telecom market outlook

TRANSCRIPT

Telecom Market Outlook

Jayesh Easwaramony

1

Jayesh Easwaramony

Vice President ICT Practice

February 2011

Developed by

ICT Research Team

Frost & Sullivan Asia Pacific

Market Outlook - Consumer centric 1

Market Outlook – enterprise centric 2

2

Key opportunities and imperatives 3

Key trends

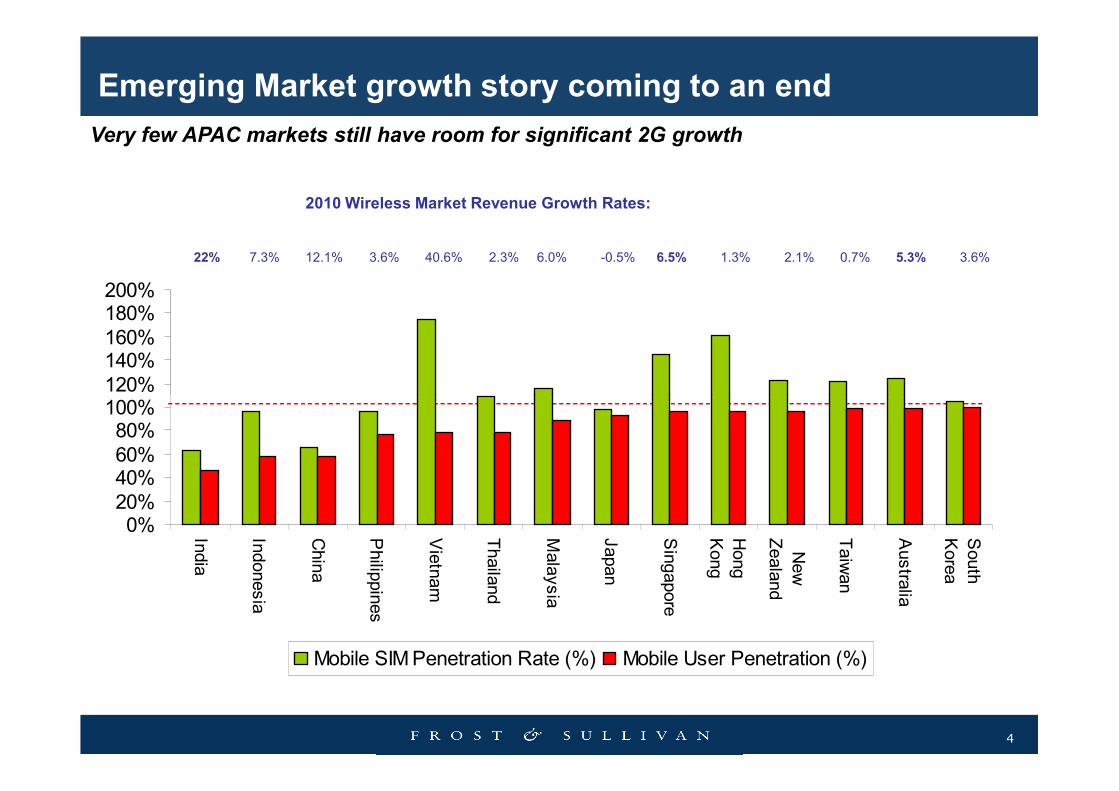

Emerging Market Growth Story is coming to an end in wireless

Collision phase in Mobile Computing/Internet ecosystem

Smart TV will be 50% of most markets by 2015

Touch will be the default input

3

Computing/Internet ecosystem to lead to emergence of 2-3

dominant platforms

Network in the Cloud will redefine Mobility

Touch will be the default input mechanism

Experience platforms will define success

Very few APAC markets still have room for significant 2G growth

120%

140%160%

180%200%

2010 Wireless Market Revenue Growth Rates:

22% 7.3% 12.1% 3.6% 40.6% 2.3% 6.0% -0.5% 6.5% 1.3% 2.1% 0.7% 5.3% 3.6%

Emerging Market growth story coming to an end

4

0%20%

40%60%

80%100%120%

India

Indonesia

China

Philip

pines

Vietnam

Thailand

Malaysia

Japan

Singapore

Hong

Kong

New

Zealand

Taiwan

Austra

lia

South

Korea

Mobile SIM Penetration Rate (%) Mobile User Penetration (%)

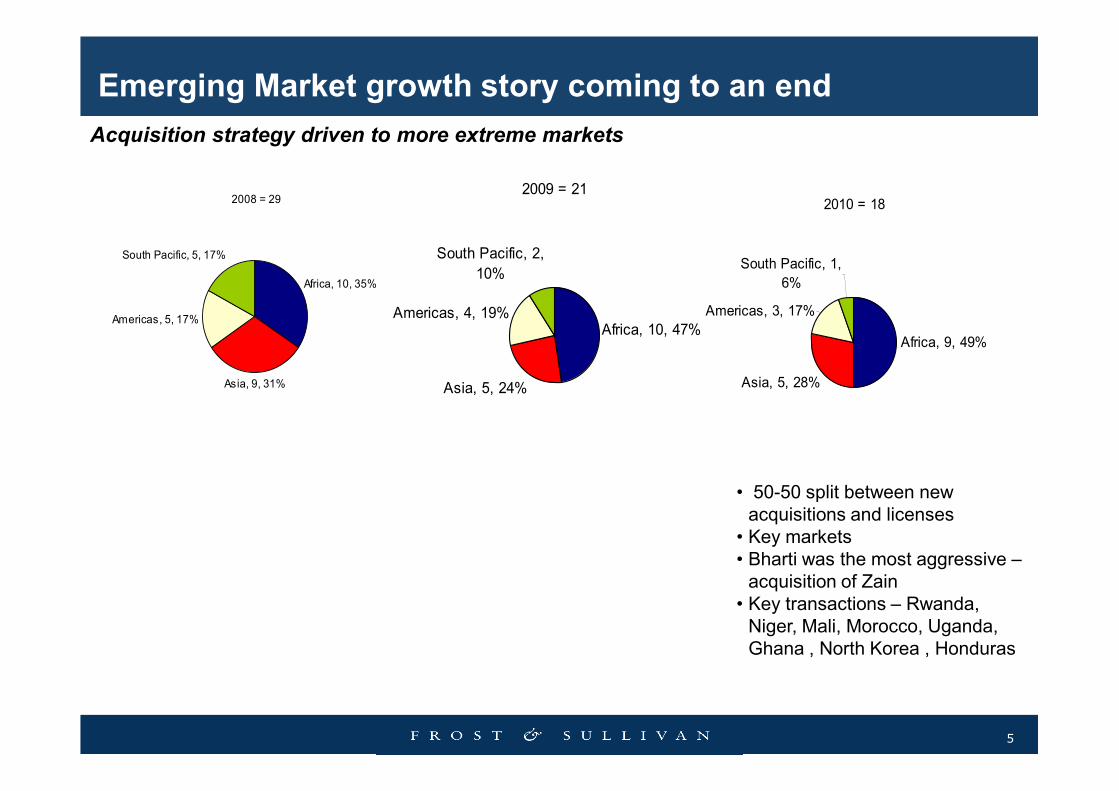

Emerging Market growth story coming to an end

2008 = 29

Africa, 10, 35%

Asia, 9, 31%

Americas, 5, 17%

South Pacific, 5, 17%

2009 = 21

Africa, 10, 47%

Asia, 5, 24%

Americas, 4, 19%

South Pacific, 2,

10%

2010 = 18

Africa, 9, 49%

Asia, 5, 28%

Americas, 3, 17%

South Pacific, 1,

6%

Acquisition strategy driven to more extreme markets

5

Asia, 5, 24%

• 50-50 split between new

acquisitions and licenses

• Key markets

• Bharti was the most aggressive –

acquisition of Zain

• Key transactions – Rwanda,

Niger, Mali, Morocco, Uganda,

Ghana , North Korea , Honduras

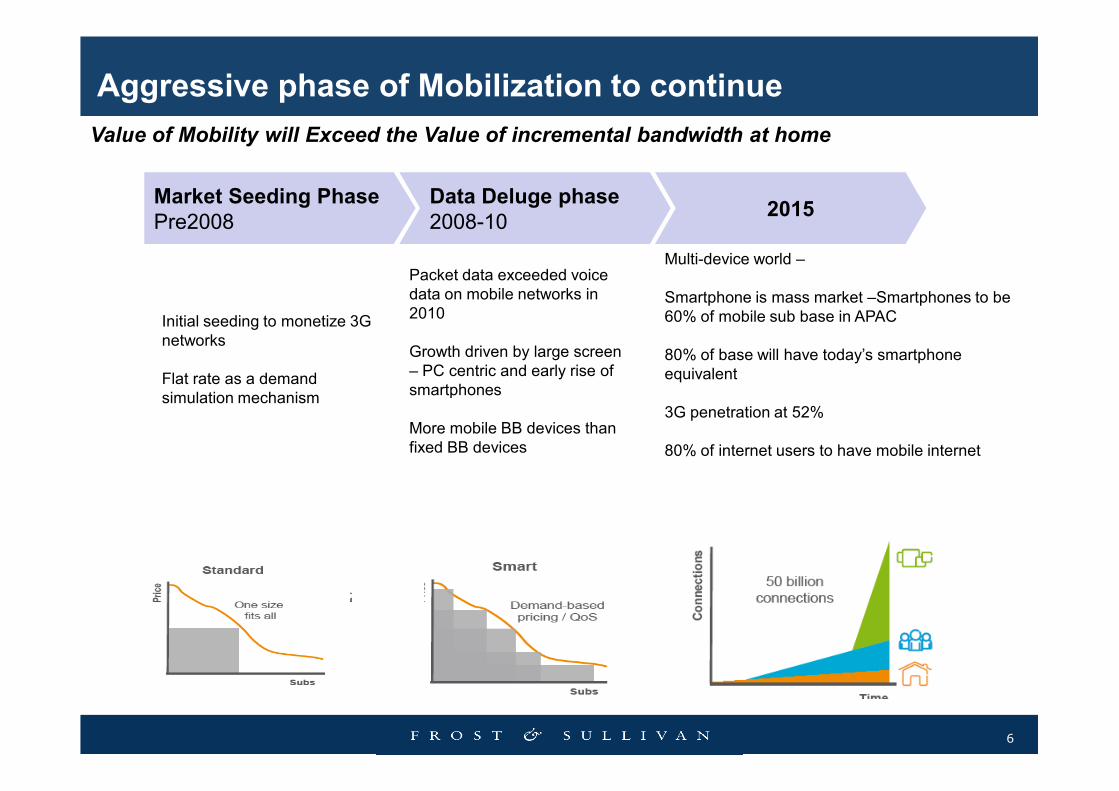

Aggressive phase of Mobilization to continue

Initial seeding to monetize 3G

networks

Flat rate as a demand

simulation mechanism

Market Seeding Phase Pre2008

Data Deluge phase2008-10

2015

Packet data exceeded voice

data on mobile networks in

2010

Growth driven by large screen

– PC centric and early rise of

smartphones

Multi-device world –

Smartphone is mass market –Smartphones to be

60% of mobile sub base in APAC

80% of base will have today’s smartphone

equivalent

Value of Mobility will Exceed the Value of incremental bandwidth at home

6

simulation mechanism smartphones

More mobile BB devices than

fixed BB devices

3G penetration at 52%

80% of internet users to have mobile internet

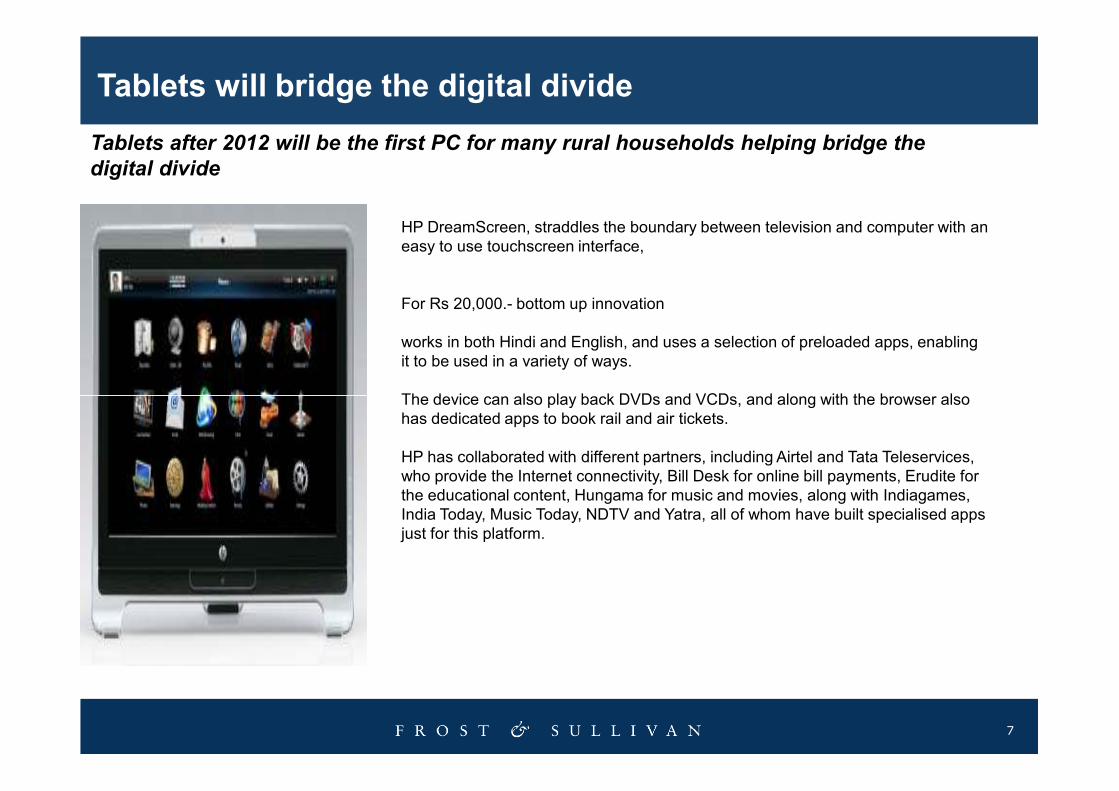

Tablets will bridge the digital divide

HP DreamScreen, straddles the boundary between television and computer with an

easy to use touchscreen interface,

For Rs 20,000.- bottom up innovation

works in both Hindi and English, and uses a selection of preloaded apps, enabling

it to be used in a variety of ways.

The device can also play back DVDs and VCDs, and along with the browser also

Tablets after 2012 will be the first PC for many rural households helping bridge the

digital divide

7

The device can also play back DVDs and VCDs, and along with the browser also

has dedicated apps to book rail and air tickets.

HP has collaborated with different partners, including Airtel and Tata Teleservices,

who provide the Internet connectivity, Bill Desk for online bill payments, Erudite for

the educational content, Hungama for music and movies, along with Indiagames,

India Today, Music Today, NDTV and Yatra, all of whom have built specialised apps

just for this platform.

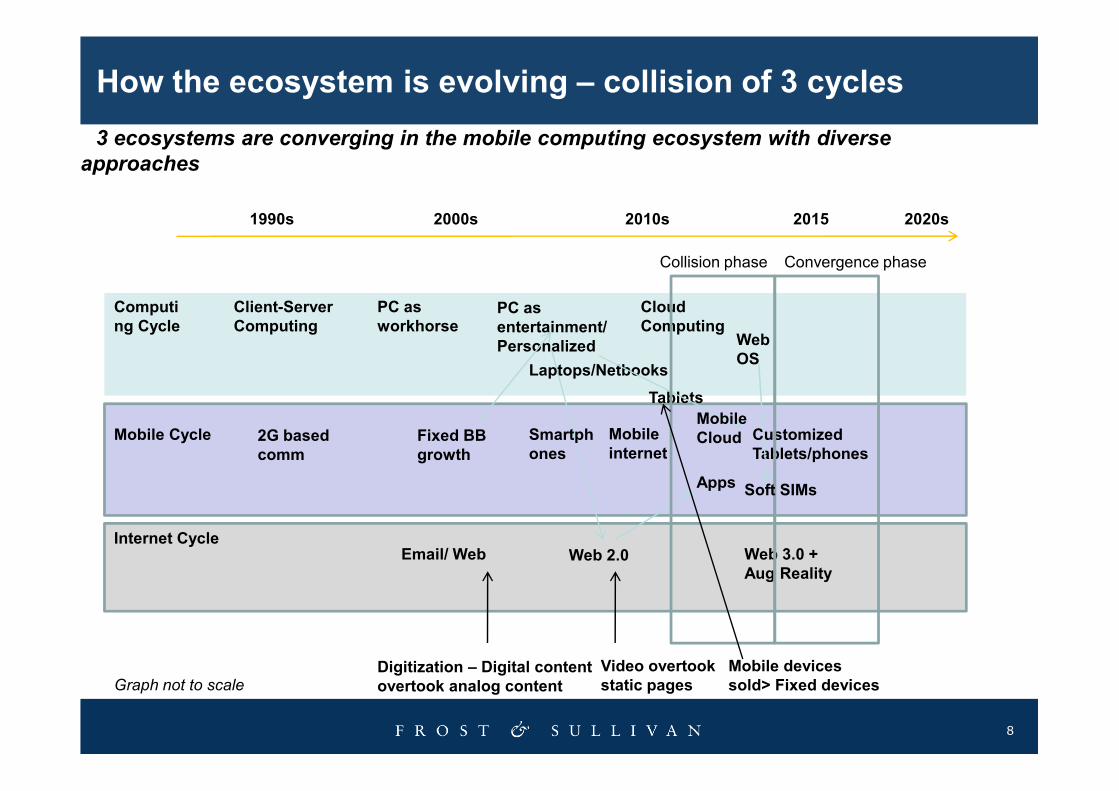

How the ecosystem is evolving – collision of 3 cycles

3 ecosystems are converging in the mobile computing ecosystem with diverse

approaches

1990s

Client-Server Computing

2000s 2010s 2020s

Cloud Computing

Web OS

PC as entertainment/Personalized

PC as workhorse

Laptops/Netbooks

Tablets

2015

Computing Cycle

Collision phase Convergence phase

8

Mobile Cycle Mobile internet

Email/ Web Web 2.0

2G based comm

Fixed BB growth

Customized Tablets/phones

Apps

Tablets

Smartphones

Digitization – Digital content overtook analog content

Web 3.0 + Aug Reality

Video overtook static pages

Internet Cycle

Mobile Cloud

Graph not to scale

Soft SIMs

Mobile devices sold> Fixed devices

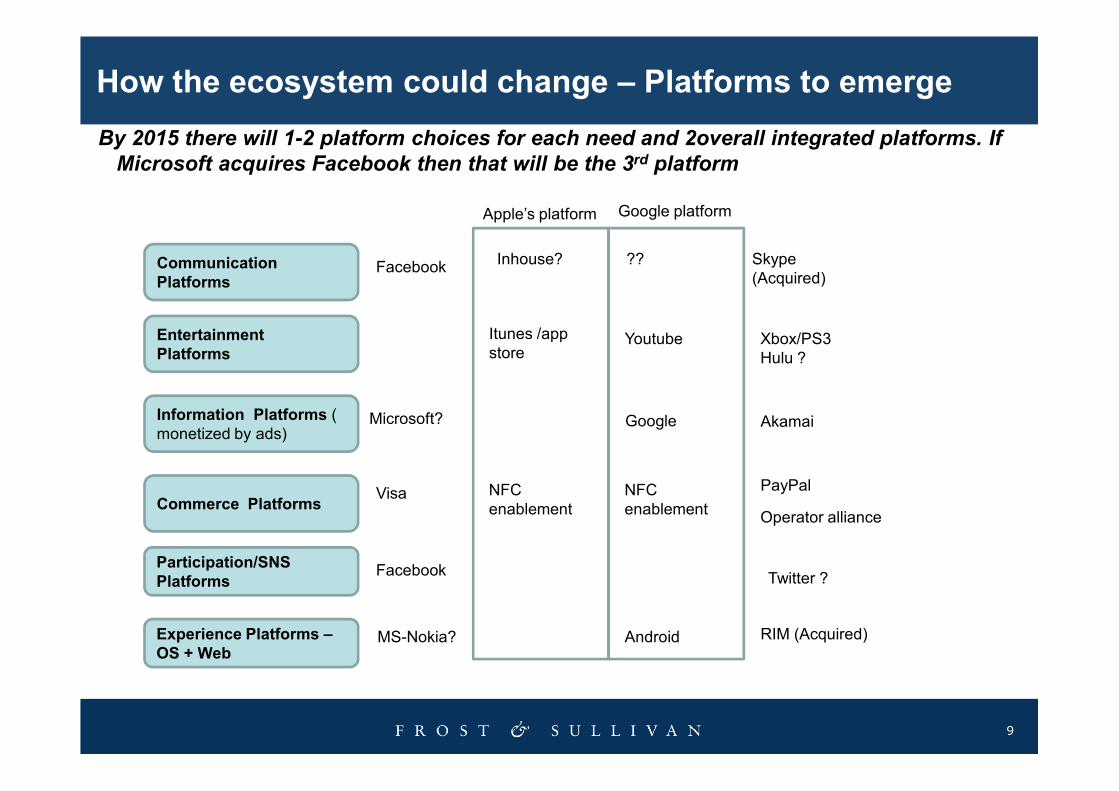

How the ecosystem could change – Platforms to emerge

By 2015 there will 1-2 platform choices for each need and 2overall integrated platforms. If

Microsoft acquires Facebook then that will be the 3rd platform

Communication Platforms

Entertainment Platforms

Facebook Inhouse?

Apple’s platform Google platform

?? Skype

(Acquired)

Itunes /app

store Youtube Xbox/PS3

Hulu ?

9

Information Platforms ( monetized by ads)

Commerce Platforms

Participation/SNS Platforms

Experience Platforms –OS + Web

Akamai

PayPalVisa

MS-Nokia? RIM (Acquired)

Operator alliance

Twitter ?

Microsoft?

Android

NFC

enablement

NFC

enablement

• End to end experience providers controi 60% of the profits

• 4 kinds of players to remain- Market Creator/Innovator, Fast Follower/Market Leader , Optimizer and Niche – Nokia failed on all 4 ☺

• Assemblers of phones and devices will provide me-too devices (25% of market)

• Assemblers will provide ‘ make your own device’ service by early 2012

Platform play – some critical observations

Devices

10

Platforms

• Players without software DNA will perish ( Qualcomm BREW)

• Speed on innovation is driven by internet companies – not hardware or software

• Hardware can be commodity in most cases unless integrated with experience platform

• Software can be used as means of other monetization e.g ad selling

• Infrastructure plays like Amazon are interesting categories still showing power in retail distribution

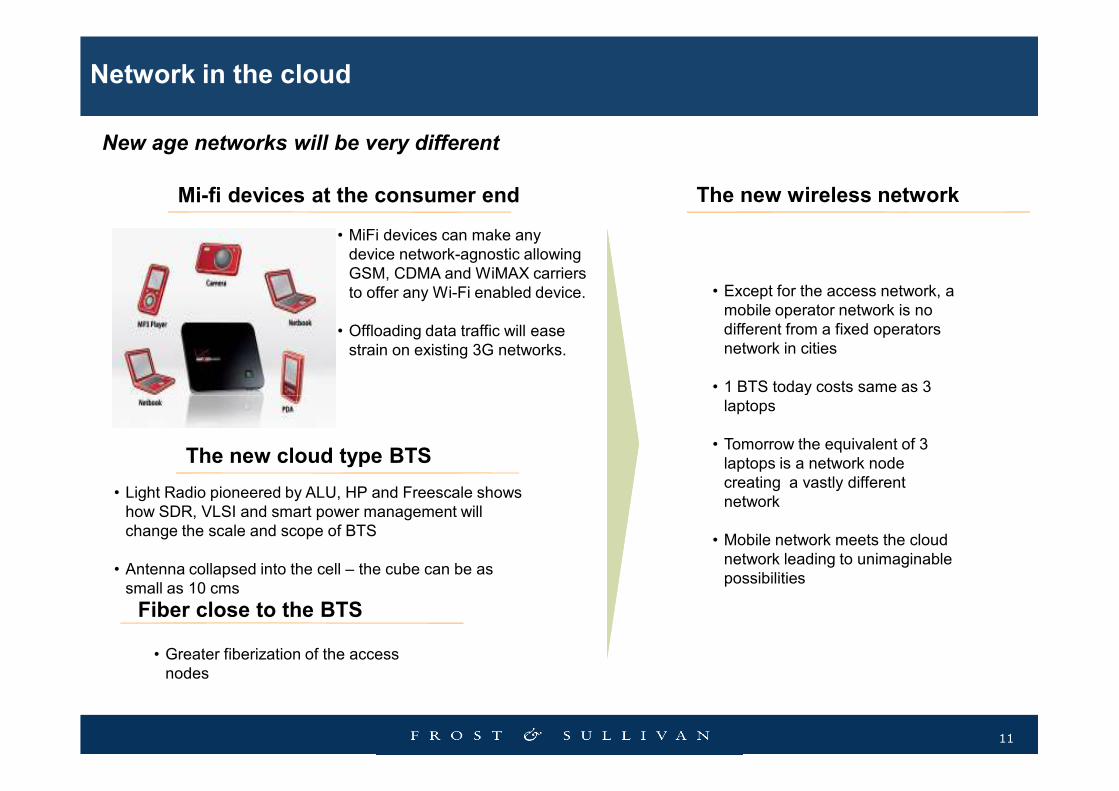

New age networks will be very different

Mi-fi devices at the consumer end

• MiFi devices can make any

device network-agnostic allowing

GSM, CDMA and WiMAX carriers

to offer any Wi-Fi enabled device.

• Offloading data traffic will ease

strain on existing 3G networks.

Network in the cloud

The new wireless network

• Except for the access network, a

mobile operator network is no

different from a fixed operators

network in cities

• 1 BTS today costs same as 3

11

The new cloud type BTS

• Light Radio pioneered by ALU, HP and Freescale shows

how SDR, VLSI and smart power management will

change the scale and scope of BTS

• Antenna collapsed into the cell – the cube can be as

small as 10 cms

Fiber close to the BTS

• Greater fiberization of the access

nodes

laptops

• Tomorrow the equivalent of 3

laptops is a network node

creating a vastly different

network

• Mobile network meets the cloud

network leading to unimaginable

possibilities

Carriers and vendors will bring services such as remote wipe, remote storage and virus

protection to smart devices to the consumer space.

Key points

• Viruses have already emerged for Android,

iOS and via SMS.

• Malware for tablet PCs is expected in 2011.

• Many vendors are already offering remote

smartphone services, largely to enterprises.

• Carriers have been slow to enter this market.

Mobile revolution will create allied opportunities for services

12

• Carriers have been slow to enter this market.

• Mobile cloud services will eventually help

overcome smartphone challenges such as

memory space, battery power and

processing speed.

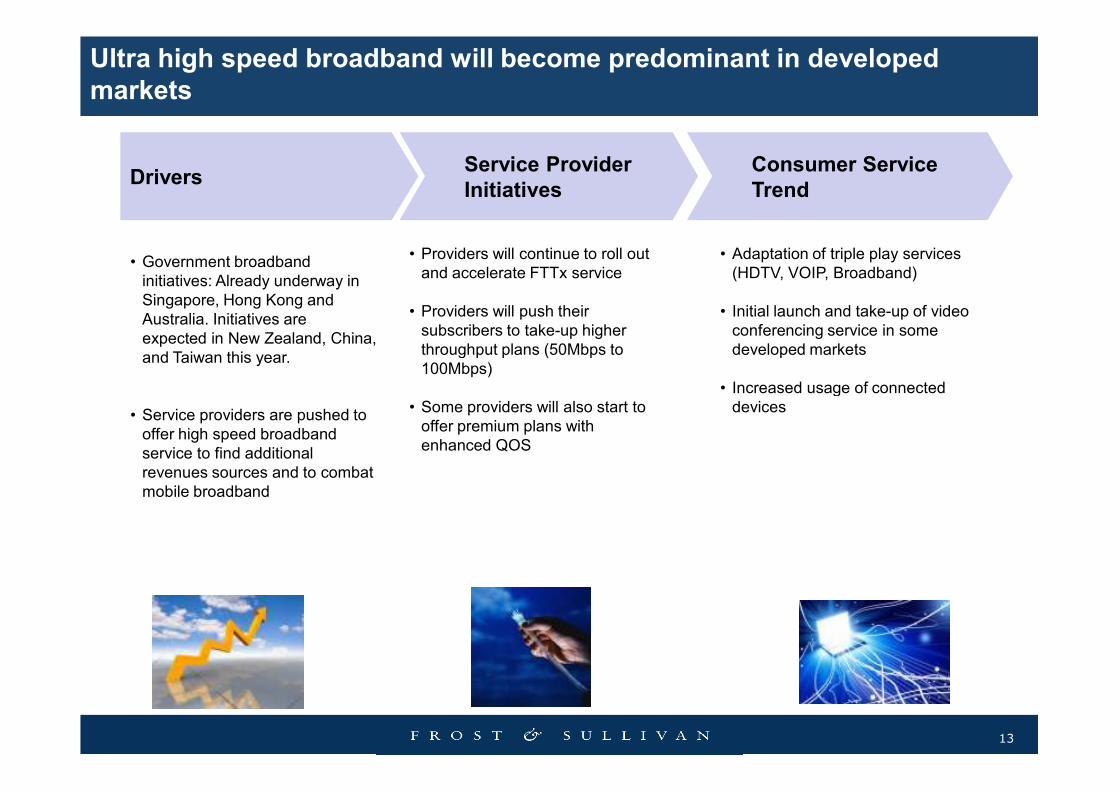

• Government broadband

initiatives: Already underway in

Singapore, Hong Kong and

Australia. Initiatives are

expected in New Zealand, China,

and Taiwan this year.

DriversService Provider Initiatives

Consumer ServiceTrend

• Providers will continue to roll out

and accelerate FTTx service

• Providers will push their

subscribers to take-up higher

throughput plans (50Mbps to

100Mbps)

• Adaptation of triple play services

(HDTV, VOIP, Broadband)

• Initial launch and take-up of video

conferencing service in some

developed markets

• Increased usage of connected

Ultra high speed broadband will become predominant in developed markets

13

• Service providers are pushed to

offer high speed broadband

service to find additional

revenues sources and to combat

mobile broadband

• Some providers will also start to

offer premium plans with

enhanced QOS

• Increased usage of connected

devices

Smart TV

Smart TVs will account for 50% of the developed market TVs by 2013

14

Swapping of content from Mobile to

TV

TV Manufacturer Portals OTT Set Top Box based

• Vanilla bundling: Providers offering multiple services with only additional discounts

• Many Providers even have multiple bills for the bundled services

Old Trend

2011

“True Bundling” will be mainstream by 2012

15

• Providers will start to offer true blended services with NG BSS & OSS capabilities

- 1 Bill for all services

• Watch content on TV, internet or mobile with one pay TV subscription

• Surf broadband through fixed connection or mobile with one subscription

• Voice calls for mobile or fixed line with one subscription

• Device bundling: although it can negatively affect profitability, providers in the

region will be forced to offer it due to competition

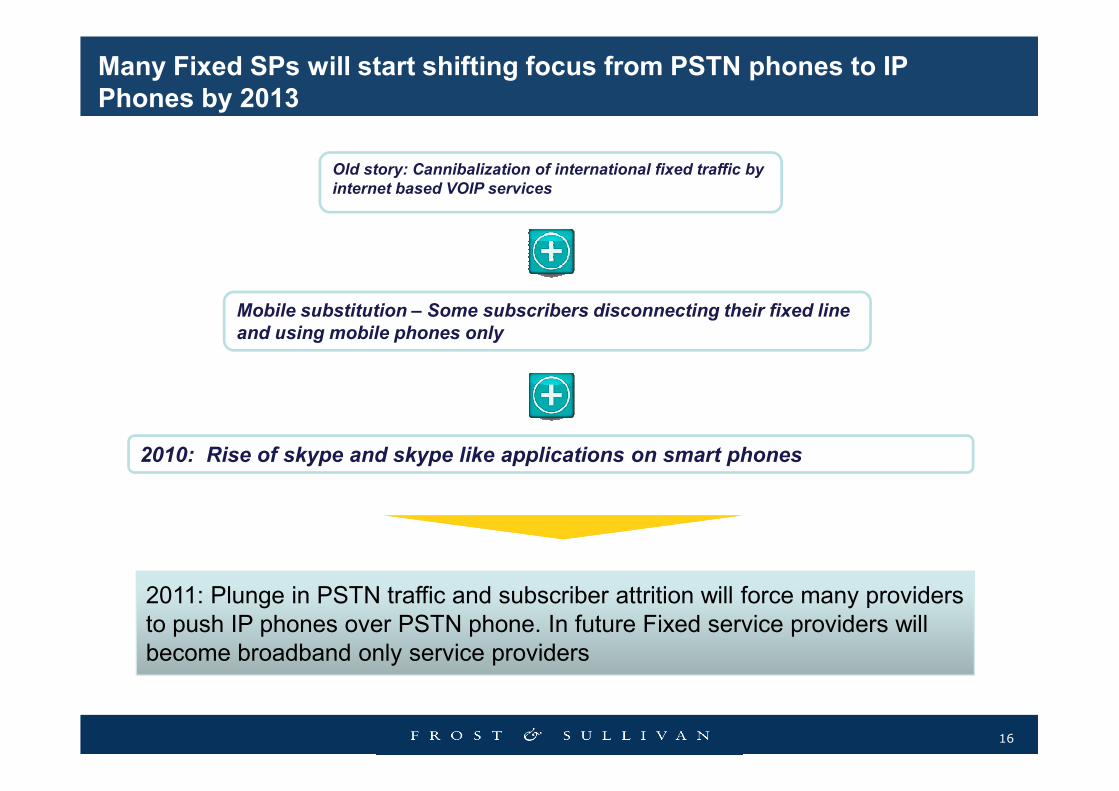

Old story: Cannibalization of international fixed traffic by

internet based VOIP services

Mobile substitution – Some subscribers disconnecting their fixed line

and using mobile phones only

Many Fixed SPs will start shifting focus from PSTN phones to IP Phones by 2013

16

2011: Plunge in PSTN traffic and subscriber attrition will force many providers

to push IP phones over PSTN phone. In future Fixed service providers will

become broadband only service providers

2010: Rise of skype and skype like applications on smart phones

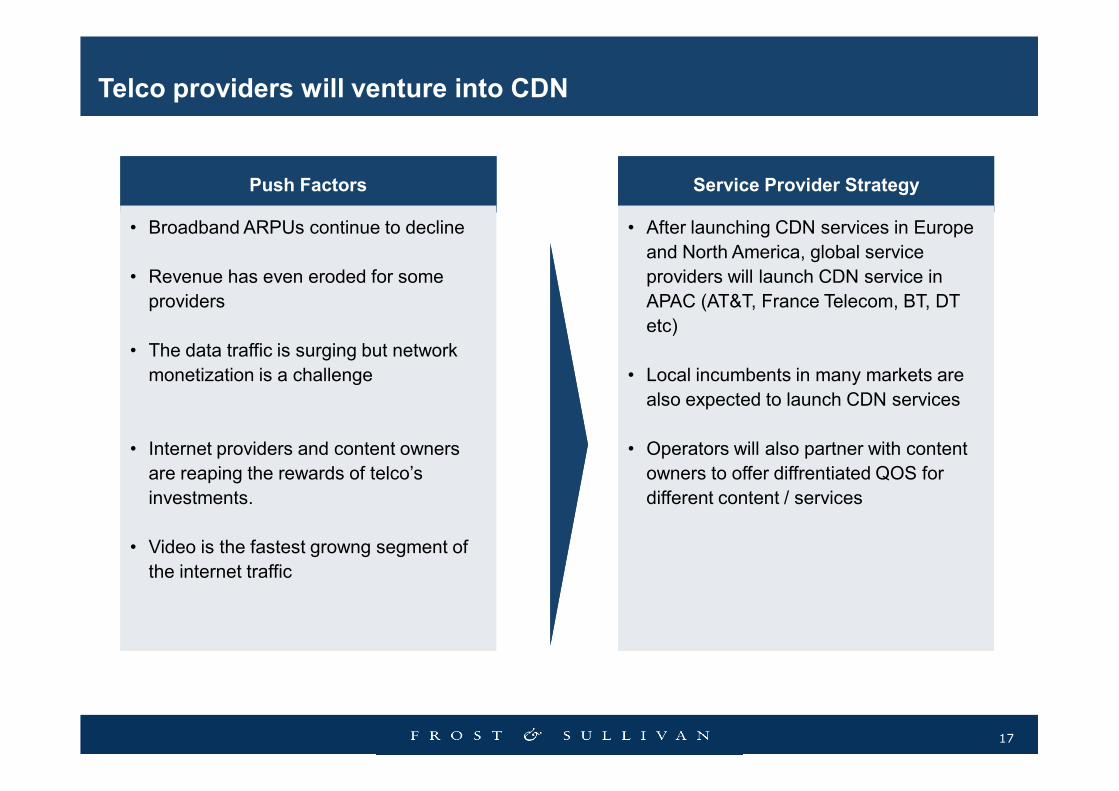

Push FactorsPush Factors Service Provider StrategyService Provider Strategy

• Broadband ARPUs continue to decline

• Revenue has even eroded for some

providers

• The data traffic is surging but network

monetization is a challenge

• Broadband ARPUs continue to decline

• Revenue has even eroded for some

providers

• The data traffic is surging but network

monetization is a challenge

• After launching CDN services in Europe

and North America, global service

providers will launch CDN service in

APAC (AT&T, France Telecom, BT, DT

etc)

• Local incumbents in many markets are

also expected to launch CDN services

• After launching CDN services in Europe

and North America, global service

providers will launch CDN service in

APAC (AT&T, France Telecom, BT, DT

etc)

• Local incumbents in many markets are

also expected to launch CDN services

Telco providers will venture into CDN

17

• Internet providers and content owners

are reaping the rewards of telco’s

investments.

• Video is the fastest growng segment of

the internet traffic

• Internet providers and content owners

are reaping the rewards of telco’s

investments.

• Video is the fastest growng segment of

the internet traffic

also expected to launch CDN services

• Operators will also partner with content

owners to offer diffrentiated QOS for

different content / services

also expected to launch CDN services

• Operators will also partner with content

owners to offer diffrentiated QOS for

different content / services

Market Outlook - Consumer centric 1

Market Outlook – enterprise centric 2

18

Key opportunities and imperatives 3

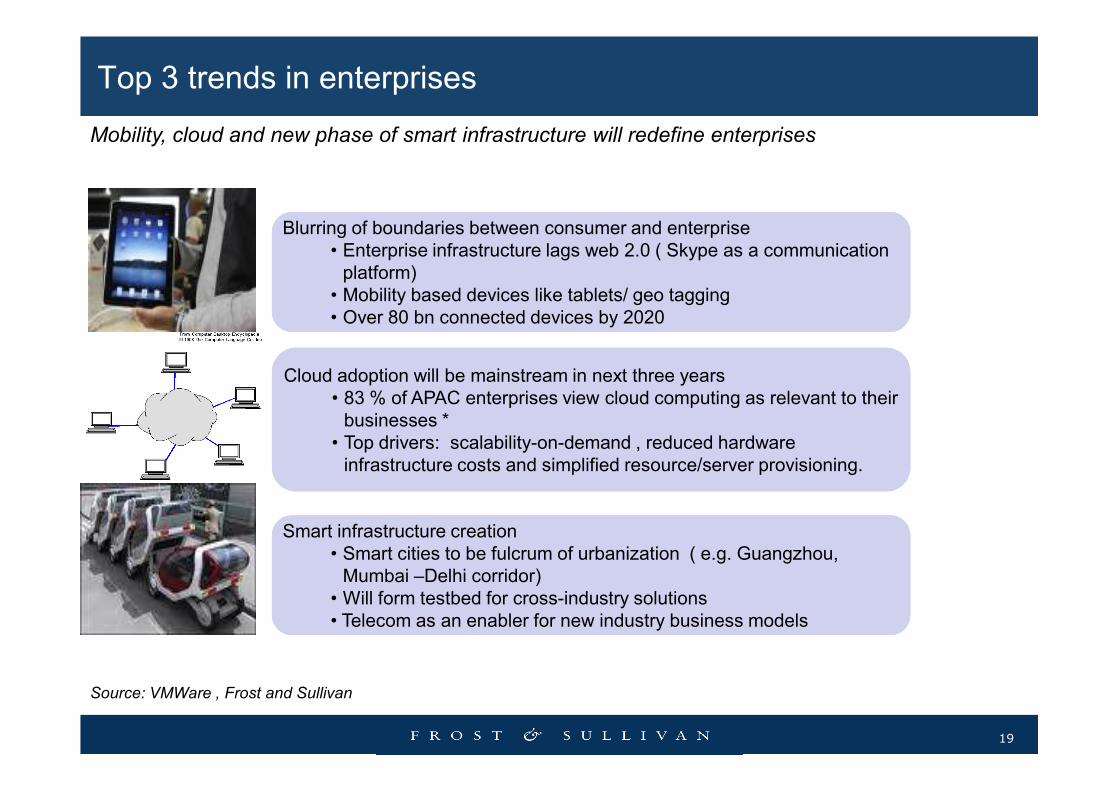

Mobility, cloud and new phase of smart infrastructure will redefine enterprises

Top 3 trends in enterprises

Blurring of boundaries between consumer and enterprise

• Enterprise infrastructure lags web 2.0 ( Skype as a communication

platform)

• Mobility based devices like tablets/ geo tagging

• Over 80 bn connected devices by 2020

Cloud adoption will be mainstream in next three years

• 83 % of APAC enterprises view cloud computing as relevant to their

19

• 83 % of APAC enterprises view cloud computing as relevant to their

businesses *

• Top drivers: scalability-on-demand , reduced hardware

infrastructure costs and simplified resource/server provisioning.

Smart infrastructure creation

• Smart cities to be fulcrum of urbanization ( e.g. Guangzhou,

Mumbai –Delhi corridor)

• Will form testbed for cross-industry solutions

• Telecom as an enabler for new industry business models

Source: VMWare , Frost and Sullivan

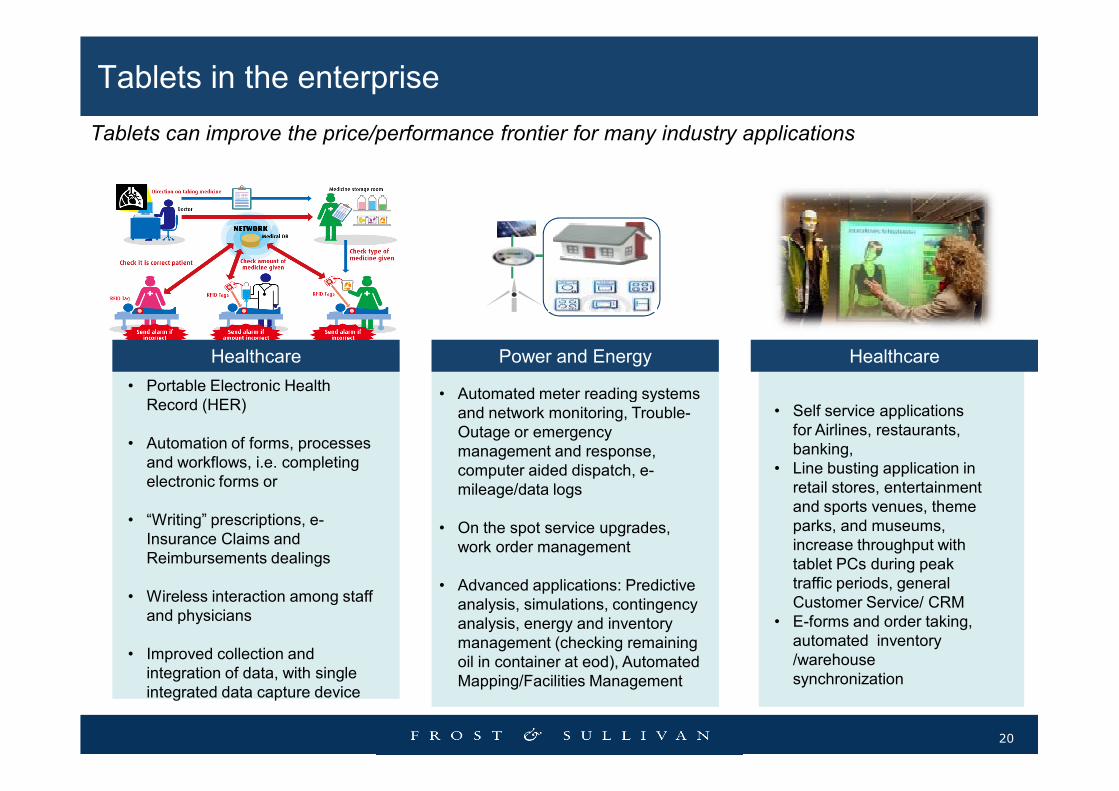

Tablets in the enterprise

• Portable Electronic Health • Automated meter reading systems

Healthcare Power and Energy Healthcare

Tablets can improve the price/performance frontier for many industry applications

20

Record (HER)

• Automation of forms, processes

and workflows, i.e. completing

electronic forms or

• “Writing” prescriptions, e-

Insurance Claims and

Reimbursements dealings

• Wireless interaction among staff

and physicians

• Improved collection and

integration of data, with single

integrated data capture device

• Automated meter reading systems

and network monitoring, Trouble-

Outage or emergency

management and response,

computer aided dispatch, e-

mileage/data logs

• On the spot service upgrades,

work order management

• Advanced applications: Predictive

analysis, simulations, contingency

analysis, energy and inventory

management (checking remaining

oil in container at eod), Automated

Mapping/Facilities Management

• Self service applications

for Airlines, restaurants,

banking,

• Line busting application in

retail stores, entertainment

and sports venues, theme

parks, and museums,

increase throughput with

tablet PCs during peak

traffic periods, general

Customer Service/ CRM

• E-forms and order taking,

automated inventory

/warehouse

synchronization

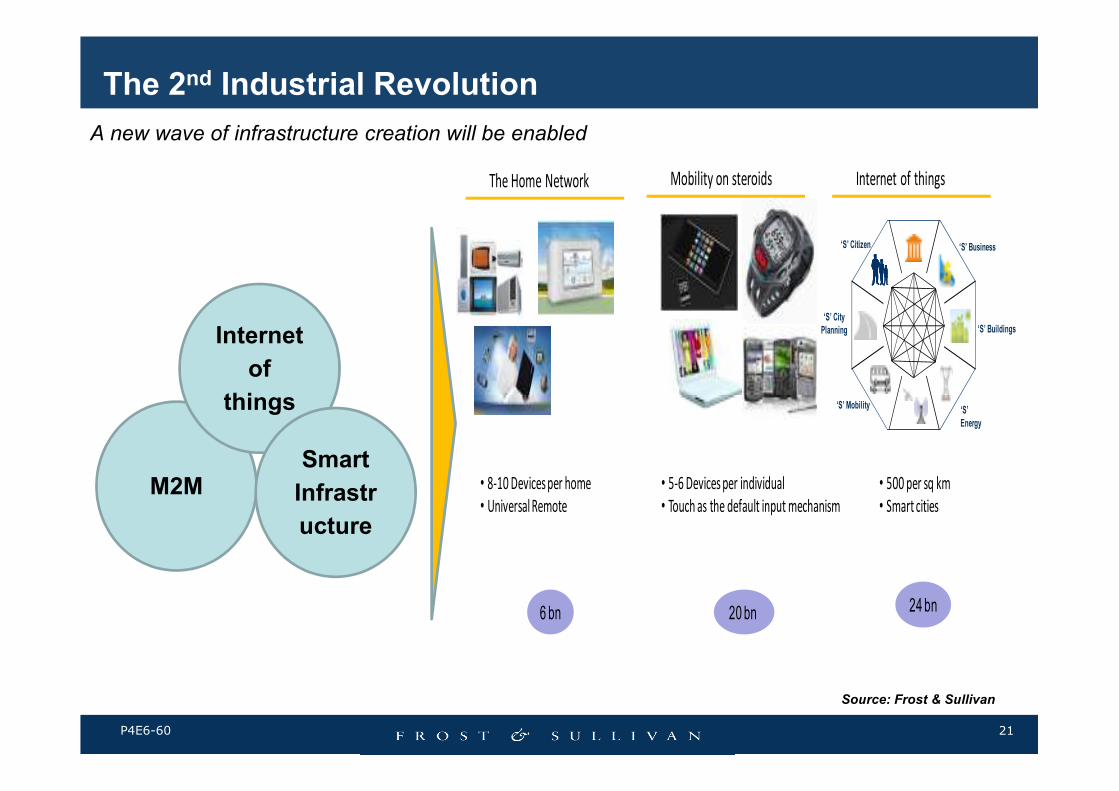

The 2nd Industrial Revolution

Internet

of

things

A new wave of infrastructure creation will be enabled

The Home Network Mobility on steroids Internet of things

‘S’ City Planning

‘S’ Business‘S’ Citizen

‘S’ Buildings

21P4E6-60

Source: Frost & Sullivan

M2M

things

Smart

Infrastr

ucture

• 8-10 Devices per home

• Universal Remote

6 bn

• 5-6 Devices per individual

• Touch as the default input mechanism

20 bn

• 500 per sq km

• Smart cities

24 bn

‘S’ Energy

‘S’ Mobility

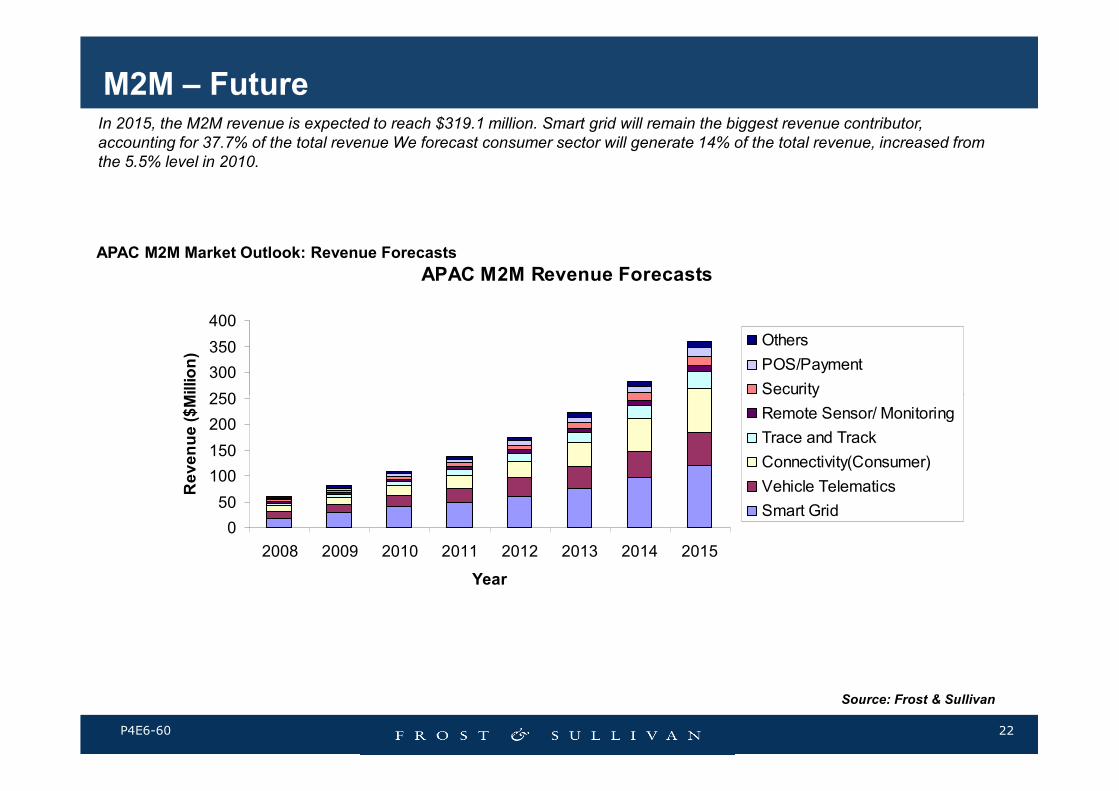

M2M – Future

APAC M2M Revenue Forecasts

250

300

350

400

Revenue ($Million)

Others

POS/Payment

Security

APAC M2M Market Outlook: Revenue Forecasts

In 2015, the M2M revenue is expected to reach $319.1 million. Smart grid will remain the biggest revenue contributor, accounting for 37.7% of the total revenue We forecast consumer sector will generate 14% of the total revenue, increased from the 5.5% level in 2010.

22P4E6-60

Source: Frost & Sullivan

0

50

100

150

200

250

2008 2009 2010 2011 2012 2013 2014 2015

Year

Revenue ($Million)

Security

Remote Sensor/ Monitoring

Trace and Track

Connectivity(Consumer)

Vehicle Telematics

Smart Grid

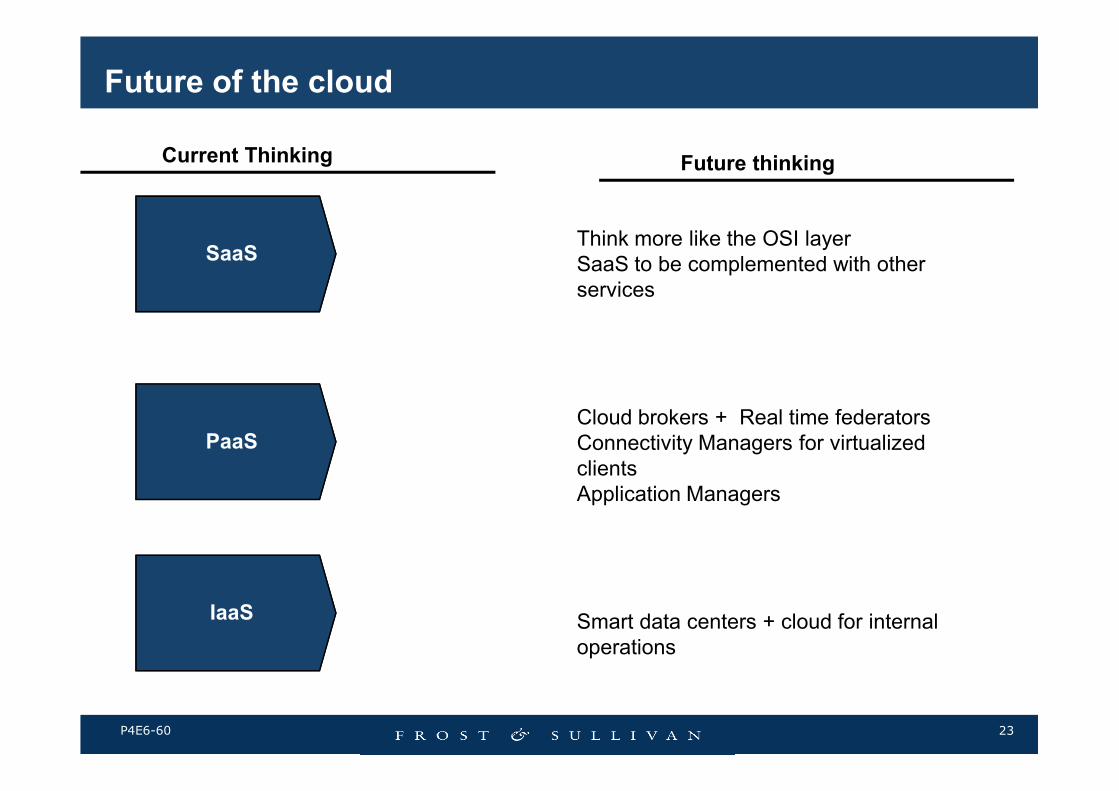

Future of the cloud

SaaS

Current Thinking Future thinking

Think more like the OSI layer

SaaS to be complemented with other

services

23P4E6-60

PaaS

IaaS

Cloud brokers + Real time federators

Connectivity Managers for virtualized

clients

Application Managers

Smart data centers + cloud for internal

operations

Market Outlook - Consumer centric 1

Market Outlook – enterprise centric 2

24

Key opportunities and imperatives 3

The key imperatives for operators include the following

Maximize the Revenue Opportunity Minimize the costs to serve Improve customer

experience

Key imperatives for ecosystem dominance

25

Increase bundling to reduce churn Explore new revenue streams

Scaling without increase in costs

Innovative pricing models

Demand shaping/yield management Common IP core and backhaul

Real-time offer management

Integrated view

Segmented offerings

Speed up time to market

Ability to differentiate

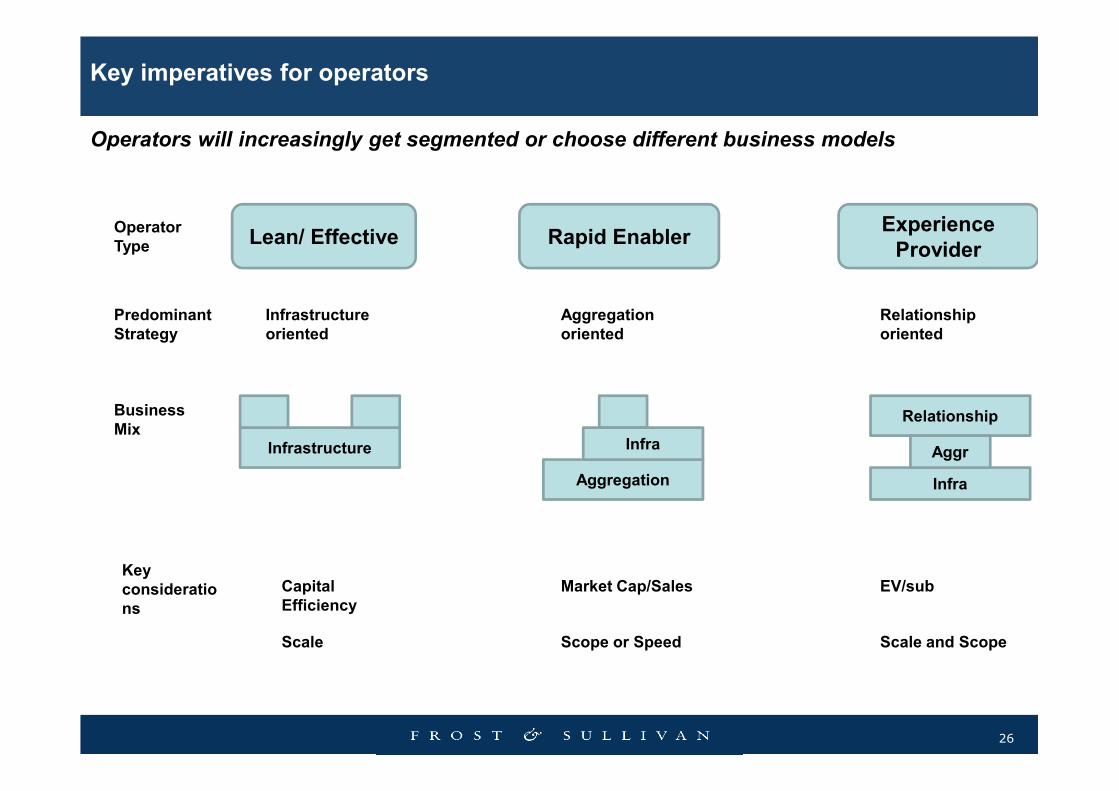

Operators will increasingly get segmented or choose different business models

Key imperatives for operators

Lean/ Effective Rapid Enabler Experience Provider

Operator Type

Predominant Strategy

Infrastructure oriented

Aggregation oriented

Relationship oriented

26

Business Mix

Key considerations

Infrastructure

Aggregation

Relationship

Infra

AggrInfra

Capital Efficiency

Market Cap/Sales EV/sub

Scale Scope or Speed Scale and Scope

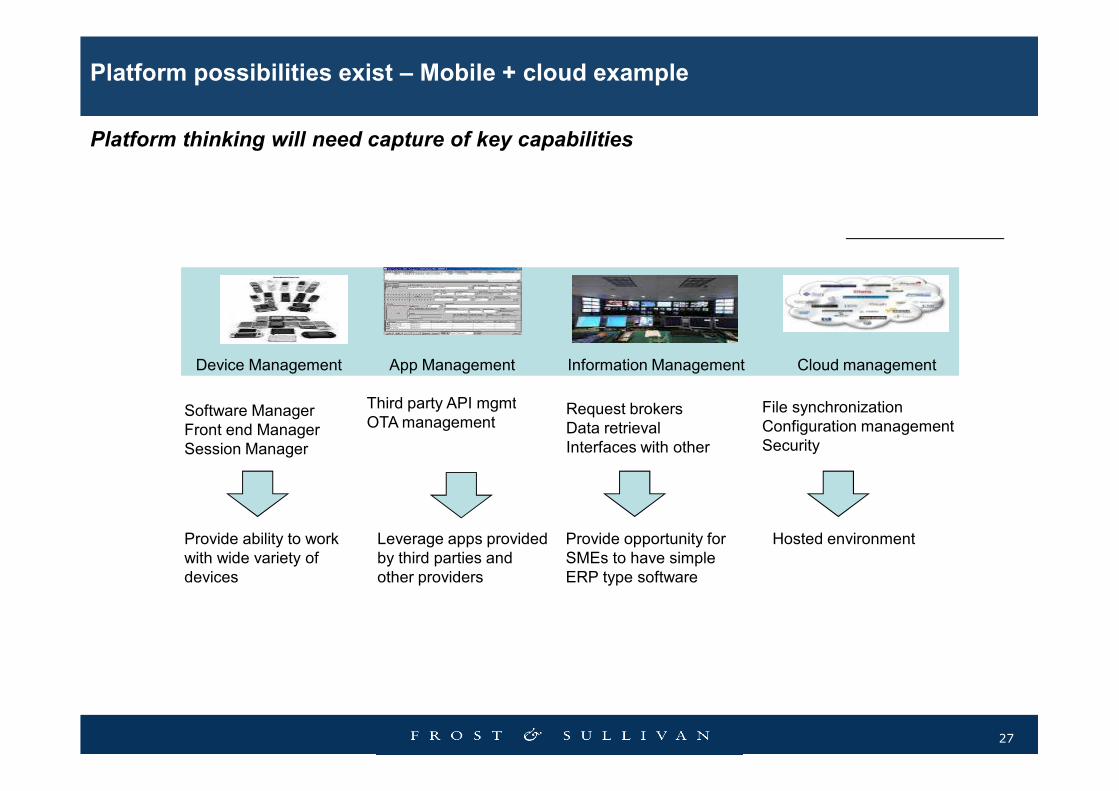

Platform thinking will need capture of key capabilities

Platform possibilities exist – Mobile + cloud example

Device Management Information Management Cloud management App Management

Third party API mgmt

27

Software Manager

Front end Manager

Session Manager

Request brokers

Data retrieval

Interfaces with other

File synchronization

Configuration management

Security

Third party API mgmt

OTA management

Provide ability to work

with wide variety of

devices

Leverage apps provided

by third parties and

other providers

Provide opportunity for

SMEs to have simple

ERP type software

Hosted environment

Global Growth Consulting Company

Gamsa Hamnida

28

Global Growth Consulting Company

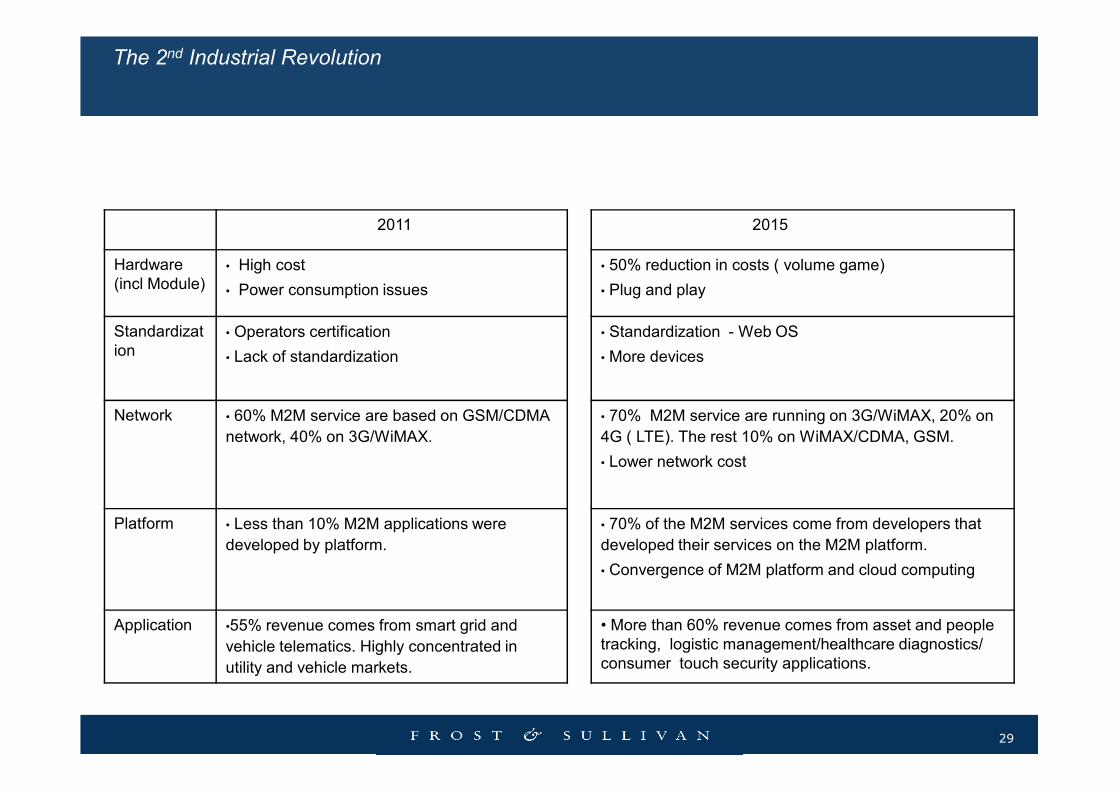

The 2nd Industrial Revolution

Hardware

(incl Module)

• High cost

• Power consumption issues

• 50% reduction in costs ( volume game)

• Plug and play

Standardizat

ion

• Operators certification

• Lack of standardization

• Standardization - Web OS

• More devices

2011 2015

29

Network • 60% M2M service are based on GSM/CDMA

network, 40% on 3G/WiMAX.

• 70% M2M service are running on 3G/WiMAX, 20% on

4G ( LTE). The rest 10% on WiMAX/CDMA, GSM.

• Lower network cost

Platform • Less than 10% M2M applications were

developed by platform.

• 70% of the M2M services come from developers that

developed their services on the M2M platform.

• Convergence of M2M platform and cloud computing

Application •55% revenue comes from smart grid and

vehicle telematics. Highly concentrated in

utility and vehicle markets.

• More than 60% revenue comes from asset and people

tracking, logistic management/healthcare diagnostics/

consumer touch security applications.

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

30

http://twitter.com/frost_sullivan

http://www.slideshare.net/FrostandSullivan

For Additional Information

Donna Jeremiah

Corporate Communications

Asia Pacific

+603 6204 5832

Mi Ok Lee

Corporate Communications

Asia Pacific - Korea

+82 2 6710 2033

31

Jayesh Easwaramony

Vice President

Asia Pacific

ICT

+65 6890 0999