stats sa 2015 first quarter labour force survey

TRANSCRIPT

Quarterly Labour Force Survey Q1: 2015

Pali LehohlaStatistician-General

@StatsSA

#Labour

The South Africa I know, the home I understand

QLFS

Outline• New master sample• Results of QLFS Q1 2015• Employment

o Sources of formal sector employmento Employment in the formal and informal sector

• Unemployment• Inactivity• Labour dynamics• Q1 2015 Highlights

The introduction of the new 2013 Master sample

New

Mas

ter

Sam

ple

The first part of the presentation will focus on the following:

• The need for the new Master sample

• The aims of the redesigned Master sample

• Detailing the differences between the old and new Master

sample

• As well as the implications of the new Master sample and

comparability.

• We will then present the results of the QLFS Q1: 2015

The QLFS Q1: 2015 is the first publication to be release based on the new 2013 Master sample

New

Mas

ter

Sam

ple

The need for a new master sample

Sample becomes less efficient over time as

information it is based on becomes outdated.

Thus statistical agencies redesign national

household samples following a Census.

This is to account for the changes in the

structure of the underlying population which

changes over time and is only captured by a

Census.

A Census is not based on a sample and collects

information on all persons in the country at a

specific point in time.

The old 2007 Master sample was based on the

2001 Census data while the redesigned 2013

Master sample is based on the 2011 Census.

New

Mas

ter

Sam

ple

The aims of the new master sample

To update the 2007 Master sample with

the latest Census information (2011

Census).

To address certain constraints as

identified in the previous design, for

example Mining employment estimates.

New

Mas

ter

Sam

ple

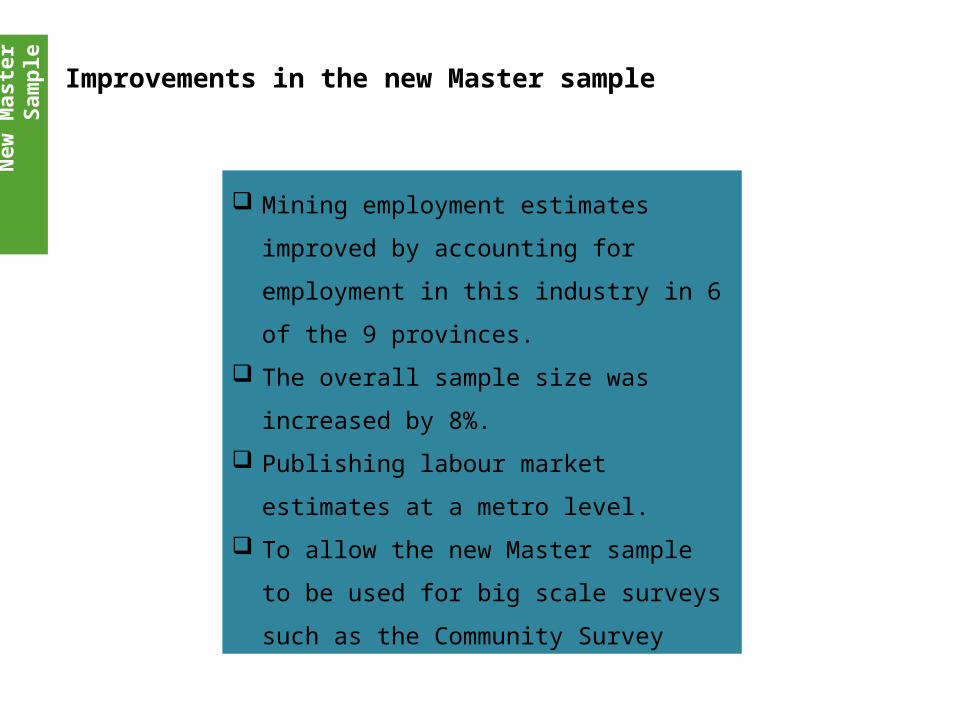

Improvements in the new Master sample

Mining employment estimates improved by

accounting for employment in this industry

in 6 of the 9 provinces.

The overall sample size was increased by

8%.

Publishing labour market estimates at a

metro level.

To allow the new Master sample to be used

for big scale surveys such as the

Community Survey

New

Mas

ter

Sam

ple

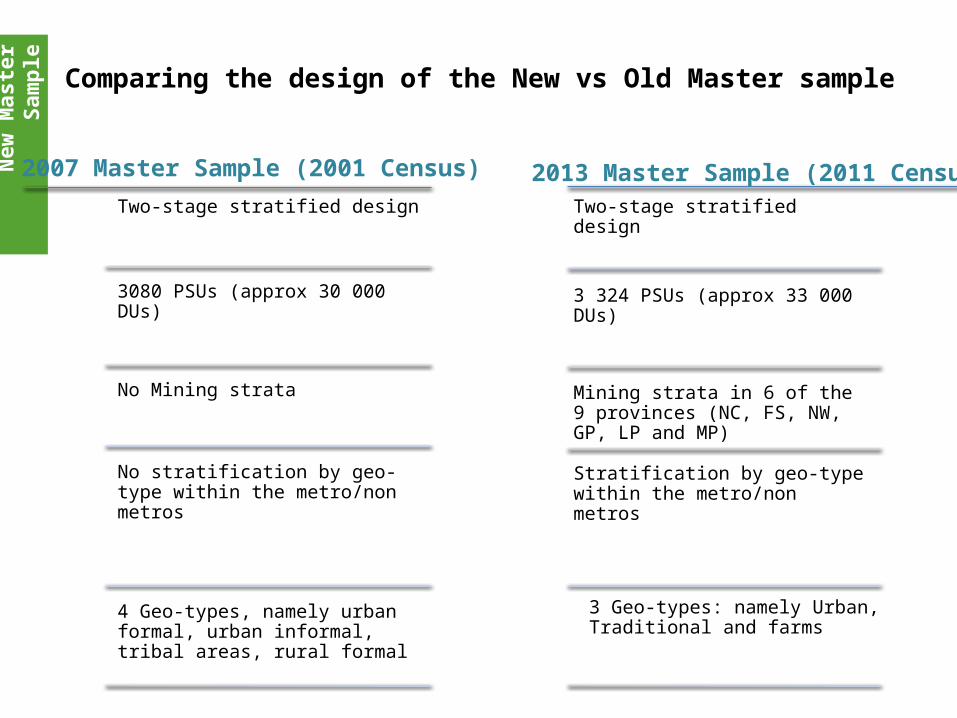

Comparing the design of the New vs Old Master sample

Two-stage stratified design

3080 PSUs (approx 30 000 DUs)

No Mining strata

No stratification by geo-type within the metro/non metros

4 Geo-types, namely urban formal, urban informal, tribal areas, rural formal

Two-stage stratified design

3 324 PSUs (approx 33 000 DUs)

Mining strata in 6 of the 9 provinces (NC, FS, NW, GP, LP and MP)

Stratification by geo-type within the metro/non metros

2007 Master Sample (2001 Census) 2013 Master Sample (2011 Census)

3 Geo-types: namely Urban, Traditional and farms

New

Mas

ter

Sam

ple

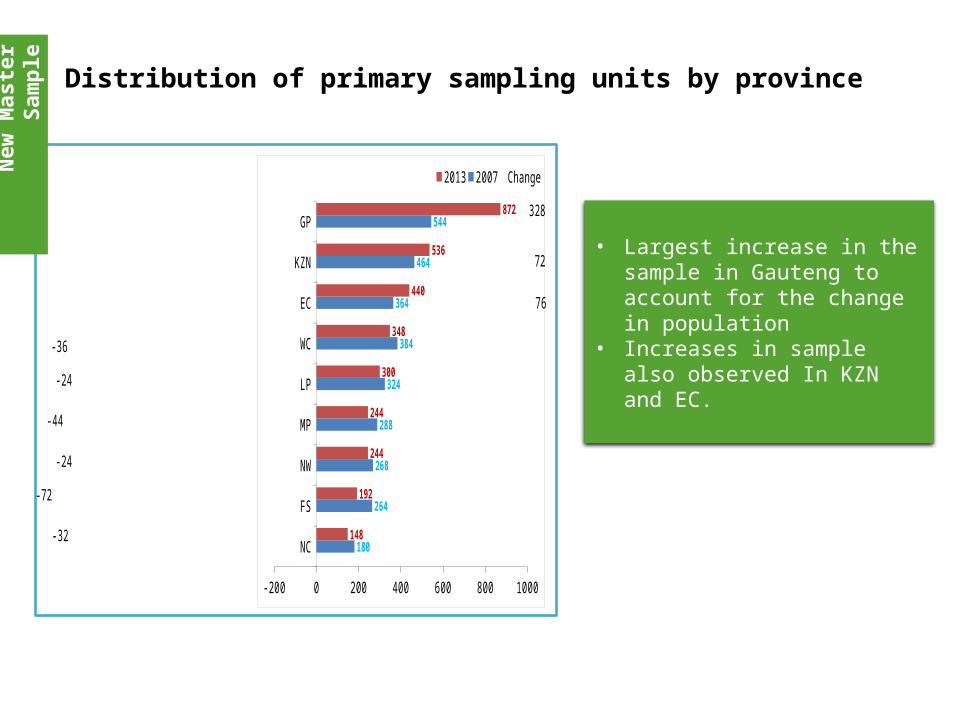

Distribution of primary sampling units by province

• Largest increase in the sample in Gauteng to account for the change in population

• Increases in sample also observed In KZN and EC.

NC

FS

NW

MP

LP

WC

EC

KZN

GP

-200 0 200 400 600 800 1000

-32

-72

-24

-44

-24

-36

76

72

328

180

264

268

288

324

384

364

464

544

148

192

244

244

300

348

440

536

872

2013 2007 Change

New

Mas

ter

Sam

ple

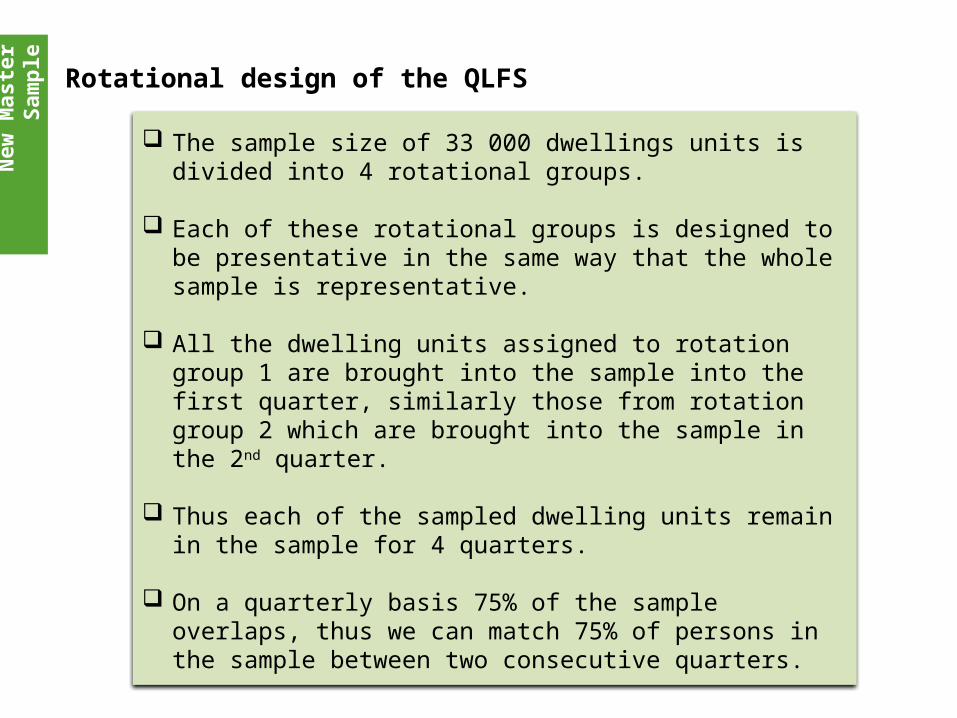

Rotational design of the QLFS

The sample size of 33 000 dwellings units is divided into 4 rotational groups.

Each of these rotational groups is designed to be presentative in the same way that the whole sample is representative.

All the dwelling units assigned to rotation group 1 are brought into the sample into the first quarter, similarly those from rotation group 2 which are brought into the sample in the 2nd quarter.

Thus each of the sampled dwelling units remain in the sample for 4 quarters.

On a quarterly basis 75% of the sample overlaps, thus we can match 75% of persons in the sample between two consecutive quarters.

New

Mas

ter

Sam

ple

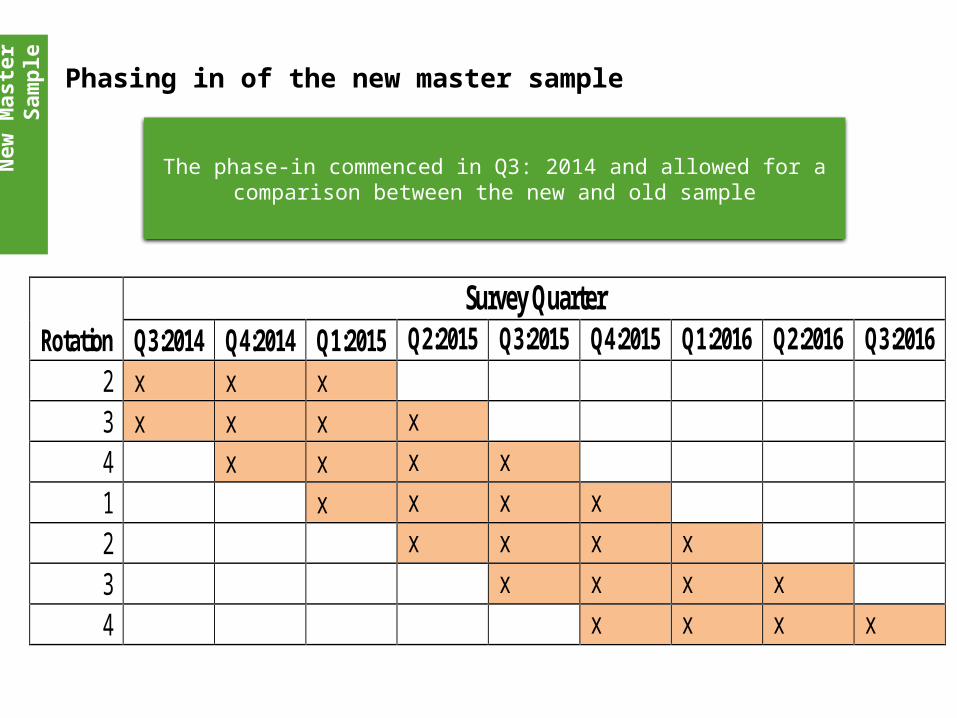

Phasing in of the new master sample

The phase-in commenced in Q3: 2014 and allowed for a comparison between the new and old sample

Rotation Survey Quarter

Q3:2014 Q4:2014 Q1:2015 Q2:2015 Q3:2015 Q4:2015 Q1:2016 Q2:2016 Q3:2016 2 x x x 3 x x x x 4 x x x x 1 x x x x 2 x x x x 3 x x x x 4 x x x x

New

Mas

ter

Sam

ple

Phasing in of the new master sample

In Q3:2014, information continued to be collected using the old sample, at the same time the new master sample was phased in as well. By Q1:

2015 the information collected was based on the new master sample

New sample phase-in 2 3Old sample 1 2 3 4

Q3: 2014Rotational groups

New sample phase-in 2 3 4Old sample 1 2 3 4

Q4: 2014Rotational groups

New sample phase-in 1 2 3 4Old sample

Q1: 2015Rotational groups

Phased out

In Q3: 2014, the overlap occurred in rotation group 2

and 3

In Q4: 2014, the overlap occurred in rotation group 2,

3 and 4

In Q1: 2015, the old sample was phased out and Q1:

2015 data collected using the new sample.

New

Mas

ter

Sam

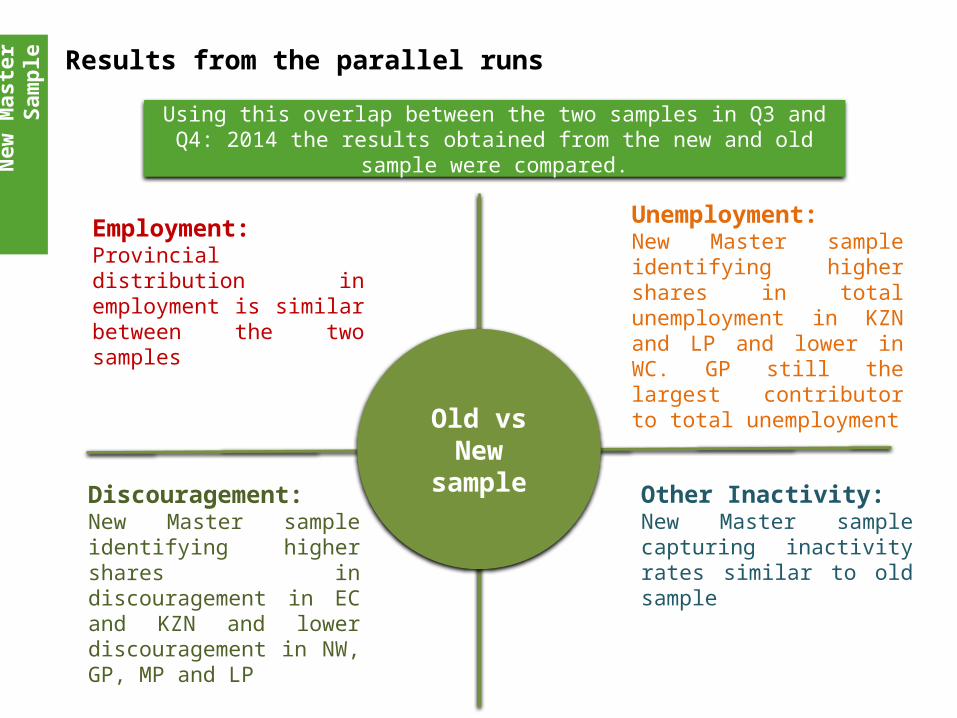

ple Results from the parallel runs

Using this overlap between the two samples in Q3 and Q4: 2014 the results obtained from the new and old sample were compared.

Employment: Provincial distribution in employment is similar between the two samples

Old vs New sample

Unemployment: New Master sample identifying higher shares in total unemployment in KZN and LP and lower in WC. GP still the largest contributor to total unemployment

Discouragement: New Master sample identifying higher shares in discouragement in EC and KZN and lower discouragement in NW, GP, MP and LP

Other Inactivity: New Master sample capturing inactivity rates similar to old sample

New

Mas

ter

Sam

ple

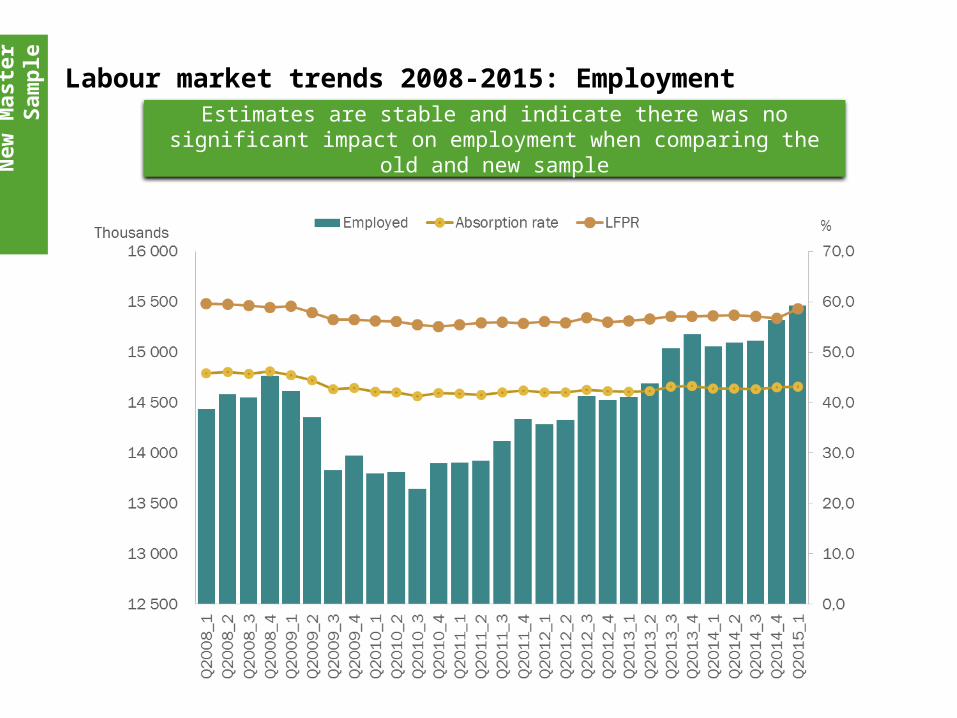

Labour market trends 2008-2015: Employment

Estimates are stable and indicate there was no significant impact on employment when comparing the old and new sample

New

Mas

ter

Sam

ple

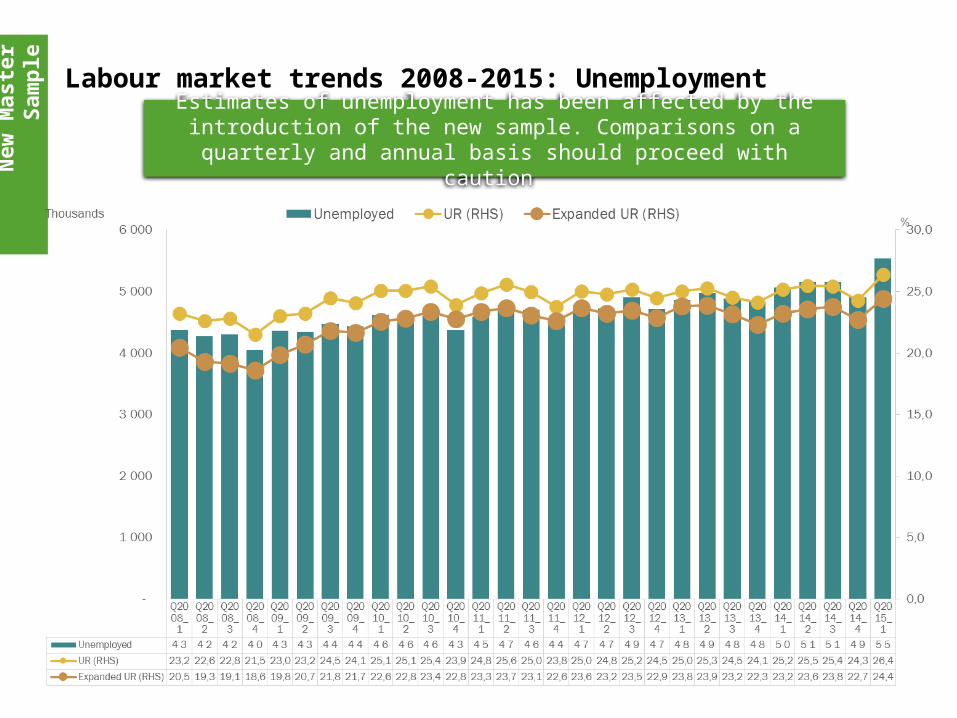

Labour market trends 2008-2015: UnemploymentEstimates of unemployment has been affected by the introduction of the

new sample. Comparisons on a quarterly and annual basis should proceed with caution

New

Mas

ter

Sam

ple

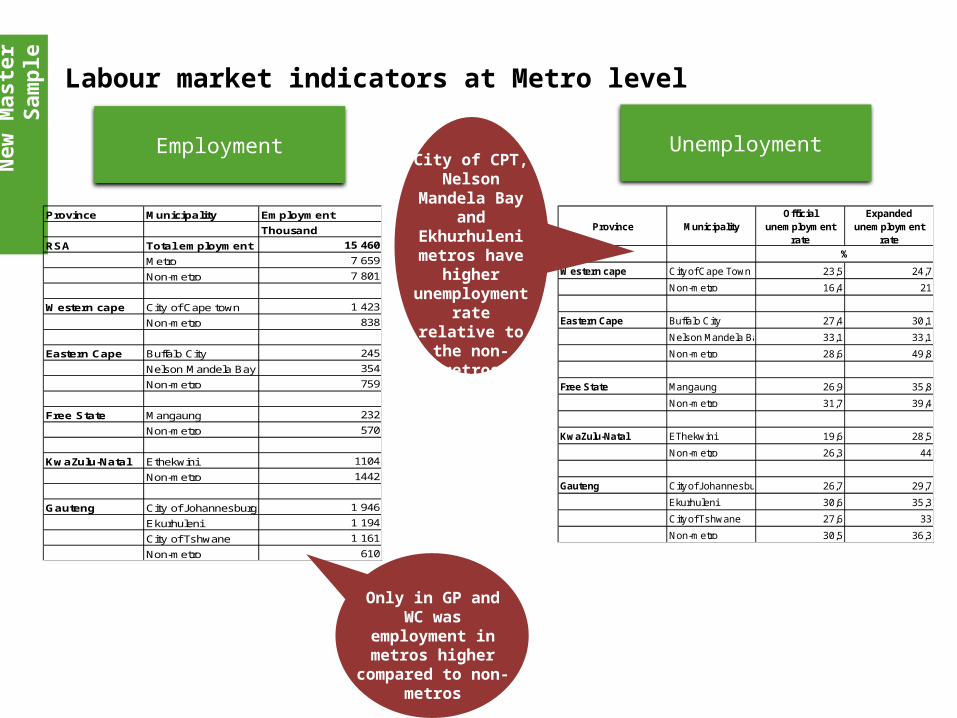

Labour market indicators at Metro level

Employment

Province Municipality Employment

Thousand

RSA Total employment 15 460

Metro 7 659

Non-metro 7 801

Western cape City of Cape town 1 423

Non-metro 838

Eastern Cape Buffalo City 245

Nelson Mandela Bay 354

Non-metro 759

Free State Mangaung 232

Non-metro 570

KwaZulu-Natal Ethekwini 1104

Non-metro 1442

Gauteng City of Johannesburg 1 946

Ekurhuleni 1 194

City of Tshwane 1 161

Non-metro 610

Unemployment

Province MunicipalityOfficial

unemployment rate

Expanded unemployment

rate

Western cape City of Cape Town 23,5 24,7

Non-metro 16,4 21

Eastern Cape Buffalo City 27,4 30,1

Nelson Mandela Bay 33,1 33,1

Non-metro 28,6 49,8

Free State Mangaung 26,9 35,8

Non-metro 31,7 39,4

KwaZulu-Natal EThekwini 19,6 28,5

Non-metro 26,3 44

Gauteng City of Johannesburg 26,7 29,7

Ekurhuleni 30,6 35,3

City of Tshwane 27,6 33

Non-metro 30,5 36,3

%

Only in GP and WC was employment in

metros higher compared to non-

metros

City of CPT, Nelson

Mandela Bay and

Ekhurhuleni metros have

higher unemployment rate relative to the non-metros

New

Mas

ter

Sam

ple

Conclusion

The updating of the old master sample using the 2011 Census brings with it efficiency gains in terms of the estimates produced.

There have been a number of improvements in the new sample including Mining estimates and estimates published at the metro level.

When comparing the old and new sample, employment estimates are stable.

The new master sample is capturing higher levels of unemployment and lower inactivity in provinces such as Gauteng. Due to the update of the master sample, the quarter on quarter and year on year comparisons may be unstable for a few quarters.

The estimates produced by the sample will be monitored over the coming quarters.

18The South Africa I know, the home I understand

QLFSL

abo

ur

Mar

ket

Q1:

2015

Results of QLFS Q1:2015

Lab

ou

r M

arke

t Q

1:20

15

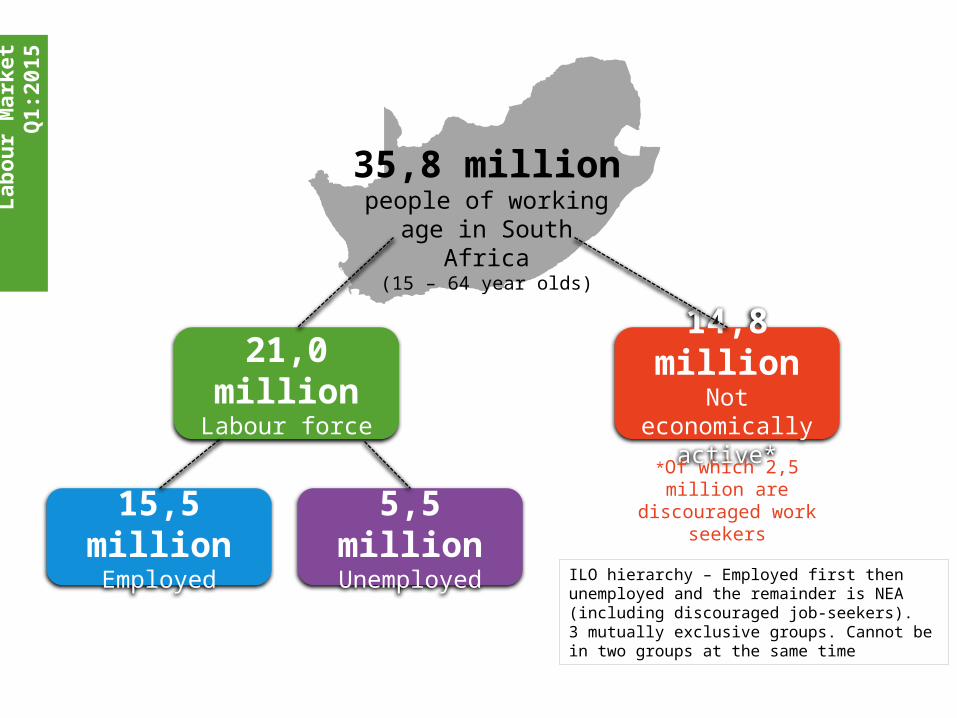

21,0 millionLabour force

15,5 millionEmployed

5,5 millionUnemployed

14,8 millionNot economically

active*

*Of which 2,5 million are discouraged work

seekers

35,8 millionpeople of working age in

South Africa(15 – 64 year olds)

ILO hierarchy – Employed first then unemployed and the remainder is NEA (including discouraged job-seekers). 3 mutually exclusive groups. Cannot be in two groups at the same time

Lab

ou

r M

arke

t Q

1:20

15

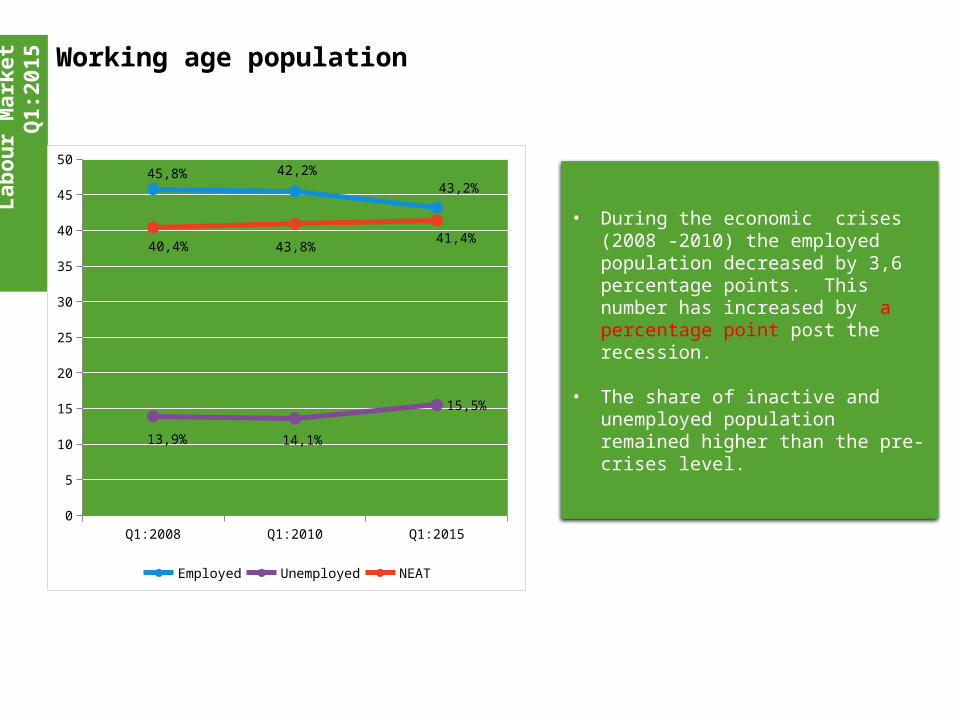

• During the economic crises (2008 -2010) the employed population decreased by 3,6 percentage points. This number has increased by a percentage point post the recession.

• The share of inactive and unemployed population remained higher than the pre-crises level.

Working age population

Q1:2008 Q1:2010 Q1:20150

5

10

15

20

25

30

35

40

45

5045,8% 42,2%

43,2%

13,9% 14,1%

15,5%

40,4% 43,8%41,4%

Employed Unemployed NEAT

Abs

orpt

ion

rate

Une

mpl

oym

ent r

ate

Lab

ou

r M

arke

t Q

1:20

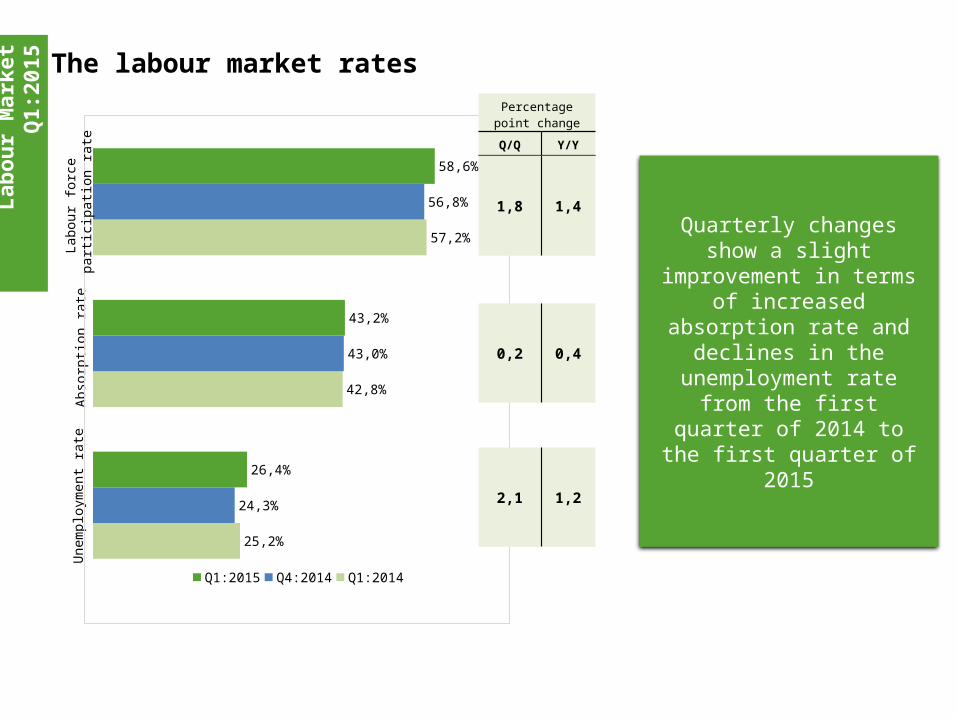

15 The labour market rates

Quarterly changes show a slight improvement in terms of increased absorption rate

and declines in the unemployment rate from the first quarter of 2014 to the

first quarter of 2015

25,2%

42,8%

57,2%

24,3%

43,0%

56,8%

26,4%

43,2%

58,6%

Q1:2015 Q4:2014 Q1:2014

Labo

ur fo

rce

part

icip

atio

n ra

tePercentage point

change

Q/Q Y/Y

1,8 1,4

0,2 0,4

2,1 1,2

Em

plo

ymen

t

Employment

2009 2010 2011 2012 2013 2014-900

-600

-300

0

300

600

900

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

Employed GDP

Th

ou

sa

nd

%

Employment changes and value-added

Em

plo

ymen

t

The year-on-year employment growth has slowed down since

the first quarter of 2014

Em

plo

ymen

t

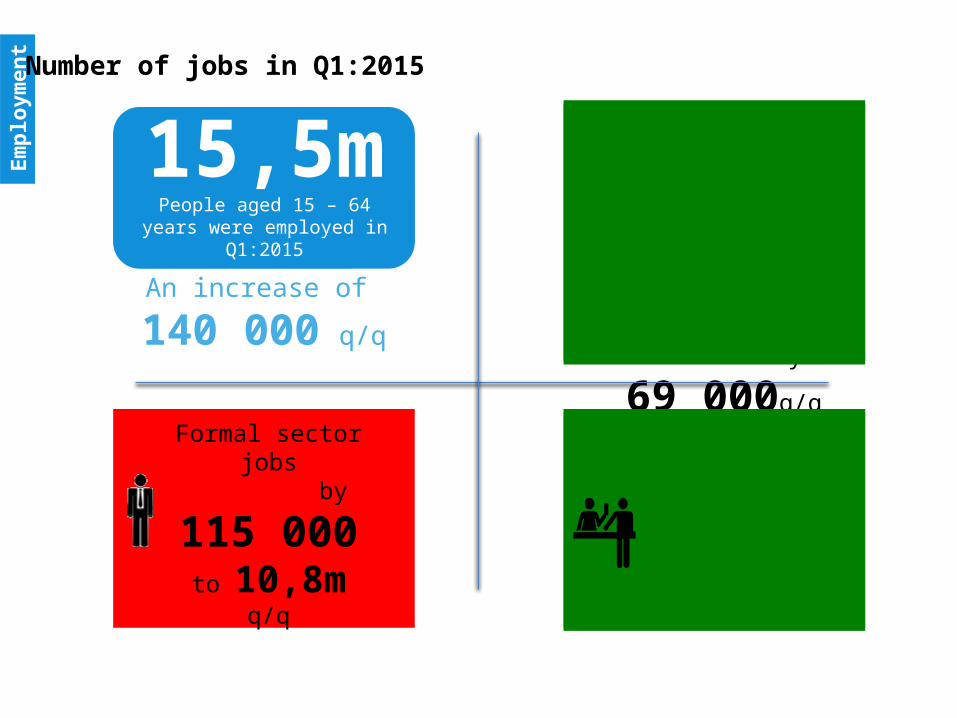

Number of jobs in Q1:2015

Jobs in the agricultural sector increased by

150 000q/qPrivate households

increased by

69 000q/q

Informal sector jobs increased by

35 000 to

2,5m q/q

15,5mPeople aged 15 – 64 years were employed in Q1:2015

An increase of

140 000 q/q

Formal sector jobs decreased by

115 000 to

10,8m q/q

15,5mPeople aged 15 – 64 years were employed in Q1:2015

EC

LP

NW

KZN

NC

MP

FS

GP

WC

RSA

33,1%

34,1%

37,8%

38,2%

40,3%

42,2%

43,0%

51,9%

53,2%

43,2%

32,7%

35,0%

39,5%

37,9%

42,1%

41,8%

41,5%

51,8%

51,4%

43,0%

Q4:2014 Q1:2015

Em

plo

ymen

t

43,2%people of working age in

South Africa(15 – 64 year olds)

Absorption rate

The Western Cape had the highest absorption rate

53,2%

33,1% The lowest absorption rate was recorded in the Eastern Cape

Percentage point change

q/q

0,2

1,8

0,1

1,5

0,4

-1,8

0,3

-1,7

-0,9

0,4

Em

plo

ymen

t

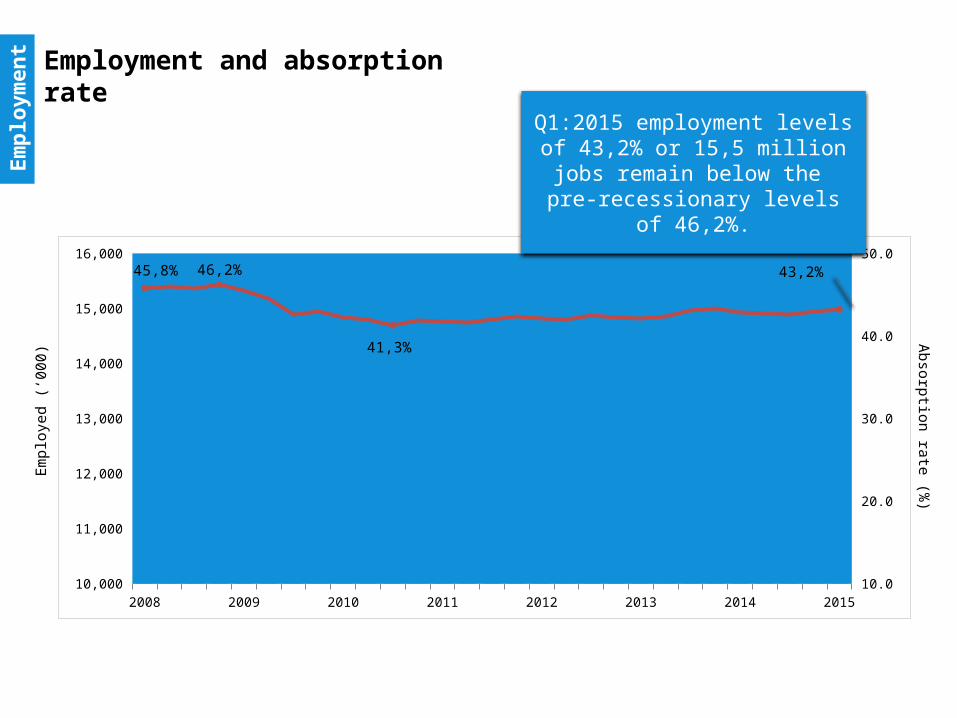

Employment and absorption rate

2008 2009 2010 2011 2012 2013 2014 201510,000

11,000

12,000

13,000

14,000

15,000

16,000

10.0

20.0

30.0

40.0

50.045,8% 46,2%

41,3%

43,2%

Q1:2015 employment levels of 43,2% or 15,5 million jobs remain

below the pre-recessionary levels of 46,2%.

Em

ploy

ed (

‘000

) Absorption rate (%

)

Em

plo

ymen

t

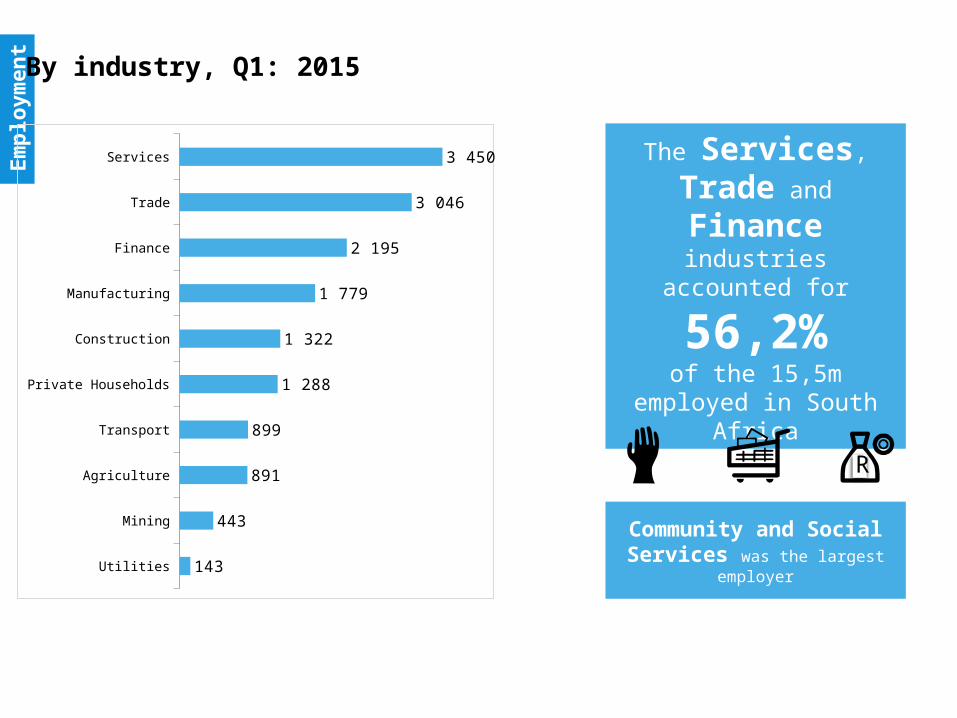

By industry, Q1: 2015

Community and Social Services was the largest employer

The Services, Trade

and Finance industries accounted for

56,2%of the 15,5m employed in

South Africa

Utilities

Mining

Agriculture

Transport

Private Households

Construction

Manufacturing

Finance

Trade

Services

143

443

891

899

1 288

1 322

1 779

2 195

3 046

3 450

R

Em

plo

ymen

t

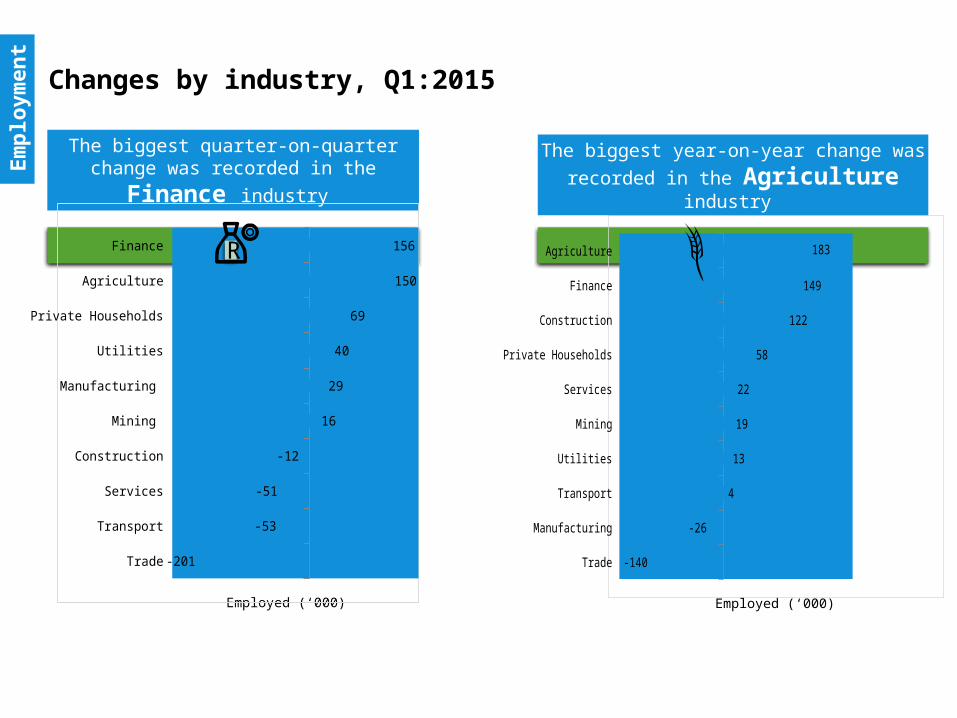

Changes by industry, Q1:2015

The biggest quarter-on-quarter change was

recorded in the Finance industry

Employed (‘000)

Trade

Manufacturing

Transport

Utilities

Mining

Services

Private Households

Construction

Finance

Agriculture

-140

-26

4

13

19

22

58

122

149

183

The biggest year-on-year change was

recorded in the Agriculture industry

Trade

Transport

Services

Construction

Mining

Manufacturing

Utilities

Private Households

Agriculture

Finance

-201

-53

-51

-12

16

29

40

69

150

156

Employed (‘000)

R

Em

plo

ymen

t

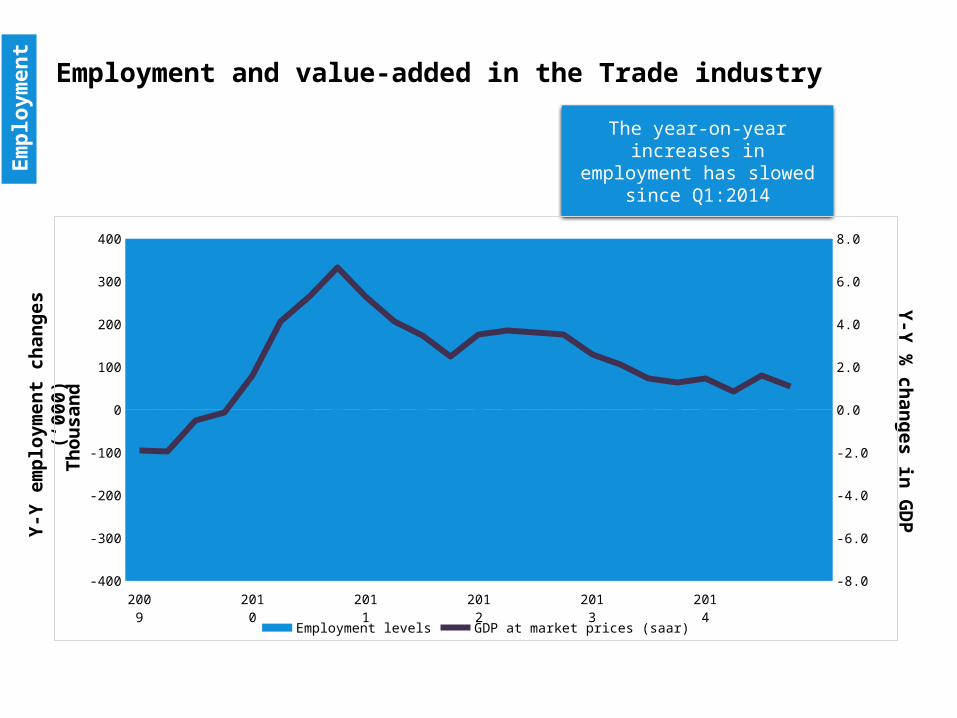

Employment and value-added in the Trade industry

Y-Y

em

plo

ymen

t ch

ang

es (

‘000

)Y

-Y %

chan

ge

s in G

DP

The year-on-year increases in employment has slowed since

Q1:2014

2009

2010

2011

2012

2013

2014

-400

-300

-200

-100

0

100

200

300

400

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

Employment levels GDP at market prices (saar)

Th

ou

sa

nd

Em

plo

ymen

t

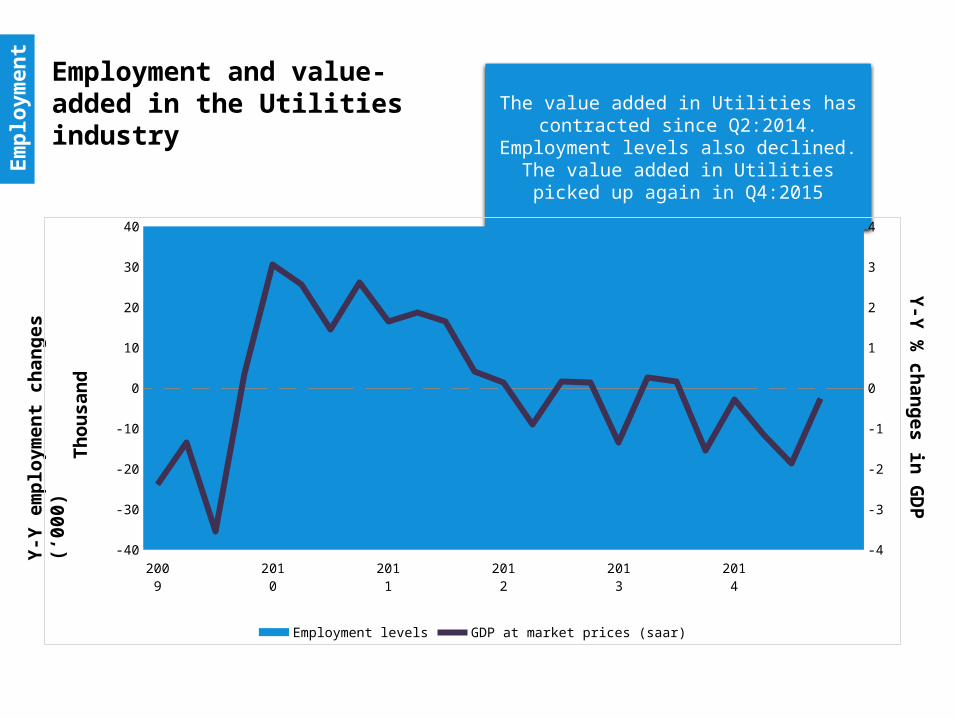

The value added in Utilities has contracted since Q2:2014. Employment levels also

declined. The value added in Utilities picked up again

in Q4:2015

Y-Y

em

plo

ymen

t ch

ang

es (

‘000

)Y

-Y %

chan

ge

s in G

DP

2009 2010 2011 2012 2013 2014-40

-30

-20

-10

0

10

20

30

40

-4

-3

-2

-1

0

1

2

3

4

Employment levels GDP at market prices (saar)

Th

ou

sa

nd

Employment and value-added in the Utilities industry

Employment and value-added in the Manufacturing industry

Y-Y

em

plo

ymen

t ch

ang

es (

‘000

)Y

-Y %

chan

ge

s in G

DP

2009 2010 2011 2012 2013 2014-300

-200

-100

0

100

200

300

-20

-10

0

10

20

GDP Employment levels

Em

plo

ymen

t

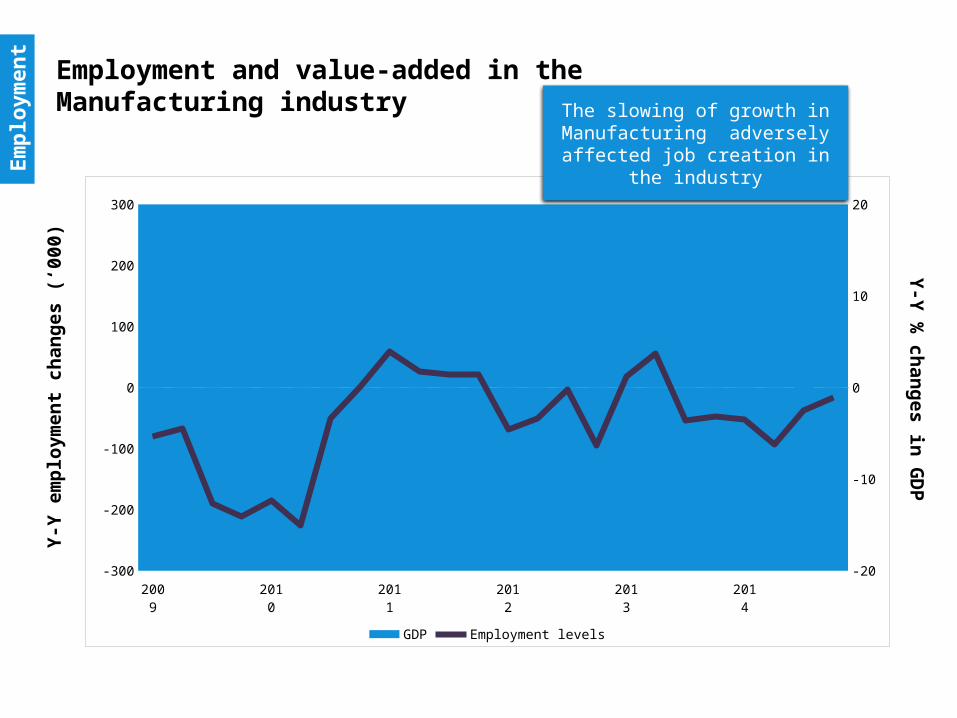

The slowing of growth in Manufacturing adversely affected

job creation in the industry

So

urc

es o

f fo

rmal

sec

tor

emp

loym

ent

Sources of formal sector employment

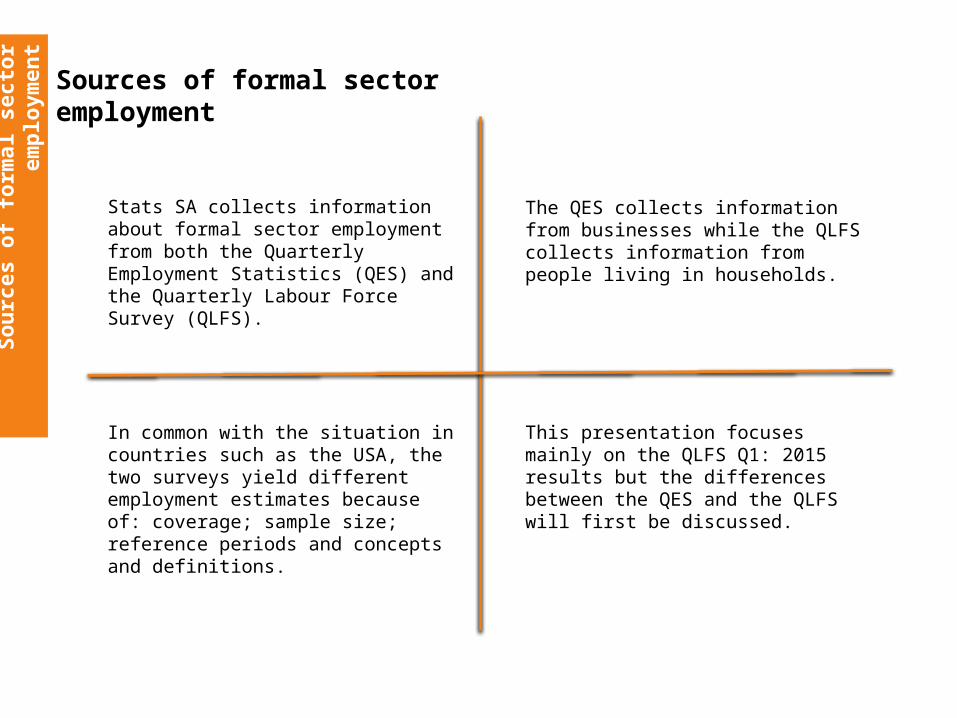

Stats SA collects information about formal sector employment from both the Quarterly Employment Statistics (QES) and the Quarterly Labour Force Survey (QLFS).

The QES collects information from businesses while the QLFS collects information from people living in households.

In common with the situation in countries such as the USA, the two surveys yield different employment estimates because of: coverage; sample size; reference periods and concepts and definitions.

This presentation focuses mainly on the QLFS Q1: 2015 results but the differences between the QES and the QLFS will first be discussed.

So

urc

es o

f fo

rmal

sec

tor

emp

loym

ent

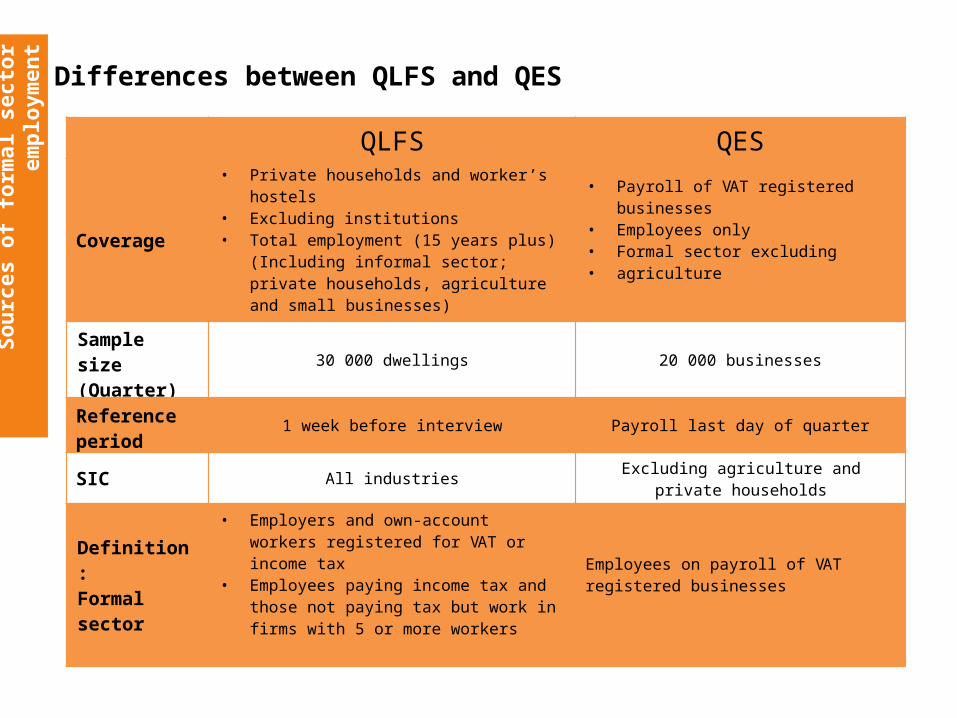

Differences between QLFS and QESQLFS QES

QLFS QES

Coverage

• Private households and worker’s hostels• Excluding institutions• Total employment (15 years plus) (Including

informal sector; private households, agriculture and small businesses)

• Payroll of VAT registered businesses• Employees only• Formal sector excluding • agriculture

Sample size(Quarter)

30 000 dwellings 20 000 businesses

Reference period

1 week before interview Payroll last day of quarter

SIC All industriesExcluding agriculture and private

households

Definition:Formal sector

• Employers and own-account workers registered for VAT or income tax

• Employees paying income tax and those not paying tax but work in firms with 5 or more workers

Employees on payroll of VAT registered businesses

So

urc

es o

f fo

rmal

sec

tor

emp

loym

ent

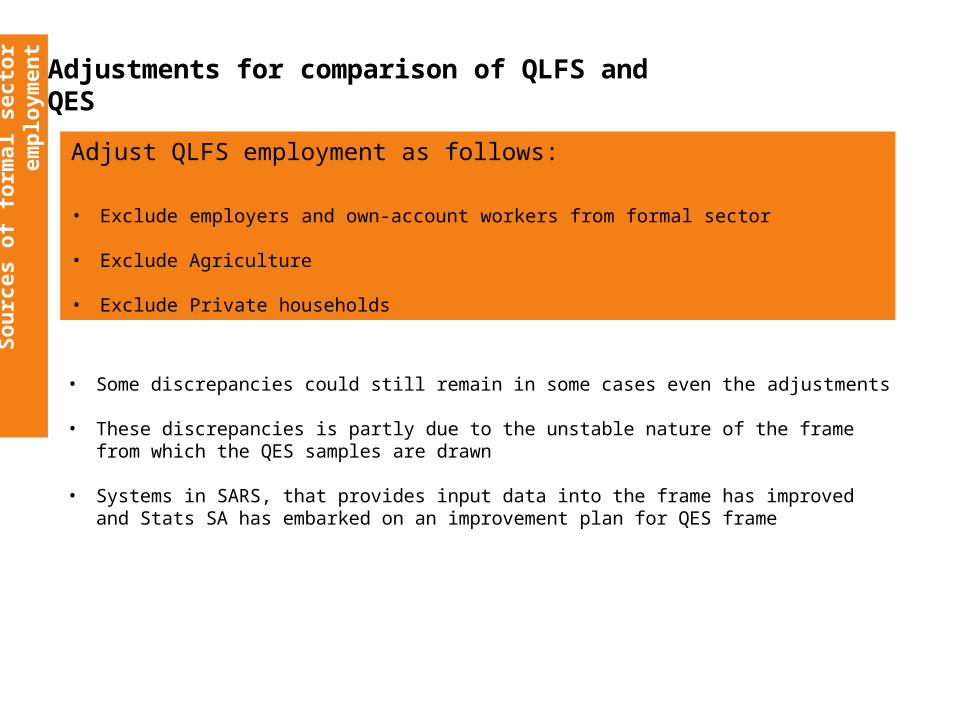

Adjustments for comparison of QLFS and QES

• Some discrepancies could still remain in some cases even the adjustments

• These discrepancies is partly due to the unstable nature of the frame from which the QES samples are drawn

• Systems in SARS, that provides input data into the frame has improved and Stats SA has embarked on an improvement plan for QES frame

Adjust QLFS employment as follows:

• Exclude employers and own-account workers from formal sector

• Exclude Agriculture

• Exclude Private households

So

urc

es o

f fo

rmal

sec

tor

emp

loym

ent

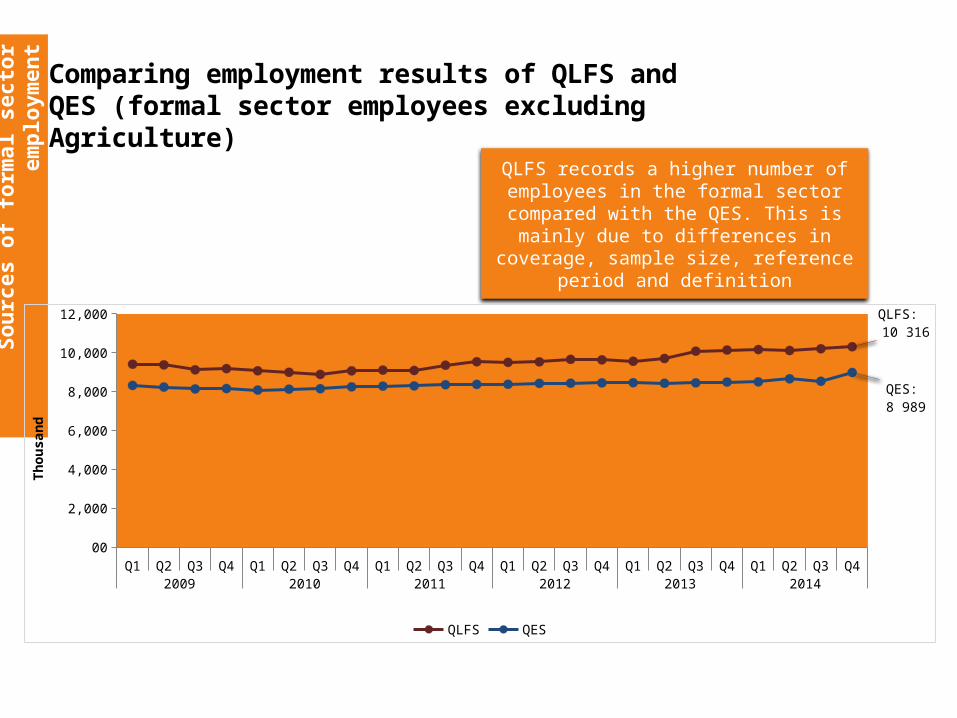

Comparing employment results of QLFS and QES (formal sector employees excluding Agriculture)

QLFS records a higher number of employees in the formal sector compared

with the QES. This is mainly due to differences in coverage, sample size,

reference period and definition

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42009 2010 2011 2012 2013 2014

00

2,000

4,000

6,000

8,000

10,000

12,000 QLFS: 10 316

QES: 8 989

QLFS QES

Th

ou

san

d

Fo

rmal

& In

form

al s

ecto

r em

plo

ymen

t

Based on QLFS results

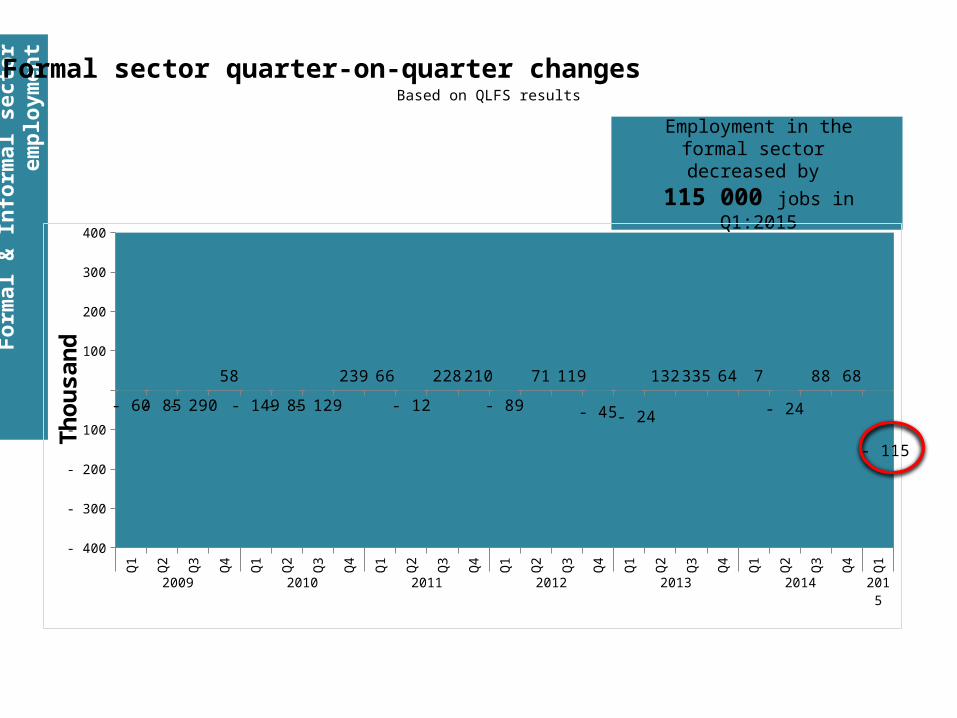

Formal sector quarter-on-quarter changes

Employment in the formal sector decreased by

115 000 jobs in Q1:2015

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q12009 2010 2011 2012 2013 2014 2015

- 400

- 300

- 200

- 100

100

200

300

400

- 60 - 85- 290

58

- 149- 85- 129

239 66

- 12

228 210

- 89

71 119

- 45 - 24

132 335 64 7

- 24

88 68

- 115Th

ou

san

d

Fo

rmal

& In

form

al s

ecto

r em

plo

ymen

t

Based on QLFS results

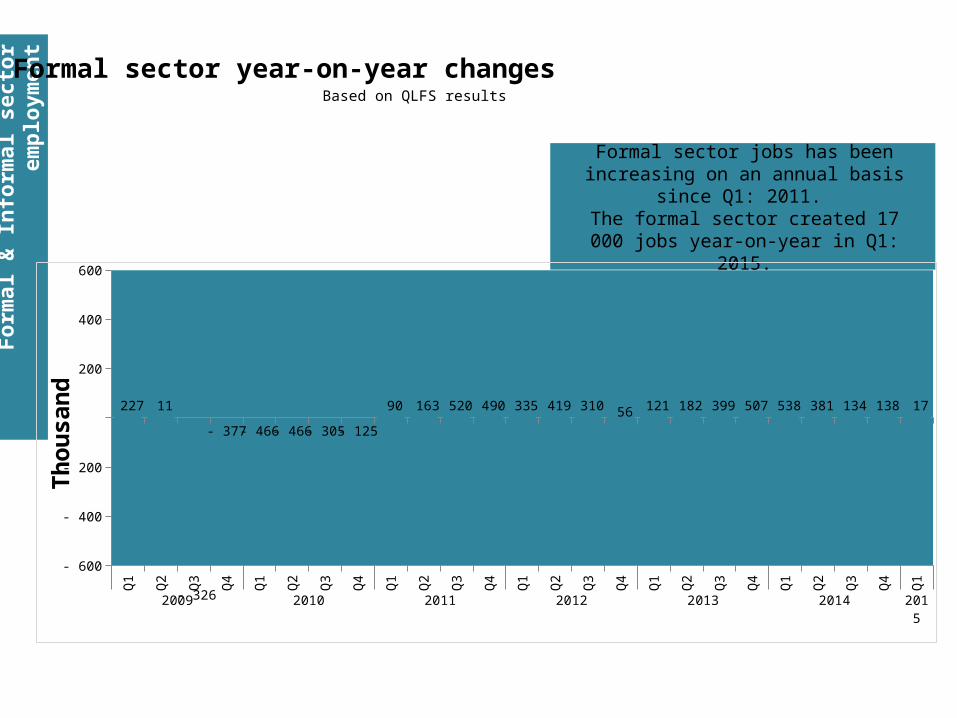

Formal sector year-on-year changes

Formal sector jobs has been increasing on an annual basis since Q1: 2011.

The formal sector created 17 000 jobs year-on-year in Q1: 2015.

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q12009 2010 2011 2012 2013 2014 2015

- 600

- 400

- 200

200

400

600

227 11

- 326

- 377 - 466 - 466 - 305 - 125

90 163 520 490 335 419 310 56 121 182 399 507 538 381 134 138 17

Th

ou

san

d

Fo

rmal

& In

form

al s

ecto

r em

plo

ymen

t

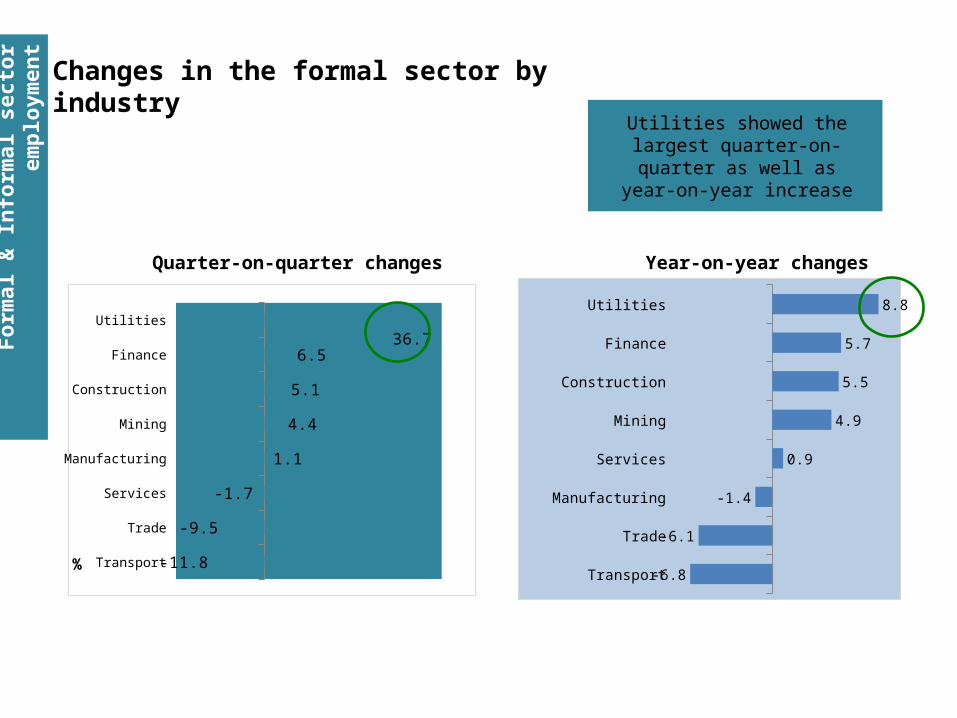

Changes in the formal sector by industry

Utilities showed the largest quarter-on-quarter as well as

year-on-year increase

Quarter-on-quarter changes Year-on-year changes

Transport

Trade

Services

Manufacturing

Mining

Construction

Finance

Utilities

-11.8

-9.5

-1.7

1.1

4.4

5.1

6.536.7

% Transport

Trade

Manufacturing

Services

Mining

Construction

Finance

Utilities

-6.8

-6.1

-1.4

0.9

4.9

5.5

5.7

8.8

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q12009 2010 2011 2012 2013 2014 2015

- 150

- 100

- 50

50

100

150

200

- 81 - 41- 135

142

- 101

144

- 15

40

- 40

30

- 43 - 32

- 20

- 4

118 24

- 17

26

- 37

123

- 110

43 28 41 35

Th

ou

san

d

Fo

rmal

& In

form

al s

ecto

r em

plo

ymen

t

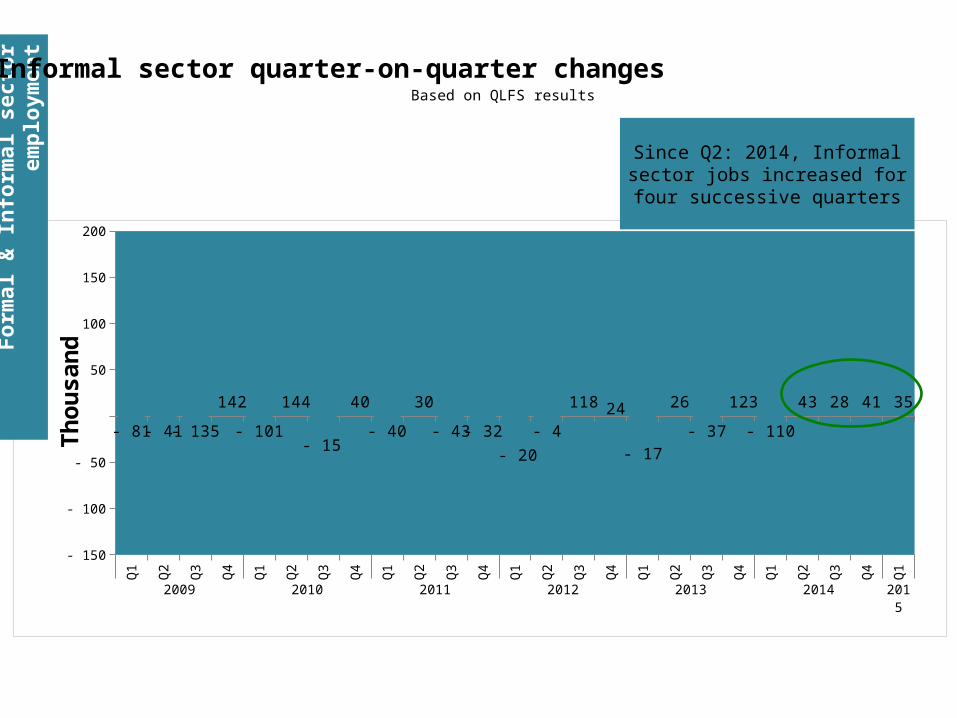

Based on QLFS results

Informal sector quarter-on-quarter changes

Since Q2: 2014, Informal sector jobs increased for four successive

quarters

Fo

rmal

& In

form

al s

ecto

r em

plo

ymen

t

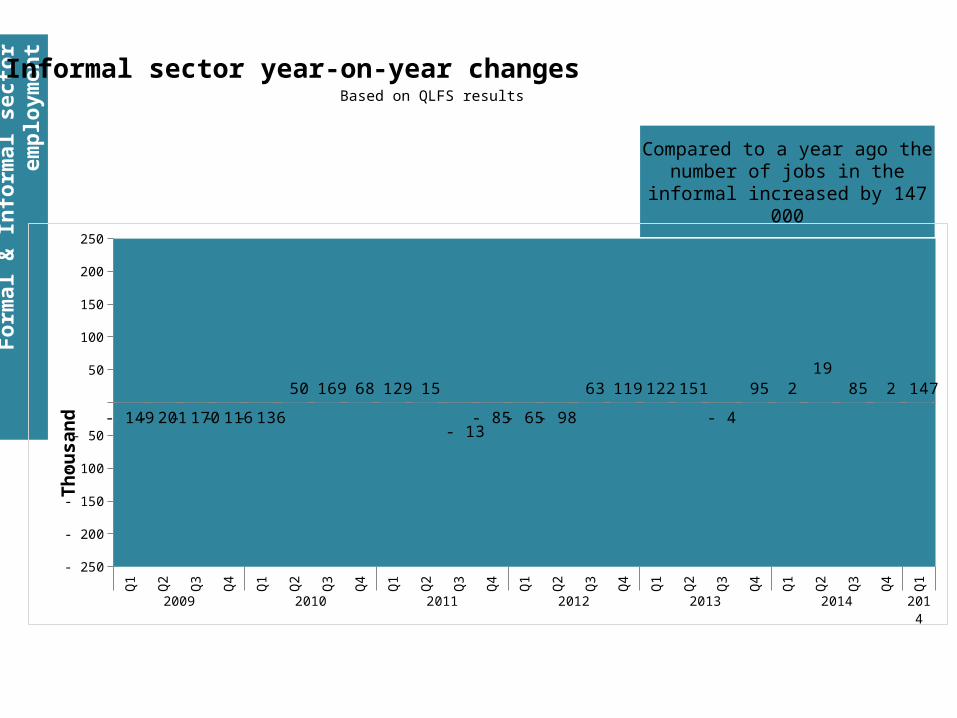

Based on QLFS results

Informal sector year-on-year changes

Compared to a year ago the number of jobs in the informal

increased by 147 000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q12009 2010 2011 2012 2013 2014 2014

- 250

- 200

- 150

- 100

- 50

50

100

150

200

250

- 149- 201- 170- 116- 136

50 169 68 129 15

- 13- 85 - 65 - 98

63 119 122 151

- 4

95 2 19

85 2 147

Th

ou

sa

nd

Fo

rmal

& In

form

al s

ecto

r em

plo

ymen

t

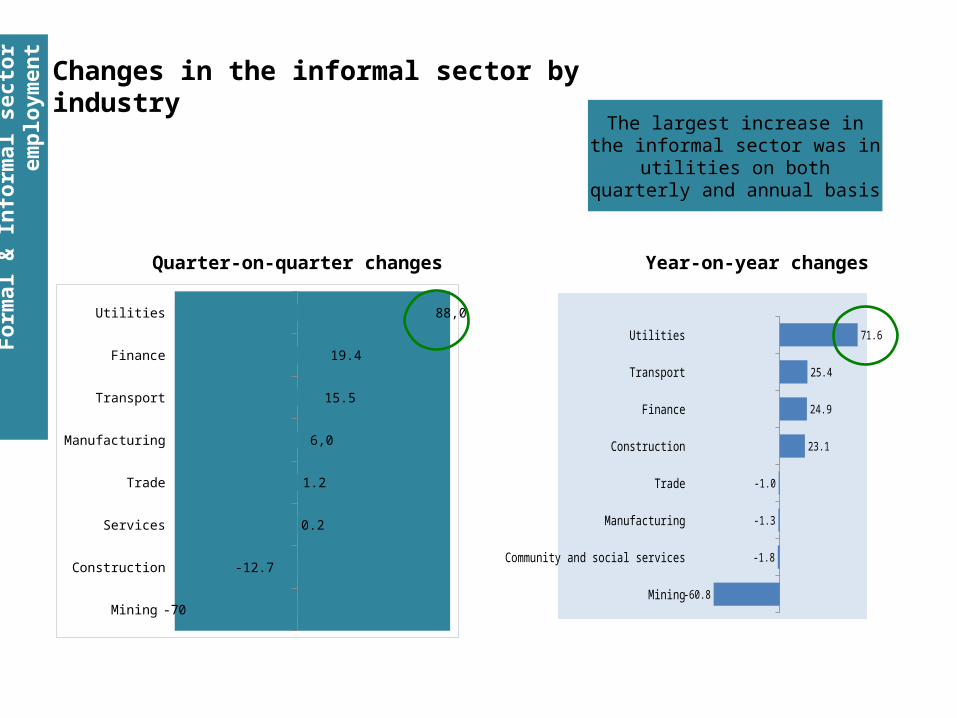

The largest increase in the informal sector was in utilities on both quarterly and annual basis

Quarter-on-quarter changes Year-on-year changes

Changes in the informal sector by industry

Mining

Construction

Services

Trade

Manufacturing

Transport

Finance

Utilities

-70

-12.7

0.2

1.2

6,0

15.5

19.4

88,0

Mining

Community and social services

Manufacturing

Trade

Construction

Finance

Transport

Utilities

-60.8

-1.8

-1.3

-1.0

23.1

24.9

25.4

71.6

Un

emp

loym

ent

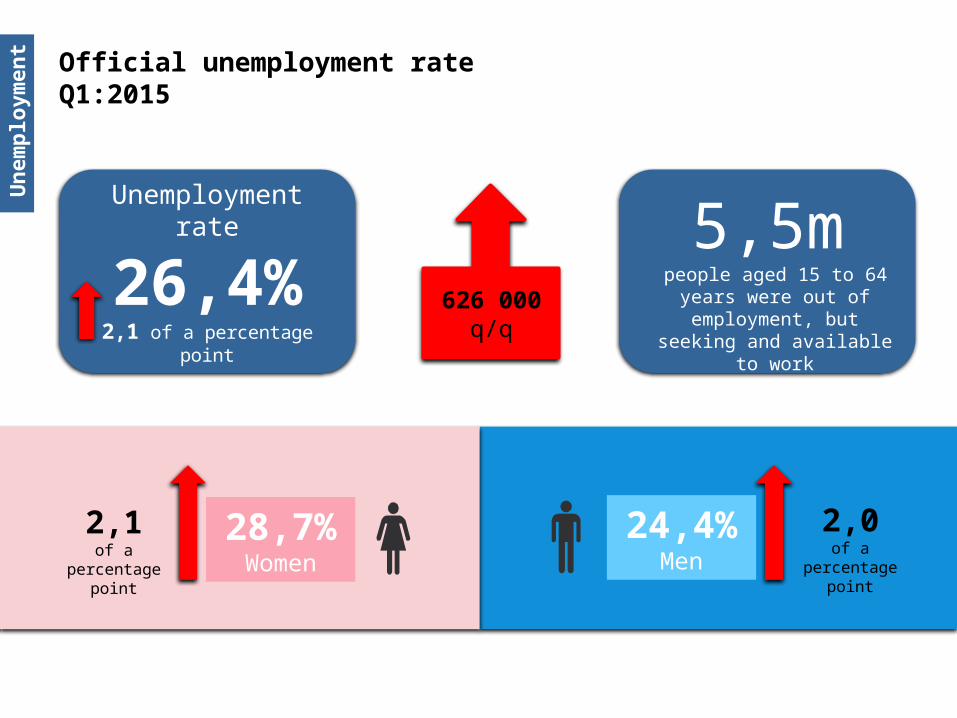

Official unemployment rate Q1:2015

28,7%Women

2,1of a percentage

point

24,4%Men

2,0of a percentage

point

Unemployment rate

26,4%2,1 of a percentage point

626 000q/q

5,5mpeople aged 15 to 64

years were out of employment, but seeking

and available to work

Un

emp

loym

ent

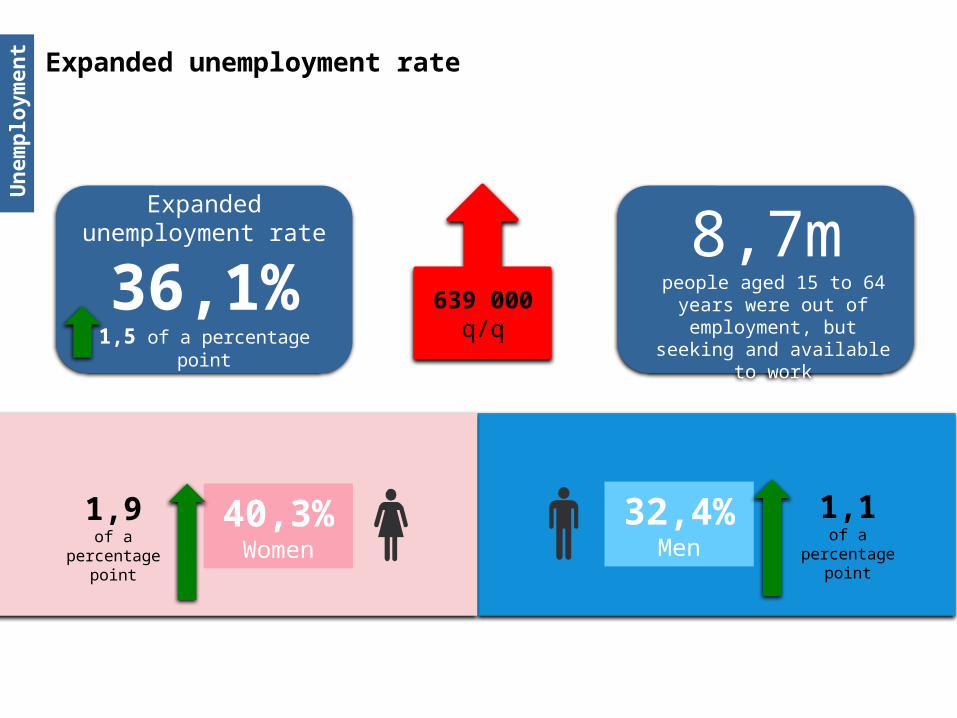

Expanded unemployment rate

40,3%Women

1,9of a percentage

point

32,4%Men

1,1of a percentage

point

639 000q/q

Expanded unemployment rate

36,1%1,5 of a percentage point

8,7mpeople aged 15 to 64

years were out of employment, but seeking

and available to work

Un

emp

loym

ent

2008 2009 2010 2011 2012 2013 2014 20150.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

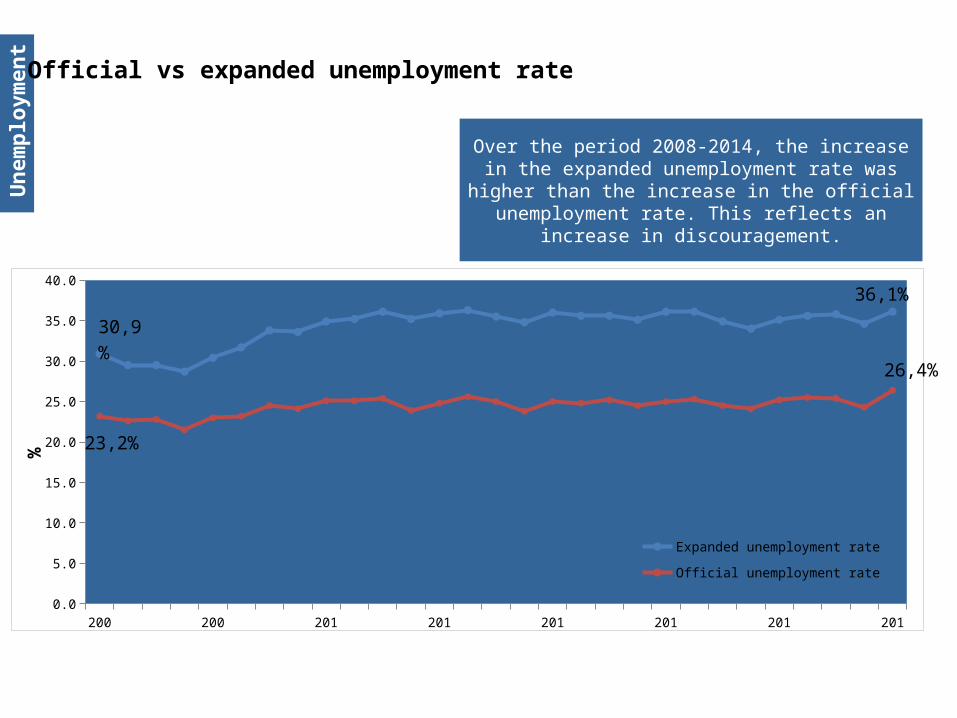

23,2%

26,4%

Expanded unemployment rate

Official unemployment rate

%

30,9%

36,1%

Over the period 2008-2014, the increase in the expanded unemployment rate was higher than the

increase in the official unemployment rate. This reflects an increase in discouragement.

Official vs expanded unemployment rate

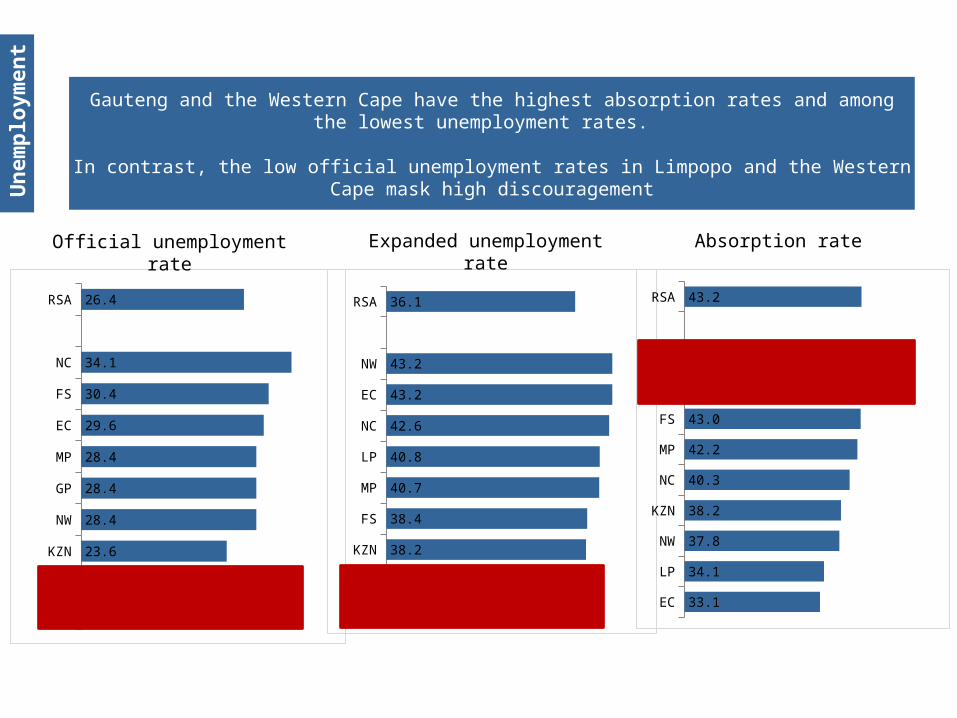

LP

WC

KZN

NW

GP

MP

EC

FS

NC

RSA

20.1

21.0

23.6

28.4

28.4

28.4

29.6

30.4

34.1

26.4

WC

GP

KZN

FS

MP

LP

NC

EC

NW

RSA

23.3

32.8

38.2

38.4

40.7

40.8

42.6

43.2

43.2

36.1

EC

LP

NW

KZN

NC

MP

FS

GP

WC

RSA

33.1

34.1

37.8

38.2

40.3

42.2

43.0

51.9

53.2

43.2

Un

emp

loym

ent

Gauteng and the Western Cape have the highest absorption rates and among the lowest unemployment rates.

In contrast, the low official unemployment rates in Limpopo and the Western Cape mask high discouragement

Expanded unemployment rate Absorption rateOfficial unemployment rate

Inactivity

Definition of inactivity

Those who do not meet the criteria of employment and unemployment are classified as the not economically active population

Inac

tivi

ty

Discouraged job-seekers

Other not economically inactive

Inactive population

Wanted to work and available to work but did not search for job due to:1. No jobs available in area.2. Unable to find for skills.3. Lost hope of finding a job.

Wanted to work but not available due to reasons such as:• Retired• Scholar/student• Housewife.• Too old/young to

work

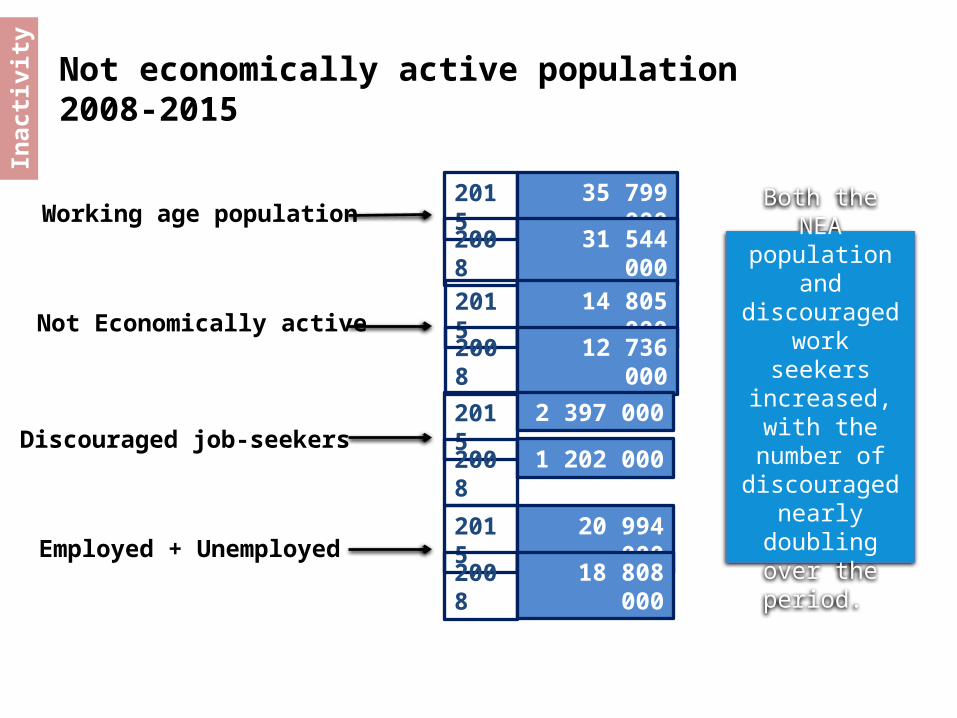

Not economically active population 2008-2015

Inac

tivi

ty

Working age population2015

Discouraged job-seekers

Employed + Unemployed

35 799 000

2008 31 544 000

Not Economically active2015 14 805 000

2008 12 736 000

2015 2 397 000

2008 1 202 000

2015 20 994 000

2008 18 808 000

Both the NEA population and discouraged work seekers

increased, with the number of discouraged

nearly doubling over the period.

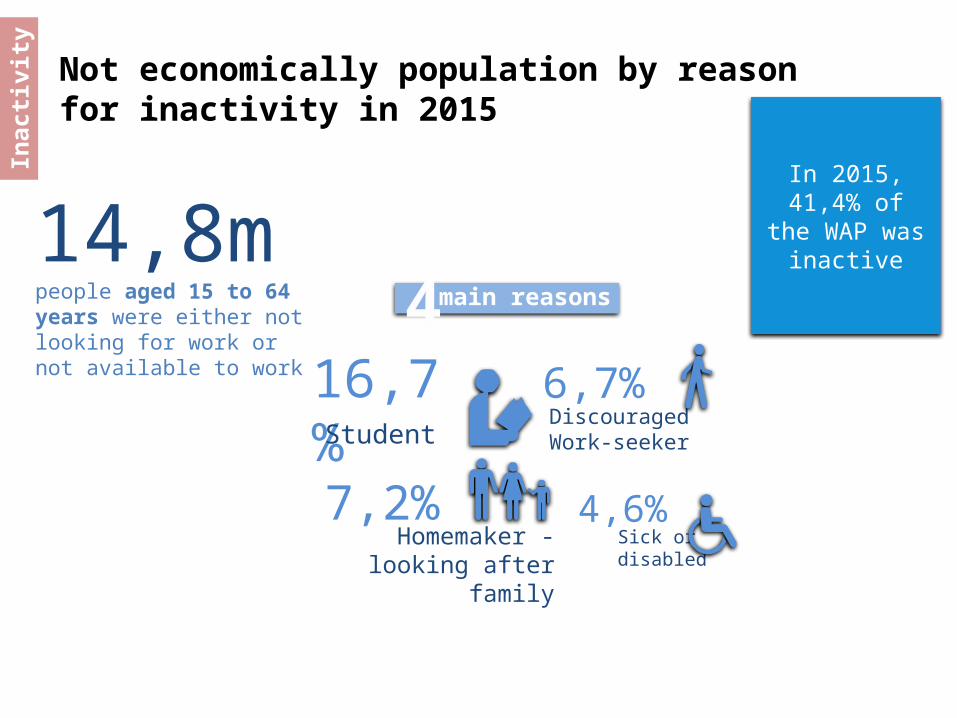

Not economically population by reason for inactivity in 2015

Inac

tivi

ty

In 2015, 41,4% of the WAP was

inactive

main reasons4

Homemaker - looking after family

16,7%7,2%

Sick or disabled

4,6%

DiscouragedWork-seeker

6,7%Student

14,8mpeople aged 15 to 64 years were either not looking for work or not available to work

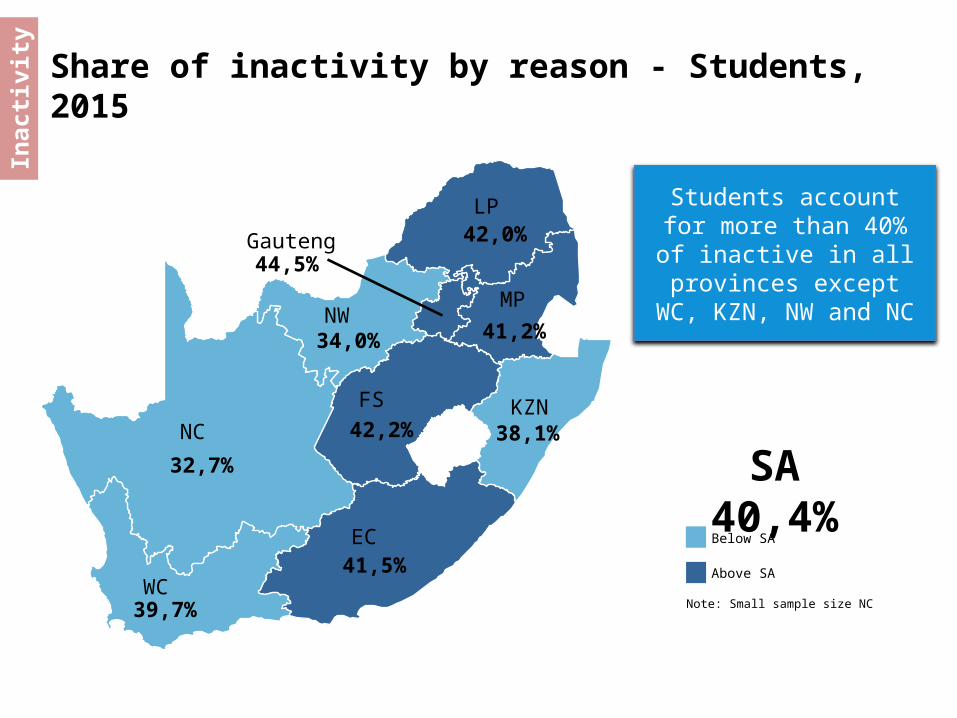

Share of inactivity by reason - Students, 2015

Students account for more than 40% of inactive in all

provinces except WC, KZN, NW and NC

Gauteng44,5%

EC41,5%

KZN38,1%

WC39,7%

FS

42,2%

NW34,0%

LP42,0%

41,2%

MP

NC

32,7% SA 40,4%

Note: Small sample size NC

Below SA

Above SA

Inac

tivi

ty

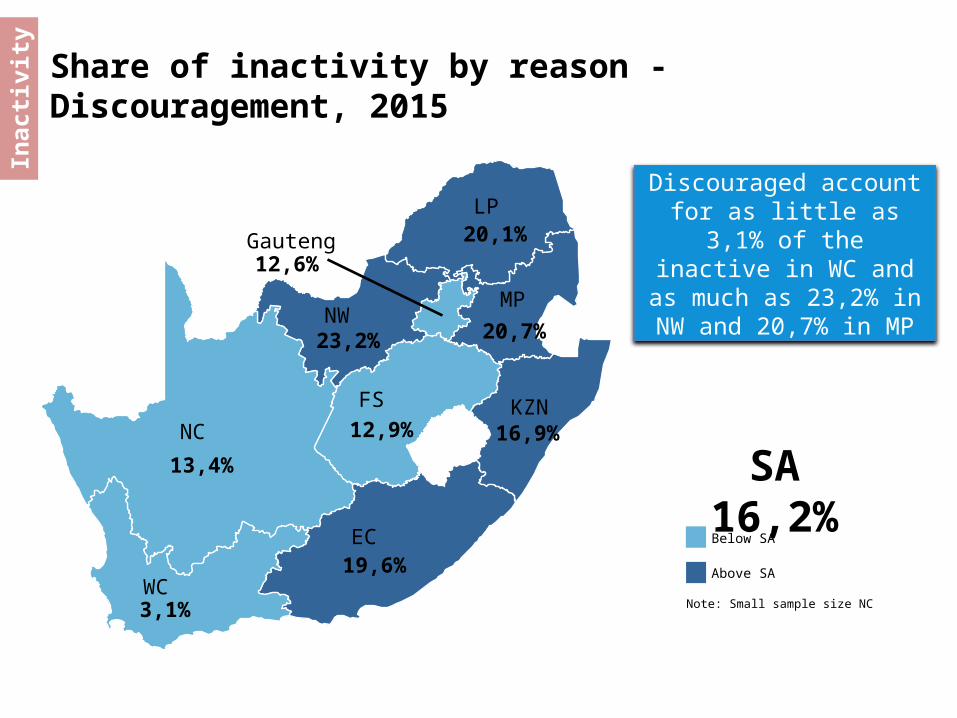

Share of inactivity by reason - Discouragement, 2015

Discouraged account for as little as 3,1% of the inactive in WC and as

much as 23,2% in NW and 20,7% in MP

Gauteng12,6%

EC19,6%

KZN16,9%

WC3,1%

FS

12,9%

NW23,2%

LP20,1%

20,7%

MP

NC

13,4% SA 16,2%

Note: Small sample size NC

Below SA

Above SA

Inac

tivi

ty

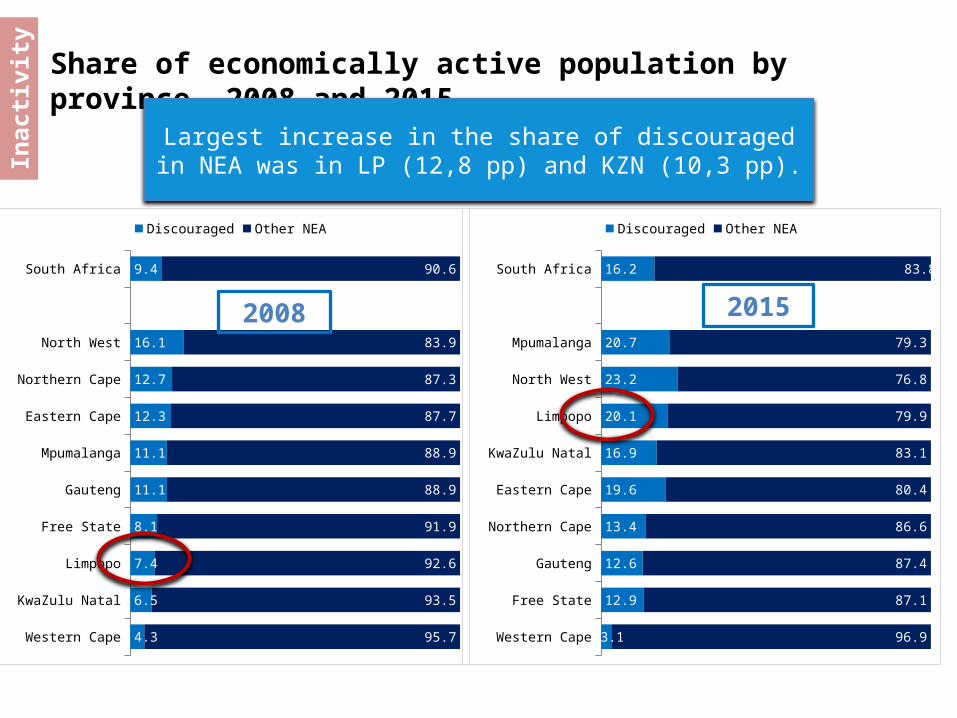

Share of economically active population by province, 2008 and 2015

Largest increase in the share of discouraged in NEA was in LP (12,8 pp) and KZN (10,3 pp).

Inac

tivi

ty

Western Cape

KwaZulu Natal

Limpopo

Free State

Gauteng

Mpumalanga

Eastern Cape

Northern Cape

North West

South Africa

4.3

6.5

7.4

8.1

11.1

11.1

12.3

12.7

16.1

9.4

95.7

93.5

92.6

91.9

88.9

88.9

87.7

87.3

83.9

90.6

Discouraged Other NEA

2008 2015

Western Cape

Free State

Gauteng

Northern Cape

Eastern Cape

KwaZulu Natal

Limpopo

North West

Mpumalanga

South Africa

3.1

12.9

12.6

13.4

19.6

16.9

20.1

23.2

20.7

16.2

96.9

87.1

87.4

86.6

80.4

83.1

79.9

76.8

79.3

83.8

Discouraged Other NEA

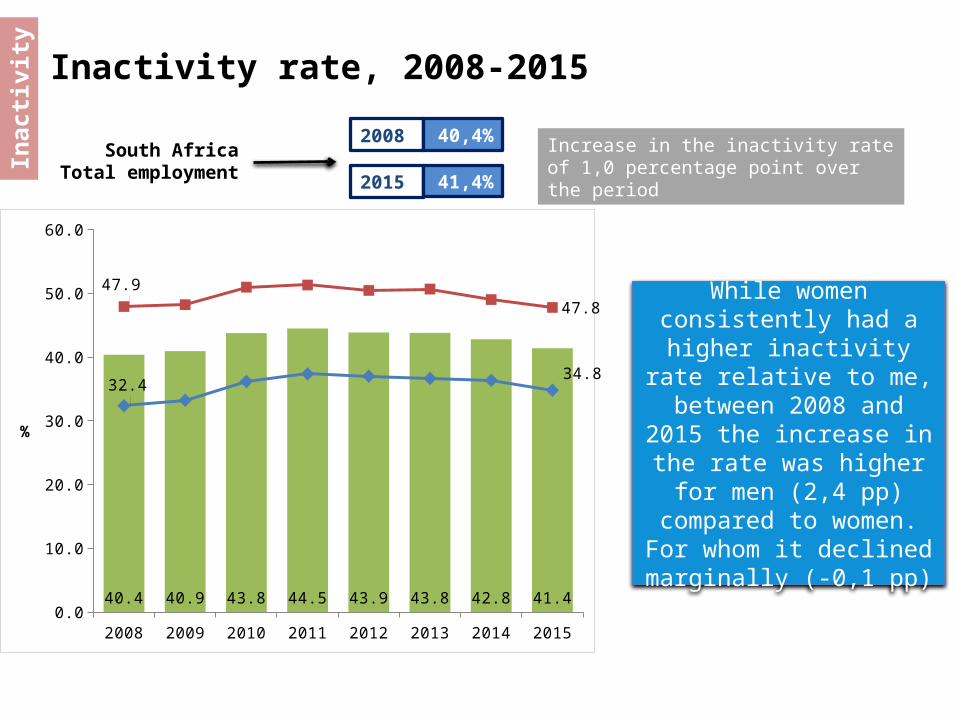

Inactivity rate, 2008-2015

Inac

tivi

ty

2008 40,4%

2015 41,4%

South Africa Total employment

Increase in the inactivity rate of 1,0 percentage point over the period

While women consistently had a higher inactivity rate

relative to me, between 2008 and 2015 the

increase in the rate was higher for men (2,4 pp)

compared to women. For whom it declined marginally

(-0,1 pp)

2008 2009 2010 2011 2012 2013 2014 20150.0

10.0

20.0

30.0

40.0

50.0

60.0

40.4 40.9 43.8 44.5 43.9 43.8 42.8 41.4

32.434.8

47.9

47.8

%

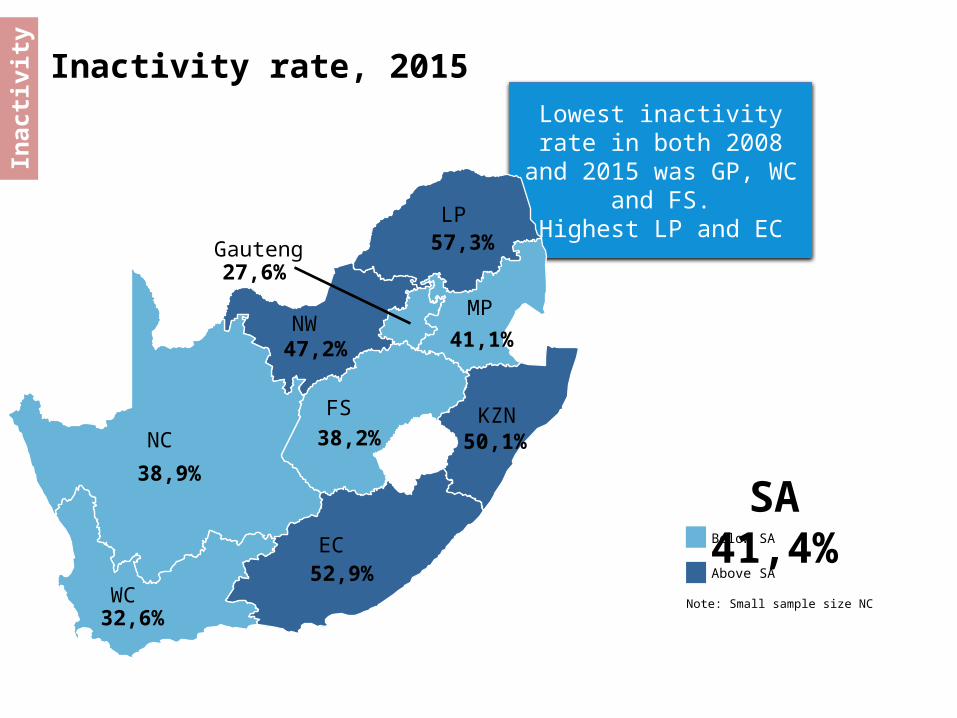

Inactivity rate, 2015

Lowest inactivity rate in both 2008 and 2015 was

GP, WC and FS.Highest LP and EC

Gauteng27,6%

EC52,9%

KZN50,1%

WC32,6%

FS

38,2%

NW47,2%

LP57,3%

41,1%

MP

NC

38,9%

SA 41,4%

Note: Small sample size NC

Below SA

Above SA

Inac

tivi

ty

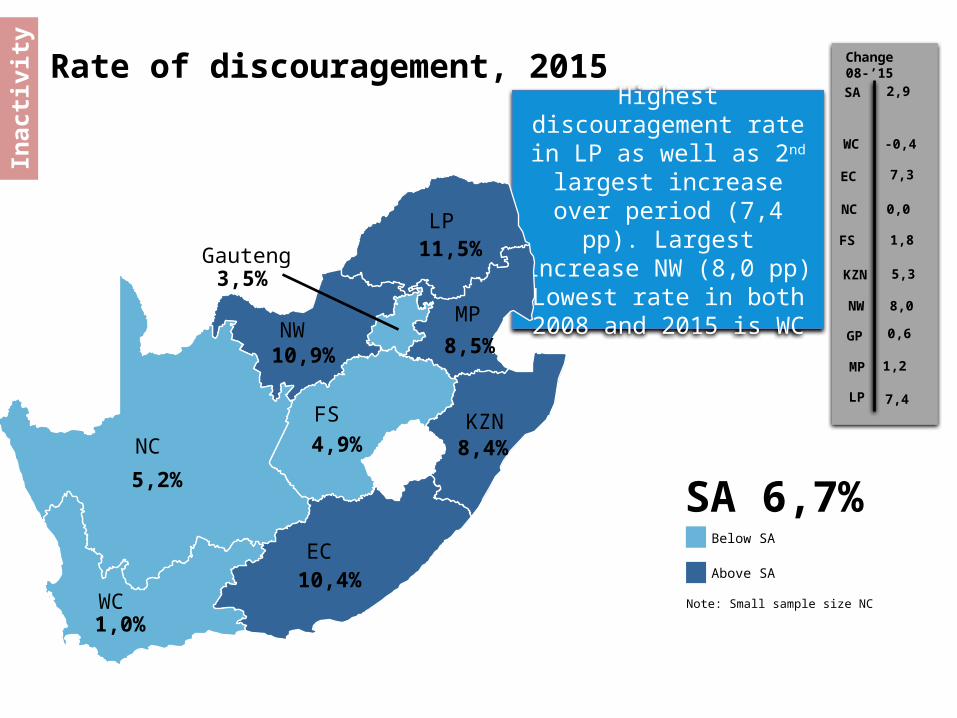

Rate of discouragement, 2015

Highest discouragement rate in LP as well as 2nd

largest increase over period (7,4 pp). Largest increase NW (8,0 pp)

Lowest rate in both 2008 and 2015 is WC

Gauteng3,5%

EC10,4%

KZN8,4%

WC1,0%

FS

4,9%

NW10,9%

LP11,5%

8,5%

MP

NC

5,2%SA 6,7%

Note: Small sample size NC

Below SA

Above SA

Inac

tivi

ty Change 08-’15

2,9

-0,4

7,3

0,0

1,8

5,3

8,0

0,6

1,2

7,4

SA

WC

EC

NC

FS

KZN

NW

GP

MP

LP

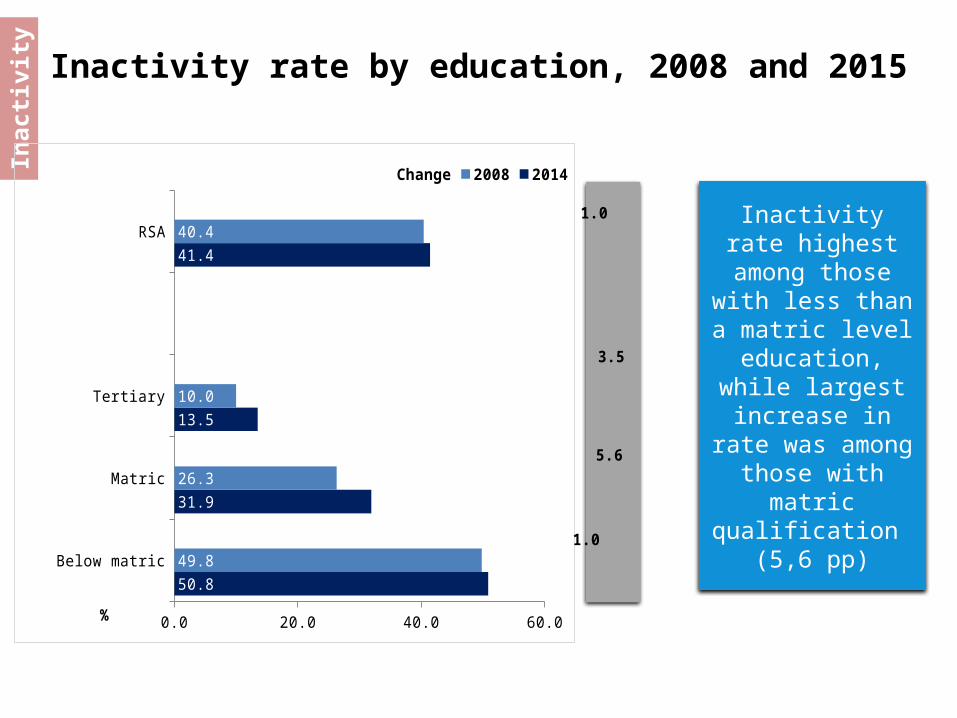

Inactivity rate by education, 2008 and 2015

Inac

tivi

ty

Inactivity rate highest among those with less

than a matric level education, while

largest increase in rate was among those with matric qualification (5,6

pp)

Below matric

Matric

Tertiary

RSA

0.0 20.0 40.0 60.0

50.8

31.9

13.5

41.4

49.8

26.3

10.0

40.4

1.0

5.6

3.5

1.0

Change 2008 2014

%

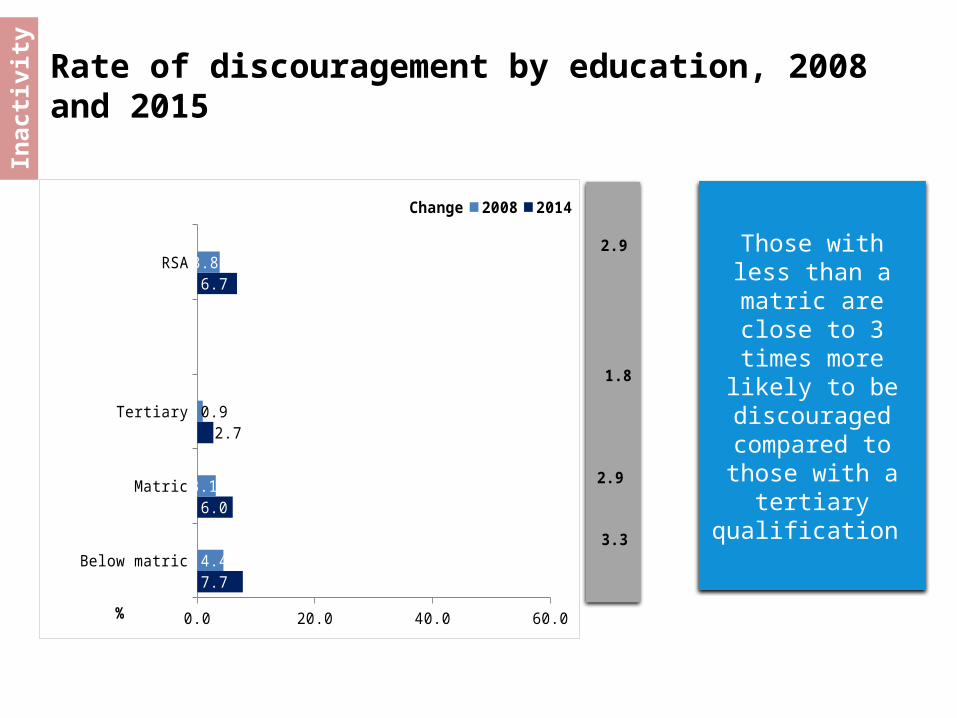

Rate of discouragement by education, 2008 and 2015

Inac

tivi

ty

Those with less than a matric are close to 3 times more likely to be

discouraged compared to those

with a tertiary qualification

Below matric

Matric

Tertiary

RSA

0.0 20.0 40.0 60.0

7.7

6.0

2.7

6.7

4.4

3.1

0.9

3.8

3.3

2.9

1.8

2.9

Change 2008 2014

%

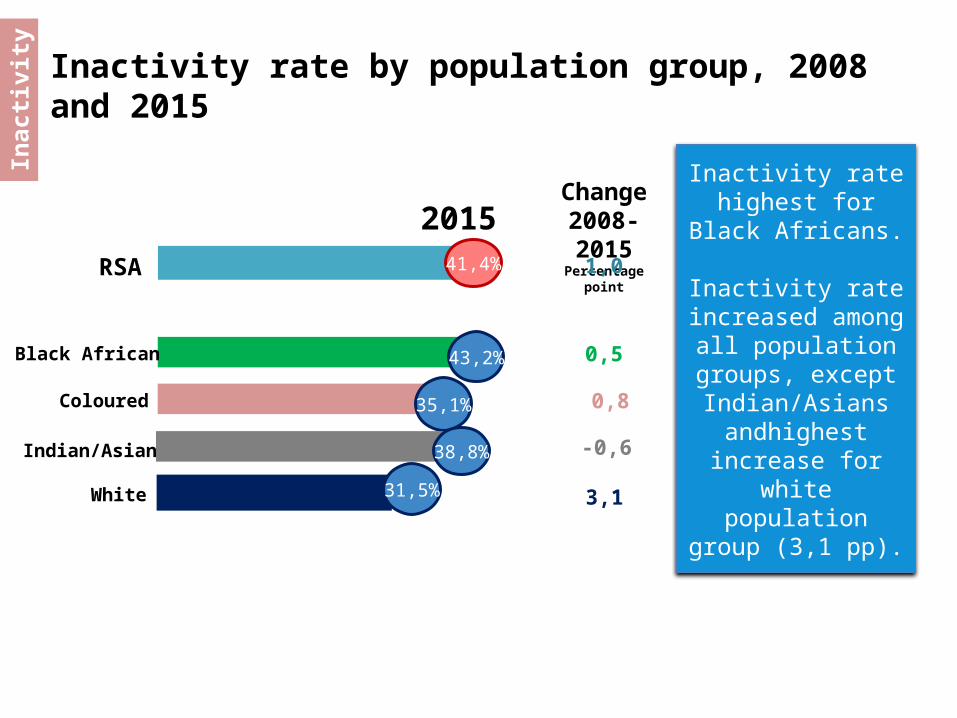

Inactivity rate by population group, 2008 and 2015

Inac

tivi

ty

Inactivity rate highest for Black

Africans.

Inactivity rate increased among all population groups,

except Indian/Asians andhighest increase for white population

group (3,1 pp).

2015

RSA

Coloured

41,4%

43,2%

35,1%

Black African

Indian/Asian 38,8%

White 31,5%

Change 2008-2015Percentage point

1,0

0,5

0,8

-0,6

3,1

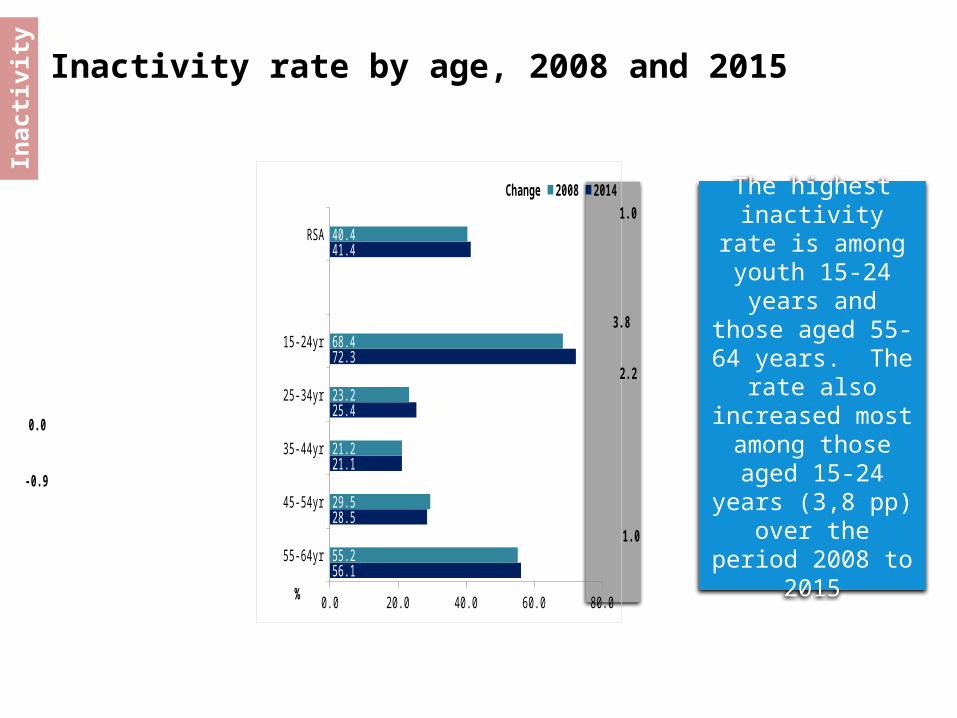

Inactivity rate by age, 2008 and 2015

Inac

tivi

ty

The highest inactivity rate is

among youth 15-24 years and those

aged 55-64 years. The rate also

increased most among those aged 15-24 years (3,8

pp) over the period 2008 to 2015

55-64yr

45-54yr

35-44yr

25-34yr

15-24yr

RSA

0.0 20.0 40.0 60.0 80.0

56.1

28.5

21.1

25.4

72.3

41.4

55.2

29.5

21.2

23.2

68.4

40.4

1.0

-0.9

0.0

2.2

3.8

1.0Change 2008 2014

%

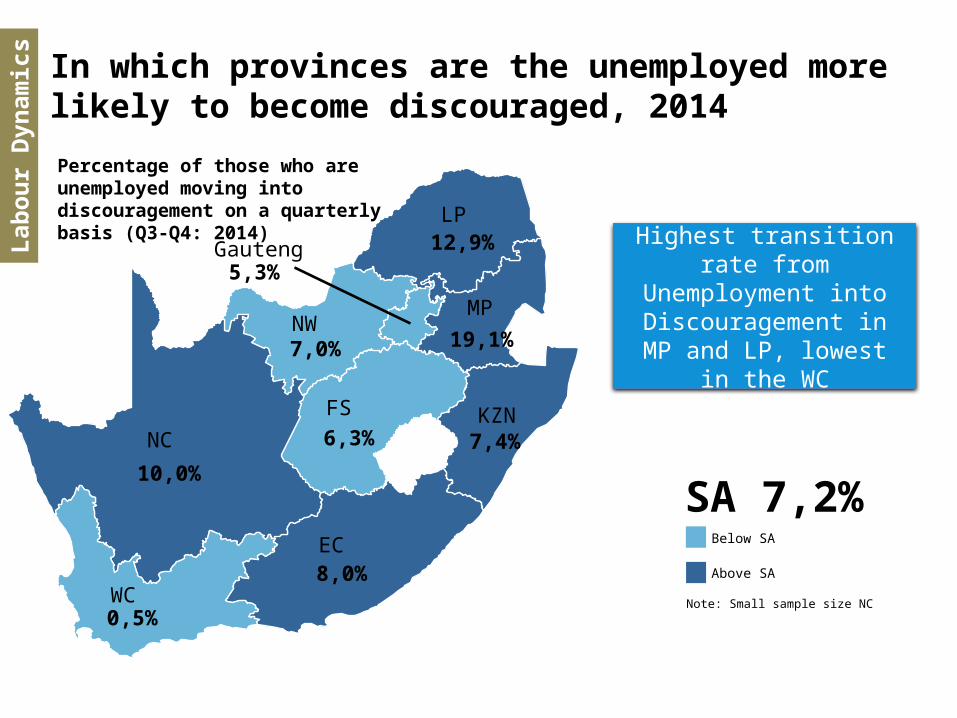

In which provinces are the unemployed more likely to become discouraged, 2014

Highest transition rate from Unemployment into Discouragement in MP

and LP, lowest in the WC

Gauteng5,3%

EC8,0%

KZN7,4%

WC0,5%

FS

6,3%

NW7,0%

LP12,9%

19,1%

MP

NC

10,0%

SA 7,2%

Note: Small sample size NC

Below SA

Above SA

Percentage of those who are unemployed moving into discouragement on a quarterly basis (Q3-Q4: 2014)

Lab

ou

r D

ynam

ics

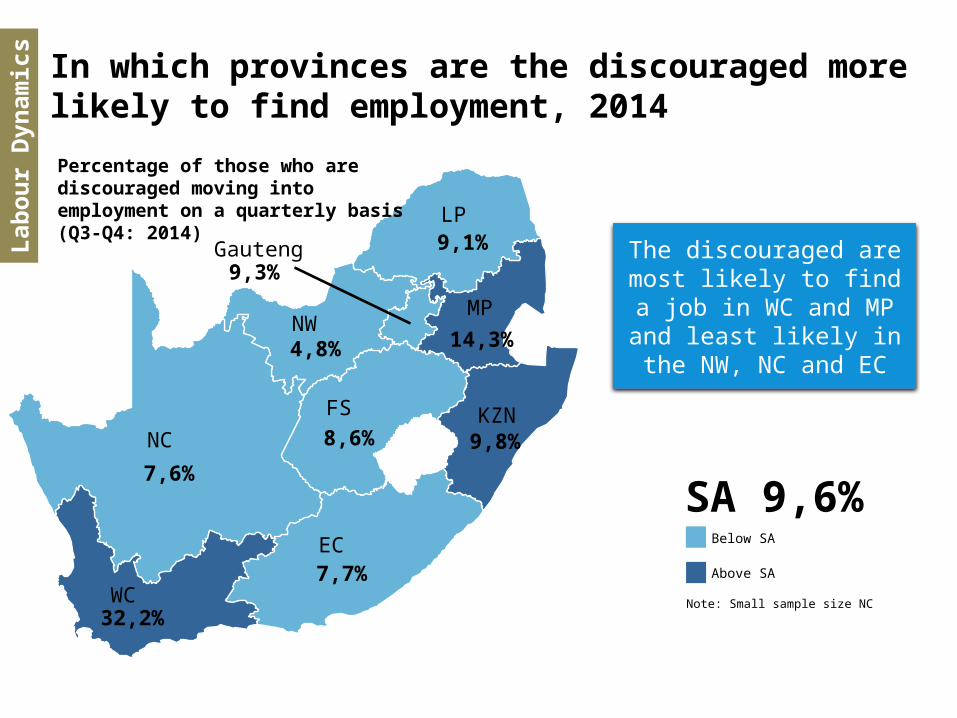

In which provinces are the discouraged more likely to find employment, 2014

The discouraged are most likely to find a job in WC

and MP and least likely in the NW, NC and EC

Gauteng9,3%

EC7,7%

KZN9,8%

WC32,2%

FS

8,6%

NW4,8%

LP9,1%

14,3%

MP

NC

7,6%

SA 9,6%

Note: Small sample size NC

Below SA

Above SA

Percentage of those who are discouraged moving into employment on a quarterly basis (Q3-Q4: 2014)

Lab

ou

r D

ynam

ics

Q1:

2015

QL

FS

Hig

hli

gh

ts

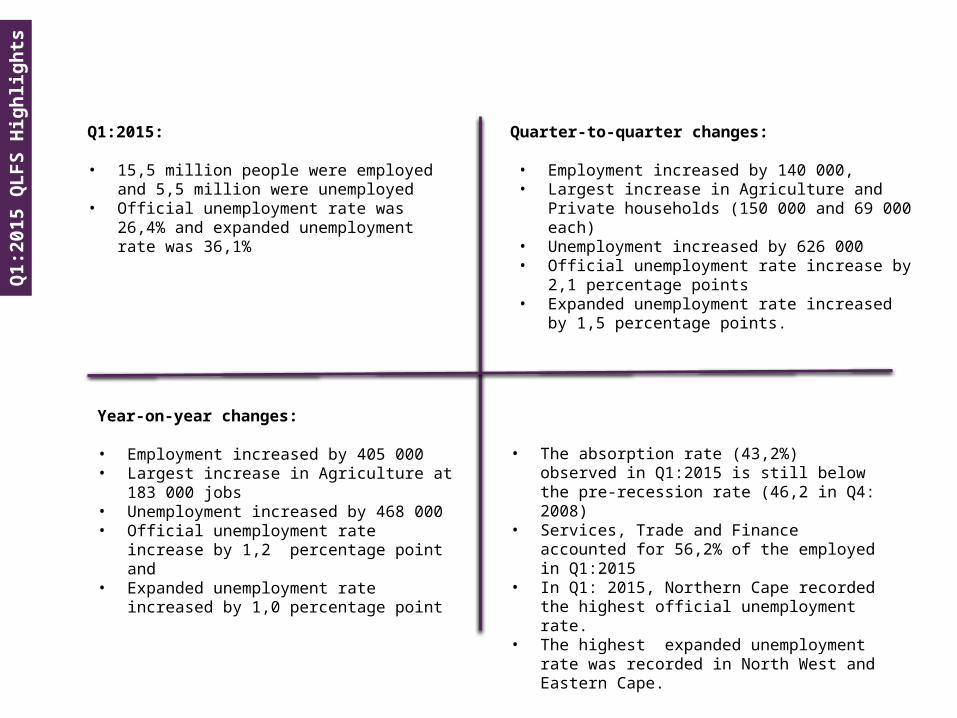

Q1:2015:

• 15,5 million people were employed and 5,5 million were unemployed

• Official unemployment rate was 26,4% and expanded unemployment rate was 36,1%

Quarter-to-quarter changes:

• Employment increased by 140 000,• Largest increase in Agriculture and Private

households (150 000 and 69 000 each)• Unemployment increased by 626 000• Official unemployment rate increase by 2,1

percentage points • Expanded unemployment rate increased by 1,5

percentage points.

Year-on-year changes:

• Employment increased by 405 000• Largest increase in Agriculture at 183 000 jobs• Unemployment increased by 468 000• Official unemployment rate increase by 1,2

percentage point and• Expanded unemployment rate increased by

1,0 percentage point

• The absorption rate (43,2%) observed in Q1:2015 is still below the pre-recession rate (46,2 in Q4: 2008)

• Services, Trade and Finance accounted for 56,2% of the employed in Q1:2015

• In Q1: 2015, Northern Cape recorded the highest official unemployment rate.

• The highest expanded unemployment rate was recorded in North West and Eastern Cape.