the microfinance in jordan.??? what is the collection average rate of the microfinance firms rate of...

TRANSCRIPT

The The MicrofinanceMicrofinance

In JordanIn Jordan

????????

What is the collection averageWhat is the collection average

rate of the Microfinance firmsrate of the Microfinance firms

in Jordan?in Jordan?

The Microfinance in JordanThe Microfinance in Jordan

Introduction:Introduction:

I would like to present a brief general presentation I would like to present a brief general presentation about the Microfinance in Jordan.about the Microfinance in Jordan.

First I will talk about the Microfinance in the Arab First I will talk about the Microfinance in the Arab world and how did it reach specifically to Jordan.world and how did it reach specifically to Jordan.

Then, I will mention the microfinance companies in Then, I will mention the microfinance companies in Jordan: their policies, organizational structure and Jordan: their policies, organizational structure and their difficulties.their difficulties.

And finally I will explain how these difficulties have And finally I will explain how these difficulties have been solved by Delta Informatics.been solved by Delta Informatics.

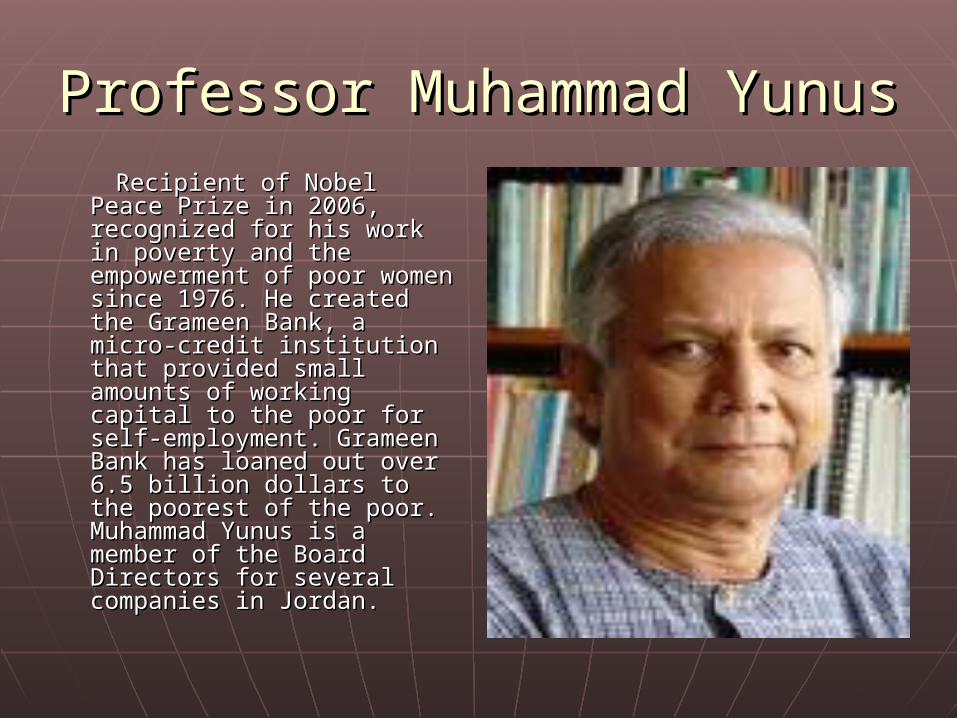

Professor Muhammad YunusProfessor Muhammad Yunus

Recipient of Nobel Peace Recipient of Nobel Peace Prize in 2006, recognized Prize in 2006, recognized for his work in poverty and for his work in poverty and the empowerment of poor the empowerment of poor women since 1976. He women since 1976. He created the Grameen created the Grameen Bank, a micro-credit Bank, a micro-credit institution that provided institution that provided small amounts of working small amounts of working capital to the poor for self-capital to the poor for self-employment. Grameen employment. Grameen Bank has loaned out over Bank has loaned out over 6.5 billion dollars to the 6.5 billion dollars to the poorest of the poor. poorest of the poor. Muhammad Yunus is a Muhammad Yunus is a member of the Board member of the Board Directors for several Directors for several companies in Jordan.companies in Jordan.

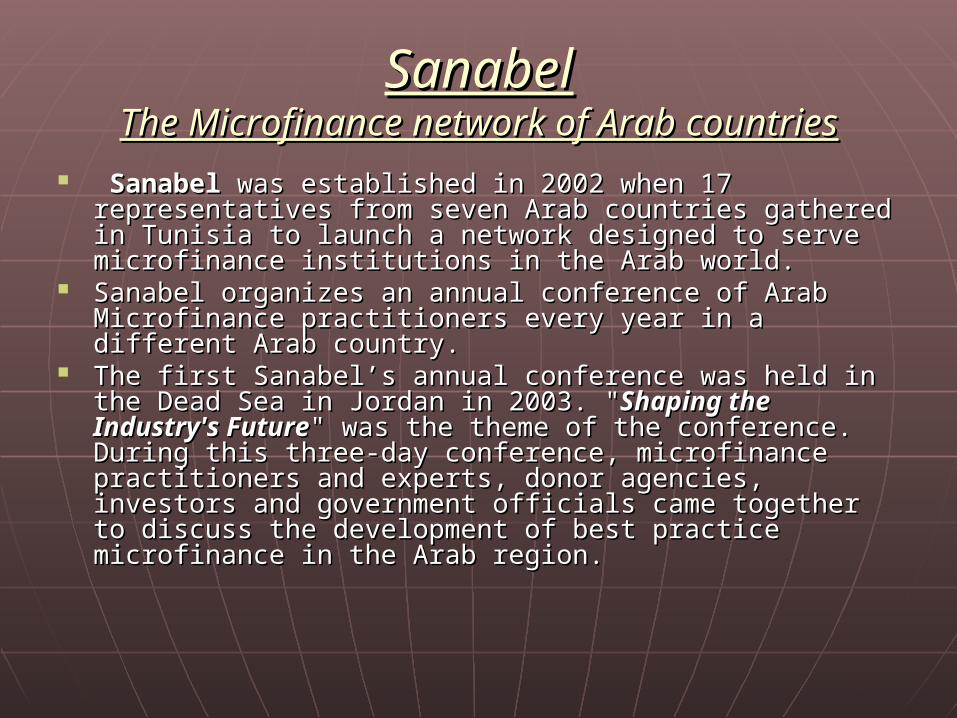

SanabelSanabelThe Microfinance network of Arab countriesThe Microfinance network of Arab countries

Sanabel Sanabel was established in 2002 when 17 representatives was established in 2002 when 17 representatives from seven Arab countries gathered in Tunisia to launch a from seven Arab countries gathered in Tunisia to launch a network designed to serve microfinance institutions in the network designed to serve microfinance institutions in the Arab world. Arab world.

Sanabel organizes an annual conference of Arab Sanabel organizes an annual conference of Arab Microfinance practitioners every year in a different Arab Microfinance practitioners every year in a different Arab country.country.

The first Sanabel’s annual conference was held in the Dead The first Sanabel’s annual conference was held in the Dead Sea in Jordan in 2003. "Sea in Jordan in 2003. "Shaping the Industry's FutureShaping the Industry's Future" " was the theme of the conference. During this three-day was the theme of the conference. During this three-day conference, microfinance practitioners and experts, donor conference, microfinance practitioners and experts, donor agencies, investors and government officials came together agencies, investors and government officials came together to discuss the development of best practice microfinance in to discuss the development of best practice microfinance in the Arab region. the Arab region.

Sanabel’s annual conferencesSanabel’s annual conferencesYEARYEAR COUNTRYCOUNTRY THEMETHEME

20032003 JordanJordan Shaping the Industry’s futureShaping the Industry’s future

20042004 EgyptEgypt Microentrepreneur awards Microentrepreneur awards

20052005 MoroccoMorocco From Microcredit to Microfinance in From Microcredit to Microfinance in the Arab Region the Arab Region

20072007 YemenYemen Serving the Poor: 10 million clients by Serving the Poor: 10 million clients by 2010 2010

20082008 TunisiaTunisia Advancing Arab Microfinance: Greater Advancing Arab Microfinance: Greater Social Impact through Inclusive Social Impact through Inclusive Financial Services Financial Services

2009-2009-MayMay

LebanonLebanon Human Capital in Microfinance: Human Capital in Microfinance: People, Passion and Value People, Passion and Value

Members & Partners of SanabelMembers & Partners of Sanabel

Membership in the network is limited Membership in the network is limited to the founders and any MFI who to the founders and any MFI who applies for membership and fulfills applies for membership and fulfills certain criteria.certain criteria.

Today Sanabel has expanded and Today Sanabel has expanded and has members in Egypt, Iraq, has members in Egypt, Iraq, Lebanon, Mauritania, Morocco, Lebanon, Mauritania, Morocco, Palestine, Saudi Arabia, Sudan ,Syria, Palestine, Saudi Arabia, Sudan ,Syria, Tunisia, Yemen and Jordan.Tunisia, Yemen and Jordan.

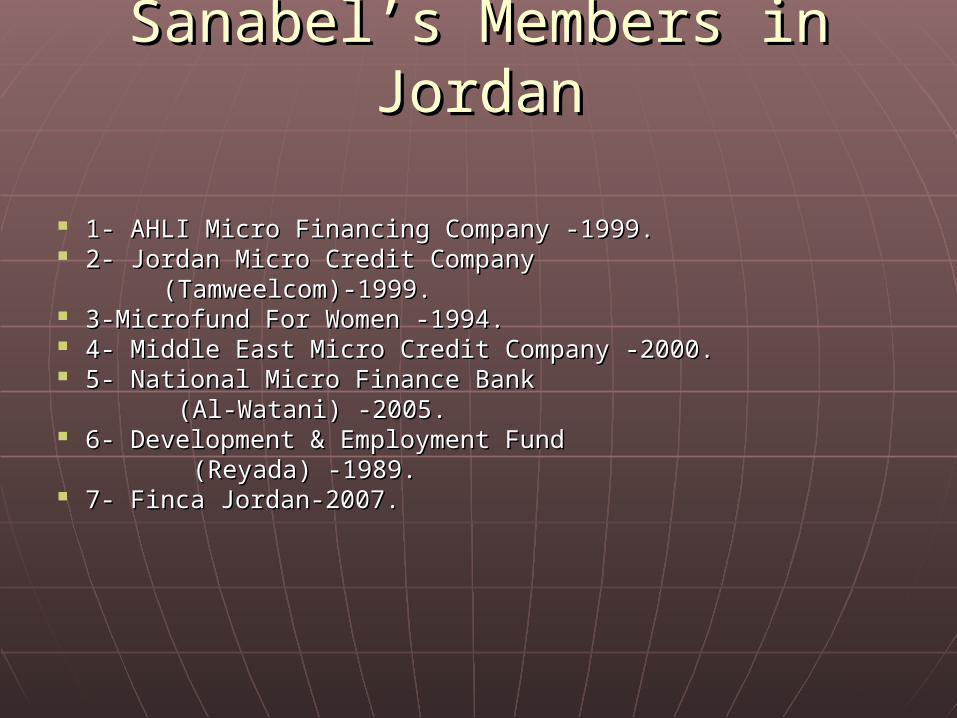

Sanabel’s Members in JordanSanabel’s Members in Jordan

1- AHLI Micro Financing Company -1999.1- AHLI Micro Financing Company -1999. 2- Jordan Micro Credit Company2- Jordan Micro Credit Company (Tamweelcom)-1999.(Tamweelcom)-1999. 3-Microfund For Women -1994.3-Microfund For Women -1994. 4- Middle East Micro Credit Company -2000.4- Middle East Micro Credit Company -2000. 5- National Micro Finance Bank5- National Micro Finance Bank (Al-Watani) -2005.(Al-Watani) -2005. 6- Development & Employment Fund6- Development & Employment Fund (Reyada) -1989.(Reyada) -1989. 7- Finca Jordan-2007.7- Finca Jordan-2007.

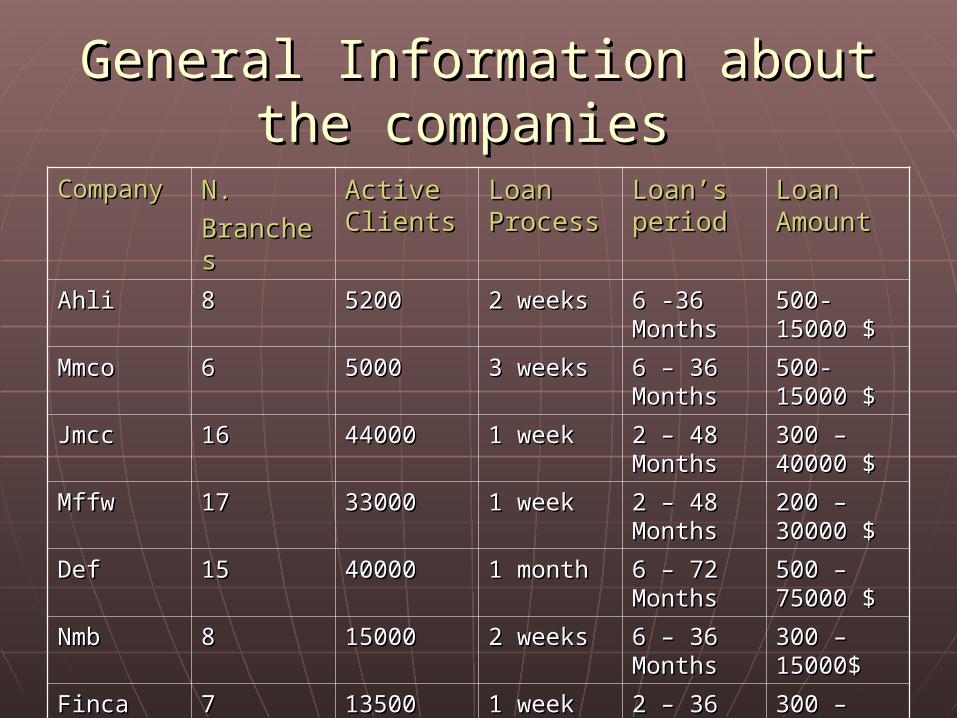

General Information about the General Information about the companies companies

CompanyCompany N.N.

BranchesBranchesActive Active ClientsClients

Loan Loan ProcessProcess

Loan’s Loan’s periodperiod

Loan Loan AmountAmount

AhliAhli 88 52005200 2 weeks2 weeks 6 -36 6 -36 MonthsMonths

500-500-15000 $15000 $

MmcoMmco 66 50005000 3 weeks3 weeks 6 – 36 6 – 36 MonthsMonths

500- 500- 15000 $15000 $

JmccJmcc 1616 4400044000 1 week1 week 2 – 48 2 – 48 MonthsMonths

300 – 300 – 40000 $40000 $

MffwMffw 1717 3300033000 1 week1 week 2 – 48 2 – 48 MonthsMonths

200 – 200 – 30000 $30000 $

DefDef 1515 4000040000 1 month1 month 6 – 72 6 – 72 MonthsMonths

500 – 500 – 75000 $75000 $

NmbNmb 88 1500015000 2 weeks2 weeks 6 – 36 6 – 36 MonthsMonths

300 – 300 – 15000$15000$

FincaFinca 77 1350013500 1 week1 week 2 – 36 2 – 36 MonthsMonths

300 – 300 – 15000$15000$

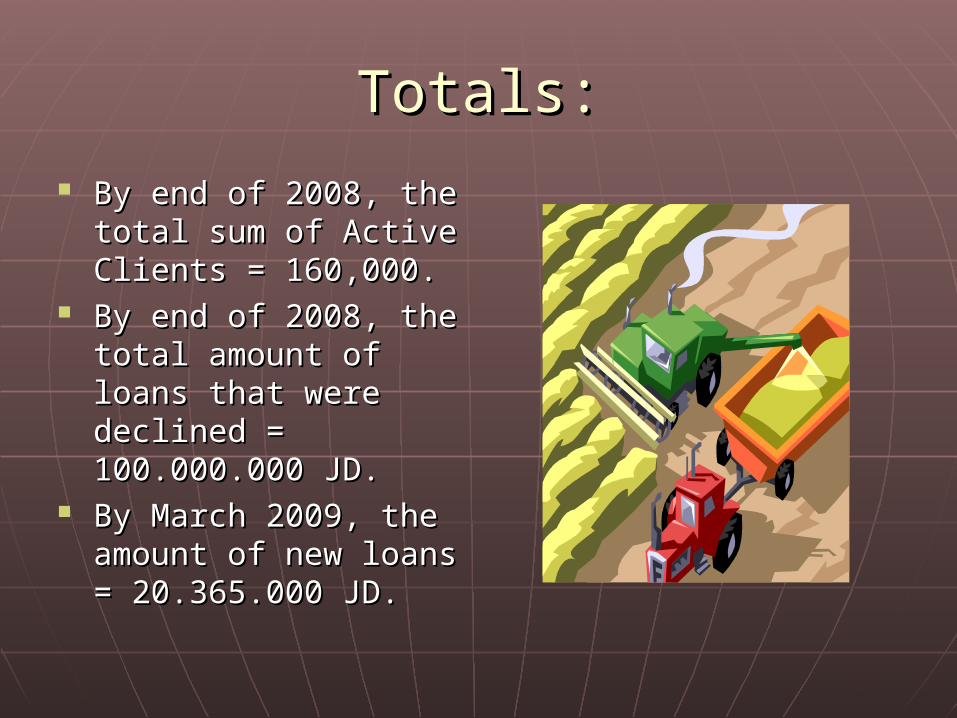

Totals:Totals:

By end of 2008, the By end of 2008, the total sum of Active total sum of Active Clients = 160,000.Clients = 160,000.

By end of 2008, the By end of 2008, the total amount of loans total amount of loans that were declined = that were declined = 100.000.000 JD.100.000.000 JD.

By March 2009, the By March 2009, the amount of new loans amount of new loans = 20.365.000 JD.= 20.365.000 JD.

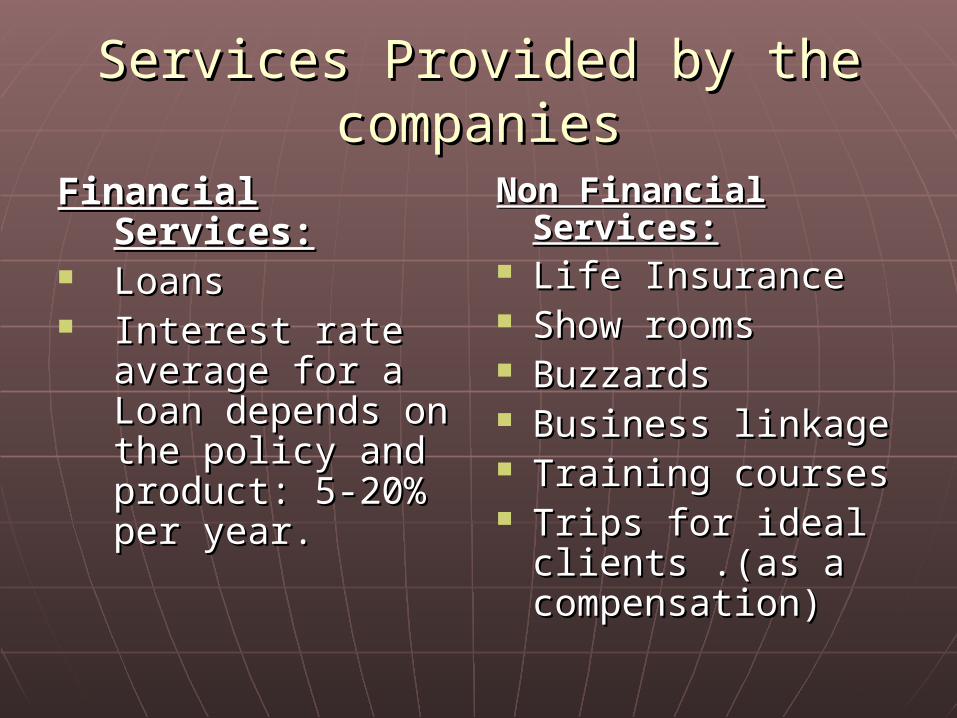

Services Provided by the Services Provided by the companiescompanies

Financial Services:Financial Services: LoansLoans Interest rate Interest rate

average for a average for a Loan depends on Loan depends on the policy and the policy and product: 5-20% product: 5-20% per year.per year.

Non Financial Non Financial Services:Services:

Life InsuranceLife Insurance Show roomsShow rooms BuzzardsBuzzards Business linkage Business linkage Training coursesTraining courses Trips for ideal Trips for ideal

clients .(as a clients .(as a compensation)compensation)

2 Types of Loans2 Types of Loans

Individual Loans:Individual Loans: Men & WomenMen & Women Business ownersBusiness owners House hold LoanHouse hold Loan Existing projectsExisting projects Start up projects (Grace Start up projects (Grace

period up to 6 months)period up to 6 months) Seasonal loan (Ramadan)Seasonal loan (Ramadan) Vehicles LoansVehicles Loans Agriculture Loans Agriculture Loans

Group Loans:Group Loans: For women onlyFor women only 2-5 persons 2-5 persons House hold loans: House hold loans:

knitting knitting Agriculture loans: Agriculture loans:

cows, sheep, cows, sheep, camels..camels..

The Islamic ProductThe Islamic Product

Only 2 companies in Jordan provide Only 2 companies in Jordan provide a loan as an Islamic Product.a loan as an Islamic Product.

1.1. DEFDEF2.2. NMBNMB3.3. FINCA (In the future)FINCA (In the future)

The Islamic Product is named The Islamic Product is named “Morabha”.“Morabha”.

Al MorabhaAl Morabha This product provides people who would prefer to This product provides people who would prefer to

apply the Islamic way since they do not agree to apply the Islamic way since they do not agree to take a loan with a certain percentage of interest. take a loan with a certain percentage of interest. They can choose the Morabha.They can choose the Morabha.

Morabha includes in it’s contract 3 subjects: the Morabha includes in it’s contract 3 subjects: the company, the trader and the client.company, the trader and the client.

The company buys the product from the trader The company buys the product from the trader and resale it to the client when the purchase and resale it to the client when the purchase price is known and must be agreed upon in price is known and must be agreed upon in advance. The profit is around( 6%-7%).advance. The profit is around( 6%-7%).

Vision & MissionVision & Mission

- The vision and the mission of the The vision and the mission of the microfinance companies in Jordan are quit microfinance companies in Jordan are quit similar in their targets.similar in their targets.

- The vision is to improve the low income The vision is to improve the low income and productive poor people’s social and and productive poor people’s social and living standards through micro and small living standards through micro and small sized enterprises. sized enterprises.

- The mission is to provide the financial and The mission is to provide the financial and non financial services to the Jordanian's non financial services to the Jordanian's lowest income so they can create jobs, lowest income so they can create jobs, build assets and increase their income.build assets and increase their income.

Difficulties of the companies:Difficulties of the companies:

1.1. CompetitionCompetition

2.2. Similarity in their productsSimilarity in their products

3.3. Division by areas. (North, Center Division by areas. (North, Center and South)and South)

4.4. Duality of a client.Duality of a client.

Duality of a clientDuality of a client

The client can be so “clever”: go to a The client can be so “clever”: go to a company to ask for a loan and right after company to ask for a loan and right after he signs the contract, he goes to another he signs the contract, he goes to another company and asks for another loan. This is company and asks for another loan. This is what we call Duality.what we call Duality.

In order to stop this duality, all companies In order to stop this duality, all companies had to sign an agreement at the Ministry had to sign an agreement at the Ministry of Planning in accordance with Delta’s of Planning in accordance with Delta’s company in 2007company in 2007

Delta InformaticsDelta Informatics Delta is an informatics company, that provides to Delta is an informatics company, that provides to

all companies an online contract of an active all companies an online contract of an active client: In a case a client has signed an agreement client: In a case a client has signed an agreement with one company, can’t go to another company with one company, can’t go to another company unless he has finished his active payments. unless he has finished his active payments.

Since it was established in Amman in 1993, Delta Since it was established in Amman in 1993, Delta Informatics has helped the firms achieve a Informatics has helped the firms achieve a competitive advantage through the following competitive advantage through the following issues:issues:

1. Reduced costs 1. Reduced costs 2. Increased productivity 2. Increased productivity 3. Higher revenues 3. Higher revenues

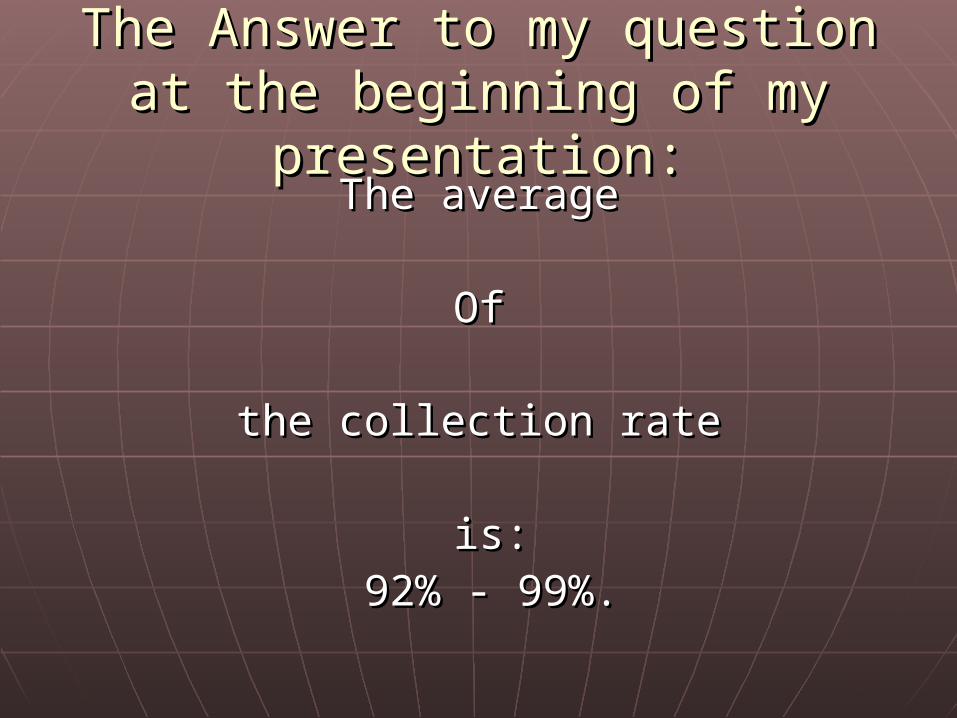

The Answer to my question at the The Answer to my question at the beginning of my presentation:beginning of my presentation:

The averageThe average

OfOf

the collection ratethe collection rate

is:is: 92% - 99%.92% - 99%.

How is it so high???How is it so high???

The Answer is:The Answer is:

The Organizational Structure in all The Organizational Structure in all firms.firms.

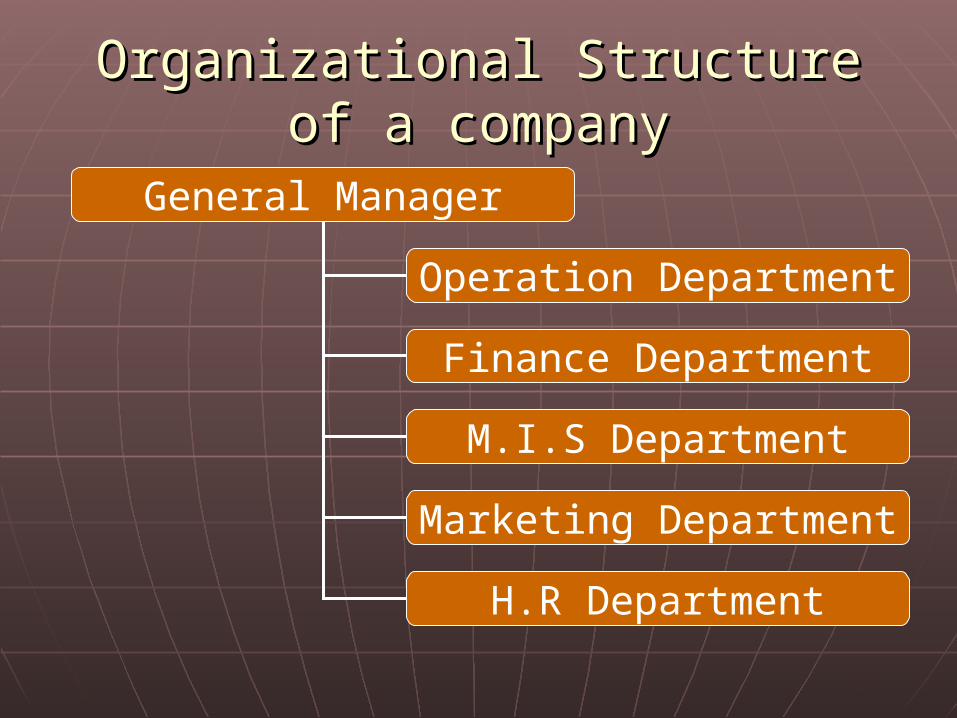

Organizational Structure of a Organizational Structure of a companycompany

Board of Directors

External Auditor General Manager Internal Auditor

Organizational Structure of a Organizational Structure of a companycompany

General Manager

Operation Department

Finance Department

M.I.S Department

Marketing Department

H.R Department

Organizational Structure of a Organizational Structure of a companycompany

Operation Department

Operation Manager

Credit Manager

Branches Managers

Supervisors

Loans Officers

ConclusionConclusion Jordan is well known as a supportive and Jordan is well known as a supportive and

active client of the world’s Microfinance.active client of the world’s Microfinance. Microfinance in Jordan is specialized with Microfinance in Jordan is specialized with

it’s organizational structure.it’s organizational structure. Their Vision and Mission are to create and Their Vision and Mission are to create and

build strong financial projects and build strong financial projects and products in Jordan.products in Jordan.

Companies know how to overcome their Companies know how to overcome their difficulties and they reduce poverty in difficulties and they reduce poverty in Jordan and that’s how they accomplish Jordan and that’s how they accomplish their goal.their goal.

Thank youThank youfor your presencefor your presence

Samer Abu DaloSamer Abu Dalo