tax lin - nexia ts · tax lin 2012: the asia pacific tax year in review issue 1 1 tax link - asia...

TRANSCRIPT

TAX link2012: The Asia Pacific Tax Year in Review Issue 1

1 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

ASIA PACIFIC

Content

Australia International Dealings

China China Taxation Update Summary (2011-2012)

Hong Kong Hong Kong Tax Update (2012-2013)

India Recent Key Amendments in International Taxation

Indonesia Indonesia Update, 2012 Indonesia Tax Audit Focus and Indonesia Transfer Pricing

Japanese New Introduction of Earnings Stripping Rule

Korea Korean Tax Law for 2013

Malaysia Public Rulings Issued in 2012

Singapore A Roundup for Singapore Major Corporate Tax Changes for Budget 2012

Vietnam Tax Changes in 2012

International Dealings The Australian Taxation Office (ATO) has introduced a new income tax schedule for the 2012 income tax year – an International Dealings Schedule 2012. The new schedule will replace the previous Schedule 25A and the Thin Capitalisation schedule which were required to be included in Income Tax Returns for all taxpayers with related party international transactions over certain threshold amounts.

The ATO says from the 2012 income tax year, all companies, partnerships and trusts with international dealings that exceed the new threshold amounts will need to complete the Schedule. It says the Schedule is being introduced to capture data regarding international transactions which will be used in, notably, risk assessment and mitigation strategies to support compliance checking activities.

The Schedule substantially increases the disclosures required by taxpayers. The new disclosures required include information regarding:

■ foreign sourced income — detailed breakdown of foreign sourced income and deductions;

■ tax haven dealings — detailed breakdown of international related party dealings with “tax haven” jurisdictions;

■ transfer pricing — details of the transfer pricing methodologies used and the level of documentation maintained for each category of international related party dealings, as well as more detail on various types of international related party services, derivatives, cost contribution arrangements and other financial transactions;

■ debt/equity rules — details of international related party financing arrangements which are characterised differently for income tax and accounting purposes;

■ permanent establishments — details of internally recorded dealings with international branches;

Australia1

2

3

4

5

6

7

8

9

10

Australia

2 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

■ employee shares — details of share based employee remuneration transactions between international related parties; and

■ restructures — details of restructuring events involving international related parties.

From the new disclosures required, it can be seen that the ATO is looking to focus on areas which it considers controversial and/or high risk. For example, transfer pricing, restructures that include offshore entities and compliance with debt/equity rules have been allbeen subject to recent ATO auditactivity.

The new Schedule will result in a significant compliance burden for taxpayers as the minimum threshold set for completing the Schedule is only $2m in annual related party transactions.

With the ATO’s continued focus on transfer pricing compliance and the increased disclosure requirements under the new Schedule and also the current reforms to the transfer pricing rules, it is increasingly important for taxpayers to develop robust transfer pricing policies and governance frameworks to support international related-party arrangements and to ensure all appropriate documentation is kept to demonstrate compliance.

The ATO sees transfer pricing as a continuing compliance risk for small to medium enterprises (SME’s). The ATO plans to undertake a number of transfer pricing reviews and transfer pricing audits, and to contact at least 200 SME’s, addressing a range of international tax issues, particularly including those with international shipping operations. The ATO will also contact SME taxpayers on their reporting obligations related to the new Schedule as part of their 2012-13 compliance programs. The new Schedule will provide the ATO with much more information than ever before regarding a taxpayer’s transfer pricing arrangements and will be a key tool used to select taxpayers for audit review. High-risk indicators associated with transfer pricing typically include a high proportion of international related-party dealings relative to the size of the business, continuing losses or low profit levels relative to industry benchmarks and certain high-risk transaction types or arrangements, such as offshore business restructures or the use of hybrid debt instruments. Loss-generating branch operations are expected to be another area of focus.

The ATO also can rely on additional measures to identify taxpayers for audit review including information gathered by the Australian Transactions Reports and Analysis Centre (AUSTRAC) regarding transactions and money flows between Australia and international tax jurisdictions.

Recent Capital Gains Tax Changes Impacting Foreign ResidentsIn the last Budget, the Government removed the 50% CGT discount for foreign residents on capital gains that will accrue after the 8 May 2012. The CGT discount will remain available for capital gains that accrued prior to this date where foreign residents choose to obtain a market valuation of assets they owned in Australia as at 8 May 2012.

Under current rules foreign residents are only subject to CGT in Australia on “taxable Australian property” which is defined primarily as;

■ Real property situated in Australia (which includes a leasehold interest in land); and

■ Assets used in carrying on a business through a permanent establishment (PE) in Australia.

However, taxable Australian property also includes:

■ indirect Australian real property interests; ■ options and rights to acquire (i) Australian real

property, (ii) assets used in carrying on a business through a PE in Australia or (iii) “indirect Australian real property interests”;

■ mining, quarrying or prospecting rights if the minerals, petroleum or quarry materials are situated in Australia; and

■ Assets owned by a taxpayer who has ceased to be a resident of Australia and has chosen to defer the CGT liability until such time as the asset has been disposed of.

The Budget changes mean that foreign residents, who acquire assets that fall within the CGT net in Australia after the 8th May 2012, will no longer be able to avail themselves of the 50% CGT discount, meaning they will pay CGT on the whole amount of any gain realised on a subsequent disposal of the asset.

Foreign residents who owned assets in Australia within the CGT net as at the 8th May 2012 will still be able to access the discount for gains accrued up to that date, provided they get a valuation of the asset, but will be no longer entitled to the discount on any gains accruing to the asset after that date.

The general exception applying for assets acquired before 20 September 1985 means that foreign residents are not subject to CGT in relation to pre-CGT taxable Australian property they may own.

Contributed by Nexia Australia

3 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

Tax Update Summary: 2011/2012

In the last five years, China has responded to its booming economy with several major tax law changes and hundreds of tax law clarifications, many of which affect foreign companies and individuals that do business in the country. In 2008, the latest Enterprise Income Tax law was enacted, virtually stripping away previous tax incentives for foreign invested companies and applying a flat tax rate of 25% for all domestic and foreign invested entities. In 2011, the Individual Income Tax system was overhauled in order to lower the tax burden for low income earners and increase the tax burden for higher income earners. The requirement that foreign workers in China participate in the Social Security system was added as well. 2012 brought with it a pilot program that will ultimately result in China having only one form of indirect taxation, doing away with Business Tax in favor of an all Valued-Added Tax system. In our quarterly newsletters we have reported each of these changes in detail, and in the following paragraphs we offer an overview of the highlights.

Since enactment of the 2008 Enterprise income Tax law (EIT), China’s State Administration of Taxation (SAT) has issued many circulars to clarify points raised in the new law. While all previous tax incentives were done away with, favorable EIT tax rates of 15% (rather than 25%) were offered to companies engaged in High Technology businesses, and related rules for how to qualify as a High Technology firm were clarified. Super deductions of an additional 50% were offered and clarified for qualifying R&D centers, along with various reductions or elimination of VAT on qualifying equipment that is purchased. More recently, incentives for foreign investment in China’s western regions have been introduced. Qualifying encouraged businesses can enjoy EIT rates of 15% until the year 2020.

Many of the circulars issued by SAT are related to foreign

companies doing business in China, either with or without Permanent Establishments or entities in the country. The deemed profit rate used in EIT calculations for foreign company Representative Offices (RO) was raised to a minimum of 15% of the RO annual operation expenses. Enforcement of the 10% withholding tax collection was enhanced by implementation rules related to foreign businesses providing services to Chinese clients. The Chinese clients now must, within 30 days of signing a service contract with a foreign company, register those contracts with their local tax authorities. Also, Business Tax of 5% applies to any transaction in which a foreign company (or Foreign Invested Enterprise in China) provides service to a Chinese client, no matter whether the service is performed in China or elsewhere. Furthermore, whereas Foreign Invested Enterprises (FIEs) in China were previously exempt from local surcharge taxes, FIEs are now required to pay the surcharge taxes, which may total as much as 11% of the Business Tax paid by the company annually. Another significant change in recent years is that many corporate restructuring activities involving entities in China, such as share transfer transactions, are subject to Enterprise Income Tax filing in China.

China’s SAT also issued an important clarification of the China-Singapore Tax Treaty, providing interpretation of terms and conditions that are being used for all of China’s tax treaties with other countries. Necessary conditions for creation of a Permanent Establishment were clarified and indeed broadened such that foreign companies dispatching their employees to work for subsidiaries in China must ensure that the employment arrangement is for the sole benefit of the China subsidiary. Additionally, the necessary conditions required to be considered a Beneficial Owner tax-protected by a given tax treaty were tightened such that a “Holding Company” outside of China must be engaged in its own substantial business other than merely holding the investment in a China subsidiary.

In 2011, China’s Individual Income Tax law was overhauled, with changes made to benefit low income earners and to place a higher tax burden on high income earners. The previous nine tier progressive tax rate scale was reduced to seven tiers in which those earning less than

China

China

4 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

RMB 15,000 per month pay less tax, and those earning in excess of RMB 40,000 per month pay considerably more tax each year. Additionally, measures are now in place to ensure that high income earners declare incomes from activities that are not salary-related. While not specifically targeting foreign workers in China, the new IIT laws and related enforcement activities no doubt affect most foreign workers in China, since foreign workers do tend to be high income earners.

Another significant change taking place in China is the current shift from a two mode indirect taxation system, which utilizes both Value-Added Tax (VAT) and Business Tax (BT), to a single mode system in which only VAT applies. BT is a turnover tax that has been paid by most service businesses, usually at a rate of 5% of business revenues. VAT, generally at a rate of 17%, is a sales tax paid on a transaction basis. Since businesses can credit VAT paid out against VAT collected, VAT is generally borne by the end user of the goods or services. However, under the two mode system, many businesses have been trapped in a situation of being doubly taxed. The change to an all VAT system now removes the possibility of double taxation as well as simplifying the entire indirect taxation of businesses.

The VAT reform program began on January 1, 2012 in Shanghai only, bringing six service industries out of the BT mode of taxation into the VAT mode. While VAT rates on the sale of goods remains at 17%, the VAT rates for the targeted services range from 6% to 17%. Exported services are either zero-rated or exempt from VAT, depending on the actual service provided. The change to the VAT system has brought about a reduction in the overall indirect tax

burden for approximately 70% of businesses that have been involved. Only the transportation services industry has experienced significant problems under the reform, and SAT and other agencies are working to find solutions. Based on the success of the Shanghai pilot program, the VAT reforms are being extended to include nine other regions in China, including Beijing, Guangzhou, Chongqing and others. The service industries selected for the initial reforms in each area may differ slightly from those in Shanghai, depending on the specific industry economic prevalence in the area. It remains unclear how foreign businesses currently liable for BT on service transactions with Chinese clients will be affected once the reforms are fully implemented, but it is assumed that VAT will be withheld and paid by the Chinese client at the time payment on invoices is made.

It would be impossible in this short article to describe details of all the changes cited above, however, it is hoped that enough information has been provided so that foreign tax professionals are aware of the dynamic nature of China taxation. It should also be noted that while China’s central government issues the laws and frequently issues clarifications related to those laws, interpretation, implementation and enforcement is done at the local level. As such, clients doing business in one area of China may experience slightly different determinations than clients in another area. It is therefore considered prudent to consult with local China tax professionals who can provide the latest and most accurate information, no matter what kind of China taxation issues may be presented to a client.

Contributed byNexia TS (Shanghai)

5 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

Hong Kong

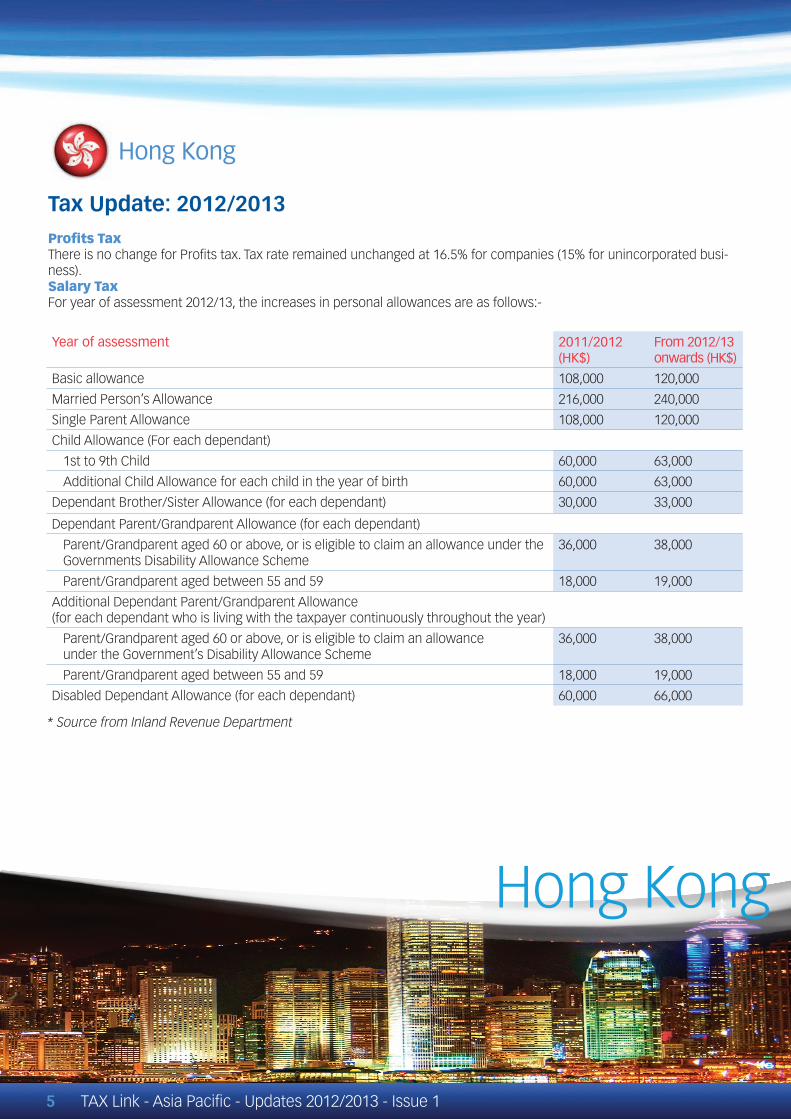

Tax Update: 2012/2013Profits TaxThere is no change for Profits tax. Tax rate remained unchanged at 16.5% for companies (15% for unincorporated busi-ness).Salary TaxFor year of assessment 2012/13, the increases in personal allowances are as follows:-

Year of assessment 2011/2012 (HK$)

From 2012/13 onwards (HK$)

Basic allowance 108,000 120,000

Married Person’s Allowance 216,000 240,000

Single Parent Allowance 108,000 120,000

Child Allowance (For each dependant)

1st to 9th Child 60,000 63,000

Additional Child Allowance for each child in the year of birth 60,000 63,000

Dependant Brother/Sister Allowance (for each dependant) 30,000 33,000

Dependant Parent/Grandparent Allowance (for each dependant)

Parent/Grandparent aged 60 or above, or is eligible to claim an allowance under the Governments Disability Allowance Scheme

36,000 38,000

Parent/Grandparent aged between 55 and 59 18,000 19,000

Additional Dependant Parent/Grandparent Allowance (for each dependant who is living with the taxpayer continuously throughout the year)

Parent/Grandparent aged 60 or above, or is eligible to claim an allowance under the Government’s Disability Allowance Scheme

36,000 38,000

Parent/Grandparent aged between 55 and 59 18,000 19,000

Disabled Dependant Allowance (for each dependant) 60,000 66,000

* Source from Inland Revenue Department

Hong Kong

6 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

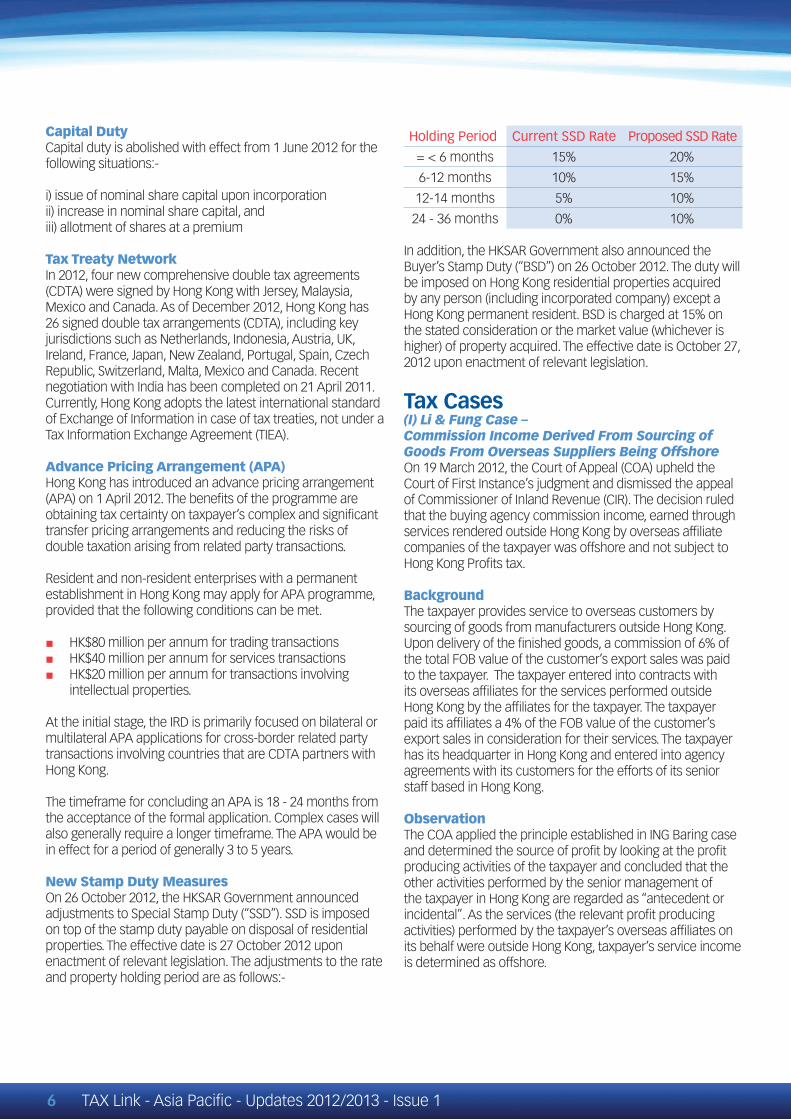

Holding Period Current SSD Rate Proposed SSD Rate

= < 6 months 15% 20%

6-12 months 10% 15%

12-14 months 5% 10%

24 - 36 months 0% 10%

In addition, the HKSAR Government also announced the Buyer’s Stamp Duty (“BSD”) on 26 October 2012. The duty will be imposed on Hong Kong residential properties acquired by any person (including incorporated company) except a Hong Kong permanent resident. BSD is charged at 15% on the stated consideration or the market value (whichever is higher) of property acquired. The effective date is October 27, 2012 upon enactment of relevant legislation.

Tax Cases(I) Li & Fung Case – Commission Income Derived From Sourcing of Goods From Overseas Suppliers Being OffshoreOn 19 March 2012, the Court of Appeal (COA) upheld the Court of First Instance’s judgment and dismissed the appeal of Commissioner of Inland Revenue (CIR). The decision ruled that the buying agency commission income, earned through services rendered outside Hong Kong by overseas affiliate companies of the taxpayer was offshore and not subject to Hong Kong Profits tax.

BackgroundThe taxpayer provides service to overseas customers by sourcing of goods from manufacturers outside Hong Kong. Upon delivery of the finished goods, a commission of 6% of the total FOB value of the customer’s export sales was paid to the taxpayer. The taxpayer entered into contracts with its overseas affiliates for the services performed outside Hong Kong by the affiliates for the taxpayer. The taxpayer paid its affiliates a 4% of the FOB value of the customer’s export sales in consideration for their services. The taxpayer has its headquarter in Hong Kong and entered into agency agreements with its customers for the efforts of its senior staff based in Hong Kong.

ObservationThe COA applied the principle established in ING Baring case and determined the source of profit by looking at the profit producing activities of the taxpayer and concluded that the other activities performed by the senior management of the taxpayer in Hong Kong are regarded as “antecedent or incidental”. As the services (the relevant profit producing activities) performed by the taxpayer’s overseas affiliates on its behalf were outside Hong Kong, taxpayer’s service income is determined as offshore.

Capital Duty Capital duty is abolished with effect from 1 June 2012 for the following situations:-

i) issue of nominal share capital upon incorporationii) increase in nominal share capital, andiii) allotment of shares at a premium

Tax Treaty NetworkIn 2012, four new comprehensive double tax agreements (CDTA) were signed by Hong Kong with Jersey, Malaysia, Mexico and Canada. As of December 2012, Hong Kong has 26 signed double tax arrangements (CDTA), including key jurisdictions such as Netherlands, Indonesia, Austria, UK, Ireland, France, Japan, New Zealand, Portugal, Spain, Czech Republic, Switzerland, Malta, Mexico and Canada. Recent negotiation with India has been completed on 21 April 2011. Currently, Hong Kong adopts the latest international standard of Exchange of Information in case of tax treaties, not under a Tax Information Exchange Agreement (TIEA).

Advance Pricing Arrangement (APA)Hong Kong has introduced an advance pricing arrangement (APA) on 1 April 2012. The benefits of the programme are obtaining tax certainty on taxpayer’s complex and significant transfer pricing arrangements and reducing the risks of double taxation arising from related party transactions.

Resident and non-resident enterprises with a permanent establishment in Hong Kong may apply for APA programme, provided that the following conditions can be met.

■ HK$80 million per annum for trading transactions ■ HK$40 million per annum for services transactions ■ HK$20 million per annum for transactions involving

intellectual properties.

At the initial stage, the IRD is primarily focused on bilateral or multilateral APA applications for cross-border related party transactions involving countries that are CDTA partners with Hong Kong.

The timeframe for concluding an APA is 18 - 24 months from the acceptance of the formal application. Complex cases will also generally require a longer timeframe. The APA would be in effect for a period of generally 3 to 5 years.

New Stamp Duty MeasuresOn 26 October 2012, the HKSAR Government announced adjustments to Special Stamp Duty (“SSD”). SSD is imposed on top of the stamp duty payable on disposal of residential properties. The effective date is 27 October 2012 upon enactment of relevant legislation. The adjustments to the rate and property holding period are as follows:-

7 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

Recent key amendments in International TaxationIn this article, we discuss certain important tax proposals introduced by Finance Act, 2012 in India in respect of international taxation. It may not be out of place to mention here that the amendments brought about by the Finance Act, 2012 has changed the landscape of Indian Corporate Taxation. The Indian Budget 2012 introduced many retrospective provisions effective from April 1961, many of which appears to be fallout from the Supreme Court Vodafone decision. Be that as it may be, some of the key amendments relating to international tax are as under:

1. Introduction of General Anti-Avoidance Rule (GAAR)2. Introduction of Advance Pricing Arrangement (APA)3. Transfer pricing provisions to be applicable to

domestic transactions.

1. Introduction of General Anti-Avoidance Rule (GAAR)

The GAAR provisions introduced by Finance Act, 2012 are contained in Chapter XA of the Indian Income Tax Act (Sections 95 to 102). Prior to this, Indian Tax Law did not have any general anti-voidance provisions. The new provisions will allow the tax authority to, notwithstanding anything contained elsewhere in the Indian Income Tax Act, declare an ‘arrangement ‘as an impermissible arrangement, if such an arrangement lacks commercial substance and is entered to obtain a tax benefit.

The detailed provisions explain that a transaction will be considered as impermissible if it satisfies anyone of the following four criteria:

a. The transaction is not at arm’s length;b. It results in misuse or abuse of the provisions

of the Act;c. It is devoid of commercial substance;d. It is carried out in a manner, which is normally not

employed for bona fide purpose.

India(II) Nice Cheer Case - Unrealised Profits From Revaluation of Fair Market Value of Trading SecuritiesThe Court of Appeal dismissed the Commissioner’s appeal and upheld the decision of the Court of First Instance on 19 June 2012. The unrealized gains arising from revaluation of fair market value of the taxpayer’s trading securities are non-taxable.

BackgroundThe taxpayer’s principal activity is investment trading. Its accounts were prepared in accordance with the financial reporting standards in Hong Kong. Under those prevailing accounting standards and practices, any unrealized gains or losses arising from the change in fair value of the trading securities listed in Hong Kong were recognized by the taxpayer in its profit and loss accounts in the relevant financial years.

The taxpayer argued that unrealized gains arising from the revaluation of the trading securities are not chargeable to Hong Kong profits tax for the purposes of section 14(1) of the IRO as they merely reflect the changes in fair value of the trading stock and are not real profits arising from trading.

On the other hand, the Commissioner argued that the unrealized gains are profits of the taxpayer since the profits have been ascertained in accordance with ordinary commercial accounting principles and section 14 of the IRO does not prevent the charging of profits tax in respect of unrealized gains from revaluation.

ObservationBased on the judgment of the case, the unrealized profits from revaluation of its market fair value for the trading securities are not taxable as the profits must be received, accrued or earned but not anticipated. The fact that the fair value fluctuations of the trading securities were included in the financial statements of the taxpayer as unrealized gains/losses does not mean such unrealized gains are “profits” for the purposes of the IRO. The issue of whether such unrealized gains are profits liable to tax is ultimately a matter of statutory interpretation.

Contributed by Chan & Co.

India

8 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

Further, the provisions will apply to all tax payers irrespective of their residential or legal status. The Central Board of Direct Tax has recently released draft guidelines for the implementation of GAAR. Under the guidelines, the provisions of GAAR will apply to income accruing or arising to the tax payer on or after 01.04.2013. An important feature in the draft guideline is the acknowledgement of the fact that the onus of proving that the transaction is an impermissible transaction will be on the tax authority. As per Media Reports, the committee set up to examine the issues relating to GAAR is expected to finalize its report by 30.09.2012 and give its recommendation. We hope going forward that the GAAR provisions are invoked only in appropriate cases to counter aggressive tax avoidance schemes and that all due care is taken to avoid any harassment of tax payers.

2. Introduction of Advance Pricing Arrangement (APA)

India has completed its first decade since transfer pricing provisions were introduced in 2001. The last decade saw significant litigation on several transfer pricing related issues. The aggregate income adjustments have seen tremendous increases over the last few years. It is believed that transfer pricing adjustments of US$8.9 billion (INR Rs 44,500 crores) were made in the latest round of concluded transfer pricing audits. To address the year by year acceleration in transfer pricing, the Finance Act, 2012 has introduced provisions to deal with advance pricing arrangements.. The key APA provisions are as follows:

■ APA introduced in the Income Tax Act,1961 under sec-tion 92CC to 92CD;

■ APA provisions will take effect from 1st July 2012 and will be available to all tax payers falling within the pur-view of Indian transfer pricing rules;

■ Validity of APA not to exceed 5 consecutive years; ■ APA to be declared as void ab initio if obtained by

fraud or misrepresentation of facts; ■ The arm’s length prices may be determined by any

method prescribed under Income Transfer Pricing Rules;

■ The APA will be binding on the signees; ■ Guidelines / Rules for Advance Pricing Agreements are

awaited.

It is a welcome move introduced by the Government of India and may go a long way in reducing the transfer pricing litigation provided the provisions are implemented in the right spirits.

3. Extension of transfer pricing provisions to domestic transactions

Until the introduction of Finance Act, 2012, transfer pricing provisions were applicable only to cross border related party transactions. The Finance Act, 2012 has extended the scope of Indian Transfer Pricing provisions to cover certain domestic transactions with related parties within India defined as “Specified domestic transactions”.Primarily, a specified domestic transaction is defined as under:

1. Expenditure for which payment is made to specified domestic related parties;

2. Transactions between a business eligible for a tax holiday and other persons having a close connection.

Highlights of the Specified Domestic Transfer Pricing provisions are:

■ Applicable from 01.04.2012; ■ Apply where the aggregate value of the transactions

entered into by the taxpayer with its domestic associ-ated enterprise exceeds 5 crore;

■ Empower a tax officer to disallow unreasonable ex-penditure incurred between domestic related parties;

■ Ensure entities claiming a tax holiday with super-nor-mal profits to comply with TP laws.

Further, detailed documentation, as specified in the Indian Transfer Pricing Rules, will now have to be maintained to prove that the transactions are at arm’s length price.

Conclusion Apart from the above, certain other amendments have also been brought about such as the obtaining of a tax residency certificate to enable access to tax treaties, amendment to the definition of royalties, widening the scope of international transactions subject to Transfer Pricing rules.

Given the nature of the amendments brought about, there will be significant impacts on tax payers. Further, some of the retrospective amendments will put undue hardship on tax payers and may lead to a further increase in litigation. One may have to see how the appellate authorities will interpret these amendments.

Contributed byChaturvedi & Shah

9 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

Indonesia Update The master plan of Economic Development Acceleration and Expansion of Indonesia, hereinafter refered to as MP3EI, is a smart, focused and scalable strategy to drive the acceleration and expansion of economic development with the aim of making Indonesia the 12th top developed nation in the world by 2025 and number 9 in the world by 2045. MP3EI seeks to encourage the creation of integrated economic activity, synergy and high value added enterprises.

The investment climate is the key of Indonesia’s economic growth. The fluctuating situation in Indonesia due to the financial crisis in Europe, means Indonesia must boost confidence and maintain the image that Indonesia has good investment quality.

Besides that, investment is also the key to achieving economic growth targets in the draft State Budget 2013. In the first quater in 2012, investment trends increased to 32.8%, which proved that investment can be a mainstay of economic growth in Indonesia.

To improve the investment climate, the Government has issued many policy documents covering certain industry and trade sectors. In the fiscal sector, the Government is providing incentives for investors in the form of tax holidays and allowances. Tax holidays have been provided for pioneer industries and tax allowances provided for certain industries and geographical regions.

a. Tax HolidaysTo enhance the role of investment in Indonesia’s economy, the Government on August 15, 2011 via the Minister of Finance Regulation No. 130/PMK.011/2011, is providing income tax exemption to certain industries known as a pioneer industries. These industries include the basic metal industry, petroleum refining industry and/

or organic chemicals derived from oil and natural gas, machinery industry, renewable resources industry and the communication equipment industry.

Tax benefits provided are a tax exemption for a maximum of 10 years and at least 5 years and a tax reduction for 2 years of 50% of tax payable from the time tax exemption is over.

Companies that can obtain tax exemption and reduction benefits are:1. A Pioneer Industry;2. Have a new capital investment plan that has been

approved by the competent authority of at least IDR 1,000,000,000,000 (one trillion rupiahs);

3. Place funds in an Indonesian Bank of at least 10% of the total investment plan;

4. An Indonesian legal entity which has endorsement as at August 14, 2010.

Submission of the application for tax exemption and reduction must be filed no later than 3 years from the date the regulation was authorized.

b. Tax AllowancesTo provide an alternative other than a Tax Holiday and to expand certain business sectors and/or regions eligible for tax incentives, on December 2011, the Government issued a policy of tax incentives through Government Regulation No. 52 Year 2011 regarding Tax Facility for Investment in Certain Business Sectors and Regions.

Government Regulation No. 52 Year 2011 is the second amendment of the Government Regulation No. 1 Year 2007, which is basically a package of policies to provide incentives such as an investment allowance, for industries that have a high priority in the national scale.

Legal entities that may be granted a tax allowance are companies in the form of limited liability companies (PT) and cooperatives (Koperasi) investing in:

1. Certain business sectors; and/or

Indonesia

Indonesia

10 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

A reduction of the withholding tax rate on dividends is expected to attract foreign investors to Indonesia.

An extension of the loss carry-forward period will be granted if the taxpayer is in the deemed industrial and bonded area, employs 500 Indonesian employees, invests in economic and social infrastructure, spendson research

and development at least 5% (five per cent) of total investment and uses domestic raw material of at least 70% in their operations.

2012 Tax Audit Focus The taxation system in Indonesia adheres to the principle of self-assessment. To ensure taxpayers compliance with theirtax obligations the Directorate General of Taxation (DGT) conducts extensive tax audits.

In the 2012 year, the DGT targetted and focused their audit activity on industries with some of the following characteristics:

1. Business sectors that have contributed significantly to the economy and tax revenue.

2. Business sectors where the level of compliance in 2011 and earlier years is still low

3. Business sectors which in 2012 have a high ability to pay

4. Business sectors which are of public concern.

The 2012 National Tax Audit Focus was on. Corporate and Individual Taxpayers. For Corporate Taxpayers the industry focus was on oil palm plantations, mining, media, chemical industry, manufacturing, automotive construction, wholesaler, banking and insurance, real estate and consulting services. For Individual Taxpayers the focus was on tax consultants, notaries, lawyers, and individuals who had relationships with corporate taxpayers in the aforementioned industries.

Indonesia Transfer Pricing The Indonesian transfer pricing regulations confirm the applicability of the arm’s length principle and the content is mainly in line with the OECD transfer pricing guidelines. Hence, at least in theory, Indonesian taxpayers can rely on internationally accepted principles and practices. However, there are some notable differences, some of which may have a significant impact on taxpayers, in particular where global transfer pricing documentation at a group level is

2. Certain business sectors and regions.3. Have a capital investment at least IDR

1,000,000,000,000 (one trillion rupiahs);4. Not operating commercially yet.

Tax facilities based on The Government Regulation No. 52 Year 2011 are :

1. A reduction in net income of 30% of the amount of capital investment, which can be claimed within 6 years, prorated at 5% per year.

2. Accelerated depreciation and amortization claims,so that assets can be depreciated in half the normal time.

3. A reduction in withholding tax rates on dividends paid to a foreign taxpayer to 10% or the lower rate according to the relevant Double Taxation Agreement in force.

4. An extension of the loss carry-forward period from 5 years to a maximum of 10 years.

The incentive reductions allowed are intended to ensure that in the early period of commercial operation, the taxpayer is not burdened by the imposition of income tax so as to accelerate the return on investment and to improve cash flow.

A reduction of the withholding tax rate on dividends is expected to attract foreign investors to Indonesia.

An extension of the loss carry-forward period will be granted if the taxpayer is in the deemed industrial and bonded area, employs 500 Indonesian employees, invests in economic and social infrastructure, spendson research and development at least 5% (five per cent) of total investment and uses domestic raw material of at least 70% in their operations.

Indonesia

11 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

prepared.In 2005 the Minister of Finance said it had received a list of 750 Foreign Direct Investment companies (PMA) that do not pay taxes because of continuous losses. (It is alleged that the transfer price is not arm’s length).

Under Indonesian Tax Law “Director General of Taxes is authorized to reallocate income and deductions between related parties and to characterize debt as equity for the purposes of the computation of taxable income to assure that the transaction are those which would have been made between independent parties...”

This is in line with Double Taxation Agreements mentioning that “[Where] conditions are made or imposed between the two [associated] enterprises in their commercial or financial relations which differ from those which would be made between independent enterprises, then any profits which would, but for those conditions, have accrued to one of the enterprises, but, by reason of those conditions, have not so accrued, may be included in the profits of that enterprise and taxed accordingly.

“Where a Contracting State includes in the profits of an enterprise of that State -- and taxes accordingly -- …, then that other State shall make an appropriate adjustment to the amount of the tax charged therein on those profits. In determining such adjustment, due regard shall be had to the other provisions of this Agreement and the competent authorities of the Contracting States shall if necessary consult each other”.

Indonesia Transfer Pricing Rules have been regulated by Tax Law since 1983 and the DGT has authority to make adjustments using Arm’s length principles (ALP), In 1993 the government set outGuidelines for Audits on Related Parties Taxpayers and Instructions for Handling Transfer Pricing Cases, whereas in 2010, the DGT issued Regulations on Applications of Arm’s Length Principle (ALP), Mutual Agreement Procedures (MAP) and Advanced Pricing Agreements (APA). Starting this year, taxpayers who transact with parties that have a special relationship where the transaction value is over Rp. 10 million are required to

have Transfer Pricing Documentation On 11 November 2011, the DGT issued Regulation No. PER-32/PJ/2011 regarding the Amendment of PER-43/PJ/2010 regarding the Determination of Arm’s Length and Common Business Principals in Transactions made between a Taxpayer and it’s related parties.

There are significant changes in these regulations which can now examine:1. Transactions conducted by resident taxpayers or a

permanent establishment (PE) in Indonesia with a foreign related taxpayer.

2. Transactions with related parties which capitalize on differences in tax rates including both income and sales taxes.

3. Transactions executed by a taxpayer with related parties where the income or expenditure does not exceed Rp 10,000,000,000 (ten billion rupiah) are not obligated to :

a. conduct comparability analysis and determine the comparable price;

b. determine an appropriate transfer pricing method;

c. implement arm’s length principles based on the result of comparable analysis and appropriate transfer pricing; and

d. document the steps taken in determining the fair value or reasonable profit in accordance with the provisions of the prevailing tax regulations.

4. Any determination of fair value or reasonable profit must be conducted to determine the transfer pricing method that best suits.

The methodologies used to calculate fairness of price can include the Comparable Uncontrolled Price (CUP) method, Resale Price method (RPM), Cost Plus method (CPM), Profit Split Margin method and Total Net Margin method (TNMM).

Contributed by KAP Kanaka Puradiredja

Japan12 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

Japanese Tax Updates: New Introduction of Earnings Stripping Rule

In order to prevent a taxable base erosion from making payments of “excessive” interest to foreign related parties, an earnings stripping rule (referred to as “ESR”) has been introduced into the corporation tax law by the 2012 Tax Reform Act and will be in effective from the tax year begin-ning on and after 1 April, 2013.

The calculation of disallowed interest under Japanese ESR is similar to that under the ESR of the USA, but is different from that of the USA in the following points.

■ While there is a safe harbor rule of debt to equity ratio in the USA’s rule, there is no safe harbor rule, but there is a de minimus rule.

■ While only the disqualified interest is subject to disal-lowance of deduction in the USA’s rule, the full amount of interest payments to a foreign related party is sub-ject to disallowance.

Although the ESR has introduced new measures the Thin Capitalization Rule (referred to as “TCR”) is still effective.

Accordingly, the amount of disallowed interest shall be determined as the calculated amount under the ESR or the calculated amount under the TCR, whichever is larger.

1. Disallowed InterestDisallowed interest shall be determined as the amount of net applicable related party interest expense (referred to

Japanas “NARPIE”) in excess of the limitation being 50% of the adjusted taxable income for the current tax year. Any ex-cess interest, which is disallowed interest, can be carried forward for 7 years and will be deductible to the extent of the excess limitation, being the limitation in excess of the NARPIE, in the tax year when the excess limitation incurs.

2. Adjusted Taxable IncomeThe adjusted taxable income is almost equivalent to the amount of tax base cash-in-flow from operations. That is, it is determined with the following items being added to or deducted from taxable income before application of the ESR or the TCR.

Additions:1. Non-taxable income with cash-in-flow, such as divi-

dend income2. Deductible expenses without cash-out-flow, such as

depreciation, amortization etc.3. NARPIE

Deductions:1. Taxable income without cash-in-flow, such as recap-

ture of reserves, or income recognized under the tax haven rule etc.

2. Non-deductible expenses with cash-out-flow, such as donations, foreign tax etc.

Entertainment expense, which is non-deductible expense with cash-out-flow, and recapture of depreciation expense for a disposed asset shall not be taken into account for determination of the adjusted taxable income. This treat-ment is favorable to taxpayers subject to the ESR because a reduction of the limitation can be avoided.

3. Net Applicable Related Party Interest Expense (NARPIE)

NARPIE is interest expense paid to an “applicable related party” of a debtor Japanese corporation after netting

Japan

13 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

of interest income earned by the debtor Japanese corporation, which is allocated in proportion to gross applicable related party interest expense over total interest expense. Interest expense includes (1) Interest on loan and debenture, (2)Original issue discount, (3) Interest portion included in leasing fee, (4) Debt guarantee fee, (5)Debt securities lending fee, (6) Repurchase price in excess of selling price in a Repo transaction, (7) Any other interest in kind and so on.

4. Applicable Related PartyRegardless of a foreign or domestic related party (a corporation and/or an individual), an applicable related party will include the related party of a debtor Japanese corporation, of which interest income is not subject to Japanese corporation tax or Japanese individual income tax on “the net taxation basis”. Since interest income received by a foreign related party without a permanent establishment (referred to as “PE” ) is not subject to Japanese corporation tax or Japanese individual income tax on the net taxation basis, an applicable related party shall be the foreign related party without a PE in Japan.

The foreign related party is a foreign corporation or a non-resident individual who has any of the following relationships with a debtor Japanese corporation:

1. Relationship of parent/subsidiary corporation through direct and/or indirect ownership of 50% or more;

2. Relationship of brother/sister corporation through direct and/or indirect ownership of 50% or more;

3. An individual shareholder who owns directly and/or indirectly 50% or more;

4. In-substance relationship, where a majority of officers or a representative director of a creditor foreign corpo-ration holds concurrent similar positions with that of a debtor Japanese corporation, where a debtor Japa-nese corporation has been doing most of its business

with a foreign creditor, or where most of the operating funds for a debtor Japanese corporation is financed by a loan from a foreign creditor;

5. A third party creditor who provides funding to a debtor Japanese corporation by way of a back-to-back loan with a guarantee provided by, or a Repo transaction of debt securities borrowed from a related party of the debtor Japanese corporation.

5. De Minimus RuleA debtor Japanese corporation shall be exempted from application of the ESR, if either of following two conditions are fulfilled:

1. The amount of NARPIE is not more than 10million yen or;

2. The ratio of gross applicable related party interest ex-pense to total interest expense is not more than 50%.

Contributed byGYOSEI Certified Tax & Accountants’ Co.

Korea

Korea

14 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

Revised Korean Tax Law for 2013 The following is the selection of revised Korean tax law for 2013 which would have an influence on international tax matters.

1. Taxation of Passive Foreign Partners by Income Sources (Special Tax Treatment Control Law of Korea, Article 100.18)

Before amendment, all income allocated from domestic private equity funds (“PEF”) to non-residents and foreign companies who are passive foreign partners of the PEF were classified as dividends. However, under the amended law, if a passive foreign partner of PEF is a pension fund or certain other type of entity incorporated in a country that has a tax treaty with Korea and the type of income is exempt from taxation in such a country (the “Qualified Passive Partner”- “QPP”), then income allocated to the QPP from the PEF will be classified in accordance with the sources of such income for Korean tax purposes and taxed as if the QPP directly owns part of the assets held by the PEF.Therefore, income allocated to the QPP out of capital gains earned by the PEF from a transfer of securities may not be taxable in Korea if a relevant tax treaty between Korea and the country in which the QPP resides, exempts the QPP from Korean taxation on such capital gains. The amended provision will be applicable from the fiscal year beginning on or after 1 Jan, 2013.

2. Tax Benefits for Certain Foreign-Currency Long-term Time Deposits Held by Non-residents (Special Tax Treatment Control Law of Korea, Article 21.2)

In order to promote a long-term and stable influx of foreign currency, interest income earned by non-residents from long-term foreign currency accounts (for those with a maturity of one year or longer) is exempt from corporate income tax or personal income tax, whichever is applicable. This exemption will be available for qualified deposits opened on or before 31 Dec, 2015.The amended provision will be applicable to qualified deposits opened on or after 1 Jan, 2013.

3. Extension and Amendment of Special Income Tax Rates for Foreign Employees (Special Tax Treatment Control Law of Korea, Article 18.2)

In an effort to attract and stabilize a strong workforce from foreign countries and to spur foreign investment, the flat tax rate applicable to foreign workers has been extended for 2 years to 31 Dec, 2014. However, to reduce the inequality in the tax burden between domestic and foreign employees, the flat tax rate has been increased from 15% to 17% for the income earned on or after 1 Jan, 2013.

4. Revision of the Provisions Concerning the Reporting of Overseas Financial Account of Korean Residents and Domestic Companies (International Tax Coordination Law of Korea, Article 34 and 34.2)

The former law mandated that overseas financial accounts (cash and securities) held by Korean residents and domestic companies exceeding KRW 1 billion were subject to reporting requirements. However, under the amended law, all types of financial assets including derivatives, etc. opened at overseas financial institutions, are subject to the

Korea

15 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

reporting requirements.

Previously, in the case when any single day’s total value of such accounts exceeds KRW 1 billion, the highest deposit balance during the year were required to report. Now, the reporting obligation will be triggered in the case when the sum of each month end’s balance of such account exceeds KRW 1 billion. 5. Clarification of Tax Treatment of Payment

for the Use of Equipment (International Tax Coordination Law of Korea, Article 29)

Before After

Income classification and withholding tax rate with regard to payments for the use of industrial, commercial or scientific equipment

■ Income Tax Law (ITL), Corporate Income Tax Law (CITL)• Treated as rental

income• Tax rate: 2%

■ Under a majority of tax treaties (with 63 coun-tries)• Treated as royalties• Tax treaties take pre

when it comes to in-come classification.

• Tax rate: limited tax rate of 0 ~ 15%

• ITL, CITL: 20%It is unclear how to tax pay-ments for the use of such equipment which are classi-fied as royalties (2% or limited tax rate)

Withholding tax rate ap-plicable to payment for equipment usage will be specified.

Payments for the use of equipment classified as roy-alties under tax treaties shall be subject to limited tax rate for royalties (0~15%)

Same as left

6. Expanded Special Treatment on Partnership Taxation (Special Tax Treatment Control Law of Korea, Article 100.15)

Foreign organizations which are similar to domestic entities and which meet the requirements to be set out by the Enforcement Decree may elect for partnership taxation regime. This change is being made to create parity between domestic and foreign businesses and attract various forms of foreign investment. This change will be effective from the tax year beginning on or after 1 Jan, 2014.

Questions regarding the above may be addressed to Mr. Young Chang Kwon, CPA, of Nexia Samduk at [email protected].

Contributed by Nexia Samduk

Malaysia

Malaysia

16 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

2. Public Ruling 2/2012: Foreign Nationals Working in Malaysia – Tax Treaty Relief

This Ruling explains the application of tax treaty relief to foreign nationals from treaty countries seconded to Malaysia by their employers that are not resident in Malaysia.

The general rule is that income from employment derived by an individual who is a resident of a contracting country may be taxed in the other country if the employment is exercised in that other country. However, where the employment in the other country is for short term purposes and for the facilitation of movement of qualified personnel, exemption of tax is granted by the country of source where the employment is exercised if all the following three conditions are satisfied (these conditions may vary from one Double Taxation Agreement to another):

■ The foreign national is present in Malaysia for periods not exceeding 183 days in the fiscal/calendar year concerned;

■ Payer of the remuneration of the foreign national working in Malaysia is not a resident of Malaysia; and

■ Remuneration of the foreign national is not borne by a Permanent Establishment (PE) in Malaysia.

3. Public Ruling 3/2012: Appeal against an Assessment

This Ruling explains the procedure in respect of appeals against assessments made or deemed made and the requirements to be complied with when making appeals.

A person who is dissatisfied with an assessment that has been made, or deemed made, on him by the DGIR has a right to appeal against that assessment. The appeal must be done by submitting Form Q not later than 30 days after the notice of assessment is received or the deemed notice of assessment is deemed to have been received, stating the grounds of appeal. If an appeal cannot be submitted within the specified period, application for extension of time for appeal could be made through Form N.

Public Rulings Issued in 2012The Inland Revenue Board of Malaysia (IRBM) issues Public Rulings for the purpose providing guidance for the public and officers of IRBM. It sets out the interpretation of the Director General of Inland Revenue (DGIR) in respect of the particular tax law, and the policy and procedure that are to be applied. A Ruling may be withdrawn, either wholly or in part, by notice of withdrawal or by publication of a new ruling which is inconsistent with it. The following is an overview of Public Rulings issued in 2012.

1. Public Ruling 1/2012: Compensation for Loss of Employment

This Ruling explains the characterisation of lump sum payments received by employees upon the termination of their employment as compensation for loss of employment and the tax treatment of compensation for loss of employment.

Pursuant to paragraph 13(1)(e) of the Income Tax Act 1967 (ITA), compensation for loss of employment is specifically included in the gross income from an employment. For the purposes of income tax exemption, the characteristics and nature of termination payments prevail over form and labelling of such payments. A payment (other than a payment by a controlled company to a director of the company who is not a full-time service director) made by an employer to an employee of his as compensation for loss of employment or in consideration of any covenant entered into by the employee restricting his right to take up other employment of the same or similar kind is given exemption pursuant to paragraph 15 of Schedule 6 of the ITA:

■ full exemption if loss of employment is due to ill health; ■ exemption of RM10,000 for each completed year of

service if the employment is with the same employer or with companies in the same group.

Malaysia

17 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

4. Public Ruling 4/2012: Deduction for Loss of Cash and Treatment of Recoveries

This Ruling (supersedes Public Ruling 5/2005 dated 14 November 2005) explains the deductibility of loss of cash in the course of business caused by theft, defalcation or embezzlement, and the income tax treatment of recoveries in respect of the loss of cash which has been given a tax deduction in an earlier year.

Loss of cash caused by theft, defalcation or embezzlement in the course of business may be allowed as a deduction in computing the adjusted income under the following circumstances:

1. Theft or embezzlement by third party if:a. banking of cash takings is a necessary part of

the operations of the business, any any loss of cash caused by theft or robbery while in transit to the bank is allowable.

b. an agent who is assigned to collect the cash embezzles the cash, the loss is allowable as a deduction.

c. Claims for loss of cash should be supported by sufficient evidence. Loss of cash that has been allowed in computing the adjusted income has to be taken as gross income of a business when such recoveries are obtained. Recovery of cash is gross income from a business for the basis period for a year of assessment in which it is receivable or deemed to have been received. The date the cash is actually received is irrelevant.

2. Theft or embezzlement by employee is allowable as it arises directly from the necessity of delegating certain duties of the business to employee.

Recovery of cash (through insurance, legal action etc.) is gross income from a business for the basis period for a YA in which it is receivable or deemed to have been received. The date the cash is actually received is irrelevant.

Income Tax (Transfer Pricing) Rules 2012

The Income Tax (Transfer Pricing) Rules 2012 was issued on 7 May 2012 under the powers conferred by paragraph 154(1)(b) of the ITA and deemed to have come into operation on 1 January 2009.

These Rules shall apply to controlled transactions for the acquisition or supply of property or services. A person shall determine and apply the arm’s length price for the acquisition or supply of property or services in accordance with the method and manner provided in these Rules.

A person shall apply the traditional transaction method (i.e. comparable uncontrolled price method, resale price

5. Public Ruling 5/2012: Clubs, Associations or Similar Institutions

This Ruling explains the taxation of clubs, associations or similar institutions which are established and controlled by its members.

Clubs, associations or similar institutions are formed not for commercial purposes but for social, recreational, sports, arts, science, literature or other purposes for the interest and benefit of their members. However, the activities of some clubs, associations or similar institutions are trade dealings which are run for a profit that is subject to tax as business profits. If a club, association or similar institution is meant for the benefit of members only, any income arising from mutual dealings with the members is not subject to tax. Any income received from activities or transactions with non-members are taxable income.

Capital expenditure incurred on assets used in business transactions with non-members to derive income from non-members only will qualify for capital allowances.

This Ruling also provides the basis to determine the portion of gift of money to be deducted from the aggregate income relating to transactions with non-members.

18 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

method or cost plus method) to determine the arm’s length price of a controlled transaction. Where the traditional method cannot be reliably applied or cannot be applied at all, the transactional profit method (i.e. profit split method or transactional net margin method) shall be applied.

It is also specifically stated that any person in a controlled transaction who provides or receives financial assistances (e.g. loans, interest bearing trade credit, advances, provision of security or guarantee etc.), directly or indirectly, to or from another person with or without consideration shall determine the arm’s length interest rate for such assistance.

Malaysian Advance Pricing Arrangement (APA) Guidelines 2012

An APA represents an arrangement between a taxpayer and the DGIR that establishes the transfer pricing methodologies to ascertain the prospective arm’s length transfer prices of specified related party transactions between the taxpayer and its foreign affiliates over a specified period of time, under specified terms and conditions. Generally, an APA will cover a minimum period of three to five years maximum.

Where the DGIR and the taxpayer have entered into a Unilateral or Bilateral/Multilateral APA, the arrangement shall, during the covered period, constitute a binding undertaking on the parties to the arrangement that the transfer price ascertained is determined in accordance with the arrangement.

Budget 2012 Proposals That Come Into Effect From 20131. Compensation for late refund of income tax

by the Inland Revenue BoardPresently, a late payment penalty of 10% will be imposed by the DGIR on the balance of tax not paid after the due date for submission of the income tax return. If the tax and penalty imposed is not paid within 60 days from the due date, a further penalty of 5% will be imposed on the outstanding amount. However, where a refund of income tax is due to a taxpayer, the taxpayer is not eligible for any compensation for the late refund of income tax by the DG. Furthermore, there is no specific time frame within which a tax refund will be paid to the taxpayer.

With effect from 2013, a taxpayer who has submitted his tax returns within the stipulated time and is due for a tax refund be paid a compensation of 2% per annum on the amount of tax refunded late by the DGIR. The compensa-tion of 2% is payable where the amount refunded is made after:

a. 90 days from the due date for electronic filing; orb. 120 days from the due date for manual filing.

However, the DGIR may require the return of the compen-sation paid to the taxpayer where:

a. the amount is wrongly paid to the taxpayer; orb. the amount ought not to be paid because the

taxpayer has submitted an incorrect return or has provided incorrect information.

The compensation will not be payable where the tax return is not submitted by the due date, or where the person ap-peals against the assessment, or where it is a tax repay-able case in which the tax set-off under Section 110 is in excess of the tax payable.

19 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

Singapore

A Roundup for Singapore Major Corporate Tax Changes for Budget 2012 The Minister for Finance, Mr Tharman Shanmugaratnam, delivered the Budget Statement for the Financial Year 2012 (“Budget 2012”) on 17 February 2012. Below are the significant corporate tax changes announced in Budget 2012.

Enhancements to Productivity and Innovation Credit SchemeUnder the Productivity and Innovation Credit Scheme, businesses are entitled to enhanced deductions or

allowances of 400% of the amount of expenditure incurred (subject to an annual ceiling) on each of six categories of qualifying activities, namely:

■ Expenditure on research and development; ■ Expenditure on the registration of intellectual property; ■ Expenditure on the acquisition of intellectual property; ■ Expenditure on design activities; ■ Expenditure on the automation of processes; and ■ Expenditure on the training of employees.

Businesses can also elect to convert tax deductions or allowances into a cash grant. For the years of assessment 2013 to 2015, the amount of the maximum cash grant is increased to S$60,000 for each year of assessment (from S$30,000). The cash grant may also be claimed on a quarterly basis from July 2012 to assist the cash flow of small and medium enterprises. Enhancements were also made to the scope of qualifying expenditure on research and development (in relation to expenditure on research and development cost sharing agreements and the development of software), the training of employees (in relation to the in-house training of employees and the training of agents) and qualifying automation equipment acquired on hire purchase terms. Enhancements to the Renovation and Refurbishment (R&R) deduction schemeBusinesses that renovate or refurbish their business premises from 16 February 2008 to 15 February 2013 currently qualify for a deduction of the R&R costs up to S$150,000 for each 3-year period. The deduction of qualifying R&R costs is provided on a straight line basis over the 3-year period. Certain R&R costs are not deductible, such as designer fees and fine art. Any unutilised R&R costs deduction cannot be transferred under the group relief system.

Singapore

3. Time bar for tax audit reduced from 6 years to 5 years

Under the Tax Audit Framework issued by the DG in Janu-ary 2009, a tax audit will not be carried out to examine records pertaining to the years of assessment which are time barred. The time bar period is provided for under Section 91(1) of the ITA which the DGIR may, within 6 years after the expiration of a year of assessment, make an as-sessment for additional assessment in respect of a person.

The time bar for tax audits is reduced from 6 years to 5 years with effect from YA 2013.

Contributed by: Nexia SSY

20 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

From the year of assessment 2013, R&R costs deduction shall become a permanent feature of the Singapore tax system, with the deduction cap to be raised to S$300,000 for every 3-year period. Any unutilised R&R costs deduction can be transferred under the group relief system from YA 2013.

All other terms and conditions of the scheme shall remain, e.g. the R&R should not involve structural changes to the premises which require prior-approval from the Commissioner of Building Control.

Enhancements to Merger and Acquisition SchemeThe Merger and Acquisition Scheme provides an allowance for the cost incurred by a Singapore company (whose ultimate holding company, if any, must also be a Singapore company) in acquiring a target company (subject to conditions). Stamp duty relief is also provided in respect of the stamp duty payable on the acquisition of the shares in the target company (subject to conditions). In Budget 2012, the following enhancements are made to the Merger and Acquisition Scheme:

■ An allowance may be claimed for transaction costs, including professional and legal fees. The amount of allowance available is 200% of the relevant expenditure incurred, up to a maximum of S$100,000 of expenditure per year.

■ Conditions that have to be satisfied by the acquiring company (or a subsidiary thereof) or the target company may now be satisfied by any subsidiary (including wholly-owned indirect subsidiaries) of the acquiring company or the target company (as the case may be).

■ The ultimate holding company of an acquiring company need not be a Singapore company if

approval is obtained from the Economic Development Board (“EDB”) under a headquarters tax incentive administered by the EDB.

Clarity on tax treatment of gains from the disposal of equityCurrently, whether gains made on the disposal of an asset by a taxpayer are taxable depends on whether such gains are considered to be income or capital in nature. This is largely a factual analysis, which depends on the specific circumstances of the taxpayer, the circumstances of the acquisition of the asset and the circumstances of the disposal of the asset.

Based on the latest IRAS guideline dated 30 May 2012, the gains derived from the disposal of ordinary shares in an investee company during the period 1 June 2012 to 31 May 2017 (both dates inclusive) is not taxable if immediately prior to the date of the share disposal, the divesting company had held at least 20% of the ordinary shares in the investee company for a continuous period of at least 24 months. This rule does not apply to a divesting company whose gains or profits from the disposal of shares are included as part of its income based on the provisions of section 26 of the Income Tax Act, Chapter 134 of Singapore; or disposal of shares in an unlisted investee company that is in the business of trading or holding Singapore immovable properties (other than the business of property development).

Contributed by: Nexia TS

21 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

Tax Changes in 2012In line with the tax reform plan for the 10-year period (2011-2020) and the short-term plan of 5-years from 2011 to 2015, the Vietnamese Government made some important changes to the country’s tax regulations in late 2011 and the beginning of 2012. In particular, it has issued some key Decrees and Circulars that change the key taxes of Vietnam with an objective of maintaining the tax revenues during 2011-2015 at a level of 23-24% of the country’s GDP. In the subsequent five years (2016-20), tax rates will be lowered on goods or services in order to encourage competition and capital accumulation.

Prior to a brief discussion on the changes, you may wish to be aware of the Vietnamese tax regulations hierarchy. In Vietnam, the highest level is the National Assembly which issues the Laws, Ordinances and Resolutions. The Government and the Prime Minister issue respective Decrees and Decisions providing guidance for implementation of those Laws, Ordinances and Resolutions. The Ministry of Finance, at the implementation stage, will accordingly issue Circulars for detailed guidance for direct implementation. Besides the above backbone tax regulations, Official Letters/Rulings will also act as an integral part of the overall tax system in Vietnam.

In accordance with the reform plan, on 27 December 2011, the Government issued Decree 121/2011/ND-CP changing and supplementing some articles of Decree 123/2008/ND-CP on Value Added Tax (VAT) and Decree 122/2011/ND-CP supplementing and amending Decree 124/2008/ND-CP dated 11 December 2008 on Corporate Income Tax (“CIT”) (both with effect from 1 March 2012). Accordingly, respective Circular 06/2012/TT-BTC on VAT was issued on 11 January 2012 and Circular 123/TT-BTC/2012 on CIT

Vietnamwas issued on 27 July 2012. There is also a new Circular 60/2012/TT-BTC issued by the Ministry of Finance on 12 April 2012 on the Foreign Contractor Withholding Tax (“FCWT”) that provides guidance on implementation of CIT and VAT for foreign organizations and individuals operating in and/or having income from Vietnam.

Among others changes, the below are considered to have big impacts on the current tax systems of Vietnam:

■ Allowance of full credit of input VAT for damaged goods. It is notable that under the previous regulations, this input VAT could not be claimed as creditable and became a cost for enterprises;

■ A deduction for CIT purposes of life insurance premiums paid for employees provided that required supporting documents are sufficient. Previously, this expense was not deductible and was treated as other income of the respective individual for Personal Income Tax (“PIT”) purposes;

■ Commission paid to agents of multi-level marketing companies is confirmed not to be subject to a cap of 10% or 15% applicable to advertising and promotion expenses;

■ Reversal of provisions for inventory devaluation, financial investment losses, bad debts, warranty and salary shall NOT be included in “other income”. It is noteworthy that income from disposals of by-products and scrap sales is to be treated as “other income” and subject to CIT at the standard rate of 25%;

■ Income from transferring Certified Emission Reductions (CERs) within one year from the date of issuance will not be taxable;

■ Taxable income to be declared with respect to the revaluation of land contributed to a joint venture over a 10-year period;

■ A reduction in the rate of withholding tax (reduced from 10% to 5%) on interest payments made from Vietnam to offshore lenders while VAT is enforceable on interest from loan agreements between non-credit institutions; and

Vietnam

22 TAX Link - Asia Pacific - Updates 2012/2013 - Issue 1

■ Moreover, a schedule of cases was made in which input VAT of expenses paid by authorized parties can be claimed by authorizing parties and typical cases which constitute payment via banking channels.

Starting from 2011, given the fact that relevant regulations were initially issued back in 2006 and recently amended for further enforcement in 2010, Transfer Pricing (“TP”) is now a hot issue in Vietnam. The current regulations required enterprises to submit an annual TP Disclosure Form (known as Form 01) and to maintain the “contemporaneous” TP documentation to support the basis of arm-length pricing between related parties. As we note in most of the tax audits performed by the tax authorities in Vietnam, TP was mostly focused on those foreign direct invested enterprises who appear to have significant volume of related-party transactions; or are under suspicion of TP manipulation, loss making, or have significant amount of tax due, or have not been audited or inspected, or are entitled to tax incentives.

Besides the above changes , the Law on Environmental Taxation took effect from 1 January 2012 to encourage enterprises and citizens to change their consumption behaviors towards environmental protection. Taxable objects will be added and tax rates adjusted to restrict polluting uses.

Contributed by: Nexia ACPA

USA

Nexia International does not accept any responsibility for the commission of any act, or omission to act by, or the liabilities of, any of its Members. Nexia International does not accept liability for any loss arising from any action taken, or omission, on the basis of this publication. Professional advice should be obtained before acting or refraining from acting on the contents of this publication. Membership of Nexia International, or associated umbrella organisations, does not constitute any partnership between Members, and Members do not accept any responsibility for the commission of any act, or omission to act by, or the liabilities of, other Members.

Nexia International is the trading name of Nexia International Limited, a company registered in the Isle of Man.Company registration number: 53513C. Registered office: 2nd floor, Sixty Circular Road, Douglas, Isle of Man, IM1 1SA.

Tax Link serves two purposes. It provides a forum for updating our clients and contacts on developments in tax legislation around the globe and for highlighting the range of tax services available from Nexia Member firms. In addition, Tax Link serves as a notice board to inform member firms on the activities of the various tax committees and focus groups within the Nexia network.

This update was edited by Stephen Rogers, Taxation Consulting Partner at Nexia Australia. If you require further information or would like to contribute articles for future editions, please contact:

Stephen Rogers [email protected]

www.nexia.com