sustainable finance: a new paradigm

TRANSCRIPT

Global Finance Journal 24 (2013) 101–113

Contents lists available at ScienceDirect

Global Finance Journal

j ourna l homepage: www.e lsev ie r .com/ locate /gf j

Sustainable finance: A new paradigm☆

Ali M. Fatemi a,⁎, Iraj J. Fooladi b

a Department of Finance, Driehaus College of Business, DePaul University, 1 East Jackson Blvd., Chicago, IL 60604, United Statesb Douglas C. Mackay Chair in Finance, School of Business Administration, Dalhousie University, Halifax, NS, B3H 3J5, Canada

a r t i c l e i n f o

☆ The helpful comments of participants at the 201⁎ Tel.: +1 312 362 8826; fax: +1 312 362 6566.

1044-0283/$ – see front matter © 2013 Elsevier Inc.http://dx.doi.org/10.1016/j.gfj.2013.07.006

a b s t r a c t

Available online 16 July 2013

Weargue that our current approach to shareholderwealthmaximizationis no longer a valid guide to creation of sustainable wealth: An emphasison short-term results has had the unintended consequence of forcingmany firms to externalize their social and environmental costs. Anunwavering faith in markets' ability to efficiently uncover long-termvalue implications of short-term results has created many unacceptableoutcomes. Given the social and environmental challenges ahead, suchpractices and their unacceptable outcomes cannot be sustained.Therefore, a shift in paradigm is called for. We propose a sustainablevalue creation framework, within which all social and environmentalcosts and benefits are to be explicitly accounted for.© 2013 Elsevier Inc. All rights reserved.

JEL Classification:G32G39

Keywords:Sustainable financeValue creationCorporate social responsibility

1. Introduction

This paper was first delivered at the 2011 meetings of Global Finance Conference, April 5–7 in Bangkok,Thailand. The April 2, 2011 edition of Bangkok Post, like other local papers, was filled with reports of theflooding that had brought death and devastation to many areas of Thailand, and the Krabi area in particular.Its front page prominently displayed a quote from Samran Thetkit, a Krabi resident: “we have harmed nature,so nature has taken revenge.” The emphatic tone of this Krabi resident was, perhaps, one of the mostremarkable features of the article reporting on the devastating floods hitting the region. Two days later, thesame paper laid out the cause and effect relationship that Mr. Thetkit had in mind. In that issue, ThawilSuwanwong, a former Thai agricultural official, blamed illegal logging for Thailand's 2011 flooding.Mr. Suwanwong was further quoted as laying the blame squarely at the doors of the Thai government,criticizing its policies in “promoting the planting of rubber and palm trees by boosting their prices”. Inessence, government's actions were held responsible for the deforestation that ultimately led to the floodingdisasters of Thailand in 2011.

Half a dozen years earlier, on a different continent and in the aftermath of Hurricane Katrina, governmentinaction was blamed for the extent of damage caused by that storm. Long before Katrina hit the Gulf Coast of

1 meetings of Global Finance Conference are acknowledged and appreciated.

All rights reserved.

102 A.M. Fatemi, I.J. Fooladi / Global Finance Journal 24 (2013) 101–113

the United States, the American Society of Engineers had warned of the inadequacies of the Gulf Coast'sdefenses against amajor storm. Thewarningswere not heeded, and the country ended up picking the storm'stab estimated atmore than $110 billion.Moving forward in time, the same society'swarnings, issued in 2009,regarding the precarious situation of New York were also treatedwith indifference.1 Summarizing the resultsof simulations of storm surge threats, the group had recommended the installation of surge barriers in NewYork harbor to protect New York City. The report was shelved and two years later hurricane Sandy hit theNortheastern seaboard and the initial estimates of damage ran well in excess of $100 billion. The commoncharacteristic of these types of governmental actions (or inaction, as the casemay be) is an apparent failure toconsider the issue of sustainability in the decisionmaking process. In our first example, tomollify the incomeaspirations of an electorate, a government chooses to adopt policies that have short-term payoffs but aredetrimental to the long-term interest of the population and are, therefore, not sustainable. In the second case,in an effort to minimize the immediate pain of imposing taxes (or otherwise finding a source of financing), agovernment ignores the longer-term needs of the society, thus exposing it to much greater risks and tomuchhigher costs over the long run.2

Similar examples of sacrificing the long-term viability of the firm in exchange for the shorter-term payoffsare plentiful and can be easily documented across the world. One of the issues that the field of financialeconomic needs to address is the question of how to minimize the occurrence of such clearly inferioroutcomes. In this paper, we argue that the solution, or at least part thereof, can be found in academia. Indeed,it can be argued that some of the blame for the occurrence of these inferior outcomes lay squarely at the doorsof academia. Given our unquestioned faith in the efficiency of the markets, we have turned managers, andother decisionmakers, one generation after another into believers of the gospel that today's share price is thebest indicator of long-term true value and that end-of the-quarter earnings numbers are the best indicators ofa firm's true economic performance. Emulating the corporate world, other sectors have followed suit byputting undue emphasis on the “immediate” and the “short-term” at the expense of longer-term benefits,thus creating inferior outcomes. However, given the current paper's focus, and without loss of generality, ouranalysis will deal with the corporate decision making process.

1.1. Inferior decision outcomes

Perhaps, one of the best ways of demonstrating the detrimental effect of putting too much faith inshort-term earnings numbers and on the share price would be to examine (albeit selectively) the careers ofsome who came to be known as the masters of such craft in producing explosive earnings numbers andskyrocketing share prices. The CFO Magazine annually recognizes such people as having reached the pinnacleof their careers and bestows upon them the CFO Excellence Award. Let us review the longer-termaccomplishments of the three of their honorees beginning with the winner of the 1998 award, Scott Sullivanof Worldcom. Less than four years after having received this award, Worldcom filed for Chapter 11bankruptcy on July 21, 2002, the largest such filing up to that point. In between the recognition and thebankruptcy, auditors unearthed a $3.8 billion fraud and an avalanche of bogus accounting entriesorchestrated by Mr. Sullivan and his colleagues in Worldcom's executive suite.

The recipient of the 1999 CFO Excellence Award was Andrew Fastow, Enron's CFO. An award thatrecognized the spectacular growth of Enron's EPS and its share price which reached a record high of $90 pershare by mid-2000. Not more than a year later a huge scandal unfolded and Enron's shareholders lost nearly$11 billion when the stock price plummeted to less than $1 per share by the end of November 2001. When

1 See New York Times, “Engineers' Warnings in 2009 Detailed Storm Surge Threat to the Region,” November 4, 2012.2 Shortsightedness of this type is not limited to national governments or large cities. Examples can be found in many smaller-sized

communities, where decision makers are much more likely to be affected by the consequences of their actions; either directly at apersonal level or indirectly through their effects on their relatives and friends. One such example, reported in the August 30, 2009edition of the New York Times, from Uniontown, Alabama is worth considering. In exchange for $30 million and the prospect of 30new jobs, county officials there decided to bury three million cubic yards of coal ash into a landfill. One can easily rule out thepossibility that such a deal could be in the long-term interest of the community, if one considers (1) that coal ash, because of its highconcentrations of toxins (such as mercury, arsenic and other substances), is considered a hazardous waste by the EPA, (2) that themain source of livelihood for the area residents is catfish farming which will be confronted by a significant risk of contaminationonce the coal ash is buried in the landfill, and (3) that the area is susceptible to flooding and tornadoes, exposing the buried materialto a high risk of uncontrolled dispersal. Indeed, the negative elements of the deal appear to overwhelm the short-term benefits.

103A.M. Fatemi, I.J. Fooladi / Global Finance Journal 24 (2013) 101–113

the dust settled, Enron was forced into bankruptcy as was its auditor Arthur Andersen (the world's largestaccounting firm at the time). Theman recognized by the CFO Excellence Award, was found to be the principalcharacter behind Enron's use of accounting loopholes, special purpose entities, poor financial reporting, andthe concealment of billions of dollars in debt from failed deals and projects.

The winner of the 2000 CFO Excellence Award was Mark Swartz of Tyco International, the man who wasconvicted in 2005 of crimes related to his receipt of $81 million in unauthorized bonuses, the use of corporatefunds to purchase art (worth $14.725 million) and a $20 million payment (disguised as investment bankingfees) to a former Tyco director (named FrankWalsh). Hewas convicted and imprisoned to serve a term of upto 25 years.

Clearly, these executives, and others like them, were recognized for their short-term performance asjudged by measures rooted in a narrow definition of shareholder value. Had the award criteria been set in amanner that would have accounted for sustainable performance, these men would obviously not have madethe cut. Indeed, it can be argued that, had the criteria formeasuring financial executives' success been definedwith sustainability in mind, the global financial system would have been less fragile, more secure and moreprosperous. To develop a better insight into the degree of fragility of this system and its non-sustainability, letus now turn attention to four high-profile executives starting with Richard S. Fuld, the former CEO of LehmanBrothers.

In 2006, the Institutional InvestorMagazinenamedMr. Fuld America's topCEO in the private sector. In 2007he had reached the pinnacle of success by having Lehmanproduce a profit of $4.2 billion (compared to a 1993loss of $102 million). In March of 2008, he appeared on Barron's list of the 30 best CEOs and was dubbed“Mr. Wall Street.” He received nearly half a billion dollars in total compensation from 1993 to 2007. InJune of 2008, when Lehman's conditions were rapidly deteriorating, Mr. Fuld expressed confidence about thefirm, declaring it sound. Yet, the bank posted a second-quarter loss of $2.8 billion caused by bad mortgageinvestments. A truer picture emerged by March of 2010 when Anton R. Valukas, the bank's court-appointedexaminer, declared that Lehman had used what amounted to financial engineering to shuffle $50 billion oftroubled assets off its books in the months before its collapse in order to conceal its dependence on leverage.

In 2009, theworld of investmentswas shocked by themagnitude of fraud committed by BernardMadoff, aformer Chairman of the NASDAQ, after he admitted to having operated what has since been described as thelargest Ponzi scheme in history. The amount missing from client accounts, including fabricated gains,was almost $65 billion and the court-appointed trustee estimated actual losses to investors of $18 billion.Mr. Madoff admitted that he began the Ponzi scheme in the early 1990s. However, federal investigatorsbelieve that the fraud began as early as the 1970s, and those charged with recovering the missing moneybelieve the investment operation may never have been legitimate.

A year later, the world witnessed one of the worst industrial accidents in the Gulf of Mexico involving BP.On April 20, 2010, following an explosion in one of its rigs that killed 11 people, oil started flowing into theGulf of Mexico at a rate of 60,000 barrels per day. Eventually more than 4.9 million barrels of oil flowed intothe Gulf. Annoyed by themanyquestions raised in its aftermath, TonyHayward, BP's CEO declared onMay30,2011 “I'd like my life back.”3 Ironically, a year earlier (in May 2009) he had declared that “…our primarypurpose in life is to create value for our shareholders. In order to do that, you have to take care of the world.”4

Fast forward to November 15, 2012, when BP pleaded guilty to 14 criminal charges related to the spill andagreed to pay a $4.5 billion fine and the total direct bill for the spill may exceed $36.5 billion.5

As a last example in this category, consider the case of MF Global, headed by Mr. John Corzine, that wasforced into bankruptcy on October 31, 2011. The firm's downfall was attributed to its heavily leveragedpurchases of debt from Spain, Italy, Portugal, Belgium& Ireland (by June 2011, it had total debt of $44.4 billion

3 See New York Times, June 3, 2010.4 Before the Nov 15, 2012 announced payments, BP was forced to spend more than $14 billion on operational response and

cleanup costs and $1 billion on early restoration projects, and paid out more than $9 billion to individuals, businesses andgovernment entities. In March 2012, BP agreed with the lawyers for plaintiffs to settle claims of economic loss, including from thelocal seafood industry, and medical claims stemming from the oil spill. The company said it expected that settlement to be anadditional $7.8 billion, which it will pay from a trust it set aside to cover such costs. Additionally, under the Clean Water Act, BP'sfines could range from $1100 for every barrel spilled through simple negligence to as much as $4300 a barrel if the company werefound to have been grossly negligent. With an estimated 4.9 million barrels of oil spilled in the accident, the company faces liabilitiesof as much as $5.4 billion to $21 billion.

5 See “For BP, The Cleanup Isn't Entirely Over,” Wall Street Journal, February 4, 2013, P. B2.

104 A.M. Fatemi, I.J. Fooladi / Global Finance Journal 24 (2013) 101–113

and an equity of only $1.4 billion). In the aftermath of its bankruptcy, it was discovered that hundreds ofmillion dollars of customer monies were missing.6 One of the many interesting and puzzling aspects of MFGlobal story was its compensation policy. In a 2010 speech at Princeton Mr. Corzine slammed excessivecompensation onWall Street. Yet, the firm's 2011 second quarter results showed that no less than 64% of itsrevenue went to compensation. Additionally, Mr. Corzine, in a last-ditch effort, made an attempt to sell MFGlobal as late as one day before its bankruptcy. However, had that deal gone through,Mr. Corzinewould havepocketed $12 million in severance pay.7 It is almost impossible to determine if the efforts to sell the firmwereaimed at saving the operations or just a self-serving ploy. Given that it subsequently became clear thathundreds ofmillions of dollars of customermonies weremissing, it is hard tomake a convincing argument infavor of the first motive.

The common trait among these four individuals and their behavior is an emphasis on immediate resultsand a lack of appreciation for the longer-termeffects of their decisions.While TonyHaywardmay havemeantwhat he said (i.e., that his objective was to create value for shareholders of BP), his behavior was indicative ofhis not having a clue about how to create sustainable value. However, it should be added that the conduct ofMr. Hayward (and his peers) is, inmanyways, the artifact of the system in which they operate. Specifically, ifour decisionmaker is compensated on the basis of end of quarter results or the corresponding observed shareprice, we cannot expect much different behavior. Nor should we have expected anything different fromRichard Fuld and John Corzine.8 In this regard, it appears that all our examples point to a common theme:doing business like there is no tomorrow. Paraphrasing Richard Branson, sustainability considerations wouldcall for conducting business as if there is a tomorrow.

It should be noted that this is not a problem confined to corporate executive suites. Too often, itmanifests itself in many personal decisions as well as those made by governmental agencies. On theformer, let us suffice with the example of a dentist by the name of Thomas McFarland who, on August 22,2008, took his boat to Townsend Inlet near Avalon on the Jersey Shore and dumped a bagful of some 300dental-type needles and other medical waste from his medical office. The dumping sullied the coast in apopular area and forced beach closings at the height of vacation time. Dr. McFarland was obviously tryingto maximize his own profits in having chosen to avoid the costs of proper disposal of medical waste byexternalizing his costs to the society at large.9

As an example of the latter, consider the story of what took place in Treece, Kansas. A thriving boom townof the early 20th century, the unofficial capital of the ore-producing zone in the US. Rich in zinc, lead and ironore, it was home to 20,000 people and thriving. The mines closed in the early 1970s and the miningcompanies left town. By 2009, the city's population had dwindled to 140 persons living in “a toxic wastedump of lead-tinged dust, contaminated soil and sinkholes; children riding their bikes around enormousmounds of pulverized rock laced with lead and iron.”10

The companies that mined Treece, Kansas and left it in such condition did so, most likely, with a singleobjective inmind; maximizing shareholder wealth. There is a possibility that they did sowhile those chargedwith the responsibility of looking after the interests of Treece and its residents were looking the other way.More likely, they did so with the full consent of these “trustees” and “responsible” officials. However, suchconsent and approval was not granted with any intendedmalice. To the contrary, it can be argued that it wasgranted out of a desire to maximize the immediate benefits accrued to the community, albeit without anyconsideration given to the sustainability of such benefits and the costs attached thereto. It can also be arguedthat these officials did somotivated by the political expediency of incentives that drive popular local elections,namely the creation of jobs and other visible/measureable benefits to the electoral base. Uniontown, Alabamais a contemporary example, on a smaller scale, ofwhatmay have happened in Treece, Kansas a century earlier.In return for a $30 million infusion of cash into the county's budget and a promise of 30 new jobs, officialsthere agreed to bury three million cubic yards of coal ash in Uniontown's landfill.11 The coal ash, from a

6 A US House of Representative report issued on November 15, 2012 concluded that John Corzine's risky bets aided the downfall ofMF Global.

7 See New York Times, “Corzine Crashes Like its 2008,” October 31, 2011.8 The only exception would have been in the case of Bernard Madoff, where he knowingly committed fraud. But, even in his case

we have a glaring disregard for the question of sustainability.9 See the Chicago Tribune, September 5, 2008.

10 See “Welcome to Our Town: Wish We Weren't Here,” New York Time, September 14, 2009.11 See “Clash in Alabama Over Landfill's Plan to Take Tennessee Coal Ash” New York Times, September 30, 2009.

105A.M. Fatemi, I.J. Fooladi / Global Finance Journal 24 (2013) 101–113

massive spill in an East Tennessee power plant, had a high enough concentration of toxins to be classified as a“hazardouswaste” by the Environmental Protection Agency.12Given that themain source of livelihood for theresidents of Uniontown is catfish farming, and that the area is subject to frequent floods and tornadoes, it isnot clear that the officials making the decision on behalf of its residents had evaluated the (admittedly harderto measure) long term costs of their decision before proceeding.13

2. The academic problem

Of course, one may blame mankind's impatience and the relative ease of identifying and measuringshorter-term costs and benefits as reasons for these kinds of failures. However, a more compelling argumentcan be forwarded that, although as advanced societies we have made significant progress on manylonger-term projects (space exploration is one example); we have not made adequate progress on issuesdealing with sustainability. Indeed, one can easily trace back the reason for this failure all the way to the fieldof education. Evaluating our students on the basis of outcomes that are dependent on their ability to performon standardized tests, and their mastery of test-taking techniques, as opposed to deep learning and dealingwith unstructured problems, we condition them to focus on the short-term. In the field of finance,we go evenfurther along this path and drill down the notion that the only thing that matters is the maximization ofshareholder's wealth. Further, invoking the efficient markets hypothesis, we turn them into true believers ofthe gospel that today's share price is the only barometer that they ever need to watch for. By implication,therefore, all other issues can be safely ignored.14

Having been so indoctrinated, it should not come as a surprise that the occupants of corporate executivesuites (or those of the boardrooms intended to provide for systems of checks and balances) have their eyesand minds trained exclusively on the short term payoffs within a me-first framework. Neither should we besurprised when officials who called the shots in Treece, Kansas, or a century later in Uniontown, Alabama didso with an apparent total disregard for the long-term consequences of their decisions. Of course, these areanecdotal examples. But, by no means are they isolated observations. A critical examination would revealmany other examples. However, whereas up to this point the offenders were able to get away with suchconduct, a different future lies ahead. Driven by dramatic changes in the dynamics of the marketplace, andinnovations in mechanisms for settling up (both ex-ante and ex-post), a radically different decision makingframework is called for. As a result, there is an acute need for a change in our paradigm. The existing models,that give rise to the kinds of unacceptable outcomes we have reviewed, are no longer tenable and a newframeworkwill need to replace the current. Otherwise, it will be just amatter of exact time as towhenwewilljoin the ranks of dinosaurs.

2.1. Sustainable value creation

The examples outlined in Section 1.1 share another common characteristic: adoption of a narrowdefinition of value; one that ignores and otherwise externalizes some of the costs of a project. These examplesshare another common feature aswell: unacceptable outcomes. A failure to take into consideration the socialand the environmental costs of a project along with its economic benefits has the potential to create theseunacceptable, and sometimes disastrous, outcomes. Alternatively stated, in order to avoid unacceptableoutcomes the decisionmaker needs to recognize, and account for, all costs and benefits (economic, social andenvironmental) before adopting (or rejecting) a project. In the words of Michael Treschow, Chairman of

12 Mercury, arsenic and other substances that are filtered out, by devices designed to control air pollution, end up in the ash andmake it highly toxic.13 For a critical review of the questionable outcomes of governmental subsidies aimed at creation of jobs see the New York Timesseries on United States of Subsidies, starting with “As Companies Seek Tax Deals, Governments Pay High Price” on December 1, 2012and concluding with “Lines Blur as Texas Gives Industries a Bonanza” and “Michigan Town Woos Hollywood, but Ends Up With a BitPart” on December 2 and 3, 2012.14 Interestingly, the arguments in favor of this emphasis on the easily identifiable and the shorter-term results and against moreinclusive and robust models have recently become intense. In contrast, elsewhere, we have made significant strides in becoming lessself-centered and more mindful, including the adoption of rules and laws aimed at protecting the rights of vulnerable groups(children, animals, etc.), and the sanctity of life (consider the extreme expenses we incur by dispatching ambulances, fire trucks andpolice to sites of minor traffic accidents).

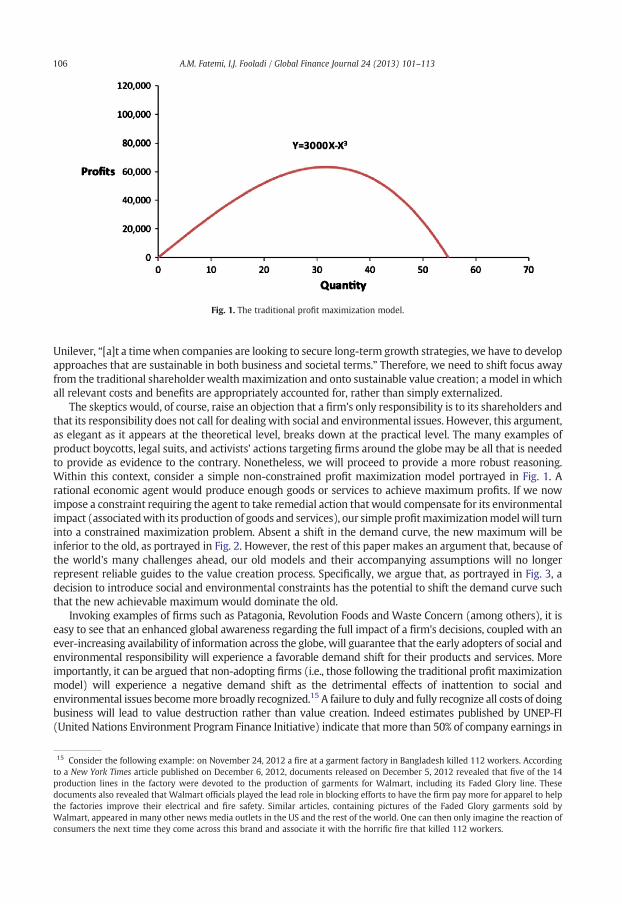

Fig. 1. The traditional profit maximization model.

106 A.M. Fatemi, I.J. Fooladi / Global Finance Journal 24 (2013) 101–113

Unilever, “[a]t a timewhen companies are looking to secure long-term growth strategies, we have to developapproaches that are sustainable in both business and societal terms.” Therefore, we need to shift focus awayfrom the traditional shareholder wealth maximization and onto sustainable value creation; a model in whichall relevant costs and benefits are appropriately accounted for, rather than simply externalized.

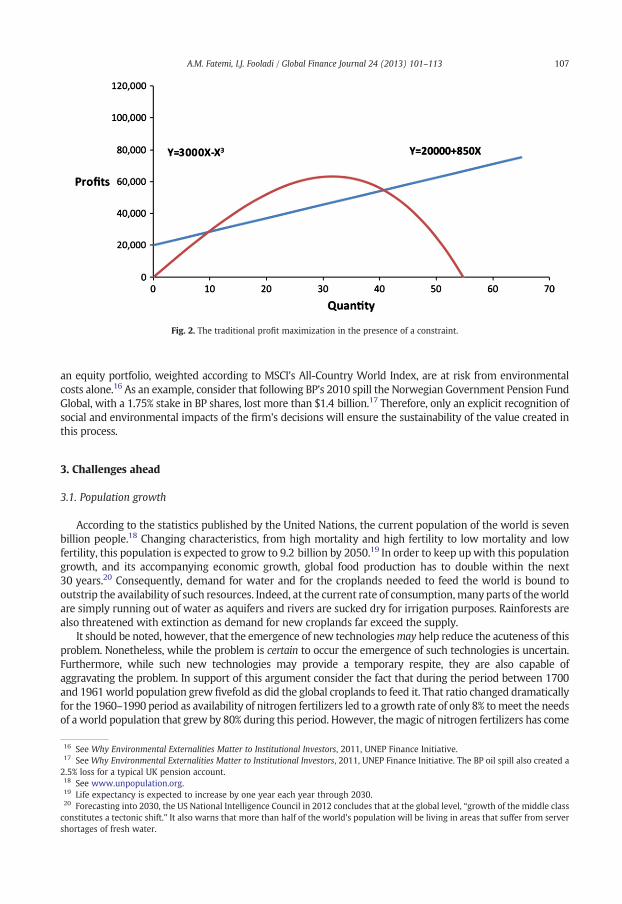

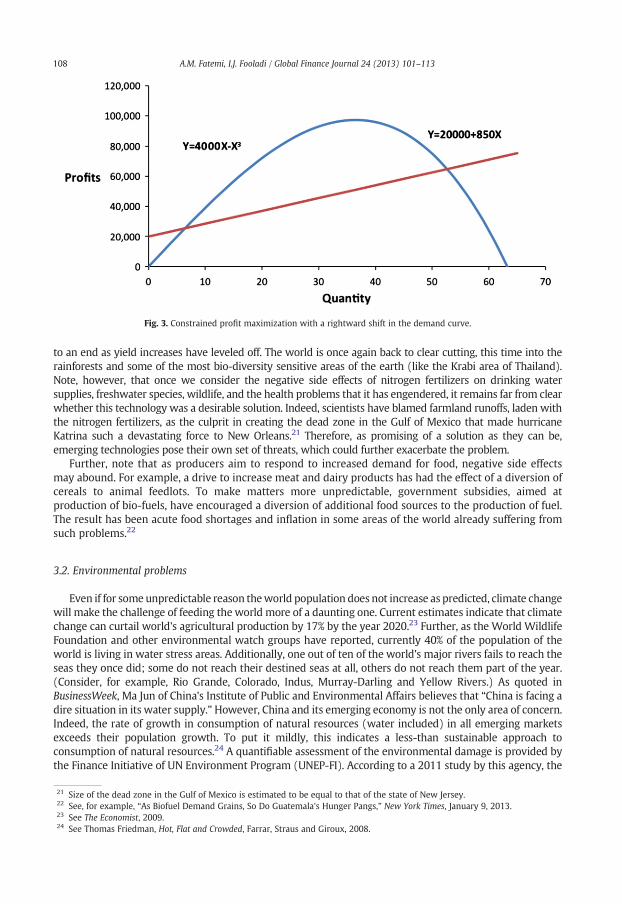

The skeptics would, of course, raise an objection that a firm's only responsibility is to its shareholders andthat its responsibility does not call for dealingwith social and environmental issues. However, this argument,as elegant as it appears at the theoretical level, breaks down at the practical level. The many examples ofproduct boycotts, legal suits, and activists' actions targeting firms around the globe may be all that is neededto provide as evidence to the contrary. Nonetheless, we will proceed to provide a more robust reasoning.Within this context, consider a simple non-constrained profit maximization model portrayed in Fig. 1. Arational economic agent would produce enough goods or services to achieve maximum profits. If we nowimpose a constraint requiring the agent to take remedial action that would compensate for its environmentalimpact (associatedwith its production of goods and services), our simple profitmaximizationmodel will turninto a constrained maximization problem. Absent a shift in the demand curve, the new maximum will beinferior to the old, as portrayed in Fig. 2. However, the rest of this paper makes an argument that, because ofthe world's many challenges ahead, our old models and their accompanying assumptions will no longerrepresent reliable guides to the value creation process. Specifically, we argue that, as portrayed in Fig. 3, adecision to introduce social and environmental constraints has the potential to shift the demand curve suchthat the new achievable maximum would dominate the old.

Invoking examples of firms such as Patagonia, Revolution Foods and Waste Concern (among others), it iseasy to see that an enhanced global awareness regarding the full impact of a firm's decisions, coupled with anever-increasing availability of information across the globe, will guarantee that the early adopters of social andenvironmental responsibility will experience a favorable demand shift for their products and services. Moreimportantly, it can be argued that non-adopting firms (i.e., those following the traditional profit maximizationmodel) will experience a negative demand shift as the detrimental effects of inattention to social andenvironmental issues becomemore broadly recognized.15 A failure to duly and fully recognize all costs of doingbusiness will lead to value destruction rather than value creation. Indeed estimates published by UNEP-FI(United Nations Environment Program Finance Initiative) indicate that more than 50% of company earnings in

15 Consider the following example: on November 24, 2012 a fire at a garment factory in Bangladesh killed 112 workers. Accordingto a New York Times article published on December 6, 2012, documents released on December 5, 2012 revealed that five of the 14production lines in the factory were devoted to the production of garments for Walmart, including its Faded Glory line. Thesedocuments also revealed that Walmart officials played the lead role in blocking efforts to have the firm pay more for apparel to helpthe factories improve their electrical and fire safety. Similar articles, containing pictures of the Faded Glory garments sold byWalmart, appeared in many other news media outlets in the US and the rest of the world. One can then only imagine the reaction ofconsumers the next time they come across this brand and associate it with the horrific fire that killed 112 workers.

Fig. 2. The traditional profit maximization in the presence of a constraint.

107A.M. Fatemi, I.J. Fooladi / Global Finance Journal 24 (2013) 101–113

an equity portfolio, weighted according to MSCI's All-Country World Index, are at risk from environmentalcosts alone.16 As an example, consider that following BP's 2010 spill the Norwegian Government Pension FundGlobal, with a 1.75% stake in BP shares, lost more than $1.4 billion.17 Therefore, only an explicit recognition ofsocial and environmental impacts of the firm's decisions will ensure the sustainability of the value created inthis process.

3. Challenges ahead

3.1. Population growth

According to the statistics published by the United Nations, the current population of the world is sevenbillion people.18 Changing characteristics, from high mortality and high fertility to low mortality and lowfertility, this population is expected to grow to 9.2 billion by 2050.19 In order to keep upwith this populationgrowth, and its accompanying economic growth, global food production has to double within the next30 years.20 Consequently, demand for water and for the croplands needed to feed the world is bound tooutstrip the availability of such resources. Indeed, at the current rate of consumption,many parts of theworldare simply running out of water as aquifers and rivers are sucked dry for irrigation purposes. Rainforests arealso threatened with extinction as demand for new croplands far exceed the supply.

It should be noted, however, that the emergence of new technologiesmay help reduce the acuteness of thisproblem. Nonetheless, while the problem is certain to occur the emergence of such technologies is uncertain.Furthermore, while such new technologies may provide a temporary respite, they are also capable ofaggravating the problem. In support of this argument consider the fact that during the period between 1700and 1961world population grew fivefold as did the global croplands to feed it. That ratio changed dramaticallyfor the 1960–1990 period as availability of nitrogen fertilizers led to a growth rate of only 8% tomeet the needsof a world population that grew by 80% during this period. However, themagic of nitrogen fertilizers has come

16 See Why Environmental Externalities Matter to Institutional Investors, 2011, UNEP Finance Initiative.17 See Why Environmental Externalities Matter to Institutional Investors, 2011, UNEP Finance Initiative. The BP oil spill also created a2.5% loss for a typical UK pension account.18 See www.unpopulation.org.19 Life expectancy is expected to increase by one year each year through 2030.20 Forecasting into 2030, the US National Intelligence Council in 2012 concludes that at the global level, “growth of the middle classconstitutes a tectonic shift.” It also warns that more than half of the world's population will be living in areas that suffer from servershortages of fresh water.

Fig. 3. Constrained profit maximization with a rightward shift in the demand curve.

108 A.M. Fatemi, I.J. Fooladi / Global Finance Journal 24 (2013) 101–113

to an end as yield increases have leveled off. The world is once again back to clear cutting, this time into therainforests and some of the most bio-diversity sensitive areas of the earth (like the Krabi area of Thailand).Note, however, that once we consider the negative side effects of nitrogen fertilizers on drinking watersupplies, freshwater species, wildlife, and the health problems that it has engendered, it remains far from clearwhether this technology was a desirable solution. Indeed, scientists have blamed farmland runoffs, laden withthe nitrogen fertilizers, as the culprit in creating the dead zone in the Gulf of Mexico that made hurricaneKatrina such a devastating force to New Orleans.21 Therefore, as promising of a solution as they can be,emerging technologies pose their own set of threats, which could further exacerbate the problem.

Further, note that as producers aim to respond to increased demand for food, negative side effectsmay abound. For example, a drive to increase meat and dairy products has had the effect of a diversion ofcereals to animal feedlots. To make matters more unpredictable, government subsidies, aimed atproduction of bio-fuels, have encouraged a diversion of additional food sources to the production of fuel.The result has been acute food shortages and inflation in some areas of the world already suffering fromsuch problems.22

3.2. Environmental problems

Even if for some unpredictable reason theworld population does not increase as predicted, climate changewill make the challenge of feeding the world more of a daunting one. Current estimates indicate that climatechange can curtail world's agricultural production by 17% by the year 2020.23 Further, as the World WildlifeFoundation and other environmental watch groups have reported, currently 40% of the population of theworld is living in water stress areas. Additionally, one out of ten of the world's major rivers fails to reach theseas they once did; some do not reach their destined seas at all, others do not reach them part of the year.(Consider, for example, Rio Grande, Colorado, Indus, Murray-Darling and Yellow Rivers.) As quoted inBusinessWeek, Ma Jun of China's Institute of Public and Environmental Affairs believes that “China is facing adire situation in its water supply.”However, China and its emerging economy is not the only area of concern.Indeed, the rate of growth in consumption of natural resources (water included) in all emerging marketsexceeds their population growth. To put it mildly, this indicates a less-than sustainable approach toconsumption of natural resources.24 A quantifiable assessment of the environmental damage is provided bythe Finance Initiative of UN Environment Program (UNEP-FI). According to a 2011 study by this agency, the

21 Size of the dead zone in the Gulf of Mexico is estimated to be equal to that of the state of New Jersey.22 See, for example, “As Biofuel Demand Grains, So Do Guatemala's Hunger Pangs,” New York Times, January 9, 2013.23 See The Economist, 2009.24 See Thomas Friedman, Hot, Flat and Crowded, Farrar, Straus and Giroux, 2008.

109A.M. Fatemi, I.J. Fooladi / Global Finance Journal 24 (2013) 101–113

annual environmental costs attributable to global human activity are estimated at $6.6 trillion, equating to11% of 2008 global GDP.25 The same report puts a price tag of $2.14 trillion on the costs of environmentaldamage caused by the world's largest 3000 publicly traded firms in 2008.

3.3. Consumption problem

Let us define sustainable consumption as one that enables the population to enjoy the available goods andservices at a level that would preserve the next generation's ability to do the same. Given this definition,current global consumption is 1.5 times its sustainable level.26 Needless to say, this ratio is a positive functionof the degree of economic development; much higher in the developed world and highest is the US. WorldWildlife Fund has estimated that if the rest of the world is granted their wish to consume at the same rate asthe average American household (while holding the US rate constant), an equivalent of 11 planet earths willbe needed to support global consumption.27 This is obviously not feasible and, therefore, theworld has to finda way of living within its means.28 Arguably, one of the easiest methods of dealing with this problemmay beto devise new methods to combat food waste. A recent report by UK's Institution of Mechanical Engineersindicates that almost asmuch as half of the food produced in theworld currently ends up inwaste each year.29

The report lists many factors as contributors to this problem: strict sell-by dates, poor infrastructure, and buyone-get-one free promotions among them. Included in this waste are vegetables as well as meats. However,transitioning into our next topic, it takes 20–50 times the amount ofwater to produce a given quantity ofmeatthan it does to produce the same amount of vegetables.

3.4. Water issues

Estimates compiled by the UN indicate that currently about 700 million people face water scarcity. Moreworrisome are the estimates that the combined effects of climate change, population growth and theincreasing per capita demand for waterwould force this number up to three billion by the year 2025. Further,it is estimated that over a billion people currently lack access to cleanwater, and that about 2.6 billion peoplelack adequate sanitation. Indeed, about 80% of diseases in the developingworld arewater related, resulting in1.8 million deaths each year due to diarrhea. Alarmingly, 90% of such deaths are children under the age of five.Finally, considering the fact that agriculture already accounts for 70% of human usage of fresh water and thatwater scarcity is only likely to worsen, many analysts have become increasingly convinced that the wars offuture are likely to have water at their root.

3.5. Climate change

Alarmed by the preponderance of scientific evidence on human-activity relatedwarming of the planet thedecade of seventies saw the birth of a vigorous debate among policy makers across the globe for possiblesolutions to the problemof climate change. However, the 1990switnessed the emergence of a powerful lobbythat began to question these findings. Financed generously by those with a vested interest in status quo, thislobby began challenging the veracity of the climate change evidence. Taking a page from the book of tacticsutilized by the tobacco industry to question the reliability of evidence, this lobby has been successful inforestalling action to combat global warming. Meanwhile, aided simply by anecdotal observations, publicopinion has been shifting in favor of some form action to combat global warming.30 The annual price tag

25 See Why Environmental Externalities Matter to Institutional Investors, 2011, UNEP Finance Initiative.26 WWF, Living Planet Report, wwf.org.27 See www.wwf.org.28 Consider, for example, fish as one component of global food chain. WWF statistics indicate that the global supply of freshwaterspecies is being depleted at an alarmingly high rate. Holding 1970 as the reference point, global freshwater species population indexstand at less than 50%.29 Global Food Waste Not, Want Not, Institution of Mechanical Engineers, January 2013.30 Extreme weather patterns, including unusually strong hurricanes and blizzards, as well as alarming patterns of air pollution havebeen contributing factors in this evolutionary process. For example, a January 14, 2013 Financial Times article reporting on the qualityof air in Beijing, indicated that the Chinese government had recorded 900 mg of particulates per square meter, compared with theusual scale of 50 (healthy) to 500 (dangerous).

110 A.M. Fatemi, I.J. Fooladi / Global Finance Journal 24 (2013) 101–113

associated with climate change is now running at $1.2 trillion, its annual human death toll is estimated at astaggering 400,000 persons, and is wiping 1.6% annually from global GDP.31 To most decision makers, and tomost electorates, this is not an acceptable outcomes and a change of course is called for.

3.6. Energy

Economic growth, particularly in China, India and the rest of the emerging markets, will give rise to anexplosive increase in demand for energy. Indeed, estimates indicate that world energy demand could nearlydouble by 2030, with India and China accounting for more than half of the increase. By that time, fossil fuelswill bemeeting 80% of theworld's energy demand. The heavy reliance on fossil fuelswill take place in spite ofa projected rate of growth of 7.2% per year in renewable sources, principally wind and solar. However, as ifclimate change is not a source of immediate risk, approximately 1000 coal-fired plants without CO2 captureare in various stages of planning and construction across the globe. Ironically, driven by a desire to become“energy self-sufficient” many countries, including the US, have started diverting agricultural products(sources of foods to many) into the production of fuel. The shortsightedness of these policies is fairly obvious,given that inmost cases production of biofuels results in a net loss of energy. Additionally, when evaluated inthe context of population growth, these kinds of policies are bound to further exacerbate the challenge offeeding theworld. For example, considering that theUnited States is currently using 40% of its crop to producebiofuel, it is not surprising that tortilla prices have doubled in Guatemala, a country that imports nearly half ofits corn. At the same time, Guatemala's lush land has proved ideal for producing raw materials for biofuels.Suchitepéquez Province, a major corn-producing region five years ago, is now carpeted with sugar cane andAfrican palm.32

4. Sustainable finance

Although not exhaustive in its presentation of the challenges ahead, the preceding list should besufficient in convincing even the most skeptical among us that business as usual is no longer a viableoption. Our current model of shareholder wealth maximization has given rise to practices that eitherexplicitly or implicitly favor the externalization of many costs of a project, thus creating unacceptableoutcomes. To return to a sustainable path, the current model needs to be discarded in favor of one thatappropriately accounts for the social and environmental costs of a project. Given the scope and themagnitude of the challenges ahead; (1) the early adopters of models that incorporate the social andenvironmental costs of doing business into their decision making framework will experience a favorabledemand shift for their products and services, and (2) the non-adopters will experience a negative demandshift as the detrimental effects of inattention to social and environmental issues become more broadlyrecognized.33 Therefore, failure to account for all costs of doing business will indeed lead to valuedestruction rather than value creation. Only an explicit recognition of social and the environmentalimpacts of the firm's decisions will ensure sustainability of the value created in this process. It should,however, be noted that doing so does not call for the NPV approach to be discarded. Rather, it calls for thefull consideration of all incremental, incidental, and opportunity costs as well as such benefits.

31 See32 Theeach ye33 A reclimateholding

Value0 ¼X

tCashFlowst= 1þ Costof Capitalð Þt

Therefore, in addition to the inclusion of usual set of cash flows, the sustainable value creationapproach calls for the explicit recognition of incremental cash flows attributable to the firm's sustainabilityefforts. Examples include enhanced brand value, increased customer loyalty, improved ability to recruitand retain talent, ability to attract new customers (including those demanding social and environmental

Climate Vulnerability Monitor: A Guide to the Cold Calculus of A Hot Planet, Fundación DARA Internacional 2012.American renewable fuel standardmandates that an increasing volume of biofuel be blended into the nation's vehicle fuel supplyar to reduce carbon dioxide emissions from fossil fuels and to bolster the nation's energy security. New York Times, Jan 6, 2013.cent decision by one of US pension funds to divest itself off of the shares of oil companies, because of their contribution tochange, is one example of the likely trend ahead. See Financial Times, January 30, 2013, “US pension fund eyes selling oils.”

111A.M. Fatemi, I.J. Fooladi / Global Finance Journal 24 (2013) 101–113

results) and the option value of entering markets restricted to firms enjoying a reputation for theirsustainability efforts. It also calls for the explicit recognition of reduced costs due to lower water andenergy usage and the lower costs of: waste, employee healthcare, agency compliance, labor action, liabilityand litigation. Further, given that socially responsible firms do a better job of managing their risks (both asa matter of definition and as supported by empirical evidence), their lower cost of capital should also beaccounted for.34

Does such an approach actually pay off, or does all of this just add up to simple academic musings?Evidence is accumulating, at a fairly rapid rate, in support of the argument that firms can “do well by doinggood.” For example, evidence compiled by SAM, and reported in its annual reports provides strong support infavor of the argument that sustainability does pay off.35 Further, indirect support can be inferred through anexamination of the rate of growth in assets under management classified as socially responsible investments.As reported by Social Investment Forum Foundation, SRI assets under management in the US grew from$639 billion in 1995 tomore than $3 trillion or one out of every eight dollars invested, in 2009. In comparison,European SRI under management was more than $7 trillion and nearly half of each dollar invested in 2009.

Meanwhile, empirical studies dealing with this question have also been accumulating at a rapid rate withthe majority of evidence in support of the notion that corporate social responsibility does create shareholdervalue. Utilizing a database provided by a large financial institution, Dimson, Karakas, and Li (2011) documentan average 4% abnormal return for firms that successfully initiate corporate social responsibility (CSR)engagement.36 They also document that when the firm's engagement is in the area of climate change orcorporate governance, the market reaction is stronger. This is consistent with the findings of El Ghoul,Guedhami, Kwok, and Mishra (2011), and Plumlee, Brown, Hayes, and Marshall (2010), who show that USfirms with superior CSR performance enjoy cheaper equity financing.

Barnea and Rubin (2005) find that at low levels of CSR expenditure, the link between theseexpenditures and a firm's value is positive, but that the relationship becomes negative when theseexpenditures go beyond a certain level. This kind of non-monotonic relationship is also reported by Gossand Roberts (2011) who study the cost of borrowing and find that firms at the lower end of the CSRspectrum bear a higher cost of borrowing. Utilizing data for 2261 firms in 43 countries over the 2002–2008period, Hawn and Ioannou (2012) examine the differential impacts of symbolic and substantive corporateESG actions on firm performance. Their results suggest that symbolic ESG actions in the presence of higherintangibles have a higher positive impact on the firm's market value. Also utilizing data from a largesample, Servaes and Tamayo (forthcoming) find that CSR activities enhance the value of the firm whenthey are accompanied by high public awareness (as proxied proxy by advertising intensity).

Evaluating the question from an investments perspective, and comparing returns of four indexes ofsocially responsible companieswith that of the S&P 500 index, Statman (2005) finds that Socially ResponsibleInvestment (SRI) indexes performed better than the S&P 500 during the 1990s and worse during the early2000s. On the other hand, comparing the characteristics of mutual funds investing in responsible firmswith agroup of randomly selected conventional funds, Bello (2005) reports that socially responsible funds do notdiffer significantly from conventional funds in characteristics such as diversification and returns. Statman andGlushkov (2009) report that an investment strategy that is long with CSR leaders and short with laggardswould have produced an annual excess risk-adjusted return of 6.12% for the period 1992–2007.

Using different CSR rankings and similar trading strategies, Derwall, Guenster, Bauer, and Koedijk (2005),Edmans (2010), and Kempf and Osthoff (2007) report similar findings on the presence of a significantrisk-adjusted outperformance. Fatemi, Fooladi, and Wheeler (2009) compare the characteristics of firms inthe DS 400 index with those of similar firms not included in the index. They report that when compared totheir control group over the period 1990–2005, firms in the DS 400 index produce statistically identicalreturns and exhibit similar market risk characteristics. However, they find that their idiosyncratic risk issignificantly lower in every year at the 1% level. They also report that firms that are added to the DS 400 indexexperience a positive abnormal returnupon the announcements of such occasions. The reverse holds forfirms

34 See Fatemi, Fooladi and Wheeler (2009) for evidence on socially responsible firms enjoying a lower risk profile.35 For example, in a comparison of the performance of sustainability leaders (top 20%) with laggards (bottom 20%) they report anoutperformance of 1.48 for the former and −1.46% for the latter, with corresponding tracking errors of 3.17 and 3.22. See “TheSustainability Yearbook 2010” SAM-Group.com.36 However, they find no market reaction where the engagement is not successful.

112 A.M. Fatemi, I.J. Fooladi / Global Finance Journal 24 (2013) 101–113

that are deleted from the index. Nofsinger andVarma (2012) study the performance of a sample of SRImutualfunds and their matching control groups over the 2000–2011 periods, and report finding that SRI fundsoutperform their peers during periods of financial crisis and underperform them during non-crisis periods.

Addressing the question from the broader sustainability perspective, Eccles, Ioannou, and Serafeim (2012)compare a group of 180 high sustainability corporations (those that voluntarily adopted environmental andsocial policies by 1993) to amatched sample of low sustainability firms. They find that high sustainability firmsexhibit fundamentally different characteristics in terms of the roles played by the boards of directors, theincentive structure of their executive, procedures for stakeholder engagement, and their tendency to be morelong-term oriented. They also report findings indicating that high sustainability firms significantly outperformtheir counterparts over the long term. Finally, in a comprehensive study of the effect of CSR on investmentperformance, Huppé (2011) reports finding a significant positive relationship between CSR and investmentperformance. However, comparing the pre- and post-2005 results, he finds that a trading strategy based on anequally-weighted, long-only portfolio of good CSR companies produced significantly lower abnormal returns inthe post-2005 period than it did in the 1992–2005 periods. He, therefore, concludes that it may have becomemore difficult to achieve superior investment results via a security selection process that is based on the CSRcriteria. As such, CSR characteristics may now be fully priced in the market value of these companies.

In summary, the majority of extant empirical evidence provides robust support for the proposition thatfirms are rewarded for their sustainability focus. Further, a growing body of evidence indicates thatexpectations of progressively better societal and environmental performance are being built into themarkets'valuation of the firm over time. This evidence combined with exponential increases in settling up costs ofsocial and environmental damage (both the ex-post and ex-ante) suggests that sustainable value creation isthe only viable way forward. Early adopter of such a framework (those that discard the traditional model thatemphasizes the short term and embrace the sustainable value creationmodel in its place)will be rewarded interms of a market value premium. Firms that choose not to adopt the model will become laggards in theprocess of creating value for shareholders.

5. Conclusions

In this paperwe argue that the old approach to shareholderwealthmaximization is no longer a valid guideto the creation of sustainable wealth. We propose the adoption of a framework that explicitly recognizes allincidental and incremental costs and benefits of a project, including all hereto externalized.We argue that (a)changes in the dynamics of the marketplace has necessitated such a shift in paradigm and that (b) firms thatfail to adopt the sustainable value creation model will become the laggards of their sector, witnessing agradual erosion in their market values. As Roberts (2004) posits “[f]irms are institutions created to servehuman needs” (p. 20) and, therefore, “[i]t is also necessary that all the relevant interests [not just those ofshareholders] are recognized and taken into account” (p. 21). As Porter and Kramer (2011) argue, the existingparadigm of value creation is outdated. In their terminology, “shared value” is the right way of thinking aboutvalue creation so that both the firm and the community benefit from the firm's activities. Alternatively, asJanicke and Jaco (2012) hypothesize, focus on sustainability will amount to the Third Industrial Revolution.These new realities call for modifications to the traditional valuation framework in a manner that takes intoaccount all social and environmental impacts of a firm's activities. If the firm chooses either to ignore suchimpacts, or to externalize them, it may be able to buy itself some time. However, the costs of ex-post settlingup will exceed their ex-ante levels by a significant margin. Indeed, emerging evidence suggests that theprobability of ruin may be much higher for such firms.37

37 This is supported by considering the fate of firms that pursue the narrow definition of shareholder wealth maximization only tofind themselves forced into bankruptcy (e.g., see the examples in the first section of this paper) as well as those that comedangerously close to ruin (e.g., BP). Further support is provided by empirical results such as those of Flammer (2011) who reportsthat during the three decades since 1980, negative environmental news has affected firm values at an increasingly negative rate (anaverage of .42% drop in the stock price during the 1980–1989 period, 0.66% drop in the 1990–1999 period, and 1.12% drop during the2000–2009 period). She also reports finding that positive news on a company's environmental behavior is rewarded by an averageincrease in stock returns of 0.84%, although the positive investor response to good environmental news has been tapering off in morerecent years. This latter finding is consistent with our proposition that good environmental, social and governance performance willbecome the new norm.

113A.M. Fatemi, I.J. Fooladi / Global Finance Journal 24 (2013) 101–113

We have labeled this the sustainable value creation model. Within this model, valuation of a firm thatignores its social and environmental responsibilitieswould require the analyst to fully account for all inherentcosts of environmental and social degradation, including those associated with cleanup, replenishment,workforce retraining, and community rebuilding, among others. Valuation of firms that have adopted thesustainable value creation framework, on the other hand, calls for a full accounting of the benefits due to suchentities. Examples include enhanced brand value, increased customer loyalty, improved talent recruitmentand retention, the option value of entering markets restricted to firms enjoying a reputation for theirsustainability efforts, and the ability to attract new customers (including those demanding social andenvironmental results). For these firms, there also needs to be an explicit recognition of the incrementalreduction of costs due to sustainability efforts; e.g., savings on water and energy usage, lower costs of waste,reduction of employee healthcare costs, lower agency compliance costs, and lower expected costs associatedwith labor action, liability and litigation. Further, given that firms operating within a sustainable frameworkare less risky, their lower cost of capital also needs to be accounted for. This paper further argues that it is onlya matter of time before good environmental, social and governance performance will become the new norm.Therefore, and as confirmed by empirical evidence, firms that fail to recognize their environmental and socialresponsibilities will find themselves valued at a discount relative to their peers.

References

Barnea, A., & Rubin, A. (2005). Corporate social responsibility as a conflict between owners.Working paper. : Simon Fraser University.Bello, Z. (2005). Socially responsible investing and portfolio diversification. Journal of Financial Research, 28(41), 57.Derwall, J., Guenster, N., Bauer, R., & Koedijk, K. (2005). The eco-efficiency premium puzzle. Financial Analysts Journal, 61(51), 63.Dimson, E., Karakas, O., & Li, X. (2011). Activism in corporate social responsibility. Paper presented at the annual meetings of the

financial management, Europe, Istanbul, Turkey.Eccles, R. G., Ioannou, I., & Serafeim, G. (2012). The impact of a corporate culture of sustainability on corporate behavior and

performance. National Bureau of Economic Research Working Paper Series No. 17950.Edmans, A. (2010). Does the stock market fully value intangibles? Employee satisfaction and equity prices.Working paper. University

of Pennsylvania.El Ghoul, S., Guedhami, O., Kwok, C. C. Y., & Mishra, D. R. (2011). Does corporate social responsibility affect the cost of capital? Journal

of Banking and Finance, 35, 2388–2406.Fatemi, A., Fooladi, I., & Wheeler, D. (2009). The Relative valuation of socially responsible firms: An exploratory study. In H. -C. de

Bettignies, & F. Lépineux (Eds.), Finance for a better world: The shift toward sustainability. Basingstoke, UK: Palgrave Macmillan.Flammer, C. (2011). Corporate social responsibility and shareholder value: The environmental consciousness of investors. MIT Sloan

School of Management.Goss, A., & Roberts, G. (2011). The impact of corporate social responsibility on the cost of bank loans. Journal of Banking and Finance,

35, 1794–1810.Hawn, O., & Ioannou, I. (2012). Do actions speak louder than words? The case of corporate social responsibility (CSR). SSRN working

paper series.Huppé, G. A. (2011). Alpha's tale: The economic value of CSR. PRI academic network conference, Sigtuna, Sweden.Janicke, M., & Jaco, Klaus (2012). A third industrial revolution? Solutions to the crisis of resource-intensive growth. SSRN working

paper series.Kempf, A., & Osthoff, P. (2007). The effect of socially responsible investing on financial performance. European Financial Management,

13, 908–922.Nofsinger, J., & Varma, A. (2012). Socially responsible funds and market crises. SSRN working paper series.Plumlee, M., Brown, D., Hayes, R. M., & Marshall, S. (2010). Voluntary environmental disclosure quality and firm value: Further

evidence. Working paper. University of Utah and Portland State University.Porter, M. E., & Kramer, M. R. (2011). Creating shared value. Harvard Business Review, 89(62), 77.Roberts, J. (2004). The modern firm. Oxford: Oxford University Press.Servaes, H., & Tamayo, A. (2013). The impact of corporate social responsibility on firm value, the role of customer awareness.

Management Science (Forthcoming).Statman, M. (2005). Socially responsible indexes: Composition and performance. SSRN working paper series.Statman, M., & Glushkov, D. (2009). The wages of social responsibility. Financial Analysts Journal, 65(33), 46.