sequential learning in dynamic graphical model hao wang, craig reeson

DESCRIPTION

Sequential learning in dynamic graphical model Hao Wang, Craig Reeson Department of Statistical Science, Duke University Carlos Carvalho Booth School of Business, The University of Chicago. Motivating example: forecasting stock return covariance matrix. - PowerPoint PPT PresentationTRANSCRIPT

Sequential learning in dynamic graphical model

Hao Wang, Craig ReesonDepartment of Statistical Science, Duke University

Carlos CarvalhoBooth School of Business, The University of Chicago

Motivating example: forecasting stock return covariance matrix

Observe p- vector stock return time series

Interested in forecast conditional covariance matrix WHY?

Buy dollar stock i

Expected return

Risks

Daily return of a portfolio (S&P500)

How to forecast: index model

Common index

Uncorrelated error terms

Covariance structure

Assumption: stocks move together only because of common movement with indexes (e.g. market)

Uncorrelated residuals? An exploratory analysis on 100 stocks

Possible signals Index explains a lots

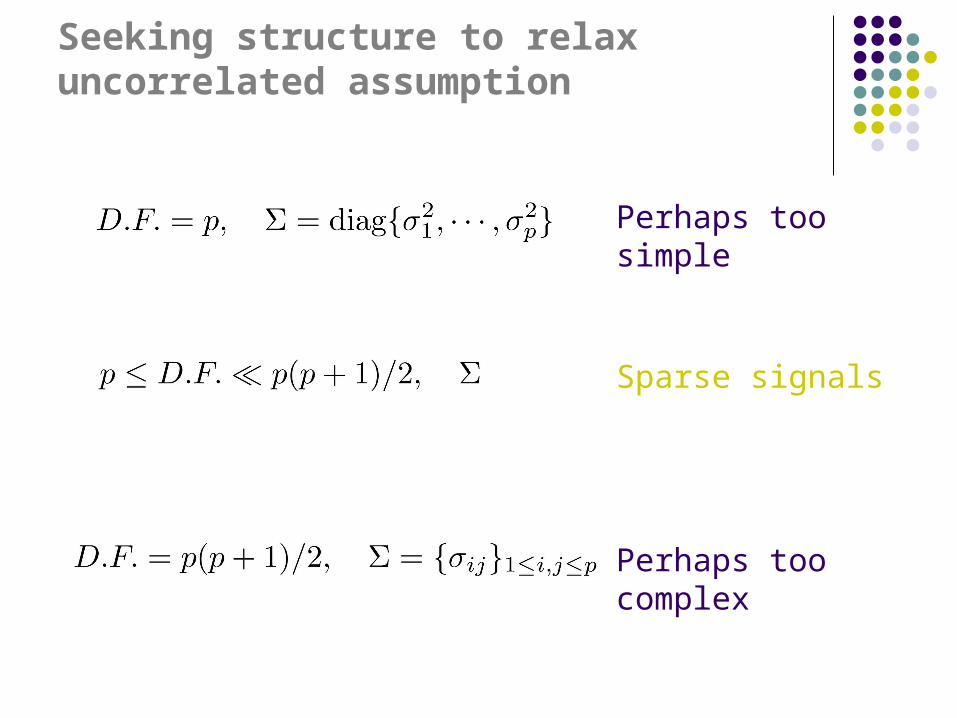

Seeking structure to relax uncorrelated assumption

Perhaps too simple

Perhaps too complex

Sparse signals

Structures: Gaussian graphical model

Graph exhibits conditional independencies ~ missing edges

International exchange rates example, p=11Carvalho, Massam, West, Biometrika, 2007

No edge:No edge:

Dynamic matrix-variate models

Example: Core class of matrix-variate DLMs

Multivariate stochastic volatility: Variance matrix discounting model for

Conjugate, closed-form sequential learning/updating and forecasting

(Quintana 1987; Q&W 1987; Q et al 1990s)

Multivariate stochastic volatility: Variance matrix discounting model for

Conjugate, closed-form sequential learning/updating and forecasting

(Quintana 1987; Q&W 1987; Q et al 1990s)

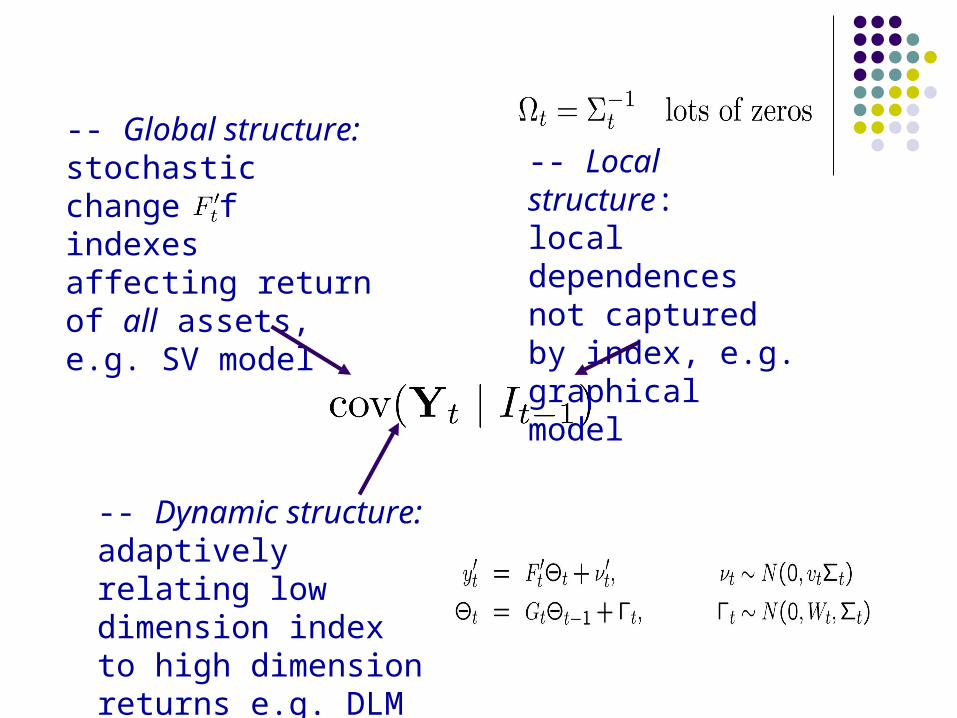

-- Global structure: stochastic change of indexes affecting return of all assets, e.g. SV model

-- Local structure: local dependences not captured by index, e.g. graphical model

-- Dynamic structure: adaptively relating low dimension index to high dimension returns e.g. DLM

Random regression vector and sequential forecasting

1-step covariance forecasts :Mild assumption:

1-step covariance forecasts :

Variance from graphical structured error terms

Variance from regression vector

Analytic updates

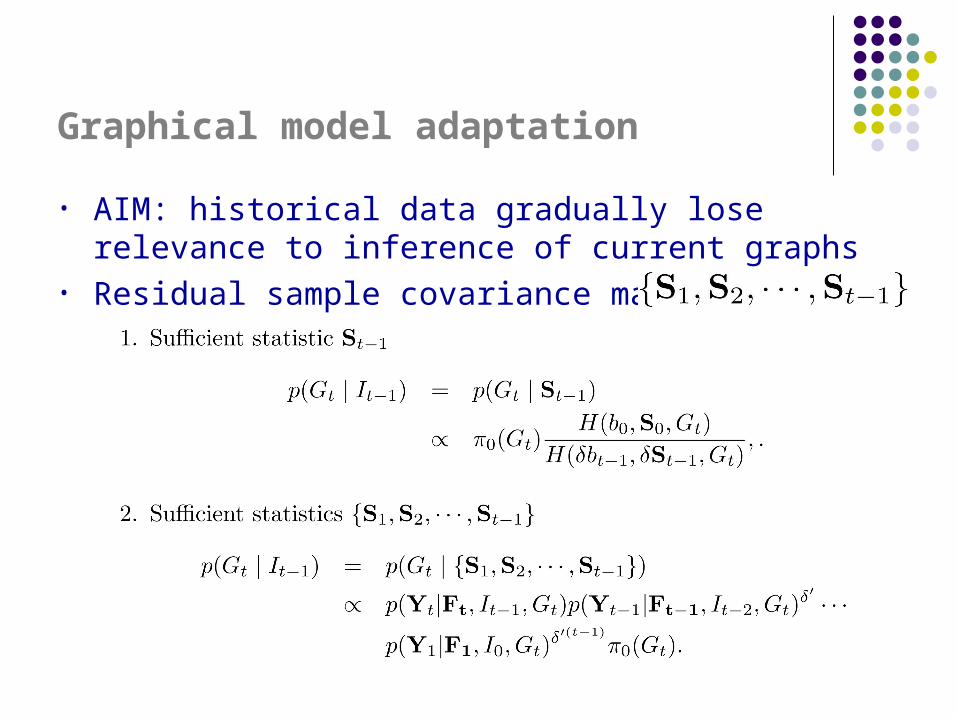

Graphical model adaptation

• AIM: historical data gradually lose relevance to inference of current graphs

• Residual sample covariance matrices

Graphical model uncertainty

Challenges: Interesting graphs?

graphsGraphical model search

Jones et al (2005) Stat Sci: static modelsMCMC Metropolis Hasting Shotgun stochastic search

Scott & Carvalho (2008): Feature inclusion

Challenges: Interesting graphs?

graphs

Keys:

>> Analytic evaluation of posterior probability of any graph …

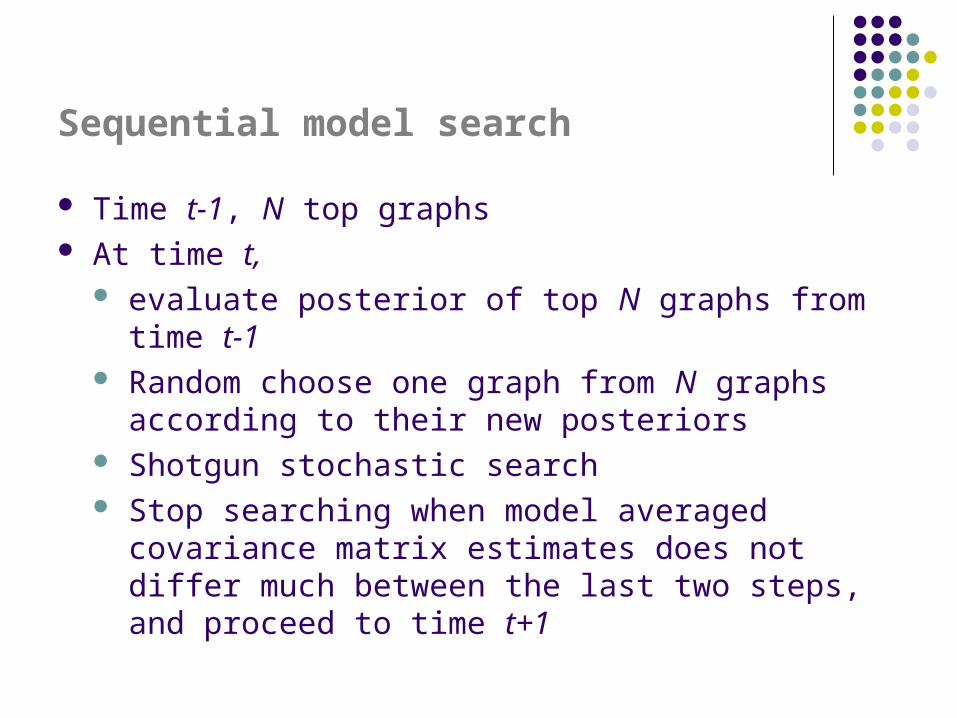

Sequential model search

Time t-1, N top graphs At time t,

evaluate posterior of top N graphs from time t-1 Random choose one graph from N graphs according

to their new posteriors Shotgun stochastic search Stop searching when model averaged covariance

matrix estimates does not differ much between the last two steps, and proceed to time t+1

100 stock example

Monthly returns of randomly selected 100 stocks, 01/1989 – 12/2008

Two index model Capital asset pricing model: market Fama-French model: market, size effect, book-to-price effect

, about 60 monthly moving window

How sparse signals help?

Time-varying sparsity

Performance of correlation matrix prediction

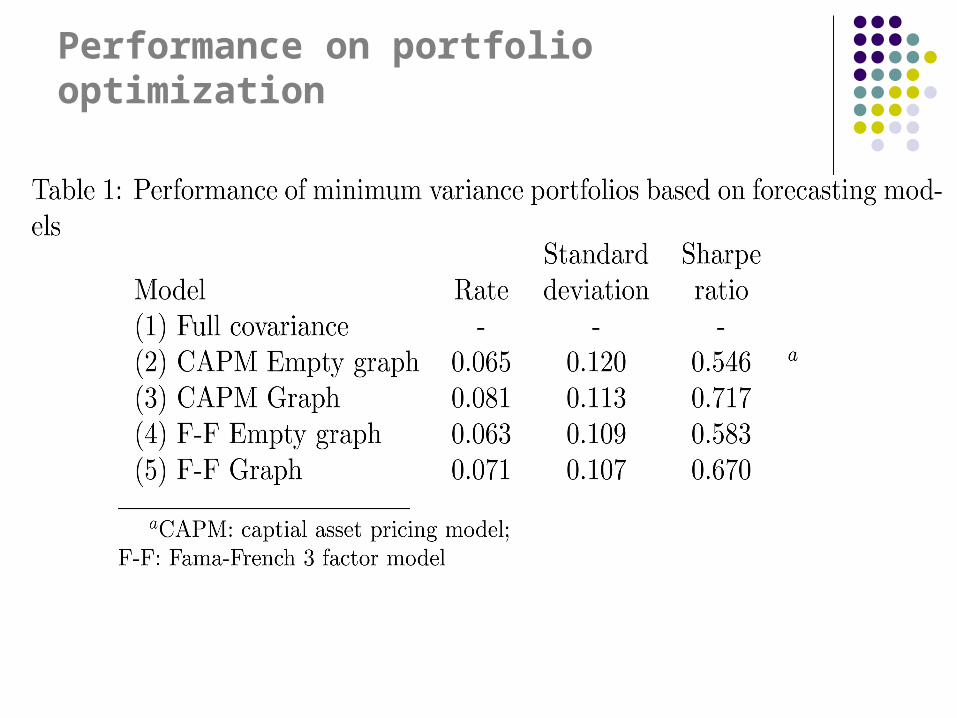

Performance on portfolio optimization

Bottom line

For either set of regression variables we chose, we will perhaps be better off by identifying sparse signals than assuming uncorrelated/fully correlated residuals