the debt trap ©2006 dr. b. c. paul. debt tends to lower money available for other things money...

TRANSCRIPT

The Debt TrapThe Debt Trap

©2006 Dr. B. C. Paul©2006 Dr. B. C. Paul

Debt Tends to Lower Money Debt Tends to Lower Money Available for Other ThingsAvailable for Other Things

Money Earned = Taxes Paid + Money Earned = Taxes Paid + Interest Paid + Food/Clothing/Shelter Interest Paid + Food/Clothing/Shelter + Items Purchased + Services + Items Purchased + Services Purchase + Savings/InvestmentsPurchase + Savings/Investments

The trap is that people sell their The trap is that people sell their lifetime of goods and services for lifetime of goods and services for wants nowwants now

Interest Paid reduces money Interest Paid reduces money available for other thingsavailable for other things

Can You Ever Win With Debt?Can You Ever Win With Debt?

Two Things normally will win.Two Things normally will win. EducationEducation

• College graduates average 23K/year more!College graduates average 23K/year more!• If you raise the money earned side faster than the If you raise the money earned side faster than the

interest paid side you win – education normally interest paid side you win – education normally doesdoes

Dark side – one of the reasons States are burying tax Dark side – one of the reasons States are burying tax increases by targeting students with cuts to higher increases by targeting students with cuts to higher education grants and appropriationseducation grants and appropriations

• If you pay student loans at currently common If you pay student loans at currently common terms over 30 years you will pay 218% of what terms over 30 years you will pay 218% of what you borrowyou borrow

Ie – you pay back $36,000 for $16,500 average student Ie – you pay back $36,000 for $16,500 average student loan debtloan debt

Observations About Education Observations About Education DebtDebt

19,500 in interest for $23,000/year is 19,500 in interest for $23,000/year is a no brainer buta no brainer but• Its enough to make one rethink their Its enough to make one rethink their

college expensescollege expenses Do you need extras at 218% of list price?Do you need extras at 218% of list price? Not working for $8/hour – but what about Not working for $8/hour – but what about

$17/hour$17/hour Do you need the nicest apartment?Do you need the nicest apartment? Is the spring break vacation worth it?Is the spring break vacation worth it? How easy should you take it in the summer?How easy should you take it in the summer?

A Second WinA Second Win Buy a HouseBuy a House

• Interest raises cost without raising incomeInterest raises cost without raising income• But if cost of housing falls more interest rises you still But if cost of housing falls more interest rises you still

win.win. How can you win buying?How can you win buying?

• Most housing is financed through creditMost housing is financed through credit You pay landlords interest as part of your rentYou pay landlords interest as part of your rent Rental units usually have a higher rate of interest than Rental units usually have a higher rate of interest than

private homesprivate homes Most rental businesses look for a profit above costsMost rental businesses look for a profit above costs Rental rates rise with value of property – home ownership Rental rates rise with value of property – home ownership

locks in payments at the value when you buy.locks in payments at the value when you buy.• Most housing pays property taxMost housing pays property tax

Most rental units pay a higher rate of property tax than Most rental units pay a higher rate of property tax than private homesprivate homes

Your Landlords ExpensesYour Landlords Expenses

Landlords need to cover vacancy costsLandlords need to cover vacancy costs• They don’t eat the cost of vacant units They don’t eat the cost of vacant units

themselvesthemselves The default rate on renters is higher than The default rate on renters is higher than

the default rate of homeowners and renters the default rate of homeowners and renters leave little to recoverleave little to recover• You pay the costYou pay the cost

Some people will take pride in ownership – Some people will take pride in ownership – you pay the cost for the average personyou pay the cost for the average person• Even if you do take good care of your apartmentEven if you do take good care of your apartment

CaveatsCaveats Real Estate markets are localReal Estate markets are local

• If speculation has over-priced housing losses can occurIf speculation has over-priced housing losses can occur• Weak local economies diminish your ability to sellWeak local economies diminish your ability to sell

Loan Set-up and closing costs plus selling costs Loan Set-up and closing costs plus selling costs will often be higher than equity built in 3 to 5 will often be higher than equity built in 3 to 5 yearsyears• Buying may not save if you move around a lotBuying may not save if you move around a lot

Home ownership is part of a lifestyle choiceHome ownership is part of a lifestyle choice• Being a slave to your money may not bring happinessBeing a slave to your money may not bring happiness

Other Possible Wins?Other Possible Wins? If your investment grows faster than the If your investment grows faster than the

interest on debt used to finance it you interest on debt used to finance it you come out aheadcome out ahead• Of course market timing and even stock Of course market timing and even stock

picking is more speculative than most thinkpicking is more speculative than most think A possible retirees suggestionA possible retirees suggestion

• Sell a home that may grow in value at 2 to 5% Sell a home that may grow in value at 2 to 5% per year and invest in higher growth optionper year and invest in higher growth option

If your rent grows 2% per year and your money If your rent grows 2% per year and your money grows at 8% the difference might finance your grows at 8% the difference might finance your retirement in partretirement in part

Recognize the idea of beating the market Recognize the idea of beating the market always carries risk of things turning the always carries risk of things turning the other wayother way

Opportunity CostOpportunity Cost

True cost of something is measured by True cost of something is measured by what it does to the whole financial picturewhat it does to the whole financial picture• Remember the Landmine about investing $5 in Remember the Landmine about investing $5 in

a 50% return investment and blowing the a 50% return investment and blowing the handling of 5 million dollarshandling of 5 million dollars

• For almost all people money is finiteFor almost all people money is finite A decision to do one thing almost always means a A decision to do one thing almost always means a

decision not to do something elsedecision not to do something else Remember favorite pony minus other pony?Remember favorite pony minus other pony?

• We constantly spend on one thing vs anotherWe constantly spend on one thing vs another• The value of the cash flow we pick vs. the other The value of the cash flow we pick vs. the other

opportunity is our opportunity cost.opportunity is our opportunity cost.

The Revolving Credit CardThe Revolving Credit Card

We can go to Macy’s and buy an We can go to Macy’s and buy an outfit for $250.outfit for $250.• Is the cost $250?Is the cost $250?

Suppose we use a credit card and Suppose we use a credit card and just revolve the balancejust revolve the balance• Ie we carry a balance pay down $250 Ie we carry a balance pay down $250

and promptly go spend a new $250and promptly go spend a new $250• Under new guidelines most credit cards Under new guidelines most credit cards

are calling for 1% of the balance plus are calling for 1% of the balance plus interest and any feesinterest and any fees

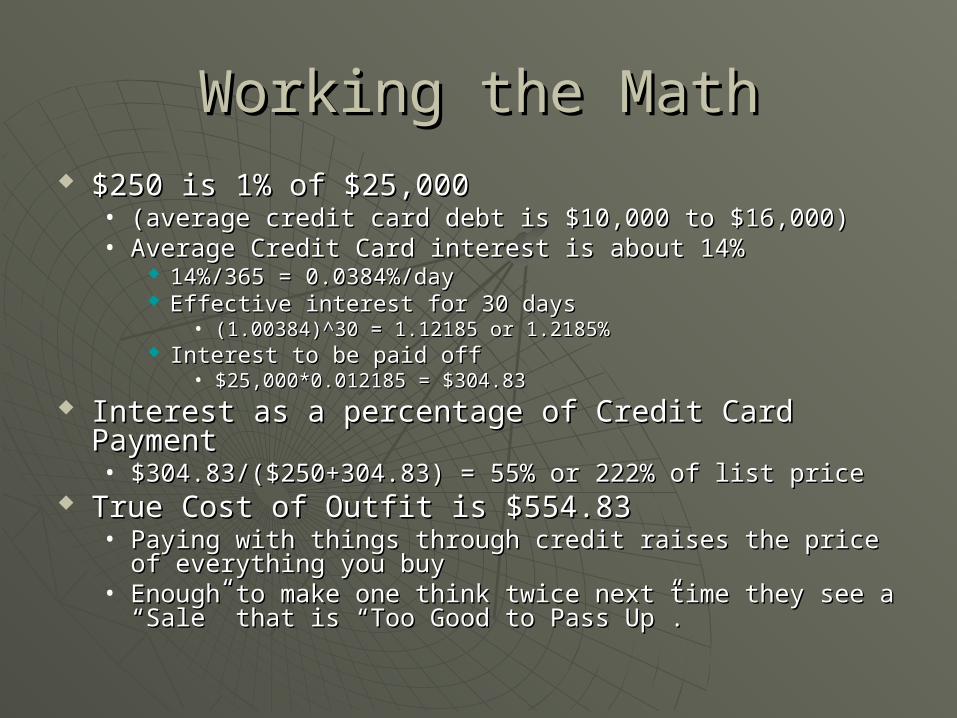

Working the MathWorking the Math $250 is 1% of $25,000$250 is 1% of $25,000

• (average credit card debt is $10,000 to $16,000)(average credit card debt is $10,000 to $16,000)• Average Credit Card interest is about 14%Average Credit Card interest is about 14%

14%/365 = 0.0384%/day14%/365 = 0.0384%/day Effective interest for 30 daysEffective interest for 30 days

• (1.00384)^30 = 1.12185 or 1.2185%(1.00384)^30 = 1.12185 or 1.2185% Interest to be paid offInterest to be paid off

• $25,000*0.012185 = $304.83$25,000*0.012185 = $304.83 Interest as a percentage of Credit Card PaymentInterest as a percentage of Credit Card Payment

• $304.83/($250+304.83) = 55% or 222% of list price$304.83/($250+304.83) = 55% or 222% of list price True Cost of Outfit is $554.83True Cost of Outfit is $554.83

• Paying with things through credit raises the price of Paying with things through credit raises the price of everything you buyeverything you buy

• Enough to make one think twice next time they see a Enough to make one think twice next time they see a “Sale” that is “Too Good to Pass Up”.“Sale” that is “Too Good to Pass Up”.

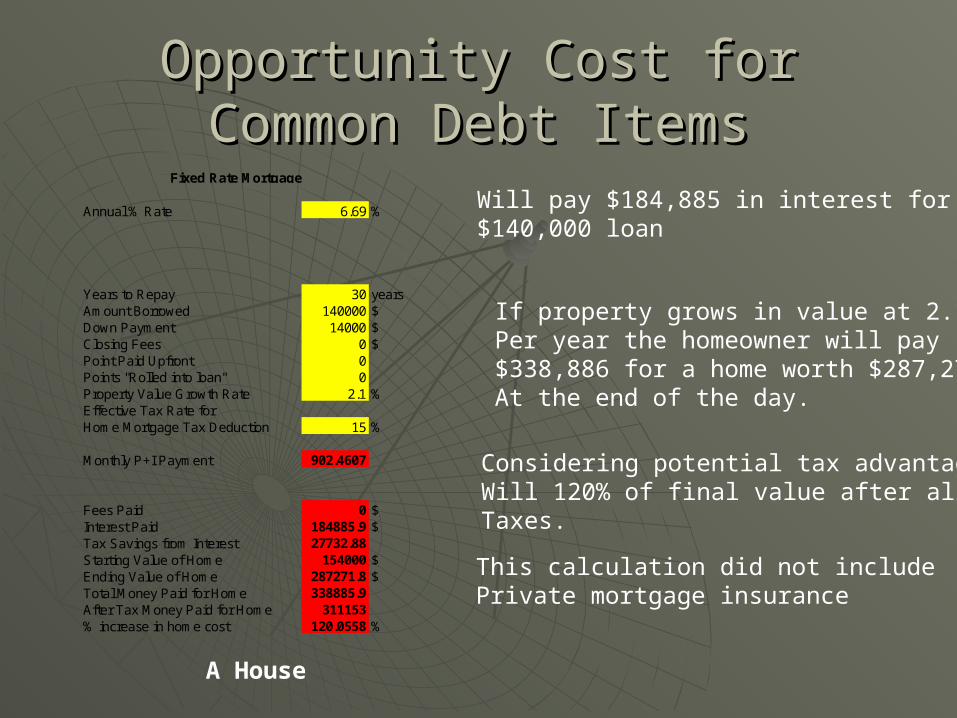

Opportunity Cost for Common Debt Opportunity Cost for Common Debt ItemsItems

Fixed Rate Mortgage

Annual % Rate 6.69 %

Years to Repay 30 yearsAmount Borrowed 140000 $Down Payment 14000 $Closing Fees 0 $Point Paid Upfront 0Points "Rolled into loan" 0Property Value Growth Rate 2.1 %Effective Tax Rate forHome Mortgage Tax Deduction 15 %

Monthly P+I Payment 902.4607

Fees Paid 0 $Interest Paid 184885.9 $Tax Savings from Interest 27732.88Starting Value of Home 154000 $Ending Value of Home 287271.8 $Total Money Paid for Home 338885.9After Tax Money Paid for Home 311153% increase in home cost 120.0558 %

Will pay $184,885 in interest for a$140,000 loan

If property grows in value at 2.1%Per year the homeowner will pay$338,886 for a home worth $287,272At the end of the day.

Considering potential tax advantagesWill 120% of final value after allTaxes.

A House

This calculation did not includePrivate mortgage insurance

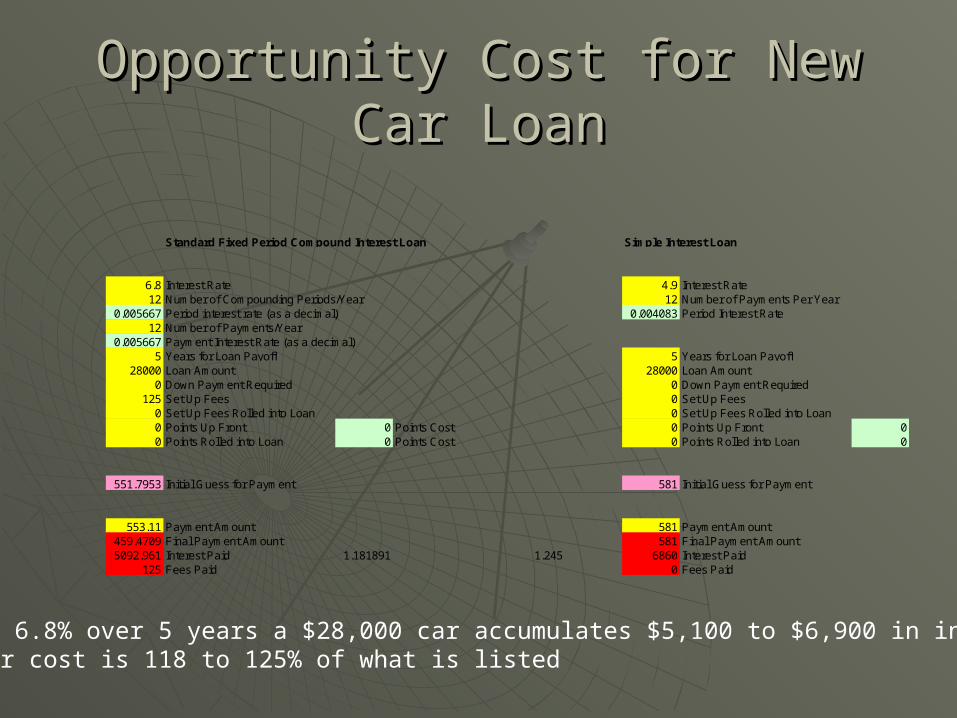

Opportunity Cost for New Car LoanOpportunity Cost for New Car Loan

Standard Fixed Period Compound Interest Loan Simple Interest Loan

6.8 Interest Rate 4.9 Interest Rate12 Number of Compounding Periods/Year 12 Number of Payments Per Year

0.005667 Period interest rate (as a decimal) 0.004083 Period Interest Rate12 Number of Payments/Year

0.005667 Payment Interest Rate (as a decimal)5 Years for Loan Payoff 5 Years for Loan Payoff

28000 Loan Amount 28000 Loan Amount0 Down Payment Required 0 Down Payment Required

125 Set Up Fees 0 Set Up Fees0 Set Up Fees Rolled into Loan 0 Set Up Fees Rolled into Loan0 Points Up Front 0 Points Cost 0 Points Up Front 00 Points Rolled into Loan 0 Points Cost 0 Points Rolled into Loan 0

551.7953 Initial Guess for Payment 581 Initial Guess for Payment

553.11 Payment Amount 581 Payment Amount459.4709 Final Payment Amount 581 Final Payment Amount5092.961 Interest Paid 1.181891 1.245 6860 Interest Paid

125 Fees Paid 0 Fees Paid

At 6.8% over 5 years a $28,000 car accumulates $5,100 to $6,900 in interestCar cost is 118 to 125% of what is listed

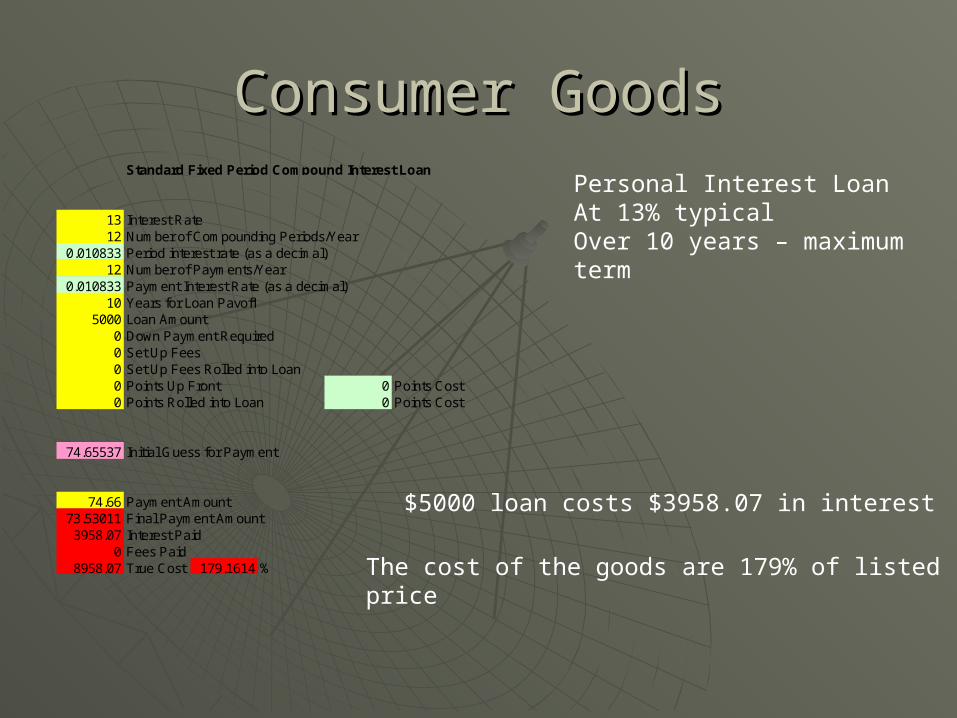

Consumer GoodsConsumer GoodsStandard Fixed Period Compound Interest Loan

13 Interest Rate12 Number of Compounding Periods/Year

0.010833 Period interest rate (as a decimal)12 Number of Payments/Year

0.010833 Payment Interest Rate (as a decimal)10 Years for Loan Payoff

5000 Loan Amount0 Down Payment Required0 Set Up Fees0 Set Up Fees Rolled into Loan0 Points Up Front 0 Points Cost0 Points Rolled into Loan 0 Points Cost

74.65537 Initial Guess for Payment

74.66 Payment Amount73.53011 Final Payment Amount3958.07 Interest Paid

0 Fees Paid8958.07 True Cost 179.1614 %

Personal Interest LoanAt 13% typicalOver 10 years – maximumterm

$5000 loan costs $3958.07 in interest

The cost of the goods are 179% of listedprice

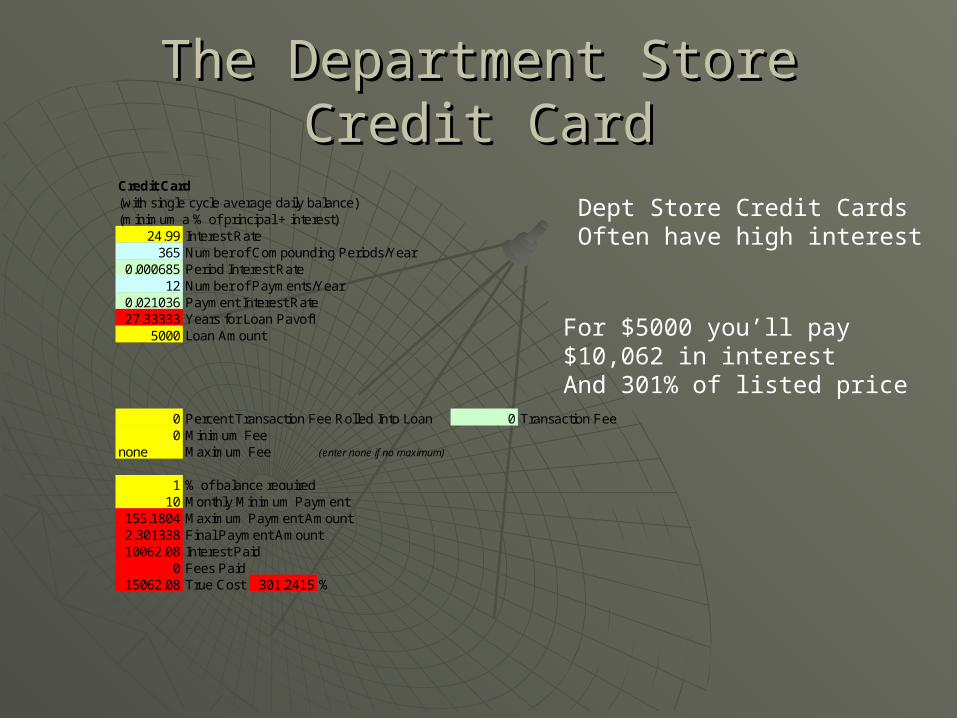

The Department Store Credit CardThe Department Store Credit Card

Credit Card(with single cycle average daily balance)(minimum a % of principal + interest)

24.99 Interest Rate365 Number of Compounding Periods/Year

0.000685 Period Interest Rate12 Number of Payments/Year

0.021036 Payment Interest Rate27.33333 Years for Loan Payoff

5000 Loan Amount

0 Percent Transaction Fee Rolled Into Loan 0 Transaction Fee0 Minimum Fee

none Maximum Fee (enter none if no maximum)

1 % of balance required10 Monthly Minimum Payment

155.1804 Maximum Payment Amount 2.301338 Final Payment Amount10062.08 Interest Paid

0 Fees Paid15062.08 True Cost 301.2415 %

Dept Store Credit CardsOften have high interest

For $5000 you’ll pay$10,062 in interestAnd 301% of listed price

Is Opportunity Cost Something that Is Opportunity Cost Something that only people in debt have?only people in debt have?

Not reallyNot really• Almost all people decide not to do Almost all people decide not to do

something for everything they decide to dosomething for everything they decide to do If I spend money I could have saved for If I spend money I could have saved for

3% interest I have an opportunity cost3% interest I have an opportunity cost If I buy a big screen TV instead of If I buy a big screen TV instead of

saving for retirement at 9% return the saving for retirement at 9% return the true cost of my big screen TV may be true cost of my big screen TV may be 30 years of lost 9% interest30 years of lost 9% interest

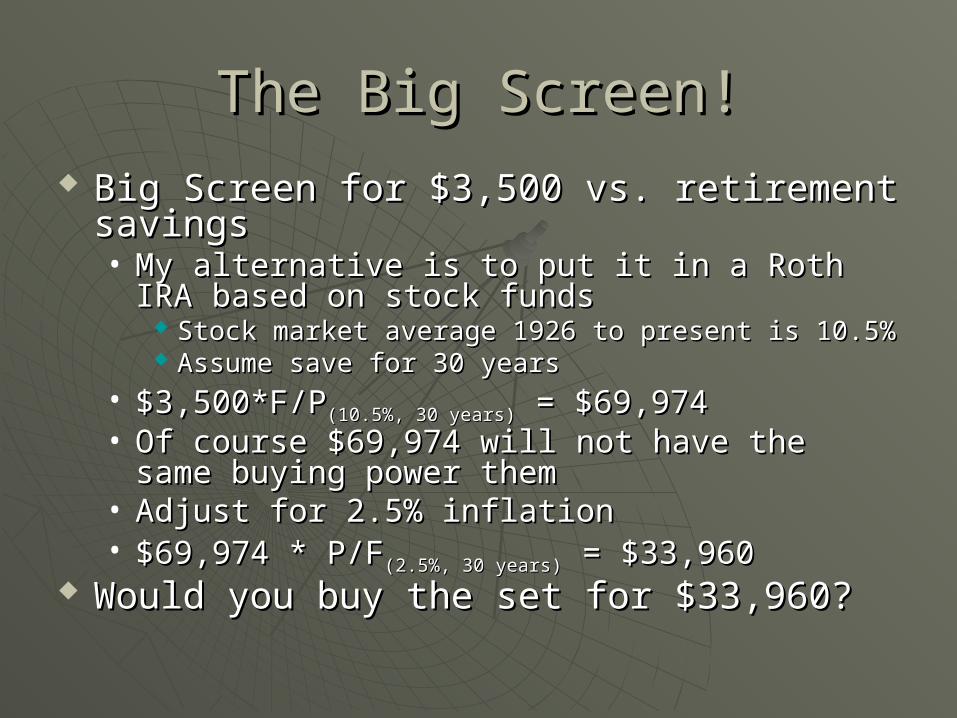

The Big Screen!The Big Screen! Big Screen for $3,500 vs. retirement Big Screen for $3,500 vs. retirement

savingssavings• My alternative is to put it in a Roth IRA based My alternative is to put it in a Roth IRA based

on stock fundson stock funds Stock market average 1926 to present is 10.5%Stock market average 1926 to present is 10.5% Assume save for 30 yearsAssume save for 30 years

• $3,500*F/P$3,500*F/P(10.5%, 30 years)(10.5%, 30 years) = $69,974 = $69,974• Of course $69,974 will not have the same Of course $69,974 will not have the same

buying power thembuying power them• Adjust for 2.5% inflationAdjust for 2.5% inflation• $69,974 * P/F$69,974 * P/F(2.5%, 30 years)(2.5%, 30 years) = $33,960 = $33,960

Would you buy the set for $33,960?Would you buy the set for $33,960?

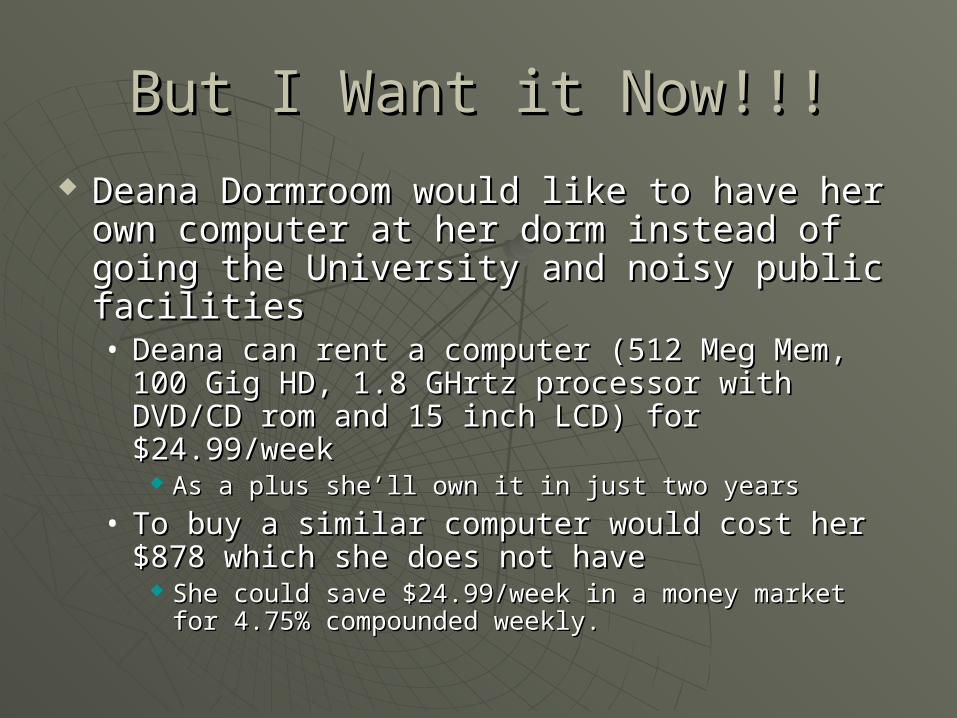

But I Want it Now!!!But I Want it Now!!!

Deana Dormroom would like to have her Deana Dormroom would like to have her own computer at her dorm instead of own computer at her dorm instead of going the University and noisy public going the University and noisy public facilitiesfacilities• Deana can rent a computer (512 Meg Mem, Deana can rent a computer (512 Meg Mem,

100 Gig HD, 1.8 GHrtz processor with DVD/CD 100 Gig HD, 1.8 GHrtz processor with DVD/CD rom and 15 inch LCD) for $24.99/weekrom and 15 inch LCD) for $24.99/week

As a plus she’ll own it in just two yearsAs a plus she’ll own it in just two years

• To buy a similar computer would cost her $878 To buy a similar computer would cost her $878 which she does not havewhich she does not have

She could save $24.99/week in a money market for She could save $24.99/week in a money market for 4.75% compounded weekly.4.75% compounded weekly.

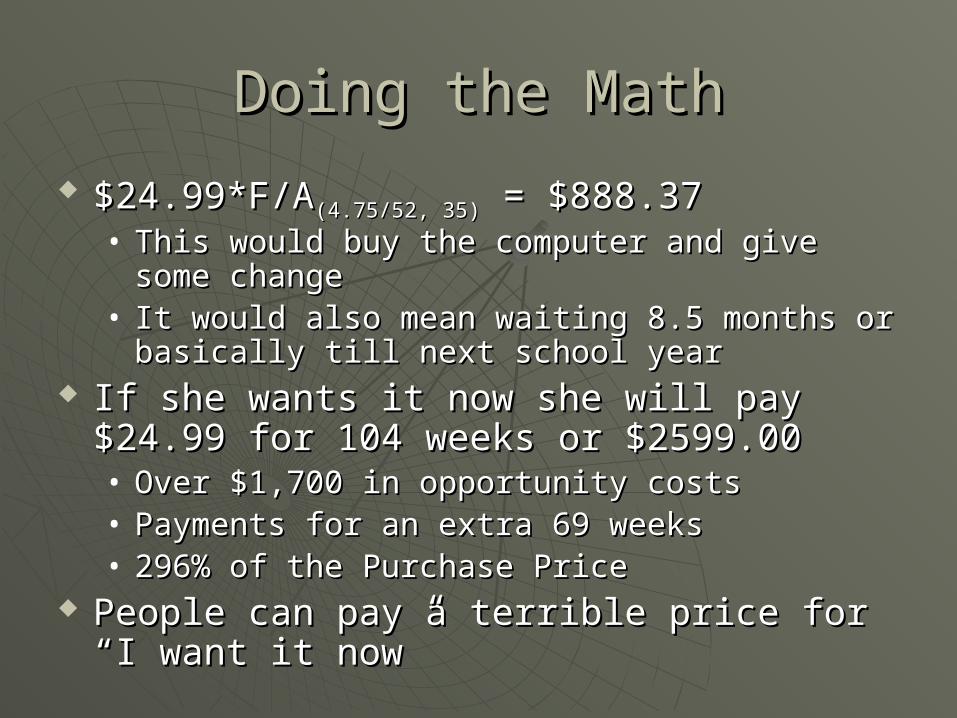

Doing the MathDoing the Math

$24.99*F/A$24.99*F/A(4.75/52, 35)(4.75/52, 35) = $888.37 = $888.37• This would buy the computer and give some This would buy the computer and give some

changechange• It would also mean waiting 8.5 months or It would also mean waiting 8.5 months or

basically till next school yearbasically till next school year If she wants it now she will pay $24.99 for If she wants it now she will pay $24.99 for

104 weeks or $2599.00104 weeks or $2599.00• Over $1,700 in opportunity costsOver $1,700 in opportunity costs• Payments for an extra 69 weeksPayments for an extra 69 weeks• 296% of the Purchase Price296% of the Purchase Price

People can pay a terrible price for “I want People can pay a terrible price for “I want it now”it now”

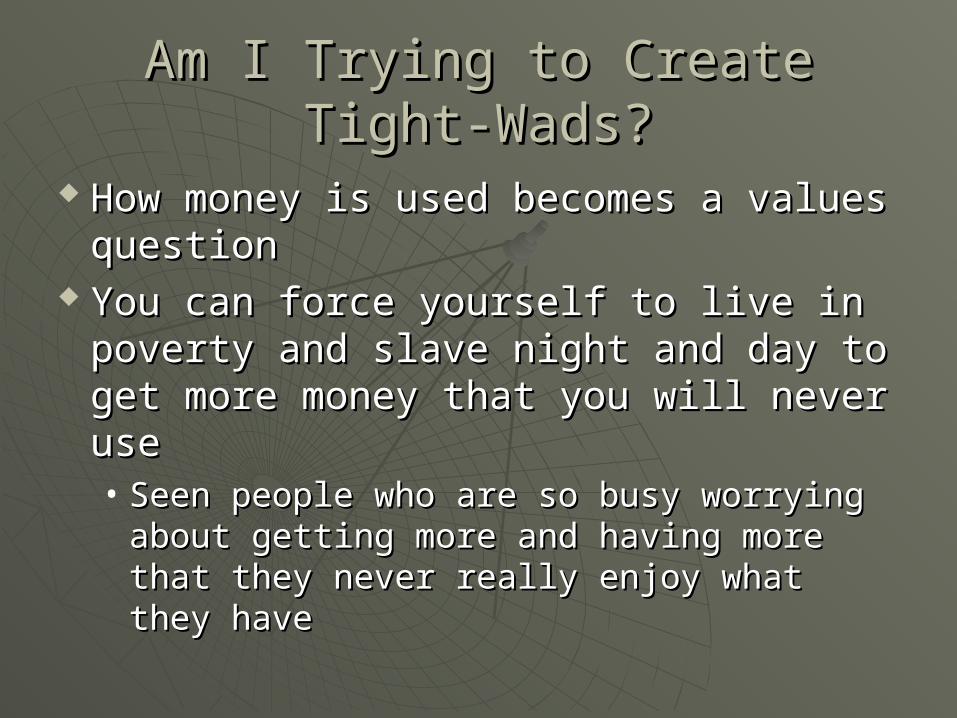

Am I Trying to Create Tight-Wads?Am I Trying to Create Tight-Wads?

How money is used becomes a values How money is used becomes a values questionquestion

You can force yourself to live in You can force yourself to live in poverty and slave night and day to get poverty and slave night and day to get more money that you will never usemore money that you will never use• Seen people who are so busy worrying Seen people who are so busy worrying

about getting more and having more that about getting more and having more that they never really enjoy what they havethey never really enjoy what they have

Some Things are Not NegotiableSome Things are Not Negotiable

Bodies need food, water, shelter, and Bodies need food, water, shelter, and coverings to functioncoverings to function• Stashing money at the cost of health and Stashing money at the cost of health and

function is probably not a good choicefunction is probably not a good choice Pitching a PackagePitching a Package

• The world judges packages by their wrappersThe world judges packages by their wrappers• The cars we drive, cloths we wear, homes we The cars we drive, cloths we wear, homes we

live in form the wrappers others seelive in form the wrappers others see If we think we can fool ourselves buying happiness If we think we can fool ourselves buying happiness

with a wrapper it usually doesn’t workwith a wrapper it usually doesn’t work Sometimes wrappers are part of the package we sell Sometimes wrappers are part of the package we sell

to make a livingto make a living• You would not want to use the cars I drive if you were a You would not want to use the cars I drive if you were a

real estate agentreal estate agent

Necessary ThingsNecessary Things

What it takes to take care of a body What it takes to take care of a body to serve youto serve you• May not need the nicest house or clothsMay not need the nicest house or cloths

What it takes to wrap up the package What it takes to wrap up the package we sell to make our livingwe sell to make our living• Watch out for excesses that have more Watch out for excesses that have more

to do with fooling yourself than realistic to do with fooling yourself than realistic market packagingmarket packaging

Every product has a limit on what can be Every product has a limit on what can be spent for packagingspent for packaging

We All Have WantsWe All Have Wants

If we look at All Cost Alternatives If we look at All Cost Alternatives problems for meeting our physical problems for meeting our physical and packaging needs we have more and packaging needs we have more available for our wantsavailable for our wants

A Problem of Opportunity CostA Problem of Opportunity Cost

Opportunity cost seems to depend on Opportunity cost seems to depend on what it is compared to.what it is compared to.

Yes it doesYes it does• So don’t lie to yourself – consider only the So don’t lie to yourself – consider only the

options that are realistically out thereoptions that are realistically out there Do consider opportunity cost when you go Do consider opportunity cost when you go

shoppingshopping• Don’t hesitate to put something back while you Don’t hesitate to put something back while you

think about itthink about it• Feel free to sleep on something or do the mathFeel free to sleep on something or do the math• If the “deal” won’t wait its probably only a deal If the “deal” won’t wait its probably only a deal

for the person pushing the merchandisefor the person pushing the merchandise

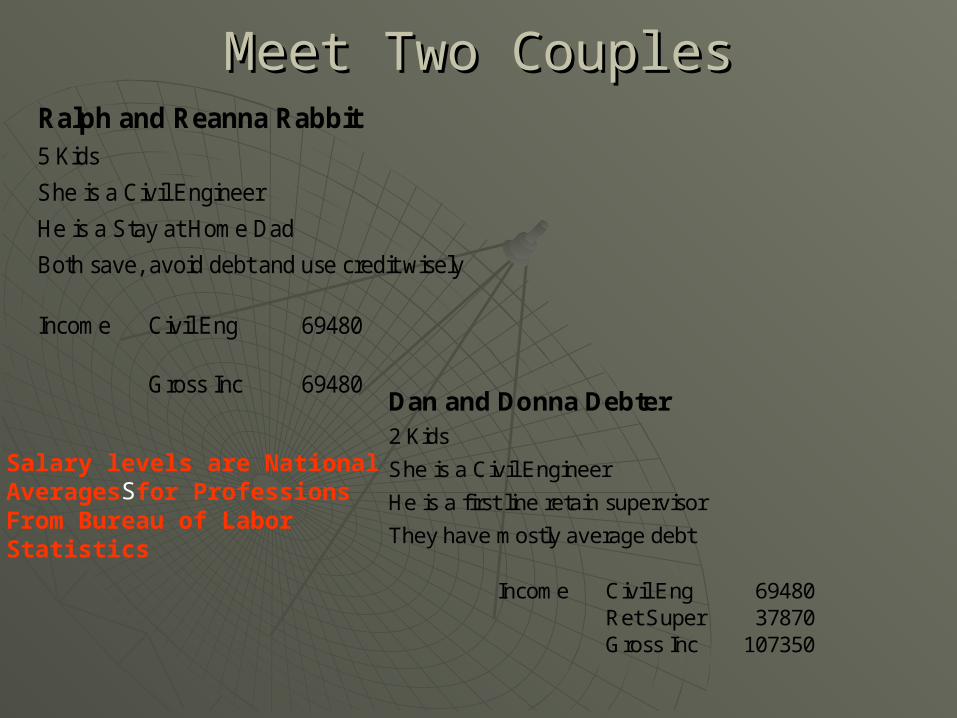

Meet Two CouplesMeet Two CouplesRalph and Reanna Rabbit5 Kids

She is a Civil Engineer

He is a Stay at Home Dad

Both save, avoid debt and use credit wisely

Income Civil Eng 69480

Gross Inc 69480Dan and Donna Debter2 Kids

She is a Civil Engineer

He is a first line retain supervisor

They have mostly average debt

Income Civil Eng 69480Ret Super 37870Gross Inc 107350

SSalary levels are NationalAverages for ProfessionsFrom Bureau of LaborStatistics

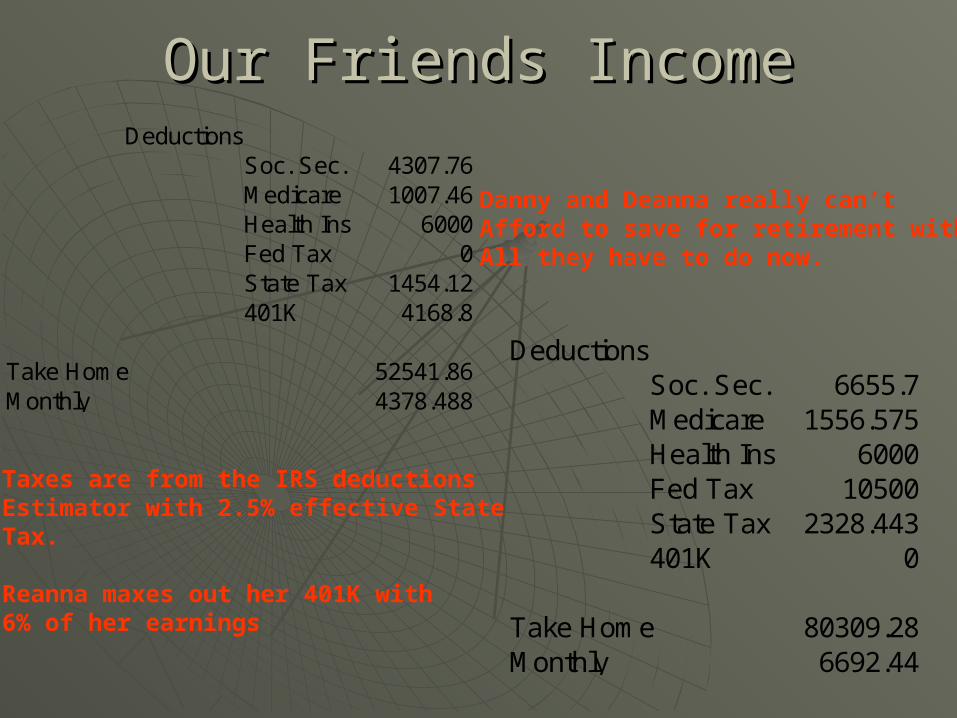

Our Friends IncomeOur Friends IncomeDeductions

Soc. Sec. 4307.76Medicare 1007.46Health Ins 6000Fed Tax 0State Tax 1454.12401K 4168.8

Take Home 52541.86Monthly 4378.488

DeductionsSoc. Sec. 6655.7Medicare 1556.575Health Ins 6000Fed Tax 10500State Tax 2328.443401K 0

Take Home 80309.28Monthly 6692.44

Taxes are from the IRS deductionsEstimator with 2.5% effective StateTax.

Reanna maxes out her 401K with6% of her earnings

Danny and Deanna really can’tAfford to save for retirement withAll they have to do now.

Their HomesTheir Homes Both bought modest Midwestern homes at rates Both bought modest Midwestern homes at rates

indicated by the Census Bureau and National indicated by the Census Bureau and National Realtors web siteRealtors web site

Both pay 2% tax, 0.9% insurance, 0.7% regular Both pay 2% tax, 0.9% insurance, 0.7% regular small repairs and have about 1% in long term small repairs and have about 1% in long term repair costsrepair costs

Ralph and Reanna took longer through school to Ralph and Reanna took longer through school to avoid student loans and then saved for a down avoid student loans and then saved for a down payment so they were 2 years later buying their payment so they were 2 years later buying their home and had to pay more for the same thinghome and had to pay more for the same thing

Both have 30 year fixed rate mortgages at the Both have 30 year fixed rate mortgages at the current average rate of 6.37% current average rate of 6.37%

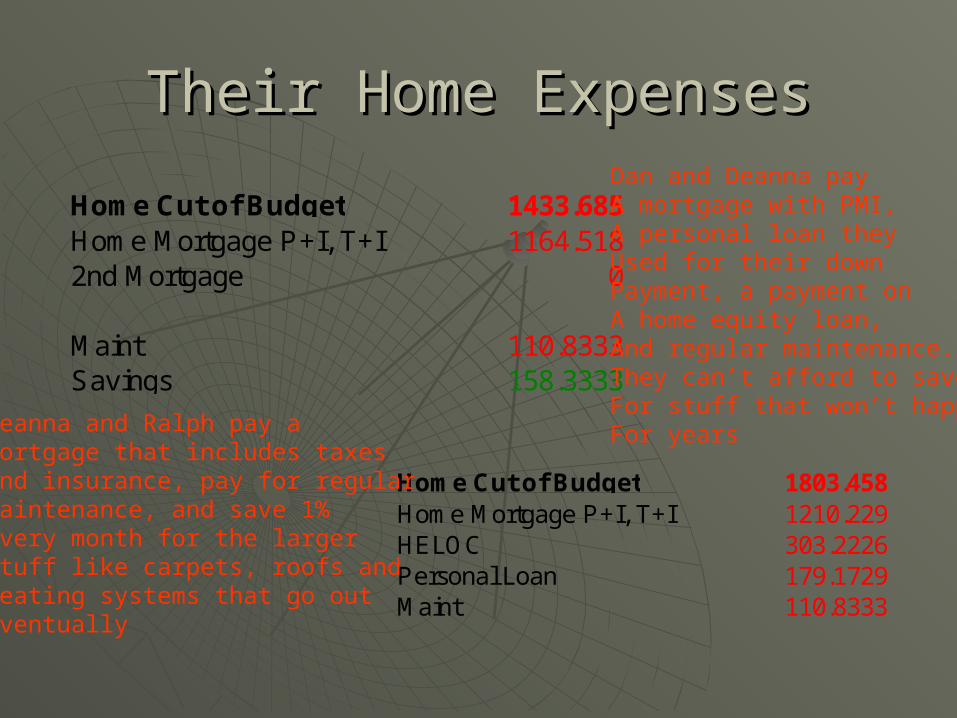

Their Home ExpensesTheir Home Expenses

Home Cut of Budget 1433.685Home Mortgage P+I, T+I 1164.5182nd Mortgage 0

Maint 110.8333Savings 158.3333

Home Cut of Budget 1803.458Home Mortgage P+I, T+I 1210.229HELOC 303.2226Personal Loan 179.1729Maint 110.8333

Reanna and Ralph pay aMortgage that includes taxesAnd insurance, pay for regularMaintenance, and save 1%Every month for the largerStuff like carpets, roofs andHeating systems that go outeventually

Dan and Deanna payA mortgage with PMI,A personal loan theyUsed for their downPayment, a payment onA home equity loan,And regular maintenance.They can’t afford to saveFor stuff that won’t happenFor years

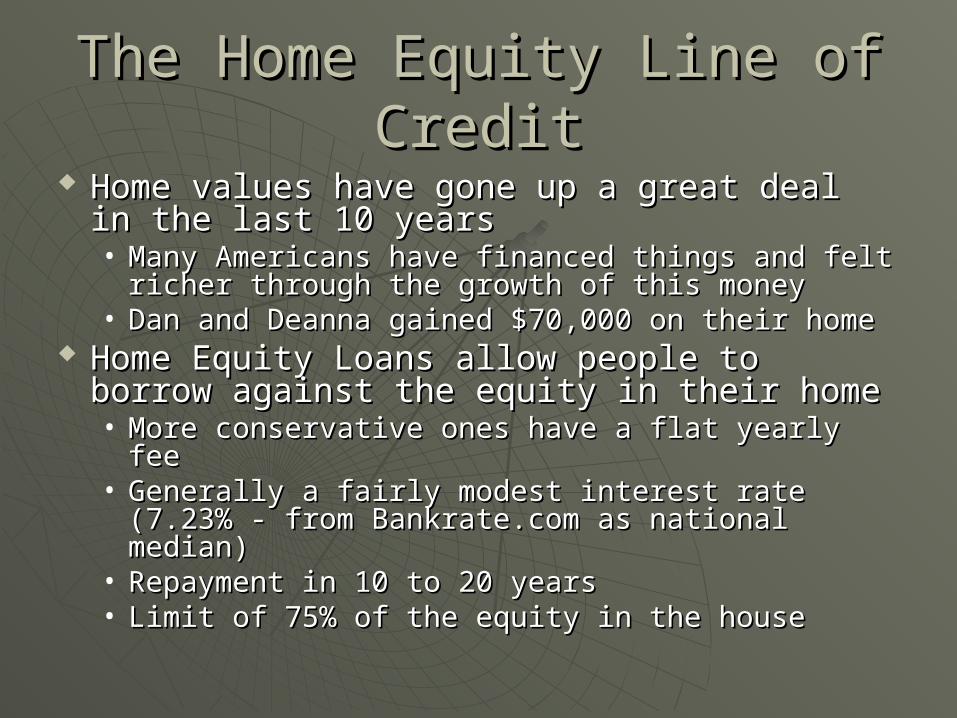

The Home Equity Line of CreditThe Home Equity Line of Credit Home values have gone up a great deal in Home values have gone up a great deal in

the last 10 yearsthe last 10 years• Many Americans have financed things and felt Many Americans have financed things and felt

richer through the growth of this moneyricher through the growth of this money• Dan and Deanna gained $70,000 on their Dan and Deanna gained $70,000 on their

homehome Home Equity Loans allow people to borrow Home Equity Loans allow people to borrow

against the equity in their homeagainst the equity in their home• More conservative ones have a flat yearly feeMore conservative ones have a flat yearly fee• Generally a fairly modest interest rate (7.23% - Generally a fairly modest interest rate (7.23% -

from Bankrate.com as national median)from Bankrate.com as national median)• Repayment in 10 to 20 yearsRepayment in 10 to 20 years• Limit of 75% of the equity in the houseLimit of 75% of the equity in the house

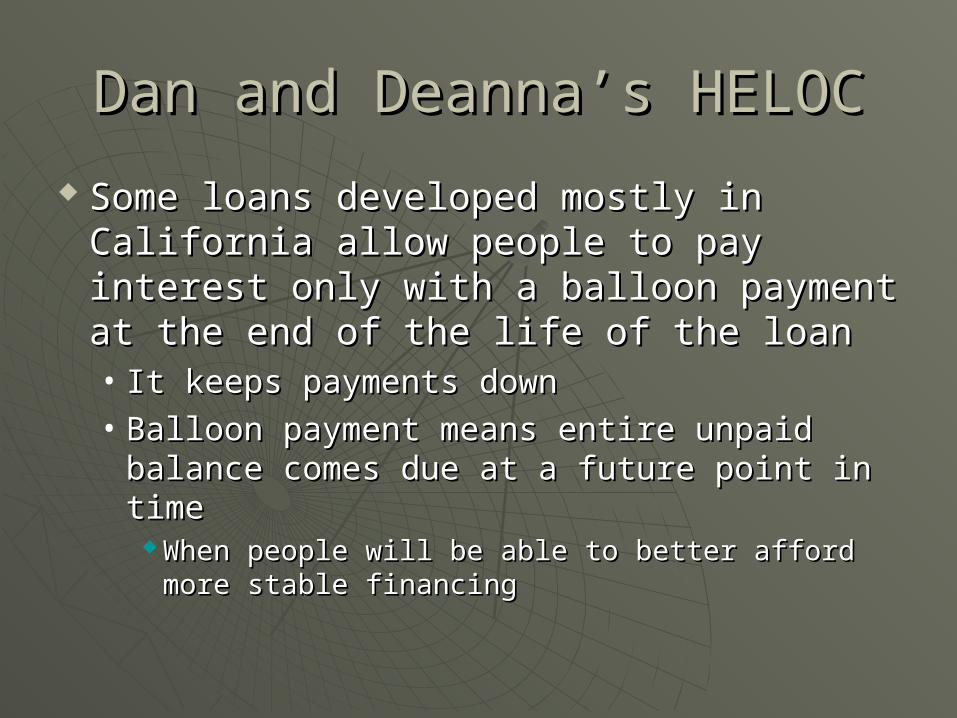

Dan and Deanna’s HELOCDan and Deanna’s HELOC

Some loans developed mostly in Some loans developed mostly in California allow people to pay interest California allow people to pay interest only with a balloon payment at the only with a balloon payment at the end of the life of the loanend of the life of the loan• It keeps payments downIt keeps payments down• Balloon payment means entire unpaid Balloon payment means entire unpaid

balance comes due at a future point in balance comes due at a future point in timetime

When people will be able to better afford When people will be able to better afford more stable financingmore stable financing

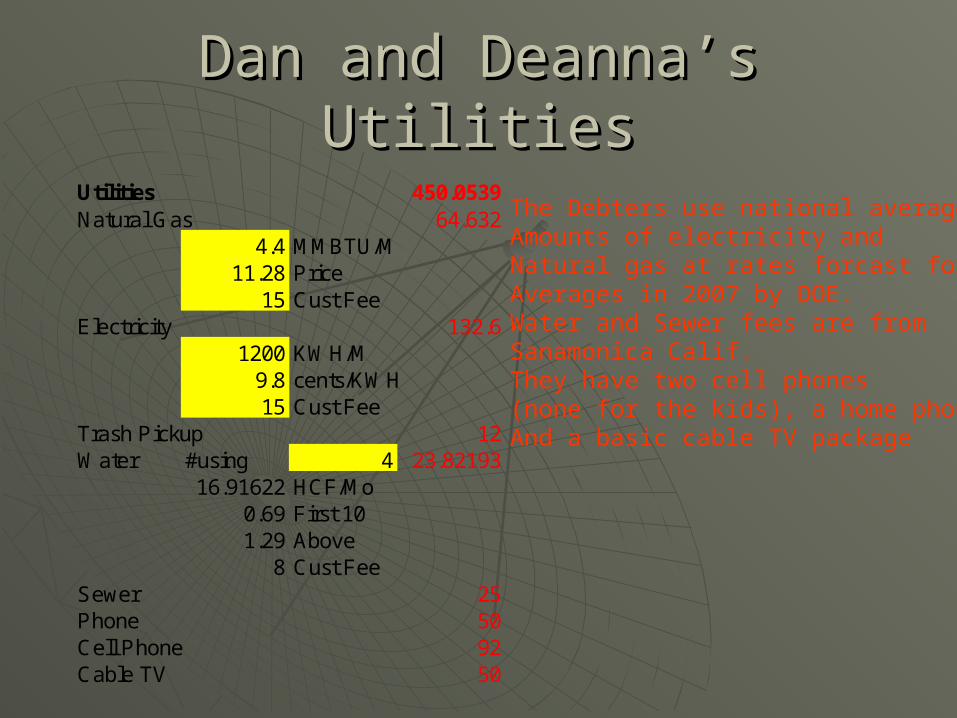

Dan and Deanna’s UtilitiesDan and Deanna’s Utilities

Utilities 450.0539Natural Gas 64.632

4.4 MMBTU/M11.28 Price

15 Cust FeeElectricity 132.6

1200 KWH/M9.8 cents/KWH15 Cust Fee

Trash Pickup 12Water #using 4 23.82193

16.91622 HCF/Mo0.69 First 101.29 Above

8 Cust FeeSewer 25Phone 50Cell Phone 92Cable TV 50

The Debters use national averageAmounts of electricity andNatural gas at rates forcast forAverages in 2007 by DOE.Water and Sewer fees are fromSanamonica Calif.They have two cell phones(none for the kids), a home phoneAnd a basic cable TV package

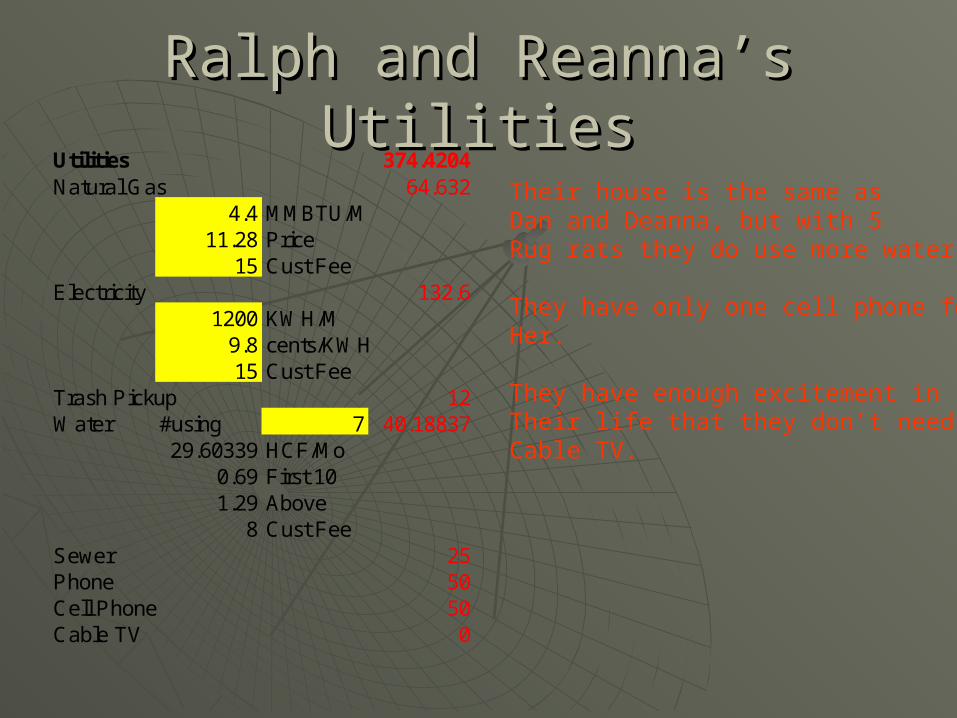

Ralph and Reanna’s UtilitiesRalph and Reanna’s UtilitiesUtilities 374.4204Natural Gas 64.632

4.4 MMBTU/M11.28 Price

15 Cust FeeElectricity 132.6

1200 KWH/M9.8 cents/KWH15 Cust Fee

Trash Pickup 12Water #using 7 40.18837

29.60339 HCF/Mo0.69 First 101.29 Above

8 Cust FeeSewer 25Phone 50Cell Phone 50Cable TV 0

Their house is the same asDan and Deanna, but with 5Rug rats they do use more water.

They have only one cell phone forHer.

They have enough excitement inTheir life that they don’t needCable TV.

Their CarsTheir Cars Most common advice is avoid new car. (They Most common advice is avoid new car. (They

loose about 30% the first year)loose about 30% the first year) Buy late model used car and drive it till it diesBuy late model used car and drive it till it dies Both couples do thisBoth couples do this DifferencesDifferences

• The Rabbits drive more miles chauffeuring kids and get The Rabbits drive more miles chauffeuring kids and get poorer gas mileage from bigger vehiclespoorer gas mileage from bigger vehicles

• The Rabbits make monthly savings payments for their The Rabbits make monthly savings payments for their carscars

Including replacementIncluding replacement And to levelize maintenance that goes up with ageAnd to levelize maintenance that goes up with age

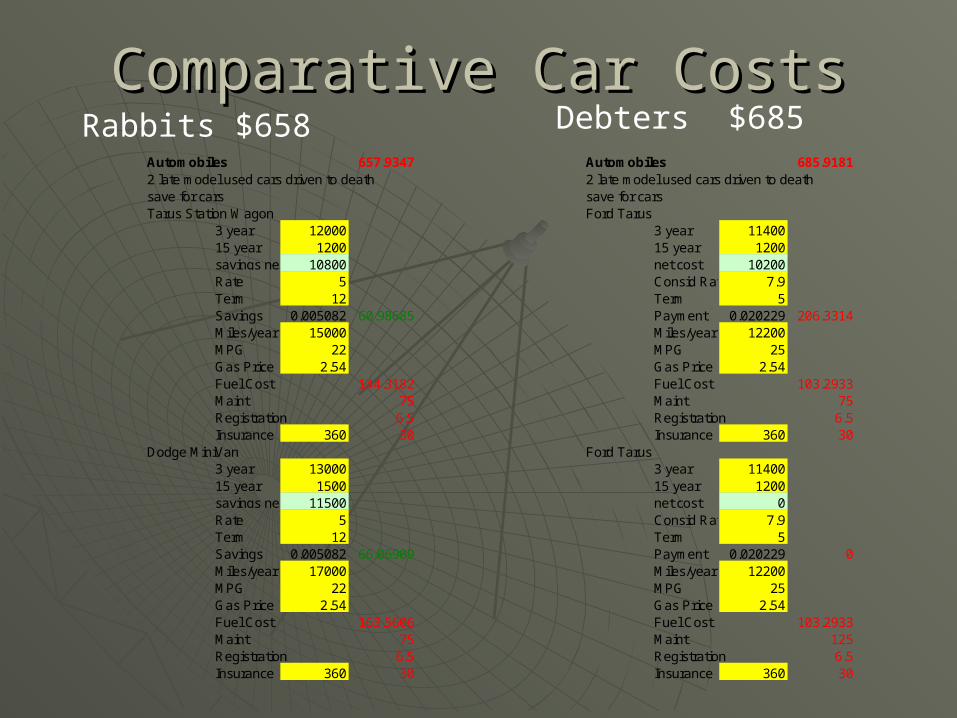

Comparative Car CostsComparative Car CostsAutomobiles 657.93472 late model used cars driven to deathsave for carsTarus Station Wagon

3 year 1200015 year 1200savings need 10800Rate 5Term 12Savings 0.005082 60.98685Miles/year 15000MPG 22Gas Price 2.54Fuel Cost 144.3182Maint 75Registration 6.5Insurance 360 30

Dodge MiniVan3 year 1300015 year 1500savings need 11500Rate 5Term 12Savings 0.005082 66.06909Miles/year 17000MPG 22Gas Price 2.54Fuel Cost 163.5606Maint 75Registration 6.5Insurance 360 30

Automobiles 685.91812 late model used cars driven to deathsave for carsFord Tarus

3 year 1140015 year 1200net cost 10200Consid Rate 7.9Term 5Payment 0.020229 206.3314Miles/year 12200MPG 25Gas Price 2.54Fuel Cost 103.2933Maint 75Registration 6.5Insurance 360 30

Ford Tarus3 year 1140015 year 1200net cost 0Consid Rate 7.9Term 5Payment 0.020229 0Miles/year 12200MPG 25Gas Price 2.54Fuel Cost 103.2933Maint 125Registration 6.5Insurance 360 30

Rabbits $658 Debters $685

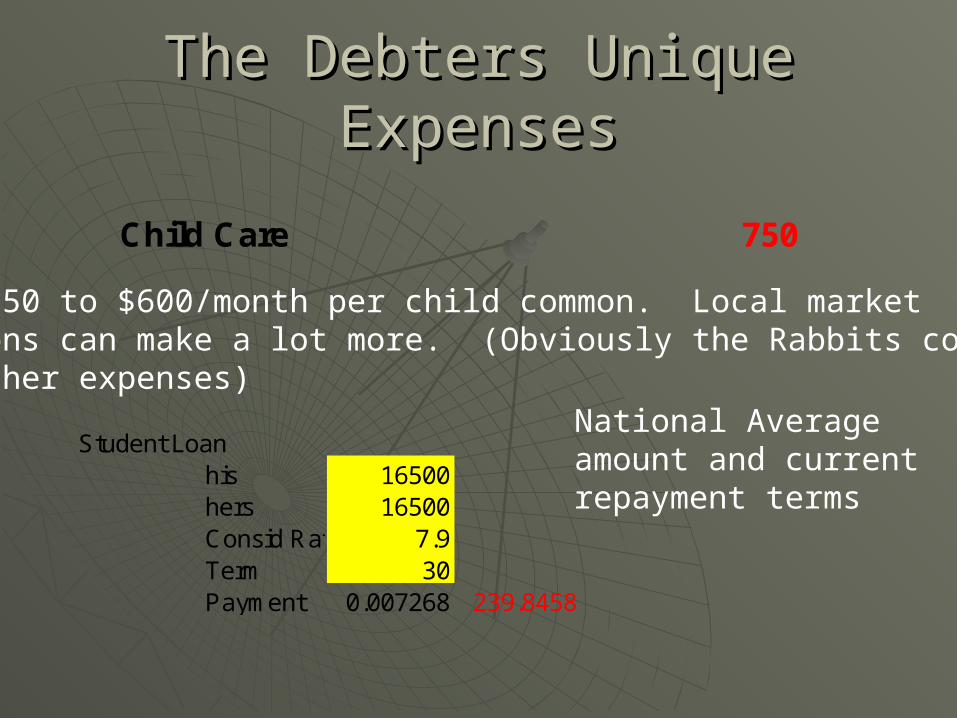

The Debters Unique ExpensesThe Debters Unique Expenses

Child Care 750

About $350 to $600/month per child common. Local marketconditions can make a lot more. (Obviously the Rabbits could havemuch higher expenses)

Student Loanhis 16500hers 16500Consid Rate 7.9Term 30Payment 0.007268 239.8458

National Averageamount and currentrepayment terms

The Reverse DowryThe Reverse Dowry

Saddling Today’s Students for Tax Saddling Today’s Students for Tax Breaks and Health CareBreaks and Health Care• Not just a democrat or republican issueNot just a democrat or republican issue• Cut amount of money to higher edCut amount of money to higher ed• Reverse the ratio of grants to loansReverse the ratio of grants to loans

between 60 and 70% of aide today is in loansbetween 60 and 70% of aide today is in loans

Big student loan payments can erase Big student loan payments can erase windfalls expected on graduationwindfalls expected on graduation• 30 year loan terms mean people will be paying for 30 year loan terms mean people will be paying for

their education to retirementtheir education to retirement

Bankruptcy Proof InvestmentsBankruptcy Proof Investments

Student loans cannot be discharged Student loans cannot be discharged in bankruptcyin bankruptcy

Retirement Savings in 401 Ks and Retirement Savings in 401 Ks and IRAs and some educational savings IRAs and some educational savings accounts cannot be taken in accounts cannot be taken in bankruptcybankruptcy

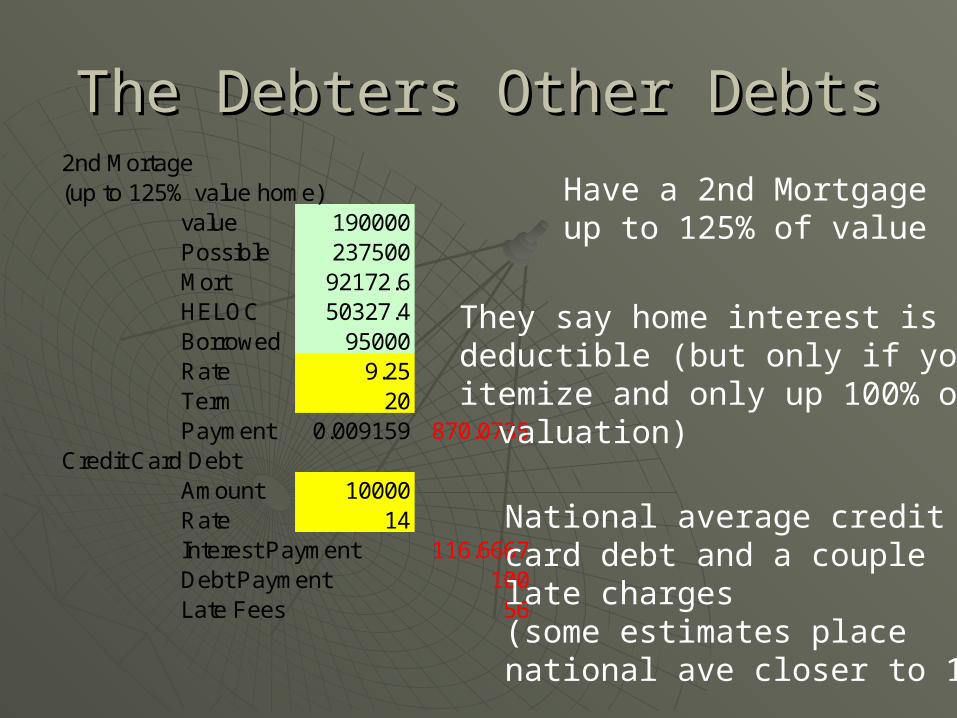

The Debters Other DebtsThe Debters Other Debts2nd Mortage(up to 125% value home)

value 190000Possible 237500Mort 92172.6HELOC 50327.4Borrowed 95000Rate 9.25Term 20Payment 0.009159 870.0735

Credit Card DebtAmount 10000Rate 14Interest Payment 116.6667Debt Payment 100Late Fees 56

Have a 2nd Mortgageup to 125% of value

They say home interest is taxdeductible (but only if youitemize and only up 100% of valuation)

National average creditcard debt and a couplelate charges(some estimates placenational ave closer to 16K)

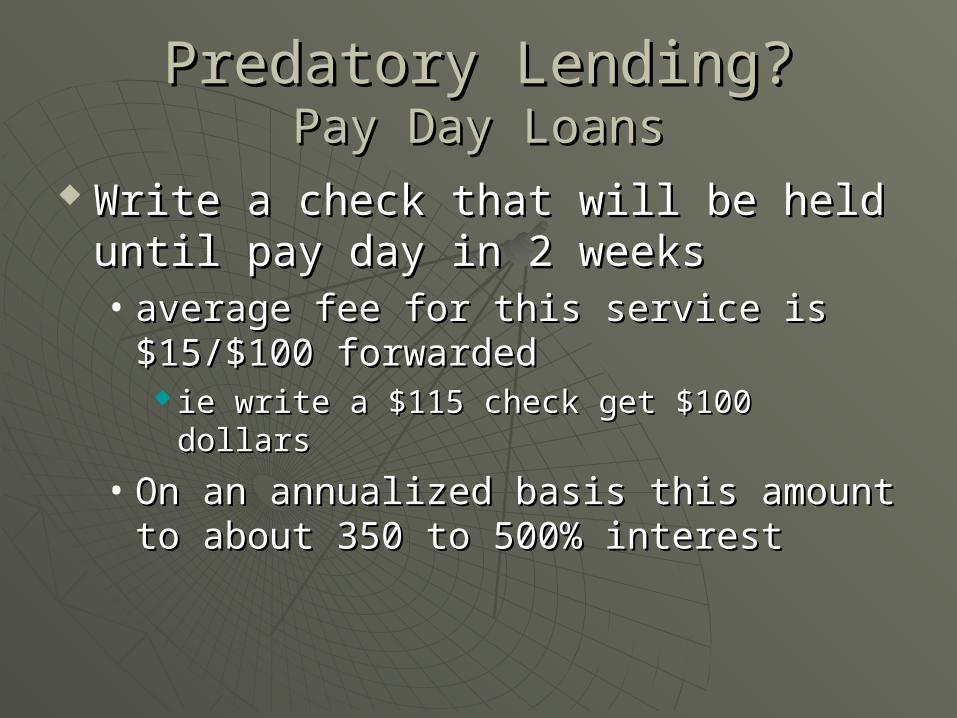

Predatory Lending?Predatory Lending?Pay Day LoansPay Day Loans

Write a check that will be held until Write a check that will be held until pay day in 2 weekspay day in 2 weeks• average fee for this service is $15/$100 average fee for this service is $15/$100

forwardedforwarded ie write a $115 check get $100 dollarsie write a $115 check get $100 dollars

• On an annualized basis this amount to On an annualized basis this amount to about 350 to 500% interestabout 350 to 500% interest

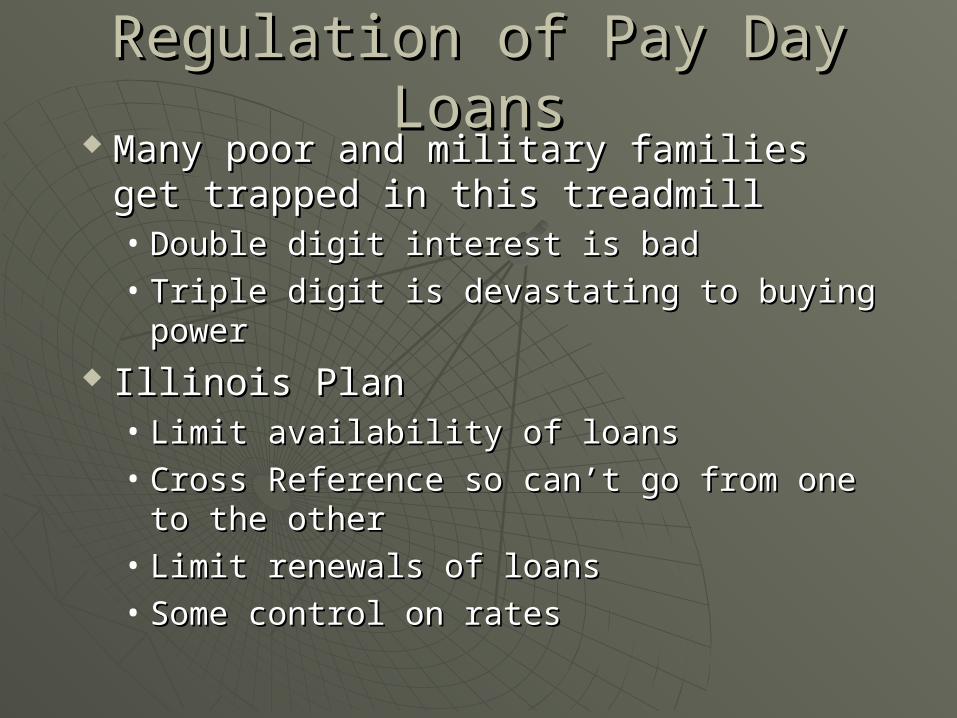

Regulation of Pay Day LoansRegulation of Pay Day Loans Many poor and military families get Many poor and military families get

trapped in this treadmilltrapped in this treadmill• Double digit interest is badDouble digit interest is bad• Triple digit is devastating to buying powerTriple digit is devastating to buying power

Illinois PlanIllinois Plan• Limit availability of loansLimit availability of loans• Cross Reference so can’t go from one to Cross Reference so can’t go from one to

the otherthe other• Limit renewals of loansLimit renewals of loans• Some control on ratesSome control on rates

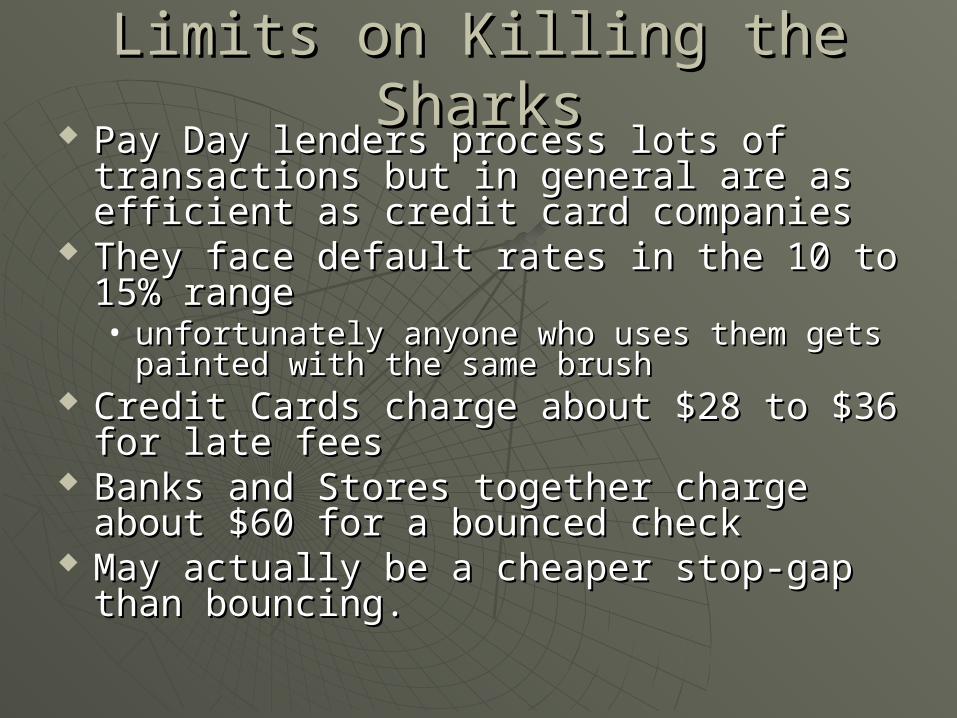

Limits on Killing the SharksLimits on Killing the Sharks Pay Day lenders process lots of Pay Day lenders process lots of

transactions but in general are as efficient transactions but in general are as efficient as credit card companiesas credit card companies

They face default rates in the 10 to 15% They face default rates in the 10 to 15% rangerange• unfortunately anyone who uses them gets unfortunately anyone who uses them gets

painted with the same brushpainted with the same brush Credit Cards charge about $28 to $36 for Credit Cards charge about $28 to $36 for

late feeslate fees Banks and Stores together charge about Banks and Stores together charge about

$60 for a bounced check$60 for a bounced check May actually be a cheaper stop-gap than May actually be a cheaper stop-gap than

bouncing.bouncing.

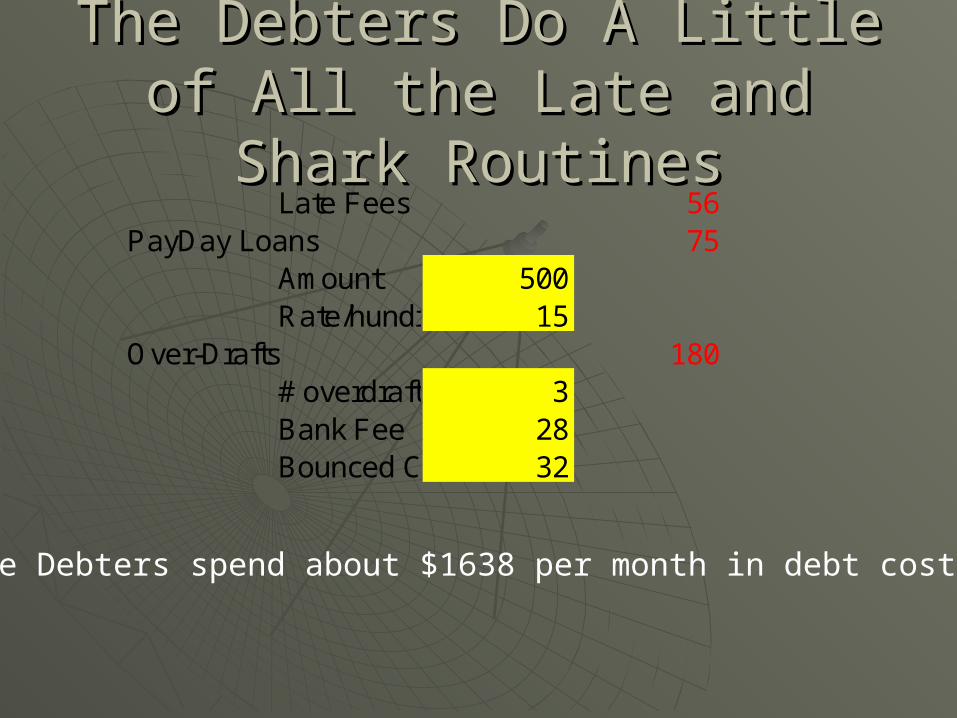

The Debters Do A Little of All The Debters Do A Little of All the Late and Shark Routinesthe Late and Shark Routines

Late Fees 56PayDay Loans 75

Amount 500Rate/hundred 15

Over-Drafts 180# overdrafts 3Bank Fee 28Bounced C 32

The Debters spend about $1638 per month in debt costs

More ComparisonsMore Comparisons

Need for two professional wardrobes, Need for two professional wardrobes, more fast foods and eating out, less more fast foods and eating out, less hand-me-down opportunities for hand-me-down opportunities for small families all take toll.small families all take toll.

More kids does mean more laundry More kids does mean more laundry costs and school activities costscosts and school activities costs

Big Contrast is the cost of items Big Contrast is the cost of items saved for vs. items paid for as crisis saved for vs. items paid for as crisis of the momentof the moment

Buying on Credit vs. SavingsBuying on Credit vs. SavingsAppliances Appliances(buy new every 12 years but Save) (buy new every 5 years with Debt Store Card)

Refridgerator 750 Regridger 1400Freezer 500 Freezer 0Rate 5 Rate 24.9Term 12 Term 5Savings 0.005082 6.352797 Payment 0.029293 41.00982

$6/month vs. $41/monthAppliances Appliances(buy new every 10 years but Save) (buy new every 5 years with Debt Store Card)

Washer C 450 Washer C 450Dryer 450 Dryer 450Rate 5 Rate 24.9Term 12 Term 5Payment 0.005082 4.574014 Payment 0.029293 26.36345

$4.5/month vs. $26/month

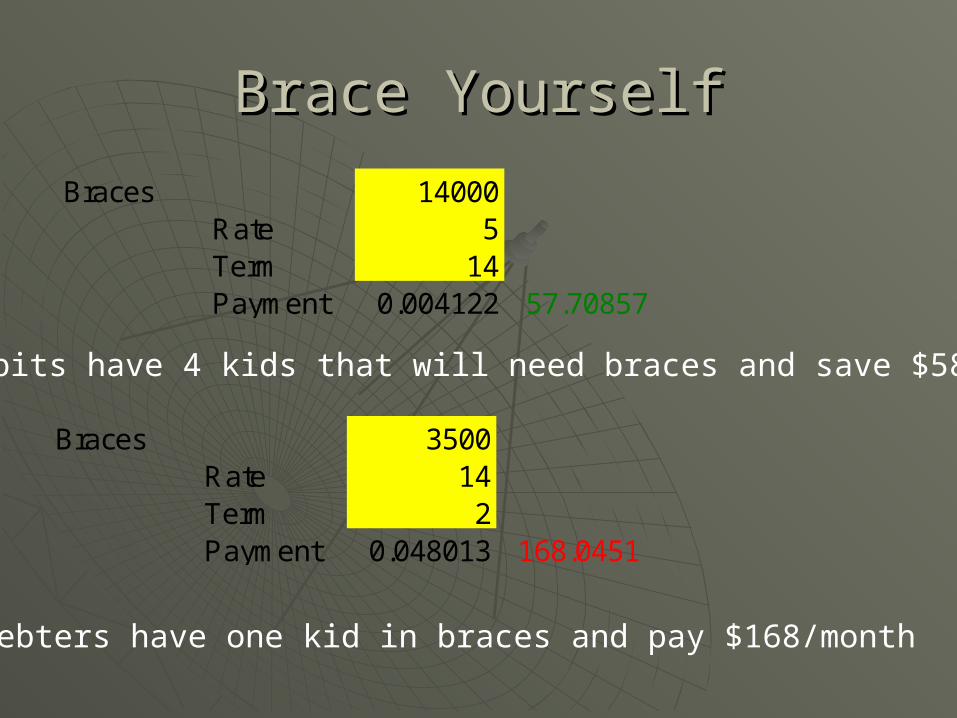

Brace YourselfBrace Yourself

Braces 14000Rate 5Term 14Payment 0.004122 57.70857

The Rabbits have 4 kids that will need braces and save $58/month

Braces 3500Rate 14Term 2Payment 0.048013 168.0451

The Debters have one kid in braces and pay $168/month

More ContrastsMore Contrasts Rabbits save about 10% of their net Rabbits save about 10% of their net

each month with another 10% available each month with another 10% available for charityfor charity

Rabbits have recommended insurance Rabbits have recommended insurance levels (about 5 to 10 times earnings) levels (about 5 to 10 times earnings) and disability insuranceand disability insurance

The Debters have no savings, no The Debters have no savings, no insurance, no charity, and are sinking insurance, no charity, and are sinking about $65/month like average -.3% about $65/month like average -.3% savings rate in the countrysavings rate in the country

What Happened to the Money?What Happened to the Money? Of the second income 80% of take Of the second income 80% of take

home pay went to pay interest.home pay went to pay interest.• Debt levels and devices will well within Debt levels and devices will well within

common practices and national averagescommon practices and national averages Even the principle part of debt plays Even the principle part of debt plays

catch-up on past purchase sapping catch-up on past purchase sapping financial energy to move forwardfinancial energy to move forward

Some would want to make this a stay Some would want to make this a stay at home parent issue - that was not at home parent issue - that was not point herepoint here

The Institution of SlaveryThe Institution of Slavery

Well known what was done to early Well known what was done to early African AmericansAfrican Americans

Indentured Servants from EuropeIndentured Servants from Europe Company Stores and housing in old Company Stores and housing in old

coal mining townscoal mining towns Debt remains an invisible enslaving Debt remains an invisible enslaving

tool todaytool today• People cheated by trinketsPeople cheated by trinkets• Underpayment of wages helps but the Underpayment of wages helps but the

trap works into Upper Middle Class trap works into Upper Middle Class

Ideas for Happiness within Your Ideas for Happiness within Your WealthWealth

Note that some of these things build on Note that some of these things build on actions and priorities - not just moneyactions and priorities - not just money

1- Build Marketable Job Skills that 1- Build Marketable Job Skills that promise personal satisfaction and promise personal satisfaction and financial rewardfinancial reward

2- Accurately Identify Needs and Wants2- Accurately Identify Needs and Wants• Lot of financial trouble comes of not being Lot of financial trouble comes of not being

able to tell the differenceable to tell the difference

Needs one 3 TypesNeeds one 3 Types• A- Needs provide for basic protection and A- Needs provide for basic protection and

physical needsphysical needs (Don’t get carried away - shelter is a need, a 4,500 (Don’t get carried away - shelter is a need, a 4,500

square foot McMansion is not)square foot McMansion is not)

• B- Needs provide for packaging the B- Needs provide for packaging the productproduct

• C- Needs include abstract emotional C- Needs include abstract emotional factors of companionship, love, self factors of companionship, love, self respect, and service to othersrespect, and service to others

illusion that these things can be bought with money lead illusion that these things can be bought with money lead many people to look and long down dead end pathsmany people to look and long down dead end paths

These things are usually earned through the things of These things are usually earned through the things of yourself that are givenyourself that are given

Product PackagingProduct Packaging Identify what things are necessary Identify what things are necessary

packaging for your careerpackaging for your career• in some places this might be a car to get you in some places this might be a car to get you

there and a professional wardrobethere and a professional wardrobe

Identify what things are necessary to Identify what things are necessary to package you for what you want to bepackage you for what you want to be

Avoid TrapsAvoid Traps• The thing of value needs to be what is in the The thing of value needs to be what is in the

package - not the packagepackage - not the package• Remember every product can only spend so Remember every product can only spend so

much on packaging and be competitivemuch on packaging and be competitive

Everything Else is a WantEverything Else is a Want Realistically analyze what your needs Realistically analyze what your needs

costcost• All Cost Alternatives techniques from this All Cost Alternatives techniques from this

class can help you look for meeting needs class can help you look for meeting needs cost effectivelycost effectively

• Include budgeting for maintenanceInclude budgeting for maintenance things break down and wear out - you know it things break down and wear out - you know it

and it should not be an “unexpected crisis” and it should not be an “unexpected crisis” when it happenswhen it happens

• Include budgeting for times of lesser abilityInclude budgeting for times of lesser ability can be old age, accident or injury, or economic can be old age, accident or injury, or economic

slow downslow down

Look at Whats Left for WantsLook at Whats Left for Wants If you have a good career and did an honest If you have a good career and did an honest

needs analysis there will be a nice chunk left needs analysis there will be a nice chunk left overover

Prioritize what you wantPrioritize what you want A lot of people would rather have modest A lot of people would rather have modest

amounts of a bunch of wants rather than being amounts of a bunch of wants rather than being the best of one wantthe best of one want

Remember to consider all cost alternativesRemember to consider all cost alternatives Remember to define things in opportunity and Remember to define things in opportunity and

absolute costabsolute cost Remember the maintenance cost that comes Remember the maintenance cost that comes

with every toywith every toy

Avoid Debt Like the PlagueAvoid Debt Like the Plague There are very few winning moves There are very few winning moves

with debtwith debt Debt makes opportunity costs far Debt makes opportunity costs far

greater than immediate product pricegreater than immediate product price Take a hard look at “I want it now”Take a hard look at “I want it now” Take a hard look at people who tell Take a hard look at people who tell

you that your happiness is based on you that your happiness is based on the package your wrapped inthe package your wrapped in• You’re the one who has to live with whats You’re the one who has to live with whats

really insidereally inside