tcioceania15 advanced manufacturing - opportunities and risks

TRANSCRIPT

Advanced Manufacturing - Opportunities and Risks David Walters 17 April 2015

Advanced Manufacturing - Opportunities and Risks for Specialist Organisations

David Walters Jeffrey Newton

Value Chain Network

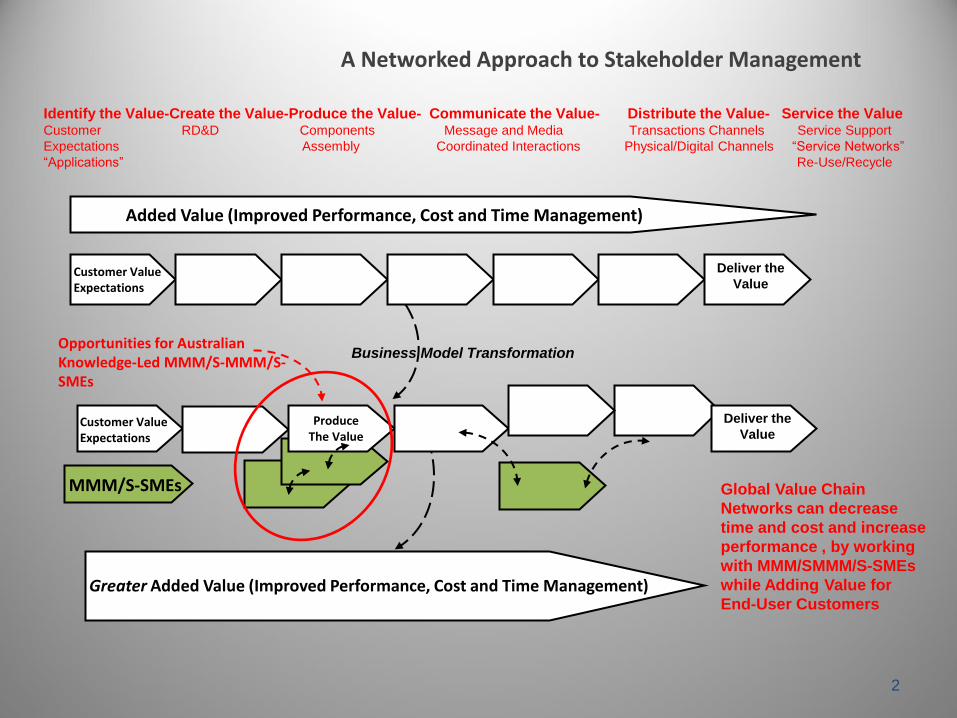

Identify the Value-Create the Value-Produce the Value- Communicate the Value- Distribute the Value- Service the Value Customer RD&D Components Message and Media Transactions Channels Service Support

Expectations Assembly Coordinated Interactions Physical/Digital Channels “Service Networks”

“Applications” Re-Use/Recycle

Deliver the

Value

Deliver the

Value

Global Value Chain

Networks can decrease

time and cost and increase

performance , by working

with MMM/SMMM/S-SMEs

while Adding Value for

End-User Customers

2

Added Value (Improved Performance, Cost and Time Management)

Greater Added Value (Improved Performance, Cost and Time Management)

Business Model Transformation

MMM/S-SMEs

Customer Value Expectations

Customer Value Expectations

A Networked Approach to Stakeholder Management

Produce The Value

Opportunities for Australian Knowledge-Led MMM/S-MMM/S-SMEs

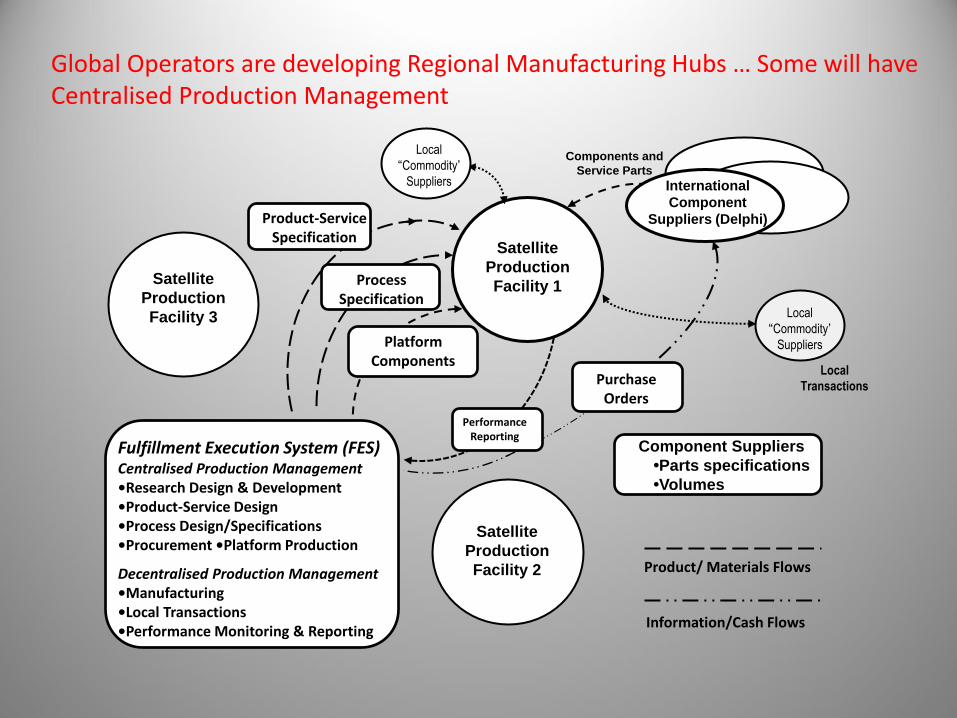

Innovation in Advanced Manufacturing Technology …. …. Automated factories, Machine-to-Machine Internet 3D printing and the ‘Connected’ Home.

Barkai and Manenti (2011) argued that current market trends, together with the digitisation of manufacturing, require the future production environment to be highly adaptable and reconfigurable to respond to rapid changes in market demand, technology innovation and changing regulations.

“Factories of the future will be a global network of production facilities managed as single virtual factory. This type of manufacturing network consolidates multiple resources and capabilities to form an end-to-end fulfillment network that we call fulfillment execution system (FES).”

Satellite

Production

Facility 1

Components and

Service Parts

International

Component

Suppliers (Delphi)

Satellite

Production

Facility 3

Satellite

Production

Facility 2

Local

“Commodity’

Suppliers

Local

Transactions

Local

“Commodity’

Suppliers

Product-Service Specification

Process Specification

Platform Components

Component Suppliers

•Parts specifications

•Volumes

Purchase Orders

Fulfillment Execution System (FES) Centralised Production Management •Research Design & Development •Product-Service Design •Process Design/Specifications •Procurement •Platform Production

Decentralised Production Management •Manufacturing •Local Transactions •Performance Monitoring & Reporting

Performance Reporting

Global Operators are developing Regional Manufacturing Hubs … Some will have Centralised Production Management

Product/ Materials Flows

Information/Cash Flows

GE Pioneering Advanced Manufacturing Technology

In February 2015 General Electric invested over $200 million in a new “flexible factory” that will produce diverse products, from jet engine parts to locomotive components, for four different GE businesses all ‘under one roof’ for the first time.

The ‘Brilliant Factory’ is one of GE's most advanced facilities bringing together automation, the Industrial Internet and 3D printing. It is built on the concept of flexibility, allowing for the manufacturing of a diverse set of products and catering to GE’s broad range of businesses, including aviation, oil & gas and rail. It will also serve both domestic and export markets, working on the principle of a ‘Shared Centre of Excellence’ on process, capability and human capital aimed at driving economies of scale.

The idea to build the first iteration of such a plant in India made sense to GE, because the company wanted to harmonise its operations there, gain size and scale quickly, and support its suppliers.

Industrie 4.0 (Siemens)

The Australian Financial Review visited the German company’s flagship Industrie 4.0 facility in Arnberg, and was told that now was a “watershed moment” for manufacturers. The reason staying up-to-date with Industrie 4.0 was the need for Australian companies to play a role in the supply chains (global value chains) of multinational companies, who have applied connectivity to processes to all stages of their products’ lifecycles and expect the same from their suppliers.

According to Siemens’ head of factory automation, Ralf-Michael Franke, this could cost as much as 2 – 3 per cent of revenue. Siemens is one of the leading companies among those in Germany’s Industrie 4.0, which its government initiated in 2011. An Australian journalist described the movement as a “headlong rush to combine three things: automated factories, machine-to-machine internet and 3D printing”. AFR/Manufacturers’ Monthly April 2015

Robotics Another influence on the industry’s “reinvention” would be increasingly affordable general-purpose robotics, the small and flexible Baxter machine is an example. Such robots would be within the reach of smaller businesses, and would see the more basic parts of manufacturing be handed over to automated processes. “By 2016, manufacturing jobs will start to shift around more intricate work, including the training and maintaining of robots, as well as working on optimising manufacturing processes,” said Bieber (Citrix).

The trend towards automation is an employment concern for some in the industry, especially on the production line. Sales for factory robots are at their highest, and in 2013 more than half of those sold worldwide were installed in this region.

Manufactures’ Monthly, April 2015

Platform Technology

Volkswagen has had a reputation for producing over-engineered products. It is reportedly trying to reduce product complexity through what it calls a modular toolkit programme, or Modularer Querbaukasten (MQB,) used in the new Audi A3 and now the VW Golf model launched in April 2013. As well as reducing product complexity the aim is to cut unit manufacturing costs by 20 per cent. This involves hefty upfront costs – one reason investment in the automotive division is projected to be €60bn between 2012 and 2016.

“When fully deployed across its factories in the US, Europe and China, Volkswagen will be able to manufacture any vehicle that local customers want close to where they live, and to do so faster, better and more cost-effectively”. Radjou and Prabhu: 2015.

Continuous Manufacturing

MIT together with Novartis is pioneering a continuous manufacturing process in the pharmaceutical industry. It is producing a copy of a standard Novartis drug, for future use; the system is still five to ten years away from commercial operation.

The number of discrete operations involved in producing the drug has been cut from 22 to 13; the processing time has been decreased from 300 hours to 40; every pill being made is monitored to ensure it meets the required specification.

Continuous manufacturing could transform the pharmaceuticals industry by replacing large, purpose-built plants supplying the global market, with smaller, regionalised plants, that could respond more rapidly to local demand, especially if a pandemic were to occur. The pilot line can fit into a shipping container, facilitating rapid deployment anywhere.

The Circular Economy/Value Chain Network

Another pressing reason for considering a coordinated approach is the interest in environmental sustainability. The circular economy/value chain network (Nguyen et al: 2014) aims to eradicate waste, not just from manufacturing processes, as lean management aspires to do, but systematically, throughout the life cycles and uses of products and their components.

Indeed, tight component and product cycles of use and reuse, aided by product design, help define the concept of a circular economy and distinguish it from the linear take–make–dispose economy, which wastes large amounts of embedded materials, energy, and labour.

Given the additional focus of the circular economy/value chain two considerations immediately come to mind; one, a far more comprehensive perspective of the network relationships is required as the life span of the processes are extended, and two, the issue of resource management sustainability assumes significance.

Reverse Innovation - Market Centricity

GE introduced reverse innovation because it found that the traditional approach of developing sophisticated products in domestic markets and simplifying them for emerging markets was not effective primarily because of declining growth rates in developed markets and innovative competitors in the emerging markets.

•GE introduced a business model based upon four fundamental principles:

•Local Growth Teams (LGTs) were established in India and China.

•The LGT management model was created featuring; delegated product-service strategy shifting decision making to sourcing/consumption markets

•LGT structures can respond to local circumstances in planning processes; opportunities and constraints, and reflect local market, finance and operations realities, and whose objectives and strategies become ‘customised’ to meet local (realistic) possibilities and constraints.

•By localising the entire RD&D-manufacturing-marketing activities, products that were very expensive when produced for domestic markets, were made accessible to health care practitioners in the emerging markets.

Data Collection, Analysis and Management Increases Operating Efficiency

GE is transforming its operations with big data and other advanced technologies. The company has introduced the term "Brilliant Factory" to represent how it is generating and analysing data to optimize operations at its 400 factories around the world.

Research by Boston Consulting Group identifies five technology tools that have the "greatest potential to influence the manufacturing landscape" and improve productivity. They are; autonomous robots, integrated computational materials engineering, digital manufacturing, the industrial Internet and flexible automation, and additive manufacturing.

GE's use of big data is changing how it serves its customers as well as its manufacturing operations. At its Monitoring & Diagnostics Center in Atlanta, a team of more than 50 engineers analyses the data that flows in every hour of every day from gas turbines and generators in 58 countries. What they are finding saved the company's customers $70 million last year.

Using this data, GE can provide predictive maintenance services for its customers so that they can keep equipment running longer and more safely. Since 2009, GE has been able to reduce the trip rates -- the rate per 1,000 hours of unforced outages in which turbines stop generating power -- by 25% for its 7F and 9F turbines.

"As we get better at doing predictive maintenance, we are able to extend the life of individual components and also extend the maintenance intervals on the unit," This data also contribute to product development efforts. GE's design teams use the data both to improve existing products and to design new models.

The changes in GE's business are not happening overnight and BCG cautions that it will take time for these new technologies to take hold in manufacturing widely, but it forecasts that a combination of these tools could reduce production costs by 20% to 40% and "radically redefine the dynamics of global competition in many industries.“ IW reporting on BCG Research 100415

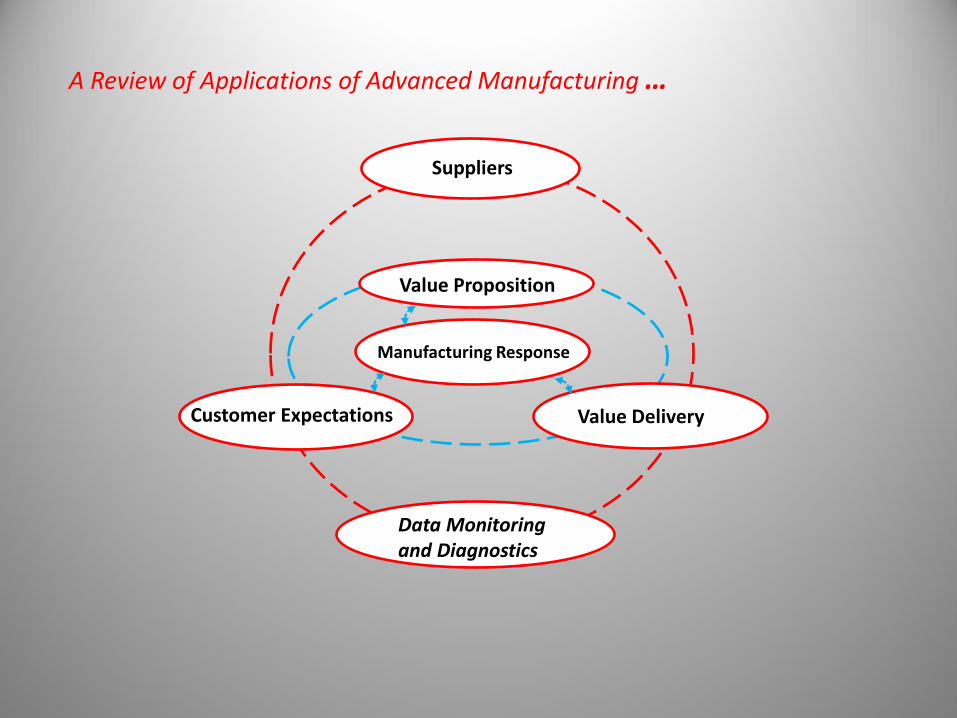

A Review of Applications of Advanced Manufacturing …

Customer Expectations

Value Proposition

Value Delivery

Manufacturing Response

Suppliers

Data Monitoring and Diagnostics

16

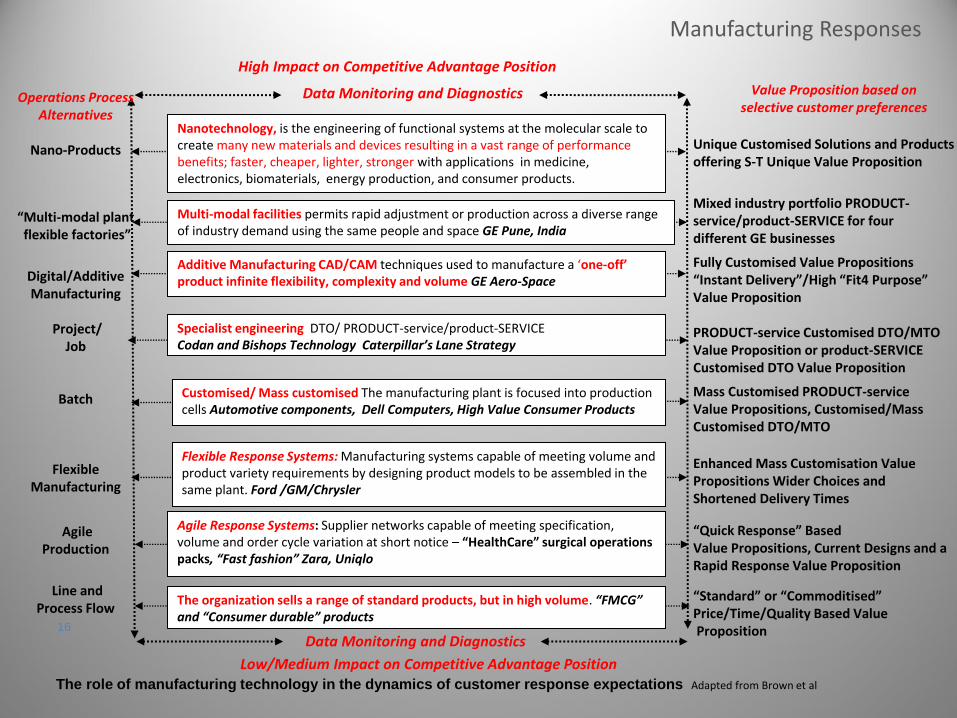

Specialist engineering DTO/ PRODUCT-service/product-SERVICE Codan and Bishops Technology Caterpillar’s Lane Strategy

Customised/ Mass customised The manufacturing plant is focused into production cells Automotive components, Dell Computers, High Value Consumer Products

Flexible Response Systems: Manufacturing systems capable of meeting volume and product variety requirements by designing product models to be assembled in the same plant. Ford /GM/Chrysler

Agile Response Systems: Supplier networks capable of meeting specification, volume and order cycle variation at short notice – “HealthCare” surgical operations packs, “Fast fashion” Zara, Uniqlo

The organization sells a range of standard products, but in high volume. “FMCG” and “Consumer durable” products

Low/Medium Impact on Competitive Advantage Position The role of manufacturing technology in the dynamics of customer response expectations Adapted from Brown et al

Operations Process Alternatives

Nano-Products

“Multi-modal plant flexible factories”

Digital/Additive Manufacturing

Project/

Job

Batch

Flexible Manufacturing

Agile Production

Line and

Process Flow

Additive Manufacturing CAD/CAM techniques used to manufacture a ‘one-off’ product infinite flexibility, complexity and volume GE Aero-Space

High Impact on Competitive Advantage Position

Value Proposition based on selective customer preferences

Unique Customised Solutions and Products offering S-T Unique Value Proposition

Mixed industry portfolio PRODUCT-service/product-SERVICE for four different GE businesses

Fully Customised Value Propositions “Instant Delivery”/High “Fit4 Purpose” Value Proposition

PRODUCT-service Customised DTO/MTO Value Proposition or product-SERVICE Customised DTO Value Proposition

Mass Customised PRODUCT-service Value Propositions, Customised/Mass Customised DTO/MTO

Enhanced Mass Customisation Value Propositions Wider Choices and Shortened Delivery Times

“Quick Response” Based Value Propositions, Current Designs and a Rapid Response Value Proposition

“Standard” or “Commoditised” Price/Time/Quality Based Value Proposition

Manufacturing Responses

Nanotechnology, is the engineering of functional systems at the molecular scale to create many new materials and devices resulting in a vast range of performance benefits; faster, cheaper, lighter, stronger with applications in medicine, electronics, biomaterials, energy production, and consumer products.

Multi-modal facilities permits rapid adjustment or production across a diverse range of industry demand using the same people and space GE Pune, India

Data Monitoring and Diagnostics

Data Monitoring and Diagnostics

Specialist- MMM/S-SMEs in the Global Value Chain

The favoured emerging model is based upon the successful German Mittelstand ….

18

19

The Mittelstand is an unconventional MMM/S-SME with its origin in Germany; it is essentially a family business with a tradition of stakeholder commitment. Its stakeholder focus believes that a primary concern for customers and concern for employee, partners, and the community are essential in generating profitable operations. Mittelstand organisations make a major contribution to Germany’s GDP and value added to the German economy.

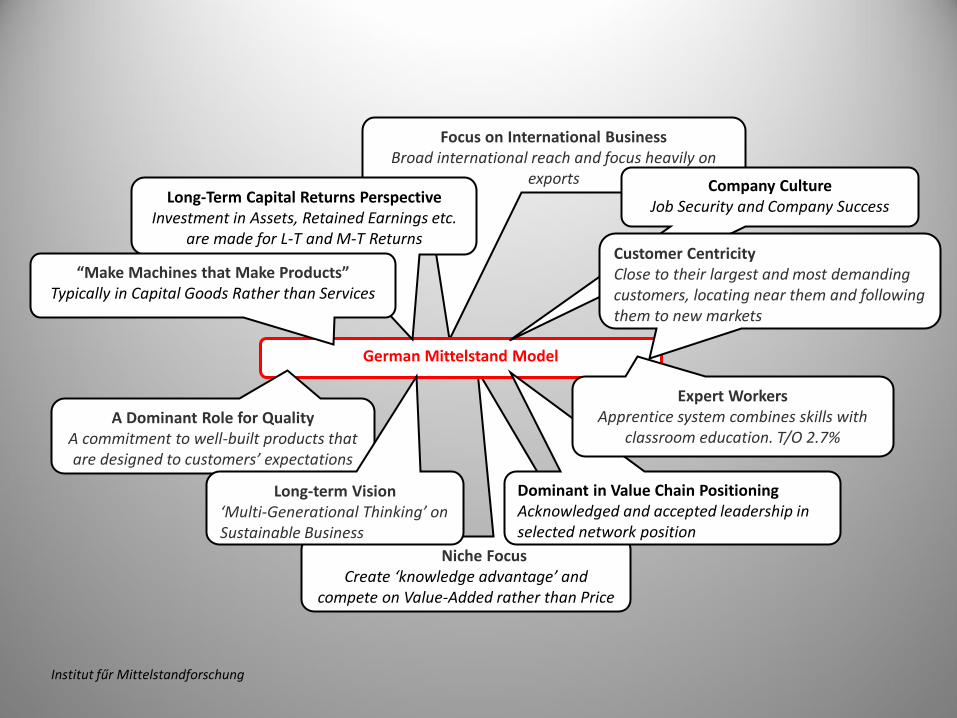

Focus on International Business Broad international reach and focus heavily on

exports

Niche Focus Create ‘knowledge advantage’ and

compete on Value-Added rather than Price

German Mittelstand Model

Long-Term Capital Returns Perspective Investment in Assets, Retained Earnings etc.

are made for L-T and M-T Returns

“Make Machines that Make Products” Typically in Capital Goods Rather than Services

A Dominant Role for Quality A commitment to well-built products that are designed to customers’ expectations

Long-term Vision ‘Multi-Generational Thinking’ on Sustainable Business

Dominant in Value Chain Positioning Acknowledged and accepted leadership in selected network position

Expert Workers Apprentice system combines skills with

classroom education. T/O 2.7%

Company Culture Job Security and Company Success

Customer Centricity Close to their largest and most demanding customers, locating near them and following them to new markets

Institut fűr Mittelstandforschung 20

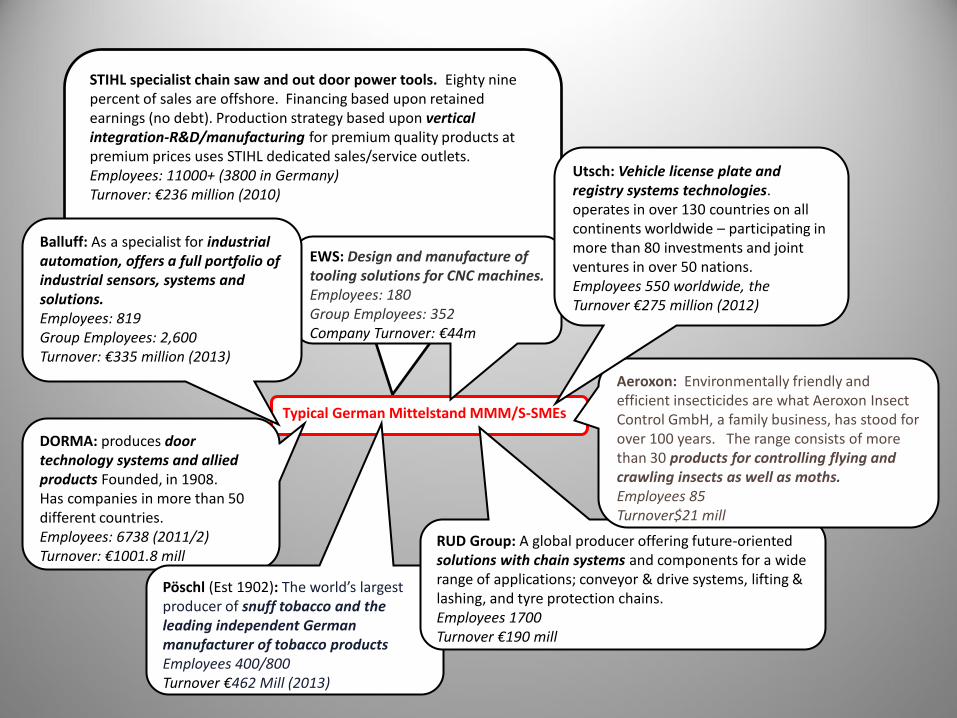

Typical German Mittelstand MMM/S-SMEs

EWS: Design and manufacture of tooling solutions for CNC machines. Employees: 180 Group Employees: 352 Company Turnover: €44m

Balluff: As a specialist for industrial automation, offers a full portfolio of industrial sensors, systems and solutions. Employees: 819 Group Employees: 2,600 Turnover: €335 million (2013)

DORMA: produces door technology systems and allied products Founded, in 1908. Has companies in more than 50 different countries. Employees: 6738 (2011/2) Turnover: €1001.8 mill

Pöschl (Est 1902): The world’s largest producer of snuff tobacco and the leading independent German manufacturer of tobacco products Employees 400/800 Turnover €462 Mill (2013)

RUD Group: A global producer offering future-oriented solutions with chain systems and components for a wide range of applications; conveyor & drive systems, lifting & lashing, and tyre protection chains. Employees 1700 Turnover €190 mill

Aeroxon: Environmentally friendly and efficient insecticides are what Aeroxon Insect Control GmbH, a family business, has stood for over 100 years. The range consists of more than 30 products for controlling flying and crawling insects as well as moths. Employees 85 Turnover$21 mill

Utsch: Vehicle license plate and registry systems technologies. operates in over 130 countries on all continents worldwide – participating in more than 80 investments and joint ventures in over 50 nations. Employees 550 worldwide, the Turnover €275 million (2012)

STIHL specialist chain saw and out door power tools. Eighty nine percent of sales are offshore. Financing based upon retained earnings (no debt). Production strategy based upon vertical integration-R&D/manufacturing for premium quality products at premium prices uses STIHL dedicated sales/service outlets. Employees: 11000+ (3800 in Germany) Turnover: €236 million (2010)

21

Successful Australian MMM/S-SMEs

Successful Australian MMM/S-SMEs

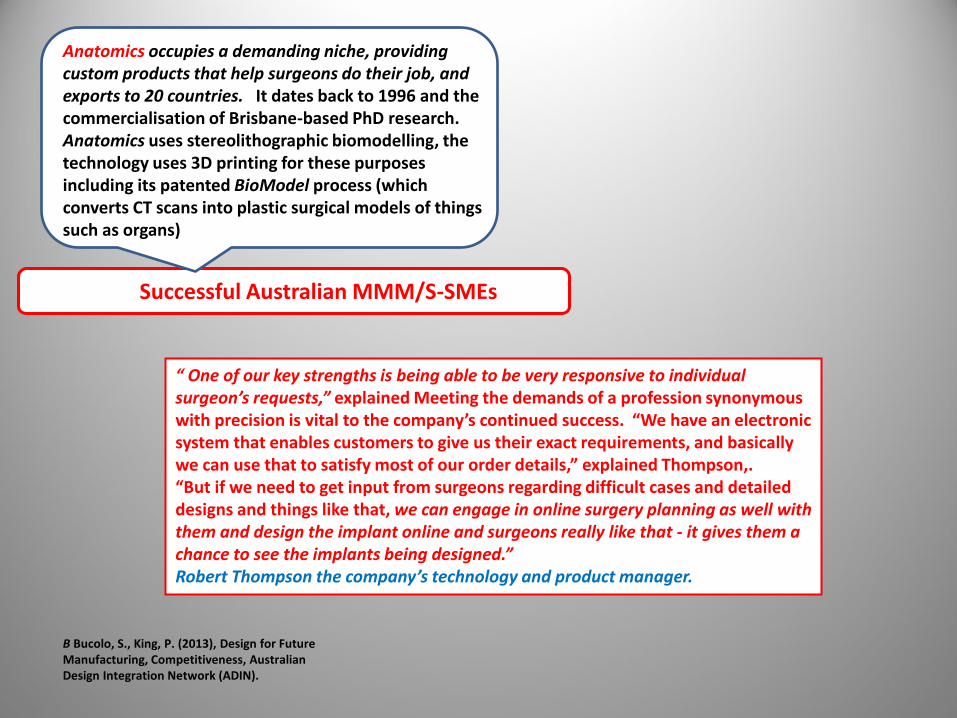

Anatomics occupies a demanding niche, providing custom products that help surgeons do their job, and exports to 20 countries. It dates back to 1996 and the commercialisation of Brisbane-based PhD research. Anatomics uses stereolithographic biomodelling, the technology uses 3D printing for these purposes including its patented BioModel process (which converts CT scans into plastic surgical models of things such as organs)

“ One of our key strengths is being able to be very responsive to individual surgeon’s requests,” explained Meeting the demands of a profession synonymous with precision is vital to the company’s continued success. “We have an electronic system that enables customers to give us their exact requirements, and basically we can use that to satisfy most of our order details,” explained Thompson,. “But if we need to get input from surgeons regarding difficult cases and detailed designs and things like that, we can engage in online surgery planning as well with them and design the implant online and surgeons really like that - it gives them a chance to see the implants being designed.” Robert Thompson the company’s technology and product manager.

B Bucolo, S., King, P. (2013), Design for Future Manufacturing, Competitiveness, Australian Design Integration Network (ADIN).

23

24

B Bucolo, S., King, P. (2013), Design for Future Manufacturing, Competitiveness, Australian Design Integration Network (ADIN). And www.codan.com.au

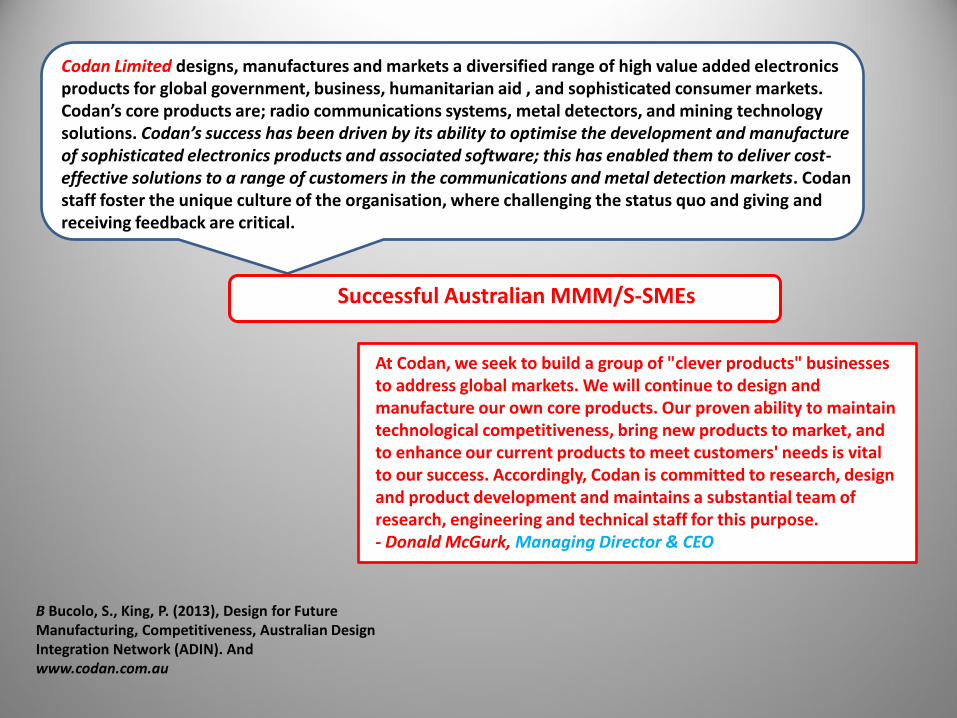

Codan Limited designs, manufactures and markets a diversified range of high value added electronics products for global government, business, humanitarian aid , and sophisticated consumer markets. Codan’s core products are; radio communications systems, metal detectors, and mining technology solutions. Codan’s success has been driven by its ability to optimise the development and manufacture of sophisticated electronics products and associated software; this has enabled them to deliver cost-effective solutions to a range of customers in the communications and metal detection markets. Codan staff foster the unique culture of the organisation, where challenging the status quo and giving and receiving feedback are critical.

At Codan, we seek to build a group of "clever products" businesses to address global markets. We will continue to design and manufacture our own core products. Our proven ability to maintain technological competitiveness, bring new products to market, and to enhance our current products to meet customers' needs is vital to our success. Accordingly, Codan is committed to research, design and product development and maintains a substantial team of research, engineering and technical staff for this purpose. - Donald McGurk, Managing Director & CEO

Successful Australian MMM/S-SMEs

25

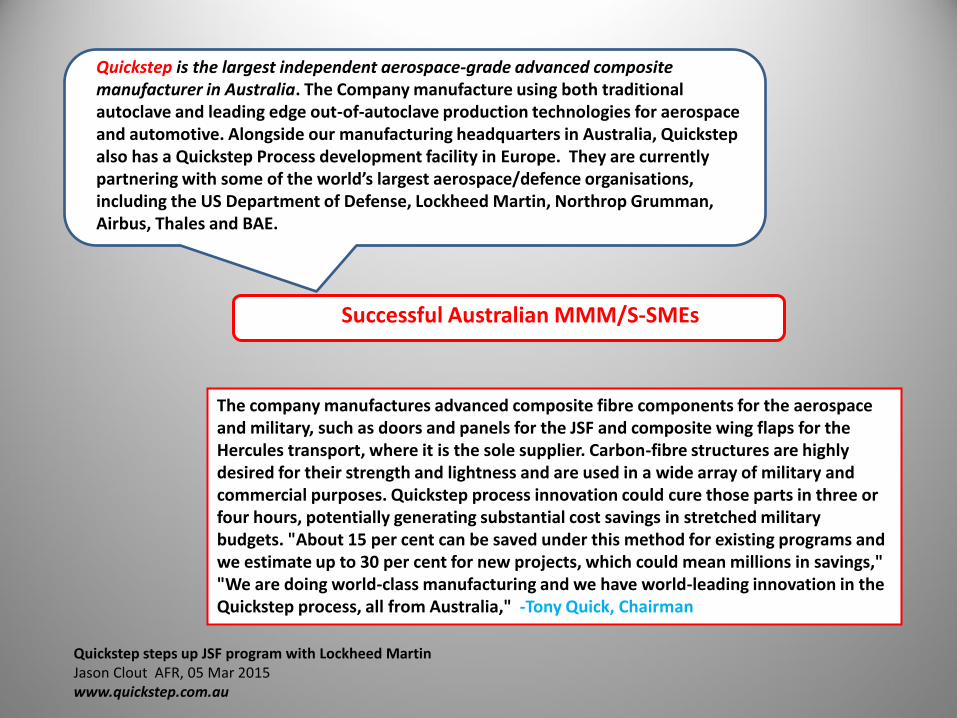

The company manufactures advanced composite fibre components for the aerospace and military, such as doors and panels for the JSF and composite wing flaps for the Hercules transport, where it is the sole supplier. Carbon-fibre structures are highly desired for their strength and lightness and are used in a wide array of military and commercial purposes. Quickstep process innovation could cure those parts in three or four hours, potentially generating substantial cost savings in stretched military budgets. "About 15 per cent can be saved under this method for existing programs and we estimate up to 30 per cent for new projects, which could mean millions in savings," "We are doing world-class manufacturing and we have world-leading innovation in the Quickstep process, all from Australia," -Tony Quick, Chairman

Quickstep is the largest independent aerospace-grade advanced composite manufacturer in Australia. The Company manufacture using both traditional autoclave and leading edge out-of-autoclave production technologies for aerospace and automotive. Alongside our manufacturing headquarters in Australia, Quickstep also has a Quickstep Process development facility in Europe. They are currently partnering with some of the world’s largest aerospace/defence organisations, including the US Department of Defense, Lockheed Martin, Northrop Grumman, Airbus, Thales and BAE.

Successful Australian MMM/S-SMEs

Quickstep steps up JSF program with Lockheed Martin Jason Clout AFR, 05 Mar 2015 www.quickstep.com.au

Considerations for Success for the Small Specialist Organisation in the GVCN …

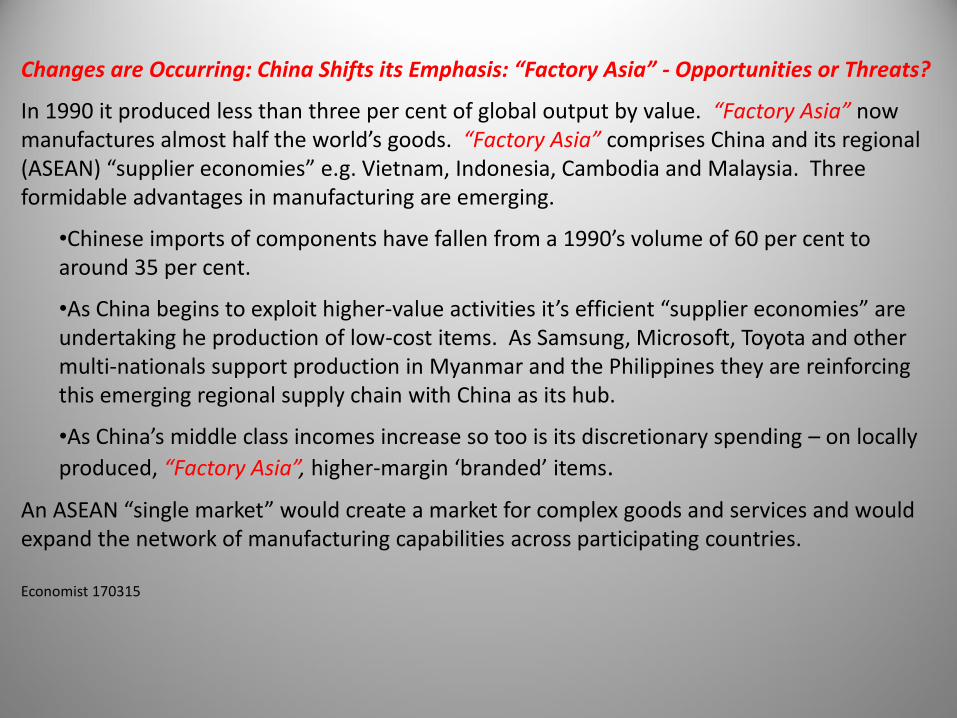

Changes are Occurring: China Shifts its Emphasis: “Factory Asia” - Opportunities or Threats?

In 1990 it produced less than three per cent of global output by value. “Factory Asia” now manufactures almost half the world’s goods. “Factory Asia” comprises China and its regional (ASEAN) “supplier economies” e.g. Vietnam, Indonesia, Cambodia and Malaysia. Three formidable advantages in manufacturing are emerging.

•Chinese imports of components have fallen from a 1990’s volume of 60 per cent to around 35 per cent.

•As China begins to exploit higher-value activities it’s efficient “supplier economies” are undertaking he production of low-cost items. As Samsung, Microsoft, Toyota and other multi-nationals support production in Myanmar and the Philippines they are reinforcing this emerging regional supply chain with China as its hub.

•As China’s middle class incomes increase so too is its discretionary spending – on locally

produced, “Factory Asia”, higher-margin ‘branded’ items.

An ASEAN “single market” would create a market for complex goods and services and would expand the network of manufacturing capabilities across participating countries. Economist 170315

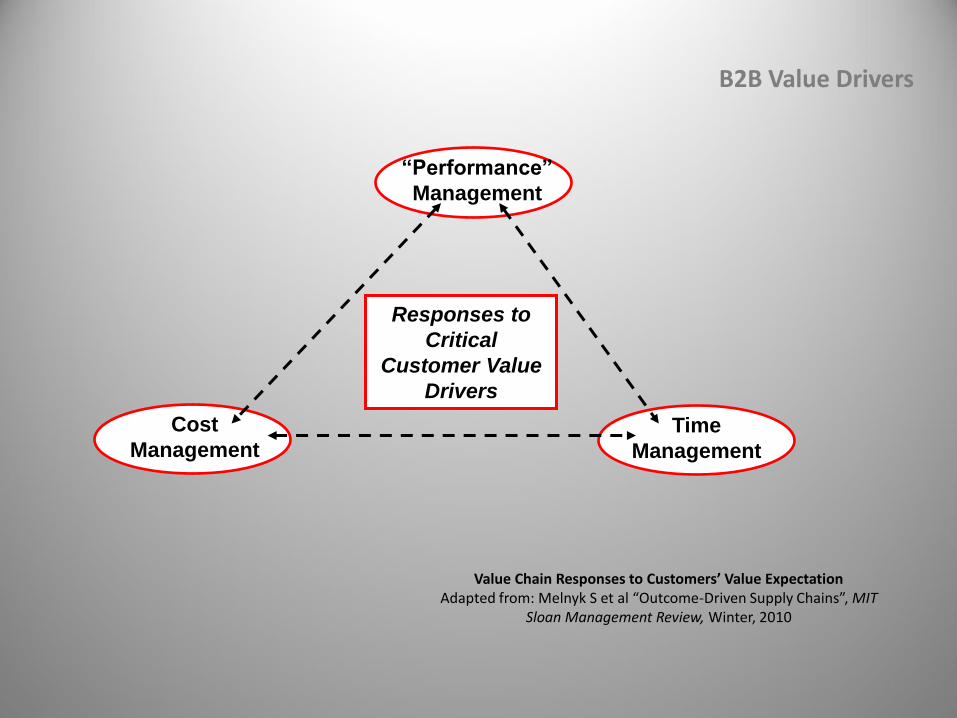

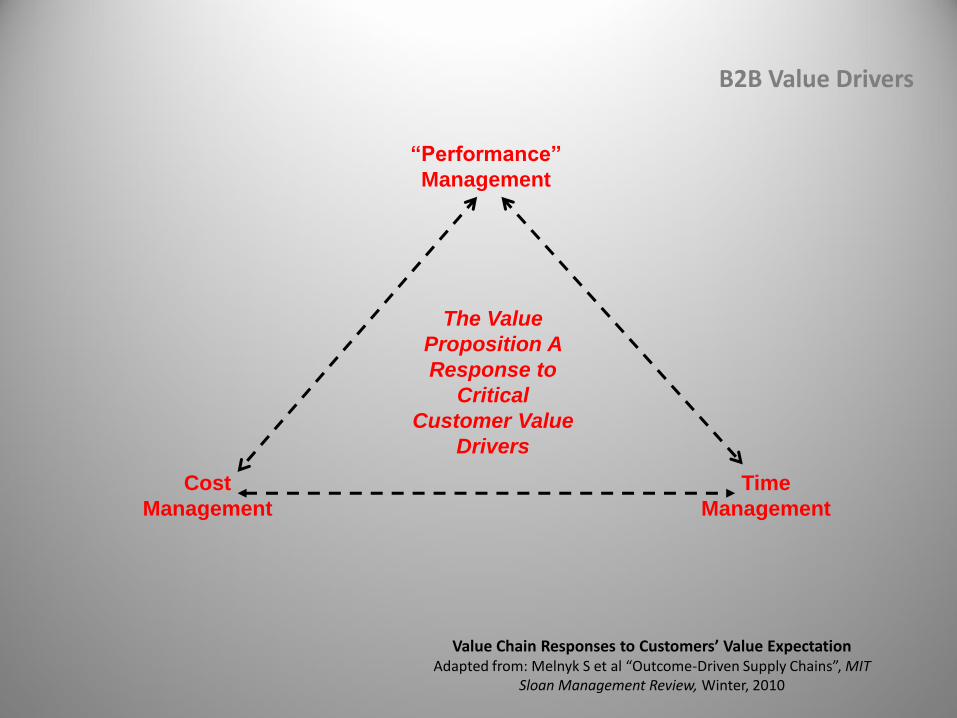

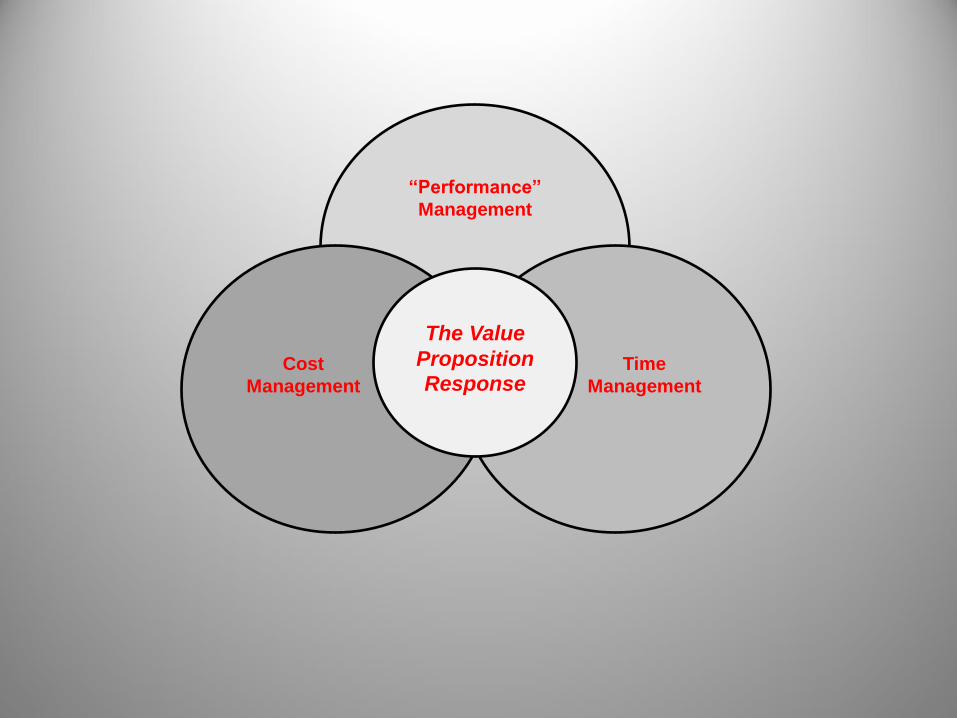

Value Chain Responses to Customers’ Value Expectation Adapted from: Melnyk S et al “Outcome-Driven Supply Chains”, MIT

Sloan Management Review, Winter, 2010

B2B Value Drivers

28

“Performance”

Management

Time

Management

Cost

Management

Responses to

Critical

Customer Value

Drivers

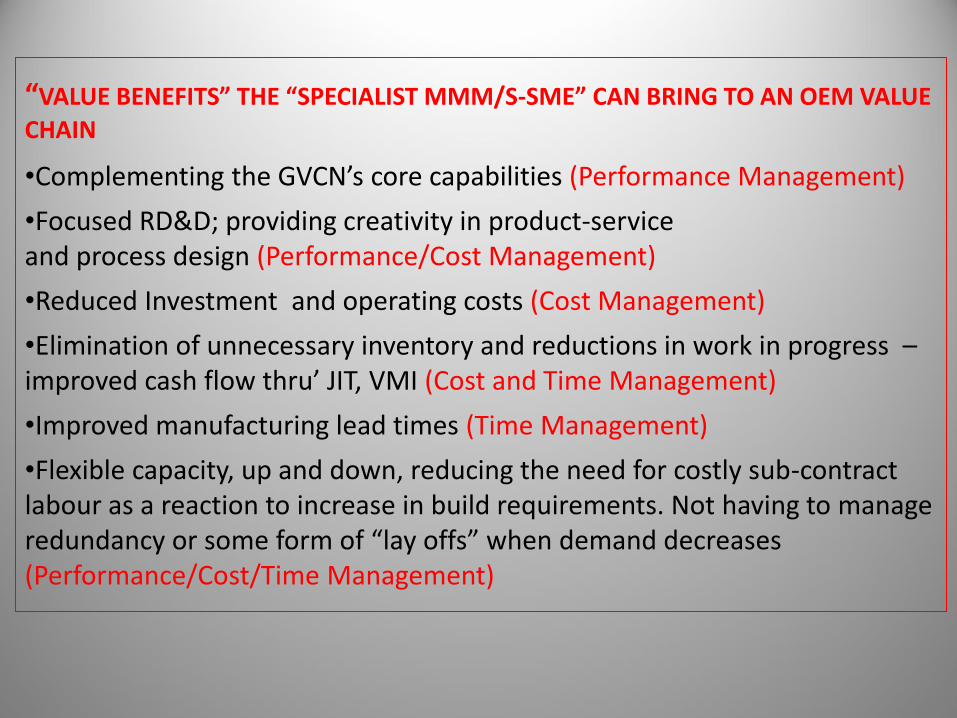

“VALUE BENEFITS” THE “SPECIALIST MMM/S-SME” CAN BRING TO AN OEM VALUE

CHAIN

•Complementing the GVCN’s core capabilities (Performance Management)

•Focused RD&D; providing creativity in product-service and process design (Performance/Cost Management)

•Reduced Investment and operating costs (Cost Management)

•Elimination of unnecessary inventory and reductions in work in progress – improved cash flow thru’ JIT, VMI (Cost and Time Management)

•Improved manufacturing lead times (Time Management)

•Flexible capacity, up and down, reducing the need for costly sub-contract labour as a reaction to increase in build requirements. Not having to manage redundancy or some form of “lay offs” when demand decreases (Performance/Cost/Time Management)

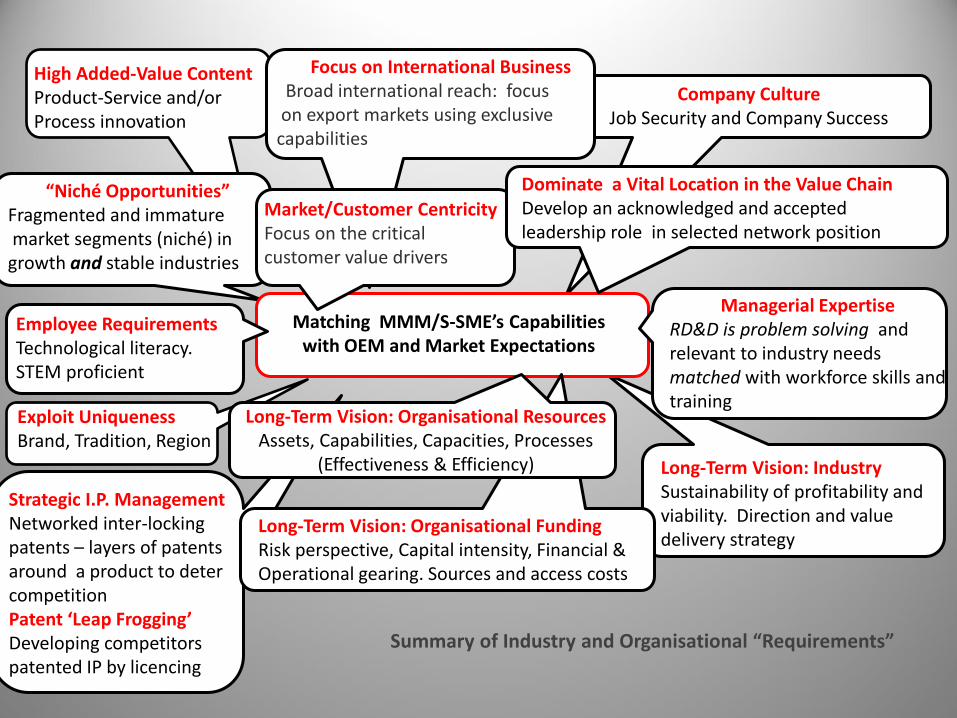

Critical Capabilities Matching MMM/S-SME’s Capabilities

with OEM and Market Expectations

“Niché Opportunities” Fragmented and immature market segments (niché) in growth and stable industries

Focus on International Business Broad international reach: focus on export markets using exclusive capabilities

Market/Customer Centricity Focus on the critical customer value drivers

Dominate a Vital Location in the Value Chain Develop an acknowledged and accepted leadership role in selected network position

Company Culture Job Security and Company Success

Managerial Expertise RD&D is problem solving and relevant to industry needs matched with workforce skills and training

Long-Term Vision: Industry Sustainability of profitability and viability. Direction and value delivery strategy

Long-Term Vision: Organisational Resources Assets, Capabilities, Capacities, Processes

(Effectiveness & Efficiency)

Long-Term Vision: Organisational Funding Risk perspective, Capital intensity, Financial & Operational gearing. Sources and access costs

Summary of Industry and Organisational “Requirements”

Employee Requirements Technological literacy. STEM proficient

Strategic I.P. Management Networked inter-locking patents – layers of patents around a product to deter competition Patent ‘Leap Frogging’ Developing competitors patented IP by licencing

High Added-Value Content Product-Service and/or Process innovation

Exploit Uniqueness Brand, Tradition, Region

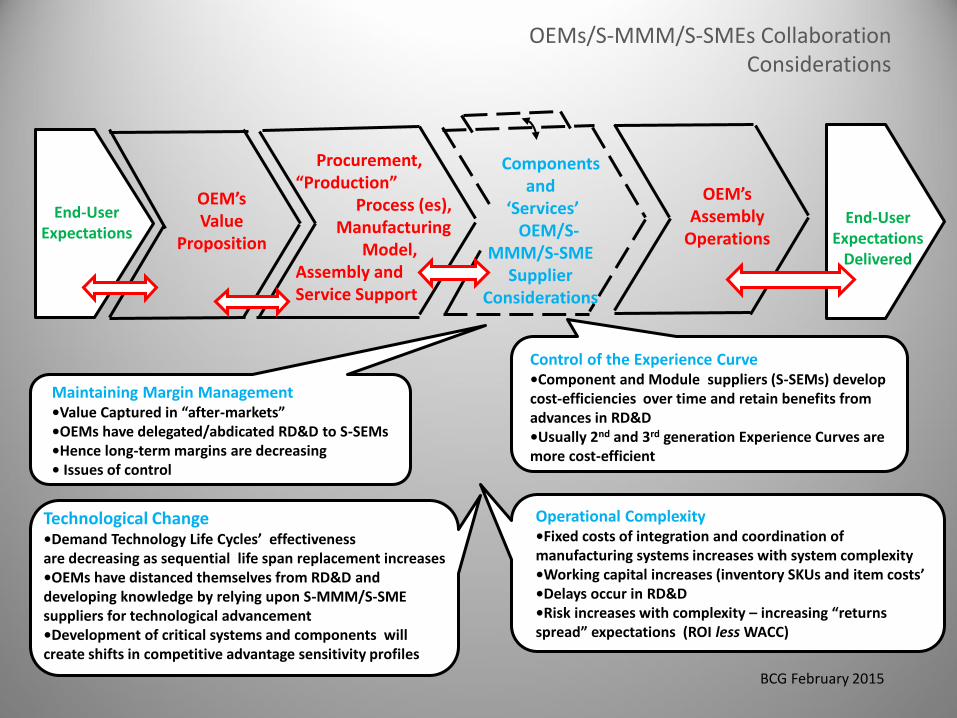

OEMs/S-MMM/S-SMEs Collaboration Considerations

Maintaining Margin Management •Value Captured in “after-markets” •OEMs have delegated/abdicated RD&D to S-SEMs •Hence long-term margins are decreasing • Issues of control

Technological Change •Demand Technology Life Cycles’ effectiveness are decreasing as sequential life span replacement increases •OEMs have distanced themselves from RD&D and developing knowledge by relying upon S-MMM/S-SME suppliers for technological advancement •Development of critical systems and components will create shifts in competitive advantage sensitivity profiles

Control of the Experience Curve •Component and Module suppliers (S-SEMs) develop cost-efficiencies over time and retain benefits from advances in RD&D •Usually 2nd and 3rd generation Experience Curves are more cost-efficient

Operational Complexity •Fixed costs of integration and coordination of manufacturing systems increases with system complexity •Working capital increases (inventory SKUs and item costs’ •Delays occur in RD&D •Risk increases with complexity – increasing “returns spread” expectations (ROI less WACC)

Components and

‘Services’ OEM/S-

MMM/S-SME Supplier

Considerations

Procurement, “Production”

Process (es), Manufacturing

Model, Assembly and Service Support

OEM’s Value

Proposition

End-User Expectations

End-User Expectations

Delivered

OEM’s Assembly

Operations

BCG February 2015

Thank you for your time ….

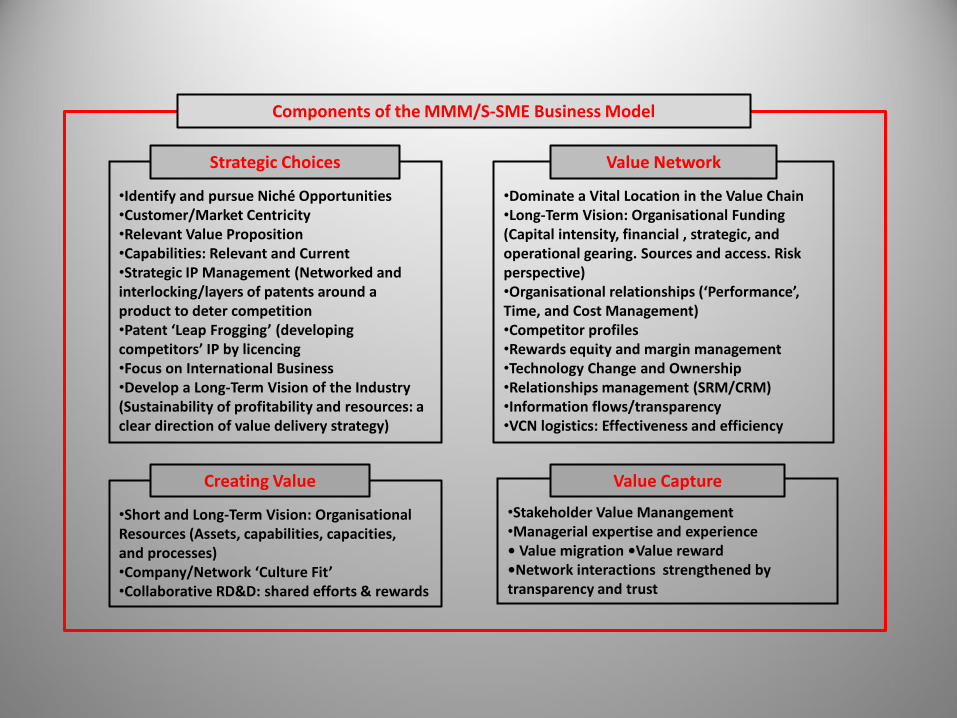

•Short and Long-Term Vision: Organisational Resources (Assets, capabilities, capacities, and processes) •Company/Network ‘Culture Fit’ •Collaborative RD&D: shared efforts & rewards

•Dominate a Vital Location in the Value Chain •Long-Term Vision: Organisational Funding (Capital intensity, financial , strategic, and operational gearing. Sources and access. Risk perspective) •Organisational relationships (‘Performance’, Time, and Cost Management) •Competitor profiles •Rewards equity and margin management •Technology Change and Ownership •Relationships management (SRM/CRM) •Information flows/transparency •VCN logistics: Effectiveness and efficiency

33

Components of the MMM/S-SME Business Model

•Identify and pursue Niché Opportunities •Customer/Market Centricity •Relevant Value Proposition •Capabilities: Relevant and Current •Strategic IP Management (Networked and interlocking/layers of patents around a product to deter competition •Patent ‘Leap Frogging’ (developing competitors’ IP by licencing •Focus on International Business •Develop a Long-Term Vision of the Industry (Sustainability of profitability and resources: a clear direction of value delivery strategy)

Strategic Choices Value Network

Creating Value

•Stakeholder Value Manangement •Managerial expertise and experience • Value migration •Value reward •Network interactions strengthened by transparency and trust

Value Capture

"IDC Manufacturing Insights sees a number of important industry drivers that will shape the manufacturing industry for the next few years, including complex value chains (relationship management), support for continuing emerging market growth (relationship management), customer centricity (relationship management), ubiquitous connectivity (knowledge and technology management), and data-driven insights (knowledge and process management); these drivers inform … the imperatives for 2015 and beyond,“

Simon Ellis, Practice Director, IDC Manufacturing Insights (2015)

INDUSTRY VALUE/PERFORMANCE DRIVERS

It is becoming necessary to identify key industry or marketplace drivers. It is suggested that such a framework revolves around the four generic, but focused industry value driver frameworks identified above as: knowledge management, technology management, process management and relationship management.

Industry Performance Drivers

35

Industry Performance Drivers

36

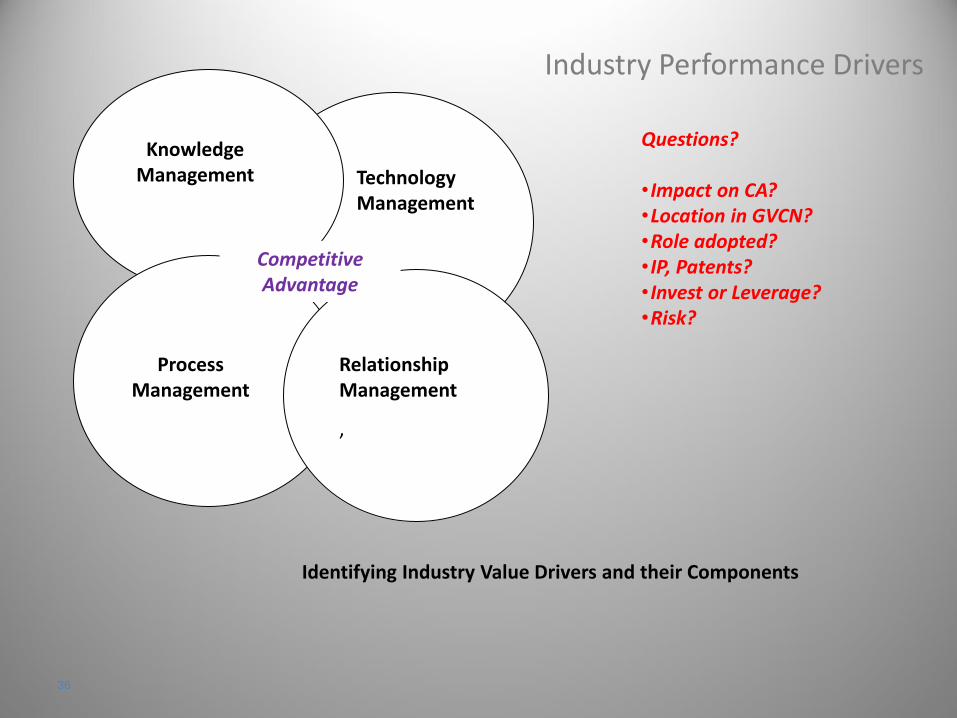

Knowledge Management

Process Management

Technology Management

Relationship Management ’

Identifying Industry Value Drivers and their Components

Questions? • Impact on CA? •Location in GVCN? •Role adopted? • IP, Patents? • Invest or Leverage? •Risk?

Competitive Advantage

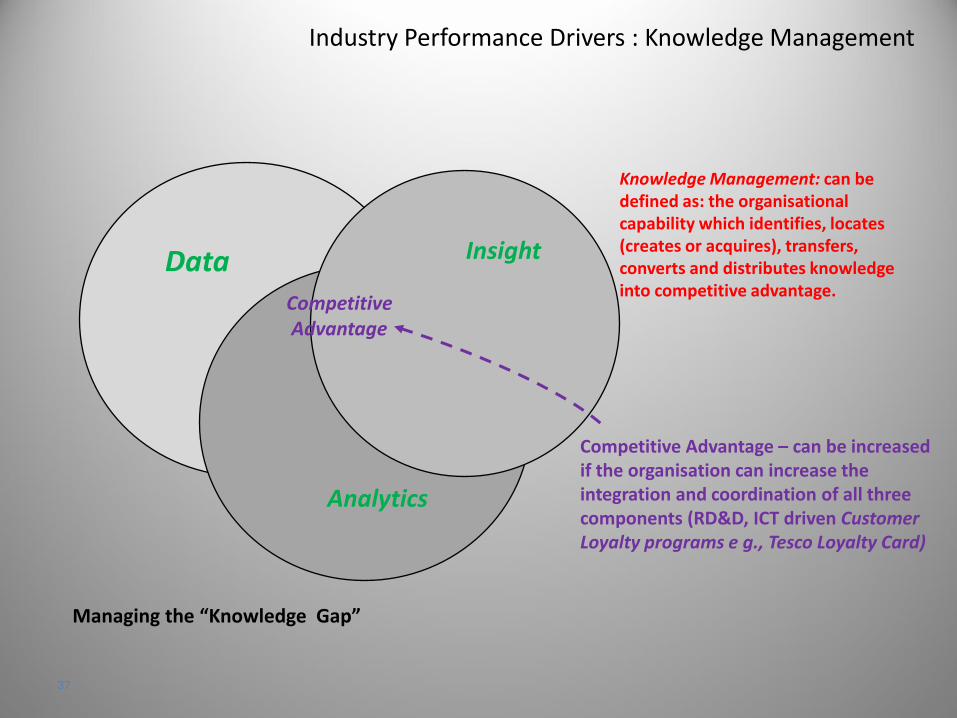

Industry Performance Drivers : Knowledge Management

37

Data Insight

Analytics

Competitive Advantage – can be increased if the organisation can increase the integration and coordination of all three components (RD&D, ICT driven Customer Loyalty programs e g., Tesco Loyalty Card)

Managing the “Knowledge Gap”

Knowledge Management: can be defined as: the organisational capability which identifies, locates (creates or acquires), transfers, converts and distributes knowledge into competitive advantage.

Competitive Advantage

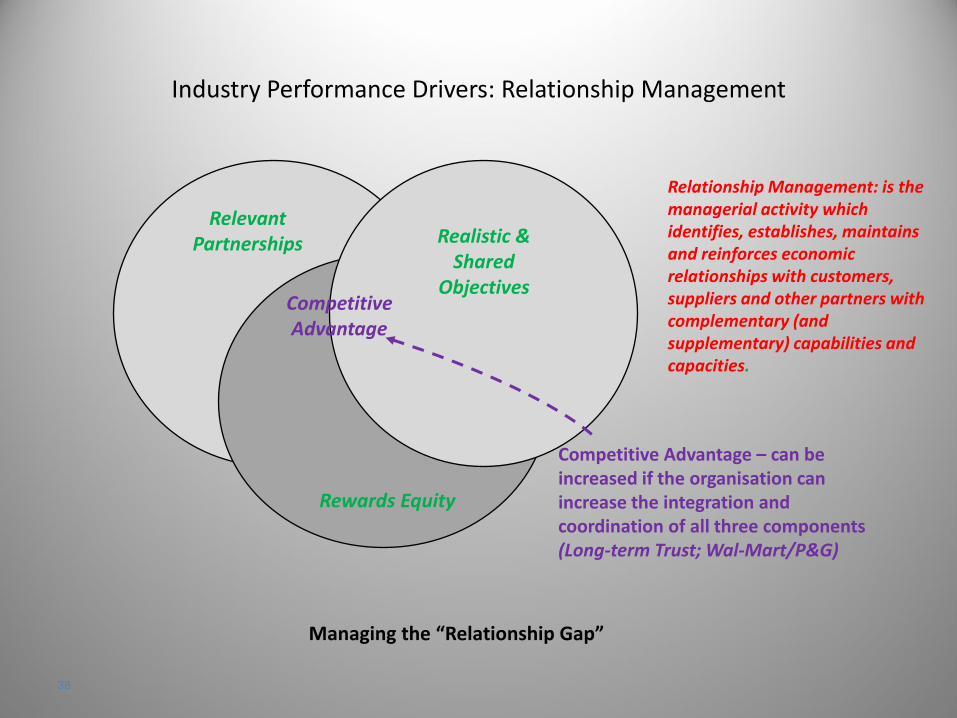

Industry Performance Drivers: Relationship Management

38

Relevant Partnerships Realistic &

Shared Objectives

Rewards Equity

Competitive Advantage – can be increased if the organisation can increase the integration and coordination of all three components (Long-term Trust; Wal-Mart/P&G)

Managing the “Relationship Gap”

Relationship Management: is the managerial activity which identifies, establishes, maintains and reinforces economic relationships with customers, suppliers and other partners with complementary (and supplementary) capabilities and capacities.

Competitive Advantage

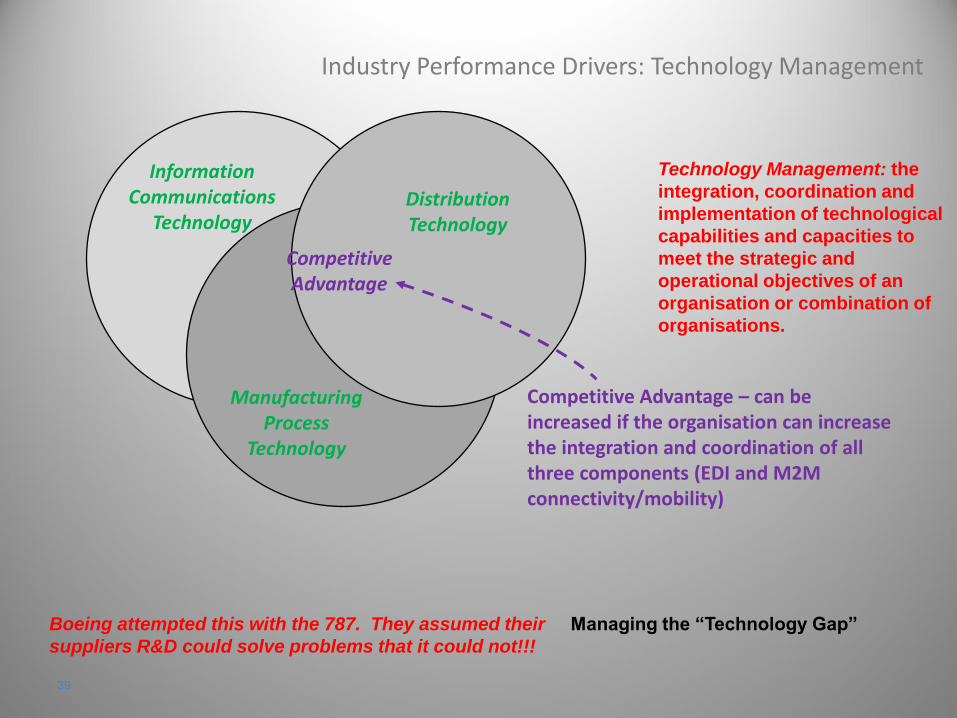

Information Communications

Technology Distribution Technology

Manufacturing Process

Technology

Competitive Advantage – can be increased if the organisation can increase the integration and coordination of all three components (EDI and M2M connectivity/mobility)

Boeing attempted this with the 787. They assumed their

suppliers R&D could solve problems that it could not!!!

Industry Performance Drivers: Technology Management

39

Technology Management: the

integration, coordination and

implementation of technological

capabilities and capacities to

meet the strategic and

operational objectives of an

organisation or combination of

organisations.

Managing the “Technology Gap”

Competitive Advantage

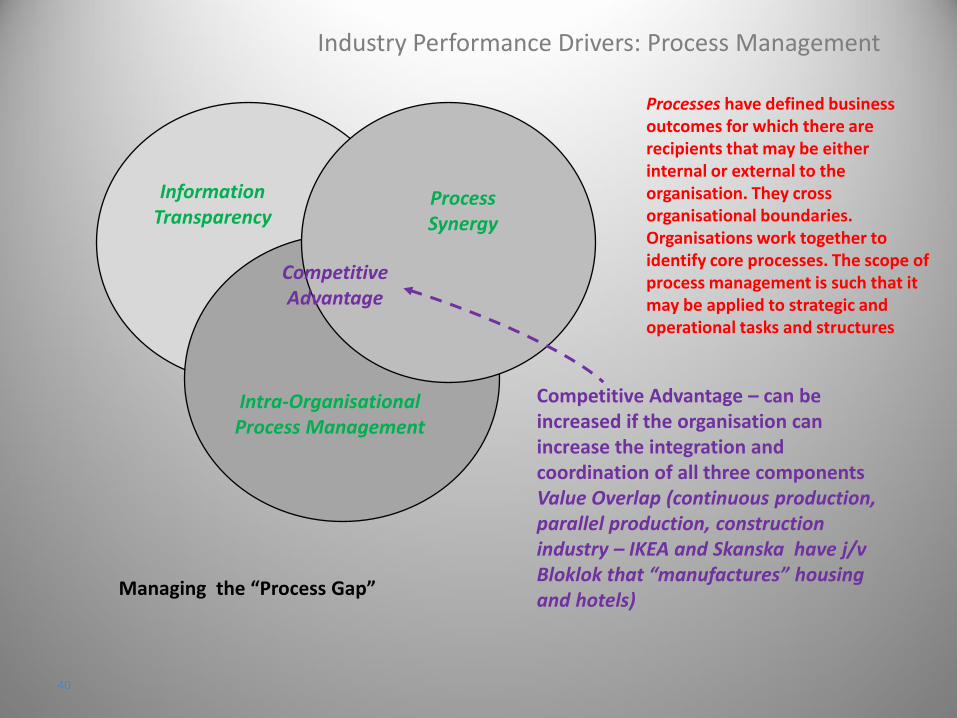

Industry Performance Drivers: Process Management

40

Information Transparency

Process Synergy

Intra-Organisational Process Management

Competitive Advantage – can be increased if the organisation can increase the integration and coordination of all three components Value Overlap (continuous production, parallel production, construction industry – IKEA and Skanska have j/v Bloklok that “manufactures” housing and hotels)

Managing the “Process Gap”

Processes have defined business outcomes for which there are recipients that may be either internal or external to the organisation. They cross organisational boundaries. Organisations work together to identify core processes. The scope of process management is such that it may be applied to strategic and operational tasks and structures

Competitive Advantage

“Performance”

Management

Time

Management

Cost

Management

The Value

Proposition A

Response to

Critical

Customer Value

Drivers

Value Chain Responses to Customers’ Value Expectation Adapted from: Melnyk S et al “Outcome-Driven Supply Chains”, MIT

Sloan Management Review, Winter, 2010

B2B Value Drivers

“Performance”

Management

Cost

Management

Time

Management

The Value

Proposition

Response

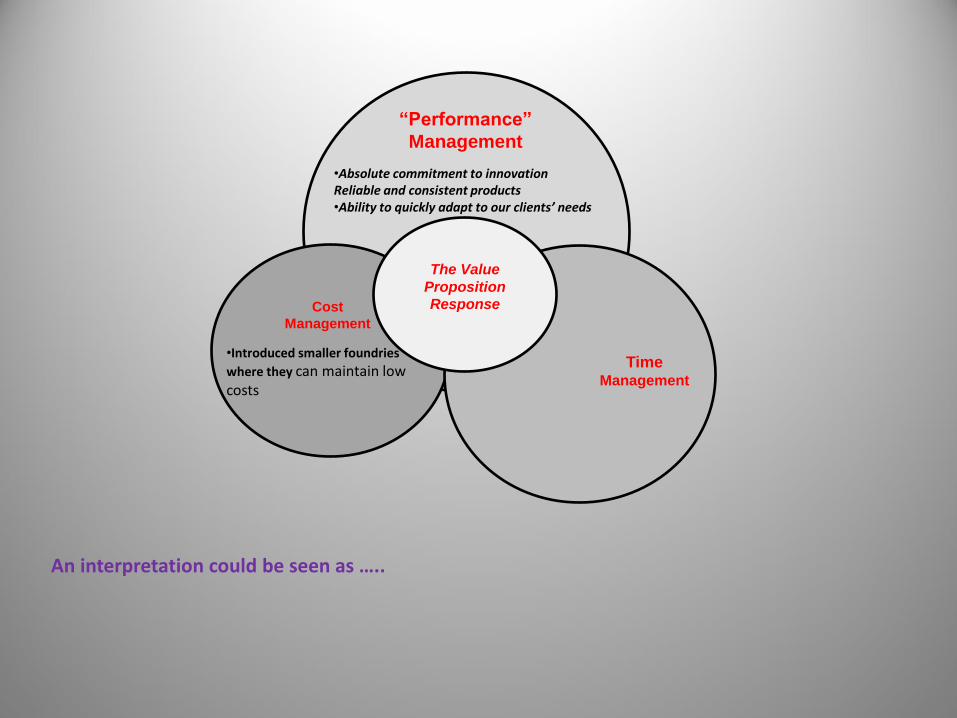

“Performance”

Management

•Absolute commitment to innovation Reliable and consistent products •Ability to quickly adapt to our clients’ needs

Cost

Management

•Introduced smaller foundries

where they can maintain low costs

Time

Management

The Value

Proposition

Response

An interpretation could be seen as …..