the current status and future of banking – global banking...

TRANSCRIPT

The Current Status and Future of Banking – Global Banking Annual Report 2017

CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of McKinsey & Company is strictly prohibited

Albania, Tirana| 14 November 2017

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

Agenda

2 McKinsey & Company

State of the industry

Digital and AA at scale

Eco-systems?

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

3 McKinsey & Company

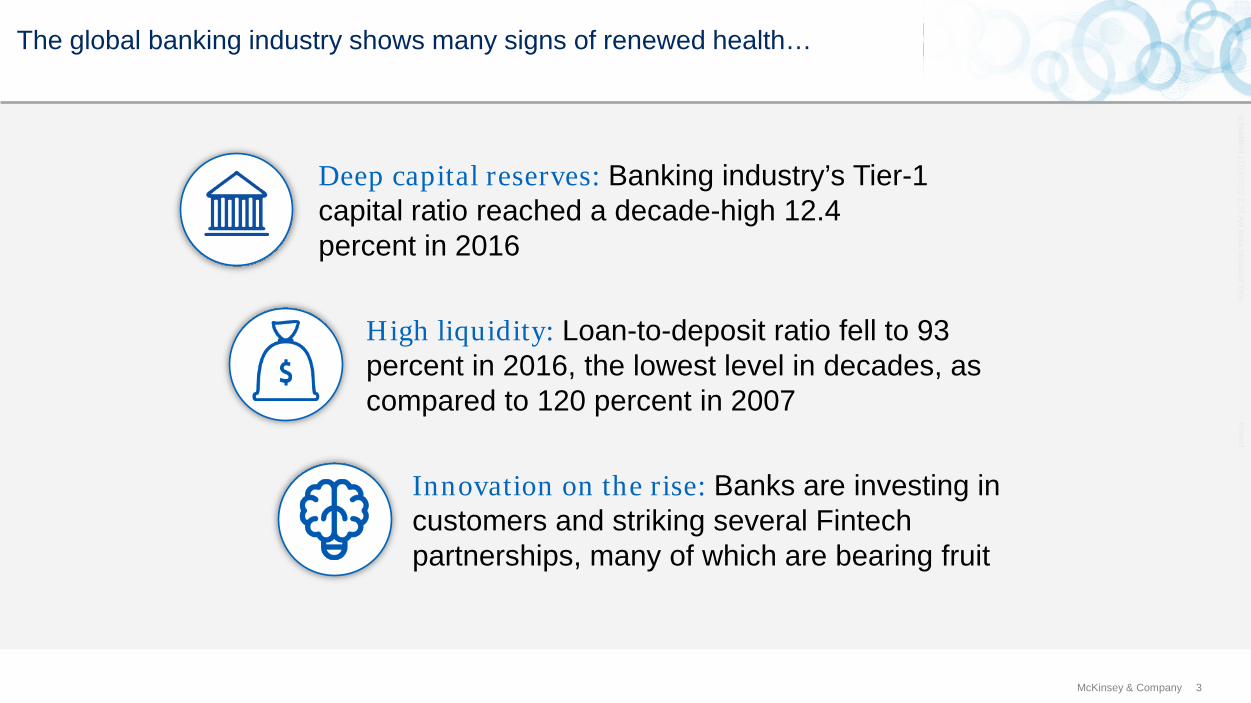

The global banking industry shows many signs of renewed health…

Innovation on the rise: Banks are investing in customers and striking several Fintech partnerships, many of which are bearing fruit

Deep capital reserves: Banking industry’s Tier-1 capital ratio reached a decade-high 12.4 percent in 2016

High liquidity: Loan-to-deposit ratio fell to 93 percent in 2016, the lowest level in decades, as compared to 120 percent in 2007

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

4 McKinsey & Company

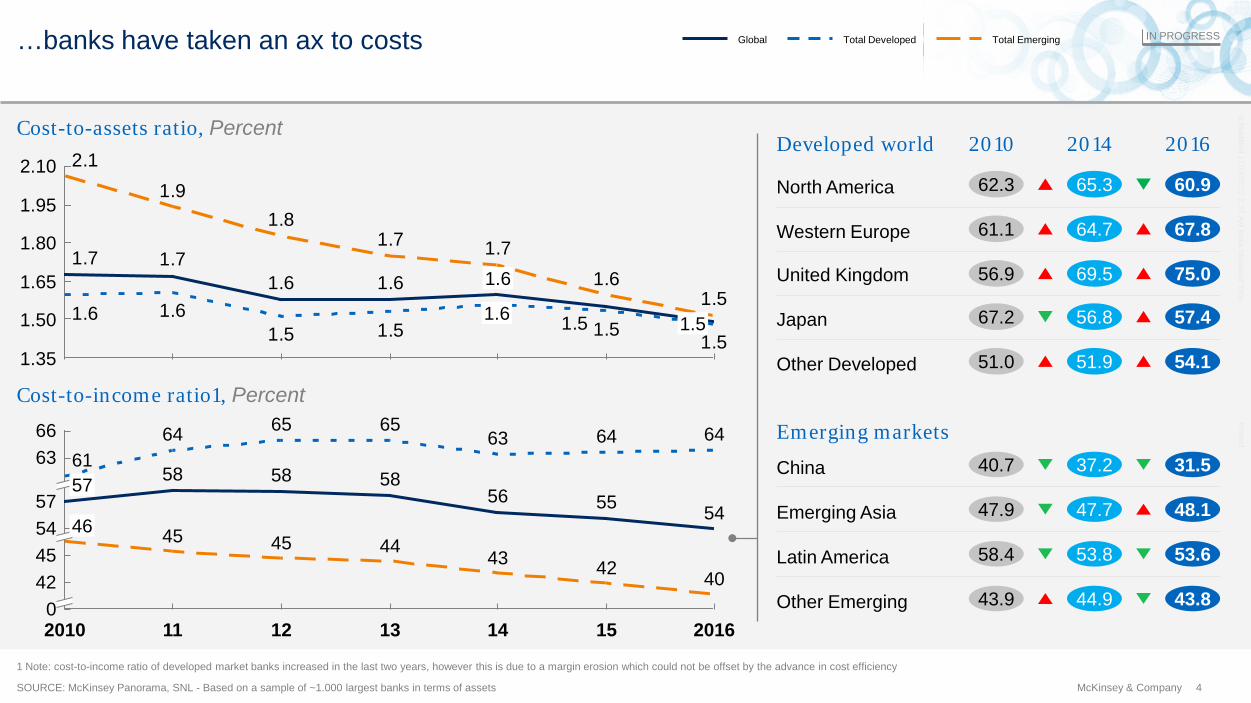

…banks have taken an ax to costs

15

45

0 14 12

57

42

11 13 2016 2010

54

66 63

58 55

64 61

46

58

64

45

58

65

40

56

45 44

64

43

63

54 57

65

42

1.5

1.61.61.71.7

1.51.51.51.5

1.61.61.5

1.61.71.7

1.81.9

2.1

1.50

2.10

1.80

1.65

1.95

1.35

1.5 1.6

1.6

Total Emerging Global Total Developed

Cost-to-income ratio1, Percent

Cost-to-assets ratio, Percent

SOURCE: McKinsey Panorama, SNL - Based on a sample of ~1.000 largest banks in terms of assets

1 Note: cost-to-income ratio of developed market banks increased in the last two years, however this is due to a margin erosion which could not be offset by the advance in cost efficiency

IN PROGRESS

2010 2016 2014 Developed world

Emerging markets 40.7 31.5 37.2 China

58.4 53.6 53.8 Latin America

43.9 43.8 44.9 Other Emerging

47.9 48.1 47.7 Emerging Asia

51.0 54.1 51.9 Other Developed

62.3 60.9 65.3 North America

61.1 67.8 64.7 Western Europe

67.2 57.4 56.8 Japan

56.9 75.0 69.5 United Kingdom

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

5 McKinsey & Company

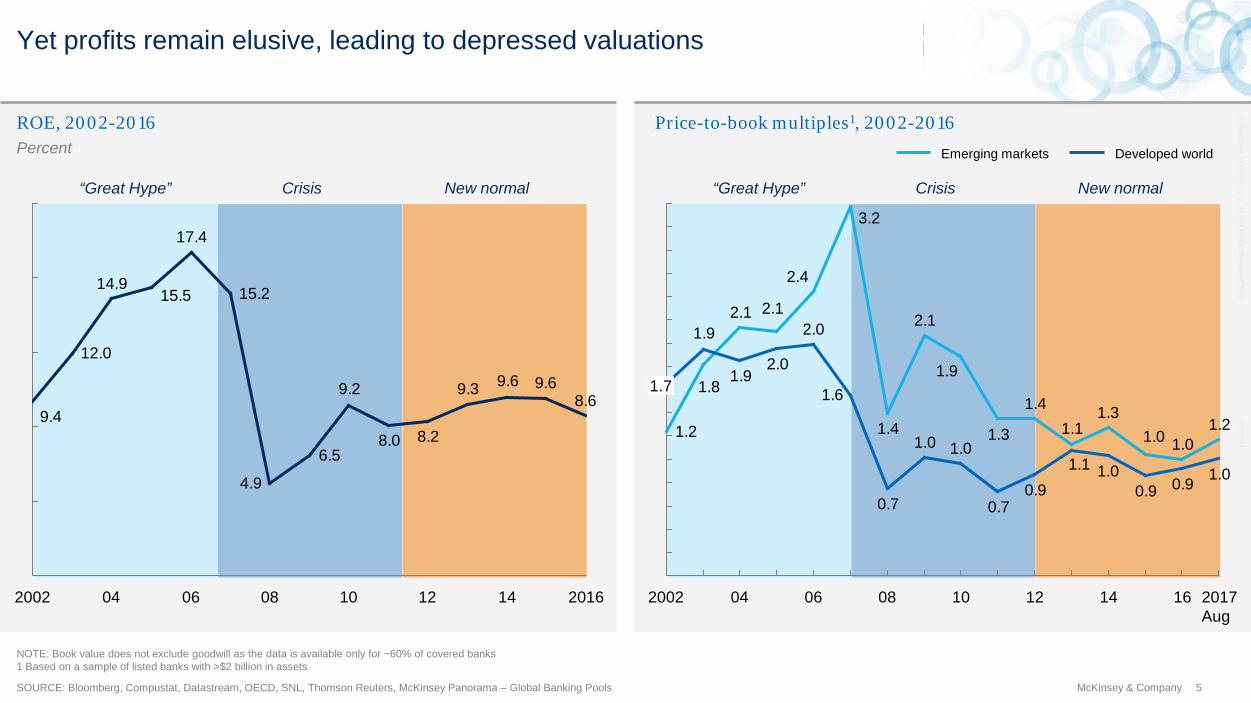

“Great Hype” Crisis New normal “Great Hype” Crisis New normal

ROE, 2002-2016 Percent

Price-to-book multiples1, 2002-2016

Yet profits remain elusive, leading to depressed valuations

8.69.69.69.3

8.28.0

9.2

6.5

4.9

15.2

17.4

14.9

12.0

9.4

15.5

08 10 06 12 04 2002 2016 14

Developed world Emerging markets

SOURCE: Bloomberg, Compustat, Datastream, OECD, SNL, Thomson Reuters, McKinsey Panorama – Global Banking Pools

NOTE: Book value does not exclude goodwill as the data is available only for ~60% of covered banks 1 Based on a sample of listed banks with >$2 billion in assets

1.21.01.0

1.31.1

1.4

1.9

2.1

1.4

3.2

2.12.1

1.8

1.2 1.3

2.4

1.00.90.91.0

0.90.7

1.01.0

0.7

1.6

2.0

2.01.9

1.9

1.1

08

1.7

04 2002 06 12 2017 Aug

14 16 10

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

6 McKinsey & Company SOURCE: SNL, McKinsey Panorama – Global Banking Pools

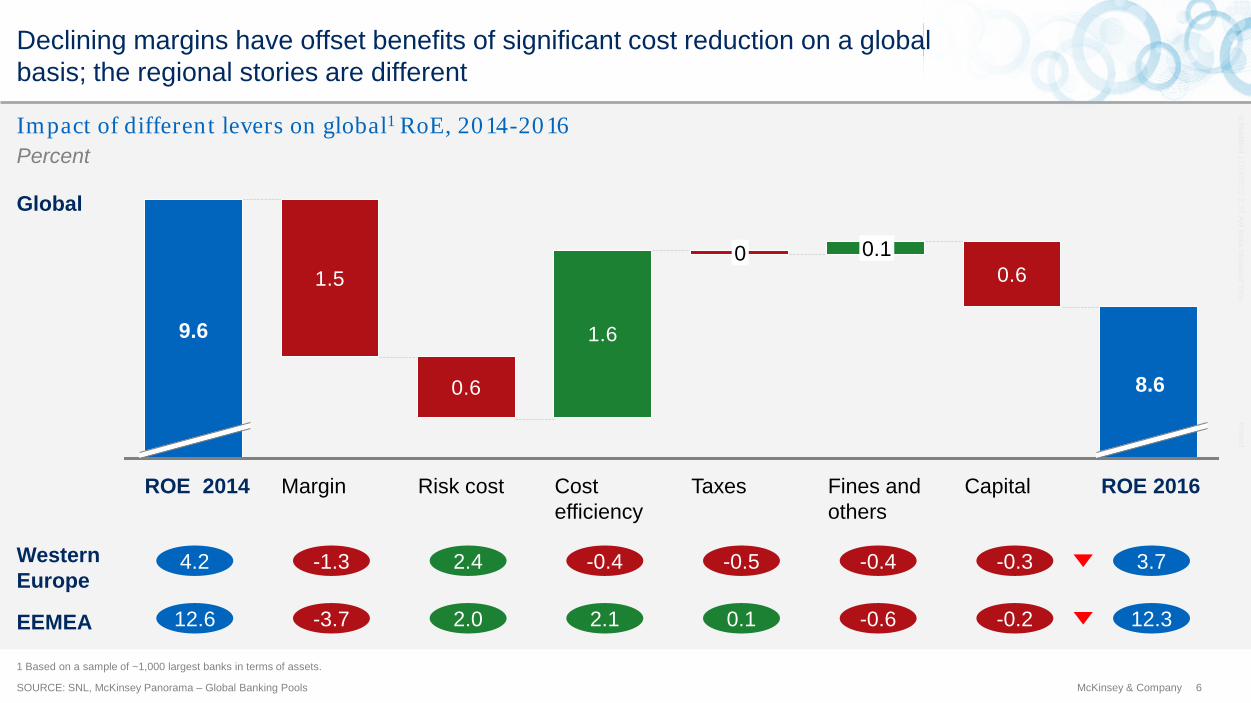

Impact of different levers on global1 RoE, 2014-2016 Percent

EEMEA

Western Europe

-1.3

-3.7

2.4

2.0

-0.4

2.1

-0.5

0.1

-0.4

-0.6

-0.3

-0.2

4.2

12.6

3.7

12.3

Global

1.5

0.6

1.6

0.6

8.6

Capital Risk cost ROE 2016 Taxes

0

Margin Fines and others

9.6

ROE 2014

0.1

Cost efficiency

1 Based on a sample of ~1,000 largest banks in terms of assets.

Declining margins have offset benefits of significant cost reduction on a global basis; the regional stories are different

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

7 McKinsey & Company

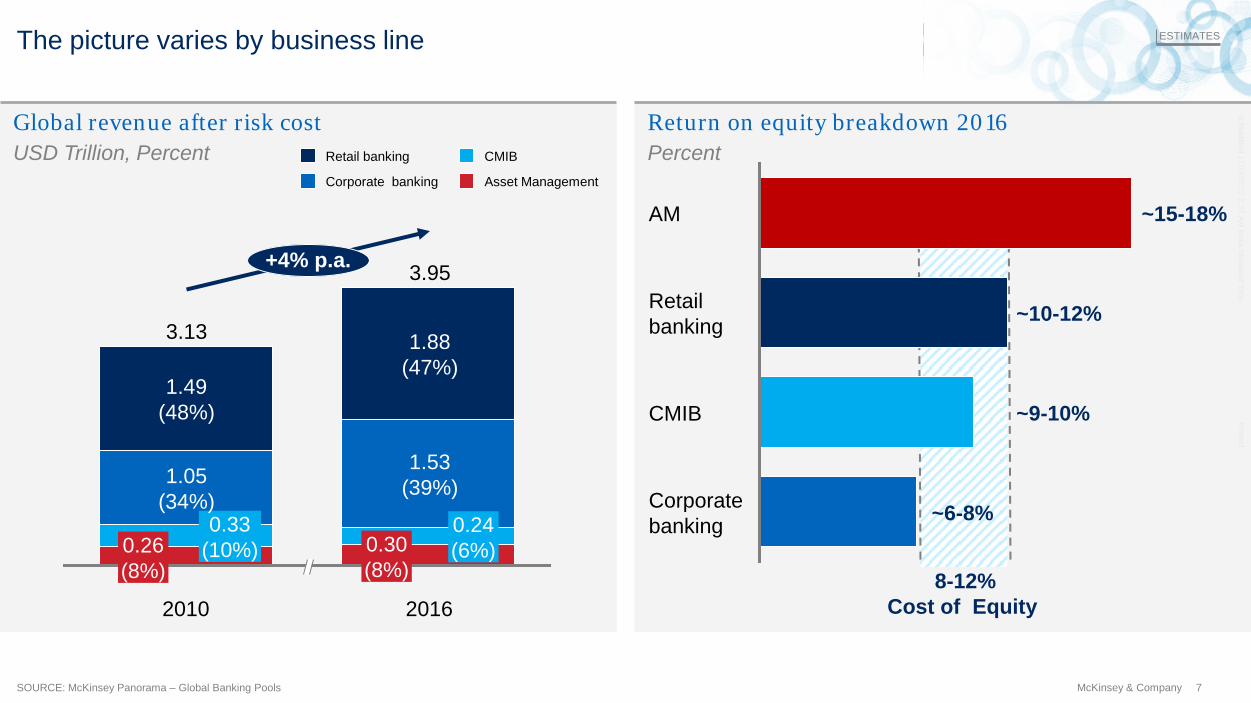

The picture varies by business line

SOURCE: McKinsey Panorama – Global Banking Pools

2016

0.30 (8%)

2010

+4% p.a.

0.33 (10%)

1.49 (48%)

0.24 (6%)

1.53 (39%)

1.88 (47%)

3.13

0.26 (8%)

1.05 (34%)

3.95

Asset Management Corporate banking

CMIB Retail banking

ESTIMATES

USD Trillion, Percent Global revenue after risk cost Return on equity breakdown 2016

Percent

~15-18%

8-12% Cost of Equity

Corporate banking

Retail banking

CMIB

AM

~10-12%

~9-10%

~6-8%

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

8 McKinsey & Company

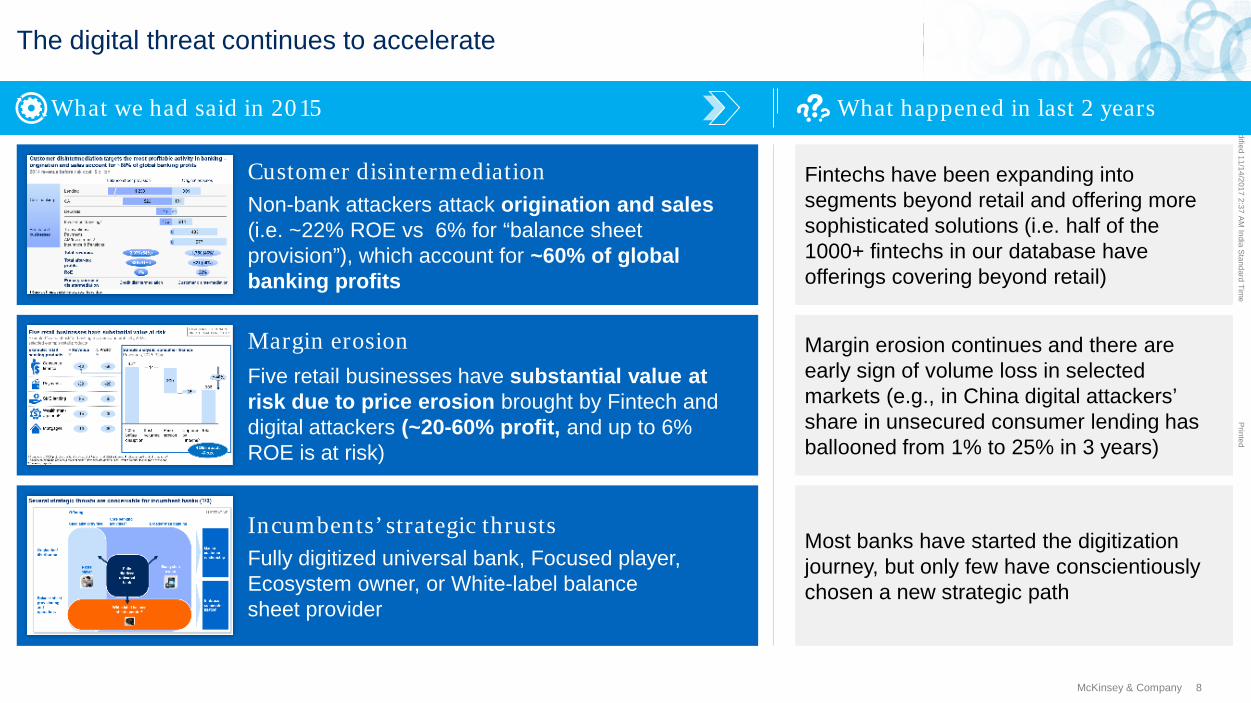

The digital threat continues to accelerate

What we had said in 2015 What happened in last 2 years

Fintechs have been expanding into segments beyond retail and offering more sophisticated solutions (i.e. half of the 1000+ fintechs in our database have offerings covering beyond retail)

Margin erosion continues and there are early sign of volume loss in selected markets (e.g., in China digital attackers’ share in unsecured consumer lending has ballooned from 1% to 25% in 3 years)

Most banks have started the digitization journey, but only few have conscientiously chosen a new strategic path

Customer disintermediation Non-bank attackers attack origination and sales (i.e. ~22% ROE vs 6% for “balance sheet provision”), which account for ~60% of global banking profits

Margin erosion Five retail businesses have substantial value at risk due to price erosion brought by Fintech and digital attackers (~20-60% profit, and up to 6% ROE is at risk)

Incumbents’ strategic thrusts Fully digitized universal bank, Focused player, Ecosystem owner, or White-label balance sheet provider

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

9 McKinsey & Company

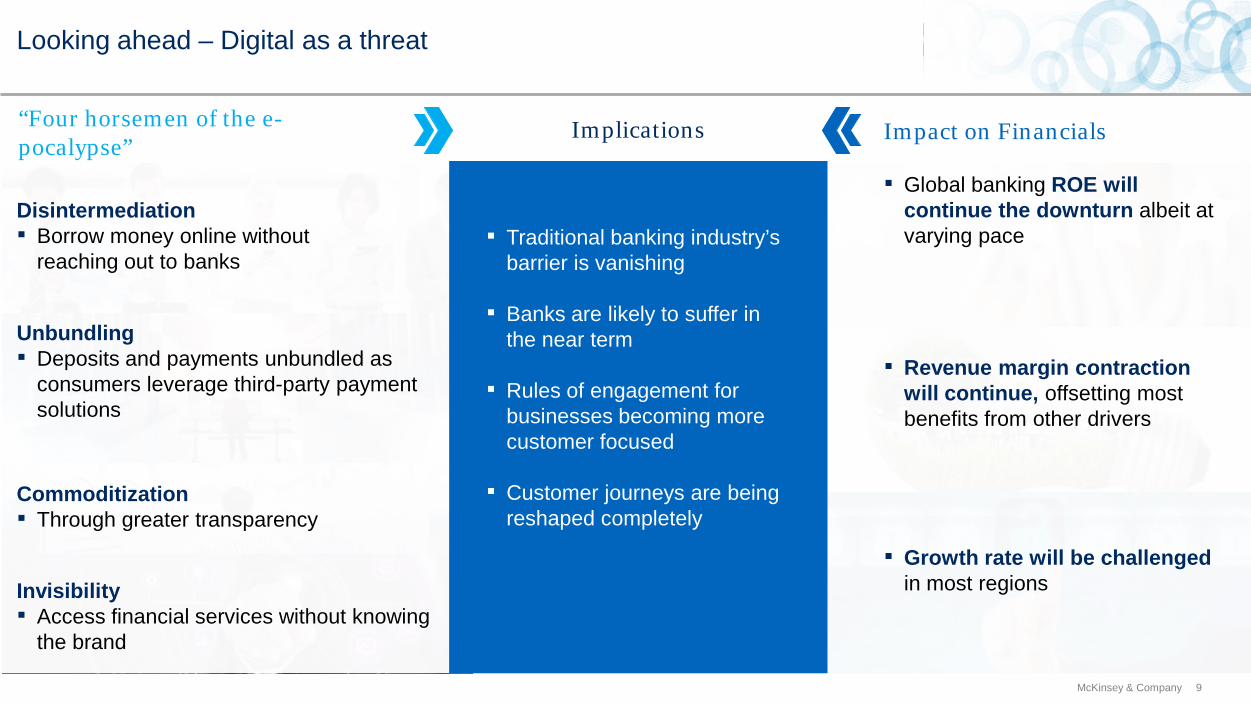

Looking ahead – Digital as a threat

▪ Traditional banking industry’s barrier is vanishing

▪ Banks are likely to suffer in the near term

▪ Rules of engagement for businesses becoming more customer focused

▪ Customer journeys are being reshaped completely

Implications “Four horsemen of the e-pocalypse”

Impact on Financials

▪ Global banking ROE will continue the downturn albeit at varying pace

▪ Revenue margin contraction will continue, offsetting most benefits from other drivers

▪ Growth rate will be challenged in most regions Invisibility

▪ Access financial services without knowing the brand

Commoditization ▪ Through greater transparency

Unbundling ▪ Deposits and payments unbundled as

consumers leverage third-party payment solutions

Disintermediation ▪ Borrow money online without

reaching out to banks

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

Agenda

10 McKinsey & Company

State of the industry

Digital and AA at scale

Eco-systems?

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

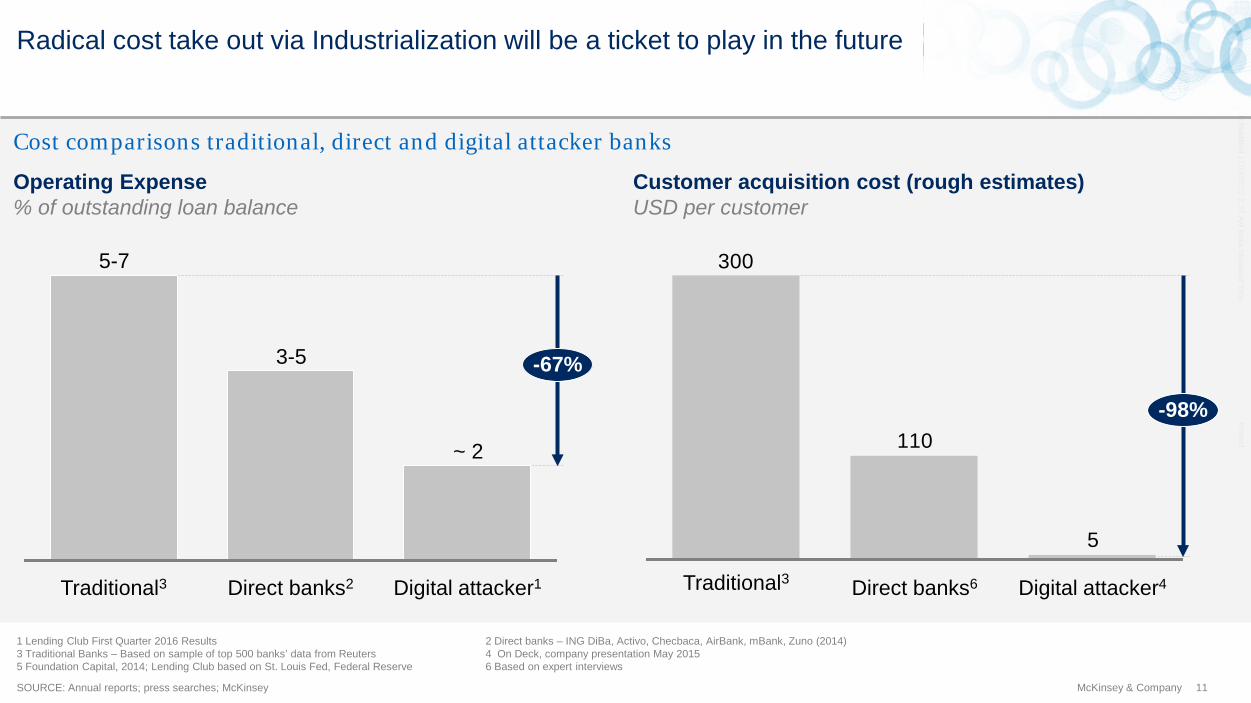

11 McKinsey & Company SOURCE: Annual reports; press searches; McKinsey

~ 2

-67%

Digital attacker1 Direct banks2

3-5

Traditional3

5-7

5

110

300

Direct banks6

-98%

Digital attacker4 Traditional3

Operating Expense % of outstanding loan balance

Customer acquisition cost (rough estimates) USD per customer

1 Lending Club First Quarter 2016 Results 2 Direct banks – ING DiBa, Activo, Checbaca, AirBank, mBank, Zuno (2014) 3 Traditional Banks – Based on sample of top 500 banks’ data from Reuters 4 On Deck, company presentation May 2015 5 Foundation Capital, 2014; Lending Club based on St. Louis Fed, Federal Reserve 6 Based on expert interviews

Radical cost take out via Industrialization will be a ticket to play in the future

Cost comparisons traditional, direct and digital attacker banks

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

12 McKinsey & Company

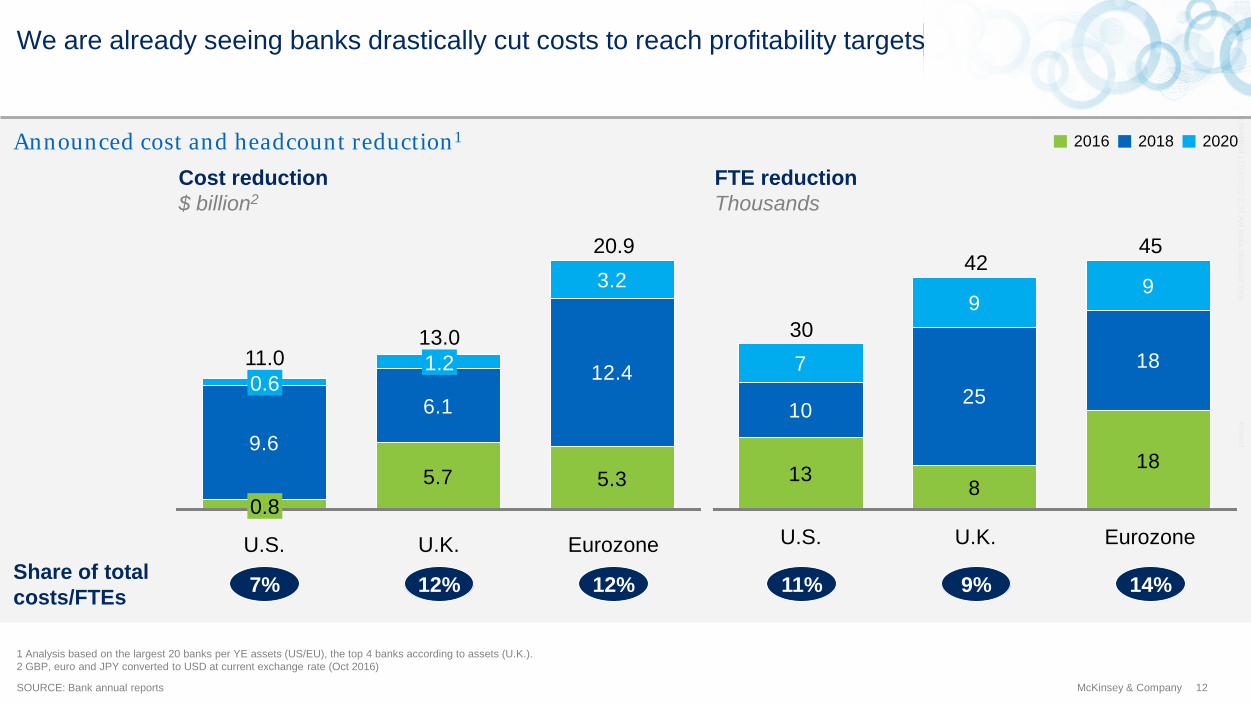

We are already seeing banks drastically cut costs to reach profitability targets

SOURCE: Bank annual reports

Cost reduction $ billion2

FTE reduction Thousands

5.7 5.3

9.6

6.112.4

3.2

U.S. U.K.

0.8

1.2

20.9

11.0 13.0

Eurozone

0.6

138

18

1025

187

99

45

Eurozone U.S.

30

42

U.K.

1 Analysis based on the largest 20 banks per YE assets (US/EU), the top 4 banks according to assets (U.K.). 2 GBP, euro and JPY converted to USD at current exchange rate (Oct 2016)

7% 12% 12% 11% 9% 14% Share of total costs/FTEs

2016 2018 2020 Announced cost and headcount reduction1

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

13 McKinsey & Company

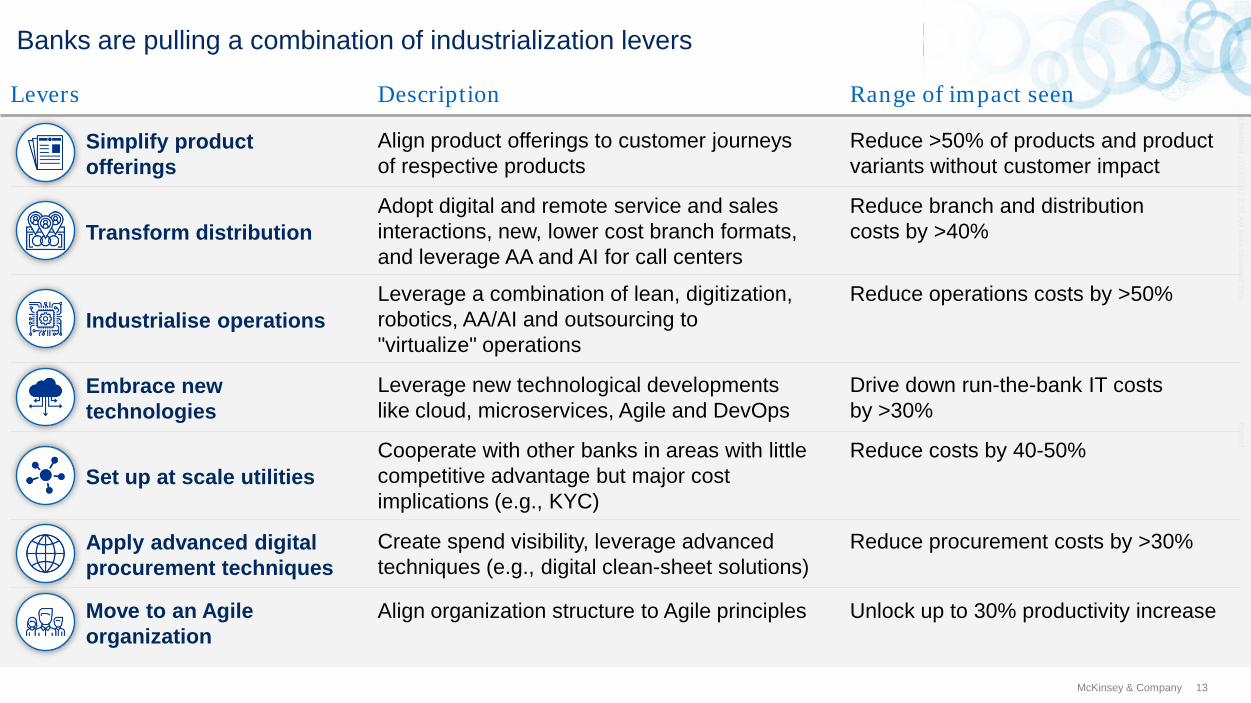

Banks are pulling a combination of industrialization levers

Levers

Industrialise operations Reduce operations costs by >50%

Embrace new technologies

Drive down run-the-bank IT costs by >30%

Set up at scale utilities Reduce costs by 40-50%

Apply advanced digital procurement techniques

Reduce procurement costs by >30%

Move to an Agile organization

Unlock up to 30% productivity increase

Transform distribution Reduce branch and distribution costs by >40%

Description

Leverage a combination of lean, digitization, robotics, AA/AI and outsourcing to "virtualize" operations

Leverage new technological developments like cloud, microservices, Agile and DevOps

Cooperate with other banks in areas with little competitive advantage but major cost implications (e.g., KYC)

Create spend visibility, leverage advanced techniques (e.g., digital clean-sheet solutions)

Align organization structure to Agile principles

Adopt digital and remote service and sales interactions, new, lower cost branch formats, and leverage AA and AI for call centers

Align product offerings to customer journeys of respective products

Simplify product offerings

Reduce >50% of products and product variants without customer impact

Range of impact seen

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

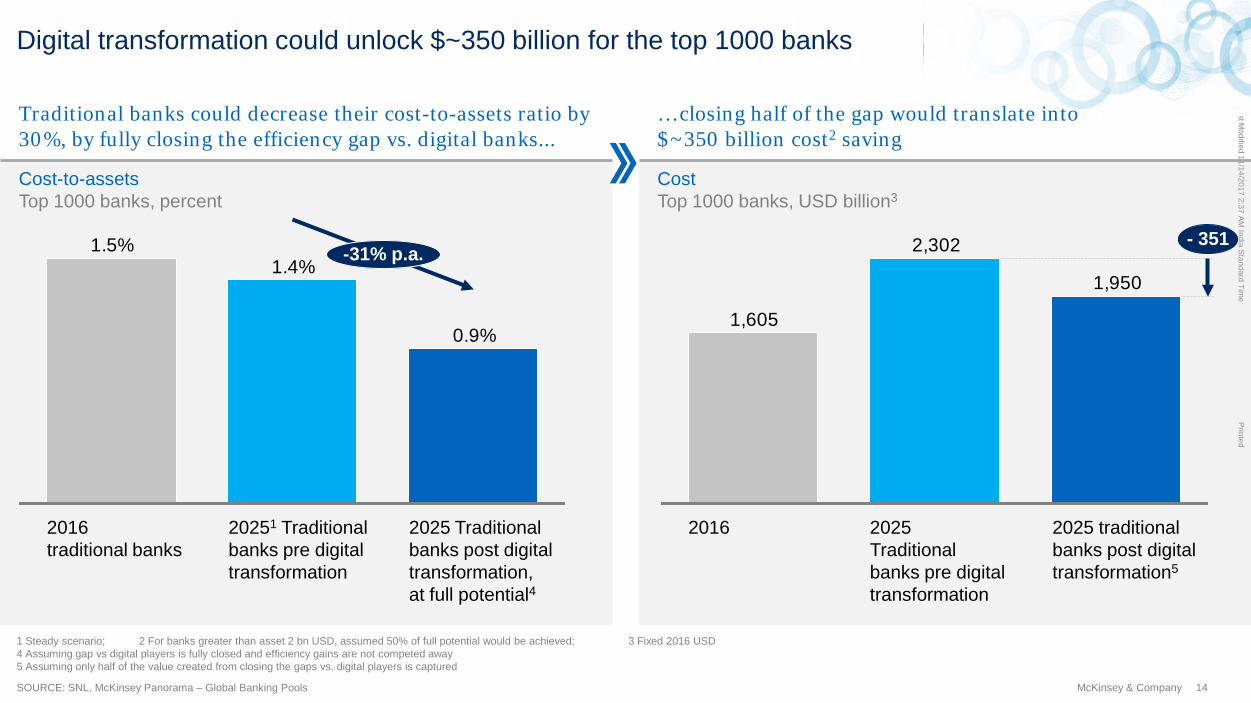

14 McKinsey & Company

0.9%

1.4%1.5%

2025 Traditional banks post digital transformation, at full potential4

-31% p.a.

2016 traditional banks

20251 Traditional banks pre digital transformation

1,950

2,302

1,605

2016 2025 Traditional banks pre digital transformation

2025 traditional banks post digital transformation5

- 351

1 Steady scenario; 2 For banks greater than asset 2 bn USD, assumed 50% of full potential would be achieved; 3 Fixed 2016 USD 4 Assuming gap vs digital players is fully closed and efficiency gains are not competed away 5 Assuming only half of the value created from closing the gaps vs. digital players is captured

SOURCE: SNL, McKinsey Panorama – Global Banking Pools

Digital transformation could unlock $~350 billion for the top 1000 banks

Cost-to-assets Top 1000 banks, percent

Cost Top 1000 banks, USD billion3

Traditional banks could decrease their cost-to-assets ratio by 30%, by fully closing the efficiency gap vs. digital banks...

… closing half of the gap would translate into $~350 billion cost2 saving

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

Agenda

15 McKinsey & Company

State of the industry

Digital and AA at scale

Eco-systems?

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

16 McKinsey & Company

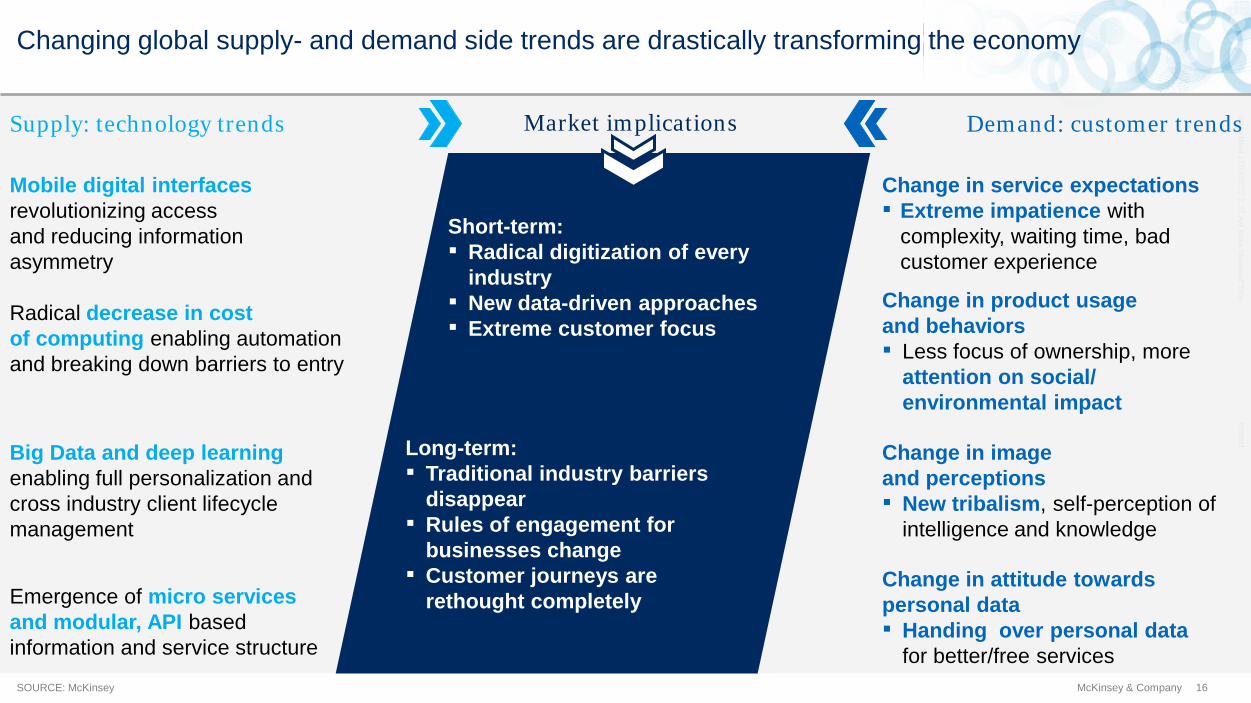

Changing global supply- and demand side trends are drastically transforming the economy

Supply: technology trends Demand: customer trends

Radical decrease in cost of computing enabling automation and breaking down barriers to entry

Change in product usage and behaviors ▪ Less focus of ownership, more

attention on social/ environmental impact

Big Data and deep learning enabling full personalization and cross industry client lifecycle management

Change in image and perceptions ▪ New tribalism, self-perception of

intelligence and knowledge

Mobile digital interfaces revolutionizing access and reducing information asymmetry

Change in service expectations ▪ Extreme impatience with

complexity, waiting time, bad customer experience

Short-term: ▪ Radical digitization of every

industry ▪ New data-driven approaches ▪ Extreme customer focus

Long-term: ▪ Traditional industry barriers

disappear ▪ Rules of engagement for

businesses change ▪ Customer journeys are

rethought completely

Market implications

Emergence of micro services and modular, API based information and service structure

Change in attitude towards personal data ▪ Handing over personal data

for better/free services SOURCE: McKinsey

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

17 McKinsey & Company

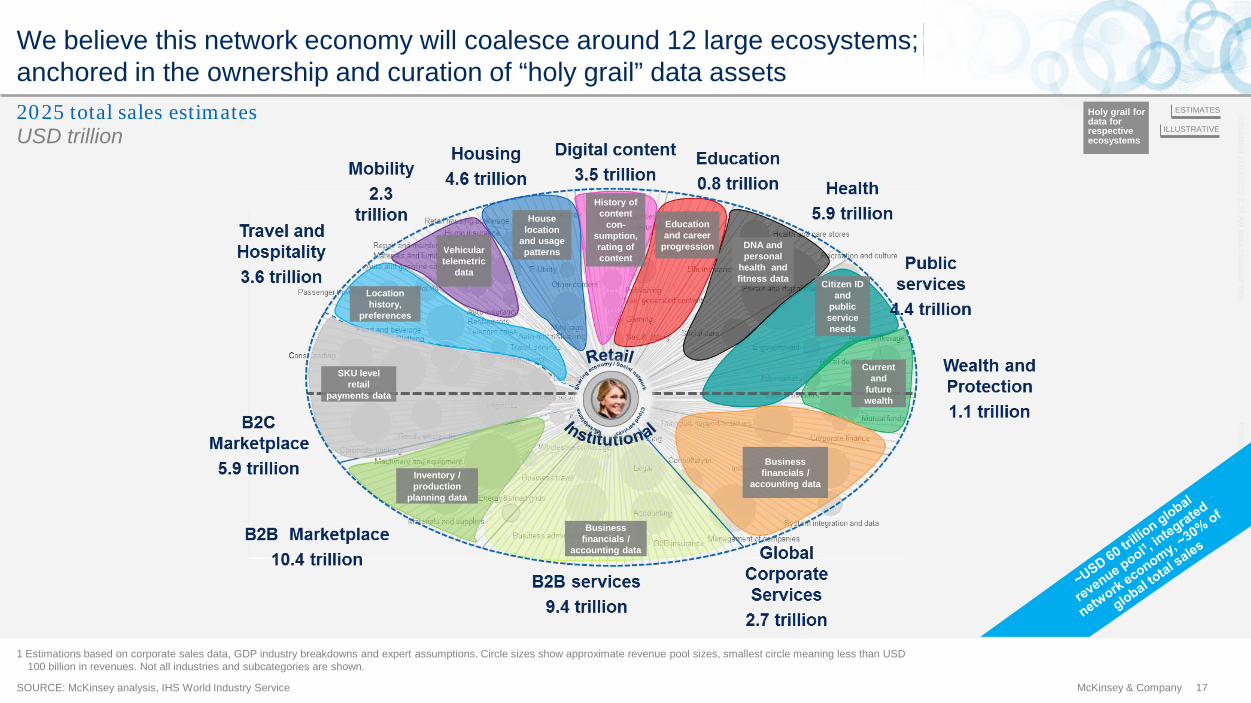

We believe this network economy will coalesce around 12 large ecosystems; anchored in the ownership and curation of “holy grail” data assets

SOURCE: McKinsey analysis, IHS World Industry Service

USD trillion 2025 total sales estimates

SKU level retail

payments data

House location

and usage patterns

History of content

con-sumption, rating of content

DNA and personal

health and fitness data

Inventory / production

planning data

Business financials /

accounting data

Vehicular telemetric

data

Education and career

progression

Citizen ID and

public service needs

Current and

future wealth

Business financials /

accounting data

Location history,

preferences

ILLUSTRATIVE

Holy grail for data for respective ecosystems

ESTIMATES

1 Estimations based on corporate sales data, GDP industry breakdowns and expert assumptions. Circle sizes show approximate revenue pool sizes, smallest circle meaning less than USD 100 billion in revenues. Not all industries and subcategories are shown.

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

18 McKinsey & Company

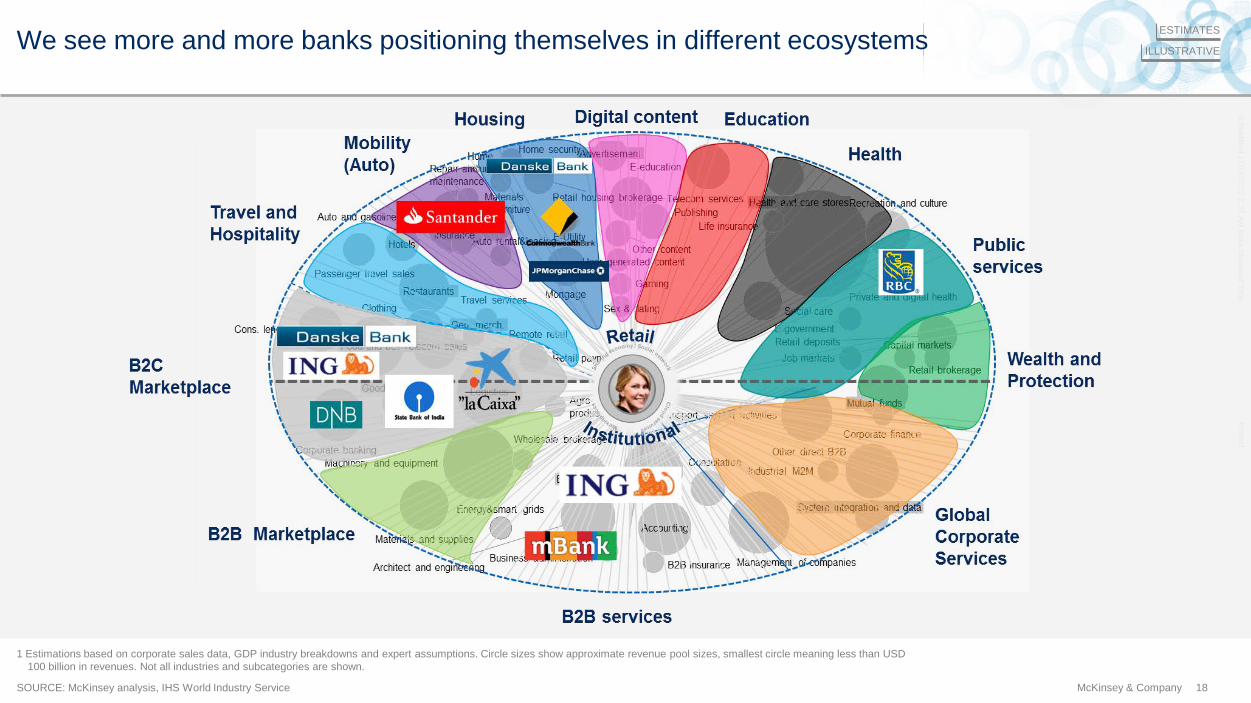

We see more and more banks positioning themselves in different ecosystems

SOURCE: McKinsey analysis, IHS World Industry Service

ILLUSTRATIVE

ESTIMATES

1 Estimations based on corporate sales data, GDP industry breakdowns and expert assumptions. Circle sizes show approximate revenue pool sizes, smallest circle meaning less than USD 100 billion in revenues. Not all industries and subcategories are shown.

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

19 McKinsey & Company

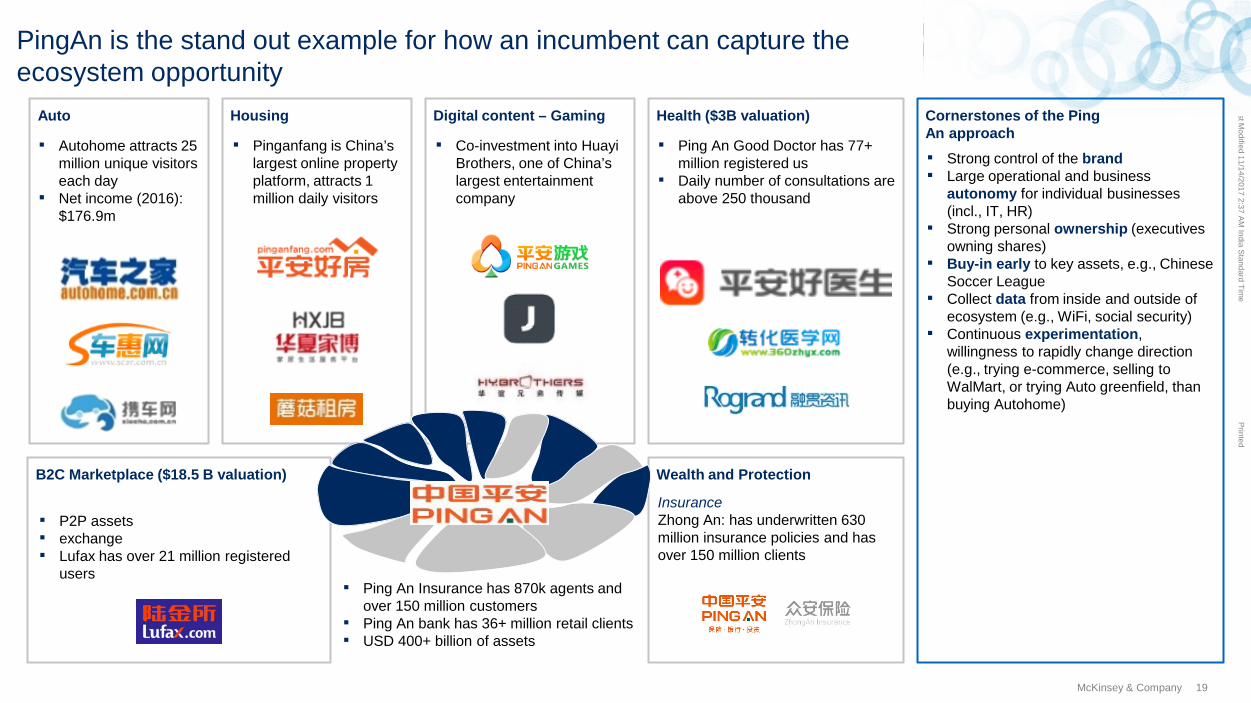

PingAn is the stand out example for how an incumbent can capture the ecosystem opportunity

Cornerstones of the Ping An approach

Housing

Wealth and Protection

Health ($3B valuation) Digital content – Gaming Auto

B2C Marketplace ($18.5 B valuation)

Insurance Zhong An: has underwritten 630 million insurance policies and has over 150 million clients

▪ Ping An Good Doctor has 77+ million registered us

▪ Daily number of consultations are above 250 thousand

▪ Co-investment into Huayi Brothers, one of China’s largest entertainment company

▪ Pinganfang is China’s largest online property platform, attracts 1 million daily visitors

▪ Autohome attracts 25 million unique visitors each day

▪ Net income (2016): $176.9m

▪ P2P assets ▪ exchange ▪ Lufax has over 21 million registered

users ▪ Ping An Insurance has 870k agents and

over 150 million customers ▪ Ping An bank has 36+ million retail clients ▪ USD 400+ billion of assets

▪ Strong control of the brand ▪ Large operational and business

autonomy for individual businesses (incl., IT, HR)

▪ Strong personal ownership (executives owning shares)

▪ Buy-in early to key assets, e.g., Chinese Soccer League

▪ Collect data from inside and outside of ecosystem (e.g., WiFi, social security)

▪ Continuous experimentation, willingness to rapidly change direction (e.g., trying e-commerce, selling to WalMart, or trying Auto greenfield, than buying Autohome)

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

20 McKinsey & Company

Banks must critically assess 4 areas before embarking on an ecosystem journey

1 2 3

4

How to set up critical building blocks?

How to monetize your ecosystem play?

What ecosystem play to follow?

Where to play?

Choose the right ecosystems and customer journeys to play in (e.g. Participate, Partner, Orchestrate or Build)

Different monetization options depending on P&L focus:

– Volume – Margin – Cross-sell – Non-banking

revenues

Critical building blocks include:

– Ecosystem offering – Customer

relationship – Data and analytics – Partnerships

Choice between a participatory, orchestrator or owner strategy

Last Modified 11/14/2017 2:37 AM

India Standard Time

Printed

21 McKinsey & Company

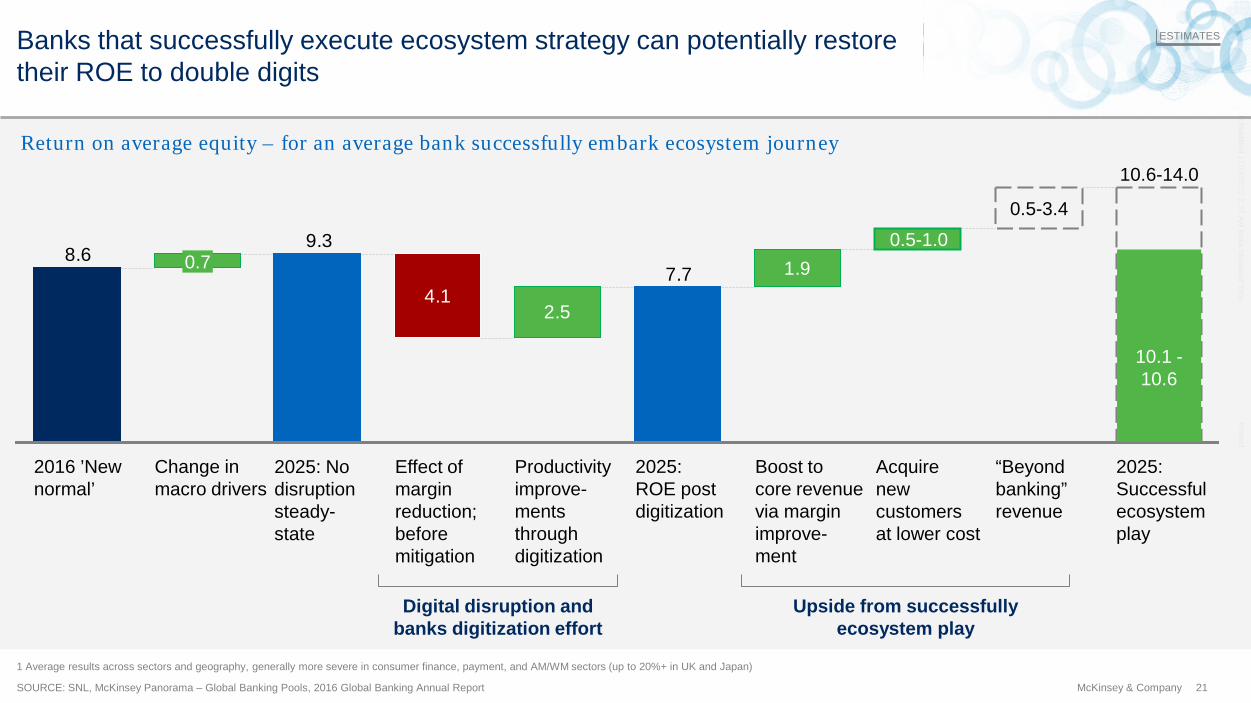

Banks that successfully execute ecosystem strategy can potentially restore their ROE to double digits

SOURCE: SNL, McKinsey Panorama – Global Banking Pools, 2016 Global Banking Annual Report

1 Average results across sectors and geography, generally more severe in consumer finance, payment, and AM/WM sectors (up to 20%+ in UK and Japan)

ESTIMATES

Upside from successfully ecosystem play

Return on average equity – for an average bank successfully embark ecosystem journey

7.7

9.38.6

1.9

2.54.1

Boost to core revenue via margin improve- ment

0.5-1.0 0.7

2025: ROE post digitization

Change in macro drivers

2016 ’New normal’

2025: Successful ecosystem play

Productivity improve-ments through digitization

10.6-14.0

“Beyond banking” revenue

0.5-3.4

Acquire new customers at lower cost

Effect of margin reduction; before mitigation

2025: No disruption steady- state

10.1 -10.6

Digital disruption and banks digitization effort