samsung electronics september, 2001. company overview divisional highlights contentscontents q2 2001...

TRANSCRIPT

Samsung ElectronicsSamsung Electronics

SeptemberSeptember, 2001, 2001

Company OverviewCompany Overview

Divisional Highlights Divisional Highlights

ContentsContentsContentsContents

Q2 2001 ResultsQ2 2001 Results

Company OverviewCompany OverviewCompany OverviewCompany Overview

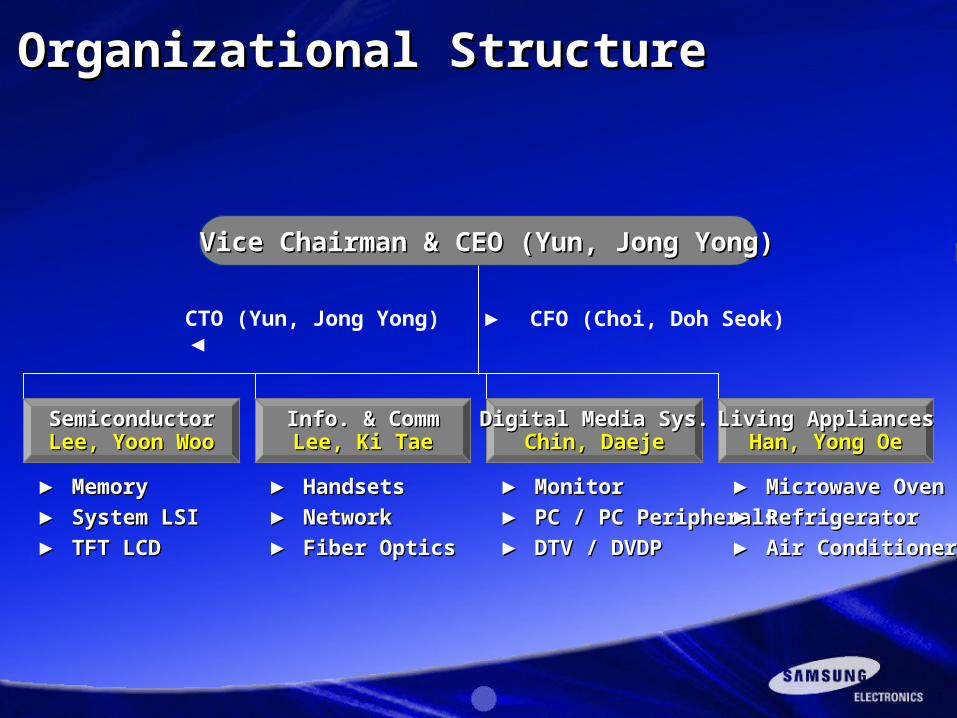

Vice Chairman & CEO (Yun, Jong Yong)Vice Chairman & CEO (Yun, Jong Yong)

▶ CFO (Choi, Doh Seok)CTO (Yun, Jong Yong) ◀

Organizational StructureOrganizational Structure

SemiconductorSemiconductorLee, Yoon WooLee, Yoon Woo

▶ ▶ MemoryMemory

▶ ▶ System LSISystem LSI

▶ ▶ TFT LCDTFT LCD

Info. & CommInfo. & CommLee, Ki TaeLee, Ki Tae

▶ ▶ HandsetsHandsets

▶ ▶ NetworkNetwork

▶ ▶ Fiber OpticsFiber Optics

Digital Media Sys.Digital Media Sys.Chin, DaejeChin, Daeje

▶ ▶ MonitorMonitor

▶ ▶ PC / PC PeripheralsPC / PC Peripherals

▶ ▶ DTV / DVDPDTV / DVDP

Living AppliancesLiving AppliancesHan, Yong OeHan, Yong Oe

▶ ▶ Microwave OvenMicrowave Oven

▶ ▶ RefrigeratorRefrigerator

▶ ▶ Air ConditionerAir Conditioner

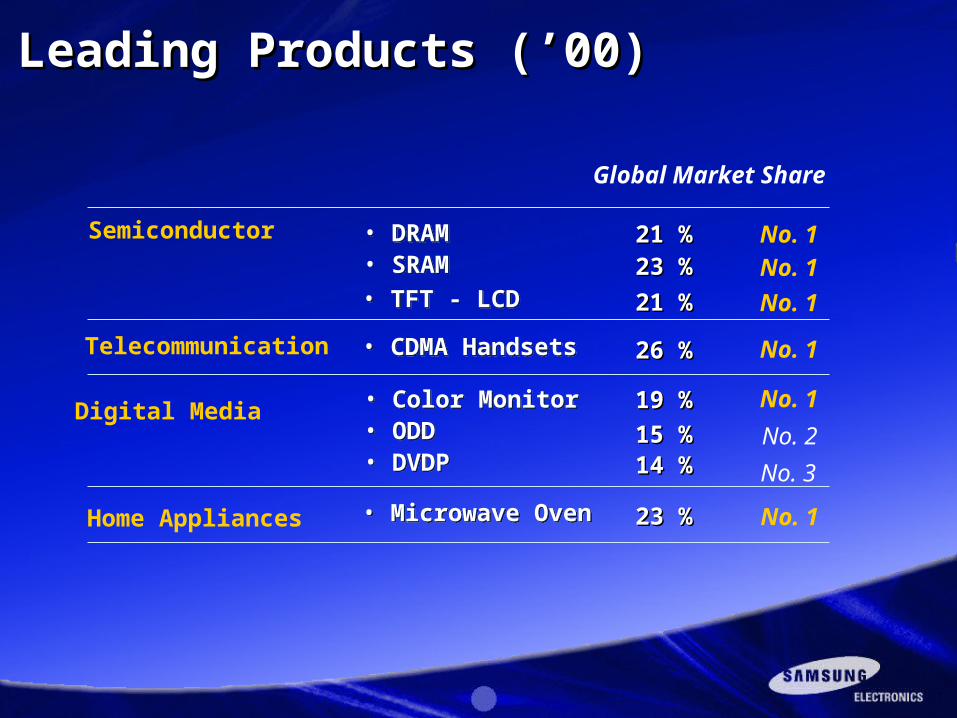

Global Market Share

No. 126 %26 %• CDMA Handsets • CDMA Handsets

No. 1No. 1

21 %21 %23 %23 %

• DRAM• SRAM

• DRAM• SRAM

No. 121 %21 %• TFT - LCD • TFT - LCD

Telecommunication

Semiconductor

No. 1

No. 215 %15 %

19 %19 %• Color Monitor• ODD• DVDP

• Color Monitor• ODD• DVDP

No. 123 %23 %• Microwave Oven • Microwave Oven

Digital Media

Home Appliances

14 %14 % No. 3

Leading Products (’00)Leading Products (’00)

Q2 2001 ResultsQ2 2001 ResultsQ2 2001 ResultsQ2 2001 Results

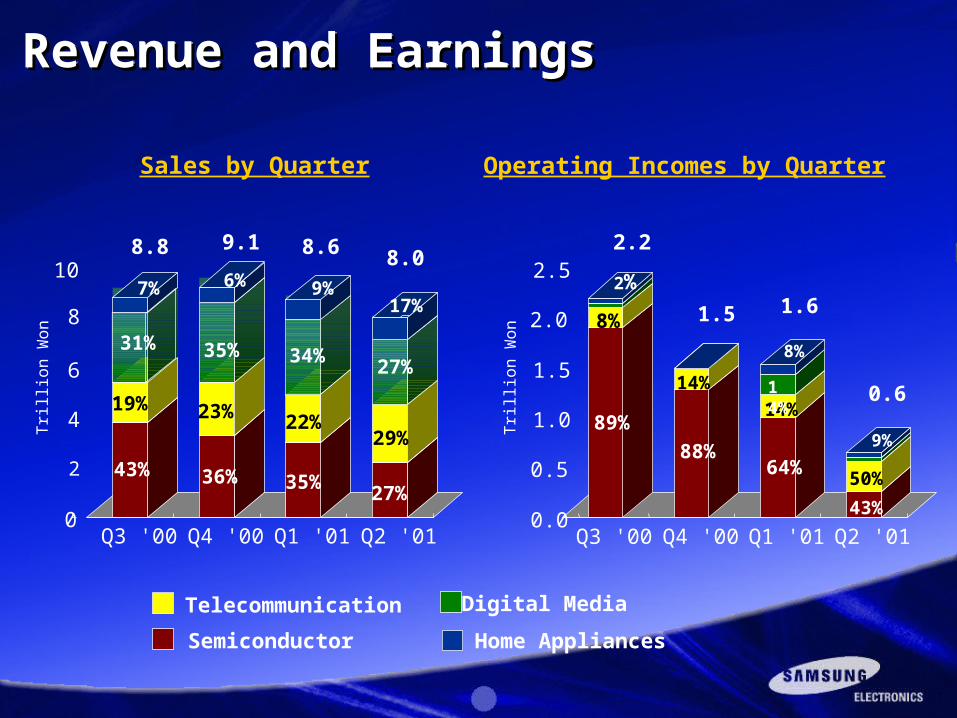

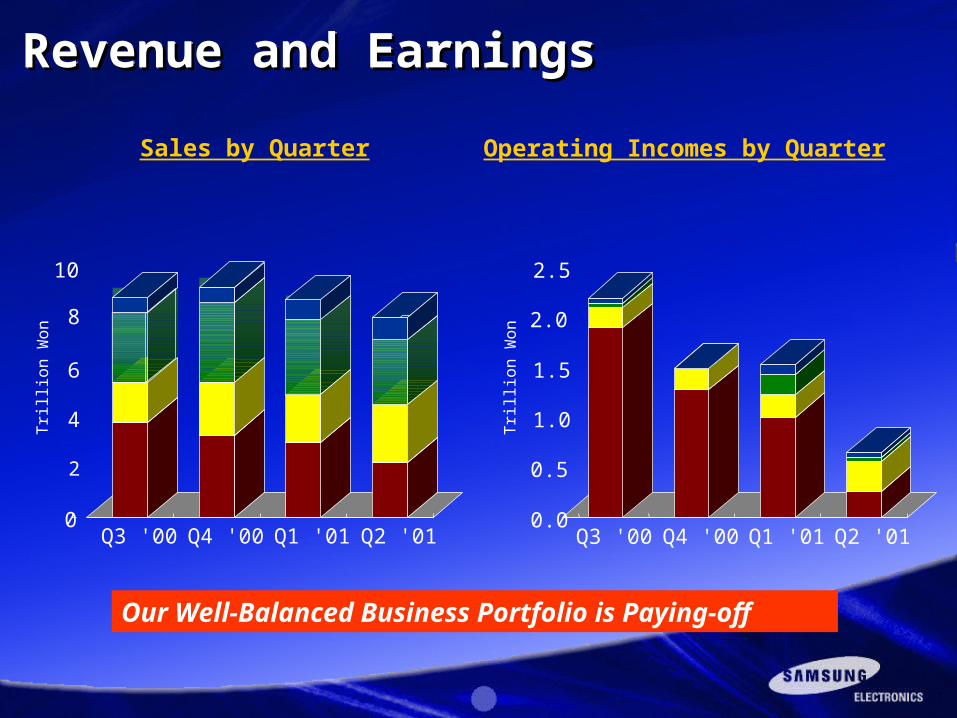

Sales by Quarter Operating Incomes by Quarter

Revenue and EarningsRevenue and EarningsRevenue and EarningsRevenue and Earnings

Digital MediaTelecommunication

Semiconductor Home Appliances

0

2

4

6

8

10

Q3 '00 Q4 '00 Q1 '01 Q2 '01

Tri

l lion W

on

0.0

0.5

1.0

1.5

2.0

2.5

Q3 '00 Q4 '00 Q1 '01 Q2 '01Tri

l lion W

on

8.8 9.1 8.6 8.02.2

1.5 1.6

0.6

43% 36% 35%27%

19% 23% 22%29%

89%

88%64%

43%

8%

14%

14%

50%

31% 35% 34% 27%

7% 9%17%

2%

14%

8%

9%

6%

Revenue and EarningsRevenue and EarningsRevenue and EarningsRevenue and Earnings

Our Well-Balanced Business Portfolio is Paying-off

0

2

4

6

8

10

Q3 '00 Q4 '00 Q1 '01 Q2 '01

Sales by Quarter Operating Incomes by Quarter

Tri

l lion W

on

0.0

0.5

1.0

1.5

2.0

2.5

Q3 '00 Q4 '00 Q1 '01 Q2 '01Tri

l lion W

on

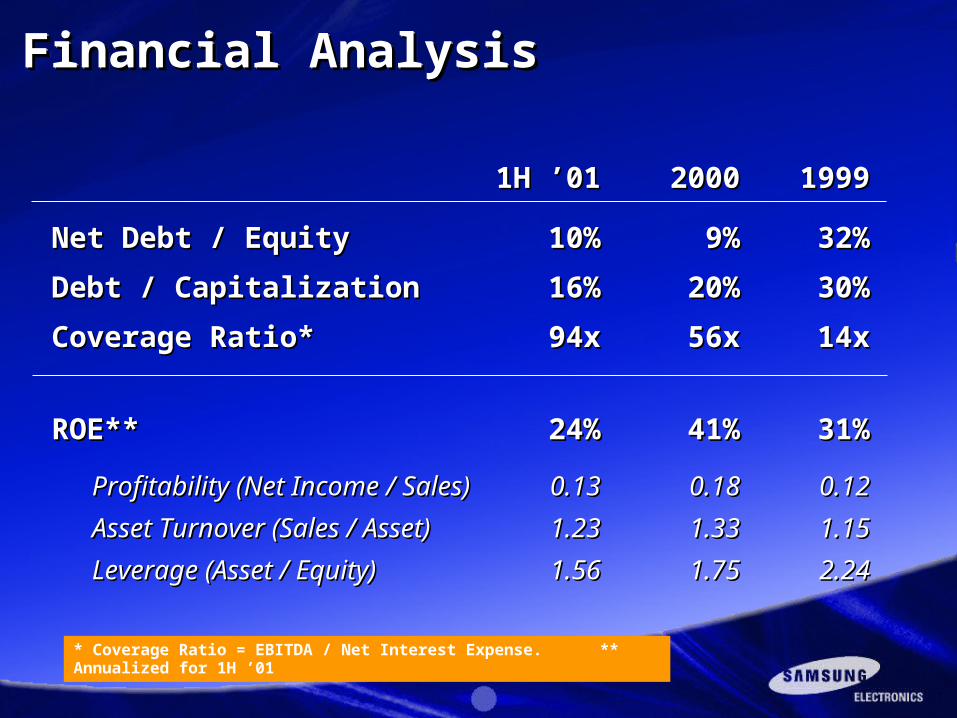

11H ’01H ’01 20002000 19991999

Net Debt / EquityNet Debt / Equity 10%10% 9%9% 32%32%

Debt / CapitalizationDebt / Capitalization 16%16% 20%20% 30%30%

Coverage Ratio*Coverage Ratio* 94x94x 56x56x 14x14x

ROE**ROE** 24%24% 41%41% 31%31%

Profitability (Net Income / Sales)Profitability (Net Income / Sales) 0.130.13 0.180.18 0.120.12

Asset Turnover (Sales / Asset)Asset Turnover (Sales / Asset) 1.231.23 1.331.33 1.151.15

Leverage (Asset / Equity)Leverage (Asset / Equity) 1.561.56 1.751.75 2.242.24

* Coverage Ratio = EBITDA / Net Interest Expense. ** Annualized for 1H ’01

Financial AnalysisFinancial AnalysisFinancial AnalysisFinancial Analysis

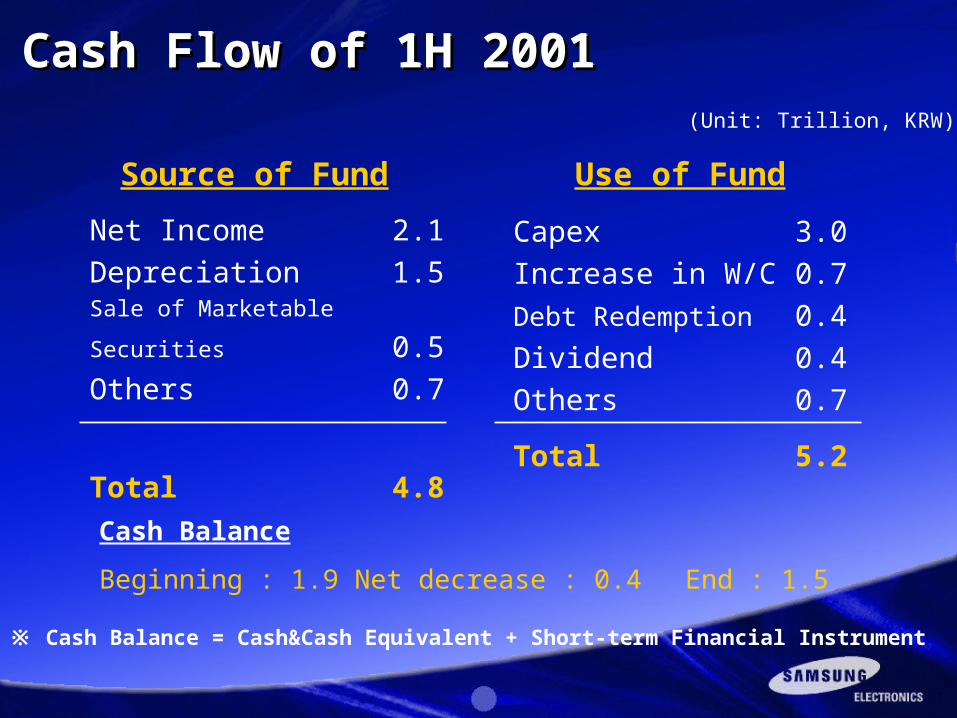

Net Income 2.1

Depreciation 1.5

Sale of Marketable Securities 0.5

Others 0.7

Total 4.8

(Unit: Trillion, KRW)

Source of Fund Use of Fund

Capex 3.0

Increase in W/C 0.7

Debt Redemption 0.4

Dividend 0.4

Others 0.7

Total 5.2

Cash Balance

Beginning : 1.9 Net decrease : 0.4 End : 1.5

※ Cash Balance = Cash&Cash Equivalent + Short-term Financial Instrument

Cash Flow of 1H 2001Cash Flow of 1H 2001Cash Flow of 1H 2001Cash Flow of 1H 2001

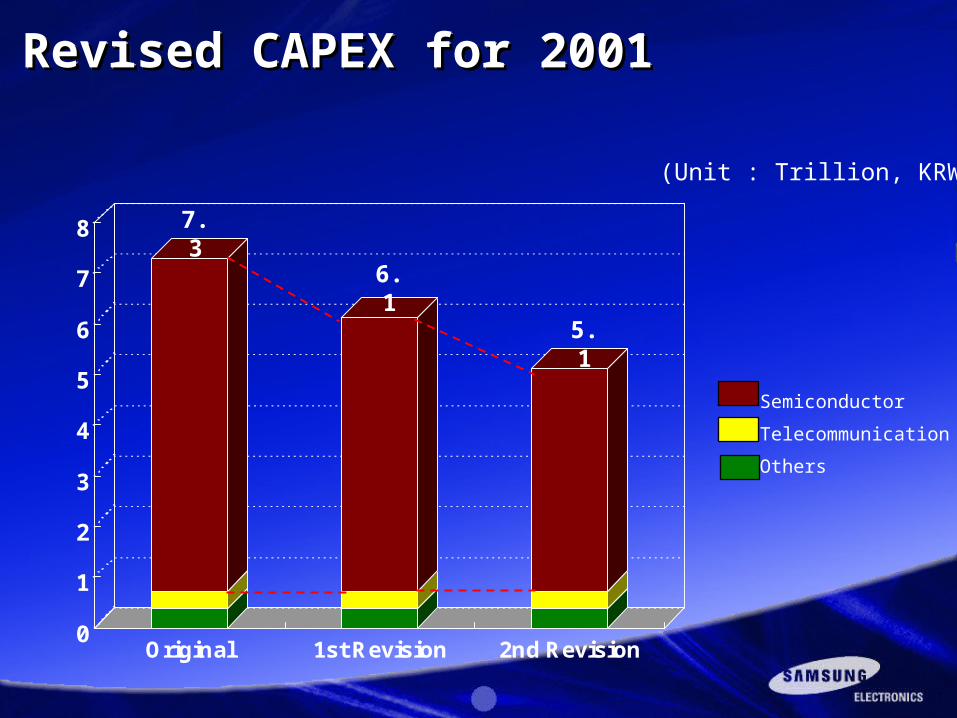

Revised CAPEX for 2001Revised CAPEX for 2001Revised CAPEX for 2001Revised CAPEX for 2001

0

1

2

3

4

5

6

7

8

Original 1st Revision 2nd Revision

Semiconductor

Telecommunication

Others

7.3

6.1

5.1

(Unit : Trillion, KRW)

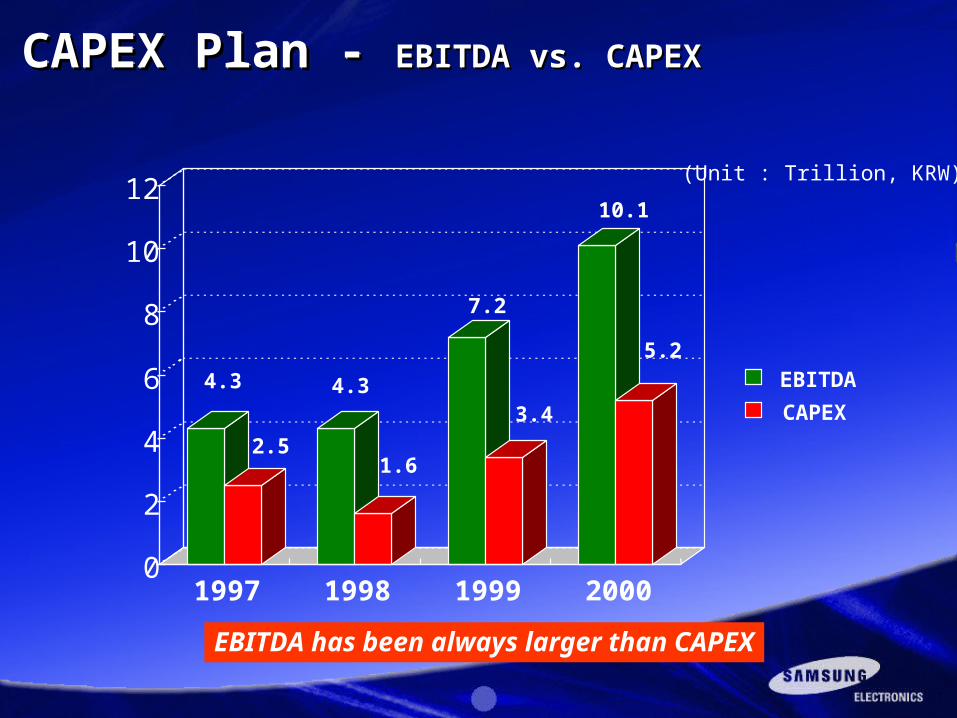

CAPEX Plan - CAPEX Plan - EBITDA vs. CAPEXEBITDA vs. CAPEXCAPEX Plan - CAPEX Plan - EBITDA vs. CAPEXEBITDA vs. CAPEX

EBITDA has been always larger than CAPEX

(Unit : Trillion, KRW)

0

2

4

6

8

10

12

1997 1998 1999 2000

EBITDA

CAPEX

4.3

2.5

4.3

1.6

7.2

3.4

10.1

5.2

Divisional HighlightsDivisional Highlights

- Semiconductor Division- Semiconductor Division

Divisional HighlightsDivisional Highlights

- Semiconductor Division- Semiconductor Division

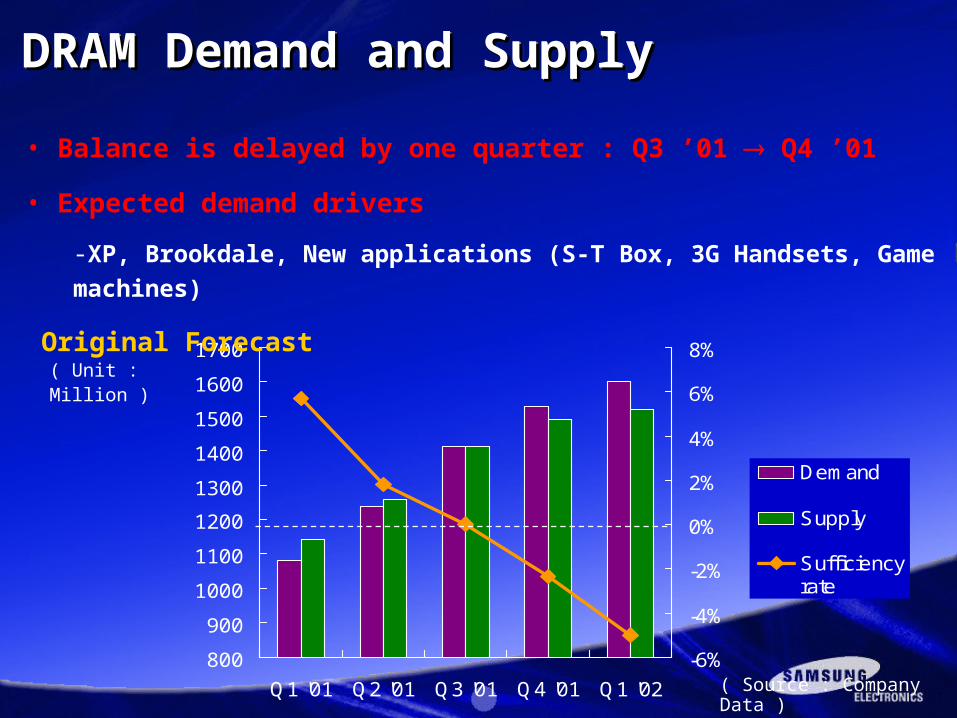

DRAM Demand and SupplyDRAM Demand and SupplyDRAM Demand and SupplyDRAM Demand and Supply

800

900

1000

1100

1200

1300

1400

1500

1600

1700

Q1 '01 Q2 '01 Q3 '01 Q4 '01 Q1 '02

-6%

-4%

-2%

0%

2%

4%

6%

8%

Demand

Supply

Sufficiencyrate

( Unit : Million )

( Source : Company Data )

• Balance is delayed by one quarter : Q3 ’01 Q4 ’01

• Expected demand drivers

-XP, Brookdale, New applications (S-T Box, 3G Handsets, Game machines)

Original Forecast

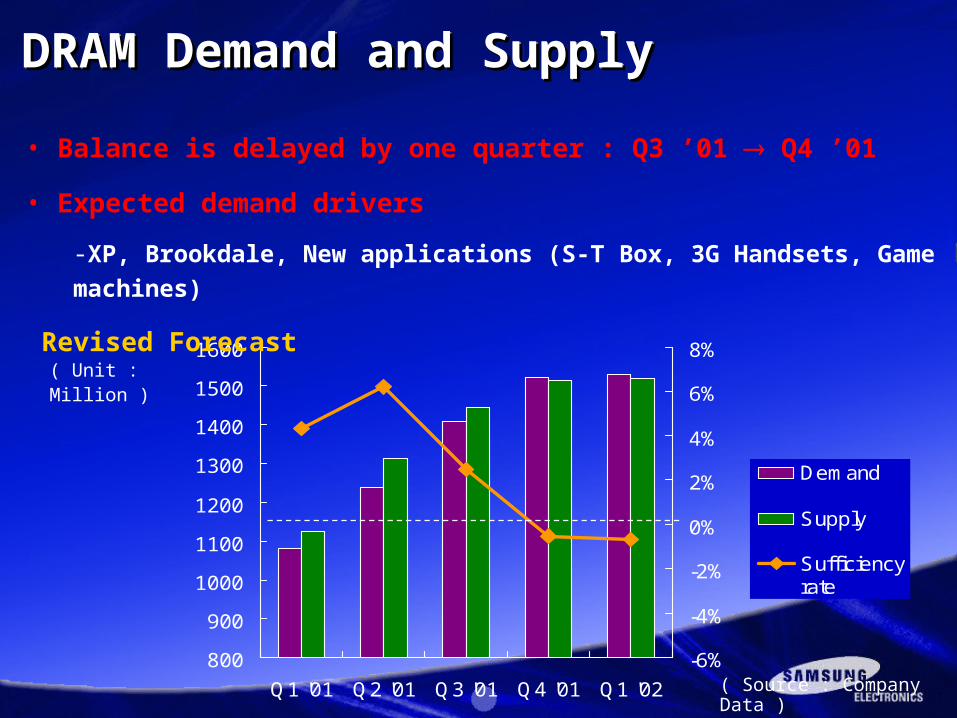

DRAM Demand and SupplyDRAM Demand and SupplyDRAM Demand and SupplyDRAM Demand and Supply

800

900

1000

1100

1200

1300

1400

1500

1600

Q1 '01 Q2 '01 Q3 '01 Q4 '01 Q1 '02

-6%

-4%

-2%

0%

2%

4%

6%

8%

Demand

Supply

Sufficiencyrate

( Unit : Million )

( Source : Company Data )

• Balance is delayed by one quarter : Q3 ’01 Q4 ’01

• Expected demand drivers

-XP, Brookdale, New applications (S-T Box, 3G Handsets, Game machines)

Revised Forecast

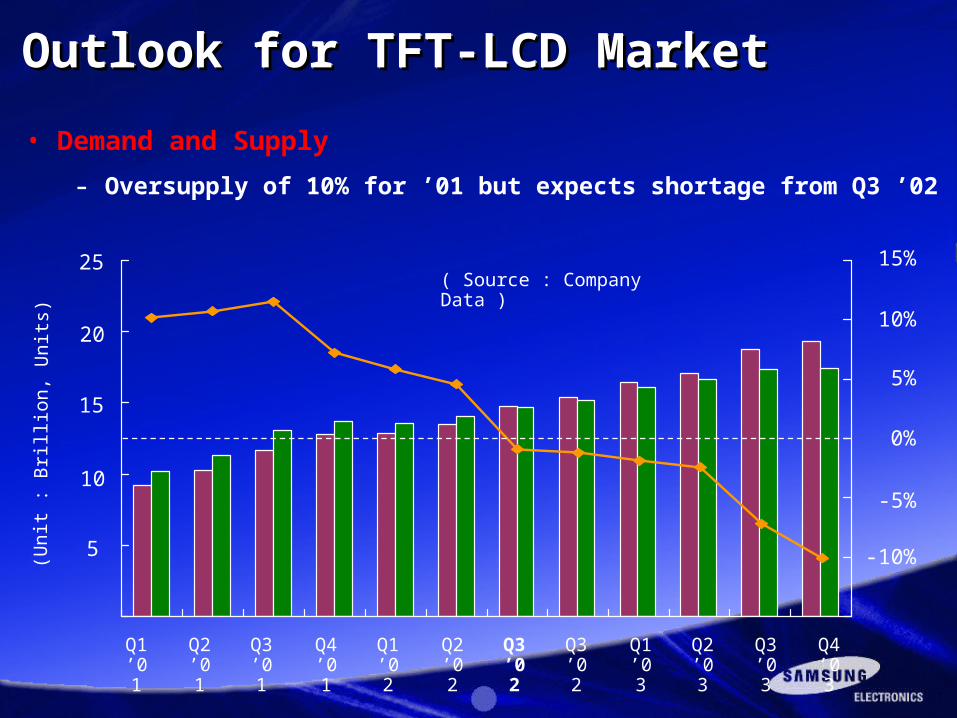

• Demand and Supply

- Oversupply of 10% for ’01 but expects shortage from Q3 ’02

Outlook for TFT-LCD MarketOutlook for TFT-LCD MarketOutlook for TFT-LCD MarketOutlook for TFT-LCD Market

( Source : Company Data )25

20

15

10

5

(Unit

: B

ril l i

on, U

nit

s)

15%

10%

5%

0%

-5%

-10%

Q1 ’01

Q2 ’01

Q3 ’01

Q4 ’01

Q1 ’02

Q2 ’02

Q3 ’02

Q3 ’02

Q1 ’03

Q2 ’03

Q3 ’03

Q4 ’03

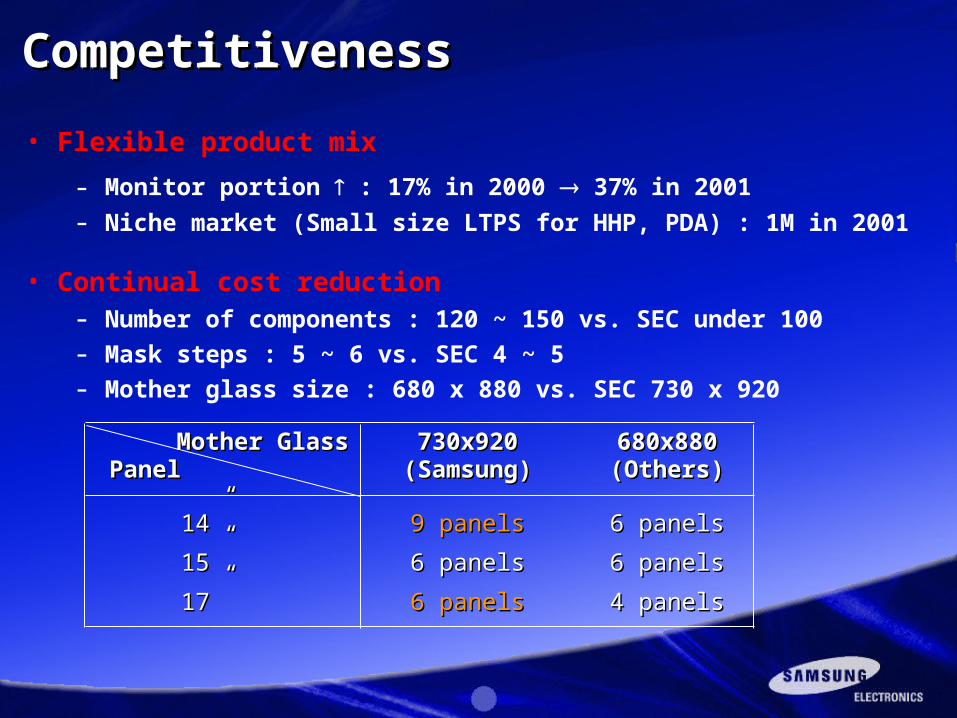

• Flexible product mix

- Monitor portion : 17% in 2000 37% in 2001

- Niche market (Small size LTPS for HHP, PDA) : 1M in 2001

• Continual cost reduction - Number of components : 120 ~ 150 vs. SEC under 100

- Mask steps : 5 ~ 6 vs. SEC 4 ~ 5

- Mother glass size : 680 x 880 vs. SEC 730 x 920

Competitiveness Competitiveness Competitiveness Competitiveness

Mother GlassMother Glass 730x920730x920 680x880680x880PanelPanel (Samsung)(Samsung) (Others)(Others)

14”14” 9 panels9 panels 6 panels6 panels

15”15” 6 panels6 panels 6 panels6 panels

17”17” 6 panels6 panels 4 panels4 panels

Divisional HighlightsDivisional Highlights

- Telecommunication Division- Telecommunication Division

Divisional HighlightsDivisional Highlights

- Telecommunication Division- Telecommunication Division

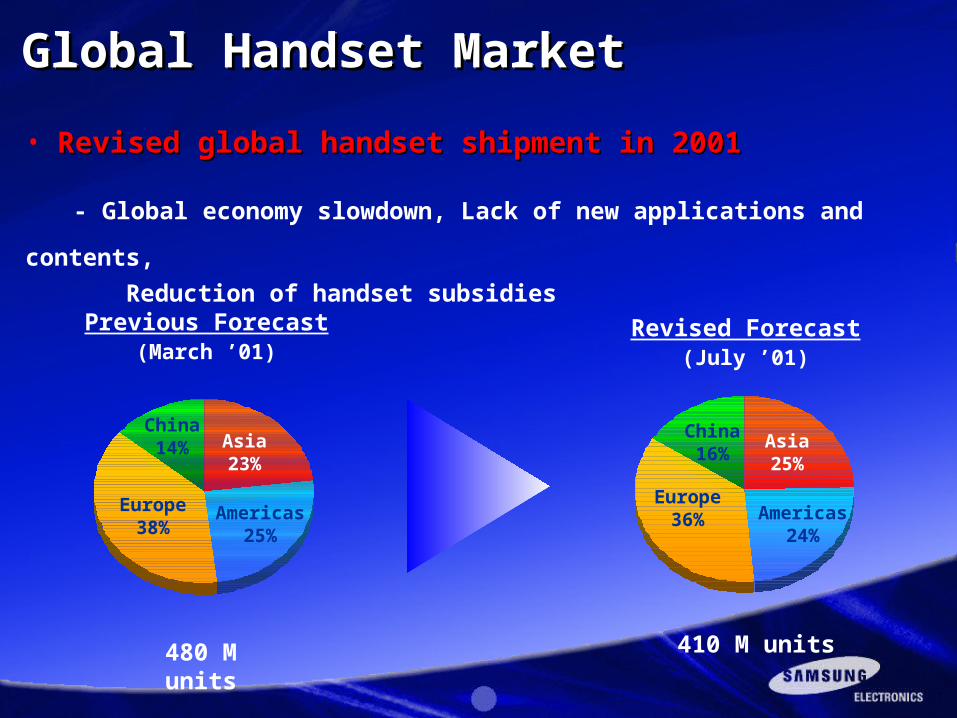

Revised Forecast(July ’01)

Previous Forecast(March ’01)

480 M units

Global Handset MarketGlobal Handset MarketGlobal Handset MarketGlobal Handset Market

• Revised global handset shipment in 2001Revised global handset shipment in 2001

- Global economy slowdown, Lack of new applications and contents,

Reduction of handset subsidies

Asia23%

Americas25%

Europe38%

China14%

410 M units

Asia25%

Americas24%

Europe36%

China16%

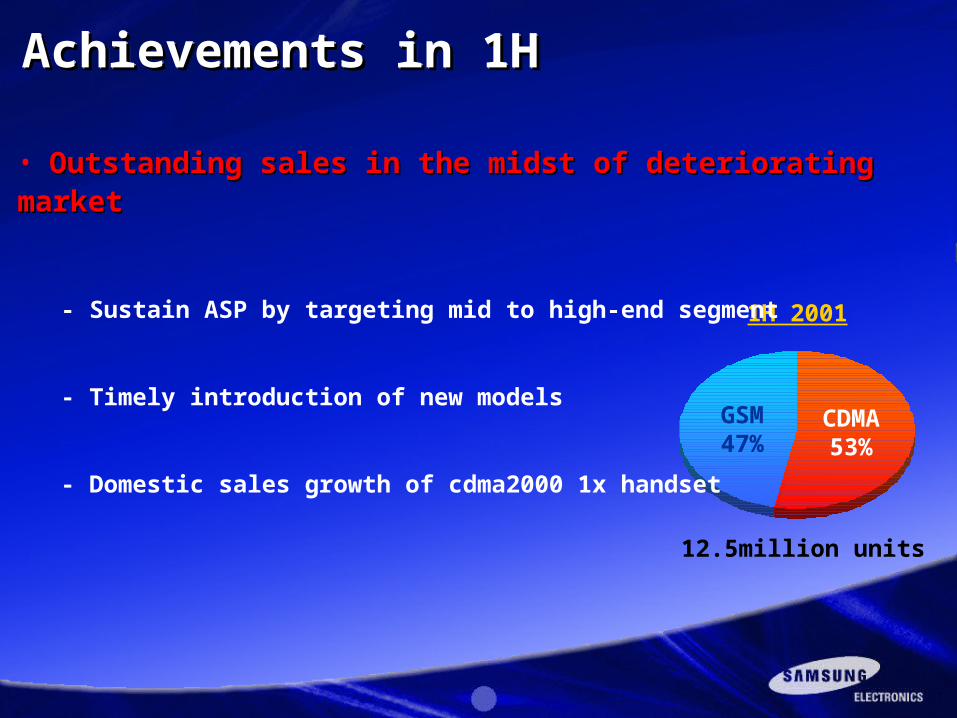

1H 2001

12.5million units

CDMA53%

GSM47%

Achievements in 1HAchievements in 1HAchievements in 1HAchievements in 1H

• Outstanding sales in the midst of deteriorating marketOutstanding sales in the midst of deteriorating market

- Sustain ASP by targeting mid to high-end segment

- Timely introduction of new models

- Domestic sales growth of cdma2000 1x handset

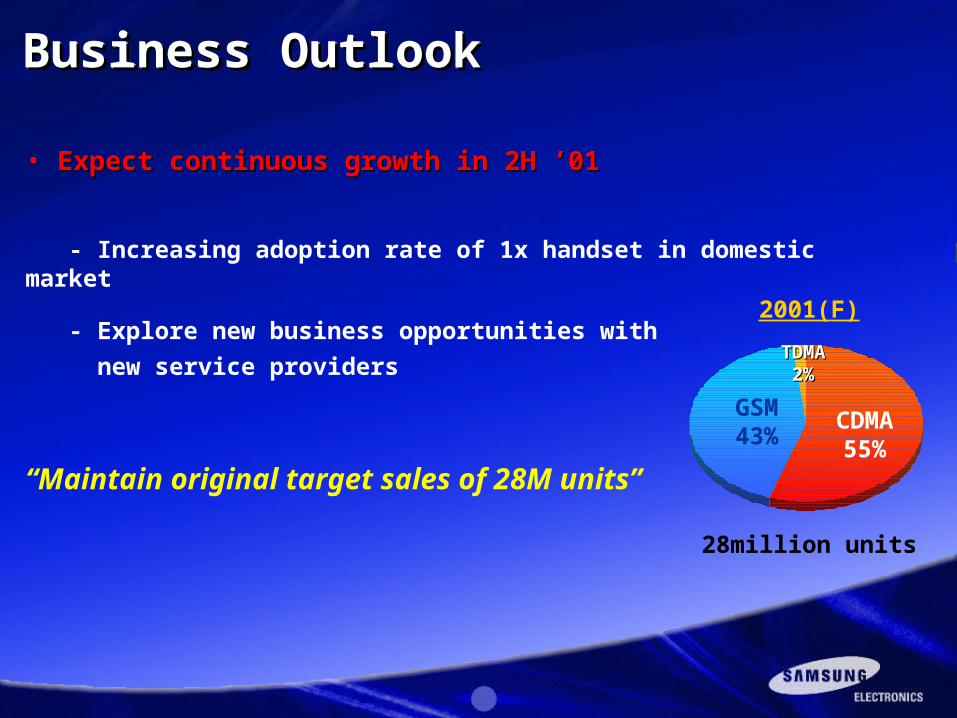

2001(F)

28million units

CDMA55%

GSM43%

Business OutlookBusiness OutlookBusiness OutlookBusiness Outlook

• Expect continuous Expect continuous ggrowthrowth in 2H ’01 in 2H ’01

- Increasing adoption rate of 1x handset in domestic market

- Explore new business opportunities with

new service providers

“Maintain original target sales of 28M units”

TDMATDMA2%2%

• Recent achievements in 1H ’01Recent achievements in 1H ’01- Strong presence in 1x system marketStrong presence in 1x system market

- CDMA contracts in China and Puerto Rico CDMA contracts in China and Puerto Rico

• 2H ’01 Outlook2H ’01 Outlook

- Domestic: 2.5G System expansion and upgrade to 1x EV-DODomestic: 2.5G System expansion and upgrade to 1x EV-DO

- Overseas: Increasing adoption of CDMA technologyOverseas: Increasing adoption of CDMA technology

* China, Japan, Brazil, India, Israel, etc.* China, Japan, Brazil, India, Israel, etc.

““Current macro environment remains challenging”Current macro environment remains challenging”

Wireless systemsWireless systemsWireless systemsWireless systems

Divisional HighlightsDivisional Highlights

- Digital Media Division- Digital Media Division

Divisional HighlightsDivisional Highlights

- Digital Media Division- Digital Media Division

Global Market Share Trends

Rank M / S

1 15%

2 12%

6 13%

5 8%

3 12%

Product 1999 2000 2001 (F)

Digital MediaDigital MediaDigital MediaDigital Media

Rank M / S

1 19%

2 15%

3 16%

4 9%

2 15%

Rank M / S

1 19%

2 14%

2 15%

3 9%

1 16%

Monitors

ODD

DVD Players

Color TVs

VCRs

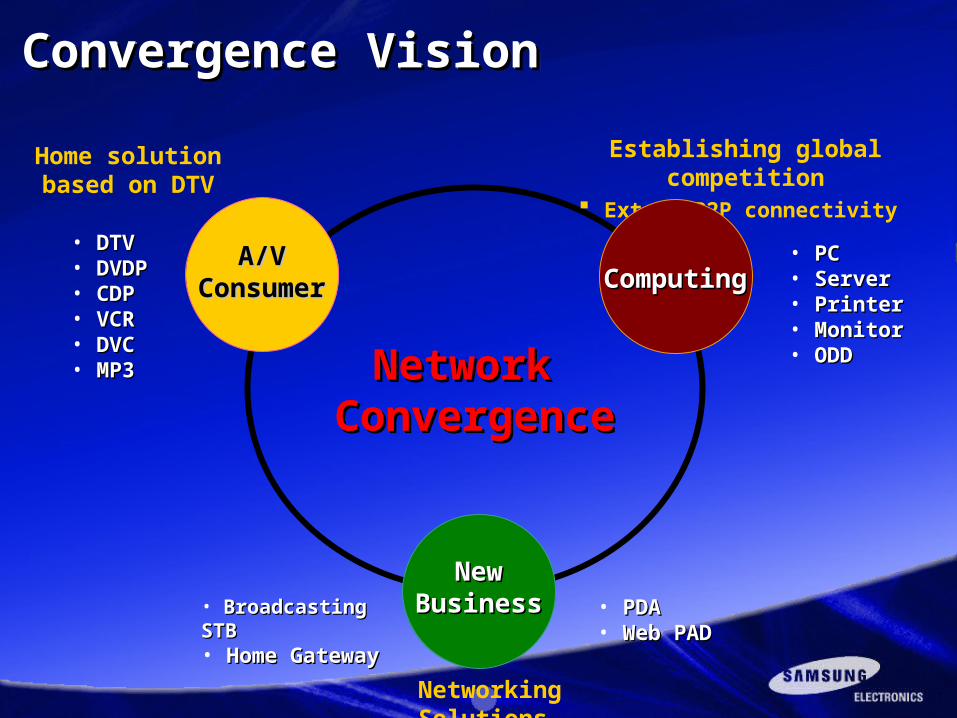

Network Network ConvergenceConvergence

• BBroadcasting STBroadcasting STB• Home GatewayHome Gateway

• PDAPDA• Web PAD Web PAD

NewNewBusinessBusiness

Networking Solutions

Establishing global competition Extend P2P connectivity

• PCPC• ServerServer• PrinterPrinter• MonitorMonitor• ODDODD

ComputingComputing

Home solution based on DTV

A/VA/VConsumerConsumer

• DTVDTV• DVDPDVDP• CDPCDP• VCRVCR• DVCDVC• MP3MP3

Convergence VisionConvergence VisionConvergence VisionConvergence Vision

THANK YOUTHANK YOUTHANK YOUTHANK YOU