the state of freight: rail and intermodal state of freight: rail and intermodal railtrends+...

TRANSCRIPT

11/19/15

1

THE STATE OF FREIGHT: RAIL AND INTERMODAL

Railtrends Conference Nov 19, 2015

Larry Gross Partner FTR 888.988.1699 x41 [email protected] @Intermodalist

www.FTRintel.com

www.FTRintel.com

11/19/15

2

3 3

DISCUSSION OVERVIEW

§ Economic Indicators § State of Freight

o Rail Carload o Intermodal (with a truck detour)

§ Fearless Forecast

ECONOMY

11/19/15

3

5 5

MANUFACTURING IS STILL (BARELY) POSITIVE ISM MANUFACTURING VS IP MANUFACTURING

ISM Manufacturing Index (>50 = Growth)

Industrial ProducIon: Manufacturing (2012=100)

30

35

40

45

50

55

60

65

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

80

85

90

95

100

105

110

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

5 Source: FTR, ISM, Federal Reserve

6

BUSINESSES: STUCK IN THE MUD ORDERS & INVENTORIES

Source: Census Bureau

Core Capital Goods Orders

$45

$50

$55

$60

$65

$70

$75

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Inventory-‐to-‐Retail Sales RaIo

1.20

1.25

1.30

1.35

1.40

1.45

1.50

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

11/19/15

4

7

CONSTRUCTION: ROOM TO GROW RESIDENTIAL VS. BUSINESS

Source: FTR, Census Bureau

ConstrucIon Spending

$200

$300

$400

$500

$600

$700

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Business Spending back to pre-recession peak, long way to go for Residential

8

GDP – RECOVERY LENGTH

Source: FTR Associates

0

1

2

3

4

5

6

Begi

nnin

g O

f Re

cove

ry =

1

Length Expressed In Timing of Current Recovery

Growth In GDP During Recoveries

1950

1954

1958

1961

1971

1975

1982

1991

2001

2010

Forecast

1950

1954

1958

1971

1975

1982

1991

1961

2001

Current Forecast

11/19/15

5

Rail Carload

10 10

RAIL CARLOADS HAVE BEEN WEAK SINCE LATE WINTER

200

250

300

350

400

450

-12% -10% -8% -6% -4% -2% 0% 2% 4% 6% 8%

10% 12%

Thou

sand

s

N.A. Total Carloads Week Ending 10/31/15

Carloads Vs. Prev. Year Carloads Source: AAR

Source: AAR

11/19/15

6

11 11

H2 TO DATE N.A. CARLOADS (EXCL. IM) VERSUS SAME PERIOD 2014

16 3

(124) (215)

(28) (11)

5 (0) (1) (2) (5) (3)

(40) (13)

2 (34)

9 (18)

(6) 28

- (440)

-500 -400 -300 -200 -100 0 100

Grain Farm Prod. Excl Grain Metallic Ores Coal Crushed Stone, Sand, Gravel Non-Metallic Minerals Grain Mill Products Food Products Primary Forest Products Lumber & Wood Products Pulp & Paper Chemicals Petroleum Products Stone, Clay, Glass Coke Metals & Metal Products Motor Vehicles & Equip Metal Scrap Other Waste & Scrap Other Commodities Intermodal (Platforms) Total

Source: AAR, FTR

12 12

EXCLUDING SPECIALS (GRAIN, COAL, CRUDE) INDUSTRIAL ECONOMY STILL LOOKS WEAK

100

120

140

160

180

200

220

240

-10% -8% -6% -4% -2% 0% 2% 4% 6% 8%

10% 12%

Thou

sand

s

N.A. Total Carloads Week Ending 10/31/15

Carloads Vs. Prev. Year Carloads Source: AAR

Source: AAR, FTR

11/19/15

7

13 13

SERVICE RECOVERY IS TAKING HOLD – AVERAGE TRAIN SPEED

22.0

22.5

23.0

23.5

24.0

24.5

25.0

25.5

26.0

26.5

1 5 9 13 17 21 25 29 33 37 41 45 49 53 4 W

eek

Mov

ing

Ave

rage

IM T

rain

Spe

ed -

MPH

Week

4-Week Avg. Train Speeds - Total Network

Average 2000-2009 2010 2011 2012 2013 2014 2015

14 14

SERVICE RECOVERY IS TAKING HOLD – YARD DWELL

22

23

24

25

26

27

28

29

1 5 9 13 17 21 25 29 33 37 41 45 49 53 4 W

eek

Mov

ing

Ave

rage

IM T

rain

Spe

ed -

MPH

Week

4-Week Avg. Yard Dwell - Total Network

Average 2000-2009 2010 2011 2012 2013 2014 2015

11/19/15

8

15 15

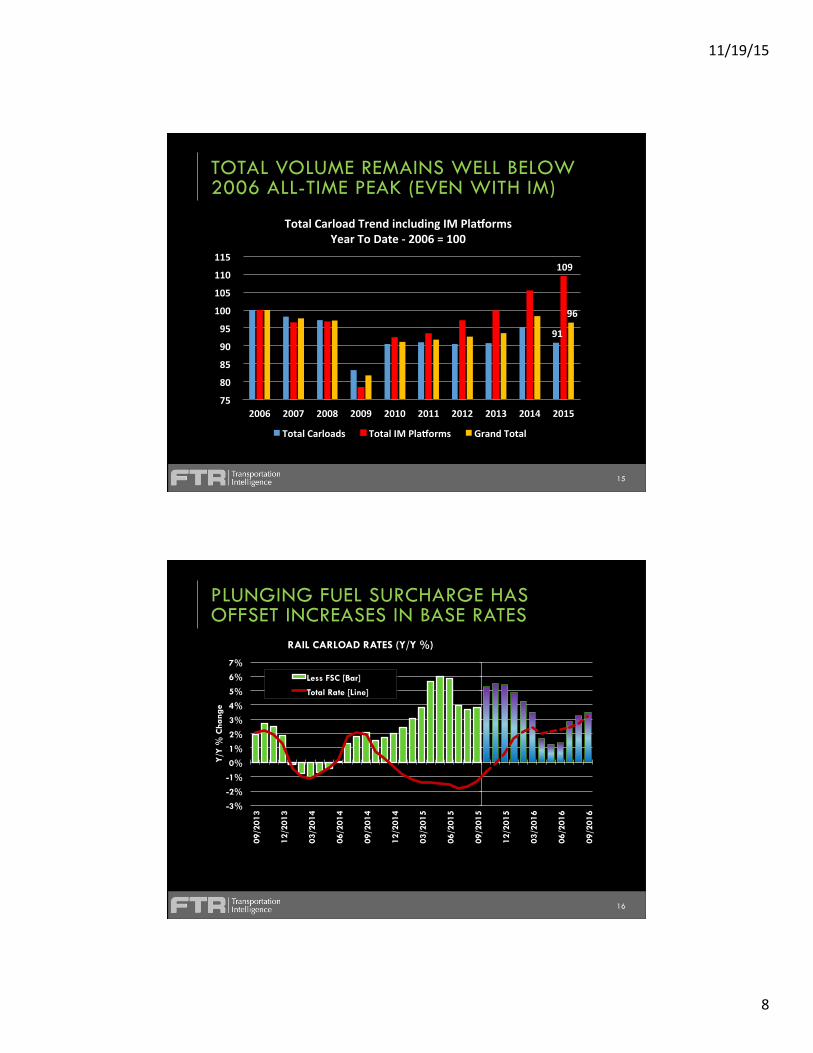

TOTAL VOLUME REMAINS WELL BELOW 2006 ALL-TIME PEAK (EVEN WITH IM)

91

109

96

75

80

85

90

95

100

105

110

115

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Total Carload Trend including IM PlaCorms Year To Date -‐ 2006 = 100

Total Carloads Total IM PlaCorms Grand Total

16 16

PLUNGING FUEL SURCHARGE HAS OFFSET INCREASES IN BASE RATES

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

09/2

013

12/2

013

03/2

014

06/2

014

09/2

014

12/2

014

03/2

015

06/2

015

09/2

015

12/2

015

03/2

016

06/2

016

09/2

016

Y/Y

% C

hang

e

RAIL CARLOAD RATES (Y/Y %)

Less FSC [Bar]

Total Rate [Line]

Source: FTR; Copyright 2014 Data is seasonally adjusted; excludes Intermodal

11/19/15

9

17 17

POSSIBLE SOURCES OF IMPROVEMENT § Lumber (Strengthening residenIal construcIon outlook) § Chemicals (Petrochemical investment fueled by low prices – late 2016 and beyond? § Intermodal

Probably not enough to fill the hole….

18 18

CARLOAD VOLUME WILL SHRINK THIS YEAR AND ONLY GROW A BIT IN 2016

Source: FTR Freightcast

Excludes Intermodal

Y/Y % Change

2015 Q1

2015 Q2

2015 Q3

2015 Q4

2016 Q1

2016 Q2

Carloads 1.4% -6.3% -4.6% -5.8% -1.1% 4.9%

Y/Y % Change

2014

2015 2016

Carloads 3.2%

-3.9% 1.3%

11/19/15

10

Intermodal

20

TRUCK LOADINGS FORECAST 4.

2%

3.3%

3.

0%

-15% -12% -9% -6% -3% 0% 3% 6% 9%

1993

19

94

1995

19

96

1997

19

98

1999

20

00

2001

20

02

2003

20

04

2005

20

06

2007

20

08

2009

20

10

2011

20

12

2013

20

14

2015

20

16

2017

Y/Y

Per

cent

Cha

nge

U.S. Truck Loadings Originated

§ Modest freight growth expected going forward

Source: FTR Trucking Update Report

Dry van will be even lower!

11/19/15

11

21

THE CUMULATIVE EFFECT OF REGULATIONS WILL BE SEVERE

Source: FTR

(50)

-

50

100

150 20

11.1

2012

.1

2013

.1

2014

.1

2015

.1

2016

.1

2017

.1

2018

.1

Thou

sand

s

Additional Driver Hires Per Quarter Required By Regulation Electronic Stability Controls Speed Limiters Training Provisions OSHA Worker Protection Minimum Insurance Safe Harbor Entry Proficiency Drug & Alcohol Data Base/Hair testing Prohibition Of Coercion Pattern Of Violation Independent Contractor Rules Safe Food Transportation Motor Carrier Protection Act HOS ELD Health Regulations and Treatment Immigration Effects Mexico Regional Equipment CSA

22

TRUCKING RATES OUTLOOK

Source: FTR Shippers Update Report

11/19/15

12

23 23

INTERMODAL HEADLINES

§ DomesIc intermodal faces headwinds § InternaIonal returns to “normal” § Import diversion conInues § Service recovery begins to take hold § Overcapacity crisis on the water

24 24

400

450

500

550

600

650

700

750

800

800

900

1000

1100

1200

1300

1400

1500

1600

Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct

Thou

sand

s

Total Intermodal: Rev. Moves - Actual (000's)

Sources: GTC, FTR, IANA; Copyright 2015

VOLUME HAS STABILIZED SINCE THE END OF THE USWC MELTDOWN

Total (Left Axis)

International (Right Axis)

Domestic (Right Axis)

Sources: IANA ETSO, GTC, FTR Copyright 2015

11/19/15

13

25 25

-15%

-10%

-5%

0%

5%

10%

15%

Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct

Total Intermodal: Year/Year % Change

Sources: GTC, FTR, IANA; Copyright 2015

INTERMODAL GROWTH HAS SLOWED

Total +3.2% YTD (Left Axis)

International +3.2% YTD (Right Axis)

Domestic +3.3% YTD (Right Axis)

Sources: IANA ETSO, GTC, FTR Copyright 2015

26 26

450

500

550

600

650

700

750

800

1200

1250

1300

1350

1400

1450

1500

1550

Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct

Thou

sand

s

Seasonally Adjusted Rev. Moves (000)

Sources: GTC, FTR, IANA; Copyright 2015 Current 12 Months

SEASONAL ADJUSTMENTS SHOW DOMESTIC NOT GROWING

Total (Left Axis)

International (Right Axis)

Domestic (Right Axis)

Sources: IANA ETSO, GTC, FTR Copyright 2015

11/19/15

14

27 27

OCTOBER WAS SEASONALLY NORMAL FOR DOMESTIC BUT NOT INT’L

Source: AAR

10.3%

10.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Volu

me

% v

s. A

vera

ge M

onth

Seasonality - Domestic - October

1.9%

6.6%

0%

2%

4%

6%

8%

10%

12%

Volu

me

% v

s. A

vera

ge M

onth

Seasonality - International - October

28 28

INTERMODAL SERVICE IS IMPROVING

28

29

30

31

32

33

34

1 5 9 13 17 21 25 29 33 37 41 45 49 53

4 W

eek

Mov

ing

Ave

rage

IM T

rain

Spe

ed -

M

PH

Week

4-Week Avg. Intermodal Train Speeds - Total Network

Average 2000-2009 2010 2011 2012 2013 2014 2015

11/19/15

15

29 29

NORTH AMERICAN IMPORTS ARE UP EXPORTS ARE NOT

Sources: Port Reports, FTR

1,000

1,200

1,400

1,600

1,800

2,000

2,200

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Oct '1

4 Nov

'14

Dec

'14

Ja

n '1

5 Fe

b '1

5 Mar

'15

Apr

'15

May

'15

Ju

n '1

5 Ju

l '15

Aug

'15

Sep

'15

Thou

sand

s

Seasonally Adjusted N.A. Imports - 000 TEUs

Month/Month Change Seasonally Adjusted Imports

Sources: FTR, GTC, Port Reports

-15% -10%

-5% 0% 5%

10% 15% 20% 25% 30% 35%

Summary: N.A. Port Activity - Y/Y Change

Total Imports Exports

30 30

INTERMODAL CONTINUES TO GAIN MARKET SHARE OF U.S. LONG-HAUL DRY VAN

7.0% 7.5% 8.0% 8.5% 9.0% 9.5%

10.0% 10.5% 11.0%

U.S. Intermodal Market Share Domestic

7.0% 7.5% 8.0% 8.5% 9.0% 9.5%

10.0% 10.5% 11.0%

U.S. Intermodal Market Share International

Sources: GTC, FTR, ETSO Report Sources: GTC, FTR, IANA ETSO Data

11/19/15

16

31 31

DOMESTIC STILL IS FACING A NUMBER OF HEADWINDS § Slowing growth in demand for long-‐haul dry van transport § Ample truck capacity available – for now § Lower fuel prices erode intermodal cost advantage

32 32

ISSUES ABOUND ON THE OCEAN

§ SubstanIal over-‐capacity due to overbuilding Ø Lower prices but lower service reliability due to blanked voyages

§ Port congesIon conInues § Some progress on chassis front but sIll problemaIc § Panama Canal expansion schedule sIll a quesIon § No ILA Contract will be signed this year § Port cartage under stress

Ø Independent contractor model is under threat Ø Port congesIon issues causing producIvity loss Ø Driver availability/cost a big concern

11/19/15

17

33

RAIL INTERMODAL RATES

Source: FTR Intermodal Update Report

-‐6%

-‐4%

-‐2%

0%

2%

4%

6%

8%

09/2013

12/2013

03/2014

06/2014

09/2014

12/2014

03/2015

06/2015

09/2015

12/2015

03/2016

06/2016

09/2016

Y/Y % Cha

nge

Rate Outlook: Intermodal

Rev/Load (w/o FSC) Rev/Load (w/ FSC)

Source: FTR; Copyright 2015

34 34

INTERMODAL GROWTH IS PROJECTED TO CONTINUE, BUT AT A SLOWER PACE

Source: FTR Freightcast

Y/Y % Change

2015 Q1

2015 Q2

2015 Q3

2015 Q4

2016 Q1

2016 Q2

International 0.6% 6.8% 4.0% 6.0% 9.9% -1.2%

Domestic 5.6% 2.2% 2.7% 2.9% 2.8% 3.5%

Total 3.1% 4.5% 3.4% 4.4% 6.3% 1.0%

Y/Y % Change

2014

2015 2016 2017

International 4.4% 4.4% 4.3% 4.7%

Domestic 5.1% 3.3% 3.6% 6.6%

Total 4.8% 3.9% 3.9% 5.6%

11/19/15

18

35

FTR Transportation Conference

September 13-15, 2016 Indianapolis, IN

www.FTRConference.com

Hand me a business card and I will be happy to send you a

copy of this presentation

Or download at

www.ftrintel.com/Railtrends

36

Stay Connected Twitter: @FTRintel

Blog: blog.ftrintel.com FTRintel.com/SOFTODAY

www.ftrintel.com

Stay in Contact www.FTRintel.com [email protected] 888.988.1699

11/19/15

19

THE STATE OF FREIGHT: RAIL AND INTERMODAL

Railtrends Conference Nov 19, 2015

Larry Gross Partner FTR 888.988.1699 x41 [email protected] @Intermodalist

www.FTRintel.com

Thanks!