the karnataka bank · pdf filethe karnataka bank limited ... allotment of rights equity...

TRANSCRIPT

Letter of Offer

October 28, 2016

For Eligible Shareholders only

The Karnataka Bank Limited

Our Bank was incorporated on February 18, 1924 as The Karnataka Bank Limited under the Indian Companies Act, 1913. The certificate of

commencement of business was obtained on May 23, 1924. Our Bank received a license to carry on the banking business in India under the

Banking Regulation Act, 1949, from the Reserve Bank of India on April 4, 1966.

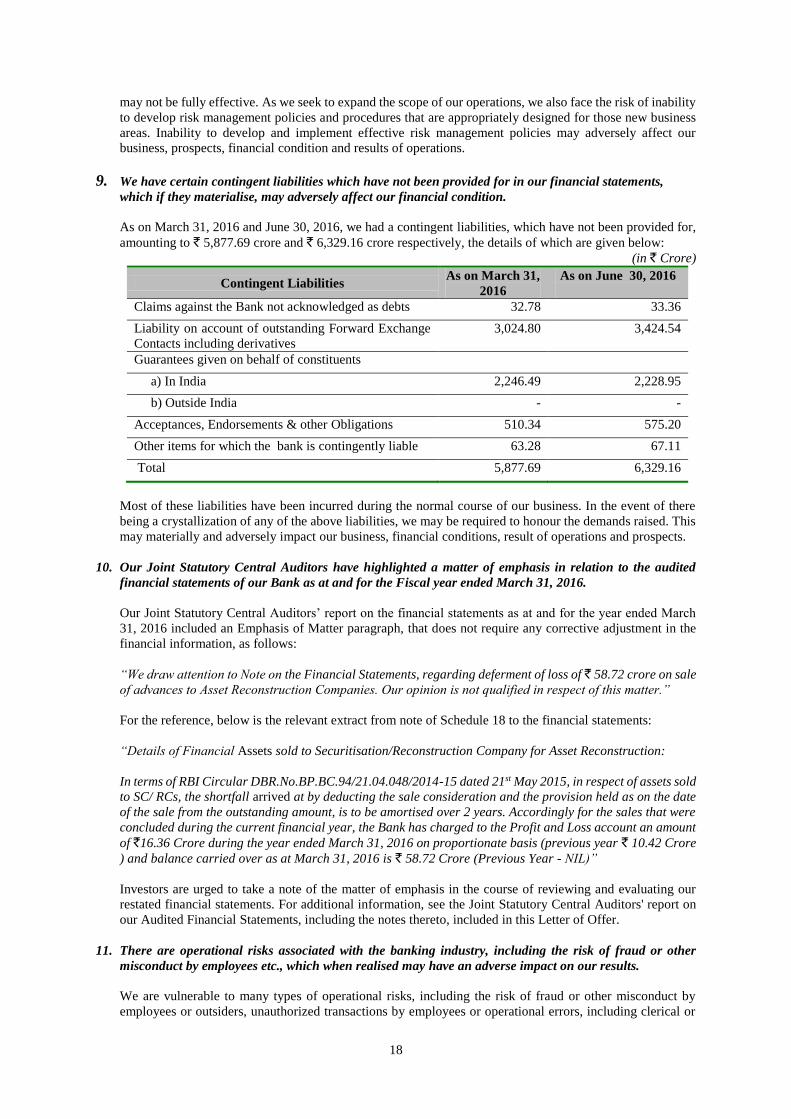

Registered Office: P.B. No. 599, Mahaveera Circle, Kankanady Mangaluru 575 002, Karnataka

Contact Person: Mr. Y.V. Balachandra, Company Secretary and Compliance Officer

Telephone: +91 (824) 2228182-4; Facsimile: +91 (824) 2225588; Email: [email protected]

Website: www.karnatakabank.com

Corporate Identity Number: L85110KA1924PLC001128

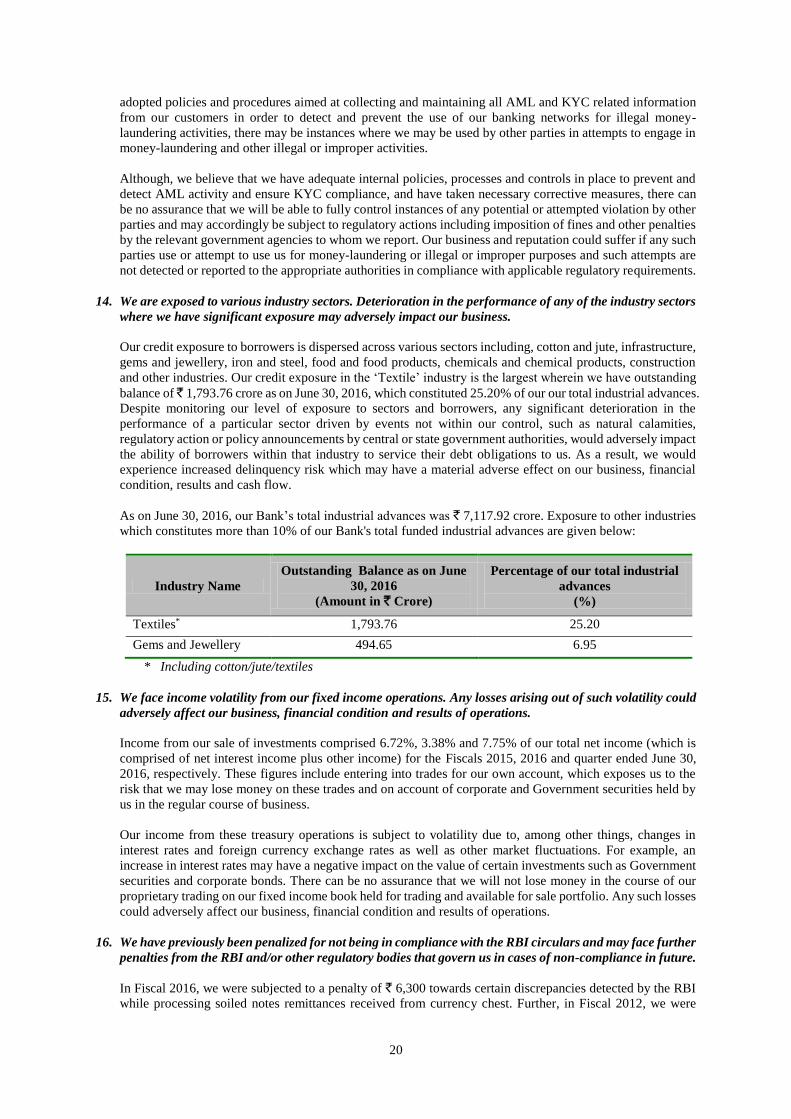

FOR PRIVATE CIRCULATION TO THE ELIGIBLE SHAREHOLDERS OF THE KARNATAKA BANK LIMITED (OUR

“BANK” OR THE “ISSUER”) ONLY

ISSUE OF UP TO 9,42,35,441 EQUITY SHARES OF FACE VALUE ` 10 EACH (“RIGHTS EQUITY SHARES”) OF OUR BANK FOR CASH

AT A PRICE OF ` 70 PER RIGHTS EQUITY SHARE (“ISSUE PRICE”) INCLUDING A PREMIUM OF ̀ 60 PER RIGHTS EQUITY SHARE

AGGREGATING UP TO ` 659.65 CRORE ON A RIGHTS BASIS TO THE ELIGIBLE SHAREHOLDERS OF OUR BANK IN THE RATIO

OF 1 (ONE) RIGHTS EQUITY SHARES FOR 2 (TWO) FULLY PAID-UP EQUITY SHARES HELD BY SUCH ELIGIBLE SHAREHOLDER

ON THE RECORD DATE, THAT IS, OCTOBER 25, 2016 (“ISSUE”). THE ISSUE PRICE OF THE RIGHTS EQUITY SHARES IS SEVEN

TIMES THE FACE VALUE OF THE EQUITY SHARES. FOR FURTHER DETAILS, PLEASE SEE “TERMS OF THE ISSUE” ON PAGE 92.

THE ENTIRE ISSUE PRICE FOR THE RIGHTS EQUITY SHARES IS PAYABLE ON APPLICATION.

GENERAL RISKS

Investment in equity and equity related securities involve a degree of risk and investors should not invest any funds in the Issue unless they can afford to

take the risk of losing their investment. Investors are advised to read the risk factors carefully before taking an investment decision in the Issue. For taking

an investment decision, investors must rely on their own examination of our Bank and the Issue including the risks involved. The Rights Equity Shares

have not been recommended or approved by the Securities and Exchange Board of India (“SEBI”) nor does SEBI guarantee the accuracy or adequacy of

this Letter of Offer. Investors are advised to refer to “Risk Factors” beginning on page 12 before making an investment in the Issue.

ISSUER’S ABSOLUTE RESPONSIBILITY

Our Bank, having made all reasonable inquiries, accepts responsibility for and confirms that this Letter of Offer contains all information with regard to

our Bank and the Issue, which is material in the context of the Issue, that the information contained in this Letter of Offer is true and correct in all material

aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts,

the omission of which makes this Letter of Offer as a whole or any such information or the expression of any such opinions or intentions misleading in

any material respect.

LISTING

The existing Equity Shares of our Bank are listed on the BSE Limited (“BSE”) and the National Stock Exchange of India Limited (“NSE”, and together

with BSE, the “Stock Exchanges”). Our Bank has received “in-principle” approvals from BSE and NSE for listing the Rights Equity Shares to be allotted

pursuant to the Issue through their respective letters, dated October 6, 2016 and October 10, 2016, respectively. For the purposes of the Issue, the Designated

Stock Exchange is the BSE.

LEAD MANAGER TO THE ISSUE REGISTRAR TO THE ISSUE

Edelweiss Financial Services Limited

14th Floor, Edelweiss House

Off C.S.T. Road, Kalina

Mumbai 400 098

Telephone: +91 (22) 4009 4400

Facsimile: +91 (22) 4086 3610

E-mail: [email protected]

Website: www.edelweissfin.com

Contact Person: Mr. Viral Shah / Mr. Vaibhav Shah

SEBI Registration No.: INM0000010650

Integrated Enterprises (India) Limited

No 30 Ramana Residency

4th Cross, Sampige Road, Malleswaram Bengaluru 560 003

Telephone: + 91 (80) 23460815-818

Facsimile: + 91 (80) 23460819

E-mail: [email protected]

Investor Grievance E-mail: [email protected]

Website: www.integratedindia.in

Contact Person: Mr. S. Vijayagopal/ Mr. E.T Balaji

SEBI Registration No: INR 000000544

ISSUE PROGRAMME

ISSUE OPENS ON

LAST DATE FOR

REQUEST FOR SPLIT

APPLICATION FORMS

ISSUE CLOSES ON

NOVEMBER 7, 2016 NOVEMBER 15, 2016 NOVEMBER 21, 2016

TABLE OF CONTENTS

SECTION I – GENERAL .................................................................................................................................... 2

DEFINITIONS AND ABBREVIATIONS .................................................................................................... 2

NOTICE TO OVERSEAS SHAREHOLDERS ............................................................................................. 8

PRESENTATION OF FINANCIAL INFORMATION ............................................................................... 10

FORWARD LOOKING STATEMENTS .................................................................................................... 11

SECTION II: RISK FACTORS ........................................................................................................................ 12

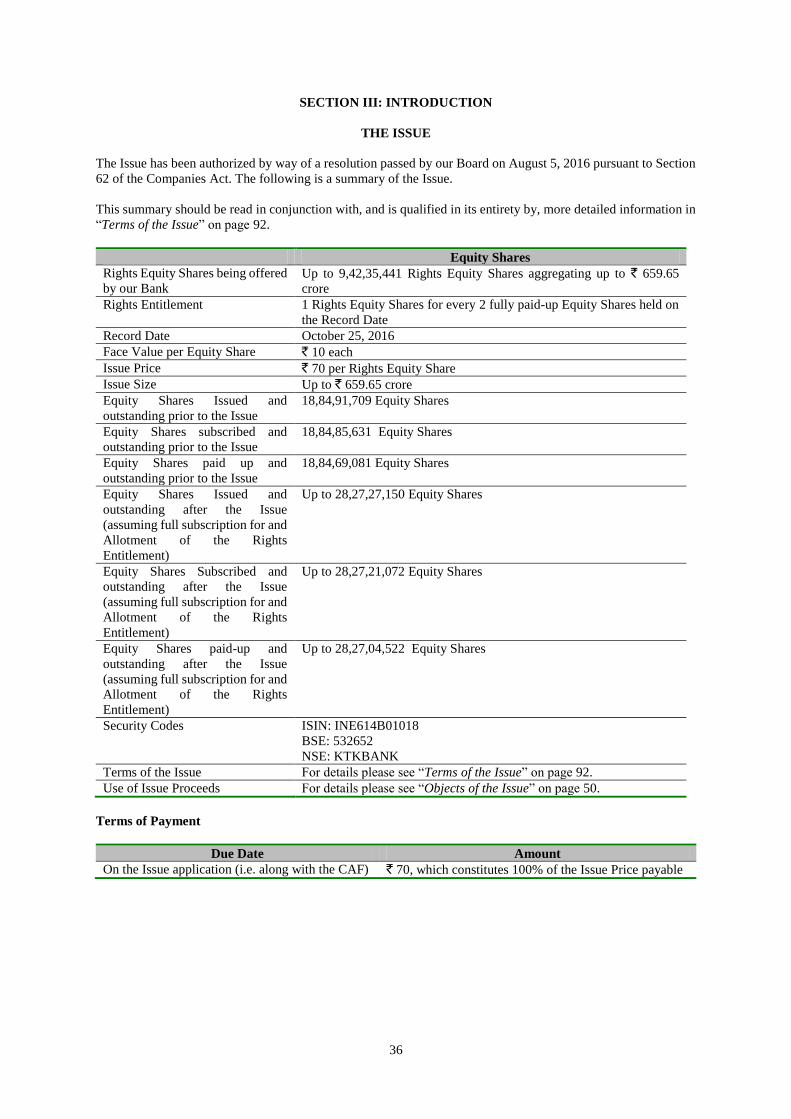

SECTION III: INTRODUCTION .................................................................................................................... 36

THE ISSUE .................................................................................................................................................. 36

SUMMARY FINANCIAL INFORMATION .............................................................................................. 37

GENERAL INFORMATION ...................................................................................................................... 42

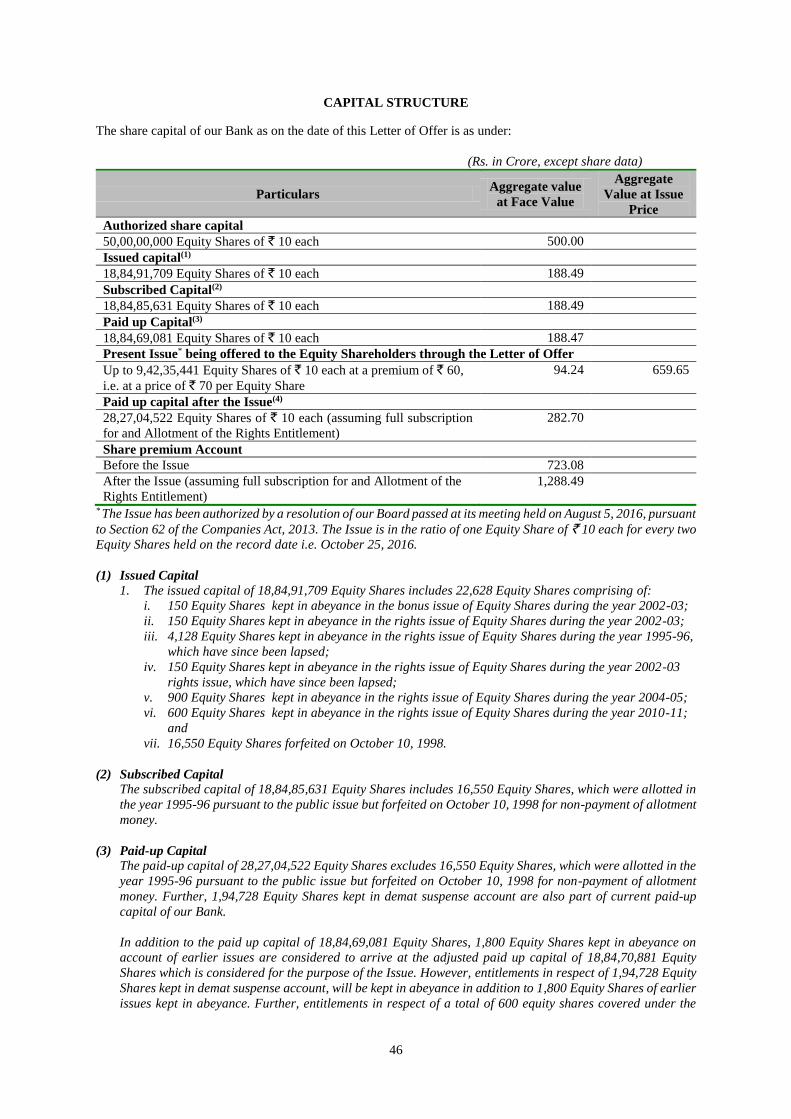

CAPITAL STRUCTURE ............................................................................................................................ 46

OBJECTS OF THE ISSUE .......................................................................................................................... 50

SECTION IV: STATEMENT OF SPECIAL TAX BENEFITS ..................................................................... 52

SECTION V: OUR MANAGEMENT .............................................................................................................. 55

SECTION VI: FINANCIAL INFORMATION ............................................................................................... 60

FINANCIAL STATEMENTS ..................................................................................................................... 60

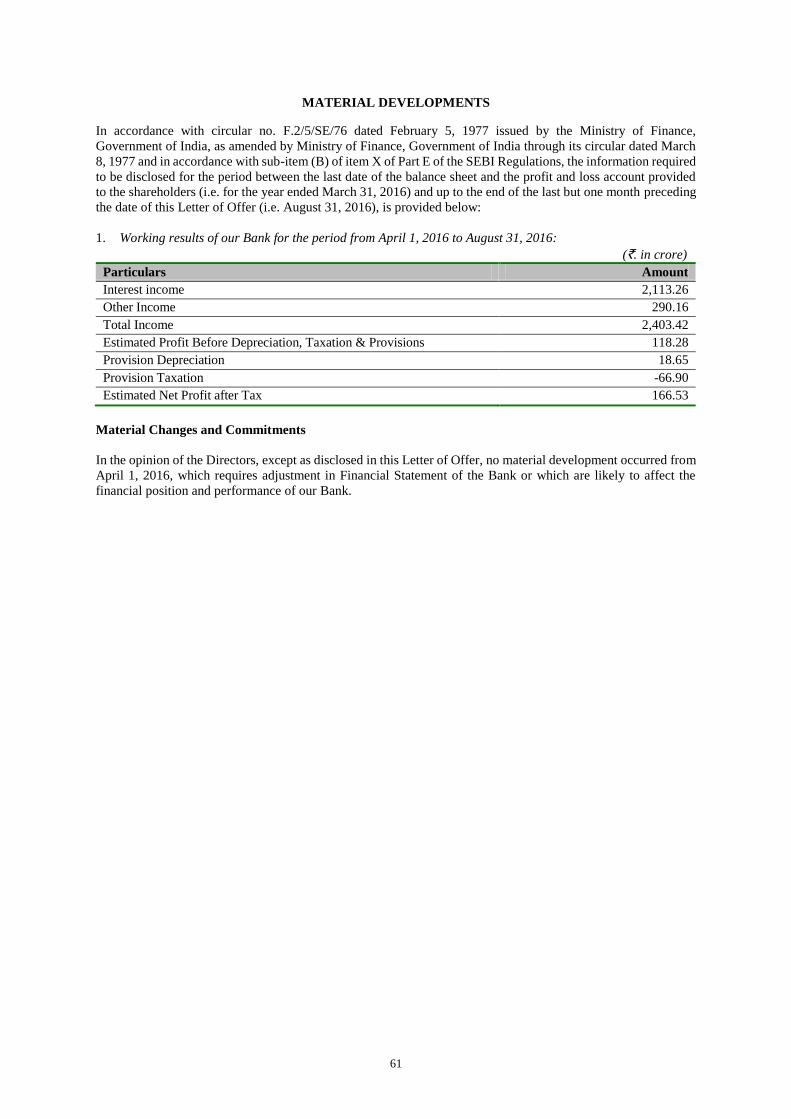

MATERIAL DEVELOPMENTS ................................................................................................................ 61

ACCOUNTING RATIOS AND CAPITALISATION STATEMENT ........................................................ 62

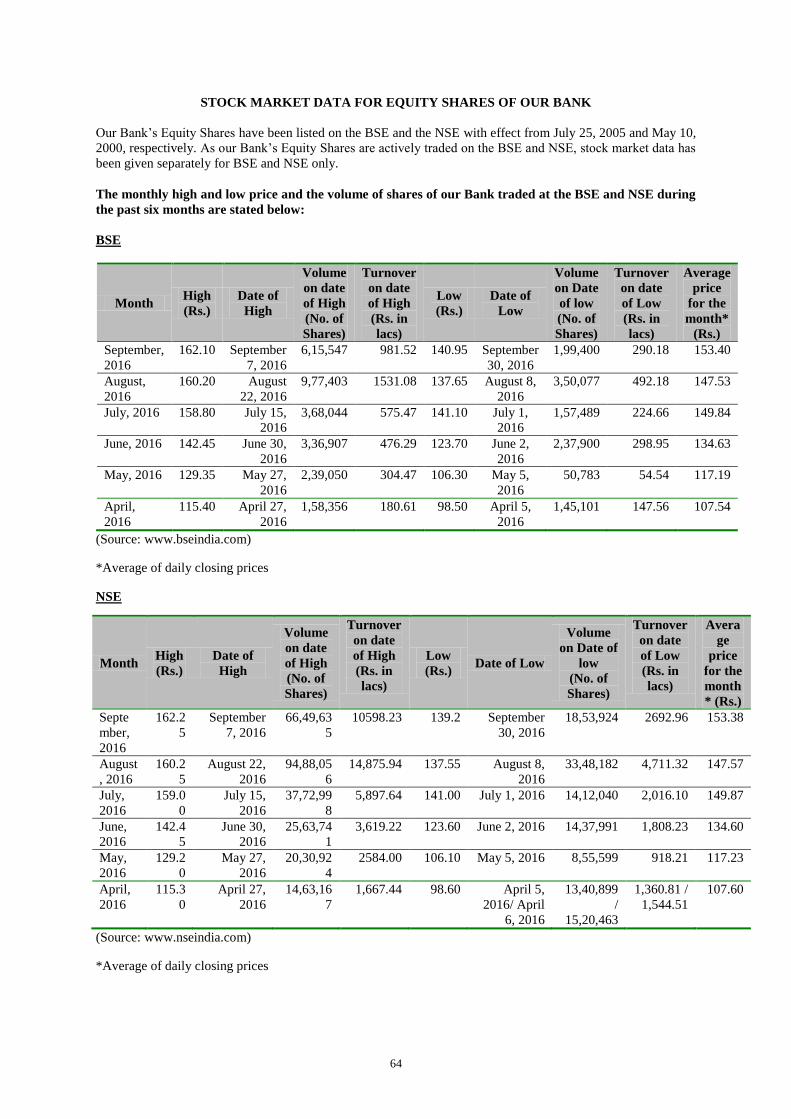

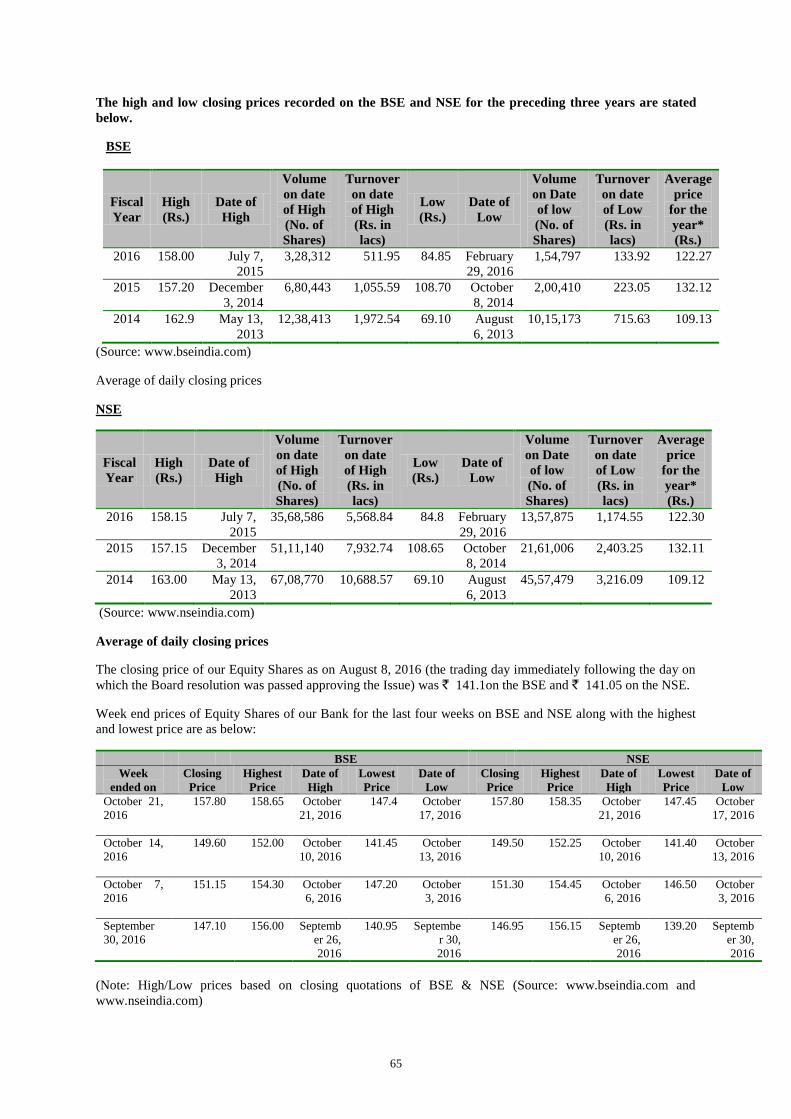

STOCK MARKET DATA FOR EQUITY SHARES OF OUR BANK ...................................................... 64

SECTION VII: LEGAL AND OTHER INFORMATION ............................................................................. 67

OUTSTANDING LITIGATION AND DEFAULTS .................................................................................. 67

GOVERNMENT AND OTHER APPROVALS .......................................................................................... 80

OTHER REGULATORY AND STATUTORY DISCLOSURES .............................................................. 81

SECTION VIII: ISSUE INFORMATION ....................................................................................................... 92

TERMS OF THE ISSUE ............................................................................................................................. 92

SECTION IX: OTHER INFORMATION ..................................................................................................... 126

MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION .................................................. 126

DECLARATION .............................................................................................................................................. 128

2

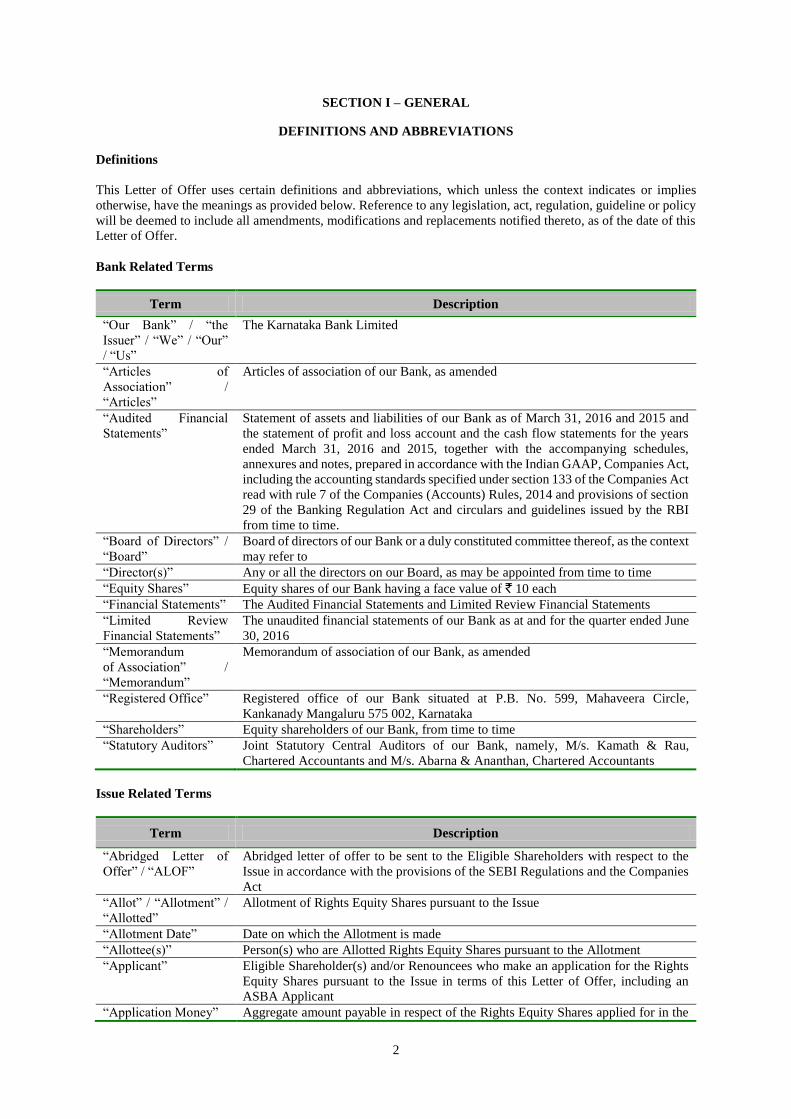

SECTION I – GENERAL

DEFINITIONS AND ABBREVIATIONS

Definitions

This Letter of Offer uses certain definitions and abbreviations, which unless the context indicates or implies

otherwise, have the meanings as provided below. Reference to any legislation, act, regulation, guideline or policy

will be deemed to include all amendments, modifications and replacements notified thereto, as of the date of this

Letter of Offer.

Bank Related Terms

Term Description

“Our Bank” / “the

Issuer” / “We” / “Our”

/ “Us”

The Karnataka Bank Limited

“Articles of

Association” /

“Articles”

Articles of association of our Bank, as amended

“Audited Financial

Statements”

Statement of assets and liabilities of our Bank as of March 31, 2016 and 2015 and

the statement of profit and loss account and the cash flow statements for the years

ended March 31, 2016 and 2015, together with the accompanying schedules,

annexures and notes, prepared in accordance with the Indian GAAP, Companies Act,

including the accounting standards specified under section 133 of the Companies Act

read with rule 7 of the Companies (Accounts) Rules, 2014 and provisions of section

29 of the Banking Regulation Act and circulars and guidelines issued by the RBI

from time to time.

“Board of Directors” /

“Board”

Board of directors of our Bank or a duly constituted committee thereof, as the context

may refer to

“Director(s)” Any or all the directors on our Board, as may be appointed from time to time

“Equity Shares” Equity shares of our Bank having a face value of ` 10 each

“Financial Statements” The Audited Financial Statements and Limited Review Financial Statements

“Limited Review

Financial Statements”

The unaudited financial statements of our Bank as at and for the quarter ended June

30, 2016

“Memorandum

of Association” /

“Memorandum”

Memorandum of association of our Bank, as amended

“Registered Office” Registered office of our Bank situated at P.B. No. 599, Mahaveera Circle,

Kankanady Mangaluru 575 002, Karnataka

“Shareholders” Equity shareholders of our Bank, from time to time

“Statutory Auditors” Joint Statutory Central Auditors of our Bank, namely, M/s. Kamath & Rau,

Chartered Accountants and M/s. Abarna & Ananthan, Chartered Accountants

Issue Related Terms

Term Description

“Abridged Letter of

Offer” / “ALOF”

Abridged letter of offer to be sent to the Eligible Shareholders with respect to the

Issue in accordance with the provisions of the SEBI Regulations and the Companies

Act

“Allot” / “Allotment” /

“Allotted”

Allotment of Rights Equity Shares pursuant to the Issue

“Allotment Date” Date on which the Allotment is made

“Allottee(s)” Person(s) who are Allotted Rights Equity Shares pursuant to the Allotment

“Applicant” Eligible Shareholder(s) and/or Renouncees who make an application for the Rights

Equity Shares pursuant to the Issue in terms of this Letter of Offer, including an

ASBA Applicant

“Application Money” Aggregate amount payable in respect of the Rights Equity Shares applied for in the

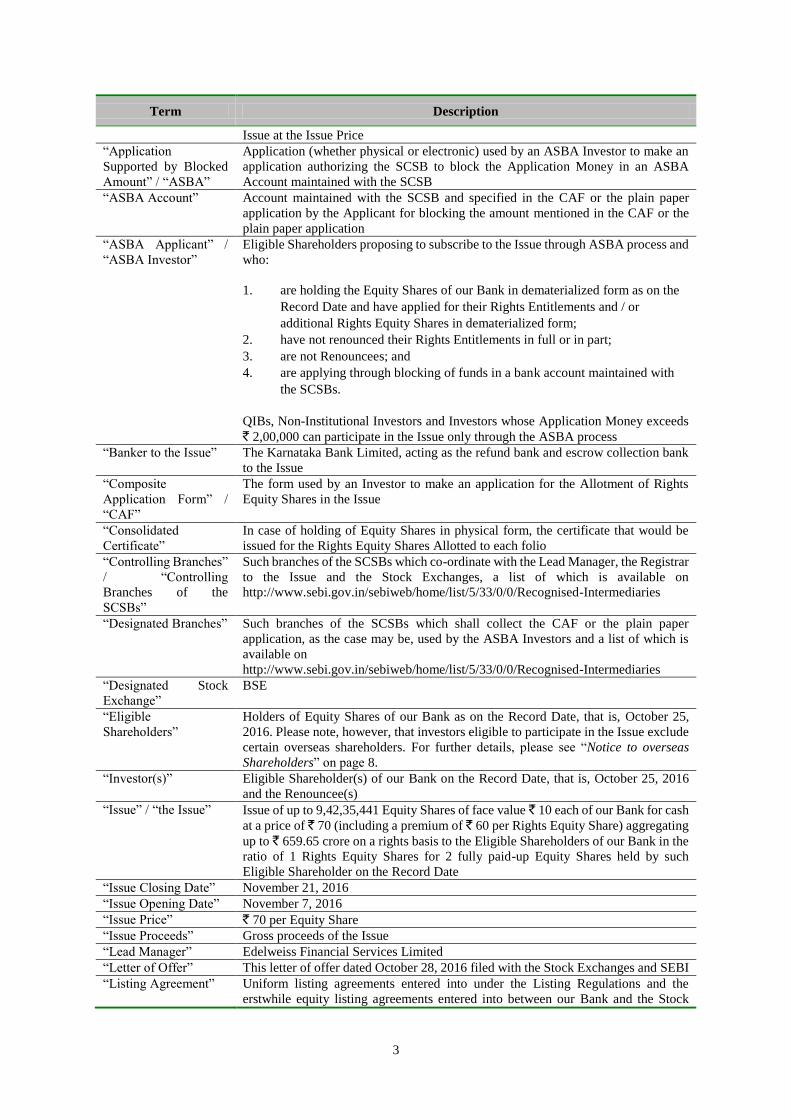

3

Term Description

Issue at the Issue Price

“Application

Supported by Blocked

Amount” / “ASBA”

Application (whether physical or electronic) used by an ASBA Investor to make an

application authorizing the SCSB to block the Application Money in an ASBA

Account maintained with the SCSB

“ASBA Account” Account maintained with the SCSB and specified in the CAF or the plain paper

application by the Applicant for blocking the amount mentioned in the CAF or the

plain paper application

“ASBA Applicant” /

“ASBA Investor”

Eligible Shareholders proposing to subscribe to the Issue through ASBA process and

who:

1. are holding the Equity Shares of our Bank in dematerialized form as on the

Record Date and have applied for their Rights Entitlements and / or

additional Rights Equity Shares in dematerialized form;

2. have not renounced their Rights Entitlements in full or in part;

3. are not Renouncees; and

4. are applying through blocking of funds in a bank account maintained with

the SCSBs.

QIBs, Non-Institutional Investors and Investors whose Application Money exceeds

` 2,00,000 can participate in the Issue only through the ASBA process

“Banker to the Issue” The Karnataka Bank Limited, acting as the refund bank and escrow collection bank

to the Issue

“Composite

Application Form” /

“CAF”

The form used by an Investor to make an application for the Allotment of Rights

Equity Shares in the Issue

“Consolidated

Certificate”

In case of holding of Equity Shares in physical form, the certificate that would be

issued for the Rights Equity Shares Allotted to each folio

“Controlling Branches”

/ “Controlling

Branches of the

SCSBs”

Such branches of the SCSBs which co-ordinate with the Lead Manager, the Registrar

to the Issue and the Stock Exchanges, a list of which is available on

http://www.sebi.gov.in/sebiweb/home/list/5/33/0/0/Recognised-Intermediaries

“Designated Branches” Such branches of the SCSBs which shall collect the CAF or the plain paper

application, as the case may be, used by the ASBA Investors and a list of which is

available on

http://www.sebi.gov.in/sebiweb/home/list/5/33/0/0/Recognised-Intermediaries

“Designated Stock

Exchange”

BSE

“Eligible

Shareholders”

Holders of Equity Shares of our Bank as on the Record Date, that is, October 25,

2016. Please note, however, that investors eligible to participate in the Issue exclude

certain overseas shareholders. For further details, please see “Notice to overseas

Shareholders” on page 8.

“Investor(s)” Eligible Shareholder(s) of our Bank on the Record Date, that is, October 25, 2016

and the Renouncee(s)

“Issue” / “the Issue” Issue of up to 9,42,35,441 Equity Shares of face value ` 10 each of our Bank for cash

at a price of ` 70 (including a premium of ` 60 per Rights Equity Share) aggregating

up to ` 659.65 crore on a rights basis to the Eligible Shareholders of our Bank in the

ratio of 1 Rights Equity Shares for 2 fully paid-up Equity Shares held by such

Eligible Shareholder on the Record Date

“Issue Closing Date” November 21, 2016

“Issue Opening Date” November 7, 2016

“Issue Price” ` 70 per Equity Share

“Issue Proceeds” Gross proceeds of the Issue

“Lead Manager” Edelweiss Financial Services Limited

“Letter of Offer” This letter of offer dated October 28, 2016 filed with the Stock Exchanges and SEBI

“Listing Agreement” Uniform listing agreements entered into under the Listing Regulations and the

erstwhile equity listing agreements entered into between our Bank and the Stock

4

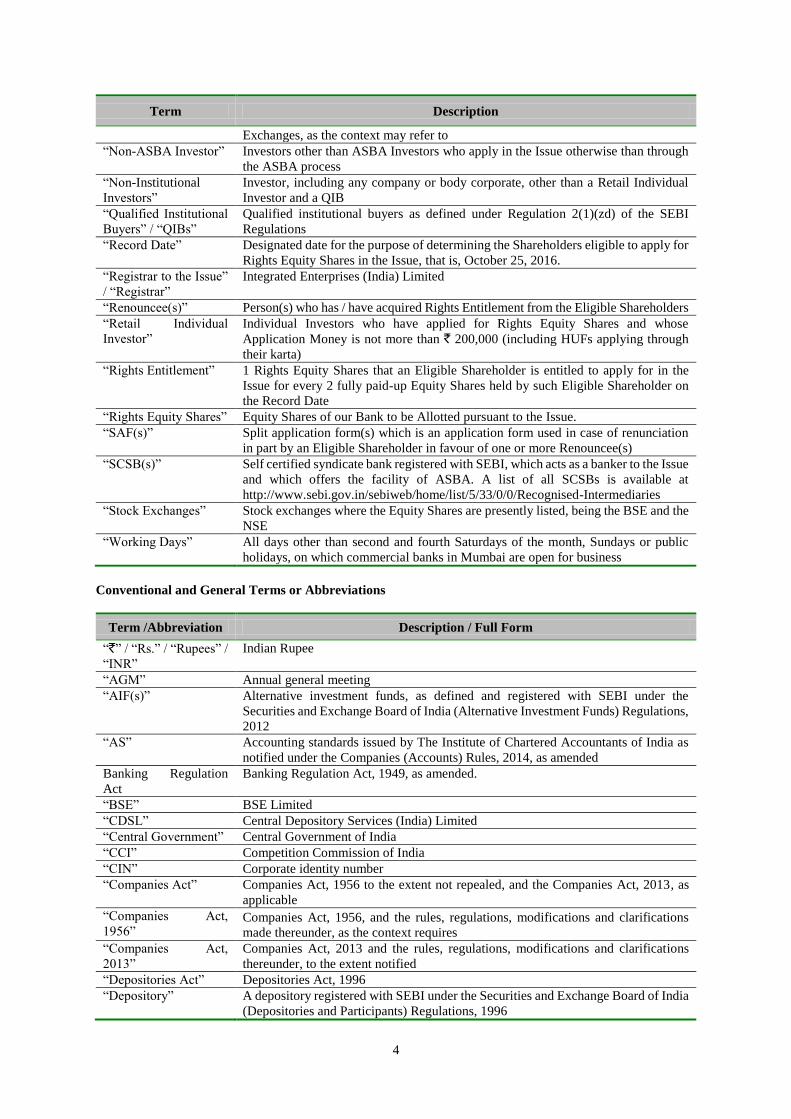

Term Description

Exchanges, as the context may refer to

“Non-ASBA Investor” Investors other than ASBA Investors who apply in the Issue otherwise than through

the ASBA process

“Non-Institutional

Investors”

Investor, including any company or body corporate, other than a Retail Individual

Investor and a QIB

“Qualified Institutional

Buyers” / “QIBs”

Qualified institutional buyers as defined under Regulation 2(1)(zd) of the SEBI

Regulations

“Record Date” Designated date for the purpose of determining the Shareholders eligible to apply for

Rights Equity Shares in the Issue, that is, October 25, 2016.

“Registrar to the Issue”

/ “Registrar”

Integrated Enterprises (India) Limited

“Renouncee(s)” Person(s) who has / have acquired Rights Entitlement from the Eligible Shareholders

“Retail Individual

Investor”

Individual Investors who have applied for Rights Equity Shares and whose

Application Money is not more than ` 200,000 (including HUFs applying through

their karta)

“Rights Entitlement” 1 Rights Equity Shares that an Eligible Shareholder is entitled to apply for in the

Issue for every 2 fully paid-up Equity Shares held by such Eligible Shareholder on

the Record Date

“Rights Equity Shares” Equity Shares of our Bank to be Allotted pursuant to the Issue.

“SAF(s)” Split application form(s) which is an application form used in case of renunciation

in part by an Eligible Shareholder in favour of one or more Renouncee(s)

“SCSB(s)” Self certified syndicate bank registered with SEBI, which acts as a banker to the Issue

and which offers the facility of ASBA. A list of all SCSBs is available at

http://www.sebi.gov.in/sebiweb/home/list/5/33/0/0/Recognised-Intermediaries

“Stock Exchanges” Stock exchanges where the Equity Shares are presently listed, being the BSE and the

NSE

“Working Days” All days other than second and fourth Saturdays of the month, Sundays or public

holidays, on which commercial banks in Mumbai are open for business

Conventional and General Terms or Abbreviations

Term /Abbreviation Description / Full Form

“`” / “Rs.” / “Rupees” /

“INR”

Indian Rupee

“AGM” Annual general meeting

“AIF(s)” Alternative investment funds, as defined and registered with SEBI under the

Securities and Exchange Board of India (Alternative Investment Funds) Regulations,

2012

“AS” Accounting standards issued by The Institute of Chartered Accountants of India as

notified under the Companies (Accounts) Rules, 2014, as amended

Banking Regulation

Act

Banking Regulation Act, 1949, as amended.

“BSE” BSE Limited

“CDSL” Central Depository Services (India) Limited

“Central Government” Central Government of India

“CCI” Competition Commission of India

“CIN” Corporate identity number

“Companies Act” Companies Act, 1956 to the extent not repealed, and the Companies Act, 2013, as

applicable

“Companies Act,

1956” Companies Act, 1956, and the rules, regulations, modifications and clarifications

made thereunder, as the context requires

“Companies Act,

2013”

Companies Act, 2013 and the rules, regulations, modifications and clarifications

thereunder, to the extent notified

“Depositories Act” Depositories Act, 1996

“Depository” A depository registered with SEBI under the Securities and Exchange Board of India

(Depositories and Participants) Regulations, 1996

5

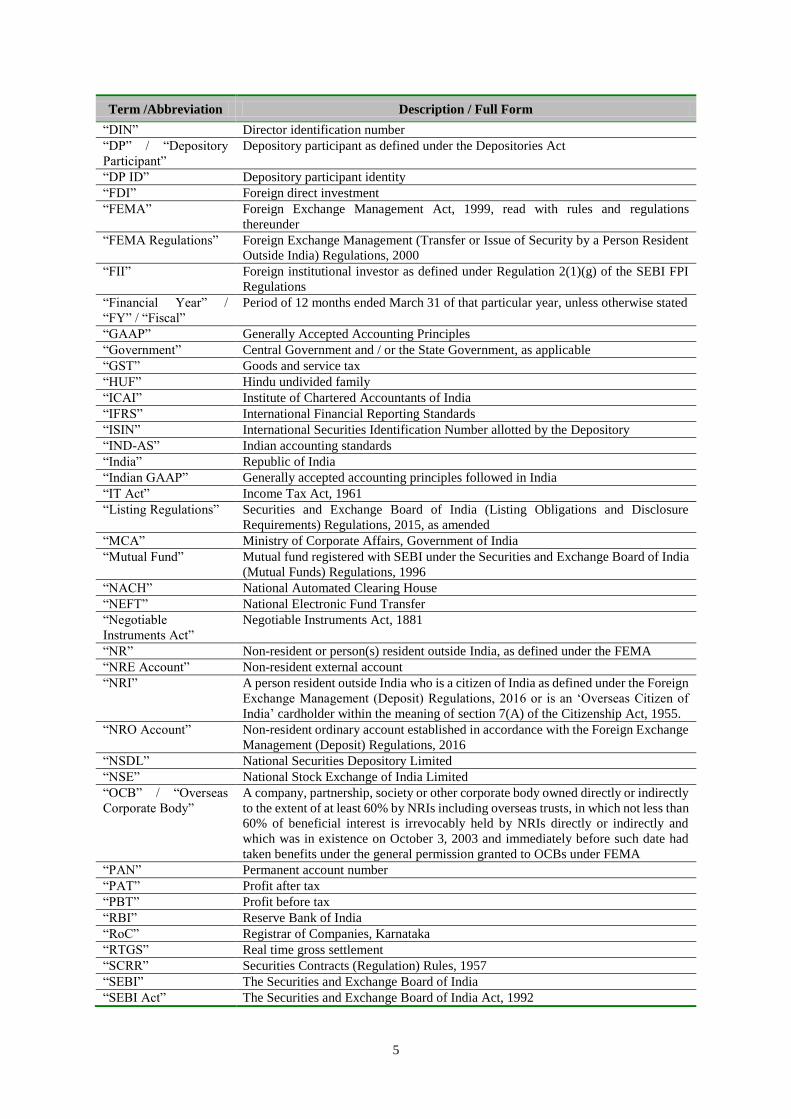

Term /Abbreviation Description / Full Form

“DIN” Director identification number

“DP” / “Depository

Participant”

Depository participant as defined under the Depositories Act

“DP ID” Depository participant identity

“FDI” Foreign direct investment

“FEMA” Foreign Exchange Management Act, 1999, read with rules and regulations

thereunder

“FEMA Regulations” Foreign Exchange Management (Transfer or Issue of Security by a Person Resident

Outside India) Regulations, 2000

“FII” Foreign institutional investor as defined under Regulation 2(1)(g) of the SEBI FPI

Regulations

“Financial Year” /

“FY” / “Fiscal”

Period of 12 months ended March 31 of that particular year, unless otherwise stated

“GAAP” Generally Accepted Accounting Principles

“Government” Central Government and / or the State Government, as applicable

“GST” Goods and service tax

“HUF” Hindu undivided family

“ICAI” Institute of Chartered Accountants of India

“IFRS” International Financial Reporting Standards

“ISIN” International Securities Identification Number allotted by the Depository

“IND-AS” Indian accounting standards

“India” Republic of India

“Indian GAAP” Generally accepted accounting principles followed in India

“IT Act” Income Tax Act, 1961

“Listing Regulations” Securities and Exchange Board of India (Listing Obligations and Disclosure

Requirements) Regulations, 2015, as amended

“MCA” Ministry of Corporate Affairs, Government of India

“Mutual Fund” Mutual fund registered with SEBI under the Securities and Exchange Board of India

(Mutual Funds) Regulations, 1996

“NACH” National Automated Clearing House

“NEFT” National Electronic Fund Transfer

“Negotiable

Instruments Act”

Negotiable Instruments Act, 1881

“NR” Non-resident or person(s) resident outside India, as defined under the FEMA

“NRE Account” Non-resident external account

“NRI” A person resident outside India who is a citizen of India as defined under the Foreign

Exchange Management (Deposit) Regulations, 2016 or is an ‘Overseas Citizen of

India’ cardholder within the meaning of section 7(A) of the Citizenship Act, 1955.

“NRO Account” Non-resident ordinary account established in accordance with the Foreign Exchange

Management (Deposit) Regulations, 2016

“NSDL” National Securities Depository Limited

“NSE” National Stock Exchange of India Limited

“OCB” / “Overseas

Corporate Body”

A company, partnership, society or other corporate body owned directly or indirectly

to the extent of at least 60% by NRIs including overseas trusts, in which not less than

60% of beneficial interest is irrevocably held by NRIs directly or indirectly and

which was in existence on October 3, 2003 and immediately before such date had

taken benefits under the general permission granted to OCBs under FEMA

“PAN” Permanent account number

“PAT” Profit after tax

“PBT” Profit before tax

“RBI” Reserve Bank of India

“RoC” Registrar of Companies, Karnataka

“RTGS” Real time gross settlement

“SCRR” Securities Contracts (Regulation) Rules, 1957

“SEBI” The Securities and Exchange Board of India

“SEBI Act” The Securities and Exchange Board of India Act, 1992

6

Term /Abbreviation Description / Full Form

“SEBI FPI

Regulations”

The Securities and Exchange Board of India (Foreign Portfolio Investors)

Regulations, 2014

“SEBI Regulations” The Securities and Exchange Board of India (Issue of Capital and Disclosure

Requirements) Regulations, 2009

“Securities Act” United States Securities Act of 1933

“State Government” Government of a State of India

“Takeover

Regulations”

The Securities and Exchange Board of India (Substantial Acquisition of Shares and

Takeovers) Regulations, 2011

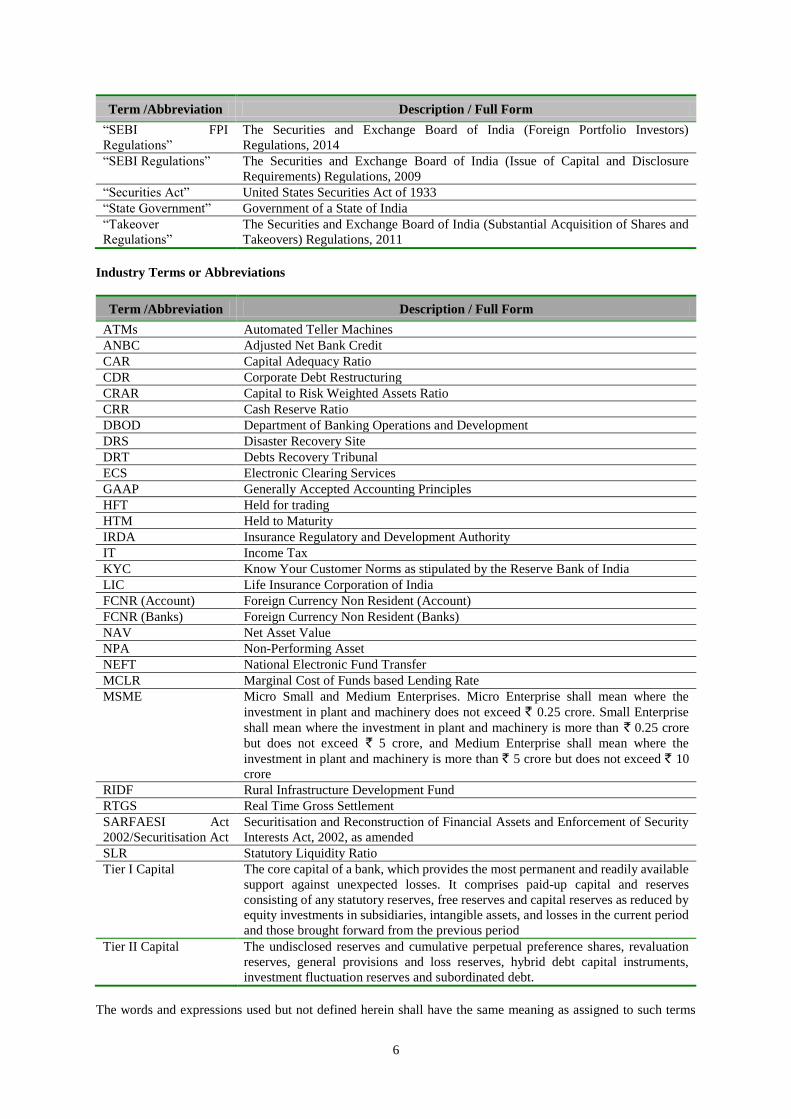

Industry Terms or Abbreviations

Term /Abbreviation Description / Full Form

ATMs Automated Teller Machines

ANBC Adjusted Net Bank Credit

CAR Capital Adequacy Ratio

CDR Corporate Debt Restructuring

CRAR Capital to Risk Weighted Assets Ratio

CRR Cash Reserve Ratio

DBOD Department of Banking Operations and Development

DRS Disaster Recovery Site

DRT Debts Recovery Tribunal

ECS Electronic Clearing Services

GAAP Generally Accepted Accounting Principles

HFT Held for trading

HTM Held to Maturity

IRDA Insurance Regulatory and Development Authority

IT Income Tax

KYC Know Your Customer Norms as stipulated by the Reserve Bank of India

LIC Life Insurance Corporation of India

FCNR (Account) Foreign Currency Non Resident (Account)

FCNR (Banks) Foreign Currency Non Resident (Banks)

NAV Net Asset Value

NPA Non-Performing Asset

NEFT National Electronic Fund Transfer

MCLR Marginal Cost of Funds based Lending Rate

MSME Micro Small and Medium Enterprises. Micro Enterprise shall mean where the

investment in plant and machinery does not exceed ` 0.25 crore. Small Enterprise

shall mean where the investment in plant and machinery is more than ` 0.25 crore

but does not exceed ` 5 crore, and Medium Enterprise shall mean where the

investment in plant and machinery is more than ` 5 crore but does not exceed ` 10

crore

RIDF Rural Infrastructure Development Fund

RTGS Real Time Gross Settlement

SARFAESI Act

2002/Securitisation Act

Securitisation and Reconstruction of Financial Assets and Enforcement of Security

Interests Act, 2002, as amended

SLR Statutory Liquidity Ratio

Tier I Capital The core capital of a bank, which provides the most permanent and readily available

support against unexpected losses. It comprises paid-up capital and reserves

consisting of any statutory reserves, free reserves and capital reserves as reduced by

equity investments in subsidiaries, intangible assets, and losses in the current period

and those brought forward from the previous period

Tier II Capital The undisclosed reserves and cumulative perpetual preference shares, revaluation

reserves, general provisions and loss reserves, hybrid debt capital instruments,

investment fluctuation reserves and subordinated debt.

The words and expressions used but not defined herein shall have the same meaning as assigned to such terms

7

under the SEBI Regulations, the Companies Act, the SEBI Act, Securities Contract (Regulation) Act, 1956 and

the Depositories Act and the rules and regulations made thereunder.

Notwithstanding the foregoing, terms specifically defined in this Letter of Offer, shall have the meanings given

to such terms in the sections where specifically defined.

8

NOTICE TO OVERSEAS SHAREHOLDERS

The distribution of this Letter of Offer, the Abridged Letter of Offer or CAF and Issue to persons in certain

jurisdictions outside India may be restricted by legal requirements prevailing in those jurisdictions. Persons into

whose possession this Letter of Offer, the Abridged Letter of Offer or CAF may come are required to inform

themselves about and observe such restrictions. Our Bank is making the Issue on a rights basis to the Eligible

Shareholders and will dispatch this Letter of Offer / Abridged Letter of Offer and CAF only to Eligible

Shareholders who have a registered address in India or who have provided an Indian address to our Bank.

No action has been or will be taken to permit the Issue in any jurisdiction where action would be required for that

purpose. Accordingly, the Rights Entitlements or Rights Equity Shares may not be offered or sold, directly or

indirectly, and this Letter of Offer, the Abridged Letter of Offer or any offering materials or advertisements in

connection with the Issue may not be distributed, in whole or in part, in any jurisdiction, except in accordance

with legal requirements applicable in such jurisdiction. Receipt of this Letter of Offer or the Abridged Letter of

Offer will not constitute an offer in those jurisdictions in which it would be illegal to make such an offer and, in

those circumstances, this Letter of Offer and the Abridged Letter of Offer must be treated as sent for information

only and should not be acted upon for subscription to the Rights Equity Shares and should not be copied or

redistributed. Accordingly, persons receiving a copy of this Letter of Offer or the Abridged Letter of Offer should

not, in connection with the issue of the Rights Equity Shares or the Rights Entitlements, distribute or send this

Letter of Offer or the Abridged Letter of Offer in or into any jurisdiction where to do so, would or might

contravene local securities laws or regulations. If this Letter of Offer or the Abridged Letter of Offer is received

by any person in any such jurisdiction, or by their agent or nominee, they must not seek to subscribe to the Rights

Equity Shares or the Rights Entitlements referred to in this Letter of Offer and the Abridged Letter of Offer.

Envelopes containing a CAF should not be dispatched from the jurisdiction where it would be illegal to make an

offer and all the person subscribing for the Equity shares in the Issue must provide an Indian address

Any person who makes an application to acquire rights and the Equity shares offered in the Issue will be deemed

to have declared, represented, warranted and agreed that he is authorized to acquire the rights and the Equity

shares in compliance with all applicable laws and regulations prevailing in his jurisdiction.

Neither the delivery of the Letter of Offer nor any sale hereunder, shall under any circumstances create any

implication that there has been no change in the Bank’s affairs from the date hereof or that the information

contained herein is correct as at any time subsequent to the date of the Letter of Offer. The contents of the Letter

of Offer should not be construed as legal, tax or investment advice. Prospective investors may be subject to

adverse foreign, state or local tax or legal consequences as a result of the offer of Equity Shares. As a result, each

investor should consult its own counsel, business advisor and tax advisor as to the legal, business, tax and related

matters concerning the offer of Equity Shares. In addition, neither our Bank nor the Lead Manager is making any

representation to any offeree or purchaser of the Equity Shares regarding the legality of an investment in the

Equity Shares by such offeree or purchaser under any applicable laws or regulations.

NO OFFER IN THE UNITED STATES

The Rights Entitlements and the Rights Equity Shares have not been and will not be registered under the Securities

Act, or any U.S. state securities laws and may not be offered, sold, resold or otherwise transferred within the

United States of America or the territories or possessions thereof (“United States” or “U.S.”), or to, or for the

account or benefit of “U.S. persons” (as defined in Regulation S of the Securities Act), except in a transaction not

subject to, or exempt from the registration requirements of the Securities Act. The offering to which this Letter of

Offer relates is not, and under no circumstances is to be construed as, an offering of any Rights Equity Shares or

Rights Entitlement for sale in the United States or as a solicitation therein of an offer to buy any of the Rights

Equity Shares or Rights Entitlement. There is no intention to register any portion of the Issue or any of the

securities described herein in the United States or to conduct a public offering of securities in the United States.

Accordingly, this Letter of Offer / Abridged Letter of Offer and the enclosed CAF should not be forwarded to or

transmitted in or into the United States at any time. In addition, until the expiry of 40 days after the commencement

of the Issue, an offer or sale of Rights Entitlements or Rights Equity Shares within the United States by a dealer

(whether or not it is participating in the Issue) may violate the registration requirement of the Securities Act.

Neither we nor any person acting on our behalf will accept a subscription or renunciation from any person, or the agent of any person, who appears to be, or who we or any person acting on our behalf has reason to believe is, either a U.S. Person or otherwise in the United States when the buy order is made. Envelopes containing a CAF should not be postmarked in the United States or otherwise dispatched from the United States or any other

9

jurisdiction where it would be illegal to make an offer, and all persons subscribing for the Rights Equity Shares Issue and wishing to hold such Equity Shares in registered form must provide an address for registration of these Equity Shares in India. We are making the Issue on a rights basis to Eligible Shareholders and the Letter of Offer

/ Abridged Letter of Offer and CAF will be dispatched only to Eligible Shareholders who have an Indian address. Any person who acquires Rights Entitlements and the Rights Equity Shares will be deemed to have declared, represented, warranted and agreed that, (i) it is not and that at the time of subscribing for such Rights Equity Shares or the Rights Entitlements, it will not be, in the United States, (ii) it is not a U.S. Person and does not have a registered address (and is not otherwise located) in the United States when the buy order is made, and (iii) it is authorised to acquire the Rights Entitlements and the Rights Equity Shares in compliance with all applicable laws

and regulations. We reserve the right to treat any CAF as invalid which: (i) does not include the certification set out in the CAF to

the effect that the subscriber is not a U.S. Person and does not have a registered address (and is not otherwise

located) in the United States and is authorized to acquire the Rights Equity Shares or Rights Entitlement in

compliance with all applicable laws and regulations; (ii) appears to us or our agents to have been executed in or

dispatched from the United States; (iii) appears to us or our agents to have been executed by a U.S. Person; (iv)

where a registered Indian address is not provided; or (v) where we believe that CAF is incomplete or acceptance

of such CAF may infringe applicable legal or regulatory requirements; and we shall not be bound to allot or issue

any Rights Equity Shares or Rights Entitlement in respect of any such CAF.

Rights Entitlements may not be transferred or sold to any person in the United States.

10

PRESENTATION OF FINANCIAL INFORMATION

Certain Conventions

All references herein to ‘India’ are to the Republic of India and its territories and possessions and the

‘Government’ or ‘GoI’ or the ‘Central Government’ or the ‘State Government’ are to the Government of India,

Central or State, as applicable. Unless otherwise specified or the context otherwise requires, all references in this

Letter of Offer to the ‘US’ or ‘U.S.’ or the ‘United States’ are to the United States of America and its territories

and possessions.

Unless the context otherwise requires, a reference to “Bank”/ “we” / “us” / “our” is a reference to The Karnataka

Bank Limited.

In this Letter of Offer, references to the singular also refer to the plural and one gender also refers to any other

gender, wherever applicable.

Financial Data

Unless stated otherwise, financial data in this Letter of Offer, with respect to our Bank, is derived from our Audited

Financial Statements and our Limited Review Finacial Statements.

Our Fiscal year commences on April 1 of each calendar year and ends on March 31 of the following calendar

year, so all references to a particular “Fiscal year” or “Fiscal” are to the 12 month period ended on March 31 of

that year.

Our Audited Financial Statements, prepared in accordance with Indian GAAP, Companies Act, including the

accounting standards specified under section 133 of the Companies Act read with rule 7 of the Companies

(Accounts) Rules, 2014 and provisions of section 29 of the Banking Regulation Act and circulars and guidelines

issued by the RBI from time to time. Further, our unaudited limited reviewed financial results for the quarter

ended June 30, 2016 (“Limited Review Financial Statements”) that appear in this Letter of Offer have been

prepared by our Bank in accordance with Indian GAAP and other applicable statutory and / or regulatory

requirements, including the requirements of the Listing Regulations. For further details of such financial

statements, please see “Financial Statements” on page 60.

Indian GAAP differs in certain significant respects from IFRS. Any reliance by persons not familiar with Indian

accounting practices on the financial disclosures based on the Indian GAAP financials presented in this Letter of

Offer should accordingly be limited. We have not attempted to explain those differences or quantify their impact

on the financial data included herein, and we urge you to consult your own advisors regarding such differences

and their impact on our financial data. For details in connection with risks involving differences between Indian

GAAP and other accounting principles and risks in relation to IFRS, please see “Risk Factors – Significant

differences exist between GAAP as applied in India and other accounting principles with which investors may be

more familiar.”, on page 35.

Certain figures contained in this Letter of Offer, including financial information, have been subject to rounding

adjustments. All decimals have been rounded off to two decimal places. In certain instances, (i) the sum or percentage change of such numbers may not conform exactly to the total figure given; and (ii) the sum of the numbers in a column or row in certain tables may not conform exactly to the total figure given for that column or row. Unless otherwise specified, all financial numbers in parenthesis represent negative figures.

Currency of Presentation

All references to ‘INR’, ‘`’, ‘Indian Rupees’, ‘Rs.’ and ‘Rupees’ are to the legal currency of India.

In this Letter of Offer, our Bank has presented certain numerical information in “crore” unit. One crore represents

1,00,00,000.

11

FORWARD LOOKING STATEMENTS

Certain statements contained in this Letter of Offer that are not statements of historical fact constitute ‘forward-

looking statements’. Investors can generally identify forward-looking statements by terminology such as

‘anticipate’, ‘believe’, ‘continue’, ‘can’, ‘could’, ‘intend’, ‘may’, ‘shall’ ‘should’, ‘will’, ‘would’, ‘future’,

‘forecast’, ‘guideline’ or other words or phrases of similar import. Similarly, statements that describe the

strategies, objectives, plans or goals of our Bank are also forward-looking statements. However, these are not the

exclusive means of identifying forward-looking statements. Forward-looking statements are not guarantees of

performance and are based on certain assumptions, discuss future expectations, describe plans and strategies

contain projections of results of operations or of financial condition or state other forward-looking information.

Forward-looking statements contained in this Letter of Offer (whether made by our Bank or any third party), are

predictions and involve known and unknown risks, uncertainties, assumptions and other factors that may cause

the actual results, performance or achievements of our Bank to be materially different from any future results,

performance or achievements expressed or implied by such forward-looking statements or other projections. All

forward-looking statements are subject to risks, uncertainties and assumptions about our Bank that could cause

actual results to differ materially from those contemplated by the relevant forward-looking statement. Important

factors that could cause actual results to differ materially from our Bank’s expectations include, among others:

volatility in interest rates and other market conditions;

our inability to manage non-performing assets

our inability to compete effectively;

ability to manage credit, market and operational risk;

laws, rules, regulations, guidelines and norms applicable to the banking industry, including priority sector

lending requirements, capital adequacy and liquidity requirements

any inability to manage maturity and interest rate mismatches between our assets and liabilities;

adverse change in the economy of India; and

certain failures, including internal or external fraud, operational errors, system malfunctions, or cyber security

incidents.

Additional factors that could cause actual results, performance or achievements to differ materially include, but

are not limited to, those discussed in “Risk Factors” beginning on page 12. Whilst our Bank believes that the

expectations reflected in such forward-looking statements are reasonable at this time, it cannot assure investors

that such expectations will prove to be correct. Given these uncertainties, Investors are cautioned not to place

undue reliance on such forward-looking statements. In any event, these statements speak only as of the date of

this Letter of Offer or the respective dates indicated in this Letter of Offer. Neither our Bank nor the Lead Manager

nor any of their respective affiliates or advisors undertakes obligation to update or revise any of them, whether as

a result of new information, future events or otherwise. If any of these risks and uncertainties materialise, or if

any of our Bank’s underlying assumptions prove to be incorrect, the actual results of operations or financial

condition of our Bank could differ materially from that described herein as anticipated, believed, estimated or

expected. All subsequent forward-looking statements attributable to our Bank are expressly qualified in their

entirety by reference to these cautionary statements.

12

SECTION II: RISK FACTORS

An investment in Equity Shares involves a high degree of risk. You should carefully consider all the information

in this Letter of Offer, including the risks and uncertainties described below, before making an investment in our

Rights Equity Shares. The financial and other implications of material impact of risks concerned, wherever

quantifiable, have been disclosed in the risk factors mentioned below. However there are a few risk factors where

the impact is not quantifiable and hence the same has not been disclosed in such risk factors.

The occurrence of any of the following events could have a material adverse effect on our business, results of

operations, financial condition and prospects and cause the market price of our Equity Shares to fall significantly,

and you may lose all or part of your investment. Additionally, our business operations could also be affected by

additional factors that are not presently known to us or that we currently consider as immaterial to our operations.

The following factors have been considered for determining the materiality:

1. Some events may not be material individually but may be found material collectively;

2. Some events may have material impact qualitatively instead of quantitatively; and

3. Some events may not be material at present but may have material impact in future.

INTERNAL RISK FACTORS AND RISK FACTORS RELATING TO OUR BUSINESS

1. We are involved in certain legal and other proceedings in India. If any of the pending cases is decided

against us, it may have a material adverse effect on our businesses, reputation, financial condition and

results of operations.

Our Bank is involved in various civil, criminal, consumer and tax related litigations which are at different

stages of adjudications before various forums. We are involved in litigations for a variety of reasons, which

generally arise in the normal course of business, when we seek to recover our dues from borrowers who

default in payment of the loans or when customers seek claims against us during the process of recovery of

our dues or for other service related issues.

Material Litigation against our Bank:

Sl. No. Brief Description No. of

Cases

Amount

Involved

(` in crore)

1. Criminal proceedings 14 Not quantifiable

2. Direct tax matters 6 859.03

3. Indirect tax matters - -

4. Civil Cases 5 Not quantifiable

The criminal proceedings against our Bank inter alia include complaints in respect to wrongful credit of

cheques, breach of trust, cheating and other related cases. We cannot assure you that the provisions we have

made for litigation will be sufficient or that new litigations will not be brought against us in the future. If we

fail to successfully defend these or other claims, or if our current provisions prove to be inadequate, our

business, financial condition and results of operations could be adversely affected.

Material Litigation by our Bank:

Sl. No. Brief Description No. of Cases Amount Involved

(` in Crore)

1. Criminal matters

Proceedings under section 138 of

the Negotiable Instruments Act

20

1.22

First Information Report (FIR) filed

by our Bank in fraud cases

181

79.74

2. Civil Proceedings 10 610.90

Our Bank intends to defend or appeal these proceedings and would be required to devote management and

13

financial resources in their defense or prosecution. It cannot be assured that any new litigation / counter suits

will not be brought against our Bank in the future, in respect to such legal proceedings. If our Bank fails to

successfully defend these or other claims, or if its current provisions prove to be inadequate, our business,

financial condition and results of operations could be adversely affected.

For further details in this regard, please refer to the chapter titled “Legal and Other Information” beginning

on page 67.

2. Our financial performance may be materially and adversely affected by fluctuating interest rates.

Our results of operations depend, to a great extent, on our net interest income. Net interest income comprised

69.73%, 70.55% and 67.66% of our total net income for the Fiscals 2015, 2016 and the quarter ended June

30, 2016, respectively, where total net income comprises the sum of our net interest income and other income.

Out of our gross advances, fixed interest rate bearing assets constituted 6.65%, 7.26% and 6.77% for the

Fiscals 2015, 2016 and the quarter ended June 30, 2016, respectively, and floating interest rate bearing assets

constituted 93.35%, 92.74% and 93.23% for the Fiscals 2015, 2016 and the quarter ended June 30, 2016,

respectively.

If the yield on our interest-earning assets does not increase at the same time or to the same extent as our cost

of funds, or if our cost of funds does not decline at the same time or to the same extent as the decrease in the

yield on our interest-earning assets, our net interest income and net interest margin would be adversely

impacted. Any systemic decline in low-cost funding available to banks in the form of current and savings

account deposits would adversely impact our net interest margin.

The implementation of RBI guidelines on the computation of lending rates based on the marginal cost of

funds methodology with effect from April 1, 2016, has led to lower lending rates, and more frequent revisions

in lending rates due to the prescribed monthly review of cost of funds. This has impacted the yield on our

interest-earning assets, our net interest income and net interest margin. Interest rates are highly sensitive to

factors beyond our control, including India's GDP growth, inflation, liquidity, the RBI’s monetary policies

and domestic and international economic and political conditions and other factors. Our cost of funding is

interest-rate sensitive and our ability to pass along any increase in interest rates depends on our borrowers'

willingness to pay higher rates and the competitive landscape in which we operate. Volatility and changes in

interest rates could affect the interest rates we charge on our interest-earning assets in a manner different from

the interest rates we pay on our interest-bearing liabilities because of the different maturity periods applicable

to our assets and liabilities. An increase in interest rates applicable to our liabilities, without a corresponding

increase in interest rates applicable to our assets, will result in a decline in net interest income.

Under the regulations of the RBI, we are required to maintain a minimum specified percentage in the form

of SLR, currently 20.75%, of our net demand and time liabilities in Government or other approved securities

or in cash. Yields on these investments are dependent to a large extent on interest rates. In a rising interest

rate environment, especially if the increase is sudden or sharp, we could be adversely affected by the decline

in the yield on our Government securities portfolio and other fixed income securities and may be required to

further provide for depreciation in the Available for Sale (“AFS”) and Held For Trading (“HFT”) categories,

which may adversely impact our business and financial performance of our Bank.

Furthermore, in the event of rising interest rates, our borrowers may not be willing to pay correspondingly

higher interest rates on their borrowings and may choose to repay their advances with us if they are able to

switch to more competitively priced advances offered by other banks. In the event of falling interest rates,

we may face more challenges in retaining our customers if we are unable to switch to more competitive rates

as compared to other banks in the market. In addition, any volatility or increase in interest rates may also

adversely affect the rate of growth of certain sectors of the Indian economy. All these factors may have a

material adverse effect on our business and financial condition and results of operations.

3. Any increase in our portfolio of NPAs, RBI-mandated provisioning requirements or restructured advances

could materially and adversely affect our business and future financial performance

For the Fiscal years 2015, 2016 and the quarter ended June 30, 2016, our gross non-performing assets (“Gross

NPA”) represented 2.95%, 3.44% and 3.92% of our total gross advances respectively, and our NPAs (net of

provisions) (“Net NPA”) represented 1.98%, 2.35% and 2.61% of net advances respectively. As at March

31, 2015 and 2016 and as at June 30, 2016, our provision coverage ratio was 50.54%, 48.39% and 48.89%,

14

respectively.

If there is any deterioration in the quality of our security or further ageing of the assets after being classified

as non-performing, an increase in provisions will be required. This increase in provisions may adversely

impact our financial performance. While we have already made provisions for non-performing assets

(“NPA”) with respect to 31.42% and 33.52% of our Gross NPAs as at March 31, 2016 and as at June 30,

2016, respectively, we may need to make further provisions if there is dilution/deterioration in the security or

downgrading of the account or recoveries with respect to such NPAs do not materialize in time or at all. Our

NPAs can be attributed to several factors, including inconsistent industrial growth, the high level of debt in

the financing of projects and capital structures of companies in India and the high interest rates in the Indian

economy, which reduced the profitability of some of our borrowers.

In addition to the above, under the directed lending norms of RBI, we are required to extend 40.00% of our

adjusted net bank credit to certain eligible sectors, which are categorised as ‘priority sectors’. We may

experience an increase in NPAs in our lending to priority sectors, particularly with regard to loans that are

granted to the agriculture and small and micro enterprises, where the borrowers are most vulnerable to

economic difficulties.

Although we are increasing our efforts to improve recovery, we cannot assure you that we will be successful

in our efforts or that the overall quality of our loan portfolio may not deteriorate in the future. If we are unable

to successfully monitor and manage our portfolio, including during economic downturns, our asset quality

and as a result, our financial condition and results of operation, could be materially and adversely affected.

Our total gross standard restructured advances were ` 1,799.77 crore, ` 1,546.69 crore and ` 1,497.70 crore

as at March 31, 2015 and 2016 and as at June 30, 2016, respectively. We restructure assets based on

borrower’s potential to restore its financial health; however, there can be no assurance that borrowers will be

able to meet their obligations under restructured advances as per regulatory requirements and certain assets

classified as restructured, may be classified as delinquent. Any resulting increase in delinquency levels may

adversely impact our business, financial condition and results of operations; for example, in January 2014,

the RBI issued a framework and in March, 2014, a corrective action plan for early identification and resolution

of stressed assets. With effect from April 1, 2014, the guidelines introduced an asset classification category

of “special mention accounts”, which comprises cases that are not yet restructured or classified as non-

performing but which exhibit early signs of stress, as specified through various parameters. Banks in India

are also required to share data with each other on certain categories of special mention accounts, set up joint

lenders’ forums and formulate action plans for resolution of these accounts. Failure to do so may result in

accelerated provisioning for such cases.

Our gross non-performing loans increased from ` 944.21 crore as at March 31, 2015 to ` 1,180.40 as of

March 31, 2016 and to ` 1,389.36 crore as at June 30, 2016. Further, guidelines issued by the RBI relating to

the identification and classification of NPAs may result in an increase in our loans classified as non-

performing and provisioning requirements. Any review on asset quality by the regulator, during specific or

general inspection, can result in additional classification of our loans as NPAs thus increasing our

provisioning requirements and adversely impacting our profitability in the future.

If we are not able to adequately control or reduce the level of non-performing assets, or if the RBI continues

to impose increasingly stringent requirements, the overall quality of our loan portfolio could deteriorate,

which may have a material adverse effect on our business, financial condition and results of operations.

4. We are required to maintain cash reserve ratio (“CRR”) and statutory liquidity ratio (“SLR”). Any increase

in these requirements could adversely affect our business, financial condition and results of operations.

As a result of the statutory reserve requirements stipulated by the RBI, we may be more exposed structurally

to interest rate risk than banks in many other countries. Under RBI regulations, we are subject to a CRR

requirement. The CRR is a bank’s balance held in a current account with the RBI calculated as a specified

percentage of its net demand and time liabilities, excluding interbank deposits. The CRR currently applicable

to banks in India is 4.00% and banks do not earn any interest on those reserves. In addition, under the Banking

Regulation Act, all banks operating in India are required to maintain SLR. The SLR is a specified percentage

of a bank’s net demand and time liabilities by way of liquid assets such as cash, gold or approved

unencumbered securities. Approved unencumbered securities consist of unencumbered Government

securities and other securities as may be approved from time to time by the RBI and would earn lower levels

15

of interest as compared to advances to customers or investments made in other securities. In the fourth bi-

monthly monetary policy statement of the RBI for the Fiscal year 2016, the ceiling on securities eligible for

SLR under the held to maturity (“HTM”) securities was aligned with the SLR and was accordingly brought

down from 22% to 21.50% with effect from January 9, 2016. Further, it was decided that both the SLR and

HTM ceiling would be brought down by 25 basis points every quarter until March 31, 2017. Currently, the

RBI requires banks to maintain a SLR of 20.75%.

The RBI may increase the CRR and SLR requirements to significantly higher proportions as a monetary

policy measure, as and when the same is warranted. Any increase in the CRR from the current levels could

affect our ability to deploy our funds or make investments, which could in turn have a negative impact on our

results of operations. If we are unable to meet the requirements of the RBI, the RBI may impose penal interest

or prohibit us from receiving any further fresh deposits, which may have a material adverse effect on our

business, financial condition and results of operations.

5. We are subject to capital adequacy norms and are required to maintain a CRAR at or above the minimum

level required by the RBI for domestic banks. There is no guarantee that we will be able to access capital

as and when it is needed for growth. If we fail to meet capital adequacy requirements, the RBI may take

certain actions, including restricting our lending and investment activities, and the payment of dividends

by us. These actions could materially and adversely affect our reputation and financial results.

We are required by the RBI to maintain a minimum capital adequacy ratio of 9.625% (including capital

conservation buffer of 0.625%) in relation to our total risk-weighted assets.

In addition, the RBI issued Basel III Capital Regulations on May 2, 2012. The Basel III Capital Regulations

require, among other things, higher levels of Tier I capital and common equity, capital conservation buffers,

maintenance of a minimum prescribed leverage ratio on a quarterly basis and higher deductions from common

equity and changes in the structure of non-equity instruments eligible for inclusion in Tier I capital. The Basel

III Capital Regulations also set out elements of regulatory capital and the scope of the capital adequacy

framework, including disclosure requirements of components of capital and risk coverage. The transitional

arrangements for the implementation of Basel III capital regulations in India began on April 1, 2013 and the

guidelines are required to be fully implemented by March 31, 2019. In accordance with the Basel III capital

regulations, currently, we are required to maintain a minimum CET-I ratio of 5.5%, a capital conservation

buffer (CCB) (comprised of common equity) of 0.625%, a minimum Tier I capital ratio of 7.00%, of our risk

weighted assets (RWA).

As at June 30, 2016, our capital adequacy ratio under the Basel III Capital Regulations was 11.64%, with a

Tier I capital adequacy ratio of 10.27%, a Tier II capital adequacy ratio of 1.37% and CET I capital adequacy

ratio of 10.27%. As at March 31, 2016, our capital adequacy ratio under the Basel III Capital Regulations

was 12.03%, with a Tier I capital adequacy ratio of 10.56%, a Tier II capital adequacy ratio of 1.47% and

CET I capital adequacy ratio of 10.56% and as at March 31, 2015, under the Basel III regulations, our CRAR,

Tier I and Tier II capital adequacy ratios were 12.41%, 10.52% and 1.89% respectively. Although we are

currently in compliance with the applicable capital adequacy requirements, certain adverse developments

could affect our ability to satisfy these requirements in the future, including deterioration in our asset quality,

decline in the value of our investments and our inability to meet any regulatory requirements or changes.

We are exposed to the risk of the RBI increasing the applicable risk weight for different asset classes from

time to time. In addition, with the approval of the RBI, banks in India may migrate to advanced approaches

for calculating risk-based capital requirements in the medium term. If we fail to meet capital adequacy

requirements, the RBI may take certain actions, including restricting our lending and investment activities,

and the payment of dividends by us.

Further, continued compliance requirements with Basel III or other capital adequacy requirements imposed

by the RBI may result in the incurrence of substantial compliance and monitoring costs. Moreover, if the

Basel Committee releases additional or more stringent guidance on capital adequacy norms which are given

the effect of law in India in the future, we may be forced to raise or maintain additional capital in a manner

which could affect our business, financial condition and results of operations. There can be no assurance that

we will be able to comply with such requirements or that any breach of applicable laws and regulations will

not have a material adverse effect on our business, financial condition and results of operations.

6. The value of our collateral may decrease or we may experience delays in enforcing our collateral if

16

borrowers default on their obligations, which may result in failure to recover the expected value of

collateral security exposing us to a potential loss. This can adversely affect our business and the financial

performance of our Bank.

A substantial portion of our loans are secured by collateral, including real estate assets such as property, plant,

equipment, inventory, receivables, current assets and pledges of financial assets such as marketable securities

and corporate guarantees. The loans to corporate customers also include working capital credit facilities that

are typically secured by a first lien on inventory, receivables and other current assets. In certain cases, we

may have taken further security of a first or second lien on fixed assets and a pledge of financial assets like

marketable securities, corporate guarantees and personal guarantees. As at June 30, 2016, 91.31% of our

advances were secured by tangible assets/bank guarantees/government guarantees, including advances

secured by fixed deposits and book debts and 8.69% of our advances were unsecured.

In the event of our borrowers defaulting on the repayment of the loans, we may not be able to realize the full

value of the collateral due to various reasons, including a possible decline in the realisable value of the

collateral, defective title, prolonged legal proceedings and fraudulent actions by borrowers.

In India, foreclosure on collateral generally requires filing a suit or an application in a court or tribunal.

Although special tribunals have been set up for expeditious recovery of debts due to banks, any proceedings

brought may be subject to delays and administrative requirements that may result in, or be accompanied by,

a decrease in the value of the collateral. The SARFAESI Act, the Recovery of Debts Due to Banks and

Financial Institutions Act 1993, as amended, and the RBI’s corporate debt restructuring mechanism have

strengthened the ability of lenders to recover NPAs by granting them greater rights to enforce security and

recover amounts owed from secured borrowers. However, there can be no assurance that this legislation will

have a favorable impact on our efforts to recover NPAs as the full effect of such legislation is yet to be

determined in practice.

Until recently, there were multiple overlapping laws and adjudicating forums dealing with financial failure

and insolvency of companies and individuals in India. Recognizing that reforms in the bankruptcy and

insolvency regime are critical for improving the business environment and alleviating distressed credit

markets, the Government of India introduced the Insolvency and Bankruptcy Code Bill in November 2015

aimed at making it easier to wind up a failing business and recover debts. While the Insolvency and

Bankruptcy Code, 2016 (the "Code"), which came into effect on May 28, 2016 is a historical development

for economic reforms in India, its effect is yet to be seen when the institutional infrastructure and

implementing rules as envisaged under the Code are formed and enforced. Until the implementation of such

infrastructure is completed, it may not be possible to determine the effects of the Code.

In addition, pursuant to RBI prudential guidelines on restructuring of advances by banks, we may not be

allowed to initiate recovery proceedings against a corporate borrower where the borrower's aggregate total

debt is ` 10 crore or more and 60.00% of the lenders by number and holding at least 75.00% or more of the

borrower's debt by value decide to restructure their advances. In such a situation, we are restricted to a

restructuring process only as approved by the majority lenders. If we own 25.00% or less of the debt of a

borrower, we could be forced to agree to an extended restructuring of debt which may not be in our interests.

As on June 30, 2016, there was one case of our Bank’s recovery issues under corporate debt restructuring

aggregating to ` 42.59 crore constituting 2.38% of the total outstanding liability of the borrower (exposure to

banking sector being ` 1,787.98 crore). In this case, since our Bank owns less than 25% of the debt, we are

bound by the decision of other creditors.

There can be no assurance that we will be able to realize the full value of the collateral, as a result of, among

other factors, delays in bankruptcy and foreclosure proceedings, the defects in the perfection of collateral and

fraudulent transfers by borrowers. A failure to recover the expected value of collateral security could expose

us to a potential loss. Such difficulties in realizing our collateral fully or at all, including if we are compelled

to restructure our loans, may have a material adverse effect on our business, financial condition, results and

cash flow.

7. Regulations in India require us to extend a minimum level of advances to certain sectors. These may

subject us to higher delinquency rates. Our inability to comply with Indian priority sector lending

requirements may require us to invest in funds with a lower return than we would otherwise obtain in the

market.

17

The RBI mandates all banks that are operating in India to direct a certain portion of their lending to specified

“Priority Sector” such as agriculture, MSMEs, housing and education, and has specified a target for domestic

banks as a percentage of ANBC of corresponding previous year. RBI regulations specify that priority sector

requirements should be met on the basis of the credit equivalent of off-balance sheet exposure rather than

ANBC, if such off-balance sheet exposure by a bank is higher than its ANBC. The RBI specifies sub-

allocation requirements, including a minimum 18% of the ANBC or equivalent credit amount of off-balance

sheet exposure, whichever is higher, to the agriculture sector (8% to small and marginal farmers), 7.5% of

the ANBC or equivalent credit amount of off-balance sheet exposure, whichever is higher, to micro

enterprises and 10% of the ANBC or equivalent credit amount of off-balance sheet exposure, whichever is

higher, to weaker sections. In the case of any shortfall by us in meeting lending requirements, we are required

to place the difference between the required lending level and our actual priority sector lending in an account

with the National Bank for Agriculture and Rural Development under the Rural Infrastructure

Development Fund Scheme, or funds with other financial institutions specified by the RBI, from which we

earn lower levels of interest as compared to loans made to the priority sector. Further, from April 1, 2016,

banks in India are required to comply with priority sector lending requirements on a quarterly basis which

can also result in lower levels of interest income and reduced profitability. Any requirements by the RBI that

specify changes in priority sector lending may adversely affect our business, financial condition and results

of operations.

As on March 31, 2016 and June 30, 2016, the total credit extended by us to priority sectors constituted 47.57%

and 47.89%, respectively of our ANBC; and the credit extended to the agriculture sector constituted 17.19%

and 16.85%, respectively of our ANBC. Though we have met the target in relation to aggregate lending

required to be made to the priority sector for the year ended March 31, 2016, we have not been able to meet

the sub targets that have been set with respect to separate sectors under it.

In the case of any shortfall by us in meeting agriculture sector lending requirements, we would subsequently

be required to place the difference between the required lending level and our actual priority sector lending

in an account with the National Bank for Agriculture and Rural Development under the Rural Infrastructure

Development Fund Scheme, or with other financial institutions specified by the RBI, from which we would

earn lower levels of interest compared to advances made to the priority sector. Further, the RBI is required to

take into account any shortfall in meeting specific priority sector lending targets, at the time of granting any

approvals sought by a bank, from time to time. Such circumstances could materially and adversely affect our

business, financial condition and results of operations.

Any change in RBI regulations may require us to increase our lending to relatively higher risk segments,

which may result in an increase in our NPAs under our direct lending portfolio. Any increase in our direct

lending to certain sectors will result in an increase in our exposure to the payment risks inherent in such

sectors, which could materially and adversely impact our business, financial condition and results of

operations.

8. Our risk management policies and procedures may not adequately address unanticipated risks. Inability

to develop and implement effective risk management policies may adversely affect our business, prospects,

financial condition and results of operations.

We have devoted significant resources to developing our risk management policies and procedures and expect

to continue to do so in the future. We have policies and procedures in place to measure, manage and control

the various risks to which we are exposed, including a Risk Management Policy that articulates our approach

to the identification, measurement, monitoring controlling and mitigation of various risks associated with our

banking operations in addition to providing certain important guidelines for strict adherence. Our other

important risk mitigants include our commercial general liability policy, standard fire and special perils

policy, burglary policy, banker’s indemnity policy and directors and officer’s liability policy and, in

compliance with the RBI’s guidelines on Basel II - Pillar 2 - Supervisory Review and Evaluation Process,

Internal Capital Adequacy Assessment Process Policy. The Risk Management Committee of the Board and

the Board reviews our risk management policies annually. Despite this, our policies and procedures to identify,

monitor and manage risks may not be fully effective. Some of our methods of managing risk are based upon

the use of observed historical market behaviour. As a result, these methods may not accurately predict future

risk exposures which could be significantly greater than indicated by the historical measures.

Management of operations, legal and regulatory risks requires, among other things, policies and procedures

to properly record and verify a large number of transactions and events, and these policies and procedures

18

may not be fully effective. As we seek to expand the scope of our operations, we also face the risk of inability

to develop risk management policies and procedures that are appropriately designed for those new business

areas. Inability to develop and implement effective risk management policies may adversely affect our

business, prospects, financial condition and results of operations.

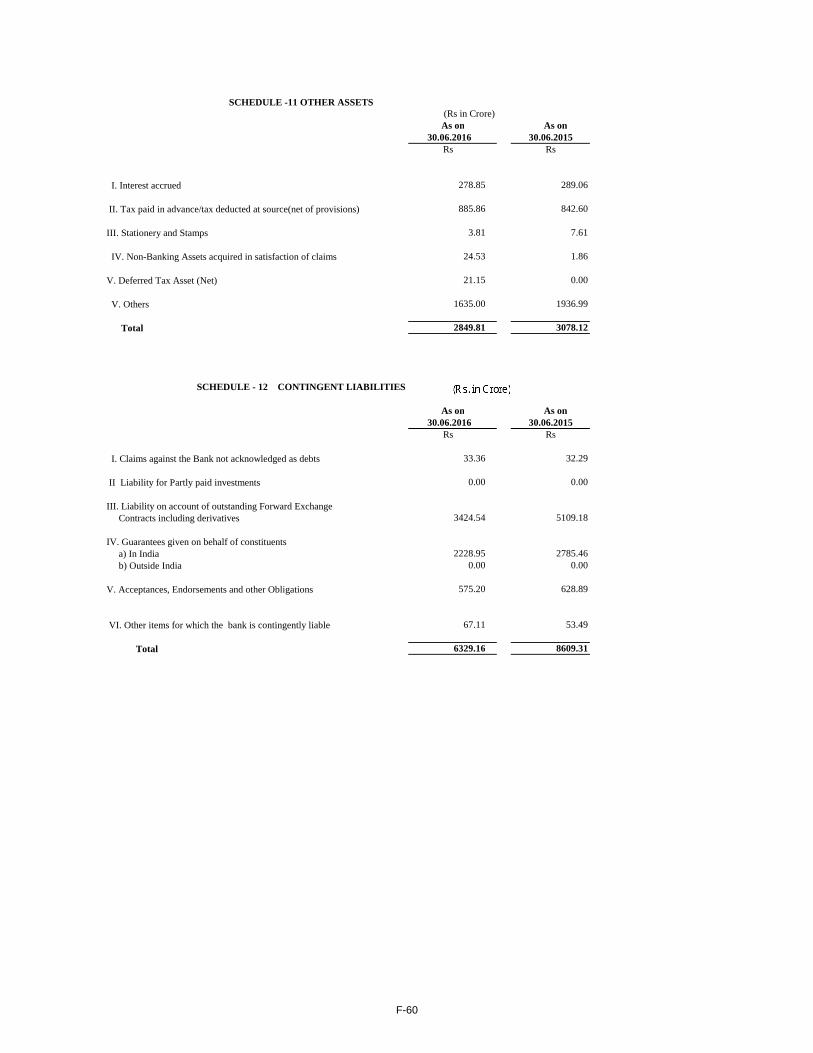

9. We have certain contingent liabilities which have not been provided for in our financial statements,

which if they materialise, may adversely affect our financial condition.

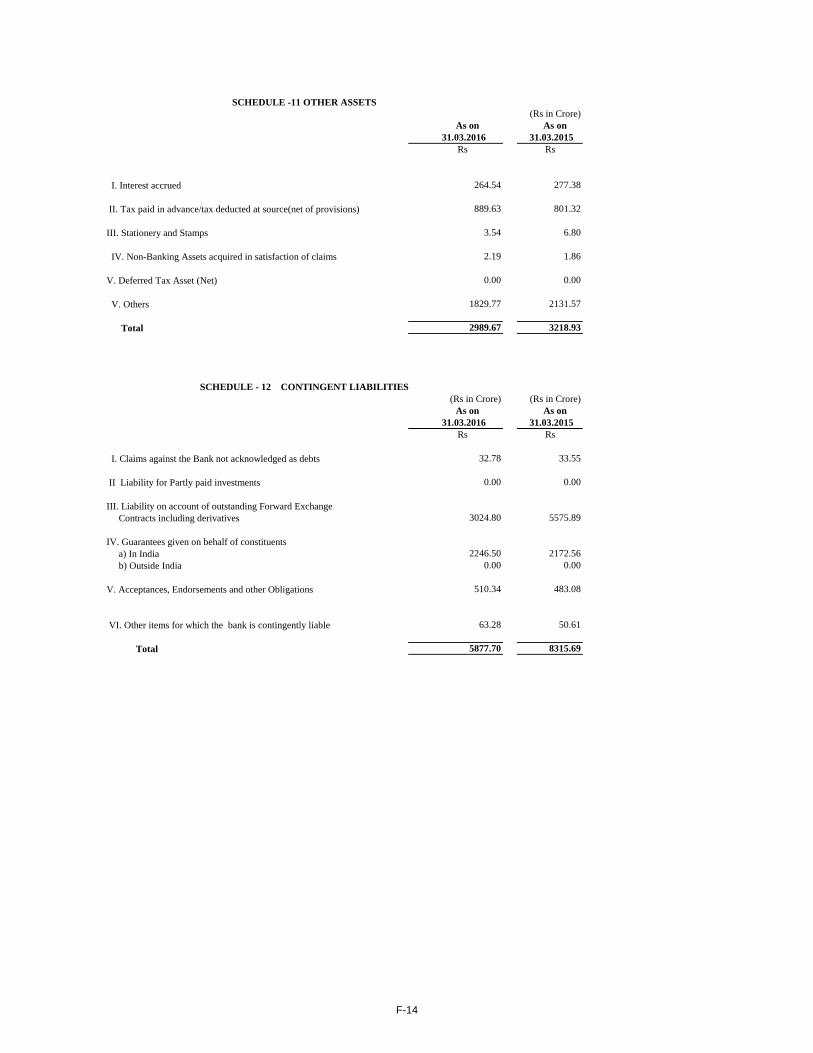

As on March 31, 2016 and June 30, 2016, we had a contingent liabilities, which have not been provided for,

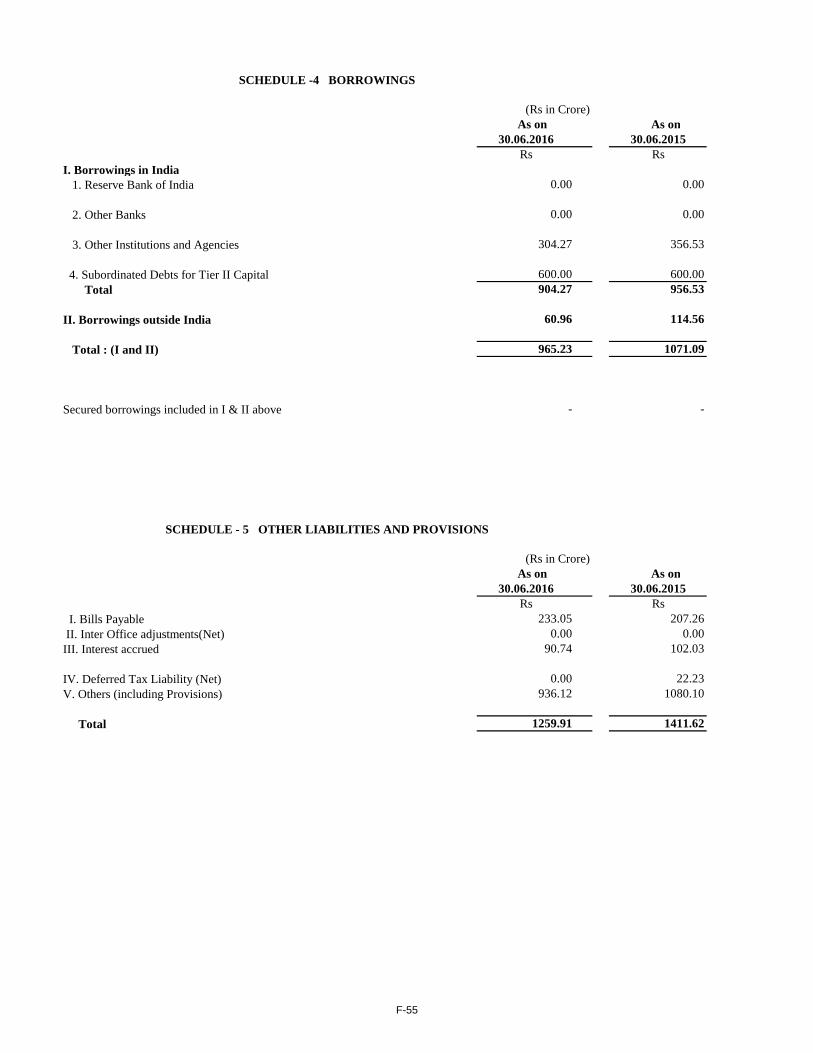

amounting to ` 5,877.69 crore and ` 6,329.16 crore respectively, the details of which are given below:

(in ` Crore)

Contingent Liabilities As on March 31,

2016

As on June 30, 2016

Claims against the Bank not acknowledged as debts 32.78 33.36

Liability on account of outstanding Forward Exchange

Contacts including derivatives

3,024.80 3,424.54

Guarantees given on behalf of constituents

a) In India 2,246.49 2,228.95

b) Outside India - -

Acceptances, Endorsements & other Obligations 510.34 575.20

Other items for which the bank is contingently liable 63.28 67.11

Total 5,877.69 6,329.16

Most of these liabilities have been incurred during the normal course of our business. In the event of there

being a crystallization of any of the above liabilities, we may be required to honour the demands raised. This

may materially and adversely impact our business, financial conditions, result of operations and prospects.

10. Our Joint Statutory Central Auditors have highlighted a matter of emphasis in relation to the audited

financial statements of our Bank as at and for the Fiscal year ended March 31, 2016.

Our Joint Statutory Central Auditors’ report on the financial statements as at and for the year ended March

31, 2016 included an Emphasis of Matter paragraph, that does not require any corrective adjustment in the

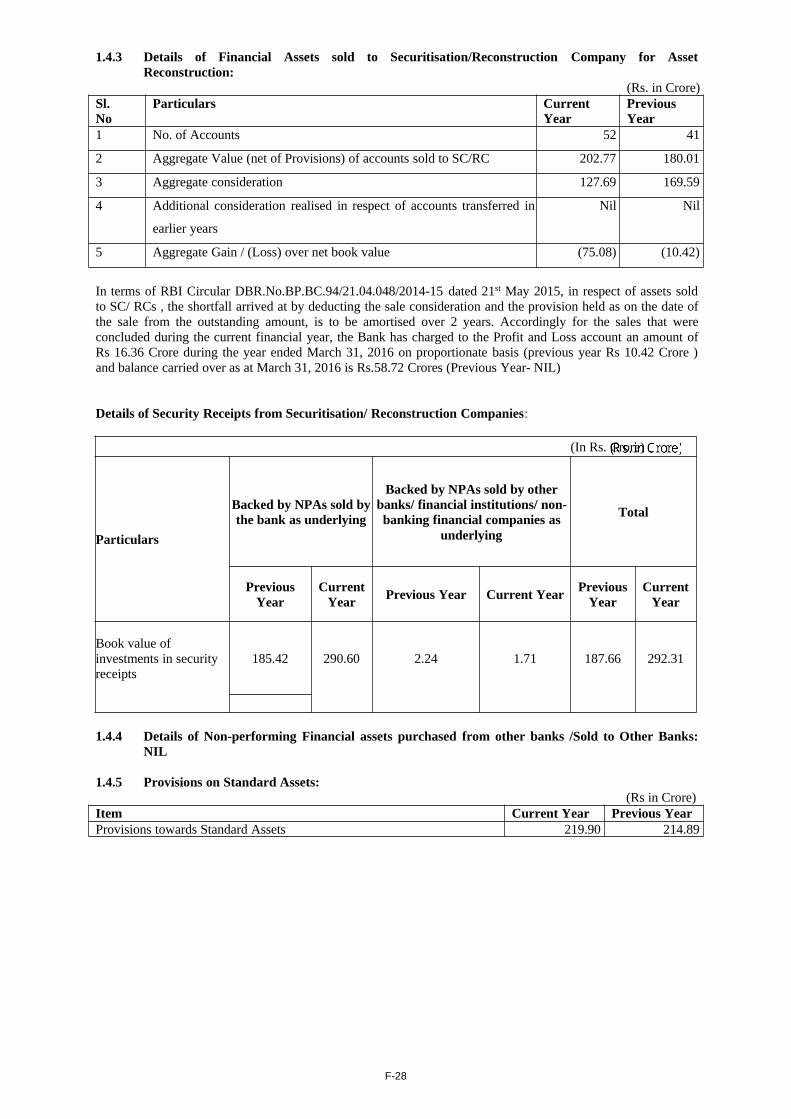

financial information, as follows:

“We draw attention to Note on the Financial Statements, regarding deferment of loss of ` 58.72 crore on sale

of advances to Asset Reconstruction Companies. Our opinion is not qualified in respect of this matter.”

For the reference, below is the relevant extract from note of Schedule 18 to the financial statements:

“Details of Financial Assets sold to Securitisation/Reconstruction Company for Asset Reconstruction:

In terms of RBI Circular DBR.No.BP.BC.94/21.04.048/2014-15 dated 21st May 2015, in respect of assets sold

to SC/ RCs, the shortfall arrived at by deducting the sale consideration and the provision held as on the date

of the sale from the outstanding amount, is to be amortised over 2 years. Accordingly for the sales that were

concluded during the current financial year, the Bank has charged to the Profit and Loss account an amount

of `16.36 Crore during the year ended March 31, 2016 on proportionate basis (previous year ` 10.42 Crore

) and balance carried over as at March 31, 2016 is ` 58.72 Crore (Previous Year - NIL)”

Investors are urged to take a note of the matter of emphasis in the course of reviewing and evaluating our

restated financial statements. For additional information, see the Joint Statutory Central Auditors' report on

our Audited Financial Statements, including the notes thereto, included in this Letter of Offer.

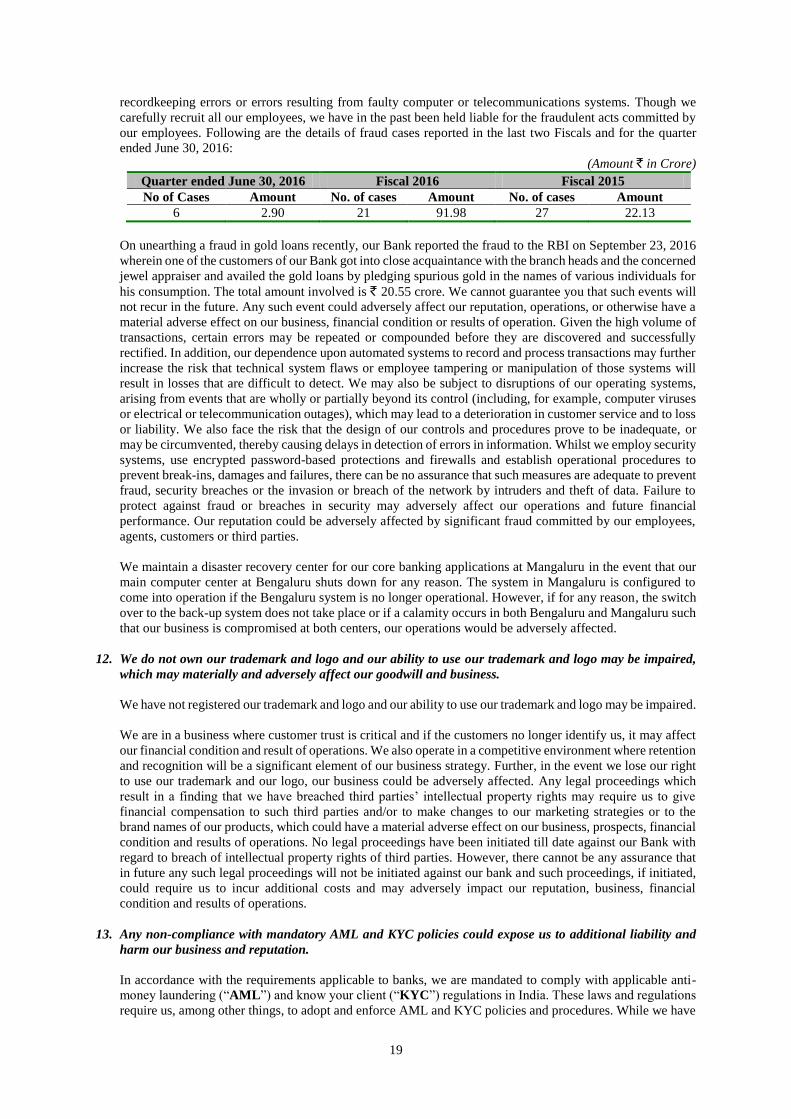

11. There are operational risks associated with the banking industry, including the risk of fraud or other

misconduct by employees etc., which when realised may have an adverse impact on our results.

We are vulnerable to many types of operational risks, including the risk of fraud or other misconduct by

employees or outsiders, unauthorized transactions by employees or operational errors, including clerical or

19

recordkeeping errors or errors resulting from faulty computer or telecommunications systems. Though we

carefully recruit all our employees, we have in the past been held liable for the fraudulent acts committed by

our employees. Following are the details of fraud cases reported in the last two Fiscals and for the quarter

ended June 30, 2016:

(Amount ` in Crore)

Quarter ended June 30, 2016 Fiscal 2016 Fiscal 2015

No of Cases Amount No. of cases Amount No. of cases Amount

6 2.90 21 91.98 27 22.13

On unearthing a fraud in gold loans recently, our Bank reported the fraud to the RBI on September 23, 2016

wherein one of the customers of our Bank got into close acquaintance with the branch heads and the concerned

jewel appraiser and availed the gold loans by pledging spurious gold in the names of various individuals for

his consumption. The total amount involved is ` 20.55 crore. We cannot guarantee you that such events will

not recur in the future. Any such event could adversely affect our reputation, operations, or otherwise have a

material adverse effect on our business, financial condition or results of operation. Given the high volume of

transactions, certain errors may be repeated or compounded before they are discovered and successfully

rectified. In addition, our dependence upon automated systems to record and process transactions may further

increase the risk that technical system flaws or employee tampering or manipulation of those systems will

result in losses that are difficult to detect. We may also be subject to disruptions of our operating systems,

arising from events that are wholly or partially beyond its control (including, for example, computer viruses