the ifc microfinance story · telenor and tameer microfinance bank ... operating costs of staff...

TRANSCRIPT

The IFC Microfinance Story Mobile Banking As An Enabler of Financial Inclusion

2

Beneficiaries:

24 mn micro loans*

Investments:

USD 3bn Cumulative

Commitments

20 years of helping shape the Microfinance Industry

Partners:

more than 200 Investee Clients**

Deposits:

150mn accounts with

USD75bn in

savings*

*MSME client loans/deposits smaller than USD10,000

**On Active and Closed Projects

IFC’s commitment and Engagement vis a vis the Pakistani

Microfinance Landscape

• First Microfinance Bank of Pakistan: Sponsored by the Aga Khan Agency of Microfinance

Equity in greenfield: US$2.03 mm

TA: US$ 200k on MIS strategy/ audit of FMBP and AKAM

• Tameer Microfinance Bank: Sponsored by Telenor Pakistan

Equity in greenfield: US$ 486k

Loan (FY09): US$3.7 mm

TA: US$ 435k for MIS development and deployment

• Kashf Microfinance Bank (Now Finca Microfinance Bank): Sponsored by Kashf NGO

Equity in greenfield: US$ 1.06 mm in KASHF Microfinance Bank

TA: US$ 200k for Business Planning, Deposit Strategy and ACLEDA/ BRI study tour

• National Rural Support Program (NRSP): TA: US$150k (on CG review, business plan strengthening (transformation

implementation plan) and deposit mobilization strategy)

Equity: US$1.7 mm

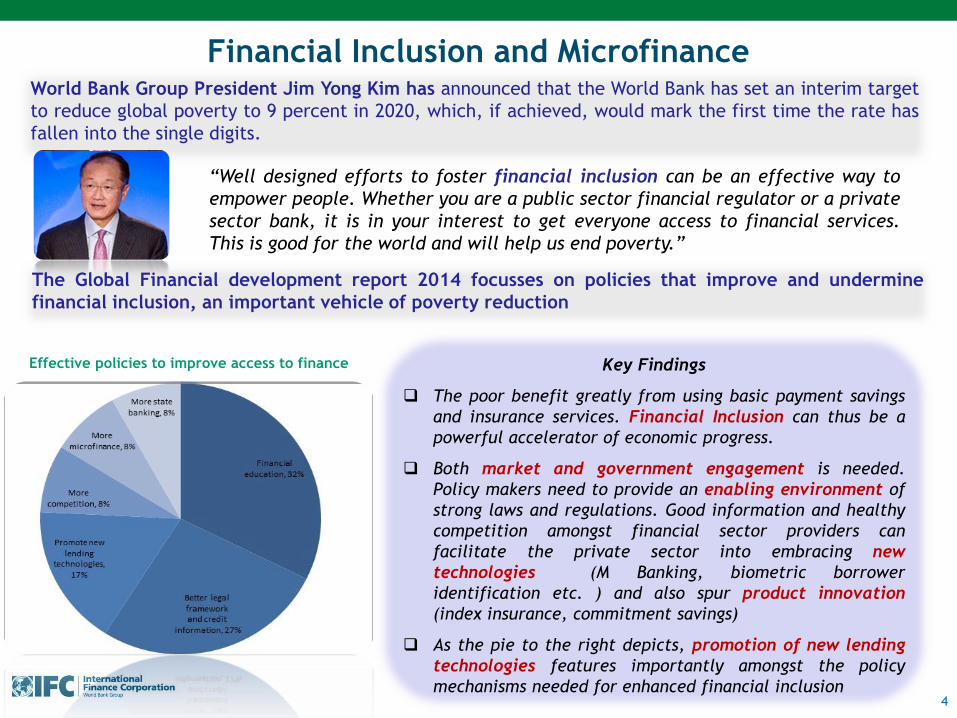

Financial Inclusion and Microfinance

4

“Well designed efforts to foster financial inclusion can be an effective way to

empower people. Whether you are a public sector financial regulator or a private

sector bank, it is in your interest to get everyone access to financial services.

This is good for the world and will help us end poverty.”

World Bank Group President Jim Yong Kim has announced that the World Bank has set an interim target

to reduce global poverty to 9 percent in 2020, which, if achieved, would mark the first time the rate has

fallen into the single digits.

The Global Financial development report 2014 focusses on policies that improve and undermine

financial inclusion, an important vehicle of poverty reduction

Effective policies to improve access to finance Key Findings

The poor benefit greatly from using basic payment savings

and insurance services. Financial Inclusion can thus be a

powerful accelerator of economic progress.

Both market and government engagement is needed.

Policy makers need to provide an enabling environment of

strong laws and regulations. Good information and healthy

competition amongst financial sector providers can

facilitate the private sector into embracing new

technologies (M Banking, biometric borrower

identification etc. ) and also spur product innovation

(index insurance, commitment savings)

As the pie to the right depicts, promotion of new lending

technologies features importantly amongst the policy

mechanisms needed for enhanced financial inclusion

Journey from social innovation to viable asset class

5

Then:

In the early 1990’s

Microfinance was

still a social

innovation that

proved that

lending to the

poor was not a

loss-making

enterprise.

Changes

• Implementation of Financial Industry

rigor:

• credit analysis

• profitability analysis

• risk analysis

• Increased emphasis on institutional

capacity and governance

• Increased participation of private sector

funders

• Creation of a network of industry

stakeholders: knowledge partners, funding

communities

• Transformation of institutions: NGOs

becoming licensed MF banks, Commercial

banks downscaling

• MFIs dominant players in some markets

Now:

Microfinance has

emerged as a

successful asset

class and a

profitable industry

Expanding reach:

Transforming

existing MFI

Through which initiatives did IFC create development impact?

6

Building

Capacity:

Greenfield

Investments

24,028

19,842

12,61510,794

9,331

0

5,000

10,000

15,000

20,000

25,000

30,000

2012 2011 2010 2009 2008

$ Loans (mn)

Building Scale:

Network

partnerships

Increasing Uptake:

Greater

product choice

Increasing Access:

Delivery Channel

innovations

The last step of the ladder now

points towards technological

innovations to take the

microfinance story forward…

IFC’s exposure

• First Microfinance Bank of Pakistan: Sponsored by the Aga Khan Agency of Microfinance

Equity in greenfield (FY09): US$2.03 mm

TA: US$ 200k on MIS strategy/ audit of FMBP and AKAM

• Tameer Microfinance Bank: Sponsored by Telenor Pakistan

Equity in greenfield (FY09): US$ 486k

Loan (FY09): US$3.7 mm

TA: US$ 435k for MIS development and deployment

• Kashf Microfinance Bank: Sponsored by Kashf NGO

PCG (FY09): US$15 mm – recently dropped due to PAR

Equity in greenfield (FY09): US$ 1.06 mm in KASHF Microfinance Bank

TA: US$ 200k for Business Planning, Deposit Strategy and ACLEDA/ BRI study tour

• National Rural Support Program (NRSP): TA (FY09): US$150k (on CG review, business plan strengthening (transformation

implementation plan) and deposit mobilization strategy)

Mobile Banking: The Context for Pakistan

8

All five cellular mobile companies and leading banks have been enthusiastic about this growing

market due to the following factors:

branchless banking managed more than 31 million transactions worth $1.5 billion in the quarter ended December 2012, a growth of 20% year-on-year, according to the State Bank of Pakistan. If one specifically looks at mobile banking, it has been growing at an annual rate of 37%, according to the SBP.

mobile banking segment has enormous room for growth since only 12% of the population has access to formal financial services while the number of mobile accounts is low in comparison

Only 9% of the total population (190 million) has a mobile banking account against a mobile penetration that stands close to 70%.

a recent study by the Boston Consulting Group, 35% of Pakistan’s adult population will be using mobile financial services by 2020. Large and growing population between 15-64 years

mobile banking kicked off in

Pakistan in 2009 with the

launch of easy-paisa – a

mobile banking solution from

Telenor and Tameer

Microfinance Bank

In the last year, most telecom

operators and banks entered

this growing segment

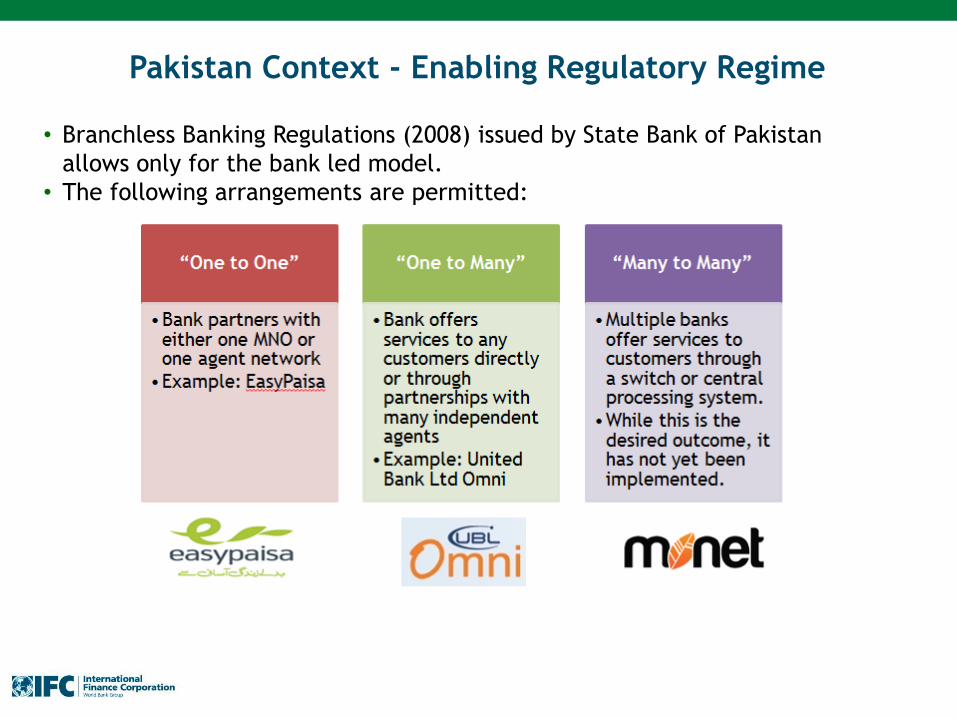

Pakistan Context - Enabling Regulatory Regime

• Branchless Banking Regulations (2008) issued by State Bank of Pakistan

allows only for the bank led model.

• The following arrangements are permitted:

9

Global Experience: M-Banking can help expand Financial Inclusion

Benefits to customers

Easy way to undertake the transactions that they need as well as access to a broad range of services

Alternative to crowded branches, being a less intimidating and often more convenient channel

Significant opportunity to reduce transaction costs – such as travel - for clients

Time saving

Branchless Banking

Non-bank retail

outlets

Technology

Electroinc

stored value

account

+

+

• Access to the formal financial system

and building financial history.

• Easy way to undertake the

transactions that they need as well as

access to a broad range of services.

• Significant opportunity to reduce

transaction costs for clients.

• Price transparency, market

information and safe alternative to

cash.

• Time saving.

Benefits To Customers

10

IFC: B-/M-Banking Deployments in Emerging Markets

11

163 live deployments ,107 deployments planned as of March 2013

LAC

17 live projects

AFRICA

87 live projects

E. EUROPE

2 live projects

ASIA

40 live projects MENA

17 live projects

Source: GSMA Deployment Tracker

- 1 live project

- 2 live projects

- 4 live projects

IFC Supports…

IFC supports a diverse set of microfinance clients

12

Compartamos

Mexico

Bandhan India

Acleda Cambodia

Xac Bank Mongolia

LAPO Nigeria

Bandham India

Equitas India

Ujjivan India

Leading MFI/ MF Banks

FINCA US

Access Germany

ProCredit

Germany

MicroCred France

Advans France

Accion

Aga Khan

Networks/ Holdings

Sekerbank Turkey

Equity Bank Kenya

BTPN Indonesia

Andara Indonesia

Acleda Cambodia

Banks with MF business

FINO India

Yellow Pepper

Technology Providers

Aavishkar India

LOK India

Rural Impact Fund

Leapfrog

Specialized MF Funds

MEF

Regmifa

MIFA

EFSE

GMF

Regional/Global Funds

FMBA Afghanistan

TRM Timor Leste

PNG MF PNG

FATEN Westbank/Gaza

Frontier MFI

RMDC Nepal

Bank Andara Indonesia

Bansicredi Brazil

Fedecredito El Salvador

ACBA Armenia

Cooperatives/Wholesalers

IFC has worked with innovative technology

entrants in the microfinance space for

optimal impact

B-/M-Banking Enabling Factors

Transformational mobile banking

Enabling regulations

- Relevant stored value account

- Agency banking

- AML/KYC

Market demand

- What is the existing unmet demand?

- What is the size of the target segment?

- How to achieve critical size?

Business model

- Revenue model for each party - Business and client ownership - Channel management

Agent management

- Selection and training of agents - Commission model - Liquidity management - Monitoring

Customer adoption

- Focused marketing and communication

- Customer education

1

2

3 4

5

13

There are 5 main enablers for successful transformational branchless/mobile banking

Number of agents needed to create a scale network varies by density and time to outlet

In denser cities, higher numbers of people can be supported by a lower number of

outlets -- because of reduced time to outlet

In rural areas, much lower numbers of people can be supported per outlet simply

because of the “tyranny of distance” imposed by physical cash transactions

Network Effects Matter

Getting the Correct Agent Network Drives Success – or Failure

Success is driven by the simultaneous growth of both outlets and users in a way that creates a

network effect that causes the service to “go viral”

-

3

6

9

12

15

Apr-

07

Jun-0

7

Aug-0

7

Oct-

07

Dec-0

7

Feb-0

8

Apr-

08

Jun-0

8

Aug-0

8

Oct-

08

Dec-0

8

Feb-0

9

Apr-

09

Jun-0

9

Aug-0

9

Oct-

09

Dec-0

9

Feb-1

0

Apr-

10

Jun-1

0

Aug-1

0

Oct-

10

Dec-1

0

Feb-1

1

Apr-

11

0

200

400

600

800

1000

1200

1400

M-P

esa

Cust

om

ers

(in

mm

)

Cust

om

ers

Per

Agent

M-Pesa: Growth of Agent Network

Customers Customers per Agent

Source: Mas & Radcliffe (2010): Mobile Payments Go Viral,

Safaricom website

14

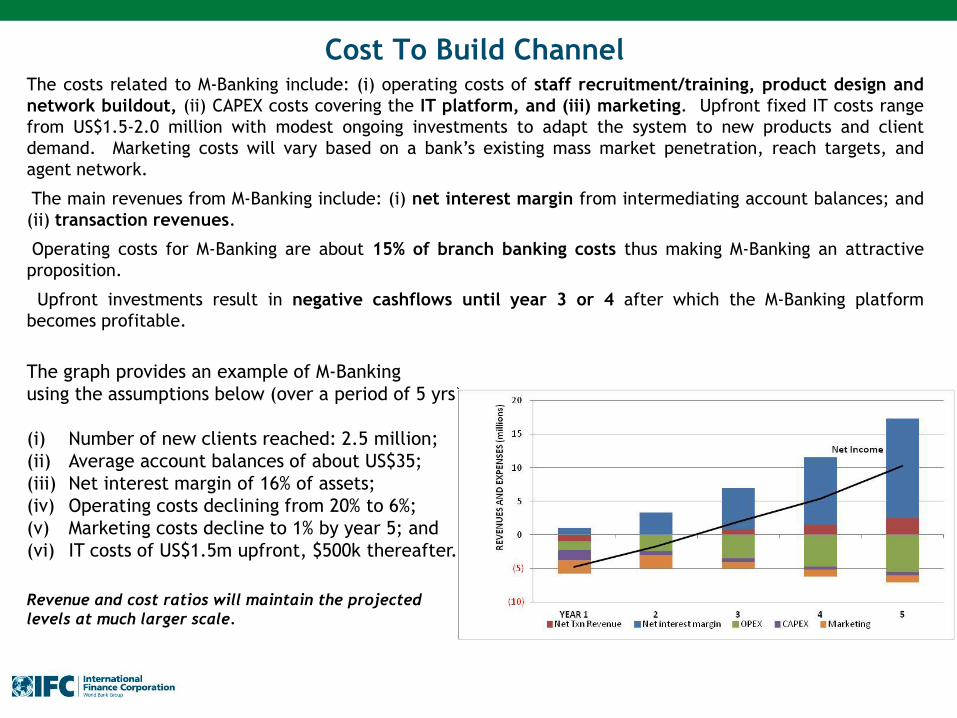

Cost To Build Channel The costs related to M-Banking include: (i) operating costs of staff recruitment/training, product design and

network buildout, (ii) CAPEX costs covering the IT platform, and (iii) marketing. Upfront fixed IT costs range

from US$1.5-2.0 million with modest ongoing investments to adapt the system to new products and client

demand. Marketing costs will vary based on a bank’s existing mass market penetration, reach targets, and

agent network.

The main revenues from M-Banking include: (i) net interest margin from intermediating account balances; and

(ii) transaction revenues.

Operating costs for M-Banking are about 15% of branch banking costs thus making M-Banking an attractive

proposition.

Upfront investments result in negative cashflows until year 3 or 4 after which the M-Banking platform

becomes profitable.

The graph provides an example of M-Banking

using the assumptions below (over a period of 5 yrs):

(i) Number of new clients reached: 2.5 million;

(ii) Average account balances of about US$35;

(iii) Net interest margin of 16% of assets;

(iv) Operating costs declining from 20% to 6%;

(v) Marketing costs decline to 1% by year 5; and

(vi) IT costs of US$1.5m upfront, $500k thereafter.

Revenue and cost ratios will maintain the projected

levels at much larger scale.

15

Case Study Equity Bank : Growth with an Agent Channel Jan 2011 – June 2012

16

M-Banking

channels make

mass market

retail banking

commercially

viable.

The channel

creates access

outside of the

branch network

footprint, and,

Costs about 15%

of traditional

branch-based

services.

Case Study: Bank South Pacific in Papua New Guinea

17

• Largest PNG Bank by customers, branches, e-channels

• BSP Rural Established May 2010 to retain core brand

– More significant innovation

– Rural Kundu Account for the Rural Market

– “One-Touch Process” for Acquisition

– Support by IFC

• Mobile Banking

– Launched as basic SMS Banking offering in 2009

– 2012 enabled Cash Agents and Payments

– Using USSD and Galaxy Tablets to open accounts in the field and deliver services

– A cash management solution for Cocoa buyers

– Integrated to eftPOS and the bank network

– Able to alleviate pressure on other bank channels

– A better customer experience which encourages banking and savings among the rural mass market

Mobile Banking Activity 2013

Mobile Banking Registrations 321,644

Unique Users Monthly 107,255

Total Transactions 6,813,610