security valuation bond valuation - bc.edu 4 bond valuation.pdf · security valuation bond...

TRANSCRIPT

1

SECURITY VALUATION

BOND VALUATION

When a corporation (or the government) wants to borrow money, it often sells a bond. An

investor gives the corporation money for the bond, and the corporation promises to give the

investor:

1. Regular coupon payments every period until the bond matures.

2. The face value of the bond when it matures.

Additional Features:

1. Payments are a legal obligation. In case of default, bondholders can force firm into

bankruptcy.

2. “Senior” or “Junior” debt pertains to who gets paid first in case of bankruptcy. In some cases

“junior” debtholders can get partially paid before senior debtholders are fully paid.

3. Call provisions: A call provision gives the corporation the right to buy back an outstanding

bond (usually at face value).

4. Put provisions: A put provision gives the bondholder the right to sell the bond back to the

corporation.

5. Convertible bonds.

Questions:

• What is the market price of a U.S. Treasury Bond?

• What is the relation between U.S. Treasury Bond prices and interest rates?

• Are U.S. interest rates expected to rise or fall?

• How should you pick a Certificate of Deposit?

Terminology

Bond: Loan made by numerous individuals and/or institutions (the bond holders) to a

firm/state/country.

Par Value: Principal amount to be paid at maturity, usually $1000, also known as Face Value.

Maturity: Amount of time that will pass until par value is paid.

Coupon: Percentage of par value that is paid every year (usually semi-annually so divide by two

to determine the payment amount).

Current Yield: Coupon amount divided by a bond’s current price.

2

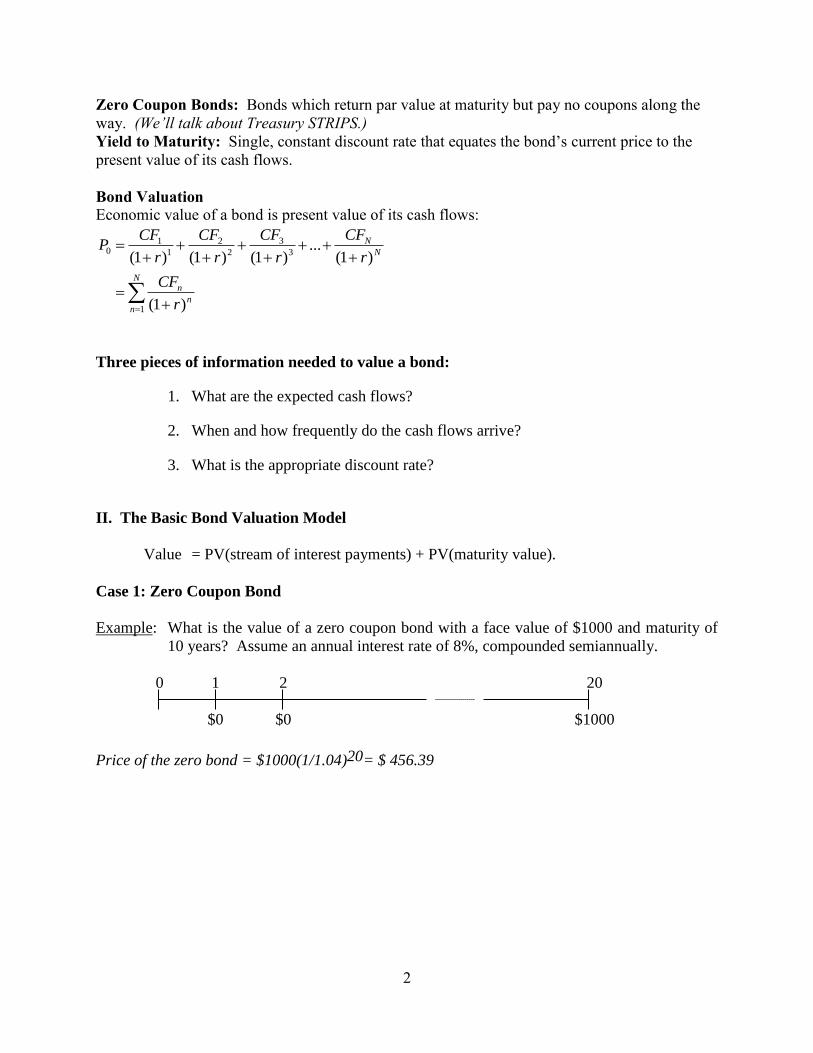

Zero Coupon Bonds: Bonds which return par value at maturity but pay no coupons along the

way. (We’ll talk about Treasury STRIPS.)

Yield to Maturity: Single, constant discount rate that equates the bond’s current price to the

present value of its cash flows.

Bond Valuation

Economic value of a bond is present value of its cash flows:

N

nn

n

N

N

r

CF

r

CF

r

CF

r

CF

r

CFP

1

3

3

2

2

1

10

)1(

)1(...

)1()1()1(

Three pieces of information needed to value a bond:

1. What are the expected cash flows?

2. When and how frequently do the cash flows arrive?

3. What is the appropriate discount rate?

II. The Basic Bond Valuation Model

Value = PV(stream of interest payments) + PV(maturity value).

Case 1: Zero Coupon Bond

Example: What is the value of a zero coupon bond with a face value of $1000 and maturity of

10 years? Assume an annual interest rate of 8%, compounded semiannually.

0 1 2 20

$0 $0 $1000

Price of the zero bond = $1000(1/1.04)20= $ 456.39

3

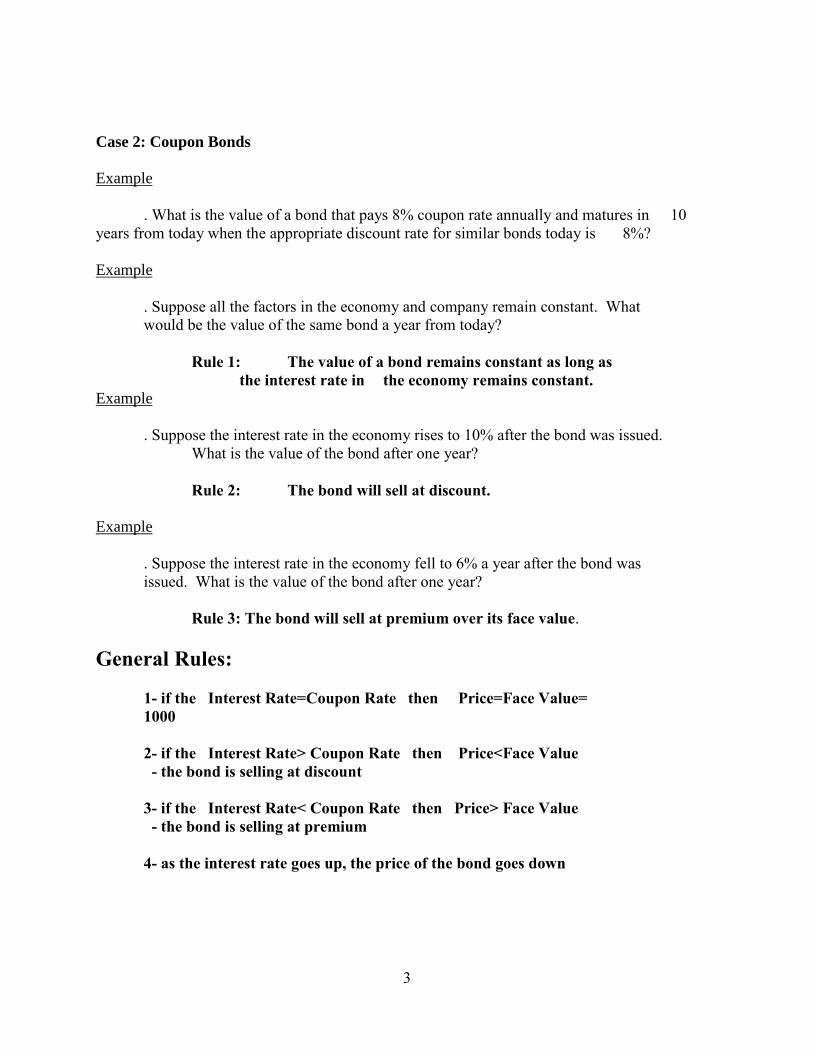

Case 2: Coupon Bonds

Example

. What is the value of a bond that pays 8% coupon rate annually and matures in 10

years from today when the appropriate discount rate for similar bonds today is 8%?

Example

. Suppose all the factors in the economy and company remain constant. What

would be the value of the same bond a year from today?

Rule 1: The value of a bond remains constant as long as

the interest rate in the economy remains constant.

Example

. Suppose the interest rate in the economy rises to 10% after the bond was issued.

What is the value of the bond after one year?

Rule 2: The bond will sell at discount.

Example

. Suppose the interest rate in the economy fell to 6% a year after the bond was

issued. What is the value of the bond after one year?

Rule 3: The bond will sell at premium over its face value.

General Rules:

1- if the Interest Rate=Coupon Rate then Price=Face Value=

1000

2- if the Interest Rate> Coupon Rate then Price<Face Value

- the bond is selling at discount

3- if the Interest Rate< Coupon Rate then Price> Face Value

- the bond is selling at premium

4- as the interest rate goes up, the price of the bond goes down

4

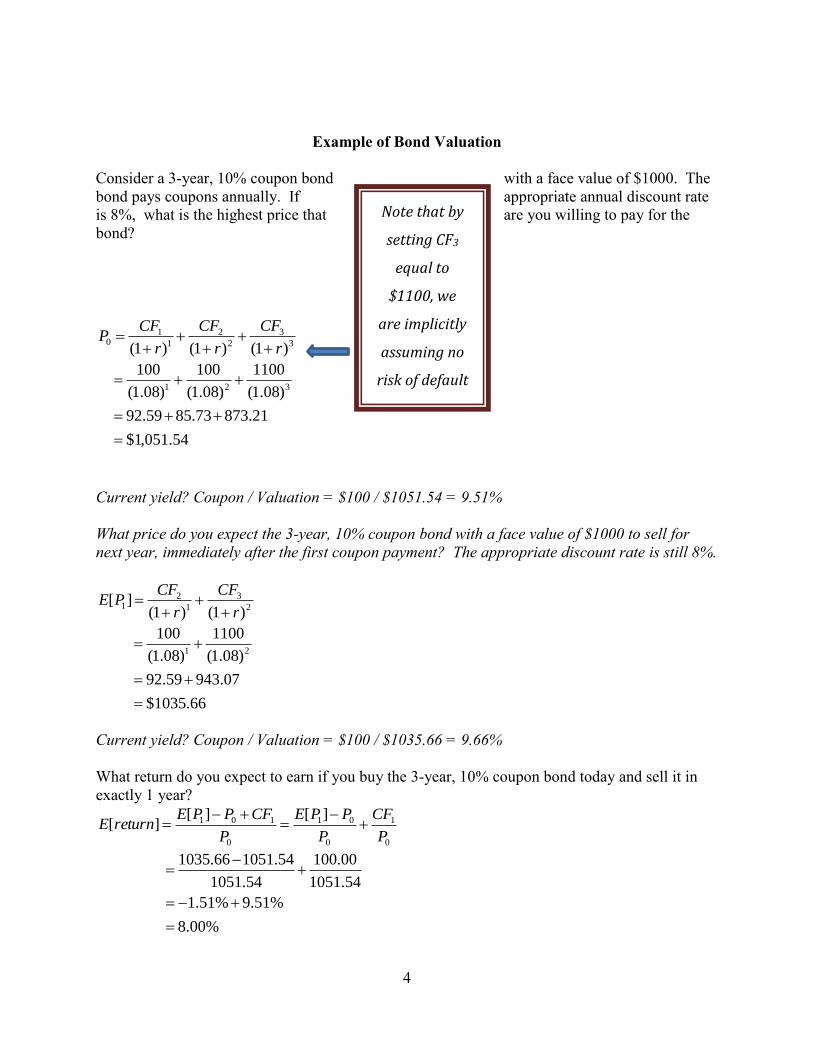

Example of Bond Valuation

Consider a 3-year, 10% coupon bond with a face value of $1000. The

bond pays coupons annually. If appropriate annual discount rate

is 8%, what is the highest price that are you willing to pay for the

bond?

3

3

2

2

1

10

)1()1()1( r

CF

r

CF

r

CFP

54.051,1$

21.87373.8559.92

)08.1(

1100

)08.1(

100

)08.1(

100321

Current yield? Coupon / Valuation = $100 / $1051.54 = 9.51%

What price do you expect the 3-year, 10% coupon bond with a face value of $1000 to sell for

next year, immediately after the first coupon payment? The appropriate discount rate is still 8%.

2

3

1

21

)1()1(][

r

CF

r

CFPE

66.1035$

07.94359.92

)08.1(

1100

)08.1(

10021

Current yield? Coupon / Valuation = $100 / $1035.66 = 9.66%

What return do you expect to earn if you buy the 3-year, 10% coupon bond today and sell it in

exactly 1 year?

0

1

0

01

0

101 ][][][

P

CF

P

PPE

P

CFPPEreturnE

%00.8

%51.9%51.1

54.1051

00.100

54.1051

54.105166.1035

Note that by

setting CF3

equal to

$1100, we

are implicitly

assuming no

risk of default

5

Between the expected capital loss of -1.51% and the current yield of 9.51%, you expect to match

the discount rate of 8%.

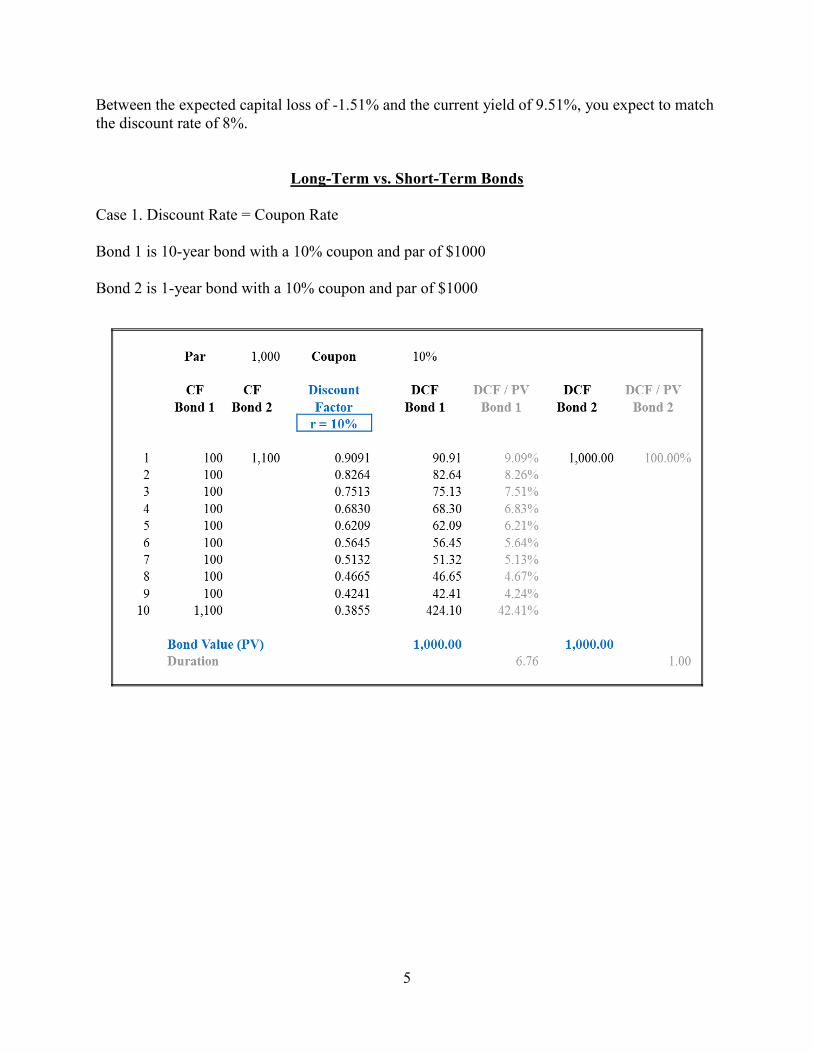

Long-Term vs. Short-Term Bonds

Case 1. Discount Rate = Coupon Rate

Bond 1 is 10-year bond with a 10% coupon and par of $1000

Bond 2 is 1-year bond with a 10% coupon and par of $1000

6

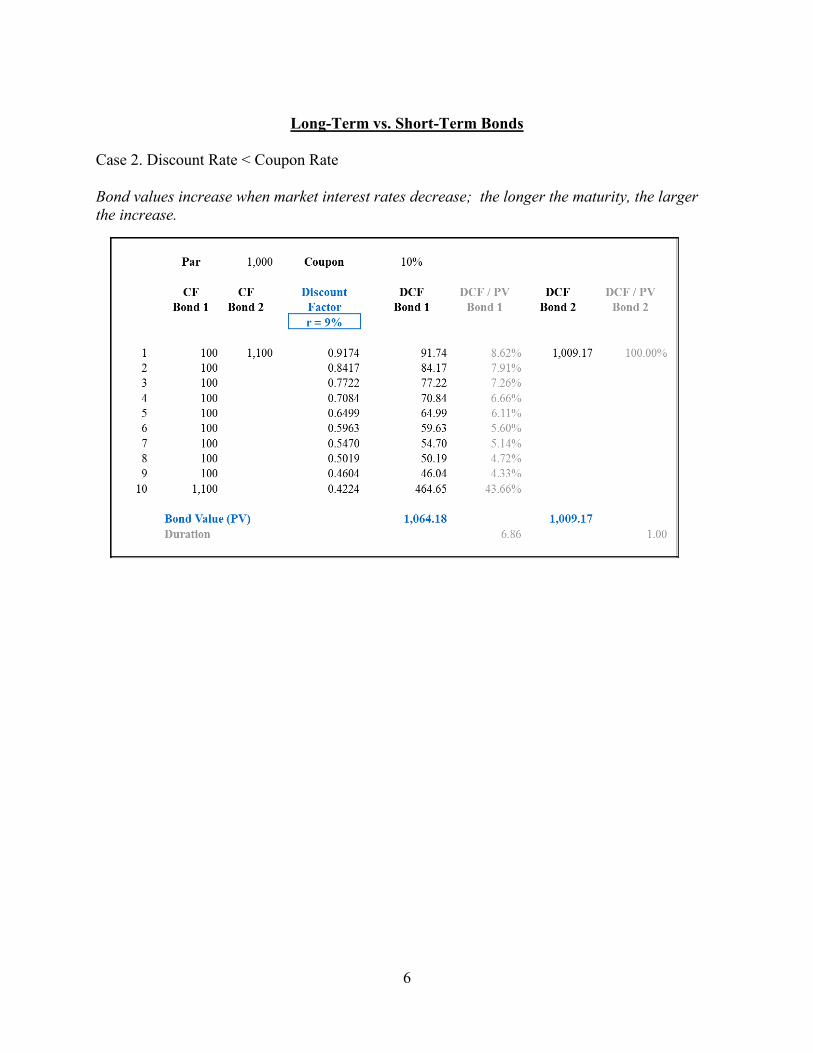

Long-Term vs. Short-Term Bonds

Case 2. Discount Rate < Coupon Rate

Bond values increase when market interest rates decrease; the longer the maturity, the larger

the increase.

7

Long-Term vs. Short-Term Bonds

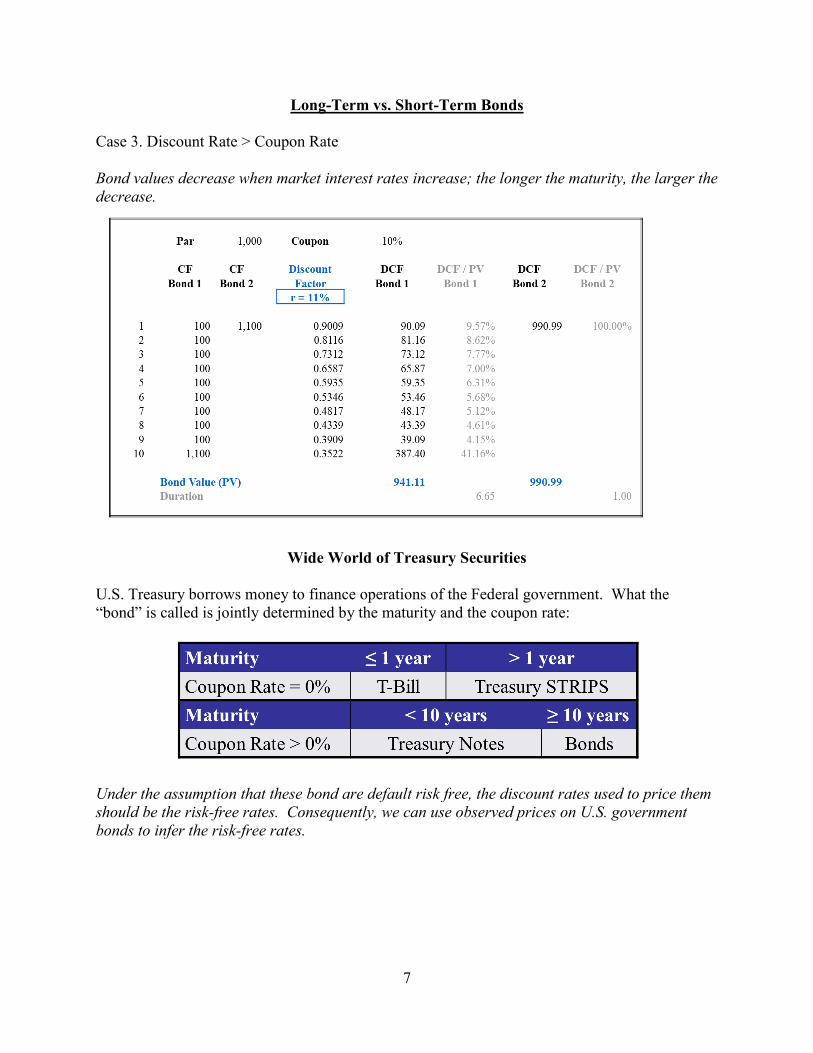

Case 3. Discount Rate > Coupon Rate

Bond values decrease when market interest rates increase; the longer the maturity, the larger the

decrease.

Wide World of Treasury Securities

U.S. Treasury borrows money to finance operations of the Federal government. What the

“bond” is called is jointly determined by the maturity and the coupon rate:

Under the assumption that these bond are default risk free, the discount rates used to price them

should be the risk-free rates. Consequently, we can use observed prices on U.S. government

bonds to infer the risk-free rates.

8

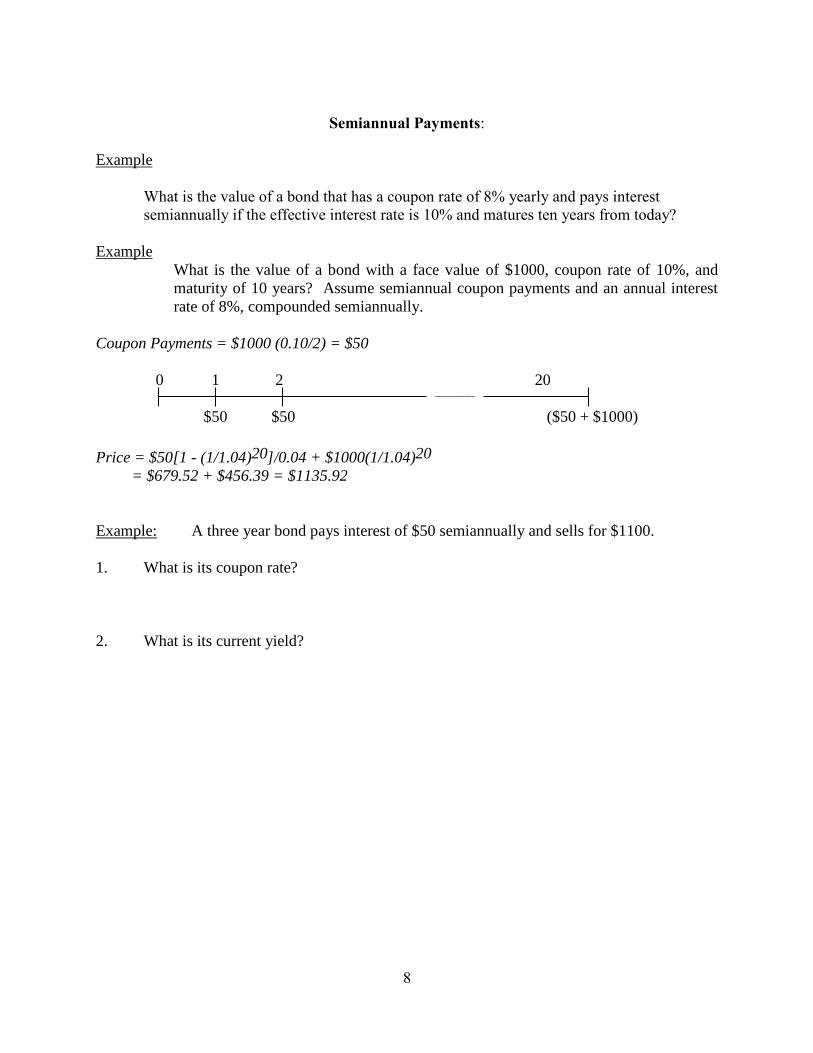

Semiannual Payments:

Example

What is the value of a bond that has a coupon rate of 8% yearly and pays interest

semiannually if the effective interest rate is 10% and matures ten years from today?

Example

What is the value of a bond with a face value of $1000, coupon rate of 10%, and

maturity of 10 years? Assume semiannual coupon payments and an annual interest

rate of 8%, compounded semiannually.

Coupon Payments = $1000 (0.10/2) = $50

0 1 2 20

$50 $50 ($50 + $1000)

Price = $50[1 - (1/1.04)20]/0.04 + $1000(1/1.04)20

= $679.52 + $456.39 = $1135.92

Example: A three year bond pays interest of $50 semiannually and sells for $1100.

1. What is its coupon rate?

2. What is its current yield?

9

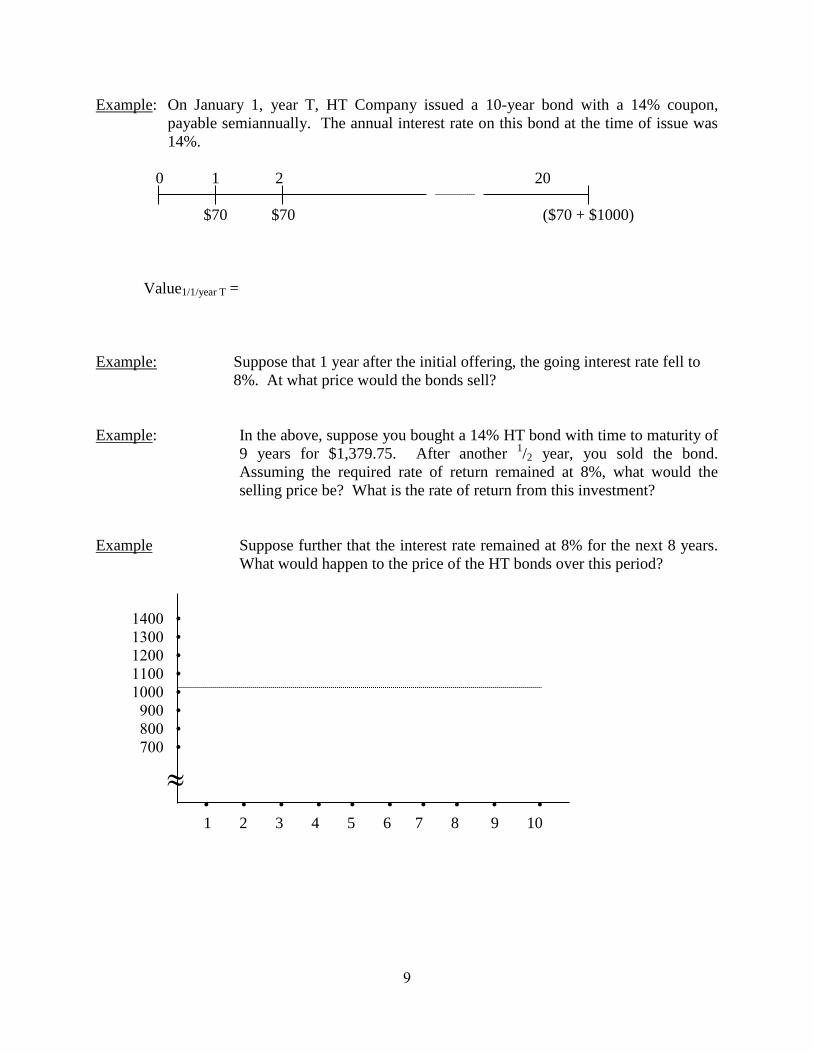

Example: On January 1, year T, HT Company issued a 10-year bond with a 14% coupon,

payable semiannually. The annual interest rate on this bond at the time of issue was

14%.

0 1 2 20

$70 $70 ($70 + $1000)

Value1/1/year T =

Example: Suppose that 1 year after the initial offering, the going interest rate fell to

8%. At what price would the bonds sell?

Example: In the above, suppose you bought a 14% HT bond with time to maturity of

9 years for $1,379.75. After another 1/2 year, you sold the bond.

Assuming the required rate of return remained at 8%, what would the

selling price be? What is the rate of return from this investment?

Example Suppose further that the interest rate remained at 8% for the next 8 years.

What would happen to the price of the HT bonds over this period?

1400 •

1300 •

1200 •

1100 •

1000 •

900 •

800 •

700 •

• • • • • • • • • •

1 2 3 4 5 6 7 8 9 10

10

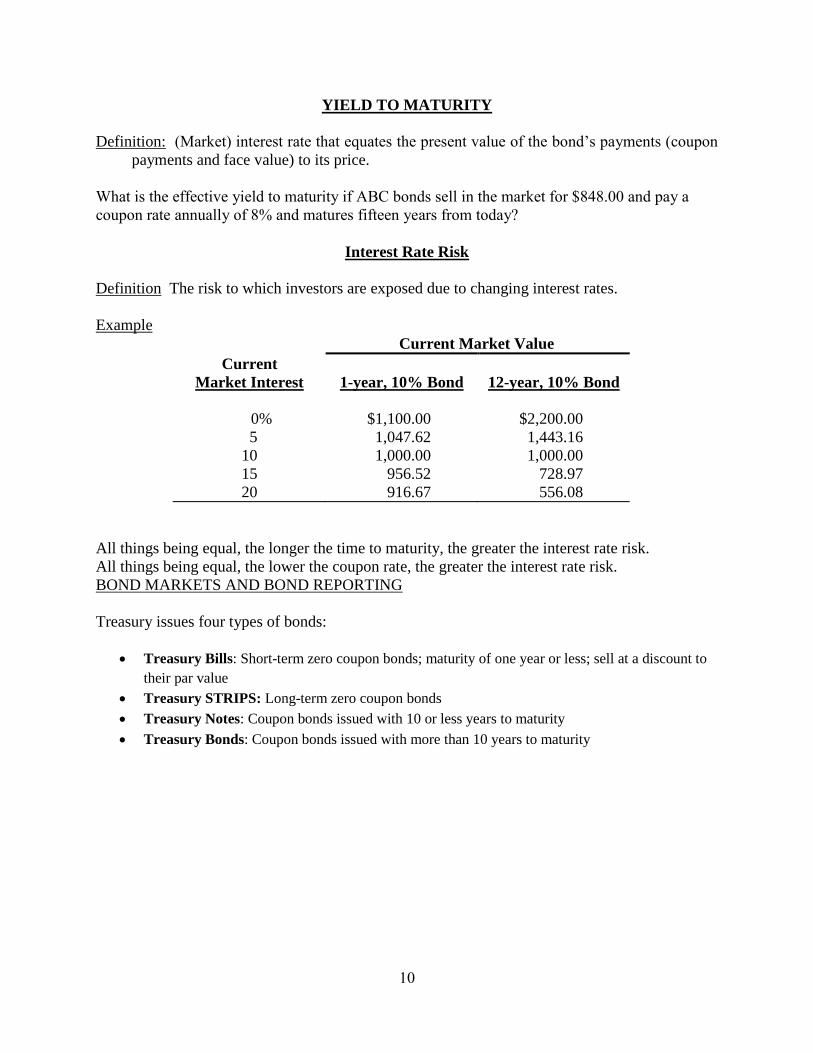

YIELD TO MATURITY

Definition: (Market) interest rate that equates the present value of the bond’s payments (coupon

payments and face value) to its price.

What is the effective yield to maturity if ABC bonds sell in the market for $848.00 and pay a

coupon rate annually of 8% and matures fifteen years from today?

Interest Rate Risk

Definition The risk to which investors are exposed due to changing interest rates.

Example

Current Market Value

Current

Market Interest

1-year, 10% Bond

12-year, 10% Bond

0% $1,100.00 $2,200.00

5 1,047.62 1,443.16

10 1,000.00 1,000.00

15 956.52 728.97

20 916.67 556.08

All things being equal, the longer the time to maturity, the greater the interest rate risk.

All things being equal, the lower the coupon rate, the greater the interest rate risk.

BOND MARKETS AND BOND REPORTING

Treasury issues four types of bonds:

Treasury Bills: Short-term zero coupon bonds; maturity of one year or less; sell at a discount to

their par value

Treasury STRIPS: Long-term zero coupon bonds

Treasury Notes: Coupon bonds issued with 10 or less years to maturity

Treasury Bonds: Coupon bonds issued with more than 10 years to maturity

11

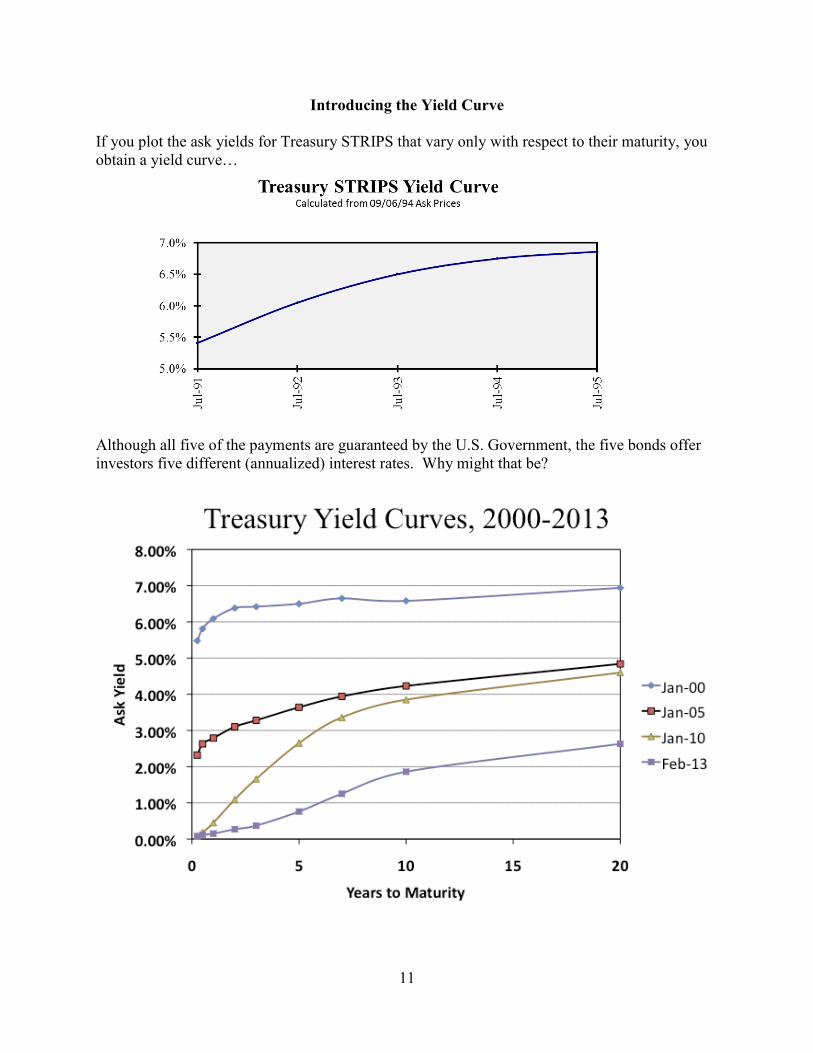

Introducing the Yield Curve

If you plot the ask yields for Treasury STRIPS that vary only with respect to their maturity, you

obtain a yield curve…

Although all five of the payments are guaranteed by the U.S. Government, the five bonds offer

investors five different (annualized) interest rates. Why might that be?

12

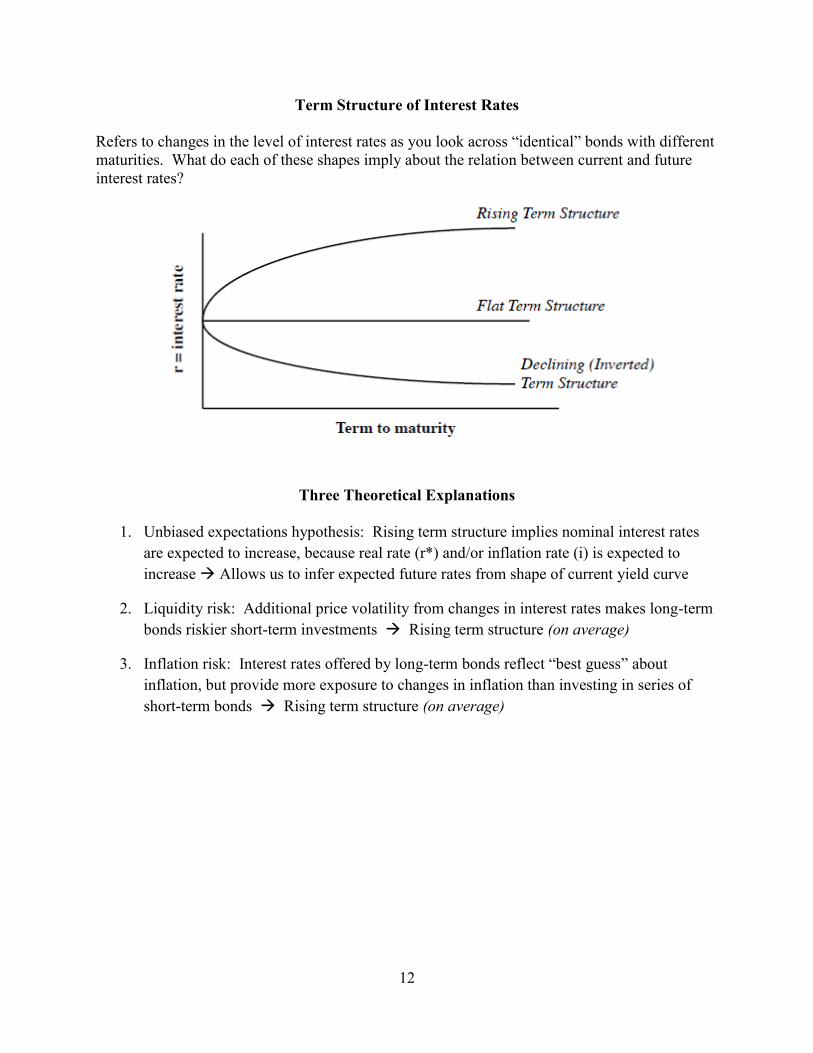

Term Structure of Interest Rates

Refers to changes in the level of interest rates as you look across “identical” bonds with different

maturities. What do each of these shapes imply about the relation between current and future

interest rates?

Three Theoretical Explanations

1. Unbiased expectations hypothesis: Rising term structure implies nominal interest rates

are expected to increase, because real rate (r*) and/or inflation rate (i) is expected to

increase Allows us to infer expected future rates from shape of current yield curve

2. Liquidity risk: Additional price volatility from changes in interest rates makes long-term

bonds riskier short-term investments Rising term structure (on average)

3. Inflation risk: Interest rates offered by long-term bonds reflect “best guess” about

inflation, but provide more exposure to changes in inflation than investing in series of

short-term bonds Rising term structure (on average)

13

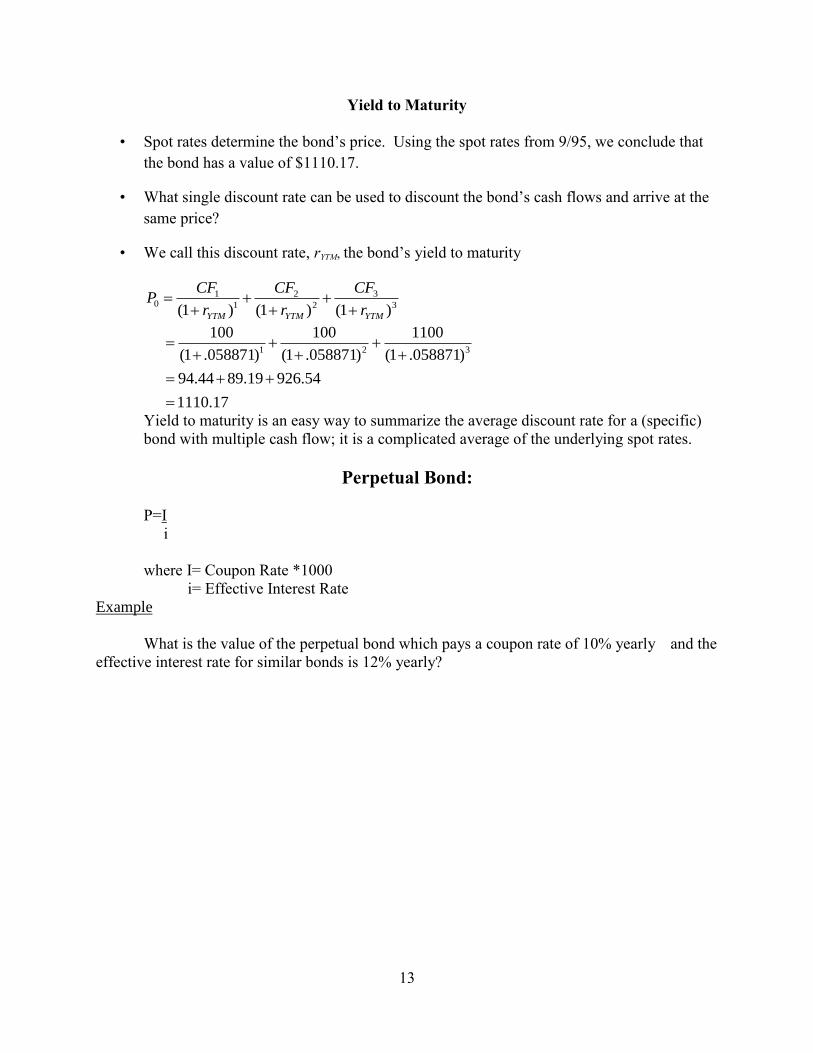

Yield to Maturity

• Spot rates determine the bond’s price. Using the spot rates from 9/95, we conclude that

the bond has a value of $1110.17.

• What single discount rate can be used to discount the bond’s cash flows and arrive at the

same price?

• We call this discount rate, rYTM, the bond’s yield to maturity

3

3

2

2

1

10

)1()1()1( YTMYTMYTM r

CF

r

CF

r

CFP

17.1110

54.92619.8944.94

)058871.1(

1100

)058871.1(

100

)058871.1(

100321

Yield to maturity is an easy way to summarize the average discount rate for a (specific)

bond with multiple cash flow; it is a complicated average of the underlying spot rates.

Perpetual Bond:

P=I

i

where I= Coupon Rate *1000

i= Effective Interest Rate

Example

What is the value of the perpetual bond which pays a coupon rate of 10% yearly and the

effective interest rate for similar bonds is 12% yearly?