sas institute ”risk forum”, 3. april 2014 adm. direktør idar kreutzer, finans norge...

TRANSCRIPT

SAS Institute ”Risk Forum”, 3. april 2014

Adm. direktør Idar Kreutzer, Finans Norge

RISIKOSTYRING SOM STRATEGISK VIRKEMIDDEL I FORSIKRING

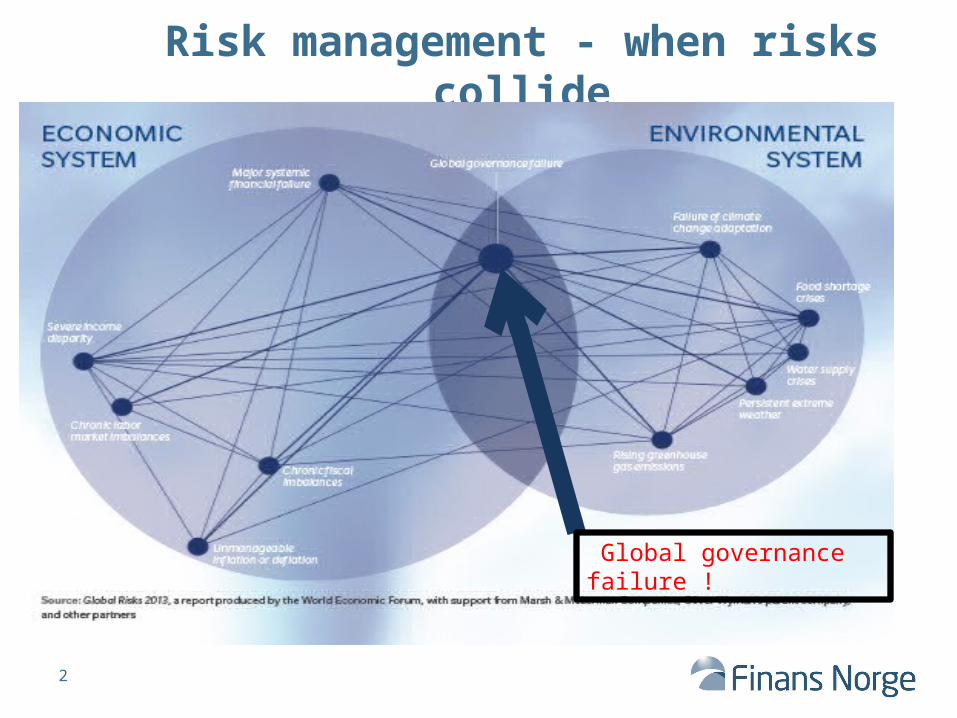

Risk management - when risks collide

Global governance failure !

2

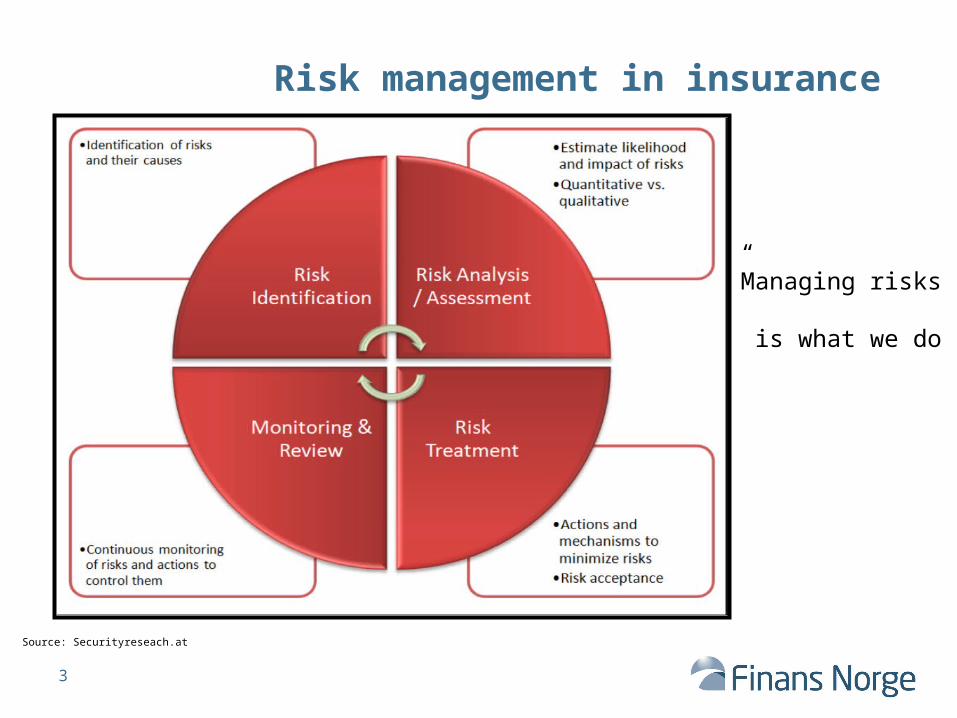

Risk management in insurance

”Managing risks

is what we do”

Source: Securityreseach.at

3

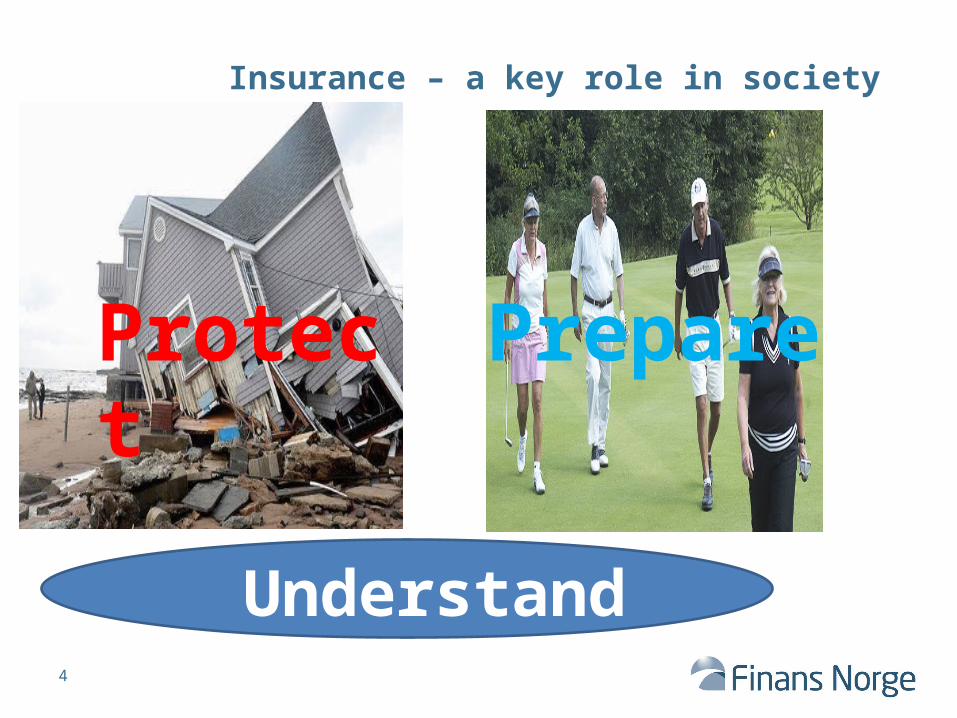

Insurance – a key role in society

Understand

PrepareProtect

4

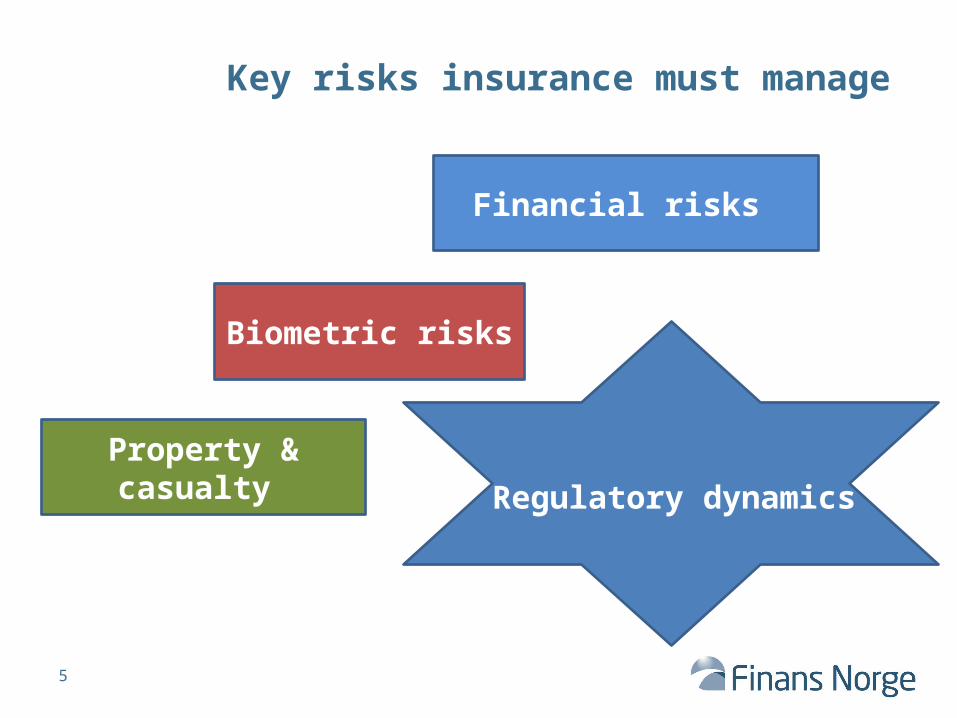

Key risks insurance must manage

Financial risks

Biometric risks

Property & casualty Regulatory dynamics

5

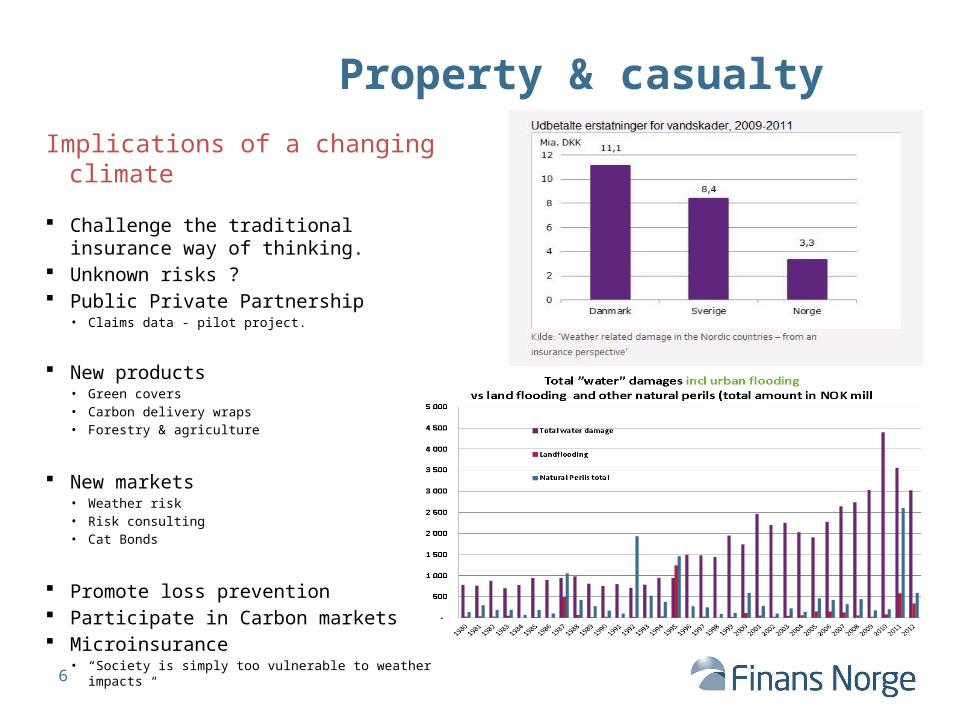

Property & casualty

Implications of a changing climate

Challenge the traditional insurance way of thinking.

Unknown risks ? Public Private Partnership

• Claims data - pilot project.

New products• Green covers• Carbon delivery wraps• Forestry & agriculture

New markets• Weather risk• Risk consulting• Cat Bonds

Promote loss prevention Participate in Carbon markets Microinsurance

• “Society is simply too vulnerable to weather impacts “

6

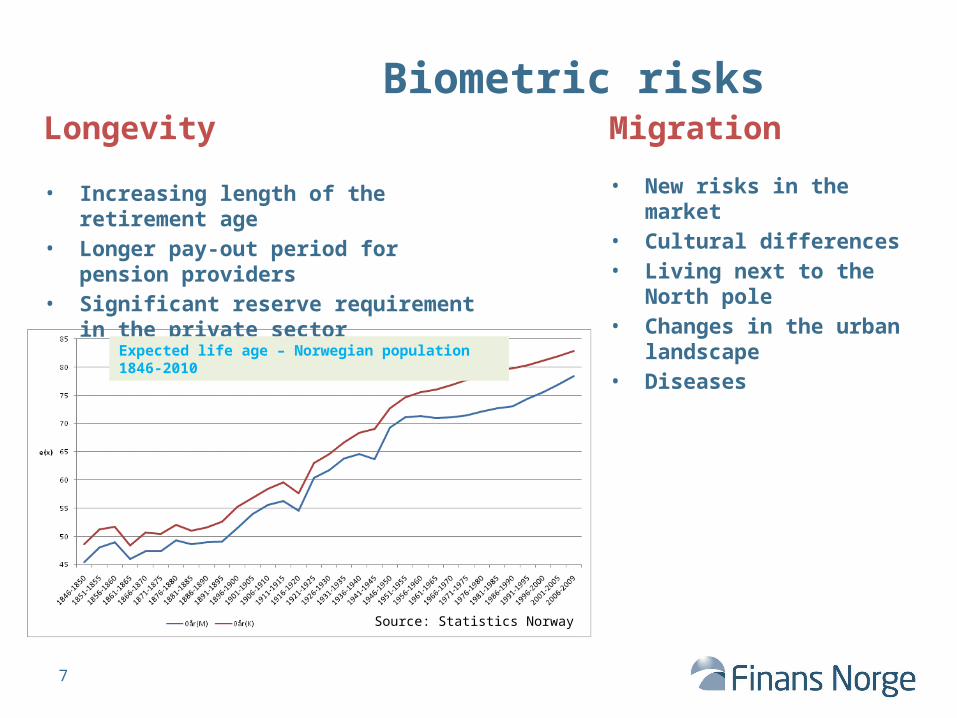

Biometric risksLongevity

• Increasing length of the retirement age• Longer pay-out period for pension

providers• Significant reserve requirement in the

private sector

Migration

• New risks in the market• Cultural differences• Living next to the North

pole• Changes in the urban

landscape• DiseasesExpected life age – Norwegian population 1846-2010

ddddddddddddddddddddd Source: Statistics Norway

7

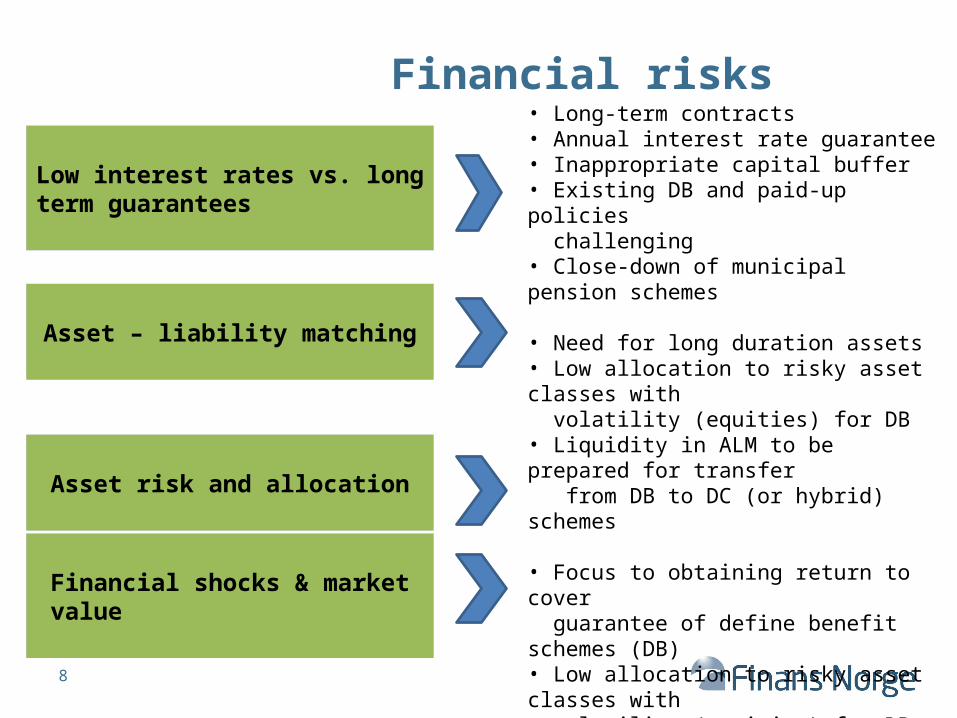

Financial risks

Low interest rates vs. long term guarantees

Asset – liability matching

Asset risk and allocation

Financial shocks & market value

• Long-term contracts• Annual interest rate guarantee• Inappropriate capital buffer • Existing DB and paid-up policies challenging• Close-down of municipal pension schemes • Need for long duration assets• Low allocation to risky asset classes with volatility (equities) for DB• Liquidity in ALM to be prepared for transfer from DB to DC (or hybrid) schemes

• Focus to obtaining return to cover guarantee of define benefit schemes (DB)• Low allocation to risky asset classes with volatility (equities) for DB. Any surplus of guarantees used to build buffers in DB • Reduce market risk • Hold to maturity management in focus

8

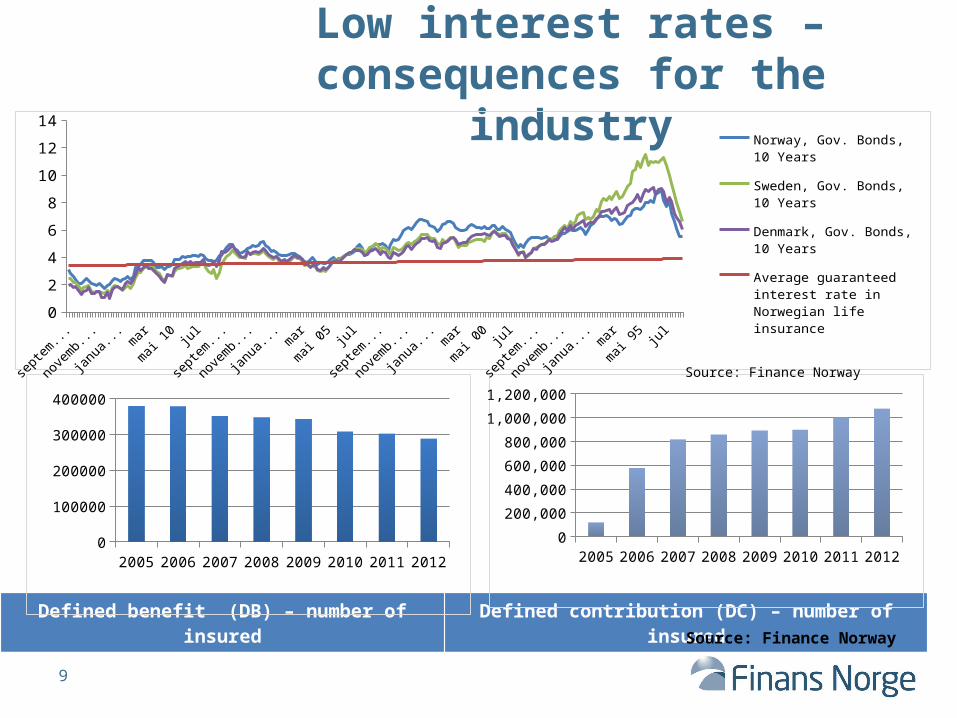

Low interest rates – consequences for the industry

Defined benefit (DB) – number of insured Defined contribution (DC) – number of insured

2005 2006 2007 2008 2009 2010 2011 20120

50000100000150000200000250000300000350000400000

2005 2006 2007 2008 2009 2010 2011 20120

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Source: Finance Norway

januar

94juli 9

5

januar

97juli 9

8

januar

00juli 0

1

januar

03juli 0

4

januar

06juli 0

7

januar

09juli 1

0

januar

12juli 1

30

2

4

6

8

10

12

14

Norway, Gov. Bonds, 10 Years

Sweden, Gov. Bonds, 10 Years

Denmark, Gov. Bonds, 10 Years

Average guaranteed interest rate in Norwegian life insurance

Source: Finance Norway

9

Liability driven investmentsValuing liabilities – and matching the duration

If the liabilities' duration is 15, then a 2 percentage points fall in interest rates alters the present value of liabilities with 30% if this change is simply carried through for the purpose of liability valuation

Which assets (apart from too few long dated bonds) yield 30% with certainty over 4 months?

Stylistic example of liabilities

2 % point fall in rates

Assets100

Liabilities100

Liabilities130

Assets100

30% increase in liabilities

Example: duration 15

Source: Bloomberg 20 yrs swap

?

2,53

3,54

4,55

5,5

SEK EUR GBP

10

Regulatory dynamics – life & pensions

Main challenges:

• Risk based capital requirements (Solvency II)

• Macro economic prudential regulation

• IFRS 4 phase II (Market Value)• Systemically important (IAIS

global capital standards)

ORSA

Capital requirement calculation

Solvency II:A new risk management system

11

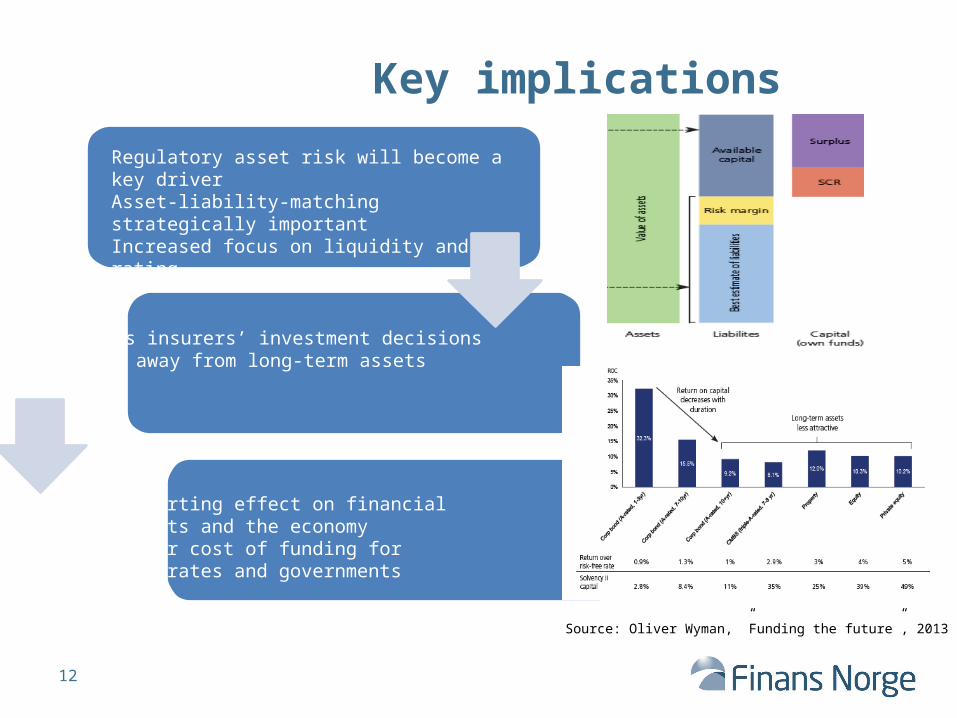

Key implications

Regulatory asset risk will become a key driverAsset-liability-matching strategically importantIncreased focus on liquidity and rating

Affects insurers’ investment decisionsMoving away from long-term assets

Distorting effect on financial markets and the economyHigher cost of funding for corporates and governments

Source: Oliver Wyman, ”Funding the future”, 2013

12

Systemic risk – not just banks?

• IAIS 10 October 2013: Global quantitative capital standards

Peter Braumüller, chair of the IAIS Executive Committee:

“It is undeniable that the business of insurance is global, and global issues demand global responses,” [...]“This is why the IAIS, whose Members constitute nearly all of the world’s insurance supervisors, has committed to develop and implement the first-ever risk based global insurance capital standard.”

13

Summary

• The times and risks are changing • Understanding and managing risks – ”that’s what we do!”

• We have to deal with a changing regulatory environment

• A well functioning insurance industry is crucial to society

14

TAKK FOR OPPMERKSOMHETEN

15