the significance of regulatory orientation, political stability and culture on consumption and price...

TRANSCRIPT

The significance of regulatoryorientation, political stability andculture on consumption and priceadequacy in insurance markets

W. Jean KwonThe School of Risk Management, St John’s University,

New York, New York, USA

Abstract

Purpose – The purpose of this paper is to examine insurance regulation theories, regulatory agencystructures and measures.

Design/methodology/approach – This study investigates significance of regulatory agencystructure, key regulatory measures, political stability and cultural dimension in insurance markets of56 developed and developing countries for 2005-2009.

Findings – It was found that insurance consumption is lower in countries with an authorityexclusively for insurance regulation but life insurance consumption is higher when the agency is partof government or when another agency is jointly responsible for insurance regulation. Market entryregulation leads to lower consumption whereas market exit regulation has the opposite effect.Solvency regulation and required use of standard forms for insurer financials lead to greaterconsumption of insurance. A positive impact on the nonlife market is observed for accountingregulation and regulator’s intervention power.

Practical implications – Price control regulation may lower consumption of insurance whereastariff rating brings about a rise in the consumption. Regulation of insurance intermediaries orcorporate governance may lower insurance consumption whereas the requirement that insurersemploy an actuary or actuaries gives rise to the consumption.

Originality/value – The author found no difference between OECD and non-OECD countries.However, corruption-freeness and inflation impact insurance consumption. Using OECD country dataonly, a negative impact was found of the single agency structure and tariff regulation in the lifeinsurance market and a positive impact of regulation by two or more agencies in the life insurancemarket and of price control regulation in the nonlife insurance market. Corruption-freeness positivelyaffects the loss ratio in the life insurance market and the combined ratio in the nonlife insurance market.

Keywords Insurance, Regulation, National cultures, Life insurance, Theory of insurance regulation,Insurance consumption (density), Price adequacy, Regulatory agency, Prudential regulation,Market conduct regulation, Antitrust regulation, Loss ratio, Combined ratio

Paper type Research paper

Regulation and insurance developmentIn today’s markets, insurance companies increasingly intertwine existing products andinvent intricate new breeds of products and market them via innovative distributionchannels[1]. Capitals and expertise may flow through in nontraditional ways, includingcaptive and insurance-linked securitization arrangements with capital market investors.The markets today are certainly bigger than ever in terms of scale and scope economies.

Do we enjoy more than ever of quality, fairly priced products and services frommore reliable insurance companies? Are the markets now with fewer imperfections?

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/1526-5943.htm

Received 17 March 2013Revised 1 April 2013Accepted 26 April 2013

The Journal of Risk FinanceVol. 14 No. 4, 2013pp. 320-343q Emerald Group Publishing Limited1526-5943DOI 10.1108/JRF-03-2013-0018

JRF14,4

320

The insurance markets are more efficient than ever but still with imperfections.Insurers may continue to fail to allocate resources efficiently or supply some services orthey may supply certain services in some suboptimal way until the problems of marketpower, negative externality, free rider or information asymmetry are removed from themarket[2].

Governments, individually and jointly, monitor financial transactions and controlmarket conducts to protect the legitimate interests and rights of the less informed:consumers from lemons problems and agency problems; and suppliers from adverseselection and moral hazard problems. Certainly, information is a public good as Stiglitz(2009) suggests. Financial intermediation helps society solve some informationasymmetry problems but does not remove them from the market. Here lies theimportance of economic regulation of the market[3].

Governments in numerous developing economies have done, or are planning,privatization, deregulation and liberalization of their insurance markets[4]. Such changesin government policy, however, will not lead to completely privatized, regulated andliberal markets. Even no government of a developed economy has done so. To putdifferently, government may be a direct supplier of insurance when the private marketdoes not provide financial security against selected high risks (e.g. major natural hazards)and such security exhibits strong traits of public goods. Government may be a facilitatorof certain financial security for all citizens (e.g. health insurance and pension) or selectedcohorts (e.g. workers’ compensation and other compulsory liability insurance).

Development and maintenance of sound risk management and financing services isessential for social stability as well. Hence, governments increasingly offer insurancecompanies new guidelines and business platforms and suggest them – sometimessuasively – to develop new products or extend life and nonlife insurance coverages tosocial sectors. For example, takaful insurance – with only 30 years of history or so –maintains a growth momentum not only in Muslim populous countries but also inseveral Western hemisphere countries. We now find specific laws and regulationsgoverning takaful operations in several countries (e.g. Indonesia, Malaysia, Jordanand Saudi Arabia), intergovernmental coordination for supervision of the market(e.g. The IFSB and the IAIS, 2006) and even initiatives to develop derivative markets(e.g. risk securitization with sukuk bond).

Another example can be microinsurance. Despite a relatively short history of andnon-existence of a universal definition for it as well as some accounting and regulatorychallenges, several governments have already introduced laws and regulatory guidelinesto promote the business for the less privileged sectors which would otherwise remainunder-serviced by the private insurance sector[5]. We even observe innovations in productdistribution and risk underwriting unique to microinsurance (e.g. marketing via MFIchannels), use of derivatives for microinsurance (Hazell et al., 2010), attempts to establishinternational standards (e.g. IAIS-CGAP collaboration) and research collaboration(Bester et al., 2009; Roth et al., 2007).

Challenges also exist in insurance markets. The markets generate new risks andfeed old risks to become catastrophic, some even traveling across economies at anever-fast rate. Interconnectedness of economies, together with convergence across theindustries in the financial services sector, has exposed us to another layer risk of whichcould stem from psychological fear as well. The Asian economic crisis in the late 1990s,for example, taught us how important it is to manage contagion risk not only within

Price adequacyin insurance

markets

321

the domestic financial services market but also across countries. The credit crisis in thelate 2000s warned us again the importance of structured and timely regulation offinancial intermediaries.

Duality in insurance regulation can put the government in a Catch 22 situation. It isresponsible for the protection of consumers, especially those in personal line markets orneeding compulsory coverage, from insurers attempting to generate excessive profits.Concurrently, government must maintain a market environment in which regulatedfirms can charge premiums sufficient to cover their expected/actual claims, expensesand reasonable profits, say, in compulsory lines of business.

It seems society is better off with both economic and social regulation of insurancemarket activities at least in selected lines of insurance business[6]. We expect that anysupervisory or regulatory intervention does society “good,” desirably generating netpositive economic benefits while preserving efficient allocation of all economicresources at the societal level. We expect that policymakers and regulators know thegoals of regulation and that they know the regulated market clearly, material risksunmistakably and the risk-capital relationship unambiguously. They are expected tohave a thorough understanding of the dynamics of economic, political and societalfactors surrounding the market. We expect that they remain regulatorily neutral andprofessionally ethical and that they are aware of the cost of regulation. Are they really?

Insurance regulation worldwide is based on the principles of prudentiality,market conduct and antitrust competition. However, specifics of the regulation varysignificantly from country to country. Neither is found uniformity in the regulatorystructure. Insurance regulation is administrated by a government agency in somecountries and by an independent – including quasi-government – agency in othercountries. Some countries use a single agency to regulate all financial services marketswhile other governments use a segmented agency structure for each of the insurance,banking and investment markets. A variation of the latter is a twin peaks approach inwhich one agency (e.g. the central bank or the securities commission) is responsible forprudential concerns (i.e. policymaking and governing actions) and the other for financialexamination and market conduct regulation.

International coordination and cooperation in insurance supervision and regulationcontinue. This paper notes two intergovernmental associations, particularly for theirdatabases. The International Association of Insurance Supervisors (IAIS) has insuranceregulatory authorities from more than 190 jurisdictions as members and maintainsInsurance Laws and Reinsurance Databases. The databases record responses to the IAISsurvey of the member authorities. 90 jurisdictions or so responded to its survey for theyear 2009 results[7]. The Organization for Economic Cooperation and Development(OECD), particularly its Insurance and Private Pensions Committee, disseminatesinsurance data via OECD Insurance Statistics. This dataset contains detailed insurancepremium and claims data by class of business for most of the OECD member states.

Governments with a less developed insurance market may to refer the policies andstandards adopted by those with a more developed market or recommended byintergovernmental agencies. The policies and standards as is for one country, however,is not necessarily a good fit for another country. Neither is there sufficient evidence thatcertain specific regulatory measures are as effective as the government intends.Lack of cross-country studies of the significance of the structure of regulatory agencyand regulatory measures in insurance markets thus warrants examination.

JRF14,4

322

This paper covers these issues, specifically:. the impact of regulatory agency structure and measures on insurance market

development (density) and price adequacy; and. the interaction between the market development and the adequacy.

This paper also estimates the impact of political stability and cultural traits on theconsumption and price adequacy. This study covers a total of 56 developing anddeveloped economies during 2005-2009.

This paper is structured as follows. The next section discusses regulation theory,regulatory agency structure and common regulatory measures in insurance markets.This second section also covers cultural trait theory using Geert-Hofstede indices. Thethird section covers empirical models and data. Key findings are summarized in thefourth section. The last one is for conclusions and implications.

Regulation literatureWhen government intervenes with private market activities, it is expected thatgovernment is capable of preventing and correcting causes of market failure and thatits regulatory and supervisory measures are economic theory-based. In reality,however, policymakers are unlikely to use only the economists’ terminology injustifying policymaking and government actions do not always ameliorate marketinefficiency, let alone societal inequity (Skipper and Kwon, 2007). For example,Chen et al. (2010) find a positive relationship between government and economicefficiency in the local governments in Taiwan. To the contrary, Rayp and van de Sijpe(2007) examine 52 developing economies to find that government expenditureefficiency is influenced not by economic policy determinants (e.g. income) but mainlyby the structural variables (e.g. past policy, illiteracy and urbanization) andgovernance indicators (e.g. rules of law).

Existing studies about efficiency in insurance often cover insurer and insurance marketefficiency. For example, Cummins et al. (1998, 1999) use data envelopment analysis (DEA)to estimate cost and revenue efficiency in the USA life and property-casualty insurancemarkets, respectively. Similar country- or market-specific studies are found for China,Italy, Japan, Pakistan, Spain, Taiwan and other countries. Fenn et al. (2008) conductstochastic frontier analysis to find that most European insurers exhibited decreasing costefficiency and that firm size and domestic market share were significant factorsdetermining X-inefficiency during 1996-2001. Eling and Luhne (2010) find a steadytechnical and cost efficiency growth internationally from conducting DEA of insurancecompanies in 36 countries between 2002 and 2006.

A few studies examine regulator efficiency in financial services markets. King andLevine (1995), for example, find the presence of a positive link between financial servicessector development and economic growth. Jacobzone et al. (2010) analyze the 1998-2005OECD survey responses to find a correlation between regulatory quality and the OECDindicators of product market regulation and the general business environment. Freytagand Masciandaro (2007) analyze the need for independence of financial (banking)supervision and the central bank using data for 48 countries for year 2004. Siegmund(2010) suggests that the central bank not regulate insurance. Shiro (2006) offers anindustry’s insight about the reform of insurance regulatory structure and its threat to themarket. Grace and Phillips (2007) examine the incentives US state governments have

Price adequacyin insurance

markets

323

to provide insurance regulatory services in an efficient manner. They find evidence ofcross-state externalities and of increasing economies of scale in the production ofinsurance regulation after controlling for regulatory externalities.

Theories of regulationTheory suggests differences in the positions policymakers assume. For example, thepremise of perfection in government regulation led to the development of the publicinterest theory of regulation, which was contended by Viscusi et al. (2005) more as ahypothesis than of a theory. The capture theory that regulation reflects the industry’sdemand for it and the regulated becomes to control the regulator, too, lacks the support ofempirical evidence. Joscow (1974) assumes that regulation is to minimize the conflictsand criticism subject to legal and procedural constraints. Under this minimization ofconflict theory, the public are not concerned with pricing as long as nominal prices do notrise and the regulated firm maximizes long-term profits. However, price alone is unlikelyto explain the economic behavior of the consumers or the firm.

Other theories hint that regulation may not always be for the equal benefit of allparties of interest. Theory of economic regulation, introduced by Stigler (1971), suggeststhat government has “the power to coerce” and uses it to restrict the decisions of theeconomic agents (e.g. citizens and businesses). Regulation is acquired by and is designedfor the benefit of the regulated that in return can offer the regulator financial and politicalsupport. Further, the entities that not only share a common regulatory interest but alsoare well organized and financed may demand regulation. Furthermore, the capturedlegislatures may create the regulatory agency and adopt policies pertaining to directmonetary subsidy, control over new entry, control over substitutes and complements aswell as price control. In contrast to this view, Viscusi et al. (2005) propose price control,quality control and market entry and exit control as the main regulatory policies.

Posner (1974) modifies Stigler’s Theory and proposes equilibrium-based theory ofregulation. The theory proposes that the regulated industry obtains some monopolyprofits from regulation and the organized consumer group obtains lower prices or betterservices than it would in an unregulated market – all at the expense of the unorganizedgroups in the regulated market. Similarly, self-interested theory of regulation by Peltzman(1976) suggests that regulators carry on activities to maximize their political support.Meier (1988) contends that capture does not occur when, for example, the industry is toosegmented to reach a common policy goal and, as an alternative, suggests political theoryof regulation that the bargaining among multiple private interest groups – the regulatedindustry, consumers, the regulator and political elites – shapes regulation.

Most of the existing theories imply that consumers – even after factoring in the presenceof strong consumer group activities – tend not to be as well organized, financed or informedas do other interest groups. In other words, policymakers and scholars stress the importanceof protecting consumers in the insurance market flourished with future-deliverablecontracts of complex nature from the potential harm by other interest groups. In fact,protection of policyholders’ interests as well as consumer education is one of the objectivesfound in the insurance acts and regulations around the world.

Regulatory agency structureDiversity rather than uniformity describes regulatory agency structures worldwide.In numerous countries, a special department or subordinate institution of the relevant

JRF14,4

324

ministry (e.g. the Ministry of Finance) carries out this oversight. The department canbe explicitly for insurance regulation and supervision (e.g. Office de Controle desAssurances of Belgium, Superintendencia de Seguros de la Nacion in Argentina and theInsurance Board in Nepal). In some other countries, such as India and Thailand, the bodyresponsible for insurance regulation is a quasi-independent authority, not housed in anyministry. A known risk under these approaches is possible gaps or overlaps incross-market regulation. This government oversight is commonly carried out at thecentral government level in most countries except, for example, Canada and the USA[8].

Convergence in regulatory structure is observed. Several countries are known for asingle agency for the entire financial services markets (e.g. Financial Services Authorityof the UK and Financial Services Agency of Japan) or for multiple but not the entiremarkets (e.g. Australian Prudential Regulatory Authority and Superintendencia deBanca y Seguros del Peru). Some other countries house the insurance regulation functionunder the country’s (de facto) central bank (e.g. Autoridade Monetaria de Macau, BankNegara Malaysia and Monetary Authority of Singapore). These approaches could beeffective in removing the aforementioned gaps and overlaps. At the same time, theycould expose the government to internal management issues that are similar in scope tothe case of financial conglomerates in the private sector. Conversely, a single roof systemmakes sense only if it yields, or is projected to yield, net positive benefits to the economy.

Regulatory measuresWe classify regulatory measures in insurance into three broad groups[9]. First,governments commonly deal with any antitrust moves that could lessen competition in themarket, thus solving problems of market power. Commonly used anti-competitionregulation tools include market entry barriers (e.g. business license, minimum initial capitaland economic-needs test), market exit barriers (e.g. receivership and special bankruptcylaw) and price-product control (e.g. preapproval of new products or price change).

Second, prudential regulation – also known as financial regulation and le controlefinancier – is to promote financial soundness of the regulated companies and to correctproblems of information asymmetry and negative externalities in the market. Weobserve that risk-based regulation – particularly RBC regulation, Solvency II and stresstests – is now supplemented by laws requiring broad disclosure of financials, strategiesand corporate (enterprise) risk management to all stakeholders as well as the public atlarge. We find use of sector-specific accounting standards as another tool for prudentialregulation, especially to minimize the impact of volatility of the liability side of thebalance sheet from which major macro-risks stem (Eatwell, 2009) and to detect anyhidden, potentially harmful, leverage[10].

Finally, market conduct regulation – developed mainly because of informationproblems – refers to government imposed rules covering inappropriate practices in themarket. Transparency in product presentation and premium rate regulation – more forpersonal lines and cash-value life insurance – are two examples of market conductregulation. Intermediary regulation and corporate governance regulation also belongto this group.

Empirical examination: models and dataAs alluded to above, we estimate the impact of national differences in regulatoryagency structure and measures, after controlling the models for key economic,

Price adequacyin insurance

markets

325

insurance market, political and cultural factors, on the demand for insurance and priceadequacy globally. This study covers the life insurance market and the nonlifeinsurance market separately as well as the national market.

Two sets of regression models are developed for this study, which can berepresented as:

Consumptioni;t ¼ b0 þ b1Penetrationi;t þ b2Agencyi;t þ b3Prudentialityi;t

þ b4Conducti;t þ b5Antitrusti;t þ b6Culturei þ b7Corrupti;t

þ b8Econi;t þ b9OECDi þ b9Yeart þ 1

ð1Þ

Price Adequacyi;t ¼ b0 þ b1Penetrationi;t þ b2Agencyi;t þ b3 Prudentialityi;t

þ b4Conducti;t þ b5Antitrusti;t þ b6Culturei þ b7Corrupti;t

þ b8Econi;t þ b9OECDi þ b9Yeart þ 1 ð2Þ

where, for parameter (matrix) estimate b, country I, year t and bold for a matrix ofvariables:

Consumption ¼ insurance density (life, nonlife and total);

Price Adequacy ¼ combined and loss ratio (life, nonlife and total);

Penetration ¼ insurance penetration ratio (life, nonlife and total);

Agency ¼ regulatory agency structure difference variables;

Prudentiality ¼ prudential regulatory measures;

Conduct ¼ market conduct regulatory measures;

Antitrust ¼ antitrust (competition) regulatory measures:

Culture ¼ standardized Geert-Hofstede Index scores;[11]

Corrupt ¼ Corruption Perceptions Index;

Econ ¼ economic environment control variables;

OECD ¼ OECD dummy;

Year ¼ year dummies for 2006, 2007, 2008 and 2009; and

1 ¼ error term.

Dependent variablesThe consumption is proxy measured by insurance density – the ratio of total premiumto total population – at three levels: one for the total insurance market (denoted asDensity Total ), one for the life market (Density Life) and one for the nonlife market(Density Nonlife). All of these ratios are based on the premium data in US dollarsas reported at the Swiss Re’s World Insurance Database: 1980-2010. The findings arepresented in Table II (Models 1 through 3).

Price adequacy is proxy measured by a set of combined ratios (the sum of theloss premium ratio and the insurer expense ratio) and another set of loss ratios. Thecombined ratios are at three levels: Combined R Total, Combined R Life and CombinedR Nonlife. Likewise, the loss ratio variables are Loss R Total, Loss R Life and LossR Nonlife. We decide not to use expense ratios in part to avoid a unity case inestimation and in part based on the assumption that insurers may control theirbusiness expenses more easily than their claims experiences.

JRF14,4

326

Separately, use of combined and loss ratios for this study requires a carefulinterpretation of the findings. For example, letting the loss amount constant, a rise ininsurance premium rate (as in a hard market or when the regulator approves premiumrate changes) can lead to a lower premium-to-loss ratio. Conversely, letting the premiumamount constant, a rise in insurance claims can lead to a higher premium-to-loss ratio.We use OECD Insurance Statistics for these variables. The findings are summarized inTables III and IV (Models 4 through 9).

Insurance penetration ratioSwiss Re (2011) reports that the insurance industry contributed – in terms of writtenpremiums – 6.9 percent of the global GDP in 2010. The contribution was higher inindustrialized economies (8.7 percent) than in emerging ones (3.0 percent). Per capitalconsumption of insurance was also higher in industrialized economies (US$3,527) thanin emerging ones (US$110) in 2010. Like these raw data, empirical studies find apossible presence of a close and positive relationship between economic developmentand insurance market development (Ward and Zurbruegg, 2000; Arena, 2008). SwissRe also reports that citizens and businesses consumed more life insurance (US$2,069and US$61) than nonlife insurance (US$1,458 and US$49) in both developed andemerging markets, respectively[12].

Empirical estimation of this relationship is often regressing insurance penetration(premiums-to-GDP) ratios to an economic development proxy. This study follows thisconventional approach but after converting the ratios using two methods. For one, weconduct log-transformation of the ratios to generate closer-to-normal distributions. Forthe other, we convert the ratios to generate standardized, relative distance indicesbetween country i and the country with the highest penetration for each year. Theconversion is based on:

1 2ðPremium=GDPÞHighest Penetration Country;Year t 2 ðPremium=GDPÞCountry i;Year t

ðPr emium=GDPÞHighest Penetration Country;Year t

ð3Þ

Using equation (3), we assign a ratio of one to the country with the highest ratio for thegiven year. For example, the conversion for year 2009 indicates that the relativecontribution of nonlife insurance to GDP in Pakistan was approximately 3.6 percent ofthe contribution in The Netherlands. For the entire five year period, The Netherlandsand Switzerland lead the nonlife insurance contribution, and South Africa andTaiwan for life insurance contribution. This paper examines this issue in two separatemarkets – Life_Penet for life and Nonlife_Penet for nonlife – and at the combinednational level (Total_Penet). We use a Swiss Re database to draw raw data for thesevariables.

Agency structureWe have four independent variables for agency structure. Commonly, a governmentregulatory agency draws its operating fund from the general revenue of the governmentwhereas an independent agency generates its fund from charging fees to the regulated.Based solely on this fact, we may expect that a government agency is less likely to beinfluenced by the regulated entities and make decisions reflecting the will of politiciansand the general public. Rate suppression, for example, can inflate combined and lossratios. It may induce more consumption of insurance. However, we cannot eliminate the

Price adequacyin insurance

markets

327

possibility that the politicians are captured by the regulated firms or that an independentagency is at risk of being captured by the regulated industry and becomes lenient forinsurers’ request for premium rate increase – thereby lowering the loss and combinedratios if we hold claims and insurer expenses constant. Further, the notion thatthe regulatory agency is politically independent and remains consistent over time andbetween political institutions may enhance consumer credibility (Llewellyn, 2006).A dummy variable (Agency Public) is employed to examine this issue.

Cihak and Podpiera (2007) find that the integrated supervisory structure tends to beassociated with quality and consistency of regulation across the regulated institutions.If so, citizens in the countries with an integrated structure would consume moreinsurance. We examine this issue with Agency Single for which a dummy code of “1”is assigned to countries with an agency exclusively for insurance regulation. We useAgency Another, another dummy-coded variable, to check possible differences inregulatory impact between countries with a twin peaks regulatory structure and othercountries[13].

Finally, we use the number of employees (Manpower) of the regulatory agency tocheck its influence on insurance consumption and price adequacy. Given theaforementioned Catch 22 nature in insurance regulation, we do not know a priori theexpected direction of the influence. We should note here that, for the sake of keepingsufficient observations, we decide not to standardize the data for Manpower (e.g. use ofthe average number of employees per insurance company or the average insurancepremium per employee). Neither are we clear whether the reported number of employeesis purely for insurance regulation or inclusive of those for regulation of other industriesin the countries without an agency exclusively for insurance regulation. The IAISInsurance Law Database is used to generate data for this set of variables.

Antitrust regulationGovernments worldwide commonly control entry to and exit from the insurancemarket. The entry control is to let only qualified insurance companies underwrite riskand the exit control is to minimize financial adversity when a license holder attempts toexit the market without fully meeting its insurance obligations. Licensing provides theregulator with leverage to compel insurers to comply with national laws. Given,however, that all the countries in the final data set report they control license, we do notinclude market entry license in the empirical models.

There are other variables in The IAIS Insurance Law Database we find that arerelated to this regulation[14]. The majority of countries grant license for business in asingle market (i.e. life or nonlife) but some countries still issue a single license forbusiness in both markets. We investigate the impact of the presence of compositeinsurers (License Composite) on insurance consumption and price adequacy. Separately,some countries (24 percent of the sample) apply an economic needs test (License EconNeeds) to control the number of insurance companies in the domestic market. Thedirection of the impact of each of these variables is not known a priori.

Checking the impact of market exit regulation, we consider two variables. Themajority of governments subject their regulated companies to preapproval for the exit(Exit Approval ), to a special law governing the exit (Exit Law) or both. Control of theexit and presence of the law are expected to increase insurance consumption. We expectno impact on price adequacy as an exit decision is a likely result – not a cause – of

JRF14,4

328

premium inadequacy. We find that all data in the final set use the preapprovalmeasure, thus dropping Exit Approval from the test. We also drop Exit Law from theprice adequacy test as it carries the value of unity in the final OECD dataset.

Capital, solvency and financial regulationConsumer protection concerns drive governments to insist on certain continuing levelsof insurer financial solidity. Thus, regulatory agencies control the initial capital forinsurance business applicants and the ongoing capital for incumbent insurers. In fact,all countries in the final data set report that they control initial capital. However, not allof them have introduced solvency formulae (Solvency Formula) or have the supervisoryauthority to intervene with the operations of insurers under extreme financial distress(Solvency Intervene). Presence of such formulae or regulatory authority is expected togenerate confidence in the consumers, thus increasing insurance consumption.Of course, extreme stringency in solvency regulation could discourage entry to andresulting higher prince in the market.

A meaningful assessment of insurers’ financial solidity is feasible only when theyare all complied to follow a uniform accounting convention (e.g. asset and liabilityvaluation using statutory accounting principle). It is expected that citizens in thecountries with a uniform convention regulation (Regulation Account) stay confidentwith insurer operations and more actively consume insurance than citizens in othercountries. So are the consumers in the countries where the government requiresthe regulated to use prescribed standardized forms for financial reporting (FilingStandard ).

Market conduct regulationSeveral variables are used to look into the impact of price and product regulation as wellas self-regulation. Price and product regulations are commonly to reduce the likelihoodthat insurers take unfair advantage of their policyholders’ knowledge about the cost ofinsurance and the contract, respectively. For instance, a government may controlpremium rates – Life Price Control and Nonlife Price Control – so as to keep the cost ofinsurance reasonable (i.e. not excessive). It is thus expected that the cost is “relatively”less adequate in the countries with a price control regulation than in other countries.Whether the control will lead to higher insurance consumption is not known a priori forthe reason that insurers may limit the supply of insurance subject to this regulation. Weexpect similar results when the regulator requires mandatory inclusion of certain policyconditions in life insurance contracts (Life Product Control ) or in nonlife contracts(Nonlife Product Control ) or when it mandates tariff rates in the life insurance market(Life Price Mandatory) or in the nonlife market (Nonlife Price Mandatory).

Two control variables reflect self-regulation[15]. One is corporate governanceregulation or equivalent applicable to insurance companies (Corporate Governance)[16].The other is regulation requiring insurance companies to employ an actuary in partfor internal auditing risk management purposes (Actuary). Presence of these measuresimplies that the market is likely orderly, thus increasing consumer confidence andinsurance consumption. Finally, we check whether regulation of insurance intermediaries(Intermediary) affects insurance consumption. None of Corporate Governance, Actuary orIntermediary is applied to the price adequacy test (Models 4-9) because of the unity in valuein the reduced OECD statistics-based dataset.

Price adequacyin insurance

markets

329

Economic and political stability[17]Insurance consumption and price is known to be affected by inflation in the localeconomy. A rise in the inflation rate, for example, may decrease not only consumptionbut also price adequacy in the insurance market, especially in life and other long-terminsurance (e.g. liability) markets[18]. We use the general inflation rate of the economy(Inflation) for the test of insurance consumption and consumer price indices (OECDCPI) for the test of price adequacy. The inflation data are from World EconomicFactbook and the CPI data from OECD Insurance Statistics.

To check differences between OECD member countries and other countries, weemploy a dummy variable (OECD). We note again that some non-OECDmember countries are also advanced economies. To proxy measure the influence ofthe local political environment, we use the Corruption Perceptions Index (CorruptionFree) published by Transparency International (2006–2010). This indicator iscalculated using data from 13 sources by ten institutions and the data sources coverthe past two years prior to the publication year. Yeh and Vaughn (2007) find that theperceived level of corruption is not significantly correlated with economic growth(thus likely insurance consumption) in general but affects adversely economic growth ofdeveloping countries.

National cultureCulture – even voodoo in some communities – tends to affect consumer’s perceptionabout insurance. Use of culture proxies often generates statistically significantevidence that culture influences the demand for life insurance (Chiu and Kwok, 2008)and nonlife insurance (Park and Lemaire, 2012). Corruption freeness is anotherdimension possibly signaling national differences. Both papers used Geert-Hofstededimensions. We offer below a brief description of the dimensions and some findingsfrom our data:

. Power distance (PDI) is the degree of inequality between families and organizationswith power and those without power. Countries with a high PDI are more likely toaccept the inequality and exhibit a higher degree of centralization of authority andleadership. Citizens of those countries thus are likely to depend on the leaders andconsume less risk financing services. Conversely, insurance is more accepted in thecountries with a low PDI (e.g. Austria, Israel and Denmark in this study).

. Individualism (IDV) measures the representative scope of care expressed by thegeneral public. Citizens in individualist countries (e.g. Australia, Canada,Hungary and The Netherlands) are likely to rely on external risk financial toolsthan retention of the risk with, say, other members in the extended family.

. Hofstede classifies societies into one with masculinity (MAS) and the other withfeminity. Ceteris paribus, members in the latter society (e.g. Sweden, Norway andThe Netherlands) care more for family and group member safety and consumemore life insurance. Whether and how this set of traits would affect nonlifeinsurance consumption is not known a priori.

. Uncertainty avoidance (UAI), as compared to tolerance, is the extent ofpreference for structured economic infrastructure and social systems. Countrieswith a high UAI (Guatemala, Uruguay, Malta and Japan) thus would consumemore risk financing services than other countries.

JRF14,4

330

These and other cultural dimension scores are not to scale and pose some difficulty inmeasuring a relative difference of a score between two countries. We overcome thisissue by employing the following standardization process so that all scores range fromzero to one:

1 2Index j

Highest 2 Index jCountry i

Index jHighest

; ð4Þ

where j is for each of the four indexes and i is for country. All other things beingconstant, we expect more of insurance consumptions in the countries with a low scorefor PDI (Power Distance) or MAS (Masculinity) or a high score for each of IDV(Individualism) or UAI (Uncertainty Avoidance).

Model and data constraintsFor empirical estimation, we use an uneven panel of country data over fiveyears (2005-2009) in part to increase the number of observations and in part to improvethe significance of test results of OLS regression. A Pearson correlation check and avariable inflation and eigenvalue check of the models for multicollinearity indicatea high and negative correlation between Power Distance and Individualism and weadd a multiplicative term (PDI*IDV) as a solution. Normality checks with kurdosis,Shapiro-Wilk and Kolmogorov-Smirnov tests lead us to log-transform insurance density(consumption) and penetration ratios.

The only known source for country data about the insurance regulators andregulatory measures is The IAIS Insurance Law Database – a collection of IAIS surveyresponses. The questionnaires were revised a few times, the latest one major revisionbeing for data year 2005. Many survey questions are designed for a yes-no answer andmissing data are found from some respondent jurisdictions. These constraints togetherlimit us to use data for a total of 68 countries that responded to the survey at least onceduring survey years 2005-2009. Most of the regulation-related variables for this studyare dummy-coded.

Two sources are used to collect insurance market data: Swiss Re’s World InsuranceDatabase for selected economic indicators, insurance penetration and density; andOECD Insurance Statistics for premium, loss and insurer expense data by market as wellas consumer price indices by country. Not all OECD member countries provide the fulldata for the Insurance Statistics. Notably, New Zealand, the UK and the USA did notprovide premium or loss data for 2005-2009. We also extract data from the CorruptionPerceptions Index by Transparency International and the Geert-Hofstede indexes.

The initial dataset covers 67 countries including all OECD member countries for theperiod of 2005-2009. A second check for serious cases of missing observations leads todeletion of data for 11 OECD countries. Employment of cultural dimension indexesalso reduces the number of surviving observations. The regression is conducted usingup to 245 observations. Some minor variations in the number exist for the run ofinsurance consumption models. Given that loss data are available from the OECDInsurance Statistics only, we delete non-OECD member countries for the price adequacyrun (Models 4 through 9).

The following of 56 countries are examined in this study, including 23 OECD countries(marked “O” here): Argentina, Australia (O), Austria (O), Belgium (O), Brazil, Canada (O),Colombia, Croatia, Cyprus, Czech Republic (O), Denmark (O), Ecuador, Egypt, El Salvador,

Price adequacyin insurance

markets

331

France (O), Germany (O), Guatemala, Hong Kong, Hungary (O), Iceland (O), Israel,Italy (O), Japan (O), Jordan, Korea (O), Latvia, Lebanon, Lithuania, Luxembourg (O),Malaysia, Malta, Mexico (O), Morocco, The Netherlands (O), Norway (O), Pakistan, Peru,the Philippines, Poland (O), Romania, Russia, Saudi Arabia, Serbia, Singapore,Slovakia (O), Slovenia, South Africa, Spain (O), Sri Lanka, Sweden (O), Switzerland (O),Taiwan, Turkey (O), the UAE, Ukraine and Uruguay. As of the data year 2009, these56 countries in the aggregate represent a population of 1.93 billion (approximately45 percent of the world population less China and India). The aggregate of the countries inthis study had 1,579 and 4,477 headquarters of life and nonlife insurance companies,respectively, in 2009. Additional 487 composite insurance companies and 588 reinsurancecompanies were also in operation in the countries during the same year.

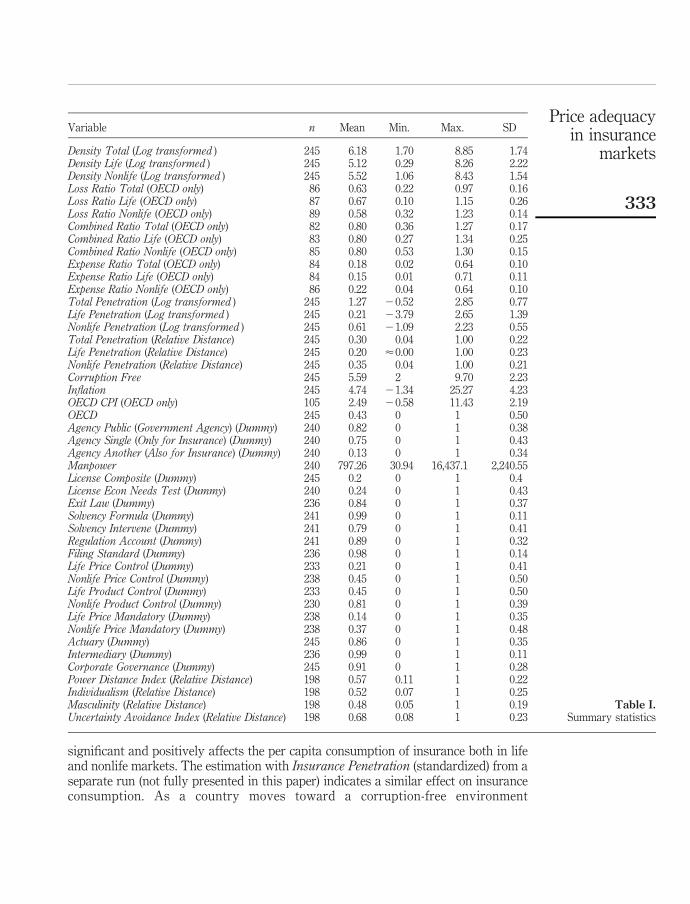

Key empirical findingsAs presented in Table I of summary statistics, we find that the regulatory agencyis commonly part of the government (82 percent) and tends to be exclusively forinsurance regulation (75 percent). Use of a dual agency structure for insuranceregulation is observed in 13 percent of the observations.

Market entry regulation (i.e. license regulation) is found in all countries – thus not usingLicense for regression – and composite insurance operations are observed in 20 percent ofthe cases. Several governments (24 percent) apply an economic needs test for evaluation ofinsurance license applications. All countries report that licensed companies must seekapproval of bankruptcy from the regulatory authority (not shown in the table) and84 percent of them have the law or regulations governing insurer’s exit from the market.

Almost all countries (99 percent) have solvency formulae (e.g. required capital)stipulated in their local laws. However, only 79 percent of the respondents have thepower to intervene with the operations of a licensed insurer before its capital falls belowthe required threshold. Most countries require companies to file their financials usingstandard forms (98 percent) and the authorities use the information for regulation andsupervision purposes (89 percent). The majority of the countries require the regulated tohire an actuary (86 percent).

Price and product regulation is observed in the sample countries. In fact, governmentstend to apply this regulation more on nonlife business than on life business.Governments apply price control more to nonlife insurance (45 percent) than to lifeinsurance (21 percent). Product control regulation is more frequent in nonlife insurance(81 percent) than in life insurance (45 percent). Tariff regulation is more frequentlyobserved in nonlife insurance (37 percent) than in life insurance (14 percent).

For the regression, we conduct a total of 18 tests in two groups. We employlog-transformed insurance penetration data for the first group of nine tests andstandardized insurance penetration scores for the second group of nine tests. All modelsare statistically significant and the findings from both groups are often similar. Yeardummies are found to be statistically significant for 2007, 2008 and 2009 in most models.The remaining part of this section discusses the findings with the log-transformedpenetration data.

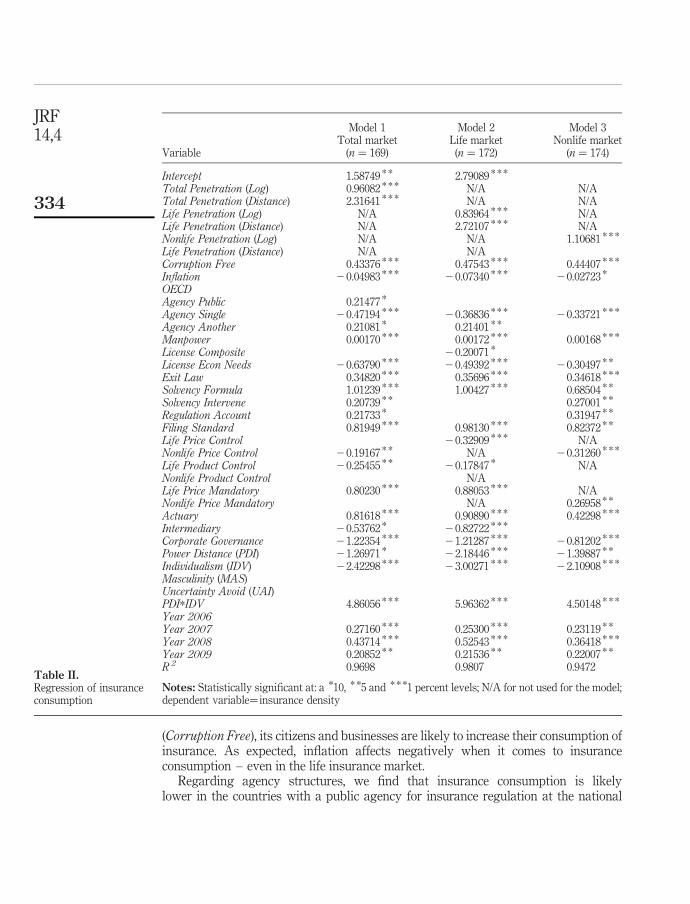

Impact on insurance consumptionTable II presents the findings from the regression using Insurance Density as thedependent variable. As expected, Insurance Penetration (log-transformed) is statistically

JRF14,4

332

significant and positively affects the per capita consumption of insurance both in lifeand nonlife markets. The estimation with Insurance Penetration (standardized) from aseparate run (not fully presented in this paper) indicates a similar effect on insuranceconsumption. As a country moves toward a corruption-free environment

Variable n Mean Min. Max. SD

Density Total (Log transformed ) 245 6.18 1.70 8.85 1.74Density Life (Log transformed ) 245 5.12 0.29 8.26 2.22Density Nonlife (Log transformed ) 245 5.52 1.06 8.43 1.54Loss Ratio Total (OECD only) 86 0.63 0.22 0.97 0.16Loss Ratio Life (OECD only) 87 0.67 0.10 1.15 0.26Loss Ratio Nonlife (OECD only) 89 0.58 0.32 1.23 0.14Combined Ratio Total (OECD only) 82 0.80 0.36 1.27 0.17Combined Ratio Life (OECD only) 83 0.80 0.27 1.34 0.25Combined Ratio Nonlife (OECD only) 85 0.80 0.53 1.30 0.15Expense Ratio Total (OECD only) 84 0.18 0.02 0.64 0.10Expense Ratio Life (OECD only) 84 0.15 0.01 0.71 0.11Expense Ratio Nonlife (OECD only) 86 0.22 0.04 0.64 0.10Total Penetration (Log transformed ) 245 1.27 20.52 2.85 0.77Life Penetration (Log transformed ) 245 0.21 23.79 2.65 1.39Nonlife Penetration (Log transformed ) 245 0.61 21.09 2.23 0.55Total Penetration (Relative Distance) 245 0.30 0.04 1.00 0.22Life Penetration (Relative Distance) 245 0.20 <0.00 1.00 0.23Nonlife Penetration (Relative Distance) 245 0.35 0.04 1.00 0.21Corruption Free 245 5.59 2 9.70 2.23Inflation 245 4.74 21.34 25.27 4.23OECD CPI (OECD only) 105 2.49 20.58 11.43 2.19OECD 245 0.43 0 1 0.50Agency Public (Government Agency) (Dummy) 240 0.82 0 1 0.38Agency Single (Only for Insurance) (Dummy) 240 0.75 0 1 0.43Agency Another (Also for Insurance) (Dummy) 240 0.13 0 1 0.34Manpower 240 797.26 30.94 16,437.1 2,240.55License Composite (Dummy) 245 0.2 0 1 0.4License Econ Needs Test (Dummy) 240 0.24 0 1 0.43Exit Law (Dummy) 236 0.84 0 1 0.37Solvency Formula (Dummy) 241 0.99 0 1 0.11Solvency Intervene (Dummy) 241 0.79 0 1 0.41Regulation Account (Dummy) 241 0.89 0 1 0.32Filing Standard (Dummy) 236 0.98 0 1 0.14Life Price Control (Dummy) 233 0.21 0 1 0.41Nonlife Price Control (Dummy) 238 0.45 0 1 0.50Life Product Control (Dummy) 233 0.45 0 1 0.50Nonlife Product Control (Dummy) 230 0.81 0 1 0.39Life Price Mandatory (Dummy) 238 0.14 0 1 0.35Nonlife Price Mandatory (Dummy) 238 0.37 0 1 0.48Actuary (Dummy) 245 0.86 0 1 0.35Intermediary (Dummy) 236 0.99 0 1 0.11Corporate Governance (Dummy) 245 0.91 0 1 0.28Power Distance Index (Relative Distance) 198 0.57 0.11 1 0.22Individualism (Relative Distance) 198 0.52 0.07 1 0.25Masculinity (Relative Distance) 198 0.48 0.05 1 0.19Uncertainty Avoidance Index (Relative Distance) 198 0.68 0.08 1 0.23

Table I.Summary statistics

Price adequacyin insurance

markets

333

(Corruption Free), its citizens and businesses are likely to increase their consumption ofinsurance. As expected, inflation affects negatively when it comes to insuranceconsumption – even in the life insurance market.

Regarding agency structures, we find that insurance consumption is likelylower in the countries with a public agency for insurance regulation at the national

Model 1 Model 2 Model 3

VariableTotal market

(n ¼ 169)Life market(n ¼ 172)

Nonlife market(n ¼ 174)

Intercept 1.58749 * * 2.79089 * * *

Total Penetration (Log) 0.96082 * * * N/A N/ATotal Penetration (Distance) 2.31641 * * * N/A N/ALife Penetration (Log) N/A 0.83964 * * * N/ALife Penetration (Distance) N/A 2.72107 * * * N/ANonlife Penetration (Log) N/A N/A 1.10681 * * *

Life Penetration (Distance) N/A N/ACorruption Free 0.43376 * * * 0.47543 * * * 0.44407 * * *

Inflation 20.04983 * * * 20.07340 * * * 20.02723 *

OECDAgency Public 0.21477 *

Agency Single 20.47194 * * * 20.36836 * * * 20.33721 * * *

Agency Another 0.21081 * 0.21401 * *

Manpower 0.00170 * * * 0.00172 * * * 0.00168 * * *

License Composite 20.20071 *

License Econ Needs 20.63790 * * * 20.49392 * * * 20.30497 * *

Exit Law 0.34820 * * * 0.35696 * * * 0.34618 * * *

Solvency Formula 1.01239 * * * 1.00427 * * * 0.68504 * *

Solvency Intervene 0.20739 * * 0.27001 * *

Regulation Account 0.21733 * 0.31947 * *

Filing Standard 0.81949 * * * 0.98130 * * * 0.82372 * *

Life Price Control 20.32909 * * * N/ANonlife Price Control 20.19167 * * N/A 20.31260 * * *

Life Product Control 20.25455 * * 20.17847 * N/ANonlife Product Control N/ALife Price Mandatory 0.80230 * * * 0.88053 * * * N/ANonlife Price Mandatory N/A 0.26958 * *

Actuary 0.81618 * * * 0.90890 * * * 0.42298 * * *

Intermediary 20.53762 * 20.82722 * * *

Corporate Governance 21.22354 * * * 21.21287 * * * 20.81202 * * *

Power Distance (PDI) 21.26971 * 22.18446 * * * 21.39887 * *

Individualism (IDV) 22.42298 * * * 23.00271 * * * 22.10908 * * *

Masculinity (MAS)Uncertainty Avoid (UAI)PDI*IDV 4.86056 * * * 5.96362 * * * 4.50148 * * *

Year 2006Year 2007 0.27160 * * * 0.25300 * * * 0.23119 * *

Year 2008 0.43714 * * * 0.52543 * * * 0.36418 * * *

Year 2009 0.20852 * * 0.21536 * * 0.22007 * *

R 2 0.9698 0.9807 0.9472

Notes: Statistically significant at: a *10, * *5 and * * *1 percent levels; N/A for not used for the model;dependent variable¼ insurance density

Table II.Regression of insuranceconsumption

JRF14,4

334

market level. However, presence of the effect at the market level cannot be confirmed.Findings for agency size (Manpower) indicate, albeit weakly, that the countries with alarge regulatory agency tend to consume more insurance than those with a small agency.

Insurance consumption is likely lower – more in the life insurance market than inthe nonlife insurance market – when the government controls the number of licensedinsurance companies (License Econ Needs). This finding suggests that removal of theeconomic-needs test could be an effective means to further develop the local insurancemarkets. Insurance consumption is also likely lower in the countries that permitcomposite insurance operations (License Composite). This effect is found statisticallysignificant only in the life insurance market.

Citizens in the markets subject to solvency formulae (Solvency Formula) tend toconsumer more insurance than those in other countries. Such a pattern is observed inboth life and nonlife markets. The impact of authority’s power to intervene with theoperations of the insurer under severe financial or operational distress (SolvencyIntervene) is observed but mainly in the nonlife market.

Presence of accounting regulation (Regulation Account) and the financial statementfiling requirement using a standard format (Filing Standard ) affects insuranceconsumption. The impact of the filing requirement is observed in both life and nonlifemarkets whereas that of the accounting regulation is in the nonlife market only.

Evidence supporting a possible impact of antitrust regulation is observed.Specifically, control of insurance price by government (e.g. prior approval of premiumrates) is likely reduce insurance consumption in both life and nonlife markets. Thisfinding is the opposite of our expectation and implies that price controlling is probablymore toward approval of the rate change requests (a practice that would benefitinsurers) than toward price suppression (a practice that would benefit consumers).A similar finding is observed when the government controls life insurance products(Life Product Control ). The positive impact of tariff pricing – a policy commonly toprotect individuals and small businesses in selected lines of business – is found to bepositive in both life and nonlife markets.

When insurers are required to employ an actuary (Actuary), consumers tend topurchase more insurance. When government regulates insurance brokers and agents(Intermediary) or when insurers are required to have a corporate governance program(Corporate Governance), insurance consumption is likely lower even at each marketlevel, implying that such requirements might increase the cost of insurance.

Regarding the role of cultural dimensions, the findings for Power Distance(standardized PDI) is as expected and countries with a low PDI score tend to consumemore insurance. The directional effect for Individualism (standardized IDV) is found tobe the opposite to our expectation in that individualist countries consume less insurancethan collectivist countries. In the individualist countries with a high PDI score(PDI*IDV), we find a positive impact of the production of these dimensions on insuranceconsumption.

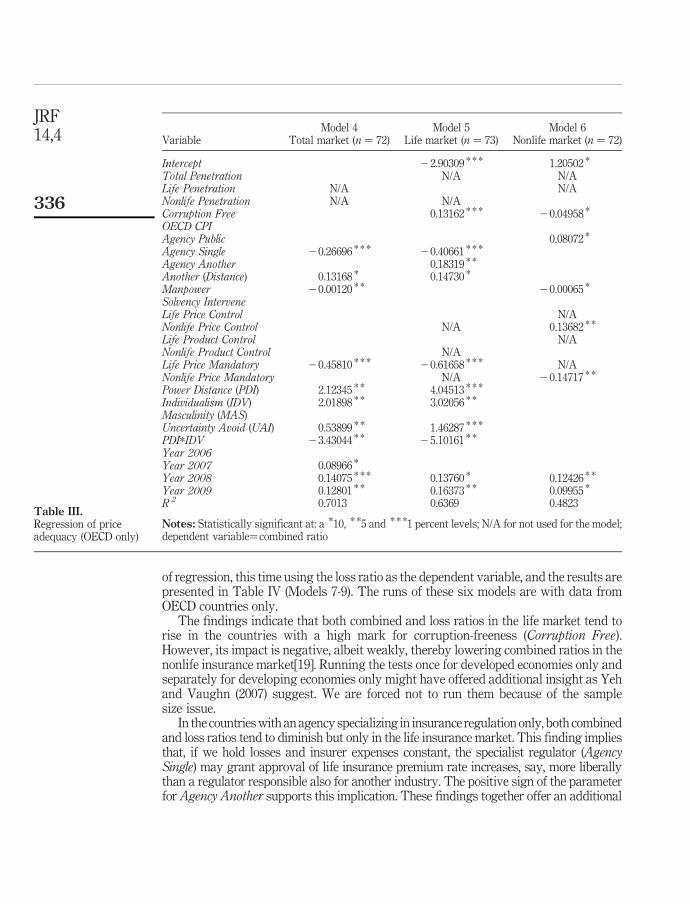

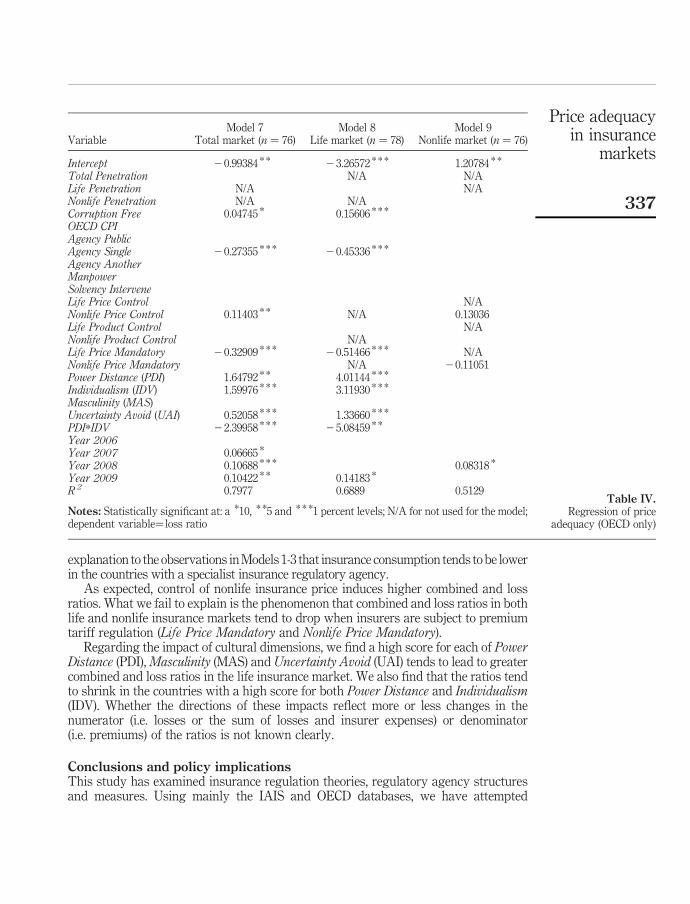

Impact on price adequacyWe employ two proxies for price adequacy, Table III presents the findings of Models4-6 in which the proxy is the combined ratio – or the sum of the loss ratio and the insurerexpense ratio. We expect that all other matters held constant, insurance companies areless capable of controlling the loss ratio than the expense ratio. Hence, we run another set

Price adequacyin insurance

markets

335

of regression, this time using the loss ratio as the dependent variable, and the results arepresented in Table IV (Models 7-9). The runs of these six models are with data fromOECD countries only.

The findings indicate that both combined and loss ratios in the life market tend torise in the countries with a high mark for corruption-freeness (Corruption Free).However, its impact is negative, albeit weakly, thereby lowering combined ratios in thenonlife insurance market[19]. Running the tests once for developed economies only andseparately for developing economies only might have offered additional insight as Yehand Vaughn (2007) suggest. We are forced not to run them because of the samplesize issue.

In the countries with an agency specializing in insurance regulation only, both combinedand loss ratios tend to diminish but only in the life insurance market. This finding impliesthat, if we hold losses and insurer expenses constant, the specialist regulator (AgencySingle) may grant approval of life insurance premium rate increases, say, more liberallythan a regulator responsible also for another industry. The positive sign of the parameterfor Agency Another supports this implication. These findings together offer an additional

Model 4 Model 5 Model 6Variable Total market (n ¼ 72) Life market (n ¼ 73) Nonlife market (n ¼ 72)

Intercept 22.90309 * * * 1.20502 *

Total Penetration N/A N/ALife Penetration N/A N/ANonlife Penetration N/A N/ACorruption Free 0.13162 * * * 20.04958 *

OECD CPIAgency Public 0.08072 *

Agency Single 20.26696 * * * 20.40661 * * *

Agency Another 0.18319 * *

Another (Distance) 0.13168 * 0.14730 *

Manpower 20.00120 * * 20.00065 *

Solvency InterveneLife Price Control N/ANonlife Price Control N/A 0.13682 * *

Life Product Control N/ANonlife Product Control N/ALife Price Mandatory 20.45810 * * * 20.61658 * * * N/ANonlife Price Mandatory N/A 20.14717 * *

Power Distance (PDI) 2.12345 * * 4.04513 * * *

Individualism (IDV) 2.01898 * * 3.02056 * *

Masculinity (MAS)Uncertainty Avoid (UAI) 0.53899 * * 1.46287 * * *

PDI*IDV 23.43044 * * 25.10161 * *

Year 2006Year 2007 0.08966 *

Year 2008 0.14075 * * * 0.13760 * 0.12426 * *

Year 2009 0.12801 * * 0.16373 * * 0.09955 *

R 2 0.7013 0.6369 0.4823

Notes: Statistically significant at: a *10, * *5 and * * *1 percent levels; N/A for not used for the model;dependent variable¼combined ratio

Table III.Regression of priceadequacy (OECD only)

JRF14,4

336

explanation to the observations in Models 1-3 that insurance consumption tends to be lowerin the countries with a specialist insurance regulatory agency.

As expected, control of nonlife insurance price induces higher combined and lossratios. What we fail to explain is the phenomenon that combined and loss ratios in bothlife and nonlife insurance markets tend to drop when insurers are subject to premiumtariff regulation (Life Price Mandatory and Nonlife Price Mandatory).

Regarding the impact of cultural dimensions, we find a high score for each of PowerDistance (PDI), Masculinity (MAS) and Uncertainty Avoid (UAI) tends to lead to greatercombined and loss ratios in the life insurance market. We also find that the ratios tendto shrink in the countries with a high score for both Power Distance and Individualism(IDV). Whether the directions of these impacts reflect more or less changes in thenumerator (i.e. losses or the sum of losses and insurer expenses) or denominator(i.e. premiums) of the ratios is not known clearly.

Conclusions and policy implicationsThis study has examined insurance regulation theories, regulatory agency structuresand measures. Using mainly the IAIS and OECD databases, we have attempted

Model 7 Model 8 Model 9Variable Total market (n ¼ 76) Life market (n ¼ 78) Nonlife market (n ¼ 76)

Intercept 20.99384 * * 23.26572 * * * 1.20784 * *

Total Penetration N/A N/ALife Penetration N/A N/ANonlife Penetration N/A N/ACorruption Free 0.04745 * 0.15606 * * *

OECD CPIAgency PublicAgency Single 20.27355 * * * 20.45336 * * *

Agency AnotherManpowerSolvency InterveneLife Price Control N/ANonlife Price Control 0.11403 * * N/A 0.13036Life Product Control N/ANonlife Product Control N/ALife Price Mandatory 20.32909 * * * 20.51466 * * * N/ANonlife Price Mandatory N/A 20.11051Power Distance (PDI) 1.64792 * * 4.01144 * * *

Individualism (IDV) 1.59976 * * * 3.11930 * * *

Masculinity (MAS)Uncertainty Avoid (UAI) 0.52058 * * * 1.33660 * * *

PDI*IDV 22.39958 * * * 25.08459 * *

Year 2006Year 2007 0.06665 *

Year 2008 0.10688 * * * 0.08318 *

Year 2009 0.10422 * * 0.14183 *

R 2 0.7977 0.6889 0.5129

Notes: Statistically significant at: a *10, * *5 and * * *1 percent levels; N/A for not used for the model;dependent variable¼ loss ratio

Table IV.Regression of price

adequacy (OECD only)

Price adequacyin insurance

markets

337

to empirically investigate the impact of the agency structure, antitrust regulation(market entry and exit), prudential regulation (accounting, capital and solvencyregulation), market conduct regulation (actuary, intermediary and corporategovernance) as well as selected factors reflecting the economic, political and culturaldimensions on insurance consumption and price adequacy both at the country level andthe market level.

We find some evidence supporting the impact of the agency structure on insuranceconsumption: that is, such consumption is lower when the country maintains anauthority exclusively for insurance regulation but the consumption in the life insurancemarket is higher when the agency is part of government or when another agency isjointly responsible for insurance regulation.

Market entry regulation likely leads to lower consumption whereas market exitregulation has the opposite effect. Solvency regulation and required use of standardforms for insurer financials all lead to greater consumption of insurance in life andnonlife markets. A positive impact on the nonlife insurance market is observed foraccounting regulation and regulator’s power to intervene with companies under severedistress. Presence of price control regulation may result in lower consumption ofinsurance whereas presence of tariff rating (presumably in selected lines of insurance)brings about a rise in the consumption. Regulation of insurance intermediaries orcorporate governance may lower insurance consumption whereas the requirement thatinsurers employ an actuary or actuaries gives rise to the consumption.

We find no difference between OECD and non-OECD countries included in this study.However, corruption-freeness and inflation have positive and negative impact, respectively,on insurance consumption. We have also examined the relationship between culturaldimensions and insurance consumption but the findings are rather unclear.

Using OECD country data only, we check the impact of the aforementioned factors onprice adequacy represented by combined and loss ratios. We find a negative impact of thesingle agency structure and tariff regulation in the life insurance market and a positiveimpact of regulation by two or more agencies in the life insurance market and of pricecontrol regulation in the nonlife insurance market. Corruption-freeness positively affectsthe loss ratio in the life insurance market and the combined ratio in the nonlife market.

The findings in the aggregate offer an insight regarding regulatory structure(e.g. public vs private; single vs integrated) and the impact of specific regulatorymeasures. However, generalization of the findings would be challenging. Theobservations for Models 4-9 are limited in number in part because of deletion of datafor several developed economies such as New Zealand, the UK and the USA. All thevariables for regulatory structure and measures are dummy-coded. The study does notinclude any control variables covering but not limited to the operating budget, thenumber of regulated insurance companies (and intermediaries) and the insurer expenseratio. A fuller scope, cross-country investigation (e.g. efficiency study) is thus called for.

With the innovations in financial services markets, we expect improvement in riskmanagement, reduced financial and macroeconomic volatility, lower intermediationcosts and enhanced information flows. An obvious outcome could be growth ofsystemic crisis possibility, contagion risk and a new stream of information complexity(Chan-Liu, 2010) and the rising cost of regulation.

Whether regulation and supervision is rule-based or principle-based shouldnot matter. The principles are to form its scope and rules to administrate those

JRF14,4

338

principles (Nicols, 2009). Regulators do not need to be smarter than the key players inthe regulated industry. What they should possess is rationality and objectivity informing and administrating regulation and supervision.

What do we picture the regulatory agency that helps us enjoy quality, fairly pricedproducts and services from reliable financial institutions? We portrait one whoseconcern is not about designing new products but working to “ascertain safety andeffectiveness” (Stiglitz, 2009) and who is mindful of balancing social and economicwelfare benefits and costs. We need the regulators who know that regulation by itself iscostly and fear risk of government failure. We need them to be able to stay proactive,minimize the impact of market imperfections and remain countercyclical to preventmarket failures. We need the ones who can align societal and economic welfare in theeconomy. We need the ones who only attend to local market matters but also enhance thecountry’s participation in regional and international coordination and cooperation. In a“good” state, societal and economic fundamentals stay solid and principles of regulationshould not be fragile and the rules that government uses to guard those fundamentalsand principles stay dynamic.

Notes

1. Part of this paper including a preliminary empirical test using fewer variables was discussedin a regional one-day academic meeting.

2. Skipper and Klein (2000) note that promoting effective competition is important for productchoice value enhancement in the insurance market. Klein (2009) addresses that marketfailures are judged against the social welfare-maximizing conditions for perfect competition.

3. Neither can we ignore the importance of tax revenue motives of government.

4. Swiss Re (2011) lists, among others, improvements in insurance supervision, marketliberalization, enhanced competition and productivity as well as product innovation as thecontributing factors to the growth of insurance premiums in Emerging Asia(Hong Kong, Korea, Singapore and Taiwan) and Latin America.

5. The technical challenges include the difficulty in separating microinsurance business fromconventional business that both regulators and microinsurance companies face. Besides,several microfinance institutions (MFIs) promote microinsurance (e.g. credit life) also ascollateral to protect their loan principals and interest income.

6. In this essay, economic regulation refers to the government control of a market withimperfections and social risk management deals with fairness and social justice. Two pointsare made here. First, market failures are not indictments of the capital market system andinsolvency is an inevitable byproduct of the market. Second, the trend in social riskmanagement is toward more stringent regulation in both developed and developingeconomies.

7. The respondents include selected regional associations (e.g. CIMA in Africa and the NAIC inthe USA) and multiple lower-level jurisdictions of a country (e.g. four US states and twoCanadian provinces).

8. Despite the century-long threat of the federal government to replace state regulation withfederal regulation and the recent reform based on the 2010 Dodd-Frank Act, insuranceregulation still largely belongs to state governments in the USA. It must be noted here thatUS states of Florida and New York now have a single agency for banking and insuranceregulation.

Price adequacyin insurance

markets

339

9. Alternatively, we can classify all areas of insurance into ex ante regulation, ex postregulation (supervision) or some combination of the two. Generally, the more a state relies onmarket forces, the less it is likely to rely on ex-ante regulatory measures. Nevertheless, weobserve some recent material changes in the regulation of the financial services sector in thatpolicymakers introduce counter-cyclical regulatory measures against the development ofmajor adversities in the economy (e.g. the recent credit crisis).

10. For example, statutory accounting principles are based in part on the bankruptcy principleas compared to the on-going concern principle in generally accepted accounting principles.

11. Geert-Hofstede cultural dimension scores are not time-sensitive.

12. For the year of 2009, for example, Taiwan (14.19 percent) and Russia (0.04 percent) had thehighest and lowest life insurance penetration ratios, respectively, among the countries in thisstudy. For nonlife insurance for the same year, the highest was The Netherlands(9.33 percent) and the lowest was Pakistan (0.33 percent).

13. These two structures can be defined as integrated and unified agency systems (Llewellyn,2006). In the former, the prudential regulation of all firms in the financial services sector iscarried out by a single agency. In the latter, an agency is responsible for prudentialregulation and market conduct regulation and supervision in a single market (e.g. insurance).Also, see Lumpkin (2002) for a description of financial supervisory agency models in theOECD area and Quintyn et al. (2007) for a cross-country analysis of regulatory institutionalchanges in banking supervision.

14. The IAIS collects data for the number of licensed companies by organizational structure(e.g. stock and mutual) and by market (e.g. direct, reinsurance and captive). However, only afew countries provide the IAIS with such data.

15. All respondents report that they exercise fit-and-proper person regulation.

16. The IAIS (2003) defines that corporate governance is regarding “the manner in which boardsof directors and senior management oversee the insurers’ business [. . .] encompasses themeans by which members of the board and senior management are held accountable andresponsible for their actions”.

17. We initially considered two proxy variables – adult literacy rate and urbanization rate – tocontrol the social environment. We dropped them after finding out that the final datasetshows near unity in the variations in both variables. The average adult literacy rate and theurbanization rate of the sample are 94.23 and 72.65 percent, respectively. The data wascollected from World Economic Factbook.

18. This paper does not separate liability lines from property lines in the nonlife insurancemarket due to data availability constraints.

19. A separate run of Models 7-9 with the cultural dimension variables results in a positive,again weakly, impact of Corrupt on the loss ratios in the nonlife insurance market.

References

Arena, M. (2008), “Does insurance market activity promote economic growth? A cross-countrystudy for industrialized and developing countries”, Journal of Risk and Insurance, Vol. 75No. 4, pp. 921-946.

Bester, H., Chamberlain, D. and Hougaard, C. (2009), Making Insurance Markets Work for thePoor: Microinsurance Policy, Regulation and Supervision (Version 6, January 12), CGAPWorking Group on Microinsurance.

Chan-Liu, J. (2010), “The globalization of finance and its implications for financial stability:an overview of the issues”, Social Science Research Network Paper 1008837.

JRF14,4

340

Chiu, A. and Kwok, C. (2008), “National culture and life insurance consumption”, Journal ofInternational Business Studies, Vol. 39, pp. 88-101.

Cihak, M. and Podpiera, R. (2007), “Experience with integrated supervisors: governance andquality of supervision”, in Masciandaro, D. and Quintyn, M. (Eds), Designing FinancialSupervision Institutions: Independence, Accountability and Governance, Chapter 8,Edward Elgar, Cheltenham.

Cummins, J.D., Tennyson, S. and Weiss, M. (1998), “Consolidation and efficiency in the US lifeinsurance industry”, Journal of Banking & Finance, Vol. 23, pp. 325-357.

Cummins, J.D., Weiss, M. and Zi, H. (1999), “Organizational form and efficiency: the coexistenceof stock and mutual property-liability insurers”, Management Science, Vol. 45,pp. 1254-1269.

Eatwell, J. (2009), “Practical proposals for regulatory reform”, in Subacchi, P. andMonsarrat, A. (Eds), New Ideas for the London Summit: Recommendations to theG20 Leaders, A Chatham House and Atlantic Council of the United States Report,Appleton, WI.

Eling, M. and Luhne, M. (2010), “Efficiency in the international insurance industry:a cross-country comparison”, Journal of Banking & Finance, Vol. 34, pp. 1497-1509.

Fenn, P., Vencappa, D., Diacon, S., Klumpes, P. and O’Brien, C. (2008), “Market structure and theefficiency of European insurance companies: a stochastic frontier analysis”, Journal ofBanking & Finance, Vol. 32, pp. 86-100.

Freytag, A. and Masciandaro, D. (2007), “Financial Supervision Architecture and Central BankIndependence”, in Masciandaro, D. and Quintyn, M. (Eds), Designing Financial SupervisionInstitutions: Independence, Accountability and Governance, Chapter 6, Edward Elgar,Cheltenham.

Grace, M. and Phillips, R. (2007), “The allocation of governmental regulatory authority:federalism and the case of insurance regulation”, Journal of Risk and Insurance, Vol. 74,pp. 207-238.

Hazell, P., Anderson, J., Balzer, J., Hastrup Clemmensen, J., Hess, U. and Rispoli, F. (2010), ThePotential for Scale and Sustainability in Weather Index Insurance for Agriculture and RuralLivelihoods, The International Fund for Agricultural Development and the World FoodProgram, Rome.

(The) IAIS (2003), Insurance Core Principles and Methodology, The International Association ofInsurance Supervisors, Basel.

(The) IFSB and the IAIS (2006), Issues in Regulation and Supervision of Takaful(Islamic Insurance), The Islamic Financial Services Board and The InternationalAssociation of Insurance Supervisors, Kuala Lumpur.

Jacobzone, S., Steiner, F., Ponton, E.L. and Job, E. (2010), “Assessing the impact of regulatorymanagement systems: preliminary statistical and econometric estimates”, OECD WorkingPapers on Public Governance 17, OECD, Paris.

King, R. and Levine, R. (1995), “Finance and growth: Schumpeter might be right”, QuarterlyJournal of Economics, Vol. 108, pp. 717-738.

Klein, R. (2009), “The insurance industry and its regulation: an overview”, in Grace, M. andKlein, R. (Eds), The Future of Insurance Regulation in the United States, Chapter 2, GeorgiaState University, Atlanta, GA.

Llewellyn, D. (2006), “Institutional structure of financial regulation and supervision: the basicissues”, paper presented at World Bank Seminar: Aligning Supervisory Structures withCountry Needs, Washington, DC, June 6-7.

Price adequacyin insurance

markets

341

Lumpkin, S. (2002), Supervision of Financial Services in the OECD Area, OECD, Paris.

Meier, K.J. (1988), The Political Economy of Regulation: The Case of Insurance, State University ofNew York Press, New York, NY.

Nicols, R. (2009), “Principles for financial supervision reform”, in Subacchi, P. andMonsarrat, A. (Eds), New Ideas for the London Summit: Recommendations to the

G20 Leaders, A Chatham House and Atlantic Council of the United States Report,Appleton, WI.

Park, S. and Lemaire, J. (2012), “The impact of culture on the demand for nonlife insurance”,ASTIN Bulletin (in press).

Peltzman, S. (1976), “Toward a more general theory of regulation”, Journal of Law & Economics,Vol. 19 No. 2, pp. 211-240.

Posner, R. (1974), “Theories of economic regulation”, Bell Journal of Economics and Management

Science, Vol. 5, Autumn, pp. 337-352.

Quintyn, M., Ramirez, S. and Taylor, M. (2007), “The fear of freedom: politicians and theindependence and accountability of financial supervisors in practice”, inMarciandro, D. and Quintyn, M. (Eds), Designing Financial Supervision Institutions:Independence, Accountability and Governance, Chapter 3, Edward Elgar, Cheltenham.

Rayp, G. and van de Sijpe, N. (2007), “Measuring and explaining government efficiency indeveloping countries”, Journal of Development Studies, Vol. 43 No. 2, pp. 360-381.

Roth, J., McCord, M. and Liber, D. (2007), The Landscape of Microinsurance in the World’s 100Poorest Countries, the Microinsurance Centre, LLC, Appleton, WI.

Shiro, J. (2006), “External forces impacting the insurance industry: threats from regulation”,Geneva Papers on Risk and Insurance – Issues and Practices, Vol. 31, pp. 25-30.

Siegmund, U. (2010), “Why central banks should not regulate insurance: some arguments fromGermany”, The Geneva Association Progress, Vol. 52, December, pp. 9-11.

Skipper, H. and Klein, R. (2000), “Insurance regulation in the public interest: the path towardssolvent, competitive markets”, Geneva Papers in Risk and Insurance – Issues and Practices,Vol. 25 No. 4, pp. 482-504.

Skipper, H.D. and Kwon, W.J. (2007), Risk Management and Insurance Perspectives in a GlobalEconomy, Wiley-Blackwell, London.

Stigler, G. (1971), “The theory of economic regulation”, Bell Journal of Economics, Vol. 2, Spring,pp. 3-21.

Stiglitz, J. (2009), “Regulation and failure”, in Moss, D. and Cisternino, J. (Eds), New Perspectiveson Regulation, The Tobin Project, Cambridge, MA.

Swiss Re (2011), World Insurance Database: 1980-2010, Swiss Re, Zurich.

Transparency International (2006-2010), Corruption Perceptions Index, TransparencyInternational, Berlin.

Viscusi, K., Harrington, J. Jr and Vernon, j. (2005), Economics of Regulation and Antitrust,Massachusetts Institute of Technology, Boston, MA.

Ward, D. and Zurbruegg, R. (2000), “Does insurance promote economic growth? Evidence fromOECD countries”, Journal of Risk and Insurance, Vol. 67, pp. 489-506.

Yeh, C.-N. and Vaughn, P. Jr (2007), “Government efficiency and economic growth”, International

Atlantic Economic Society, Vol. 13, pp. 399-400.

JRF14,4

342

Further reading

Alexander, K., Dhumale, R. and Warwell, J. (2006), Global Governance of Financial Systems:The International Regulation of Systemic Risk, Oxford University Press, New York, NY.

Chen, Y.-C., Chiu, Y.-H. and Huang, C.-W. (2010), “Government administration efficiency andeconomic efficiency for 23 districts in Taiwan”, International Journal of OrganizationalInnovation, Vol. 2 No. 4, pp. 5-34.

Euromonitor International (Annual), World Economic Factbook, Euromonitor International,Washington, DC.

Hofstede, G. (1983), “The cultural relativity of organizational practices and theories”, Journal ofInternational Business Studies, Vol. 14, pp. 75-89.

Hofstede, G. (2001), Culture’s Consequences: Comparing Values, Behaviors, Institutions andOrganizations across Nations, 2nd ed., Sage, Thousand Oaks, CA.

Kwon, W.J. (2011), “Economic rationale for insurance regulation”, in Liedtke, P. andMonkiewicz, J. (Eds), The Fundamentals of Future Insurance Regulation andSupervision: A Global Perspective, Palgrave MacMillan, Basingstoke.

Masciandaro, C. and Quintyn, M. (2007), Financial Supervision Institutions: Independence,Accountability and Governance, Edward Elgar, Cheltenham.

OECD (Annual), Insurance Statistical Yearbook, OECD, Paris.

Swiss Re (2011), “Insurance in emerging markets: growth drivers and profitability”, Sigma 5.

Van Der Ende, J., Ayadi, R. and O’Brien, C. (2006), The Future of Insurance Regulation andSupervision in the EU: New Developments, New Challenges, Centre for European PolicyStudies, Brussels.

White, L.J. (1996), “Competition versus harmonization: an overview of international regulation offinancial services”, in Barfield, C.E. (Ed.), International Financial Markets: HarmonizationVersus Competition, AEI Press, Washington, DC.

Corresponding authorW. Jean Kwon can be contacted at: [email protected]

Price adequacyin insurance

markets

343

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints