settlement agreement · jean-luc brunet offer of settlement ... settlement agreement, ......

TRANSCRIPT

| Settlement Agreement | March 16, 2005 2005-002

IN THE MATTER OF THE UNIVERSAL MARKET INTEGRITY RULES

AND

IN THE MATTER OF

DESJARDINS SECURITIES INC.,

JEAN-PIERRE DE MONTIGNY

AND

JEAN-LUC BRUNET

OFFER OF SETTLEMENT

A. INTRODUCTION

1. Market Regulation Services Inc. (“RS”) has conducted an investigation (the

“Investigation”) into the conduct of Desjardins Securities Inc. (“Desjardins”),

Jean-Pierre De Montigny (“De Montigny”), and Jean-Luc Brunet (“Brunet)

(hereinafter referred to as the “Respondents”).

2

2. The Investigation has disclosed matters for which RS seeks certain sanctions

against the Respondents pursuant to Rule 10.5 of the Universal Market Integrity

Rules (“UMIR”).

3. If this Offer of Settlement is accepted by the Respondents, the resulting

settlement agreement (the “Settlement Agreement”), which has been negotiated

in accordance with Part 3 of UMIR Policy 10.8, is conditional upon the approval

by a hearing panel (the “Hearing Panel”) of the Hearing Committee appointed

under Part 10 of UMIR Policy 10.8.

4. The Respondents agree to waive all rights under UMIR to a hearing or to an

appeal or review if the Settlement Agreement is approved by the Hearing Panel.

5. RS and the Respondents jointly recommend that the Hearing Panel accept this

Settlement Agreement.

B. AGREEMENT AS TO REQUIREMENTS CONTRAVENED

6. It is agreed that the following Requirements have been contravened by

Desjardins:

(a) Between November 2002 and August 2004, Desjardins failed to comply

with its trading compliance and supervision obligations, contrary to Rule

7.1(1) and Policy 7.1 of UMIR.

(b) In the period April 1 to April 8, 2004, Desjardins conducted 17 client trades

where it traded along side a client order without recording client consent on

the client ticket, contrary to UMIR 5.3(6).

3

(c) In four of the above trades in (b), Desjardins failed to properly complete the

client trade ticket, contrary to UMIR 10.11 and the Trading Rules, referred

to in UMIR.

7. It is agreed that the following Requirement has been contravened by De

Montigny:

(a) Between November 2002 and August 2004, De Montigny failed to comply

with his trading supervision obligations, contrary to UMIR 7.1(4).

8. It is agreed that the following Requirement has been contravened by Brunet:

(a) Between November 2002 and August 2004, Brunet failed to comply with his

trading compliance obligations, contrary to UMIR 7.1(4).

C. ADMITTED FACTS

9. RS relies upon the admitted facts which are set out in the Statement of

Allegations attached as Appendix “A” to this Settlement Agreement.

D. DISPOSITION 10. For the contraventions in paragraph 6 above, Desjardins and RS have agreed

upon the following disposition:

(a) A fine of $1,500,000 payable by Desjardins to RS;

(b) The Board of Directors of Desjardins shall certify to RS, by April 30, 2005,

that the firm’s trading compliance and supervision system complies with

UMIR; and,

(c) Costs of $125,000 payable to RS.

4

11. For the contravention in paragraph 7 above, De Montigny and RS have agreed

upon the following disposition:

(a) A fine of $300,000 payable by De Montigny to RS.

12. For the contravention in paragraph 8 above, Brunet and RS have agreed upon

the following disposition:

(a) A fine of $35,000 payable by Brunet to RS.

13. If this Settlement Agreement is accepted by a Hearing Panel, the Respondents

agree to pay the amounts referred to in paragraphs 10-12 within 30 days of

such acceptance.

E. PROCEDURES FOR ACCEPTANCE OF OFFER OF SETTLEMENT AND APPROVAL OF SETTLEMENT AGREEMENT

14. The Respondents shall have until Tuesday, March 8, at 5:00 p.m. to accept the

Offer of Settlement and serve an executed copy thereof on RS.

15. This Settlement Agreement shall be presented to a Hearing Panel at a public

hearing (the “Approval Hearing”) held for the purpose of approving the

Settlement Agreement, in accordance with the procedures described in UMIR

Policy 10.8 in addition to any other procedures as may be agreed upon between

the parties. The Respondents acknowledge that RS shall notify the public and

media of the Approval Hearing in such manner and by such media as RS sees

fit.

16. Pursuant to Part 3.4 of UMIR Policy 10.8, the Hearing Panel may accept or

reject this Settlement Agreement.

5

17. In the event the Settlement Agreement is accepted by a Hearing Panel, the

matter becomes final, there can be no appeal or review of the matter, the

disposition of the matter agreed upon in this Settlement Agreement will be

included in the permanent record of RS in respect of the Respondents, and RS

will publish a summary of the Requirements contravened, the facts, and the

disposition agreed upon in the Settlement Agreement.

18. In the event the Hearing Panel rejects the Settlement Agreement, RS may

proceed with a hearing of the matter before a differently constituted Hearing

Panel pursuant to Part 3.7 of UMIR Policy 10.8 and this Settlement Agreement

may not be referred to without the consent of all parties.

F. OTHER MATTERS

19. The Respondents agree that, in the event the Respondents fail to comply with

any of the terms of the Settlement Agreement, RS may enforce this settlement

in any manner it deems appropriate and may, without limiting the generality of

the foregoing, suspend the Respondents’ access to marketplaces regulated by

RS until RS determines that the Respondents are in full compliance with all

terms of the Settlement Agreement.

20. The Respondents agree that none of them, or anyone on their behalf, will make

a public statement inconsistent with this Settlement Agreement.

6

IN WITNESS WHEREOF the parties have signed this Settlement Agreement as of

the dates noted below.

DATED at Montreal on the 8th day of March, 2005.

“Sylvain Perreault” “Desjardins Securities Inc.” Witness Signature Desjardins Securities Inc. Sylvain Perreault Name of Witness Desjardins Securities Address of Witness

DATED at Montreal on the 8th day of March, 2005.

“Sylvain Perreault” “Jean-Pierre De Montigny” Witness Signature Jean-Pierre De Montigny Sylvain Perreault Name of Witness Desjardins Securities Address of Witness

DATED at Montreal on the 9th day of March, 2005.

“Daniel R. Bissonnette” “Jean-Luc Brunet” Witness Signature Jean-Luc Brunet Daniel R. Bissonnette Name of Witness 2140 Place Des Flamants, Laval (QC) Address of Witness

DATED at Toronto, Ontario on the 11th day of March, 2005.

7

Per: “Maureen Jensen”

Maureen Jensen Vice President Market Regulation, Eastern Region Market Regulation Services Inc.

8

This foregoing Settlement Agreement is hereby accepted this 16th day of March, 2005,

by the following hearing panel constituted to review the terms thereof:

Per: “Honourable John B. Webber, Q.C.” Panel Chair Per: “John J. Huckstep” Per: “Donald H. Page” Panel Member Panel Member

IN THE MATTER OF THE UNIVERSAL MARKET INTEGRITY RULES

AND

IN THE MATTER OF

DESJARDINS SECURITIES INC., JEAN-PIERRE DE MONTIGNY

AND JEAN-LUC BRUNET

OFFER OF SETTLEMENT

Market Regulation Services Inc. Suite 900, Box 939 145 King Street West Toronto, Ontario M5H 1J8

Jane P. Ratchford Chief Counsel, Eastern Region Investigations and Enforcement

Telephone: 416-646-7229 Facsimile: 416-646-7259

10

IN THE MATTER OF THE UNIVERSAL MARKET INTEGRITY RULES

AND

IN THE MATTER OF

DESJARDINS SECURITIES INC.,

JEAN-PIERRE DE MONTIGNY, and

JEAN-LUC BRUNET

STATEMENT OF ALLEGATIONS

REQUIREMENTS CONTRAVENED

Desjardins Securities Inc. (“Desjardins”) agrees that it contravened Rules 5.3(6), 7.1(1) and 10.11 and Policy 7.1 of the Universal Market Integrity Rules ("UMIR").

Jean-Pierre De Montigny (“De Montigny”) agrees that he contravened Rule 7.1(4) and Policy 7.1 of UMIR.

Jean-Luc Brunet (“Brunet”) agrees that he contravened Rule 7.1(4) and Policy 7.1 of UMIR.

The text of the relevant requirements is set out at Schedule "A".

11

THE FACTS RELIED UPON

General

Overview

In the period November 2002 to August 2004 (“the Relevant Period”), Desjardins experienced a period of growth, particularly in its institutional business. With such growth came the commensurate responsibility to ensure that the firm had the necessary compliance and supervisory systems in place to respond to the increased trading demands on the firm. The facts herein establish that Desjardins failed to do so, contrary to its trading supervision obligations under UMIR Rule 7.1 and Policy 7.1.

RS Trade Desk Reviews (“TDRs”) in 2002, 2003 and 2004 found that Desjardins had insufficient supervision of trading practices and procedures and UMIR deficiencies, most notably related to audit trail violations.

In addition, Desjardins’ own internal quarterly reviews in 2003 and 2004 evidenced serious trade desk supervisory issues concerning several matters, most notably the lack of daily testing mandated by Desjardins’ own policies and procedures manual and serious audit trail violations.

Although some attempts were made to rectify these deficiencies, they continued and in fact, RS’s 2004 TDR findings for the TDR conducted in June 2004 were more extensive than those for the previous two years.

The continued lack of daily testing on the trade desks and the other compliance and supervisory failings resulted from a culture within the firm that did not place a priority on the creation and implementation of an effective trading supervision system.

The compliance department of a firm is responsible for monitoring and reporting to senior management adherence to UMIR and the firm’s own policies and procedures. Between November 2002 and August 2004, Jean-Luc Brunet (“Brunet”) was the Vice-President Compliance and Chief Compliance

12

Officer. Quarterly testing by the firm’s compliance staff identified problems with supervision of the various trading desks and the lack of daily testing being performed there (as required by the firm’s policies and procedures). The quarterly reports were provided to senior management.

However, Brunet failed to effectively address the various deficiencies described in the quarterly reports and by RS in the 2002, 2003 and 2004 TDRs, most notably related to the firm’s policies and procedures. As will be noted below in more detail, Brunet also failed to meet all his compliance objectives as set by the Board of Directors for the 2003 year.

As such, Brunet failed to meet his compliance responsibilities under UMIR 7.1(4) and Policy 7.1.

In the Relevant Period, De Montigny was President, Chief Operating Officer, Ultimate Designated Person and a member of the Board of Directors. When he assumed these positions in June 2001, his mandate was to expand the firm’s business, particularly the non-retail sectors. He succeeded in fulfilling this mandate. In fulfilling the business mandate, he also had the responsibility of ensuring that Desjardins had a trading supervision and compliance system that was adapted and expanded to effectively meet the supervision and compliance needs of the firm resulting from the increased growth.

The senior personnel charged with various supervisory and compliance functions reported ultimately to De Montigny. He was aware of RS’s TDR findings and the results of Desjardins internal reviews. Yet, he failed to make it a priority to effectively address these ongoing compliance and supervision issues, and continued with his mandate to expand the business despite these issues. All of this made De Montigny responsible within the firm in respect of the ongoing, and increasingly worsening, compliance and supervision issues in the Relevant Period and evidence his failure to fulfill his obligations under UMIR 7.1(4) and Policy 7.1.

13

In addition to this failing, RS’s Order Handling Regulatory Review conducted in the week of April 1-8, 2004 disclosed 17 instances of Desjardins trading alongside a client, without recording the client’s consent for each order, in violation of UMIR Rule 5.3(6). In connection with some of these trades, several audit trail violations (UMIR 10.11) were also detected. Personnel

Desjardins has institutional trading departments in Vancouver, Montreal and Toronto. It operates full service brokerage branch offices, primarily located in Quebec, as well as an on-line brokerage division.

In the Relevant Period, Desjardins’ institutional trading increased and as of 2004, comprised approximately 10% of its business. The remaining 90% is comprised of retail and discount brokerage trading.

As stated above, in the Relevant Period, De Montigny was President, Chief Operating Officer and Ultimate Designated Person.

In this position, and as a member of the Board of Directors, De Montigny was the most senior officer at the firm. He had ultimate responsibility under UMIR Rule 7.1(4) and Policy 7.1 to ensure that all employees of the firm, especially his direct reports, were fully and properly supervised, as necessary, to ensure the compliance of these employees with UMIR and its policies. The facts herein establish that he failed to do so.

As stated above, Jean-Luc Brunet was the Vice-President Compliance and Chief Compliance Officer (“VP-Compliance”) between November 2002 and mid-August 2004. He reported to De Montigny pre-April 2003 and thereafter to the Vice-President Risk, described below. The VP-Compliance was responsible for compliance supervision of the retail sales operation, the institutional sales and trading desk.

In addition, Brunet was responsible for responding to, and interacting directly with, RS in the TDR process.

14

Yves Gauthier was hired as the Vice-President, Integrated Risk Management (“VP-Risk”) in April 2003. He reports directly to De Montigny and became the ADP in September, 2004.

In the period January 2003 to December 2003, the head traders (who were also called VPs - Trading) in Toronto and Montreal, reported to Eric Bouchard, Senior Vice-President, Equity Capital Markets (SVP – Markets), who in turn reported to De Montigny.

The SVP-Markets is responsible for trading supervision.

From January 2004 to present, there has been one head trader (VP – Trading) for Montreal, Toronto and Vancouver, who works from Toronto. He reports to François Ruel, who replaced Eric Bouchard, as SVP-Markets, in December 2003. Committee Structure

The Risk Management Committee (“Risk Committee”) was initiated in May 2003 with the advent of the newly appointed position of VP Risk. It is comprised of all members of the Senior Management team.

The mandate of the Risk Committee is to support the Board of Directors, Audit Committee and President and COO in fulfilling their responsibilities in regard to risk management.

The Risk Committee is chaired by De Montigny and meets at least monthly. The VP-Risk also reports to this committee.

The Audit and Ethics Committee (“Audit Committee”) is a Board Committee comprised of outside directors without management functions, with the primary function of reviewing audited financial statements of the firm. It also provides an oversight of the implementation of the corrective actions necessary to address the compliance issues brought forward by the VP-Risk. De Montigny attends Audit Committee meetings in his role as President and COO. The VP-Risk reports to the Audit Committee at its quarterly meeting.

15

The Board of Directors of Desjardins is comprised of De Montigny and other senior management from Desjardins together with external members. The Board of Directors’ meets at least quarterly, generally after the Audit Committee meetings. Desjardins Internal Policies and Procedures

In the Relevant Period, Desjardins’ policies and procedures required that daily reviews be conducted by trade desk staff who reported to VP-Trading and that quarterly trade desk reviews be conducted by compliance staff.

The daily reviews were to encompass the following:

• synchronization of clocks

• audit trail issues such as trade ticket completeness

• order marking

• manipulative and deceptive trading/artificial pricing/wash trading

• frontrunning

• insider trading

• personal trading

• NCIB violations

• grey and restricted list trading

The daily reviews were to be approved by the VP-Trading. Issues of concern were to be escalated to the SVP-Markets.

The mandate of the quarterly review was described in Desjardins’ policies and procedures as follows: “The quarterly trade desk review is a regulatory requirement to ensure compliance to trading policies and procedures of the firm, and regulatory organizations…The results of this report will be reviewed with the Senior officers, the President and the Audit Committee.”

This review included a random sampling of tickets and blotters, among other things.

16

From November 2002 to June 2004, there was one staff position dedicated to trade desk compliance at Desjardins, who conducted the quarterly reviews referred to below.

The VP-Compliance and VP-Risk received the quarterly reports issued under the direction of the VP-Compliance, as did the SVP-Markets. De Montigny was also aware of the findings in the Relevant Period. Chronology of Events – Supervision and Compliance Issues November 2002 – October 2003

In November 2002, RS conducted a TDR at Desjardins.

By letter dated January 31, 2003 addressed to De Montigny, Desjardins was provided by RS with its 2002 TDR findings. This letter was also copied to the VP-Compliance and other compliance personnel.

The 2002 TDR found that:

the policies and procedures for compliance testing were not sufficiently detailed to satisfy Part 3 of the Policy.

the firm was not completing all tests required under Part 3 of the

Policy;

restricted list trading violations detected internally were not being fully documented;

there were deficiencies in Audit Trail requirements; and,

there were deficiencies in Client Principal disclosure.

Desjardins was required to review its policies and procedures and to submit internal testing to RS, both within 60 days.

By letter dated February 28, 2003, Desjardins responded to RS concerning the 2002 TDR findings. It undertook to review its policies and procedures and submit a revised manual to RS, to conduct trader training and conduct

17

internal quarterly reviews to address concerns regarding audit trail requirements and client principal disclosure problems. Desjardins described the problem in not conducting testing as a “staffing problem”, which was now resolved.

RS was also advised that in addition to testing for completeness of trading tickets throughout each quarter, testing would also be conducted on a surprise basis. Exceptions would be addressed immediately. The problem with client principal disclosure was described as a systems problem which would be resolved.

On the basis of these representations, RS advised Desjardins by letter dated February 28, 2003 that it appeared to have addressed RS’s concerns.

In response to the 2002 TDR, under the direction of the VP-Compliance, the Desjardins compliance staff member responsible for conducting the quarterly reviews sent a detailed memo to all trading personnel in both the retail and institutional areas. The memo was harshly worded and listed the percentages of the deficiencies in the audit trail compliance and principal disclosure noted in the 2002 TDR. It was noted that “Desjardins must take immediate action to correct these practices”.

A training session was held on March 11, 2003 for trade ticket completeness to meet regulatory standards. As well, an email dated August 29, 2003 attaching the rules and guidelines pertaining to manipulative and deceptive trading was also provided to staff.

Desjardins conducted internal quarterly reviews dated April 2003, June 2003 and September 2003. Recurring high levels of deficiencies in the audit trail (always over 50%) dominated the areas of concern in the quarterly reviews.

The April 2003 quarterly review noted that the retail department in Toronto and Montreal, and the Vancouver institutional branch, did not complete daily reviews on a timely basis or to a satisfactory level of attention. On an interim basis, the compliance department was to perform the daily reviews

18

for Montreal and Toronto institutional department pending a permanent solution.

This review was provided to RS in early April 2003. RS reviewed it and asked that the next quarterly review be provided so it could monitor the firm’s progress. RS has no record of the next quarterly review being submitted in 2003 and it was later requested as part of RS investigation (the June 2003 review referred to below).

The June 2003 quarterly review noted that the institutional department and retail trading departments were fragmented in terms of leadership and that this needed to be addressed. It also noted that the Toronto and Montreal institutional departments were not completing daily reviews and that the retail departments in Toronto, Montreal and the Vancouver institutional branch were not completing daily reviews on a timely basis or with a satisfactory level of attention.

In addition, the June review noted a high degree of jitney trading in Toronto which needed to be monitored closely.

To address the issue of daily reviews, specific personnel on the various trading desks were assigned the responsibility for such reviews.

Based on the April and June quarterly reviews, it was clear to the VP-Risk and VP-Compliance that there were serious and persistent issues with the trade desks themselves, especially the institutional desks, and that the senior management responsible for such supervision, such as the head traders and the SVP Markets, needed to be more effective in the supervision and training of staff.

The September 2003 quarterly report noted that “an attitude continues to exist that certain sections of trading tickets are unimportant”. An increase in missing information on trade tickets increased from the June quarterly review.

19

In addition, the September 2003 quarterly review noted that despite the assignment of responsibility specific to trading desk staff, the Toronto retail trading desk was not performing daily reviews and that the Montreal retail trading desk and Vancouver institutional desk problems continued regarding the completeness and timeliness of daily reviews.

This report specifically referenced the SVP-Markets and VPs trading as those with supervisory responsibility under UMIR 7.1 for the daily reviews.

With respect to jitney trading, it was noted that procedures were not being followed by the Toronto desk to have such trades “passed through” the Montreal desk.

The Audit Committee met on February 19, 2003, May 2003 and August 2003. There is no evidence of any discussion of the RS 2002 TDR or UMIR related issues at any of these 3 meetings.

The first meeting of the Risk Committee was June 10, 2003. It met again on September 22, 2003. There was no evidence of discussion of the 2002 TDR or UMIR related issues at either meeting.

The Board of Directors met on May 14 and August 13, 2003. There was no discussion of the 2002 TDR or UMIR related issues at either meeting.

In summary, in the period November 2002 to October 2003, Desjardins was alerted to various serious supervisory deficiencies both through RS’s 2002 TDR and Desjardins own internal quarterly reviews, including the lack of daily testing, audit trail deficiencies and problems relating to client principal disclosure.

Although some efforts were made to address these issues at the trade desk level, they were ineffective, as the lack of daily testing on several trade desks and serious audit trail issues persisted. In fact, as will be noted below, audit trail deficiencies were worse in the last quarter of 2003.

20

Moreover, these issues were not escalated to the Risk Committee or to the Board of Directors, either through the Audit Committee or directly to the full Board. November 2003 – August 2004

On October 8, 2003, RS completed its 2003 TDR. RS’s findings were provided to Desjardins by letter dated November 10, 2003 addressed to the VP-Risk and copied to the VP-Compliance.

RS’s findings included the repeat finding that Desjardins’ policies and procedures for compliance testing were not sufficiently detailed to satisfy Part 3 of UMIR Policy 7.1, that the firm was not completing all tests required under Part 3 and that the firm’s own quarterly testing of April 2003 and June 2003 had also found significant deficiencies.

In addition, there was the repeat finding of audit trail deficiencies (47% deficiency rate based on tickets tested), which was consistent with Desjardins’ own internal quarterly tests in 2003.

As a result of these findings, Desjardins was required by RS to review UMIR Policy 7.1 and implement policies and procedures specific to the firm that met or exceeded requirements, to submit findings and reviews to the Board of Directors and to provide a copy of the revised policies and procedures to RS, including steps to be implemented to rectify the audit trail deficiencies.

The Risk Committee met on November 4, 2003. The VP-Risk provided a progress report which included a summary of RS’s 2003 TDR findings. These findings had been verbally discussed between RS and Desjardins staff prior to the sending of the formal letter dated November 10, 2003.

The main findings of the VP-Risk progress report were as follows:

• Improvement noted as compared to the previous review, however necessary remedial action will have to be taken;

21

• A great many mistakes and omissions on the trade tickets, representing significant operational risks of transaction errors.

• Lack of supervision and stringent tracking of the traders in the institutional and retail sectors.

• High number of jitney transactions which needed further review.

The steps and remedial action contemplated noted in the VP-Risk report were as follows:

• Duties as to the supervision of the trades, in particular for the institutional sector and in respect of the retail sector in Toronto, would be better structured and defined.

• For each section, specific duties were assigned for the daily review of the transactions and, more specifically, with respect to quality control regarding the trade tickets.

• Training sessions and a review guide were prepared to meet quality requirements.

The Audit Committee met on November 12, 2003. The same progress report was presented by the VP-Risk to this Committee.

On November 12, 2003, the Board of Directors met. The Minutes do not reflect any discussion of the 2003 TDR or any UMIR matters.

On November 28, 2003, RS issued Market Integrity Notice 2003-025, Guidelines on Trading Supervision Obligations. It reminded firms of the requirement under UMIR Rule 7.1 and Policy 7.1 to have adequate policies and procedures for trading supervision and that a failure in this regard could result in enforcement action.

On December 1, 2003, Desjardins completed its next internal quarterly review. The review found, among other things, that there was a high deficiency with audit trail issues (65% deficiency in tickets sampled), that 78% of short sales were not declared as such and in the review for manipulative and

22

deceptive trading, found that off-marketplace transactions were being conducted where there was a change of beneficial ownership.

It also found that the Toronto retail and institutional trading desks, Derivative Group, Market Makers and Preferred Shares desk, were not conducting any daily reviews. There was no evidence of daily reviews being kept by the Montreal retail institutional desk.

By letter dated December 10, 2003, the VP-Risk and VP-Compliance responded to RS’s 2003 TDR findings on behalf of Desjardins. The letter was copied to De Montigny and the SVP-Markets. The letter stated that Desjardins was in the process of identifying and recruiting resources to conduct the daily reviews and that such staff would report directly to the VP-Trading and be closely monitored by the VP-Compliance. The firm expected the VP-Compliance to be in a position in early 2004 to report on the effectiveness of these procedures. Lastly, the letter advised that Desjardins had reported results of its own internal reviews and corrective actions to be taken to the Risk and Audit Committees and that Desjardins had provided a training session in respect of audit trail requirements.

In December 2003, Ruel replaced Bouchard as SVP-Markets and the Head Trader position was subsequently consolidated. These changes were in an effort to address the supervisory and compliance issues, but, as seen below, proved ineffective.

It was clear to De Montigny by December 2003, that the VP-Compliance did not have the ability and resources to address the ongoing compliance issues at the firm.

On February 19, 2004, the Audit Committee met. RS’s 2003 TDR was provided and discussed at the meeting together with Desjardins’ response letter of December 10, 2003. The VP-Risk provided a progress report which referenced these materials.

23

The Audit Committee was provided with a report from the VP-Compliance which detailed the March, June and September 2003 internal quarterly reports and the deficiencies noted therein regarding audit trail requirements and the lack of daily testing. The progress report confirmed that these deficiencies were similar to RS’s 2003 TDR findings.

One of the action plans presented at the meeting was “conducting, on a quarterly basis, a trade desk compliance review of Montreal and Toronto, taking into account RS’s 2003 TDR findings”. The Minutes of the meeting do not reflect any further discussion relating to the 2003 TDR.

The Board of Directors met on the afternoon of February 19, 2004. The Minutes from the November 12, 2003 Audit Committee were tabled. The Board also reviewed the Corporate Objectives for the Compliance Sector for the 2003 year, which had previously been approved by the Board. These included:

• drafting of a compliance manual

• drafting and implementing various policies and procedures in the

matter of compliance and regulatory management for the

institutional sector

• drafting and implementing various general policies and procedures

in respect of compliance and regulatory management.

The Board was advised that these objectives had not been met.

As a result, the Board charged De Montigny with the corporate goal for 2004 to “Improve the management processes for the Compliance Sector”. This included “fixing” the deficiencies noted in RS’s TDRs.

On March 31, 2004, Desjardins conducted its next quarterly review. The review stated that no daily reviews were performed for market makers, the retail trading desk in Toronto, derivative group or the institutional desks in

24

Montreal and Toronto or the preferred shares desk in Toronto. The Montreal Retail Desk was continuing not to keep evidence of reviews.

The report noted the continued audit trail deficiencies (46%) and client principal designation issues. In addition, the review for manipulative and deceptive trading noted improper off-marketplace trading.

The quarterly report was provided under the direction of the VP-Compliance to the VP-Risk and the SVP-Markets (now François Ruel). It clearly demonstrated that Desjardins’ supervision and compliance systems continued to be inadequate.

Despite the representations made by Desjardins to RS concerning such issues in its letter of December 10, 2003, unacceptable levels of audit trail deficiencies and lack of daily reviews persisted into 2004.

In April 2004, the Risk Committee decided to hire a new person to supervise at the trade desk level.

On May 6, 2004, the Audit Committee met. The VP-Risk submitted a progress report to March 31, 2004. There is no mention of RS’s 2003 TDR, or any follow up as a result thereof or in relation to the various deficiencies identified by both RS and Desjardins’ internal testing at the Audit Committee meeting on February 19, 2004.

The Minutes for the Board of Directors’ meeting held on the afternoon of May 6, 2004 do not contain any discussions of these matters, although the Minutes for the Audit Committee meeting of February 19, 2004 would have been provided to Board members in advance of the meeting.

The Risk Committee met on May 25 and June 21, 2004. Neither the 2003 TDR nor any other trading desk or audit concerns were on the agendas for these meetings.

On June 28, 2004, the new position of Compliance Manager, Trading Desk Toronto, was filled.

25

On June 30, 2004, RS completed its 2004 TDR. By letter dated August 19, 2004, addressed to De Montigny and copied to the VP-Compliance and VP-Risk, RS provided Desjardins with its findings, including:

the policies and procedures for compliance testing had deteriorated

to a level of non-confidence by RS in Desjardins’ ability to supervise for compliance – this included:

(i) lack of internal testing by trade desks continually noted in internal Desjardins reviews but not escalated by the Head of Compliance to be rectified;

(ii) insufficient or lack of testing for double-printing, restricted trading,

manipulative and deceptive trading, order handling, order designation and short sales; and,

(iii) insufficient sample sizes for quarterly testing of short sales and

manipulative and deceptive trading and sample sizes were actually reduced after problems were encountered in earlier periods.

42% deficiency rate in audit trail requirements;

deficiencies with respect to exposure of client orders required under

UMIR 6.3;

Client Principal Disclosure deficiencies;

both internal testing and RS TDR testing found instances of short

sale from proprietary inventories not being properly marked;

no testing had been undertaken for short sale from inventory accounts and client principal trades being marked non-client

and not inventory;

there were unacceptable delays in the provision of information by

Desjardins to RS requests during the TDR; and,

26

some Desjardins compliance staff did not have access to all of the

information necessary to effectively review the firm’s compliance.

These 2004 TDR findings represented a worsening trend from the two previous RS TDRs.

On August 19, 2004, Mr. Brunet ceased to be the VP-Compliance and on August 25, 2004, Mr. Brunet was replaced with a new VP-Compliance.

In summary, in the period November 2002 to August 2004, while these compliance and supervisory issues were reported to the Risk and Audit Committees and to the full Board of Directors, there was little or no follow-up by either the Audit Committee or the full Board after the meetings of February 19, 2004. The same problems persisted thereafter and in fact, as evidenced by the 2004 TDR findings, matters got worse and senior management continued to be unable to resolve them.

Although the position of Compliance Manager, Trading Desk Toronto was created and filled in this time period, the 2004 TDR results and Desjardins own internal testing, demonstrate that this step, although positive, was too little, too late.

The hiring of a new VP-Compliance was a positive step but only occurred after Desjardins received RS’s 2004 TDR findings. Again, this step was too little too late. It should have been taken by at least December 2003.

In particular, De Montigny, who was charged by the Board of Directors with the corporate objective to rectify the compliance and supervisory issues, including those identified in the 2003 TDR, was ineffective in advancing this objective. As stated above, the firm’s compliance and supervisory systems remained inadequate and ineffective and continued to worsen through the summer of 2004.

27

Client Priority/Audit Trail Issues

In the period April 1 to April 8, 2004, Desjardins conducted 17 client trades where it traded alongside the client order without marking client consent on the client ticket, contrary to UMIR 5.3(6).

In addition, in respect of 4 of the trades, trade tickets were CFO’d without either proper time stamping or adequate records of changes to the terms of the order, contrary to UMIR 10.11.

It is imperative that the audit trail for trades be complete as it is one of the cornerstones of an effective compliance and supervision system and one of the ways which a firm and its traders evidences compliance with other UMIR rules.

III. CONCLUSION

The firm and De Montigny allowed a culture of non-compliance to exist throughout the firm’s trading operation, as evidenced by the firm’s own internal reviews and RS’s TDR reviews, while the firm and De Montigny pursued and met the goal of increased business growth. This resulted in Desjardins potentially exposing its clients to market integrity risks that a comprehensive and effective trading supervision and compliance system is designed to prevent.

It was only as a result of RS’s investigation and the continued interaction between Desjardins and RS’s TDR group that Desjardins and De Montigny have now begun to take meaningful steps to rectify these deficiencies and put in place an effective supervision system which takes into account the firm’s business growth in the Relevant Period.

The facts also establish that Brunet was without sufficient authority and resources to solve the compliance issues by himself.

Although serious in nature, the contraventions referred to herein did not result in any harm or financial loss to Desjardins’ customers, or to any other market

28

participants, nor did it give rise to financial gain to Desjardins or any of its employees.

The facts herein establish that in the Relevant Period, Desjardins, De Montigny and Brunet failed to establish an effective compliance and trading supervision system for the firm’s trading operation, contrary their respective obligations under UMIR 7.1 and Policy 7.1.

March 8, 2005 Market Regulation Services Inc.

Suite 900, Box 939 145 King Street West Toronto, Ontario M5H 1J8 Investigations and Enforcement Telephone: 416-646-7229 Facsimile: 416-646-7259

TO: Ms Julie-Martine Loranger Gowling Lafleur Henderson LLP 1 Place Ville Marie 37th Floor Montreal, Quebec H3B 3P4

AND TO: René Brabant R. Brabant, Lawyers 10886 Boulevard Saint-Vital Montréal-Nord, QC H1H 4T4

29

Excerpts from the Universal Market Integrity Rules 5.3 Client Priority

(1) A Participant shall give priority to its client orders over all of its non-client or principal orders in the same security and on the same side of the market, unless the non-client or principal order is executed at a price above the client’s limit price (for a buy order) or below the client’s limit price (for a sell order).

(2) A Participant shall give priority to its client market orders over its non-client or principal orders in the same security and on the same side of the market.

(3) Subsections (1) and (2) shall not apply to allocations made by a trading system of a marketplace, provided that any client orders of the Participant were entered immediately upon receipt by the Participant and were not subsequently changed or removed from the system (other than changes or removals made on the instruction of the client).

(4) Subsections (1) and (2) shall not apply to client orders where the client has specifically given the Participant discretion with respect to execution of an order or where the Participant is making a bona fide attempt to obtain best execution for a client order, provided that no director, officer, partner, employee or agent of the Participant with knowledge of open client orders for a security that have not been fully executed enters a non-client or principal order on the same side of the market in such security.

(5) Subsections (1) and (2) shall not apply with respect to a particular client order where the client has specifically consented to the Participant trading ahead or alongside that order.

(6) The Participant shall record the specific consent referred to in subsection (5) on the order ticket.

7.1 Trading Supervision Obligations

(1) Each Participant shall adopt written policies and procedures to be followed by directors, officers, and employees of the Participant that are adequate, taking into account the business and affairs of the Participant, to ensure compliance with these Rules and each Policy.

(4) The head of trading together with each person who had authority or

supervision over or responsibility to the Participant for an employee of the Participant shall fully and properly supervise such employee as necessary to ensure the compliance of the employee with these Rules and each Policy.

10.11 Audit Trail Requirements

(1) In addition to any information required to be recorded by a Participant in accordance with Part 11 of the Trading Rules, each Participant shall:

30

(a) immediately following the receipt or origination of an order, record:

(i) all order designations required by clause (b) of subsection (1) of Rule 6.2,

(ii) the identifier of any investment adviser or registered representative receiving the order, and

(iii) any information respecting the special terms attaching to the order required by subsection (2) of Rule 6.2, if applicable;.

(b) immediately following the entry of an order to trade on a marketplace, add to the record :

(i) the identifier of the Participant through which any trade would be cleared and settled,

(ii) the identifier assigned to the marketplace on which the order is entered; and

(c) immediately following the variation or correction of an order, add to

the record any information required by clause (a) which has been changed.

POLICY 7.1 – POLICY ON TRADING SUPERVISION OBLIGATIONS

Part 1 – Responsibility for Supervision and Compliance

For the purposes of Rule 7.1, a Participant shall supervise its employees, directors and officers and, if applicable, partners to ensure that trading in securities on a marketplace (an Exchange, QTRS or ATS) is carried out in compliance with the applicable Requirements (which includes provisions of securities legislation, UMIR, the Trading Rules and the Marketplace Rules of any applicable Exchange or QTRS). An effective supervision system requires a strong overall commitment on the part of the Participant, through its board of directors, to develop and implement a clearly defined set of policies and procedures that are reasonably designed to prevent and detect violations of Requirements.

The board of directors of a Participant is responsible for the overall stewardship of the firm with a specific responsibility to supervise the management of the firm. On an ongoing basis, the board of directors must ensure that the principal risks for non-compliance with Requirements have been identified and that appropriate supervision and compliance procedures to manage those risks have been implemented.

Management of the Participant is responsible for ensuring that the supervision system adopted by the Participant is effectively carried out. The head of trading and any other person to whom supervisory responsibility has been delegated must fully and properly supervise all employees under their supervision to ensure their compliance with Requirements. If a supervisor has not followed the supervision procedures adopted by

31

the Participant, the supervisor will have failed to comply with their supervisory obligations under Rule 7.1(4).

When the Market Regulator reviews the supervision system of a Participant (for example, when a violation occurs of Requirements), the Market Regulator will consider whether the supervisory system is reasonably well designed to prevent and detect violations of Requirements and whether the system was followed.

The compliance department is responsible for monitoring and reporting adherence to rules, regulations, requirements, policies and procedures. In doing so, the compliance department must have a compliance monitoring system in place that is reasonably designed to prevent and detect violations. The compliance department must report the results from its monitoring to the Participant’s management and, where appropriate, the board of directors, or its equivalent. Management and the board of directors must ensure that the compliance department is adequately funded, staffed and empowered to fulfil these responsibilities.

Part 2 – Minimum Element of a Supervision System For the purposes of Rule 7.1, a supervision system consists of both policies and procedures aimed at preventing violations from occurring and compliance procedures aimed at detecting whether violations have occurred.

The Market Regulator recognizes that there is no one supervision system that will be appropriate for all Participants. Given the differences among firms in terms of their size, the nature of their business, whether they are engaged in business in more than one location or jurisdiction, the experience and training of its employees and the fact that effective jurisdiction can be achieved in a variety of ways, this Policy does not mandate any particular type or method of supervision of trading activity. Furthermore, compliance with this Policy does not relieve Participants from complying with specific Requirements that may apply in certain circumstances. In particular, Participants are reminded that, in accordance with subsection (2) of Rule 10.1, the entry of orders must comply with the Marketplace Rules on which the order is entered and the Marketplace Rules on which the order is executed. (For example, for Participants that are Participating Organizations of the TSE, reference should be made to the Policy on “Connection of Eligible Clients of Participating Organizations”).

Participants must develop and implement supervision and compliance procedures that exceed the elements identified in this Policy where the circumstances warrant. For example, previous disciplinary proceedings, warning and caution letters from the Market Regulator or the identification of problems with the supervision system or procedures by the Participant or the Market Regulator may warrant the implementation of more detailed or more frequent supervision and compliance procedures.

32

Regardless of the circumstances of the Participant, however, every Participant must:

1. Identify the relevant Requirements, securities laws and other regulatory requirements that apply to the lines of business in which the Participant is engaged (the “Trading Requirements”).

2. Document the supervision system by preparing a written policies and procedures manual. The manual must be accessible to all relevant employees. The manual must be kept current and Participants are advised to maintain a historical copy.

3. Ensure that employees responsible for trading in securities are appropriately registered and trained and that they are knowledgeable about the Trading Requirements that apply to their responsibilities. Persons with supervisory responsibility must ensure that employees under their supervision are appropriately registered and trained. The Participant should provide a continuing training and education program to ensure that its employees remain informed of and knowledgeable about changes to the rules and regulations that apply to their responsibilities.

4. Designate individuals responsible for supervision and compliance. The compliance function must be conducted by persons other than those who supervised the trading activity.

5. Develop and implement supervision and compliance procedures that are appropriate for the Participant’s size, lines of business in which it is engaged and whether the Participant carries on business in more than one location or jurisdiction.

6. Identify the steps a firm will take when violations of Requirements, securities laws or other regulatory requirements have been identified. This may include cancellation of the trade, increased supervision of the employee or the business activity, internal disciplinary measures and/or reporting the violation to the Market Regulator or other regulatory organization.

7. Review the supervision system at least once per year to ensure it continues to be reasonably designed to prevent and detect violations of Requirements. More frequent reviews may be required if past reviews have detected problems with supervision and compliance. Results of these reviews must be maintained for at least five years.

8. Maintain the results of all compliance reviews for at least five years.

9. Report to the board of directors of the Participant or, if applicable, the partners, a summary of the compliance reviews and the results of the supervision system review. These reports must be made at least annually. If the Market Regulator or the Participant has identified significant issues concerning the supervision system or compliance procedures, the board of directors or, if applicable, the partners, must be advised immediately.

33

Part 3 - Minimum Compliance Procedures for Trading on a Marketplace

A Participant must develop and implement compliance procedures for trading in securities on a marketplace that are appropriate for its size, the nature of its business and whether it carries on business in more than one location or jurisdiction. Such procedures should be developed having regard to the training and experience of its employees and whether the firm or its employees have been previously disciplined or warned by the Market Regulator concerning the violations of the Requirements.

In developing compliance procedures, Participants must identify any exception reports, trading data and/or other documents to be reviewed. In appropriate cases, relevant information that cannot be obtained or generated by the Participant should be sought from sources outside the firm including from the Market Regulator.

The following table identifies minimum compliance procedures for monitoring trading in securities on a marketplace that must be implemented by a Participant. The compliance procedures and the Rules identified below are not intended to be an exhaustive list of the Rules and procedures that must be complied with in every case. Participants are encouraged to develop compliance procedures in relation to all the Rules that apply to their business activities.

The Market Regulator recognizes that the requirements identified in the following table may be capable of being performed in different ways. For example, one Participant may develop an automated exception report and another may rely on a physical review of the relevant documents. The Market Regulator recognizes that either approach may comply with this Policy provided the procedure used is reasonably designed to detect violations of the relevant Rule. The information sources identified in the following table are therefore merely indicative of the types of information sources that may be used.

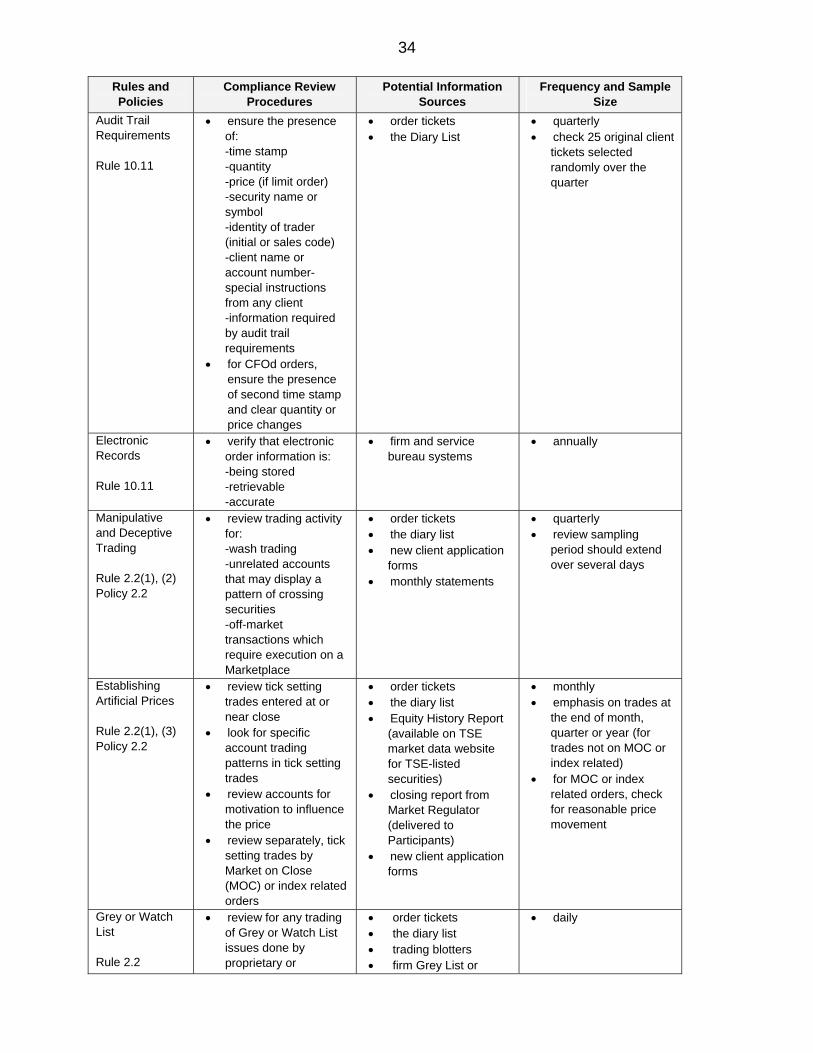

Minimum Compliance Procedures for Trading Supervision

Rules and Policies

Compliance Review Procedures

Potential Information Sources

Frequency and Sample Size

Synchronization of Clocks Rule 10.14

• confirm accuracy of clocks and computer network times

• remove unused or non-functional machines

• time clocks • Trading Terminal

system time • OMS system time

• Daily

34

Rules and Policies

Compliance Review Procedures

Potential Information Sources

Frequency and Sample Size

Audit Trail Requirements Rule 10.11

• ensure the presence of: -time stamp -quantity -price (if limit order) -security name or symbol -identity of trader (initial or sales code) -client name or account number-special instructions from any client -information required by audit trail requirements

• for CFOd orders, ensure the presence of second time stamp and clear quantity or price changes

• order tickets • the Diary List

• quarterly • check 25 original client

tickets selected randomly over the quarter

Electronic Records Rule 10.11

• verify that electronic order information is: -being stored -retrievable -accurate

• firm and service bureau systems

• annually

Manipulative and Deceptive Trading Rule 2.2(1), (2) Policy 2.2

• review trading activity for: -wash trading -unrelated accounts that may display a pattern of crossing securities -off-market transactions which require execution on a Marketplace

• order tickets • the diary list • new client application

forms • monthly statements

• quarterly • review sampling

period should extend over several days

Establishing Artificial Prices Rule 2.2(1), (3) Policy 2.2

• review tick setting trades entered at or near close

• look for specific account trading patterns in tick setting trades

• review accounts for motivation to influence the price

• review separately, tick setting trades by Market on Close (MOC) or index related orders

• order tickets • the diary list • Equity History Report

(available on TSE market data website for TSE-listed securities)

• closing report from Market Regulator (delivered to Participants)

• new client application forms

• monthly • emphasis on trades at

the end of month, quarter or year (for trades not on MOC or index related)

• for MOC or index related orders, check for reasonable price movement

Grey or Watch List Rule 2.2

• review for any trading of Grey or Watch List issues done by proprietary or

• order tickets • the diary list • trading blotters • firm Grey List or

• daily

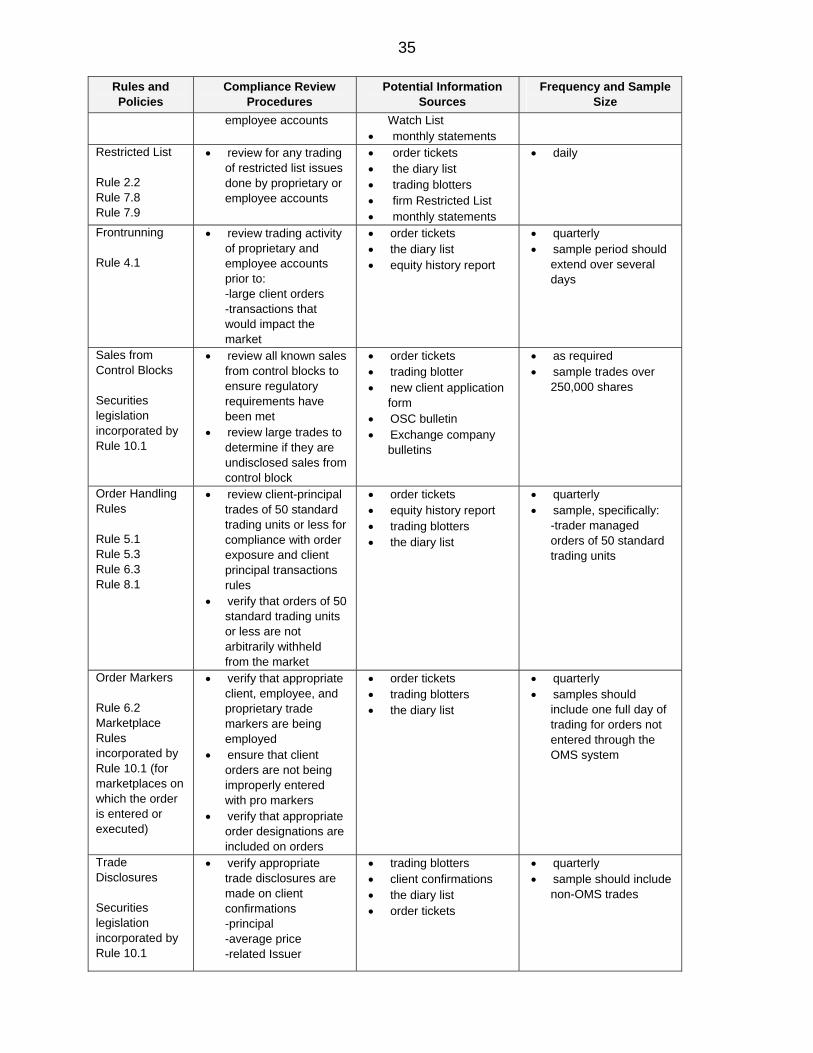

35

Rules and Policies

Compliance Review Procedures

Potential Information Sources

Frequency and Sample Size

employee accounts Watch List • monthly statements

Restricted List Rule 2.2 Rule 7.8 Rule 7.9

• review for any trading of restricted list issues done by proprietary or employee accounts

• order tickets • the diary list • trading blotters • firm Restricted List • monthly statements

• daily

Frontrunning Rule 4.1

• review trading activity of proprietary and employee accounts prior to: -large client orders -transactions that would impact the market

• order tickets • the diary list • equity history report

• quarterly • sample period should

extend over several days

Sales from Control Blocks Securities legislation incorporated by Rule 10.1

• review all known sales from control blocks to ensure regulatory requirements have been met

• review large trades to determine if they are undisclosed sales from control block

• order tickets • trading blotter • new client application

form • OSC bulletin • Exchange company

bulletins

• as required • sample trades over

250,000 shares

Order Handling Rules Rule 5.1 Rule 5.3 Rule 6.3 Rule 8.1

• review client-principal trades of 50 standard trading units or less for compliance with order exposure and client principal transactions rules

• verify that orders of 50 standard trading units or less are not arbitrarily withheld from the market

• order tickets • equity history report • trading blotters • the diary list

• quarterly • sample, specifically:

-trader managed orders of 50 standard trading units

Order Markers Rule 6.2 Marketplace Rules incorporated by Rule 10.1 (for marketplaces on which the order is entered or executed)

• verify that appropriate client, employee, and proprietary trade markers are being employed

• ensure that client orders are not being improperly entered with pro markers

• verify that appropriate order designations are included on orders

• order tickets • trading blotters • the diary list

• quarterly • samples should

include one full day of trading for orders not entered through the OMS system

Trade Disclosures Securities legislation incorporated by Rule 10.1

• verify appropriate trade disclosures are made on client confirmations -principal -average price -related Issuer

• trading blotters • client confirmations • the diary list • order tickets

• quarterly • sample should include

non-OMS trades

36

Rules and Policies

Compliance Review Procedures

Potential Information Sources

Frequency and Sample Size

Normal Course Issuer Bids Marketplace Rules (e.g. Rule 6-501 and Policy 6-501 of TSE and Policy 5.6 of CDNX)

• review NCIBs for: -maximum stock purchase limits of 5% in 1 year or 2% in 30 days are observed -purchases for NCIBs are not occurring while a sale from control is being made -purchases are not made on upticks -trade reporting to Exchange (if the firm reports on behalf of issuer)

• order tickets • the diary list • trading blotters • new client application

form

• quarterly

Part 4 – Specific Procedures Respecting Client Priority and Best Execution

Participants must have written compliance procedures reasonably designed to ensure that their trading does not violate Rule 5.3 or 5.1. At a minimum, the written compliance procedures must address employee education and post-trade monitoring.

The purpose of the Participant’s compliance procedures is to ensure that pro traders do not knowingly trade ahead of client orders. This would occur if a client order is withheld from entry into the market and a person with knowledge of that client order enters another order that will trade ahead of it. Doing so could take a trading opportunity away from the first client. Withholding an order for normal review and order handling is allowed under Rules 5.3 and 5.1, as this is done to ensure that the client gets a good execution. To ensure that the Participants’ written compliance procedures are effective they must address the potential problem situations where trading opportunities may be taken away from clients.

Potential Problem Situations

Listed below are some of the potential problem situations where trading opportunities may be taken away from clients.

1. Retail brokers or their assistants withholding a client order to take a trading opportunity away from that client.

2. Others in a brokerage office, such as wire operators, inadvertently withholding a client order, taking a trading opportunity away from that client.

3. Agency traders withholding a client order to allow others to take a trading opportunity away from that client.

4. Proprietary traders using knowledge of a client order to take a trading opportunity away from that client.

5. Traders using their personal accounts to take a trading opportunity away from a client.

37

Written Compliance Procedures

It is necessary to address in the written compliance procedures the potential problem situations that are applicable to the Participant. Should there be a change in the Participant’s operations where new potential problem situations arise then these would have to be addressed in the procedures. At a minimum, the written compliance procedures for employee education and post-trade monitoring must include the following points.

Education

• Employees must know the Rules and understand their obligation for client priority and best execution, particularly in a multiple market environment.

• Participants must ensure that all employees involved with the order handling process know that client orders must be entered into the market before non-client and proprietary orders, when they are received at the same time.

• Participants must train employees to handle particular trading situations that arise, such as, client orders spread over the day, and trading along with client orders.

Post-Trade Monitoring Procedures

• All brokers’ trading must be monitored as required by Rule 7.1.

• Complaints from clients and Registered Representatives concerning potential violations of the rule must be documented and followed-up.

• All traders’ personal accounts and those related to them, must be monitored daily to ensure no apparent violations of client priority occurred.

• At least once a month, a sample of proprietary inventory trades must be compared with contemporaneous client orders.

• In reviewing proprietary inventory trades, Participants must address both client orders entered into order management systems and manually handled orders, such as those from institutional clients.

• The review of proprietary inventory trades must be of a sample size that sufficiently reflects the trading activity of the Participant.

• Potential problems found during these reviews must be examined to determine if an actual violation of Rule 5.3 or 5.1 occurred. The Participant must retain documentation of these potential problems and examinations.

• When a violation is found, the Participant must take the necessary steps to correct the problem.

Documentation

38

• The procedures must specify who will conduct the monitoring.

• The procedures must specify what information sources will be used.

• The procedures must specify who will receive reports of the results.

• Records of these reviews must be maintained for five years.

• The Participant must annually review its procedures.

…..