAFT METHODOLOGY

The PR19 top team: David Black, Aileen Armstrong and John Russell

THE WATER REPORT July/August 2017 9

PR19 DRAFT METHODOLOGY|REPORT

to get the upfront bene�ts, but a truly stretching plan may mean missing out on some performance based rewards. Black says those choices are ultimately for com-panies to make, but he senses “an appetite from some companies to push forward in this price review”. He adds that this time around, outperformance will be more re-warding (through beefed up outcome de-livery incentives (ODIs) and cost sharing mechanisms and so on – see p14-15) so companies will be motivated to deliver as well as plan to the best of their abilities.

For the �rst time, plans in the bottom category will face disincentives – in the form of reduced cost sharing rates and potentially capped ODI rewards (see p12-13). Black explains it can be di�cult for Ofwat to know whether it is e�ectively protecting the interests of customers if the evidence a company presents is poor; the disincentive is intended to send a clear message to companies that there will be a cost to such slackness.

Business plan assessmentOfwat’s initial assessment will focus on the following nine areas: engaging cus-tomers; addressing a�ordability and vul-nerability; delivering outcomes; securing long-term resilience; targeted controls, markets and innovation; securing cost e�ciency; aligning risk and return; ac-counting for past delivery; and securing con�dence and assurance.

Again, Black won’t rank the list, saying they are “all relevant factors”. Other than ambition and innovation, the key desir-able characteristic is a “high quality plan” which Ofwat de�nes thus: “A high-quality plan will mean that a company’s propos-als are e�cient, resilient, a�ordable and include stretching performance commit-ments that really deliver for customers. It also means that the company provides a high degree of con�dence that the busi-ness plan will be delivered. A high-quality business plan will also provide a focused and persuasive vision for the future with clear evidence appropriately used and with well set out and robust reasoning to support the company’s proposals.”

Ofwat seems to have made a concerted e�ort to be more transparent about the process it will use to assess plans than at PR14; it came in for criticism from some quarters about its enhanced choices last time around and why they had made the cut. Black remarks: “We’ve not exactly set

out a scoring approach” but have set out “what criteria we will look at and how tests will be done”.

Simpli�cation and assuranceUnlike in PR14 where there was no pre-scription around how business plans should be presented, this time around Of-wat has set out a framework within which companies should work. �ere is a clear plea to keep things short(ish) and simple. Ofwat admits the free hand it gave the in-dustry at the last review made it “di�cult to �nd the relevant supporting evidence in the business plans;” an acknowledge-ment perhaps that the policy of “letting a hundred �owers bloom” as someone at the time put it resulted in a bit of an over-grown garden that it was di�cult to wade through. �e framework for PR19 features:❙ A single main document of no more than 200 pages for water only companies and 300 pages for water and sewerage companies.❙ Signposted areas for Ofwat to refer to when carrying out its initial assessments.❙ Clear explanations of proposals, sup-ported by strong evidence. ❙ A summary of how the plans will de-liver the PR19 themes and the UK and Welsh Government strategic policy state-ments.❙ Excluding the very small companies, all �rms must complete a common data table for each price control, to support consis-

tency and comparability. ❙ An expectation that plans will be pub-lished in their entirety with only “very good reasons” to justify the excise of in-formation.

Ofwat has allowed more freedom on assurance, asking companies and boards to provide an assurance statement that demonstrates the plan and the underpin-ning data are high quality, resilient, and in line with statutory obligations. Compa-nies will be able to submit their data ta-bles, narratives and commentaries using a new secure data capture platform. TWR❙ See p10-15 for further PR19 analysis.

❙ Great customer service that shows real innovation, reliability and responsiveness, matching the experience that customers get from the best companies in other sectors.

❙ “Long-term resilience in the round.” This is about considering all aspects of resilience – �nancial resilience, resilience of corporate structures and operational and systems resilience.

❙ Aªordable bills that oªer value for money and the scope for price reductions if this is what customers want.

❙ Innovation and new ways of working. This will include working with customers to co-create and co-deliver; greater use of markets; changing culture and building on best practice from the water sector and other sectors.

“MORE OF WHAT MATTERS IN PR19” – THE FOUR THEMES

THE PR19 JIGSAW: HOW IT ALL FITS TOGETHER

Crow

n Cop

yrigh

t

July/August 2017 THE WATER REPORT10

REPORT|PR19 DRAFT METHODOLOGY

The industry has known since Ofwat published a decision document in May 2016 that multiple price con-trols would be a feature of PR19. As

widely consulted on, there are to be four main wholesale controls: one each for the new water resources and bioresources markets and one each for the remaining wholesale water and wastewater activities. On top of that, there is to be a standalone control speci�cally for �ames Water’s Tideway activities.

Ofwat will set wholesale controls using a “building block” approach, for a period of �ve years (see diagram). �ese blocks incorporate:❙ Returns and depreciation of the Regula-tory Capital Value (RCV)❙ An assessment of e�cient totex during the 2020-25 period❙ Funding expenditure to be recovered within the period (determined by the pay as you go ratio; and expenditure added to the RCV and recovered in future periods (through future returns and depreciation).❙ An allowance for corporation tax.

From 1 April 2020, RCV will be split so half remains indexed to the retail price in-dex and the remainder, plus all RCV addi-tions, will be indexed to a more customer-friendly index, which Ofwat is proposing should be CPIH (see p14-15).

Weighted average revenue controls will be used for non competitive retail, with the jury out on arrangements for the com-petitive retail segment.

Wholesale: network plus controls�e water and wastewater network plus controls will be set on broadly the same basis as the wholesale water and waste-water controls at PR14. Network plus water will contain all the water RCV not allocated to the water resources control

(which will be done using an unfocused approach). Likewise, network plus waste-water will contain all the wastewater RCV not allocated to the bioresources control (which will be done using a focused ap-proach). Each company will propose its own allocations of RCV between the con-trols for Ofwat to review.

A couple of speci�c considerations to mention are:❙ Developer services charges – Ofwat proposes including these within the scope of the network plus revenue controls but with an adjustment mechanism for changes in the volume of developer ser-vices over 2020-25, to be applied at the end of the period.❙ Water trading incentives – Ofwat pro-poses to maintain PR14 water trading in-centives, both export and import, for new water trades agreed in 2020-25. It notes the incentives have little a�ected AMP6 plans, but suggests this may be because the incentives were only con�rmed a�er dra� water resources management plans had been submitted. “2020-25 may be the �rst time we can fully assess their impact,” it says. Payments will re�ect the move to separate controls.

Wholesale: new market controls �e methodology crystallises Ofwat’s plans for introducing water and biore-sources markets. It reiterates that water trading is slow; removing barriers, en-couraging third parties to sell water into public supply and – further down the line – enabling third parties in England to supply non household water retailers di-rect (the bilateral market) could all bene�t customers. In bioresources, the regulator believes there is scope to drive e�ciency from increased optimisation of activities across the companies – and, again looking

PR19: MULTIPLE CONTROLS AND NEW MARKETSOfwat’s draft methodology has con�rmed its direction of travel on markets and controls, and �eshed out new detail.

further ahead – greater participation from �rms operating in wider waste markets.

Both new markets will feature infor-mation requirements to enable others to identify opportunities to o�er services, if they can provide them at a lower cost and/or a higher quality. In addition for water resources, water companies will be required to produce a bid assessment framework “to create more clarity and con�dence to third parties that their bids to supply water resources, leakage or de-mand management services will be as-sessed fairly”.

Unless resolved, external factors look set to hinder the development of both these new markets. �e government’s de-cision not to progress primary legislation to enact abstraction reform at this time will undoubtedly constrain the potential of water trades, while an ongoing wrangle over the di�erent regulations that govern food waste and sludge could hold up cross sector collaboration and codigestion. Of-wat’s senior director for Water 2020 David Black admits there could be “increased opportunity” without these dark clouds on the horizon. But he sees neither as “an absolute barrier to the development of these markets”. �e message being: make progress where you can.

�e water resources control contains a number of features to cater for the future development of a bilateral market: ❙ Bilateral market entry should trigger an in-period revenue adjustment. Ofwat comments: “Otherwise, customers would be funding duplicate investment in water resources and we would be protecting companies from exposure to the bilateral market.” �e adjustment uses water re-sources yield as a measure of capacity.❙ Access pricing – companies must sub-mit proposed access prices as part of their business plans. �ey need to show how their proposed access prices align with their own costs and how they will help fa-cilitate the bilateral market on an equiva-lent basis. Further details on these aspects are promised for autumn. ❙ Exposure to utilisation risk – despite opposition from most companies, Ofwat is to press on and expect the industry to share the risk of large scale under or over investment in capacity. It said: “We ex-pect water companies proposing signi�-cant investment in new water resources to also propose long-term risk sharing arrangements as part of their business

THE WATER REPORT July/August 2017 11

PR19 DRAFT METHODOLOGY|REPORT

plans for us to review. �is is a targeted and proportionate approach and allows the arrangements to be tied to the nature of the investment over the long term.”

Among Ofwat’s proposals for the biore-sources market are:❙ �e return and depreciation on e�-ciently incurred investment will be recov-erable in the 2020-25 period. Post-2020 investment incorporates all investment – there is to be no distinction between maintaining existing bioresources treat-ment capacity and building new capacity.❙ More details on how allowed average revenue will be calculated for each charg-ing year have been shared. ❙ A penalty will be applied for signi�cant inaccuracies in sludge volume forecasts in companies’ business plans for variations greater than ±3% from the forecast used in setting the revenue control. Revenue will be returned to customers where �ve year total sludge volumes are greater than 7% of those used in setting the revenue control. �ese adjustments will be applied as part of the 2020-25 reconciliation at PR24.

Wholesale: direct procurementDirect procurement – the plan to require water companies to procure high value project services and �nance competitively rather than under their own auspices – remains work in progress but more detail has surfaced. Ofwat has retained its view that companies should consider direct procurement for relatively discrete, large-scale enhancement projects expected to cost over £100 million based on whole-life totex. �e methodolgy provides some guidance on the most suitable projects and Ofwat states explicitly that it expects companies to consider using direct pro-curement for suitable projects when busi-ness planning, with particular focus on tenders that are likely to deliver the great-est customer bene�t.

�e methodology considers and sees the merit in a number of tender mod-els – for example, those including and excluding initial design, and those that use an ‘early’ and ‘late’ approach. It will allow companies the �exibility to choose and will consider as part of its initial as-sessment of business plans whether the proposed tender model will deliver the anticipated bene�ts.

Unlike Ofgem with OFTOs, Ofwat has decreed it will not run any tenders. “Com-panies will be the purchaser and will run

the procurement process, then manage the competitively appointed provider (CAP).” It adds that it expects appoin-tees to run a fair and open procurement process and not to bid into the process in their own area.

In terms of contract term, the regula-tor advises 15-25 years. Companies will be allowed to recover the cost of tender-ing a project under base totex allowances under their existing price controls. �eir licences will be amended to allow them to recover the CAP’s revenue from their customers.

Finally in the wholesale controls space, catchment markets get a �eeting men-tion: “In addition to promoting markets in water resources, bioresources and direct procurement, water companies should also consider that greater use of markets in other parts of the value chain. For example water companies could make greater use of markets in catchment management.” Black comments that such initiatives are enabled by the totex framework and do not need special provision beyond it.

Retail controlsPR19 retail controls are complicated by the division between competitive non household and monopoly household re-tail, as well as by the absence of switch-ing opportunity in Wales for all except the

largest (50Ml) water customers. For domestic customers, the intention

is to continue to use a weighted average revenue control, where appropriate taking account of di�erent costs by customer type for residential retail activities in England and Wales. An average revenue control will also be used for business retail customers in Wales not subject to competition.

Ofwat is going to continue to consider setting price controls for business re-tail activities of incumbent England and Welsh companies that are subject to com-petition. It does not plan to set price con-trols for companies that have exited the market as the former customers of these companies are protected by the retail exit code. A small number of monopoly wa-ter companies have not exited the market and hence their customers do not have the backstop protections of this code. Of-wat is still considering what form of price regulation should apply here.

Finally, the regulator is consulting on three-year retail price controls, on the grounds that business retail competition in England could yield valuable informa-tion – for instance on the cost of retail activities and the broader service bene�ts for customers. Ofwat says a three year control would enable bene�ts to be passed on to customers more quickly than a stan-dard �ve year control.

THE BUILDING BLOCKS OF THE WHOLESALE REVENUE CONTROLS

July/August 2017 THE WATER REPORT12

REPORT|PR19 DRAFT METHODOLOGY

The customer understandably sits front and centre of the PR19 meth-odology. Ofwat had previously set out its approach to customer en-

gagement in its Customer engagement policy statement and expectations for PR19. To recap, this demands companies un-derstand their customers better through a “step change” in customer engagement using a wider range of techniques than at PR14. And on top of the seven principles of good customer engagement in play at the last review, Ofwat has added seven more, including customer participation (its Tapped In work from March); engage-ment on long term resilience; engagement with business end customers on wholesale services; better use of customer data (its Unlocking the value of customer data work from last month, see report p22-23); and communications expectations.

Customer engagement will of course be central to the assessment of business plans, with support provided by Custom-er Challenge Groups.

Aªordability and resilience�e regulator has been highlighting since at least March (when Jonson Cox spoke to Water UK’s City Conference) that it sees signi�cant scope for bill reductions and/

or investment in service for 2020-25 from bargain basement �nancing costs and e�ciency savings. Anyone who hoped growing evidence of the need for greater resilience would mean prices would be entirely trumped by investment will have been disappointed by the regulator’s on-going prioritisation of a�ordable bills for all. It wants to see plans that are a�ord-able and value for money, with companies demonstrating understanding of how dif-ferent customer types will be impacted and making an e�ort to keep bill pro�les as well as levels under control.

It also wants evidence of long term af-fordability. �e methodology paper says: “We, as well as customers and the CCGs, want to see companies being fair to future generations. Companies should make ap-propriate decisions on investment and costs to ensure they are not storing up problems for subsequent price control pe-riods and future customers.”

Finally, there is an expectation to bet-ter help those who struggle to pay. Ofwat notes only 1% of all customers are on social tari�s, although 11% of English customers and 15% of Welsh customers spend more than 5% of their disposable income on water bills. According to the paper: “Companies need to o�er a range

PR19: CUSTOMERS AND OUTCOMESCompanies are charged with balancing aªordability and resilience for customers, and will be put to the test with stretching outcomes and incentives.

of assistance options and be more pro-active in getting those to customers who struggle, or are at risk of struggling, to pay their bills. �ey need to work with other organisations to help these customers.”

�e initial assessment of business plans will scrutinise each of these three aspects of a�ordability against �ve principles us-ing both qualitative and quantitative mea-sures.

On top of this, for the �rst time vulner-ability will be an explicit part of the price review. Ofwat plans to use qualitative information to assess how business plans support customers in circumstances that make them vulnerable, based on chal-lenges it set in its 2016 Vulnerability re-port. �is will include scrutiny of how companies use data and engage with oth-ers to support those in vulnerable circum-stances and how targeted, e�cient and e�ective companies’ measures to address vulnerability are. CCGs are expected to assist here and provide an independent assessment of company e�orts.

Moreover, vulnerability has been ear-marked as an area for bespoke perfor-mance commitments (PCs - see below), backed up by a requirement for �rms to develop common measures for address-ing vulnerability, and to report on the data they gather.

However, while keeping bills a�ord-able is a priority, the methodology is equally clear that companies must also deliver services that are “resilient in the round” – which in Ofwat’s eyes means operationally, �nancially and corpo-rately resilient. �e a�ordability and re-silience demands together amount to a real challenge for �rms. Ofwat has pro-duced seven resilience principles to help companies understand what it expects of them (see box). Its initial assessment of business plans will seek to establish �rst, how well the company has identi�ed and prioritised risk to systems and services; second, how well it has assessed and selected mitigation options; and third, whether customers support company proposals.

�e theme of resilience is woven throughout the methodology, featuring prominently, for instance, in the sections on outcomes and cost assessment. Ofwat gently reminds companies too that it will only fund activities additional to those funded under previous price controls: in short, it won’t allow customers to pay twice.

PROPOSED COMMON PERFORMANCE COMMITMENTS FOR PR19

Crow

n Cop

yrigh

t

THE WATER REPORT July/August 2017 13

PR19 DRAFT METHODOLOGY|REPORT

Outcomes �e outcomes framework will govern how all of this, and more, translates into actual deliverables for customers. �e methodology cements Ofwat’s message when it consulted on outcomes late last year: that PCs will be more stretching and outcome delivery incentives (ODIs) will pack more of a punch.

On a practical level, the ten common PCs consulted on in November have evolved considerably. �ere are now 14 common commitments in the frame, with standard de�nitions (see diagram).

�ese cover the most important issues for customers such as reducing leakage, supply interruptions, the environment, resilience and asset health. �ese com-mon PCs enable customers and stake-holders to understand the performance commitment levels companies are signing up to, compared with other companies.

�ere is also a greater focus on resil-ience than was apparent in November: two common PCs are devoted to resil-ience and a further four to asset health. Senior director of Water 2020 David Black comments: “We’ve been working with the sector on developing these, to standardise asset health measures… the common metrics make it easier and more transparent to measure asset health across the companies… We’ve also got common PCs around resilience and this is very much to try to look forward.”

Bespoke PCs are also permitted, though a number of must-cover areas have been earmarked, including: vulnerability, envi-ronmental impact, resilience and the Ab-straction Incentive Mechanism.

Stretch and SIMOfwat is expecting companies to stretch themselves across the board, but is setting some particular parameters for certain common PCs. For supply interruptions and sewer �ooding, for instance, it ex-pects companies to set their PC levels at least at upper quartile performance level in 2024-25. Black explains: “PR14 had very much a historical approach to upper quartile performance. Now water compa-nies should be looking at where they proj-ect upper quartile will be so that in 2025, customers aren’t paying for something that was e�cient in 2017.”

On leakage, the regulator has told com-panies to set more stretching PCs than last time around: “We expect companies

to justify their proposals against options including a 15% reduction by 2025 or up-per quartile performance on leakage per property per day.”

�e Service Incentive Mechanism is in for an overhaul too. Black says: “SIM has been a success and there has certainly been improvement. However there were signs of convergence… and there is evidence that the sector is still lagging behind perfor-mance in other sectors. We see that from the UK Customer Service Index (UKCSI) and evidence coming out of the retail review. We really want companies to press forward [as] customer service is one of the themes of the review so we thought very hard about how we can de�ne an incentive to encourage companies to stretch in this space.”

�e SIM will be replaced by two new mechanisms:❙ C-MeX – for domestic customers. Com-panies are to be assessed on both perfor-mance with customers who make contact and more general customer satisfaction. More contact channels including social me-dia are to be factored in too and in period incentives will be applied. Higher rewards will be available for companies which dem-onstrate upper quartile performance in comparison to other sectors in UKCSI.❙ D-MeX – �is new measure will gauge developer satisfaction. Phone surveys are likely though the mechanism is still in de-velopment.

No measure has been proposed to gauge retailer satisfaction with wholesal-ers at this stage.

ODIs�ese performance incentives are to be beefed up considerably. �e overall range for value of ODIs will be increased to -3% to +3% RORE (this is the upper end and it is unlikely a company would hit the extremes; Ofwat recommends a range of +/- 1%-3%). PR14 design restrictions are to be removed and �nancial ODIs and in-period incentives are to be the default where customers are supportive (with companies expected to smooth bill impacts). End-of-period ODIs will a�ect revenue rather than Regulatory Capital Value. Ofwat will also encourage compa-nies to provide contextual information on performance, such as league tables.

Earning rewards will be challenging; Ofwat says average performance is likely to incur a penalty – it suggests �rms “are able to manage this risk by ensuring they

deliver for customers”. However super rewards are to be available for frontier-shi�ing performance on common PCs: “We will encourage companies to propose enhanced, higher, rewards for signi�cant performance improvement which moves the industry forwards as part of their ODIs for the common PCs,” the paper says. “�is proposal mimics how a com-petitive market rewards and spreads in-novation. �e enhanced rewards should be accompanied by increased penalties for very poor performance.”

Black elaborates on the super rewards policy: “�is is very much linked to the innovation theme and what we can do to promote more innovation in the sector.

One of the barriers to innovation is that when companies look at options that are less tried and tested, o�en these new ways have greater potential. We really wanted to recognise that when companies do a brave thing and push the boundaries beyond what is delivered today, that the compa-nies should be entitled to take a higher level of reward…It is very much focused on payment by results so where innovation succeeds, companies get a higher return but where it doesn’t succeed, customers shouldn’t have to pay for that.” TWR

❙ Resilience must be considered in the round and over the short, medium and long terms. ❙ Resilient ecosystems and biodiversity underpin many of the key services provided by companies.❙ Resilience decisions should be informed by engage-ment with customers.❙ Companies should consider a full range of mitigation actions including collaboration with other companies. ❙ Plans should provide best value solutions for the long term. ❙ Choices on resilience should inform outcomes.❙ Board assurance on the above is needed.

OFWAT’S RESILIENCE PRINCIPLES

It is very much focused on payment by results

so where innovation succeeds, companies

get a higher return but where it doesn't succeed,

customers shouldn't have to pay for that.

July/August 2017 THE WATER REPORT14

REPORT|PR19 DRAFT METHODOLOGY

In the preceding pages, we have dis-cussed what Ofwat wants companies to deliver for customers at PR19 and what it expects of them. In the �nal part of

our analysis here, we look at how the regu-lator plans to incentivise companies to de-liver and the returns it will allow them to earn for the risk they will be taking.

�e driving logic behind the regulator’s plan is to align the interests of compa-nies and their investors with the interests of their customers. �is means a greater proportion of reward hingeing on de-livery of what matters to customers. For companies – some more than others – it’s all looking pretty tight.

Cost of capitalAs usual Ofwat will set the cost of capital for wholesale services by allowing a re-turn on RCV, in reference to an e�cient notional capital structure. �e cost of cap-ital will be set at company level, then the cost of capital for each wholesale control set with reference to this.

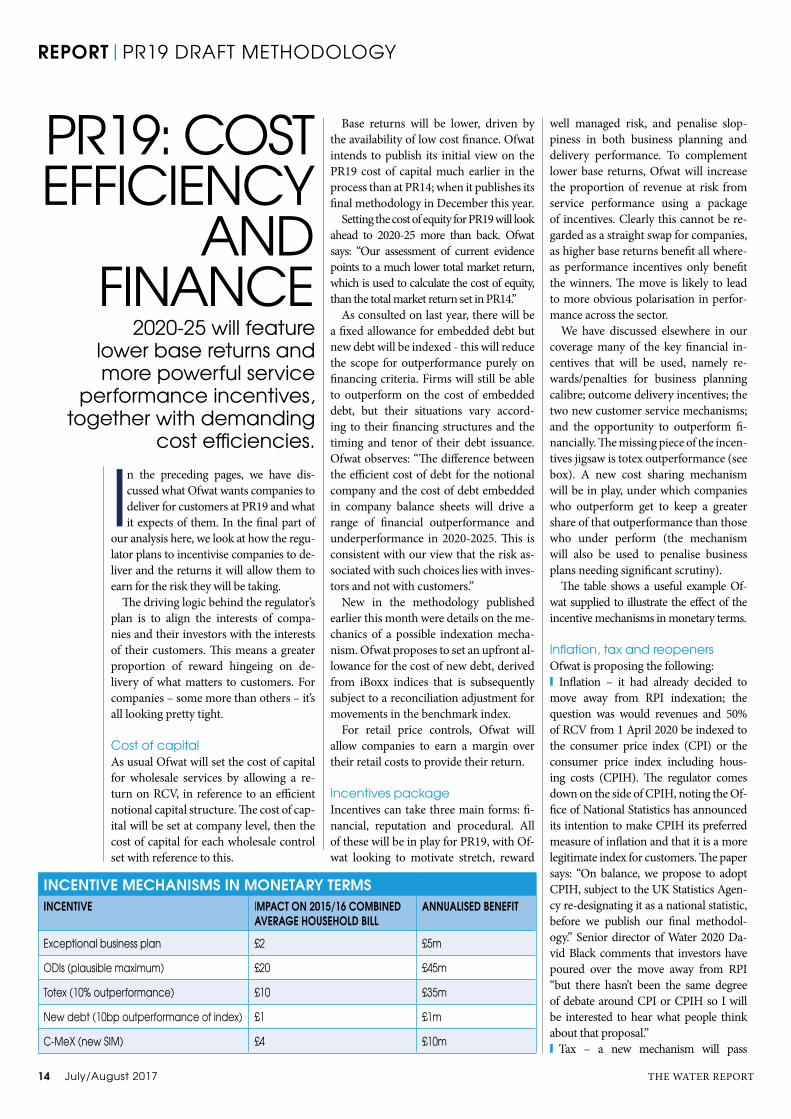

PR19: COST EFFICIENCY

AND FINANCE

2020-25 will feature lower base returns and more powerful service

performance incentives, together with demanding

cost e�ciencies.

INCENTIVE MECHANISMS IN MONETARY TERMSINCENTIVE IMPACT ON 2015/16 COMBINED

AVERAGE HOUSEHOLD BILLANNUALISED BENEFIT

Exceptional business plan £2 £5m

ODIs (plausible maximum) £20 £45m

Totex (10% outperformance) £10 £35m

New debt (10bp outperformance of index) £1 £1m

C-MeX (new SIM) £4 £10m

Base returns will be lower, driven by the availability of low cost �nance. Ofwat intends to publish its initial view on the PR19 cost of capital much earlier in the process than at PR14; when it publishes its �nal methodology in December this year.

Setting the cost of equity for PR19 will look ahead to 2020-25 more than back. Ofwat says: “Our assessment of current evidence points to a much lower total market return, which is used to calculate the cost of equity, than the total market return set in PR14.”

As consulted on last year, there will be a �xed allowance for embedded debt but new debt will be indexed - this will reduce the scope for outperformance purely on �nancing criteria. Firms will still be able to outperform on the cost of embedded debt, but their situations vary accord-ing to their �nancing structures and the timing and tenor of their debt issuance. Ofwat observes: “�e di�erence between the e�cient cost of debt for the notional company and the cost of debt embedded in company balance sheets will drive a range of �nancial outperformance and underperformance in 2020-2025. �is is consistent with our view that the risk as-sociated with such choices lies with inves-tors and not with customers.”

New in the methodology published earlier this month were details on the me-chanics of a possible indexation mecha-nism. Ofwat proposes to set an upfront al-lowance for the cost of new debt, derived from iBoxx indices that is subsequently subject to a reconciliation adjustment for movements in the benchmark index.

For retail price controls, Ofwat will allow companies to earn a margin over their retail costs to provide their return.

Incentives package Incentives can take three main forms: �-nancial, reputation and procedural. All of these will be in play for PR19, with Of-wat looking to motivate stretch, reward

well managed risk, and penalise slop-piness in both business planning and delivery performance. To complement lower base returns, Ofwat will increase the proportion of revenue at risk from service performance using a package of incentives. Clearly this cannot be re-garded as a straight swap for companies, as higher base returns bene�t all where-as performance incentives only bene�t the winners. �e move is likely to lead to more obvious polarisation in perfor-mance across the sector.

We have discussed elsewhere in our coverage many of the key �nancial in-centives that will be used, namely re-wards/penalties for business planning calibre; outcome delivery incentives; the two new customer service mechanisms; and the opportunity to outperform �-nancially. �e missing piece of the incen-tives jigsaw is totex outperformance (see box). A new cost sharing mechanism will be in play, under which companies who outperform get to keep a greater share of that outperformance than those who under perform (the mechanism will also be used to penalise business plans needing signi�cant scrutiny).

�e table shows a useful example Of-wat supplied to illustrate the e�ect of the incentive mechanisms in monetary terms.

In�ation, tax and reopenersOfwat is proposing the following: ❙ In�ation – it had already decided to move away from RPI indexation; the question was would revenues and 50% of RCV from 1 April 2020 be indexed to the consumer price index (CPI) or the consumer price index including hous-ing costs (CPIH). �e regulator comes down on the side of CPIH, noting the Of-�ce of National Statistics has announced its intention to make CPIH its preferred measure of in�ation and that it is a more legitimate index for customers. �e paper says: “On balance, we propose to adopt CPIH, subject to the UK Statistics Agen-cy re-designating it as a national statistic, before we publish our �nal methodol-ogy.” Senior director of Water 2020 Da-vid Black comments that investors have poured over the move away from RPI “but there hasn’t been the same degree of debate around CPI or CPIH so I will be interested to hear what people think about that proposal.” ❙ Tax – a new mechanism will pass

THE WATER REPORT July/August 2017 15

PR19 DRAFT METHODOLOGY|REPORT

through material changes in tax to custom-ers. Customers will bene�t where there are reductions in tax rates that were not antici-pated at the time of the price determination. ❙ Re-openers – there will be a high evi-dential bar. “�ere is no presumption that the Noti�ed Items that apply in 2015-20 should remain for 2020-25.”

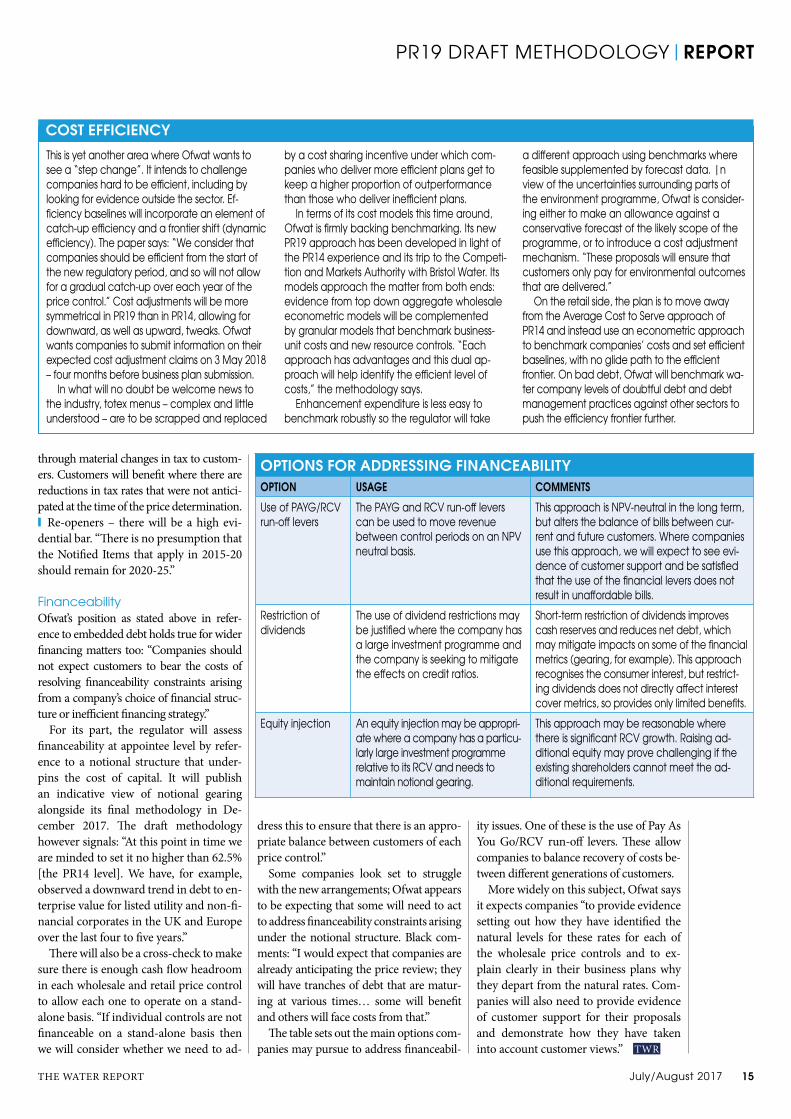

FinanceabilityOfwat’s position as stated above in refer-ence to embedded debt holds true for wider �nancing matters too: “Companies should not expect customers to bear the costs of resolving �nanceability constraints arising from a company’s choice of �nancial struc-ture or ine�cient �nancing strategy.”

For its part, the regulator will assess �nanceability at appointee level by refer-ence to a notional structure that under-pins the cost of capital. It will publish an indicative view of notional gearing alongside its �nal methodology in De-cember 2017. �e dra� methodology however signals: “At this point in time we are minded to set it no higher than 62.5% [the PR14 level]. We have, for example, observed a downward trend in debt to en-terprise value for listed utility and non-�-nancial corporates in the UK and Europe over the last four to �ve years.”

�ere will also be a cross-check to make sure there is enough cash �ow headroom in each wholesale and retail price control to allow each one to operate on a stand-alone basis. “If individual controls are not �nanceable on a stand-alone basis then we will consider whether we need to ad-

dress this to ensure that there is an appro-priate balance between customers of each price control.”

Some companies look set to struggle with the new arrangements; Ofwat appears to be expecting that some will need to act to address �nanceability constraints arising under the notional structure. Black com-ments: “I would expect that companies are already anticipating the price review; they will have tranches of debt that are matur-ing at various times… some will bene�t and others will face costs from that.”

�e table sets out the main options com-panies may pursue to address �nanceabil-

ity issues. One of these is the use of Pay As You Go/RCV run-o� levers. �ese allow companies to balance recovery of costs be-tween di�erent generations of customers.

More widely on this subject, Ofwat says it expects companies “to provide evidence setting out how they have identi�ed the natural levels for these rates for each of the wholesale price controls and to ex-plain clearly in their business plans why they depart from the natural rates. Com-panies will also need to provide evidence of customer support for their proposals and demonstrate how they have taken into account customer views.” TWR

This is yet another area where Ofwat wants to see a “step change”. It intends to challenge companies hard to be e�cient, including by looking for evidence outside the sector. Ef-�ciency baselines will incorporate an element of catch-up e�ciency and a frontier shift (dynamic e�ciency). The paper says: “We consider that companies should be e�cient from the start of the new regulatory period, and so will not allow for a gradual catch-up over each year of the price control.” Cost adjustments will be more symmetrical in PR19 than in PR14, allowing for downward, as well as upward, tweaks. Ofwat wants companies to submit information on their expected cost adjustment claims on 3 May 2018 – four months before business plan submission.

In what will no doubt be welcome news to the industry, totex menus – complex and little understood – are to be scrapped and replaced

by a cost sharing incentive under which com-panies who deliver more e�cient plans get to keep a higher proportion of outperformance than those who deliver ine�cient plans.

In terms of its cost models this time around, Ofwat is �rmly backing benchmarking. Its new PR19 approach has been developed in light of the PR14 experience and its trip to the Competi-tion and Markets Authority with Bristol Water. Its models approach the matter from both ends: evidence from top down aggregate wholesale econometric models will be complemented by granular models that benchmark business-unit costs and new resource controls. “Each approach has advantages and this dual ap-proach will help identify the e�cient level of costs,” the methodology says.

Enhancement expenditure is less easy to benchmark robustly so the regulator will take

a diªerent approach using benchmarks where feasible supplemented by forecast data. |n view of the uncertainties surrounding parts of the environment programme, Ofwat is consider-ing either to make an allowance against a conservative forecast of the likely scope of the programme, or to introduce a cost adjustment mechanism. “These proposals will ensure that customers only pay for environmental outcomes that are delivered.”

On the retail side, the plan is to move away from the Average Cost to Serve approach of PR14 and instead use an econometric approach to benchmark companies’ costs and set e�cient baselines, with no glide path to the e�cient frontier. On bad debt, Ofwat will benchmark wa-ter company levels of doubtful debt and debt management practices against other sectors to push the e�ciency frontier further.

COST EFFICIENCY

OPTIONS FOR ADDRESSING FINANCEABILITYOPTION USAGE COMMENTSUse of PAYG/RCV run-oª levers

The PAYG and RCV run-oª levers can be used to move revenue between control periods on an NPV neutral basis.

This approach is NPV-neutral in the long term, but alters the balance of bills between cur-rent and future customers. Where companies use this approach, we will expect to see evi-dence of customer support and be satis�ed that the use of the �nancial levers does not result in unaªordable bills.

Restriction of dividends

The use of dividend restrictions may be justi�ed where the company has a large investment programme and the company is seeking to mitigate the eªects on credit ratios.

Short-term restriction of dividends improves cash reserves and reduces net debt, which may mitigate impacts on some of the �nancial metrics (gearing, for example). This approach recognises the consumer interest, but restrict-ing dividends does not directly aªect interest cover metrics, so provides only limited bene�ts.

Equity injection An equity injection may be appropri-ate where a company has a particu-larly large investment programme relative to its RCV and needs to maintain notional gearing.

This approach may be reasonable where there is signi�cant RCV growth. Raising ad-ditional equity may prove challenging if the existing shareholders cannot meet the ad-ditional requirements.

July/August 2017 THE WATER REPORT16

REPORT|SRC21

As we have previously re-ported, the Water Industry Commission for Scotland has adopted the principles of

Ethical Based Regulation (EBR) for Scot-tish Water’s forthcoming price control – the Strategic Review of Charges 2021-27 (SRC21). �e regulator says it intends to conduct a transparent and collabora-tive price review, and – having signed a Cooperation Agreement with Scottish

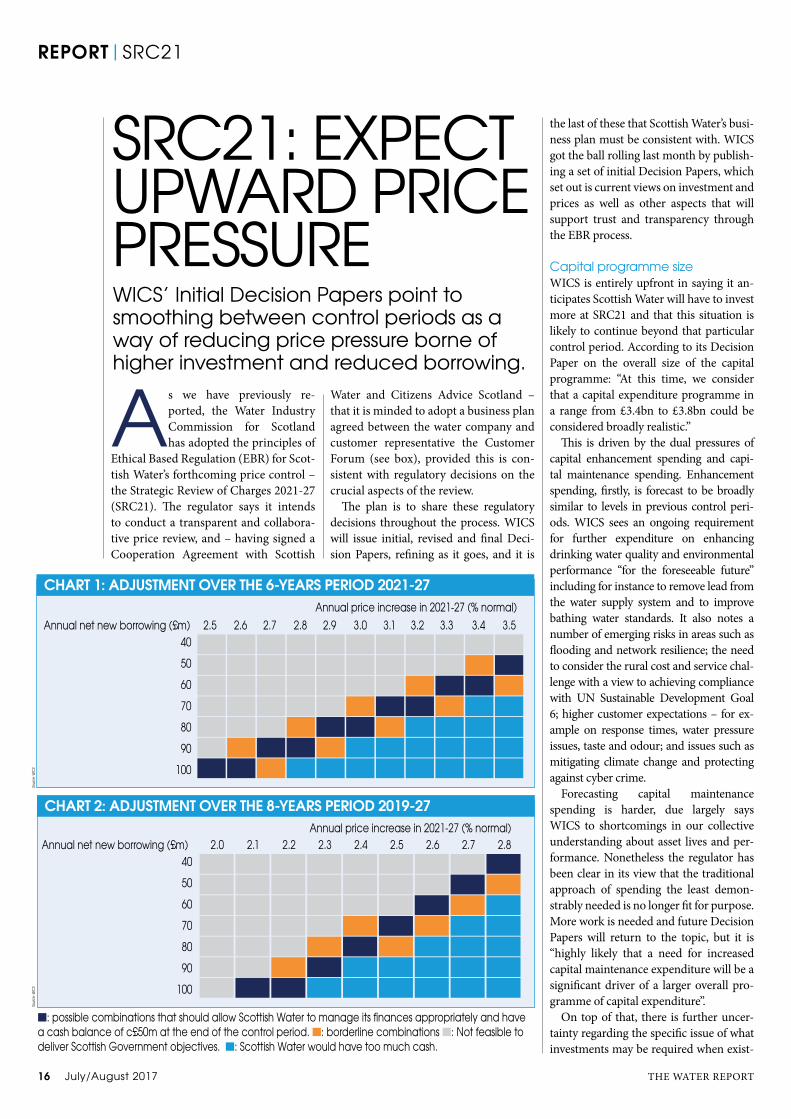

CHART 1: ADJUSTMENT OVER THE 6-YEARS PERIOD 2021-27

Annual net new borrowing (£m) 2.5 2.6 2.7 2.8 2.9 3.0 3.1 3.2 3.3 3.4 3.5405060708090

100

Annual price increase in 2021-27 (% normal)

CHART 2: ADJUSTMENT OVER THE 8-YEARS PERIOD 2019-27

Annual net new borrowing (£m) 2.0 2.1 2.2 2.3 2.4 2.5 2.6 2.7 2.8405060708090

100

Annual price increase in 2021-27 (% normal)

SRC21: EXPECT UPWARD PRICE PRESSUREWICS’ Initial Decision Papers point to smoothing between control periods as a way of reducing price pressure borne of higher investment and reduced borrowing.

Water and Citizens Advice Scotland – that it is minded to adopt a business plan agreed between the water company and customer representative the Customer Forum (see box), provided this is con-sistent with regulatory decisions on the crucial aspects of the review.

�e plan is to share these regulatory decisions throughout the process. WICS will issue initial, revised and �nal Deci-sion Papers, re�ning as it goes, and it is

the last of these that Scottish Water’s busi-ness plan must be consistent with. WICS got the ball rolling last month by publish-ing a set of initial Decision Papers, which set out is current views on investment and prices as well as other aspects that will support trust and transparency through the EBR process.

Capital programme sizeWICS is entirely upfront in saying it an-ticipates Scottish Water will have to invest more at SRC21 and that this situation is likely to continue beyond that particular control period. According to its Decision Paper on the overall size of the capital programme: “At this time, we consider that a capital expenditure programme in a range from £3.4bn to £3.8bn could be considered broadly realistic.”

�is is driven by the dual pressures of capital enhancement spending and capi-tal maintenance spending. Enhancement spending, �rstly, is forecast to be broadly similar to levels in previous control peri-ods. WICS sees an ongoing requirement for further expenditure on enhancing drinking water quality and environmental performance “for the foreseeable future” including for instance to remove lead from the water supply system and to improve bathing water standards. It also notes a number of emerging risks in areas such as �ooding and network resilience; the need to consider the rural cost and service chal-lenge with a view to achieving compliance with UN Sustainable Development Goal 6; higher customer expectations – for ex-ample on response times, water pressure issues, taste and odour; and issues such as mitigating climate change and protecting against cyber crime.

Forecasting capital maintenance spending is harder, due largely says WICS to shortcomings in our collective understanding about asset lives and per-formance. Nonetheless the regulator has been clear in its view that the traditional approach of spending the least demon-strably needed is no longer �t for purpose. More work is needed and future Decision Papers will return to the topic, but it is “highly likely that a need for increased capital maintenance expenditure will be a signi�cant driver of a larger overall pro-gramme of capital expenditure”.

On top of that, there is further uncer-tainty regarding the speci�c issue of what investments may be required when exist-

■: possible combinations that should allow Scottish Water to manage its �nances appropriately and have a cash balance of c£50m at the end of the control period. ■: borderline combinations ■: Not feasible to deliver Scottish Government objectives. ■: Scottish Water would have too much cash.

Sourc

e: W

ICS

Sourc

e: W

ICS

THE WATER REPORT July/August 2017 17

SRC21|REPORT

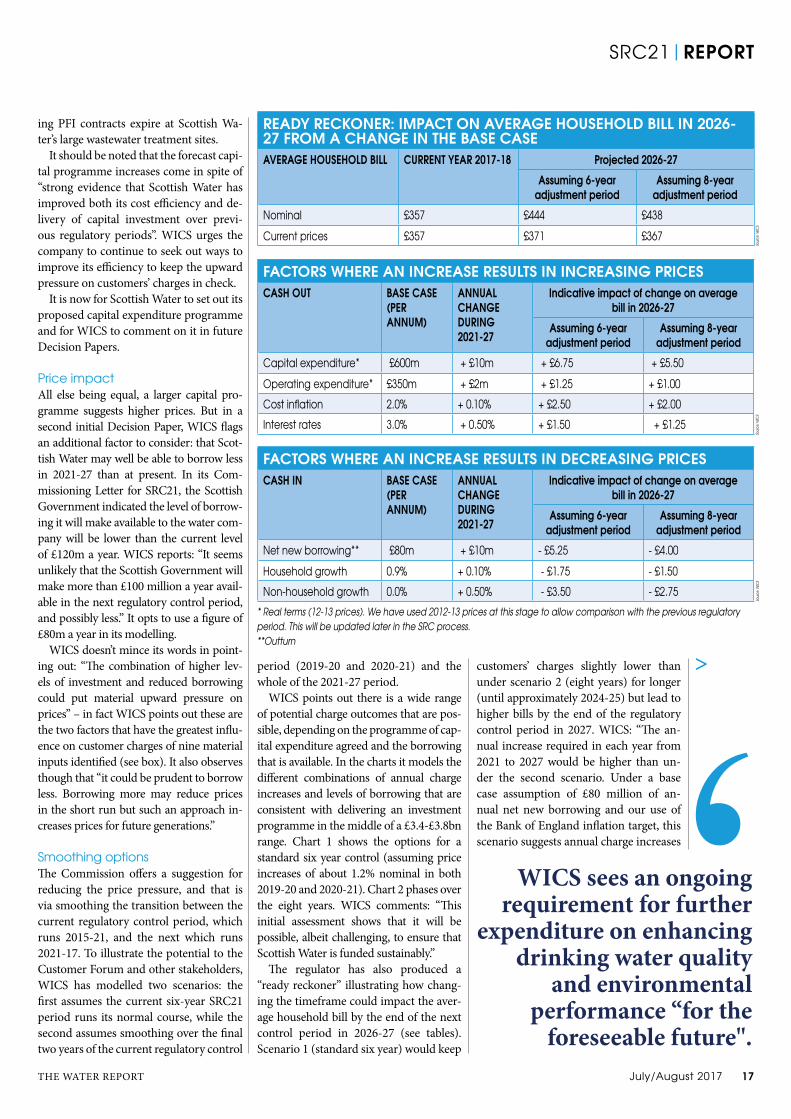

READY RECKONER: IMPACT ON AVERAGE HOUSEHOLD BILL IN 2026-27 FROM A CHANGE IN THE BASE CASEAVERAGE HOUSEHOLD BILL CURRENT YEAR 2017-18 Projected 2026-27

Assuming 6-year adjustment period

Assuming 8-year adjustment period

Nominal £357 £444 £438Current prices £357 £371 £367

FACTORS WHERE AN INCREASE RESULTS IN INCREASING PRICESCASH OUT BASE CASE

(PER ANNUM)

ANNUAL CHANGEDURING 2021-27

Indicative impact of change on average bill in 2026-27

Assuming 6-yearadjustment period

Assuming 8-yearadjustment period

Capital expenditure* £600m + £10m + £6.75 + £5.50Operating expenditure* £350m + £2m + £1.25 + £1.00Cost in�ation 2.0% + 0.10% + £2.50 + £2.00Interest rates 3.0% + 0.50% + £1.50 + £1.25

FACTORS WHERE AN INCREASE RESULTS IN DECREASING PRICESCASH IN BASE CASE

(PER ANNUM)

ANNUAL CHANGEDURING 2021-27

Indicative impact of change on average bill in 2026-27

Assuming 6-yearadjustment period

Assuming 8-yearadjustment period

Net new borrowing** £80m + £10m - £5.25 - £4.00Household growth 0.9% + 0.10% - £1.75 - £1.50Non-household growth 0.0% + 0.50% - £3.50 - £2.75

* Real terms (12-13 prices). We have used 2012-13 prices at this stage to allow comparison with the previous regulatory period. This will be updated later in the SRC process.**Outturn

ing PFI contracts expire at Scottish Wa-ter’s large wastewater treatment sites.

It should be noted that the forecast capi-tal programme increases come in spite of “strong evidence that Scottish Water has improved both its cost e�ciency and de-livery of capital investment over previ-ous regulatory periods”. WICS urges the company to continue to seek out ways to improve its e�ciency to keep the upward pressure on customers’ charges in check.

It is now for Scottish Water to set out its proposed capital expenditure programme and for WICS to comment on it in future Decision Papers.