the belknap press of harvard university press cambridge, mass. - 2014

TRANSCRIPT

The Belknap Press of Harvard University Press Cambridge, Mass. - 2014

The Major Results of This Study

First, one should be wary of any economic determinism in regard to inequalities of wealth and income. The history of the distribution of wealth has always been deeply political, and it cannot be reduced to purely economic mechanism.Second, the dynamics of wealth distribution reveal powerful mechanisms pushing alternately toward convergence and divergence. Furthermore, there is no natural, spontaneous process to prevent destabilizing, inegalitarian forces from prevailing permanently.

Convergence

The main forces for convergence are the diffusion of knowledge and investment in training and skills. The law of supply and demand, as well as the mobility of capital and labour, which is a variant of that law, may always tend toward convergence as well, but their influence is less powerful than the diffusion of knowledge and skill. By adopting the modes of production of the rich countries and acquiring skills comparable to those found elsewhere, the less developed countries have leapt forward in productivity and increased their national incomes. The Technological convergence process may be abetted by open borders for trade, but it is fundamentally a process of the diffusion and sharing of knowledge – the public good par excellence – rather than a market mechanism.

Forces of divergence

First, top earners can quickly separate themselves from the rest by a wide margin.Second, there is a set of forces of divergence associated with the process of accumulation and concentration of wealth when growth is weak and the return on capital is high. This second process is potentially more destabilizing than the first, and it no doubt represents the principal threat to an equal distribution of wealth over the long run.

Two basic patterns

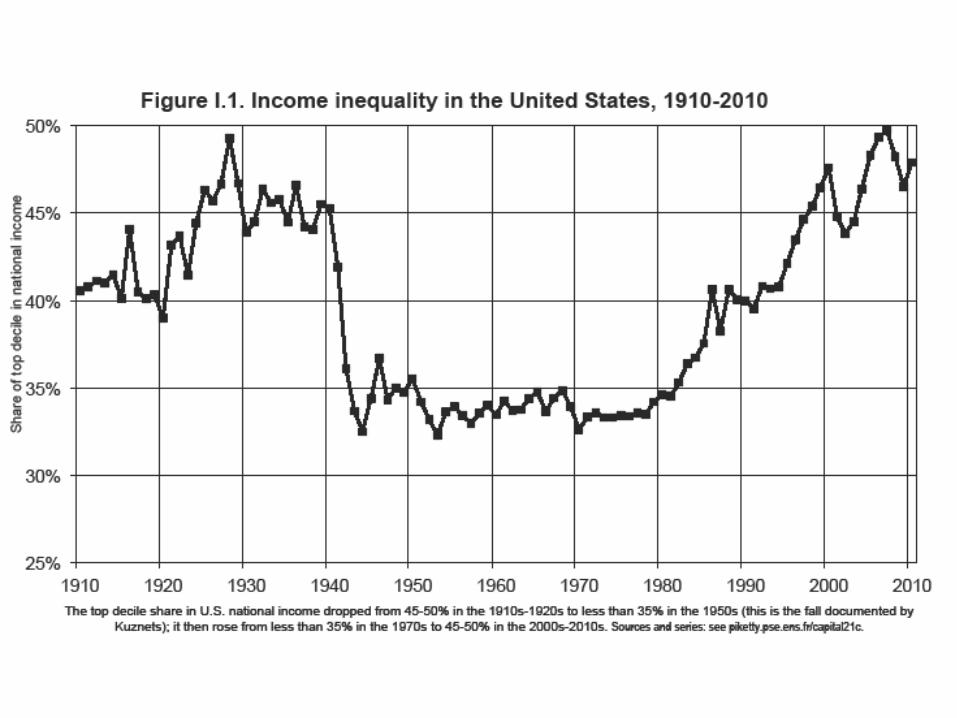

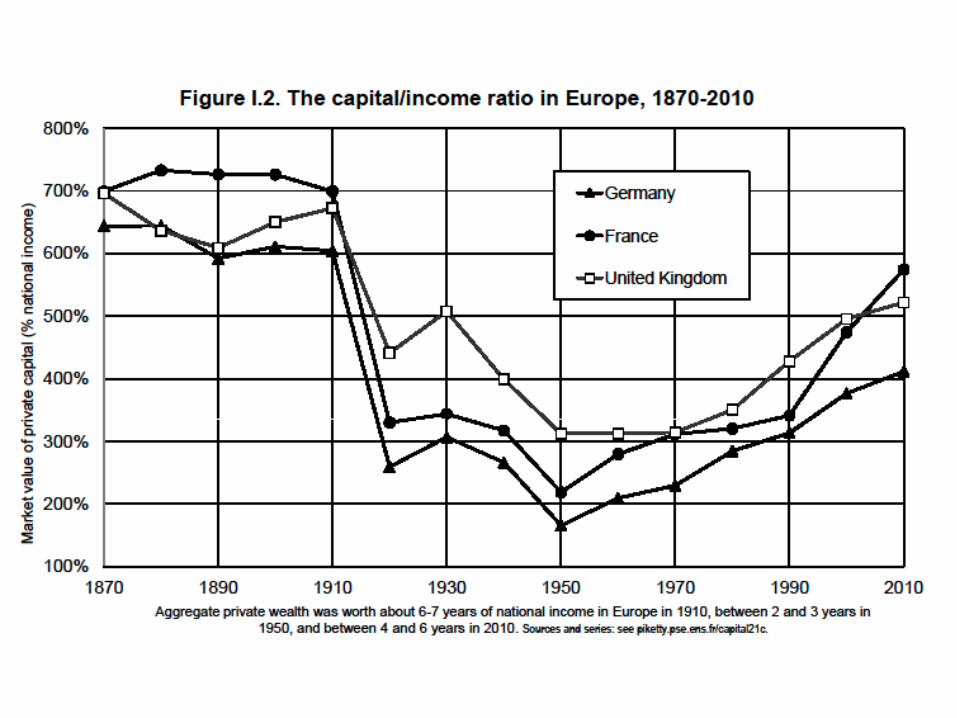

Fig. I.1 and I.2 show two basic patterns. Each graph represents the importance of one of these divergent processes. Both graph depict “U-shaped curves” that is, a period of decreasing inequality followed by one of increasing inequality. One might assume that the realities the two graphs represent are similar. In fact they are not. The phenomena underlying the various curves are quit different and involve distinct economic, social, and political processes. Fig. I.1 represents income inequality in the United States, while the curves in Fig. I.2 depict the capital/income ratio in several European countries (Japan is similar).

Two forces of divergence

In Fig. I. 1 the spectacular increase in inequality largely reflects an unprecedented explosion of top managers of large firms from the rest of the population. One possible explanation is that the skills and productivity of these top managers rose suddenly in relation to those of other workers. Another explanation is that these top managers by and large have the power to set their own remunerations.In Fig. I. 2, the “U-shaped curve” reflects an absolutely crucial transformation. The return of high capital/income ratios over the past few decades can be explained in large part by the return to a regime of relatively slow growth. In slowly growing economies, past wealth naturally takes on disproportionate importance, because it takes only a small flow of new savings to increase the stock of wealth steadily and substantially. The fundamental inequality r>g will play a crucial role. When the rate of return on capital significantly exceeds to growth rate of the economy, than it logically follows that inherited wealth grows faster than output and income. Inherited wealth will dominate wealth amassed from a lifetime’s labour.

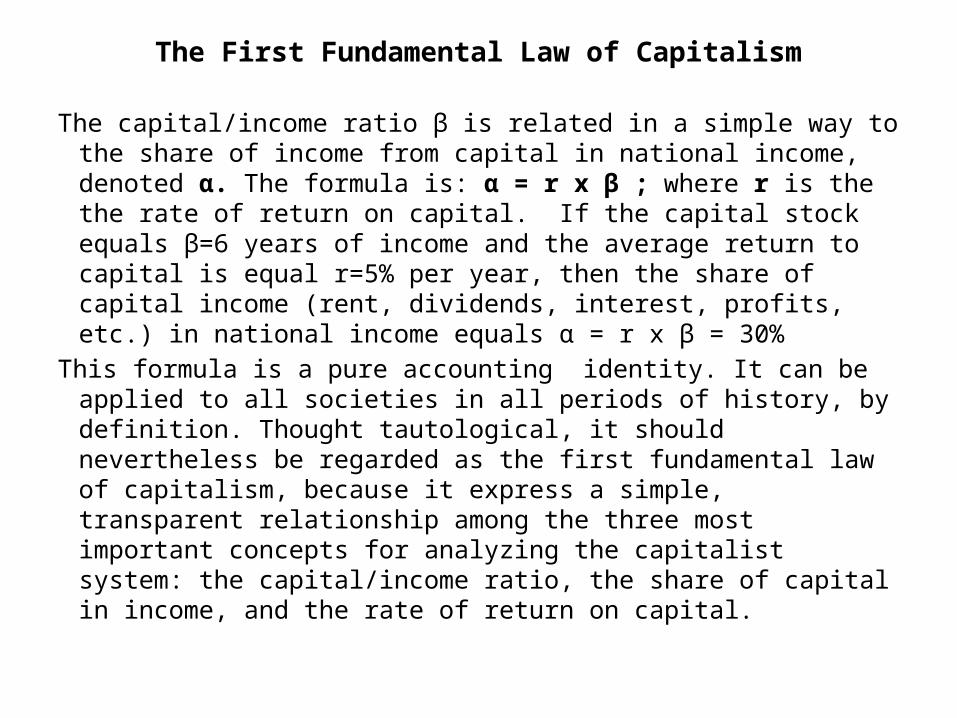

The First Fundamental Law of Capitalism

The capital/income ratio β is related in a simple way to the share of income from capital in national income, denoted α. The formula is: α = r x β ; where r is the the rate of return on capital. If the capital stock equals β=6 years of income and the average return to capital is equal r=5% per year, then the share of capital income (rent, dividends, interest, profits, etc.) in national income equals α = r x β = 30%

This formula is a pure accounting identity. It can be applied to all societies in all periods of history, by definition. Thought tautological, it should nevertheless be regarded as the first fundamental law of capitalism, because it express a simple, transparent relationship among the three most important concepts for analyzing the capitalist system: the capital/income ratio, the share of capital in income, and the rate of return on capital.

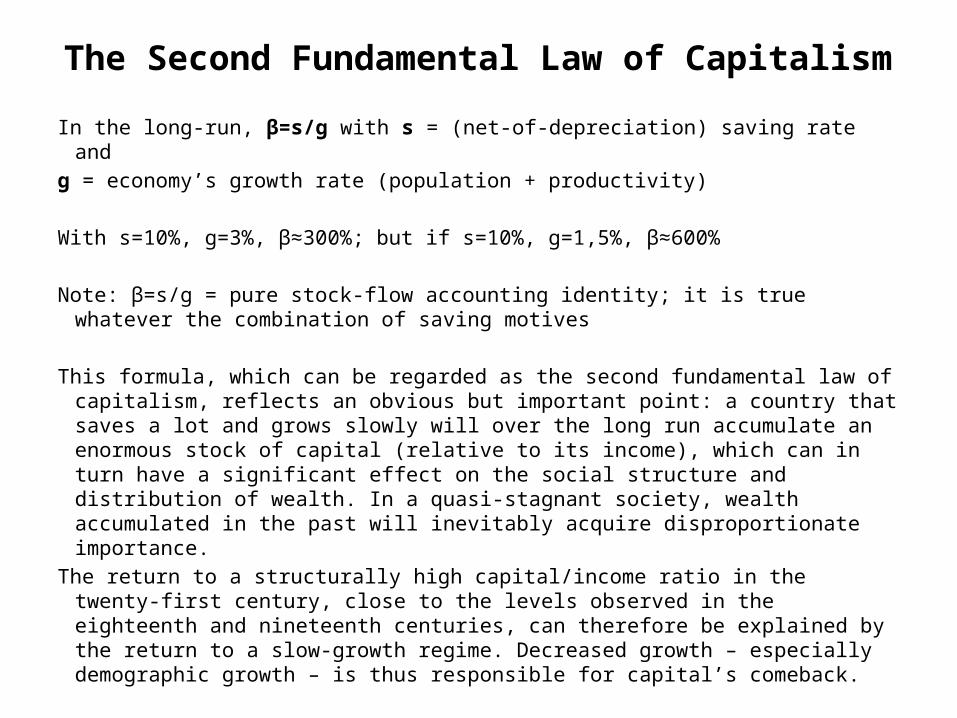

The Second Fundamental Law of Capitalism

In the long-run, β=s/g with s = (net-of-depreciation) saving rate and g = economy’s growth rate (population + productivity) With s=10%, g=3%, β≈300%; but if s=10%, g=1,5%, β≈600%

Note: β=s/g = pure stock-flow accounting identity; it is true whatever the combination of saving motives

This formula, which can be regarded as the second fundamental law of capitalism, reflects an obvious but important point: a country that saves a lot and grows slowly will over the long run accumulate an enormous stock of capital (relative to its income), which can in turn have a significant effect on the social structure and distribution of wealth. In a quasi-stagnant society, wealth accumulated in the past will inevitably acquire disproportionate importance.

The return to a structurally high capital/income ratio in the twenty-first century, close to the levels observed in the eighteenth and nineteenth centuries, can therefore be explained by the return to a slow-growth regime. Decreased growth – especially demographic growth – is thus responsible for capital’s comeback.

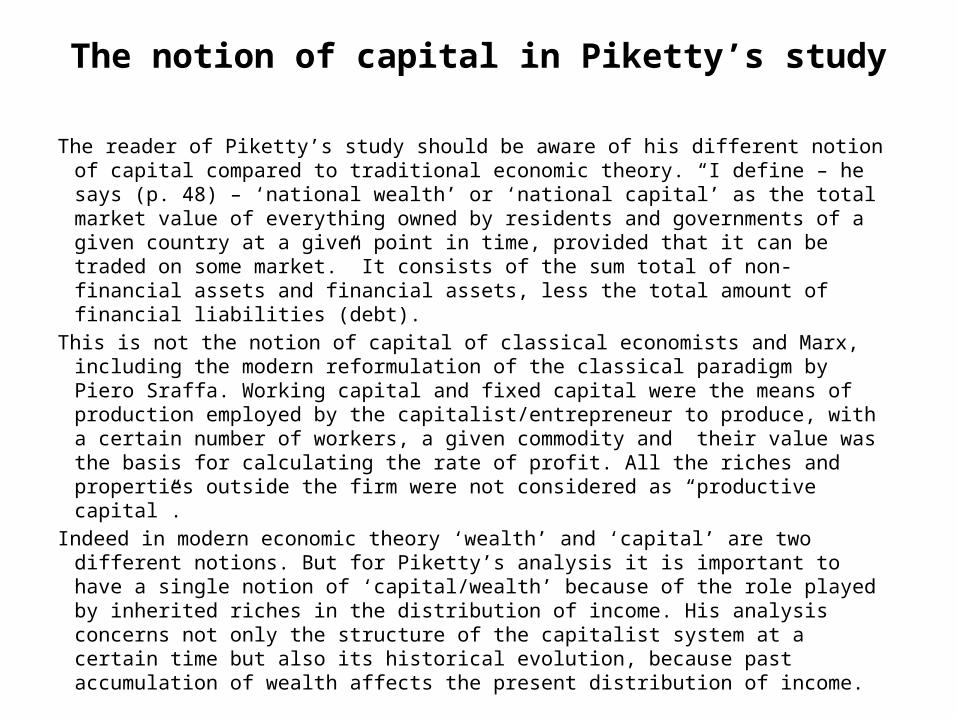

The notion of capital in Piketty’s study

The reader of Piketty’s study should be aware of his different notion of capital compared to traditional economic theory. “I define – he says (p. 48) – ‘national wealth’ or ‘national capital’ as the total market value of everything owned by residents and governments of a given country at a given point in time, provided that it can be traded on some market.” It consists of the sum total of non-financial assets and financial assets, less the total amount of financial liabilities (debt).

This is not the notion of capital of classical economists and Marx, including the modern reformulation of the classical paradigm by Piero Sraffa. Working capital and fixed capital were the means of production employed by the capitalist/entrepreneur to produce, with a certain number of workers, a given commodity and their value was the basis for calculating the rate of profit. All the riches and properties outside the firm were not considered as “productive capital”.

Indeed in modern economic theory ‘wealth’ and ‘capital’ are two different notions. But for Piketty’s analysis it is important to have a single notion of ‘capital/wealth’ because of the role played by inherited riches in the distribution of income. His analysis concerns not only the structure of the capitalist system at a certain time but also its historical evolution, because past accumulation of wealth affects the present distribution of income.

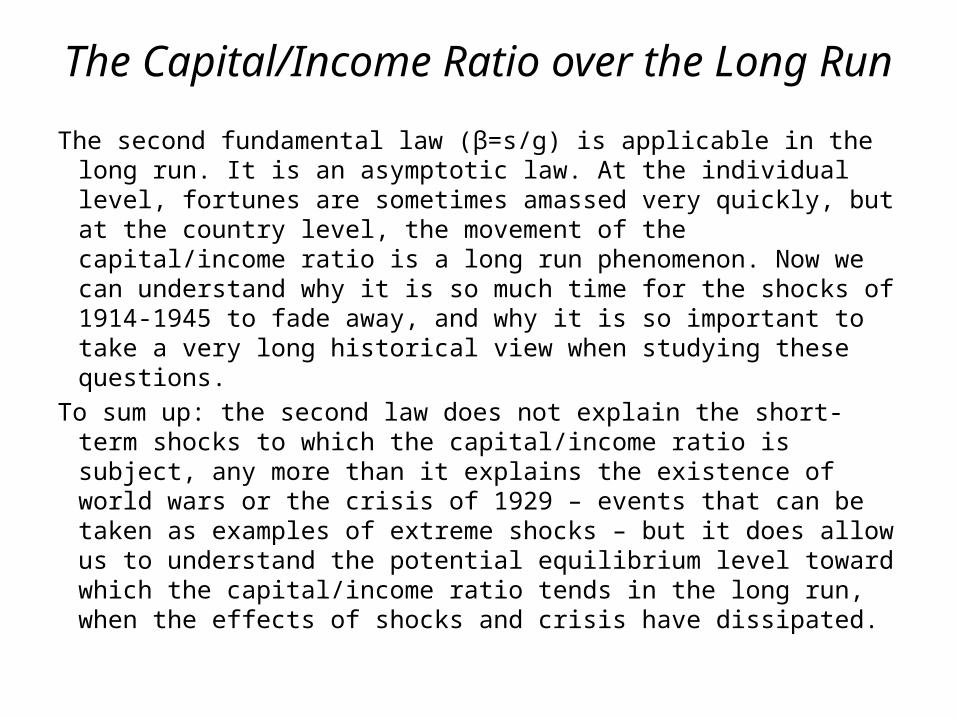

The Capital/Income Ratio over the Long Run

The second fundamental law (β=s/g) is applicable in the long run. It is an asymptotic law. At the individual level, fortunes are sometimes amassed very quickly, but at the country level, the movement of the capital/income ratio is a long run phenomenon. Now we can understand why it is so much time for the shocks of 1914-1945 to fade away, and why it is so important to take a very long historical view when studying these questions.

To sum up: the second law does not explain the short-term shocks to which the capital/income ratio is subject, any more than it explains the existence of world wars or the crisis of 1929 – events that can be taken as examples of extreme shocks – but it does allow us to understand the potential equilibrium level toward which the capital/income ratio tends in the long run, when the effects of shocks and crisis have dissipated.

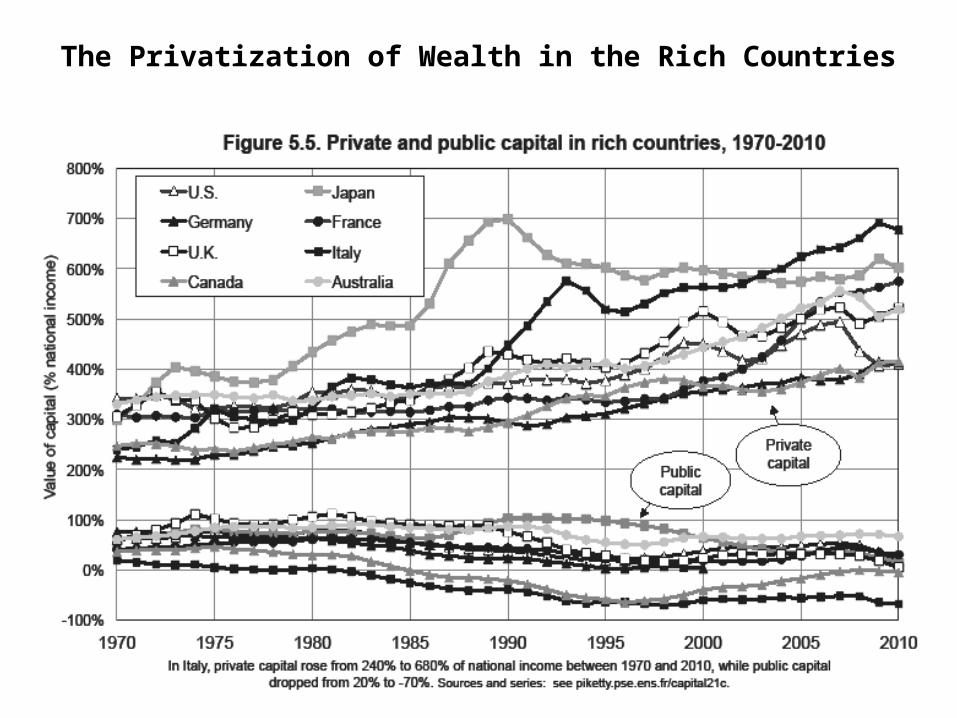

The Privatization of Wealth in the Rich Countries

The Privatization of Wealth in the Rich Countries

The very sharp increase in private wealth observed in the rich countries, and especially in Europe and Japan, between 1970 and 2010, can be explained largely by slower growth coupled with continued high savings. The explanation is privatization. The proportion of public capital in national capital has dropped sharply in recent decades, especially in France and Germany, where net public wealth represented as much as a quarter or even a third of total national wealth in the period 1950-1970, whereas today it represents a few percent (public assets are just enough to balance public debt). This evolution reflects a quite general phenomenon that has affected all eight leading developed economies. In other words, the revival of private wealth is partly due to the privatization of national wealth.

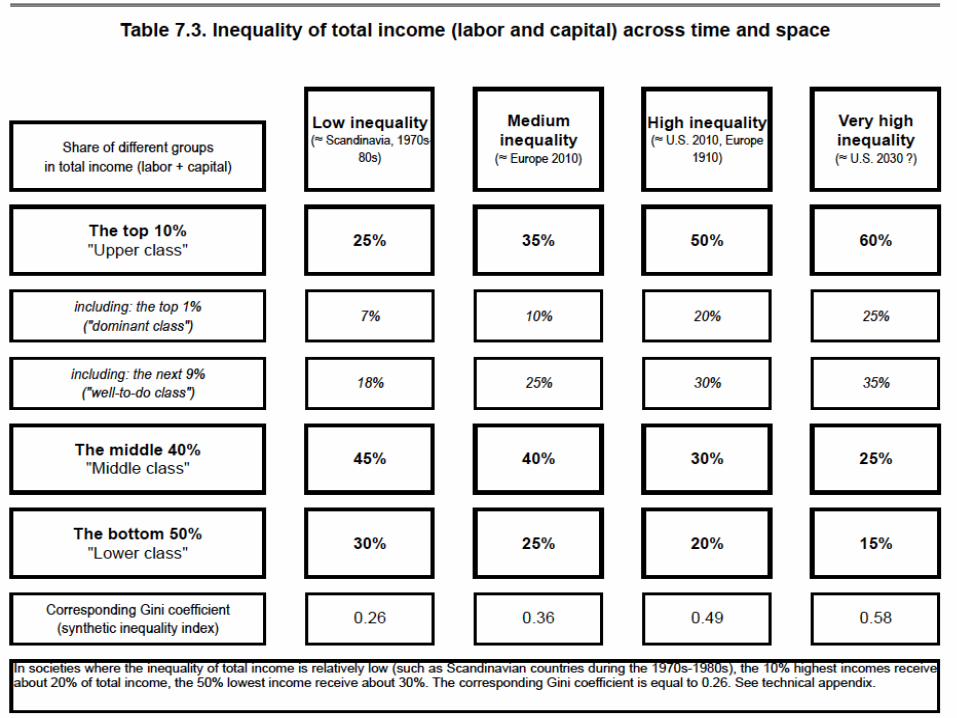

Inequality and concentration: preliminary bearings

In all societies, income inequality is the result of adding up these two components: inequality of income from labor and inequality of income from capital: to what extent do individuals with high income from labor also enjoy high income from capital?

In Table 7.3 note that inequality of total income is closer to inequality of income from labor than to inequality of capital, which comes as a surprise, since income from labor generally accounts for two-thirds to three-quarters of total national income. The top decile of the income hierarchy received about 25% of national income in the egalitarian society of Scandinavia in the 1970s and 1980s. In more inegalitarian societies the top decile claimed as much as 50% of national income (with about 20% going to top centile). This was true in France and Britain during the Ancien Régime as well as the Belle Epoque and is true in the United States today.

The Explosion of US Inequality after 1980

Inequality in the US started from a lower peak on the eve of WWI but at its low point after WWII stood above inequality in Europe. Europe in 1914-1945 witnessed the suicide of rentier society, but nothing of the sort occurred in the US.

Inequality reached its lowest ebb in the US between 1950 and 1980: the top decile of the income hierarchy claimed 30 to 35% of US national income, or roughly the same level of France today. Since 1980, however, income inequality has exploded in the US. The upper decile’s share increased from 30-35% of national income in the 1970s to 45-50% in the 2000s, an increase of 15 points of national income.

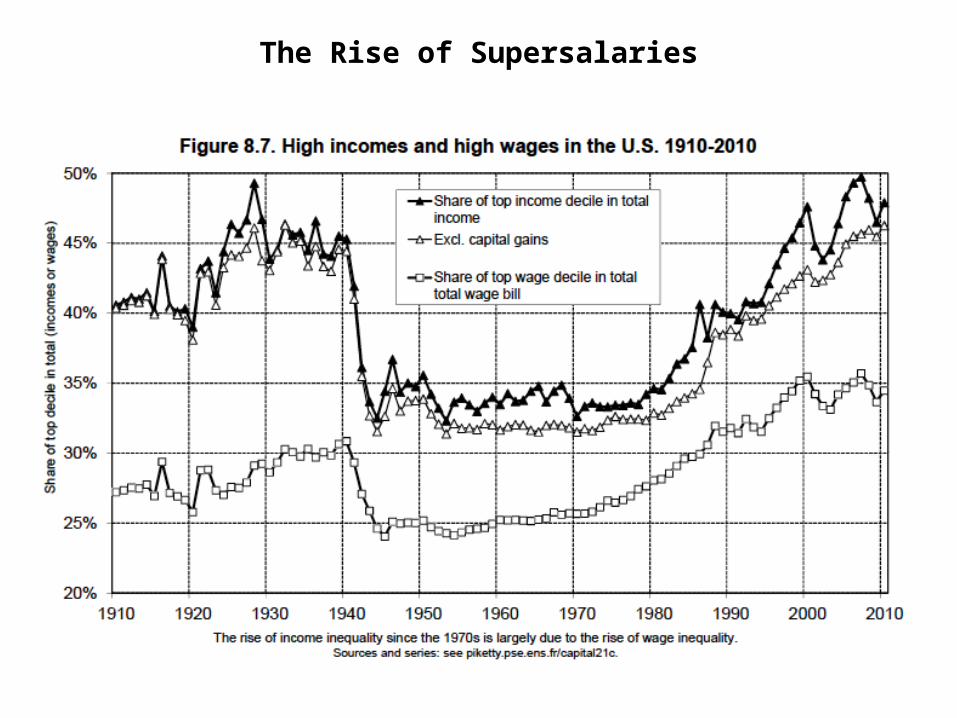

The Rise of Supersalaries

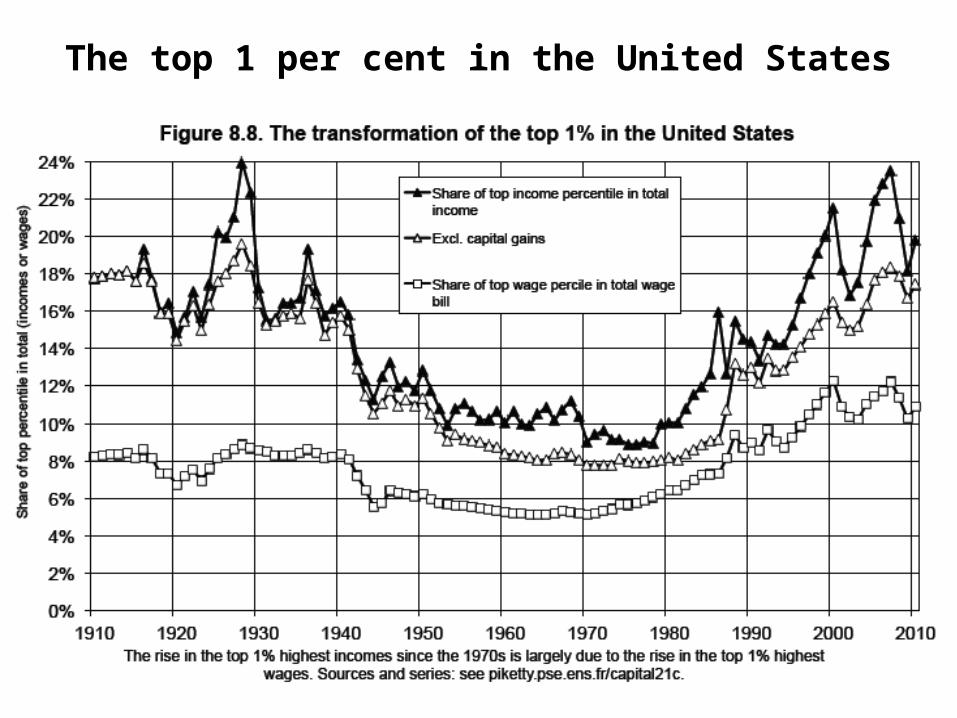

The top 1 per cent in the United States

Institutional factors and inequality

Personal skill and productivity do not explain the recent change in inequality. The increase in wage inequality in the US is due mainly to increased pay at the very top end of the distribution. It is hard to see any discontinuity between the 9% and the 1% regardless of that criteria we use: years of education, selectivity of educational institutions or professional experience.

Two distinct phenomena have been at work in recent decades. First, the wage gap between college graduates and those who go no further than high school has increased. Second, the top 1% (and even more the top 0.1%) have seen their remuneration take off.

Moreover, the explosion of very high salaries occurred in some developed countries but not others. This suggests that institutional differences between countries rather than general and a priori universal causes such as technological change played a central role.

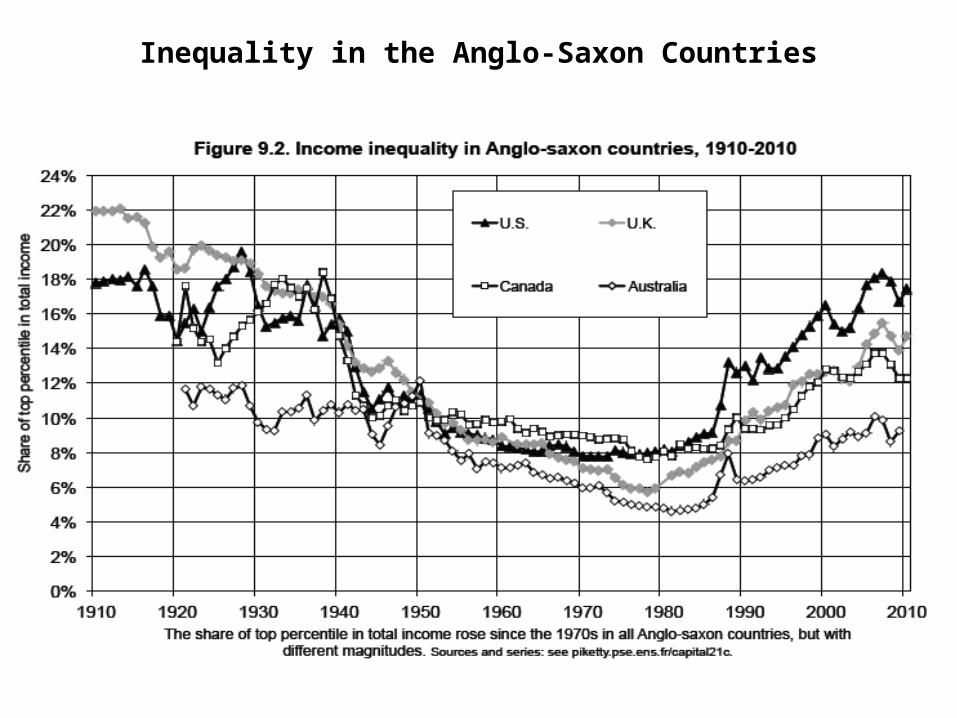

Inequality in the Anglo-Saxon Countries

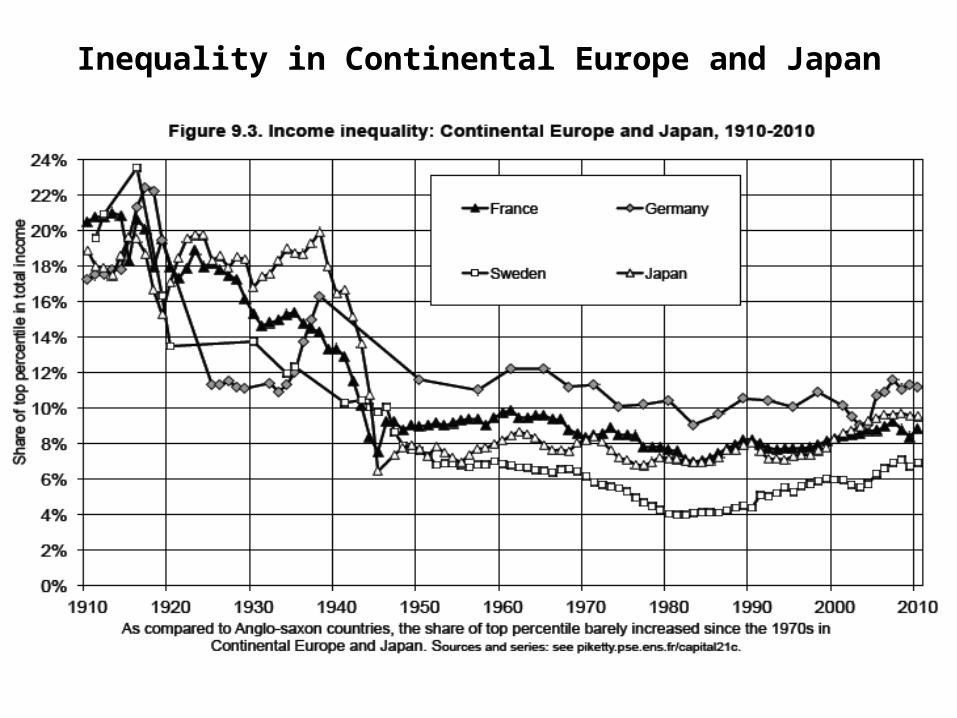

Inequality in Continental Europe and Japan

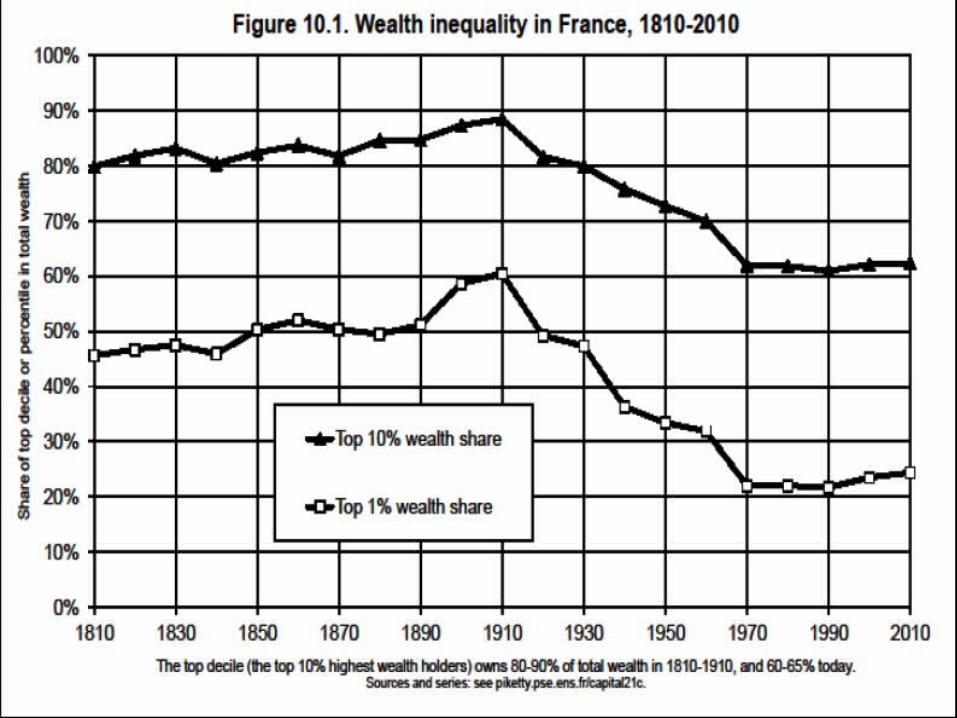

Hyperconcentrated Wealth in France

In France the structure of capital was totally transformed between the 18th and the beginning of the 20th century (landed capital was almost entirely replaced by industrial and financial capital and real estate), but total wealth, measured in years of national income, remained relatively stable. In particular, the French Revolution had relatively little effect on the capital/income ratio (β). The Revolution also had relatively little effect on the distribution of wealth (α).

In 1810-1820, wealth was probably slightly less unequally distributed than during the Ancien Régime: both before and after the Revolution, France was a patrimonial society characterized by a hyperconcentration of capital, in which inheritance and marriage played a key role. At the bottom, France remained the same society, with the same basic structure of inequality, from the Ancien Régime to the Third Republic, despite the economic and political change that took place in the interim.

Why is the rate of return on capital greater than the growth rate

It is an incontrovertible historical reality that r was indeed greater than g over a long period of time. Economic growth was virtually nil throughout much of human history: combining demographic with economic growth, we can say that annual growth rate from antiquity to the seventeenth century never exceeded 0.1-0.2% for long. Despite the many historical uncertainties, there is no doubt that the rate of return on capital was always considerably greater than this: the central value observed over the long run is 4-5% a year.

Throughout most of human history, the inescapable fact is that the rate of return on capital was always at least 10 to 20 times greater than the rate of growth of output (and income). Indeed this fact is to a large extent the very foundation of society itself: it is what allowed a class of owners to devote themselves to something other than their own subsistence.

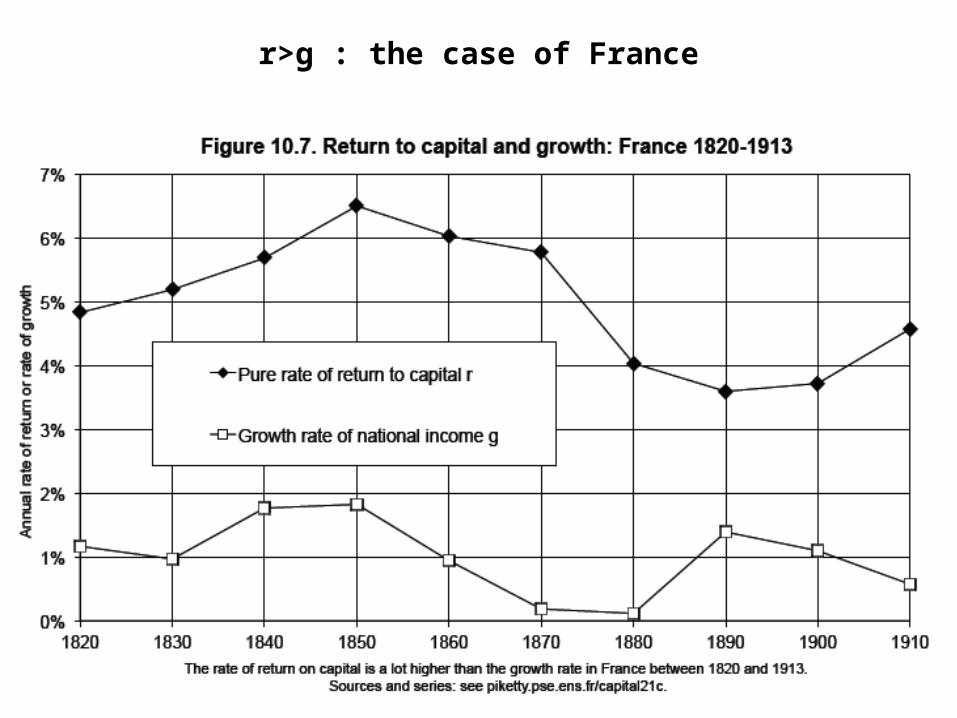

r>g : the case of France

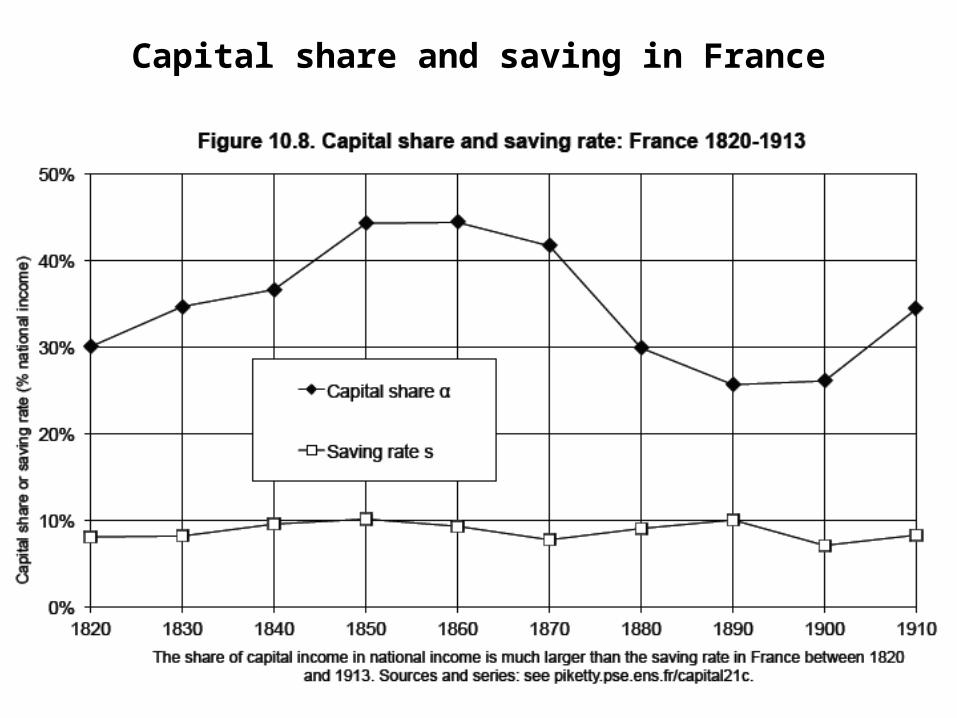

Capital share and saving in France

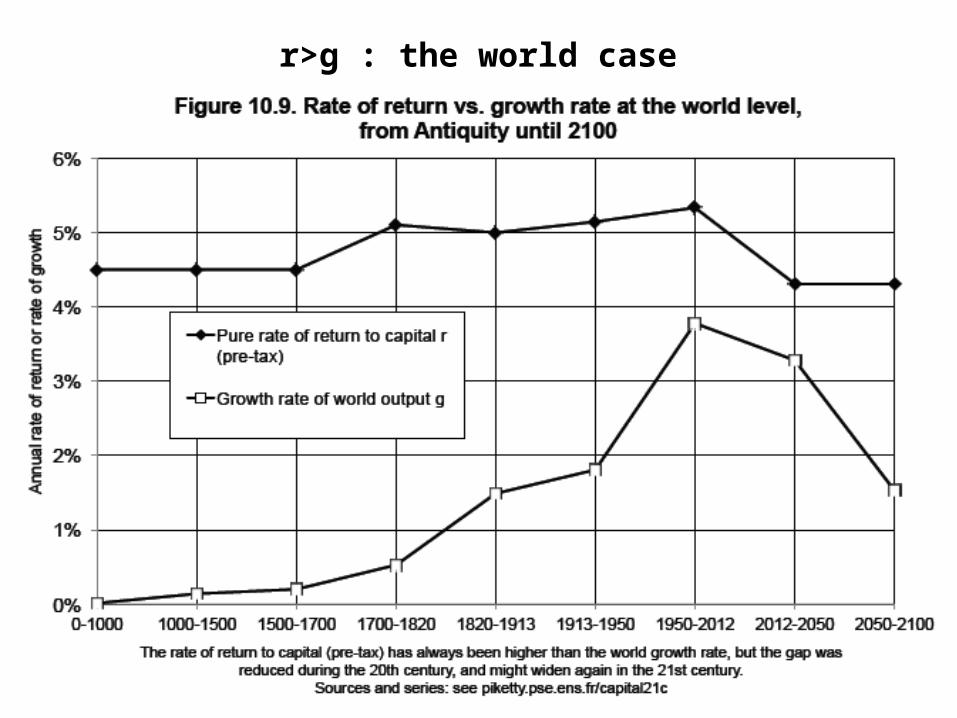

r>g : the world case

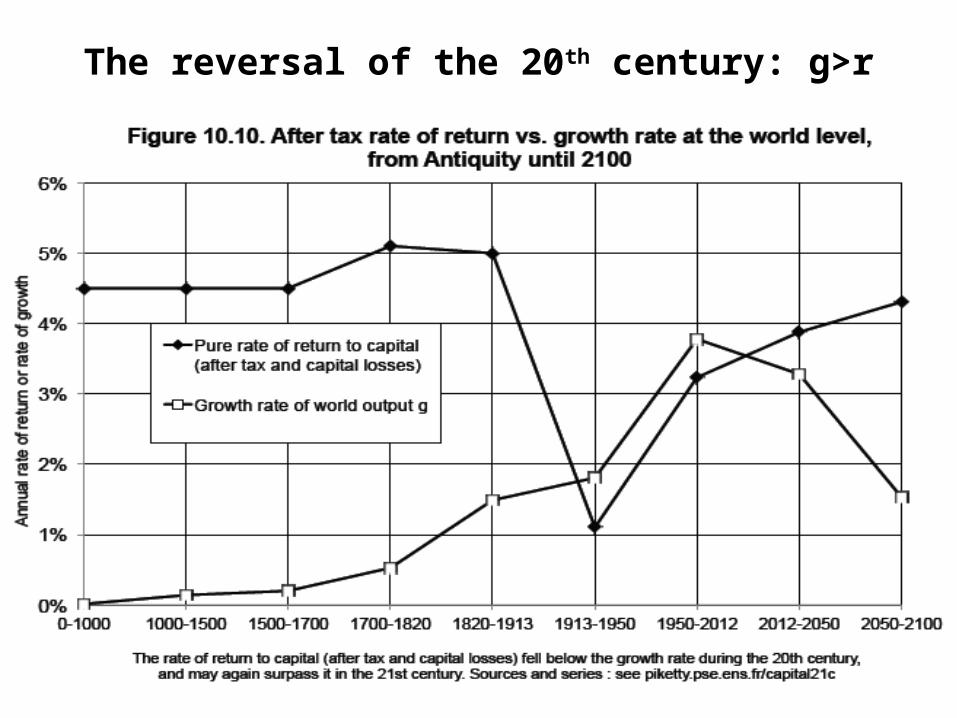

The reversal of the 20th century: g>r

As Fig. 10.9 shows, r – generally 4-5% - has throughout history always been distinctly greater than the global growth rate, but the gap between the two shrank significantly during the 20th century, especially in the second half of the century, when the global economy grew at a rate of 3.5-4% a year. In all likelihood, the gap between r and g would return to a level comparable to that which existed during the Industrial Revolution.

It is easy to see that taxes on capital – and shocks of various kind – can play a central role. Before WWI, taxes on capital were very low. We may therefore assume that the rate of return on capital was virtually the same after tax as before. After WWI, the tax rates on top incomes, profits, and wealth quickly rose to high levels. Since the 1980s, however, as the ideological climate changed dramatically under the influence of financial globalization and heightened competition between states for capital, these same tax rates have been falling and in some cases have almost entirely disappeared.

The reversal of the 20th century: g>r

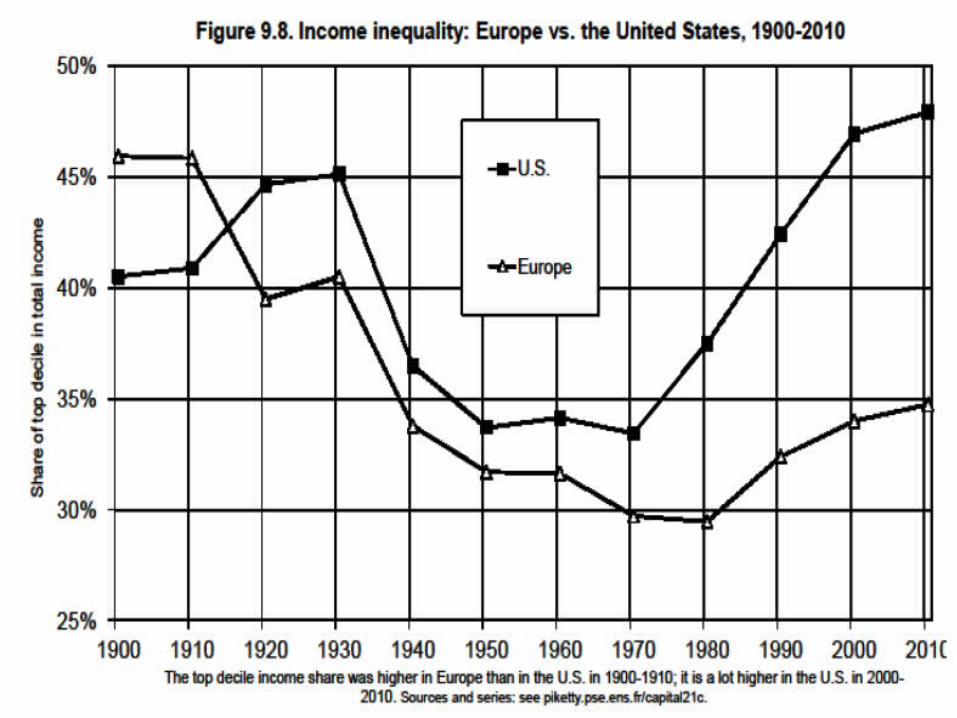

Inequality in US and Europe

At the eve of WWI, the top decile’s share was 45-50% of national income in all European countries, compared with a little more than 40% in the US. By the end of WWII, the US had become slightly more inegalitarian than Europe: the top decile’s share decreased on both continents owing to the shocks of WWII.

The strong divergence, beginning in 1970-1980, led to the following situation in 2000-2010: the top decile’s share of US national income reached 45-50%, or roughly the same level as Europe in 1900-1910. In Europe, we see wide variation, from the most inegalitarian case (Britain, with a top decile share of 40%) to the most egalitarian (Sweden, less than 30%), with France and Germany in between (around 35%).

If we calculate (somewhat abusively) an average for Europe based on these four countries, we can make a very clear international comparison: the US was less inegalitarian than Europe in 1900-1910. slightly more inegalitarian in 1950-1960, and much more inegalitarian in 2000-2010 (see Fig. 9.8)

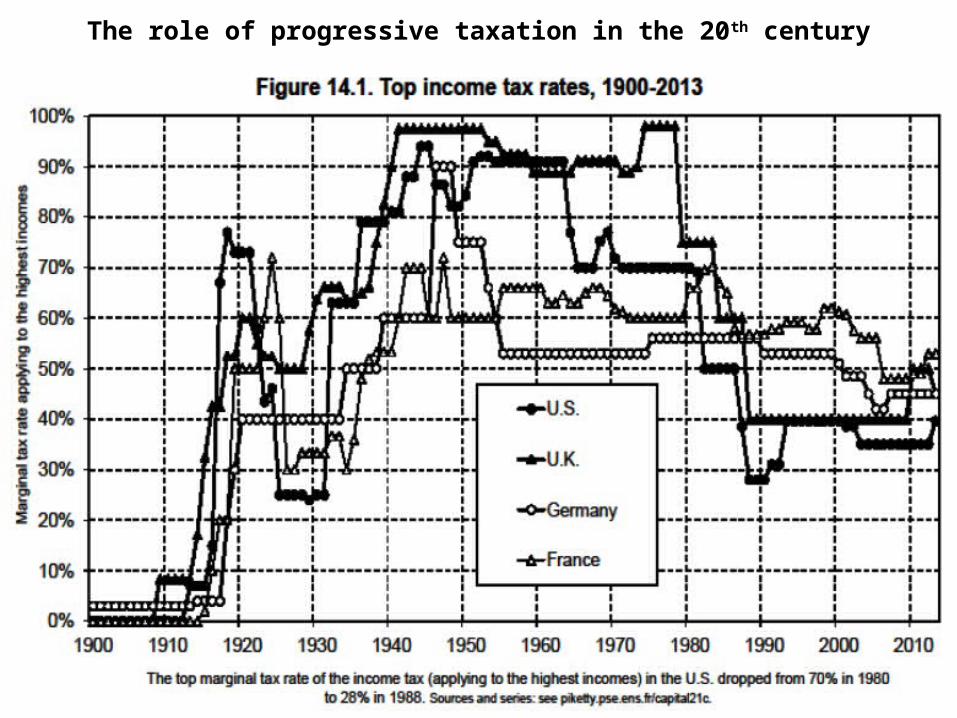

The role of progressive taxation in the 20th century

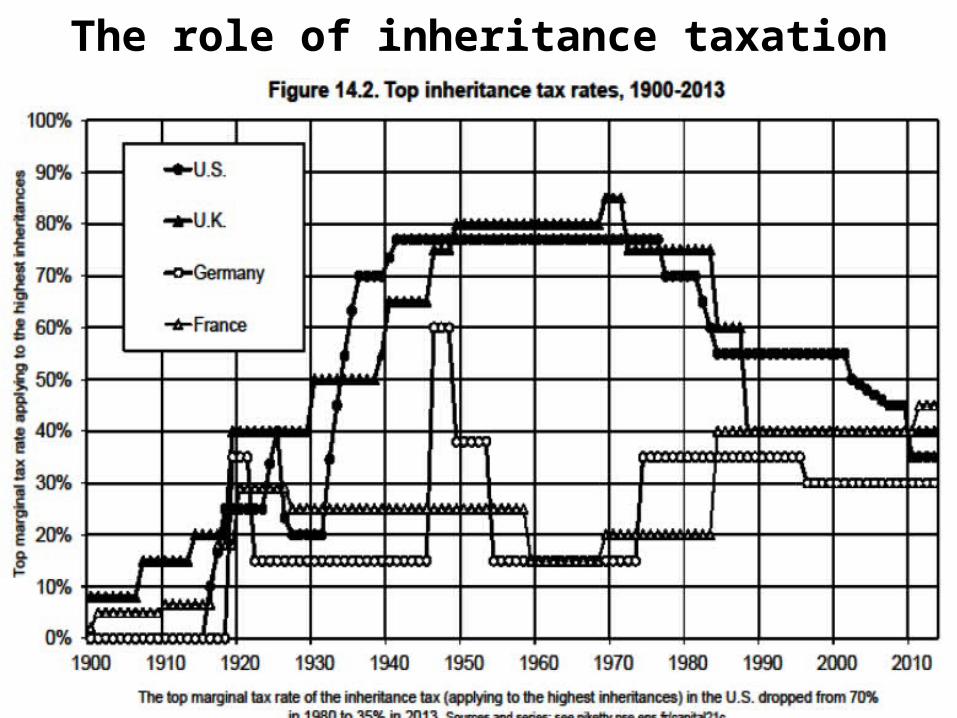

The role of inheritance taxation

The political meaning of taxation

The major 20th century innovation in taxation was the creation and development of the progressive income tax. This institution, which played a key role in the reduction of inequality in the last century, is today seriously threatened by international tax competition. It may also be in jeopardy because its foundations were never clearly thought through, owing to the fact that it was instituted in an emergency that left little time for reflection. The same is true of the progressive tax on inheritances, which was the second major fiscal innovation in the 20th century and has also been challenged in recent decades.

Taxation is not a technical matter. It is pre-eminently a political and philosophical issue, perhaps the most important of all political issues. Without taxes, society has no common destiny, and collective action is impossible.

ConclusionThe principal destabilizing force of a market economy is that the private

rate of return on capital (r) can be significantly higher for long periods of time than the rate of growth of income and output (g). The inequality r>g implies that the wealth accumulated in the past grows more rapidly than output and wages. This inequality expresses a fundamental logical contradiction. The entrepreneur inevitably tends to become a rentier, more and more dominant over those who own nothing but their labor.

To be sure, one could tax capital income heavily enough to reduce the private return on capital to less than the growth rate. But if one did that indiscriminately, one would risk killing the motor of accumulation.

The right solution is a progressive annual tax on capital, to regulate the globalized patrimonial capitalism of 21st century. The difficulty is that a global tax on capital requires a high level of international cooperation and regional political integration. It is not within the reach of the nation-states in which earlier social compromises were hammered out. Only global and regional integration, such as the European Union, can lead to effective regulation of the globalized patrimonial capitalism of the 21st century.