san diego convention center and stadium project meetings … · 2016-08-24 · san diego convention...

TRANSCRIPT

San Diego Convention Center and Stadium Project Meetings Market and Impact Analysis Submitted to: Conventional Wisdom Corp. David O’Neal Chairman 2703 Rew Circle Ocoee, Florida 34761 August 23, 2016

w w w . h u n d e n p a r t n e r s . c o m

August 23, 2016 Conventional Wisdom Corp. David O’Neal Chairman 2703 Rew Circle Ocoee, Florida 34761

Dear Mr. O’Neal,

As you know, Conventional Wisdom Corp. engaged Hunden Strategic Partners (HSP) to perform a convention and meetings market analysis for the proposed San Diego Convention Center and Stadium Project initiated by the NFL San Diego Chargers franchise. The study has determined demand and projected impacts associated with the Project, specifically with relation to attendance, room nights generated, and potential incremental hotel rates associated with compression from the convention activity, as well as compression from NFL games. The attached is our final report.

This deliverable has been prepared under the following general assumptions and limiting conditions: § The findings presented herein reflect analysis of primary and secondary sources of information

that are assumed to be correct. HSP utilized sources deemed to be reliable, but cannot guarantee their accuracy.

§ No responsibility is taken for changes in market conditions after the date of this report and no obligation is assumed to revise this report to reflect events or conditions occurring after the date of this report.

§ HSP has no control over the timing of the Project opening. § Macroeconomic events affecting travel and the economy cannot be predicted and may impact

the development and performance of the project.

We have enjoyed serving you on this engagement and look forward to providing you with continuing service.

Sincerely yours,

Robin Scott Hunden

Hunden Strategic Partners

TABLE OF CONTENTS

----------- Executive Summary

Chapter 1 Demand and Impact

Appendix A Convention Industry Overview and Trends

Appendix B Convention Market Competitive and Comparable Analysis

Appendix C Influence of Comparable Downtown Stadiums

Appendix D Meeting Planner Interviews

Appendix E Hotel Market Analysis

Appendix F Comparable Convention City Hotel Tax Rate Data

Chargers Stadium and Convention Center Study Executive Summary - Page 2

PROJECT OVERVIEW Conventional Wisdom Corp. (Client) contracted with Hunden Strategic Partners (HSP) to perform a multi-pronged study related to the proposed San Diego Convention Center and Stadium Project initiated by the San Diego Chargers NFL franchise (Project). The study included an analysis of the likely market that the Project would penetrate for meetings, conferences and conventions, the experience of other similar facilities and cities, and the ultimate impact that the Project would have on the City of San Diego.

HSP conducted market research to determine the number and type of events that have the following characteristics:

! Interested in holding conventions and meetings in San Diego,

! Require dates between August 1st and January 31st, and

! Require up to 150,000 square feet of exhibition space (between August and January), and/or will use the entire facility with approximately 260,000 square feet of exhibition space.

HSP profiled the proposed mix-use Project, focusing on the convention facilities, as well as the potential opportunities and constraints provided by NFL usage. HSP also analyzed the loss of room nights and related impact, if the Project is not built.

The results of the study provide a better understanding of the market for conventions and similar events. The market analysis helps inform the demand and projected impact associated with the Project, specifically in relation to attendance, room nights generated, and potential incremental hotel room rates associated with increased demand from the convention activity, as well as from NFL games.

San Diego Convention Center and Stadium Project

The ballot measure supporting this Project calls for approximately 385,000 square feet of net leasable exhibit hall, meeting room and ballroom space. An initial, preliminary conceptual design for the project – subject to change – allocates the space as follows:

! 130,000 square foot exhibit hall,

! 30,000 square feet of swing space

! 100,000 square feet of stadium event level exhibit space,

! 63,000 square feet of ballroom space,

! 80,000 square feet of meeting rooms,

The Project would include approximately 61,000 seats, including club seats, loge seats, suites and other premium seat options. There is an expansion option to increase seating capacity to approximately 72,000 seats.

Chargers Stadium and Convention Center Study Executive Summary - Page 3

KEY FINDINGS Based on HSP’s research of the market, the performance of the existing facility, meeting planner interviews, experience in other markets, and analysis of similar situations, the following conclusions have been reached:

! More than 200,000 San Diego Hotel Room Nights Annually. Based on the analysis, the Project will induce and retain more than 2 million new hotel room nights to City of San Diego hotels in the first ten years of operation and average approximately 225,000 room nights per year by stabilization. Most of these additional hotel room nights will be due to new conventions and other groups coming to San Diego that currently are not able to be accommodated. Others will be due to the impact of Chargers home games, major concerts and other sporting events to be scheduled. In total, San Diego hotel room revenue is expected to increase by more than $750 million over the first ten years.

! Event Demand Leads to Major ADR Increases. Strong demand that pushes occupancy and rates higher and ripples out to surrounding areas generated by large events will increase hotel room revenue by nearly $200 million over the first ten-year period.

! Major Hotel Tax Revenue Increase. HSP expects hotel tax revenue of more than $125 million over the first ten years solely due to the Project.

! Hundreds of New Events. The new Project is expected to be available for non-NFL events 95 percent of days per year, leading to more than 100 events per year, nearly all of which will be new to the City of San Diego, except existing NFL and college bowl games.

! Hundreds of Thousands of Attendees. HSP estimates that the Project’s events will attract more than 200,000 non-Sports and Entertainment attendees per year and more than 900,000 total attendees per year.

! Consistent Convention Activity in Multiple Venues is Preferred. Given that the existing convention venue and the Project would likely be managed to maximize combined impact and market penetration, the Project helps continue, and respond to, a major trend in the convention industry of pursuing and hosting numerous overlapping or back-to-back mid-sized conventions that provide consistent hotel usage. This is in contrast to the prior “space race” where cities have attempted to lure the few largest conventions. The drawback to this “space race” strategy is that there is often a large time gap between major events. Cities like San Francisco, Seattle and Indianapolis – all successful convention cities – have adjusted their focus to filling the calendar with consistent medium-sized conventions that can occur simultaneously or back-to-back. Convention centers today and their major hotel partners have recognized that having a “two-piston” convention engine, where one mid-sized show is occurring while another moves in or out, is more likely to lead to consistently full-hotels.

! Football Schedule Allows for Long-Term Convention Bookings During Peak Times. HSP conducted an analysis of the calendar associated with groups that would likely come to a San Diego convention facility if dates were available. HSP also analyzed a draft, theoretical and conservatively projected long-range schedule for the Chargers. The NFL has worked well with

Chargers Stadium and Convention Center Study Executive Summary - Page 4

other cities that have or had convention needs associated with stadium spaces, such as Houston, Indianapolis, Seattle and St. Louis. The San Diego Chargers intend to work with the NFL to establish that during each season, one Sunday per month could be booked and blocked long term and more than a year in advance for conventions, along with every Monday and Thursday from mid-September through mid-November. The team and league will also enable three of these long-term bookings to be secured during the critical mid-September to mid-November eight-week time period (one each month), which is a busy time for conventions. This provides calendar availability and certainty for 67 percent or more of the days in this critical time period, as well as 100 percent availability from February through August (and possibly January – August, if there is no post-season play). For dates that become available after the NFL calendar is issued, the facility can sell available dates to groups that have shorter booking windows. These groups tend to pay more in hotel rates as the hotels are already filled with other long-term bookings.

! Football Calendar Dovetails Well with Convention Facilities During Holidays. Given that the Chargers are likely to play during and around holiday weekends such as Thanksgiving, Christmas and New Year’s, and conventions almost universally avoid scheduling during these times, HSP’s analysis suggests that, relative to a convention-only facility, those holiday periods at the proposed Project would likely be occupied with NFL or other events, such as concerts or the circus, during many of these periods, generating hotel room nights that would not otherwise be generated at a convention-only center.

! Benefits of a Downtown Convention and Sports Facility. The City of San Diego has experienced the positive impact of having the MLB San Diego Padres located downtown, which played a major role in revitalizing downtown and the Gaslamp Quarter’s restaurants, shopping, hotels and the overall convention environment. HSP’s analysis of other cities where the NFL stadium moved downtown shows the positive impact such a move can make on the downtown area, the overall city’s image and economy. It also makes for a fun and impactful pre- and post-game environment.

In conclusion, HSP’s analysis shows that the proposed Project would have a major positive impact on the City of San Diego’s hotels and the overall local economy.

TABLE OF CONTENTS ----------- Executive Summary

Chapter 1 Demand and Impact

Appendix A Convention Industry Overview and Trends

Appendix B Convention Market Competitive and Comparable Analysis

Appendix C Influence of Comparable Downtown Stadiums

Appendix D Meeting Planner Interviews

Appendix E Hotel Market Analysis

Appendix F Comparable Convention City Hotel Tax Rate Data

Chargers Stadium and Convention Center Study Chapter 1 - Page 2

DEMAND & IMPACT PROJECTIONS This chapter shows the expected level of demand and impact generated from the proposed Project. The projections in this analysis include the net new events, attendance, daytrips, hotel room nights, hotel revenue (as well as other spending impacts) in the city resulting from the Project.

The projection assumes that the Project is operated and marketed in a manner consistent with or better than the existing San Diego Convention Center.

Convention Center

The first table shows the breakdown of available convention dates. Other than certain dates for NFL games, the facility will be open and available for group business. As mentioned previously, the NFL and Chargers have indicated they will work to allow multiple long-term bookings during the NFL seasons for all Mondays through Thursdays as well as one weekend per month during the critical mid-September to mid-November convention season. While some dates during the season will not be known to be available until the NFL schedule is released, those dates will be available for short-term bookings, also known as “backfill” dates.

Chargers Stadium and Convention Center Study Chapter 1 - Page 3

Table 1-1

Potential Convention Booking Days Analysis

NFL Season Days

Percent of Available

Convention Days Long-Term Booking Days 94 67%Short-Term Booking Days 29 21%Total Bookable Convention Days 123 87%

NFL Days 18 13%Total Convention Days 141 100%Available Convention Days 141Holiday Periods 12Total Days (Sept - Jan) 153

Non-NFL Season Days

Percent of Available

Convention Days

Long-Term Booking Days 203 100%Total Bookable Convention Days 203 100%Holiday Periods 9Total Days 212

Total Year Days

Percent of Available

Convention DaysTotal Long-Term Bookable Days 297 86%Total Short-Term Bookable Days 29 8%Total Bookable Days 326 95%NFL Days 18 5%Total Convention Days 344 100%Holiday Period Days 21Total Days 365

Source: HSP

As shown, of the total available convention days that could be booked in the year, the Project would be able to book 95 percent to those dates. Nearly all of those, 86 percent of total potential dates, would be able to be booked long-term in advance of the event, while only nine percent of dates would fall in the short-term booking category. The dates needed by the NFL (18) total only five percent of days in the year. The NFL actually takes up fewer dates than the 21 days that are not bookable for conventions due to major holiday weekends or periods. However, the benefit of this combined facility is that it would likely be booked for an NFL or other sporting event (such as a bowl game or other event) during the November and December holiday periods. In this regard, hotels that otherwise would be struggling for demand during these periods would be full due to sports events.

Chargers Stadium and Convention Center Study Chapter 1 - Page 4

The table below shows the events by type projected for the Project.

Table 1-2 Event Demand Projections

Event Type

Conventions, Conferences and Trade ShowsEntire FacilityAll but Multipurpose Exhibition SpacePartial Exhibit, Ballroom & Meeting Rooms

Total

Event Demand Projections

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

3 4 5 5 5 5 5 5 5 59 11 13 15 15 15 15 15 15 156 7 8 10 10 10 10 10 10 10

18 22 26 30 30 30 30 30 30 30

Consumer ShowsEntire FacilityAll but Multipurpose Exhibition SpacePartial Exhibit, Ballroom & Meeting Rooms

Total

2 3 3 3 3 3 3 3 3 32 3 3 3 3 3 3 3 3 30 0 0 0 0 0 0 0 0 0

4 5 6 6 6 6 6 6 6 6

Corporate EventsAll but Multipurpose Exhibition SpacePartial Exhibit, Ballroom & Meeting Rooms

Total

2 3 3 4 4 4 4 4 4 412 15 19 22 24 24 24 24 24 24

14 18 22 26 28 28 28 28 28 28

Sports & Entertainment Events (including NFL)Entire Facility

Football Field Only

Football Field and Partial Remainder of Building

Total

8 8 8 8 8 8 8 8 8 8

6 6 6 6 6 6 6 6 6 6

0 0 0 0 0 0 0 0 0 0

14 14 14 14 14 14 14 14 14 14

BanquetsFull ballroomTwo-thirds of ballroomOne-third of ballroom

Total

2 2 2 2 2 2 2 2 2 22 2 2 2 2 2 2 2 2 2

14 16 18 19 19 19 19 19 19 19

18 20 22 24 24 24 24 24 24 24

Meetings Room EventsAll meeting roomsTwo-thirds of meeting roomsOne-third of meeting rooms

Total

4 5 6 6 6 6 6 6 6 65 7 9 10 10 10 10 10 10 109 12 15 16 16 16 16 16 16 16

18 24 30 32 32 32 32 32 32 32

Total All Events 86 103 120 132 134 134 134 134 134 134

Source: HSP

The number of events projected will increase from 86 in Year 1 to 134 by stabilization. The number of events that will take up a majority of the building is 39, which includes eight assumed NFL game day events. When considering that there are 52 weeks in a year and a maximum-occupied facility can reasonable accommodate approximately 46 weeks/weekends per year (when subtracting major holiday periods), the projection is reasonable and perhaps conservative, given HSP’s analysis of the market’s desire to hold events in the City of San Diego. HSP assumed four total sports and entertainment events would be held, which could be concerts, other major spectator events or other sporting events, such as bowl games.

The next table shows the number of attendees projected in the first ten years.

Chargers Stadium and Convention Center Study Chapter 1 - Page 5

Table 1-3 Projected Attendance (Individuals, Not Attendee Days)

Event Type Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Conventions, Conferences and Trade Shows 31,800 39,500 47,200 53,000 53,000 53,000 53,000 53,000 53,000 53,000Consumer Shows 28,900 43,400 43,400 43,400 43,400 43,400 43,400 43,400 43,400 43,400Corporate Events 15,500 20,400 24,300 29,100 31,000 31,000 31,000 31,000 31,000 31,000Sports & Entertainment Events (including NFL) 686,000 686,000 686,000 686,000 686,000 686,000 686,000 686,000 686,000 686,000Banquets 39,500 42,600 45,800 47,400 47,400 47,400 47,400 47,400 47,400 47,400Meetings Room Events 27,700 36,300 45,000 47,300 47,300 47,300 47,300 47,300 47,300 47,300

Total All Events 829,400 868,200 891,700 906,200 908,100 908,100 908,100 908,100 908,100 908,100

Non-Sports/Entertainment Attendance 143,400 182,200 205,700 220,200 222,100 222,100 222,100 222,100 222,100 222,100

Source: HSP

A total of 143,400 non-sports/entertainment attendees are projected in the first year, ramping up to 222,100 by stabilization. When including sports and entertainment attendees, the total exceeds 900,000 by stabilization.

The next table shows the projected share of attendees coming to events that are likely to bring a spouse, partner or other family member. In a location that is not as attractive a destination, there would be very limited spousal attendance. However, in locations like San Diego, San Francisco, Hawaii and others, the allure of the destination brings added visitation by family members. An extended stay before or after the event is typical, although HSP’s analysis is conservative and did not count extended stays.

Table 1-4

Estimated Spouse Ratio

Conventions, Conferences and Trade Shows 35%Consumer Shows 35%Corporate Events 25%Sports & Entertainment Events (including NFL) 10%Banquets 33%Meetings Room Events 25%

Source: HSP

These spousal, partner or other family attendees are not counted as part of the ticketed or official event attendance.

The next table shows the total estimated attendee and spouse “days.” Attendee days are a product of the number of attendees multiplied by the number of days in their event, which was conservatively estimated to only match the number of nights they would stay. For example, if an event is three days and two nights, the model only counts the number of nights.

Chargers Stadium and Convention Center Study Chapter 1 - Page 6

Table 1-5 Total Attendee & Spouse Days

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Conventions, Conferences and Trade ShowsEntire Facility 31,590 42,120 52,650 52,650 68,250 68,250 68,250 68,250 68,250 68,250 All but Multipurpose Exhibition Space 58,793 71,858 84,923 97,988 97,988 97,988 97,988 97,988 97,988 97,988 Partial Exhibit, Ballroom & Meeting Rooms 15,444 18,018 20,592 25,740 25,740 25,740 25,740 25,740 25,740 25,740

Total 105,827 131,996 158,165 176,378 191,978 191,978 191,978 191,978 191,978 191,978

Consumer ShowsEntire Facility 42,120 63,180 63,180 63,180 63,180 63,180 63,180 63,180 63,180 63,180 All but Multipurpose Exhibition Space 28,220 42,331 42,331 42,331 42,331 42,331 42,331 42,331 42,331 42,331 Partial Exhibit, Ballroom & Meeting Rooms - - - - - - - - - -

Total 70,340 105,511 105,511 105,511 105,511 105,511 105,511 105,511 105,511 105,511

Corporate EventsAll but Multipurpose Exhibition Space 7,275 10,913 10,913 14,550 14,550 14,550 14,550 14,550 14,550 14,550 Partial Exhibit, Ballroom & Meeting Rooms 18,188 22,734 28,797 33,344 36,375 36,375 36,375 36,375 36,375 36,375

Total 25,463 33,647 39,709 47,894 50,925 50,925 50,925 50,925 50,925 50,925

Sports & Entertainment Events (including NFL)Entire Facility 589,600 589,600 589,600 589,600 589,600 589,600 589,600 589,600 589,600 589,600 Football Field Only 165,000 165,000 165,000 165,000 165,000 165,000 165,000 165,000 165,000 165,000 Football Field and Partial Remainder of Building - - - - - - - - - -

Total 754,600 754,600 754,600 754,600 754,600 754,600 754,600 754,600 754,600 754,600

BanquetsFull ballroom 14,000 14,000 14,000 14,000 14,000 14,000 14,000 14,000 14,000 14,000 Two-thirds of ballroom 9,100 9,100 9,100 9,100 9,100 9,100 9,100 9,100 9,100 9,100 One-third of ballroom 29,400 33,600 37,800 39,900 39,900 39,900 39,900 39,900 39,900 39,900

Total 52,500 56,700 60,900 63,000 63,000 63,000 63,000 63,000 63,000 63,000

Meetings Room EventsAll meeting rooms 30,000 37,500 45,000 45,000 45,000 45,000 45,000 45,000 45,000 45,000 Two-thirds of meeting rooms 15,625 21,875 28,125 31,250 31,250 31,250 31,250 31,250 31,250 31,250 One-third of meeting rooms 9,750 13,000 16,250 17,333 17,333 17,333 17,333 17,333 17,333 17,333

Total 55,375 72,375 89,375 93,583 93,583 93,583 93,583 93,583 93,583 93,583

Total All Events 1,064,104 1,154,828 1,208,259 1,240,965 1,259,596 1,259,596 1,259,596 1,259,596 1,259,596 1,259,596

Source: HSP

As shown, the number of visitor days is projected at just over one million in the first year, then increase to more than 1.2 million by stabilization.

The next table shows the projected share of attendees by event type that are spending the night and requiring lodging. The balance includes those who are either daytrippers or are spending the night with friends or family.

Table 1-6

Percent of Attendees Requiring Hotel Lodging

Conventions, Conferences and Trade Shows 90%Consumer Shows 6%Corporate Events 40%Sports & Entertainment Events (including NFL) 15%Banquets 10%Meetings Room Events 33%

Source: HSP

Chargers Stadium and Convention Center Study Chapter 1 - Page 7

Certain event types generate a high rate of hotel room nights, while other more local events, such as consumer shows, do not. High rate of hotel room nights occur with conventions and tradeshows, where most attendees are coming for several days and spending the night in hotels. For example, an estimated 20 percent of fans attending Chargers games are from outside the market, but HSP lowered the estimate of lodgers to 15 percent for all sports/entertainment events to be conservative. The ratio of visiting attendees is due to the attractiveness of San Diego combined with the desire of many opposing team fans to see their team play in an attractive environment.

The next table shows the total estimated daytrips. Daytrips result from the percentage of attendees who come just for the day, by event type. Nearly all, except NFL attendees and consumer show attendees, will be from outside the immediate area.

Table 1-7 Total Daytripper Days

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Conventions, Conferences and Trade ShowsEntire Facility 3,159 4,212 5,265 5,265 6,825 6,825 6,825 6,825 6,825 6,825 All but Multipurpose Exhibition Space 5,879 7,186 8,492 9,799 9,799 9,799 9,799 9,799 9,799 9,799 Partial Exhibit, Ballroom & Meeting Rooms 1,544 1,802 2,059 2,574 2,574 2,574 2,574 2,574 2,574 2,574

Total 10,583 13,200 15,816 17,638 19,198 19,198 19,198 19,198 19,198 19,198

Consumer ShowsEntire Facility 39,593 59,389 59,389 59,389 59,389 59,389 59,389 59,389 59,389 59,389 All but Multipurpose Exhibition Space 26,527 39,791 39,791 39,791 39,791 39,791 39,791 39,791 39,791 39,791 Partial Exhibit, Ballroom & Meeting Rooms - - - - - - - - - -

Total 66,120 99,180 99,180 99,180 99,180 99,180 99,180 99,180 99,180 99,180

Corporate EventsAll but Multipurpose Exhibition Space 4,365 6,548 6,548 8,730 8,730 8,730 8,730 8,730 8,730 8,730 Partial Exhibit, Ballroom & Meeting Rooms 10,913 13,641 17,278 20,006 21,825 21,825 21,825 21,825 21,825 21,825

Total 15,278 20,188 23,826 28,736 30,555 30,555 30,555 30,555 30,555 30,555

Sports & Entertainment Events (including NFL)Entire Facility 501,160 501,160 501,160 501,160 501,160 501,160 501,160 501,160 501,160 501,160 Football Field Only 140,250 140,250 140,250 140,250 140,250 140,250 140,250 140,250 140,250 140,250 Football Field and Partial Remainder of Building - - - - - - - - - -

Total 641,410 641,410 641,410 641,410 641,410 641,410 641,410 641,410 641,410 641,410

BanquetsFull ballroom 12,600 12,600 12,600 12,600 12,600 12,600 12,600 12,600 12,600 12,600 Two-thirds of ballroom 8,190 8,190 8,190 8,190 8,190 8,190 8,190 8,190 8,190 8,190 One-third of ballroom 26,460 30,240 34,020 35,910 35,910 35,910 35,910 35,910 35,910 35,910

Total 47,250 51,030 54,810 56,700 56,700 56,700 56,700 56,700 56,700 56,700

Meetings Room EventsAll meeting rooms 20,100 25,125 30,150 30,150 30,150 30,150 30,150 30,150 30,150 30,150 Two-thirds of meeting rooms 10,469 14,656 18,844 20,938 20,938 20,938 20,938 20,938 20,938 20,938 One-third of meeting rooms 6,533 8,710 10,888 11,613 11,613 11,613 11,613 11,613 11,613 11,613

Total 37,101 48,491 59,881 62,701 62,701 62,701 62,701 62,701 62,701 62,701

Total All Events 817,741 873,499 894,923 906,365 909,744 909,744 909,744 909,744 909,744 909,744

Percent of Total Visitor Days 76.8% 75.6% 74.1% 73.0% 72.2% 72.2% 72.2% 72.2% 72.2% 72.2%

Source: HSP

The number of daytrips is expected to increase from more than 817,000 in Year 1 to nearly 910,000 by stabilization. The percentage of total visitor days represented by daytrips is 72.2 percent by stabilization.

The next table shows the total estimated overnights. This is a result of the percentage of attendees who come and stay overnight, by event type.

Chargers Stadium and Convention Center Study Chapter 1 - Page 8

Table 1-8 Total Overnighter Days

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Conventions, Conferences and Trade ShowsEntire Facility 28,431 37,908 47,385 47,385 61,425 61,425 61,425 61,425 61,425 61,425 All but Multipurpose Exhibition Space 52,913 64,672 76,430 88,189 88,189 88,189 88,189 88,189 88,189 88,189 Partial Exhibit, Ballroom & Meeting Rooms 13,900 16,216 18,533 23,166 23,166 23,166 23,166 23,166 23,166 23,166

Total 95,244 118,796 142,348 158,740 172,780 172,780 172,780 172,780 172,780 172,780

Consumer ShowsEntire Facility 2,527 3,791 3,791 3,791 3,791 3,791 3,791 3,791 3,791 3,791 All but Multipurpose Exhibition Space 1,693 2,540 2,540 2,540 2,540 2,540 2,540 2,540 2,540 2,540 Partial Exhibit, Ballroom & Meeting Rooms - - - - - - - - - -

Total 4,220 6,331 6,331 6,331 6,331 6,331 6,331 6,331 6,331 6,331

Corporate EventsAll but Multipurpose Exhibition Space 2,910 4,365 4,365 5,820 5,820 5,820 5,820 5,820 5,820 5,820 Partial Exhibit, Ballroom & Meeting Rooms 7,275 9,094 11,519 13,338 14,550 14,550 14,550 14,550 14,550 14,550

Total 10,185 13,459 15,884 19,158 20,370 20,370 20,370 20,370 20,370 20,370

Sports & Entertainment Events (including NFL)Entire Facility 88,440 88,440 88,440 88,440 88,440 88,440 88,440 88,440 88,440 88,440 Football Field Only 24,750 24,750 24,750 24,750 24,750 24,750 24,750 24,750 24,750 24,750 Football Field and Partial Remainder of Building - - - - - - - - - -

Total 113,190 113,190 113,190 113,190 113,190 113,190 113,190 113,190 113,190 113,190

BanquetsFull ballroom 1,400 1,400 1,400 1,400 1,400 1,400 1,400 1,400 1,400 1,400 Two-thirds of ballroom 910 910 910 910 910 910 910 910 910 910 One-third of ballroom 2,940 3,360 3,780 3,990 3,990 3,990 3,990 3,990 3,990 3,990

Total 5,250 5,670 6,090 6,300 6,300 6,300 6,300 6,300 6,300 6,300

Meetings Room EventsAll meeting rooms 9,900 12,375 14,850 14,850 14,850 14,850 14,850 14,850 14,850 14,850 Two-thirds of meeting rooms 5,156 7,219 9,281 10,313 10,313 10,313 10,313 10,313 10,313 10,313 One-third of meeting rooms 3,218 4,290 5,363 5,720 5,720 5,720 5,720 5,720 5,720 5,720

Total 18,274 23,884 29,494 30,883 30,883 30,883 30,883 30,883 30,883 30,883

Total All Events 246,363 281,329 313,336 334,600 349,853 349,853 349,853 349,853 349,853 349,853

Percent of Total Visitor Days 23.2% 24.4% 25.9% 27.0% 27.8% 27.8% 27.8% 27.8% 27.8% 27.8%

Source: HSP

The number of overnights is expected to increase from approximately 246,000 in Year 1 to more than 349,000 by stabilization. The percentage of total visitor days represented by overnighters is 27.6 percent by stabilization.

The next table shows the total estimated room nights, after making assumptions for the number of guests per room night. While many corporate visitors travel and stay in a hotel alone, many group and leisure visitors do not.

Chargers Stadium and Convention Center Study Chapter 1 - Page 9

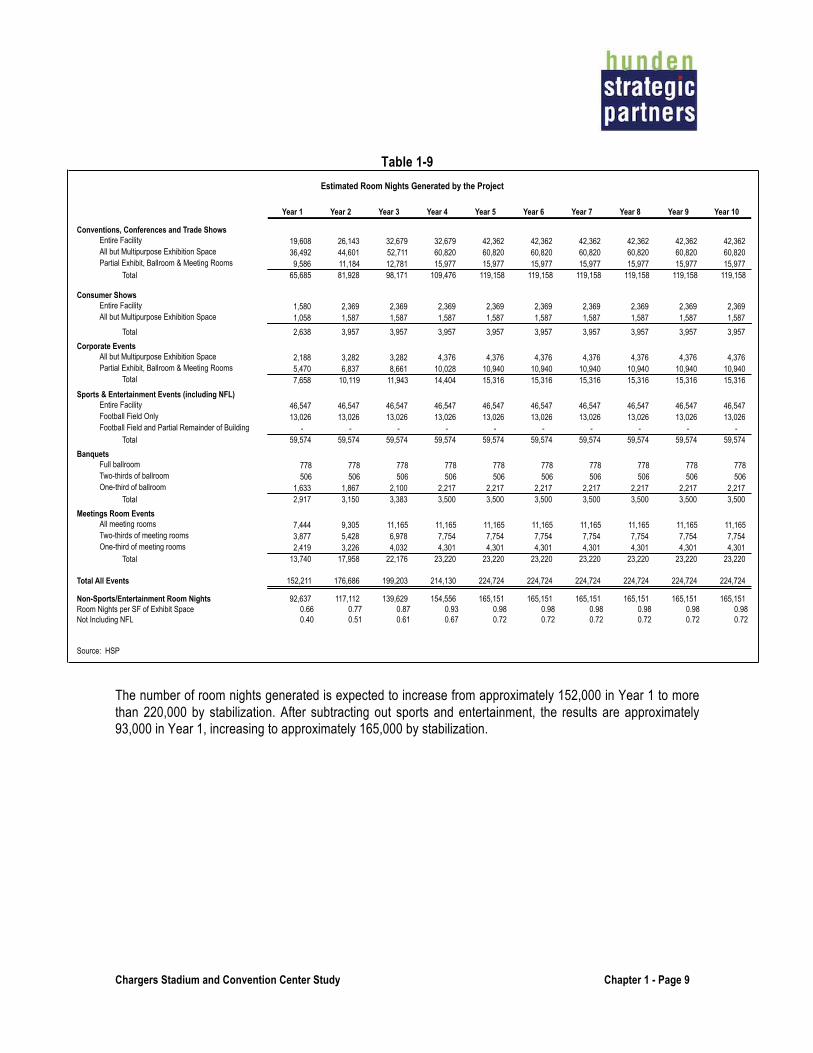

Table 1-9 Estimated Room Nights Generated by the Project

Conventions, Conferences and Trade ShowsEntire FacilityAll but Multipurpose Exhibition SpacePartial Exhibit, Ballroom & Meeting Rooms

Total

Consumer ShowsEntire FacilityAll but Multipurpose Exhibition Space

Estimated Room Nights Generated by the Project

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

19,608 26,143 32,679 32,679 42,362 42,362 42,362 42,362 42,362 42,362 36,492 44,601 52,711 60,820 60,820 60,820 60,820 60,820 60,820 60,820 9,586 11,184 12,781 15,977 15,977 15,977 15,977 15,977 15,977 15,977

65,685 81,928 98,171 109,476 119,158 119,158 119,158 119,158 119,158 119,158

1,580 2,369 2,369 2,369 2,369 2,369 2,369 2,369 2,369 2,369 1,058 1,587 1,587 1,587 1,587 1,587 1,587 1,587 1,587 1,587

Total

Corporate EventsAll but Multipurpose Exhibition SpacePartial Exhibit, Ballroom & Meeting Rooms

Total

Sports & Entertainment Events (including NFL)Entire FacilityFootball Field OnlyFootball Field and Partial Remainder of Building

Total

BanquetsFull ballroomTwo-thirds of ballroomOne-third of ballroom

Total

Meetings Room EventsAll meeting roomsTwo-thirds of meeting roomsOne-third of meeting rooms

Total

2,638 3,957 3,957 3,957 3,957 3,957 3,957 3,957 3,957 3,957

2,188 3,282 3,282 4,376 4,376 4,376 4,376 4,376 4,376 4,376 5,470 6,837 8,661 10,028 10,940 10,940 10,940 10,940 10,940 10,940 7,658 10,119 11,943 14,404 15,316 15,316 15,316 15,316 15,316 15,316

46,547 46,547 46,547 46,547 46,547 46,547 46,547 46,547 46,547 46,547 13,026 13,026 13,026 13,026 13,026 13,026 13,026 13,026 13,026 13,026

- - - - - - - - - - 59,574 59,574 59,574 59,574 59,574 59,574 59,574 59,574 59,574 59,574

778 778 778 778 778 778 778 778 778 778 506 506 506 506 506 506 506 506 506 506

1,633 1,867 2,100 2,217 2,217 2,217 2,217 2,217 2,217 2,217 2,917 3,150 3,383 3,500 3,500 3,500 3,500 3,500 3,500 3,500

7,444 9,305 11,165 11,165 11,165 11,165 11,165 11,165 11,165 11,165 3,877 5,428 6,978 7,754 7,754 7,754 7,754 7,754 7,754 7,754 2,419 3,226 4,032 4,301 4,301 4,301 4,301 4,301 4,301 4,301

13,740 17,958 22,176 23,220 23,220 23,220 23,220 23,220 23,220 23,220

Total All Events

Non-Sports/Entertainment Room NightsRoom Nights per SF of Exhibit SpaceNot Including NFL

Source: HSP

152,211 176,686 199,203 214,130 224,724 224,724 224,724 224,724 224,724 224,724

92,637 117,112 139,629 154,556 165,151 165,151 165,151 165,151 165,151 165,151 0.66 0.77 0.87 0.93 0.98 0.98 0.98 0.98 0.98 0.980.40 0.51 0.61 0.67 0.72 0.72 0.72 0.72 0.72 0.72

The number of room nights generated is expected to increase from approximately 152,000 in Year 1 to more than 220,000 by stabilization. After subtracting out sports and entertainment, the results are approximately 93,000 in Year 1, increasing to approximately 165,000 by stabilization.

Chargers Stadium and Convention Center Study Chapter 1 - Page 10

IMPACT ANALYSIS The incremental impact of the Project will increase economic activity and result in additional room nights, restaurant spending, retail spending, increased fiscal impact, income, earnings and employment for the City of City of San Diego economy.

The net new and recaptured direct spending discussed earlier is considered to be the Direct Impact, which is is in addition to any natural growth.

From the direct spending figures, further impact analyses will be completed.

! Indirect Impacts are the supply of goods and services resulting from the initial direct spending. For example, a convention attendee’s direct expenditure on a hotel room causes the hotel to purchase linens and other items from suppliers. The portion of these hotel purchases that are within the local economy is considered an indirect economic impact.

! Induced Impacts embody the change in local spending due to the personal expenditures by employees whose incomes are affected by direct and indirect spending. For example, a waitress at a restaurant may have more personal income as a result of the convention attendee’s visit. The amount of the increased income that the employee spends in the area is considered an induced impact.

! Fiscal Impacts represent the incremental tax revenue collected by the community due to the net new economic activity. Fiscal impacts provide an offset to the potential public expenditures required to support the development.

! Earnings and Employment Impacts include the incremental employment provided not only onsite, but due to the spending associated with it. For example, the direct, indirect and induced impacts generate spending, support new and ongoing businesses and ultimately result in ongoing employment for citizens.

There are a variety of impacts to the city’s hotels from the Project, including increases in existing visitor spending due to better facilities, new group attendee spending, new exhibitor spending, new corporate transient spending and new leisure spending.

The following table summarizes the daytrip and overnight visitor activity expected over ten years.

Table 1-10 Net New Visitors and Room Nights

Year 1 Year 2 Year 3 Year 4 Year 5

New Daytrip Visitor Days 677,491 733,249 754,673 766,115 769,494

New Overnighter Days 246,363 281,329 313,336 334,600 349,853

New Room Nights 152,211 176,686 199,203 214,130 224,724

Source: Hunden Strategic Partners

Net New Visitors and Room Nights

Year 10 Total

769,494 7,548,490

349,853 3,274,746

224,724 2,090,577

Chargers Stadium and Convention Center Study Chapter 1 - Page 11

As shown, over ten years, more than 7.5 million daytrip visitor days and nearly 3.2 million overnights are expected to be new to the City of San Diego. New room nights from the overnights are projected to total nearly 2.1 million over the ten-year period.

Impact Projections

While the basis for the impact projections is the number of room nights to the City of San Diego, additional impact occurs as well, from the compression of these room nights on an already highly occupied hotel set. This will cause increased room rates during events, especially NFL games and large conventions. Both the new room nights and increased rates generate increased revenue for City of San Diego hotels. In addition, hundreds of thousands of daytrips will result in money being spent in the City of San Diego hotels before and after events at the Project, whether on game days, during consumer shows or before/after other events like banquets, meetings and conferences.

Increased Hotel Rate Analysis

The next table shows the increase in hotel revenue due to ADR (average daily rate), also known in the industry as compression, from major events. HSP selected only those events that would either take up most or all of the building and generate significant room nights, as well as NFL games. Smaller conventions, conferences, trade shows, consumer shows, banquets and meetings were not included.

HSP identified other cities with downtown NFL stadiums to better understand the impact of home games on room rates. The following table summarizes hotel compression rates due to NFL home and away games for comparable NFL markets with downtown stadiums for selected dates, where comparisons were available for the upcoming season. While the increased rates occur most strongly in the downtown area surrounding the stadiums, the ripple effects of the rate increases push out to all city hotels during “city-wide” events.

Chargers Stadium and Convention Center Study Chapter 1 - Page 12

Table 1-11 Hotel Compression Due to NFL Home/Away Games*

Comparable Market Hotel Type Hotel Property # of Rooms Home Rate Home Date Away Rate Away Date Increase/DecreaseFull Service/Luxury Four Seasons Baltimore 257 559.00$ 10/9/16 489.00$ 10/23/16 13%

Stadium Hotel Holiday Inn Express Baltimore at the Stadiums 123 279.00$ 10/9/16 205.00$ 10/23/16 27%

Convention Center Hotel Hilton Baltimore 757 159.00$ 10/9/16 165.00$ 10/23/16 -4%

Select Service Residence Inn 188 189.00$ 10/9/16 239.00$ 10/23/16 -26%

Boutique Kimpton Hotel Monaco 202 249.00$ 10/9/16 249.00$ 10/23/16 0%

Average 305 287.00$ 269.40$ 6%

Full Service/Luxury The Westin Convention Center 616 289.00$ 12/4/16 349.00$ 10/16/16 -21%

Convention Center Hotel Wyndham Grand Pittsburgh 712 304.00$ 12/4/16 304.00$ 10/16/16 0%

Select Service Holiday Inn Express and Suites 135 282.00$ 12/4/16 209.00$ 10/16/16 26%

Boutique Kimpton Hotel Monaco 248 305.00$ 12/4/16 279.00$ 10/16/16 9%

Average 428 295.00$ 285.25$ 3%

Full Service/Luxury The Westin 575 174.00$ 9/11/16 161.00$ 9/18/16 7%

Convention Center Hotel JW Marriott 1005 389.00$ 9/11/16 229.00$ 9/18/16 41%

Select Service Holiday Inn Express Indianapolis Downtown 108 192.00$ 9/11/16 160.00$ 9/18/16 17%

Boutique The Alexander 209 207.00$ 9/11/16 170.00$ 9/18/16 18%

Average 240.50$ 180.00$ 25%

Full Service/Luxury Fairmont Olympic Hotel 450 349.00$ 10/16/16 319.00$ 10/23/16 9%

Stadium Hotel Silver Cloud Hotel - Seattle Stadium 211 499.00$ 10/16/16 289.00$ 10/23/16 42%

Convention Center Hotel Westin Seattle 891 249.00$ 10/16/16 249.00$ 10/23/16 0%

Select Service Hilton Garden Inn Seattle Downtown 222 229.00$ 10/16/16 229.00$ 10/23/16 0%

Boutique The Maxwell Hotel 139 219.00$ 10/16/16 169.00$ 10/23/16 23%

Average 383 309.00$ 251.00$ 19%

Full Service/Luxury Hilton Nashville Downtown 330 479.00$ 10/23/16 379.00$ 11/20/16 21%

Convention Center Hotel Omni Nashville 800 499.00$ 10/23/16 399.00$ 11/20/16 20%

Select Service Holiday Inn Express 287 419.00$ 10/23/16 299.00$ 11/20/16 29%

Boutique Union Station Hotel 125 529.00$ 10/23/16 409.00$ 11/20/16 23%

Average 386 481.50$ 371.50$ 23%

Comparable Market Average 320.36$ 270.41$ 12.3%Rate Differential 49.95$

* For home game dates when hotels are not sold out as of 7/15/16

Source: Expedia.com Advertised Rate, Smith Travel Research

Baltimore

Pittsburgh

Seattle

Nashville

Indianapolis

As the table shows, using a simple average, rates increased by $49.95, or 12.3 percent, during home game football weekends. While rates in the City of San Diego may increase by more or less, this sampling provides a solid indication that home games in downtown facilities provide room night compression.

HSP notes that NFL games are also more likely to generate in-bound tourism when the city is a compelling destination. San Diego has both an ideal climate when many other cities are cold during the NFL season and is a popular destination generally. Internal data from the Chargers suggest that home game attendance is made up of a significant portion of visiting fans. These visiting fans’ spending provides significant impact to the City of San Diego. With the new stadium located downtown in a walkable environment, HSP expects even more inbound fans to games. HSP expects that existing out-of-town fans will continue to come, but will spend more on downtown hotel rooms, and additional fans will come that are not coming today, due to the improved location.

The following table shows the projection of room revenue from incremental spending on existing room nights.

Chargers Stadium and Convention Center Study Chapter 1 - Page 13

Table 1-12 Projection of Room Revenue from Incremental Spending on Existing Room Nights Projection of Room Revenue from Incremental Spending on Existing Room Nights

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10Number of Impacted Hotel Rooms (all SD Hotels) 44,326 44,326 44,326 44,326 44,326 44,326 44,326 44,326 44,326 44,326 Estimated Annual Occupancy (all SD Hotels 72.0% 72.0% 72.0% 72.0% 72.0% 72.0% 72.0% 72.0% 72.0% 72.0%Estimated Annual Rate (all SD Hotels) 160.68$ 164.70$ 168.81$ 173.03$ 177.36$ 181.79$ 186.34$ 191.00$ 195.77$ 200.67$ Annual Room Nights in Impacted Group Hotels (000s) 11,649 11,649 11,649 11,649 11,649 11,649 11,649 11,649 11,649 11,649 Annual Room Revenue in Impacted Group Hotels (000s) 1,871,730$ 1,871,730 1,871,730 1,871,730 1,871,730 1,871,730 1,871,730 1,871,730 1,871,730 1,871,730 Estimated Nights per Year of Intense Compression 25 30 35 38 41 41 41 41 41 41 Average Estimated ADR Increase due to Compression 14.67$ 15.03$ 15.41$ 15.79$ 16.19$ 16.59$ 17.01$ 17.43$ 17.87$ 18.32$ Increase in Room Revenue from Compression (000s) 11,478$ 14,240$ 17,133$ 19,250$ 21,116$ 21,644$ 22,185$ 22,739$ 23,308$ 23,891$

Source: HSP

HSP assumed that during major events, considered “city-wide” events, that rooms would become more scarce, allowing hotel yield managers to increase rates, as is the standard practice in the industry. The rate during these compression periods was assumed to increase an average of nearly $15 per occupied room in the first year. The increase on the one-third of rooms (approximately 15,000) located downtown is expected to be more than $25. Based on the number of existing occupied room nights during these intense compression nights, HSP estimated an increase in hotel revenue for existing hotels’ occupied rooms beginning at $11.5 million and increasing to nearly $24 million by Year 10.

The daily spending by visitors and the overnight spending by overnight visitors all contribute to the economic impact of the Project. Spending by category, conservatively estimated based on a number of inputs, was populated in the model. Other spending includes entertainment, such as concerts and tours, as well as other non-specified spending. These are shown in the next table.

Table 1-13 Estimated Spending Per Visitor per Day

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10Spending per New Visitor - OvernightOnsite Food & Beverage $18.49 $18.95 $19.43 $19.91 $20.41 $20.92 $21.44 $21.98 $22.53 $23.09Offsite Food & Beverage $43.13 $44.21 $45.31 $46.44 $47.60 $48.79 $50.01 $51.26 $52.55 $53.86Total Food & Beverage $61.62 $63.16 $64.74 $66.36 $68.01 $69.71 $71.46 $73.24 $75.07 $76.95

Lodging Spending $149.52 $155.79 $161.65 $166.78 $171.59 $175.88 $180.28 $184.78 $189.40 $194.14Retail Spending $21.51 $22.04 $22.59 $23.16 $23.74 $24.33 $24.94 $25.56 $26.20 $26.86Transportation Spending $11.81 $12.11 $12.41 $12.72 $13.04 $13.37 $13.70 $14.04 $14.40 $14.76Other Spending $6.14 $6.30 $6.45 $6.62 $6.78 $6.95 $7.12 $7.30 $7.49 $7.67Total Direct Spending $250.60 $259.40 $267.84 $275.64 $283.16 $290.24 $297.50 $304.94 $312.56 $320.37

Spending per Visitor - Day TripOnsite Food & Beverage $12.94 $13.27 $13.60 $13.94 $14.29 $14.64 $15.01 $15.39 $15.77 $16.16Offsite Food & Beverage $23.72 $24.31 $24.92 $25.54 $26.18 $26.84 $27.51 $28.20 $28.90 $29.62Total Food & Beverage $36.66 $37.58 $38.52 $39.48 $40.47 $41.48 $42.52 $43.58 $44.67 $45.79

Retail Spending $14.41 $14.77 $15.14 $15.52 $15.90 $16.30 $16.71 $17.13 $17.56 $17.99Transportation Spending $9.45 $9.69 $9.93 $10.18 $10.43 $10.69 $10.96 $11.24 $11.52 $11.80Other Spending $5.53 $5.67 $5.81 $5.95 $6.10 $6.26 $6.41 $6.57 $6.74 $6.91Total Direct Spending $66.05 $67.70 $69.40 $71.13 $72.91 $74.73 $76.60 $78.52 $80.48 $82.49

Source: HSP

The per-person per-day spending for overnight guests totals more than $250 in Year 1 and increases with inflation, assumed at 2.5 percent. The daily spending per person for day trips is expected to be approximately $66 in the first year.

The table below shows the direct net new spending, based on the analysis.

Chargers Stadium and Convention Center Study Chapter 1 - Page 14

Table 1-14 Direct Net New Spending to San Diego (000s)

Year 1 Year 2 Year 3 Year 4 Year 5

Food & Beverage $40,019 $45,323 $49,354 $52,450 $54,936Lodging $48,314 $58,068 $67,782 $75,056 $81,147Retail $15,060 $17,031 $18,504 $19,636 $20,543Transportation $9,314 $10,511 $11,384 $12,055 $12,591Other $5,260 $5,927 $6,407 $6,776 $7,069Total $117,967 $136,861 $153,430 $165,974 $176,286

Source: Hunden Strategic Partners

Direct Net New Spending to San Diego (000s)

Year 10 Total

$62,155 $538,061$91,810 $767,567$23,243 $201,455$14,245 $123,692$7,998 $69,525

$199,451 $1,700,300

Spending on lodging and food/beverage are the largest components of direct net new spending to the City of San Diego; however, the impact on hotels is the focus. Between the new room nights generated and the increased ADR from compression, more than $91 million in annual new hotel revenue is expected by Year 10, totaling more than $767 million over the first ten years.

The following table shows the new earnings associated with the new economic activity.

Table 1-15 Net New Earnings from Direct New Spending (000s)

Year 1 Year 2 Year 3 Year 4 Year 5

Net New Earnings from Direct New Spending (000s)

Year 10 TotalNet New EarningsFrom Direct $38,391 $44,434 $49,671 $53,639 $56,896From Indirect $12,786 $14,844 $16,654 $18,023 $19,150From Induced $14,033 $16,275 $18,239 $19,726 $20,948Total $65,211 $75,553 $84,563 $91,388 $96,994

Source: Hunden Strategic Partners

$64,373 $549,574$21,666 $184,631$23,700 $202,082

$109,740 $936,287

Over ten years, the new earnings generated by the new spending is expected to total more than $936 million.

The following table shows the new full-time equivalent employment (FTE) associated with the new economic activity.

Table 1-16 Net New Full-Time Equivalent Jobs from New Earnings

Year 1 Year 2 Year 3 Year 4 Year 5

Net New Full-Time Equivalent Jobs from New Earnings

Year 10

Net New FTE JobsFrom Direct 2,105 2,366 2,568 2,697 2,784 From Indirect 714 802 869 913 942 From Induced 838 942 1,021 1,072 1,106 Total 3,657 4,110 4,458 4,681 4,831

Source: Hunden Strategic Partners

2,784 942

1,106 4,831

Chargers Stadium and Convention Center Study Chapter 1 - Page 15

The number of full-time equivalent supported jobs by the Project is expected to be more than 4,800 by stabilization.

Fiscal Impact

The fiscal impact of the Project is the benefit to the community via taxes generated. HSP has estimated the net new hotel taxes generated by City of San Diego hotels due to the Project.

The following table shows the projections of new hotel room taxes from City of San Diego hotels generated over the first ten years of operation.

Table 1-17 Fiscal Impact - Net New Hotel Tax from New Lodging Spending at San Diego Hotels due to Project (000s)

Year 1 Year 2 Year 3 Year 4 Year 5

Fiscal Impact - Net New Hotel Tax from New Lodging Spending at San Diego Hotels due to Project (000s)

Year 10 Total Existing Hotel Occupancy Tax (10.5%) $5,073 $6,097 $7,117 $7,881 $8,520Deposit to SD Tourism and Marketing Fund (2.0%) $966 $1,161 $1,356 $1,501 $1,623Proposed Hotel Occupancy Tax (4.0%) $1,933 $2,323 $2,711 $3,002 $3,246Total $7,972 $9,581 $11,184 $12,384 $13,389

$9,640 $80,595$1,836 $15,351$3,672 $30,703$15,149 $126,649

Source: Hunden Strategic Partners

In total, taxes generated from the City of San Diego hotel room revenues are expected to increase by more than $126 million during the first ten-year period.

The following table shows the summary of estimated ten-year impacts for the Project.

Chargers Stadium and Convention Center Study Chapter 1 - Page 16

Table 1-18

Summary of 10-Year Estimated Impacts

Net New Spending (millions)Direct $1,700Indirect $571Induced $672Total $2,943

Net New Earnings (millions)From Direct $550From Indirect $185From Induced $202Total $936

New Hotel Tax from New Downtown Hotel Revenue (millions)Existing Hotel Occupancy Tax (10.5%) $80.6Deposit to SD Tourism and Marketing Fund (2.0%) $15.4Proposed Hotel Occupancy Tax (4.0%) $30.7Total $126.6

Source: Hunden Strategic Partners

The net new spending for the Project totals $2.9 billion over the first ten-year period, including more than $930 million in new earnings, and more than $126 million in new hotel taxes generated at City of San Diego hotels.

TABLE OF CONTENTS ----------- Executive Summary

Chapter 1 Demand and Impact

Appendix A Convention Industry Overview and Trends

Appendix B Convention Market Competitive and Comparable Analysis

Appendix C Influence of Comparable Downtown Stadiums

Appendix D Meeting Planner Interviews

Appendix E Hotel Market Analysis

Appendix F Comparable Convention City Hotel Tax Rate Data

Chargers Stadium and Convention Center Study Appendix A - Page 2

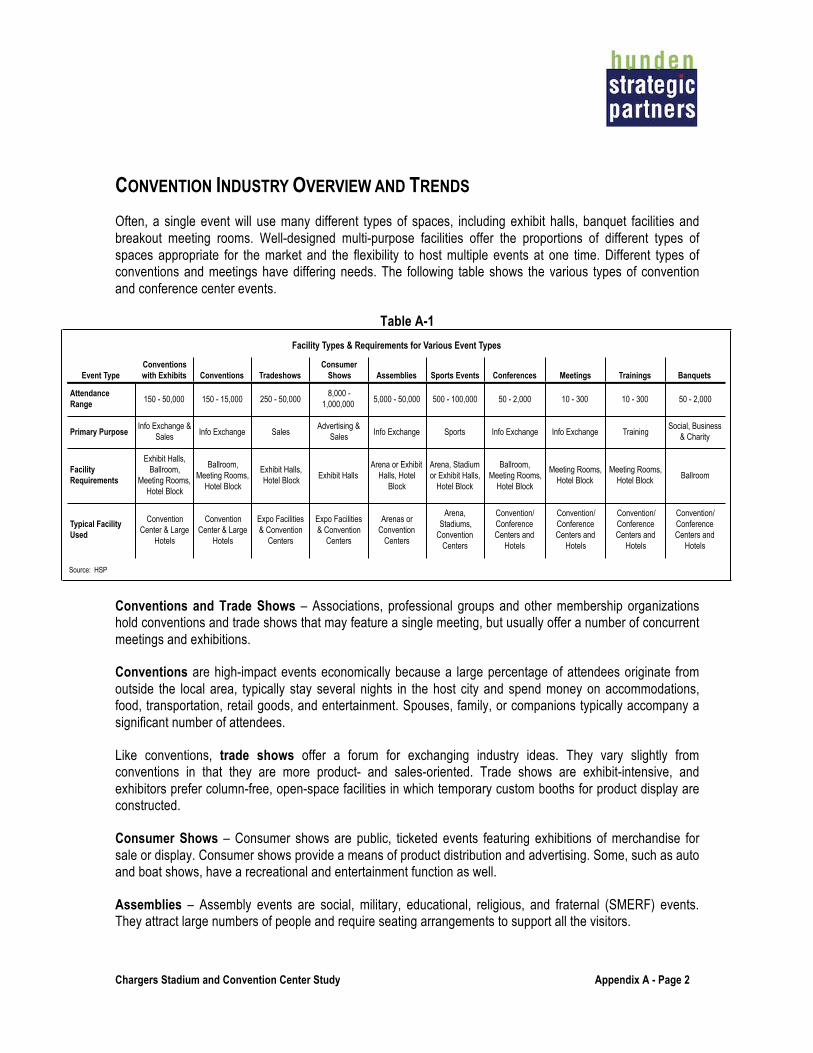

CONVENTION INDUSTRY OVERVIEW AND TRENDS Often, a single event will use many different types of spaces, including exhibit halls, banquet facilities and breakout meeting rooms. Well-designed multi-purpose facilities offer the proportions of different types of spaces appropriate for the market and the flexibility to host multiple events at one time. Different types of conventions and meetings have differing needs. The following table shows the various types of convention and conference center events.

Table A-1 Facility Types & Requirements for Various Event Types

Event TypeConventions with Exhibits Conventions Tradeshows

Consumer Shows Assemblies Sports Events Conferences Meetings Trainings Banquets

Attendance Range 150 - 50,000 150 - 15,000 250 - 50,000

8,000 - 1,000,000 5,000 - 50,000 500 - 100,000 50 - 2,000 10 - 300 10 - 300 50 - 2,000

Primary PurposeInfo Exchange &

Sales Info Exchange SalesAdvertising &

Sales Info Exchange Sports Info Exchange Info Exchange TrainingSocial, Business

& Charity

Facility Requirements

Exhibit Halls, Ballroom,

Meeting Rooms, Hotel Block

Ballroom, Meeting Rooms,

Hotel Block

Exhibit Halls, Hotel Block Exhibit Halls

Arena or Exhibit Halls, Hotel

Block

Arena, Stadium or Exhibit Halls,

Hotel Block

Ballroom, Meeting Rooms,

Hotel Block

Meeting Rooms, Hotel Block

Meeting Rooms, Hotel Block Ballroom

Typical Facility Used

Convention Center & Large

Hotels

Convention Center & Large

Hotels

Expo Facilities & Convention

Centers

Expo Facilities & Convention

Centers

Arenas or Convention

Centers

Arena, Stadiums,

Convention Centers

Convention/ Conference Centers and

Hotels

Convention/ Conference Centers and

Hotels

Convention/ Conference Centers and

Hotels

Convention/ Conference Centers and

Hotels

Source: HSP

Conventions and Trade Shows – Associations, professional groups and other membership organizations hold conventions and trade shows that may feature a single meeting, but usually offer a number of concurrent meetings and exhibitions.

Conventions are high-impact events economically because a large percentage of attendees originate from outside the local area, typically stay several nights in the host city and spend money on accommodations, food, transportation, retail goods, and entertainment. Spouses, family, or companions typically accompany a significant number of attendees.

Like conventions, trade shows offer a forum for exchanging industry ideas. They vary slightly from conventions in that they are more product- and sales-oriented. Trade shows are exhibit-intensive, and exhibitors prefer column-free, open-space facilities in which temporary custom booths for product display are constructed.

Consumer Shows – Consumer shows are public, ticketed events featuring exhibitions of merchandise for sale or display. Consumer shows provide a means of product distribution and advertising. Some, such as auto and boat shows, have a recreational and entertainment function as well.

Assemblies – Assembly events are social, military, educational, religious, and fraternal (SMERF) events. They attract large numbers of people and require seating arrangements to support all the visitors.

Chargers Stadium and Convention Center Study Appendix A - Page 3

Sports and Entertainment – Includes a variety of sports at any level of competition that can be played indoors. Typically, such events are held in arenas or stadiums; however, many events, including boxing, wrestling, cheerleading, and basketball, can be held in exhibit facilities with temporary seating/stands.

Conferences – Conferences are meetings typically held by associations, professional groups, educational institutions, and other membership organizations. These events usually require space for general sessions, food service facilities and breakout rooms.

Corporate, Training and Other Meetings – Corporate meetings include training seminars, professional and technical conferences, business/job fairs, incentive trips and management meetings.

Banquets – Banquets are typically locally generated events, from social and wedding events to the annual Chamber of Commerce event, which can be the largest of its kind in a given city.

The following figure shows the comparison of supply and demand growth beginning in 1987.

Figure A-1

100

120

140

160

180

200

220

240

1987

19

88

1989

19

90

1991

19

92

1993

19

94

1995

19

96

1997

19

98

1999

20

00

2001

20

02

2003

20

04

2005

20

06

2007

20

08

2009

20

10

2011

20

12

2013

20

14

Inde

x

National Exhibit Space Supply & Demand

Exhibit Space Supply Growth Net Square Feet of Paid Exhibit Space Source: MEHD 2009, HSP

While demand is now increasing at a higher rate than supply, the gap in the supply/demand index still provides meeting and event planners an edge in negotiations. The increase in supply has led to increased competition amongst convention centers. Most existing facilities are in some form of expansion or renovation

Chargers Stadium and Convention Center Study Appendix A - Page 4

to update aging facilities, add new technology features and services and add space to attract larger events. The following table shows a comparison of past and current technology trends.

Table A-2 Convention Facilities Technology Status

Ten-Year ComparisonType Ten Years Ago Today

FacilityFacility Website 87% 100%Internet Access 77% 100%Wireless Internet 60% 94%Teleconferencing 58% 72%Video Conferencing 50% 66%Social Media Presence 0% 54%Security Access Cards 43% 44%

Online Event PlanningBooking Events 20% 19%Ordering Supplies for Events 18% 31%Booking Accommodations 16% 23%

Source: PricewaterhouseCoopers

Industry investment in technology during the next five years will be necessary to enhance business and individuals' experiences and drive demand for services. Ultimately, technology will need to be used as a tool that enhances business and individuals' experiences to drive demand for services.

The following table shows meeting duration as a percentage of total events.

Table A-3

Duration0.5 day1.0 day1.5 days2.0 days2.5 days3.0 days3.5 days4.0 days4.5 days5.0 days

More than 5 days

Source: Meetings Media, HSP

Typical Meeting Duration

Percent of Total8%14%7%16%14%20%7%5%4%4%2%

Source: Meetings Media, HSP

Typical Meeting Duration

Chargers Stadium and Convention Center Study Appendix A - Page 5

The importance of a quality hotel package increases the longer the duration of meetings and events. Without a good hotel package, these longer meetings and events are very difficult to secure.

The next set of tables presents the trend of important industry metrics such as exhibit hall demand, occupancy, attendance, room nights and critical financial information from surveyed participants by PricewaterhouseCoopers.

Table A-4 U.S. Convention Center Characteristics

Exhibit Hall Events

Average Number Events Average Attendance

SizeAverage Event

CountAverage Total Attendance

Average Number of Room Nights

Conventions / Trade Shows

Consumer Shows Total

Conventions / Trade Shows

Consumer Shows

Less than 100,000 square feet 322 218,300 34,200 27 22 49 1,600 3,300100,000 to 500,000 square feet 370 627,000 182,000 45 24 69 3,600 9,500More than 500,000 square feet 219 1,119,200 927,500 54 24 78 9,100 17,500

Source: PricewaterhouseCoopers

Convention Center All Events

As shown, the 2013 annual attendance of consumer shows is greater at smaller convention centers with less than 100,000 square feet of exhibit space than that of convention or trade shows. The number of annual exhibit event attendance is nearly split evenly between the two types of events for mid-sized convention centers. Larger convention centers, with more than 500,000 square feet of exhibit space, are opposite of their smaller counterparts, with convention and trade show attendance accounting for the largest portion of the annual exhibit event attendance. In general, convention centers should generate from .25 to .75 room nights per square foot of exhibit space. The average for larger convention centers is about .50 to .60 room nights per square foot of exhibit space.

The following table shows annual exhibit hall occupancy broken down by conventions / trade shows, consumer shows and other events.

Chargers Stadium and Convention Center Study Appendix A - Page 6

Figure A-2

19%$27%$

38%$11%$

11%$

8%$13%$

11%$6%$

0%

10%

20%

30%

40%

50%

60%

Less than 100,000 square feet 100,000 to 500,000 square feet More than 500,000 square feet

Annual Exhibit Hall Occupancy

Conventions / Trade Shows Consumer Shows Other Events

Source: PricewaterhouseCoopers

As the amount of exhibit space increases so does its utilization by convention and trade shows. Occupancy was higher in the larger facilities, led by convention and trade show occupancy. Exhibit hall occupancy, which can only practically reach 70 percent due to move in/out days and holidays, ranged from 42 percent in smaller buildings to 51 percent in larger buildings, on average.

The following figure shows the seasonality of conventions.

Chargers Stadium and Convention Center Study Appendix A - Page 7

Figure A-3

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

January February March April May June July August September October November December

Perc

ent o

f Con

vent

ions

Occ

urin

g

Seasonality of U.S. Conventions

Source: Meetings Market Report

Chargers Stadium and Convention Center Study Appendix A - Page 8

Meeting Planner Preferences

This table shows the factors for host city selections ranked by importance.

Table A-5

Factor1 = Very

Important2 = Moderately

Important3 = Not

Important

Hotel room prices and quality 80% 13% 7%Hotel room availability and capacity 80% 12% 8%Convention center and exhibition hall size and quality 76% 15% 9%

Facilities "under one roof" (i.e. meeting rooms , exhibit halls, hotels in one facility complex or connected) 61% 27% 12%Labor costs and service issues 58% 36% 7%Proximity of HQ hotel(s) to the convention center 54% 28% 19%Destination appeal to attendees 48% 41% 11%

Concentration of our members, clients or industry professionals in the city and region 48% 41% 11%Airport capacity and airfares 48% 37% 15%Total population, demographics 27% 38% 35%Road and highway access 26% 49% 24%Climate / weather 17% 54% 29%Cultural and entertainment amenities 13% 57% 30%

Source: R7M Research & Consulting

Event Site-Selection Trends - Factors for Host City Selection

The quality and availability of hotels and convention facilities are the most important considerations.

Chargers Stadium and Convention Center Study Appendix A - Page 9

The following table shows specific selection factors for selecting a meeting destination.

Table A-6

ConventionAssociation

MeetingCorporate Meeting

Number, Size and Quality of Meeting Rooms 93% 69% 81%

Negotiable Food, Beverage and Room Rates 87% 80% 79%

Cost of Hotel or Meeting Facility 82% 80% 80%

Number, Size and Quality of Sleeping Rooms 79% 54% 72%

Quality of Food Service 70% 63% 70%

Source: Meetings Market Report

Important Factors when Selecting a U.S. Meeting Destination

As shown, this reinforces the importance of the availability of the right spaces and the fees for those spaces as primary factors.

This table highlights changes in event and meeting planner’s events and shows.

Table A-7

Changes in Event & Meeting Planner's Events and Shows

Changes PercentageIncreased Negotiations 72%Requiring more telecom/internet bandwidth and related services 72%Shorter booking windows, they are booking closer to the event dates 68%Requiring higher-quality food and beverage 52%Event attendance is growing 40%Events are getting larger in terms of space requirements 40%Requiring attendance promotion assistance 32%Short Events in terms of total number of days 28%Events attendance is declining 20%Events are getting smaller in terms of space requirements 20%Asking for more Public Relations assistance and outreach to city and regional leaders 16%Shorter event day periods 12%Focusing more on event design and ambiance 12%Longerevent day periods 8%Longer booking windows, they are booking futher from the event dates 8%Other 4%

Source: Red 7 Media Research & Consulting

As shown, event and meeting planners are utilizing their leverage, being in a buyer’s market, to increase negotiations for better deals. Their events and shows are requiring more telecom/internet bandwidth and higher-quality food and beverage.

Chargers Stadium and Convention Center Study Appendix A - Page 10

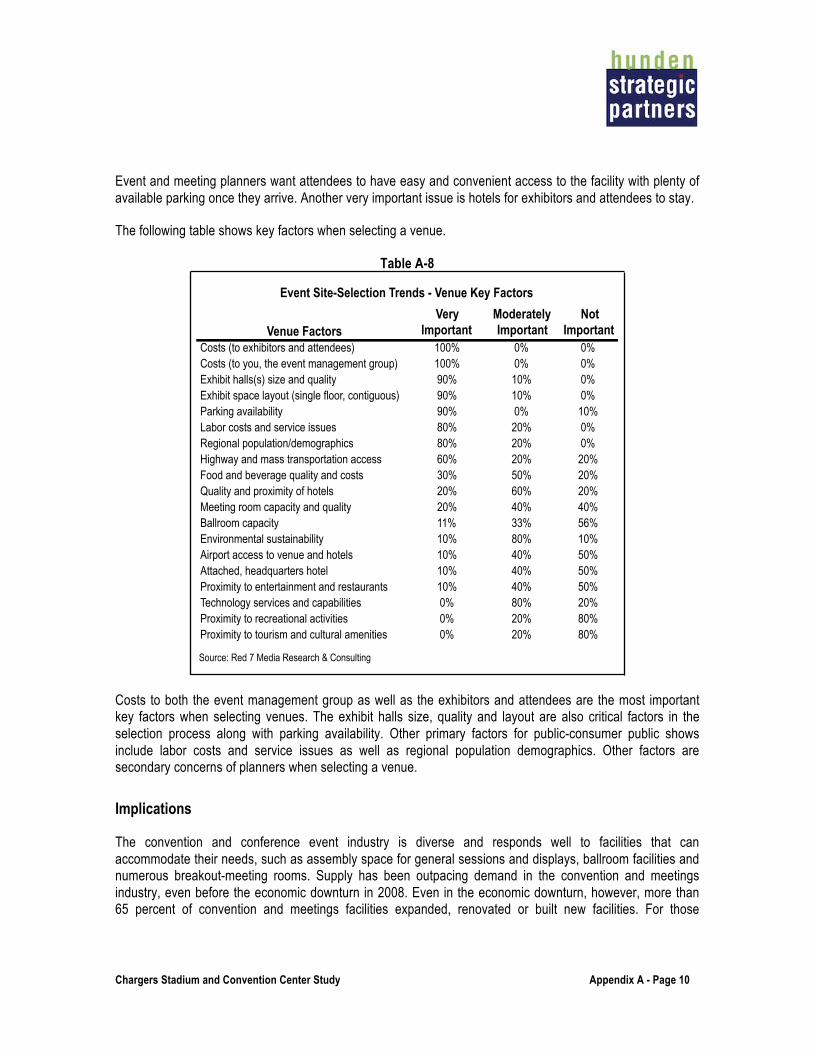

Event and meeting planners want attendees to have easy and convenient access to the facility with plenty of available parking once they arrive. Another very important issue is hotels for exhibitors and attendees to stay.

The following table shows key factors when selecting a venue.

Table A-8

Event Site-Selection Trends - Venue Key Factors

Venue FactorsVery

ImportantModerately Important

Not Important

Costs (to exhibitors and attendees) 100% 0% 0%Costs (to you, the event management group) 100% 0% 0%Exhibit halls(s) size and quality 90% 10% 0%Exhibit space layout (single floor, contiguous) 90% 10% 0%Parking availability 90% 0% 10%Labor costs and service issues 80% 20% 0%Regional population/demographics 80% 20% 0%Highway and mass transportation access 60% 20% 20%Food and beverage quality and costs 30% 50% 20%Quality and proximity of hotels 20% 60% 20%Meeting room capacity and quality 20% 40% 40%Ballroom capacity 11% 33% 56%Environmental sustainability 10% 80% 10%Airport access to venue and hotels 10% 40% 50%Attached, headquarters hotel 10% 40% 50%Proximity to entertainment and restaurants 10% 40% 50%Technology services and capabilities 0% 80% 20%Proximity to recreational activities 0% 20% 80%Proximity to tourism and cultural amenities 0% 20% 80%

Source: Red 7 Media Research & Consulting

Costs to both the event management group as well as the exhibitors and attendees are the most important key factors when selecting venues. The exhibit halls size, quality and layout are also critical factors in the selection process along with parking availability. Other primary factors for public-consumer public shows include labor costs and service issues as well as regional population demographics. Other factors are secondary concerns of planners when selecting a venue.

Implications

The convention and conference event industry is diverse and responds well to facilities that can accommodate their needs, such as assembly space for general sessions and displays, ballroom facilities and numerous breakout-meeting rooms. Supply has been outpacing demand in the convention and meetings industry, even before the economic downturn in 2008. Even in the economic downturn, however, more than 65 percent of convention and meetings facilities expanded, renovated or built new facilities. For those

Chargers Stadium and Convention Center Study Appendix A - Page 11

communities with the right mix of facilities and attractiveness, the return on investment can be quite measurable, in jobs, business activity and tax revenue.

Since 2013, the meetings and convention business has been expanding at a rapid pace, in many cases faster than the growth in corporate or leisure business. However, events are shorter today than in the past and companies often send fewer attendees or booth attendants/salespeople. Overall, the industry today is about the same size as is was in 2000, yet with many more facilities and adjacent hotel packages to choose from.

Important factors in the decision process of choosing a convention or meeting site include availability of nearby hotel rooms, cost of travel, and meeting space in the facility and hotels. The most important types of meeting space now are the number of breakout meeting rooms and ballrooms. Expo and exhibition space are still important, but less so now than in the past. Higher rated business (e.g. corporate, medical, associations that are willing to pay more for better facilities and experiences) needs many breakout rooms and high quality ballrooms to conduct their trainings and other meetings.

Is investment in this industry worth it? For those that construct and manage the right set of facilities within an attractive market, yes. Those that put the right package together (hotels and the right kinds of function space in a walkable environment) will generate new meetings and event business. Enhancing the ‘fun’ side of the community, such as a nearby downtown or entertainment/restaurant district, will provide the community more to sell against its competitors. Ultimately, those cities with a competitive package will generate a constant flow of group and event business that will support a number of hotels, restaurants and jobs.

TABLE OF CONTENTS ----------- Executive Summary

Chapter 1 Demand and Impact

Appendix A Convention Industry Overview and Trends

Appendix B Convention Market Competitive and Comparable Analysis

Appendix C Influence of Comparable Downtown Stadiums

Appendix D Meeting Planner Interviews

Appendix E Hotel Market Analysis

Appendix F Comparable Convention City Hotel Tax Rate Data

Chargers Stadium and Convention Center Study Appendix B – Page 2

CONVENTION MARKET COMPETITIVE AND COMPARABLE ANALYSIS This appendix provides an analysis of existing convention centers and exposition halls that are connected or adjacent to professional football stadiums. While these cities differ in size, function space and hotel offerings, the facilities are similar in their types of spaces, have similarly sized meeting and event facilities and are comparable in that they all utilize professional football stadiums for non-football events. The focus in this chapter is specifically regarding the benefits and challenges of such an arrangement during the NFL season. S

The following table lists the comparable convention centers, cities, and size statistics.

Table B-1 Comparable Stadium & Convention Center Complexes

Facility Location

Combined Metropolitan

Population 2015

Annual Visitors in Millions

Total Function

Space (SF)

Total Exhibit

Space (SF)

Total Ballroom

Space (SF)

Total Meeting Space

Stadium Field Space

Number of Breakout Room

Georgia World Congress Center and Georgia Dome Atlanta 6,365,108 51.0 1,759,818 1,366,000 58,722 233,096 102,000 106Moscone Center North, South and West ** San Francisco 8,713,914 24.6 916,571 538,660 81,119 296,792 -- 87NRG Convention Center and NRG Stadium Houston 6,855,069 17.5 880,765 706,213 0 77,352 97,200 59Indiana Convention Center and Lucas Oil Stadium Indianapolis 2,372,530 26.0 912,551 558,000 57,072 114,479 183,000 87America's Center and Dome at America's Center Saint Louis 2,916,447 23.9 659,741 358,000 27,625 129,116 145,000 98CenturyLink Event Center and CenturyLink Field Seattle 4,602,591 38.1 355,555 255,555 0 0 100,000 0

Proposed San Diego Convention/Stadium San Diego 3,299,521 34.3 385,000 250,000 64,500 70,500 100,000 64

** This facility is not attached to a stadium. Figures represent pre-expansion.Source: Various Event Facilities and CVBs, Hunden Strategic Partners

San Francisco, California

San Francisco is a major cultural, commercial, and financial center on the West Coast of the U.S. The city is well known as both one of the most expensive cities to live in or visit, while also being one of the most popular cities to live in or visit. Approximately 25 million visitors travel to San Francisco annually according to San Francisco Travel, the official tourism agency for the city. The San Francisco Bay area includes San Jose, Oakland, Berkeley, Palo Alto, and the high-tech industry known as Silicon Valley, However, all of the important media is headquartered in San Francisco. The historic and urban core of the entire region is downtown San Francisco. San Francisco is the nation's second most densely populated city (after New York) and is the hub of the nation's fifth largest metropolitan area, with 8,7 million people in 2015.

The Moscone Center only books conventions and conferences, in order to serve its purpose of generating room nights and maximizing revenues for the city’s hotels. Trade and consumer shows go elsewhere in the metro region such as San Mateo. The bulk of the conventions tend to revolve around the medical and technology fields, especially given the site of Silicon Valley only 40 miles southeast of the center. Nearly every convention is a national association convention or large corporate business meeting, which are booked years in advance.

Chargers Stadium and Convention Center Study Appendix B – Page 3

The San Francisco Moscone Center is the city’s major convention center located downtown that has three separate, non-contiguous exhibition halls and three separate buildings, two of which are attached through underground corridors. The North and South Halls are underground, with the Yerba Buena Gardens sitting atop the North Hall at street level. The buildings are on three adjacent blocks in the South of Market neighborhood. The three buildings consist of more than 20 square blocks and has more than 916,000 square feet of function space.

In 2015, the center hosted 44 conventions, which accounted for nearly 1.2 million hotel room nights. Downtown San Francisco has approximately 32,000 hotel rooms in the area and approximately 65,000 rooms in the city.

The following figure shows an aerial view of the Moscone South and North buildings.

Figure B-1

Moscone South was the original facility and opened in 1981. Moscone South's exhibit level is underground and covers one city block. The South Hall has 260,560 square feet of column-free exhibit space that can be separated into three sections (A, B & C). The exhibit halls are attached to the Moscone North's exhibit halls through a 225-foot concourse and can be closed off for separate conventions. The Moscone South complex includes the Gateway Ballroom. Also above ground is the Esplanade Level, which encompasses a 14,000 square-foot lobby, a 42,675 square-foot flexible ballroom and a 2,870 square-foot breakout room.

Moscone North opened in 1992 as an underground expansion of Moscone Center. Moscone North's exhibit level also covers an 11-acre city block. The North Hall features an 181,440 square-foot exhibit hall that can be separated into a large hall (D) and a smaller hall (E). Attendees can flow into the Moscone South exhibit level or be separated in the case of different simultaneous events. However, management always tries to sell

Chargers Stadium and Convention Center Study Appendix B – Page 4

Moscone South and North wings together for single events, rather than splitting them into separate meetings. The lower level also includes breakout meeting rooms. Like the Moscone South facility, the North facility includes a 15,300 square-foot street-level lobby that is column-free and naturally lighted, complete with its own semi-circular drive for multiple shuttle busses. The North and South blocks have entry drives that mirror each other along Howard Street for a convenient single-area entry-point.

Moscone West opened in 2003 and is a three-floor complex on the block just west of the Moscone North site. The street-level plan is an exhibition space with small meeting rooms around the periphery. The second and third floors include a wraparound view of the downtown area with nearly 100,000 square feet of carpeted meeting space that has the ability to be divided into as many as 19 meeting rooms. The second and third floor lobbies have 28,261 square feet of pre-function space. All loading docks are located below street level.

Over the next three years, the Moscone Center is undergoing a $350 million expansion project that will join the two largest currently disconnected exhibit halls into one large underground hall featuring 580,000 contiguous square feet. New ballroom and meeting room space will be built above a portion of both the North and South Moscone blocks, which is where the majority of the construction and expansion are taking place. Howard Street will still run between the two blocks and on top of the new contiguous exhibition hall.

The Moscone Center has found that conventions are growing faster than the facility can keep up, and in numerous cases, are in danger of losing large annual conventions. The potential lost business was the key driver for the expansion to combine the South and North buildings into one contiguous space of 580,000 square feet, with new above-grade buildings featuring more meeting space. Conventions and conferences prefer the above-ground sense of light and security from the street level or below-grade level, which is why the West building is usually the first building to be reserved years in advance. The sales staff can either reserve the entire three-block center for a convention, or separate the buildings. Typically, Moscone South and North are sold together, and after the expansion project, will effectively be one single building.

As long as the path between the two convention spaces is short and easy, two convention centers can certainly work together to host one large event. Two non-contiguous centers are not preferred but are, nevertheless, very doable, as long as the second convention center also has full kitchen and food service capabilities.

Overhead skywalks that can attach two conference or convention buildings are a desirable plan to keep people from feeling isolated from the other part of the convention. Visitors would prefer to walk if there is a direct and safe connection, rather than rely on shuttles between buildings.

Houston, Texas

The Houston metropolitan area in southeast Texas is the fifth largest in the nation and has approximately six million people. Houston has a robust economy heavily based in industrial sectors such as energy, oil, aeronautics and transportation. In addition, the Houston area is a hub for academic and medical research institutions, and in terms of business, only New York City is home to more Fortune 500 companies than Houston. The area has professional sports in every major league except the National Hockey League.

The following figure shows NRG Park and the surrounding area.

Chargers Stadium and Convention Center Study Appendix B – Page 5

Figure B-2

Houston’s NRG Park, which includes the NRG Stadium, NRG Center, NRG Arena and NRG Astrodome, holds the primary facilities that provide the exposition function for the area. NRG Center is the focus of this analysis as it holds the largest exhibition spaces and hosts the majority of exposition-type events as well as conventions.

NRG Center has 11 exhibit hall divisions each with at least 37,500 square feet of space and the largest divisible space being 166,000 square feet. The NRG Arena also has 706,000 square feet of contiguous space to supplement the NRG Center. Having space this large and a 70,000-seat climate-controlled stadium allows for a few annual meetings that cannot be held elsewhere. Those meetings tend to be religious organizations and direct-selling groups that hold annual meetings and congresses.

Sporting events, consumer shows and trade shows contribute a large number of use days to each of the facilities in NRG Park. Sporting events are concentrated between NRG Stadium, Astrodome and Arena and they include professional and high school football, college basketball, cheer competitions and even athletic runs on the park grounds. Consumer shows and trade shows range from multiple car shows and gun and knife shows to health and beauty expos and home and garden shows. Many family shows from Disney, Sesame Street and Lego also fill NRG Park’s schedule. Other local events such as high school graduations reserve the NRG Center to host their ceremony, as well.