spring global outlook ms 13th march 2016

TRANSCRIPT

March 13, 2016

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision. For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report. += Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to NASD/NYSE restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.*

M O R G A N S T A N L E Y R E S E A R C H

Spring Global Strategy Outlook Playing Good Defense

More Concerned: Weaker growth forecasts and rising political risk lead us to close our positive tactical stance and lower exposure in global equities, and to moderate our EU credit weight after the sharp ECB driven rally. We add to cash, US Treasuries and JGBs given significant changes to our policy and rate forecasts. We remain JPY and USD bulls, and bearish on AxJ FX.

The Burden of Proof: Growth is weak. We think this is widely known. The more relevant question is whether the burden of proof lies with the bulls to prove that this is already in the price, or with the bears to prove that it isn’t. We think the answer favors Credit, but also discuss how the ‘burden of proof’ affects the best ways to play offense and defense.

Global Equities – More Cautious: We lower our 12-month price targets and see a negative bull/bear return skew across markets. We like US equities most, Europe and EM equities least, and focus on reasonably priced ways to find ‘quality’ across regions.

Global FX – USD Run Not Over: The USD bull run is not over, while we are increasingly concerned that the EUR will be pulled lower by European political risk over the summer. We avoid AxJ FX, see further downside in commodity FX, and remain bullish on the JPY.

Global Rates – Summer Bulls: Lower growth and fewer expected Fed hikes lead us to materially lower our yield forecasts. The best risk/reward lies in Treasuries, the worst is in EU Sovereigns.

EM Fixed Income – Hunt for Alpha: The sell-off has created a better landscape for relative value. We continue to prefer Credit over Local Rates over FX, and forecast 6.6% total return for EM Sovereigns.

Global Credit – Preferred Beta: Credit is best positioned to deliver reasonable risk-adjusted returns in a slow growth backdrop. Carry drives returns even as higher defaults eat into HY returns. US IG is our preferred form of beta.

Global Securitized Credit – Mixed Prospects: Tighter financial conditions and fundamental challenges impact performance. CLO AAAs offer defensive carry but CMBS faces headwinds without the valuation cushion of IG corporates.

Global Volatility – Finding Value: We like buying equity and rates volatility after recent drop to hedge our cautious macro forecast. EUR and JPY vols are best to buy, but EM FX vols will be hard to monetize.

M O R G A N S T A N L E Y R E S E A R C H G L O B A L S T R A T E G Y T E A M

Morgan Stanley & Co. LLC Matthew Hornbach Gordian Kemen Adam S. Parker Vishwanath Tirupattur Adam Richmond

Morgan Stanley & Co. International plc+ Hans Redeker Graham Secker Andrew Sheets

Morgan Stanley Asia Limited+ Jonathan Garner

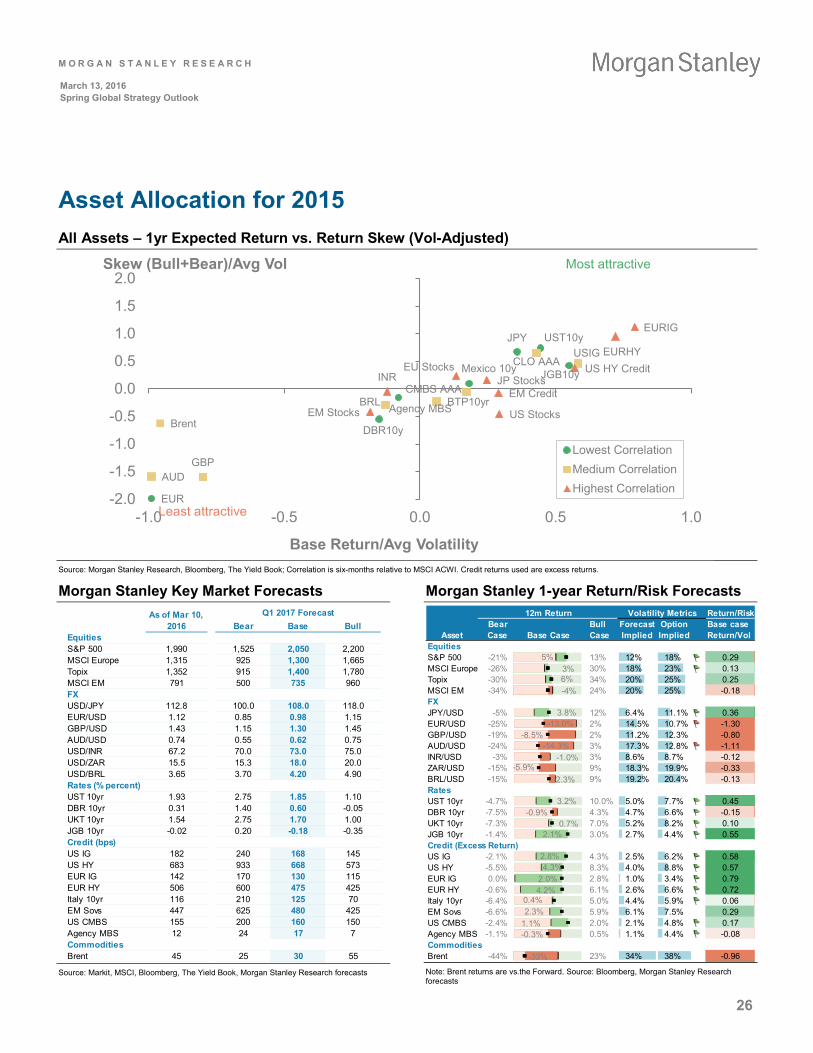

MS Cross Asset Allocations

Note: For a 6-12m view. See Page 27 for Details. Note: Adam Parker, Graham Secker and Jonathan Garner are Equity Analysts and they are not opining on fixed income securities. Their views are clearly delineated. Due to the nature of the fixed income market, the issuers or bonds of the issuers recommended or discussed in this report may not be continuously followed. Accordingly, investors must regard this report as providing stand-alone analysis and should not expect continuing analysis or additional reports relating to such issuers or bonds of the issuers.

Global Asset Allocation – +EquitiesCreditGovernment BondsCash

Within these asset classes, our relative allocations:

Equities – +USEuropeJapanEM

Credit – +USEuropeEMSecuritized

Government Bonds – +TreasuriesBundsJGBsEM Local

FX – +USDEURJPYEM

CurrentPrevious

M O R G A N S T A N L E Y R E S E A R C H

2

March 13, 2016 Spring Global Strategy Outlook

Table of Contents Cross-Asset Strategy: Burden of Proof .................................................................................................................................................3 Global Equities: Sell the Recent Rally ...................................................................................................................................................8 Global Government Bonds: Year of the Bull ....................................................................................................................................... 12 Global FX: The Bullish JPY, USD and CHF Trio ................................................................................................................................. 14 Global EM Fixed Income: The Case For Alpha ................................................................................................................................... 16 Global Credit: Springing Back to Life................................................................................................................................................... 18 Global Securitized Products: Tighter, Lower and Wider ...................................................................................................................... 20 Crude Oil: Low and Range-bound Through Mid-17 ............................................................................................................................. 22 Global Volatility: Value in Vol .............................................................................................................................................................. 24 What We Debated ............................................................................................................................................................................... 25 Asset Allocation for 2015 ..................................................................................................................................................................... 26 Morgan Stanley Key Economic Forecasts ........................................................................................................................................... 29 Morgan Stanley Global Currency Forecasts ........................................................................................................................................ 30 Morgan Stanley Government Bond Yield / Spread Forecasts ............................................................................................................. 31

What’s Changed?

What's Changed - Economics

2016e 2017e 2016e 2017e 2016e 2017eGDPG10 1.8 1.8 1.5 1.6 -0.3 -0.2 US 1.9 1.8 1.7 1.6 -0.2 -0.2 Euro Area 1.8 1.8 1.5 1.8 -0.3 0.0 Japan 1.2 0.8 0.6 0.5 -0.6 -0.3 UK 2.0 2.3 1.7 2.3 -0.3 0.0EM (%Y) 4.4 5.0 4.0 4.7 -0.4 -0.3 China 6.7 6.6 6.5 6.4 -0.2 -0.2 India 7.9 8.0 7.5 7.7 -0.4 -0.3 Brazil -3.0 1.2 -4.3 0.6 -1.3 -0.6 Russia -0.8 1.7 -2.1 0.9 -1.3 -0.8

CPI (%Y)G10 1.5 2.1 0.8 1.9 -0.7 -0.2 US 1.7 2.3 1.2 1.9 -0.5 -0.4 Euro Area 1.3 1.8 0.2 1.7 -1.1 -0.1 Japan 1.0 2.5 -0.2 2.0 -1.2 -0.5 UK 1.3 1.5 0.8 1.7 -0.5 0.2EM 3.7 3.2 3.8 3.4 0.1 0.2 China 1.1 1.1 1.1 1.1 0.0 0.0 India 4.9 4.5 5.0 4.5 0.1 0.0 Brazil 8.2 6.0 9.2 7.2 1.0 1.2 Russia 7.8 6.4 8.9 7.3 1.1 0.9

Monetary Policy Rate (% p.a.)G10 0.6 1.1 0.2 0.4 -0.4 -0.7 US 1.1 2.1 0.6 1.1 -0.5 -1.0 Euro Area 0.1 0.1 -0.5 -0.5 -0.6 -0.6 Japan 0.1 0.1 -0.3 -0.3 -0.4 -0.4 UK 1.0 1.5 0.5 1.0 -0.5 -0.5EM 5.4 5.3 5.4 5.2 0.0 -0.1 China 3.9 3.9 4.1 3.9 0.3 0.0 India 6.5 6.8 6.5 6.8 0.0 0.0 Brazil 15.3 13.3 14.3 13.3 -1.0 0.0 Russia 8.0 6.5 10.0 7.5 2.0 1.0

OLD FORECASTS NEW FORECASTS Change from Last ForecastWhat's Changed - AssetsBase Case Forecasts OLD NEW Δ

Q4 2016 Q1 2017EquitiesS&P 500 2,175 2,050 -6%MSCI Europe 1,500 1,300 -13%Topix 1,640 1,400 -15%MSCI EM 850 735 -14%FXUSD/JPY 115.0 108.0 -6%EUR/USD 1.00 0.98 -2%GBP/USD 1.40 1.30 -7%AUD/USD 0.62 0.62 0%USD/INR 70.0 73.0 4%USD/ZAR 18.8 18.0 -4%USD/BRL 4.45 4.20 -6%Rates (% percent) (bp Δ)

UST 10yr 2.70 1.85 -85DBR 10yr 1.20 0.60 -60UKT 10yr 2.60 1.70 -90JGB 10yr 0.85 -0.18 -103Credit (bps) (bp Δ)

US IG 175 168 -7US HY 582 668 86EUR IG 115 130 15EUR HY 510 475 -35Italy 10yr 100 125 25EM Sovs 400 480 80US CMBS 135 160 25Agency MBS 27 17 -10CommoditiesBrent 29 30 3%

M O R G A N S T A N L E Y R E S E A R C H

3

March 13, 2016 Spring Global Strategy Outlook

Cross-Asset Strategy: Burden of Proof Andrew Sheets

Key Investment Ideas • Growth remains weak and the probability of a global

recession has risen. The challenge is that these concerns are not entirely unexpected by the markets. In many cases, the more defensive an asset is today, the richer it tends to be.

• US and EM Credit are pricing in a worse environment than what we forecast. We are less confident this is the case for stocks. We see the JPY and UST-DBR spread as two of the few reasonably-priced defensive strategies available.

• Relative to current market pricing, we see worsening risk-reward in Europe. We lower European Equities, moderate allocation to European Credit post the ECB rally, and see poor risk-reward in peripheral sovereigns, GBP and EUR.

Our global growth outlook is weak and skewed to the downside. The challenge is that this outcome does not feel entirely unexpected. Global equity markets are down -12% since the summer. G3 interest rates and inflation expectations are near historical lows. Investor cash balances remain high. Across many different investments, the more defensive something is, the richer it trades relative to history.

The question, therefore, shifts to where the burden of proof lies. Is the onus on the bears to prove that, after a correction, this isn’t just another post-crisis growth scare? Or has it shifted to the bulls to show that after the recent bounce, further upside is possible even under a restrained macro backdrop?

We think the answer depends on where you look. In areas like US Corporate and EM Sovereign Credit, we think valuations discount a growth environment worse than our below-consensus forecasts. In areas like Global Equities, AxJ FX, and US Equity and Rates volatility, we are less sure. On balance, this leads us to reduce risk. We close our positive tactical stance (see Oversold, February 15, 2015) and reduce weights in Global Equities (-3%), moderate EU Credit (-1%), and add to US Treasuries (+2%), JGBs (+1%) and cash (+1%).

If we went solely by our new price targets (see page 2), we should reduce exposure even more, moving underweight equities and overweight bonds. We are not making this shift because the two other elements of our framework, long-run risk premiums and our cycle models, tell us not to. But we are on watch. In such a backdrop, it is imperative to ask both “where

can I still find reasonably-priced defense?” and “where is the most optionality to the upside?” We address both.

The Macro Challenges

Let’s start with the macroeconomic challenges, before moving to the question of whether they are in the price. There are a multitude of issues confronting the market. More detailed discussions can be found in the accompanying Spring Economic Outlook, but here is a quick summary.

Effectiveness of central bank policy – Central banks hold a declining number of less effective policy tools. Their latest foray, negative rates, may do more harm than good. How bad is it if central banks are powerless to boost the economy?

Well, it clearly isn’t good. But it also isn’t as “unprecedented” (and therefore bad) as often portrayed. Prior to 2010, central bank easing was usually unable to stop market declines (2002, 2008). And this makes sense; policy can’t change the course of the underlying economy, it can only nudge it one way or the other.

The lack of additional policy tools is one reason there is more downside to our equity bear cases than in ’13 or ’14. The good news is that (a) we think this keeps conventional G3 policy extremely accommodative, with just one Fed hike in ’16, and (b) this lack of additional policy tools won’t matter if data continues to stabilize. Good (data) is good.

Exhibit 1 We Forecast Growth to Fall Short of Expectations

Source: Morgan Stanley Research forecasts, Bloomberg

Growth – Given the lack of policy tools, we think growth will matter more for markets than central banks. And our growth forecasts are not inspiring. Our economists are below consensus on global, EM and DM growth and have raised their probability of a global recession within the next 12 months to 30%. This is a major reason many of our price targets have come down, although as we will discuss shortly, some appear to discount weaker growth than others.

Real GDP (%Q SAAR)2015 2016e 2017e

MS Forecast 2.4 1.7 1.6Consensus 2.4 2.1 2.3

MS Forecast 1.5 1.5 1.8Consensus 1.5 1.6 1.6

MS Forecast 0.5 0.6 0.5Consensus 0.6 0.7 0.6

MS Forecast 2.2 1.7 2.3Consensus 2.2 2.1 2.2

US

Euro Area

Japan

UK

– +EquitiesCreditGovernment BondsCash

M O R G A N S T A N L E Y R E S E A R C H

4

March 13, 2016 Spring Global Strategy Outlook

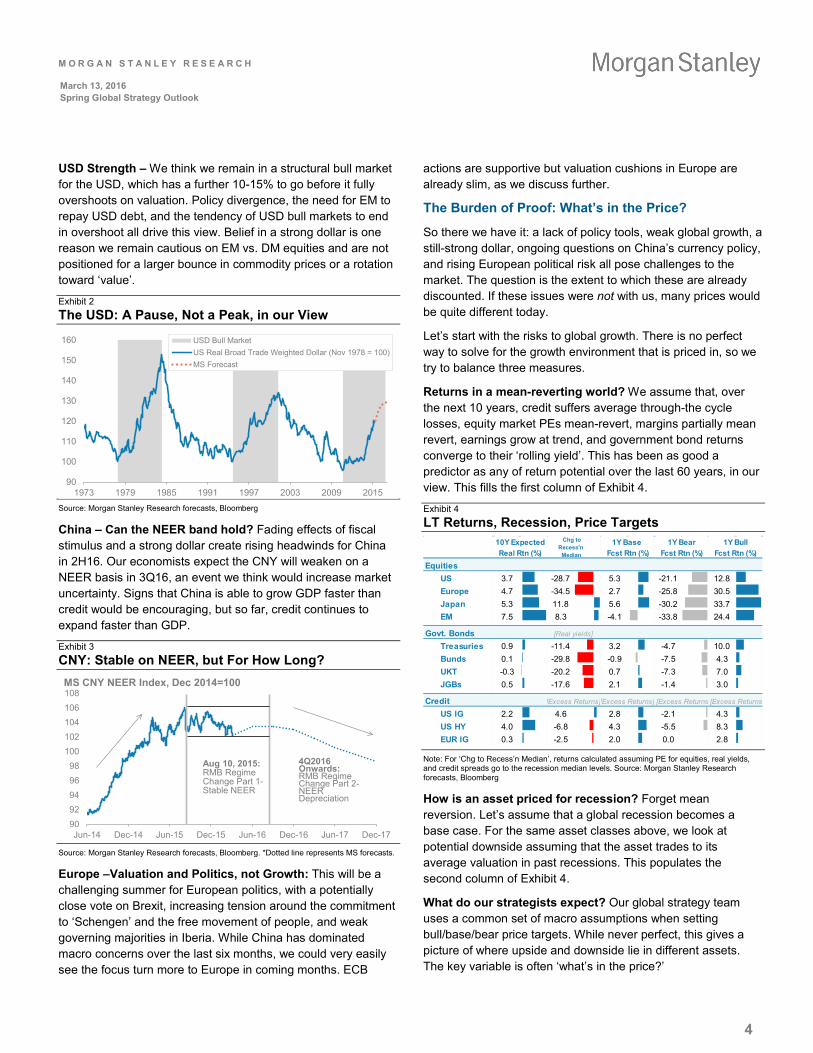

USD Strength – We think we remain in a structural bull market for the USD, which has a further 10-15% to go before it fully overshoots on valuation. Policy divergence, the need for EM to repay USD debt, and the tendency of USD bull markets to end in overshoot all drive this view. Belief in a strong dollar is one reason we remain cautious on EM vs. DM equities and are not positioned for a larger bounce in commodity prices or a rotation toward ‘value’.

Exhibit 2 The USD: A Pause, Not a Peak, in our View

Source: Morgan Stanley Research forecasts, Bloomberg

China – Can the NEER band hold? Fading effects of fiscal stimulus and a strong dollar create rising headwinds for China in 2H16. Our economists expect the CNY will weaken on a NEER basis in 3Q16, an event we think would increase market uncertainty. Signs that China is able to grow GDP faster than credit would be encouraging, but so far, credit continues to expand faster than GDP.

Exhibit 3 CNY: Stable on NEER, but For How Long?

Source: Morgan Stanley Research forecasts, Bloomberg. *Dotted line represents MS forecasts.

Europe –Valuation and Politics, not Growth: This will be a challenging summer for European politics, with a potentially close vote on Brexit, increasing tension around the commitment to ‘Schengen’ and the free movement of people, and weak governing majorities in Iberia. While China has dominated macro concerns over the last six months, we could very easily see the focus turn more to Europe in coming months. ECB

actions are supportive but valuation cushions in Europe are already slim, as we discuss further.

The Burden of Proof: What’s in the Price?

So there we have it: a lack of policy tools, weak global growth, a still-strong dollar, ongoing questions on China’s currency policy, and rising European political risk all pose challenges to the market. The question is the extent to which these are already discounted. If these issues were not with us, many prices would be quite different today.

Let’s start with the risks to global growth. There is no perfect way to solve for the growth environment that is priced in, so we try to balance three measures.

Returns in a mean-reverting world? We assume that, over the next 10 years, credit suffers average through-the cycle losses, equity market PEs mean-revert, margins partially mean revert, earnings grow at trend, and government bond returns converge to their ‘rolling yield’. This has been as good a predictor as any of return potential over the last 60 years, in our view. This fills the first column of Exhibit 4.

Exhibit 4 LT Returns, Recession, Price Targets

Note: For ‘Chg to Recess’n Median’, returns calculated assuming PE for equities, real yields, and credit spreads go to the recession median levels. Source: Morgan Stanley Research forecasts, Bloomberg

How is an asset priced for recession? Forget mean reversion. Let’s assume that a global recession becomes a base case. For the same asset classes above, we look at potential downside assuming that the asset trades to its average valuation in past recessions. This populates the second column of Exhibit 4.

What do our strategists expect? Our global strategy team uses a common set of macro assumptions when setting bull/base/bear price targets. While never perfect, this gives a picture of where upside and downside lie in different assets. The key variable is often ‘what’s in the price?’

90

100

110

120

130

140

150

160

1973 1979 1985 1991 1997 2003 2009 2015

USD Bull MarketUS Real Broad Trade Weighted Dollar (Nov 1978 = 100)MS Forecast

9092949698

100102104106108

Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 Dec-16 Jun-17 Dec-17

MS CNY NEER Index, Dec 2014=100

Aug 10, 2015: RMB RegimeChange Part 1-Stable NEER

4Q2016Onwards: RMB RegimeChange Part 2-NEER Depreciation

EquitiesUS 3.7 -28.7 5.3 -21.1 12.8Europe 4.7 -34.5 2.7 -25.8 30.5Japan 5.3 11.8 5.6 -30.2 33.7EM 7.5 8.3 -4.1 -33.8 24.4

Govt. BondsTreasuries 0.9 -11.4 3.2 -4.7 10.0Bunds 0.1 -29.8 -0.9 -7.5 4.3UKT -0.3 -20.2 0.7 -7.3 7.0JGBs 0.5 -17.6 2.1 -1.4 3.0

Credit [Excess Returns][Excess Returns]

US IG 2.2 4.6 2.8 -2.1 4.3US HY 4.0 -6.8 4.3 -5.5 8.3EUR IG 0.3 -2.5 2.0 0.0 2.8

1Y BullFcst Rtn (%)

1Y BearFcst Rtn (%)

[Excess Returns]

[Real yields]

[Excess Returns]

10Y ExpectedReal Rtn (%)

1Y Base Fcst Rtn (%)

Chg to Recess'n Median

M O R G A N S T A N L E Y R E S E A R C H

5

March 13, 2016 Spring Global Strategy Outlook

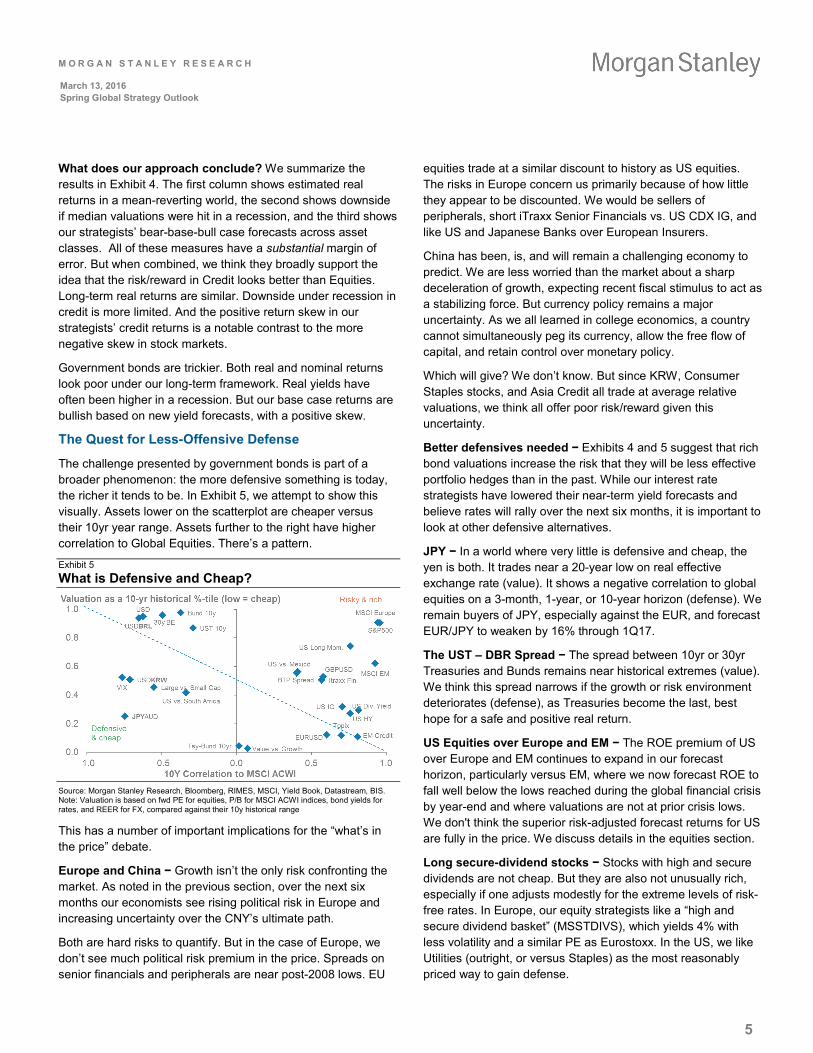

What does our approach conclude? We summarize the results in Exhibit 4. The first column shows estimated real returns in a mean-reverting world, the second shows downside if median valuations were hit in a recession, and the third shows our strategists’ bear-base-bull case forecasts across asset classes. All of these measures have a substantial margin of error. But when combined, we think they broadly support the idea that the risk/reward in Credit looks better than Equities. Long-term real returns are similar. Downside under recession in credit is more limited. And the positive return skew in our strategists’ credit returns is a notable contrast to the more negative skew in stock markets.

Government bonds are trickier. Both real and nominal returns look poor under our long-term framework. Real yields have often been higher in a recession. But our base case returns are bullish based on new yield forecasts, with a positive skew.

The Quest for Less-Offensive Defense

The challenge presented by government bonds is part of a broader phenomenon: the more defensive something is today, the richer it tends to be. In Exhibit 5, we attempt to show this visually. Assets lower on the scatterplot are cheaper versus their 10yr year range. Assets further to the right have higher correlation to Global Equities. There’s a pattern.

Exhibit 5 What is Defensive and Cheap?

Source: Morgan Stanley Research, Bloomberg, RIMES, MSCI, Yield Book, Datastream, BIS. Note: Valuation is based on fwd PE for equities, P/B for MSCI ACWI indices, bond yields for rates, and REER for FX, compared against their 10y historical range

This has a number of important implications for the “what’s in the price” debate.

Europe and China − Growth isn’t the only risk confronting the market. As noted in the previous section, over the next six months our economists see rising political risk in Europe and increasing uncertainty over the CNY’s ultimate path.

Both are hard risks to quantify. But in the case of Europe, we don’t see much political risk premium in the price. Spreads on senior financials and peripherals are near post-2008 lows. EU

equities trade at a similar discount to history as US equities. The risks in Europe concern us primarily because of how little they appear to be discounted. We would be sellers of peripherals, short iTraxx Senior Financials vs. US CDX IG, and like US and Japanese Banks over European Insurers.

China has been, is, and will remain a challenging economy to predict. We are less worried than the market about a sharp deceleration of growth, expecting recent fiscal stimulus to act as a stabilizing force. But currency policy remains a major uncertainty. As we all learned in college economics, a country cannot simultaneously peg its currency, allow the free flow of capital, and retain control over monetary policy.

Which will give? We don’t know. But since KRW, Consumer Staples stocks, and Asia Credit all trade at average relative valuations, we think all offer poor risk/reward given this uncertainty.

Better defensives needed − Exhibits 4 and 5 suggest that rich bond valuations increase the risk that they will be less effective portfolio hedges than in the past. While our interest rate strategists have lowered their near-term yield forecasts and believe rates will rally over the next six months, it is important to look at other defensive alternatives.

JPY − In a world where very little is defensive and cheap, the yen is both. It trades near a 20-year low on real effective exchange rate (value). It shows a negative correlation to global equities on a 3-month, 1-year, or 10-year horizon (defense). We remain buyers of JPY, especially against the EUR, and forecast EUR/JPY to weaken by 16% through 1Q17.

The UST – DBR Spread − The spread between 10yr or 30yr Treasuries and Bunds remains near historical extremes (value). We think this spread narrows if the growth or risk environment deteriorates (defense), as Treasuries become the last, best hope for a safe and positive real return.

US Equities over Europe and EM − The ROE premium of US over Europe and EM continues to expand in our forecast horizon, particularly versus EM, where we now forecast ROE to fall well below the lows reached during the global financial crisis by year-end and where valuations are not at prior crisis lows. We don't think the superior risk-adjusted forecast returns for US are fully in the price. We discuss details in the equities section.

Long secure-dividend stocks − Stocks with high and secure dividends are not cheap. But they are also not unusually rich, especially if one adjusts modestly for the extreme levels of risk-free rates. In Europe, our equity strategists like a “high and secure dividend basket” (MSSTDIVS), which yields 4% with less volatility and a similar PE as Eurostoxx. In the US, we like Utilities (outright, or versus Staples) as the most reasonably priced way to gain defense.

M O R G A N S T A N L E Y R E S E A R C H

6

March 13, 2016 Spring Global Strategy Outlook

Volatility – VIX, Volatility in EM Equities, Nasdaq, US 5yr, EUR and JPY FX crosses all trade near 15-year averages. We think that is a pretty reasonable price for owning volatility in these markets outright as defense in a recessionary backdrop.

Risks to Our View (the Bull & Bear Cases)

The following are not our central scenario, but are realistic enough to address.

The Bull Case

We hear quite a bit that the biggest problem facing the market is that “there is no bull case”. We disagree and provide a plausible scenario below.

Growth – (Another) False Alarm: The market, for all its wisdom, got too bearish on global growth at some point in 2010, 2011, 2012, 2014, and 2015. One has to at least consider the same may be true again. Consumer spending and confidence continue to hold up in the US and Europe on the back of rising employment, fiscal policy is less restrictive at the margin, and US ISM has improved for two straight months. Since 1948, the average 12-month return for the S&P 500 after ISM drops below 50, but there is no recession, is 15.7%.

We think US Banks, European Value stocks, and inflation breakevens offer the best risk-reward if growth fears ebb.

Exhibit 6 ISM Below 50 Doesn’t Always Mean ‘Recession’

Source: Morgan Stanley Research, Bloomberg, NBER, Haver Analytics

The Equity Risk Premium Matters − Downgrades to our growth estimates imply that equities are now less attractive, and bonds more attractive, compared with our year-ahead outlook. The risk is that this is already largely priced in through an unusually large gap in long-run expected returns between the two asset classes (the Equity Risk Premium). Exhibit 7 shows the level of long-run nominal EPS growth that would be required for equities to outperform government bonds by an ‘average’ amount (~400bp p.a.) across regions. The levels are extremely modest. The bull case is that this drives more money toward equities.

Exhibit 7 The Bar for EPS Growth is Low

Note: Annual nominal earnings growth implied by current equity valuations and the actual rates curve plus 400bp premium. Source: Morgan Stanley Research, MSCI, RIMES

The USD has actually peaked – Our base case assumes this is a secular USD bull market that has further to go against DM and EM FX. A more bullish scenario is that the recent USD pause is actually a peak, reducing pressure on EMFX and commodity prices and extending the rotation into value.

The Bear Case

Global recession– Our economists put the probability of global recession at 30%, the highest of this cycle. While the US remains our favored equity market on the theory that it will command a premium in a low-growth, choppy market, its premium could be at risk if a full-blown recession causes the market to sell anything trading at a premium. Buying volatility in US and EM equities, entering IG credit curve flatteners in the US (CDX 5s10s), buying US 5yr receivers and OTM puts on AUD/JPY are all strategies that we think have significant upside in a recession scenario, and limited downside in our base case.

No recession but stocks still de-rate – Even without a recession, equity markets could decide to pay a lower multiple given the difficult macro. We are most concerned about de-rating in EU Insurance, US Tech, and Global Staples.

Central banks misread markets – We view negative rates as an unhelpful and ineffective policy tool. A key risk is that policymakers think the policy is misunderstood and simply needs more time. Even if growth doesn’t tip into recession, more rate cuts exceeding market expectations could push risk markets lower, in our view.

Currency & growth risks in Asia − In our base case China is able to stabilize near-term growth with fiscal and monetary stimulus. In our bear case, that fails, increasing the risk of a larger currency adjustment. That scenario could also pose risks to Japan, where our forecasts are already materially below consensus and fiscal and monetary tools look limited.

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

30

40

50

60

70

80

1948 1958 1968 1978 1988 1998 2008

Mfg PMI

2.42.1

1.5

3.2

1.9

1.3

0.3

2.6

1.9

0.2

0.0

1.9

-0.50.00.51.01.52.02.53.03.5

US Europe Japan EM ($)

(%) Implied Growth (Nov-15)Implied Growth (Today)Current Bond Yield (10yr)

M O R G A N S T A N L E Y R E S E A R C H

7

March 13, 2016 Spring Global Strategy Outlook

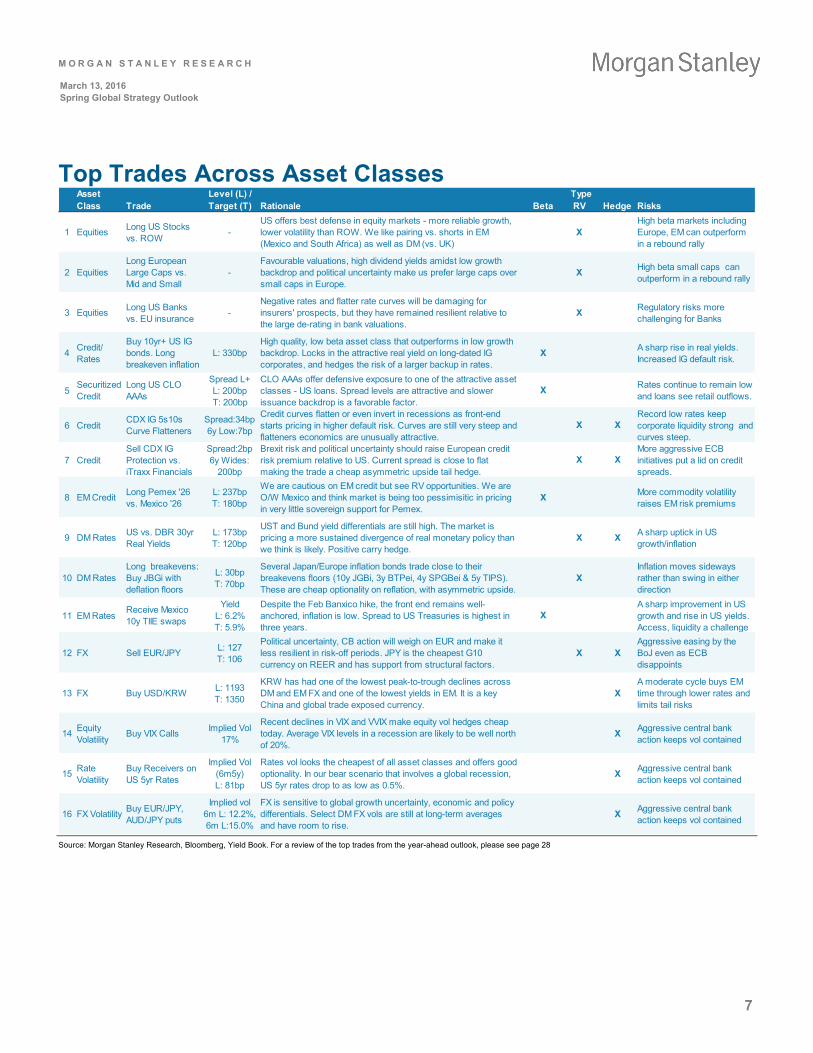

Top Trades Across Asset Classes

Source: Morgan Stanley Research, Bloomberg, Yield Book. For a review of the top trades from the year-ahead outlook, please see page 28

Level (L) /Trade Target (T) Rationale Beta RV Hedge Risks

1 Equities Long US Stocks vs. ROW

-US offers best defense in equity markets - more reliable growth, lower volatility than ROW. We like pairing vs. shorts in EM (Mexico and South Africa) as well as DM (vs. UK)

XHigh beta markets including Europe, EM can outperform in a rebound rally

2 EquitiesLong European Large Caps vs. Mid and Small

-Favourable valuations, high dividend yields amidst low growth backdrop and political uncertainty make us prefer large caps over small caps in Europe.

X High beta small caps can outperform in a rebound rally

3 Equities Long US Banks vs. EU insurance

-Negative rates and flatter rate curves will be damaging for insurers' prospects, but they have remained resilient relative to the large de-rating in bank valuations.

X Regulatory risks more challenging for Banks

4 Credit/ Rates

Buy 10yr+ US IG bonds. Long breakeven inflation

L: 330bp High quality, low beta asset class that outperforms in low growth backdrop. Locks in the attractive real yield on long-dated IG corporates, and hedges the risk of a larger backup in rates.

X A sharp rise in real yields. Increased IG default risk.

5Securitized Credit

Long US CLO AAAs

Spread L+ L: 200bp T: 200bp

CLO AAAs offer defensive exposure to one of the attractive asset classes - US loans. Spread levels are attractive and slower issuance backdrop is a favorable factor.

X Rates continue to remain low and loans see retail outflows.

6 CreditCDX IG 5s10s Curve Flatteners

Spread:34bp 6y Low:7bp

Credit curves flatten or even invert in recessions as front-end starts pricing in higher default risk. Curves are still very steep and flatteners economics are unusually attractive.

X XRecord low rates keep corporate liquidity strong and curves steep.

7 CreditSell CDX IG Protection vs. iTraxx Financials

Spread:2bp 6y Wides:

200bp

Brexit risk and political uncertainty should raise European credit risk premium relative to US. Current spread is close to flat making the trade a cheap asymmetric upside tail hedge.

X XMore aggressive ECB initiatives put a lid on credit spreads.

8 EM Credit Long Pemex '26 vs. Mexico '26

L: 237bp T: 180bp

We are cautious on EM credit but see RV opportunities. We are O/W Mexico and think market is being too pessimisitic in pricing in very little sovereign support for Pemex.

X More commodity volatility raises EM risk premiums

9 DM Rates US vs. DBR 30yr Real Yields

L: 173bp T: 120bp

UST and Bund yield differentials are still high. The market is pricing a more sustained divergence of real monetary policy than we think is likely. Positive carry hedge.

X X A sharp uptick in US growth/inflation

10 DM RatesLong breakevens: Buy JBGi with deflation floors

L: 30bp T: 70bp

Several Japan/Europe inflation bonds trade close to their breakevens floors (10y JGBi, 3y BTPei, 4y SPGBei & 5y TIPS). These are cheap optionality on reflation, with asymmetric upside.

XInflation moves sideways rather than swing in either direction

11 EM RatesReceive Mexico 10y TIIE swaps

Yield L: 6.2% T: 5.9%

Despite the Feb Banxico hike, the front end remains well-anchored, inflation is low. Spread to US Treasuries is highest in three years.

XA sharp improvement in US growth and rise in US yields. Access, liquidity a challenge

12 FX Sell EUR/JPY L: 127 T: 106

Political uncertainty, CB action will weigh on EUR and make it less resilient in risk-off periods. JPY is the cheapest G10 currency on REER and has support from structural factors.

X XAggressive easing by the BoJ even as ECB disappoints

13 FX Buy USD/KRW L: 1193 T: 1350

KRW has had one of the lowest peak-to-trough declines across DM and EM FX and one of the lowest yields in EM. It is a key China and global trade exposed currency.

XA moderate cycle buys EM time through lower rates and limits tail risks

14 Equity Volatility

Buy VIX Calls Implied Vol 17%

Recent declines in VIX and VVIX make equity vol hedges cheap today. Average VIX levels in a recession are likely to be well north of 20%.

X Aggressive central bank action keeps vol contained

15 Rate Volatility

Buy Receivers on US 5yr Rates

Implied Vol (6m5y) L: 81bp

Rates vol looks the cheapest of all asset classes and offers good optionality. In our bear scenario that involves a global recession, US 5yr rates drop to as low as 0.5%.

X Aggressive central bank action keeps vol contained

16 FX Volatility Buy EUR/JPY, AUD/JPY puts

Implied vol 6m L: 12.2%, 6m L:15.0%

FX is sensitive to global growth uncertainty, economic and policy differentials. Select DM FX vols are still at long-term averages and have room to rise.

X Aggressive central bank action keeps vol contained

Asset Class

Type

M O R G A N S T A N L E Y R E S E A R C H

8

March 13, 2016 Spring Global Strategy Outlook

Global Equities: Sell the Recent Rally Jonathan Garner Asia/ GEMs Adam S. Parker, Ph.D. United States Graham Secker Europe

The bottom line is that we are sellers of the recent rally, which has seen MSCI ACWI rise 9% since the trough on 11th February, reversing 80% of the losses year to date. Our new 12-month forward base, bull and bear case target prices are given in Exhibit 1 together with our prior forecasts. We see downside to the base case in EM and only very limited upside in the US, Japan and Europe.

Exhibit 1 Revised and Previous Bull, Base and Bear Targets for Major Regions

Source: MSCI, Rimes, Bloomberg, Morgan Stanley Research forecasts. Data as of March 10, 2016

Revisions to our house macro view are unequivocally negative versus the scenarios for 2016 and 2017 published in our prior year-ahead update in late November. Most notably, our base case forecast for 3.0% global GDP growth in 2016 is

below that in 2015, and we also look for a more muted recovery to 3.4% in 2017. Our FX team continues to expect the US dollar to strengthen and is today revising its yen forecast to expect a near-term acceleration of the recent trend to yen appreciation. Our commodities teams do not expect a sustained recovery in oil and base metals, and our rates team expects yields to move lower in the short to medium term.

Factoring in this macro view, recent trends in earnings announcements, and the other components of our earnings models, we anticipate that earnings will decline yoy in 2016 versus 2015 in EM, Europe and Japan, rising only modestly in the US (see Exhibit 3).

We are significantly below bottom-up consensus on earnings cumulatively to end 2017 in all four major regions: by 6% for the US, 8% for Europe, 16% for Japan, and 19% for EM. We are marginally above consensus for US earnings in 2016 but below consensus elsewhere. Only in the US do we see ROE stabilizing through the end of 2016. Elsewhere we expect further declines, although some improvement is likely as we head into 2017.

Exhibit 2 Trailing ROE for Major Regions with MS forecasts for 2016 and 2017 – No Inflexion Point in Sight Near term

Source: MSCI, Rimes, Morgan Stanley Research. Data as of March 9, 2016

In terms of our multiple assumptions, we have brought our 12m forward PE target down from 16.5x to 16.0x for the S&P 500, from 15.0x to 14.0x for Europe, and from 14.4x to 14.0x for Japan. We have left our base case multiple target unchanged for EM at 11.6x. The start of the Fed hike cycle has coincided with a reduction in consensus forward PE multiples globally, as we discussed in our year-ahead piece. But this has occurred to a greater extent than we anticipated in DM equities, particularly in Japan. We note that the current forward PE multiple on consensus estimates is somewhat

Bear Base Bull Bear Base Bull1525 2050 2200 1600 2175 2425

-23.4% 3.0% 10.6% -19.6% 9.3% 21.9%925 1,300 1,665 1100 1500 1720

-29.7% -1.2% 26.6% -16.4% 14.0% 30.8%915 1400 1780 1230 1640 1880

-32.3% 3.6% 31.6% -9.0% 21.3% 39.0%500 735 960 590 850 980

-36.7% -7.1% 21.4% -25.4% 7.5% 23.9%

MSCI Europe 1315

TOPIX 1352

MSCI EM 791

Index Current Price

New Target Price Old Target Price

S&P 500 1990-5%

0%

5%

10%

15%

20%

25%

1996 2001 2006 2011 2016

Trailing ROE for Major Regions TOPIXMSCI EMMSCI APxJMSCI EuropeS&P 500

MS Forecasts

Key Investment Ideas • We are sellers of the recent rally. There is downside to

our 12m forward Base Case Target Prices for EM (-7%) and Europe (-1%), and only modest upside for the US (+3%) and Japan (+4%).

• Earnings will likely decline yoy in 2016 versus 2015 in EM (-7%), Europe (-4%) and Japan (-6%), rising only in the US (+4%). We are significantly below consensus earnings estimates for 2017 in all regions (more so in EM and Japan than in Europe and US).

• Most preferred to least preferred: US (1), Japan (2), Europe (3) & EM (4) on our risk-adjusted returns forecast.

• We favour high FCF yield and dividend yield names globally and identify where our sector and style preferences differ between regions.

Equities – +USEuropeJapanAPxJEM

M O R G A N S T A N L E Y R E S E A R C H

9

March 13, 2016 Spring Global Strategy Outlook

below our new base case assumptions in EM and Japan, broadly in line for the SPX, and somewhat above for Europe.

Our bear case target prices are materially lower than before, reflecting our economics team’s revised bear case scenario (20% probability) of a two-year slump in global economic activity through both 2016 and 2017, and hence a more material decline in earnings in the bear case than envisaged previously. Our bull case target prices are reduced to a lesser degree.

Exhibit 3 MS Top-down EPS Estimates and Bull, Bear and Base Case PE Targets versus Consensus

Source: MSCI, Rimes, Morgan Stanley Research forecasts

Contextualising the current earnings recession

Equities globally are now in an earnings recession, which in our base case continues almost everywhere except the US, where we forecast a modest recovery. In aggregate, MSCI ACWI earnings peaked in US$ terms in August 2014 and have since declined by 11%, whilst in local currency terms earnings peaked in February 2015 and have since declined by 6%. Exhibit 4 contextualises the current earnings recession versus the 6 prior such earnings recessions in MSCI World since 1970 and 3 prior episodes in EM since 1995. The current earnings recession is already the longest in the history of EM at 27 months, although its depth thus far is on par with the relatively mild 2001/02 experience. Our forecast is that it continues over at least the next 12 months. For DM, the earnings recession is also relatively shallow thus far – and not particularly long lived at just 13 months’ duration.

Exhibit 4 Historical Precedents of MSCI World and MSCI EM Earnings Recessions (Local Currency Terms)

Source: MSCI, Rimes, Morgan Stanley Research. Data as of March 9, 2016

What’s in the Price?

We do not view current global equity valuations as particularly cheap to history or priced attractively in relation to our base or bear case outlooks. For MSCI ACWI, valuations across a range of metrics are in line to marginally above long-run average levels since 1988 (see Exhibit 5). On a consensus forward PE basis for all four major regions, valuations are well above 5-year average levels, although that period does include the lengthy Eurozone sovereign crisis.

Exhibit 5 MSCI AC World – Absolute Valuations vs History for the Market and the Median stock – Slightly Above the Long-term Average on Most Metrics

Source: MSCI, IBES, FactSet, Worldscope, Morgan Stanley Research. *Note: All data used starts from Jan-1988. Data as of March 9, 2016

2015 2016 2017 Mar-18 2016 2017

118.5 122.7 127.1 128.1 119.0 134.9-0.7% 3.6% 3.6% 4.0% 2.0% 13.4%86.8 82.9 90.9 92.7 88.6 99.9

-4.5% -4.5% 9.6% 9.3% 3.9% 12.8%91.8 86.4 96.3 100.4 103.6 113.45.9% -5.9% 11.5% 19.4% 12.4% 9.5%58.4 54.4 61.3 63.3 65.1 75.0

-18.9% -6.8% 12.7% 12.8% 6.4% 15.2%118.5 125.1 132.1 133.1 119.0 134.9-0.7% 5.6% 5.6% 6.0% 2.0% 13.4%87.2 91.4 107.5 110.5 88.6 99.9

-4.0% 4.7% 17.7% 12.9% 3.9% 12.8%91.8 103.5 121.0 125.7 103.6 113.45.9% 12.7% 16.9% 17.6% 12.4% 9.5%58.4 65.8 77.3 79.9 65.1 75.0

-18.9% 12.7% 17.5% 16.3% 6.4% 15.2%118.5 110.6 105.5 104.9 119.0 134.9-0.7% -6.6% -4.6% -5.0% 2.0% 13.4%86.3 74.5 69.8 71.9 88.6 99.9

-5.0% -13.7% -6.3% -2.0% 3.9% 12.8%91.8 80.2 71.8 70.5 103.6 113.45.9% -12.6% -10.5% -7.0% 12.4% 9.5%58.4 48.5 44.9 45.5 65.1 75.0

-18.9% -17.0% -7.4% -4.3% 6.4% 15.2%

BEA

R C

ASE

S&P 500 14.5x 14.2x 16.1x

MSCI Europe 13.0x 12.5x 14.7x

TOPIX 13.0x 13.2x 12.6x

MSCI EM 11.0x 10.4x

10.4x 11.7x

11.7x

12.0x 10.4x 11.7x

BU

LL C

ASE

S&P 500 16.5x 14.2x 16.1x

MSCI Europe 15.0x 12.5x 14.7x

TOPIX 14.2x 13.2x 12.6x

MSCI EM

Consensus 12m Fwd

P/E Current

BA

SE C

ASE

S&P 500 16.0x 14.2x 16.1x

MSCI Europe 14.0x 12.5x 14.7x

TOPIX 14.0x 13.2x 12.6x

MSCI EM 11.6x

IndexMS Top-Down EPS / YoY % Consensus EPS /

YoY %MS Fwd

P/EMar-17

Consensus Fwd P/E5Y Avg

# EPS decline (%) since peak level Date of Peak Date of Trough # of months of EPS

decline since peak

1 -21.5% Sep-74 Jan-76 162 -20.7% Sep-80 May-83 323 -34.9% Aug-89 Jun-93 464 -9.6% Apr-98 Jun-99 145 -38.3% Feb-01 Sep-02 196 -59.7% Nov-07 Jan-10 267 -5.7% Feb-15 ? 13

# EPS decline (%) since peak level Date of Peak Date of Trough # of months of EPS

decline since peak

1 -56.2% Jan-98 Jun-99 172 -14.1% Aug-01 Jul-02 113 -39.3% Oct-08 Nov-09 134 -14.3% Dec-13 ? 27

MSCI WORLD

MSCI EM

Latest Avg Median Max MinTrailing Price / Earnings 20.7 20.6 20.3 45.9 11.8 0.0 1.9 52Trailing Dividend Yield (%) 2.8 2.4 2.4 4.3 1.4 -1.0 -19.7 12Trailing Price / Book Value 2.0 2.2 2.3 4.1 1.3 -0.7 -12.3 25Trailing Price / Cash Earnings 9.7 9.5 9.8 17.5 5.3 0.1 -0.4 49Trailing Price / Sales 1.3 1.0 1.1 1.9 0.6 1.0 22.7 85Trailing EV / Sales 1.6 1.3 1.4 2.3 0.9 0.9 16.2 83Trailing EV / EBITDA 10.1 8.9 9.0 15.0 6.0 0.7 12.0 79Trailing EV / EBIT 16.8 14.5 14.6 25.4 9.0 0.7 15.0 74N12M Price / Earnings 14.8 14.6 14.7 25.5 5.6 0.0 0.7 54

Trailing Price / Earnings 20.0 19.1 19.6 29.0 10.9 0.3 2.1 58Trailing Dividend Yield (%) 2.3 2.0 1.9 3.4 1.5 -1.0 -20.7 17Trailing Price / Book Value 2.0 1.9 2.0 2.8 1.3 0.2 2.1 60Trailing Price / Cash Earnings 11.3 9.8 10.2 12.8 5.8 0.8 10.9 80Trailing Price / Sales 1.6 1.1 1.1 1.7 0.7 1.6 49.1 98Trailing EV / Sales 2.0 1.4 1.4 2.1 1.0 1.6 42.1 99Trailing EV / EBITDA 11.2 9.4 9.5 11.8 6.3 1.3 17.8 96Trailing EV / EBIT 17.1 14.8 15.2 19.6 9.3 0.9 12.6 84N12M Price / Earnings 15.6 14.6 15.1 19.4 9.1 0.5 3.3 65

AVERAGE 0.4 8.6 65

Med

ian

Stoc

k

Versus History*Standard

Deviations vs Avg

% From

Median

%ile vs Historical

Range

Mar

ket

M O R G A N S T A N L E Y R E S E A R C H

10

March 13, 2016 Spring Global Strategy Outlook

Exhibit 6 illustrates the implied percent upside to MSCI ACWI equities on a 12M view. A reading of 0% suggests a combination of 12M forward PE and EPS growth that the market can be assumed to be currently discounting for. For example, the current consensus 12M forward PE is 15.0x. Were that to apply in March 2017, we can say that the market today is priced for a -1% US$ return if earnings grow at a +2%US$ EPS CAGR. This is closest to our base case scenario mapping across to MSCI ACWI our four regional index targets (they account for around 93% of MSCI ACWI).

Exhibit 6 Implied % Upside/Downside to MSCI ACWI Equities on a 12M View Under Different EPS Growth and PE Assumptions – Highlighting our Bull, Base and Bear scenarios

Source: MSCI, IBES, FactSet, Worldscope, Morgan Stanley Research. Data as of March 9, 2016

How do we make money in equities for the remainder of 2016?

Given our shift to an overall Underweight stance on equities, the question is how should clients position to make money for the remainder of 2016? We approach this question in three ways: a) regional selection; b) factor efficacy analysis on a global basis; and c) key sector and style picks between regions. (Our various regional and country stock focus lists offer up-to-date ideas at the stock level).

Regional preferences: 1) US, 2) Japan, 3) Europe, 4) EM

At the regional level we rank US first, followed by Japan, Europe, and EM. This rank order flows from the risk-adjusted returns forecast in Exhibit 7. On an information ratio basis (forecast base case return divided by the forecast deviation between the bull and bear case) the US scores best, just ahead of Japan, and Europe and EM worst (see Exhibit 7). Japan outscores Europe by a clear margin. The house FX forecast of one-year forward euro weakness and yen strength versus the US dollar favours Europe to outperform Japan. However, Europe has major idiosyncratic negatives in the forecast horizon, including the upcoming Brexit referendum at

the end of June and macro uncertainties to the base case surrounding the potential breakdown of the Schengen agreement for borderless travel within Europe. Japan arguably has potential idiosyncratic positive catalysts on the horizon. These include a larger than consensus supplementary budget and corporate tax cut and the possibility that Prime Minister Abe calls a snap election to propose delaying the second consumption tax hike due in early 2017. In our base case we assume the consumption tax hike goes ahead.

Exhibit 7 MS Risk-adjusted Returns for Regional Indices

Source: MSCI, Rimes, Morgan Stanley Research forecasts. Data as of March 10, 2016.

The state of the world where our regional hierarchy would most go awry would be if China’s growth rebounds on a sustained basis in 2H 2016, whilst the US economy slows materially in the run-up to the next Presidential election. Commodity prices would recover sustainably in this scenario, whilst the US dollar would likely weaken, in particular versus the CNY.

Factor efficacy – continue to focus on dividend yield and FCF yield

Exhibit 8 explores changes year-to-date in factor efficacy by region in driving one-month YTD returns versus full year 2015. The data is sorted for Quintile 1 less Quintile 5 performance in relation to a range of valuation, earnings revisions, price momentum and other factors. We think there are key lessons to be learned regarding what is “working” so far this year, which can be integrated with our overall macro and asset class views elsewhere in this document to drive successful strategies in equities.

Most notable in our view are the strong returns to the normalized PE, historical FCF yield, and dividend yield factors year to date across the major regions. In contrast, high ROE − although it has worked well in the US and to a lesser extent in Europe − has underperformed recently in Japan, APxJ and EM. Estimate revisions breadth has been choppy. Price momentum and sales growth have had the most negative returns of all the factors analysed across the major regions in the last two months. Our top-down economic view sees further pressures on growth for the remainder of the year,

-10 -8 -6 -4 -2 0 2 4 6 8 1011.0 -44 -41 -38 -36 -33 -30 -27 -25 -22 -19 -1611.5 -41 -38 -36 -33 -30 -27 -24 -21 -18 -15 -1212.0 -38 -36 -33 -30 -27 -24 -21 -18 -15 -11 -812.5 -36 -33 -30 -27 -24 -21 -18 -14 -11 -8 -413.0 -33 -30 -27 -24 -21 -18 -14 -11 -7 -4 013.5 -31 -28 -24 -21 -18 -14 -11 -7 -4 0 414.0 -28 -25 -22 -18 -15 -11 -8 -4 0 4 714.5 -26 -22 -19 -15 -12 -8 -4 -1 3 7 1115.0 -23 -19 -16 -12 -9 -5 -1 3 7 11 1515.5 -20 -17 -13 -9 -6 -2 2 6 10 15 1916.0 -18 -14 -10 -6 -3 1 6 10 14 18 2316.5 -15 -11 -8 -4 0 5 9 13 18 22 2717.0 -13 -9 -5 -1 4 8 12 17 21 26 30

MSCI ACWI Price Up/Downside

2Y EPS CAGR (%)

12M Fwd PE In Mar-

17

Bear Case : -30% downside; PE: 13.6x; EPS CAGR: -8%

Bull Case : +17% upside; PE: 15.3x; EPS CAGR: +9%

Base Case : -1% downside; PE: 14.7x; EPS CAGR: +3%

Category S&P 500 MSCI Europe TOPIX MSCI EMBase Case Price Target Upside (%) 3.0% -1.2% 3.6% -7.1%

Historical Annualized Volatility (%)

15.1% 17.5% 23.7% 19.1%

Bull-Bear Skew 33.9% 56.3% 63.9% 58.1%

Base Case PT Upside / Bull-Bear Skew

0.09 -0.02 0.06 -0.12

M O R G A N S T A N L E Y R E S E A R C H

11

March 13, 2016 Spring Global Strategy Outlook

whilst our rates strategists expect bond yields to move lower near term – with the US 10-year troughing at 1.45% in Q3 before only gently rising thereafter. This suggests to us that investors should continue to focus on FCF and dividend yield over sales growth and ROE as factors going forward.

Exhibit 8 Factor Efficacy Year to Date 2016 versus 2015 for Major Global Equity Regions (Quintile1-Quintile5 Monthly Return Spread)

Source: MSCI, Rimes, Morgan Stanley Research

Exhibit 9 screens for our leading ideas with high historical FCF yields from amongst the universe of large-cap stocks (over US$10bn market cap) rated Overweight by MS analysts in each region.

Exhibit 9 Global Stock Ideas with High FCF Yields

Note: For important disclosures and valuation methodology and risks, please see disclosures at the end of this report. Source: Morgan Stanley Research, Bloomberg. Data as of March 9, 2016

Sector and Style Preferences between Regions

Our final key sector and style preferences between regions have been discussed separately in prior reports but are summarized for convenience in Exhibit 10. Within the defensive sectors we prefer Utilities in the US and EM but prefer Telcos and Healthcare in Europe and Staples in Japan. Within the growth sectors we prefer Consumer Discretionary over IT in the US and Japan but prefer IT over Consumer Discretionary in Europe and EM. (This to a significant degree reflects divergence in business models within the hetereogenous IT sectors across geographies). Within the macro-variable dependent sectors we broadly disfavor Materials except in Europe. In EM and Japan we are positive Real Estate over other financial sectors. In the US we are more positive financials than elsewhere (but with a skew to specific themes such as the US credit card companies). We are generally cautious Energy.

Exhibit 10 Sector and Style Preferences Between Regions

Source: Morgan Stanley Research

PeriodNorth

America Europe Japan APxJ & EMAsia ex. Japan

Normalized P/E Avg 2015 (0.5%) (1.4%) 0.2% (0.7%) (0.7%)Jan 2016 3.9% 1.6% 2.1% 3.1% 3.0%Feb 2016 3.0% 2.7% 1.7% 3.4% 2.7%

FCF Yield Avg 2015 0.5% 0.8% (0.2%) 0.3% 0.4%Jan 2016 5.1% 1.2% 1.9% 3.7% 4.4%Feb 2016 3.0% 2.4% 1.5% 1.3% 2.0%

Dividend Yield Avg 2015 (0.8%) (1.2%) 0.3% (0.0%) 0.1%Jan 2016 0.9% 1.6% 1.1% 2.4% 3.6%Feb 2016 1.7% 0.8% 2.5% 4.2% 4.4%

Buyback Yield Avg 2015 0.6% 0.2% (0.0%) (0.3%) (0.6%)Jan 2016 3.1% 2.7% (0.2%) 2.5% 3.8%Feb 2016 1.2% 1.3% 0.6% 1.0% 1.2%

Capex-to-Depreciation Avg 2015 (0.1%) 0.6% (0.5%) 0.6% 0.7%

Jan 2016 1.9% 0.6% 1.3% 1.2% 1.7%Feb 2016 0.6% 0.7% 0.7% (0.7%) (1.0%)

Accruals Avg 2015 0.1% (0.2%) (0.5%) 0.9% 0.8%Jan 2016 0.3% 2.0% 2.6% 1.6% 1.2%Feb 2016 0.3% 1.5% 0.6% 1.9% 2.0%

ROE Avg 2015 0.8% 1.1% (0.1%) 0.3% 0.2%Jan 2016 5.8% 2.6% (1.2%) 3.0% 3.3%Feb 2016 1.3% 0.4% (2.9%) (1.0%) (1.2%)

Net Margin Z-score

Avg 2015 0.9% 1.5% 0.1% 0.8% 0.8%

Jan 2016 1.3% (0.5%) 0.5% 0.1% 0.6%Feb 2016 (1.2%) (2.5%) (2.5%) (2.3%) (2.3%)

YoY Sales Growth

Avg 2015 (0.0%) 1.2% (0.2%) 0.4% 0.2%

Jan 2016 (2.4%) (0.1%) (2.2%) 1.3% 1.4%Feb 2016 (3.1%) (1.8%) (3.2%) (3.4%) (3.3%)

9-M. Price Momentum Avg 2015 1.8% 1.6% (0.6%) 1.2% 1.0%

Jan 2016 1.2% 2.7% 1.8% 1.6% 1.9%Feb 2016 (2.5%) (1.7%) (3.1%) (3.1%) (2.9%)

Up vs. Down Revisions

Avg 2015 0.6% 0.7% (0.5%) 1.0% 0.7%

Jan 2016 (1.5%) 0.8% 3.6% 2.9% 2.4%Feb 2016 (1.6%) (0.7%) 0.2% (0.8%) (0.8%)

Stocks Share price, last Country GICS sector Stock

ratingMcap in USD Bn

FY2016 Div Yield

FY2016 FCF Yield

Delta Air Lines Inc 47 USA Industrials OW 37.8 1.5% e 14.5% eQualcomm Inc 52 USA IT OW 78.4 3.7% e 9.7% eLyondellbasell Industries Nv 83 USA Materials OW 34.6 3.9% e 9.0% e

Intl Airlines Group 7 Spain Industrials OW 15.5 4.5% e 9.3% eITV 233 UK Cons Disc. OW 13.6 3.1% e 6.7% eImperial Brands 3,690 UK Cons Staples OW 50.9 4.3% e 6.6% e

Sony 2,632 Japan Cons Disc. OW 22.2 2.1% e 27.8% eToyota Motor 5,972 Japan Cons Disc. OW 162.7 4.2% e 9.7% eNTT 4,904 Japan Telecom Services OW 89.3 2.5% e 9.4% e

Korea Electric Power 57,300 S. Korea Utilities OW 30.7 5.1% e 10.0% eInfosys Limited 1,177 India IT OW 38.0 3.0% e 6.6% eChunghwa Telecom 105 Taiwan Telecom OW 24.8 5.5% e 6.0% e

S&P 500

MSCI Europe

TOPIX

MSCI EM

S&P 500 MSCI Europe TOPIX MSCI EM

Defensive Sectors

Utilities Over Consumer

Staples

Telcos and Health Care over Utilities

and StaplesStaples over Utilities Utilities over

Staples

Growth Sectors

Consumer Discretionary

Over IT

Industrials and IT over Consumer Discretionary

Consumer Discretionary over IT

IT over Consumer

Discretionary

Macro-variable dependent Sectors

Financials Over Energy and Materials

Banks over EnergyReal Estate over

Materials

Real Estate over Energy and Materials

Style Preference

Mega/Large Cap, Modest Growth

Bias

Large-caps, High & Secure Dividend

Yield

Shareholder Rewards and Corporate Governance

Best Business Models

(Quality)

M O R G A N S T A N L E Y R E S E A R C H

12

March 13, 2016 Spring Global Strategy Outlook

Global Government Bonds: Year of the BullMatthew Hornbach United States Anton Heese Europe Koichi Sugisaki Japan

The global backdrop for rates markets looks so supportive that 2016 may become known as the ‘Year of the Bull’. Indeed, the year got off to a very bullish start. Our economists forecast below-consensus growth and inflation across most of the developed and emerging world. They are telling us that the global economy will no longer accelerate in 2016, and most major economies will perform worse in 2016 than in 2015. And, as a result, the ECB and BoJ will keep easing policy and the BoE and Fed will push rate hikes further out. At this point, our economists expect the ECB and BoJ to continue with their negative interest rate policies (NIRP) – an ominous sign for risk sentiment.

To make the outlook for rates markets more bullish, our China experts suggest that the PBoC will eventually guide the trade-weighted renminbi weaker such that USD/CNY will end 2016 at 6.93 (+6% from spot) and end 2017 at 7.30 (+12% from spot). That compares with the 5% appreciation in USD/CNY since August 10, 2015 – the day before the PBoC altered its currency regime. The combination of a continued slowdown in China and NIRP in the developed world makes it easier to see developed sovereign bond yields remaining low – and at some point going lower. In this context, we lowered our forecasts for yields in the US and the UK, in the euro area and Japan. Over the next 12 months, we have sovereign yields falling to local lows in 3Q16 before rebounding higher.

By the end of 1Q17, we have 10-year UST yields roughly unchanged versus spot, 10-year DBR and UKT yields slightly

higher than spot, and 10-year JGB yields slightly lower than spot.

• In the US, our economists look for the Fed to delay its next rate hike until the December 2016 FOMC meeting – a big change from their previous expectation of three hikes this year. Our economists expect quarterly real GDP growth to stay below 2.0% through 2017. Annual growth in 2016 and 2017, 1.7% and 1.6% on their forecasts respectively, represents a notable downshift from 2.4% Y/Y growth in 2015. Our economists also expect core PCE inflation at 1.4% to miss the Fed’s median projection of 1.6% Q4/Q4 in 2016, as the Y/Y rate inflects downward in 2Q16. With the Fed hiking again, but only in December, policy plays out in 2016 much like in 2015. We expect a mid-year rally to take 10y Treasury yields down to 1.45% − a new cycle low – by the end of 3Q16. 2-year yields re-test the 0.60% level at the same time, but rebound more strongly as the next rate hike approaches in December. By year-end, the 2s10s curve flattens to 0.80% from 1.00% spot and versus the forward at 0.84%. The marginal pickup vs. forwards means playing the yield curve continues to offer little reward for the risk, so we continue to focus on duration over curve.

• In Euro, further ECB easing is well anticipated by the market but the weak inflation and faltering growth outlook means we expect 2y rates to remain well anchored around current levels (-50 to -60bp). We expect longer maturities to trade directionally with global rates, but with a lower beta because investor demand is likely to be impaired if yields fall further while the expansion of the ECB purchase program is likely to moderate any sell-off. Short-dated inflation breakevens remain very cheap, but the risk is that they remain cheap as long as the realized inflation outlook is weak. We expect a modest tightening of sovereign spreads in the short term, due to the ramping up of QE purchases, but are concerned about political risks and slightly weaker growth over the next 12 months, so that we forecast generally flat spreads.

• In the UK, the binary risk around the EU referendum will keep the rates outlook uncertain until the end of June. Assuming our base case of the UK staying in the EU is realized, we expect gilts to largely trade in line with USTs, reflecting similar global growth concerns as well as a similar domestic economic outlook. However, as we approach year-end, and the Fed moves to raise rates again, we expect gilts to underperform cross market, as

Key Investment Ideas • We suggest investors go long duration across G4

bond markets over the next six months – a period over which we expect yield curves to bull-flatten by more than forwards in the US and UK. We suggest US and UK 2s10s curve flatteners vs. steepeners in Germany and Japan. For the next 12 months, we prefer 5s30s flatteners in the UK vs. 5s30s steepeners in Germany.

• We think pricing of global breakeven inflation offers investors a compelling opportunity to purchase protection against higher-than-expected inflation outcomes over the coming year. Given downside risks evident in energy markets, we suggest investors purchase linkers with at-the-money deflation floors.

Government Bonds – +TreasuriesBundsJGBsEM Local

M O R G A N S T A N L E Y R E S E A R C H

13

March 13, 2016 Spring Global Strategy Outlook

the market starts to price in the first rate hike our economists forecast in February 2017. The combination of rate hikes being priced in, but still strong demand for duration globally, causes the 2s10s curve to flatten. We expect UK breakevens to remain well supported and trade at a premium to other inflation markets.

• In Japan, our economists expect further rate cuts totaling at least 20bp ahead of the July Upper House election, and have few (if any) concerns about the prospect of BoJ tapering, given that the core CPI inflation rate (excluding fresh foods) looks highly unlikely to climb near 2.0% by 2017. Thus, we expect that the JGB market will continue to be driven mostly by supply/demand and BoJ rate cut speculation. NIRP has effectively eliminated the ‘floor’ for short- to medium-term yields, for which reason the balance of risks to JGB rates is probably weighted to the downside. Thus, we lowered our yield forecast significantly with the 10y yield falling to around -0.2% by 1Q17. We expect the JGB curve to bull-steepen through the 10y sector and bull-flatten through the super-long end. The super-long sector is likely to outperform on the curve, as domestic investors looking to avoid negative yields take on greater duration risk. We expect the 30y yield to fall to 0.4% in 1Q17.

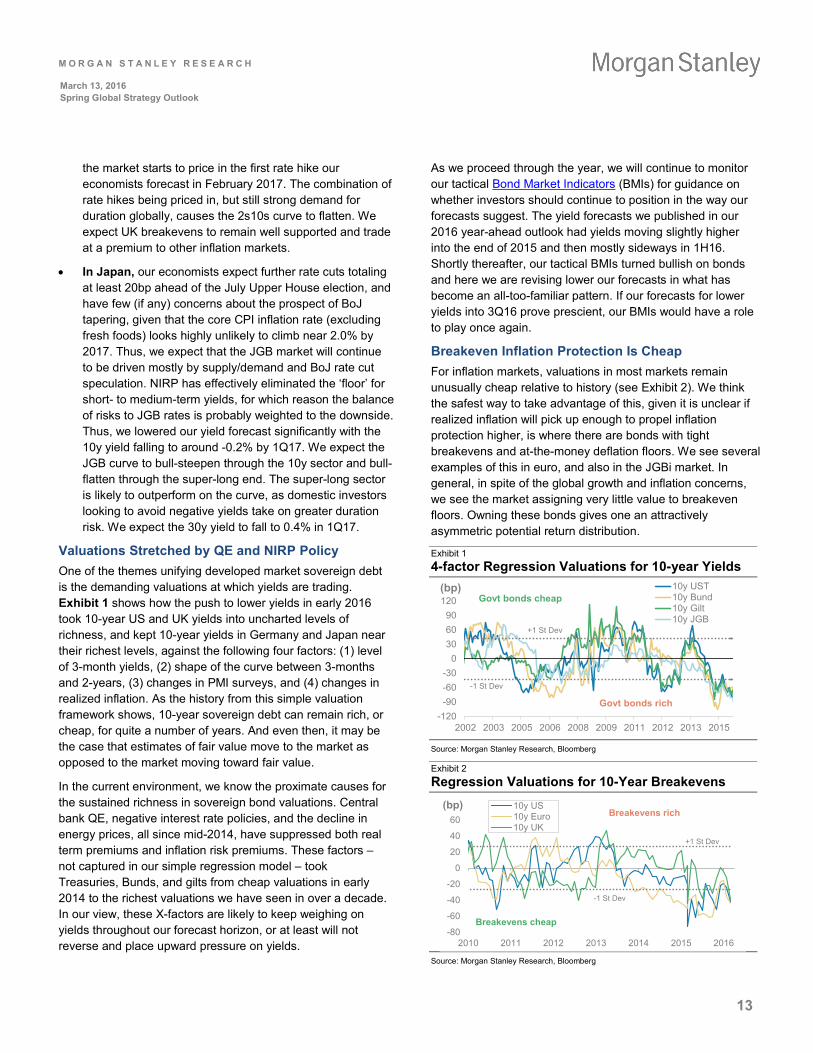

Valuations Stretched by QE and NIRP Policy One of the themes unifying developed market sovereign debt is the demanding valuations at which yields are trading. Exhibit 1 shows how the push to lower yields in early 2016 took 10-year US and UK yields into uncharted levels of richness, and kept 10-year yields in Germany and Japan near their richest levels, against the following four factors: (1) level of 3-month yields, (2) shape of the curve between 3-months and 2-years, (3) changes in PMI surveys, and (4) changes in realized inflation. As the history from this simple valuation framework shows, 10-year sovereign debt can remain rich, or cheap, for quite a number of years. And even then, it may be the case that estimates of fair value move to the market as opposed to the market moving toward fair value.

In the current environment, we know the proximate causes for the sustained richness in sovereign bond valuations. Central bank QE, negative interest rate policies, and the decline in energy prices, all since mid-2014, have suppressed both real term premiums and inflation risk premiums. These factors – not captured in our simple regression model – took Treasuries, Bunds, and gilts from cheap valuations in early 2014 to the richest valuations we have seen in over a decade. In our view, these X-factors are likely to keep weighing on yields throughout our forecast horizon, or at least will not reverse and place upward pressure on yields.

As we proceed through the year, we will continue to monitor our tactical Bond Market Indicators (BMIs) for guidance on whether investors should continue to position in the way our forecasts suggest. The yield forecasts we published in our 2016 year-ahead outlook had yields moving slightly higher into the end of 2015 and then mostly sideways in 1H16. Shortly thereafter, our tactical BMIs turned bullish on bonds and here we are revising lower our forecasts in what has become an all-too-familiar pattern. If our forecasts for lower yields into 3Q16 prove prescient, our BMIs would have a role to play once again.

Breakeven Inflation Protection Is Cheap For inflation markets, valuations in most markets remain unusually cheap relative to history (see Exhibit 2). We think the safest way to take advantage of this, given it is unclear if realized inflation will pick up enough to propel inflation protection higher, is where there are bonds with tight breakevens and at-the-money deflation floors. We see several examples of this in euro, and also in the JGBi market. In general, in spite of the global growth and inflation concerns, we see the market assigning very little value to breakeven floors. Owning these bonds gives one an attractively asymmetric potential return distribution.

Exhibit 1 4-factor Regression Valuations for 10-year Yields

Source: Morgan Stanley Research, Bloomberg

Exhibit 2 Regression Valuations for 10-Year Breakevens

Source: Morgan Stanley Research, Bloomberg

-120-90-60-30

0306090

120

2002 2003 2005 2006 2008 2009 2011 2012 2013 2015

(bp) 10y UST10y Bund10y Gilt10y JGB

Govt bonds cheap

Govt bonds rich

+1 St Dev

-1 St Dev

-80

-60

-40

-20

0

20

40

60

2010 2011 2012 2013 2014 2015 2016

(bp) 10y US10y Euro10y UK

Breakevens rich

Breakevens cheap

+1 St Dev

-1 St Dev

M O R G A N S T A N L E Y R E S E A R C H

14

March 13, 2016 Spring Global Strategy Outlook

Global FX: The Bullish JPY, USD and CHF Trio Hans Redeker Global Head of FX Strategy

The Currencies to Buy: JPY, USD and CHF

The JPY remains our currency of the year, with Japan’s strong foreign asset position and pension fund repatriation needs catapulting it higher. Our benign outlook for Japanese foreign risk appetite adds to envisaged JPY strength, overwhelming the efforts of the Bank of Japan to control the appreciation of the JPY. While yen strength has been our call for some time, we have changed our CHF outlook and now expect strength. The ability of Swiss-based portfolio managers to export long-term capital against the current account surplus has diminished. If the risk outlook within the Eurozone remains more negative than elsewhere, we would expect the CHF to strengthen.

The USD completes the main trio of appreciating currencies, supported by continued repatriation demand coming out of EM countries. Since the USD has not converted into an investment currency yet, the Fed’s ability to dampen USD appreciation will remain limited and not go beyond a tactical impact. The strategic USD outlook will remain determined by the poor investment outlook elsewhere in the world and the related increase of non-US savings. The inability to find adequate local investment opportunities for these savings should lead to a permanent flow of funds into the USD. We think the SEK outperforms in Europe, with efforts by the Riksbank to prevent SEK appreciation increasingly lacking credibility as the relative growth outlook becomes stronger.

The Currencies to Sell: EUR

Outside the JPY, CHF, USD and the SEK, it is hard to find a positive currency story. In fact, the outlook has weakened further in some cases, such as GBP and the EUR. Tightening global liquidity conditions, which are the result of falling currency reserves, Japan’s taking funds back into the JPY instead of their previous foreign investments, and an overvalued USD becoming even more overvalued, suggest that creditors will be more selective about where to place funds. Entities with particularly large balance sheets may find it harder to fund exposures under previously lucrative conditions.

Exhibit 1 Major FX Forecasts

Source: Morgan Stanley Research forecasts

We think that FX investors will start to become more worried about the large balance sheets in the European banking sector. In 2011, the EUR and European equities fell simultaneously as EMU’s peripheral sovereign risk outlook caused an asset sell-off. Peripheral banks’ investments put the quality of their balance sheets into doubt, and investors were rattled by a sharp rise of non-performing loans and questioned the ability of peripheral sovereign bonds to provide the backbone for these balance sheets. Back then, it was the asset side that mattered. Regulatory changes and the OMT establishing a quasi ‘lender of last resort’ capacity for the ECB stabilised the situation from July 2012. This time it is not so much the asset outlook that concerns EUR traders. Instead, it is the capacity to fund large balance sheets, the impact on bank credit spreads, and the ability and willingness of banks to provide credit that may send the EUR lower. Concretely, banks cutting balance sheets may tighten their lending standards. Thus, weakening global liquidity conditions may impact monetary velocity the most where balance sheets are still most

2Q16 3Q16 4Q16 1Q17EUR/USD 1.06 1.03 1.00 0.98

Before 1.03 1.01 1.00 0.99GBP/USD 1.45 1.38 1.32 1.30

Before 1.41 1.40 1.40 1.41USD/JPY 110 105 106 108

Before 121 118 115 112USD/INR 71.0 72.0 73.0 73.0

Before 68.5 69.3 70.0 69.0USD/KRW 1280 1310 1350 1350

Before 1260 1280 1300 1280USD/TRY 3.20 3.25 3.35 3.32

Before 3.15 3.20 3.25 3.26

Key Investment Ideas • The JPY, USD and the CHF are expected to rally as

cross-border capital flows ease.

• The anticipated decline in risk appetite suggests to us staying short the EM/commodity FX block.

• Low EM asset returns combined with ambitiously sized balance sheets should increase local savings.

• Failure to find adequate local non-US investment opportunities should lead to capital exports, boosting USD.

• US repatriation demand will likely remain the dominant reason for USD strength.

• We have become more bearish on INR, KRW and GBP and have upgraded our JPY call further.

FX – +USDEURJPYEM

M O R G A N S T A N L E Y R E S E A R C H

15

March 13, 2016 Spring Global Strategy Outlook

ambitious. The recent decline in EMU monetary velocity has come on the heels of tighter global monetary conditions.

Generally, when monetary velocity declines, the central bank should compensate with an adequate increase in base money. The more that money supply growth is driven by the central bank’s pumping base money into the system, instead of via commercial bank lending activities, the more the currency will come under selling pressure. In the case of the EUR, traders and investors need to watch indications of global liquidity conditions and the impact on European bank funding and lending conditions. The more Japan repatriates, global currency reserves fall, and the USD rallies as EM pushes local savings into USD-denominated holdings, the more the EUR is likely to come under selling pressure.

The Currencies to Sell: GBP

The expected decline in the GBP is not only due to Brexit related concerns. Other concerns include a pro-cyclical fiscal policy, the important UK financial sector being challenged by globally low rates, increasing regulation pushing financial sector productivity lower, and a current account deficit fluctuating around 4%. All of this will make it more difficult to fund Britain’s financial needs at current attractive levels, arguing for a lower GBP. Should the UK vote for Brexit on the 23 June, GBP/USD could fall as low as 1.20, taking the EUR with it.

The Currencies to Sell: EMFX

We stay bearish the commodity and EM FX block, but there are some new nuances as weakness moves away from LatAm and high-beta FX and towards AxJ. Against the USD, LatAm currencies may still lose between 8-10%, but after accounting for carry, we think being short AxJ is more attractive. LatAm fundamentals remain weak, and we expect commodity prices to remain soft. However, improved external positions and central bank pushback may mean LatAm currencies are not going to be the underperformers within EM this year.

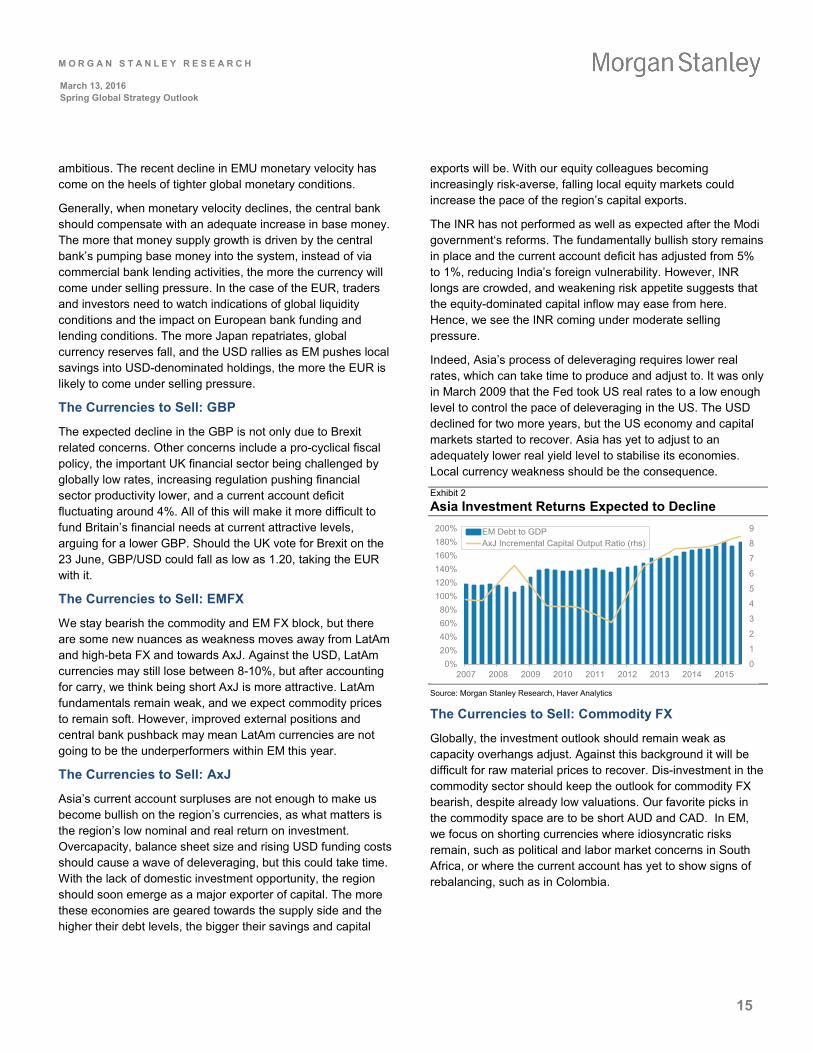

The Currencies to Sell: AxJ

Asia’s current account surpluses are not enough to make us become bullish on the region’s currencies, as what matters is the region’s low nominal and real return on investment. Overcapacity, balance sheet size and rising USD funding costs should cause a wave of deleveraging, but this could take time. With the lack of domestic investment opportunity, the region should soon emerge as a major exporter of capital. The more these economies are geared towards the supply side and the higher their debt levels, the bigger their savings and capital

exports will be. With our equity colleagues becoming increasingly risk-averse, falling local equity markets could increase the pace of the region’s capital exports.

The INR has not performed as well as expected after the Modi government‘s reforms. The fundamentally bullish story remains in place and the current account deficit has adjusted from 5% to 1%, reducing India’s foreign vulnerability. However, INR longs are crowded, and weakening risk appetite suggests that the equity-dominated capital inflow may ease from here. Hence, we see the INR coming under moderate selling pressure.

Indeed, Asia’s process of deleveraging requires lower real rates, which can take time to produce and adjust to. It was only in March 2009 that the Fed took US real rates to a low enough level to control the pace of deleveraging in the US. The USD declined for two more years, but the US economy and capital markets started to recover. Asia has yet to adjust to an adequately lower real yield level to stabilise its economies. Local currency weakness should be the consequence.

Exhibit 2 Asia Investment Returns Expected to Decline

Source: Morgan Stanley Research, Haver Analytics

The Currencies to Sell: Commodity FX

Globally, the investment outlook should remain weak as capacity overhangs adjust. Against this background it will be difficult for raw material prices to recover. Dis-investment in the commodity sector should keep the outlook for commodity FX bearish, despite already low valuations. Our favorite picks in the commodity space are to be short AUD and CAD. In EM, we focus on shorting currencies where idiosyncratic risks remain, such as political and labor market concerns in South Africa, or where the current account has yet to show signs of rebalancing, such as in Colombia.

0

1

2

3

4

5

6

7

8

9

0%20%40%60%80%

100%120%140%160%180%200%

2007 2008 2009 2010 2011 2012 2013 2014 2015

EM Debt to GDPAxJ Incremental Capital Output Ratio (rhs)

M O R G A N S T A N L E Y R E S E A R C H

16

March 13, 2016 Spring Global Strategy Outlook

Global EM Fixed Income: The Case for Alpha Gordian Kemen & EM Fixed Income Strategy Team

EM adjustment not complete: Our economists have downgraded both DM and EM growth for 2016 and 2017, expecting 2016 global growth at 3% vs. 3.3% previously, and pushing out the turnaround to late 2016. More importantly, EM is still not taking steps to deal with its problems, and structural reforms to lift productivity are still missing. EMFX is left do the heavy lifting in the adjustment process; and this is where we expect another bout of weakness over the next year.

Risks still skewed to the downside: The macro bear case sees larger downside than the upside in our bull case. This factors in the potential volatility on the back of growing political risks related to further erosion of the EU project, Brexit and geopolitics. Our oil forecasts have a similarly negative skew, with the base case for Brent still averaging US$30 for 2016. Finally, given the debt overhang and tight financial conditions, we cannot rule out a more disorderly end to the EM credit cycle. However, we confine this scenario to our bear case. In our base case, our EM bank analysts expect NPLs to rise further and take a toll on ROE, but they do not expect more negative capital shortfalls and eventual spillovers to sovereigns.

EM flows also a challenge: Both push factors (less US monetary accommodation) and pull factors (depressed EM growth) are likely to challenge overall flows into EM this year, just as in 2015. Since May 2015, EM debt dedicated funds have seen outflows of 13% of AUM. Low sovereign supply has

thus far been a partial offset, particularly in hard currency. Yet, with widening fiscal deficits, supply is likely to pick up. Therefore, if outflows from EM continue, this would in turn put pressure on bond yields.

Valuations have improved, however: Spreads on sovereign credit have only been wider 11% of days over the past 10 years, mainly during the global financial crisis, meaning spreads look cheap in the absence of a global recession. This cheapness is less clear when compared to US credit. EM IG credits provide 1.2% yield pickup over US IG, towards the lower end of the range since the taper tantrum, while HY only provides 0.9% compared to 5% a year ago. This supports our view that globally elevated risk premia are also behind the current wide EM spreads. It also caps the potential spread tightening in EM, as our US colleagues expect US IG spreads to tighten only 20bp in the coming year.

In local rates, most markets lagged core rates in the recent rally, with spreads widening to historically wide levels that provide a cushion to absorb higher UST yields. Across most curves, the front end is pricing in more tightening than our economists expect, providing protection against EM FX depreciation.

Ability to capture carry makes sovereign credit the preferred asset class: We project total returns of 6.6% over 12m, although less than 1% in the next 6 months. While we project spreads to widen to 480bp, given that UST yields are expected to remain flat, most of the high carry can be captured. Our spread forecasts also factor in a negative skew, with a bear case of 625bp vs. 425bp in the bull case.

Anticipated FX depreciation limits local rates total return, but opportunities exist: On a 12-month basis, expected return for the GBI-EM is negative in USD terms, given our expectation of 8-10% FX depreciation against the USD. However, we expect small positive returns after FX hedging in the next quarter as many countries still have steep local market curves and rates can move slightly lower on the back of UST move. In addition, the total return profile improves dramatically if FX hedges are taken off after 6 months, which is when we expect the depreciation to relent.

Neutral stance with focus on selective opportunities: The negative skew still reinforces a cautious approach, especially in the coming 6 months. Therefore, we advocate a very selective approach in our near-term asset allocation. However, lower core yields are expected to keep EM carry opportunities on the radar over the next 12 months. We maintain a preference for external debt.

Key Investment Ideas • Both EM fundamentals and flows remain challenged.

Better valuations and carry over a 12-month horizon offer a partial offset for total return, but given the multitude of risks that remain, especially in the next 6 months, we maintain a cautious approach and focus on selective alpha opportunities.

• We still favour sovereign credit where we project total returns of 6.6% over 12 months. We see less value in CEEMEA over time and recommend gradual reallocation to LatAm instead. Long Pemex vs Mexico remains one of our key trades in external debt, and we like the Argentina GDP warrant.

• Anticipated FX depreciation limits local rates total returns. Dexterity in FX hedging, however, can still deliver attractive total returns in a number of countries. Mexico remains one of our key OW’s here.

M O R G A N S T A N L E Y R E S E A R C H

17

March 13, 2016 Spring Global Strategy Outlook

Local Rates Allocation