the expanded role of investor relations: socially responsible investing, shareholder activism, and...

TRANSCRIPT

This article was downloaded by: [University of Newcastle (Australia)]On: 25 September 2014, At: 19:56Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registeredoffice: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

International Journal of StrategicCommunicationPublication details, including instructions for authors andsubscription information:http://www.tandfonline.com/loi/hstc20

The Expanded Role of InvestorRelations: Socially ResponsibleInvesting, Shareholder Activism, andOrganizational LegitimacyNur Uysalaa Marquette University, Milwaukee, Wisconsin, USAPublished online: 17 Jun 2014.

To cite this article: Nur Uysal (2014) The Expanded Role of Investor Relations: Socially ResponsibleInvesting, Shareholder Activism, and Organizational Legitimacy, International Journal of StrategicCommunication, 8:3, 215-230, DOI: 10.1080/1553118X.2014.905478

To link to this article: http://dx.doi.org/10.1080/1553118X.2014.905478

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the“Content”) contained in the publications on our platform. However, Taylor & Francis,our agents, and our licensors make no representations or warranties whatsoever as tothe accuracy, completeness, or suitability for any purpose of the Content. Any opinionsand views expressed in this publication are the opinions and views of the authors,and are not the views of or endorsed by Taylor & Francis. The accuracy of the Contentshould not be relied upon and should be independently verified with primary sourcesof information. Taylor and Francis shall not be liable for any losses, actions, claims,proceedings, demands, costs, expenses, damages, and other liabilities whatsoever orhowsoever caused arising directly or indirectly in connection with, in relation to or arisingout of the use of the Content.

This article may be used for research, teaching, and private study purposes. Anysubstantial or systematic reproduction, redistribution, reselling, loan, sub-licensing,systematic supply, or distribution in any form to anyone is expressly forbidden. Terms &Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

International Journal of Strategic Communication, 8: 215–230, 2014Copyright © Taylor & Francis Group, LLCISSN: 1553-118X print / 1553-1198 onlineDOI: 10.1080/1553118X.2014.905478

The Expanded Role of Investor Relations: SociallyResponsible Investing, Shareholder Activism, and

Organizational Legitimacy

Nur UysalMarquette University, Milwaukee, Wisconsin, USA

Investors increasingly use ownership rights to influence a corporation’s corporate social responsi-bility (CSR) practices and policies, challenging the traditional role of investor relations. However,shareholder activism with respect to CSR has thus far not received any scholarly attention in the fieldof strategic communication. This multidisciplinary study examines shareholder activism as a drivefor change in CSR behavior. Using a case study approach, the study analyzes a shareholder resolu-tion sponsored by NYC Public Pension Funds that resulted in an engagement process with CONSOLEnergy Inc. regarding environmental responsibility. As a result of the engagement process, the com-pany implemented a series of proactive procedural and structural changes. These findings suggestthat reactive responses to societal demands of shareholders can elicit more proactive measures inCSR behavior that the target company would not have enacted otherwise. Consequently, the paperargues that an expanded role of investor relations pushes corporations to meet or even exceed societalexpectations of a broader set of stakeholders. This change in practice ensures that corporations arecommitted to conducting socially desired actions in return for legitimacy in society.

Socially Responsible Investing (SRI)—an approach that integrates the three dimensions ofcorporate social responsibility (CSR), namely social, environmental, and economic responsibil-ities, into investment processes—has carved out a niche in the financial world in recent years.According to the recent report issued by Forum for Sustainable and Responsible Investment,socially responsible investing is currently estimated to contribute by $4 trillion to the $33.5 tril-lion total investment in the U.S. marketplace (US SIF, 2013). Motivated by the SRI movement,many shareholder activists attempt to influence corporate behavior by advocating for improvedCSR (Investor Responsibility Research Center, 2013).

Lee and Lounsbury (2011) referred to this type of shareholder activism on social and environ-mental issues as “social shareholder activism” (p. 156). As social shareholder activists believe thatcorporations must achieve more than financial profit, they voice their concerns, aiming to changeunjust and harmful corporate practices that affect the welfare of nonshareholding stakeholders.

In their dual role, social shareholder activists challenge corporations from within throughinstitutional mechanisms, such as filing shareholder resolutions. In the words of Weber, Rao,

Correspondence should be sent to Nur Uysal, Diederich College of Communication, Marquette University, P. O.Box 1881, Milwaukee, Wisconsin 53201-1881, USA. E-mail: [email protected]

Dow

nloa

ded

by [

Uni

vers

ity o

f N

ewca

stle

(A

ustr

alia

)] a

t 19:

56 2

5 Se

ptem

ber

2014

216 UYSAL

and Thomas (2009), these shareholders are “activists in the suits” rather than “activist in thestreets” (p. 106). Gillan and Starks (1998) argued that the shareholder activism arises whenshareholders are dissatisfied with the performance of the corporation. These scholars defineda shareholder activist as “an investor who tries to change the status quo through ‘voice,’ withouta change in the control of the firm” (p. 3). Pertinent literature suggests that shareholder activismcan facilitate the creation of legitimate agenda items in corporate decision-making processes(Agle, Mitchell, & Sonnefeld, 1999). According to Lee and Lounsbury (2011) and Logsdon andvan Buren (2008), it can also elicit changes in corporate policies and practices through volun-tary compliance. As such, shareholder activism for CSR has important social implications thatdeserve a theoretical explanation and an extensive examination from a strategic communicationperspective.

Being a stakeholder group that possesses power, legitimacy, and urgency (Mitchell, Agle, &Wood, 1997), shareholders are in a unique position, whereby they can voice society’s expecta-tions from within the corporations. However, shareholder activism is an area that has not receivedany scholarly attention in the field of communication. Indeed, strategic communication schol-ars have acknowledged the need for greater theory development efforts and more comprehensiveempirical inquiries (Botan & Hazleton, 2006; Laskin, 2009; Toth, 2010). Grounded in a societalperspective, this study aims to shed some light on the interactions between social shareholderactivists and target corporations.

The concept of organizational legitimacy will be used as a theoretical lens through whichcorporate responses to societal expectations of shareholders will be explored. Suchman (1995)defined organizational legitimacy as “the generalized perception” that the actions of an organi-zation are acceptable and desirable within a social system (p. 574). According to DiMaggio andPowell (1983), organizational legitimacy relies on the organization maintaining a network of sup-portive stakeholders with legitimacy-determining power. Thus, strategic communication, definedas the “purposeful use of communication by an organization to fulfill its mission,” is central toestablishing organizational legitimacy (Hallahan, Holtzhausen, van Ruker, Vercic, & Sriramesh,2007, p. 4). In this context, strategic communication can improve organizational ability to relatereflectively to the social environment (Bentele & Nothhaft, 2010; Zerfass, 2008).

This study examines shareholder activism as a drive for corporate change in CSR behavior.After a brief overview of the legal and procedural framework for shareholder activism, the studyanalyzes a case whereby a social shareholder resolution sponsored by NYC Pension Funds, alarge public pension fund in the United States, resulted in an engagement process with CONSOLInc., an American energy company. Moreover, the study demonstrates the ways in which thecompany responds to the proposed changes requested in the shareholder resolution. Given thatthe social activism by shareholders has expanded its scope in recent years, and the strategic com-munication in this process has gained significant importance (Kiefer, 2013; Lee & Lounsbury,2011), this study offers an important new venue for investor relations theory and research withinthe strategic communication domain.

Socially Responsible Investing and Shareholder Activism

Social shareholder activism is one of the main components of socially responsible investing(SRI)—an investment movement seeking to consider social good along with financial returns

Dow

nloa

ded

by [

Uni

vers

ity o

f N

ewca

stle

(A

ustr

alia

)] a

t 19:

56 2

5 Se

ptem

ber

2014

SOCIAL SHAREHOLDER ACTIVISM 217

(Guay, Doh, & Sinclair, 2004). The Forum for Sustainable and Responsible Investment—the U. S.membership association for professionals, corporations, institutions, and organizations engagedin socially responsible investing—describes SRI investment as follows:

SRI recognizes that corporate responsibility and societal concerns are valid parts of investment deci-sions. SRI considers both the investor’s financial needs and an investment’s impact on society. SRIinvestors encourage corporations to improve their practices on environmental, social, and governanceissues. (2013, para. 2)

SRI thus broadly refers to the financial investment that meets social, ethical (including religious),and environmental criteria. For example, Interfaith Center on Corporate Responsibility (ICCR),a coalition that represents 275 faith-based institutional investors, use investment assets accordingto the values of its members and thus acts as a vehicle to pressure corporations to behave respon-sibly. ICCR (2013) describes its mission as “through the lens of faith, ICCR builds a more justand sustainable world by integrating social values into investor actions” (Our Mission, para. 1).Socially responsible investors typically examine a company’s internal operating behavior (suchas employment policies and benefits), external practices (such as effects on the environment andindigenous people), and its product line (such as tobacco or defense equipment) to determinewhether they should invest in the company (Guay et al., 2004).

Socially responsible investing is a form of social movement that involves activism effortsaimed at influencing corporate behavior and policy-making through channeling or withdraw-ing investment (Weber et al., 2009). In public relations literature, activism is defined as theefforts to promote, hinder, or direct social, political, economic, or environmental change (Smith& Ferguson, 2010). Activists recognize issues earlier and pursue socially preferred resolutionsto these issues (Coombs & Holladay, 2012; Uysal & Yang, 2013). Likewise, by taking actionsinstead of selling their holdings, shareholder activists move beyond the norms of passivity tochange unjust and harmful corporate practices that affect the welfare of nonshareholding stake-holders (Rowley & Moldoveanu, 2003). Thus, social shareholder activism is a form of stakeholderactivism representing various social interests and goals.

The profile of social shareholder activists has proliferated in recent years (Gillan & Starks,2007). In particular, institutional shareholders—organizations that trade securities in largequantities—have increasingly started to engage with shareholder activism on various social andenvironmental issues (Smith, 2012). Institutional investors, such as pension funds and mutualfunds, are among corporations’ most significant shareholders. Thus, when they are dissatisfiedwith a particular corporation, they typically do not resort to selling their holdings in the corpora-tion, but rather attempt to influence the corporate decision-making processes through institutionalmechanisms.

Filing resolutions at corporations is one of the institutional mechanisms through which share-holder activists voice their concerns about social issues and draw public attention to these issues(Gillan & Starks, 1998). A social shareholder resolution can ask a company “to adopt a humanrights policy or to issue a report on how it plans to mitigate risk pertaining to greenhouse gasemissions” (Sjöström, 2008, p. 142). Shareholder resolutions thus provide a formal tool for share-holder activists to voice their societal concerns and exert pressure on corporations regarding theCSR issues.

Dow

nloa

ded

by [

Uni

vers

ity o

f N

ewca

stle

(A

ustr

alia

)] a

t 19:

56 2

5 Se

ptem

ber

2014

218 UYSAL

Shareholder Activism through Filing Resolutions

In the United States, for many decades, shareholders have been actively pressuring cor-porate management to address corporate governance and corporate social responsibilityissues. Institutionally, shareholder activism largely derives from the Securities and ExchangeCommission (SEC). Under Rule 14a-8 of the Securities Exchange Act of 1934 (ShareholderProposal Rule), any shareholder that continuously holds shares equivalent to $2000 of stock incorporation (or 1% of the equity market value) for at least one year is allowed to include oneresolution with a 500-word supporting statement in the proxy. The statement is required of acorporation when soliciting shareholder votes prior to its general shareholder meeting for all pro-posals to be voted upon by the shareholders. The SEC (2013) explains the function of a resolution,or a proposal, as the following:

A shareholder proposal is your recommendation or requirement that the company and/or its boardof directors take action, which you intend to present at a meeting of the company’s shareholders.Your proposal should state as clearly as possible the course of action you believe the company shouldfollow. (SEC, Shareholder Proposal, para. 1)

In essence, the shareholder resolution rule provides all shareholders with an institutionalmechanism through which to inform corporate boards on the issues—corporate governance orCSR—they consider important. When the target corporation receives the shareholder resolution,it can respond to the proposal in three ways: a) petition the SEC for the omission of the resolutionfrom the proxy; b) ignore the resolution and allow all shareholders vote on its merits at the generalmeeting; and c) engage with the shareholder activists who sponsored the resolution to discuss theproposed changes (Gillan & Starks, 2007). As such, corporate responses to social shareholderresolutions vary depending on corporate-, issue-, and sponsor-level factors. These variations canbe better understood within the typology of corporate responses to social issues (Clarkson, 1995).

Accordingly, corporations can respond to CSR issues either in a reactive, defensive, accom-modative, or proactive way. Under a reactive response, the corporation petitions the SEC toexclude the resolution from the proxy ballot by writing a no-action letter. Under a defensiveapproach, the corporation ignores the resolution and its sponsors and does not send it to theSEC for exclusion either. The resolution will then be included in the proxy ballot that disclosesimportant information about the issues to be voted at the corporation’s annual meeting. Corporatemanagement not only opposes to almost all shareholder resolutions that go to a vote, but also rec-ommends a “no” vote on resolutions in their proxy statement. Under an accommodative approach,the corporation chooses to engage in a conversation with the sponsors and agrees to take actions,often resulting in a withdrawal outcome.

Clearly, the three outcomes of social shareholder resolutions—omission, voting, andwithdrawal—are different with respect to assessing corporate responses to societal issues. Thewithdrawn resolutions suggest a sense of agreement through engagement whereas SEC omissionand proxy voting present more adversarial forms of engagement. However, in an environmentof heightened and networked stakeholder activism for CSR issues, a more proactive corporatestrategy is to anticipate responsibility and move beyond the expectations of not only shareholdersbut also a broader set of stakeholders. This shift in strategy can be achieved through an investorrelations function which is anchored in society.

Dow

nloa

ded

by [

Uni

vers

ity o

f N

ewca

stle

(A

ustr

alia

)] a

t 19:

56 2

5 Se

ptem

ber

2014

SOCIAL SHAREHOLDER ACTIVISM 219

Filing Shareholder Resolution as an Engagement Strategy

Shareholders generally withdraw resolutions from the ballot if they receive indication from thecorporate managers that desired actions on the issue outlined in the resolution would be taken(Carleton, Nelson, & Weisbach, 1998; Logsdon & van Buren, 2009). Academic and business, aswell as shareholder activist circles, tend to describe these ongoing interactions as a dialogue (see,for example, Investor Network on Climate Risk, 2013; Logsdon & van Buren, 2008). However,in public relations literature, dialogue refers to a “relational interaction” on an equal level (Kent& Taylor, 1998, p. 323). Furthermore, for a dialogue to exist, “parties must view communicatingwith each other as the goal of a relationship” (p. 324).

Clearly, the concept of dialogue in public relations literature does not refer to the formal inter-actions between shareholder activists and target corporations, during which the issue outlined inthe resolution is addressed. Instead, the term engagement in public relations means an attempt tocreate a conversation or communicate. Through this continuous communication process, organi-zations exchange conversations with their publics and reassess their policy and practice (Heath& Palenchar, 2009). Thus, in order to fully capture its meaning, this study refers to this formalprocess between shareholder activists and corporate management as engagement.

The engagement process starts with initial communication with corporations, often in the formof a shareholder letter, in which the concerns held by shareholder activists are raised. Such com-munication may work well in facilitating the engagement process on the social issue betweenshareholder activists and corporations and may last for a number of months (Logsdon & vanBuren, 2008). The subsequent withdrawal of a resolution, resulting from a shareholder activist-corporate engagement, generally indicates that some form of agreement has been reached oncorporate actions to address the social issue under consideration prior to proxy vote. GravesWaddock, and Rehbein (2001) observed that shareholder activists viewed withdrawal of theirresolutions as victories because “they typically only withdraw when management shows sincer-ity and legitimate commitment and progress to implement the requested change” (p. 296). Guayet al. (2004) noted, “the best possible outcome from a shareholder dialogue is that the companyagrees to substantial changes in practice” (p. 134). For this reason, communication researcherscan use withdrawn resolutions as an empirical setting to study the shareholder activist-corporateengagement process.

Organizational Legitimacy: A Theoretical Framework

Organizational legitimacy is a summative reflection of the relationship between an organizationand its environment. Parsons (1960) defined legitimacy as the “appraisal of action in terms ofshared or common values in the context of the involvement of the action in the social system”(p. 1975). Meyer and Rowan (1977) posited that meeting and adhering to the expectations ofa social system’s norms and values is the central element of legitimacy. Expanding on thisliterature, Suchman (1995) defined organizational legitimacy as “a generalized perspective orassumption that the actions of an entity are desirable, proper, or appropriate within sociallyconstructed system of norms, values, beliefs, and definitions” (p. 574).

Recognizing the perceptual and dynamic nature of organizational legitimacy, Suchman (1995)posited that stakeholder communication is the key to ensuring that the company receives public

Dow

nloa

ded

by [

Uni

vers

ity o

f N

ewca

stle

(A

ustr

alia

)] a

t 19:

56 2

5 Se

ptem

ber

2014

220 UYSAL

support. DiMaggio and Powell (1983) explained that, in order to ensure legitimacy, organiza-tions seek to establish congruence between the social values associated with, or implied by, theiractivities and the norms of acceptable behavior in the larger social system in which they operate.In sum, if the two value systems are congruent, organizational legitimacy is achieved.

Organizational legitimacy has strategic and institutional aspects (Deephouse & Suchman,2008; Suchman, 1995). The institutional aspect emphasizes the incorporation of societal expecta-tions into organizational policies and practices to ensure legitimacy and recognizes stakeholdersa source of pressure for change (DiMaggio & Powell, 1983; Sandhu, 2009). Consequently, orga-nizations are expected to change their structures or processes to conform to societal expectations.These institutional changes typically create both horizontal complexities, such as growing num-ber of job titles, occupational specialties, and increasing number of departments; and verticalcomplexities, such as increasing number of levels of authority within an organizational structure(Deephouse & Suchman, 2008).

For example, organizations develop boundary roles, allowing them to gain a sense of thesocial environment and implement changes in order to conform to the societal expectations andnorms (Aldrich & Herker, 1977). In the context of seeking and maintaining legitimacy, cre-ation of boundary spanning roles (e.g., affirmative action officers, CSR officers) is considered“an organization’s response to environmental influence” (Aldrich & Herker, 1977, p. 219). Raoand Sivakumar (1999) noted that the boundary spanning roles and structures signal the commit-ment of the organization to the accepted beliefs and values, and thus represent the organizationfavorably to the valued constituencies. Then, societal pressures exerted by shareholders—a pow-erful stakeholder group with legitimate claims (Mitchell et al., 1997)—are expected to induceinstitutional changes, such as creating new boundary spanning roles and structures within theorganization.

Although the institutional aspect of organizational legitimacy focuses on the organizationaladjustment to the social environment, the strategic aspect emphasizes the ways in which orga-nizations deploy symbols to garner societal support in their activities. Focusing on the cognitiveprocesses, strategic legitimacy views communication as a symbolic act intended to signal com-pliance (Meyer & Rowan, 1977). CSR reports are an example of this attempt. Similar to Boyd’s(2000) concept of actional legitimacy, strategic legitimacy is enacted through rhetorical tacticsengaged on a regular basis.

Proposing an integrative approach, Suchman (1995) argued that strategic and institutionalaspects of legitimacy are two sides of the same coin. From this perspective, the strategic approachis that of “corporations looking out of” their boundaries and working to secure legitimacy, whilethe institutional view is that of “society looking into” the corporation and imposing conditionsfor its legitimacy (p. 577). In response to societal pressures, “concrete institutional arrange-ments combine normative and cognitive processes together in varying amounts” (Deephouse &Suchman, 2008, p. 68). From a societal perspective, strategic communication plays a key role inthis context by improving organizational ability to relate reflectively to the social environment.

THE CASE: CONSOL ENERGY INC. AND NEW YORK CITY PENSION FUNDS

On November 25, 2008, Jerome Richey, the General Counsel and Corporate Secretary ofCONSOL Energy, Inc., received a shareholder letter from Thomas DiNapoli at New York City

Dow

nloa

ded

by [

Uni

vers

ity o

f N

ewca

stle

(A

ustr

alia

)] a

t 19:

56 2

5 Se

ptem

ber

2014

SOCIAL SHAREHOLDER ACTIVISM 221

Pension Funds (NYC Funds). In the letter, DiNapoli informed the company that the NYC Fundswere sponsoring a resolution on corporation’s responses to climate change (CONSOL EnergyInc. U. S. Securities and Exchange Commission Filings, 2009a). Attached to the letter was acopy of the resolution, in which a resolved clause was preceded by a series of whereas clausesthat discussed the importance of the issue and benefits of corporate disclosures. The resolvedclause stated:

RESOLVED: The proposal requests a report (reviewed by a board committee of independent direc-tors) on how the company responds to rising public pressure to significantly reduce the social andenvironmental harm associated with carbon dioxide emissions from the company’s operations andfrom the use of its primary products.

As such, the first step of shareholder activist-corporate engagement, known as “jawboning”(Carleton et al., 1998, p. 41), took place. The shareholder letter was sent to the corporation,explaining why the corporation was targeted and specifying the action the institution requests.Comptroller of the NYC Funds described the funds’ role in social shareholder activism as“pressuring many of America’s largest companies to improve workplace condition, protectthe environment, promote human rights abroad, and adhere to accepted corporate governancestandards” (New York City Public Pension Funds Fall Post Season Report, 2010, p. 17).

CONSOL Energy Inc. is headquartered in Pittsburg, Pennsylvania and employs over9,000 staff, generating $5,236 billion in revenue (CONSOL Energy Inc. Form 10-K, 2013). Thecompany first took an adversarial approach and filed a no-action letter to the SEC to excludethe resolution from its proxy materials through a private attorney (Davis, Letter to Division ofCorporate Finance SEC, December 30, 2008). In the nine-page letter, Attorney Davis explainedthat, under Rule 14a-8(i)(7), the SEC should grant the no-action relief for CONSOL because theresolution pertained to “an internal assessment of the risks or liabilities that the company facesas a result of its operations that may adversely affect the environment or the public’s health”(p. 4). Davis also provided several arguments by citing examples of the SEC’s previous no-actiondecisions.

The SEC responded to CONSOL’s no-action request, allowing the corporation to omit theNYC resolution from its proxy materials (CONSOL Energy Inc. U. S. Securities and ExchangeCommission Filings, 2009b). Consequently, the NYC Funds’ resolution requesting a report fromCONSOL Energy on how the corporation responded to climate change concerns was initiallyfound to be “an internal assessment” relating to ordinary business operations of the corporation.There was no engagement between the parties.

The NYC Funds filed the same resolution at CONSOL in the following year (CONSOLEnergy Inc. U.S. Securities and Exchange Commission Filings, 2010). This time, the resolu-tion was withdrawn by the NYC Funds before the annual meeting because CONSOL agreedto “adopt reforms to address risks long-term associated with climate change or poor environ-mental practices” and “provided substantial information on its R&D projects aimed at reducingcarbon emissions” (New York City Public Pension Funds Fall Post Season Report, 2010, p. 18).The NYC Funds subsequently announced the withdrawal outcome as an “achievement” underthe “Social and Environmental Issues-Shareholder Proposals” category of its 2010 Post SeasonReport.

Dow

nloa

ded

by [

Uni

vers

ity o

f N

ewca

stle

(A

ustr

alia

)] a

t 19:

56 2

5 Se

ptem

ber

2014

222 UYSAL

METHOD

In this research project, a case study approach was adopted, as it was deemed the most suit-able methodology for illuminating the process of shareholder activist-corporate engagement.Moreover, it enabled gaining a better understanding of the role of organizational legitimacyefforts in this process. Case study is an essential form of social science research that providesan intensive and systematic analysis of an individual unit, such as a person, an event, or an orga-nization (Wimmer & Dominick, 2006). This approach may involve several data sources, suchas documents, archival records, and artifacts, depending on the subject of the case study. Often,in studies of this type, focus is on a key case that can shed light on the research phenomena athand (Yin, 2011). This case study is guided by the explanation building approach that consistsof the construction of a description and illustration of the phenomenon under investigation—including causes, processes, and outcomes—based on the theoretical framework chosen to informthe phenomenon (Yin, 2011).

To analyze the shareholder activist-corporate engagement between NYC Pension Funds andCONSOL Energy, a textual analysis of the written correspondence—including three corpo-rate letters, one no-action letter, and two proxy statements—was conducted. Corporate filings(e.g., proxy statements, no-action letters) were obtained from the U.S. Securities and ExchangeCommission’s Electronic Data-Gathering, Analysis, and Retrieval (EDGAR) system. The proxystatement, also known as a Form DEF 14A, includes shareholder resolutions and must be filedwith SEC before the annual meeting.

In addition to the SEC filings, CONSOL’s strategic communication materials were analyzed.According to Mahoney (1991), CEO letters, annual reports, and sustainability reports are funda-mental components of financial public relations. For that reason, three CEO letters, three annualreports (2010–2012), and two sustainability reports (2011–2012) were included in the analysisperformed as a part of this study. The analysis also included the content published on the corpo-rate Website and its subsections, as well as news releases archived in the company’s electronicpressroom, found under the Investor Relations section of its Website. To assess media coveragein this process, a multiyear search (January 2009–August 2012) of the Factiva and Lexis/Nexisdatabases of news content was conducted. More specifically, documents in which “CONSOLEnergy” appeared in the headline and the lead paragraph of the story (along with “CSR,” “envi-ronmental sustainability,” or “climate change”) were selected for review. The specified period waschosen, as it covers the engagement process that started with the NYC Public Pension Funds’ let-ter to CONSOL Energy regarding the resolution. Finally, three news stories about the case wereadded to the data pool, as well as two interview transcripts conducted with CONSOL Energy’sKatharine Fredriksen, senior vice president of Environmental Strategy and Regulatory Affairs.

RESULTS

The research question guiding this study is how organizational legitimacy efforts play out in theengagement process between NYC Funds, an institutional investor group that filed a social reso-lution, and CONSOL Energy, the targeted corporation. The analysis showed that CONSOL hasimplemented a series of changes following the withdrawal agreement with NYC Funds in 2010.Most notably, in 2011, the company first created a new position in its organizational structure and

Dow

nloa

ded

by [

Uni

vers

ity o

f N

ewca

stle

(A

ustr

alia

)] a

t 19:

56 2

5 Se

ptem

ber

2014

SOCIAL SHAREHOLDER ACTIVISM 223

hired Katharine Fredriksen as senior vice president of Environmental Strategy and RegulatoryAffairs (Litvak, 2011). In her role, Fredriksen is responsible for the leadership, planning,direction, operation and strategy for environmental affairs, compliance, permitting, and relatedregulatory and legislative affairs within all business units of the company. Fredriksen seems topossess relevant academic and professional background for consulting the company on environ-mental issues, as she holds a bachelor’s degree in Marine Biology and has completed postgraduatework in Civil and Environmental Engineering. Before joining CONSOL, Fredriksen worked as aSenior Policy Advisor to the Secretary on environmental and energy issues at the U.S. Departmentof Treasury, as well as an Environmental Protection Specialist at the U.S. EnvironmentalProtection Agency (Forbes Profiles, 2013). In an interview with Pittsburg Business Journal,Fredriksen emphasized the importance of listening to “what CONSOL shareholders care about”and “what has the most impact on the company”:

We realize that our violations (both coal and gas divisions) were going up and not down. (Becauseof) that realization of going through this process, we’re elevating compliance. The focus has beenon environmental performance. Now a component of compensation relies on whether we achieveenvironmental performance (goals). (Litvak, 2012, para 4)

Fredriksen’s thus devised a plan of actions to achieve the company’s goal to be “a good stewardof the environment” (Gough, 2013, para. 3). On March 22nd, 2012, CONSOL Energy producedits first corporate responsibility report that summarized the corporate activities undertaken in2011. This initiative was publicized via a news release, in which Fredriksen announced, ”Weused the Global Reporting Initiative reporting principles in the development of this report andare purposefully investing time and effort to make sure we set ambitious targets suitable for ourbusiness and in line with our core value” (PRNewswire, 2012, para. 9).

The report outlined the company’s environmental responsibility activities, provided informa-tion on its greenhouse gas and air emissions, as well as included the metrics on coal and gasemission intensity (CONSOL Energy 2011 Corporate Responsibility Report). The Research andDevelopment (R&D) efforts aimed at developing strategic technology for business operationswith “smaller environmental footprints” (p. 49) were also outlined in the report. Brett Harvey, thecompany chairman, introduced the report in his CEO letter to public, stating:

CONSOL Energy’s first corporate social responsibility report has been created to clearly communi-cate who we are, what we believe, and how we conduct our business. Responsibility is a fundamentalprinciple that has driven CONSOL Energy’s actions since its inception nearly 150 years ago. Further,this report demonstrates just how strongly the company’s ethics and core values influence the busi-ness decisions CONSOL Energy makes every day. (CONSOL Energy 2011 Corporate ResponsibilityReport, Chairman & CEO Statement, para. 3)

In closing the letter, Harvey noted that this report would serve as “an invitation to a continuingdialogue with our partners, employees and the communities in which we operate” (CONSOLEnergy 2011 Corporate Responsibility Report, para. 6). In the content index of the report, it wasnoted that the report was based on the Global Reporting Initiative (GRI) guidelines. This wasconfirmed through a verification search on the GRI’s Disclosure Database for CONSOL Energy’sCorporate Social Responsibility Report, which indicated that the GRI’s G3.1 framework wasused.

Dow

nloa

ded

by [

Uni

vers

ity o

f N

ewca

stle

(A

ustr

alia

)] a

t 19:

56 2

5 Se

ptem

ber

2014

224 UYSAL

CONSOL published its second CSR Report, covering the corporate activities undertaken in2012 (PRNewswire, 2013). The 2012 report was more robust than its predecessor was, and fol-lowed the GRI’s G3.1 Reporting Guidelines by providing Profile Disclosures and ManagementApproach Disclosures, as well as 17 Performance Indicators. A verification search was once againconducted on the GRI’s Disclosure Database, indicating that the CONSOL’s 2012 CSR Reportwas reported at the B (medium) level. The report also provided more specific information on airand greenhouse gas emissions (CONSOL Energy 2012 Corporate Responsibility Report).

Indeed, further analysis of the report indicated that the company spent $267.4 million onenvironmental compliance. In addition, corporate R&D efforts focused on coordinated collab-oration aimed at replacing half of the typical diesel fuel requirements with natural gas (CONSOLEnergy 2012 Corporate Responsibility Report). Furthermore, the corporation actively soughtthird party endorsement. The company received a number of local and regional awards (e.g.,Virginia Reclamation Award) and recognitions for its environmentally responsible practices,which were extensively communicated to stakeholders (see, for example, Gough, 2013).

DISCUSSION

This study examined social shareholder activism and conducted a case study to gain an insightinto how a shareholder resolution sponsored by NYC Public Pension Funds has initiated anengagement process with CONSOL Energy regarding an environmental responsibility issue.Overall, the findings showed that reactive corporate responses to societal demands of share-holder activists elicited a series of progressive changes in corporate social responsibility behavior.A number of theoretical and practical implications have emerged in relation to the investorrelations function.

A Societal View to Investor Relations: The Case of Social Shareholder Activism

Organizational theory scholars assert that changing social norms and expectations voiced bystakeholders constitute a source of pressure for organizations to maintain legitimacy throughorganizational adjustment (DiMaggio & Powell, 1983; Meyer & Rowan, 1977). The findings ofthe case study showed that CONSOL Energy not only produced its first CSR report, as it wasdemanded in the shareholder resolution, but it also created a new position titled EnvironmentalStrategy and Regulatory Affairs, which was filled by a highly qualified person, capable of proac-tively addressing environmental issues. These findings suggest that reactive corporate responsesto societal demands of shareholders may induce other, more proactive, outcomes.

Shareholder resolutions on societal issues function as an early, internal warning system thatallows organizations to address issues proactively. Rehbein, Waddock, and Graves (2004) arguedthat shareholder resolutions can “identify and define problems for firms and thereby signal anemerging gap between a corporation’s polices and stakeholder demands” (p. 242). Sjöström(2008) viewed shareholder activism as “the canary in the coal mine” (p. 146), suggesting thatsocial shareholder resolutions cue corporations on the socially desired actions. Social shareholderactivism can thus help organizations narrow the legitimacy gap, which arises due to discrepancybetween an organization’s actions and society’s expectations of this organization (Sethi, 1979).If the issues that shareholders voiced in the resolutions are not handled well, they can evolve

Dow

nloa

ded

by [

Uni

vers

ity o

f N

ewca

stle

(A

ustr

alia

)] a

t 19:

56 2

5 Se

ptem

ber

2014

SOCIAL SHAREHOLDER ACTIVISM 225

into crisis (Heath & Palenchar, 2009). In such cases, shareholder activists tend to bring the issueto the attention of the media. In addition, they seek alliances with other stakeholder groups—including activists, customers, and governmental agencies—in order to strengthen their positionand increase their pressure on corporate management (MacLeod, 2009).

Therefore, reactive responses to societal demands of shareholders can trigger more proactivemeasures that the target company would not have enacted otherwise. This dynamic places agreater pressure on shareholder activists to elicit progressive changes in organizations throughengagement. It also suggests a greater responsibility for the investor relations function, as itis required to facilitate the engagement process between shareholder activists and corporatemanagements and mediate their different rationalities.

Shareholder activism for societal issues provides an excellent context in which the interests ofshareholders and nonshareholding stakeholders are aligned for the greater societal good. Socialshareholder activism has thus challenged a previous understanding of shareholders as a homoge-nous, static group with a single motivation of maximizing profit. Indeed, a significant weaknessin the current understanding of investor relations lies in the conception of discrete, dyadic rela-tionship between the organization and its shareholders—a view prevalent in the managementliterature (e.g., Clarkson, 1995; Freeman, 1984).

This perspective does not capture the potential complex interactions within the broader net-work of organization-stakeholder relationships. In the CSR contexts, in particular, stakeholdersoften interact, cooperate, and form alliances with other stakeholders, including shareholders. Forexample, a shareholder group may seek support of other, more powerful, shareholder groups inorder to increase its bargaining power and enhance the salience of the issue under consideration(MacLeod, 2009). Additionally, recognition of the specific roles of particular shareholder groups,such as SRI funds, provides further understanding of the multifaceted relationships that have beenobscured by the traditional understanding.

Given the complex and nuanced relationships between investors and organizations, furtherdevelopment of investor relations theory can benefit from a societal perspective. Several issuesshould be considered: (1) shareholders are not a homogenous group; (2) shareholder groupscan sometimes compete against and sometimes complement each other; (3) shareholders mayform strategic alliances, or cooperate, to increase the persuasive power of their combined claim;and, (4) shareholders’ potential to influence other shareholders and the organization is oftendetermined by the particular nature of their role.

An Integrative Approach to Organizational Legitimacy: The Role of Communication

The findings reported here indicate that, given the complex and nuanced relationships betweenshareholders and corporations, the concept of organizational legitimacy—a central concept in thefields of strategic communication and management as well as sociology—could enrich the the-orizing efforts in investor relations. Indeed, strategic communication is essential for establishingorganizational legitimacy. In line with Suchman’s (1995) integrative approach, CONSOL under-took both institutional and strategic legitimacy efforts in response to NYC Funds’ concerns aboutclimate change.

Moving beyond the expectations, CONSOL first implemented a structural change by creatinga new position titled Environmental Strategy and Regulatory Affairs—a boundary-spanning role(Aldrich & Heker, 1977; Rao & Sivakumer, 1999). This initiative was an institutional legitimacy

Dow

nloa

ded

by [

Uni

vers

ity o

f N

ewca

stle

(A

ustr

alia

)] a

t 19:

56 2

5 Se

ptem

ber

2014

226 UYSAL

effort to increase the organization’s perceived competence and responsibility to publics’ interests(Boyd, 2000). On the other hand, as part of its strategic legitimacy efforts, CONSOL undertookseveral symbolic acts intended to signal compliance. The company produced its first CSR reportto indicate its conformity to the desirable standards (Schultz & Wehmeier, 2010). Further, thecompany sought third party endorsements by obtaining awards and certifications regarding itsenvironmental responsibility (Deephouse & Suchman, 2008). CONSOL used rhetorical tactics tocommunicate the changes undertaken at the organization (Boyd, 2000).

Hallahan et al. (2007) noted that strategic communication concerns “the strategic applicationof communication and how an organization functions as a social actor to advance its mission”(p. 7). Therefore, strategic communication enabled the stakeholders to evaluate the organization’sconformity to the acceptable standards, and thereby determine its legitimacy. More importantly,the engagement process with the NYC Funds resulted in a withdrawal agreement and helpedthe company reflect on its environmental practices. As Heath (2006) argued that the dialogue ofsociety is best when it helps organizations be more reflective and work for legitimacy.

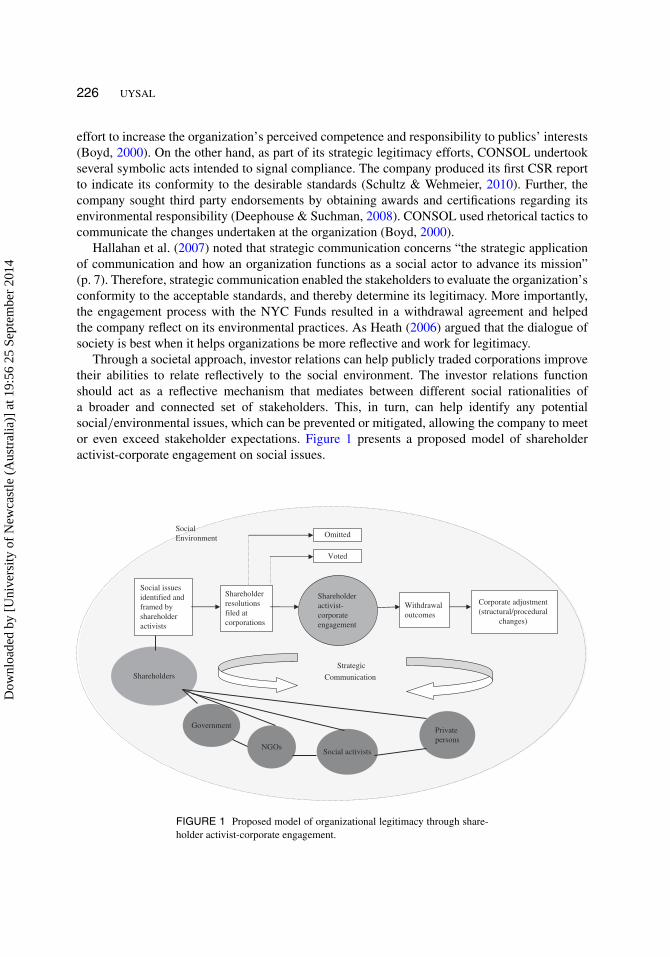

Through a societal approach, investor relations can help publicly traded corporations improvetheir abilities to relate reflectively to the social environment. The investor relations functionshould act as a reflective mechanism that mediates between different social rationalities ofa broader and connected set of stakeholders. This, in turn, can help identify any potentialsocial/environmental issues, which can be prevented or mitigated, allowing the company to meetor even exceed stakeholder expectations. Figure 1 presents a proposed model of shareholderactivist-corporate engagement on social issues.

Social issues identified and framed by shareholder activists

Shareholder resolutions filed at corporations

Corporate adjustment (structural/procedural

changes)

Withdrawal outcomes

Shareholder activist-corporate engagement

Social Environment

Strategic

Communication

Government

NGOs

Private persons

Shareholders

Social activists

Omitted

Voted

FIGURE 1 Proposed model of organizational legitimacy through share-holder activist-corporate engagement.

Dow

nloa

ded

by [

Uni

vers

ity o

f N

ewca

stle

(A

ustr

alia

)] a

t 19:

56 2

5 Se

ptem

ber

2014

SOCIAL SHAREHOLDER ACTIVISM 227

In this context, the role of investor relations is to reach agreements on mutually acceptablesocial expectations shaped by a broader set of stakeholders through engagement. By adoptingthis approach, corporations can be fully cognizant of the societal norms and expectations. Moreimportantly, they can ensure that the public is aware of their firm commitment to conductingsocially desired actions in return for legitimacy in society.

This case study is notable in that it is one of the first attempts to analyze the manner in whichorganizations seek legitimacy in the context of social shareholder activism from a strategic com-munication perspective. Thus, its findings lay the groundwork for future research in financialstrategic communication. Presently, research in the field of shareholder activism for corporatesocial and environmental responsibility is at initial stages, as evidenced by the marked paucityof published articles in management and business ethics journals (e.g., Strategic ManagementJournal, Journal of Business Ethics, and Business & Society).

As this study has demonstrated, an interdisciplinary body of knowledge in strategic commu-nication can improve our understanding of shareholder activism. Future research in this fieldshould examine how shareholder activists use strategic communication to interact, corporate, andform alliances with other shareholders, as well as with nonshareholding stakeholders. In partic-ular, new communication technologies have enabled shareholder activist organizations to formnetworks of alliances that were previously not feasible (MacLeod, 2009). As You Sow, for exam-ple, an online shareholder advocacy group, launches many social media campaigns to influenceCSR practices. Future research should examine the nature of corporation-issue-sponsor triplet toexplore the variations in corporate responses to social shareholder resolutions.

ACKNOWLEDGMENTS AND FUNDING

This article is a part of a larger research project on shareholder activism for corporate socialresponsibility. The author would like to thank Alexander Laskin and the anonymous reviewerswhose invaluable comments guided the revision of this article. The author also would like tothank Katerina Tsetsura, Maureen Taylor, Michael Kent, and Sarah Bonewits Feldner for theirinsightful comments. This article received research funding from The Greater Milwaukee JournalFoundation / Walter Jay and Clara Charlotte Damm Fund.

REFERENCES

Agle, B. R., Mitchell, R. K., & Sonnefeld, J. A. (1999). Who matters to CEOs? An investigation of stakeholder attributesand salience, corporate performance, and CEO values. Academy of Management Journal, 42, 507–525.

Aldrich, H. E., & Herker, D. (1977). Boundary spanning roles and organization structure. Academy of ManagementReview, 2, 217–230.

Bentele, G., & Nothhaft, H. (2010). Strategic communication and the public sphere from a European perspective.International Journal of Strategic Communication, 4, 93–116.

Botan, C. H., & Hazleton, V. (2006). Public relations in a new age. In C. Botan & V. Hazelton (Eds.), Public relationstheory II (pp. 1–18). Mahwah, NJ: Lawrence Erlbaum.

Boyd, J. (2000). Actional legitimation: No crisis necessary. Journal of Public Relations Research, 12, 341–353.Carleton, W. T., Nelson, J. M., & Weisbach, M. S. (1998). The influence of institutions on corporate governance through

private negotiations: Evidence from TIAA-CREF. The Journal of Finance, 53(4), 1335–1362.

Dow

nloa

ded

by [

Uni

vers

ity o

f N

ewca

stle

(A

ustr

alia

)] a

t 19:

56 2

5 Se

ptem

ber

2014

228 UYSAL

Clarkson, M. E. (1995). A stakeholder framework for analyzing and evaluating corporate social performance. Academyof Management Review, 20(1), 92–117.

CONSOL Energy 2011 Corporate Responsibility Report. Retrieved from http://consolenergy.com/CorporateResponsibilityReport/2011New/index.html

CONSOL Energy 2012 Corporate Responsibility Report. Retrieved from http://consolenergy.com/CorporateResponsibilityReport/2012New/index.html

CONSOL Energy Inc. Form 10-K. (2013). United States Securities and Exchange Commission Form 10-K. Retrievedfrom http://www.sec.gov/Archives/edgar/data/1070412/000119312513046119/d483833d10ka.htm

CONSOL Energy Inc. U. S. Securities and Exchange Commission Filings. (2009a). New York City PublicPension Funds shareholder letter. Retrieved from http://www.sec.gov/divisions/corpfin/cf-noaction/14a-8/2009/nyccomptroller022709-14a8.pdf

CONSOL Energy Inc. U. S. Securities and Exchange Commission Filings. (2009b). No-action letter to New York CityPublic Pension Funds Shareholder Resolution. Retrieved from http://www.sec.gov/divisions/corpfin/cf-noaction/14a-8/2009/nyccomptroller022709-14a8.pdf

CONSOL Energy Inc. U.S. Securities and Exchange Commission Filings. (2010). New York City PublicPension Funds shareholder resolution. Retrieved from http://www.sec.gov/divisions/corpfin/cf-noaction/14a-8/2010/nyccomptroller022309-14a8.pdf

Coombs, W. T., & Holladay, S. J. (2012). Fringe public relations: How activism moves critical pr toward the mainstream.Public Relations Review, 38, 880–887.

Deephouse, D. L., & Suchman, M. (2008). Legitimacy in organizational institutionalism. In R. Greenwood, C. Oliver, R.Suddaby, & K. Sahlin-Anderson (Eds.), The Sage handbook of organizational institutionalism (pp. 49–77). ThousandOaks, CA: Sage.

DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality inorganizational fields. American Sociological Review, 48, 147–160.

Forbes Profiles. (2013). Fredriksen, K. Retrieved from http://www.forbes.com/profile/fredriksen/Forum for Sustainable and Responsible Investment. (2013). Socially responsible investing facts. Retrieved from

http://www.ussif.org/sribasicsFreeman, R. E. (1984). Strategic management: A stakeholder approach. New York, NY: Cambridge University Press.Gillan, S. L., & Starks, L. T. (1998). A survey of shareholder activism: motivation and empirical evidence. Contemporary

Finance Digest, 2, 10–34.Gillan, S. L., & Starks, L. T. (2007). The evolution of shareholder activism in the United States. Journal of Applied

Corporate Finance, 19, 557–3.Gough, P. J. (2013, March). CONSOL wins two environmental cleanup. Pittsburgh Business Times Awards. Retrieved

from http://www.bizjournals.com/pittsburgh/print-edition/2012/04/20/katharine-fredriksen-consol-energy-inc.htmlGraves, S. B., Waddock, S., & Rehbein, K. (2001). Fad and fashion in shareholder activism: The landscape of shareholder

resolutions. Business and Society Review, 106, 293–314.Guay, T., Doh, J. P., & Sinclair, G. (2004). Non-governmental organizations, shareholder activism, and socially

responsible investments: Ethical, strategic, and governance implications. Journal of Business Ethics, 52, 125–139.Hallahan, K., Holtzhausen, D., van Ruler, B., Vercic, D., & Sriramesh, K. (2007). Defining strategic communication.

International Journal of Strategic Communication, 1, 3–35.Heath, R. L. (2006). Onward into more fog: Thoughts on public relations’ research directions. Journal of Public Relations

Research, 18, 93–114.Heath, R. L., & Palenchar, M. J. (2009). Strategic issues management: Organizations and public policy challenges.

Thousand Oaks, CA: Sage.Interfaith Center on Corporate Responsibility (ICCR). (2013). Interfaith Center on Corporate Responsibility. Retrieved

from http://www.iccr.orgInvestor Network on Climate Risk. (2013). Corporate dialogues. Retrieved from http://www.ceres.org/incr/engagement/

corporate-dialogues.Investor Responsibility Research Center. (2013). Mission. Retrieved from http://irrcinstitute.org/about.php?page=

mission&nav=2Kent, M. L., & Taylor, M. (1998). Building dialogic relationships through the World Wide Web. Public Relations Review,

24, 321–334.

Dow

nloa

ded

by [

Uni

vers

ity o

f N

ewca

stle

(A

ustr

alia

)] a

t 19:

56 2

5 Se

ptem

ber

2014

SOCIAL SHAREHOLDER ACTIVISM 229

Kiefer, P. (2013). Proactive comms key for rise in shareholder activism. PRWeek. Retrieved from http://www.prweekus.com/proactive-comms-key-for-rise-in-shareholder-activism/article/276385/

Laskin, A. V. (2009). A descriptive account of the investor relations profession: A national study. Journal of BusinessCommunication, 46, 208–233.

Lee, M. P., & Lounsbury, M. (2011). Domesticating radical rant and rage: An exploration of the consequences ofenvironmental shareholder resolutions on corporate environmental performance. Business and Society, 50, 155–188.

Litvak, A. (2011, December 30). New faces in the Burgh: Katharine Fredrikson, CONSOL Energy Inc. PittsburghBusiness Times. Retrieved from http://www.bizjournals.com/pittsburgh/print-edition/2011/12/30/katharine-fredriksen-consol-energy-inc.html

Litvak, A. (2012, April 20). Five minutes with Katharine Fredrikson, CONSOL Energy Inc. Pittsburgh Business Times.Retrieved from http://www.bizjournals.com/pittsburgh/print-edition/2012/04/20/katharine-fredriksen-consol-energy-inc.html?page=all

Logsdon, J. M., & van Buren, H. J. (2008). Justice and large corporations: What do activist shareholders want? Business& Society, 47, 523–548.

MacLeod, M. (2009). Emerging investor networks and the construction of corporate social responsibility. Journal ofCorporate Citizenship, 34, 69–96.

Mahoney, W. F. (1991). Investor relations: The professional’s guide to financial marketing and communications. NewYork, NY: New York Institute of Finance.

Meyer, J. W., & Rowan, B. (1977). Institutional organizations: Formal structures as myth and ceremony. American Journalof Sociology, 80, 340–363.

Mitchell, R. K., Agle, B. R., & Wood, D. J. (1997). Toward a theory of stakeholder identification and salience: Definingthe principle of who and what really counts. Academy of Management Review, 22, 853–886.

New York City Public Pension Funds Fall Post Season Report. (2010). Retrieved from http://www.comptroller.nyc.gov/bureaus/bam/corp_gover_pdf/2010-Shareholder-report.pdf

Parsons, T. (1960). Structure and process in modern societies. New York, NY: Free Press.PRNewswire (2012). CONSOL Energy publishes 2011 Corporate Social Responsibility Report. Retrieved from http://

www.prnewswire.com/news-releases/consol-energy-publishes-2011-corporate-responsibility-report-144267855.htmlRao, H., & Sivakumar, K. (1999). Institutional sources of boundary spanning structures: The establishment of investor

relations departments in the Fortune 500 industrials. Organizational Science, 10, 27–42.Rehbein, K., Waddock, S., & Graves, S. B. (2004). Understanding shareholder activism: Which corporations are targeted?

Business and Society, 43, 239–267.Rowley, T. J., & Moldoveanu, M. (2003). When will stakeholders groups act? An interest and identity model of

stakeholder group mobilization. Academy of Management Review, 28, 204–219.Sandhu, S. (2009). Strategic communication: An institutional perspective. International Journal of Strategic

Communication, 3, 72–92.Schultz, F., & Wehmeier, S. (2010). Institutionalization of corporate social responsibility within corporate commu-

nications: combining institutional, sensemaking and communication perspectives. Corporate Communications: AnInternational Journal, 15, 9–29.

Securities and Exchange Commission (SEC). (2013). Shareholder proposals. Retrieved from http://www.sec.gov/interps/legal/cfslb14.htm

Sethi, S. P. (1979). A conceptual framework for environmental analysis of social issues and evaluation of businessresponse patterns. Academy of Management Review, 4, 63–74.

Sjöström, E. (2008). Shareholder activism for corporate social responsibility: What do we know? SustainableDevelopment, 16, 141–154.

Smith, M. P. (2012). Shareholder activism by institutional investors: Evidence from CalPERS. Journal of Finance, 51,227–232.

Smith, M., & Ferguson, D. (2010). Activism 2.0. In R. Heath (Ed.), Handbook of public relations (pp. 395–408), ThousandOaks, CA: Sage.

Suchman, M. C. (1995). Managing legitimacy: Strategic and institutional approaches. Academy of Management Review,20, 571–610.

Toth, E. (2010). Reflections on the field. In R. L. Heath (Ed.), Handbook of public relations. (pp. 689–715). ThousandOaks, CA: Sage.

US SIF: The Forum for sustainable and responsible investment (2013). Programs. Retrieved from http://www.ussif.org/

Dow

nloa

ded

by [

Uni

vers

ity o

f N

ewca

stle

(A

ustr

alia

)] a

t 19:

56 2

5 Se

ptem

ber

2014

230 UYSAL

Uysal, N., & Yang, A. (2013). The power of activist networks in the mass self-communication era: A triangulation studyof the impact of WikiLeaks on the stock value of Bank of America. Public Relations Review, 39, 459–469.

Weber, K., Rao, H., & Thomas, L. G. (2009). From streets to suites: How the antibiotech movement affected Germanpharmaceutical firms. American Sociological Review, 74, 106–127.

Wimmer, R. D., & Dominick, J. R. (2006). Mass media research: An introduction (8th ed.). Boston, MA: Wadsworth.Yin, R. K. (2011). Applications of case study research. Thousand Oaks, CA: Sage Publications.Zerfass, A. (2008). Corporate communication revisited: Integrating business strategy and strategic communication. In A.

Zerfass, A. van Ruler, & K. Sriramesh (Eds.) Public Relations Research: European and International Perspectivesand Innovations (pp. 65–96). Wiesbaden, Germany: VS Verlag fur Socialwissenschaften.

Dow

nloa

ded

by [

Uni

vers

ity o

f N

ewca

stle

(A

ustr

alia

)] a

t 19:

56 2

5 Se

ptem

ber

2014