stora enso key facts

DESCRIPTION

Key facts about Stora Enso, spring 2009TRANSCRIPT

Stora Enso Key facts

2

Stora Enso in brief

•

Stora Enso is a forest products company producing newsprint and book paper, magazine paper, fine paper, consumer board, industrial

packaging

and wood

products•

12.7 million tonnes of paper and board

•

6.9 million m3

of sawn and processed wood products

•

Sales 2008 EUR 11.0 billion•

Approximately 29 000 employees in more than 35 countries

•

Market capitalisation EUR 4.4 billion•

Shares listed on Helsinki and Stockholm stock exchanges

3

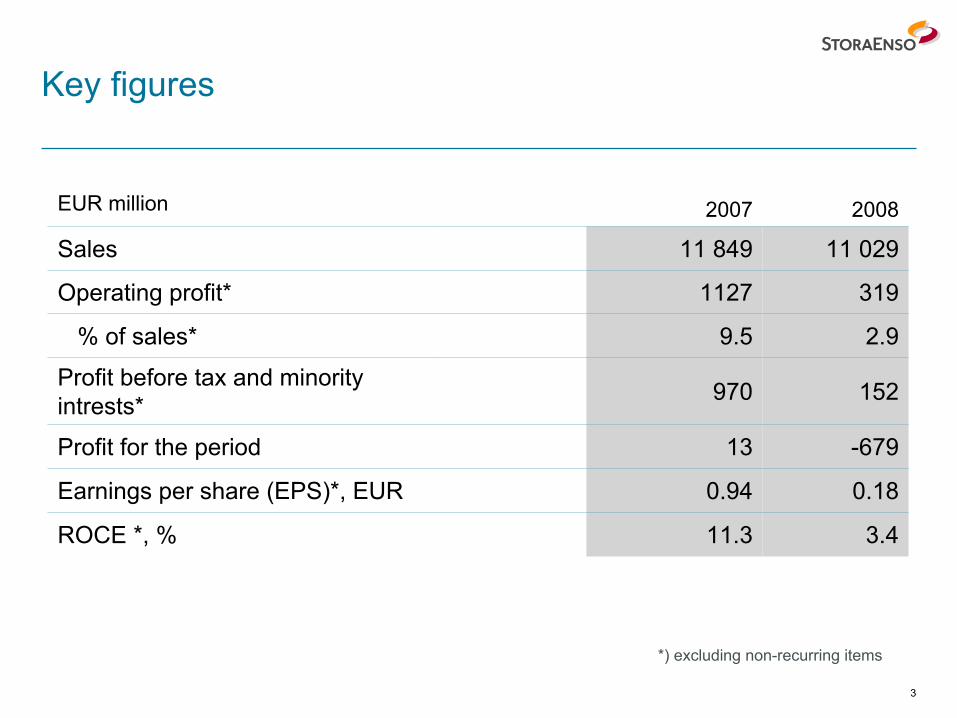

Key figures

EUR

million 2007 2008

Sales 11 849 11 029

Operating

profit* 1127 319

% of sales* 9.5 2.9

Profit

before

tax

and minority intrests* 970 152

Profit

for the period 13 -679

Earnings

per share

(EPS)*, EUR 0.94 0.18

ROCE *, % 11.3 3.4

*) excluding non-recurring items

4

Group Executive Team

CEO

Jouko

Karvinen

Wood Supply, HR,Sustainability

Elisabet

Salander

Björklund

Technology & Strategy

Bernd Rettig

CFO

Markus Rauramo

Wood Products

Hannu

Kasurinen

Packaging

Mats Nordlander

Fine Paper

Hannu

Alalauri

Publication Paper

Juha

Vanhainen

5

Production plants

Production plants

Pulp in bales

6

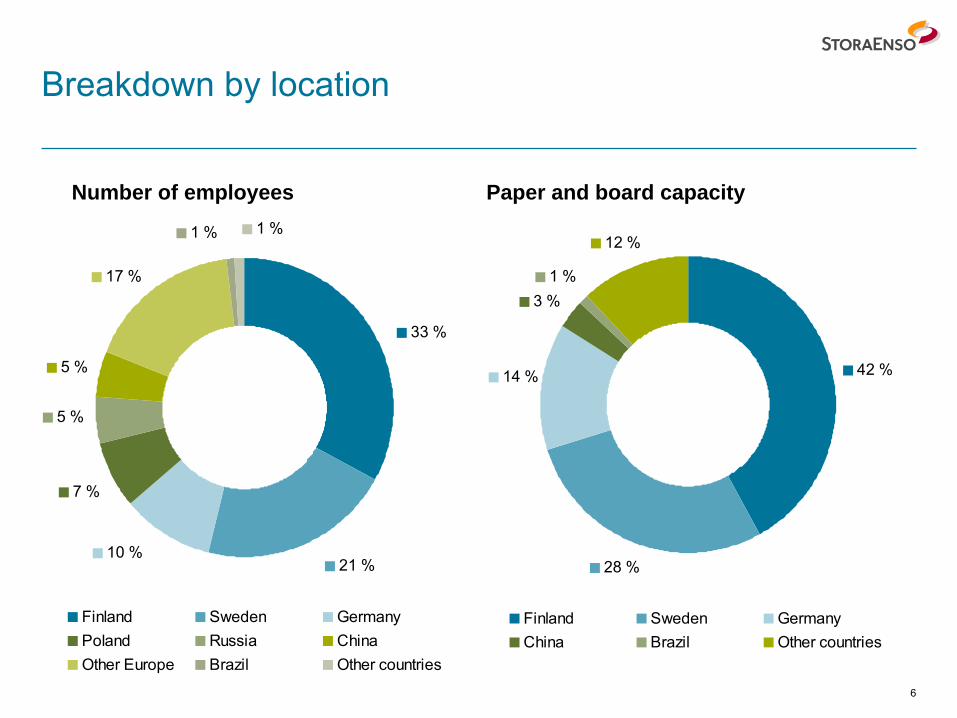

Breakdown by location

Number of employees Paper and board capacity

21 %10 %

7 %

5 %

5 %

1 % 1 %

17 %

33 %

Finland Sweden GermanyPoland Russia ChinaOther Europe Brazil Other countries

28 %

14 %

3 %1 %

12 %

42 %

Finland Sweden GermanyChina Brazil Other countries

7

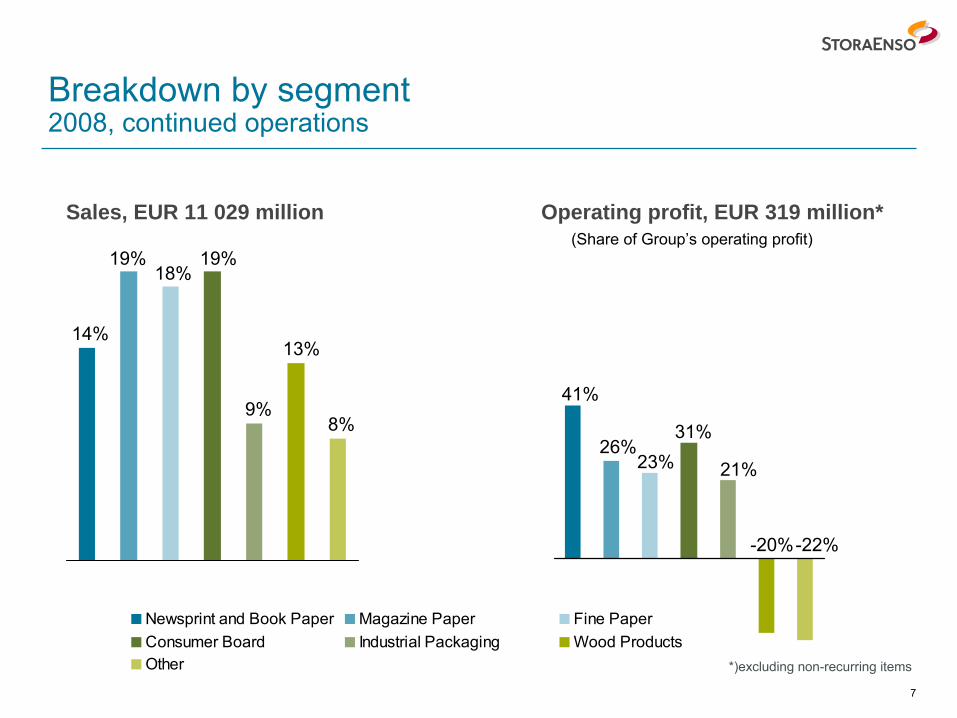

Breakdown by segment 2008, continued operations

Operating profit, EUR 319 million*(Share

of Group’s

operating

profit)

*)excluding non-recurring items

41%

26%31%

21%

-22%-20%

23%

Sales, EUR 11 029 million

14%

19%18%

19%

13%

9%8%

Newsprint and Book Paper Magazine Paper Fine PaperConsumer Board Industrial Packaging Wood ProductsOther

8

Ownership by distribution 31 Dec 2008

% of shares % of voting power

(Non-Finnish/ Non-Swedish shareholders)

25 %

2 %

30 %

3 %

4 %

15 %21 %

Finnish Institutions Finnish state Finnish private shareholdersSwedish institutions Swedish private shareholders ADRsUnder nominee names

12 %

2 %

13 %

3 %11 %

46 %

13 %

Business areas

10

What

we

do

Publication paper•

Newsprint

and book

paper: standard

newsprint, imroved

newsprint, and directory

and book

paper

•

Magazine paper: super-calendered, uncoated machine-finished, machine-

finished coated, and coated magazine paper

Fine paper•

Graphic paper (art books, upmarket magazines, catalogues)

•

Office paper (document printing paper, envelope paper, business forms, note pads etc.)

11

What

we

do

(continued)

Packaging•

Consumer

board: liquid

packaging

board, food service board, cartonboard

and graphical board

•

Industrial

packaging: corrugated packaging, containerboard, cores and

coreboard, laminating paper, paper sacks, sack and kraft

paper

Wood products•

Value added products for the construction and joinery industries

•

Sawn and processed wood products to timber retailers, merchants and importer-distributors

12

Newsprint

and Book

Paper

Products•

Standard newsprint, imroved

newsprint,

and directory

and book

paper.

Capacity •

3.0 million t/a

13

Newsprint and Book Paper

Newsprint and Book Paper

Maxau

Kvarnsveden

SachsenLangerbrugge

Hylte

Varkaus

Anjala

14

Magazine Paper

Products•

Super-calendered

(SC), uncoated

machine-finished (MF), machine- finished coated (MFC), and coated

(LWC, MWC, HWC) magazine paper.

Capacity•

3.0 million

t/a

15

Magazine Paper

Magazine Paper

Dawang

Veitsiluoto

Arapoti

Langerbrugge

Kotka

Kabel

MaxauCorbehem

Kvarnsveden

16

Fine Paper

Products•

Graphic paper (coated fine paper) is used in art books annual reports, upmarket magazines and catalogues. Office paper (uncoated fine paper) products include document printing paper, digital paper, envelope paper, business forms and paper used in school notebooks and writing pads.

Capacity •

3.2 million t/a

17

Fine Paper

Office papers

Graphic papers

Sheeting plant

Suzhou

Uetersen

Nymölla

ImatraVarkaus

OuluVeitsiluoto

Mendelsham

Antwerp

18

Consumer

Board

Products•

Liquid packaging board, food service board, cartonboard

and graphical

board.

Capacity•

2.5

million t/a

19

Consumer Board

Consumer Board

Plastic Coating Plants

Barcelona

ImatraIngeroisKarhulaFors

SkoghallForshaga

20

Industrial

Packaging

Products•

Corrugated

packaging, containerboard,

cores and coreboard, laminating paper, paper sacks, sack and kraft

paper.

Capacity•

Corrugated

packaging

1.5 billion

m2

•

Cores

0.3 million

t/a

21

Industrial Packaging

Laminating Papers

Containerboards

Corrucated

Packaging

Corenso

Pasir

Gudang

Foshan

Hangzhou

Wisconsin Rapids

Tolosana

Saint-Seurin-

Sur-L’Isle

Milton KeynesBolton

JülichKrefeld

Páty

EdamMosina

Tychy ŁodźOstrolęka

KaunasSkene

Bäckefors

RigaTallinn

LukhovitsyArzamas

BalabanovoJönköpingVikingstad Imatra

LoviisaKotka

Mohed

PoriKristiinankaupunki

RuovesiLahti

Heinola

22

Wood Products

Products•

Mass-customised, value-added products for industrial end-uses. These include glue-laminated, stress-graded and finger-jointed products and components for the construction and joinery industries. Sawn and processed wood products to timber retailers, merchants and importer-distributors.

Capacity •

Sawn

timber

6.9 million

m3

of which

3.2 million

m3

value-added

products

23

Wood Products

Wood Products

Nebolchi

Impilahti

Launkalne

Alytus

Ala

UimaharjuKitee

NäpiKopparfors

Gruvön

Veitsiluoto

Varkaus

TolkkinenKotka

Imavere

Swietajno

Murów

Amsterdam

Plana

PfarrkirchenZdirecBrandSollenauYbbs

Bad St. Leonhard

Honkalahti

Appendix

25

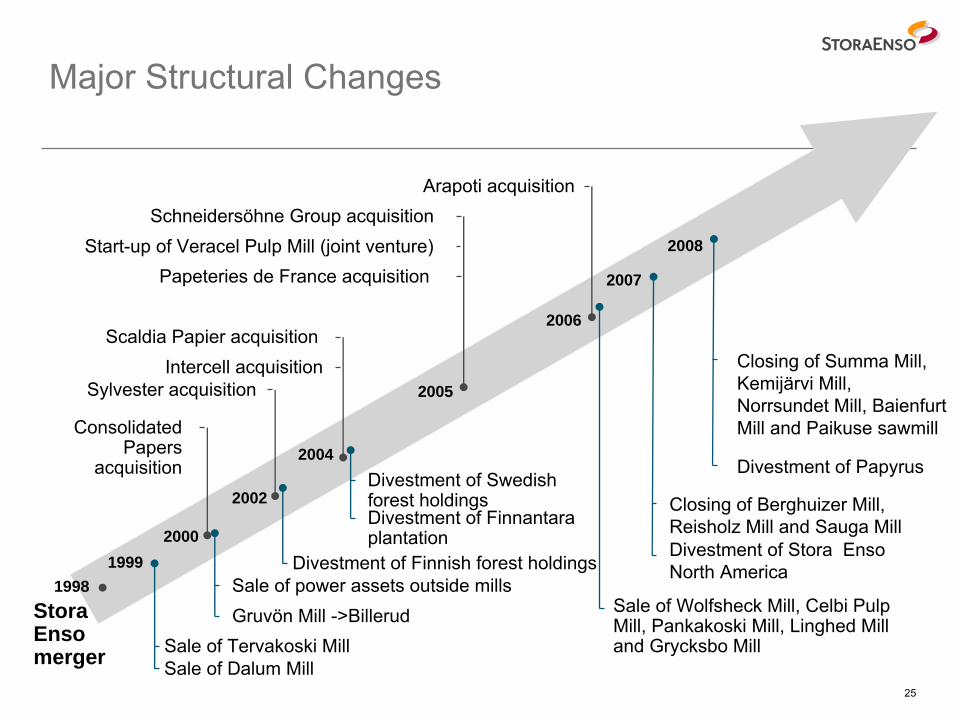

Major Structural Changes

Gruvön

Mill ->BillerudSale of power assets outside mills

Divestment of Finnish

forest holdings

Divestment of Swedish

forest holdingsDivestment of Finnantara

plantation

Sylvester acquisitionIntercell

acquisitionScaldia

Papier

acquisition

Papeteries

de France acquisition

Schneidersöhne

Group acquisition

ConsolidatedPapers

acquisition

Stora Enso merger

Start-up of Veracel

Pulp Mill (joint venture)

19981999

2000

2002

2004

2005

2006

Sale of Dalum MillSale of Tervakoski Mill

Arapoti

acquisition

Sale of Wolfsheck

Mill, Celbi

Pulp Mill, Pankakoski

Mill, Linghed

Mill and Grycksbo

Mill

2007

Divestment

of Stora Enso North America

2008

Closing

of Berghuizer

Mill, Reisholz

Mill

and Sauga

Mill

Divestment

of Papyrus

Closing

of Summa Mill, Kemijärvi Mill, Norrsundet

Mill, Baienfurt

Mill

and Paikuse

sawmill

26

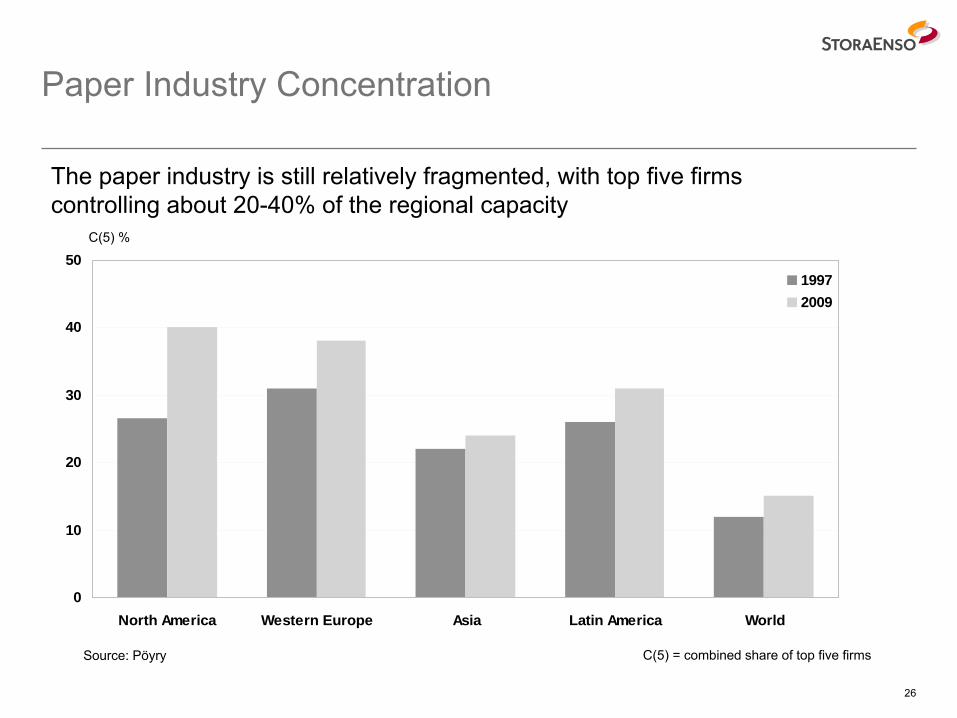

Paper Industry Concentration

Source: Pöyry

0

10

20

30

40

50

North America Western Europe Asia Latin America World

19972009

The paper industry is still relatively fragmented, with top five

firms controlling about 20-40% of the regional capacity

C(5) = combined share of top five firms

C(5) %

27

Long-term Demand Growth

by Region through 2025 Paper

and Paperboard

-1

0

1

2

3

4

5

6

7

0 20 40 60 80 100

Demand

growth, %/a

Source: PöyryShare of consumption in 2006, %

JapanNorth America

Western Europe

India

Latin AmericaRest of Asia

Oceania

China

Middle

EastRussia

Average

1.9%/a

Eastern EuropeAfrica