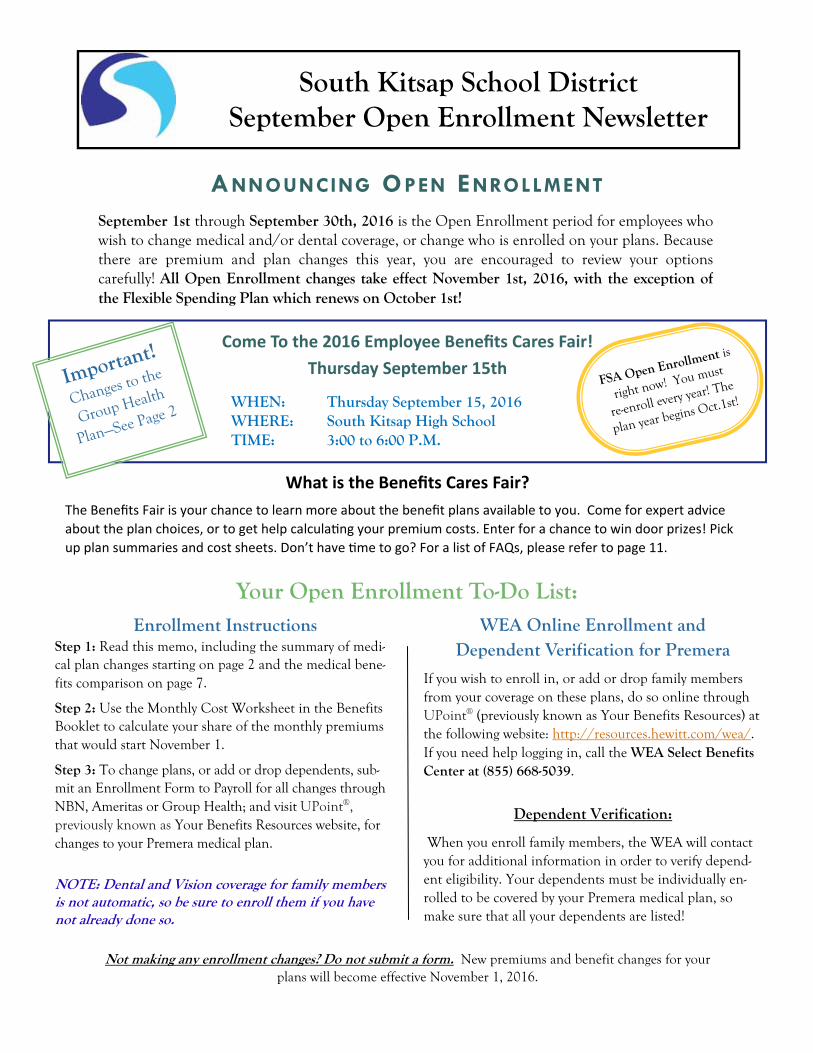

south kitsap school district september open enrollment...

TRANSCRIPT

Your Open Enrollment To-Do List:

South Kitsap School District September Open Enrollment Newsletter

Enrollment Instructions Step 1: Read this memo, including the summary of medi-cal plan changes starting on page 2 and the medical bene-fits comparison on page 7.

Step 2: Use the Monthly Cost Worksheet in the Benefits Booklet to calculate your share of the monthly premiums that would start November 1.

Step 3: To change plans, or add or drop dependents, sub-mit an Enrollment Form to Payroll for all changes through NBN, Ameritas or Group Health; and visit UPoint®, previously known as Your Benefits Resources website, for changes to your Premera medical plan.

NOTE: Dental and Vision coverage for family members is not automatic, so be sure to enroll them if you have not already done so.

September 1st through September 30th, 2016 is the Open Enrollment period for employees who wish to change medical and/or dental coverage, or change who is enrolled on your plans. Because there are premium and plan changes this year, you are encouraged to review your options carefully! All Open Enrollment changes take effect November 1st, 2016, with the exception of the Flexible Spending Plan which renews on October 1st!

WHEN: Thursday September 15, 2016 WHERE: South Kitsap High School TIME: 3:00 to 6:00 P.M.

Come To the 2016 Employee Benefits Cares Fair!

Thursday September 15th

ANNOUNCING OPEN ENROLLMENT

FSA Open Enrollment is

right now! You must

re-enroll every year! The

plan year begins Oct.1st!

Important!

Changes to the

Group Health

Plan—See Page 2

WEA Online Enrollment and Dependent Verification for Premera

If you wish to enroll in, or add or drop family members from your coverage on these plans, do so online through UPoint® (previously known as Your Benefits Resources) at the following website: http://resources.hewitt.com/wea/. If you need help logging in, call the WEA Select Benefits Center at (855) 668-5039.

Dependent Verification:

When you enroll family members, the WEA will contact you for additional information in order to verify depend-ent eligibility. Your dependents must be individually en-rolled to be covered by your Premera medical plan, so make sure that all your dependents are listed!

What is the Benefits Cares Fair?

The Benefits Fair is your chance to learn more about the benefit plans available to you. Come for expert advice

about the plan choices, or to get help calcula ng your premium costs. Enter for a chance to win door prizes! Pick

up plan summaries and cost sheets. Don’t have me to go? For a list of FAQs, please refer to page 11.

Not making any enrollment changes? Do not submit a form. New premiums and benefit changes for your plans will become effective November 1, 2016.

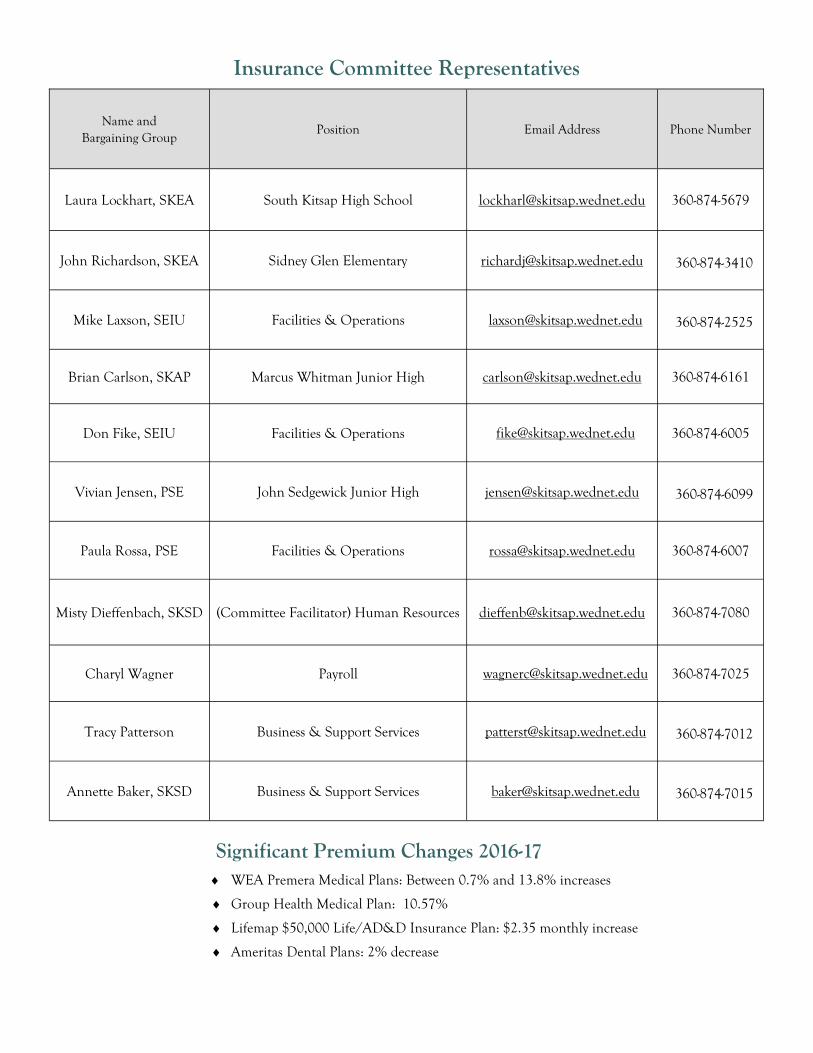

Insurance Committee Representatives

Laura Lockhart, SKEA South Kitsap High School [email protected] 360-874-5679

John Richardson, SKEA Sidney Glen Elementary [email protected] 360-874-3410

Mike Laxson, SEIU Facilities & Operations [email protected] 360-874-2525

Brian Carlson, SKAP Marcus Whitman Junior High [email protected] 360-874-6161

Don Fike, SEIU Facilities & Operations [email protected] 360-874-6005

Vivian Jensen, PSE John Sedgewick Junior High [email protected] 360-874-6099

Paula Rossa, PSE Facilities & Operations [email protected] 360-874-6007

Misty Dieffenbach, SKSD (Committee Facilitator) Human Resources [email protected] 360-874-7080

Charyl Wagner Payroll [email protected] 360-874-7025

Tracy Patterson Business & Support Services [email protected] 360-874-7012

Annette Baker, SKSD Business & Support Services [email protected] 360-874-7015

Name and Bargaining Group

Position Email Address Phone Number

Significant Premium Changes 2016-17 WEA Premera Medical Plans: Between 0.7% and 13.8% increases

Group Health Medical Plan: 10.57%

Lifemap $50,000 Life/AD&D Insurance Plan: $2.35 monthly increase

Ameritas Dental Plans: 2% decrease

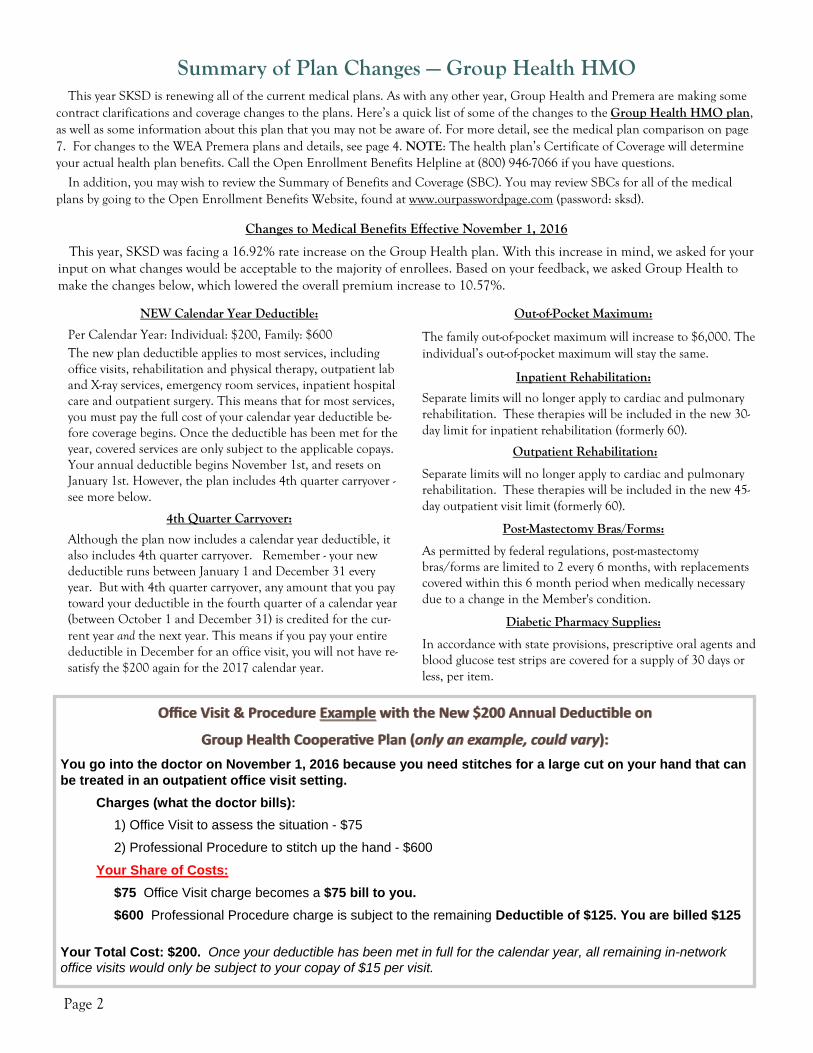

Summary of Plan Changes — Group Health HMO This year SKSD is renewing all of the current medical plans. As with any other year, Group Health and Premera are making some

contract clarifications and coverage changes to the plans. Here’s a quick list of some of the changes to the Group Health HMO plan, as well as some information about this plan that you may not be aware of. For more detail, see the medical plan comparison on page 7. For changes to the WEA Premera plans and details, see page 4. NOTE: The health plan’s Certificate of Coverage will determineyour actual health plan benefits. Call the Open Enrollment Benefits Helpline at (800) 946-7066 if you have questions.

In addition, you may wish to review the Summary of Benefits and Coverage (SBC). You may review SBCs for all of the medical plans by going to the Open Enrollment Benefits Website, found at www.ourpasswordpage.com (password: sksd).

NEW Calendar Year Deductible:

Per Calendar Year: Individual: $200, Family: $600 The new plan deductible applies to most services, including office visits, rehabilitation and physical therapy, outpatient lab and X-ray services, emergency room services, inpatient hospital care and outpatient surgery. This means that for most services, you must pay the full cost of your calendar year deductible be-fore coverage begins. Once the deductible has been met for the year, covered services are only subject to the applicable copays. Your annual deductible begins November 1st, and resets on January 1st. However, the plan includes 4th quarter carryover - see more below.

4th Quarter Carryover:

Although the plan now includes a calendar year deductible, it also includes 4th quarter carryover. Remember - your new deductible runs between January 1 and December 31 every year. But with 4th quarter carryover, any amount that you pay toward your deductible in the fourth quarter of a calendar year (between October 1 and December 31) is credited for the cur-rent year and the next year. This means if you pay your entire deductible in December for an office visit, you will not have re-satisfy the $200 again for the 2017 calendar year.

Out-of-Pocket Maximum:

The family out-of-pocket maximum will increase to $6,000. The individual’s out-of-pocket maximum will stay the same.

Inpatient Rehabilitation:

Separate limits will no longer apply to cardiac and pulmonary rehabilitation. These therapies will be included in the new 30-day limit for inpatient rehabilitation (formerly 60).

Outpatient Rehabilitation:

Separate limits will no longer apply to cardiac and pulmonary rehabilitation. These therapies will be included in the new 45-day outpatient visit limit (formerly 60).

Post-Mastectomy Bras/Forms:

As permitted by federal regulations, post-mastectomy bras/forms are limited to 2 every 6 months, with replacements covered within this 6 month period when medically necessary due to a change in the Member's condition.

Diabetic Pharmacy Supplies:

In accordance with state provisions, prescriptive oral agents and blood glucose test strips are covered for a supply of 30 days or less, per item.

Changes to Medical Benefits Effective November 1, 2016

This year, SKSD was facing a 16.92% rate increase on the Group Health plan. With this increase in mind, we asked for your input on what changes would be acceptable to the majority of enrollees. Based on your feedback, we asked Group Health to make the changes below, which lowered the overall premium increase to 10.57%.

Office Visit & Procedure Office Visit & Procedure ExampleExample with the New $200 Annual Deduc ble on with the New $200 Annual Deduc ble on

Group Health Coopera ve Plan (Group Health Coopera ve Plan (only an example, could varyonly an example, could vary):):

You go into the doctor on November 1, 2016 because you need stitches for a large cut on your hand that can be treated in an outpatient office visit setting.

Charges (what the doctor bills):

1) Office Visit to assess the situation - $75

2) Professional Procedure to stitch up the hand - $600

Your Share of Costs:

$75 Office Visit charge becomes a $75 bill to you.

$600 Professional Procedure charge is subject to the remaining Deductible of $125. You are billed $125

Your Total Cost: $200. Once your deductible has been met in full for the calendar year, all remaining in-network office visits would only be subject to your copay of $15 per visit.

Page 2

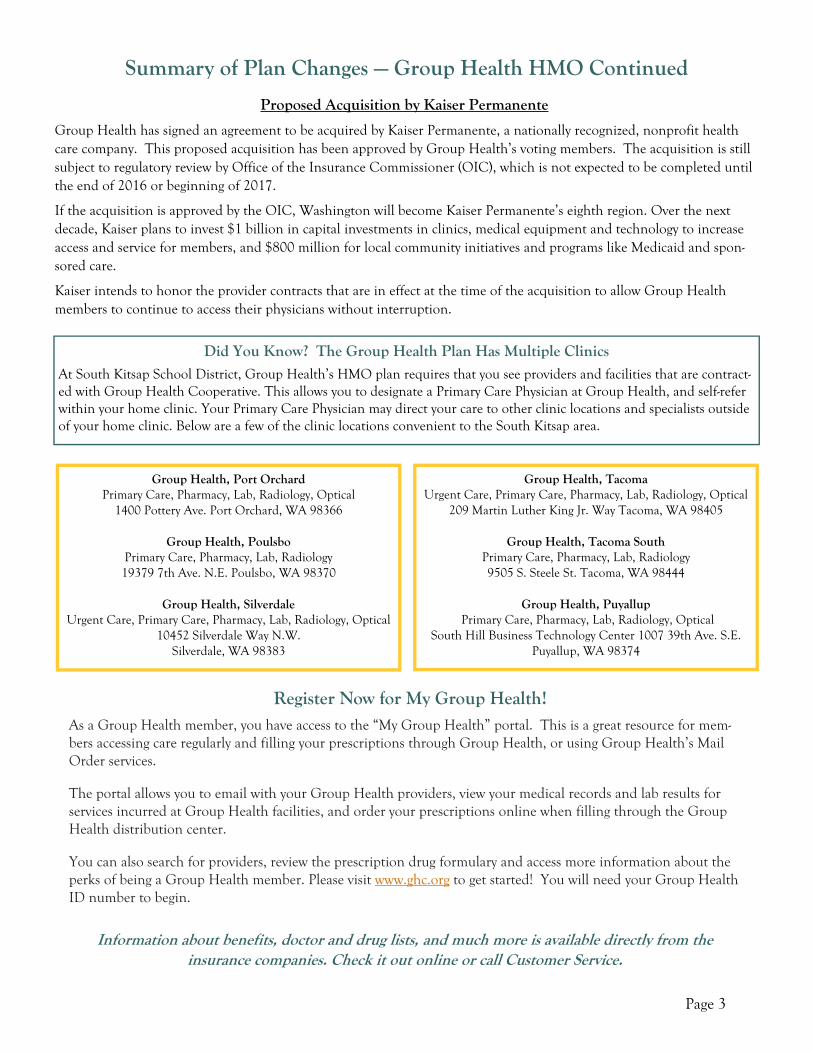

Summary of Plan Changes — Group Health HMO Continued

Page 3

Proposed Acquisition by Kaiser Permanente

Group Health has signed an agreement to be acquired by Kaiser Permanente, a nationally recognized, nonprofit health care company. This proposed acquisition has been approved by Group Health’s voting members. The acquisition is still subject to regulatory review by Office of the Insurance Commissioner (OIC), which is not expected to be completed until the end of 2016 or beginning of 2017.

If the acquisition is approved by the OIC, Washington will become Kaiser Permanente’s eighth region. Over the next decade, Kaiser plans to invest $1 billion in capital investments in clinics, medical equipment and technology to increase access and service for members, and $800 million for local community initiatives and programs like Medicaid and spon-sored care.

Kaiser intends to honor the provider contracts that are in effect at the time of the acquisition to allow Group Health members to continue to access their physicians without interruption.

Did You Know? The Group Health Plan Has Multiple Clinics At South Kitsap School District, Group Health’s HMO plan requires that you see providers and facilities that are contract-ed with Group Health Cooperative. This allows you to designate a Primary Care Physician at Group Health, and self-refer within your home clinic. Your Primary Care Physician may direct your care to other clinic locations and specialists outside of your home clinic. Below are a few of the clinic locations convenient to the South Kitsap area.

Group Health, Port Orchard Primary Care, Pharmacy, Lab, Radiology, Optical

1400 Pottery Ave. Port Orchard, WA 98366

Group Health, Poulsbo Primary Care, Pharmacy, Lab, Radiology 19379 7th Ave. N.E. Poulsbo, WA 98370

Group Health, Silverdale Urgent Care, Primary Care, Pharmacy, Lab, Radiology, Optical

10452 Silverdale Way N.W. Silverdale, WA 98383

Group Health, Tacoma Urgent Care, Primary Care, Pharmacy, Lab, Radiology, Optical

209 Martin Luther King Jr. Way Tacoma, WA 98405

Group Health, Tacoma South Primary Care, Pharmacy, Lab, Radiology 9505 S. Steele St. Tacoma, WA 98444

Group Health, Puyallup Primary Care, Pharmacy, Lab, Radiology, Optical

South Hill Business Technology Center 1007 39th Ave. S.E. Puyallup, WA 98374

Information about benefits, doctor and drug lists, and much more is available directly from the insurance companies. Check it out online or call Customer Service.

Register Now for My Group Health! As a Group Health member, you have access to the “My Group Health” portal. This is a great resource for mem-bers accessing care regularly and filling your prescriptions through Group Health, or using Group Health’s Mail Order services.

The portal allows you to email with your Group Health providers, view your medical records and lab results for services incurred at Group Health facilities, and order your prescriptions online when filling through the Group Health distribution center.

You can also search for providers, review the prescription drug formulary and access more information about the perks of being a Group Health member. Please visit www.ghc.org to get started! You will need your Group Health ID number to begin.

EasyChoice A Changes (continued)

Office Visits (Primary): The copay will increase from $15 to $25. Specialist: A new $35 copay for specialist office visits will apply.

Prescription Drugs: The copay for generic drugs at the retail pharmacy will increase from $5 to $10. Copays for mail order prescriptions will increase to $20 for generic and 30% for pre-ferred and non-preferred.

Outpatient Diagnostic Testing: The first $1,000 of outpatient diagnostic lab and x-ray services each calendar year will no longer be covered in full. Rather, the first $250 per year will be subject to 20% coinsurance, and thereafter, deductible and coinsurance will apply to all services.

EasyChoice B Changes

Network Change: The network will change to Premera’s smaller Heritage Prime network. See page 5 for more details.

Office Visits (Specialist): A new $40 copay for specialist office visits will apply.

Basic Plan Changes

Network: The network will remain Premera’s smaller Heritage Prime network.

Deductible: The deductible will increase to $2,100 per person.

Out-of-Pocket Maximum: The annual out-of-pocket maximum will increase to $6,600 per person.

Office Visits (Primary): The copay will increase from $30 to $35.

Office Visits (Specialist): A new $50 copay for specialist office visits will apply.

Prescription Drugs: The prescription deductible will increase to $750 per person. The prescription out-of-pocket maximum will be combined with the medical out-of-pocket maximum.

Prescription Drug Copays: Retail copays for non-preferred drugs will increase from $45 to $50. Copays for mail order ge-neric drugs will increase from $15 to $30, and mail order non-preferred drug copays will increase from $90 to $100.

Q-HDHP Changes

Deductible: The deductible will increase to $1,750 per person. The deductible when you enroll dependents will be $3,500.

Out-of-Pocket Maximum: The annual individual out-of-pocket maximum will increase to $5,000. This limit will apply to each individual enrolled on the family plan, and the aggregate family out-of-pocket maximum will be $10,000.

Summary of Plan Changes—Premera WEA Plans

Plan 5 Benefits Changes

Out-of-Pocket Maximum: The annual out-of-pocket maximum will increase to $1,000 per person.

Office Visits (Primary): The copay will increase from $15 to $20.

Office Visits (Specialist): A new $30 copay for specialist office visits will apply.

Prescription Drugs: The copay for mail order generic prescrip-tions will increase from $15 to $20.

Plan 2 Benefits Changes

Deductible: The deductible will increase to $300 per person.

Out-of-Pocket Maximum: The annual out-of-pocket maximum will increase to $2,000 per person.

Office Visits (Specialist): A new $35 copay in-network / $40 out-of-network for specialist office visits will apply.

Prescription Drugs: Copays for mail order drugs will increase to $20 for generic, $40 for preferred, and $65 for non-preferred.

Plan 3 Benefits Changes

Deductible: The deductible will increase to $500 per person.

Out-of-Pocket Maximum: The annual out-of-pocket maximum will increase to $3,000 per person.

Office Visits (Specialist): A new $40 copay in-network/ $50 out-of-network for specialist office visits will apply.

Prescription Drugs: Copays for mail order drugs will increase to $30 for generic, $50 for preferred, and $70 for non-preferred.

EasyChoice A Changes

Deductible: The deductible will increase to $1,250 per person.

New Physician Network for EasyChoice B Plan

On November 1st, the EasyChoice B provider network will change to Premera’s smaller Heritage Prime Network, the same network that the Basic Plan currently uses. Check to see wheth-er your physician will be in the new network on November 1st, and note that on January 1, 2017, Heritage Prime will no long-er be contracted with portions of the Swedish, Providence, and CHI Franciscan Health Systems. See page 5 for more details.

Massage Therapy—Outpatient Rehab Authorization Required

Massage therapy, occupational therapy and physical therapy will require prior authorization through eviCore on all plans. Massage therapy requires diagnosis and referral by a health care provider, and must be medically necessary.

Here’s a quick list of only some of the changes to the WEA Premera plans. For more detail, see the medical plan comparison on page 7. For a more complete list of changes, please review the WEA Benefit Changes document on the Open Enrollment Benefits Website. NOTE: The health plan’s Certificate of Coverage will determine your actual health plan benefits. Call the Open Enroll-ment Benefits Helpline at (800) 946-7066 if you have questions.

Page 4

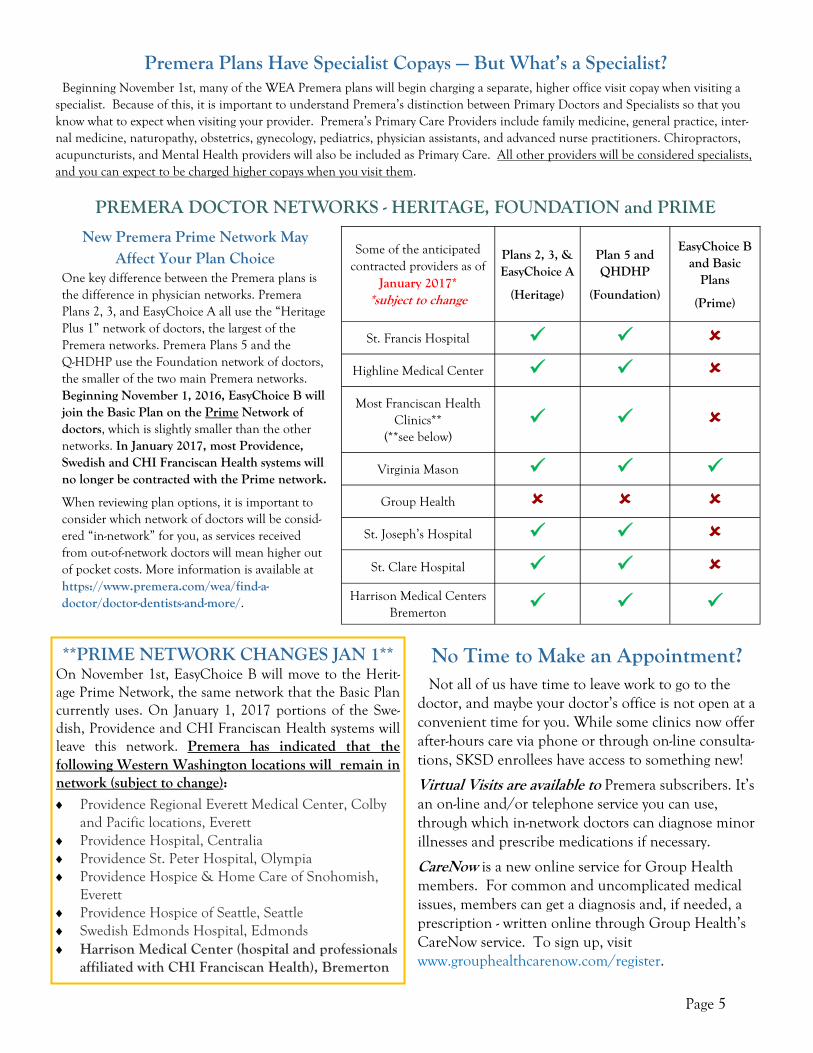

New Premera Prime Network May Affect Your Plan Choice

One key difference between the Premera plans is the difference in physician networks. Premera Plans 2, 3, and EasyChoice A all use the “Heritage Plus 1” network of doctors, the largest of the Premera networks. Premera Plans 5 and the Q-HDHP use the Foundation network of doctors, the smaller of the two main Premera networks. Beginning November 1, 2016, EasyChoice B will join the Basic Plan on the Prime Network of doctors, which is slightly smaller than the other networks. In January 2017, most Providence, Swedish and CHI Franciscan Health systems will no longer be contracted with the Prime network.

When reviewing plan options, it is important to consider which network of doctors will be consid-ered “in-network” for you, as services received from out-of-network doctors will mean higher out of pocket costs. More information is available at https://www.premera.com/wea/find-a-doctor/doctor-dentists-and-more/.

PREMERA DOCTOR NETWORKS - HERITAGE, FOUNDATION and PRIME

Some of the anticipated contracted providers as of

January 2017* *subject to change

Plans 2, 3, & EasyChoice A

(Heritage)

Plan 5 and QHDHP

(Foundation)

EasyChoice B and Basic

Plans

(Prime)

St. Francis Hospital Highline Medical Center Most Franciscan Health

Clinics** (**see below)

Virginia Mason

Group Health St. Joseph’s Hospital

St. Clare Hospital Harrison Medical Centers

Bremerton

Not all of us have time to leave work to go to the doctor, and maybe your doctor’s office is not open at a convenient time for you. While some clinics now offer after-hours care via phone or through on-line consulta-tions, SKSD enrollees have access to something new!

Virtual Visits are available to Premera subscribers. It’s an on-line and/or telephone service you can use, through which in-network doctors can diagnose minor illnesses and prescribe medications if necessary.

CareNow is a new online service for Group Health members. For common and uncomplicated medical issues, members can get a diagnosis and, if needed, a prescription - written online through Group Health’s CareNow service. To sign up, visit www.grouphealthcarenow.com/register.

No Time to Make an Appointment?

Beginning November 1st, many of the WEA Premera plans will begin charging a separate, higher office visit copay when visiting a specialist. Because of this, it is important to understand Premera’s distinction between Primary Doctors and Specialists so that you know what to expect when visiting your provider. Premera’s Primary Care Providers include family medicine, general practice, inter-nal medicine, naturopathy, obstetrics, gynecology, pediatrics, physician assistants, and advanced nurse practitioners. Chiropractors, acupuncturists, and Mental Health providers will also be included as Primary Care. All other providers will be considered specialists, and you can expect to be charged higher copays when you visit them.

Premera Plans Have Specialist Copays — But What’s a Specialist?

**PRIME NETWORK CHANGES JAN 1**On November 1st, EasyChoice B will move to the Herit-age Prime Network, the same network that the Basic Plan currently uses. On January 1, 2017 portions of the Swe-dish, Providence and CHI Franciscan Health systems will leave this network. Premera has indicated that the following Western Washington locations will remain in network (subject to change):

Providence Regional Everett Medical Center, Colby and Pacific locations, Everett

Providence Hospital, Centralia Providence St. Peter Hospital, Olympia Providence Hospice & Home Care of Snohomish,

Everett Providence Hospice of Seattle, Seattle Swedish Edmonds Hospital, Edmonds Harrison Medical Center (hospital and professionals

affiliated with CHI Franciscan Health), Bremerton

Page 5

Information about the Q-HDHP Plan Thinking About Enrolling in the High Deductible Health Plan? Here’s Some of What You Need to Know.

With its lower premium, the Qualified High Deductible Health Plan (Q-HDHP) has become an attractive choice for employees. But the plan is different than traditional plans, so it is important that you understand how it works before you enroll.

A Q-HDHP is a health plan that can be paired with a tax-qualified Health Savings Account (HSA). Almost all medical charges are subject to the high deductible that you must pay first, before the plan starts to help pay for the cost of any covered services - the one exception is full coverage for preventive care provided by in-network providers.

The deductible and out-of-pocket maximum: If you enroll only yourself, your in-network deductible is $1,750 per calendar year. Once you meet your deductible, you will then pay 20% of the cost of your care, including prescription drugs, until your total costs reach $5,000 — the annual out-of-pocket maximum. This cost-sharing fully resets every January 1st; there is no “fourth quarter carry-over” on this plan.

Thinking of enrolling with family? This Q-HDHP is different from the lower-deductible PPO plans, because when you enroll with one or more family members, the higher $3,500 Family Deductible must be satisfied in its entirety before coinsurance begins for any covered family member. The one exception is preventive care, which is covered in full if you see an in-network provider. Es-sentially, when you enroll with any family members, the individual deductible no longer applies; it is replaced by the shared family deductible.

Though each person enrolled on the family plan has an individual out-of-pocket maximum of $5,000, the most a family would pay per calendar year is $10,000. To comply with the Affordable Care Act, Premera will now cover 100% of allowed charges for the re-mainder of the calendar year for each individual once the individual’s out of pocket maximum has been satisfied—even if the plan covers more than one person!

If you are considering enrolling in the Q-HDHP during this Open Enrollment period, it is important to consider the trade-offs: the premiums you would pay vs. the financial exposure from the higher deductibles and annual out-of-pocket maximums. If you are considering this, also consider setting aside your premium savings into a Health Savings Account. Read below!

In order to open and contribute money into an HSA, you mustbe covered by a Q-HDHP and may not be enrolled in other com-prehensive group insurance coverage, Medicare, a Health Care Flexible Spending Account (unless it is limited purpose), or be eligible for reimbursement from a Health FSA or HRA through a spouse or parent.

HSAs have annual contribution limits for individual and familyaccounts, with additional “catch-up” contributions allowed for people age 55 or older.

If you enroll in the Q-HDHP with a family member who is notenrolled in any other non-HDHP health plan that covers the same items your HDHP covers, you may then contribute up to the family maximum to your HSA.

Medical expenses for your children who are not your tax depend-ents or your domestic partner, children of your domestic partner who are not your adopted or stepchildren, and relatives who do not meet the IRS definition of a “qualified dependent relative” are NOT eligible for tax-free reimbursement under your HSA.

You may use tax-free HSA money in your HSA account for“qualified health expenses.” HSA funds used for non-qualified expenses are subject to income taxes and penalties. IRS Publica-tion 502 contains the entire list of qualified expenses.

If you dis-enroll mid-calendar year from a Q-HDHP (e.g., at OpenEnrollment next year), and you have contributed more than the monthly pro-rated contribution to your HSA for 2016 or 2017, you will be required to withdraw the overage as taxable income.

2016 HSA Contribution Limits

For Individual Enrollment: $3,350 (Increases to $3,400 for 2017) For Family Enrollment: $6,750 Annual Catch-Up Contribution if an individual is age 55 or older:

$1,000 Refer to IRS Publication 969 or consult your tax advisor for details.

Have questions about whether the Q-HDHP and HSA is right for you? Call the friendly and knowledgeable folks at the Open Enroll-ment Benefits Helpline at (800) 946-7066.

About Health Savings Accounts Health Savings Accounts (HSAs) are tax-favored savings accounts available only to individuals enrolled in a Q-HDHP. You can make tax-free contributions to your HSA and then use the tax-free money to pay for eligible health-related expenses. The HSA is really just a bank account that you own. Money that you contribute to the account remains yours from year to year, any interest it earns is tax-free, or it can be invested. Unlike the Health Care Flexible Spending Account (FSA), the HSA is not a “use it or lose it” plan. Use of depos-ited funds is available to you even after you are no longer enrolled in a Q-HDHP, or if you are no longer employed. HSAs are gov-erned by the IRS and have specific rules about when and how much money you can contribute, how the money can be used and for whom. It is important to know these rules to avoid tax penalties. We have outlined only a few important HSA facts below:

Page 6

Qui

ck 2

016-

2017

Med

ical

Pla

n C

ompa

riso

n

Thi

s is

a b

rief

in-n

etw

ork

com

pari

son

of th

e m

ost f

requ

ently

use

d m

edic

al p

lan

serv

ices

. For

impo

rtan

t det

ails

, and

to s

ee

plan

lim

itatio

ns a

nd e

xclu

sion

s, p

leas

e re

fer

to th

e pl

an s

umm

arie

s an

d co

mpa

riso

ns o

n th

e B

enef

its W

ebsi

te.

Pla

n 5

Pla

n 2

Pla

n 3

Eas

yCho

ice

A

Eas

yCho

ice

B

Bas

ic P

lan

QH

DH

P

GH

In-N

etw

ork

Pro

vide

rs

Foun

datio

n H

erita

ge P

lus

1 H

erita

ge P

lus

1 H

erita

ge P

lus

1 H

erita

ge P

rim

e H

erita

ge P

rim

e Fo

unda

tion

Gro

up H

ealth

C

oope

rativ

e O

NLY

Out

-of-N

etw

ork

All

Oth

er

Prov

ider

s A

ll O

ther

Pr

ovid

ers

All

Oth

er

Prov

ider

s A

ll O

ther

Pr

ovid

ers

All

Oth

er

Prov

ider

s A

ll O

ther

Pr

ovid

ers

All

Oth

er

Prov

ider

s N

o C

over

age

Ded

ucti

ble

In-N

etw

ork

In

divi

dual

: $20

0 Fa

mily

: $60

0 In

divi

dual

: $30

0 Fa

mily

: $90

0 In

divi

dual

: $50

0 Fa

mily

: $1,

500

Indi

vidu

al:

$1,2

50

Fam

ily: $

3,75

0

Indi

vidu

al: $

750

Fam

ily: $

2,25

0 In

divi

dual

: $2,

100

Fam

ily: $

4,20

0 In

divi

dual

: $1,

750

Fam

ily: $

3,50

0 In

divi

dual

: $20

0 Fa

mily

: $60

0

Med

ical

O

ut-o

f-Poc

ket M

ax

Indi

vidu

al:

$1,0

00

Fam

ily: $

3,00

0

Indi

vidu

al:

$2,0

00

Fam

ily: $

6,00

0

Indi

vidu

al: $

3,00

0 Fa

mily

: $9,

000

Indi

vidu

al:

$4,0

00

Fam

ily: $

8,00

0

Indi

vidu

al:

$3,5

00

Fam

ily: $

7,00

0

Indi

vidu

al: $

6,60

0 Fa

mily

: $13

,200

In

divi

dual

: $5,

000

Fam

ily: $

10,0

00

Indi

vidu

al: $

2,00

0 Fa

mily

: $6,

000

Coi

nsu

ran

ce

In-N

etw

ork

90%

80%

80%

80%

75%

70%

80%

100%

Off

ice

Vis

its

and

Cop

ays

Pr

imar

y: $

20

Spec

ialis

t: $3

0 Pr

imar

y: $

25

Spec

ialis

t: $3

5 Pr

imar

y: $

30

Spec

ialis

t: $4

0 Pr

imar

y: $

25

Spec

ialis

t: $3

5 Pr

imar

y: $

30

Spec

ialis

t: $4

0 Pr

imar

y: $

35

Spec

ialis

t: $5

0 D

educ

tible

and

co

insu

ranc

e ap

ply.

$1

5 co

pay

Ded

uctib

le a

pplie

s

Inpa

tien

t H

ospi

tal

Stay

s

$15

0 pe

r da

y up

to

thre

e da

ys.

Ded

uctib

le a

nd

coin

sura

nce

ap

ply.

$150

per

day

up

to th

ree

days

. D

educ

tible

and

co

insu

ranc

e

appl

y.

$300

per

day

up

to th

ree

days

. D

educ

tible

and

C

oins

uran

ce.

Ded

uctib

le a

nd

Coi

nsur

ance

D

educ

tible

and

C

oins

uran

ce

Ded

uctib

le a

nd

Coi

nsur

ance

D

educ

tible

and

co

insu

ranc

e ap

ply.

$100

cop

ay p

er d

ay

up to

thre

e da

ys.

Ded

uctib

le a

pplie

s

Dia

gnos

tic

Lab

and

X-r

ay S

ervi

ces

Ded

uctib

le a

nd

coin

sura

nce

ap

ply.

Ded

uctib

le a

nd

coin

sura

nce

ap

ply.

Ded

uctib

le a

nd

coin

sura

nce

appl

y.

1st $

250

subj

ect

to c

oins

uran

ce

only

. The

n D

e-du

ctib

le a

nd c

oin-

sura

nce

appl

y.

Ded

uctib

le a

nd

coin

sura

nce

ap

ply.

Ded

uctib

le a

nd

coin

sura

nce

appl

y.

Ded

uctib

le a

nd

coin

sura

nce

appl

y. D

educ

tible

app

lies.

Ret

ail P

resc

ript

ion

D

rugs

D

educ

tible

w

aive

d D

educ

tible

w

aive

d D

educ

tible

w

aive

d

$500

D

educ

tible

w

aive

d fo

r ge

neri

cs

$250

D

educ

tible

w

aive

d fo

r ge

neri

cs

$750

/ $

1,50

0 D

educ

tible

wai

ved

for

gene

rics

Ded

uctib

le

appl

ies

Ded

uctib

le

wai

ved

Pref

erre

d G

ener

ic

$10

$10

$15

$10

$5

$15

$15

Pref

erre

d B

rand

$1

5$2

0$2

530

%$3

0$3

0$3

0N

on-P

refe

rred

$3

0$3

5$4

030

%$4

5$5

0n/

aSp

ecia

lty$5

0$5

0$6

030

%30

%30

%n/

aT

his

com

pari

son

is in

tend

ed a

s an

illu

stra

tion

of c

over

age

only

and

not

a g

uara

ntee

of c

over

age.

In

the

case

of a

ny d

iscr

epan

cy, t

he c

ontr

act s

hall

prev

ail.

You

pay

20%

Pre

scri

ptio

n

Out

-of-P

ocke

t Max

Indi

vidu

al:

$2,0

00

Fam

ily: $

4,00

0

Indi

vidu

al:

$2,0

00

Fam

ily: $

4,00

0

Indi

vidu

al: $

2,00

0 Fa

mily

: $4,

000

Indi

vidu

al:

$2,5

00

Fam

ily: $

5,00

0

Indi

vidu

al:

$2,5

00

Fam

ily: $

5,00

0

Shar

ed w

ith

M

edic

al

Shar

ed w

ith

M

edic

al

Shar

ed w

ith

M

edic

al

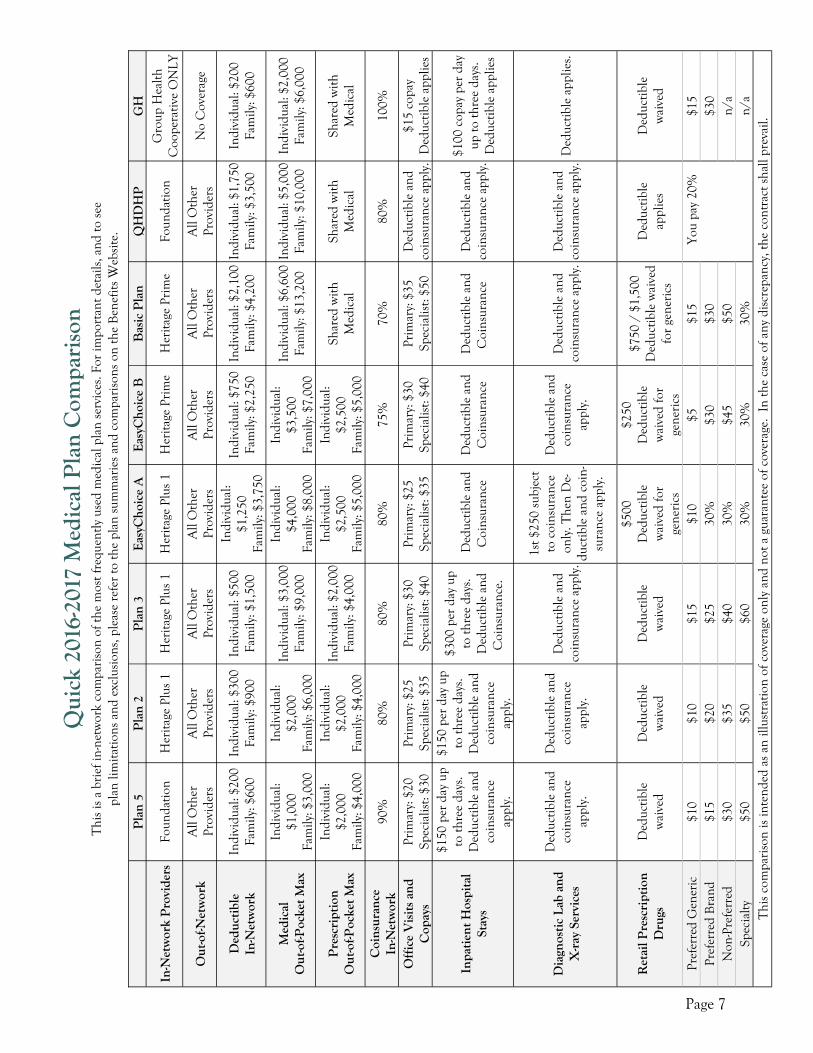

Page 7

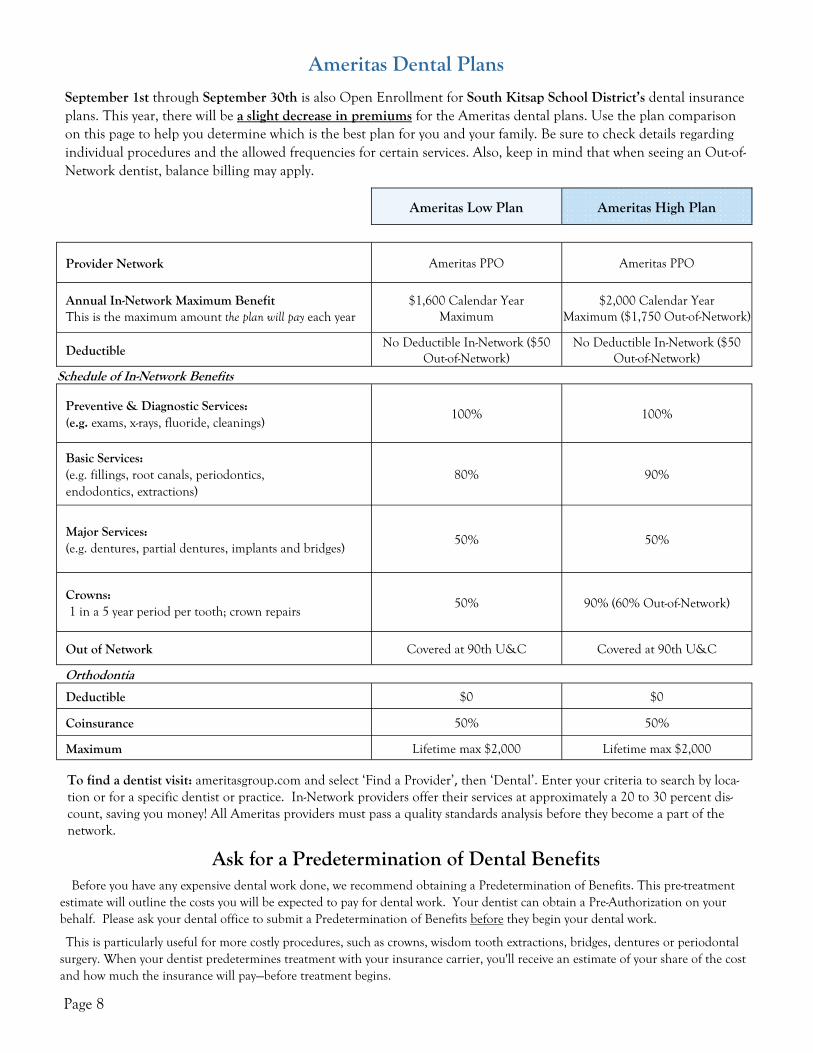

Ameritas Dental Plans

Ask for a Predetermination of Dental Benefits Before you have any expensive dental work done, we recommend obtaining a Predetermination of Benefits. This pre-treatment

estimate will outline the costs you will be expected to pay for dental work. Your dentist can obtain a Pre-Authorization on your behalf. Please ask your dental office to submit a Predetermination of Benefits before they begin your dental work.

This is particularly useful for more costly procedures, such as crowns, wisdom tooth extractions, bridges, dentures or periodontal surgery. When your dentist predetermines treatment with your insurance carrier, you'll receive an estimate of your share of the cost and how much the insurance will pay—before treatment begins.

September 1st through September 30th is also Open Enrollment for South Kitsap School District’s dental insurance plans. This year, there will be a slight decrease in premiums for the Ameritas dental plans. Use the plan comparison on this page to help you determine which is the best plan for you and your family. Be sure to check details regarding individual procedures and the allowed frequencies for certain services. Also, keep in mind that when seeing an Out-of-Network dentist, balance billing may apply.

Ameritas Low Plan Ameritas High Plan

Provider Network Ameritas PPO Ameritas PPO

Annual In-Network Maximum Benefit This is the maximum amount the plan will pay each year

$1,600 Calendar Year Maximum

$2,000 Calendar Year Maximum ($1,750 Out-of-Network)

Deductible No Deductible In-Network ($50

Out-of-Network) No Deductible In-Network ($50

Out-of-Network) Schedule of In-Network Benefits

Preventive & Diagnostic Services: (e.g. exams, x-rays, fluoride, cleanings)

100% 100%

Basic Services: (e.g. fillings, root canals, periodontics, endodontics, extractions)

80% 90%

Major Services: (e.g. dentures, partial dentures, implants and bridges)

50% 50%

Crowns: 1 in a 5 year period per tooth; crown repairs

50% 90% (60% Out-of-Network)

Out of Network Covered at 90th U&C Covered at 90th U&C

Orthodontia

Deductible $0 $0

Coinsurance 50% 50%

Maximum Lifetime max $2,000 Lifetime max $2,000

To find a dentist visit: ameritasgroup.com and select ‘Find a Provider’, then ‘Dental’. Enter your criteria to search by loca-tion or for a specific dentist or practice. In-Network providers offer their services at approximately a 20 to 30 percent dis-count, saving you money! All Ameritas providers must pass a quality standards analysis before they become a part of the network.

Page 8

Flexible Spending Plan Open Enrollment Begins NOW! The Flexible Spending Plan Year Runs from 10/1/2016—9/30/2017

Many employees save hundreds of tax dollars each year and you can too. Every year employees and their families face out-of-pocket costs for health care expenses that are not paid for by insurance. By signing up now for the District’s Flexible Spending Account (FSA) you can cover these costs with tax-free money. The SKSD FSA allows you to set aside up to $2,550 per plan year!

Here’s how it works: First, estimate what you expect to personally spend on your health-related expenses for yourself and if applicable, for your spouse and/or children in the 2016-2017 plan year. (Don’t count any money you pay as a premium share.) Next, sign up for the District’s Flex-Plan, and have part or all of that expense set aside through payroll deduction. This way, your FSA contributions go into your reimbursement account without being taxed. Finally, after you have incurred eligible health-related expenses, you can get reimbursed from your account with tax-free money! But plan carefully - this is a “use-it-or-lose it” program. Only $500 of any un-reimbursed funds will roll over to the next plan year.

Limited-Purpose FSA: If you are enrolled on the District’s Q-HDHP, or on your spouse’s, you cannot put money into a Health Savings Account (HSA) if you also have a Health FSA that covers the same services as your Q-HDHP. But you can still sign up for a “limited-purpose FSA” for out-of-pocket dental and vision expenses only, and still contribute to your HSA.

Have kids in daycare? If you pay for daycare for dependent family members so that you can go to work, you may also set aside up to $5,000 per year for tax-free reimbursement of daycare costs. Be sure to review your materials for details about how this plan works.

In Network (NBN Providers)

Out-of-Network (Submit claims for reimbursement)

Vision Exam One every 365 days

Paid at 100% Up to $50

Frames One pair every 730 days

A wide selection of frames paid at

100% Up to $45

Lenses One pair every 365 days (basic lenses, does not include cosmetic extras)

Single Paid at 100%* Up to $55

Bifocal Paid at 100%* Up to $85

Trifocal Paid at 100%* Up to $105

Lenticular Paid at 100%* Up to $125

Contact Lenses and Fitting

Once every 365 days, in lieu of frames and lenses.

$250 allowance $100 allowance

*Paid in full up to the allowed amount. Cost shares exceeding theallowed amount are payable by the subscriber.

NBN Vision Plan Eligible employees are automatically enrolled in the

NBN Vision Plan. The monthly premium for vision is withheld from your District Contribution. Below are the plan highlights.

Life and Long Term Disability Insurance—Protect Your Family

SKSD’s employees are automatically covered for Life Insurance and Long Term Disability insurance. These benefits protect your income. Here’s a brief summary:

Life and AD&D Insurance: Life and AD&D insurance is a mandatory benefit, and the monthly premium is taken from your District contribution. The benefit amount is $50,000. (Question: Have you experienced changes in your life that might cause you to update your beneficiary arrangement?)

Long Term Disability Insurance: LTD insurance is another mandatory benefit with the premium withheld from your District contribution. After you are disabled for 90 calendar days, LTD insurance can pay 60% of your pre-disability income, to a maximum of $7,000 per month. Partial disability benefits are available. If you remain disabled according to the policy, benefits may be payable until 65, standard ADEA.

Voluntary Life and AD&D Insurance: You may purchase voluntary life insurance in increments of $10,000 up to a maximum of $300,000. The monthly premium would be deducted from your paycheck. Your District Contribution cannot pay for this insurance. Coverage for a spouse, partner, and children is also available. Depending on your election amount and whether you’re applying outside your initial eligibility window, you may be required to complete a Medical History Statement, and you may be denied coverage because of your health.

Voluntary Short Term Disability (VSTD) Insurance: You may purchase VSTD insurance to help cover your lost income during the waiting period for LTD. This is a voluntary plan paid for by you.

Page 9

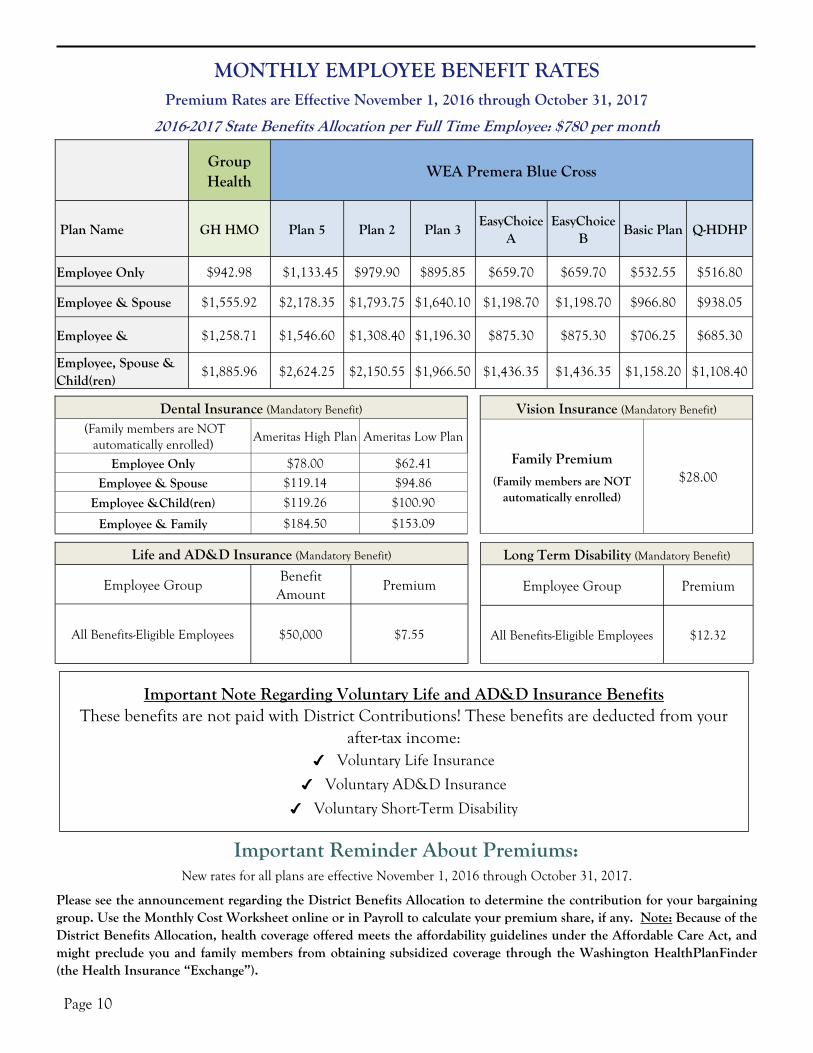

Group Health

WEA Premera Blue Cross

Plan Name GH HMO Plan 5 Plan 2 Plan 3 EasyChoice

A EasyChoice

B Basic Plan

Employee Only $942.98 $1,133.45 $979.90 $895.85 $659.70 $659.70 $532.55

Employee & Spouse $1,555.92 $2,178.35 $1,793.75 $1,640.10 $1,198.70 $1,198.70 $966.80

Employee & $1,258.71 $1,546.60 $1,308.40 $1,196.30 $875.30 $875.30 $706.25

Employee, Spouse & Child(ren)

$1,885.96 $2,624.25 $2,150.55 $1,966.50 $1,436.35 $1,436.35 $1,158.20

Q-HDHP

$516.80

$938.05

$685.30

$1,108.40

Important Reminder About Premiums: New rates for all plans are effective November 1, 2016 through October 31, 2017.

Please see the announcement regarding the District Benefits Allocation to determine the contribution for your bargaining group. Use the Monthly Cost Worksheet online or in Payroll to calculate your premium share, if any. Note: Because of the District Benefits Allocation, health coverage offered meets the affordability guidelines under the Affordable Care Act, and might preclude you and family members from obtaining subsidized coverage through the Washington HealthPlanFinder (the Health Insurance “Exchange”).

Dental Insurance (Mandatory Benefit) (Family members are NOT

automatically enrolled) Ameritas High Plan Ameritas Low Plan

Employee Only $78.00 $62.41

Employee & Spouse $119.14 $94.86

Employee &Child(ren) $119.26 $100.90

Employee & Family $184.50 $153.09

Long Term Disability (Mandatory Benefit)

Employee Group Premium

All Benefits-Eligible Employees $12.32

Life and AD&D Insurance (Mandatory Benefit)

Employee Group Benefit Amount

Premium

All Benefits-Eligible Employees $50,000 $7.55

Vision Insurance (Mandatory Benefit)

Family Premium

(Family members are NOT automatically enrolled)

$28.00

MONTHLY EMPLOYEE BENEFIT RATES Premium Rates are Effective November 1, 2016 through October 31, 2017

2016-2017 State Benefits Allocation per Full Time Employee: $780 per month

Important Note Regarding Voluntary Life and AD&D Insurance Benefits These benefits are not paid with District Contributions! These benefits are deducted from your

after-tax income: ✔ Voluntary Life Insurance

✔ Voluntary AD&D Insurance

✔ Voluntary Short-Term Disability

Page 10

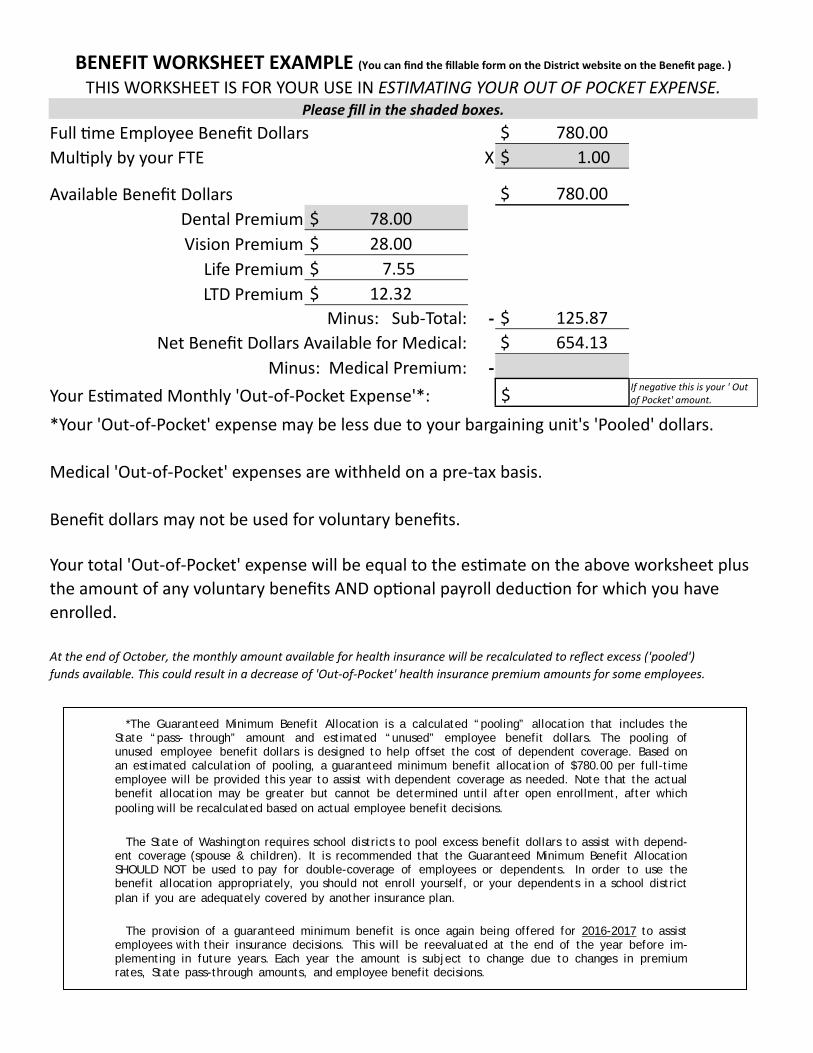

*The Guaranteed Minimum Benefit Allocation is a calculated “pooling” allocation that includes the State “pass- through” amount and estimated “unused” employee benefit dollars. The pooling of unused employee benefit dollars is designed to help offset the cost of dependent coverage. Based on an estimated calculation of pooling, a guaranteed minimum benefit allocation of $780.00 per full-time employee will be provided this year to assist with dependent coverage as needed. Note that the actual benefit allocation may be greater but cannot be determined until after open enrollment, after which pooling will be recalculated based on actual employee benefit decisions.

The State of Washington requires school districts to pool excess benefit dollars to assist with depend-

ent coverage (spouse & children). It is recommended that the Guaranteed Minimum Benefit Allocation SHOULD NOT be used to pay for double-coverage of employees or dependents. In order to use the benefit allocation appropriately, you should not enroll yourself, or your dependents in a school district plan if you are adequately covered by another insurance plan.

The provision of a guaranteed minimum benefit is once again being offered for 2016-2017 to assist

employees with their insurance decisions. This will be reevaluated at the end of the year before im-plementing in future years. Each year the amount is subject to change due to changes in premium rates, State pass-through amounts, and employee benefit decisions.

BENEFIT WORKSHEET EXAMPLE (You can find the fillable form on the District website on the Benefit page. )

THIS WORKSHEET IS FOR YOUR USE IN ESTIMATING YOUR OUT OF POCKET EXPENSE. Please fill in the shaded boxes.

Full me Employee Benefit Dollars $ 780.00

Mul ply by your FTE X $ 1.00

Available Benefit Dollars $ 780.00

Dental Premium $ 78.00

Vision Premium $ 28.00

Life Premium $ 7.55

LTD Premium $ 12.32

Minus: Sub‐Total: ‐ $ 125.87

Net Benefit Dollars Available for Medical: $ 654.13

Minus: Medical Premium: ‐

Your Es mated Monthly 'Out‐of‐Pocket Expense'*: $ If nega ve this is your ' Out of Pocket' amount.

*Your 'Out‐of‐Pocket' expense may be less due to your bargaining unit's 'Pooled' dollars.

Medical 'Out‐of‐Pocket' expenses are withheld on a pre‐tax basis.

Benefit dollars may not be used for voluntary benefits.

Your total 'Out‐of‐Pocket' expense will be equal to the es mate on the above worksheet plus

the amount of any voluntary benefits AND op onal payroll deduc on for which you have

enrolled.

At the end of October, the monthly amount available for health insurance will be recalculated to reflect excess ('pooled')

funds available. This could result in a decrease of 'Out‐of‐Pocket' health insurance premium amounts for some employees.

FAQ: A Quick Guide to the Most Common Questions

Making Changes to Your Coverage: What is a Qualifying Event?

Outside of Open Enrollment, the IRS rules say that your elections cannot be changed unless you experience a life event that qualifies as an official change in status — in other words, a “Qualifying Event.”

Some examples of Qualifying Events include: Birth, adoption, a dependent no

longer eligible, death Marriage, divorce; start or end of a

qualifying domestic partnership Change in employment that affects

eligibility or causes a significant change in cost

Spouse or dependent is provided or loses access to group insurance through his/her employer for the first time

Other rules apply as well. So when you choose your medical plan and the fami-ly members who will have coverage with you, keep in mind that you are usually making a year-long commitment.

But if you do experience a true Quali-fying Event, do not delay! Your applica-tion and applicable documentation to change your benefits must be received within 30 calendar days of the event – otherwise you’ll have to wait until the next Open Enrollment period.

*When adding a newborn, the IRS allows enroll-ment within 60 calendar days of date of birth.

If I change plans may I keep my doctor? That depends on the plan you choose. In many cases the answer is yes, but a few of the plans have a more limited net-work, so check the insurance carrier’s website before you decide.

When may I enroll in the Flexible Spending Plan? You may enroll in the FSA when you’re newly hired, and again each year during the FSA Open Enroll-ment. Re-enrollment is not automatic, so you must actively enroll each year in order to participate.

What plan am I on? Log in to Employee Self Service, check your paystub, con-tact Payroll, log in to your insurance company’s website, look at an old EOB, or call your insurance company to check.

What are my Vision Plan benefits? See page 9 for a summary of your vision benefits through NBN, or visit the Open Enrollment Benefits Website at www.ourpasswordpage.com (password: sksd).

Why is my plan changing? Some plan changes result from changes to federal and state laws. However, most benefits change to help lower premium cost increases. Other reasons may be that the plan is no longer offered by the carri-er, or there is another plan that better fits the needs of employees and their families.

When do Open Enrollment changes take effect? Changes to benefits and plan premiums take effect on November 1. Don’t forget to check your paycheck!

May I enroll in a Health Savings Account (HSA)? Yes, but only if you’re en-rolled on an HSA-Qualified High Deductible Health Plan. Otherwise, you can enroll on an Health Flexible Spending Account (Health FSA).

May I add or drop my medical coverage mid-year? Generally, no. The deci-sions you make during Open Enrollment will remain in place for the entire plan year. The only exceptions occur when you have a “Qualifying Event.” See more information to the right.

When will I receive new medical insurance cards? Due to the volume of en-rollments being processed, some people may not receive their cards until after November 1, but don’t panic! You can often call Customer Service during the first week of November to access all of your member information. If they can’t find your information, call Payroll to confirm your enrollment and to get help.

When I have to pay up-front for a service that is covered by insurance, how do I submit a claim? Complete and submit a claim form which can be found in the Forms section on the Benefits Website or obtained from the insurance car-rier.

How do I submit a reimbursement request for my Flex-Plan? Complete a claim form and mail to Navia Benefit Solutions along with supporting docu-mentation. Navia Benefit Solutions (previously Flex-Plan Services) has recently released a new smartphone app! You can download the app and submit a pic-ture of your bill. You can also submit claims via fax, email, or the web. Don’t forget to keep your receipts!

Can’t find the answer to your question? Call the Open Enrollment Benefits Helpline at 206-957-7066 or toll-free at 1-800-946-7066.

Check your November paycheck! Are your deductions and enroll-ments codes accurately reflecting what you elected during Open En-rollment? If not, don’t delay, con-tact Payroll right away! We will do what we can to get things right for you.

Check Your Paycheck!

Page 11

Patient and Consumer Protections—Required Notices

The world of insurance is complicated, and there are many protections that are built into your plans and into the laws that help keep consumers informed and aware of their rights. You can find all of the notices related to your benefits coverage on the Open Enrollment Benefits Website at www.ourpasswordpage.com (password: “sksd”), but please start here for a brief description of some of these protections:

Summary of Benefits and Coverage (SBC) Notice Complying with the Affordable Care Act of 2009

IMPORTANT NOTICE REGARDING YOUR COVERAGE

The Patient Protection and Affordable Care Act of 2009 requires all group

health insurance plans to provide a Summary of Benefits

and Coverage (SBC) for each of the health

plans offered to eligible employees.

This statement is your notice, as a benefits-eligible employee, that all

available SBCs can be found posted in electronic format at the Employee

Benefits Website at www.ourpasswordpage.com. Use the password “sksd”.

You may also request an SBC be sent directly

to you by calling the Benefits Helpline at (206) 957-7066 or

toll free at (800) 946-7066.

Women’s Health & Cancer Rights: These are a series of protec-tions that require insurers to allow certain minimum amounts of time in the hospital after childbirth. In addition, Federal law specifi-cally requires that insurers provide coverage for mastectomies as well as breast reconstruction after cancer surgery.

Medicare Part D Creditable Coverage: Employees and their family members who are eligible for coverage through Medicare need to maintain creditable prescription drug coverage in order to avoid certain Medicare penalties. Last year, Premera determined that EasyChoice A and the Basic Plan did not provide creditable cover-age with regard to Medicare Part D. The other plans provide cred-itable coverage that is as good as or better than what is available for Medicare-eligible individuals. This determination is made each year.

Genetic Information Nondiscrimination: Employers and health plans are not allowed to request or require that employees undergo a genetic test, and may not collect genetic information about em-ployees or their families in connection with health plan enrollment.

HIPAA Special Enrollment Rights: Generally, the enrollment deci-sions you make during the annual Open Enrollment are irrevocable for the entire year. However, certain changes in your situation will allow you to add or drop coverage. These include marriage, divorce, birth, death, or loss or gain of eligibility for other group coverage. Generally, requests to change coverage must take place within 30 days of the qualifying event.

Notice of Availability and Privacy Practices: Because SKSD spon-sors a self-insured vision plan and a Flexible Benefits Plan adminis-tered by a Third-Party, we distribute a HIPAA “Notice of Privacy Practices” at least once every three years. The Notice of Privacy Prac-tices describes how medical and personal information about you may be used or disclosed and how you can get access to this infor-mation. You can also obtain a copy of the Notice of Privacy Practic-es at any time by going to the District’s Benefits Website.

USERRA Rights: Individuals serving in military also have certain employment and special enrollment rights.

Page 12

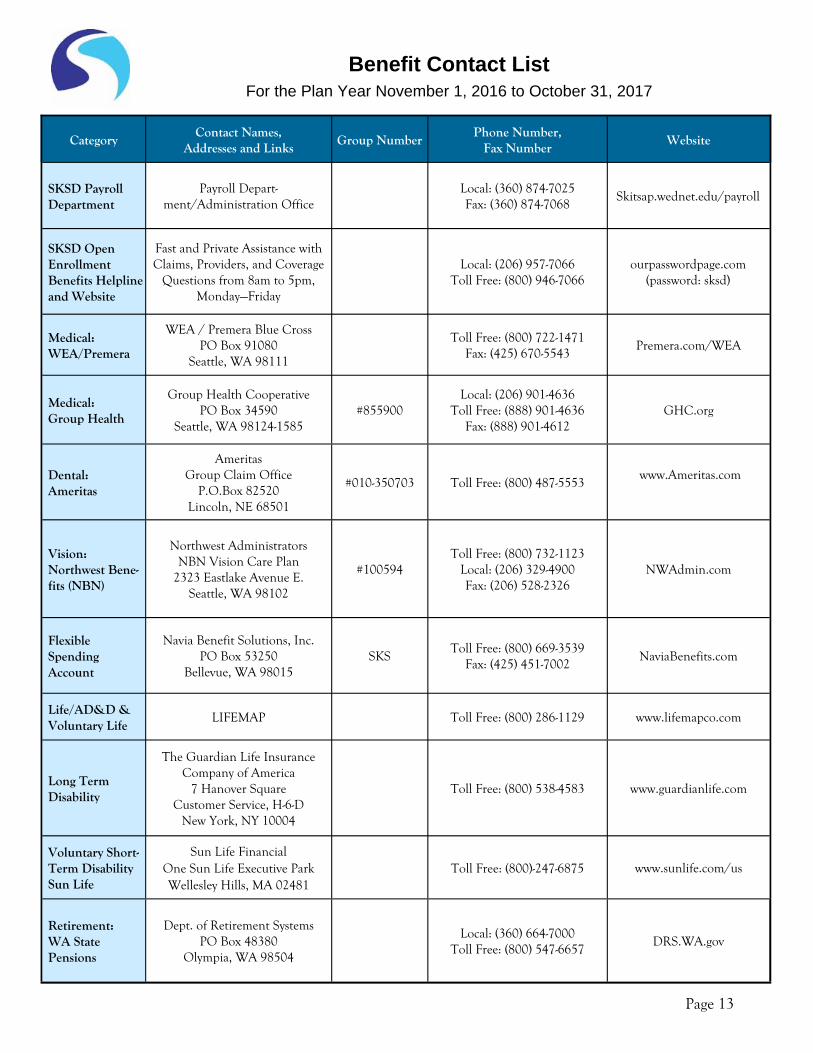

Benefit Contact List For the Plan Year November 1, 2016 to October 31, 2017

Category Contact Names,

Addresses and Links Group Number

Phone Number, Fax Number

Website

SKSD Open Enrollment Benefits Helpline and Website

Fast and Private Assistance with Claims, Providers, and Coverage

Questions from 8am to 5pm, Monday—Friday

Local: (206) 957-7066 Toll Free: (800) 946-7066

ourpasswordpage.com (password: sksd)

Medical: WEA/Premera

WEA / Premera Blue Cross PO Box 91080

Seattle, WA 98111

Toll Free: (800) 722-1471 Fax: (425) 670-5543

Premera.com/WEA

Medical: Group Health

Group Health Cooperative PO Box 34590

Seattle, WA 98124-1585 #855900

Local: (206) 901-4636 Toll Free: (888) 901-4636

Fax: (888) 901-4612 GHC.org

Dental: Ameritas

Ameritas Group Claim Office

P.O.Box 82520 Lincoln, NE 68501

#010-350703 Toll Free: (800) 487-5553 www.Ameritas.com

Vision: Northwest Bene-fits (NBN)

Northwest Administrators NBN Vision Care Plan

2323 Eastlake Avenue E. Seattle, WA 98102

#100594 Toll Free: (800) 732-1123

Local: (206) 329-4900 Fax: (206) 528-2326

NWAdmin.com

Flexible Spending Account

Navia Benefit Solutions, Inc. PO Box 53250

Bellevue, WA 98015 SKS

Toll Free: (800) 669-3539 Fax: (425) 451-7002

NaviaBenefits.com

Life/AD&D & Voluntary Life

LIFEMAP Toll Free: (800) 286-1129 www.lifemapco.com

Long Term Disability

The Guardian Life Insurance Company of America

7 Hanover Square Customer Service, H-6-D

New York, NY 10004

Toll Free: (800) 538-4583 www.guardianlife.com

Retirement: WA State Pensions

Dept. of Retirement Systems PO Box 48380

Olympia, WA 98504

Local: (360) 664-7000 Toll Free: (800) 547-6657

DRS.WA.gov

SKSD Payroll Department

Payroll Depart-ment/Administration Office

Local: (360) 874-7025 Fax: (360) 874-7068

Skitsap.wednet.edu/payroll

Voluntary Short-Term Disability Sun Life

Sun Life Financial One Sun Life Executive ParkWellesley Hills, MA 02481

Toll Free: (800)-247-6875 www.sunlife.com/us

Page 13

WHAT YOU NEED TO DO IMMEDIATELY

Report all workplace injuries to your supervisor immedi-ately and seek medical treatment, if needed. Within 24 hours, complete the SKSD Employee’s Accident/Incident Report (Form 79) and submit to the designated staff in your building or department. This contact person will fax the form to the District Safety Office. By doing so within 24 hours, your supervisor and/or the District Safe-ty Officer, Tom Adams, will be able to investigate, identify, and correct any unsafe condition that may exist in the workplace. Tom Adams can be reached directly at 360-874-6002 or via email at

WORKERS’ COMPENSATION PROGRAM - WORK RELATED INJURY OR OCCUPATIONAL DISEASE INVOLVING MEDICAL TREATMENT

South Kitsap School District is subject to Washington State’s industrial insurance laws and has been approved by Washington State as a self insured employer. Self insured employers must provide all benefits required by law. The Department of Labor and Industries regulates compliance with these laws. Our self insured program applies to work related injuries and occupational disease. By being self insured, the South Kitsap School District as-sumes the cost of medical charges and compensation ex-penses, as well as benefits prescribed by law associated with work related injuries and occupational disease, through our self insured provider (Olympic Educational Service District 114 Workers’ Compensation Trust). Fund-ing for these benefits comes directly from the South Kitsap School District budget; not paid by separate funds or the Department of Labor and Industries.

Medical Treatment

As a Washington worker, you are entitled to treatment from a qualified medical provider of your choice.

Medical Provider’s Office

Tell your medical provider this is a work related injury or occupational disease and that South Kitsap School Dis-trict is a self insured employer. Complete a Physician’s Initial Report and request that it be sent to our self in-sured provider. The claims adjuster will evaluate your claim for eligible benefits.

Self Insured Provider

Olympic Educational Service District 114 Workers’ Compen-sation Trust

Terri Sugg, Claims Adjuster 2530 W 19th St

Port Angeles, W A 98363 Phone: 1-800-643-4369

Complete the Self Insured Accident Report

Contact Landa Fuchs in Business and Support Services at 360-874-7013 or via email at [email protected] to receive a claim number and instructions to file a claim (SIF-2). She will assist you in this process and sub-mit the completed claim to our self insured pro-vider. Olympic Educational Service District Work-ers' Compensation Trust manages claims for South Kitsap School District employees. Terri Sugg is the claims adjuster assigned to our district.

MEDICAL DOCUMENTATION RESPONSIBILITY

All medical provider documents related to your claim must be provided no later that the following business day after your medical appointment. These can be sent to Jenni Ballew, c/o Business and Support Services. She will provide copies to our self insured provider. If you miss work due to your injury, a written clearance is re-quired from your medical provider before you can return to work. Failure to provide medical documentation may result in a delay of eligible benefits.

RETURN TO WORK PROGRAM

South Kitsap School District offers an extensive alterna-tive duty program in our ongoing effort to return in-jured workers to gainful employment within the re-striction necessitated by medical condition. We believe that returning an injured worker to alternative duty can enhance healing and assist the employee’s return to full capacity by moving them from a disabling atmos-phere to one of wellness. We offer both modified and light duty options. We will evaluate each claim on a case-by-case basis to determine whether modified and/or light duty work is available and appropriate.

IMPORTANT!

Your employer cannot deny you the right to file a claim and your employer cannot penalize you or discriminate against you for filing a claim. Every worker is entitled to workers’ compensation benefits for any injury or illness which results from his/her job. Any false claim filed by a worker may be prosecuted to the full extent of the law. If you have questions or concerns, contact Business and Support Services (360-871-7013) Olympic Educational Service District, W orkers’ Compensation Trust (1-800- 643-4369), or the Department of Labor and Industries, Self Insurance Section (360-902-6901).

ADDITIONAL RESOURCES

South Kitsap School District Website, Staff Section www.skitsap.wednet.edu Department of Labor and Industries www.lni.wa.gov

Workers Compensation - Injury Reporting

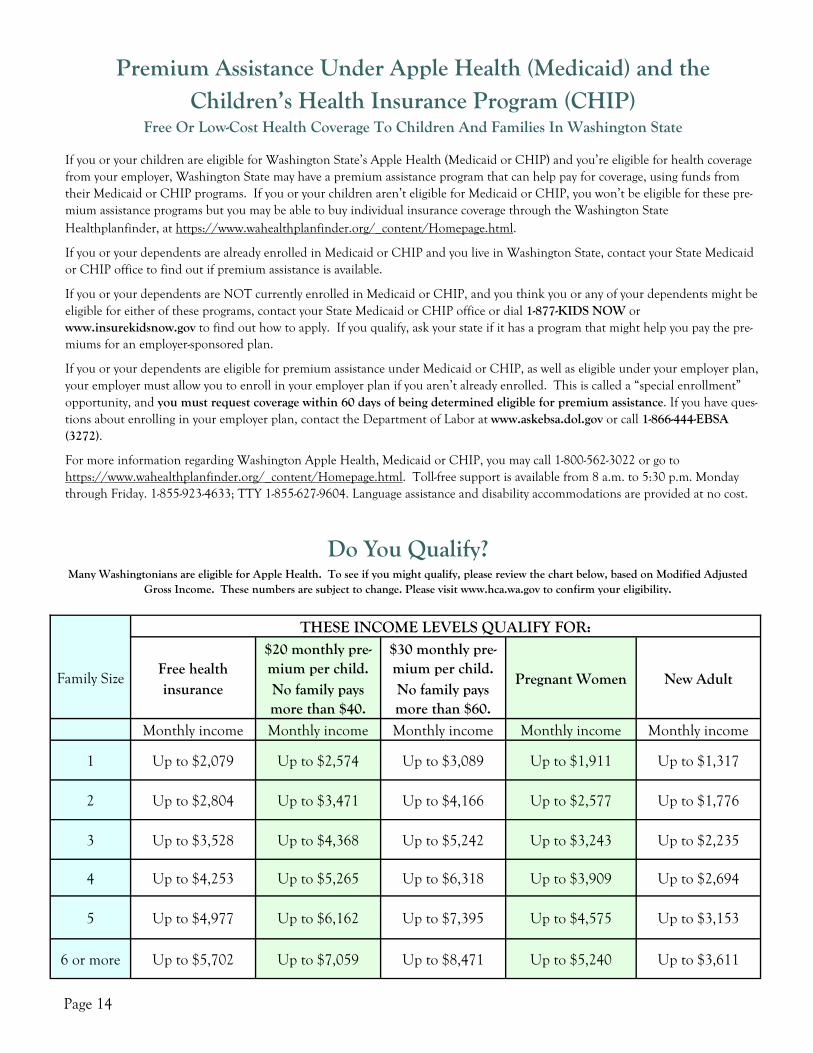

Premium Assistance Under Apple Health (Medicaid) and the Children’s Health Insurance Program (CHIP)

Free Or Low-Cost Health Coverage To Children And Families In Washington State

If you or your children are eligible for Washington State’s Apple Health (Medicaid or CHIP) and you’re eligible for health coverage from your employer, Washington State may have a premium assistance program that can help pay for coverage, using funds from their Medicaid or CHIP programs. If you or your children aren’t eligible for Medicaid or CHIP, you won’t be eligible for these pre-mium assistance programs but you may be able to buy individual insurance coverage through the Washington State Healthplanfinder, at https://www.wahealthplanfinder.org/_content/Homepage.html.

If you or your dependents are already enrolled in Medicaid or CHIP and you live in Washington State, contact your State Medicaid or CHIP office to find out if premium assistance is available.

If you or your dependents are NOT currently enrolled in Medicaid or CHIP, and you think you or any of your dependents might be eligible for either of these programs, contact your State Medicaid or CHIP office or dial 1-877-KIDS NOW or www.insurekidsnow.gov to find out how to apply. If you qualify, ask your state if it has a program that might help you pay the pre-miums for an employer-sponsored plan.

If you or your dependents are eligible for premium assistance under Medicaid or CHIP, as well as eligible under your employer plan, your employer must allow you to enroll in your employer plan if you aren’t already enrolled. This is called a “special enrollment” opportunity, and you must request coverage within 60 days of being determined eligible for premium assistance. If you have ques-tions about enrolling in your employer plan, contact the Department of Labor at www.askebsa.dol.gov or call 1-866-444-EBSA (3272).

For more information regarding Washington Apple Health, Medicaid or CHIP, you may call 1-800-562-3022 or go to https://www.wahealthplanfinder.org/_content/Homepage.html. Toll-free support is available from 8 a.m. to 5:30 p.m. Monday through Friday. 1-855-923-4633; TTY 1-855-627-9604. Language assistance and disability accommodations are provided at no cost.

Do You Qualify? Many Washingtonians are eligible for Apple Health. To see if you might qualify, please review the chart below, based on Modified Adjusted

Gross Income. These numbers are subject to change. Please visit www.hca.wa.gov to confirm your eligibility.

THESE INCOME LEVELS QUALIFY FOR:

Family Size Free health insurance

$20 monthly pre-mium per child.

$30 monthly pre-mium per child.

Pregnant Women New Adult No family pays more than $40.

No family pays more than $60.

Monthly income Monthly income Monthly income Monthly income Monthly income

1 Up to $2,079 Up to $2,574 Up to $3,089 Up to $1,911 Up to $1,317

2 Up to $2,804 Up to $3,471 Up to $4,166 Up to $2,577 Up to $1,776

3 Up to $3,528 Up to $4,368 Up to $5,242 Up to $3,243 Up to $2,235

4 Up to $4,253 Up to $5,265 Up to $6,318 Up to $3,909 Up to $2,694

5 Up to $4,977 Up to $6,162 Up to $7,395 Up to $4,575 Up to $3,153

6 or more Up to $5,702 Up to $7,059 Up to $8,471 Up to $5,240 Up to $3,611

Page 14

New Health Insurance Marketplace Coverage Options and Your Health Coverage

PART A: General Information When key parts of the health care law take effect in 2014, there will be a new way to buy health insurance: the Health

Insurance Marketplace. To assist you as you evaluate options for you and your family, this notice provides some basic

information about the new Marketplace and employmentbased health coverage offered by your employer.

What is the Health Insurance Marketplace?

The Marketplace is designed to help you find health insurance that meets your needs and fits your budget. The

Marketplace offers "one-stop shopping" to find and compare private health insurance options. You may also be eligible

for a new kind of tax credit that lowers your monthly premium right away. Open enrollment for health insurance

coverage through the Marketplace begins in October 2013 for coverage starting as early as January 1, 2014.

Can I Save Money on my Health Insurance Premiums in the Marketplace?

You may qualify to save money and lower your monthly premium, but only if your employer does not offer coverage, or

offers coverage that doesn't meet certain standards. The savings on your premium that you're eligible for depends on

your household income.

Does Employer Health Coverage Affect Eligibility for Premium Savings through the Marketplace?

Yes. If you have an offer of health coverage from your employer that meets certain standards, you will not be eligible

for a tax credit through the Marketplace and may wish to enroll in your employer's health plan. However, you may be

eligible for a tax credit that lowers your monthly premium, or a reduction in certain cost-sharing if your employer does

not offer coverage to you at all or does not offer coverage that meets certain standards. If the cost of a plan from your

employer that would cover you (and not any other members of your family) is more than 9.5% of your household

income for the year, or if the coverage your employer provides does not meet the "minimum value" standard set by the

Affordable Care Act, you may be eligible for a tax credit.1

Note: If you purchase a health plan through the Marketplace instead of accepting health coverage offered by your

employer, then you may lose the employer contribution (if any) to the employer-offered coverage. Also, this employer

contribution -as well as your employee contribution to employer-offered coverage- is often excluded from income for

Federal and State income tax purposes. Your payments for coverage through the Marketplace are made on an after-

tax basis.

How Can I Get More Information?

For more information about your coverage offered by your employer, please check your summary plan description or

contact .

The Marketplace can help you evaluate your coverage options, including your eligibility for coverage through the

Marketplace and its cost. Please visit HealthCare.gov for more information, including an online application for health

insurance coverage and contact information for a Health Insurance Marketplace in your area.

1 An employer-sponsored health plan meets the "minimum value standard" if the plan's share of the total allowed benefit costs covered

by the plan is no less than 60 percent of such costs.

Form Approved OMB No. 1210-0149 (expires 1-31-2017)

Payroll Department at South Kitsap School District.

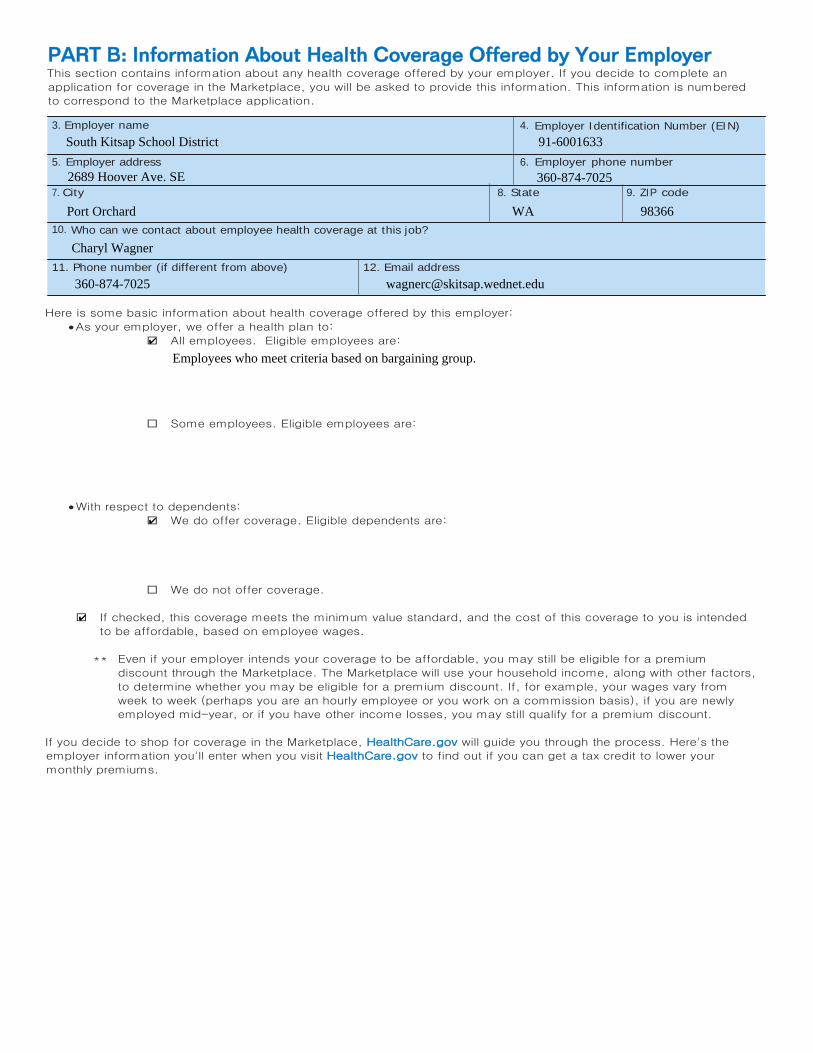

PART B: Information About Health Coverage Offered by Your Employer This section contains information about any health coverage offered by your employer. If you decide to complete an

application for coverage in the Marketplace, you will be asked to provide this information. This information is numbered

to correspond to the Marketplace application.

3. Employer name 4. Employer Identification Number (EIN)

5. Employer address 6. Employer phone number

7. City 8. State 9. ZIP code

10. Who can we contact about employee health coverage at this job?

11. Phone number (if different from above) 12. Email address

Here is some basic information about health coverage offered by this employer:

• As your employer, we offer a health plan to:

All employees. Eligible employees are:

Some employees. Eligible employees are:

• With respect to dependents:

We do offer coverage. Eligible dependents are:

We do not offer coverage.

If checked, this coverage meets the minimum value standard, and the cost of this coverage to you is intended

to be affordable, based on employee wages.

** Even if your employer intends your coverage to be affordable, you may still be eligible for a premium

discount through the Marketplace. The Marketplace will use your household income, along with other factors,

to determine whether you may be eligible for a premium discount. If, for example, your wages vary from

week to week (perhaps you are an hourly employee or you work on a commission basis), if you are newly

employed mid-year, or if you have other income losses, you may still qualify for a premium discount.

If you decide to shop for coverage in the Marketplace, HealthCare.gov will guide you through the process. Here's the

employer information you'll enter when you visit HealthCare.gov to find out if you can get a tax credit to lower your

monthly premiums.

South Kitsap School District 91-6001633

2689 Hoover Ave. SE 360-874-7025

Port Orchard WA 98366

Charyl Wagner

360-874-7025 [email protected]

✔

✔

✔

Employees who meet criteria based on bargaining group.

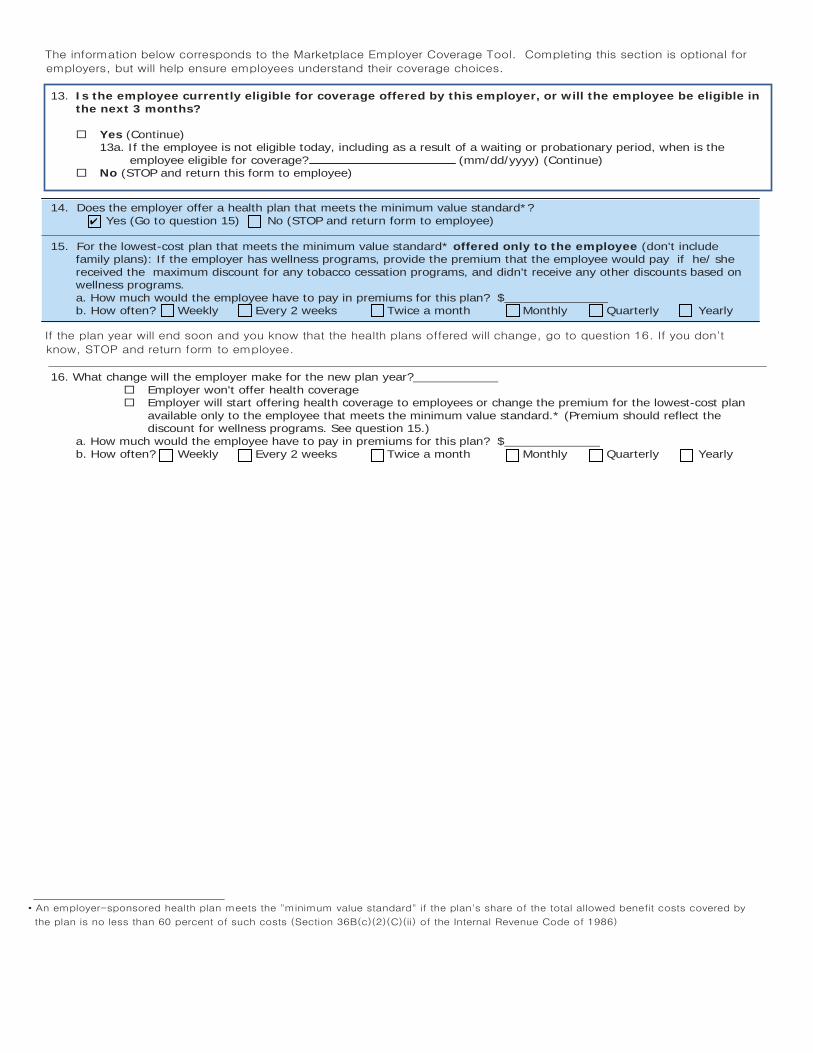

The information below corresponds to the Marketplace Employer Coverage Tool. Completing this section is optional for

employers, but will help ensure employees understand their coverage choices.

13. Is the employee currently eligible for coverage offered by this employer, or will the employee be eligible inthe next 3 months?

Yes (Continue)13a. If the employee is not eligible today, including as a result of a waiting or probationary period, when is the

employee eligible for coverage? (mm/dd/yyyy) (Continue) No (STOP and return this form to employee)

14. Does the employer offer a health plan that meets the minimum value standard*?Yes (Go to question 15) No (STOP and return form to employee)

15. For the lowest-cost plan that meets the minimum value standard* offered only to the employee (don't includefamily plans): If the employer has wellness programs, provide the premium that the employee would pay if he/ shereceived the maximum discount for any tobacco cessation programs, and didn't receive any other discounts based onwellness programs.a. How much would the employee have to pay in premiums for this plan? $b. How often? Weekly Every 2 weeks Twice a month Monthly Quarterly Yearly

If the plan year will end soon and you know that the health plans offered will change, go to question 16. If you don't

know, STOP and return form to employee.

16. What change will the employer make for the new plan year? Employer won't offer health coverage Employer will start offering health coverage to employees or change the premium for the lowest-cost plan

available only to the employee that meets the minimum value standard.* (Premium should reflect the discount for wellness programs. See question 15.)

a. How much would the employee have to pay in premiums for this plan? $b. How often? Weekly Every 2 weeks Twice a month Monthly Quarterly Yearly

• An employer-sponsored health plan meets the "minimum value standard" if the plan's share of the total allowed benefit costs covered by

the plan is no less than 60 percent of such costs (Section 36B(c)(2)(C)(ii) of the Internal Revenue Code of 1986)

✔

South Kitsap School District - COBRA Initial Notice

**Continuation Coverage Rights Under COBRA**

Introduction

You’re getting this notice because you recently gained coverage under a South Kitsap School District group health plan (the Plan). This notice has important information about your right to COBRA continuation coverage, which is a temporary extension of coverage under the Plan. This notice explains COBRA continuation coverage, when it may become available to you and your family, and what you need to do to protect your right to get it. When you become eligible for COBRA, you may also become eligible for other coverage options that may cost less than COBRA continuation coverage.

The right to COBRA continuation coverage was created by a federal law, the Consolidated Omnibus Budget Reconciliation Act of 1985 (COBRA). COBRA continuation coverage can become available to you and other members of your family when group health coverage would otherwise end. For more information about your rights and obligations under the Plan and under federal law, you should review the Plan’s Summary Plan Description or contact the Plan Administrator.

You may have other options available to you when you lose group health coverage. For example, you may be eligible to buy an individ-ual plan through the Health Insurance Marketplace. By enrolling in coverage through the Marketplace, you may qualify for lower costs on your monthly premiums and lower out-of-pocket costs. Additionally, you may qualify for a 30-day special enrollment period for another group health plan for which you are eligible (such as a spouse’s plan), even if that plan generally doesn’t accept late enrollees.

What is COBRA continuation coverage?

COBRA continuation coverage is a continuation of Plan coverage when it would otherwise end because of a life event. This is also called a “qualifying event.” Specific qualifying events are listed later in this notice. After a qualifying event, COBRA continuation cov-erage must be offered to each person who is a “qualified beneficiary.” You, your spouse, and your dependent children could become qualified beneficiaries if coverage under the Plan is lost because of the qualifying event. Under the Plan, qualified beneficiaries who elect COBRA continuation coverage must pay for COBRA continuation coverage.

If you’re an employee, you’ll become a qualified beneficiary if you lose your coverage under the Plan because of the following qualifying events:

Your hours of employment are reduced, or Your employment ends for any reason other than your gross misconduct.

If you’re the spouse of an employee, you’ll become a qualified beneficiary if you lose your coverage under the Plan because of the fol-lowing qualifying events:

Your spouse dies; Your spouse’s hours of employment are reduced; Your spouse’s employment ends for any reason other than his or her gross misconduct; Your spouse becomes entitled to Medicare benefits (under Part A, Part B, or both); or You become divorced or legally separated from your spouse.

Your dependent children will become qualified beneficiaries if they lose coverage under the Plan because of the following qualifying events:

The parent-employee dies; The parent-employee’s hours of employment are reduced; The parent-employee’s employment ends for any reason other than his or her gross misconduct; The parent-employee becomes entitled to Medicare benefits (Part A, Part B, or both); The parents become divorced or legally separated; or The child stops being eligible for coverage under the Plan as a “dependent child.”

When is COBRA continuation coverage available?

The Plan will offer COBRA continuation coverage to qualified beneficiaries only after the Plan Administrator has been notified that a qualifying event has occurred. The employer must notify the Plan Administrator of the following qualifying events:

The end of employment or reduction of hours of employment; Death of the employee; or The employee’s becoming entitled to Medicare benefits (under Part A, Part B, or both).

For all other qualifying events (divorce or legal separation of the employee and spouse or a dependent child’s losing eligibility for coverage as a dependent child), you must notify the Plan Administrator within 60 days after the qualifying event occurs. Please notify, in writing:

South Kitsap School District Payroll Office Attn: Charyl Wagner 2689 Hoover Ave SE Port Orchard, WA 98366

For some qualifying events (e.g., divorce or legal separation), you must also supply the appropriate legal documentation.

How is COBRA continuation coverage provided?

Once the Plan Administrator receives notice that a qualifying event has occurred, COBRA continuation coverage will be offered to each of the qualified beneficiaries. Each qualified beneficiary will have an independent right to elect COBRA continuation coverage. Covered employees may elect COBRA continuation coverage on behalf of their spouses, and parents may elect COBRA continuation coverage on behalf of their children.

COBRA continuation coverage is a temporary continuation of coverage that generally lasts for 18 months due to employment termina-tion or reduction of hours of work. Certain qualifying events, or a second qualifying event during the initial period of coverage, may permit a beneficiary to receive a maximum of 36 months of coverage.

There are also ways in which this 18-month period of COBRA continuation coverage can be extended: