tax deduction at source recent developments - icai - recent... · summary of topics •recent cbdt...

TRANSCRIPT

Gautam Nayak

Chartered Accountant

Tax Deduction at Source – Recent Developments Full Day Seminar on Direct Taxes, Kolkata

10th May, 2014

1 CNK

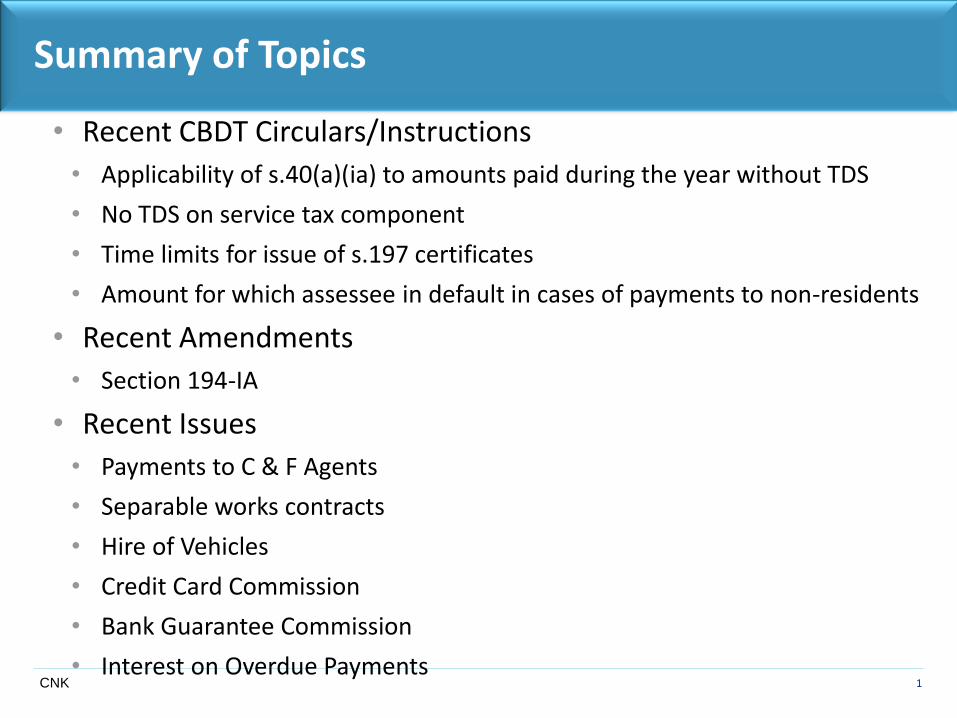

Summary of Topics

• Recent CBDT Circulars/Instructions

• Applicability of s.40(a)(ia) to amounts paid during the year without TDS

• No TDS on service tax component

• Time limits for issue of s.197 certificates

• Amount for which assessee in default in cases of payments to non-residents

• Recent Amendments

• Section 194-IA

• Recent Issues

• Payments to C & F Agents

• Separable works contracts

• Hire of Vehicles

• Credit Card Commission

• Bank Guarantee Commission

• Interest on Overdue Payments

2 CNK

Summary of Topics

• Recent Issues…

• Lease Premium

• Reimbursement of Expenses

• Surcharge & Education Cess on DTAA rates

• Grossing up for payments to non-residents under section 206AA

• Credit of TDS

• Interest u/s 201(1A)

• Fees for late filing u/s 234E

3 CNK

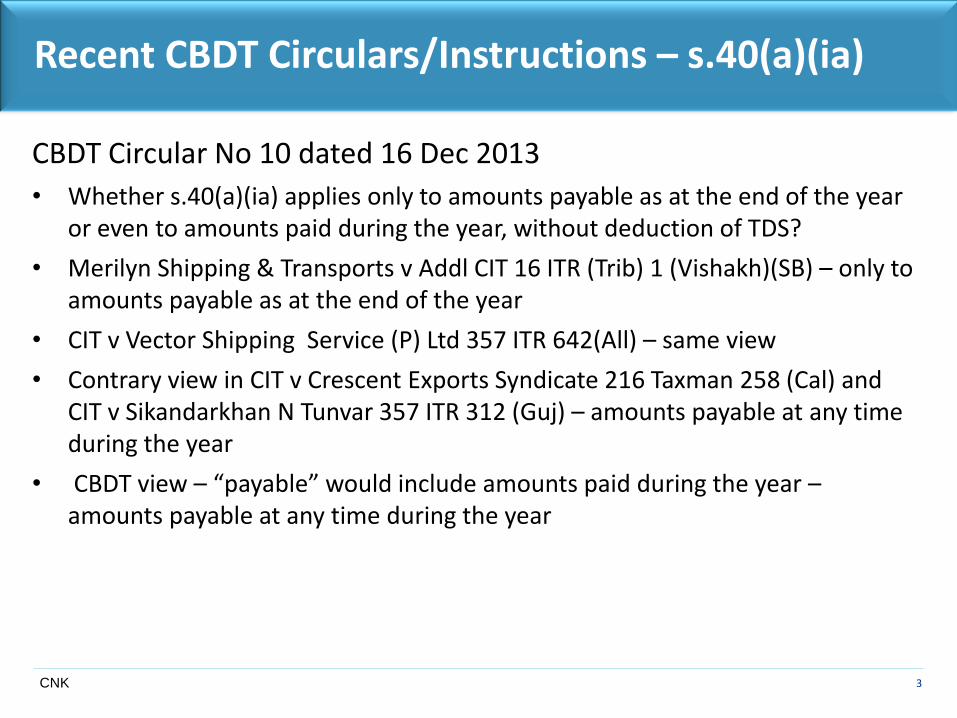

Recent CBDT Circulars/Instructions – s.40(a)(ia)

CBDT Circular No 10 dated 16 Dec 2013

• Whether s.40(a)(ia) applies only to amounts payable as at the end of the year or even to amounts paid during the year, without deduction of TDS?

• Merilyn Shipping & Transports v Addl CIT 16 ITR (Trib) 1 (Vishakh)(SB) – only to amounts payable as at the end of the year

• CIT v Vector Shipping Service (P) Ltd 357 ITR 642(All) – same view

• Contrary view in CIT v Crescent Exports Syndicate 216 Taxman 258 (Cal) and CIT v Sikandarkhan N Tunvar 357 ITR 312 (Guj) – amounts payable at any time during the year

• CBDT view – “payable” would include amounts paid during the year – amounts payable at any time during the year

4 CNK

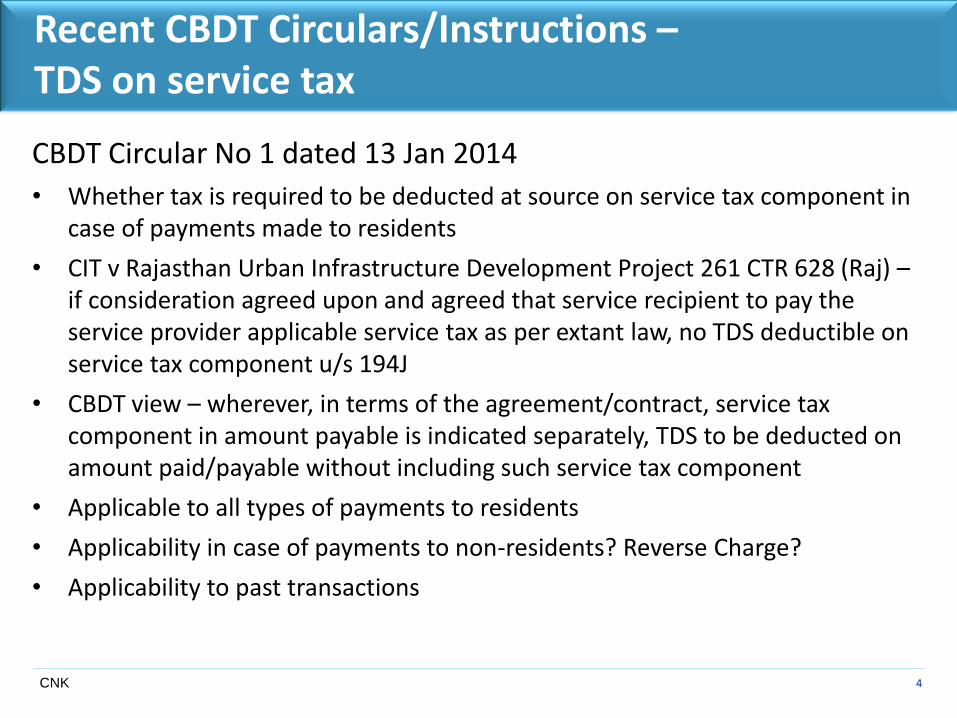

Recent CBDT Circulars/Instructions – TDS on service tax

CBDT Circular No 1 dated 13 Jan 2014

• Whether tax is required to be deducted at source on service tax component in case of payments made to residents

• CIT v Rajasthan Urban Infrastructure Development Project 261 CTR 628 (Raj) – if consideration agreed upon and agreed that service recipient to pay the service provider applicable service tax as per extant law, no TDS deductible on service tax component u/s 194J

• CBDT view – wherever, in terms of the agreement/contract, service tax component in amount payable is indicated separately, TDS to be deducted on amount paid/payable without including such service tax component

• Applicable to all types of payments to residents

• Applicability in case of payments to non-residents? Reverse Charge?

• Applicability to past transactions

5 CNK

Recent CBDT Circulars/Instructions – S.197 certificates

CBDT Instruction No 1 dated 15 Jan 2014

• Time Limit for issue of certificates u/s.197 for nil or lower deduction of tax at source

• Citizens Charter – time line for a decision on application for no deduction of tax or deduction of tax at lower rate is one month

• Instances brought to notice of CBDT about considerable delay in issuing certificates by AOs

• Commitment to taxpayers as per Citizens Charter must be scrupulously adhered to

• All applications must be disposed of within stipulated time frame

6 CNK

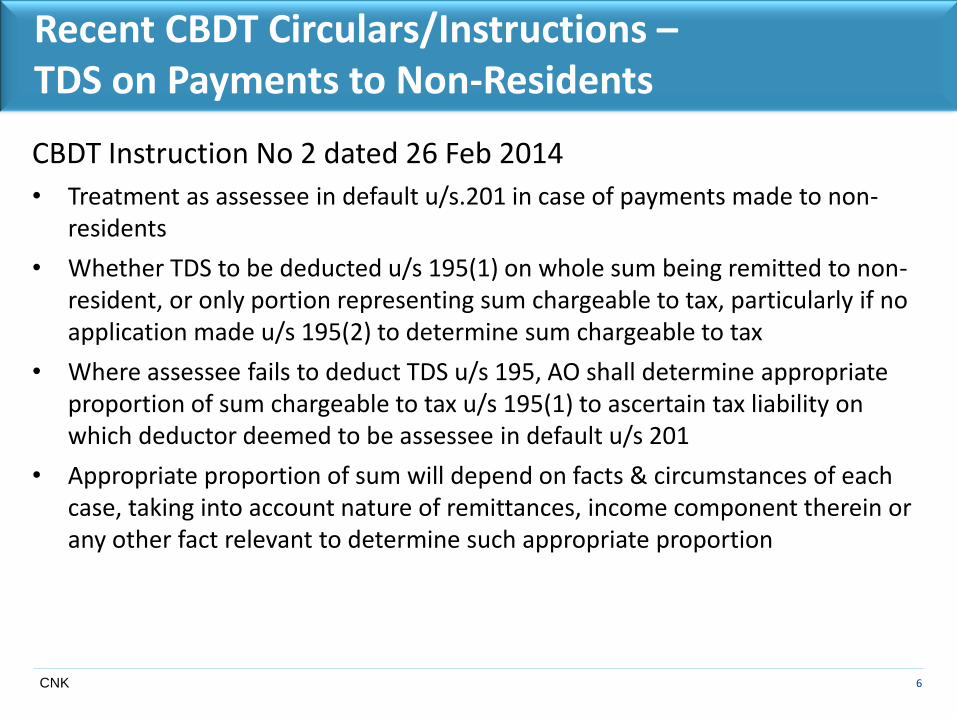

Recent CBDT Circulars/Instructions – TDS on Payments to Non-Residents

CBDT Instruction No 2 dated 26 Feb 2014

• Treatment as assessee in default u/s.201 in case of payments made to non-residents

• Whether TDS to be deducted u/s 195(1) on whole sum being remitted to non-resident, or only portion representing sum chargeable to tax, particularly if no application made u/s 195(2) to determine sum chargeable to tax

• Where assessee fails to deduct TDS u/s 195, AO shall determine appropriate proportion of sum chargeable to tax u/s 195(1) to ascertain tax liability on which deductor deemed to be assessee in default u/s 201

• Appropriate proportion of sum will depend on facts & circumstances of each case, taking into account nature of remittances, income component therein or any other fact relevant to determine such appropriate proportion

7 CNK

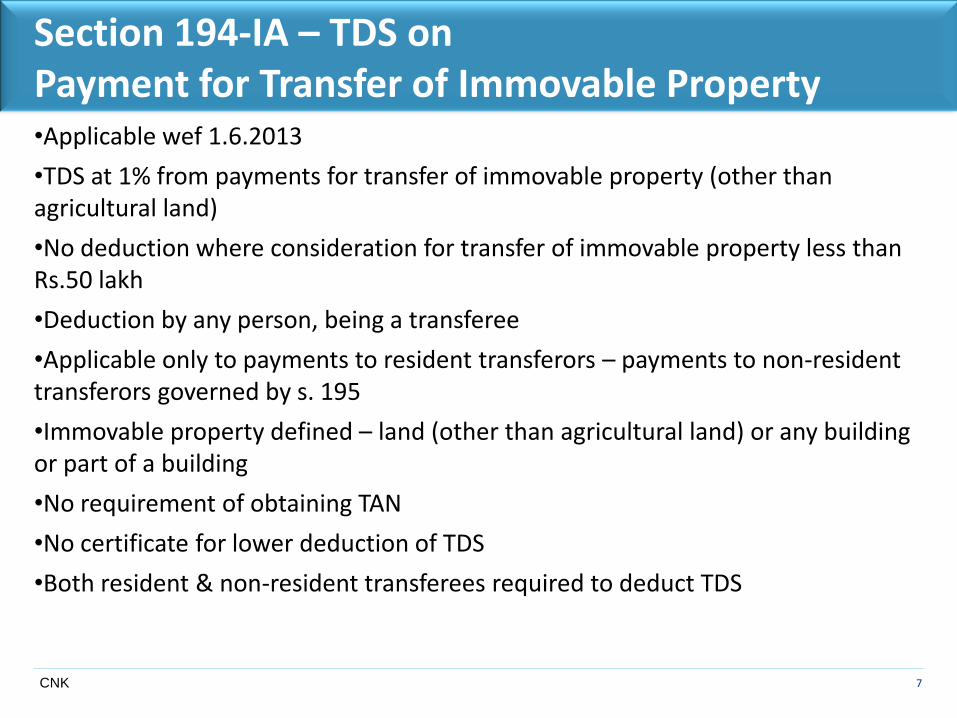

Section 194-IA – TDS on Payment for Transfer of Immovable Property •Applicable wef 1.6.2013

•TDS at 1% from payments for transfer of immovable property (other than agricultural land)

•No deduction where consideration for transfer of immovable property less than Rs.50 lakh

•Deduction by any person, being a transferee

•Applicable only to payments to resident transferors – payments to non-resident transferors governed by s. 195

•Immovable property defined – land (other than agricultural land) or any building or part of a building

•No requirement of obtaining TAN

•No certificate for lower deduction of TDS

•Both resident & non-resident transferees required to deduct TDS

8 CNK

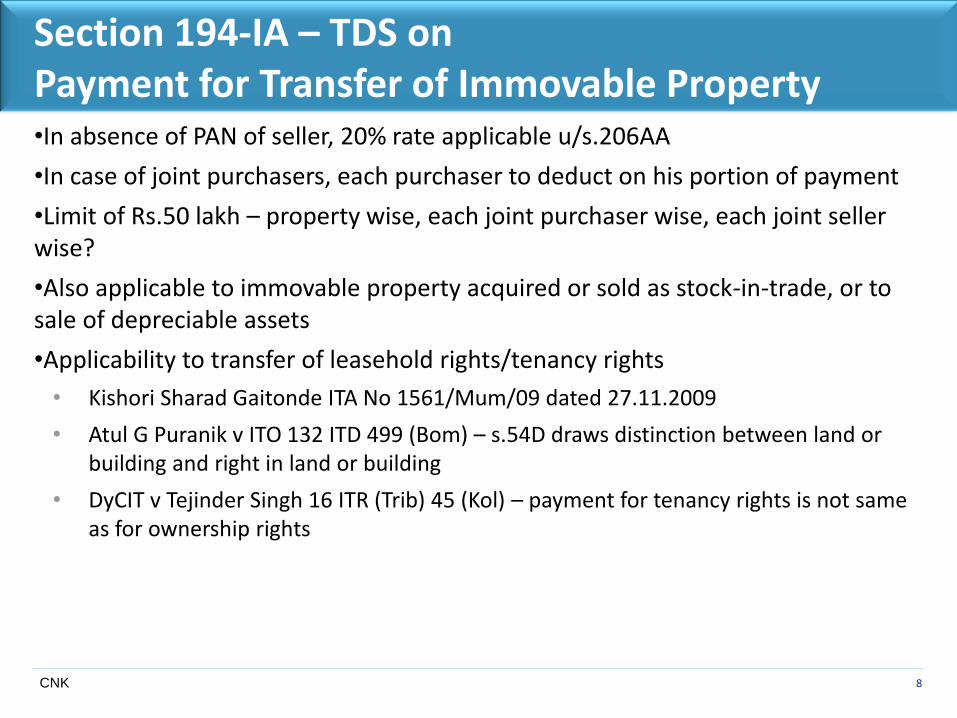

Section 194-IA – TDS on Payment for Transfer of Immovable Property •In absence of PAN of seller, 20% rate applicable u/s.206AA

•In case of joint purchasers, each purchaser to deduct on his portion of payment

•Limit of Rs.50 lakh – property wise, each joint purchaser wise, each joint seller wise?

•Also applicable to immovable property acquired or sold as stock-in-trade, or to sale of depreciable assets

•Applicability to transfer of leasehold rights/tenancy rights

• Kishori Sharad Gaitonde ITA No 1561/Mum/09 dated 27.11.2009

• Atul G Puranik v ITO 132 ITD 499 (Bom) – s.54D draws distinction between land or building and right in land or building

• DyCIT v Tejinder Singh 16 ITR (Trib) 45 (Kol) – payment for tenancy rights is not same as for ownership rights

9 CNK

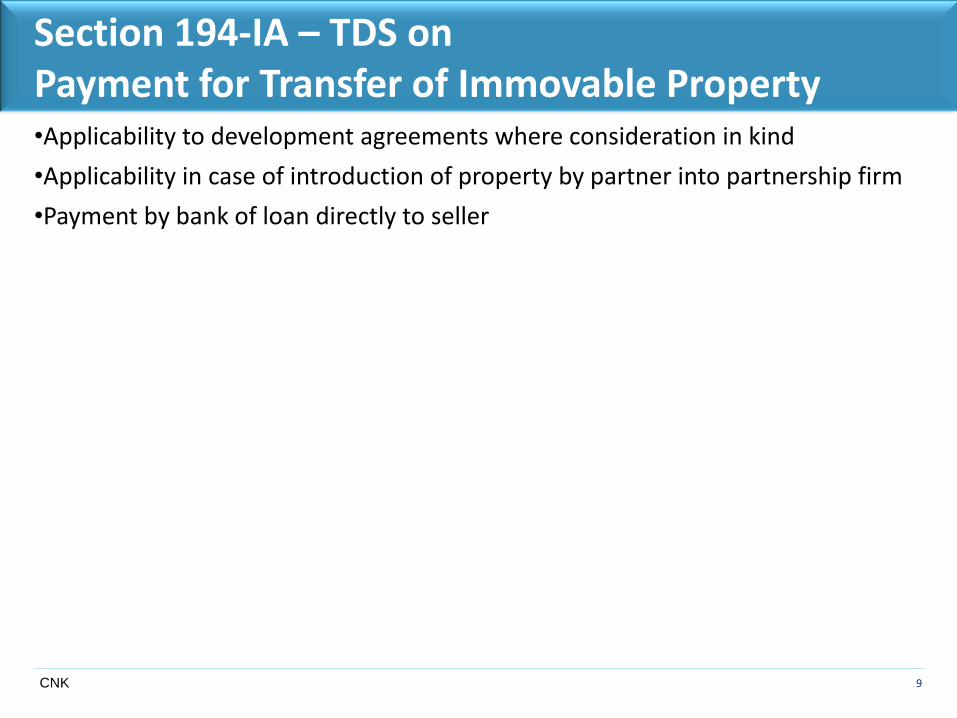

Section 194-IA – TDS on Payment for Transfer of Immovable Property •Applicability to development agreements where consideration in kind

•Applicability in case of introduction of property by partner into partnership firm

•Payment by bank of loan directly to seller

10 CNK

Recent Issues

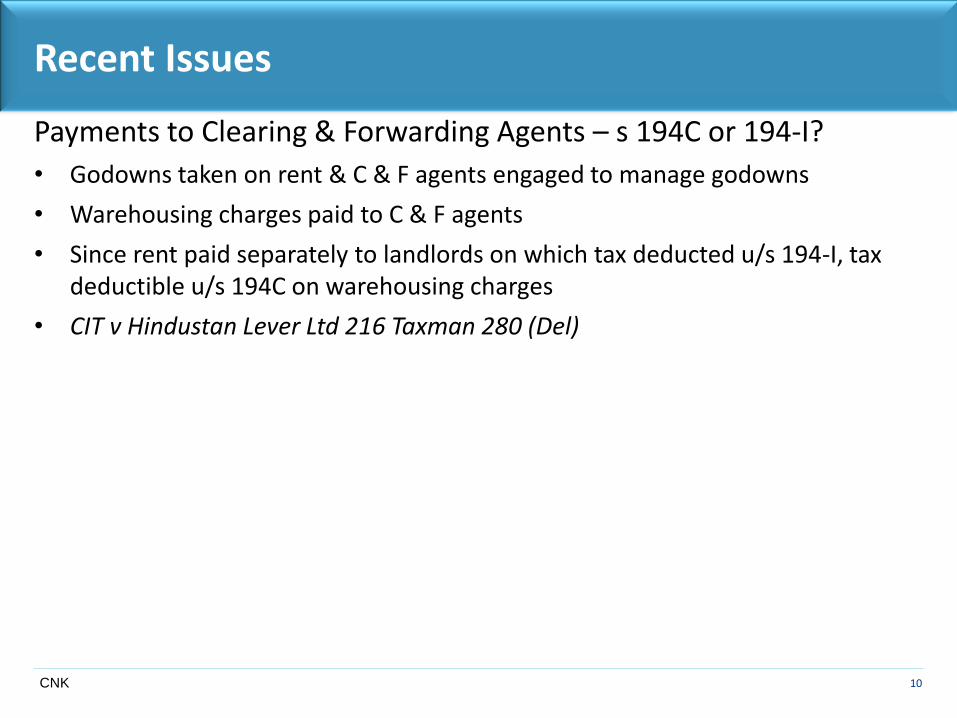

Payments to Clearing & Forwarding Agents – s 194C or 194-I?

• Godowns taken on rent & C & F agents engaged to manage godowns

• Warehousing charges paid to C & F agents

• Since rent paid separately to landlords on which tax deducted u/s 194-I, tax deductible u/s 194C on warehousing charges

• CIT v Hindustan Lever Ltd 216 Taxman 280 (Del)

11 CNK

Recent Issues

Works Contracts – TDS on Gross Payment or only on Labour Charges?

• Contract for repairing of transformers

• Contract divided into various components – supply of coil, transformer oil, other items and labour charges

• TDS attracted only to labour charges and not to supply of materials

• CIT v Executive Engineer (Electricity Stores), Distribution Division 94 DTR 167 (All)

12 CNK

Recent Issues

Hire of Vehicles for Transportation – s 194C or 194-I?

• Buses hired for transportation of staff or Trucks hired for transportation of goods

• Manned by contractor’s employees

• All expenses to be borne by transporter

• Payment on per trip basis

• Transportation – s.194C ?

• Hire of Movable Property – s.194-I ?

• Royalty – s.194J ?

13 CNK

Recent Issues

Hire of Vehicles for Transportation – s 194C or 194-I?

• CIT vs. Poompuhar Shipping Corporation Ltd. 282 ITR 3 (Mad). – Ships hired for transport is not contract of transport

• Poompuhar Shipping v ITO 360 ITR 527 (Mad) – Time charter amounts to royalty, being hire of ships

• CBDT Circular No.558 dated 28.3.1990, 183 ITR (St.) 158

• Great Eastern Shipping Co. Ltd. v. State of Karnataka 136 STC 519 (Kar) – tug with crew given for use by port trust – maintenance by owner – transfer of right to use

• State of AP v. Rashtriya Ispat Nigam Ltd. 126 STC 114 (SC), Rashtriya Ispat Nigam Ltd. v. CTO 77 STC 182 (AP) - delivery of possession to be distinguished from custody – not uncommon to find transferee in possession while transferor has custody

• Domain over & Control of Vehicle – with whom?

14 CNK

Recent Issues

Hire of Vehicles for Transportation – s 194C or 194-I?

• Lotus Valley Education Society v. ACIT 13 ITR (Trib) 61 (Del) – Payment to Bus Operators providing pick up and drop facility to students and staff – s.194C, not s.194-I

• Tata AIG General Insurance Co Ltd v. ITO 43 SOT 215 (Mum) – arrangement for providing cars of particular category for transportation of employees and guests from one place to another – no specific cars earmarked and identified - hire of buses for transport of employees from station to office - s.194C, not s.194-I

• ACIT v. Accenture Services (P) Ltd. 44 SOT 290 (Mum) – agreement with transport service providers for transport of employees – for provision of transport services, and not hire of vehicles – s.194C, not s.194-I

• ACIT v Delhi Public School 24 ITR (Trib) 531 – contract for students transport – per trip on specified routes – transport arrangement & not vehicle hire

15 CNK

Recent Issues

Hire of Vehicles for Transportation – s 194C or 194-I?

• ITO v. Indianoil Corpn. 15 taxmann.com 210 (Del) – transport trucks under contract for transport of petroleum products – s.194C, not s.194-I

• Bharat Electronics Ltd. v. DCIT 20 taxmann.com 3 (Del) – employee transport buses – s.194C, not s.194-I

• CIT v. Reliance Engg. Associates (P) Ltd. 21 taxmann.com 539 (Guj) – contractors for transportation services for goods and passengers by buses, cars, Sumos, utility vans – s.194C, not s.194-I

• Three Star Granites (P) Ltd. v. ACIT 41 taxmann.com 91 (Ker) – vehicles for loading & unloading & transportation of products - payment on hourly use basis – no work other than making available machinery with operator – contract of hire of vehicles, not transportation contract

16 CNK

Recent Issues

Credit Card Commission

• Whether commission covered by s.194H ?

• Merchant establishments pay commission to bank with whom affiliated

• Commission shared by this bank with credit card issuing bank

• Credit card issuing bank recovers amount from customer, deducts its share of commission, pays to merchant’s bank, which deducts its share of commission and pays balance to merchant

• No agency relationship – mere facilitation – akin to normal bank charges

• Dy. CIT v. Vah Magna Retail (P) Ltd. ITA No. 905/Hyd/2011 dated 10th April 2012

• Tata Teleservices Ltd v Dy CIT 140 ITD 451 (Bang)

• ACIT v Jet Airways (India) Ltd 146 ITD 682 (Bom)

17 CNK

Recent Issues

Bank Guarantee Commission

• Whether commission covered by s.194H ?

• Commission or Brokerage – ejusdem generis

• Confined to payments made to agents

• Not applicable to principal to principal transactions

• Kotak Securities Ltd. v. DCIT (ITA No 6657/Mum/11 dated 3.2.2012)

18 CNK

Recent Issues

Interest on Overdue Payments

• Whether covered by s.194A

• Definition of Interest – s.2(28A) – interest payable in any manner in respect of monies borrowed or debt incurred

• CIT v. Visakhapatnam Port Trust 144 ITR (AP) – interest payable on unpaid purchase money – not independent source - DTAA

• CIT v. Vijay Shipbreaking Corpn. 261 ITR 113 (Guj) – unpaid purchase price was debt incurred or debt claim

• Nirma Industries Ltd. v. DCIT 283 ITR 402 (Guj), CIT v. Indo Matsushita Carbon Co Ltd. 286 ITR 201 (Mad), Phatela Cotgin Industries (P) Ltd. v. CIT 303 ITR 411 (P & H) – source of sale proceeds and source of interest is same – in reality, two methods of realising sale consideration (in context of s.80-I)

• ITO v. Parag Mahasukhlal Shah 143 TTJ (Ahd) 606 – dealer in ball bearings – interest on overdue payments – part of unpaid purchase price

19 CNK

Recent Issues

Lease premium

• Whether covered by s.194-I

• Definition of rent – any payment by whatever name called under any lease, sub-lease, tenancy or other agreement or arrangement for the use of any land or building………….

• Premium paid for lease of land – whether rent?

• Krishak Bharati Co-op. Ltd v ACIT 210 Taxman 123 (Del) - CIT v Panbari Tea Co Ltd 57 ITR 422 (SC) referred to

• S.105 of TP Act draws distinction between price paid for transfer of a right to enjoy property (premium) and rent to be paid periodically to lessor

• May be circumstances where parties may camouflage real nature of transaction by using clever phraseology – in some cases, so-called premium is in fact advance rent and in others rent is deferred price

• Not the form but the substance of the transaction that matters

20 CNK

Recent Issues

Lease premium

• Nomenclature used may not be decisive or conclusive but helps the court to ascertain the intention of the parties

• If the premium represents the whole or part of the price of the land it cannot be rent

• Decision is fact dependant – to be discerned from conduct of parties or surrounding circumstances

• Advantage in form of highly depressed or nominal rent would indicate that premium is in nature of advance rent

• Navi Mumbai SEZ (P.) Ltd 147 ITD 261 (Mum)

• Wadhwa & Associates Realtors (P) Ltd 146 ITD 694 (Mum)

• ITO v Indian Newspaper Society 144 ITD 668 (Del)

• Contrary view in Foxconn India Developer (P) Ltd v ITO 53 SOT 213 (Chen)

21 CNK

Recent Issues

Reimbursement of Expenses

• Whether subject to TDS

• Payment made to agent, where agent made payment to advertising agency after deducting TDS – no deduction required on payment to agent where no profit element – CIT v Harbanslal Malhotra & Sons (P) Ltd 217 Taxman 112 (Cal)

• Reimbursement of clearing house agent charges to clearing & forwarding agent, where agent had deducted and deposited TDS – no profit element in payment to agent – CIT v Gujarat Narmada Valley Fertilizers Co Ltd 217 Taxman 114 (Guj)

• Ship management company paid salaries to employees of shipping company – reimbursement by shipping company to ship management company at actuals – no TDS required – CIT v Vector Shipping Services (P) Ltd 357 ITR 642(All)

22 CNK

Recent Issues

DTAA Rates

• Whether inclusive of surcharge and education cess

• Management fees & interest paid to a resident of France

• TDS at rate specified in treaty, without adding surcharge and education cess

• DTAA silent on surcharge & cess – taxpayer can avail of benefit

• ITO v M Far Hotels Ltd 58 SOT 261 (Coch)

• Definition of tax under DTAA relevant

• Sunil V Motiani v ITO 59 SOT 37 (Mum) – India-UAE DTAA – rate inclusive of surcharge and cess

• DIC Asia Pacific Pte Ltd. v. Asstt. DIT 52 SOT 447 (Kol) – India-Singapore DTAA

• DDIT v J P Morgan Securities Asia (P) Ltd 42 Taxmann.com 33 (Mum) – India-Singapore DTAA

• Parke Davis and Company LLC v ACIT 41 Taxmann.com 193 (Mum) – India US DTAA

23 CNK

Recent Issues

Grossing up u/s. 206AA

• Whether s.206AA applicable to non-residents?

• Whether grossing up to be done at rate of 20%?

• Bosch Ltd v ITO 141 ITD 38 (Bang)

• S.206AA applicable also to non-residents – to esnure that there is no evasion of tax even by foreign entities

• Income shall be increased to such amount as would after deduction of tax thereto at the rate in force for the financial year in which such income is payable, be equal to the net amount payable

• Literal reading of section implies that income should be increased at the rates in force for the financial years and not the rates at which the tax is to be withheld

• Grossing up of amount is to be done at rates in force for the financial year in which such income is payable and not at 20% as specified u/s 206AA

24 CNK

Recent Issues

Credit for TDS

• S.199(3) amended wef AY 2008-09 – CBDT may make rules for grant of TDS credit

• Rule 37BA(4) – Credit for TDS deducted and paid shall be granted on basis of information relating to TDS furnished by deductor to income tax authority or person authorised by such authority and information in return of income in relation to such credit, subject to verification in accordance with risk management strategy formulated by CBDT

25 CNK

Recent Issues

Court on Its Own Motion v. CIT 210 Taxman 452 (Del)

• 2 types of problems faced by taxpayers

• failure & difficulty in getting credit of TDS

• adjustment of past demands or arrears from tax payable

• To be addressed & tackled separately

• Centralised computerisation of records, filing, processing of returns & issue of refunds laudable

• Problem on account of wrong/incorrect data uploaded in centralised computer system

• AOs were to have verified and corrected arrears before uploading

• S.245 requires prior intimation to assessee before adjustment of refund to enable response

26 CNK

Recent Issues

Court on Its Own Motion v. CIT 210 Taxman 452 (Del)

• Affidavit filed by CBDT

• CPC adjusts refunds against existing demands without following procedure u/s.245

• 22.93 lakh cases of adjustment of refunds – Rs.4800 crore

• In few cases where prior intimation sent, AOs refused to accept objections, CPC insisted that AOs to rectify

27 CNK

Recent Issues

Court on Its Own Motion v. CIT 210 Taxman 452 (Del)

• Procedure u/s.245 to be followed – advance intimation to be given to assessee, opportunity to file response , response to be considered and examined by AO

• AO to intimate CPC regarding his findings, who will then process refund, and adjust any demand payable

• Time limit may be fixed for AO to intimate CPC

• Where adjustment already made of non-existing, fictitious demands, revenue cannot take stand that adjustment possible contrary to s.245 – liability to interest also arises

• Opportunity given to Revenue to rectify & correct records and issue refunds with interest without putting harsh burden & inconveniencing assessees

28 CNK

Recent Issues

Court on Its Own Motion v. CIT 210 Taxman 452 (Del)

• Failure to get credit for TDS – 2 categories

• Amount reflected in 26AS, but incorrect entries in return or small mismatch

• TDS deducted but TDS return not correctly filled in or uploaded

• Taxpayers forced to make double payment

• In FY 2010-11 & 2011-12, 43% & 39% of returns filed in Delhi found defective

• Demand of Rs.3,000 crore for FY 2010-11 – reduced to Rs.1900 crore after rectification

• In spite of writing letters to deductors to rectify TDS details, deductors fail & neglect to do so

• No adverse consequence or action against such deductors

• Deductee is out of pocket & harassed, but deductor does not suffer

29 CNK

Recent Issues

Court on Its Own Motion v. CIT 210 Taxman 452 (Del)

• CBDT response

• deductors are informed on processing u/s.200A of errors – no penal provisions for failure to correct

• Communication of mismatch to deductors by CPC – also sent to CIT(TDS) for follow up

• Response is unconvincing & unsatisfactory

• Small & insignificant mismatches, if technical, should be condoned or ignored

• Amount reflected in Form 26AS should not be denied credit for small or technical mismatch

• AO can subsequently revise, if found incorrect later on

30 CNK

Recent Issues

CBDT Instructions relating to TDS credit problems

• Instruction No 5/2013 dated 8.7.2013 – TDS Mismatch

• In cases of TDS mismatch, where assessee approaches AO with TDS certificate, AO to give TDS credit after verification of payment of TDS

• AO may also verify with AO(TDS) re true & correct position about TDS certificate

• AO(TDS) may compel deductor to furnish correction statement

• Instruction No 11/2013 dated 27.8.2013 – Unmatched Challans reflected in Form 26AS

• AO(TDS)/CPC(TDS) to issue letters to deductors to verify & correct challans

• If necessary, to be asked to file correction statements

31 CNK

Recent Issues

TDS Credit

• Credit given on basis of Form 26AS

• Merely because the Department's system does not indicate the amount of TDS for which credit claimed, assessee cannot be made to pay tax again. It is for the Dept to check the error in its system or point out the fallacy in the assessee's claim – 3i Infotech Ltd v Dy CIT – SA No 07/Mum/2013 dated 1.2.2013

• Department required to give credit for TDS once valid TDS certificate produced, or even where TDS certificates not issued by deductor, on basis of evidence produced by assessee regarding deduction and on basis of indemnity bond – Citicorp Finance (India) Ltd v Addl CIT – ITA No 8532/Mum/2011 dated 13.9.2013

• Where details of TDS were available in Form 26AS, credit could not be denied in final computation, even if assessee had claimed credit of lesser amount in return and there was no default in furnishing any documents – Vaghjibhai S Vishnoi v ITO 36 taxmann.com 371 (Guj)

32 CNK

Recent Issues

TDS Credit

• To be given in year in which relevant income offered to tax

• Back-to-back rent agreements – net rent nil

• AO denied TDS credit as no rent income

• If amount received after TDS, and amount admittedly not chargeable to tax, credit for TDS to be allowed in year of deduction - Arvind Murjani Brands (P) Ltd v ITO 137 ITD 173 (Mum)

• Amount of payment mentioned in TDS certificate partly offered to tax in earlier year

• Entire TDS credit claimed during the current year

• ITO allowed TDS credit pertaining only to income offered to tax during the year

• No dispute that part amount offered to tax in earlier year

• Income relating to TDS having been offered to tax in earlier year, TDS credit not having been claimed in those years, no disallowance of TDS can be done – NCC Maytas JV v ACIT 2013-TIOL-1045-ITAT-HYD

33 CNK

Recent Issues

Interest u/s 201(1A)

• In cases of delayed payment of TDS, interest @ 1.5% per month or part of a month payable from date on which tax was deducted to date on which tax is actually paid

• Not from due date of payment

• Case where tax deducted on 12

May, payment due on 7

June, paid on 10

June

• Whether interest payable for one month or two months?

• TDS(CPC) levying interest for two months

34 CNK

Recent Issues

TDS Statement Late Filing Fees – s.234E

• Wef 1.7.2012

• Rs.200 per day of delay of filing TDS statements

• Not to exceed amount of tax deductible

• In addition to penalty u/s 272A(2)(k) – Rs.100 per day of delay

• Narath Mapila LP School v UoI (Ker) dated 18.12.2013 – Challenge to Constitutional Validity – Interim Stay granted for 2 months

• Adithya Bizorp Solutions India Pvt Ltd v UoI (Kar) dated 19.2.2014 – Constitutional Validity - Enforcement of Notices issued by CPC(TDS) stayed until further orders

• Rashmikant Kundalia v UoI (Bom) dated 28.4.2014 – Challenge to Validity – operation of notices levying fees stayed

• Om Prakash Dhoot v UoI (Raj) dated 15.4.2014 – notices issued – recovery subject to final outcome of writ petition

35 CNK

Thank you