tax benefits of lilo tranasactions - faculty...

TRANSCRIPT

The tax benefits of Lease-in Lease-out (LILO) transactions

Jacob Thomas Yale University

School of Management (203) 432-5977

First version: December, 2006 Current Version: January, 2007

Abstract Tax shelters have received recent scrutiny in the financial economics literature because of their impact on firm decisions. While the source of tax benefits for many types of shelters are fairly straightforward, they are not as evident for Lease in Lease out (LILO) transactions. This paper uses spreadsheet models to understand how tax benefits are generated in LILO transactions and to identify factors that enhance the magnitude of those tax benefits.

I thank Sandi Lin of Cambridge Finance for assistance with developing the spreadsheet models, and Jeff Gramlich and Frank Zhang for extensive comments.

The tax benefits of Lease-in Lease-out (LILO) transactions

1. Introduction

Recent press articles on tax shelters have brought to the fore the pervasive use of

shelters and the many millions of dollars of profits that appear to have been sheltered.

Examples of incidents receiving press coverage include the unprecedented criminal

proceedings against KPMG tax partners and the large tax disputes relating to transfer

pricing by pharmaceutical firms.1 Financial economists recognize the importance of

understanding the role and impact of tax shelters on financial decisions, and have recently

initiated efforts to understand such transactions.2 This paper focuses on Lease-in Lease-out

(LILO) transactions, one of many shelters that are currently the subject of legal disputes

between taxpayers and the IRS. Unlike other tax shelters, such as those relating to transfer

pricing and dividend recapture, where the source of tax benefits created is transparent, it is

not immediately obvious how LILO transactions create value for the contracting parties. I

examine here the cash flows associated with a hypothetical LILO transaction to determine

how tax benefits are created, and to understand the factors that enhance those tax benefits.

According to Boraks (2003) the IRS has identified 56 companies that initiated

LILO transactions through 1999.3 A number of large banks have revealed in their financial

statements that the IRS has disallowed LILO transactions and is seeking back taxes. The

potential impact of LILO transaction being reversed is so widespread that the FASB issued

in July, 2006 a Staff Position (FSP FAS 13-2) to provide guidance on accounting for the

1 See for example the New York Times article “U.S. Adding New Wrinkles In Shelter Case” by Lynnlee

Browning (Section C3 on 10/31/2006) and the Wall Street Journal article “Merck Tax Disputes Could Cost It Up to $5.58 Billion” by John Carreyrou and Jesse Drucker (Section A3 on 11/8/2006).

2 See, for example, Graham and Tucker (2006) and Desai, Foley, and Hines (2005). 3 Revenue Ruling 99-14 effectively choked off any new LILO transactions, however the status of

transactions initiated prior to 1999 is still in dispute.

2

potential reversal of leveraged lease transactions. This interpretation is effective for fiscal

years beginning after December 15, 2006, and analysts are eager to see if the quarterly

statements filed in 2007 will provide new information about the number and magnitude of

firms engaged in LILO transactions.

The following is a brief description of a typical LILO transaction. A tax-indifferent

owner of long-lived equipment (often an overseas state or local government entity) and a

US taxpayer (usually a large bank) enter simultaneously into a head lease that transfers the

equipment’s usage rights to the taxpayer and a sublease that transfers those rights back to

the original owner. The periodic head lease payments to be paid by the taxpayer are

replaced by the following two payments: i) a prepayment at the beginning of the

transaction and ii) a deferred payment to be paid a few years after the end of the head lease.

The prepayment represents about 80 percent of the equipment value and the present value

of the deferred payment represents approximately 10 percent; in effect the head lease

rentals cover approximately 90 percent of equipment value. To make the prepayment, the

taxpayer borrows a substantial fraction from a third party bank (about 70 percent of

equipment value) and the balance (about 10 percent of equipment value) is covered by an

equity investment, made from the taxpayer’s corporate funds. The taxpayer also pays about

5 percent of equipment value to the owner (as incentive to engage in the transaction) and

pays various transactions costs, including fees to promoters (another 5 percent of

equipment value).

Upon receiving the prepayment of head lease rents, the owner is required to

immediately invest it in interest-bearing deposits and securities, which are held in trust, and

those funds are used to make the periodic rental payments that come due under the

3

sublease. Over a so-called “base” period of the sublease, which represents about two-thirds

of the years covered by the sublease, the sublease rental payments being made by the

owner are used in their entirety to retire the principal and repay interest on the loan taken

by the taxpayer to make the prepayment. At the end of this base period, the owner has the

right to terminate the transaction by exercising an early buyout option (EBO). If the EBO is

exercised, the residual prepayment funds held in trust (primarily the equity investment plus

accmulated interest) are returned to the taxpayer. If the EBO is not exercised, the taxpayer

chooses among different options, which allow the taxpayer to either transfer the equipment

to a third party or require the owner to continue with the sublease.

For this analysis I will consider the case where the owner exercises the EBO and the

transaction is terminated at the end of the base period. Not only is this the most likely

outcome, as suggested by promoters’ descriptions of LILO transactions as well as analyses

of the interests of the owners and taxpayers under the different options, stripping out the

complex cash flow patterns associated with other options allows me to identify more

directly the primary source of tax benefits.

It is not apparent how tax benefits are created under the scenario when the EBO is

exercised. While it is true that the owner and taxpayer have different tax rates, no

depreciation tax shields are transferred to the taxpayer, since ownership for tax purposes

remains with the owner. Also, focusing on the tax position of the taxpayer (since the owner

pays no taxes) does not provide any obvious reasons why the deductions associated with

head lease outflows are not offset by income associated with sublease inflows. Consider,

for example, the portion of the head lease prepayment that is financed by taxpayer

borrowing. The taxpayer borrows that amount from a third party lender, and pays it to the

4

owner in lieu of periodic head lease rentals that come due over the base period. The owner

then deposits those funds in an interest-bearing account and the principal and interest from

that account are used to make the corresponding periodic sublease payments owed to the

taxpayer, which are then used to settle the principal and interest owed on the original

borrowing. Since the interest rate on the taxpayer’s borrowing equals the interest rate

earned on the deposit made by the owner, the rent prepaid to the owner plus the interest

paid by the taxpayer to the third party bank should equal the sublease rentals received by

the taxpayer.

My analysis reveals that the underlying source of tax benefits is the arbitrage

created because a LILO is effectively two sequential loans: the taxpayer borrows money

from third parties, lends the money to the owner as a prepayment, and the owner then lends

the money back to third parties. Tax arbitrage is created because the taxpayer deducts

interest on the funds used to make the prepayment whereas the owner pays no taxes on the

interest earned on that prepayment.4

The benefits actually available from tax arbitrage are affected by the following

factors. Since the transaction is structured as a head lease/sublease, rather than an explicit

loan from the taxpayer to the owner, the prevailing tax rules require that the taxpayer’s rent

deductions be spread out over the life of the lease in such a way as to reduce sharply the

present value of the tax benefits created by this arbitrage. That lost value is re-created by

paying a portion of the head lease payments as a deferred payment, as it allows the

taxpayer to accelerate the deductions associated with the prepayment. However, since the

deferred tax payment itself creates negative tax arbitrage (the transaction now flows in the 4 Even though the prepayment is partially financed by the taxpayer making an equity investment, it is

reasonable to assume that this equity investment also generates interest deductions, since the taxpayer is typically a bank with a highly leveraged balance sheet and most investments are effectively debt-financed.

5

opposite direction to that for the prepayment), certain adjustments are necessary before the

deferred payment can contribute its own tax benefits. Those adjustments are as follows:

a) the deferred rent payment should be projected using an inflated discount rate, and b) that

overstated deferred payment should not actually be paid. Inserting an early termination

option that allows the taxpayer to settle the liability for deferred rents by paying a fair

deferred rent, projected using market interest rates, is one way to avoid making the

overstated deferred payment. Even though the excess interest and rent deductions taken

(based on the overstated deferred payment) are recaptured at early termination, the net

effect of these adjustments is the creation of additional tax benefits.

Overall, the tax benefits created in actual LILO transactions by prepaying most

head lease rents and deferring the payment of the remaining rents equals about 10 to 15

percent of equipment value, for the case when the transaction is terminated early by

exercising the EBO. That benefit is available to pay various transactions costs and to be

shared between the taxpayer and the owner.

The rest of this paper is organized as follows. In Section 2, I elaborate on the main

features of LILO transactions that are relevant to the case when the EBO is exercised. This

description focuses on operational features and holds aside the tax treatment. In Section 3, I

describe the simulations I conducted to determine how the tax benefits are created. Given

the complex interaction between different features of the transaction, I consider each of the

main features separately to illustrate how the tax benefits arise.

2. Operational features of LILO transactions (excluding tax benefits)

Consider a tax-exempt owner of an asset that is the subject of a LILO transaction.

Assume that the asset has a remaining useful life of 50 years. Panel A of Figure 1 illustrates

6

the conceptual positions underlying the head lease/sublease combination described next.

The owner enters into a 40-year head lease with a taxpayer under which the rights to use

the asset are transferred to the taxpayer in exchange for periodic market rentals (L1, L2,

and so on through L40) for each year of the head lease. The two parties also agree to enter

into a sublease for 32 years under which the rights to use the asset are transferred back to

the owner. (The head lease typically runs over 80 percent of the remaining useful life of the

asset, and the sublease typically runs over 80 percent of the head lease.) I assume that the

sublease rental for each of the 32 years corresponds exactly with the head lease rentals for

those years (L1, L2, and so on through L32). Since there is no material change caused by

the head lease/sublease combination during that 32 year period, the head lease and sublease

cash flows should net out.

Panel B of Figure 1 incorporates the head lease feature that replaces the periodic

rental payments with a prepayment and a deferred payment, payable at the beginning and

end of the head lease, respectively. The prepayment is funded primarily by debt, obtained

from a third party lender. The remainder of the prepayment is funded by the taxpayer, and

is typically referred to as the equity investment in the transaction. The debt requires that

principal and interest be paid back according to a 25-year schedule (P&I1, P&I2, and so on

through P&I 25). The loan repayment schedule is set up so that it matches the sublease

payments over the first 25 years.

Panel C completes the relevant details that describe the EBO scenario, under which

the transaction is terminated at year 25. The prepayment of head lease payments handed

over to the Owner at the beginning of the transaction is held in two separate accounts,

corresponding to the debt and equity sourcing of the prepayment. The debt account

7

generates payments each period that correspond exactly with the principal and interest

payments required to be repaid by the taxpayer to the Lender (P&I 1, P&I 2, through

P&I 25). As mentioned earlier, these payments also equal the sublease rent payments due

each period through the termination date (L1, L2, through L25). In effect the amounts

withdrawn from the debt account are used by the owner to make the sublease rental

payments to the taxpayer, and the taxpayer uses those funds to make the required principal

and interest payments on the loan. The funds built up in the equity account are repaid with

interest to the taxpayer at the termination date.

3. Spreadsheet simulations

For the simulations, I assume the following conditions for a hypothetical piece of

equipment that is subject to a LILO transaction that is initiated on 1/1/1998.

a) market rentals are estimated to be $6.3 million for the next seven years and $7.7 million for the following seven years, at which point the EBO is exercised. b) the owner is tax exempt, and the taxpayer pays taxes at a flat 35 percent rate. c) market interest rates for the low-risk cash flows associated with this transaction are 7 percent, and the taxpayer can borrow at this low risk rate for any prepayment of head lease rentals. d) the IRS-specified rate for calculating interest and rental deductions is 7.7 percent, e) the two interest rates assumed in the transaction (for calculating the deferred head lease payment and for calculating interest deductions/sub lease rentals) are also assumed to be 7 percent for the base case (they will be increased in other cases to determine the benefits of an inflated rate).

The market rentals assumed in typical LILO transactions tend to follow the pattern

described above, where for the first stage of the lease they run at a constant level equal to

10 percent below the average rental (of $7 million in this case) and then increase to a level

of 10 percent above that average for the second stage. I abbreviated the lease period to just

14 years, relative to the longer periods discussed in section 2, to economize on the size of

the spreadsheet models.

8

If the transaction had been set up without any prepayments or deferred payments for

the head lease, I assume that the market rentals that should be paid under the head lease (7

payments of $6.3 million followed by 7 more payments of $7.7 million) would exactly

cancel out the sublease rentals, and both parties are neutral to the transaction as neither

party gains or loses economic value. In Section 3.1 I consider the impact of prepaying all

the head lease rentals on 1/1/1998, and then consider in Section 3.2 the impact of deferring

all the head lease rentals and making a single payment on 1/1/2020.

3.1 Prepayment only

I begin the prepayment case by discussing a hypothetical tax treatment, where the

prepayment is deductible immediately. Even though the prevailing tax rules for such

transactions require that the prepayment be deducted over the life of the lease, the

immediate deductibility treatment is useful for purposes of illustration. Table 1 describes in

the top and bottom panels the relevant cash flows as viewed from the taxpayer’s and

owner’s perspective, respectively. Since the recipient of that prepayment (Owner) is tax-

exempt, it can be shown that the appropriate prepayment is $59.8 million, which is the

present value of the 14 head lease payments discounted at 7 percent (calculation described

later). For convenience, I will round all dollar amounts to the nearest one-tenth of a million.

Columns A, B, and C in Table 1 provide the cash inflows, outflows, and net pre-tax flows

to the taxpayer over the life of the transaction, column D calculates the tax-related

outflows, and column E reports the net after-tax cash flows to the taxpayer. The present

value of those cash flows is $6.8 million (bottom of column E), discounted at the after-tax

discount rate of 4.55 percent (corresponding to the pre-tax interest rate of 7 percent and a

tax rate of 35 percent).

9

By using an after-tax discount rate of 4.55 percent for the taxpayer, I am assuming

that the transaction is associated with an all-debt capital structure. As described in Section

2, most of the investment in this transaction is explicitly funded by the loan to the taxpayer.

Even the so-called equity investment by the taxpayer can be viewed as being implicitly

financed mostly by debt, which is issued by the taxpayer at the corporate level. Finance

theory associates debt with a corporate-level investment based on the “debt capacity” of the

investment. The low risk and high collateral value associated with the equity investment

(which is typically invested in Treasury bonds) suggests that it is appropriate to view the

equity investment as also being largely debt-financed.5 It should be noted that the debt

underlying the prepayment generates interest tax shields for the taxpayer, and these tax

shields represent one of the tax benefits associated with the transaction. However, since

these tax shields are implicitly incorporated in the 4.55 percent after-tax discount rate, they

are not explicitly noted in the spreadsheet models.6

Columns F through J report the corresponding cash flows to the owner, and the

present values of the after-tax net cash flows discounted at 7 percent is 0 (see bottom of

column J). In effect, the owner is indifferent between receiving the original periodic head

lease payments or the prepayment of $59.8 million. Columns K and L confirm that

investing that prepayment at 7 percent generates the exact amounts required to make the

sublease rentals to be paid by the owner to the taxpayer.

5 This view is supported further when the taxpayer is a bank with a capital structure that leans substantially

toward debt. 6 An alternative presentation is to consider the debt underlying the prepayment, and the associated interest

payments. I found this presentation to be somewhat cumbersome. When considering the case of inflated interest rates, however, I will use this alternative presentation (see discussion underlying Table 4).

10

Assuming immediate deductibility of the prepayment, the transaction generates $6.8

million in tax benefits because the taxpayer deducts the interest associated with the amount

borrowed to make the prepayment, captured here by an after-tax discount rate of 4.55

percent rather than the pre-tax rate of 7 percent, and the owner pays no tax on the

corresponding interest income earned on the prepayment. To confirm that these tax benefits

are due entirely to the asymmetric tax treatment of interest income and expense, I

calculated the amount of prepayment that would be necessary if the owner is also taxed at a

35 percent rate. That prepayment rises to $70.2 million, being the present value of the 14

rental payments discounted at 4.55 percent. The after-tax value of the difference between

the two prepayments ($70.2 versus $59.8 million) is equal to the tax benefit of $6.8 million

noted in Table 1.

Table 2 describes how that $6.8 million tax benefit is reduced sharply when the

prepayment is deducted over the life of the head lease using the 110/90 methodology

allowed under the safe harbor leasing rules in Treasury Reg. §1.467-3.7 Under these rules,

the prepayment of $59.8 million is spread equally over the 14 years of the head lease (or

$4.3 million per year) and the taxpayer is allowed to assign 110 percent of that equal

allocation during the first half of the lease (or $4.7 million per year) and then 90 percent of

that allocation during the second half of the lease (or $3.8 million per year). Column D in

Table 2 shows that assignment, and the present value of the net after-tax cash flows in

column F is $1.3 million. In essence, even though the tax arbitrage described in Table 1 is

still available in this illustration, the 110/90 allocation rules for prepaid rents reduces

sharply the tax benefits available (from $6.8 million in Table 1 to $1.3 million in Table 2).

7 See Darrow (2000), for example, for a description of Sec. 467(b) of the Internal Revenue Code and the

related Treasury regulations.

11

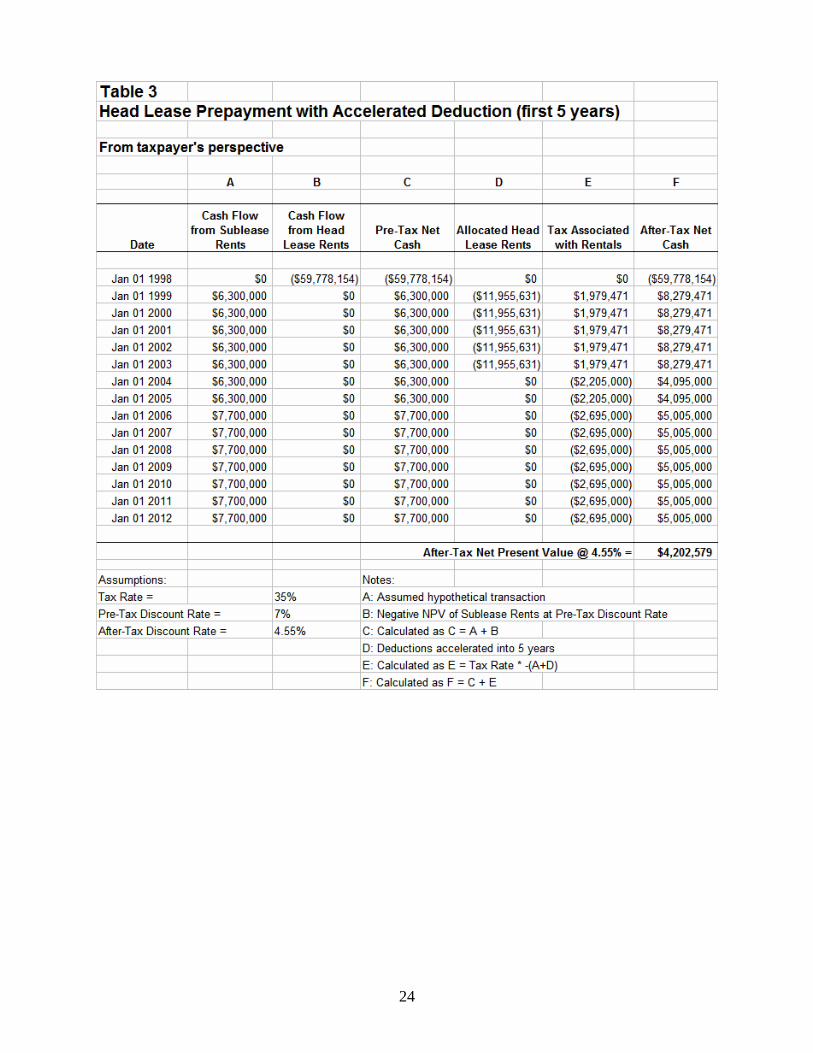

The next case examined for prepaid rentals, described in Table 3, is intended to be

representative of the structure of actual LILO transactions and results in tax benefits within

the range bracketed by Tables 1 and 2. In this case I anticipate the presence of a deferred

payment (described in Section 3.2), which is likely to be a much larger dollar amount than

the prepayment (since it is a future value to be paid many years hence). The 110/90 rule

allocates the sum of the prepayment and deferred payment equally over the lease period,

and allows full deduction of that allocated rent if it has been prepaid but only allows a

deduction equal to the present value of that allocation (plus built up interest as explained in

Section 3.2) if it is going to be deferred. In terms of this case, the rules assign the

prepayment to the allocated rent over the first few years, until the prepayment is completely

consumed. I have assumed that the presence of a deferred payment causes the prepayment

to be deducted over the first 5 years, rather than 14 years. The NPV of the special tax

benefits are now worth $4.2 million. While this tax position is not as attractive as that

described in Table 1 ($6.8 million), the presence of a large deferred payment improves

substantially the special tax benefits described in Table 2 ($1.3 million) because of the

accelerated deduction allowed. In sum, a prepayment of $59.8 million is capable of

generating tax benefits of about $4.2 million, provided a deferred payment is available to

squeeze the deductions associated with the prepayment back into the first 5 years.

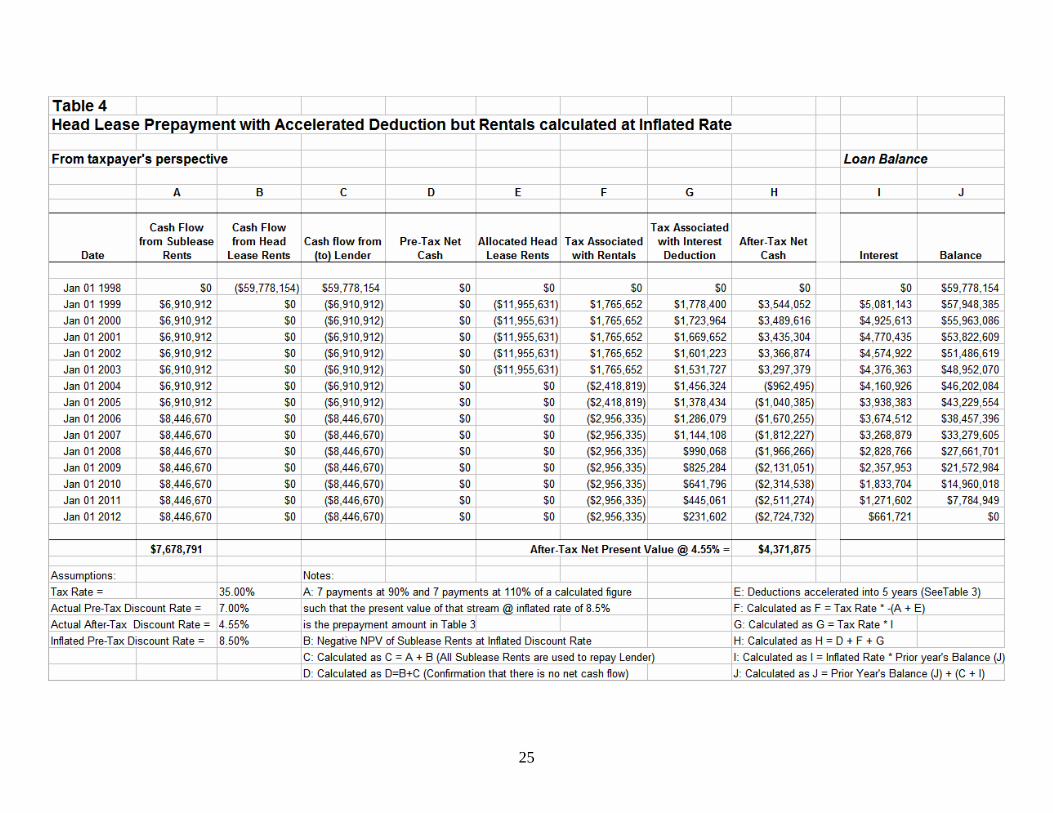

The final case considered for prepaid rentals examines the impact of raising the

interest rate assumed for both the debt financing obtained for the prepayments as well as

for the rate at which the prepayment grows in order to make sublease rentals. Table 4

describes the impact of raising that rate from 7 percent to 8.5 percent for the case discussed

in Table 3. Unlike the prior cases where the interest cost of debt was incorporated in the

12

after-tax discount rate of 4.55 percent, here the debt-related amounts need to be accounted

for separately (see columns I and J). The cash flows in column A describe the sublease

rentals that would be stipulated by the contract, such that their present value at the higher

discount rate of 8.5 percent equals the same prepayment of $59.8 million. Since the same

overstated interest rate is used throughout the transaction, the pre-tax cash inflows and

outflows offset exactly, and the owner continues to remain unaffected by the transaction

(cash flows to owner not shown in Table 4). While the pre-tax cash flows to the taxpayer

also offset exactly (see columns A through D), the tax effects (see columns E through G)

and resulting after-tax cash flows (column H) create value to the taxpayer. The main

finding is that the net value of tax benefits is $4.4 million for the inflated rate of 8.5 percent

(bottom of column H), which exceeds the $4.2 million in tax benefits in Table 3, calculated

using the 7 percent rate.

While using an inflated rate for the prepayment provides a relatively small increase

in tax benefits, one potential reason to use an inflated rate here is to reduce the incongruity

between this rate and the rate underlying the deferred payment. As described next in

Section 3.2, using an inflated rate for the deferred payment generates a substantial increase

in tax benefits.

3.2 Deferred payment only

To investigate the tax benefits created by deferring rental payments, I return to the

base case with offsetting head lease and sublease rents, and replace the scheduled payments

under the head lease with a single deferred payment of $264.9 million to be paid to the

Owner on January 1, 2020. This date is arbitrary (it is typically deferred until five years

after the head lease expires) and is used only to show the effect of a delayed deferred

13

payment. The amount of the deferred payment is based on a discount rate equal to the pre-

tax interest cost of 7 percent, to ensure that the owner is indifferent between the deferred

payment and the periodic rentals.

As with the prepayment case described in Section 3.1, I begin with the hypothetical

tax treatment where the deferred payment is deductible when paid in 2020 and switch later

to the 110/90 rules as they apply to deferred payments. Column A in Table 5 describes the

cash inflows to the taxpayer from sublease rents, column B reports the future value at 7

percent of equivalent amounts that would have been paid under the head lease, and column

C computes the total deferred payment of $264.9 million. Columns E through H can be

ignored here as they have been inserted to make this Table comparable to subsequent

Tables that are based on the prevailing 110/90 rules. Columns I and J describe the tax

effects, and column K describes the after-tax cash flows. The main finding is that deferring

head lease payments reverses the tax arbitrage created by prepaying those rents, and the

transaction causes a net value loss of $19 million (shown at the bottom of column K).8

Table 6 amends the Table 5 calculations to incorporate the 110/90 allocation rules

that apply to this transaction. As described for the prepayment, the deferred payment is first

divided equally among the 14 periods corresponding to the lease and the first 7 years are

assigned an amount equal to 110 percent of that equal amount, whereas the last 7 years are

assigned 90 percent of that amount ($20.8 and $17 million in column E, respectively).

Unlike the prepayment case, however, those allocated amounts have not yet been paid, and

the rules limit the rental deduction to the present value of those amounts, discounted back

from the year 2020 using the IRS-designated rate of 7.7 percent (see column F). Since 8 Stated differently, since the taxpayer can only earn 4.55 percent on the funds generated by deferring head

lease rental payments, making a deferred payment that grows at 7 percent leaves the taxpayer substantially worse off.

14

those present value amounts have also not yet been paid, the tax rules allow taxpayers to

accumulate the unpaid balances (column H) and deduct an imputed interest at the same 7.7

percent (column G). (The accumulated balances in column H also include the unpaid

imputed interest.) Column I describes the tax on sublease rental income, and column J

describes the tax savings due to deducting the present value of allocated rents as well as the

imputed interest. Column K presents the net after-tax cash flows for each year, and the

bottom of that column shows that even though the net loss created by deferring head lease

payments is reduced to $1.3 million when the 110/90 rules are applied, deferred payments

do not by themselves create value. The only purpose of deferring head lease payments

identified so far is to accelerate the deductions allowed for prepaid rentals (see discussion

for Table 3 results).

Table 7 describes the impact of increasing the discount rate used to calculate the

deferred payment from the market rate of 7 percent to 8.5 percent. The format is similar to

Table 6. The higher discount rate increases the deferred payment from $264.9 million to

$328.1 million. While this increased deferred payment also raises the deductions taken in

each year, the burden of paying the higher deferred payment increases the economic loss

suffered by the taxpayer to $12.5 million (from $1.3 million in Table 6).

Using inflated discount rates creates an asymmetry between the value distributed to

the taxpayer and the owner. While the taxpayer suffers a large loss, the owner is better off

because the inflated interest rate results in too high a deferred payment, relative to the fair

deferred payment of $264.9 million (based on a market rent of 7 percent). One way to

remove that asymmetry is to insert an early termination clause, similar to the EBO that is

included in LILO transactions, under which the owner is paid a fair termination payment.

15

The fair termination amount equals the future value of the head lease rental payments,

projected at the market rate of 7 percent, rather than the inflated rate of 8.5 percent. A

termination obviates the need to make the large deferred payment of $328.1 million, and

yet it allows the taxpayer to deduct inflated rent and interest amounts based on that inflated

deferred payment (during the period before the early termination). To be sure, those excess

deductions are recaptured at the early termination. Since the allocated rent and interest

deductions taken by the taxpayer are based on an inflated deferred payment, derived from

the higher 8.5 percent rate, they add up over time to a number greater than the fair deferred

payment actually made at termination. This difference is included as taxable income at the

termination date.

Table 8 provides a fuller description of the early termination case. The early

termination date is set at 1/1/2012 when the last lease rental payment is made. Column A

provides the periodic sublease rental cash inflows to the taxpayer. Columns B and C show

that the owner requires a fair termination value of $154.2 million, being the present value at

2012 of the periodic head lease rents it was entitled to collect. Columns N and O show that

the fair termination value to the taxpayer is only $130.9 million for the same rents, this

difference being caused by the owner and taxpayer having an after-tax discount rate of 7

and 4.55 percent, respectively. The difference between $154.2 million and $130.9 millions

is the loss caused to the taxpayer because the deferral is in effect a reverse tax arbitrage

(similar to the losses described in Table 5 through 7). Columns D and E describe the

calculation of the nominal deferred payment that is based on the inflated 8.5 percent rate,

and columns F through M repeat the calculation for tax effects and net after-tax cash flows

from Table 7.

16

The row for 2012 requires additional explanation because of the cash flows

associated with early termination. Column C includes the $154.2 million fair price that the

taxpayer has to pay the owner as a deferred payment in 2012. The $102.3 million in

column H and $55.1 million in column I represent the taxable income that is created by the

recapture of allocated rental deductions and interest deductions in all prior years.

The present value of the net after-tax cash flows to the taxpayer reported in column

M indicate an overall benefit of $0.7 million, which is dramatically different from the loss

of $12.5 million in Table 7. Even though deferring rental payments is fundamentally not

tax advantageous, indicated by the difference between what the owner and the taxpayer

view as a fair deferred payment for the periodic rentals, it can generate net tax benefits

when an inflated rate is used to project the nominal deferred payment and the transaction is

terminated before the overstated deferred payment is due.

Finally, I consider the impact of pushing out the deferred payment an additional 18

years, from January 1, 2020 to January 1, 2038. Those calculations are presented in Table

9. Pushing out the deferred payment date increases the actual deferred payment amount to

$1,424.6 million dollars. This higher deferred payment increases the tax deductions

allowed over the lease period (relative to those in Table 8) because the mismatch between

the inflated rate of 8.5 percent used to generate the deferred payment and the lower IRS

rate of 7.7 percent is applied on a larger allocated rent. The benefit of delaying the

overstated deferred payment is indicated by the net tax benefit of $1.9 million reported as

at the bottom of column M, which is higher than the $0.7 million reported in Table 8.

17

2.3 Summary

In sum, LILO transactions generate tax benefits from two sources. First, a

prepayment of head lease rents by the taxpayer allows for tax arbitrage, because the

taxpayer takes interest deductions on the amounts borrowed to make the prepayment but

the owner pays no taxes on the interest income earned by the prepayment. The magnitude

of this tax benefit is increased if some of the head lease payments are deferred, as the

deductions associated with the prepayment can then be accelerated under the 110/90 rules.

Tax benefits can be increased slightly by selecting an inflated interest rate for the

borrowing underlying the prepayment. Second, a deferred payment can generate additional

tax benefits, beyond those created by accelerating the deductions associated with the

prepayment, if an inflated discount rate is used to calculate the deferred payment but that

inflated deferred rent is not actually paid. (One way to do so is to insert an early

termination option under which the inflated deferred rent is settled by making a fair

deferred payment.) Pushing the date of that inflated deferred payment further out into the

future increases the tax benefits from this second source.

The common features of actual LILO transactions conform remarkably to the tax

benefits projected by the spreadsheet model in the paper. The periodic head lease payments

are replaced by an advance payment and a deferred payment. The nominal interest rates

underlying the amounts borrowed to make the advance payment as well as the interest rates

used to project the deferred payment are inflated, relative to the market and IRS-

denominated rates that apply in each case. The deferred payment is delayed well past the

end of the head lease. Finally, the transactions allow for an early termination.

18

19

References:

Boraks, David. 2003. A new tax battle for big banks: LILO deals. American Banker (August 27).

Darrow, J.E. 2000. Tax accounting for leases under Section 467 final regulations. Journal of Taxation of Investments. Boston: (17) 143–5.

Desai, M.A., Foley, C.F., Hines Jr., J.R. 2005. The demand for tax haven operations. Unpublished working paper, .Harvard University, Cambridge, MA.

Graham, J R. and A.L. Tucker. 2006. Tax shelters and corporate debt policy. Journal of Financial Economics (81) 563–94.

Panel B: Head lease with prepayment and deferred payment and sub lease

Panel A: Head lease and sub lease

Owner Taxpayer

L1

L2

L3

L31

L32

Prepayment

Deferred Payment

Sublease Rentals

Head Lease Rentals

Lender

P&I 1

P&I 2

P&I 24

P&I 25

Princip. & Int. Payments

Owner Taxpayer

L1

L2

L3

L31

L32

L2

L1

Figure 1 Simplified cash flows associated with LILO transactions

20

L44

L31

L32

L3

L45

Sublease Rentals

Head Lease Rentals

Owner

L1

L2

L24

L25

Sublease Rentals

Taxpayer

Prepayment

Head Lease Rentals

Lender

P&I 1

P&I 2

P&I 24

P&I 25

Princip. & Int. Payments

EquityAccount

DebtAccount

P&I 1

P&I 2

P&I 24

P&I 25

Termination Payment

Payments from Debt A/C

Payments from Equity A/C

Panel C: Head lease with prepayment and sub lease for early buyout option (EBO) scenario

21

22

23

24

25

26

27

28

29

30