savings bank account services by karnataka bank

TRANSCRIPT

1

Chapter-1

Introduction to financial services

Since 1990 there has been an upsurge in the financial services provided by various banks in financial institutions. Efficiency of emerging financial system largely depends upon the

quality and variety of financial services provided by banks and NBFC’s. The term financial services can be defined as “activities benefits and satisfactions

connected with the sale of money, that offer to users and customers, financial related value.”

Suppliers of financial services include the following type of sectors. Banking companies, financial institutions and non banking financial company.

Characteristics of financial services:

1. Intangible

2. Direct sale 3. Heterogeneity

4. Fluctuation in demand 5. Protect customers interest 6. Labour intensive, personalized service

7. Geographical dispersion 8. Lack of special identity

9. Information based 10. Require quality labour

Types of financial services

1. Merchant Banking:

A merchant banker is a financial intermediary who helps to transfer capital from those who possess it to those who need it. Merchant banking includes a wide range of activities such as

management of customer’s securities, portfolio management, project counseling and appraisal, underwriting of shares and debentures, loan syndication, acting as banker for the refund orders,

handling interest and dividend warrants etc. 2. Loan Syndication:

This is more or less similar to ‘consortium financing’. But, this work is taken up by the merchant banker as a lead manager. It refers to a loan arranged by a bank called lead manager for

a borrower who is usually a large corporate customer or a government department. The other banks who are willing to lend can participate in the loan by contributing a amount suitable to their own lending policies. Since a single bank cannot provide such a huge sum as loan, a

number of banks join together and form a syndicate.

3. Leasing:

A lease is an agreement under which a company or a firm, acquires a right to make use of a capital asset like machinery, on acquire any ownership to the asset, but he can use it and have

full control over it. He is expected to pay for all maintenance charges and repairing and operating costs.

2

4. Mutual Funds:

A mutual fund refers to a fund raised by a financial services company by pooling the

savings of the public. It is invested in a diversified portfolio with a view to spreading and minimizing risk. The fund provides Investment Avenue for small investors who cannot

participate in the equities of big companies.

5. Factoring

Factoring refers to the process of managing the sales ledger of a client by a financial service company. In other words, it is an arrangement under which a financial intermediary

assumes the credit risk in the collection of book debts for its clients. The entire responsibility of collecting the book debts passes on to the factor. His services can be compared to a del credre agent who undertakes to collect debts.

6. Forfeiting:

Forfeiting is a technique by which a forfeiter (financing agency) discounts an export bill and pay ready cash to the exporter who can concentrate on the export front without bothering about collection of export bills. The forfeiter does so without any recourse to the exporter and the

exporter is protected against the risk of non-payment of debts by the importers.

7. Venture capital:

A venture capital is another method of financing in the form of equity participation. A venture capitalist finances a project based on the potentialities of a new innovative project. It is

in contrast to the conventional ‘security based financing’. Much thrust is given to new ideas or technological innovations.

8. Custodial services:

It is yet another line of activity which has gained importance, of late. Under this, a

financial intermediary mainly provides services to clients, particularly to foreign investors, for a prescribed fee. Custodial services provide agency services like safe keeping of shares and

debentures, collection of interest and dividend and reporting of matters on corporate developments and corporate securities to foreign investors.

9. Corporate advisory services:

Financial intermediaries particularly banks have set up corporate advisory services

branches to render services exclusively to their corporate customers. For instance, some banks have extended computer terminals to their corporate customers so that they can transact some of their important banking transactions by sitting in their own office.

10.Securitization:

Securitization is a technique whereby a financial company converts its ill-liquid, non-negotiable and high value financial assets into securities of small value which are made tradable and transferable. A financial institution might have a lot of its assets which are long term in

nature. In such cases, securitization would help the financial institution to raise cash against such assets by means of issuing securities of small values to the public.

11. New products in forex market:

New products have also emerged in the forex markets of developed countries. Some of

these products are yet to make full entry in Indian markets. Among them the following are the important ones: Forward contracts, Options, Swaps

3

Chapter-2

COMMERCIAL BANKS

In modern economy commercial Banks Play an important role in the financial sector. A Bank is an institution dealing in money and credit. Credit money is the major component of

money supply in a modern economy. Commercial banks are the creators of credit. The strength of economy of any country basically depends on a sound and solvent banking system. A Commercial bank is a profit seeking business firms dealing in money or rather claims to money.

It safeguards the savings of the public and give loans and advances. The Banking Companies Act of 1949, defines banking company as “accepting for the purpose of lending or investment of

deposit money from the public, repayable on demand or otherwise and withdrawable by cheque, drafts, order or otherwise”.

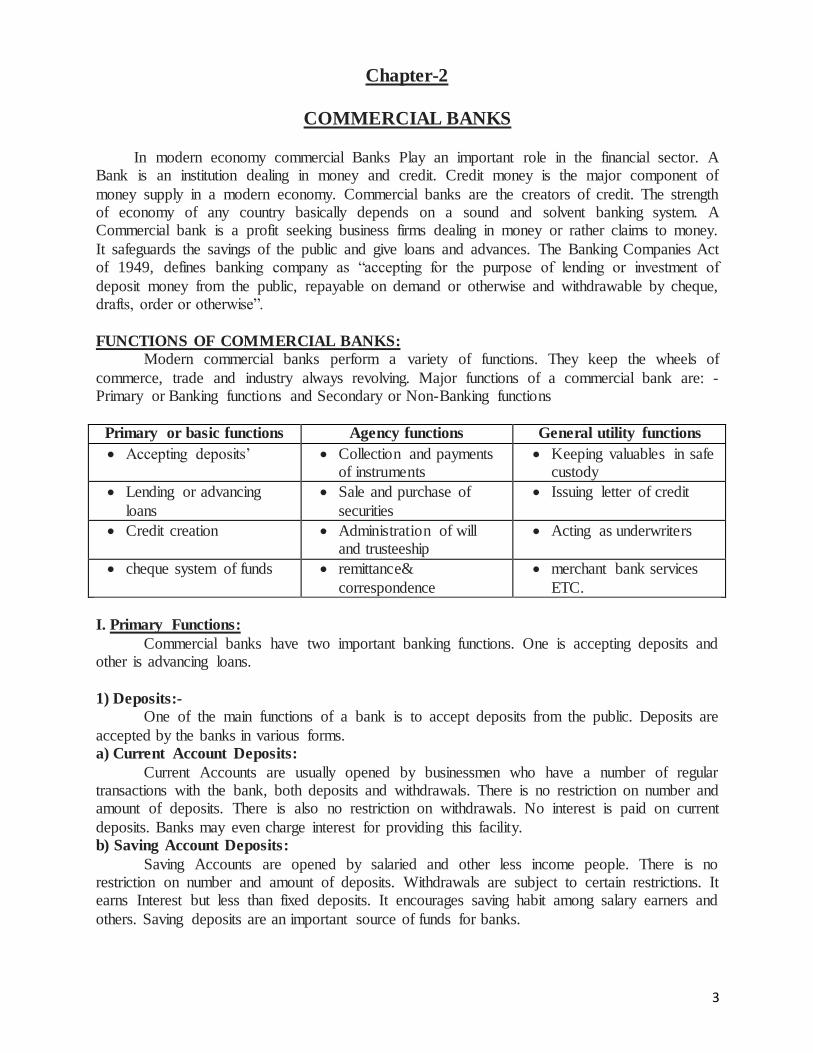

FUNCTIONS OF COMMERCIAL BANKS:

Modern commercial banks perform a variety of functions. They keep the wheels of

commerce, trade and industry always revolving. Major functions of a commercial bank are: - Primary or Banking functions and Secondary or Non-Banking functions

Primary or basic functions Agency functions General utility functions

Accepting deposits’ Collection and payments of instruments

Keeping valuables in safe custody

Lending or advancing

loans

Sale and purchase of

securities

Issuing letter of credit

Credit creation Administration of will and trusteeship

Acting as underwriters

cheque system of funds remittance&

correspondence

merchant bank services

ETC.

I. Primary Functions:

Commercial banks have two important banking functions. One is accepting deposits and other is advancing loans.

1) Deposits:- One of the main functions of a bank is to accept deposits from the public. Deposits are

accepted by the banks in various forms. a) Current Account Deposits:

Current Accounts are usually opened by businessmen who have a number of regular transactions with the bank, both deposits and withdrawals. There is no restriction on number and amount of deposits. There is also no restriction on withdrawals. No interest is paid on current

deposits. Banks may even charge interest for providing this facility. b) Saving Account Deposits:

Saving Accounts are opened by salaried and other less income people. There is no restriction on number and amount of deposits. Withdrawals are subject to certain restrictions. It earns Interest but less than fixed deposits. It encourages saving habit among salary earners and

others. Saving deposits are an important source of funds for banks.

4

c) Fixed Account Deposits: Deposits in fixed account are time deposits. Money under this account is deposited for a

certain fixed period of time varying from 15 days to several years. A high rate of interest is paid. If money is withdrawn before expiry date, the depositor receives lower rate of interest.

d) Recurring Account Deposits: In Recurring deposit, a specified amount is regularly deposited by account holder, at an

internal of usually a month. This is to form the habit of small savings among the people. At the

end of maturity period, the account holder gets a substantial amount.

2) Loans and Advances: Banks not only mobilize money but also lend to its credit worthy customers for

maximizing profits. Loans and Advances are granted.

a) Overdraft: Commercial banks grant overdraft facility to current account holders Under this system a

borrower is allowed to draw more than what is deposited in his account. The borrower is granted to a fixed additional amount against collateral security. Interest is charged for actual amount drawn.

b) Cash Credit:

Cash credit is given by the bank to any businessman to meet regular working capital

needs, against the security of goods or personal security. Interest is charged on actual amount drawn by the customer. c) Discounting of Bills:

When the holder of the bill is not in a position to wait till the maturity of the bill and requires cash urgently, he sells the bill of exchange to bank. Bank advance credit by discounting

bills of exchange, government securities or any other approved financial instruments. The bank purchases the instruments at a discount. d) Money at Call:

Banks also grant loans for a very short period, generally not exceeding 7 days. Such advances are repayable immediately at a short notice hence they are called as Money at Call or

Call money. These loans are given to dealers or brokers in stock market against Collateral Securities. f) Direct Loans:

Loans are given to customers against the security of moveable properties. Their maturity varies from 1 to 10 years. Interest has to be paid on entire loan amount sanctioned. Loans are of

many types like personal loans, term loans, call loans, participative loans, collateral loans etc. g) Loans to Agriculture: Banks grant short-term credit to agriculture at a lower rate of interest. Loans are granted

for irrigation, purchase of equipments, inputs, cattle etc. h) Loans To Industries:

Banks grant secured loans to small and medium scale industries to meet their working capital needs. The time period may be from one to five years. It may be in the form of Overdraft, cash credit or direct loan.

i) Loans to Foreign Trade: Loans are granted to export and import in the form of direct loans, discounting of bills,

guarantee for deferred payments etc. Here the rate of interest is low. j) Consumer Credit / Personal loans:

Banks also grant credit to household in a limited amount to buy some durable consumer

goods like television sets, refrigerators, washing machine etc. Such consumer credit is repayable in installments.

5

II. Agency Services:

Banks perform certain functions on behalf of their customers. While performing these services, banks act as agents to their customers, hence these are called as agency services.

Important agency functions are a) Collection: Commercial banks collect cheques, drafts, bills, promissory notes, dividends,

subscriptions, rents and any other receipts which are to be received by the customer. For these services banks charge a nominal amount.

b) Payment: Banks also makes payments on behalf of their customers like paying insurance premium, rent, taxes, electricity and telephone bills etc for such services commission is charged.

c) Income Tax Consultant: Commercial banks act as income-tax consultants. They prepare and finalise the

income tax returns of their clients. d) Sale and Purchase Of Financial Assets: As per the customers instruction banks undertake sale and purchase of securities, shares

and any other financial assets. Nominal charges are charged by a bank. e) Trustee, Executor and Attorney:

As a trustee, banks becomes the custodian and manager of customer funds. Bank also acts as executor of deceased customer’s will. As an Attorney the banks sign the documents on behalf of customer.

f) E- Banking: Through Electronic Banking, a customer can operate his bank account through internet.

He can make payments of various bills. He can even transfer money from one place to another.

III. Utility Services:

Modern Commercial banks also performs certain general utility services for the community, such as

a) Letter Of Credit: Banks also deal in foreign trade. They issue letter of credit and provide guarantee to foreign traders for the soundness of their customers.

b) Transfer Of Funds: Banks arrange transfer of funds cheaply and safely from one place to another. Transfer

can be in the form of Demand draft, Mail transfer Travelers’ cheques etc. c) Underwriting: This facility is provided to Joint Stock Companies and to government to enable them to

raise funds. Banks guarantee the purchase of certain proportion of shares, if not sold in the market.

d) Locker Facility: Safe Lockers are provided to the customers. So that they can deposit their valuables like Jewellery, Securities, Shares and other documents.

e) Credit Cards: Credit card facility have been introduced by commercial banks. It enables the holder to

minimize the use of hard cash. Credit card is a convenient medium of exchange which enables its holder to buy goods and services from member – establishment without using money.

6

Chapter-3

Industry profile

Banking in India in the modern sense originated in the last decades of the 18th century. The among the first banks were Bank of Hindustan, which established in 1770 and liquidated in

1829-32; and General Bank of India, established 1786 but failed in 1791. The largest bank, and the oldest still in existence, is the State Bank of India. It originated as the Bank of Calcutta in June 1806. In 1809, it was renamed as the Bank of Bengal. This was one of the three banks

funded by a presidency government, the other two were the Bank of Bombay and the Bank of Madras. The three banks were merged in 1921 to form the Imperial Bank of India, which upon

India's independence, became the State Bank of India in 1955. For many years the presidency banks had acted as quasi-central banks, as did their successors, until the Reserve Bank of India was established in 1935, under the Reserve Bank of India Act, 1934.

In 1960, the State Banks of India was given control of eight state-associated banks under

the State Bank of India (Subsidiary Banks) Act, 1959. These are now called its associate banks. In 1969 the Indian government nationalized 14 major private banks. In 1980, 6 more private banks were nationalized. These nationalized banks are the majority of lenders in

the Indian economy. They dominate the banking sector because of their large size and widespread networks.

The Indian banking sector is broadly classified into scheduled banks and non-scheduled

banks. The scheduled banks are those which are defined under the 2nd Schedule of the Reserve

Bank of India Act, 1934. The scheduled banks are further classified into: nationalized banks; State Bank of India and its associates; Regional Rural Banks (RRBs); foreign banks; and

other Indian private sector banks. The term commercial banks refer to both scheduled and non-scheduled commercial banks which are regulated under the Banking Regulation Act, 1949. By 2010, banking in India was generally fairly mature in terms of supply, product range and

reach-even though reach in rural India still remains a challenge for the private sector and foreign banks. The Reserve Bank of India is an autonomous body, with minimal pressure from the

government. By 2013 the Indian Banking Industry employed 1,175,149 employees and had a total of

109,811 branches in India and 171 branches abroad and manages an aggregate deposit of 67504.54 billion (US$1.1 trillion or €840 billion) and bank credit of 52604.59

billion (US$830 billion or €650 billion). The net profit of the banks operating in India was 1027.51 billion (US$16 billion or €13 billion) against a turnover of 9148.59 billion (US$140 billion or €110 billion) for the financial year 2012-13.

On 28 Aug, 2014,Pradhan Mantri Jan Dhan Yojana (Hindi: प्रधानमंत्री जन धन योजना) Prime Minister's People Money Scheme) is a scheme for comprehensive financial inclusion launched by the Prime Minister of India, Narendra Modi. Run by Department of

Financial Services, Ministry of Finance, on the inauguration day, 1.5 Crore (15 million) bank accounts were opened under this scheme. By 10 January 2015,11.5 crore accounts were opened,

with around 8698 crore (US$1.4 billion) were deposited under the scheme, which also has an option for opening new bank accounts with zero balance.

7

Chapter-4

Company profile

Karnataka Bank is a major private sector

banking institution based in the coastal city of Mangalore in Karnataka, India. The Reserve Bank of

India has designated Karnataka Bank as an A1+-class scheduled commercial bank. The bank now has a national presence with a network of some 628

branches across 21 states and two Union territories. It has over 6000 employees and 6.7 million customers, including farmers and artisans in villages and small towns throughout the country. Its shares are entirely privately owned by some 1,29,862 shareholders.

Karnataka bank says ”Our Mission Is To Be A Technology Savvy, Customer Centric Progressive Bank

With A National Presence, Driven By The Highest Standards Of Corporate Governance And Guided By Sound

Ethical Values."

The bank has the Best Bank Award for "Managing IT Risk" under small bank category for the year 2010-11, instituted by Institute for Development and Research in Banking

Technology (IDRBT). Shri Anand Sinha, deputy governor, Reserve Bank of India and chairman, IDRBT presented the award to Shri P. Jayarama Bhat, managing director at a function held in Hyderabad on 4 August 2011 in the presence of Shri B. Sambamurthy, director, IDRBT.

Karnataka Bank was incorporated on 18 February 1924, and commenced business on 23

May 1924. Its founders established it at Mangalore. Among the founders, who created the bank to serve the South Kanara region, was B. R. Vysaray Achar. Another important personality associated with the bank was K. S. N. Adiga, who served as Chairman from 1958 to 1979.

In the 1960s Karnataka Bank acquired three smaller banks. In 1960 Karnataka Bank

acquired the Sringeri Sharada Bank, which was established in 1942 and which had four branches when Karnataka acquired it. Four years later, Karnataka Bank took over the assets and liabilities of the Chitradurg Bank (also known as Chitradurg Bank), which was established in

1868 in Mysore State and was the oldest bank in Mysore. Lastly, in 1966 Karnataka Bank took over the assets and liabilities of the Bank of Karnataka, in Hubli. Bank of Karnataka had been

established in 1946 and had opened one branch in Belgaum in 1947. In 2000, Karnataka Bank signed a memorandum of understanding with Infosys

Technologies to develop a core-banking solution called FINACLE. Over 221 branches were networked up to March 31, 2004. The main motto of this program is "Anytime/Anywhere

banking". In 2002, the bank concluded a pact with Corporation Bank for sharing its ATMs. The total business turnover of the Bank was 68928.32 crore as on 31st March 2014, an

increase of 12.51% over the preceding year. The total assets of the Bank increased from 41526.38 crore to 47028.80 crore recording a growth of 13.25% for the year 2013-14.

Karnataka Bank has been striving to keep pace with advances in banking technology by adopting core banking and Internet banking, and establishing its "Money Plant" automated teller machine system.

8

Chapter-5

Savings bank account services provided by Karnataka Bank Ltd.

Karnataka Bank presents an array of savings bank services, ideally designed to suit the

needs of various segments of the society. Karnataka bank has divided its customers into various

segments based on age, profession etc meeting their individual demands. The various savings

bank account services provided by Karnataka Bank to its customers are as follows.

KBL Kishore

KBL Tarun

KBL Salary Privilege

KBL Vanitha

SB General

SB Money Sapphire

SB Money Platinum

9

KBL Kishore:

KBL Kishore is a savings bank account with an objective to encourage savings habits among school children between the age of 12 years to 18 years.

Features:

No minimum balance

Simplified account opening procedures

Free of charge Demand Drafts for the purpose of exam fee, prospectus fee, tuition fee

etc.

Free transfer of funds up to Rs. 50,000/- per month from parent’s account to student’s

account

Debit card with per day cash withdrawal limit of Rs. 5000/- and purchase limit of Rs.

1500/-

‘Cyber Kid’ – internet banking facility

KBL Tarun:

KBL Tarun is an exclusive savings bank account for students aged between 18 years and

25 years. Features:

Any branch banking with no minimum balance

Simplified account opening procedures

Free of charge Demand Drafts for the purpose of exam fee, prospectus fee, tuition fee

etc.

DD’s can be purchased from any branch

Free transfer of funds up to Rs. 50,000/- per month from parent’s account to student’s

account

Multi city cheque facility

Money plant VISA international debit cards

Fastest way of interbank fund transfers through RTGS/ NEFT

Free SMS alert facility, monthly e-statement, cheque books.

10

KBL Salary Privilege:

KBL salary privilege is a savings bank account, an exclusive banking option for employees of state/ central Govt. corporations, bodies, PSUs, MNCs, educational institutions and other reputed companies / firms / concerns.

Features:

No minimum balance Multicity cheque facility

DD’s can be purchased from any branch Free transfer of funds up to Rs. 50,000/- per month from parent’s account to student’s

account Multi city cheque facility Money plant VISA international debit cards

Fastest way of interbank fund transfers through RTGS/ NEFT Free SMS alert facility, monthly e-statement, cheque books.

Free registration to ‘money click’ internet banking facility KBL Vanitha:

Karnataka Bank introduced KBL Vanitha Savings Bank Account with an objective to

encourage savings habits among women and to help overcome the fear of managing their wealth.

Features:

Free fund transfer up to Rs. 50,000/- per month to 2 savings account in the name of

children. Multi branch banking facility Money plant VISA international debit card

Internet banking Online payment through debit card

Mobile banking (M-commerce) available free Free SMS alert facility for all debit and credit transactions of Rs. 5000/- and above. All risk insurance cover for jewellery of Rs. 50,000/- *

SB General:

SB General is a savings bank account services with general features like

Features:

Minimum monthly average balance of Rs. 1000/- Any branch cash deposit and withdrawal Payment of multi city cheques

Fund transfers within the bank are available with free of charges up to a limit

11

SB Money Sapphire:

A specially designed savings bank account with a host of free facilities. Features:

Monthly average balance of Rs. 10,000/-

Any branch cash deposit & withdrawal Payment of multi city cheques Cheque collection are available with enhanced free limits

Free funds transfer within the bank Purchase of demand drafts

SB Money Platinum:

Savings bank account loaded with maximum benefits

Features:

Monthly average balance of Rs. 5,00,000/-

Free payment of multi city cheques Cheque collections are free

Any branch cash deposit and withdrawal are available with maximum free limits Free fund transfer within the bank

The above SB schemes (SB general, SB money sapphire, SB money platinum) have the following features in common:

Money plant VISA international debit cards Internet banking facility

Free cheque books Free SMS alerts, monthly e-statements

Fast collection of cheques- cheques can be deposited at any branch

Other than the above varieties of savings accounts serving different purposes there are some more types of savings accounts like:

SB Gen- without a cheque book – with a monthly average balance requirement of Rs. 200/-

SB ILSB account – An insurance linked savings bank account.

The above both have all the facilities like free SMS alerts, money plant VISA debit card, internet

banking, debit card payments etc.*

12

Chapter - 6

Findings

The Reserve Bank of India has designated Karnataka Bank as an A1+-class scheduled

commercial bank.

The bank has the Best Bank Award for "Managing IT Risk" under small bank category

for the year 2010-11.

The Karnataka Bank has designed variety type of SB a/c’s ranging the monthly average

minimum balance of Rs. 0/- to Rs.5,00,000.

The bank provides free debit card, internet banking and SMS alerts to almost every type

of SB a/c.

The transaction limit of Rs.5000/- per day in KBL Kishore account is a bit high.

Suggestions

Karnataka Bank needs to work on its KBL Kishore SB a/c on the maximum withdrawal

and shopping limit through debit card.

Karnataka Bank also should look at the monthly average balance of Rs.5,00,000 in SB

policy SB Money Platinum.

SMS alerts for KBL Vanitha is only above the transactions of Rs.5000/- and above this

need to be taken care off.

SB Gen with monthly average balance of Rs.200/- has no cheque book option, which is

to be considered.

Conclusion

Overall Karnataka Bank is an private sector bank awarded A1+ class scheduled bank by

RBI

Karnataka Bank has faster services like fund transfers e-payments.

The bank always keeps pace with the technology and introduces technology into its

services.

The savings account services provided by Karnataka Bank reaches all the segments of the

country which is an added advantage

If Karnataka Bank takes care of some of the issues in their SB a/c policies it can attract

more number of customers worldwide creating them a path to expand globally.