stratecast customer focused operations analyst briefing

TRANSCRIPT

Easier Said Than Done: Customer-Focused Operations is Much More Than Network Management

or Real Time Billing

Karl Whitelock, Senior Consulting Analyst

Stratecast a division of Frost & Sullivan

OSS BSS Global Competitive Strategies (OSSCS)

July 31, 2008

2

Agenda

• Factors Driving Business Transformation

• Market Trends and Issues – OSS/BSS Operational

Capabilities

• Stratecast – The Last Word

3

Multi-Industry Convergence is Changing Our World

Communications

Technology

IPMobile

PSTN

Entertainment

Our

ConvergingWorld

Advertising

Media

Computing (IT)

4

“Customer Centric” Offerings – Early Market Successes

Complex Customer Services

Business or

Consumer

Real Time Business Management

Blyk.co.uk

5

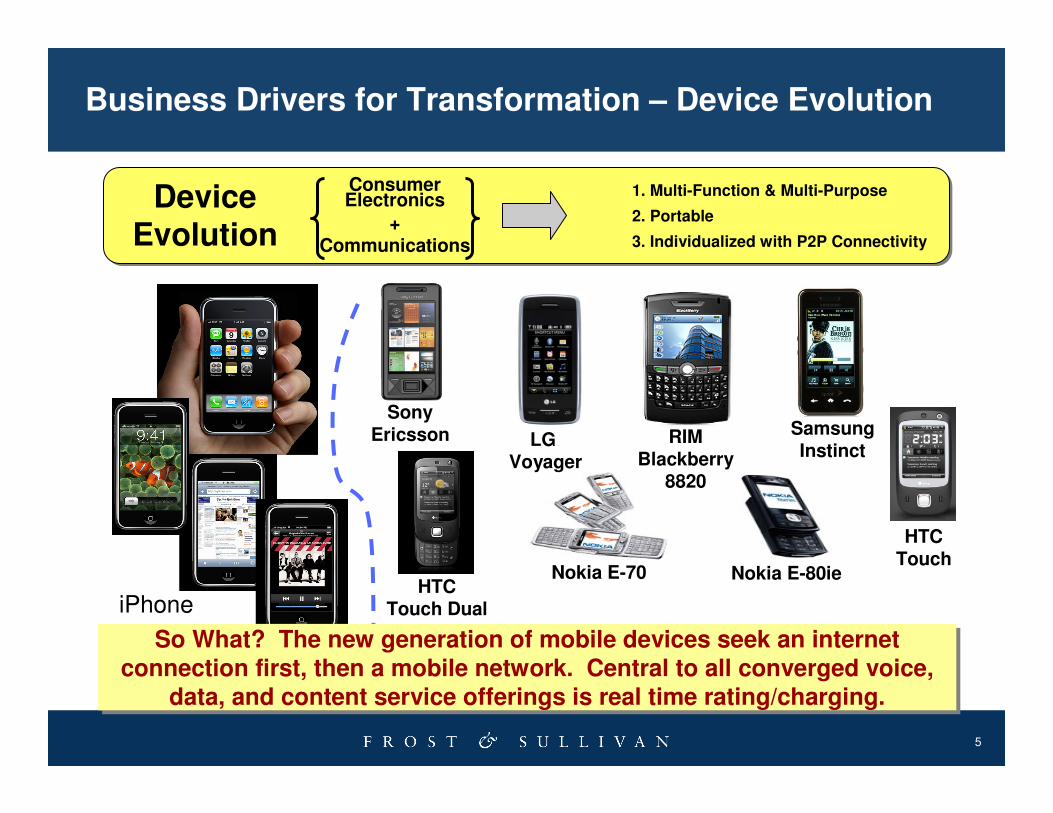

Business Drivers for Transformation – Device Evolution

Device Evolution

1. Multi-Function & Multi-Purpose

2. Portable

3. Individualized with P2P Connectivity

Consumer Electronics

+Communications

Nokia E-80ieNokia E-70

RIMBlackberry

8820

iPhone

SonyEricsson LG

Voyager

HTCTouch Dual

HTCTouch

SamsungInstinct

So What? The new generation of mobile devices seek an internet connection first, then a mobile network. Central to all converged voice,

data, and content service offerings is real time rating/charging.

So What? The new generation of mobile devices seek an internet connection first, then a mobile network. Central to all converged voice,

data, and content service offerings is real time rating/charging.

6

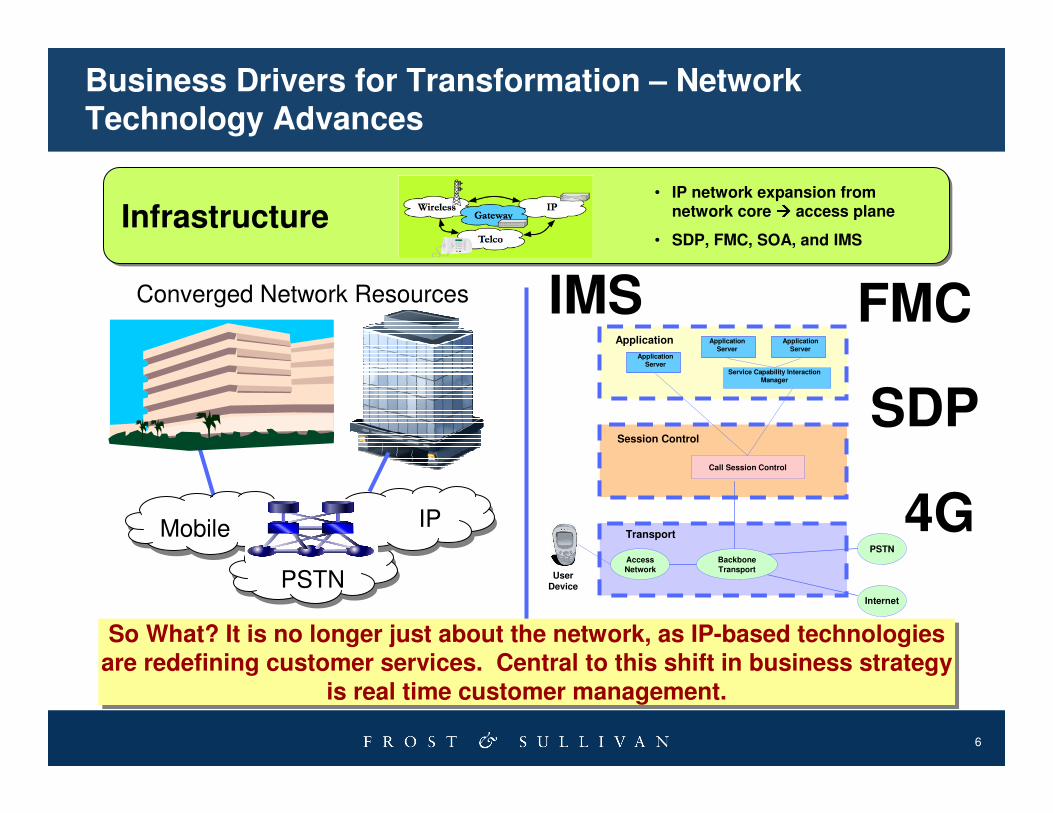

Infrastructure• IP network expansion from

network core ���� access plane

• SDP, FMC, SOA, and IMS

Business Drivers for Transformation – Network Technology Advances

User Device

Transport

Session Control

Application

Internet

PSTNAccess

Network

Backbone

Transport

Call Session Control

Service Capability Interaction Manager

Application Server

Application Server

Application Server

FMC

SDP

IMS

4G

Converged Network Resources

IPMobile

PSTN

So What? It is no longer just about the network, as IP-based technologies are redefining customer services. Central to this shift in business strategy

is real time customer management.

So What? It is no longer just about the network, as IP-based technologies are redefining customer services. Central to this shift in business strategy

is real time customer management.

7

Business Drivers for Transformation – CSP Business Maturation

So What? It isn’t just mobile or fixed line or video or data access. It’s the “need” to offer customers what they want when they want it. Today’s

“lifestyle services” have a real time customer focus.

So What? It isn’t just mobile or fixed line or video or data access. It’s the “need” to offer customers what they want when they want it. Today’s

“lifestyle services” have a real time customer focus.

CSP Business Maturation

• Multi-Service• Multi-Technology• Multi-Industry (Comms, IT, Media, Entertainment,

Advertising)

8

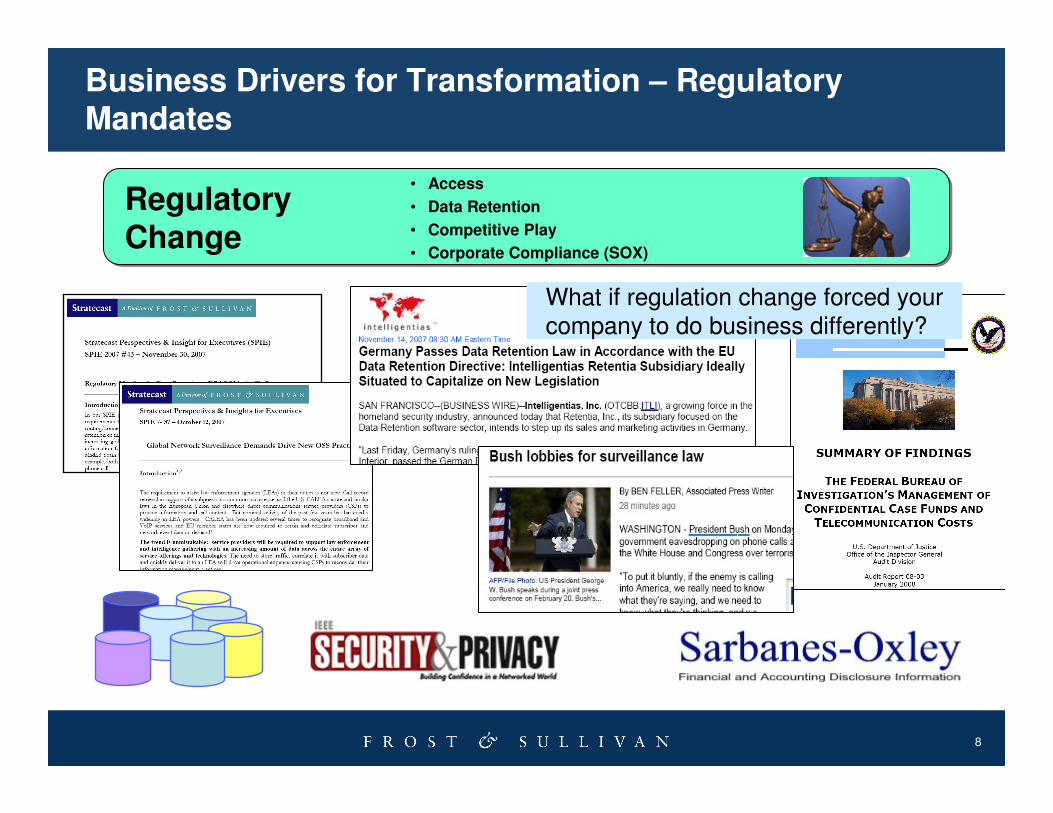

Business Drivers for Transformation – Regulatory Mandates

Regulatory Change

• Access

• Data Retention

• Competitive Play

• Corporate Compliance (SOX)

What if regulation change forced your

company to do business differently?

9

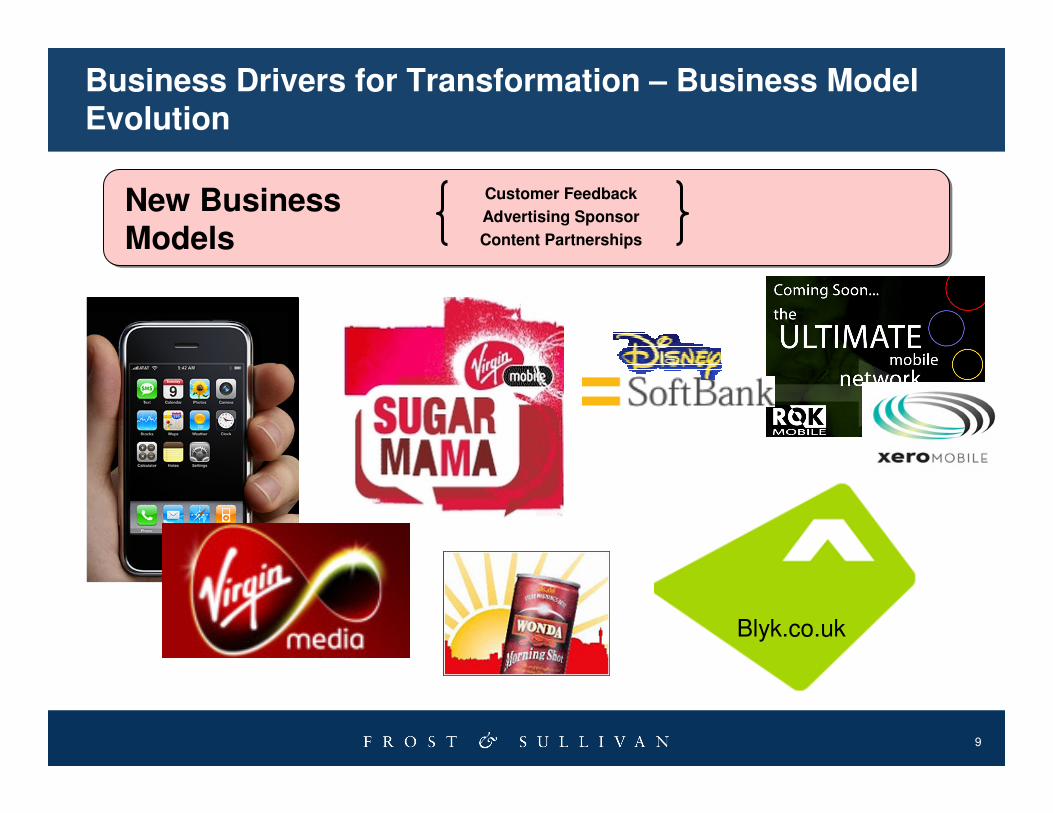

Business Drivers for Transformation – Business Model Evolution

New Business Models

Customer Feedback

Advertising Sponsor

Content Partnerships

Blyk.co.uk

10

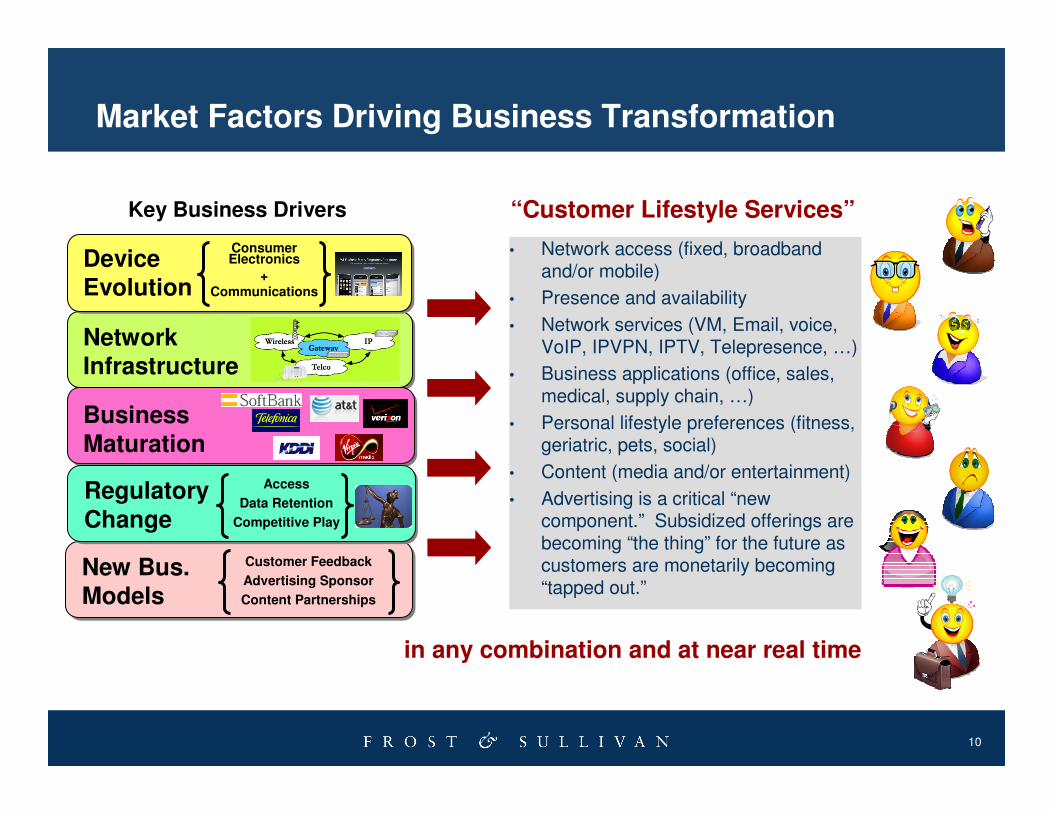

Market Factors Driving Business Transformation

Network Infrastructure

Business

Maturation

Device Evolution

Consumer Electronics

+

Communications

New Bus. Models

Customer Feedback

Advertising Sponsor

Content Partnerships

Regulatory

Change

Access

Data Retention

Competitive Play

Key Business Drivers

• Network access (fixed, broadband and/or mobile)

• Presence and availability

• Network services (VM, Email, voice, VoIP, IPVPN, IPTV, Telepresence, …)

• Business applications (office, sales, medical, supply chain, …)

• Personal lifestyle preferences (fitness, geriatric, pets, social)

• Content (media and/or entertainment)

• Advertising is a critical “new component.” Subsidized offerings are becoming “the thing” for the future as customers are monetarily becoming “tapped out.”

“Customer Lifestyle Services”

in any combination and at near real time

11

Agenda

• Factors Driving Business Transformation

• Market Trends and Issues – OSS/BSS Operational Capabilities

• Stratecast – The Last Word

12

OSS/BSS Operational Capabilities Summary

• Market Trends and Issues – OSS/BSS Operational Capabilities

• Real Time Support for Complex “Customer Lifestyle Services”

• Common View of the Customer Data Record

• Customer Experience Management

• Product Lifecycle Management

• Changing Regulatory Conditions

• Business Service Monitoring and Process Management

• Enterprise-wide Use of Analytics

• Flexibility to Address Changing Business Models

• CSP Business Transformation Governance – Sustainability of Business Architecture

• Service Oriented Architecture (SOA)

• Single supplier – Business Solution Approach

13

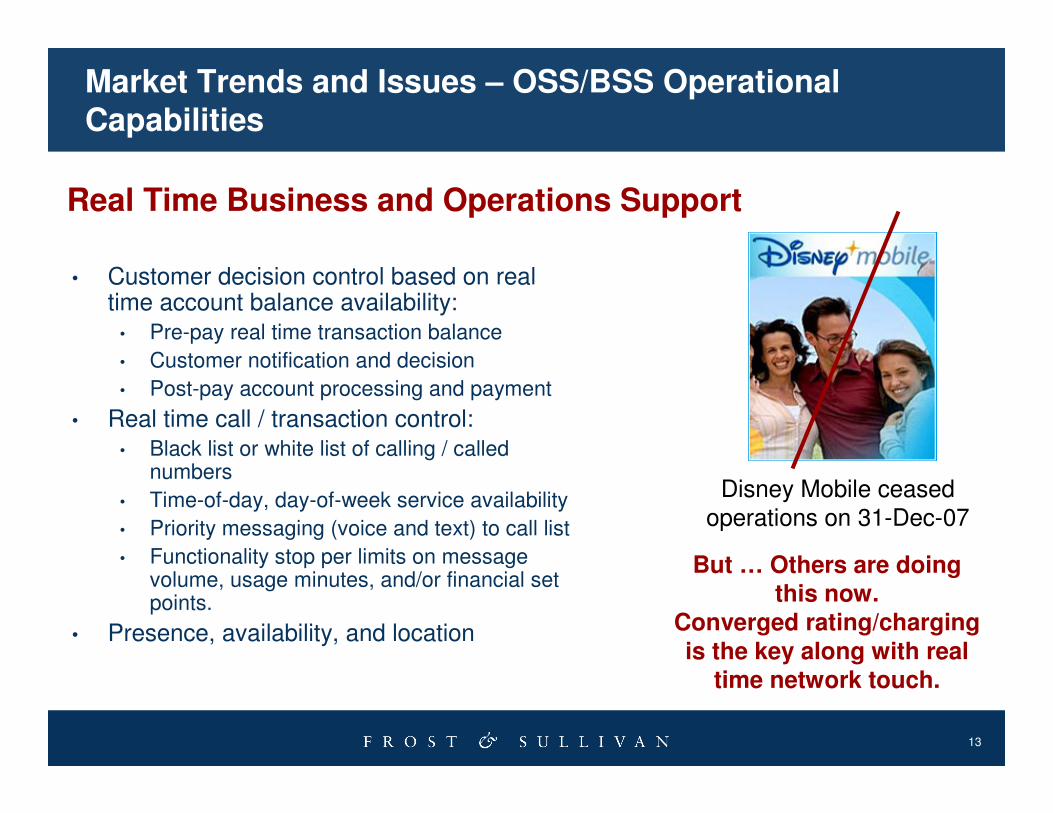

Market Trends and Issues – OSS/BSS Operational Capabilities

• Customer decision control based on real time account balance availability:

• Pre-pay real time transaction balance

• Customer notification and decision

• Post-pay account processing and payment

• Real time call / transaction control:

• Black list or white list of calling / called numbers

• Time-of-day, day-of-week service availability

• Priority messaging (voice and text) to call list

• Functionality stop per limits on message volume, usage minutes, and/or financial set points.

• Presence, availability, and location

Real Time Business and Operations Support

Disney Mobile ceased

operations on 31-Dec-07

But … Others are doing this now.

Converged rating/charging

is the key along with real time network touch.

14

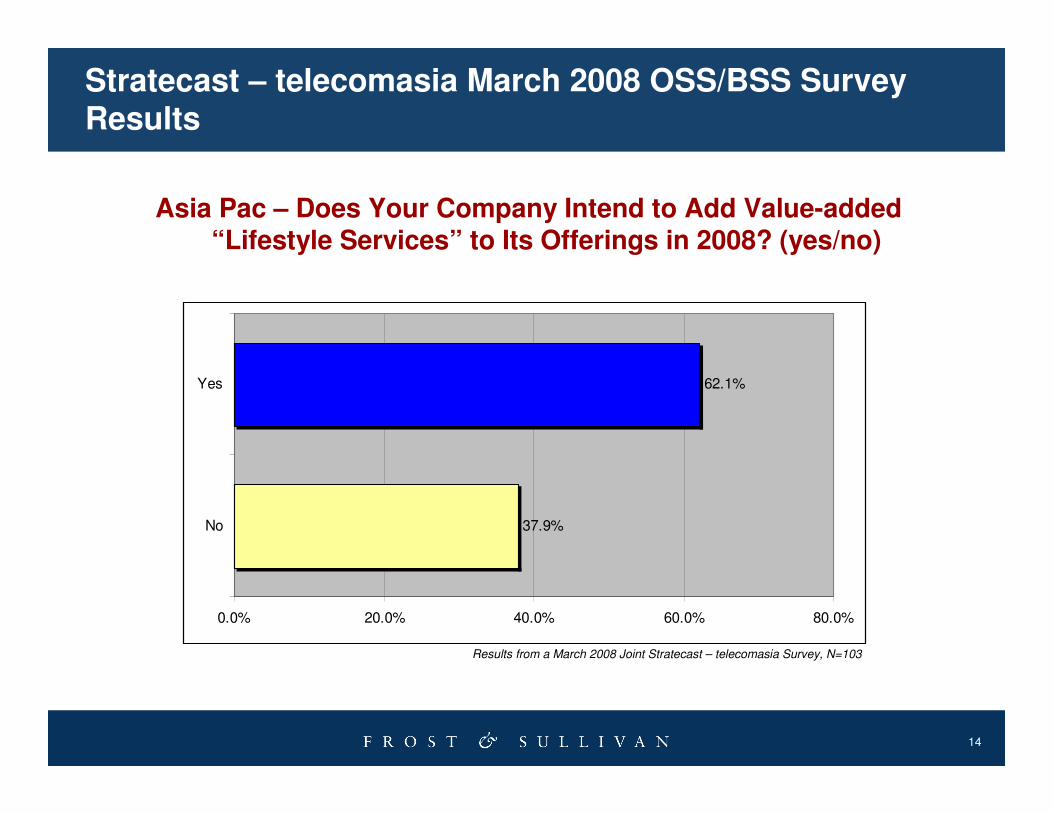

Stratecast – telecomasia March 2008 OSS/BSS Survey Results

Asia Pac – Does Your Company Intend to Add Value-added “Lifestyle Services” to Its Offerings in 2008? (yes/no)

37.9%

62.1%

0.0% 20.0% 40.0% 60.0% 80.0%

No

Yes

Results from a March 2008 Joint Stratecast – telecomasia Survey, N=103

15

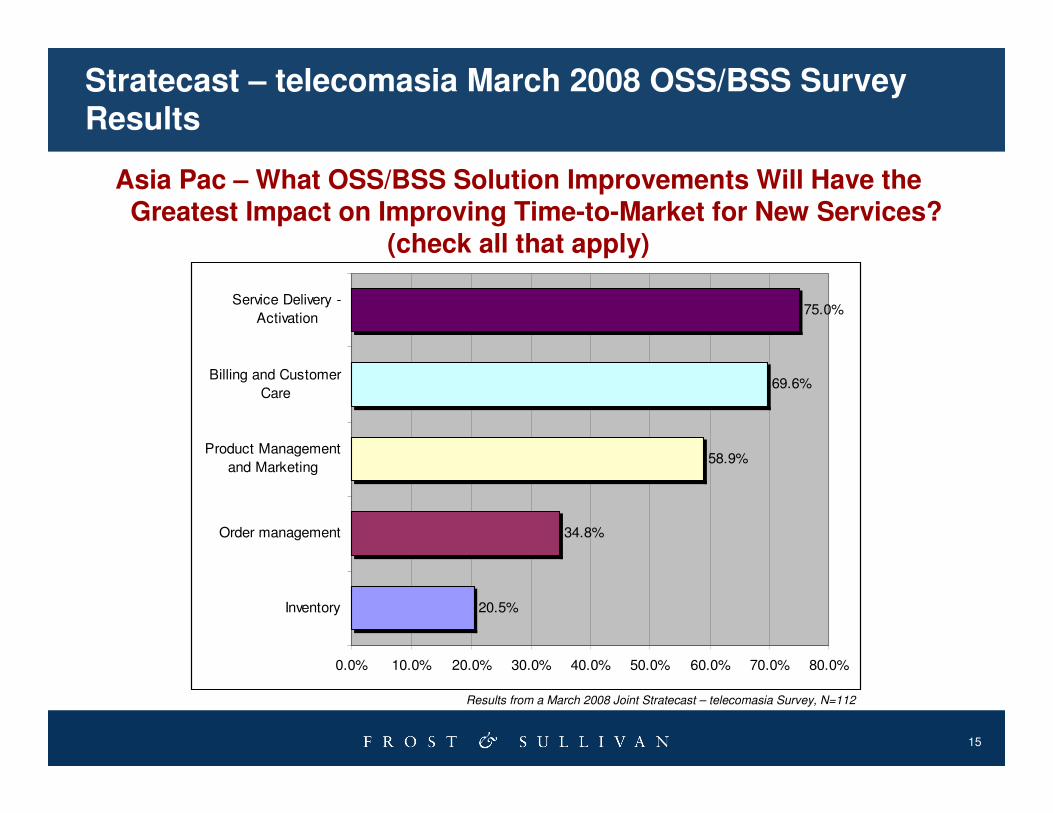

Stratecast – telecomasia March 2008 OSS/BSS Survey Results

20.5%

34.8%

58.9%

69.6%

75.0%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% 80.0%

Inventory

Order management

Product Management

and Marketing

Billing and Customer

Care

Service Delivery -

Activation

Results from a March 2008 Joint Stratecast – telecomasia Survey, N=112

Asia Pac – What OSS/BSS Solution Improvements Will Have the Greatest Impact on Improving Time-to-Market for New Services?

(check all that apply)

16

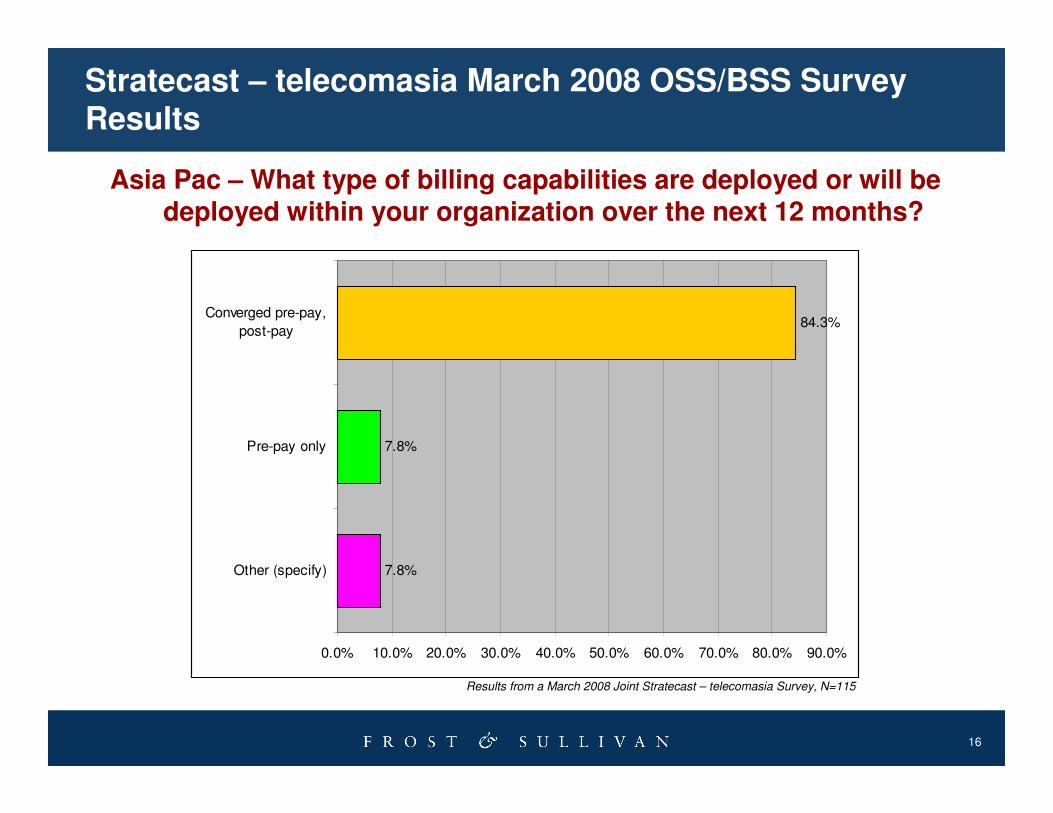

Stratecast – telecomasia March 2008 OSS/BSS Survey Results

Results from a March 2008 Joint Stratecast – telecomasia Survey, N=115

Asia Pac – What type of billing capabilities are deployed or will be deployed within your organization over the next 12 months?

7.8%

7.8%

84.3%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% 80.0% 90.0%

Other (specify)

Pre-pay only

Converged pre-pay,

post-pay

17

Market Trends and Issues – OSS/BSS Operational Capabilities

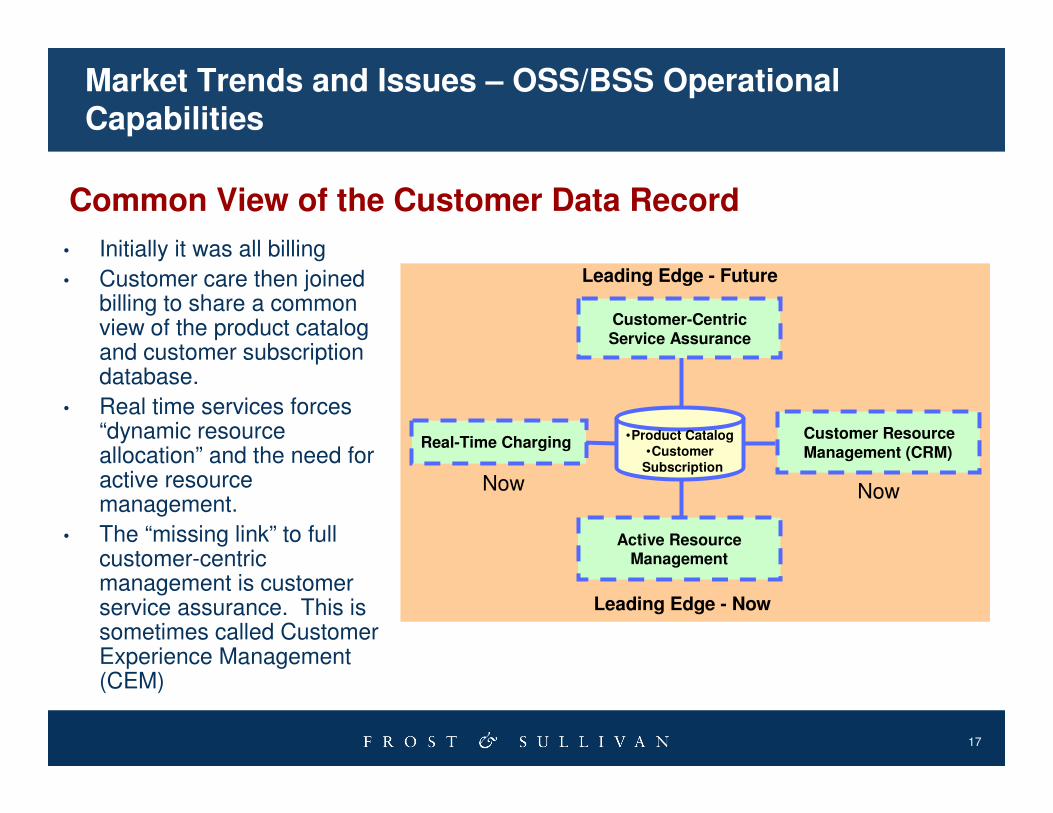

• Initially it was all billing

• Customer care then joined billing to share a common view of the product catalog and customer subscription database.

• Real time services forces “dynamic resource allocation” and the need for active resource management.

• The “missing link” to full customer-centric management is customer service assurance. This is sometimes called Customer Experience Management (CEM)

Common View of the Customer Data Record

•Product Catalog

•Customer

Subscription

Customer Resource Management (CRM)

Active Resource Management

Customer-Centric Service Assurance

Now Now

Leading Edge - Now

Leading Edge - Future

Real-Time Charging

18

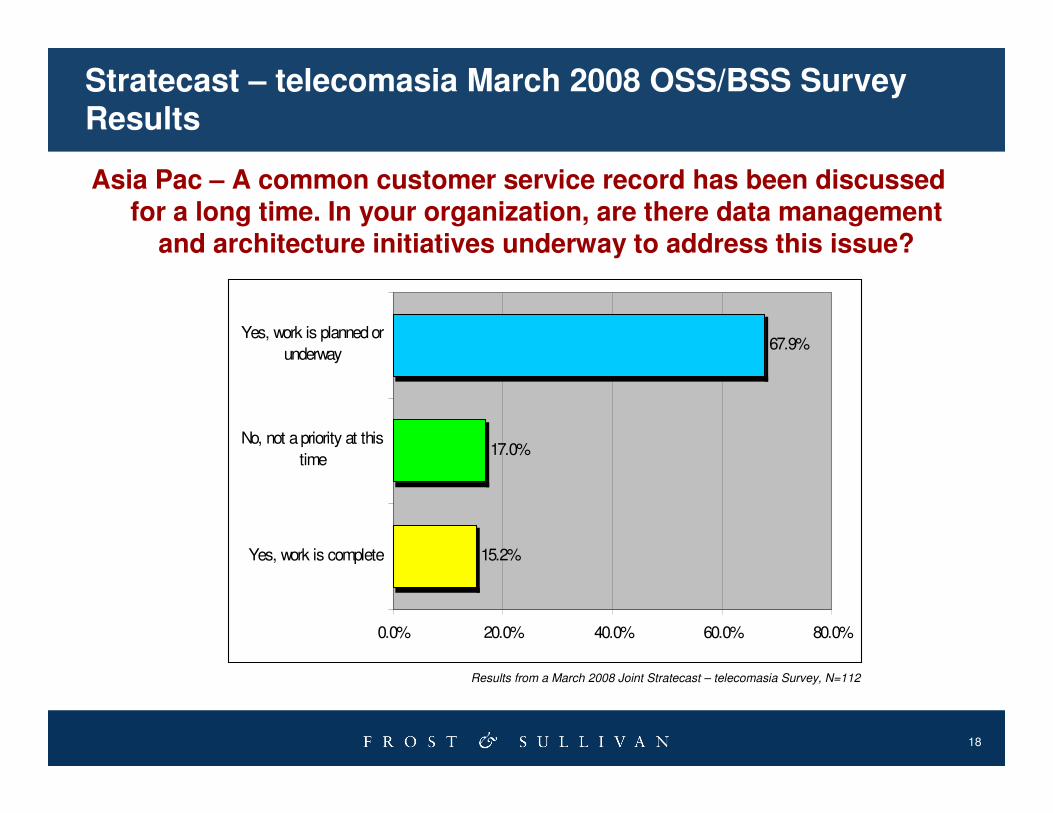

Stratecast – telecomasia March 2008 OSS/BSS Survey Results

Results from a March 2008 Joint Stratecast – telecomasia Survey, N=112

Asia Pac – A common customer service record has been discussed for a long time. In your organization, are there data management

and architecture initiatives underway to address this issue?

15.2%

17.0%

67.9%

0.0% 20.0% 40.0% 60.0% 80.0%

Yes, work is complete

No, not a priority at this

time

Yes, work is planned or

underway

19

Market Trends and Issues – OSS/BSS Operational Capabilities

• CEM is the practice of collecting customer usage information for use by both business and technical departments

• The major push for CEM is coming from the mobile and converged services markets.

• It is focused on both consumer and enterprise customers.

Customer Experience Management (CEM)

Mobile Customer

Mobile Customer

20

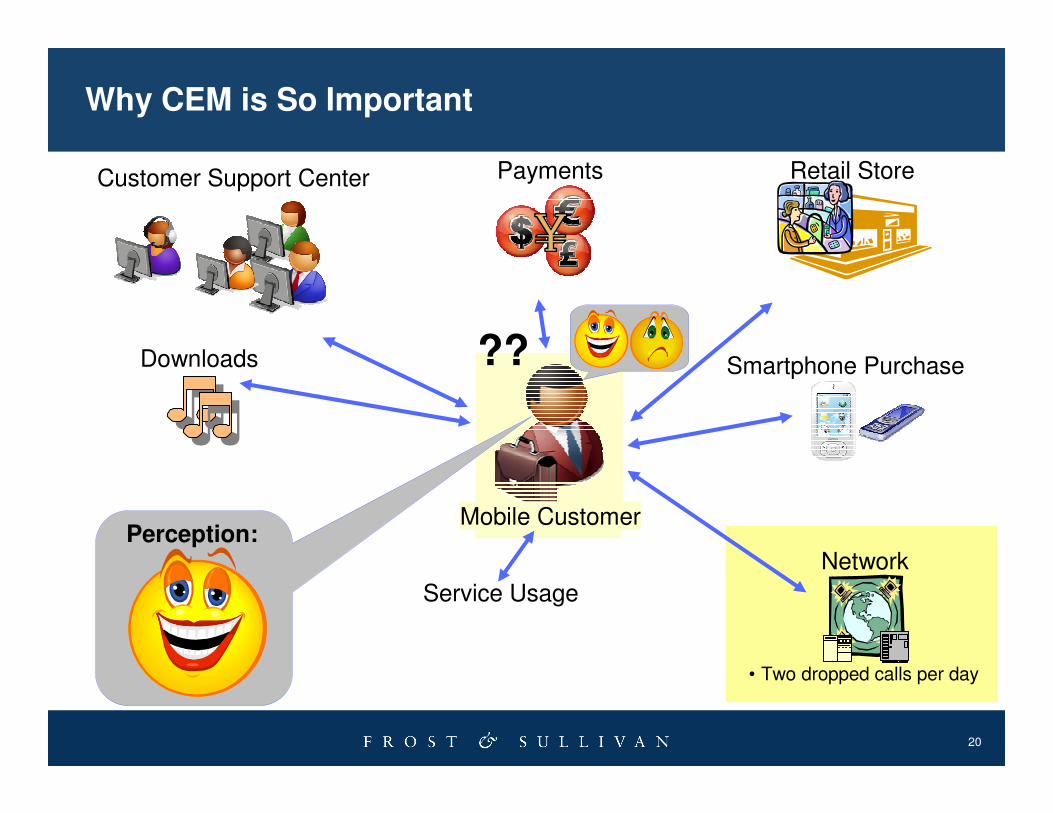

Why CEM is So Important

Mobile Customer

Network

• Two dropped calls per day

Downloads

Payments

Smartphone Purchase

Customer Support Center Retail Store

Service Usage

??

Perception:

21

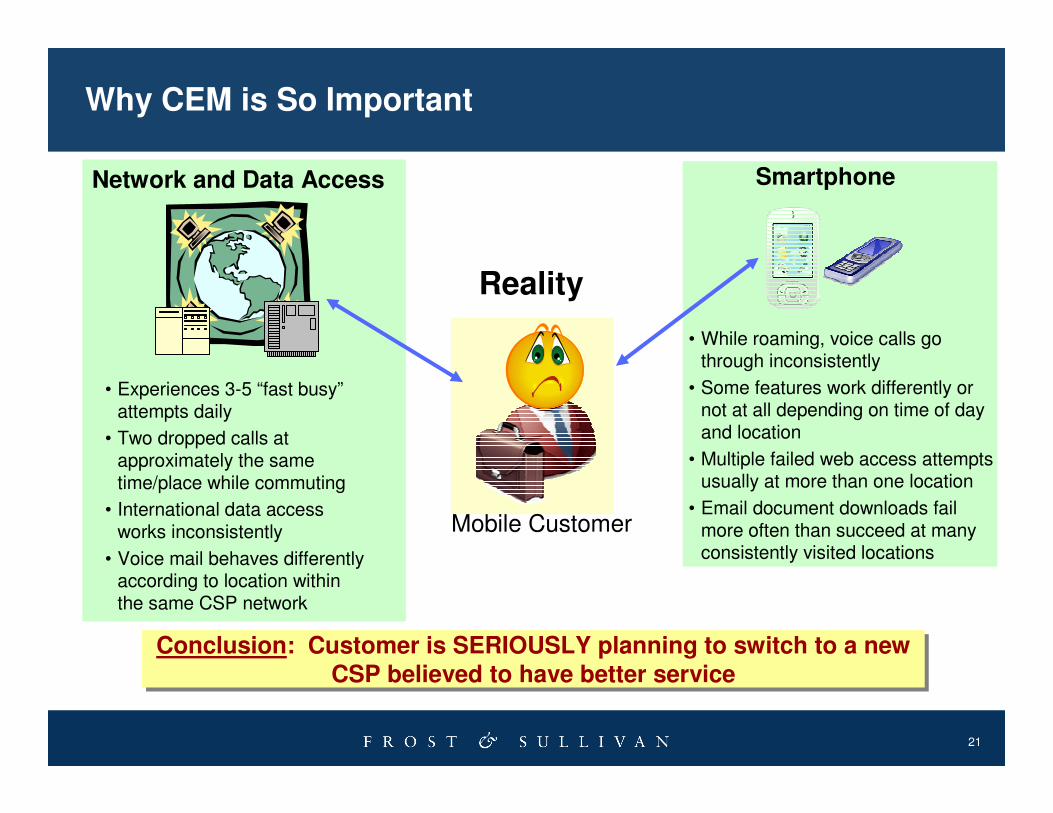

Why CEM is So Important

Mobile Customer

SmartphoneNetwork and Data Access

Conclusion: Customer is SERIOUSLY planning to switch to a new CSP believed to have better service

Conclusion: Customer is SERIOUSLY planning to switch to a new CSP believed to have better service

• While roaming, voice calls go through inconsistently

• Some features work differently or not at all depending on time of day and location

• Multiple failed web access attempts usually at more than one location

• Email document downloads fail more often than succeed at many consistently visited locations

• Experiences 3-5 “fast busy”attempts daily

• Two dropped calls at approximately the same time/place while commuting

• International data access works inconsistently

• Voice mail behaves differently according to location within the same CSP network

Reality

22

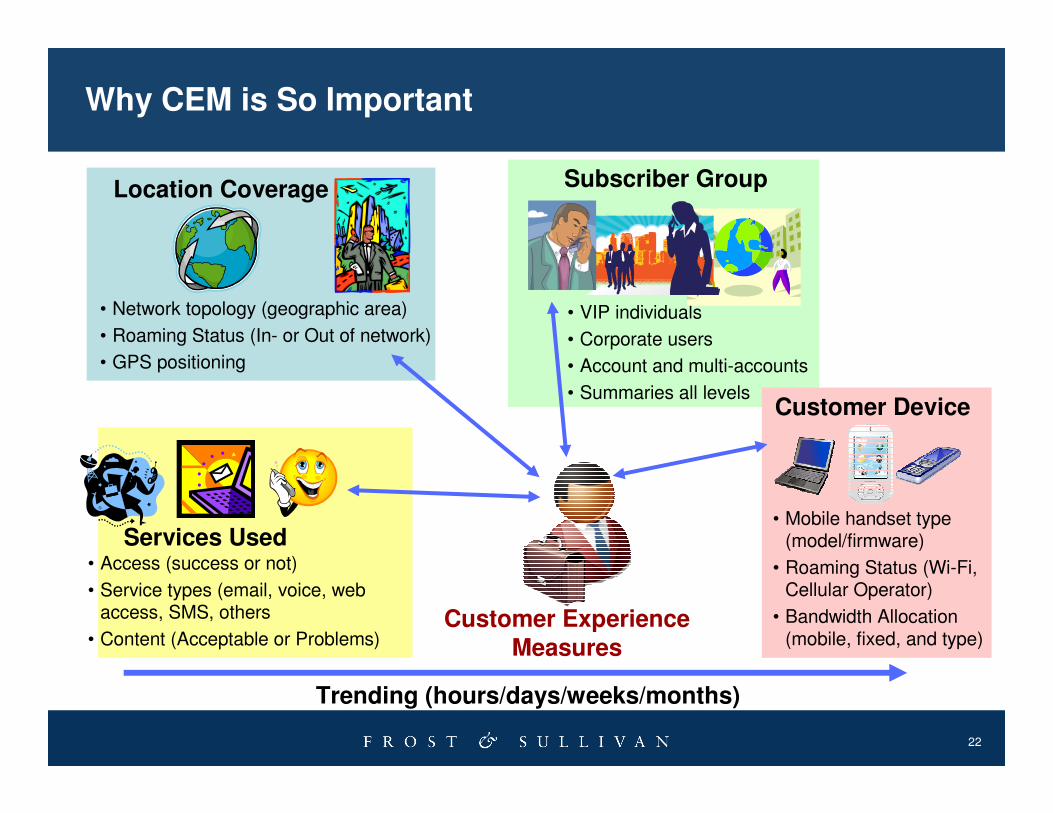

• VIP individuals

• Corporate users

• Account and multi-accounts

• Summaries all levels

Subscriber Group

Why CEM is So Important

Customer Experience

Measures

• Mobile handset type (model/firmware)

• Roaming Status (Wi-Fi, Cellular Operator)

• Bandwidth Allocation (mobile, fixed, and type)

Customer Device

Services Used• Access (success or not)

• Service types (email, voice, web access, SMS, others

• Content (Acceptable or Problems)

Trending (hours/days/weeks/months)

Location Coverage

• Network topology (geographic area)

• Roaming Status (In- or Out of network)

• GPS positioning

23

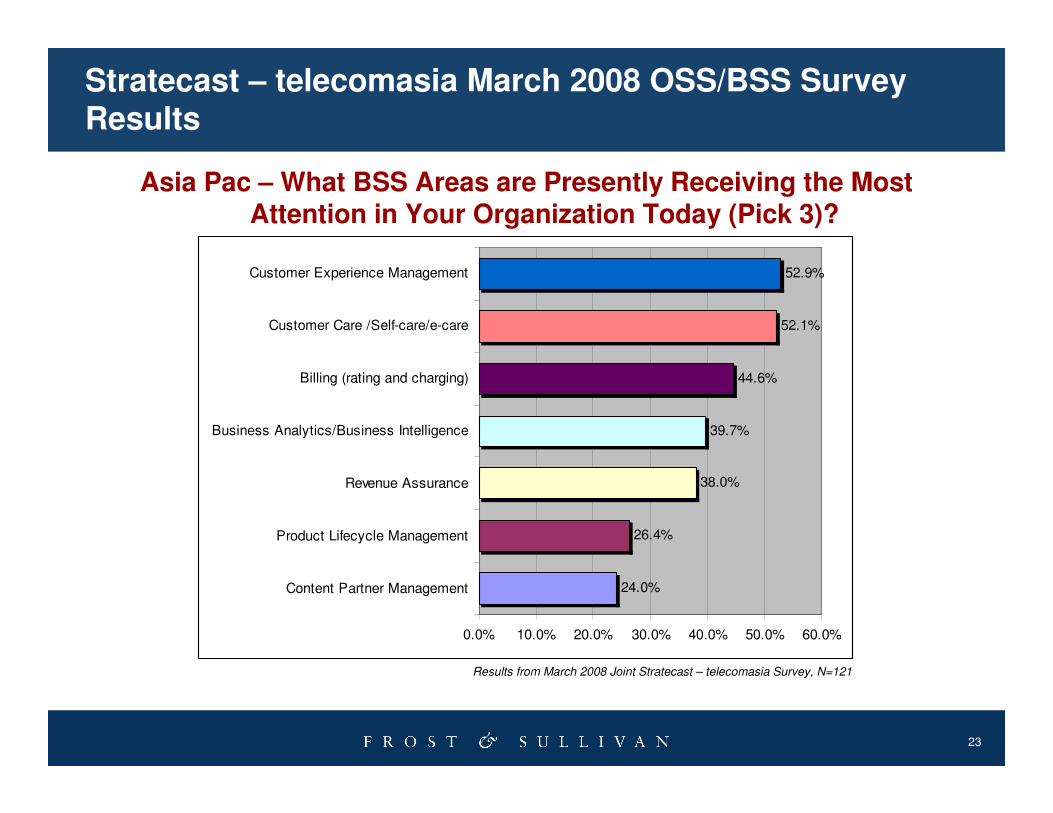

Stratecast – telecomasia March 2008 OSS/BSS Survey Results

24.0%

26.4%

38.0%

39.7%

44.6%

52.1%

52.9%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0%

Content Partner Management

Product Lifecycle Management

Revenue Assurance

Business Analytics/Business Intelligence

Billing (rating and charging)

Customer Care /Self-care/e-care

Customer Experience Management

Results from March 2008 Joint Stratecast – telecomasia Survey, N=121

Asia Pac – What BSS Areas are Presently Receiving the Most Attention in Your Organization Today (Pick 3)?

24

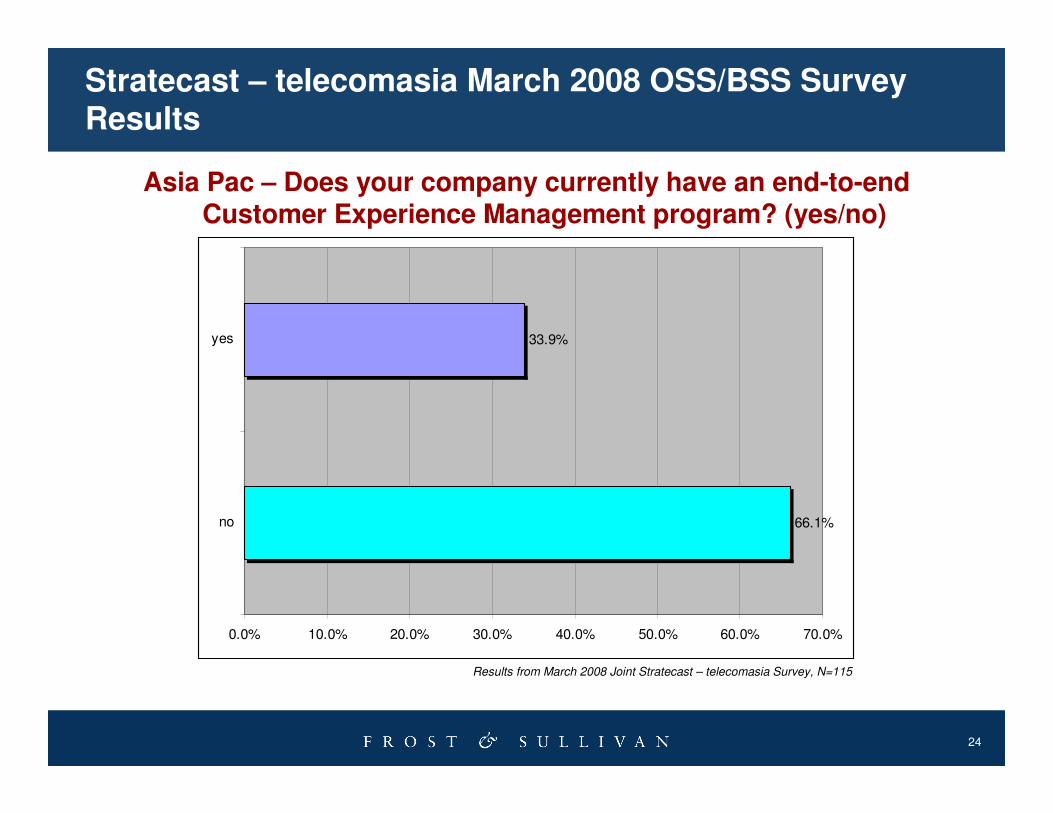

Stratecast – telecomasia March 2008 OSS/BSS Survey Results

Results from March 2008 Joint Stratecast – telecomasia Survey, N=115

Asia Pac – Does your company currently have an end-to-end Customer Experience Management program? (yes/no)

66.1%

33.9%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0%

no

yes

25

Stratecast – The Last Word

• Customer lifestyle services featuring a combination of

voice, data, entertainment, presence and availability are

quickly becoming a reality.

• Operators overwhelmingly look to billing for subscriber behaviour clues and customer experience data.

• Current CSP attitudes suggest a move toward fewer vendors and less systems integration activity.

• Competition isn’t just the cablecom for a telecom operator …

26

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by taking our survey.

What would you like to see from Frost & Sullivan?

27

For Additional Information

• To leave a comment, ask the analyst a question, or receive the

free audio segment that accompanies this presentation, please contact Stephanie Ochoa, Analyst Briefing Coordinator, at (210)

247-2421 or via email, [email protected].