stanlib absolute return franchise...

TRANSCRIPT

STANLIB Absolute Return Franchise Brochure

01Our belief Our franchise model

02Overview The team Investment philosophy

03Investment process and portfolio construction

04Centralised research

05Investment risk management

06Broader risk management Environmental, social and governance factors Capabilities

07Products for individuals Products for institutions Contact details

08Appendices

Appendix 1: Investment Team collaboration

Appendix 2: Team profiles

STANLIBFocused Investing

1

Our beliefThere is no ‘one size fits all’ investment solution for clients. Diverse clients need diverse investment outcomes. We therefore look at investments through many lenses and from many angles to give us an in-depth understanding of an ever changing investment landscape. Our investment model thus houses multiple focused units with unique philosophies, which cater for diverse client needs.

Our franchise modelThe STANLIB investment team consists of franchises made up of specialist teams of investment professionals. They manage clients’ assets in their area of expertise, namely: fixed interest, property, equities, multi-asset allocation, multi-management and alternatives.

These specialist investment teams handle market changes with agility and speed, as they are supported by dedicated research, trade, implementation, risk management and compliance teams.

Our multi-specialist franchise model truly reflects the complex investment world we operate in and echoes our desire to deliver tailored solutions for diverse clients. The result is a broad investment offering designed to deliver our investment promise to clients.

STANLIB is a leading asset management company in Africa, with assets under management and administration of R551 billion* for over 400 000 retail and institutional clients across the African continent. We have a physical presence in ten African countries and are able to leverage from a wider Standard Bank Group Africa footprint.

STANLIB – Focused Investing

The power of focus and the strength of diversity

STANLIB - built to meet the ever-evolving needs of our clients

*As at December 2014

2

OverviewThe STANLIB Absolute Return team aims to achieve consistent performance with low variation in returns through all business cycles. We focus on capital protection and preservation, and in our aim to achieve these two objectives, we rely on asset class diversification (traditional and alternative asset classes), security selection and dedicated risk management.

The teamThe Absolute Return Franchise is headed by Eben Maré and Marius Oberholzer who have in excess of 30 years combined industry experience, while analyst Bhekinkosi Khuzwayo has more than six years industry experience and they leverage off each other’s skills to ensure consistent performance.

Eben Maré Marius OberholzerCo-Head of Absolute Return FranchisePhD, MSc, BSc (Hons)

Co-Head of Absolute Return FranchiseMSc, BCom

Bhekinkosi KhuzwayoAnalystBSc (Hons)

Investment philosophyOur absolute return philosophy is to manage portfolios consisting of the widest possible array of global and domestic asset classes that exhibit low or negative correlations to each other, so as to achieve the target performance and risk control objectives.

Our views on financial markets can be summed up in three key points:

Љ We believe that markets are reasonably, but not perfectly, efficient due to behavioural biases. As a result, we believe that active management can exploit the instances when the markets are “wrong”

Љ We believe that over time, financial markets revert to their means. As result we employ the past as a “guide” to the future in portfolio construction and security selection

Љ We believe that diversification reduces portfolio risk. However, we recognise that diversification has its limitations in addressing tail risks and so we complement it with bespoke protection in order to limit downside capture at the portfolio level

Our investment approach is simple. We believe that if we avoid / limit losses then we allow our clients the opportunity to compound returns on an increasingly higher capital base. Over time, this compounding allows us to deliver on our clients’ objectives. History has shown that by limiting fund losses during equity market downturns, we are able to compound fund returns to deliver comparable performance to the equity market post the recovery, but with substantially lower volatility and capital risk.

3

Investment process and portfolio constructionThe Absolute Return team uses a strategic asset allocation that has been back tested over many years to prove that it is capable of providing the required returns under even the most adverse economic and market conditions. The team may deviate from the strategic asset allocation in order to make prudent minor tactical changes as and when circumstances dictate that such deviation. This would however, be limited to 10% on either side of the strategic asset allocation for each of the major asset classes.

Ongoing investment interrogation

Asset allocation

Portfolio construction and security selection

Bespoke protection - derivatives

Risk measurement

Asset allocation

Our analysts use a ‘bootstrap’ methodology, with a wide range of asset class data to determine the optimal strategic allocation for our return objectives. The bootstrap methodology employs data going back to 1971 to determine the most appropriate asset allocation to meet the return objectives. This determines the long-term strategic asset allocation. Tactical asset allocation decisions are made after a thorough bottom-up analysis of the opportunities in the growth and defensive asset classes. We analyse historical and forecasted risk/return profiles to solve for optimal risk/return profiles where the optimal portfolio displays the best return for that given level of risk.

The asset allocation selected becomes our default, or market equilibrium position. We then allow tilts around this asset allocation to exploit market anomalies or valuation opportunities using Black Litterman and Ulf models.

Portfolio construction and security selection

Core to our portfolio construction process is the low risk strategic asset allocation model. The correlations and asset mix is such that portfolios are able to benefit positively in bull markets and limit the downside in bear markets.

Within each asset class, the lower risk assets are carefully selected based on quantitative and qualitative screens. An analysis on the quality of management of those underlying assets also plays a part. We outsource the management of the individual asset classes to the appropriate STANLIB franchise specialists. Co-Heads of Absolute Return, Eben Maré and Marius Oberholzer, manage the equities, Head of Money Market, Ansie van Rensburg, manages cash, Head of Bonds, Victor Mphaphuli, manages bonds and Head of Listed Property, Keillen Ndlovu, manages property. International exposures are managed by Eben Maré.

STANLIB holds a quarterly asset allocation meeting, where the fundamentals of each asset class is analysed and guidance provided in terms of which asset classes should be overweight or underweight a strategic benchmark. The portfolio managers are participants in this meeting and their views are noted, debated and reflected in the final outcome.

At the total portfolio level, the sell discipline is determined by the strategic asset allocation and the minor/short-term tactical consideration, taking into account the global and domestic macroeconomic factors influencing asset class performance. For example, the selling of equities may be required merely as part of a re-balancing exercise or on the basis that equity valuations have become “stretched” and no longer represent good value.

At the underlying asset class level, the sell discipline is performed by the respective franchise specialist and is fundamentally based, with specific reference to the investment return and risk characteristics which are appropriate for the mandate.

We believe that the returns of the various asset classes revert to mean over time. Past and expected performance is considered as part of the asset allocation decision. When deciding on the exposure to growth assets the following is also considered:

Љ Price to earnings (P/E) ratios versus the ten year average Љ HOLT system to assess what is priced in at current market

prices Љ Discounted cash flow analysis to assess absolute

valuations

When deciding on the exposure to defensive assets we consider the following:

Љ Duration Љ Break-even analysis to make decisions between inflation-

linked bonds (ILB’s), nominal bonds and cash Љ Bond fair value calculation

We limit the number of equity counters to a maximum of 20 to ensure meaningful conviction positions at an overall portfolio level.

4

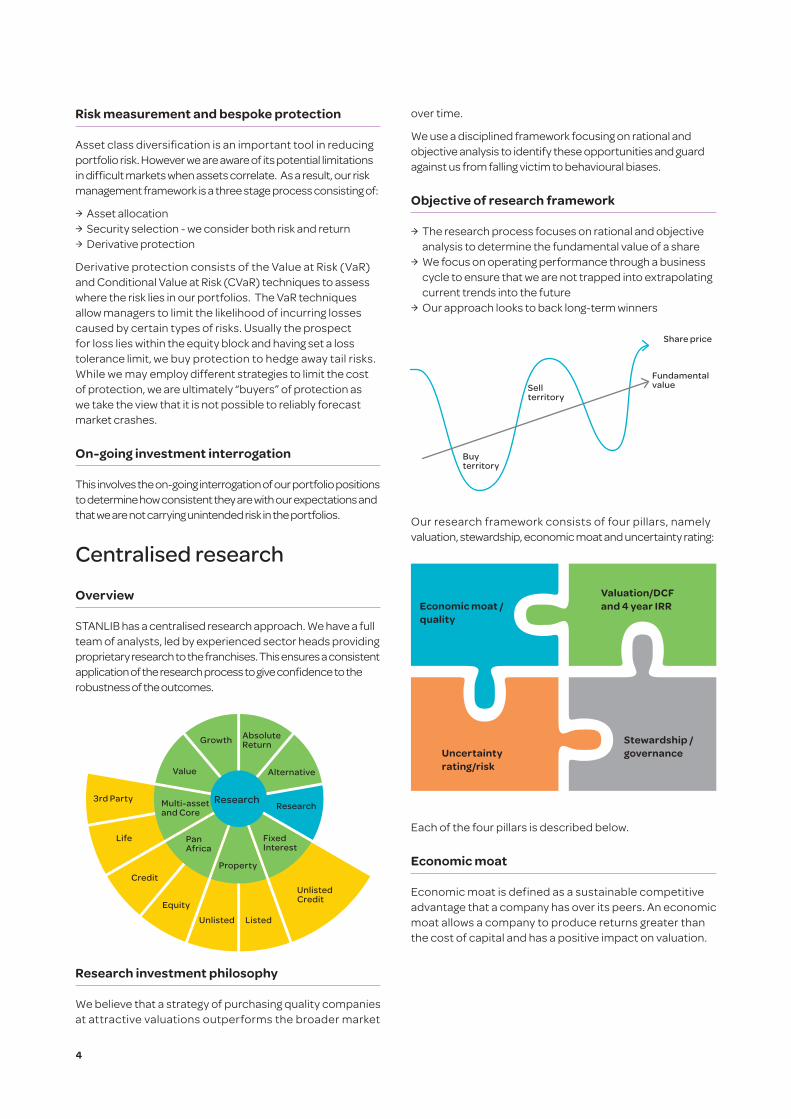

Risk measurement and bespoke protection

Asset class diversification is an important tool in reducing portfolio risk. However we are aware of its potential limitations in difficult markets when assets correlate. As a result, our risk management framework is a three stage process consisting of:

Љ Asset allocation Љ Security selection - we consider both risk and return Љ Derivative protection

Derivative protection consists of the Value at Risk (VaR) and Conditional Value at Risk (CVaR) techniques to assess where the risk lies in our portfolios. The VaR techniques allow managers to limit the likelihood of incurring losses caused by certain types of risks. Usually the prospect for loss lies within the equity block and having set a loss tolerance limit, we buy protection to hedge away tail risks. While we may employ different strategies to limit the cost of protection, we are ultimately “buyers” of protection as we take the view that it is not possible to reliably forecast market crashes.

On-going investment interrogation

This involves the on-going interrogation of our portfolio positions to determine how consistent they are with our expectations and that we are not carrying unintended risk in the portfolios.

Centralised research

Overview

STANLIB has a centralised research approach. We have a full team of analysts, led by experienced sector heads providing proprietary research to the franchises. This ensures a consistent application of the research process to give confidence to the robustness of the outcomes.

ResearchResearch

Fixed Interest

Property

Pan Africa

Multi-asset and Core

Value

Growth Absolute Return

Alternative

3rd Party

Life

Credit

Equity

Unlisted Listed

Unlisted Credit

Research investment philosophy

We believe that a strategy of purchasing quality companies at attractive valuations outperforms the broader market

over time.

We use a disciplined framework focusing on rational and objective analysis to identify these opportunities and guard against us from falling victim to behavioural biases.

Objective of research framework

Љ The research process focuses on rational and objective analysis to determine the fundamental value of a share

Љ We focus on operating performance through a business cycle to ensure that we are not trapped into extrapolating current trends into the future

Љ Our approach looks to back long-term winners

Buy territory

Sell territory

Share price

Fundamental value

Our research framework consists of four pillars, namely valuation, stewardship, economic moat and uncertainty rating:

Economic moat / quality

Valuation/DCF and 4 year IRR

Uncertainty rating/risk

Stewardship / governance

Each of the four pillars is described below.

Economic moat

Economic moat is defined as a sustainable competitive advantage that a company has over its peers. An economic moat allows a company to produce returns greater than the cost of capital and has a positive impact on valuation.

5

Stewardship

The quality of a company’s management and governance structures are key determinants in how a company performs. We assess the quality of management and governance structures through a detailed questionnaire dealing with:

Љ Accounting transparency Љ Board independence Љ Ownership and management incentives Љ Strategy and execution; and Љ Commitment to social and environmental issues

Stewardship provides a holistic view of the impact of management and the board on all stakeholders. The questionnaire includes King III and UN Principles of Responsible Investing (PRI) considerations and is reviewed periodically to ensure that it remains relevant.

Valuation

Discounted cash flow (DCF) models are used in conjunction with other valuation techniques to determine the fair value of each company. This is followed by a calculation of what the annualised return expectation is for an investment, over a four year period.

In forecasting earnings and performance metrics for companies, analysts test for reasonableness in their assumptions, by referencing long run returns generated by companies.

Uncertainty rating

Predicting future earnings is made more difficult when a company has a history of producing volatile earnings or is expected to produce volatile earnings in the future. Therefore, a company that has a stable and consistent approach to renewing corporate value would provide greater predictability with regard to its fair value. The uncertainty rating therefore allows us to consider the margin of safety that we require for an investment in a share.

Combining the four pillars

The process of integrating the four research pillars to compile a research view is set out in the schematic below. The output is a risk-adjusted rating.

Uncertainty and star rating

Company forecasts and valuation

Moat Economic inputsStewardship

Investment risk managementThe approach to investment risk at STANLIB is proactive, which means being prepared for unlikely events and learning from market crises. This applies to both market and non-market risks such as counterparty, operational, leverage and liquidity. Risk is the responsibility of the portfolio manager and is integrated into the investment team’s decision-making process. Each franchise is responsible for the monitoring and measuring of investment risks and the implementation of internal risk controls consistent with their risk appetite, investment philosophy and process. The oversight for investment risk is the responsibility of the Portfolio Analytics, Risk and Implementation Team and for operational risk, the responsibility of the STANLIB Compliance Team. These oversight functions ensure independence, clear accountability and enable portfolio managers to improve their investment process. The risk management framework is aligned with the investment objectives and investment horizon, and tackles multiple aspects of risk, as opposed to being limited to a single measure such as tracking error. Furthermore, an effective, integrated risk framework measures, monitors and manages exposures to economic and fundamental drivers of risk and return across asset classes in order to avoid the overexposure to any one risk factor.

Portfolio Analytics, Risk and Implementation

The Portfolio Analytics, Risk and Implementation Team (PARI) at STANLIB provides an oversight function via a consistent and unbiased process for evaluating investment risks for each franchise. The objective of the PARI Team is to verify that portfolio managers are investing in line with their investment philosophy and within risk limits. The team monitors and manages the following investments risks:

Љ Credit Љ Liquidity Љ Derivatives Љ Market concentration; and Љ Investment risk

The objective of the team is to quantify, decompose, evaluate and communicate both benchmark and peer-relative risk and return. In order to achieve these objectives, the PARI Team:

Љ Makes all investment risks transparent to the franchises Љ Identifies and communicates to senior management all

risks that may lead to extreme performance; and Љ Identifies each franchise’s strengths and weaknesses via

detailed performance and attribution analysis

This function complements the STANLIB compliance function, which is responsible for ensuring that the franchises operate within client-specified guidelines and regulatory limits.

6

There are three components to STANLIB’s risk management framework:

Љ Risk measurement: the team does not only consider aggregate portfolio risk such as volatility or tracking error, which rely on individual volatilities and correlations of asset classes and managers. Volatility, tracking error and correlations capture the overall risk of the portfolio but do not distinguish between the sources of risk, which may include market risk, sector risk, credit risk and interest rate risk etc.

Љ Risk monitoring: enables the team to monitor changes in the sources of risk on a regular and timely basis. Portfolio decomposition plays an important role in stress testing. The sources of risk are stressed by the team to assess the impact on the portfolio. Risk is managed for normal times but the team are cognisant of and aim to be prepared for extreme events

Љ Risk-adjusted investment management: this function aligns the investment decision-making process with the risk management. It suggests ways in which portfolio managers can adjust their portfolios in response to expected changes in risk

These three components of the robust risk management framework are essential. Risk measurement means having the right tools to measure risk accurately. Risk monitoring means observing the risk measures on a regular and timely basis. Risk-adjusted investment management means using the information from the measurement and monitoring of risks in order to ensure that the portfolio management process is aligned with expectations of risk and risk tolerance. Moreover, each component is interdependent and should be aligned with our clients’ investment objectives. This interconnectedness is essential for a robust risk management framework at STANLIB and for the investment process to be fully aligned and integrated.

Broader risk managementCompliance and investment risk management are the cornerstones of our business. To this end, we have robust risk management, compliance and governance structures. Our highly experienced Middle Office consists of Compliance, Legal, and Risk Management, which provide systems and processes to ensure that mandate compliance is monitored.

In addition to the portfolio monitoring tools mentioned above, we use the STATPRO system to measure our performance relative to benchmarks and indices, where appropriate. STATPRO is also used for performance attribution. Risk management is effected through appropriate diversification

across sectors and counters and ensuring that investment sizes are within limits.

We have made provision for IT and business recovery facilities including office space. Our robust systems are designed to ensure that our organisation operates efficiently at all times. Insurance policies for professional indemnity as well as directors’ and officers’ liability are in place, through Standard Bank Insurance Brokers (Pty) Ltd.

Environmental, social and governance factorsSTANLIB is committed to and is a signatory of the United Nations Principles for Responsible Investing (UNPRI). In addition, we manage assets in accordance with the Code for Responsible Investing in South Africa (CRISA).

The work done with respect to the full implementation of these principles includes, but is not limited to, continuous monitoring of corporate governance and reputation risk, assessment of health and safety as well as environmental practices and shareholder activism.

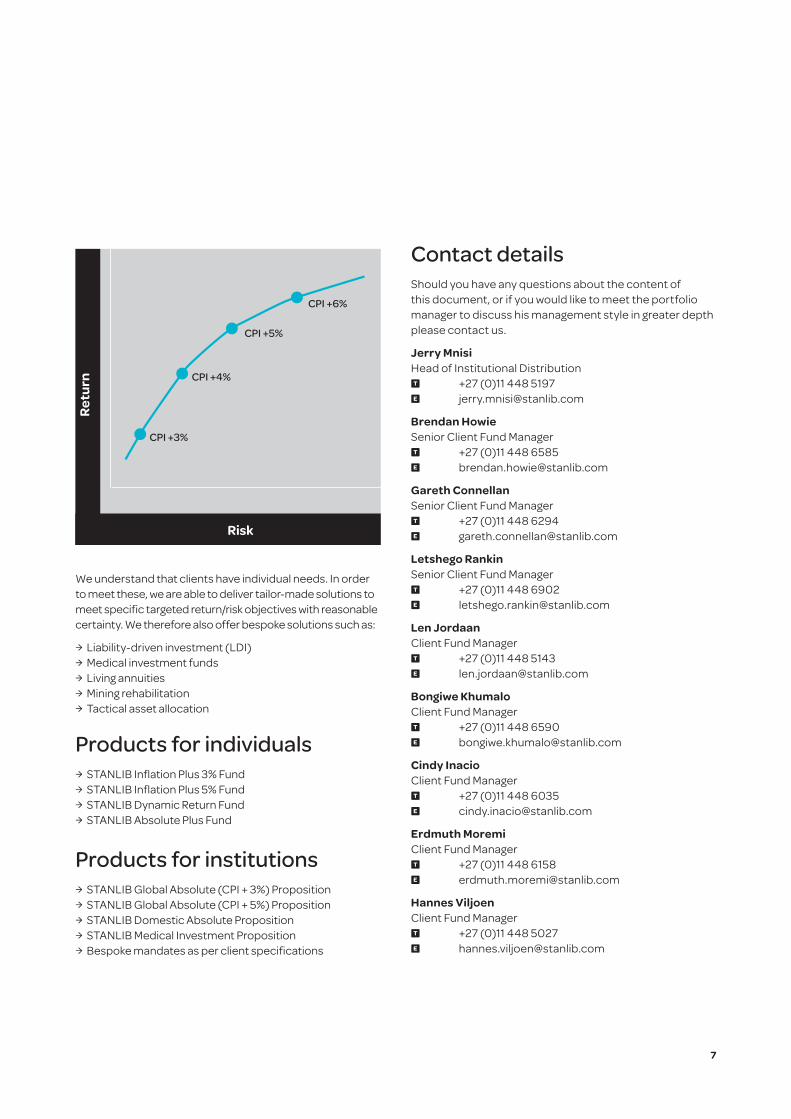

CapabilitiesThe majority of the assets that we manage fall into four solutions:

Љ CPI +3% over 36 months with capital protection over 12 months

Љ CPI +4% over 36 months with capital protection over 12 months

Љ CPI +5% over 36 months with capital protection over 12 months

Љ CPI +6% over 36 months with capital preservation over 12 months

7

Return

Risk

CPI +3%

CPI +4%

CPI +5%

CPI +6%

We understand that clients have individual needs. In order to meet these, we are able to deliver tailor-made solutions to meet specific targeted return/risk objectives with reasonable certainty. We therefore also offer bespoke solutions such as:

Љ Liability-driven investment (LDI) Љ Medical investment funds Љ Living annuities Љ Mining rehabilitation Љ Tactical asset allocation

Products for individuals Љ STANLIB Inflation Plus 3% Fund Љ STANLIB Inflation Plus 5% Fund Љ STANLIB Dynamic Return Fund Љ STANLIB Absolute Plus Fund

Products for institutions Љ STANLIB Global Absolute (CPI + 3%) Proposition Љ STANLIB Global Absolute (CPI + 5%) Proposition Љ STANLIB Domestic Absolute Proposition Љ STANLIB Medical Investment Proposition Љ Bespoke mandates as per client specifications

Contact detailsShould you have any questions about the content of this document, or if you would like to meet the portfolio manager to discuss his management style in greater depth please contact us.

Jerry MnisiHead of Institutional Distribution T +27 (0)11 448 5197 E [email protected]

Brendan HowieSenior Client Fund Manager T +27 (0)11 448 6585 E [email protected]

Gareth ConnellanSenior Client Fund Manager T +27 (0)11 448 6294 E [email protected]

Letshego RankinSenior Client Fund Manager T +27 (0)11 448 6902 E [email protected]

Len JordaanClient Fund Manager T +27 (0)11 448 5143 E [email protected]

Bongiwe KhumaloClient Fund Manager T +27 (0)11 448 6590 E [email protected]

Cindy InacioClient Fund Manager T +27 (0)11 448 6035 E [email protected]

Erdmuth MoremiClient Fund Manager T +27 (0)11 448 6158 E [email protected]

Hannes ViljoenClient Fund Manager T +27 (0)11 448 5027 E [email protected]

8

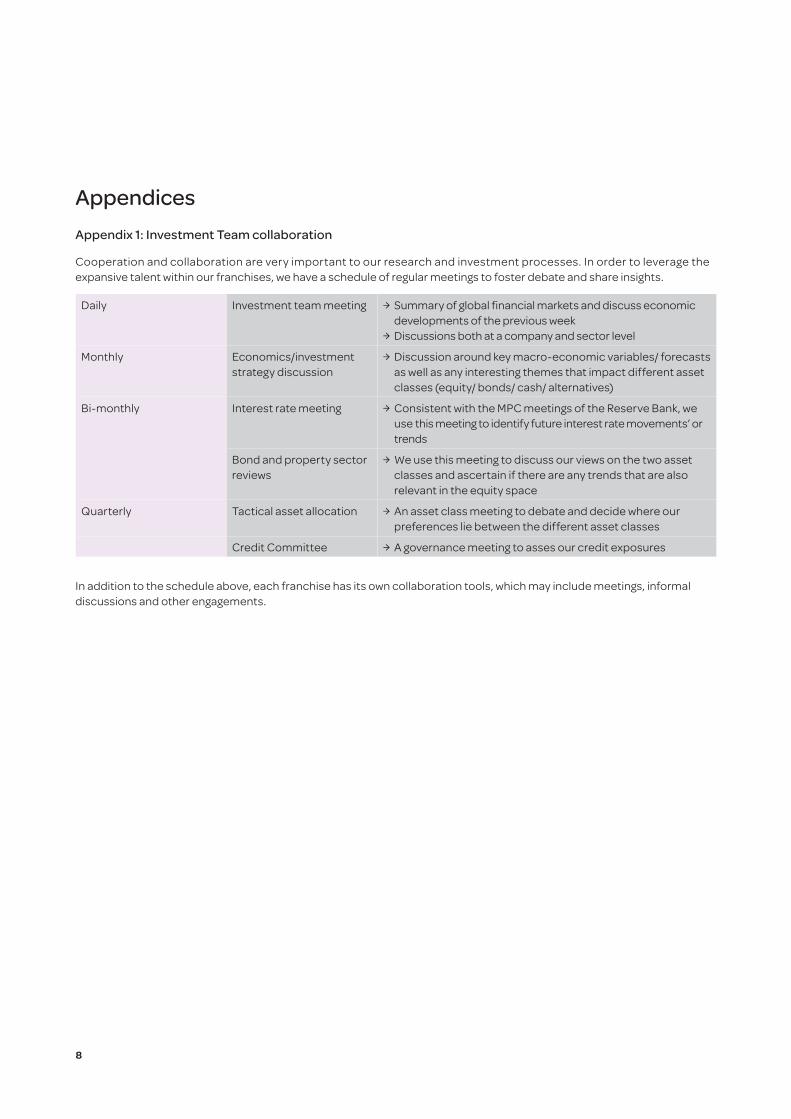

AppendicesAppendix 1: Investment Team collaboration

Cooperation and collaboration are very important to our research and investment processes. In order to leverage the expansive talent within our franchises, we have a schedule of regular meetings to foster debate and share insights.

Daily Investment team meeting Љ Summary of global financial markets and discuss economic developments of the previous week

Љ Discussions both at a company and sector level

Monthly Economics/investment strategy discussion

Љ Discussion around key macro-economic variables/ forecasts as well as any interesting themes that impact different asset classes (equity/ bonds/ cash/ alternatives)

Bi-monthly Interest rate meeting Љ Consistent with the MPC meetings of the Reserve Bank, we use this meeting to identify future interest rate movements’ or trends

Bond and property sector reviews

Љ We use this meeting to discuss our views on the two asset classes and ascertain if there are any trends that are also relevant in the equity space

Quarterly Tactical asset allocation Љ An asset class meeting to debate and decide where our preferences lie between the different asset classes

Credit Committee Љ A governance meeting to asses our credit exposures

In addition to the schedule above, each franchise has its own collaboration tools, which may include meetings, informal discussions and other engagements.

9

Appendix 2: Team Profiles

Eben Mare – BSc(Hons), MSc, PhD

Co-Head of Absolute Return Franchise

Industry experience - 24 years

Eben joined STANLIB in 2009 as portfolio manager for absolute return funds and was appointed as Head of the franchise in 2012.

Over the past two decades, Eben has worked at the forefront of industry developments in the fields of risk management, quantitative analysis and derivative instruments; including spells as GM at Nedcor Investment Bank (with responsibility for derivatives trading and Domestic Treasury), CEO of Syfrets Securities, and Head of Market Risk at Absa Capital.

Eben began his working career as a scientist, first at the CSIR and then at the Council for Nuclear Safety.

With a doctorate in Applied Mathematics, Eben has held a position as Associate Professor of Mathematics and Applied Mathematics at the University of Pretoria. He continues to do active research in his spare time.

Marius Oberholzer –MSc, BCom

Co-Head of Absolute Return Franchise

Industry experience - 14 years

Marius joined STANLIB in September 2013 as Co-Head of the Absolute Return Franchise. His focus is on local and global equity growth components of the absolute portfolios as well as input into strategic and tactical asset allocation decisions.

Marius joined from Sarala Capital in Cape Town, where he was a Managing Partner responsible for providing strategic direction for the firm. His role was focused on corporate finance solutions and spearheading the group’s unlisted investment activities.

Between 2000 and 2012, Marius worked at TT International in London and Hong Kong where he focused primarily on managing their Asian Opportunities Long Short Equity Hedge Fund.

Marius holds a BCom (Stellenbosch) and an MSc in Global Finance from the Hong Kong University of Science and Technology and New York University.

Bhekinkosi Khuzwayo – BSc(Hons)

Analyst

Industry experience - 6 years

Bheki joined STANLIB in 2012 as an Analyst in the Absolute Return Franchise.

He built his professional experience through the Cadiz Graduate Recruitment Programme, with rotation through various divisions within the Cadiz group. He joined their Quantitative Research Team in 2007 and over five years built up his expertise and reputation as one of South Africa’s most highly-rated sell-side analysts in quantitative research.

Bheki graduated in Maths and Economics at the University of the Witwatersrand in 2005 and received Honours with distinction in Pure Mathematics the following year.

10

Legal NoticesCollective investment schemes in securities are generally medium to long-term investments. The value of participatory interests may go down as well as up and past performance is not necessarily a guide to the future. An investment in the participations of a collective investment scheme in securities is not the same as a deposit with a banking institution. Participatory interest prices are calculated on a net asset value basis, which is the total value of all assets in the Fund including any income accrual and less any permissible deductions from the Fund divided by the number of participatory interests in issue. Permissible deductions include brokerage, UST, auditor’s fees, bank charges, trustee/custodian fees and the service charge levied by STANLIB Collective Investments (RF) Limited (“the Manager”). Where exit fees are applicable, participatory interests are redeemed at the net asset value where after the exit fee is deducted and the balance is paid to the investor. A Portfolio of a collective investment scheme in securities may borrow up to 10% of the market value of the Fund to bridge insufficient liquidity as a result of the redemption of participatory interests, and may also engage in scrip lending.

Where different classes of participatory interests apply to certain Portfolios, they would be subject to different fees and charges. A schedule of fees and charges and maximum commissions is available on request from the Manager. Commission and incentives may be paid and if so, would be included in the overall costs. The exposure limit to a single security in this Portfolio can be greater than is permitted for other Portfolios in terms of the Collective Investment Schemes Control Act, 2002 (“the Act”). Details are available from the Manager. A Fund of Funds Portfolio only invests in other collective investment schemes, which levy their own charges, which could result in a higher fee structure for these portfolios. A Feeder Fund Portfolio only invests in the participatory interests of a single Portfolio of a collective investment scheme apart from assets in liquid form. The Manager reserves the right to close certain Portfolios from time to time in order to manage them more efficiently. More details are available from the Manager. Forward pricing is used.

Fluctuations or movements in exchange rates may cause the value of underlying international investments to go up or down. The Manager undertakes to repurchase participatory interests at the price calculated according to the requirements of the Collective Investment Schemes Control Act, 2002, and on the terms and conditions of the relevant Deeds. Payment will be made within 14 days of receipt of a valid repurchase form. Any capital gain realized on the disposal of a participatory interest in a collective investment scheme is subject to Capital Gains Tax (CGT). The Manager is obliged to report on the weighted average cost method for CGT purposes. All portfolios are valued on a daily basis at 15h30, except for some Fund of Funds Portfolios and Feeder Fund Portfolios, which are valued at 17h00. Investments and Repurchases will receive the price of the same day if received prior to 15h30. The Fund Charges document (including the Performance Fee Frequently Asked Questions) is available on www.stanlib.com (“Investment for Individuals” section).

Contact details of Trustees: Standard Chartered Bank, 4 Sandown Valley Crescent, Sandton, 2196. Telephone 011 291 8042.

STANLIB Collective Investments (RF) Limited Reg. No. (1969/003468/06)

Liberty is a member of the Association for Savings and Investment of South Africa. The Manager is a member of the Liberty group of companies.

Document relevant as of 27 February 2015

Compliance number: 2519HX

17 Melrose Boulevard Melrose Arch 2196 PO Box 203 Melrose Arch 2076T 0860 123 003 (SA only) T +27 (0)11 448 6000 E [email protected] W stanlib.comGPS coordinates S 26.13433°, E 028.06800° W

STA

NLI

B A

sset

Man

agem

ent L

imite

d | R

eg. N

o. 19

69/0

027

53/0

6 | A

utho

rised

FSP

in te

rms o

f the

FA

IS A

ct, 2

00

2 (L

icen

ce N

o. 2

6/10

/719

)