smart option for planning for retirement, now at bealelee.com

TRANSCRIPT

©2012 Brookstone Capital Management, LLC. All rights reserved. 1172012

Where do you think

we‟re headed?History Shows that the market typically

moves in cycles. In the past 105 years, there

have been three bull markets and three bear

markets. The chart shows that we may have

entered a bear market.

Value of the Dow Jones Industrial Average for 105 Years (1906-2011)

Bull

Bear

18 Years

5 Years25 Years

11 Years

17 Years

17 Years

1906-1924 1925-

1929

1930-1954 1955-1965 1966-1982 1983-1999 2000-?

What do investors want?

Not to lose money

Hope to get or stay rich

Banish fear of being poor

Leave money to kids and or spend money in retirement

How will you get there?

Adding new managers that will enhance your current mix of investments and

supplement them during an economic cycle when

traditional investments do not work.

How will you get there?

Typically, investors have used

three strategies to get there:

1. Asset allocation

2. Market timing

3. Buy and hold

Diversification works…Asset Class Examples Using Vanguard Mutual Funds

Timeline goes from top of the Tech Bubble through the bear market of

2000-2002 and recovery to the peak in October 2007

S&P500

Pacific Index

REIT Index

Small Cap

Total Bond Index

European Index

Emerging Markets

until it doesn‟t…

S&P500

Pacific Index

REIT Index

Small Cap

Total Bond Index

European Index

Emerging Markets

Asset Class Examples Using Vanguard Mutual FundsAfter October 2007, equities marched in relative unison.

Bonds offered the only significant diversification.

SMARToption

Find Non-Correlated AssetsCorrelation Sphere

Traditional

investment assets

correlate to “1” in

this area

Hedged Equity

Market timing• The idea is to move money to

bonds and cash when the market

is going to go down

OR• Tactically move between asset

classes during different cycles in

the economy

• Timing the market involves calling

it right twice, not just once, and

that's nearly impossible

Market timing

• Most investors tend to let the competing

emotions of fear and greed dictate their

investment decisions

• This leads to the tendency to invest after a

significant increase in prices and sell during

down periods, the opposite of buying low and

selling high.

Market timing

• This phenomenon has been widely

documented, included in a 2003 Dalbar

Study*

• It shows that the average investor

stayed invested in equity funds for less

than 3 years, buying when stocks went

up and selling when the going got tough

*2003 Dalbar, Inc., “Quantitative Analysis of Investment Behavior”.

Market timing

The end result was that investors earned an

average of 2.57% from 1984 to 2003, a

hair below inflation of 3.14%, and far short

of the 12.2% annual gain on the S&P 500

for the same period

Market timingThe record on professionals timing the market is just as

abysmal.

• The Hulbert Financial Digest* has tracked what would have

happened if every year an investor put his money into the

prior year‟s top performing market timing newsletter.

• Over 21 years the result would have been an annualized

loss of 31.4 percent a year.

• In the real world, that‟s equivalent to investing $10,000 in

January 1981 and finding that all you have left at the end of

2002 is $2.32.

*Mark Hulbert, Hulbert Financial Digest, http://www.fundadvice.com/FEhtml/PsychHurdles/0304b.html

Market timing

The Bottom Line: It is very difficult to

time the market successfully!

Buy and Hold Investors

American Airlines1980 to January 12, 2012

$4.44

$8

$13.62$20.87

$36.13

$2.34

$37.05

$0.32

Buy and Hold Investors

Eastman Kodak1962 to January 12, 2012

1972

$66

1987

$68

1996

$80

2009

$2.96

1/2012

$0.52

Buy and Hold Investors

Microsoft2000 to January 12, 2012

April 3, 2000

$32.53 January 23, 2012

$25.70

Buy and Hold Investors

If you bought and held a 60/40

portfolio* (stocks/bonds),

what it would have done…

e.g. 2008

30%

OR

If you bought the S&P 500

in 2000 and held it through

2011

You would be about even

*Lipper Diversified Growth and Income Index

Are there other financial

tools I can use to protect

and grow wealth?

THE STRIKING PRICE | SATURDAY, JANUARY 8, 2011

By STEVEN M. SEARS

Using options to manage the risk of a downturn

may be a good idea.

How to Collar a Black Swan

“…pension funds and other institutional

investors …can no longer rely solely on

macro-economic analysis to adjust portfolios.

They have to be cognizant of tail risk and risk

management on an ongoing basis. The idea

of tail risk, essentially that the unexpected will

happen from time to time, is one of the key

traits of the modern stock market”.

Joann Hill, ProShares Head of Investment Strategies (2010 IMN Superbowl of Indexing keynote presentation).

“alternative strategies that include options add value to a

portfolio and outperform traditional strategies in risk

reduction”

What are other Institutional

investors saying?

“portfolio managers that do not use options can not

adequately protect against market risk”.

James E. Keohane, Healthcare of Ontario Pension Plan Senior Vice-President (2010 IMN Superbowl of Indexing presentation).

How Options Work

Options are:Contracts to either BUY or SELL a specific

investment at a specific price

The purchase price of an option is called the

PREMIUM – you pay for

this if you exercise your

option or not.

Options:The contracts establish a specific price called the

STRIKE PRICE at which the contract may be

exercised

OPTIONS have a shelf life –

Also called an expiration date,

which is the latest date you can

“exercise” you option or close out your position

There are two types of

Options

CALLS and PUTS

CALL = BuyThe purchase of a call option gives the owner the

right but not the obligation to BUY 100 shares of the

underlying security at the STRIKE price on or before

the expiration date.

The buyer has the right but not the obligation

to BUY the shares.

The seller of the option does have the obligation

to sell the shares to the buyer.

PUT = SellConversely, the purchase of a put option

gives the owner the right but not the

obligation to SELL 100 shares of the

underlying security at the STRIKE

price at anytime before the expiration

date.

In this case the seller of the put is required to

buy the security at the strike price at the

buyer‟s request.

Buyers of options

Including both puts and calls spend money.

They pay the premium.

Including both puts and calls collect money.

They collect the premium.

Seller of options

3 Ways SMARToption Uses Options

1. Buy long-term puts

2. Sell short-term covered calls

3. Sell short-term puts

PUT OptionsPut options are usually purchased as protection

against falling stock prices. You pay the premium

upfront so that if the underlying stock falls below

the strike price, your potential loss is limited.

This protective put works like an insurance policy.

PUT OptionsIf you buy a put option on the S&P 500 (SPY):

You pay some money upfront, and you have the right to sell SPY

at a certain price, no matter how much SPY declines. If SPY goes

below your strike price, the value of you put will increase. The

more the SPY falls, the higher your put will be worth.

You can sell the put for a profit anytime before the expiration date.

If the SPY stays above the strike price, you still can sell the put

anytime before the expiration date, but for less than what you paid.

The Covered Call A strategy in which an investor sells or “writes” a call optioncontract while at the same time owning an equivalentnumber of shares of the underlying stock or index fund, likeSPY.

The stock or index fund is generally held in the samebrokerage account from which the investor writes thecall, and fully collateralizes, or "covers," the obligationconveyed by writing a call option contract.

This strategy is the most basic and most widely usedstrategy combining the flexibility of listed options with stockownership.

The Covered Call • If you sell a covered call on the SPY, you collect

some money upfront, and you have the obligationto deliver your shares of SPY if it hits the strikeprice.

• If SPY stays below the strike price, you get to keepthe premium you collected.

• If SPY approaches the strike price, instead ofwaiting for your shares of SPY to be “called away”you can buy the calls back and close the position.

PUT OptionsIf you sell a put option on the SPY:You collect the premium immediately adding cash to you

account, and you have the obligation to buy shares of SPY if

it hits the strike price.

If SPY stays above the strike price, you get to keep the

premium you collected

If SPY approaches the strike price, instead of being forced to

buy SPY at that price, you can buy the puts back and close

out the position.

Are options risky?

Not any more risky than buying astock is risky.

It‟s the investment strategy that cansignificantly lower risks, not the optionsthemselves.

When correctly applied and activelymanaged they can be tailored for specificpurposes and market conditions.

Are options risky?

When incorrectly applied or leftunmanaged, these strategies can exposeinvestors to unacceptable losses.

In the past when these strategies failed, theymade headlines in the news.

Options ended up with the blameinstead of the investment strategy.

Are options risky?

► OCC is a participant in every options transaction,serving as the intermediary between buyers andsellers.

► You do not deal with any person on the other sideof the transaction, you are dealing with the OCC

► OCC issues, guarantees and clears all option tradesplaced on the U.S. options exchanges.

► Ensures that all of the rules involved in the salestransactions will be followed and that each side willperform as promised.

The Options Clearing

Corporation (OCC)

The use of exchange-listed

options has been growing

at a phenomenal rate.

*2010 Options Industry Council Benchmark Study

In the last ten years trading

volume has increased by

nearly 500%, with more than

3.8 billion contracts traded in

2010.*

500

%

1.Generate income

2.Hedging

3.Diversification

4.Locking in profits

Why should you have options

in your portfolio?

How SMARToption works

A two-pronged approach that

mathematically minimizes large losses in

your portfolio

Hedged Equity Strategy

+ Proprietary Monthly

Trading Strategy

How SMARToption works

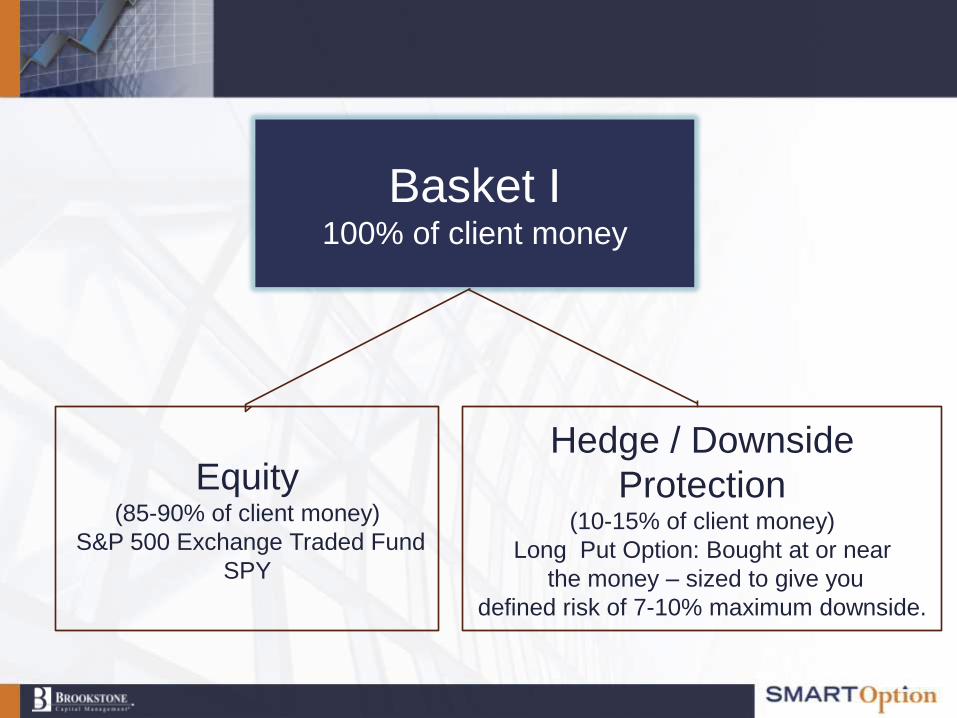

SMARToption

Basket IEquity + Hedge/Downside

Protection

Basket IIMonthly Options Trading

Consists of:

• S&P 500 exchange traded fund

• a put option to minimize risk

The option portion of Basket I is specifically designed to limit a portfolio‟s

exposure to falling markets. The option component is an investment

similar to an insurance policy on your house. The deductible for this

policy (amount you pay for protection) is specifically chosen to limit (not

eliminate) losses.

Basket I

If Market is Put is

Basket I100% of client money

Hedge / Downside

Protection(10-15% of client money)

Long Put Option: Bought at or near

the money – sized to give you

defined risk of 7-10% maximum downside.

Equity(85-90% of client money)

S&P 500 Exchange Traded Fund

SPY

By investing in a broad-based index fund such as SPY, it

automatically reduces company/ sector risk through

diversification across multiple companies and even markets

(e.g.US/International).

Buying and holding the index ETF also eliminates futile

attempts in market timing and/or predicting future values of

individual stocks.

This strategy is possible because protection from significant

declines does not come from prophesy but from the Basket I

hedge.

Basket I

Basket IIWe sell out of the money

Puts and Calls against our positions in

Basket I

(Brings cash into the account)

1. Sell Put on SPY 2. Sell Call on SPY

When puts and calls are sold, they generate

premium or „income‟ that is added to your account.

This independent income generating component of

the strategy generates income to the account in all

market conditions.

Basket II

This income also helps to offset the cost of the hedge used

in Basket I. It incorporates multiple specified adjustment and

liquidation points to minimize risk and maximize the

frequency and size of monthly returns.

These adjustment and liquidation points were extensively

back-tested and then proven through implementation over

the past 14 years.

Basket II has been quantitatively designed in type, size, &

frequency to provide market-neutral returns.

Basket II

Basket II – Selling out of the money

Puts and Calls against our positions in Basket I1. Sell a put

2. Sell a call

1. Put strike

price

2. Call strike

priceS&P 500 current

market price

Sweet spot over the

market. Take profits on

both the put and call if

market remains within

sweet spot

If the market moves down

toward put strike, we have

a stop order to buy back

the put here

If the market moves up

toward call strike, we

have a stop order to

buy back the call here

Put in the $ Call in the $

Basket II

Adjustments

Original Put

strike price

Original Call

closed for

profit

S&P 500

original price

Sweet spot over the

market moves with

the market

If the market moves down

toward put strike, we have

adjustment points that

enable us to stay in the

trade and increase the

probability of success to

over 80%

If the market moves

down toward put

strike, we will take

profits on the original

call and sell a new

call which brings in

more premium

S&P 500

new price

New Call

Basket I - 100% of a client‟s portfolio is invested in Basket I. 85-90% is

invested in SPY equity shares and 10-15% is invested in a hedge through a

long-term option on SPY.

SMARToption‟s – 2 components

Basket II is an independent income generating component

of the strategy which has been quantitatively designed in

type, size, & frequency to provide market-neutral returns.*

*Based on past performance

The proof is in the

performance.

The Key to SMARToption‟s Success

Bull

Bear

UpsideCapture has

averaged 70% of

the S&P 500

returns in bull

markets

Downside Capture

has averaged 5% of the

S&P 500 returns in bear

markets

100%

-100%

70%

-5%

SMARToption captures substantial

upside in bull marketsand minimizes losses

in bear markets!

Market CyclesSMARToption vs S&P 500*

SMARToption* S&P 500

Bull 1 49.23% 71.17%

Bear 1 24.41% -37.61%

Bull 2 53.61% 82.85%

Bear 2 -3.60% -37.00%

Bull 3 44.50% 48.97%

Important Notes: All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is no guarantee of future results and there can be

no assurance, and clients should not assume, that future performance will be comparable to past performance.

*Since inception, 1997, gross of fees

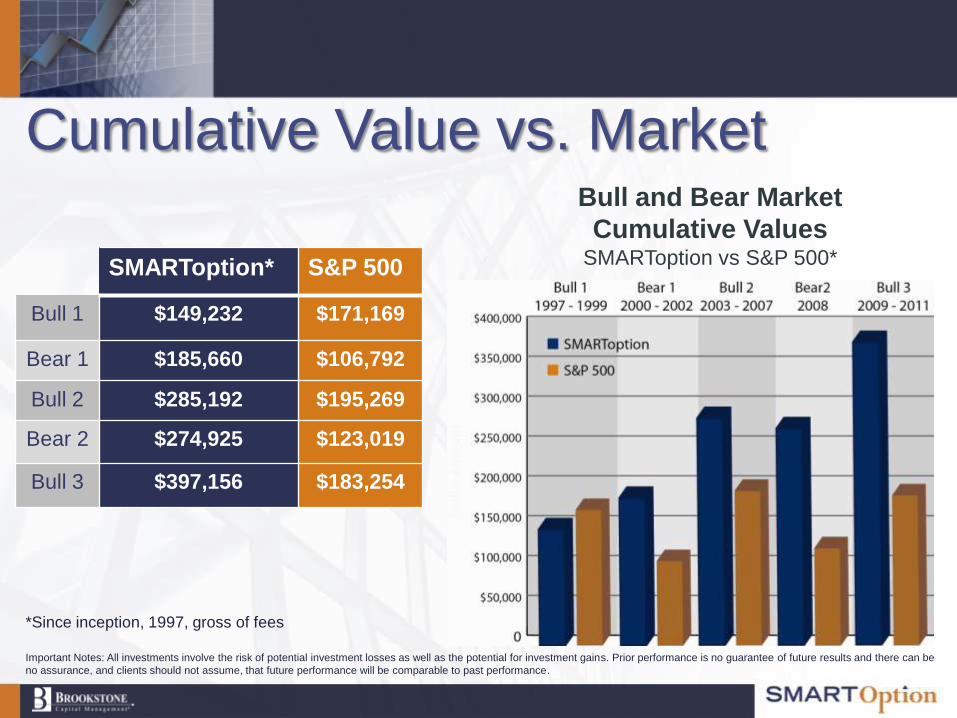

Cumulative Value vs. MarketBull and Bear Market

Cumulative ValuesSMARToption vs S&P 500*SMARToption* S&P 500

Bull 1 $149,232 $171,169

Bear 1 $185,660 $106,792

Bull 2 $285,192 $195,269

Bear 2 $274,925 $123,019

Bull 3 $397,156 $183,254

Important Notes: All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is no guarantee of future results and there can be

no assurance, and clients should not assume, that future performance will be comparable to past performance.

*Since inception, 1997, gross of fees

The Key to SMARToption‟s SuccessDown Years for the S&P 500*

From 2000-

2002, hedging

protected the

downside and

actually provided a

profit!

In 2008, when S&P

500 lost 37%, we

were down only

3.6% before fees!

Prevent large losses!

8.42%

-9.10%

12.97%

-11.89%

12.22%

-22.10%

-3.6%

-37.00%

Important Notes: All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is no guarantee of future results and there can be

no assurance, and clients should not assume, that future performance will be comparable to past performance.

*Since inception, 1997, gross of fees

Reduces Risk

Increases Returns Risk vs. Return1997- 2011

Risk – Standard Deviation

An

nu

ali

zed

Retu

rn

Important Notes: All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is no guarantee of future results and there can be

no assurance, and clients should not assume, that future performance will be comparable to past performance.

Client in SMARToption

since 1997

Aggregate Growth vs. Indices*1997 – 2011

4.5

4.0

3.5

3.0

2.5

2.0

1.5

1.012/97 12/99 12/01 12/03 12/05 12/07 12/09

SMARToption

S&P 500

Important Notes: All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is no guarantee of future results and there can be

no assurance, and clients should not assume, that future performance will be comparable to past performance.

*Net of fees

If you are in the market and not

hedged when the market drops

40%, it’s a lifestyle change!

Take the Good with the bad

Client in SMARToption

since 2003Aggregate Growth vs. Indices*

2003 – 20112.6

2.4

2.2

2.0

1.8

1.6

1.4

1.2

1.0

SMARToption

S&P 500

1/04 1/05 1/06 1/07 1/08 1/09 1/10 1/11

Important Notes: All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is no guarantee of future results and there can be

no assurance, and clients should not assume, that future performance will be comparable to past performance.

*Net of fees

The proof is in the performanceSMARToption vs S&P 500

Cumulative Returns 1997 – 2011

SMARToption (Gross of Fees)

S&P 500

297%

83%

Important Notes: All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is no guarantee of future results and there can be

no assurance, and clients should not assume, that future performance will be comparable to past performance.

The proof is in the performance

SMARToption (Gross of Fees)

S&P 500

$183,254

$397,156

Growth of $100,000

Cumulative Returns 1997 – 2011

Important Notes: All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is no guarantee of future results and there can be

no assurance, and clients should not assume, that future performance will be comparable to past performance.

GIPS®

In the past, investors had great difficulty obtaining meaningful

comparisons of accurate investment performance data.

Making apples-to-apples comparisons of investment

performance was problematic,

and the existence of country-specific

guidelines for performance presentation

further complicated matters.

Are a big deal!

There was a need for a practitioner-driven set of ethical

principles and a standardized, industry-wide approach to

calculating and reporting investment results.

The foundation for the GIPS standards

was first established in 1987.

To develop one globally accepted

set of standards, the GIPS

committee began work in 1995 to get

them formally endorsed

Are a big deal!

After an extensive period of public comment, the AIMR Board

of Governors (now known as the CFA Institute) formally

endorsed the GIPS standards in February 1999.

Since their introduction, the GIPS standards have gathered

momentum with investment management firms worldwide

adopting these voluntary, ethical standards for calculating

and presenting historical investment performance.

Organizations in 34 countries sponsor and promote the

standards.

Are a big deal!

• GIPS compliant firms voluntarily go beyond legal reporting

requirements to demonstrate a commitment to open,

honest, and ethical practices.

• To claim compliance, an investment firm must demonstrate

adherence to comprehensive and rigorous rules governing

input data, calculation methodology, composite

construction, disclosures, and presentation and reporting.

• GIPS compliant firms must have their data audited and

verified by a qualified third party firm.

Are a big deal!

Investments that adhere to GIPS® should assure

investors that the firms’ investment performance

is complete and fairly presented.

Are a big deal!

Fees

Fees

How can we do this?

SMARToption will have a SET FEE SCHEDULE!

Fees will be deducted quarterly for a total of 2.25% annually.

The FEE SCHEDULE is not-negotiable and cannot be altered.

You will not see any other fees taken out of your account

NO transaction fees

NO ticket charges

NO trading costs

Wrap fee structure

A wrap fee structure is where both:

● Asset management fees for advisory services

● Transaction fees for execution services

are wrapped into a single fee charged to the client.

In a Wrap Fee arrangement, a client’s costs are the

same regardless of the number of transactions in an

account.

Total Expense Structure

The underlying vehicle is an S&P 500 ETF,

which has a very low expense ratio of

0.0945%.

TOTAL ANNUAL FEE: 2.25% + 0.0945 = 2.3445%

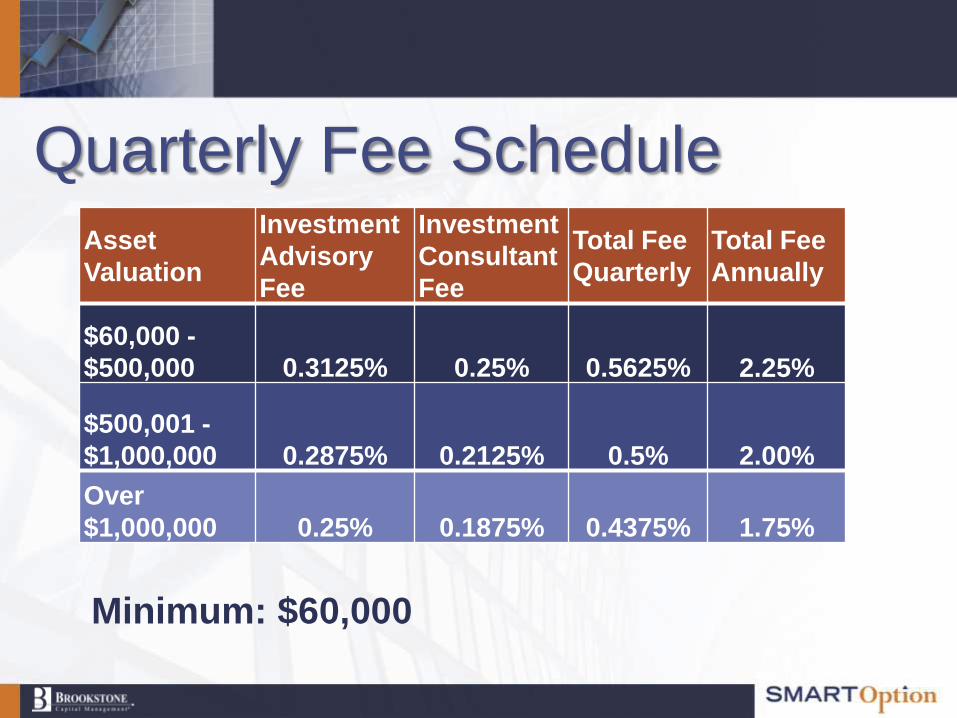

Quarterly Fee Schedule

Asset

Valuation

Investment

Advisory

Fee

Investment

Consultant

Fee

Total Fee

Quarterly

Total Fee

Annually

$60,000 -

$500,000 0.3125% 0.25% 0.5625% 2.25%

$500,001 -

$1,000,000 0.2875% 0.2125% 0.5% 2.00%

Over

$1,000,000 0.25% 0.1875% 0.4375% 1.75%

Minimum: $60,000

It‟s all about transparency

► With fee-based money management youknow what you are paying for upfront.

► Your advisor’s interest is in-line with yours.The better your investments performs thehigher the fee they will receive.

► When compared to other fee structures forcomparable products, this fee schedule isquite reasonable.

Expense Ratios► According to the Investment Company Institute (ICI) the average

expense ratio for a mutual fund that is actively managed is 1.45%.

► This includes fees paid to the manager of the fund, administrative

costs, marketing and distribution services.

► The expense ratio is not deducted from your account, rather the

investment return you receive is already net of the fees.

► Plus on top of that you will also pay your advisor a fee. Typically

1%-2%.

► Assuming 1.5% (advisory fee) + 1.45% (average expense ratio

mutual fund) this brings the total cost of owning a mutual fund to

about 3.0%, not to mention trading and transaction fees that may

apply!

This Putnam Fund has an expense ratio of

1.58%

+ 1.50% Management fee + Other transaction costs $$$

► The underlying holdings in the account consist of an

ETF (SPY) and options (puts and calls), all of which

are highly-traded, marketable securities.

Therefore, the strategy is 100% liquid at all times as

we could simply sell these securities if needed at any

time.

► To optimize the strategy, we would strongly

discourage you from taking funds out of the

SMARToption Model, so that you can receive the full

benefit of the model‟s performance.

Liquidity

► SMARToption is positioned as the core “growth”

strategy and so short-term liquidity should be

addressed elsewhere in your financial plan.

Liquidity

Technology

Technology AdvantageOne of the most sophisticated and highest performing

strategies in the industry, SMARToption requires advanced

technology to be able to implement across thousands of

accounts.

►We have developed a proprietary electronic system which

facilitates implementation, monitoring, and adjustment of the

strategy.

►By specifically designing our interface consistent with our

strategy, we have dramatically simplified implementation and

management activities such as trading, new account

investment, reporting, etc.

OperationsTrading Systems

● Broker-Specific Trading and Order Management Systems

● Proprietary/Custom Trader Software

Monitoring/Coverage

● Continuous oversight /monitoring during trading hours

● Multiple traders monitoring positions and executions (redundancy)

● Automated email/phone notifications on market price, adjustment &

liquidation points

Back Office/Reporting

● Captools (GIPS® Compliant) performance software

Industry Recognition

SMARToption‟s

Recognition and Awards

5 Star Rated for

3 Years

2008-2009-2010

SMARToption‟s

Recognition and Awards

#1Market-Neutral

Manager

For 1 and 5 Years**August 22, 2011

SMARToption‟s

Recognition and Awards

3, 5, 7 and 10 YearsTop 1% of Large Cap Money Managers

for Returns* *As of 2010

SMARToption‟s

Recognition and Awards

3, 5, 7 and 10 YearsTop 1% of Large Cap Money Managers

for Low Risk* *As of 2010

SMARToption‟s

Recognition and Awards

3 Years(among the top 10 performers in its peer group of

several thousand large cap money managers as

maintained by Informa Investment Solutions)

PSN TOP Gun

GIPS® compliant (verified through end of 2010)

demonstrated returns over 14 years.

SMARToption‟s

Recognition and Awards

In bull, bear and flat market conditions

Performance

is GIPS®

Verified

Core Equity

SMARToption as a Core

HoldingSatellite

Positions (such

as Real

Estate, Commo

dities, Bonds, E

merging

Markets etc.)

SMARToption

SMARToption as a Large

Cap Holding

SMARToption

SMARToption as an

Alternative Holding

SMARToption

Performance results are presented in U.S. dollars and are gross-of-actual-fees and trading expensesand reflect the reinvestment of dividends and capital gains. Actual fees may vary based on, amongother factors, account size and custodial relationship. No current or prospective client should assumefuture performance of any specific investment strategy will be profitable or equal to pastperformance levels. All investment strategies have the potential for profit or loss. Changes ininvestment strategies, contributions or withdrawals may cause the performance results of yourportfolio to differ materially from the reported composite performance. Different types ofinvestments involve varying degrees of risk, and there can be no assurance that any specificinvestment will either be suitable or profitable for a client's investment portfolio. Historicalperformance results for market indices and/or categories generally do not reflect the deduction oftransaction and/or custodial charges or the deduction of an investment-management fee, theincurrence of which would have the effect of decreasing historical performance results. Economicfactors, market conditions, and investment strategies will affect the performance of any portfolio andthere are no assurances that it will match or outperform any particular benchmark. Swan WealthAdvisors, “the Firm”, claims compliance with the Global Investment Performance Standards (GIPS®).To receive a complete list and description of the firm’s composites and/or a presentation that adheresto the GIPS® standards, please contact the Firm at the address listed.

©2012 Brookstone Capital Management, LLC. All rights reserved.