structuring indirect rates

TRANSCRIPT

Structuring Indirect RatesDonna M. Dominguez | June 22, 2016

http://blogs.aronsonllc.com/fedpoint/

2© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Course Objective

• To provide knowledge in understanding your company’s indirect rate structure to:

– Yield Auditable Rates that Comply with Federal Regulations

– Structure Competitive Indirect Rates

3© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Agenda

• Definitions

• Composition of Indirect Pools and Bases

• Various Indirect Rate Structures

• Wrap Rates

• Q & A

4© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Definitions

5© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

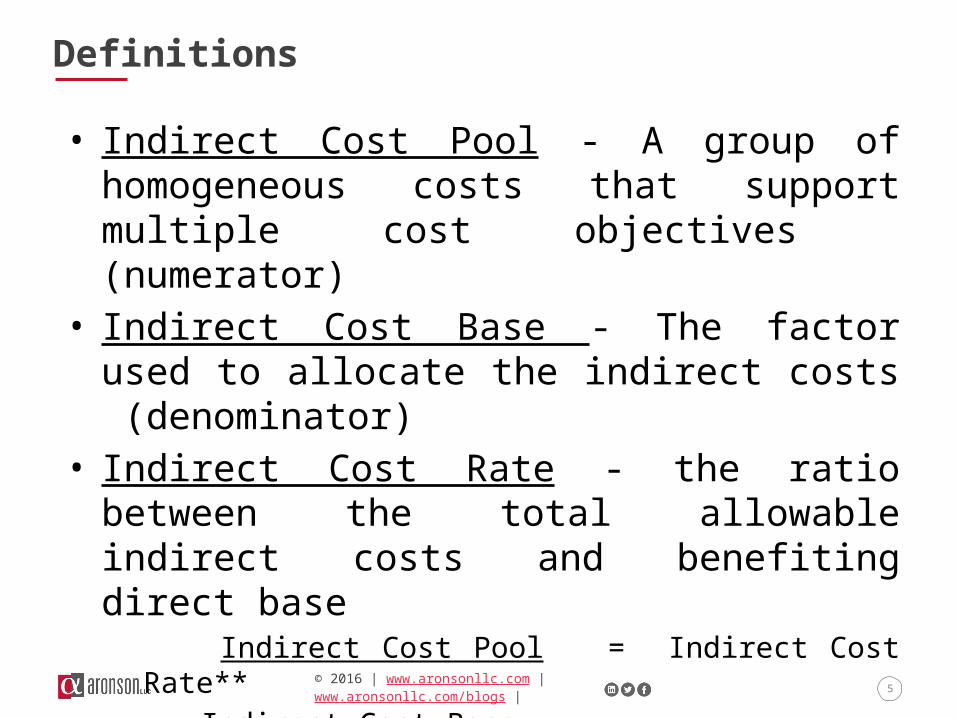

Definitions

• Indirect Cost Pool - A group of homogeneous costs that support multiple cost objectives (numerator)

• Indirect Cost Base - The factor used to allocate the indirect costs (denominator)

• Indirect Cost Rate - the ratio between the total allowable indirect costs and benefiting direct base Indirect Cost Pool = Indirect Cost Rate** Indirect Cost Base

**An indirect cost rate percentage is calculated by dividing he pool by the base

6© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Composition of Indirect Pools and Bases

7© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

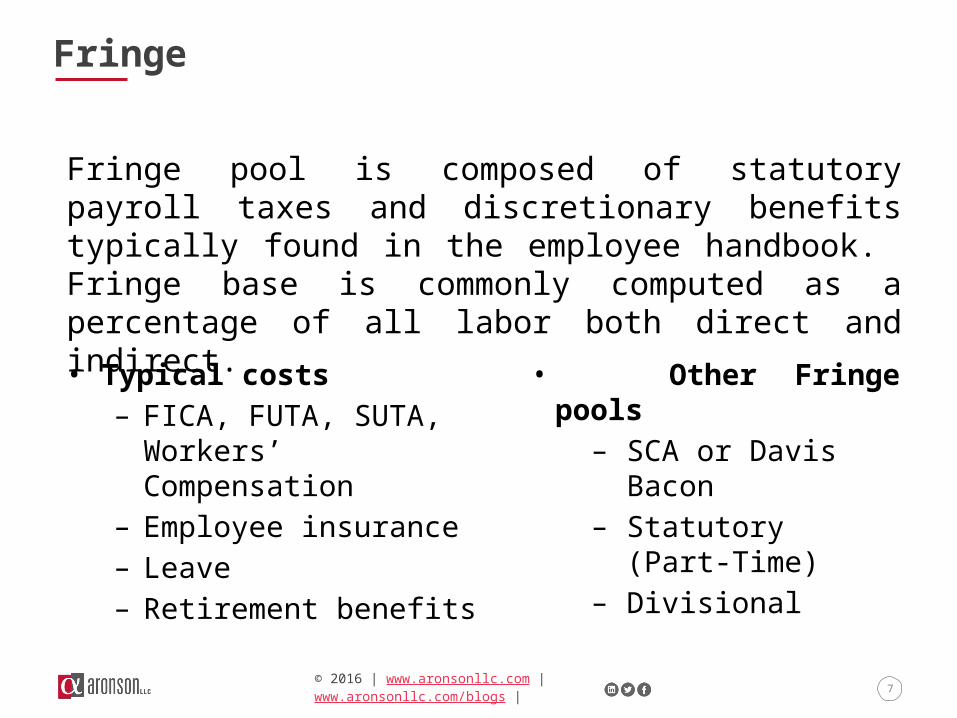

Fringe

• Typical costs

– FICA, FUTA, SUTA, Workers’ Compensation

– Employee insurance– Leave– Retirement benefits

• Other Fringe pools– SCA or Davis Bacon– Statutory (Part-Time)– Divisional

Fringe pool is composed of statutory payroll taxes and discretionary benefits typically found in the employee handbook. Fringe base is commonly computed as a percentage of all labor both direct and indirect.

8© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

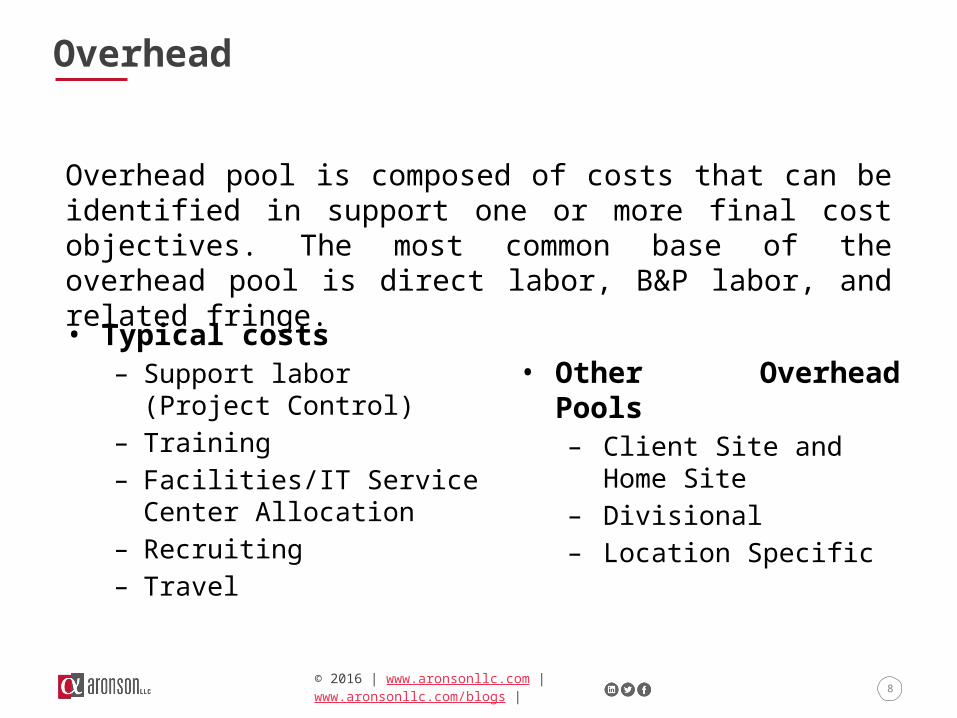

Overhead

• Typical costs– Support labor (Project Control)– Training– Facilities/IT Service Center

Allocation– Recruiting – Travel

• Other Overhead Pools– Client Site and Home Site– Divisional– Location Specific

Overhead pool is composed of costs that can be identified in support one or more final cost objectives. The most common base of the overhead pool is direct labor, B&P labor, and related fringe.

9© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Service Centers

Service Centers or intermediate pools are set up to collect costs that are attributable to multiple cost objectives in order that they may be fairly and equitably allocated in a causal/benefit relationship. • Most common: Facilities and IT/Communication • Reasonable basis allocation methods: Labor Hours, Labor Dollars,

Headcount, or Square Footage• Typical costs in a facility service center

– Rent– Supplies– Property taxes– Depreciation

10© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

General and Administrative

•Typical costs– Accounting & Finance– Contract Administration– General Management– Facilities/IT Service Center

Allocation– Business Development

• Other G&A pools

– Segments

G&A pool is composed of indirect expenses that cannot be easily attributed to any specific contract objective but are for the general benefit of the company as a whole. There are two types of G&A base total costs input or value added (the most common value added G&A base is over total costs before B&P/IR&D and SM&H base).

11© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Subcontract & Material Handling

Subcontract & Material Handling pool is composed of costs that support the award and administration of subcontracts and purchase orders. The most common base of the subcontract & material handling pool is subcontract labor, subcontractor travel & ODCs, and materials.

• Typical costs– Subcontracts labor & ODCs– Accounts Payable for Subcontractors– Facilities/IT Service Center Allocation– Travel

12© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Various Indirect Rate Structures

13© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

What is Your Indirect Rate Structure ?

• Single Rate Structure– G&A rate only

• Two Tier Rate Structure – Overhead (one or more) and G&A

• Three Tier Rate Structure– Fringe– Overhead (one or more)– G&A

14© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Wrap Rates

15© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

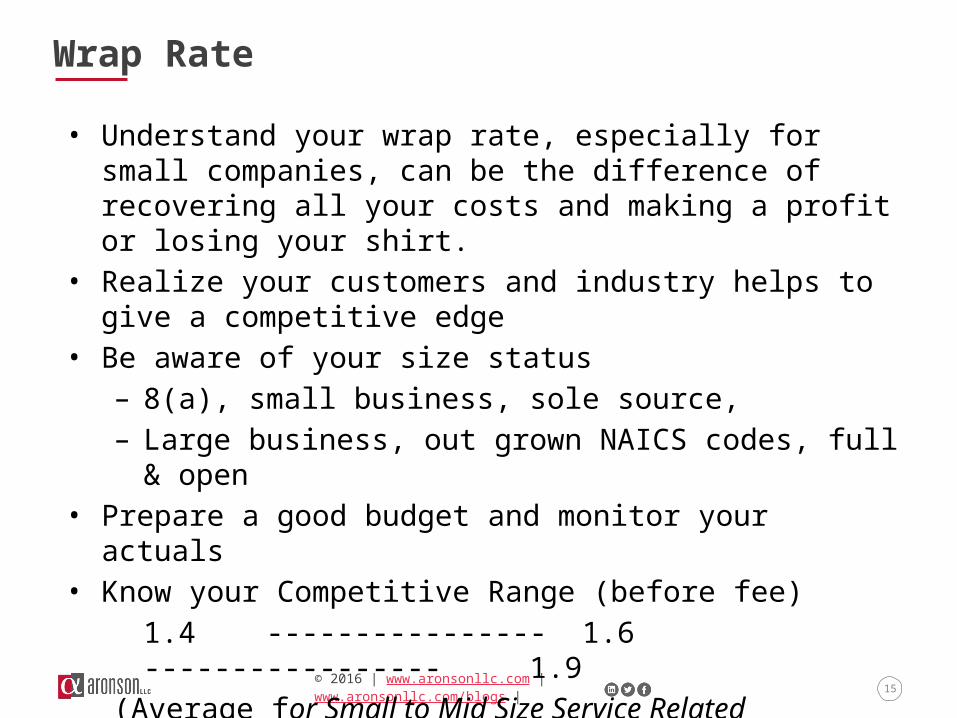

Wrap Rate

• Understand your wrap rate, especially for small companies, can be the difference of recovering all your costs and making a profit or losing your shirt.

• Realize your customers and industry helps to give a competitive edge• Be aware of your size status

– 8(a), small business, sole source,– Large business, out grown NAICS codes, full & open

• Prepare a good budget and monitor your actuals• Know your Competitive Range (before fee)

1.4 ---------------- 1.6 ----------------- 1.9(Average for Small to Mid Size Service Related Government Contractor)

16© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

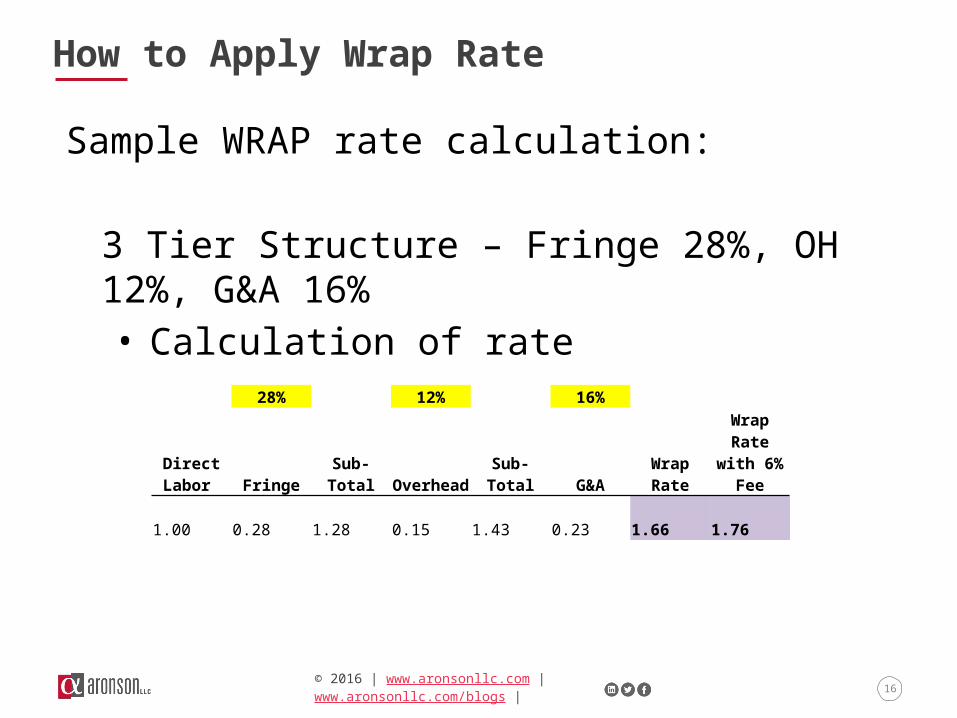

How to Apply Wrap Rate

Sample WRAP rate calculation:

3 Tier Structure – Fringe 28%, OH 12%, G&A 16%• Calculation of rate

28% 12% 16%

Direct Labor Fringe Sub-Total Overhead Sub-Total G&A

Wrap Rate

Wrap Rate with 6% Fee

1.00 0.28 1.28 0.15 1.43 0.23 1.66 1.76

17© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

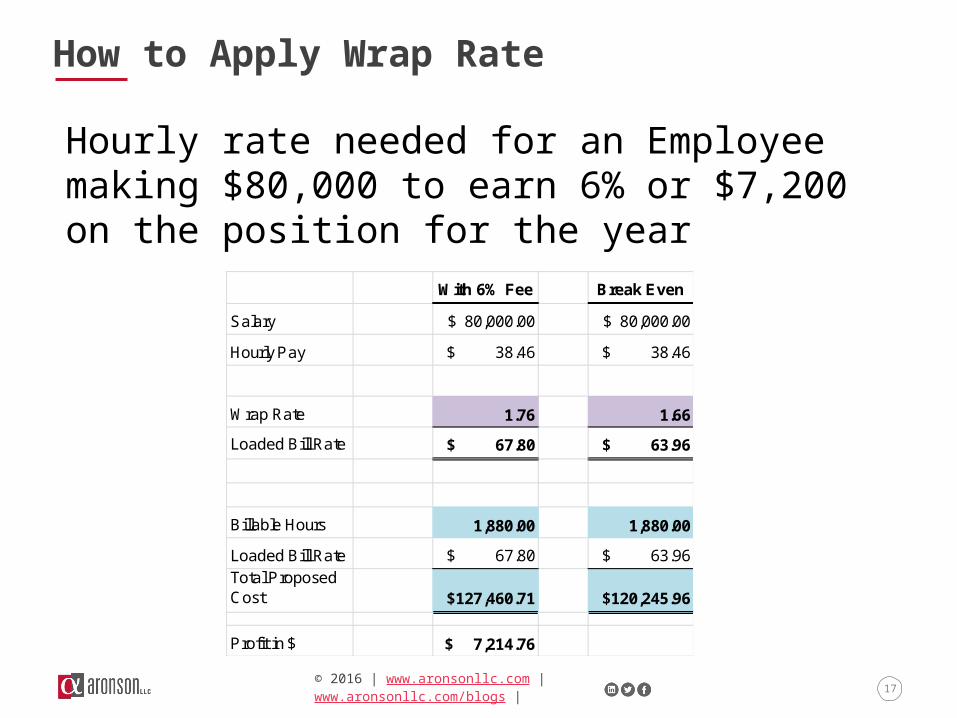

How to Apply Wrap Rate

Hourly rate needed for an Employee making $80,000 to earn 6% or $7,200 on the position for the year

With 6% Fee Break Even

Salary $ 80,000.00 $ 80,000.00

Hourly Pay $ 38.46 $ 38.46

Wrap Rate 1.76 1.66

Loaded Bill Rate $ 67.80 $ 63.96

Billable Hours 1,880.00 1,880.00

Loaded Bill Rate $ 67.80 $ 63.96 Total Proposed Cost $127,460.71 $120,245.96

Profit in $ $ 7,214.76

18© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

About Aronson LLC

• Thinking ahead for clients for more than 50 years• 225+ professionals located in Rockville, MD• 80+ professionals dedicated to supporting government contractors • Aronson helps clients rethink the way they approach their business

through innovative, industry-specific services and advice:– Audit, Assurance and Tax– Deltek Systems and Outsourcing– Financial and Contract Compliance– GSA Schedules

• www.aronsonllc.com/blogs/fedpoint/ – News and trends and insight for today’s savvy government contractor

19© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

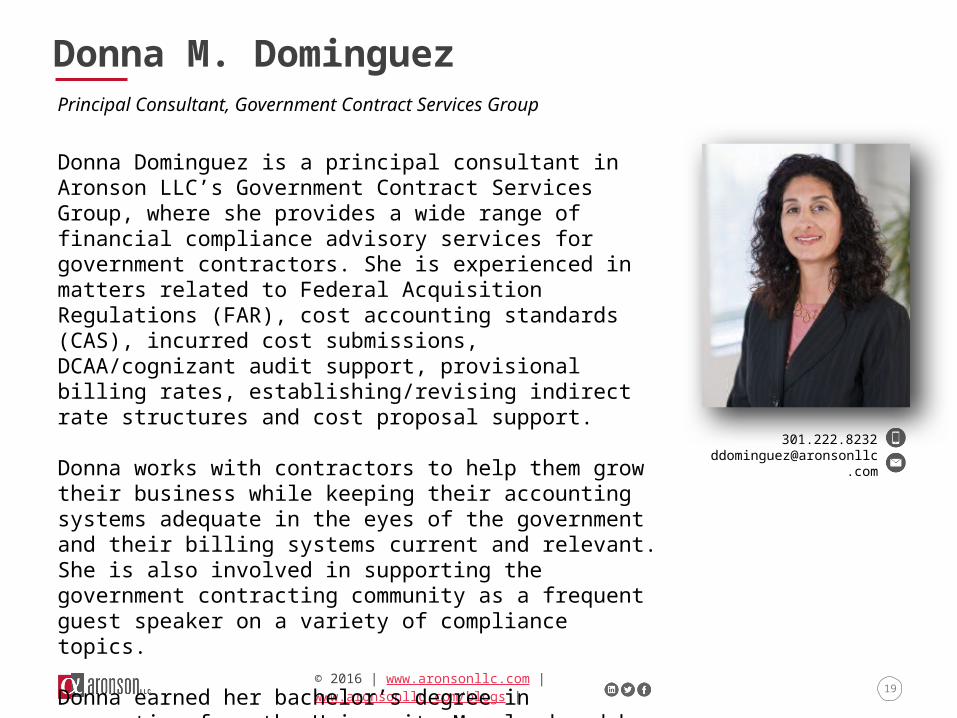

Donna Dominguez is a principal consultant in Aronson LLC’s Government Contract Services Group, where she provides a wide range of financial compliance advisory services for government contractors. She is experienced in matters related to Federal Acquisition Regulations (FAR), cost accounting standards (CAS), incurred cost submissions, DCAA/cognizant audit support, provisional billing rates, establishing/revising indirect rate structures and cost proposal support. Donna works with contractors to help them grow their business while keeping their accounting systems adequate in the eyes of the government and their billing systems current and relevant. She is also involved in supporting the government contracting community as a frequent guest speaker on a variety of compliance topics. Donna earned her bachelor’s degree in accounting from the University Maryland and has completed additional coursework in contracts administration. She is a contributor to Aronson’s Fed Point blog and has co-authored articles for NCMA Contract Management Magazine.

Principal Consultant, Government Contract Services Group

301.222.8232

Donna M. Dominguez

20© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Q & A

21© 2016 | www.aronsonllc.com | www.aronsonllc.com/blogs |

301.222.8232

Contact Donna Dominguez / Aronson LLC

https://www.linkedin.com/in/donna-dominguez-664b26b

https://twitter.com/Aronsonllc