technological links and predictable returns · 2018-01-10 · technological links and predictable...

TRANSCRIPT

Technological Links and Predictable Returns

Charles M. C. Lee, Stephen Teng Sun, Rongfei Wang, and Ran Zhang**

September 10, 2017

Abstract

This paper finds evidence of return predictability across technology-linked firms.

Employing a classic measure of technological closeness between firms, we show that

the returns of technology-linked firms have strong predictive power for focal firms’

returns. A long-short strategy based on this effect yields monthly alpha of 117 basis

points. This effect is distinct from industry momentum, and is more pronounced for

more innovative firms, firms with higher investor inattention, and firms with higher

costs of arbitrage. We find a similar lead-lag relation between the earnings surprises,

analyst revisions, and innovation-related activities (such as patent and citation counts)

of technology-linked firms. Our results are broadly consistent with sluggish price

adjustment to more nuanced technological news.

JEL classification: G10, G11, G14, O30

Keywords: Technology momentum, stock returns, return predictability, patents,

technological closeness, limited attention, market efficiency

** Corresponding author: Charles M.C. Lee, Joseph McDonald Professor of Accounting, Graduate

School of Business, Stanford University, 655 Knight Way, Stanford, CA 94305-7298; Tel: (650)

721-1295; Fax: (650) 725-9932; Email: [email protected]. Stephen Teng Sun

([email protected]) is Assistant Professor of Economics at the Guanghua School of Management,

Peking University. Rongfei Wang ([email protected]) is a PhD Candidate in Accounting at

the Guanghua School of Management, Peking University. Ran Zhang ([email protected])

is Associate Professor of Accounting at the Guanghua School of Management, Peking University.

1

Technological Links and Predictable Returns

September 10, 2017

Abstract

This paper finds evidence of return predictability across technology-linked firms.

Employing a classic measure of technological closeness between firms, we show that

the returns of technology-linked firms have strong predictive power for focal firms’

returns. A long-short strategy based on this effect yields monthly alpha of 117 basis

points. This effect is distinct from industry momentum, and is more pronounced for

more innovative firms, firms with higher investor inattention, and firms with higher

costs of arbitrage. We find a similar lead-lag relation between the earnings surprises,

analyst revisions, and innovation-related activities (such as patent and citation counts)

of technology-linked firms. Our results are broadly consistent with sluggish price

adjustment to more nuanced technological news.

JEL classification: G10, G11, G14, O30

Keywords: Technology momentum, stock returns, return predictability, patents,

technological closeness, limited attention, market efficiency

2

1. Introduction

The valuation of firms’ technological capabilities is becoming increasingly

important for investors as society becomes more innovation-driven. For many firms

today, technological prowess is an important determinant not only of short-term

profitability but also of long-term survival. At the same time, a firm’s technological

capabilities are notoriously difficult to measure. Moreover, a growing literature

reports that investors do not seem particularly good at valuing these capabilities. For

example, investors tend to misvalue innovation (Cohen, Diether and Malloy, 2013) or

undervalue innovative efficiency and originality (Hirshleifer, Hsu, and Li, 2013,

2017). In this paper, we find that investors also seem to overlook another potentially

important source of technology-related information: recent price-relevant news

affecting other technologically linked firms.

Firms do not conduct its technological research in isolation; frequently, they

interact with each other intensively, leading to an innovation process characterized by

knowledge spillovers (Jaffe, Trajtenberg, and Henderson, 1993). Given the

particular nature of innovation and its ever-growing role in firm behavior and

valuation, it is important that we go beyond firms’ own innovation characteristics and

examine the implications of firms’ interactions in innovation. Firms working on

areas of innovation that substantially overlap with each other could be subject to

similar input or output linkages, which become important transmission channels for

common price shocks (Acemoglu et al., 2012). Firms with similar technologies can

also benefit from the spillover effect of each other’s innovation activity along

3

technological lines (Bloom, Schankerman, and Van Reenen, 2013). Specifically,

firms working on similar technologies may use similar inputs of production, with the

inputs here being broadly interpreted as anything required in the production process,

i.e., valuable human resources, key raw materials, production and management

equipment and structures including Information and Communication Technology

(ICT) or intangible knowledge in production. For example, breakthroughs in

production technology led to dramatic cost reductions in silicon chips, which in turn

greatly impacted on the vitality of the electronics industry that relies on these chips as

a raw material. Similarly, technological progress in touch screen technology today

bodes well for the firms making products that use these touch-screens.

In this paper, we examine how shocks to one firm affect other firms that are

closely related in terms of their technological expertise. While previous studies

document rich asset pricing implications of several types of relationship between

firms, including product market link, customer-supplier link, geographical link, labor

market link, and alliance link (Hou, 2007; Cohen and Frazzini, 2008; Cohen and Lou,

2012; Li, Richardson, and Tuna, 2014; Huang, 2015; Lee, Ma, and Wang, 2015; Li,

2015; Cao, Chordia, and Lin, 2016), relatively little work has been done on the

pricing implications of technological affinity. If investors understand and take into

account the ex ante publicly available technological links, prices of the focal firm

should fully adjust when news about its technology-linked firms arrives at the market.

On the other hand, if investors are slow to understand and/or do not pay enough

attention to the news affecting firms that are closely-aligned in technological space,

4

stock prices of focal firms will exhibit a predictable lag with respect to recent news

affecting its technology-linked peers. Therefore, one asset pricing implication of

investors’ limited processing capability and attention with respect to technological

links is that price movements across linked firms are predictable: specifically, focal

firm prices will adjust with a lag to shocks experienced by linked firms.

To better illustrate our idea that news about one firm could translate into other

firms in the technology space, consider the celebrated “Steve Jobs Patent” (patent

number 7,479,949, with Steve Jobs as Co-inventors), which was granted on January

20, 2009. This patent, titled “Touch screen device, method, and graphical user

interface for determining commands by applying heuristics”, is the core patent of

Apple’s multi-touch technology, which is widely used today in iPhones and iPads.

The granting of this patent was accompanied by extensive media coverage right after

the grant date and in subsequent years.1 During the [t, t+2] window of the patent

grant date, the abnormal return of Apple is 10.56%, which largely accounted for the

firm’s abnormal returns for the entire month of January.2

Although Steve Jobs and Apple are the most direct beneficiaries of this patent

grant, the event is also significant for the broader field of multi-touch technology.

This is because multi-touch technology has wide applicability to many products

beyond iPhones and iPads.3 For example, touch screens can be used in products

1 For example: http://www.dailytech.com/Apple+Awarded+MultiTouch+Patent/article14073.htm. The

wide influence of the “Steve Jobs Patent” is also reflected in the enormous number of forward citations:

as of August 31, 2017, it has been cited more than 1,000 times, according to the google patent website.

https://patents.google.com/patent/US7479949B2/. 2 The 3-day abnormal return is defined as 3-day cumulative market adjusted return, where the market

return is the CRSP value-weighted average return. 3 As the title suggests, multi-touch technology allows two or more fingers to be used on the

touchscreen, and this enables devices to recognize and respond to more than one touch at the same time.

5

such as televisions, interactive screens, and ATMs. This technology also has

application in contexts as wide as in-car instrument panels, intelligent home

appliances, hospitality counters, among others. According to Research and Markets,

a market research company, the global market for multi-touch screen alone was

valued at $6 billion in 2016, and is projected to reach $16 billion by 2023.4

Therefore, while the granting of this patent confers some monopoly power upon

Apple, it also is an endorsement of the potential value and the technological feasibility

of multi-touch technology as a whole. It seems likely that other firms with similar

technological expertise will also benefit from this new information.

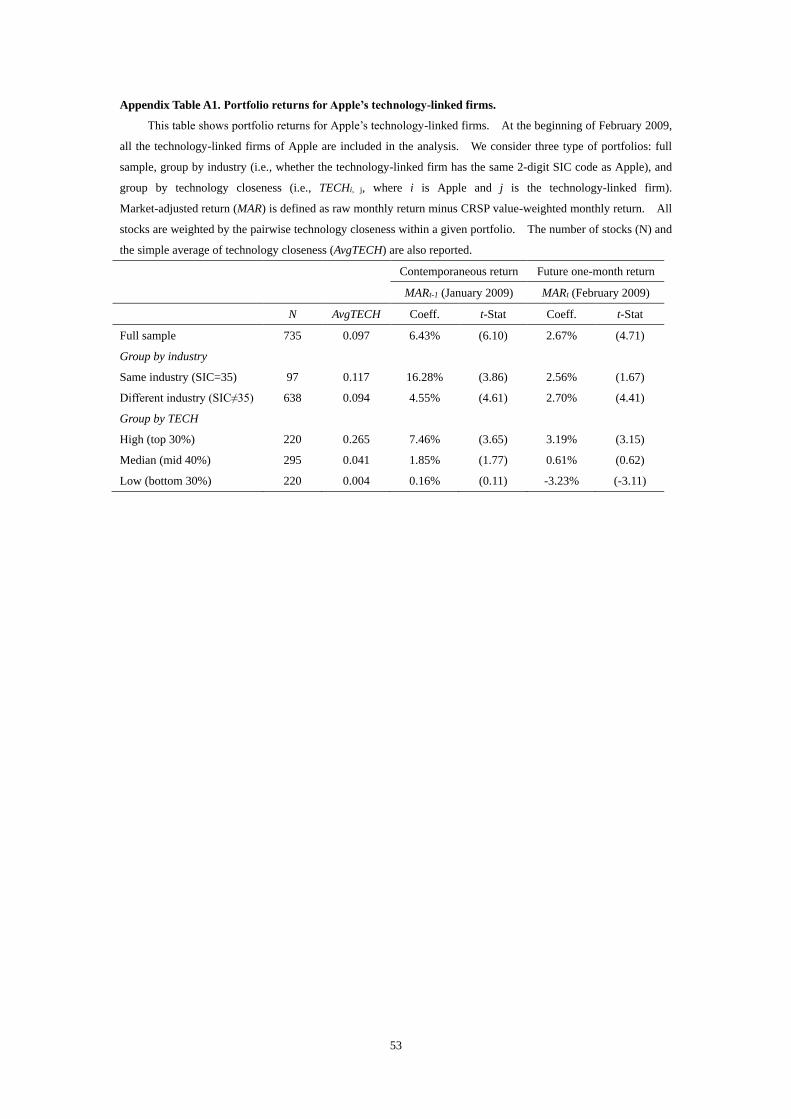

In Appendix Table A1, we report the returns for a portfolio of firms that are most

closely linked to Apple in terms of their technology, in the months surrounding the

approval of the Steve Jobs patent. Market-adjusted return (MAR) is defined as raw

monthly return minus CRSP value-weighted monthly return, and all stocks within a

given portfolio are weighted by a measure of technology closeness following Jaffe

(1986). For the month of the patent grant (January 2009), the full-sample MAR is

6.43% (t=6.10). In the subsequent month (February), the full-sample MAR is 2.67%

(t=4.71). These results suggest some contemporaneous stock comovement, as well

as some lead-lag effect. Interestingly, the effect of the contemporaneous

comovement is stronger for firms in the same 2-digit industry as Apple, while the

lead-lag return predictability is more pronounced for firms in different industries. In

fact, we find that technological proximity is directly related to the intensity of these

The multi-touch technology greatly expands the range of functionality that devices can support. For

instance, pinch to zoom is a classic function that works with multi-touch technology. 4 https://www.thestreet.com/story/14257336/1/.

6

results – both contemporaneous comovement and lead-lag return predictability are

stronger in the portfolio with the closest technology-link. These anecdotal findings

suggest that the pricing implications are stronger for firms with closer technological

ties.5 The Steve Jobs example demonstrates that technological affinity, an idea that

was first documented in Jaffe (1986), can capture an important dimension of

inter-firm relationship. To the extent that investors do not immediately recognize the

price relevance of this information, we would expect a diffused price adjustment

process along the lines of these technological links.

To test for the return predictability of technology-linked firms more generally,

we implement the following portfolio strategy. For each focal firm i, we calculate

the weighted return of a portfolio of firms that share similar technology as the focal

firm, 𝑇𝐸𝐶𝐻𝑅𝐸𝑇𝑖 = ∑ 𝑇𝐸𝐶𝐻𝑖𝑗 ∙ 𝑅𝐸𝑇𝑗𝑗≠𝑖 / ∑ 𝑇𝐸𝐶𝐻𝑖𝑗𝑗≠𝑖 where 𝑅𝐸𝑇𝑗 is the return of

firm j and 𝑇𝐸𝐶𝐻𝑖𝑗 measures the degree of technology closeness between firm i and j.

Specifically, we adopt the classic approach first pioneered in Jaffe (1986) and

developed in Bloom, Schankerman, and Van Reenen (2013) to calculate 𝑇𝐸𝐶𝐻𝑖𝑗,

which exploits firm-level data on patent distribution out of 427 different technology

classes to locate firms in a multidimensional technology space.

We then sort focal firms into decile portfolios based on lagged returns of their

technology-linked firms, and find strong evidence that lagged returns of those

technology-linked firms have significant return predictability for focal firms.

Specifically, a portfolio that goes long in those focal firms whose technology-linked

5 This results also indicate that it is important to use the degree of technology closeness as weights to

calculate technology-linked returns (TECHRET).

7

firms performed best in the prior month and goes short in those focal firms whose

technology-linked firms performed worst in the prior month, yields an equal-weighted

return of 117 basis points (t=5.47) per month. For the analogous value-weighted

portfolio, the returns are 69 basis points per month (t=3.19). We refer to this return

predictability as “technology momentum”. In subsequent tests, we show these return

prediction results are robust to a variety of controls, including size, book-to-market,

gross profitability, asset growth, R&D intensity, short-term reversal and medium-term

price momentum variables.

It is natural for firms in the same industry to share similar technologies, so

perhaps the return predictability we document is a rediscovery of the well-known

industry momentum effect (Moskowitz and Grinblatt, 1999; Hou, 2007). On the

other hand, prior studies report that while firms’ technology space has some overlap

with their product market space, firms in distinct product markets or industries also

often invest in similar technologies.6 Empirically, we also find that firms in the

closest technology-linked cohorts can come from many different industries.7

To formally test the prediction that the technology momentum effect that we

6 For example, Bloom, Schankerman, and Van Reenen (2013) document that while IBM, Apple,

Motorola, and Intel are all close in technology space, as demonstrated in their patenting activity and

joint research partnerships, but only IBM and Apple compete in the same PC market and only Motorola

and Intel compete in the semiconductor market. They also document firms competing in the same

industry (or more specifically, the same product market) may invest R&D in distinct technologies.

For instance, Gillette and Valance both compete in batteries but Gillette does R&D mainly in personal

care products while Valance developed a new phosphate technology for lithium ion batteries. 7 In our tests, an average (median) patent technology class contains firms from 10 (10) different

2-digit SIC industries and 31 (26) different 4-digit SIC industries. The average HHI concentration

ratio in a patent technology class by different 2-digit (4-digit) industry is 0.37 (0.21), showing that

various industries indeed secure patents in the same technology class. An HHI concentration ratio

close to 1 in our case means the majority of patents in one technology class comes from one industry

while a smaller ratio means patents are more evenly distributed among different industries in a given

technology class. In comparison, the HHI concentration ratio based on sales for an average 3-digit

SIC industry in Hou and Robinson (2006) is 0.54.

8

documented is not driven by the industry momentum effect identified by Moskowitz

and Grinblatt (1999), we incorporate past and current industry returns in our tests and

find that the technology-linked results are even stronger in the presence of industry

controls. In further tests, we also control for supplier and customer returns, and

pseudo-conglomerate returns, and find that our main results continue to hold.

Overall, these tests show that the technology momentum that we documented is

distinct from return momentum arising from industry links, customer-supplier links,

and standalone-conglomerate firm links.

To establish the robustness of this return predictability result, we conduct a series

of additional tests. First, we examine the predictive relation in sample sub-periods.

Dividing the full sample into four sub-periods, we find a clear and robust lead-lag

return relation in every sub-period. Next, we examine the sensitivity of our results to

the age of the technological closeness measure. Specifically we compute the

closeness measure based on patent issuance data that is available in year t, t-1, t-2, and

t-3. Our results show that measures of TECHRET relying on lagged one-, two-, and

even three-year technology closeness data still significantly predict focal firm returns,

although the predictive power decreases as the technology mapping becomes more

stale. Evidently, investors can form trading strategies like ours even with relatively

old measures of technological closeness.

Finally, we perturb the length of the return estimation and holding periods.

Following Moskowitz and Greenblatt (1999), we use various (L, H) strategies,

whereby the technology momentum portfolios are formed on L-month lagged returns,

9

held for H months, and rebalanced monthly. We examine various different lags (L =

1, 3, 6, and 12) and a variety of different holding periods (H = 1, 6, 12, 24, 36). We

find that the profitability of shorter-term strategies is not sensitive to the length of

ranking period L. The equal-weighted raw monthly return for (1,1) strategy and

(12,1) strategy is 1.17% and 1.11%, respectively. We also find that the profits decay

monotonically and diminish to be insignificant in the longer holding period H.

Specifically, we observe no sign of any return reversal in the longer period, indicating

that the return predictability of technology momentum cannot be explained by

investors’ overreaction.

Having established the robustness of the main result, we then conduct a series of

cross-sectional tests to shed light on how this result varies across different firms and

types of news. Ex ante, we posit that the magnitude of the delayed price reaction

will be an increasing function of: (a) the relevance of technology-linked firm news to

the focal firm, (b) the extent to which investors are inattentive, and (c) the relative

costs of arbitrage.

Specifically, we expect a stronger effect for focal firms that are more

innovation-driven (as measured by the size of their R&D spending and patent-related

activities, both scaled by book equity). If the technology momentum we document

represents a market inefficiency driven by investors’ limited attention and information

processing capacity, we should find a stronger effect for firms that investors are more

likely to overlook. To test this hypothesis, we use firm size, analyst coverage, and

institutional ownership as proxies for investor attention. Finally, if the return

10

predictability reflects mispricing, we would expect to see a greater effect in situations

where arbitrage costs are higher (firms with greater idiosyncratic volatility, or in the

case of bad news).8

Our test results support all these conjectures. We find strong evidence that the

technology-linked momentum effect is more pronounced when the focal firm is:

smaller, has fewer analysts covering them, has lower institutional ownership, and

exhibits higher arbitrage costs (proxied by idiosyncratic volatility and bad news).

The effect is also much stronger (more than doubled) for firms with higher than

median R&D spending and patent-related activities. These results further support

the view that technology momentum is a mispricing phenomenon driven by investors’

limited attention, valuation uncertainty, and arbitrage costs.

Finally, we conduct a series of tests designed to establish the fundamental nature

of the lead-lag pattern observed in returns. An alternative to the mispricing

explanation is that firms with similar technology are exposed to similar risk factors,

and that variations in these risk factors are driving the lead-lag return pattern. It is

not easy to think of examples of risk factors that might behave in ways that give rise

to these patterns. Nevertheless, a risk-based argument is difficult to rule out using

evidence based on stock return correlations alone.

In our final set of tests, we turn to measures of real activity and show that

technological linkages are helpful in identifying lead-lag correlation in the operating

performance as well as the innovation-related activities of tech-linked firms.

8 Prior studies suggest bad news tend to be incorporated into price more slowly (Hong, Lim, and Stein,

2000), either because investors are more reluctant to sell their losers, or because short-selling is more

costly to implement (Beneish, Lee, and Nichols, 2015).

11

Specifically, we find that the lagged earnings surprises (SUEs) of the

technology-linked firms are strong predictors of focal firm earnings surprises (SUEs),

even after controlling SUEs of the focal firm from the last four quarters. In fact, the

SUEs of the tech-linked firms have predictive power for the focal firm’s SUE over the

next four quarters. We observe a similar pattern in analyst forecast revisions

(FREV). Specifically, we find that, after including a host of control variables, lagged

FREVs of the tech-linked firms have strong predictive power for the FREV of the

focal firm. These earnings-based results strongly suggest that the return patterns we

documented earlier have their root in lead-lag patterns in firm fundamentals.

Furthermore, we find a similar lead-lag pattern in two important

innovation-related activities: the patent and citation counts. Specifically, we show

that the average number of patents granted in a given year to a portfolio of

technology-linked firms (where each peer firm is weighted by its pairwise closeness

to the focal firm) has significant predictive power for the patent applications of the

focal firm in the subsequent year. Similarly, the citation counts of technology-linked

peers (the number of forward life-time citations received by patents granted in a given

year) is a significant predictor of the citation counts of the focal firm. These results

are robust to the inclusion of a myriad of control variables, including year and

industry (or firm) fixed effects. Taken together, the patent and citation counts results

document a strong “innovation spillover” effect along technology-linked firms, which

lends further credence to the sluggish price adjustment hypothesis.

The remainder of the paper is organized as follows. Section 2 lays out the

12

background for the setting we examine in the paper. Section 3 describes the data and

variables. Section 4 provides our main results on technology momentum. Section

5 conducts more extensive robustness tests while Section 6 examines the mechanisms

in more detail. Section 7 explores the real effects of the technological link and

Section 8 concludes.

2. Background

Our paper is broadly related to several strands of literature. Firstly, there is a

rich literature documenting the patterns and consequences of investors’ limited

attention to information with substantial value implications. Theoretical works

starting with Merton (1987) examine the effect of investor inattention in security

prices, followed by later studies including Hong and Stein (1999), Hirshleifer and

Teoh (2003), and Peng and Xiong (2006). The general message from these models

is that delayed information recognition due to investors’ limited attention can give rise

to return predictability, beyond explanations by traditional asset pricing models. A

growing empirical literature is lending substantial support for these models’

predictions.9 In particular, Cohen and Frazzini (2008) find investors pay limited

attention to the performance of focal firm’s economically linked firms, i.e., the

customer firms. Consequently, focal firm’s stock price does not immediately

incorporate news involving linked firms, generating predictable future price

movement. We here study a more nuanced but nevertheless important link between

9 Exemplary works include Huberman and Regev (2001), Barber and Odean (2007), DellaVigna and

Pollet (2009), Hou (2007), Menzly and Ozbas (2010), and Hong, Torous and Valkanov (2007).

13

firms: their distance in technology space. Given limited investor attention, we posit

the value implications of this link will only be fully priced gradually over time,

particularly for firms that are more costly to arbitrage.10

Secondly, our work relates to research that examines investors’ limited

information processing capacity and its ramifications. Investors’ biased

interpretation of information could lead to a significant delay in the impounding of

information into asset prices. Tversky and Kahneman (1974) and Daniel, Hirshleifer,

and Subrahmanyam (1998), among others, show that this bias could stem from

investors overweighting their own prior beliefs and underweighting observable public

signals. Numerous recent empirical works lend support to this view. For example,

investors under-react to public announcements of corporate events (Kadiyala and Rau,

2004), stock splits (Ikenberry and Ramnath, 2002), and goodwill write-offs (Hirschey

and Richardson, 2003). Some of this work shows industry peer firms’ stock return

portends the focal firm’s stock return. For instance, Hou (2007) finds a lead-lag

pattern between weekly returns of large firms and small firms from the same industry,

and Jiang, Qian and Yao (2016) find industry leaders’ R&D growth could have

predictability for stock returns of other firms in the same industry, due to R&D

spillover effects. Our study of technology-linked momentum is a context where

investors are subject to limited information processing capacity along the

technological links, which often transcend industry links.

Thirdly, our work joins a burgeoning literature that studies the asset pricing

10 We use idiosyncratic volatility as a proxy for cross-sectional differences in arbitrage costs. Firms

with greater idiosyncratic volatility are generally more costly for investors to trade (see Baker and

Wurgler, 2006).

14

implications of firms’ innovation-related activities. Existing works find various

aspects of firm’s innovation activity, such as R&D intensity (Chan, Lakonishok, and

Sougiannis, 2001), R&D growth (Penman and Zhang, 2002; Eberhart, Maxwell, and

Siddique, 2004; Lev, Sarath, and Sougiannis, 2005), patent citations (Gu, 2005;

Matolcsy and Wyatt, 2008), and more recently, innovative efficiency (Hirshleifer, Li

and Hsu, 2013) and innovative originality (Hirshleifer, Li and Hsu, 2017) have strong

predictability for its future operating performance and stock return. Our work is

distinct from the existing literature in that we study the effect innovations by

technologically related peer firms, rather than innovations at the focal firm itself.

Our work is inspired by Bloom, Schankerman, and Van Reenen (2013), who

demonstrate that a firm’s technology space and product market space provide two

distinct inter-firm networks, as two firms in different product market industries could

produce patent in the same technology class and share similar innovative

knowledge.11 Utilizing the measure of technology closeness originally from Jaffe

(1986), they demonstrate the effect of peer firms’ R&D spending could be

decomposed into technology spillover effect (on technology space) and product

market stealing effect (on product market space). Our paper also makes use of this

approach to parametrize the distance between two firms in technology space and

complements the literature that has focused exclusively on the product market space.

In this dimension, our paper belongs to a growing accounting and finance literature 11 It is useful to note that the Bloom, Schankerman, and Van Reenen (2013) capture the effects of

concurrent R&D spending, our return prediction captures the information contained in other tech peers’

both existing and new knowledge stock. For example, stock return of a technology peer firm could

reflect investor valuation of new patent, or about valuation change to certain technology embedded in

existing patents due to news reflecting potential new usage or news about new innovations that will

make the existing technology obsolete.

15

that studies the wide implications of previously understudied firms’ technological link,

for example, corporate cash-holding (Qiu and Wan, 2014), M&A (Bena and Li, 2014),

bankruptcy (Qiu, Wang and Wang, 2016), strategic alliances (Li, Qiu and Wang, 2017)

and analysts coverage and forecast (Tan, Wang and Yao, 2016). Particularly relevant

to our work, Tan, Wang and Yao (2016) provide strong evidence that an information

spillover effect exists between two technologically related firms and it has substantial

implications for analyst coverage.

Lastly, our work is related to a concurrent working paper by Bekkerman and

Khimich (2017; hereafter BK) that also examines the pricing implications of firms’

technological link. We became aware of BK’s work only as we were wrapping up

our own. The motivating research question and main results of the two studies are

similar. However, our paper differs from BK in several important respects. First,

BK apply textual analysis to patent documents to determine technological affinity,

while our paper measures pairwise distance using patent class distribution (Jaffe,

1986).12 One advantage of our measure is that it measures the degree of technology

closeness between firms, providing an economically meaningful weighting scheme to

construct a weighted-average return of technology-linked firms. Second, due to

more stringent data requirements, BK only examine stock returns from 1997 onward,

while our approach enables us to study a much longer time period (from 1963

onward). Finally, we provide an extensive set of test results that document a lead-lag

12 The Jaffe (1986) approach is gaining wide acceptance in economics. A growing empirical

literature in accounting and finance has also utilized the this approach to measure the distance between

firms’ in technology space (such as Bena and Li, 2014; Qiu and Wan, 2015; Qiu, Wang and Wang,

2016; Li, Qiu, and Wang, 2016; Tan, Wang, and Yao, 2016). None of these studies focus on the issue

of lead-lag patterns in returns.

16

relationship in the fundamentals of technology-linked firms (i.e., unexpected earnings,

analyst forecast revisions, patent and citation counts). Overall, the two papers

corroborate well with each other, and provide complementary evidence that firms’

technological links contain valuable information that market prices only fully

incorporate gradually over time.

3. Data and Variables

The main data set used in this study is the Google patent data generously

provided by Kogan et al. (2017).13 Specifically, Kogan et al. (2017) use Optical

Character Recognition (OCR) technology and a number of textual analysis algorithms

to extract relevant information from the patent document, and then map the identified

assignees to the Center for Research in Security Prices (CRSP) unique identifiers

(PERMNO). This dataset covers 1.9 million CRSP matched patents granted by the

US Patent and Trademark Office (USPTO) from 1926 to 2010.14 We extract CRSP

matched patent information from the Google patent data to construct our

technology-linked variables.

Since we focus on the stock market implication for the patent information, it is

important to identify patents that are publicly available to investors to avoid

look-ahead bias. In particular, there are two important time points for each patent:

the application date and the grant date. The application date is the date that the

13 The Google patent data are available at: https://iu.app.box.com/patents. 14 The Google patent data has a more extensive coverage than the NBER patent data developed by Hall,

Jaffe, and Trajtenberg (2001). For example, during the same period covered by the NBER patent data

(1976-2006), the Google patent data adds an average of 2,187 patents per year to the NBER patent data

and corrects some errors.

17

inventors apply for a new patent to the USPTO, the grant date is the date that the

patent gets formally issued by the USPTO, and the lag between the two dates is on

average two to three years. Unless there is a federal holiday, the USPTO issues

patents every Tuesday, and its publication, Official Gazette, lists detail information of

the patents granted on that day.15 Thus the investors are able to get the patent

information freely from the patent offices on the grant date.16 Examining abnormal

stock turnover around patent grant date, Kogan et al. (2017) provide evidence that

patent grant conveys important information to the market and is reflected in the stock

price. Therefore, we use the grant date as our key time point to identify the patent

information.

Our main sample consists of firms in the intersection of the Google patent data,

CRSP and COMPUSTAT. We focus the analysis on common stocks (CRSP share

codes 10 and 11) and exclude financial firms with one-digit SIC codes of six. To

insure that the relevant accounting and patent information is publicly known to

investors in the market, we impose at least a six-month gap between fiscal-year end

month and stock returns in our stock return tests. Specifically, we first match the

Google patent data for grant year t with COMPUSTAT accounting data for the same

fiscal year t, and then match to CRSP stock returns data from July year t+1 to June

year t+2, as in Fama and French (1992). We require firms to have non-missing

15 The USPTO patent information is available at: https://www.uspto.gov/patent. 16 We note that after the American Inventors Protection Act (AIPA), which came into effect on

November 30, 2000, the USPTO began publishing patent applications 18 months after the application

date. For patents that were filed after November 30, 2000, the market had full knowledge of the

patent at the publication date (which is 18 months after the application date) or the grant date,

depending on which is earlier. In contrast, for the patents filed before November 30, 2000, the grant

date was the earliest time for the market to know the patent.

18

market equity and SIC classification code from CRSP, and non-negative book equity

data at the end of previous fiscal year from COMPUSTAT. We further restrict our

sample to firms that have at least one patent granted in the rolling-window of past five

years.17 In order to reduce the impact of micro-cap stocks, we exclude from our

sample stocks that are priced below one dollar a share at the beginning of the holding

period. 18 Moreover, we employ the return correction approach suggested in

Shumway (1997) for the delisting bias, though these adjustments have no effect on

our results.

In addition to stock returns, we obtain institutional holdings data from the

Thomson Reuters 13F dataset, and analyst forecast data from Institutional Brokers’

Estimate System (IBES) unadjusted files. Specifically, in each month we get most

recent mean consensus forecasts as well as the analyst coverage number immediately

prior to the portfolio formation date. Following Jegadeesh et al. (2004), analyst

forecast revision is defined as the change of one-year-ahead earnings consensus

forecasts for the same fiscal year in a given month, scaled by the beginning price of

the month.

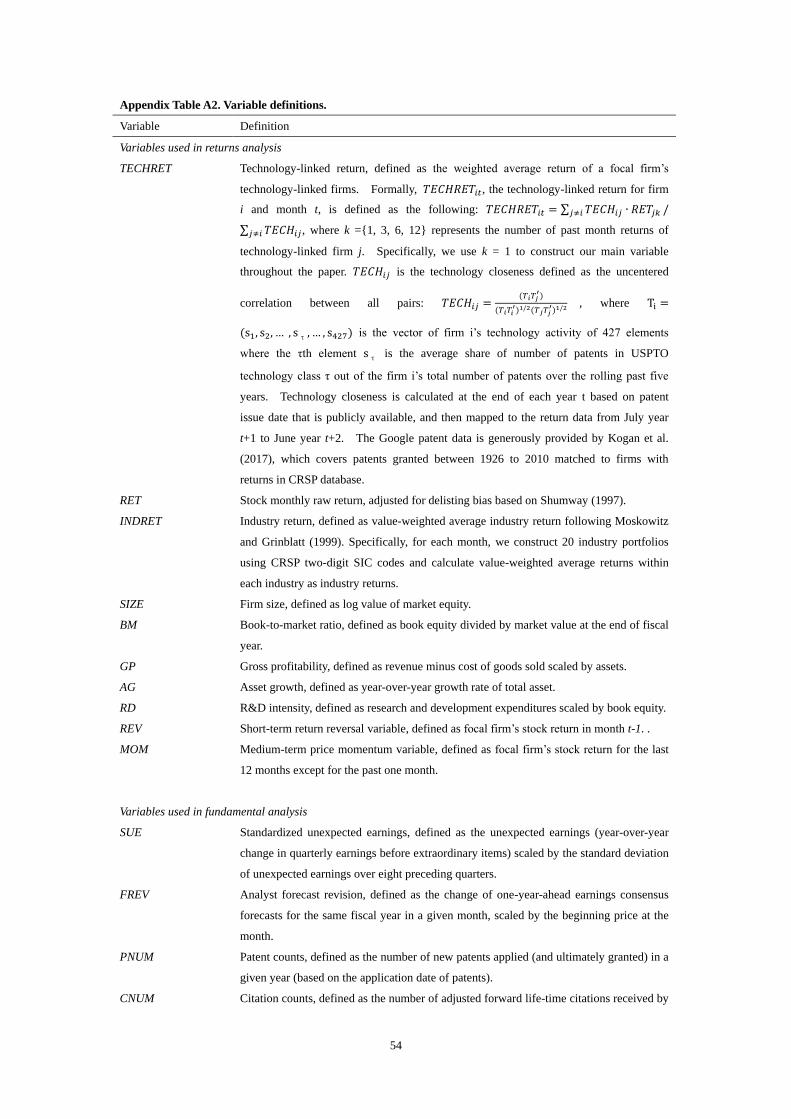

We measure technology-linked return (TECHRET) as the average monthly return

of technology-linked firms in the technology space weighted by pairwise technology

closeness, which is determined on the basis of 427 different technology classes

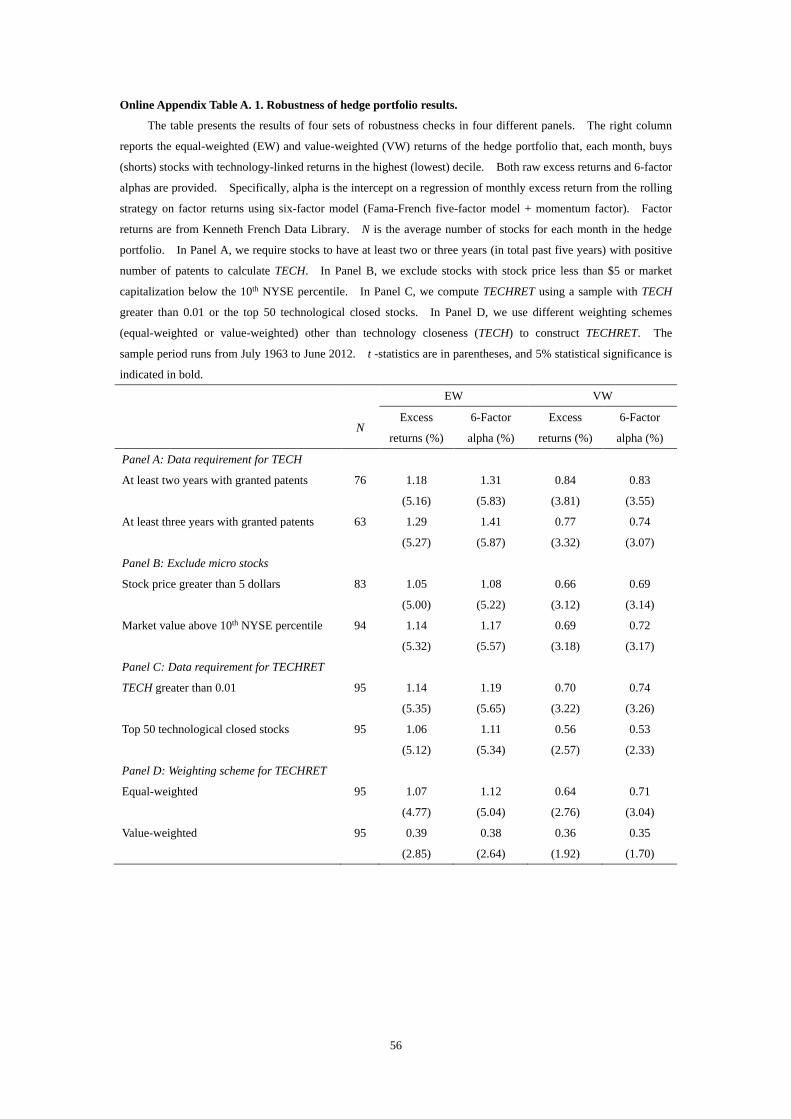

defined by USPTO for all patents. Formally, technology-linked return for firm i and 17 In the robustness tests (Panel A, Online Appendix Table A.1), we further require the sample firms to

have at least two or three years with granted patents in the rolling-window of past five years, and our

results are robust with this alteration. 18 In the robustness tests (Panel B, Online Appendix Table A.1), we exclude stocks with price below

five dollars a share or market capitalizations below the 10th percentile of NYSE stocks in our analysis,

and find results unchanged.

19

month t is defined as:

𝑇𝐸𝐶𝐻𝑅𝐸𝑇𝑖𝑡 = ∑ 𝑇𝐸𝐶𝐻𝑖𝑗 ∙ 𝑅𝐸𝑇𝑗𝑘𝑗≠𝑖

/ ∑ 𝑇𝐸𝐶𝐻𝑖𝑗𝑗≠𝑖

where k ={1, 3, 6, 12} represents the number of past month returns of

technology-linked firm j. Unless otherwise noted, we use k = 1 to construct our

main variable throughout the paper. We also take k = 3, 6, 12 in our robustness tests.

Following Jaffe (1986) and Bloom, Schankerman, and Van Reenen (2013), 𝑇𝐸𝐶𝐻𝑖𝑗

is the technology closeness defined as the uncentered correlation between all pairs,

𝑇𝐸𝐶𝐻𝑖𝑗 =(𝑇𝑖𝑇𝑗

′)

(𝑇𝑖𝑇𝑖′)1/2(𝑇𝑗𝑇𝑗

′)1/2

where 𝑇𝑖 = (𝑠1, 𝑠2, … , 𝑠𝜏, … , 𝑠427) is the vector of firm i’s technology activity of 427

elements and the τth element 𝑠𝜏 is the average share of number of patents in USPTO

technology class τ out of the firm i’s total number of patents over the rolling past five

years. Technology closeness ranges between zero and one, depending on the degree

of overlap in technology space, and is symmetric in firm ordering (i.e., 𝑇𝐸𝐶𝐻𝑖𝑗 =

𝑇𝐸𝐶𝐻𝑗𝑖 ). Note that by construction the TECH essentially acts as a weight in

calculating the average stock return of technology-linked firms and is biased toward

firms more technologically close to the focal firm (i.e., firms more adjacent to the

focal firm in technology space is given higher weights). TECH is calculated at the

end of each year t based on patent grant date that is publicly available, and then

mapped to the return data from July year t+1 to June year t+2. Other variables are

defined in Appendix Table A2.

The final sample consists of 561,989 firm-month observations spanning July

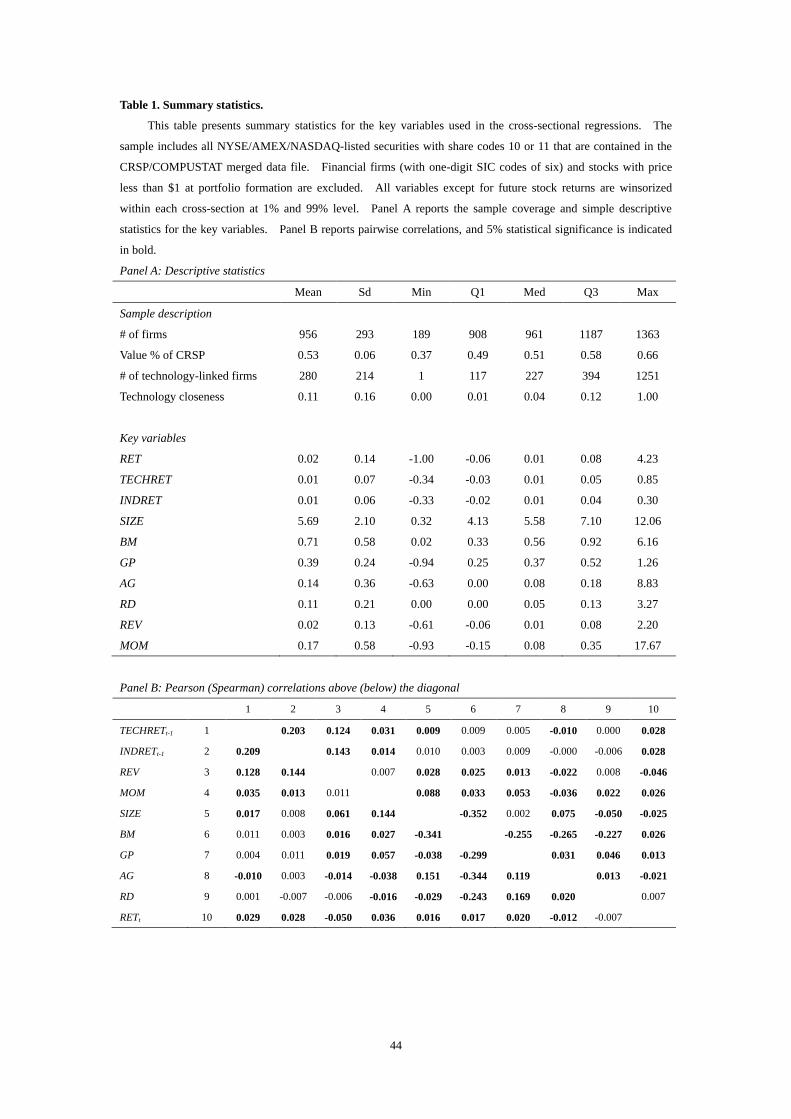

1963 to June 2012 (i.e., 588 months). Panel A of Table 1 presents the descriptive

20

statistics of sample firms. The number of firms varies from a low of 189 firms in

July 1963 and a high of 1,363 firms in June 2012. The sample firms cover almost 53%

of the CRSP common stock universe in terms of market capitalization. This is

unsurprising since we only include the sample firms with at least one patent granted in

the past five years. We note that the average number of linked firms in the

technology space is 280, and the pairwise technology closeness (TECH) has the

average of 0.11 and standard deviation of 0.16, indicating that the technological link

is quite pervasive and sparse.19 Panel A of Table 1 reports summary statistics for our

key variables. The average technology-linked return (TECHRET) is 0.01. The

distribution pattern is quite similar to industry momentum return (INDRET), and less

volatile than firm past one-month return (REV).

In Panel B of Table 1, several correlation coefficients are noteworthy. The

Pearson correlation between TECHRETt-1 and RETt is 0.028, providing raw evidence

for the lead-lag effect along the technological link. Although TECHRETt-1 exhibits

trivial correlations with a bunch of traditional return predictors (i.e., size,

book-to-market, gross profitability, asset growth, R&D intensity), it is considerably

positively correlated with industry momentum return (INDRETt-1), past one-month

return (REV) and medium-term momentum (MOM) (Pearson correlations are 0.203

for INDRETt-1, 0.124 for REV, and 0.031 for MOM). In the subsequent analysis, we

show the return predictability of TECHRETt-1 remains after controlling for other

variables under various settings.

19 In the robustness tests (Panel C, Online Appendix Table A.1), we only include sample firms of

which the technology-linked firms have TECH larger than 0.01 or rank in the top 50 in terms of TECH,

our main results are unchanged.

21

4. Empirical Results

4.1. Portfolio tests

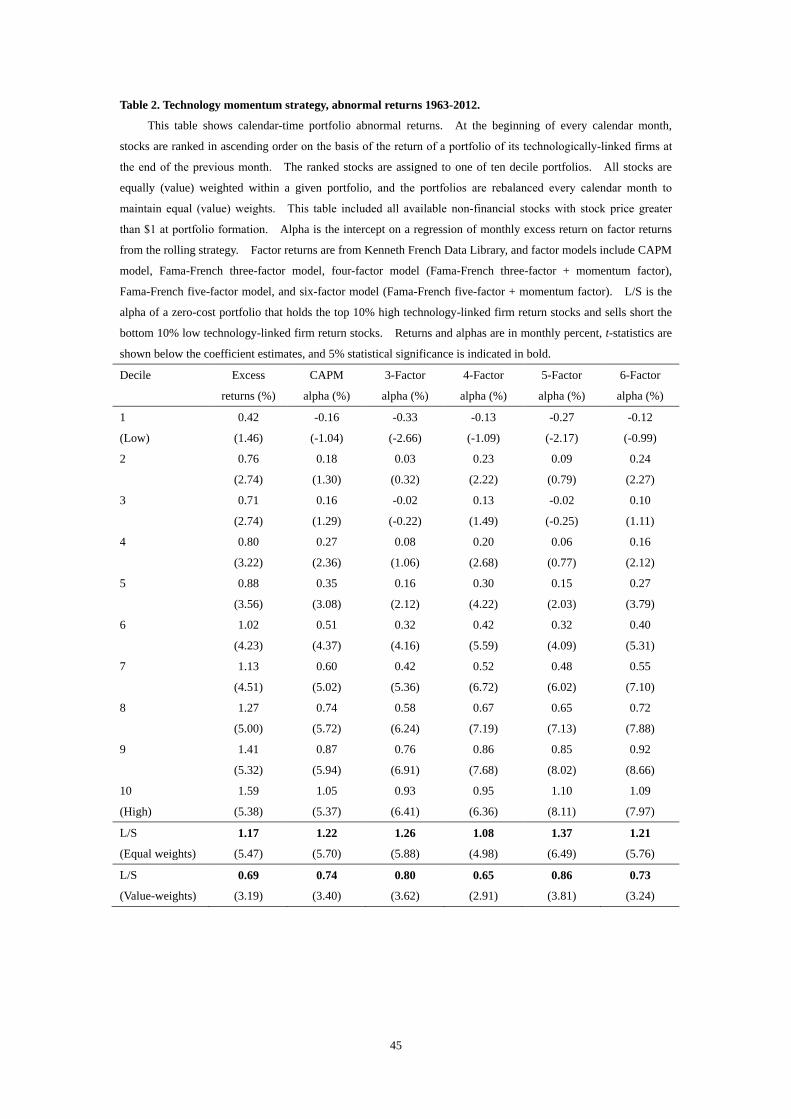

Table 2 shows the basic results of our paper. At the beginning of each month,

we sort all firms into deciles based on the return of their technology-linked portfolios

in the previous month. The decile portfolios are then rebalanced at the beginning of

each month to maintain either equal or value weights. The bottom lines show the

returns of a zero-cost portfolio that hold the top 10% high technology-linked firm

return stocks and sells short the bottom 10% low technology-linked firm return

stocks.

In Table 2, we find strong evidence consistent with technology-linked firm

returns predict focal firm returns. Specifically, taking the strategy of going long in

firms whose technology-linked firms performed best in the prior months and selling

short those firms whose technology-linked firms performed worst (L/S), yields

equal-weighted returns of 117 basis points per month (t = 5.47), or roughly 14.1% per

year. The corresponding value-weighted returns from the L/S portfolio are 69 basis

points per month (t = 3.19), or about 8.3% per year. In the next five columns, we

control for other known return determinants. The technology-momentum strategy

delivers CAPM abnormal returns of 1.22% (0.74%) per month for the equal (value)

weighted portfolios. The strategy delivers Fama and French (1993) abnormal returns

of 1.26% (0.80%) per month for the equal (value) weighted portfolios. Adjusting

returns for the stock’s own price momentum by augmenting the factor model with

22

Carhart’s (1997) momentum factor has the only negative but negligible effect on the

results. Subsequent to the portfolio formation, the baseline long-short portfolio

earns an abnormal return of 1.08% (0.65%) per months for equal (value) weighted

portfolios. Lastly, we adjust returns using the Fama and French (2015) five-factor

model and using the five-factor model plus the momentum factor. Those

adjustments have little effect on the results: subsequent to the portfolio formation, the

baseline zero-cost portfolio earns abnormal returns of 1.37% (0.86%) and 1.21%

(0.73%) for equal (value) weighted portfolios. The results show that after

controlling for common risk factors, high (low) technology-momentum stocks earn

high (low) subsequent (risk-adjusted) returns.20

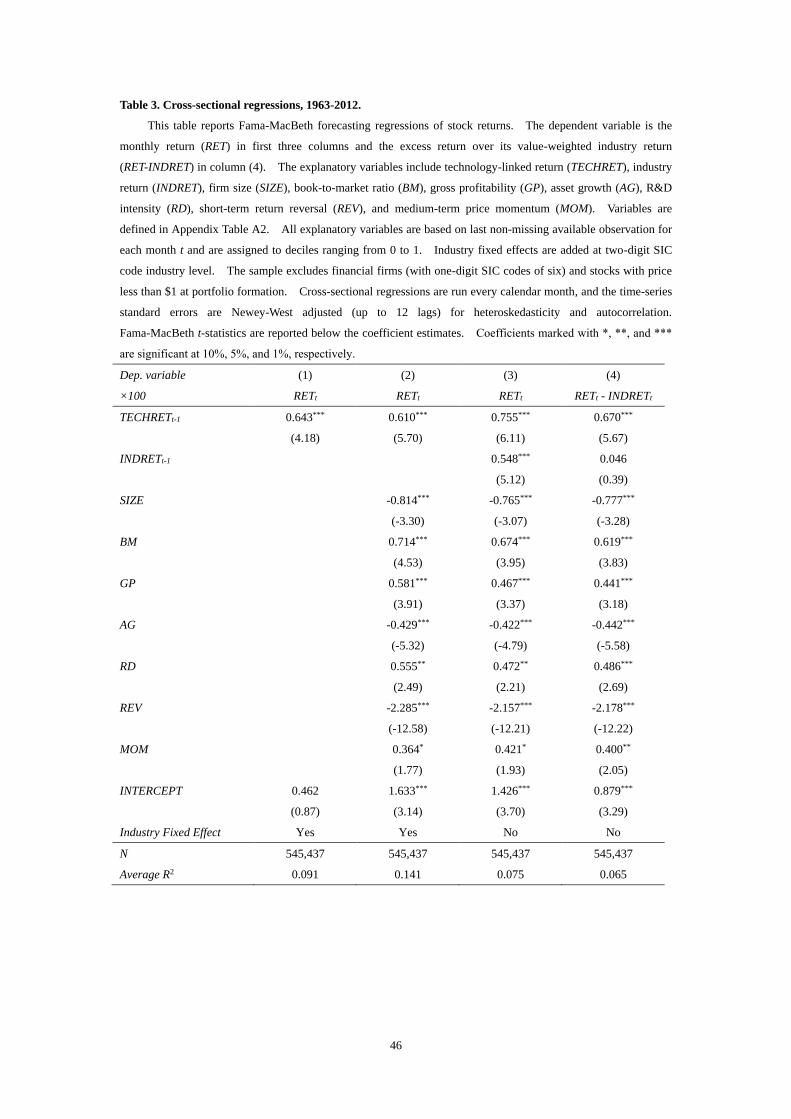

4.2. Regression results

In this section, we formally test our hypothesis in a regression framework,

controlling for other determinants of firm return and isolate the marginal effect of our

main variable, lagged technology-linked returns. Specifically, in Table 3, we

conduct forecasting regressions of focal firm returns using Fama and MacBeth (1973)

regressions. The dependent variable in columns 1-3 is the focal firm return in month

t (RETt). The independent variable of interest is the return of the focal firm’s

technology-linked firms in month t-1 (TECHRETt-1). We also include the

20 In Panel D of Online Appendix Table A.1, we show the portfolio results using alternative weighting

schemes. Specifically, for the equal-weighted scheme (i.e., constructing TECHRET by giving all

technology-linked firms equal weights), the long-short portfolio earns raw returns of 1.07% (0.64%)

per month for equal (value) weighted portfolios. For the value-weighted scheme (i.e., weighting

returns of technology-linked firms by their market capitalization), the long-short portfolio return

decrease to 0.39% (0.36%) per month for equal (value) weighted portfolios. These portfolio returns

are smaller than the TECH-weighted (i.e., weighting returns of technology-linked firms by the degree

of technology closeness to focal firms) baseline results in Table 2, supporting the value of technology

closeness (TECH) weighting scheme.

23

value-weighted industry return of the focal firm in month t-1 (INDRETt-1) as an

independent variable, following Cohen and Lou (2012) and Moskowitz and Grinblatt

(1999). Other control variables include lagged size, book-to-market, gross

profitability, asset growth, R&D intensity. Lastly, we include REV, a short-term

return reversal variable, defined as the focal firm’s stock return in month t-1, to

control for the short term reversal effect of Jegadeesh and Titman (1993), and MOM, a

medium-term price momentum variable, defined as the focal firm’s stock return for

the last 12 months except for the past one month, to control for the momentum effect

of Chan, Jegadeesh, and Lakonishok (1996). Cross-sectional regressions are run

every calendar month and the time-series standard errors are Newey-West adjusted

(up to 12 lags) for heteroskedasticity and autocorrelation.

Table 3 column 1-3 report the basic results. Consistent with the portfolio

results, TECHRETt-1 is a strong predictor of next month’s technology-linked focal

firm return in all three specifications. Specifically, before controlling for any other

variables, the coefficient of TECHRETt-1 in column 1 is 0.643 with a t-statistic of 4.18,

indicating that the average monthly return spread of the focal firms in the top and

bottom technology-linked return deciles is 64.3 basis point. In column 2, we include

size, book-to-market, gross profitability, asset growth, R&D intensity, reversal, and

momentum as control variables. The magnitude and significance of the coefficient

of TECHRETt-1 are almost the same as in column 1. In column 3, we further include

lagged industry return as a control variable. Both the magnitude and the significance

of the coefficient of TECHRETt-1 are getting even more pronounced to predict focal

24

firm’s return for month t after adding the industry momentum control variable, which

indicates that the technology momentum effect we documented cannot be explained

by the industry momentum effect documented by Hou (2007).

To better distinguish our technology-momentum effect from the previously

known industry momentum effect, we further report results of taking the

industry-adjusted return (calculated as the difference between a focal firm’s return this

month and its contemporaneous industry return) instead of the raw return as a

dependent variable. By subtracting the industry return from focal firm return, we

purge out stock return continuation that arises from industry wide return

auto-correlations. Column 4 of Table 3 indicates that, even after subtracting this

industry-wide information, TECHRETt-1 remains a strong predictor of focal firms’

returns next month. The magnitude and significance of the coefficient for

TECHRETt-1 are virtually the same when we use industry-adjusted returns. Finally,

consistent with the prior literature (Cohen and Lou, 2012), if the part of predictable

returns of focal firms is solely attributable to delayed information processing, rather

than industry-wide return continuation, we should see past industry returns have no

predictive power for (RETt-INDRETt). Consistent with this prediction, we find that

the coefficient on past industry returns, INDRETt-1, is indistinguishable from zero in

column 4. The coefficients for the control variables are also consistent with prior

literature: size, asset growth, and reversal variable are significantly negative related to

future returns, while the coefficient of book-to-market, gross profitability, R&D

intensity, and momentum are positive.

25

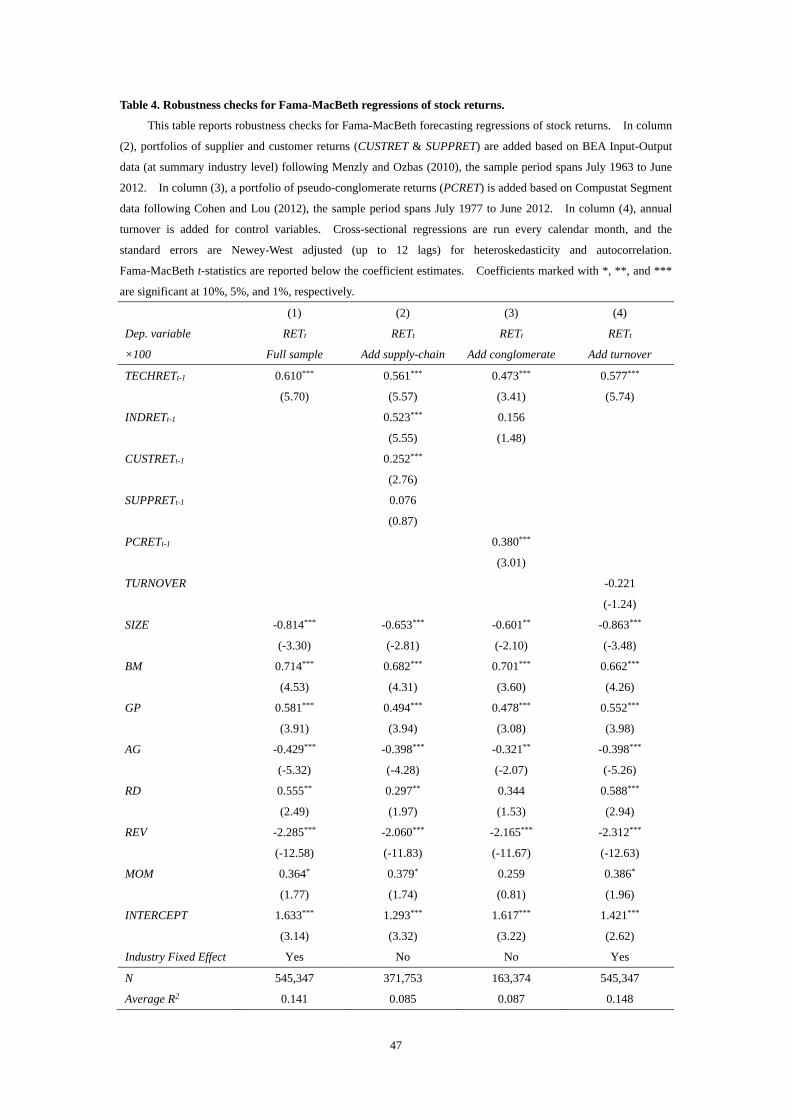

We further control for supplier and customer returns (Menzly and Ozbas, 2010),

pseudo-conglomerate returns (Cohen and Lou, 2012), and stock turnover in Table 4.

The results confirm the return predictability along the supply-chain as well as in the

complicated firms, and low turnover stocks require higher future returns. We note

that the magnitude and significance of the coefficient for TECHRETt-1 are

qualitatively the same as our main results, indicating that the information diffused

along the technological link cannot be explained by the information shocks from

supply-chain, business segment, or the illiquidity of stocks.

5. Other Robustness Tests

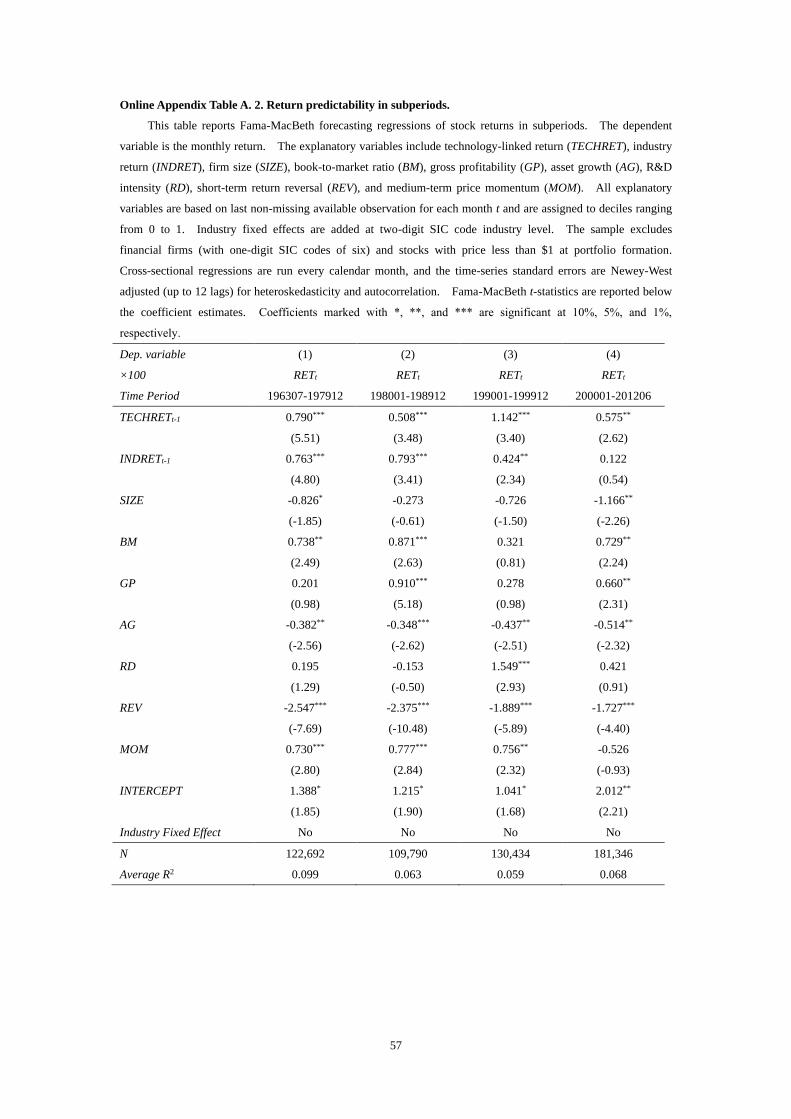

5.1. Technology-linked return predictability across time

In Online Appendix Table A.2, we examine whether the return predictability

power of technology-linked firms varies across time. We divide our full sample

periods into 1963-1979, 1980-1989, 1990-1999, and 2000-2012. We then exactly

repeat our baseline analysis from Table 3 for each subperiod. Our results hold up

well to this time disaggregation. The coefficients of TECHRETt-1 are all positive and

statistically significant after controlling for various return determinants.

In fact, the only surprise in Online Appendix Table A.2 is that there appears to be

little industry momentum in the last subperiod, which runs from 2000-2012. The

coefficient of INDRETt-1 is not significant for 2000-2012, while it is significant for the

first three subperiods. It is hard to say whether this just reflects noise in a short

sample or the fact that more arbitrageurs have caught on to the industry momentum

26

effects and are beginning to drive them out of existence. In any case, what is

noteworthy from our perspective is that though the average degree of industry

momentum may be declining over time, the technology momentum that we

documented have been robust across four periods.

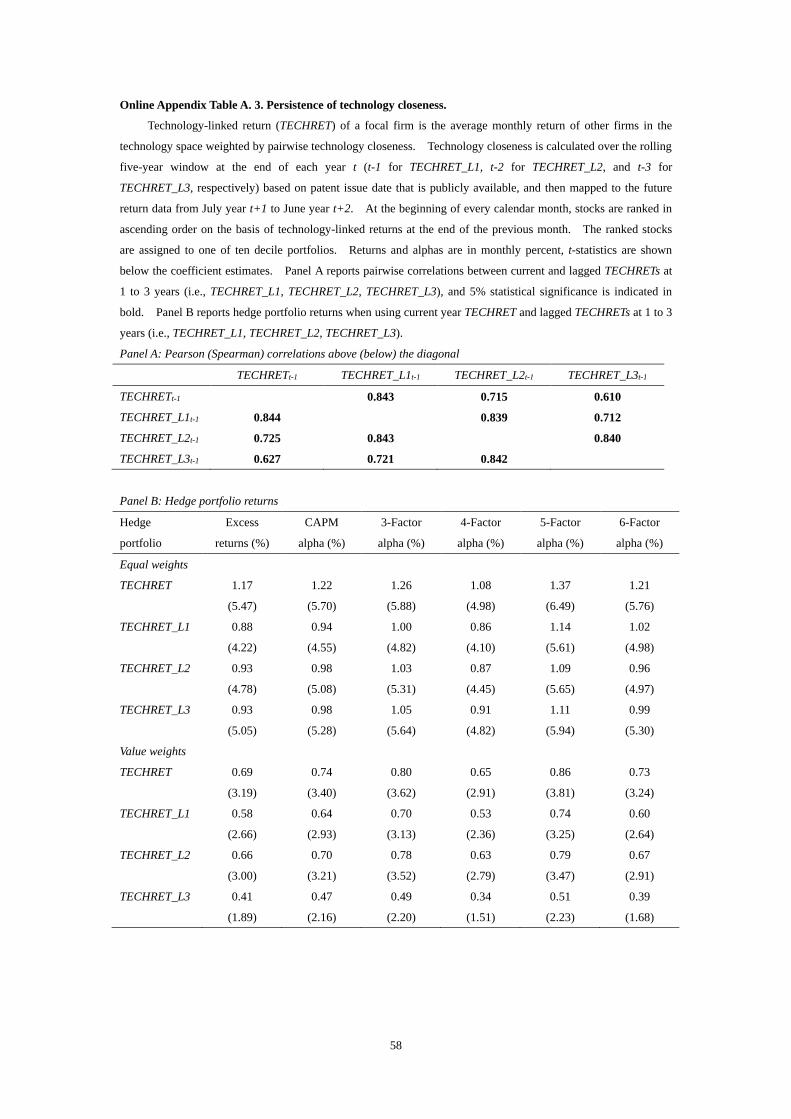

5.2. Persistence of technology closeness

In this section, we examine the persistence, or stickiness, of technology closeness.

More specifically, we examine the return predictability power when our technology

momentum strategy is based on the lagged one-, two-, three-year technology

closeness measures. Panel A of Online Appendix Table A.3 shows the correlations

for TECHRETt-1, TECHRET_L1t-1, TECHRET_L2t-1, TECHRET_L3t-1. The results

show that the correlation between TECHRETt-1 and its corresponding one-, two-,

three-year lagged measures are remarkably positive and significant. For instance,

the Pearson correlation coefficients between TECHRETt-1 and TECHRET_L1t-1 is

0.843. When the lagged year increases, the correlation coefficient decreases, but the

Pearson correlation between TECHRETt-1 and TECHRET_L3t-1 is still positive and

significant, with the coefficient of 0.610.

In Panel B, we find that technology closeness is quite sticky, in that both

and its lagged forms predict focal firm returns, while the predictability

power is lower, but still significant, for the lagged forms. Specifically, the one-year

lagged TECHRET_L1t-1 generates equal weighted returns of 88 basis points per month

(t=4.22), or roughly 10.6% per year. Controlling for other known return

determinants generates equally good or even better results. Comparing to

t-1TECHRET

27

TECHRETt-1, the return predictability power of TECHRET_L1t-1 is lower but still

quite good. Results for TECHRET_L2t-1 and TECHRET_L3t-1 further confirm the

return predictability of technology-linked returns, while predictability power

decreases when the lagged year increases. But even the technology momentum

strategy based on three-year lagged technology closeness measures works quite well,

which means that firm locations in technology space are quite stable, and even for

investors who do not have timely information on patent could still be able to make

good return predictions based on this strategy.

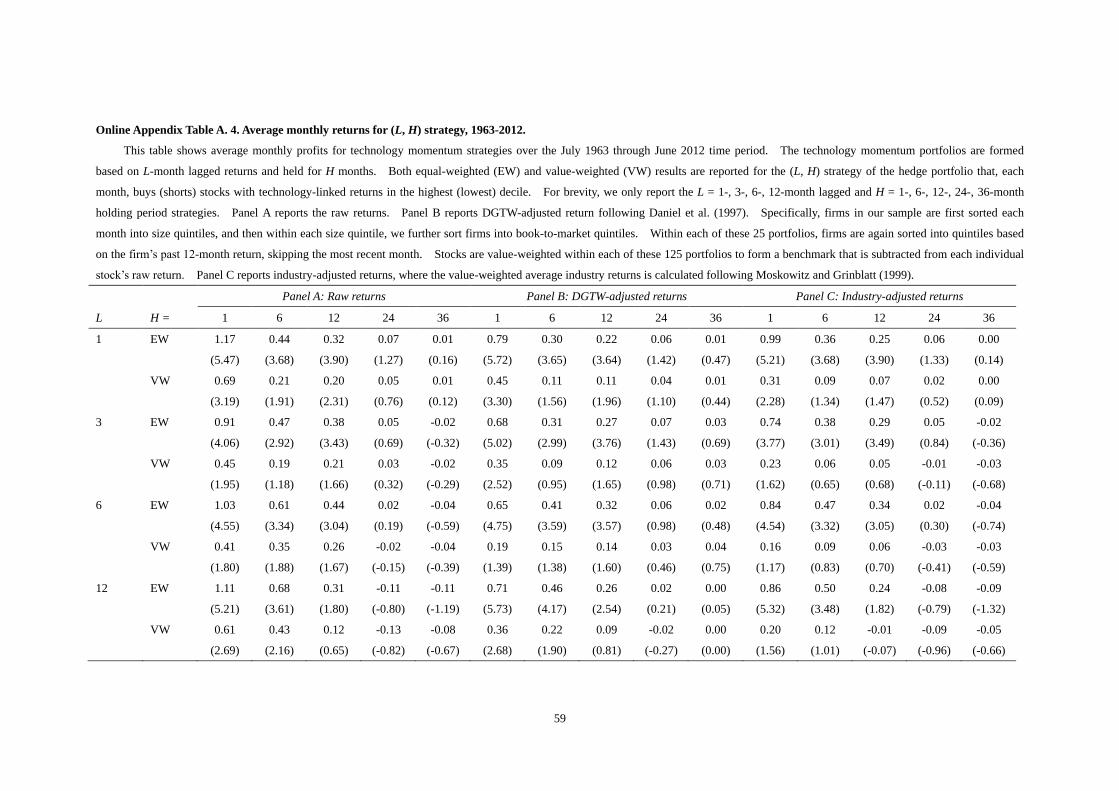

5.3. Predictability for time-period beyond one month

In Online Appendix Table A.4, we consider the profitability of (L, H) strategies

following Moskowitz and Greenblatt (1999) to show the speed of information

diffusion. In the (L, H) strategy, the technology momentum portfolios are formed

based on L-month lagged returns, held for H months, and rebalanced monthly. Both

equal-weighted and value-weighted results are reported for the (L, H) strategy of the

hedge portfolio that, each month, buys (shorts) stocks with technology-linked returns

in the highest (lowest) decile. For brevity, we only report the L = 1-, 3-, 6-,

12-month lagged and H = 1-, 6-, 12-, 24-, 36-month holding period strategies.

Among the strategies that we consider, the short-term (1,1) strategy (i.e., L=1,

H=1) is the most profitable. This result is robust to Daniel et al. (1997) (DGTW)

characteristic-adjusted returns and industry-adjusted returns, which is consistent with

prior regression results. Moreover, the profitability of short-term strategy is less

sensitive to the length of ranking period L. For example, the equal-weighted raw

28

monthly return for (1,1) strategy and (12,1) strategy is 1.17% and 1.11%, respectively.

And the equal-weighted DGTW-adjusted and industry-adjusted monthly return for

(1,1) strategy is 0.79% and 0.99%, respectively. We also note that the

value-weighted returns are smaller than the equal-weighted returns in all the strategies,

indicating that the speed of information diffusion is quicker in firms with big size.

While the return predictability along the technological link is considered to be a

short-term effect, we still find significant profits for strategies with longer holding

period H. For example, the equal-weighted raw monthly return for (1, 12) strategy is

0.32% with t-statistics of 3.90. However, the return predictability diminished to

insignificant in the longer holding period, and the decay is much quicker for

value-weighted portfolios, supporting the view that the information diffusion along

the technological link is a gradual process.

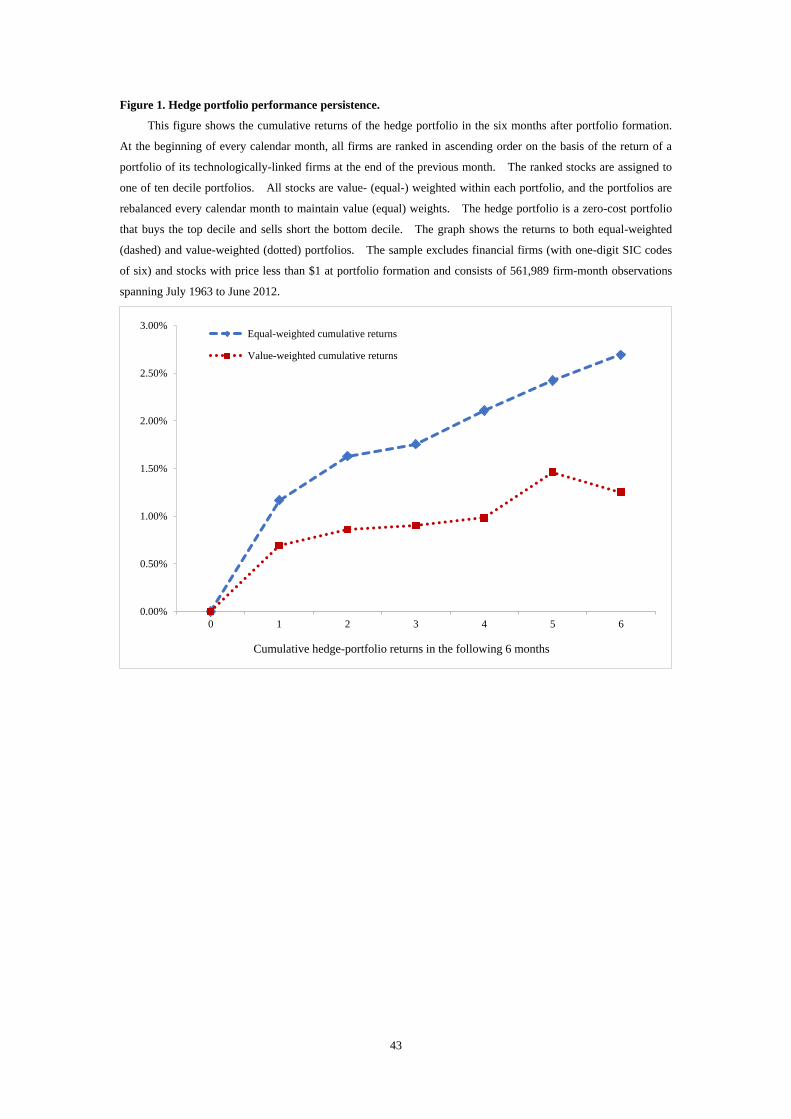

We further examine the long-run return patterns of our technology momentum

effect. It is possible that investors become enthusiastic about news to certain

technologies in some firms first and overreact by buying into other technologically

related firms in a lagged fashion. If this is the main driver behind the strong return

predictability we documented, then we should expect to see a full reversal in longer

periods. On the other hand, if the effect we document indeed reflects updating of

shocks to focal firms’ real fundamental values, we should see no reversal in the future.

In Figure 1, we test these two alternative hypotheses by showing the cumulative

returns to the hedge portfolio in the six months after portfolio formation. Consistent

with the results in Online Appendix Table A.4, we also observe modest additional

29

upward drift through month six. Extending the holding period to 12 or 24 months

produces similar patterns. Similar to the return lag reported in other inter-firm

studies (Moskowitz and Grinblatt, 1999; Cohen and Frazzini, 2008; Cohen and Lou,

2012), we see no reversal over the long-run, suggesting that we are capturing a

mechanism of delayed updating of focal firm prices to reflect information important

to their fundamental values.

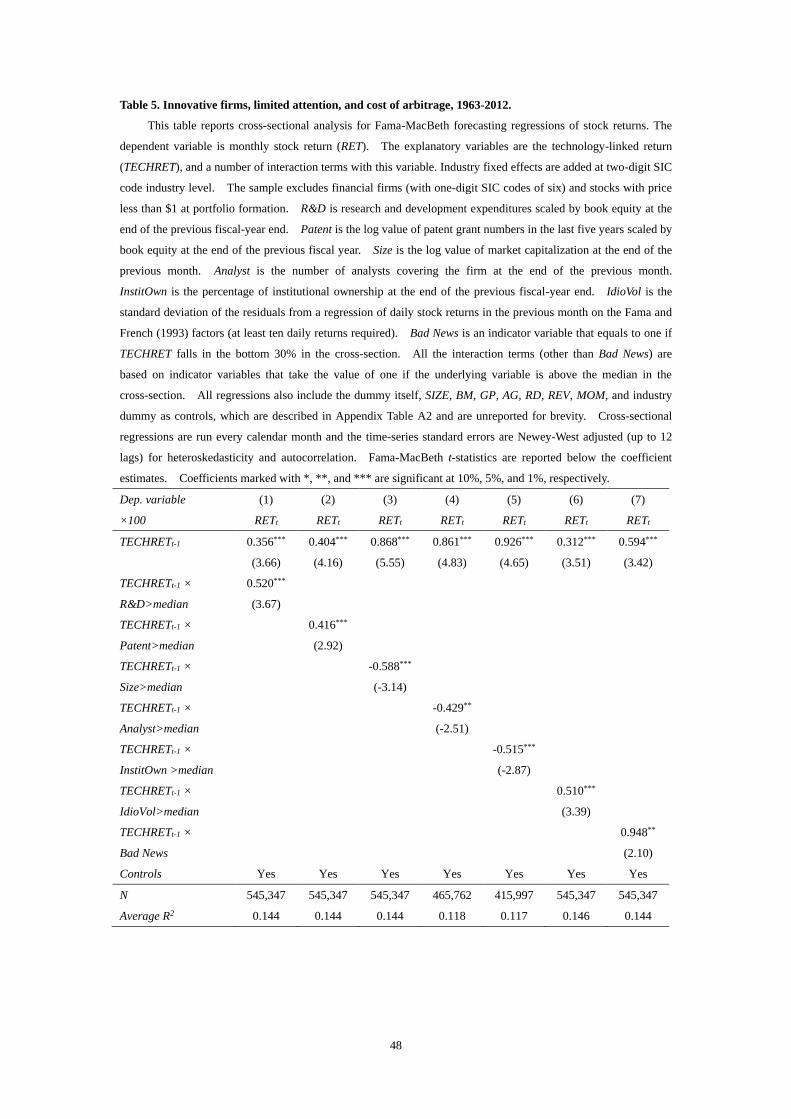

6. Innovative Firms, Limited Attention, and Cost of Arbitrage

6.1. More innovative firms

In this section, we examine the mechanism of technology-linked momentum

effect in more depth. Ex ante, we posit that the magnitude of the delayed price

reaction will be an increasing function of: (a) the relevance of technology-linked firm

news to the focal firm, (b) the extent to which investors are inattentive, and (c) the

relative costs of arbitrage. We begin by examining whether the technology

momentum effect is more pronounced for more innovative firms. We expect so for

two reasons: first, compared with traditional firms, more innovative firms are harder

to value and thus the information diffusion could be slower (Hirshleifer, Hsu, and Li,

2013); second, comparing a firm that takes innovation more seriously with a firm that

barely does innovation, the former is more likely to be affected by innovation shocks

and shocks to its technology-linked peers in particular. Thus, if our return effect is

truly driven by investors’ limited capacity and resources, combined with the valuation

difficulty of more innovative firms, we would expect that the more innovative the

30

firm, the more severe the lag in incorporating information into prices, and thus the

stronger the return predictability. Specifically, for each of the two innovation

intensity measures, we create a dummy variable that equals one if a focal firm is

above the sample median in a given year in terms of the innovation intensity measure

and zero otherwise. The prediction is that the coefficient on the interaction term of

TECHRETt-1 with the dummy variables is positive, i.e., these firms that are more

innovative should have more pronounced return predictability.

Columns 1-2 of Table 5 report the results. The regression specification is

similar to those in Table 3, i.e., a Fama-MacBeth predictive regression with the

dependent variable being the focal firm return (RETt) in the following month. In

addition to the interaction term between the categorical variable and TECHRETt-1, the

categorical variable itself and all control variables from the full specification (Table 3,

column 3) are also included, which are not reported for brevity. The coefficient

estimate on the interaction term between the R&D dummy and TECHRETt-1 is

positive and statistically significant, 0.520 (t=3.67), which implies that the magnitude

of the documented return effect is larger for firms with more R&D spending. In the

same vein, column 2 shows that the coefficient on the interaction term between the

Patent dummy and TECHRETt-1 is positive and statistically significant, 0.416 (t=2.92).

The difference is also economically large, as the technology momentum effect for

more innovative firms is over twice as large as that of other firms. These findings

confirm our prediction that more innovative firms exhibit a stronger return effect.

6.2. Investors’ limited attention

31

If the technology-momentum we documented is due to investors’ limited

attention, we should observe a stronger return effect for firms with less investor

attention. We employ three variables that are commonly used in the literature to

capture investor inattention: firm size, analyst coverage and institutional ownership.

Firms with smaller size, lower analyst coverage, and less institutional holding receive

less attention from investors and, therefore, should have more sluggish short-term

stock price reactions to the information contained in technology-linked firms and a

greater predictability of stock returns. Hirshleifer, Hsu, and Li (2013) report that

their innovative efficiency strategy is more pronounced for small firms. Analyst

stock coverage and institutional ownership are commonly used in the literature as

proxies for investor attention, and a number of papers show that return predictability

is stronger for firms with fewer analysts following and more institutional holdings

(Hou, 2007; Cohen and Frazzini, 2008; Menzly and Ozbas, 2010; Hirshleifer, Hsu,

and Li, 2013; Jiang, Qian, and Yao, 2015).

To test this prediction, we define a dummy variable to capture the size effect

that equals one if a focal firm is above the sample median in a given month in terms

of the log value of market capitalization and zero otherwise. Similarly, we capture

the analyst coverage effect by defining a dummy variable that equals one if the

number of analysts following a focal firm at the end of the previous month is above

the sample median and zero otherwise; and we define a dummy variable to capture the

institutional ownership effect that equals one if the institutional holding at the end of

the previous fiscal-year end of a focal firm is above the sample median. The results

32

of the test are reported in column 3 to 5 of Table 5. The coefficient estimates on the

interaction term between the size dummy and TECHRETt-1 , between the analyst

coverage dummy and TECHRETt-1, and between the institutional ownership dummy

and TECHRETt-1 are all negative and statistically significant. This lends support to

our hypothesis that the return effect is driven by investors’ inattention of this

underlying information of technology-linkage.

6.3. Cost of arbitrage

We also expect to see a stronger return effect for stocks with more binding limits

to arbitrage, as investors are less able (or willing) to fully update these firms’ prices

(Hirshleifer, Teoh, and Yu, 2011; Beneish, Lee, and Nichols, 2015). Specifically, we

use two measures to proxy for the cost of arbitrage: idiosyncratic volatility (IdioVol)

and Bad News. We interpret firms with higher idiosyncratic volatility as having a

higher cost of arbitrage, since an arbitrageur’s demand for a stock is inversely related

to the stock’s arbitrage risk, which is essentially its idiosyncratic risk (Wurgler and

Zhuravskaya, 2002). Existing research also suggests that the slow diffusion of bad

news into price more could happen because investors are more reluctant to sell their

losers, or because short-selling is more costly to implement (Beneish, Lee, and

Nichols, 2015). Therefore, we expect the technology momentum that we

documented will be more pronounced for bad news.

To test this prediction, we define IdioVol as the standard deviation of the

residuals from a regression of daily stock returns in the previous month on the Fama

and French (1993) factors (at least ten daily returns required). Also, following Hong,

33

Lim, and Stein (2000), we define Bad News as an indicator variable that equals to one

if TECHRETt-1 falls in the worst-performing 30%, and zero otherwise.21 The results

of the test are reported in column 6 and 7 of Table 5. The coefficient estimates on

the interaction term between the idiosyncratic volatility dummy and TECHRETt-1 is

positive and statistically significant. Column 6 of Table 5 shows that the coefficient

estimate on the interaction term between an indicator of bad news and past

technology-linked return (TECHRETt-1) is also positive and statistically significant,

0.948 (t=2.10). For comparison, the unconditional coefficient on TECHRETt-1 from

Table 3 is 0.643. Both of these findings lend support to our prediction that

technology-linked momentum effect has an even larger impact on

difficult-to-arbitrage stocks.

7. Prediction of Fundamentals

The preceding sections document a robust return lead-lag effect along the

technological link, consistent with the argument of sluggish price adjustment. An

alternative to the mispricing explanation is that firms with similar technology are

exposed to similar risk factors, and that variations in these risk factors are driving the

lead-lag return pattern. To rule out this possibility, we further examine how shocks

to one firm affect other firms along the technology space in real quantities,

establishing the fundamental nature of the lead-lad pattern observed in returns. This

could reflect two scenarios. First, common shocks could originate due to input or

21 According to the untabulated results, min, mean, and max TECHRETt-1 for Bad News=1 is -0.05,

0.01, and 0.00, respectively.

34

output linkages or news about underlying technological change, and then propagate

along the technological link (Acemoglu et al., 2012). Second, firms may benefit

from the spillover effects of other firms’ innovation-related activities along the

technological link (Bloom, Schankerman, and Van Reenen, 2013).

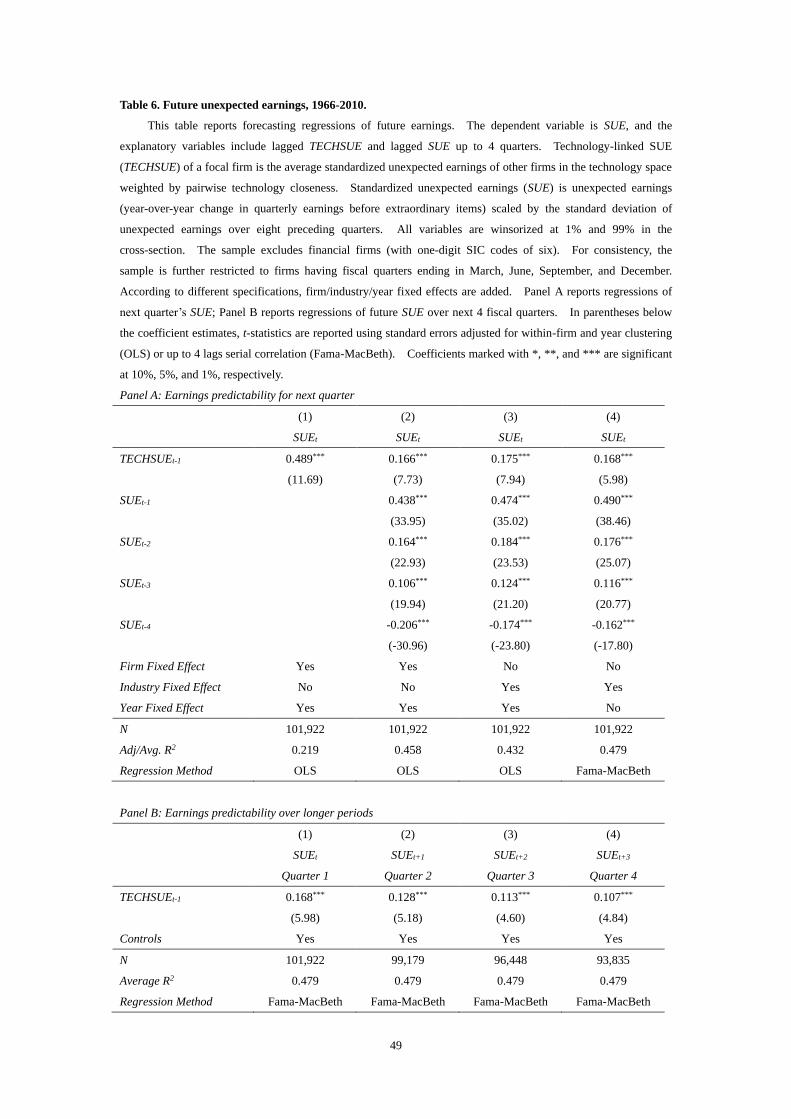

7.1. Unexpected earnings

We first examine firms’ future earnings predictability in multivariate regressions

and report results in Table 6. In particular, we test whether the performance of the

technology-linked firms predicts future performance of the focal firm. The

dependent variable is standardized unexpected earnings (SUE), and the explanatory

variables include one-quarter lagged technology-linked SUE (TECHSUE) and lagged

SUE up to 4 quarters. For consistency, the sample is further restricted to firms

having fiscal quarters ending in March, June, September, and December.

Panel A of Table 6 contains regression results under various specifications.

Column 1 presents specification using one-quarter lagged TECHSUE with firm and

time fixed effects, we find a significant positive association between SUE and

one-quarter lagged TECHSUE. We add lags of SUE as control variables in column

2-4 to reflect the serial correlation of SUE. Consistent with Bernard and Thomas

(1989), the first three lags of SUE are positively associated with future SUE, and the

coefficient of the fourth lag SUE is negative and significant. The predictive

coefficient of one-quarter lagged TECHSUE decreases to 0.168 in column 4 and is

still statistically and economically significant. The Newey-West adjusted t-statistics

is 5.98, and there is a difference of 0.10 ((0.69-0.09)*0.168) in future SUE between

35

the first and third quartile.

In Panel B of Table 6, we report cross-sectional regressions of future SUE over

next four quarters with control variables of up-to-four-lag serial correlations of lagged

SUE. The predictability of one-quarter lagged TECHSUE decreases monotonically

from 0.169 to 0.107 from column 1 to column 4, indicating that the TECHSUE may

be informative with decay for the focal firms over the next four quarters.

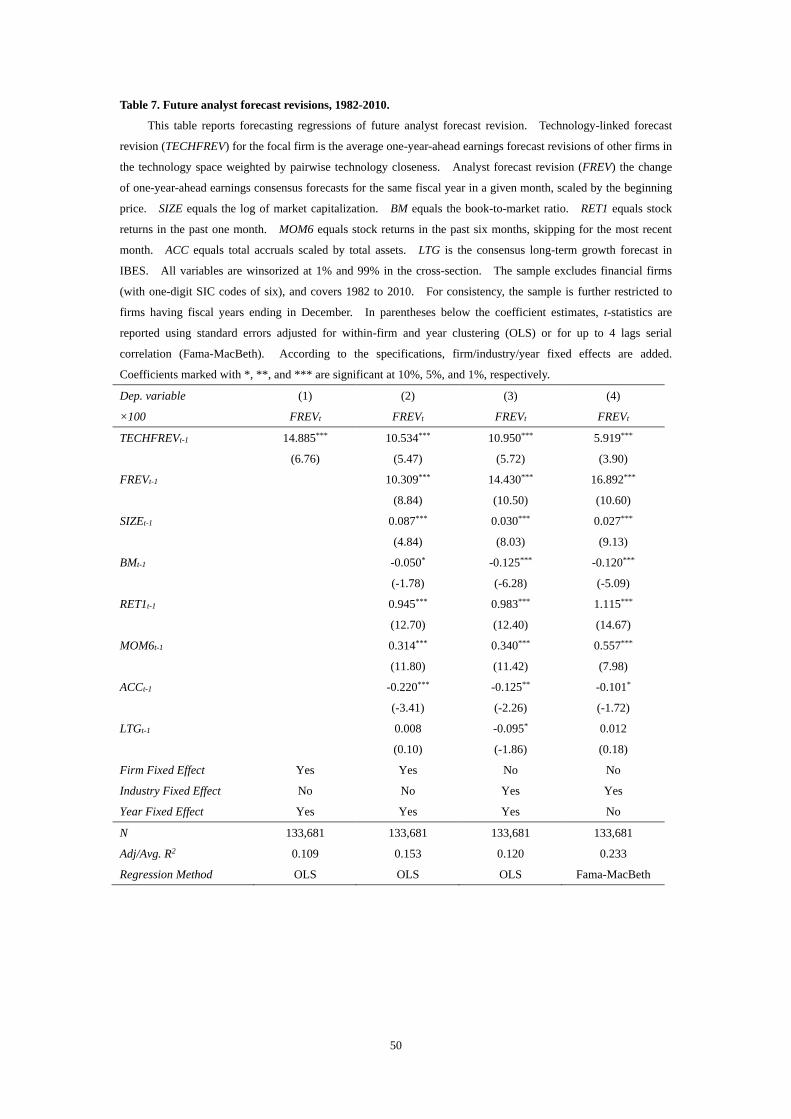

7.2. Analyst forecast revisions

Next, we examine the analyst behavior along the technological link. As analysts

play an important role in information diffusion and are less likely to be subject to the

behavioral biases or constraints as investors, if we find similar predictability patterns

in analyst forecast revisions, this will provide further support that the technology

momentum we documented is indeed driven by investors’ limited attention and

information processing capacity.

We report results from regressing analyst forecast revisions (FREV) on the main

explanatory variables in Table 7. TECHFREV is technology-linked firms’ analyst

forecast revision in month t-1, and control variables include lagged value of FREV,

size, book-to-market ratio, past performance, accruals, and long-term growth forecast,

following So (2013). For consistency, the sample is further restricted to firms

having fiscal years ending in December. In all of the four columns, the coefficients

of TECHFREV are positively related to future forecast revisions and are highly

significant. For example, in column 4, after controlling for a host of variables, the

coefficient of 5.919 (t=3.90) on TECHFREV implies a difference of around 0.03 in

36

future FREV between the first and third quartile. Given the difference in FREV

between the first and third quartile is around 0.12, the effect of TECHFREV is

economically large. This result indicates that similar to investors, analysts are also

less attentive to the fundamental performance of the technology-linked firms.

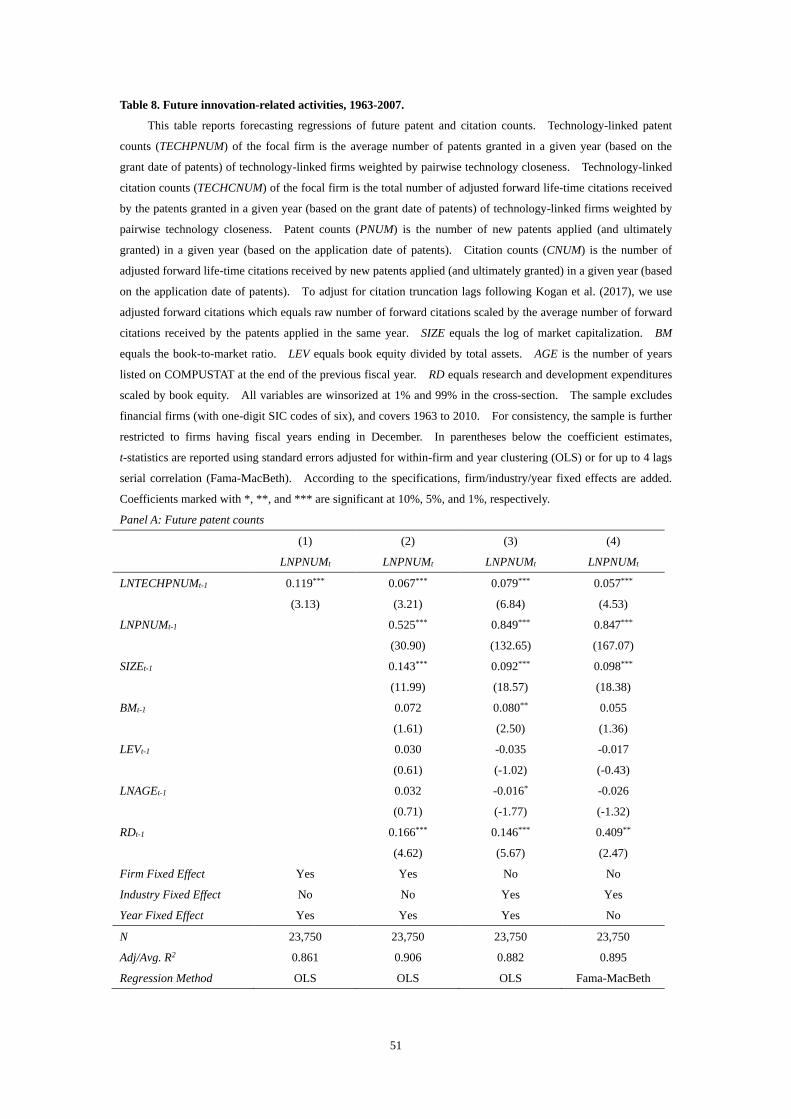

7.3. Innovation-related activities

In addition to the earnings-based results above, we also examine the predictability

of future innovation-related activities along the technological links. We consider

two important innovation-related activities: the patent and citation counts. First we

define patent counts (PNUM) as the number of new patents applied in a given year,

and citation counts (CNUM) as the number of adjusted forward life-time citations

received by new patents applied in a given year. After that, we calculate

technology-linked patent counts (TECHPNUM) and technology-linked citation counts

(TECHCNUM) in the same way as TECHRET. Finally, we take the log value of

innovation-related variables in the multivariate regressions.22 Control variables

include lagged log value of PNUM and CNUM, size, book-to-market ratio, leverage,

age, and R&D intensity. For consistency, the sample is further restricted to firms

having fiscal years ending in December.

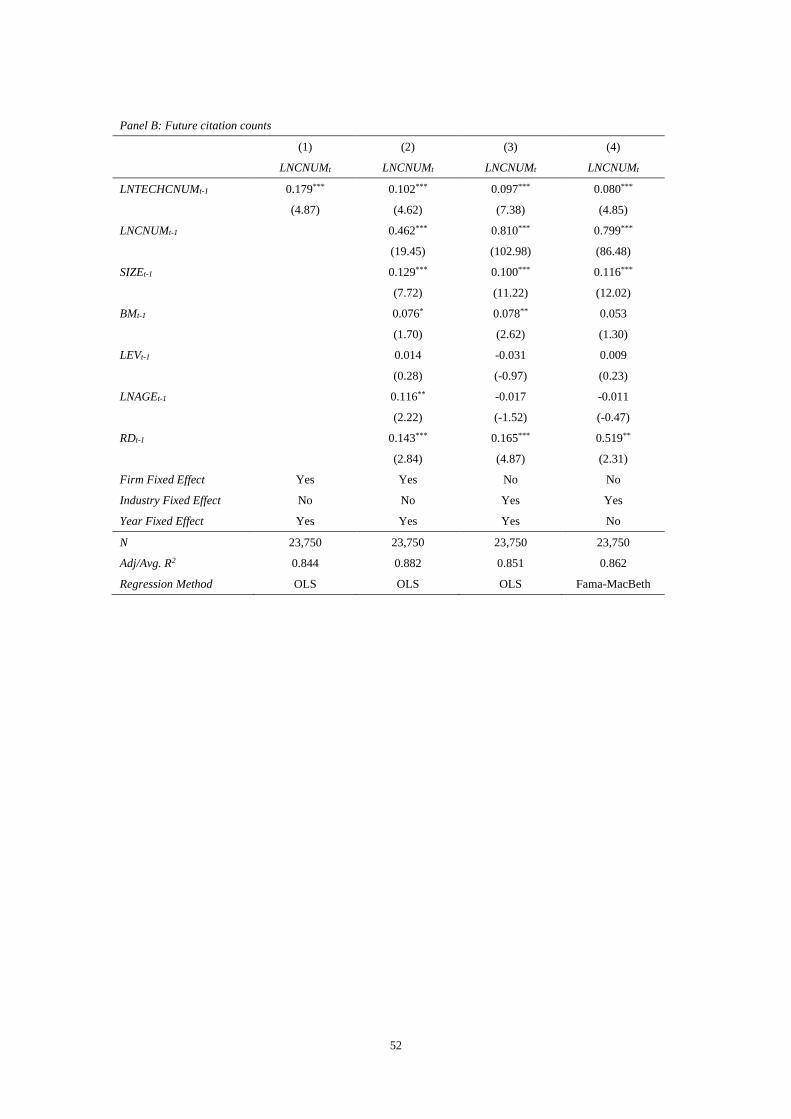

We report the regression results of future innovation-related activities in Table 8.

Panel A presents the results of future patent counts. The coefficient of

LNTECHPNUM is significantly positive, indicating that more patents granted for the 22 There are two types of truncation problems in patents data, one is the application-grant lags that

affects patent counts, the other is citation truncation lags that affects citation counts (Hall, Jaffe, and

Trajtenberg, 2001, 2005). To adjust for application-grant lags, we follow Hall, Jaffe, and Trajtenberg

(2001) to take 3-year lag and end our sample period in 2007. To adjust for citation truncation lags, we

follow Kogan et al. (2017) to scale the raw number of forward citations by the average number of

forward citations received by the patents applied in the same year (i.e., adjusted forward citations).

37

technology-linked firms in year t-1, the focal firms will have more applied (and

ultimately granted) patents in year t. For illustration, in column 4, the coefficient of

0.057 (t=4.53) on LNTECHPNUM implies that 1% increase in TECHPNUM in year

t-1 will predict 0.057% increase in PNUM for the focal firm in year t. Panel B

shows the results of future citation counts. Similarly, the significantly coefficient of

LNTECHCNUM indicates that the citation counts of technology-linked peers is a

significant predictor of citation counts of the focal firm. These results demonstrate

that technology-linked firms’ innovation-related activities are positively associated

with focal firm’s in terms of both quantity and quality. They are robust to various

settings (i.e., year, industry, or firm fixed effects), highlighting the technology

spillover effect along the technological links, consistent with Bloom, Schankerman,

and Van Reenen (2013).

To summarize, the above evidence strongly suggests that the return patterns we

documented earlier have their root in lead-lag patterns in firm fundamentals, and other

than investors, sell-side analysts are also subject to these same inattentions. These

results are largely consistent with the mispricing explanation of return predictability.

8. Conclusion

Our paper established that technology-linked firms’ stock returns predict focal

firms’ stock returns. This technology momentum effect that we documented is

robust to controlling for a variety of variables including size, book-to-market, gross

profitability, asset growth, R&D intensity, and short-term reversal and medium-term

38

price momentum. Furthermore, it cannot be explained by previously documented

industry momentum, customer momentum, or standalone-conglomerate momentum.

In a series of additional tests, we find a clear and robust return predictability in

every subperiod. We also show that even relying on lagged one- to three-year

technology closeness data, the technology momentum strategy still earns significant

returns, which demonstrates that technology closeness is particularly sticky.

Furthermore, the profitability of the short-term strategy is not sensitive to the length

of ranking period, ranges from 1 to 12 months. Specifically, we observe no sign of

any return reversal in the longer period, indicating that the return predictability of

technology momentum cannot be explained by stock overreaction.

We also conduct cross-sectional analysis and find the technology momentum is

stronger for more innovative firms. Further analysis shows that firms subject to

more investor inattention as well as firms with higher arbitrage costs are associated

with stronger predictability of the technology momentum effect. These findings

provide further support for psychological biases or constraints contributing to return

effect that we documented.

Finally, we show that technology-linked firms’ current shocks have significant

predictability over focal firm’s future real activities. Specifically, technology-linked

firms’ unexpected earnings, and innovation-related activities have strong predictable

power over focal firms’ corresponding measures. The evidence that the forecast

revisions of technology-linked firms predict their focal firms’ future revisions further

support the view that sell-side analysts are subject to these same constraints.

39

Our paper makes an important contribution to the asset pricing literature by

making a strong case that not only firms’ own innovation characteristics but also

shocks to technology-linked firms play an important role in the valuation of these

firms. Specifically, the significant return predictability along the technological link

supports the argument that efficient market is an on-going process, not a destination.

40

References

Acemoglu, D., Carvalho, V. M., Ozdaglar, A., & Tahbaz-Salehi, A. 2012. The network origins of aggregate

fluctuations. Econometrica, 80(5), 1977-2016.

Barber, B. M., & Odean, T. 2007. All that glitters: The effect of attention and news on the buying behavior of

individual and institutional investors. Review of Financial Studies, 21(2), 785-818.

Baker, M., & Wurgler, J. 2006. Investor sentiment and the cross-section of stock returns. The Journal of

Finance, 61(4), 1645-1680.

Bekkerman, R., & Khimich, N. 2017. Technological similarity and stock return cross-predictability: Evidence from

patent big data. Working paper.

Bena, J., & Kai, L. 2014. Corporate innovations and mergers and acquisitions. The Journal of Finance, 69(5),

1923–1960.

Beneish, M., Lee, C, & Nichols, D. 2015. In short supply: Short-sellers and stock returns. Journal of Accounting

and Economics, 60(2), 33-57.

Bernard, V. L., & Thomas, J. K. 1989. Post-earnings-announcement drift: Delayed price response or risk premium?.

Journal of Accounting Research, 27(27), 1-36.

Bloom, N., Schankerman, M., & Van Reenen, J. 2013. Identifying technology spillovers and product market rivalry.

Econometrica, 81(4), 1347-1393.

Carhart, M. M. 1997. On persistence in mutual fund performance. The Journal of Finance, 52(1), 57-82.

Cao, J., Chordia, T., & Lin, C. 2016. Alliances and return predictability. Journal of Financial and Quantitative

Analysis, 51(5), 1689-1717.

Chan, L. K., Jegadeesh, N., & Lakonishok, J. 1996. Momentum strategies. The Journal of Finance, 51(5),

1681-1713.

Chan, L. K., Lakonishok, J., & Sougiannis, T. 2001. The stock market valuation of research and development

expenditures. The Journal of Finance, 56(6), 2431-2456.

Cohen, L., & Frazzini, A. 2008. Economic links and predictable returns. The Journal of Finance, 63(4),

1977-2011.

Cohen, L., & Lou, D. 2012. Complicated firms. Journal of Financial Economics, 104(2), 383-400.

Cohen, L., Diether, K., & Malloy, C. 2013. Misvaluing innovation. Review of Financial Studies, 26(3), 635-666.

Cooper, M. J., Gulen, H., & Schill, M. J. 2008. Asset growth and the cross-section of stock returns. The Journal of

Finance, 63(4), 1609-1651.

Daniel, K., Grinblatt, M., Titman, S., & Wermers, R. 1997. Measuring mutual fund performance with

characteristic-based benchmarks. The Journal of Finance, 52(3), 1035-1058.

Daniel, K., Hirshleifer, D. A., & Subrahmanyam, A. 1998. Investor psychology and security under-and

overreactions. The Journal of Finance, 53(6), 1839-1885.

DellaVigna, S., & Pollet, J. M. 2009. Investor inattention and Friday earnings announcements. The Journal of

Finance, 64(2), 709-749.

Eberhart, A. C., Maxwell, W. F., & Siddique, A. R. 2004. An examination of long-term abnormal stock returns and

operating performance following R&D increases. The Journal of Finance, 59(2), 623-650.

Fama, E. F., & MacBeth, J. D. 1973. Risk, return, and equilibrium: Empirical tests. Journal of Political