structural risk models

DESCRIPTION

Structural Risk Models. Elementary Risk Models. Single Factor Model Market Model Plus assumption residuals are uncorrelated Constant Correlation Model Assume all asset returns have same pair-wise correlation Cov(R i , R j ) = i j. Elementary Models. Full-Covariance Model - PowerPoint PPT PresentationTRANSCRIPT

Structural Risk Models

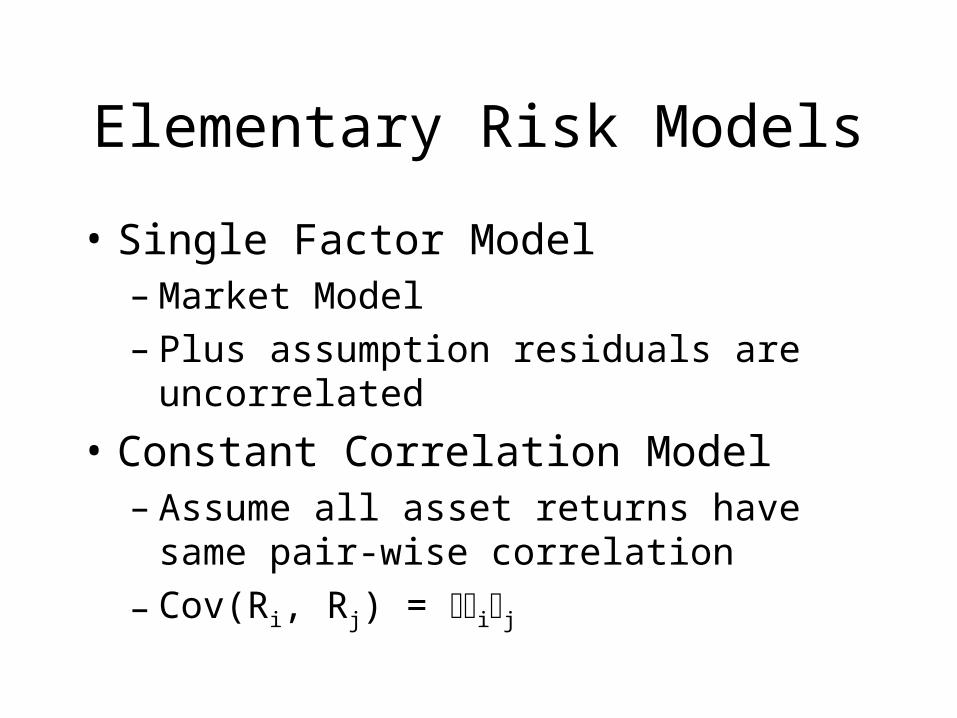

Elementary Risk Models

• Single Factor Model– Market Model– Plus assumption residuals are uncorrelated

• Constant Correlation Model– Assume all asset returns have same pair-wise

correlation

– Cov(Ri, Rj) = ij

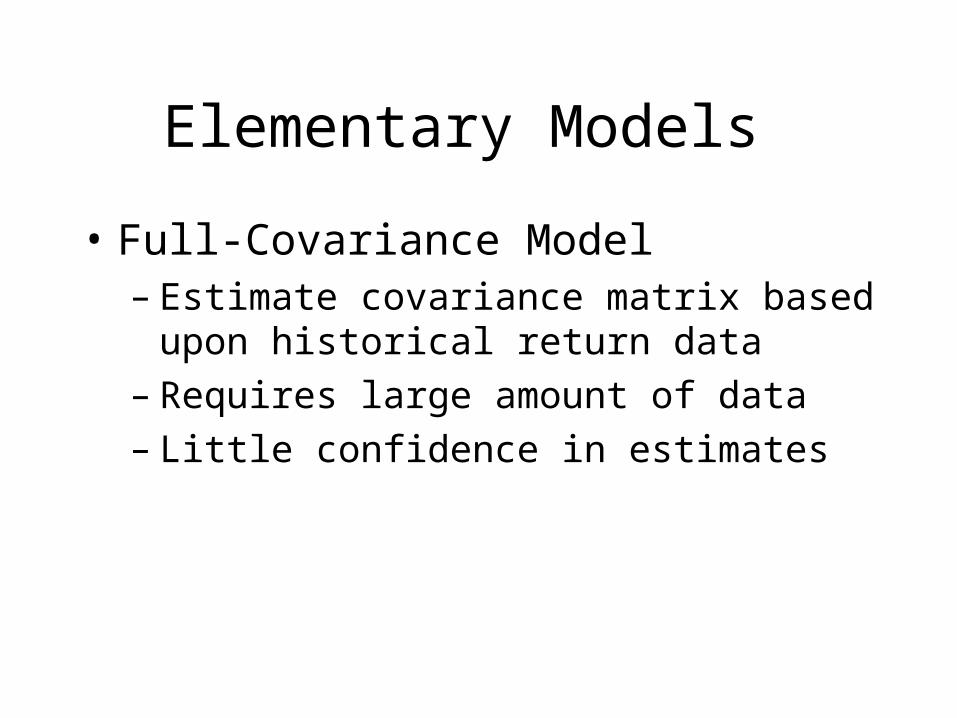

Elementary Models

• Full-Covariance Model– Estimate covariance matrix based upon

historical return data– Requires large amount of data– Little confidence in estimates

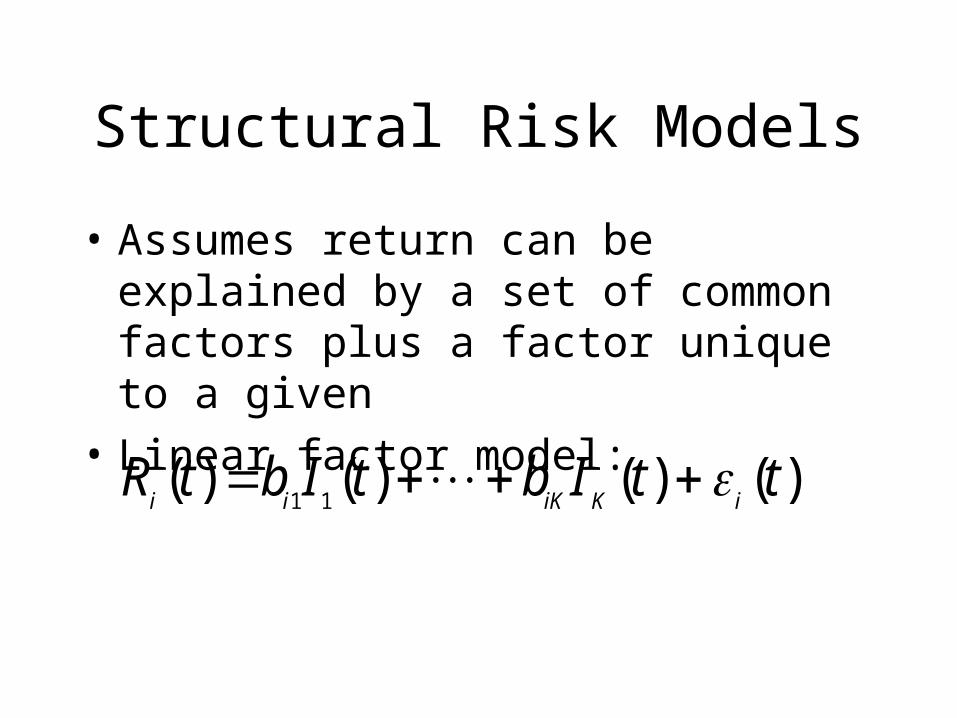

Structural Risk Models

• Assumes return can be explained by a set of common factors plus a factor unique to a given

• Linear factor model:

)()()()(11

ttIbtIbtRiKiKii

Choosing Factors

• External Influences– Outside Economic factors– Examples

• Changes in inflation

• Changes Exchange rates

• Changes in industrial production

Choosing Factors

• Statistical Factors – Statistical procedure for determining factors– Principal Components Analysis– Factor Analysis

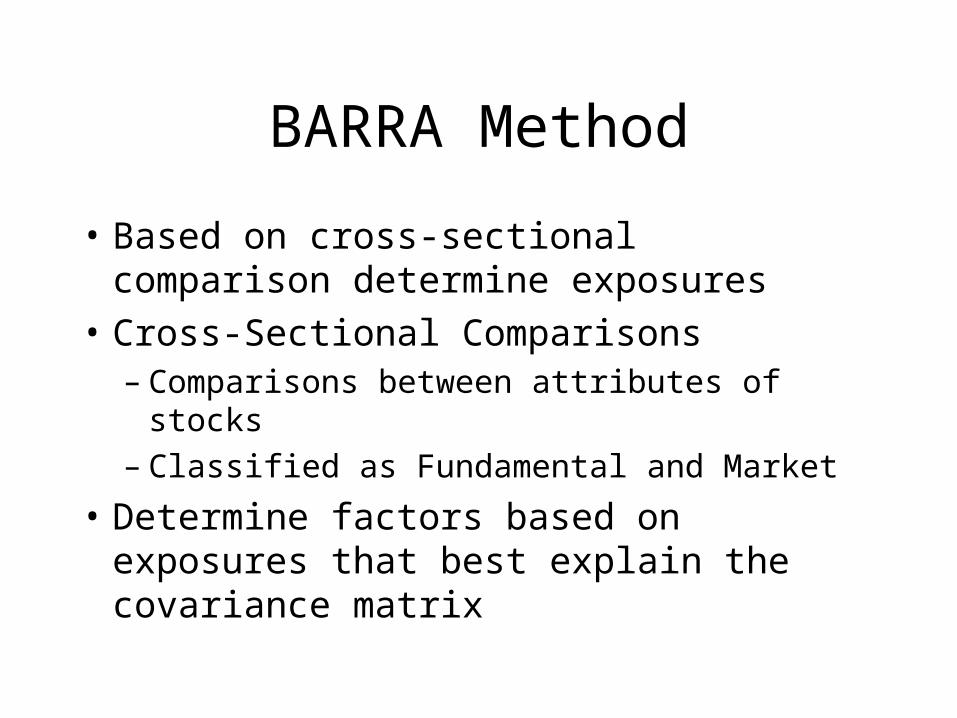

BARRA Method

• Based on cross-sectional comparison determine exposures

• Cross-Sectional Comparisons– Comparisons between attributes of stocks– Classified as Fundamental and Market

• Determine factors based on exposures that best explain the covariance matrix

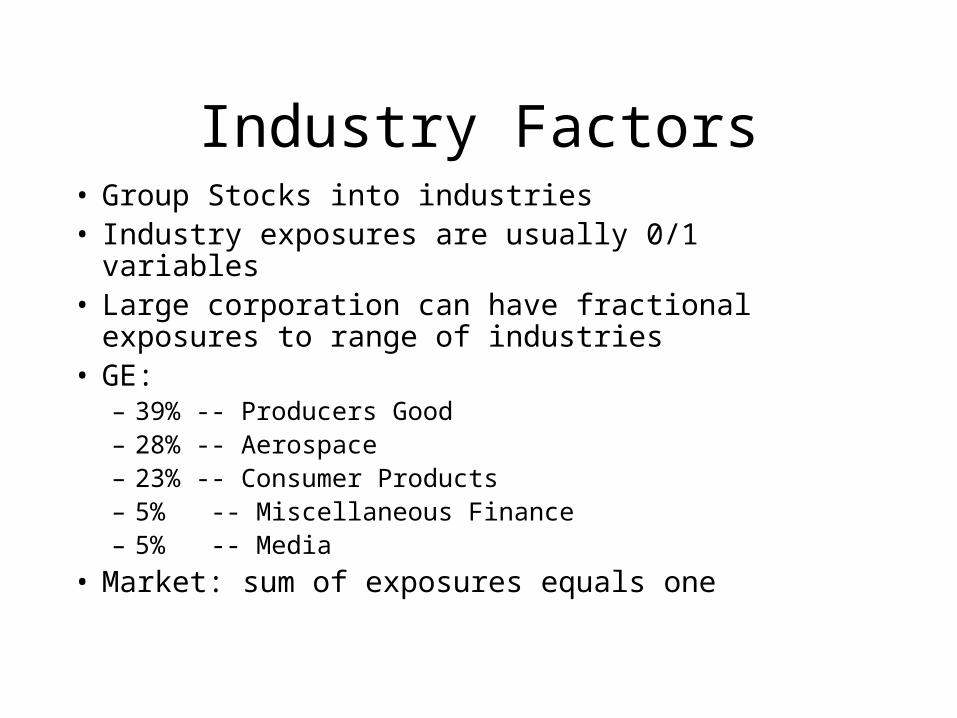

Industry Factors• Group Stocks into industries• Industry exposures are usually 0/1 variables• Large corporation can have fractional exposures to range

of industries• GE:

– 39% -- Producers Good– 28% -- Aerospace– 23% -- Consumer Products– 5% -- Miscellaneous Finance– 5% -- Media

• Market: sum of exposures equals one

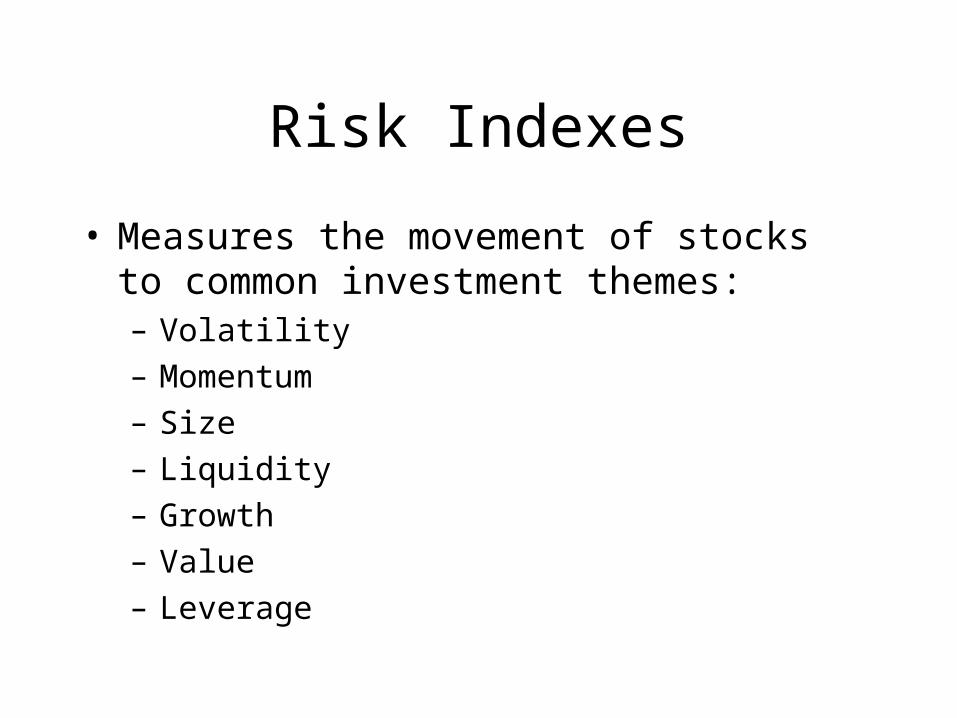

Risk Indexes

• Measures the movement of stocks to common investment themes:– Volatility

– Momentum

– Size

– Liquidity

– Growth

– Value

– Leverage

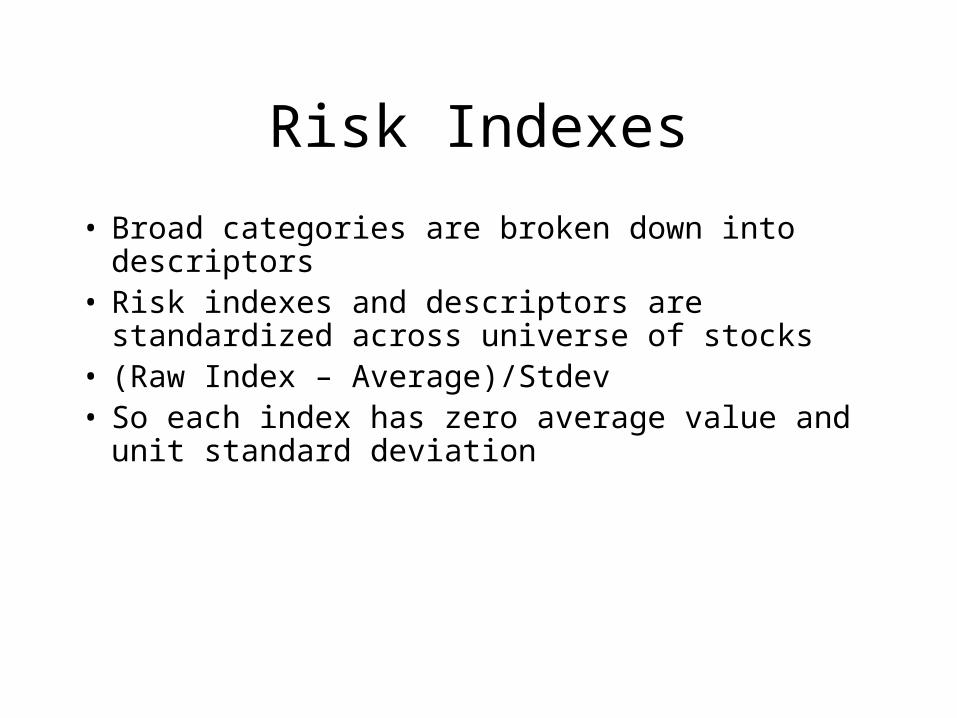

Risk Indexes

• Broad categories are broken down into descriptors• Risk indexes and descriptors are standardized across

universe of stocks• (Raw Index – Average)/Stdev• So each index has zero average value and unit standard

deviation

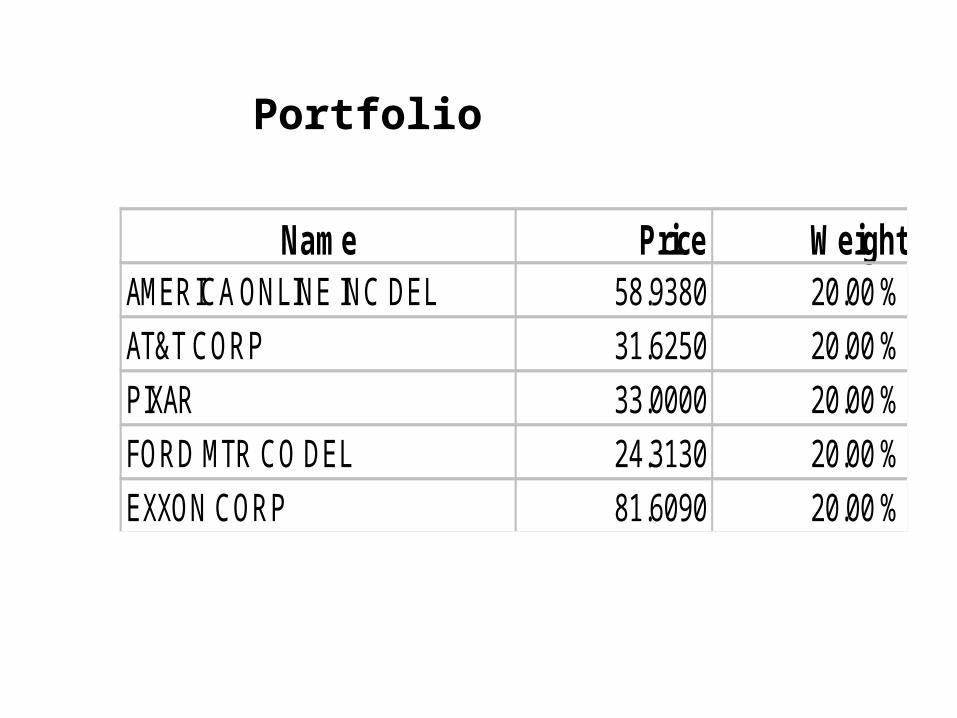

Name Price WeightAMERICA ONLINE INC DEL 58.9380 20.00 %

AT&T CORP 31.6250 20.00 %

PIXAR 33.0000 20.00 %

FORD MTR CO DEL 24.3130 20.00 %

EXXON CORP 81.6090 20.00 %

Portfolio

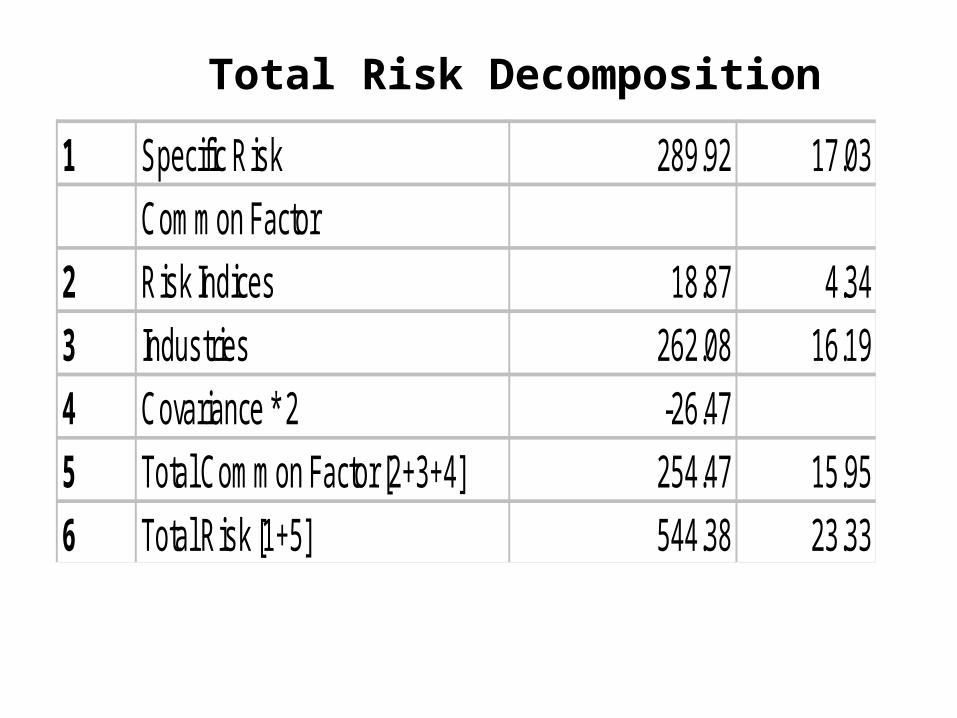

1 Specific Risk 289.92 17.03

Common Factor

2 Risk Indices 18.87 4.34

3 Industries 262.08 16.19

4 Covariance * 2 -26.47

5 Total Common Factor [2+3+4] 254.47 15.95

6 Total Risk [1+5] 544.38 23.33

Total Risk Decomposition

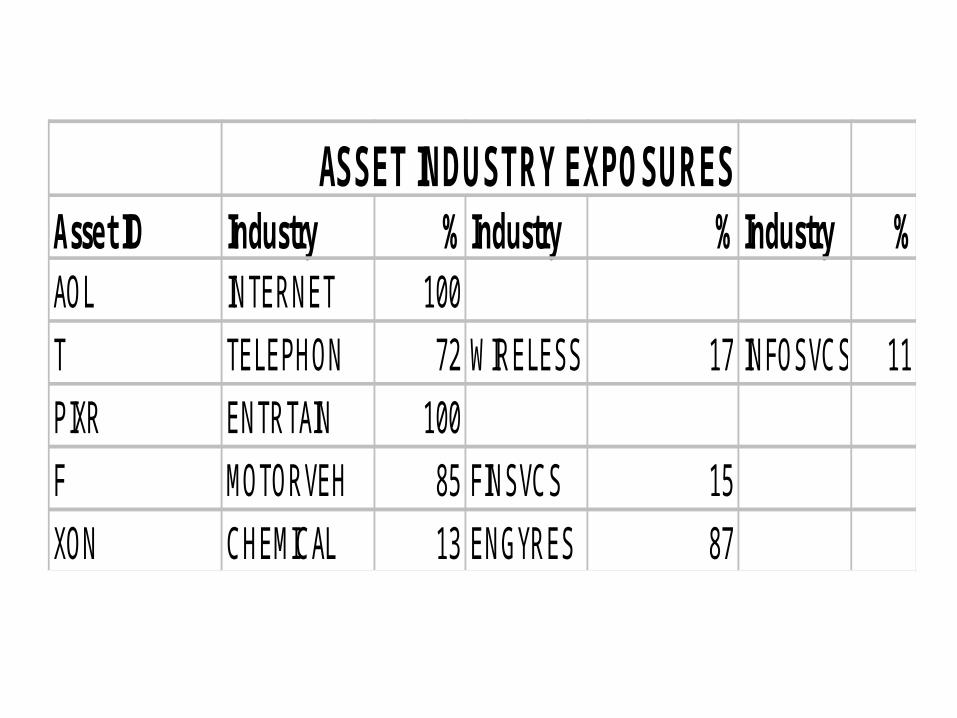

ASSET INDUSTRY EXPOSURESAsset ID Industry % Industry % Industry %AOL INTERNET 100

T TELEPHON 72 WIRELESS 17 INFOSVCS 11

PIXR ENTRTAIN 100

F MOTORVEH 85 FINSVCS 15

XON CHEMICAL 13 ENGYRES 87

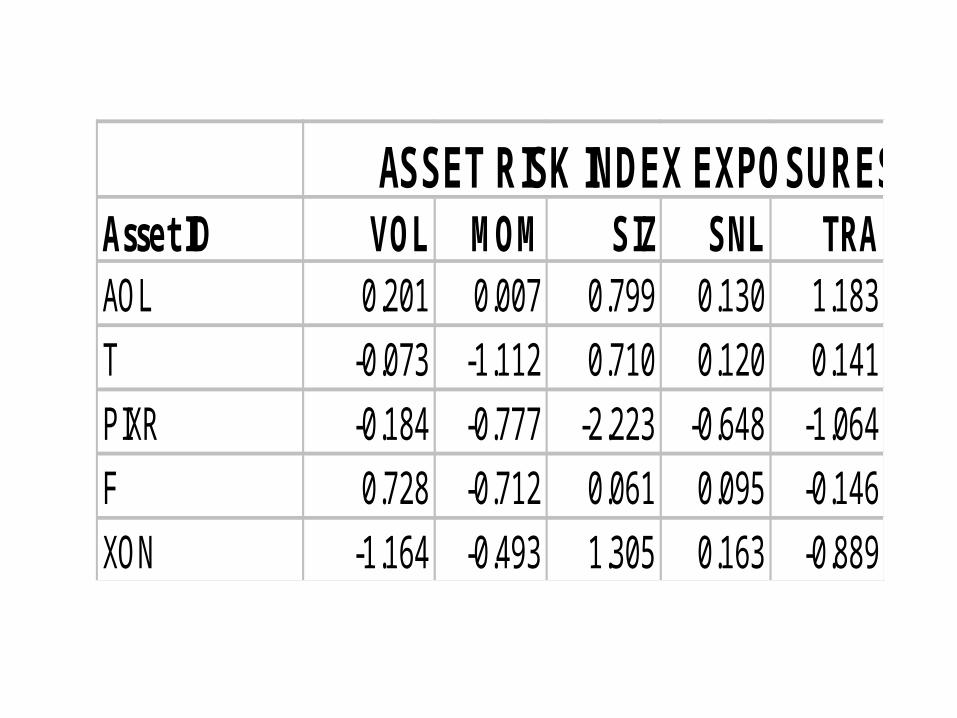

ASSET RISK INDEX EXPOSURES (Std Dev)Asset ID VOL MOM SIZ SNL TRAAOL 0.201 0.007 0.799 0.130 1.183

T -0.073 -1.112 0.710 0.120 0.141

PIXR -0.184 -0.777 -2.223 -0.648 -1.064

F 0.728 -0.712 0.061 0.095 -0.146

XON -1.164 -0.493 1.305 0.163 -0.889

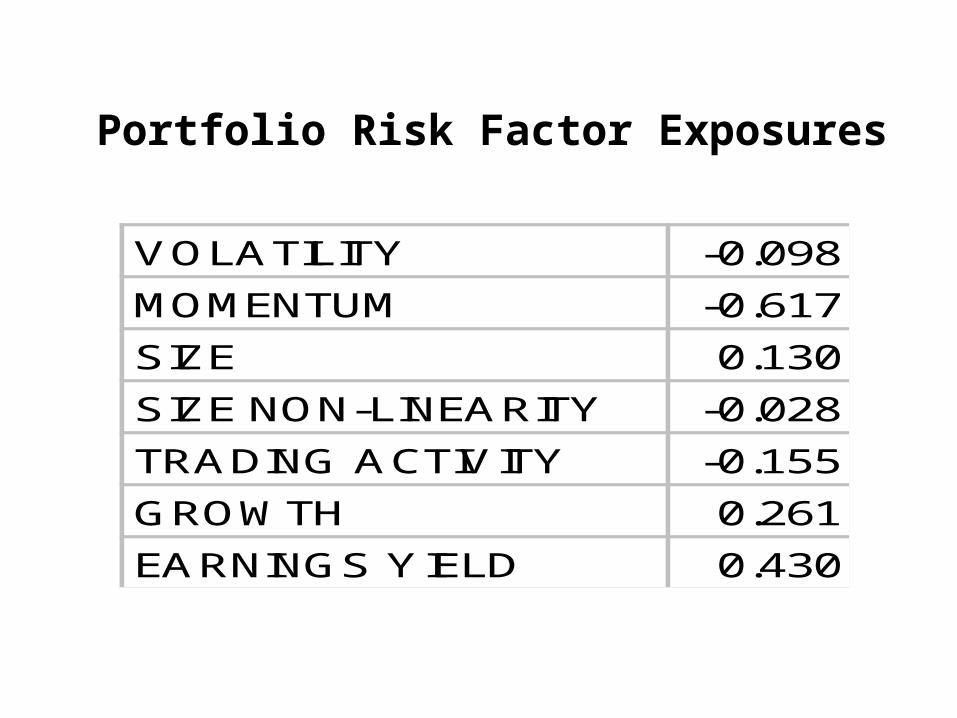

VOLATILITY -0.098

MOMENTUM -0.617

SIZE 0.130

SIZE NON-LINEARITY -0.028

TRADING ACTIVITY -0.155

GROWTH 0.261

EARNINGS YIELD 0.430

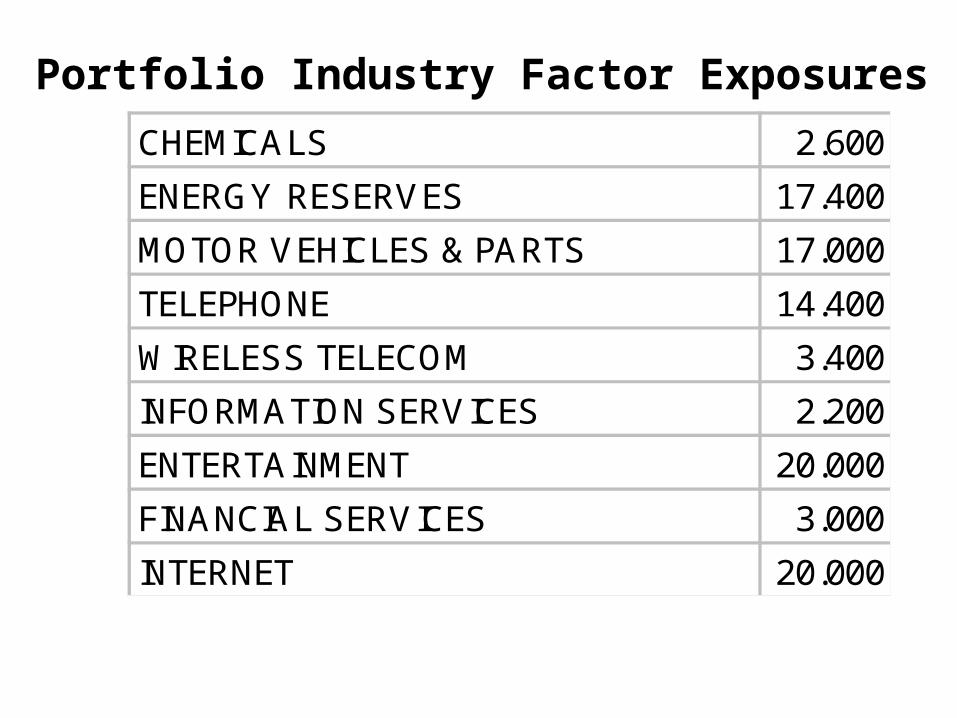

Portfolio Risk Factor Exposures

CHEMICALS 2.600

ENERGY RESERVES 17.400

MOTOR VEHICLES & PARTS 17.000

TELEPHONE 14.400

WIRELESS TELECOM 3.400

INFORMATION SERVICES 2.200

ENTERTAINMENT 20.000

FINANCIAL SERVICES 3.000

INTERNET 20.000

Portfolio Industry Factor Exposures

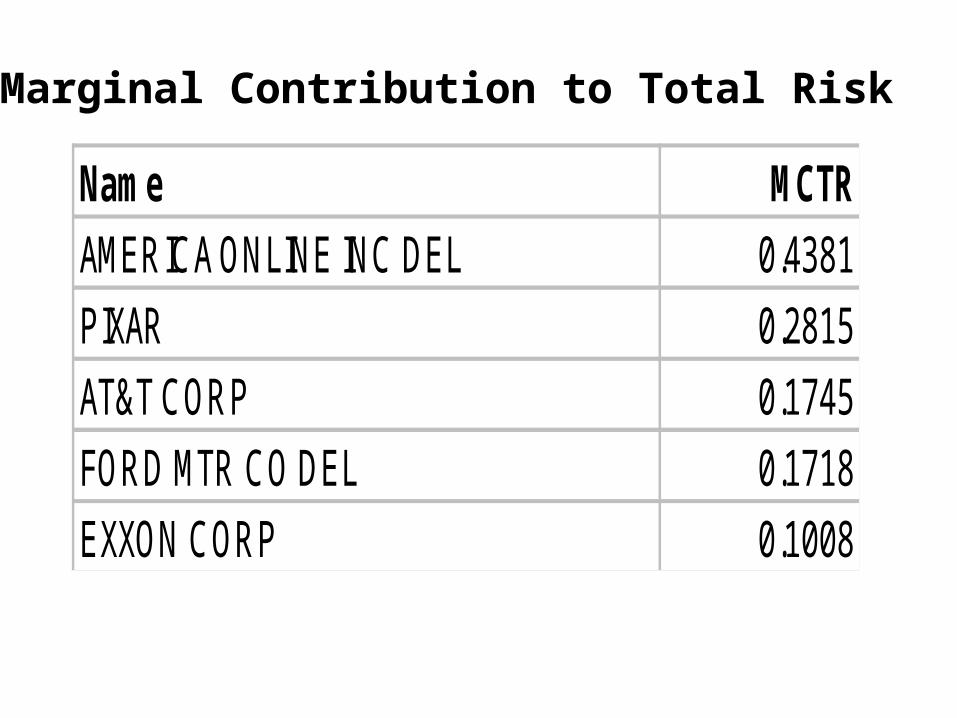

Name MCTR

AMERICA ONLINE INC DEL 0.4381

PIXAR 0.2815

AT&T CORP 0.1745

FORD MTR CO DEL 0.1718

EXXON CORP 0.1008

Marginal Contribution to Total Risk

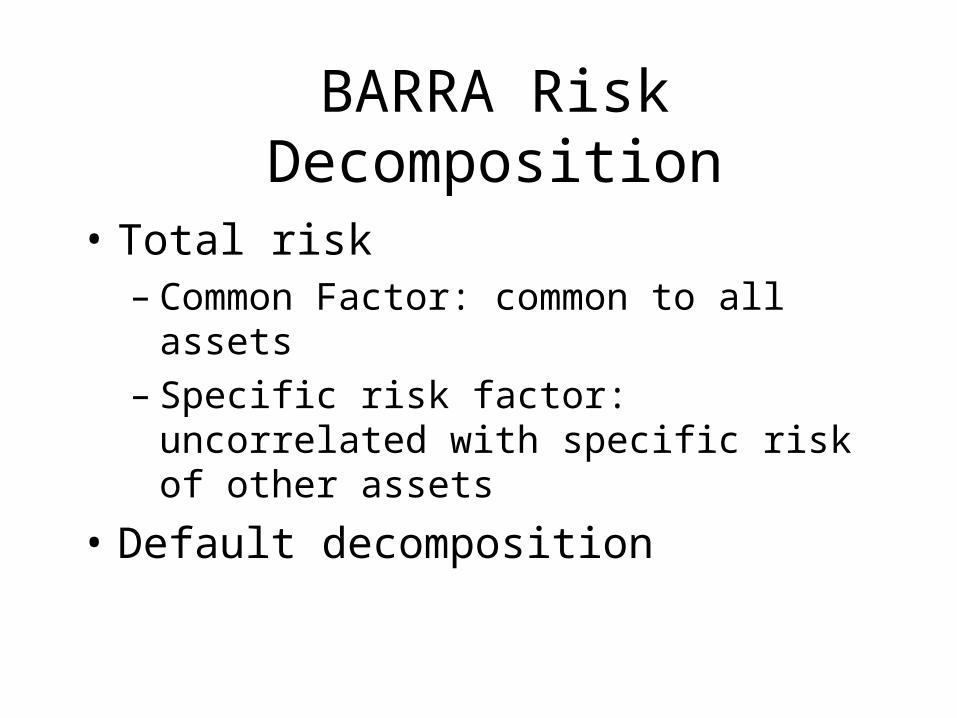

BARRA Risk Decomposition

• Total risk– Common Factor: common to all assets– Specific risk factor: uncorrelated with specific

risk of other assets

• Default decomposition

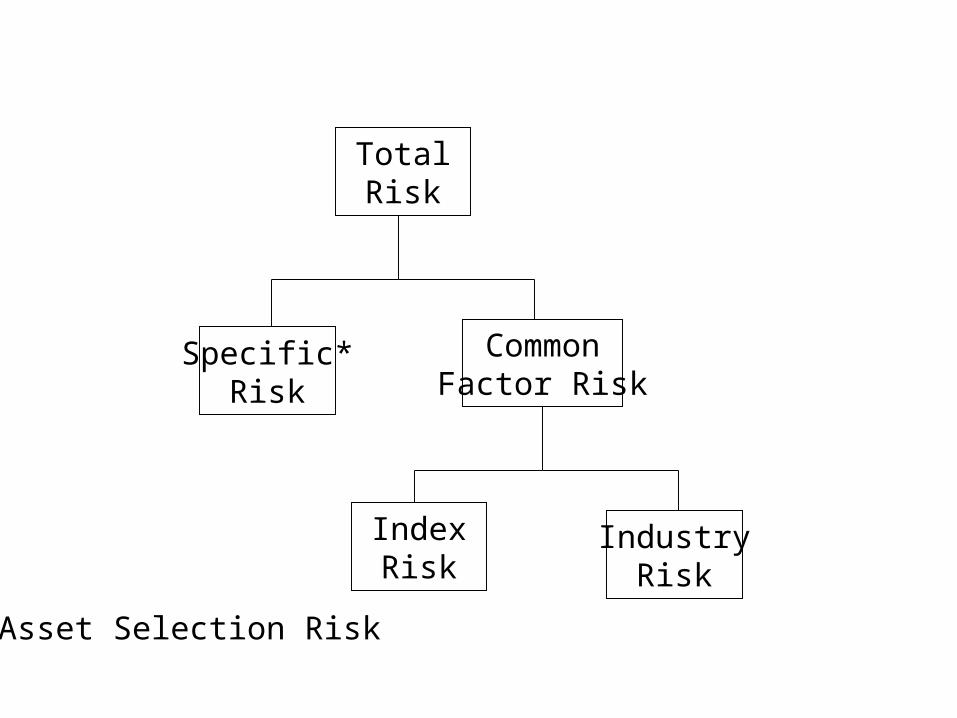

TotalRisk

Specific*Risk

CommonFactor Risk

IndexRisk

IndustryRisk

*Asset Selection Risk

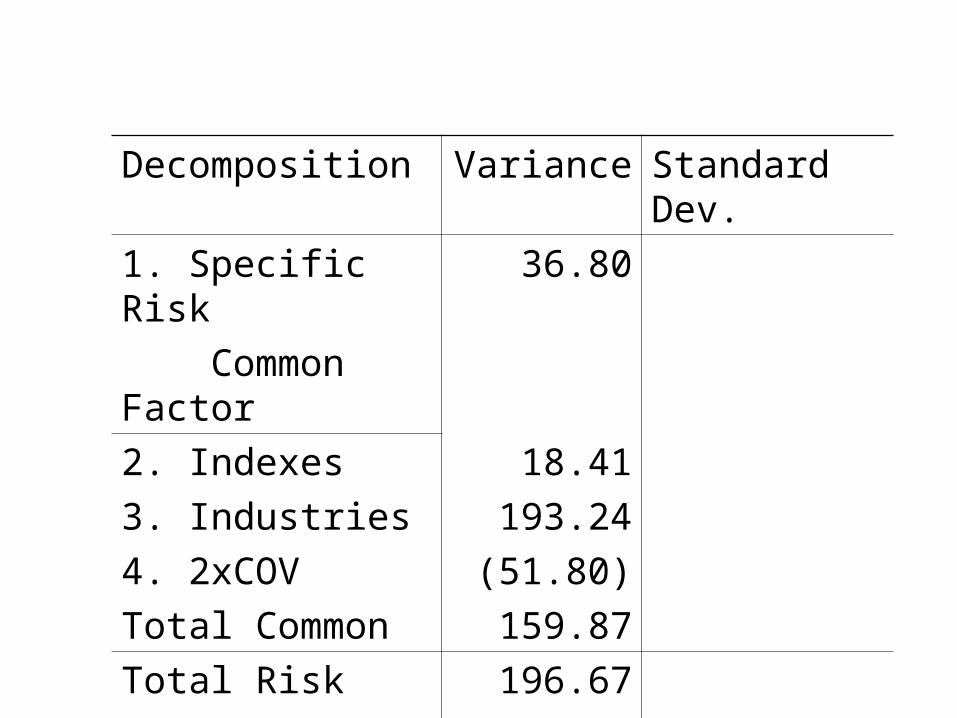

Decomposition Variance Standard Dev.

1. Specific Risk 36.80

Common Factor

2. Indexes 18.41

3. Industries 193.24

4. 2xCOV (51.80)

Total Common 159.87

Total Risk 196.67

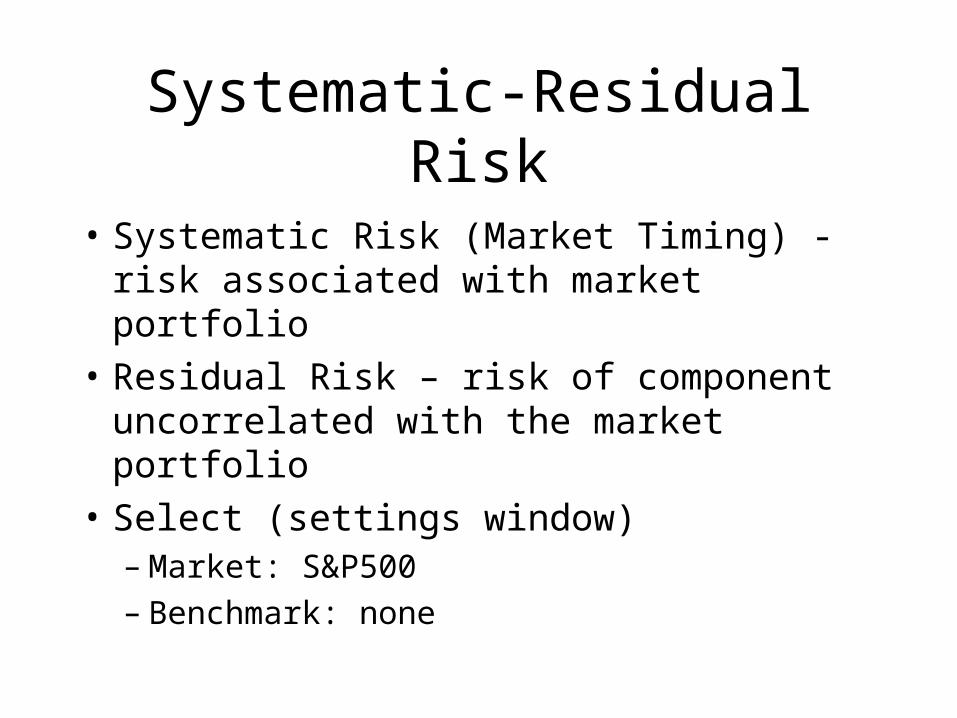

Systematic-Residual Risk

• Systematic Risk (Market Timing) - risk associated with market portfolio

• Residual Risk – risk of component uncorrelated with the market portfolio

• Select (settings window)– Market: S&P500– Benchmark: none

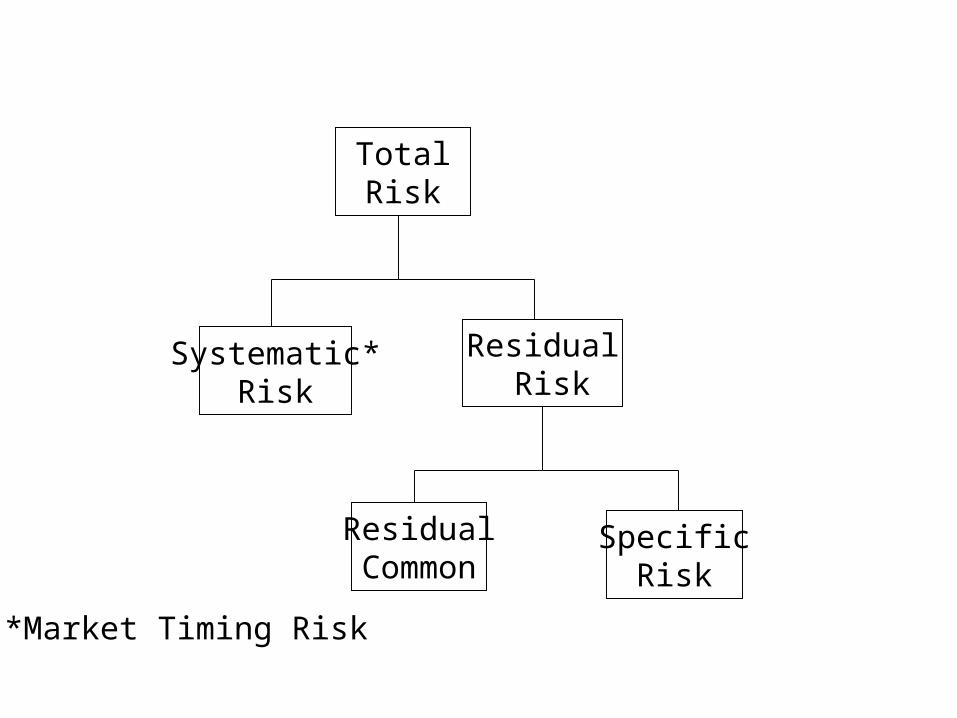

TotalRisk

Systematic*Risk

Residual Risk

ResidualCommon

SpecificRisk

*Market Timing Risk

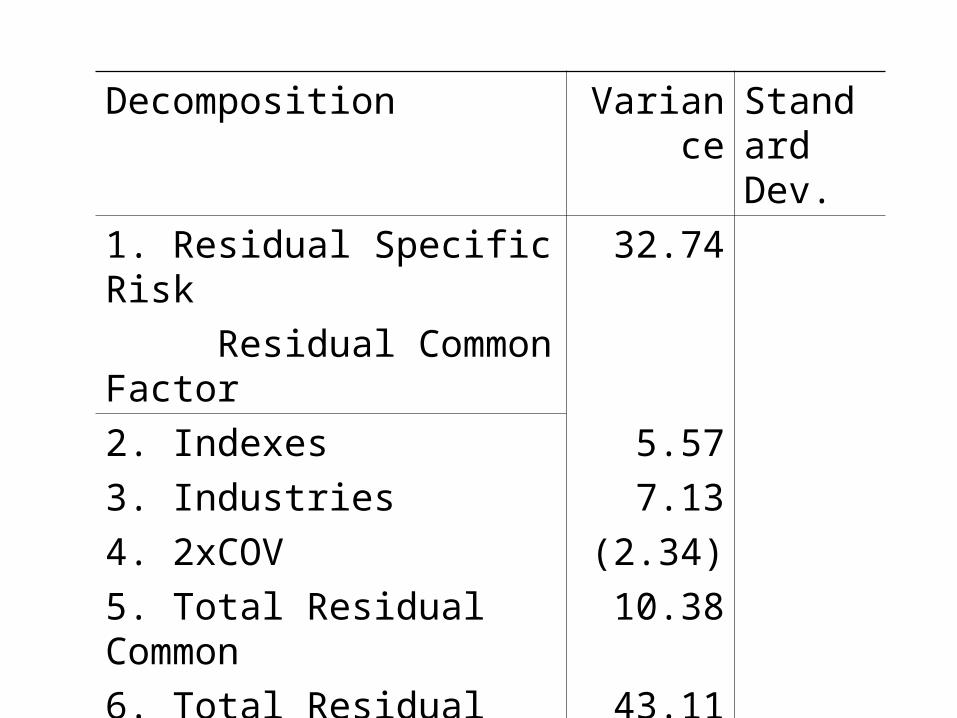

Decomposition Variance Standard Dev.

1. Residual Specific Risk 32.74

Residual Common Factor

2. Indexes 5.57

3. Industries 7.13

4. 2xCOV (2.34)

5. Total Residual Common 10.38

6. Total Residual 43.11

7. Systematic

8. Total Risk

153.56

196.67

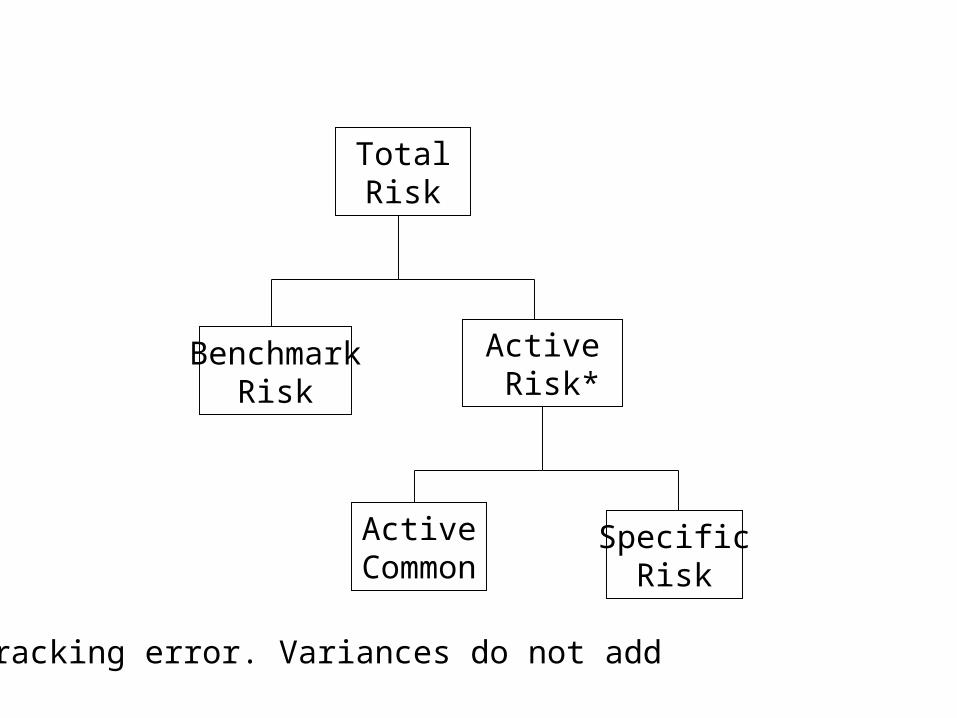

Active Risk Decomposition

• Benchmark risk – risk associated with benchmark

• Active risk – risk associated with deviations from benchmark: tracking error

• Select – market: none– benchmark: S&P500

TotalRisk

BenchmarkRisk

Active Risk*

ActiveCommon

SpecificRisk

*Tracking error. Variances do not add