samatha project final 130510

TRANSCRIPT

INTRODUCTION

MEANING OF FUNDS:

The term “funds” has a variety of meanings. There are people who take it

synonymous to cash and to them there is no difference between a funds flow statement

and cash flow statement while other include marketable securities besides cash in the

definition of the term “funds”. The International Accounting Standard No. 7 on

‘statement of changes in financial position’ also recognizes the absence of a single

generally accepted definition of the term According to the standard, the term fund

generally refers to cash, cash to cash equivalents, or to working capital. Of these, the

last definition of the term is by far the most common definition of fund.

There are also two concept gross working capital refers to the firm’s investment in

current assets while the term net working capital means excess of current assets over

current liabilities. It is in the latter sense in which the term funds is generally used.

The meaning of the two terms current assets and current liabilities have already

been explained. However, for the sake of ready reference, we are giving the below

meaning of these two terms current assets and current liabilities, besides explaining non-

current assets and non-current liabilities

CURRENT ASSETS:

The term current assets include assets, which are acquired with the intention of

converting them during the normal business operations of the company. However, the

best definition of the terms current assets has been given by Grady in the following

words for accounting purposes, the term current assets is used to designate cash and

other assets or resources commonly identified as those which are reasonable expected to

be realized in cash or sold or consumed during the normal operating cycle of the

business.

The broad categories of current assets, therefore, are

1) Cash including fixed deposits with banks

0

2) Accounts receivable, i.e trade debtors and bills receivable

3) Inventory i.e., customs, port authorities, advance income tax, etc.,

4) Advances recoverable i.e., the advances given to supplier of goods and services or

deposit with government or other public authorities, e.g., customs, port authorities,

advance income tax etc.,

5) Pre-paid expenses i.e., cost of unexpired services, e.g., insurance premium paid in

advance, etc.,

According to the companies at regarding presentation of financial statement

where investments even though held temporarily are to be shown separately

from current assets.

CURRENT LIABILITIES:

The term current liabilities is used practically such obligation whose liquidation is

reasonably expected to require the use of assets classified as current assets in the same

balance sheet or the creation of other current liabilities or those expected to be satisfied

within a relatively short period of time usually one year.

The more modern version designates current liabilities as all obligations that will require

within the coming year or the operating cycle whichever is longer

(1) The use of existing current assets or

(2) The creation of other current liabilities

In other words, the mere fact that an amount is due within a year does not make it

a current liability unless it is payable out of existing current assets or by creation of

current liabilities.

The term current liabilities also includes amounts set a part or provided for any

known liability of which the amount cannot be determined with sub-stantial accuracy e.g.,

provision for taxation, pension etc., these liabilities are technically called provision rather

than liabilities. The broad categories of current liabilities are:

1

(1) Accounts payable e.g., bills payable and trade creditors.

(2) Outstanding expenses i.e., expenses for which services have been received by the

business but for which the payment has not been made.

(3) Short-term loans i.e., loans from banks, etc, which are payable within one year

from the date of balance sheet.

(4) Advance payments received by the business for the services to be rendered or goods to be

supplied in future.

Provisions against current assets. Provisions against current assets such as provision

for doubtful debts, provision for loss of stock, provision for discount on debtors

etc., are treated as current liabilities, since they reduce the amount of current

assets.

NON-CURRENT ASSETS:

All assets other than current assets come within the category of non-current

assets. Such assets include goodwill, land, building, balance of the profit and loss

account, discount on issue of share and debentures, preliminary expenses, etc.,

NON-CURRENT LIABILITIES:

All liabilities come within the category of non-current liabilities. They include

shares capital, long-term loans, debentures, share premium, credit balance in the

profit and loss account, revenue and capital reserves (e.g., general reserve, dividend

equalization fund, debentures sinking fund, capital redemption reserve) etc.

The basic financial statements i.e., the balance sheet and profit and loss

account or income statement of business, reveal the net effect of the various

transaction on the operational and financial position of the company. The balance

sheet gives a summary of the assets and liabilities of an undertaking at a

particular point of time. The assets side of a balance sheet show the deployment.

2

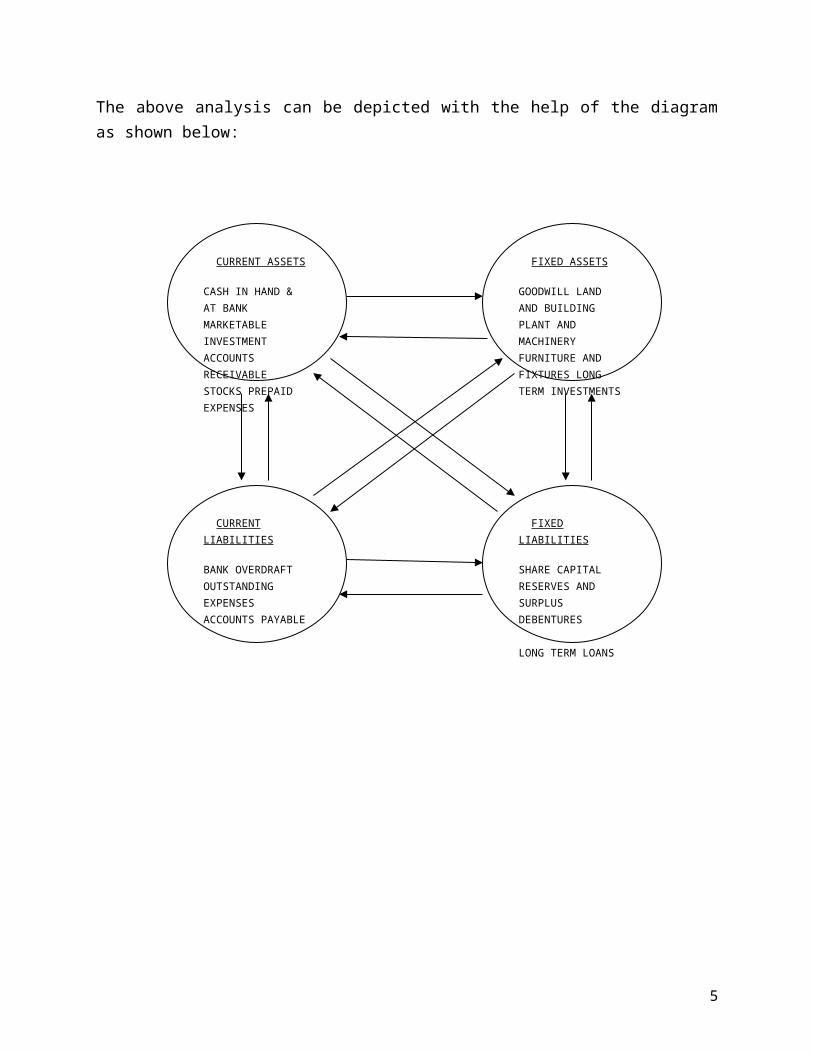

The above analysis can be depicted with the help of the diagram as shown below:

3

CURRENT ASSETS

CASH IN HAND & AT BANK MARKETABLE INVESTMENT ACCOUNTS RECEIVABLE STOCKS PREPAID EXPENSES

FIXED ASSETS

GOODWILL LAND AND BUILDING PLANT AND MACHINERY FURNITURE AND FIXTURES LONG TERM INVESTMENTS

CURRENT LIABILITIES

BANK OVERDRAFT OUTSTANDING EXPENSES ACCOUNTS PAYABLE

FIXED LIABILITIES

SHARE CAPITAL RESERVES AND SURPLUS DEBENTURES LONG TERM LOANS

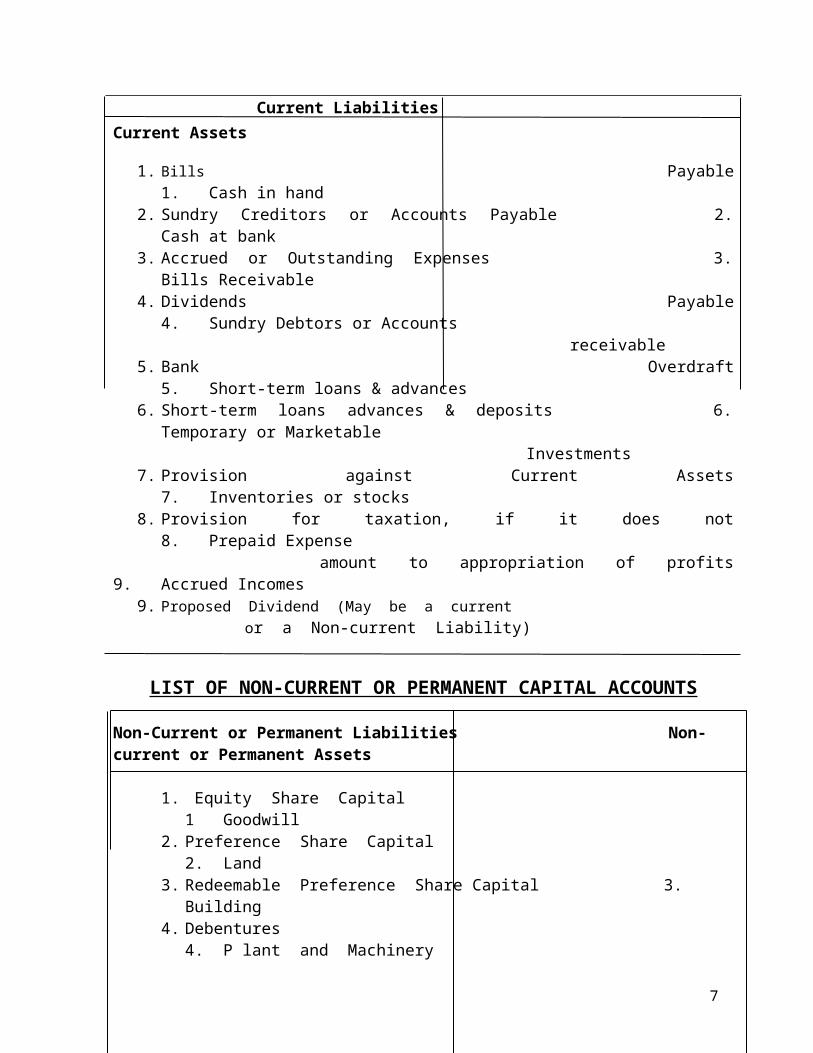

LIST OF CURRENT OR WORKING CAPITAL ACCOUNTS

Current Liabilities Current Assets

1. Bills Payable 1. Cash in hand2. Sundry Creditors or Accounts Payable 2. Cash at bank3. Accrued or Outstanding Expenses 3. Bills Receivable4. Dividends Payable 4. Sundry Debtors or Accounts

receivable5. Bank Overdraft 5. Short-term loans & advances6. Short-term loans advances & deposits 6. Temporary or Marketable

Investments7. Provision against Current Assets 7. Inventories or stocks 8. Provision for taxation, if it does not 8. Prepaid Expense

amount to appropriation of profits 9. Accrued Incomes9. Proposed Dividend (May be a current

or a Non-current Liability)

LIST OF NON-CURRENT OR PERMANENT CAPITAL ACCOUNTS

Non-Current or Permanent Liabilities Non-current or Permanent Assets

1. Equity Share Capital 1 Goodwill2. Preference Share Capital 2. Land 3. Redeemable Preference Share Capital 3. Building 4. Debentures 4. P lant and Machinery 5. Long-term Loans 5. Furniture and Fittings6. Share Premium Account 6. Trade Marks 7. Share Forfeited Account 7. Patent Rights8. Profit and Loss Account (Balance of 8. Long-Term investment

Profit, i.e., credit balance)9. Capital Reserve 9. Debit balance of Profit and Loss

Account10. Capital redemption Reserve 10. Discount on Issue of Shares 11. Provosion for depreciation against 11. Discount on Issue of Debentures

fixed assets12. Appropriation of Profits: 12. Preliminary Expensesa) General Reserve 13. Other Deferred Expensesb) Dividend Equalization Fundc) Insurance Fundd) Compensation Funde) Sinkingstmen Fundf) Invet Fluctuation Fundg) Provision for Taxationh) Proposed Dividend

4

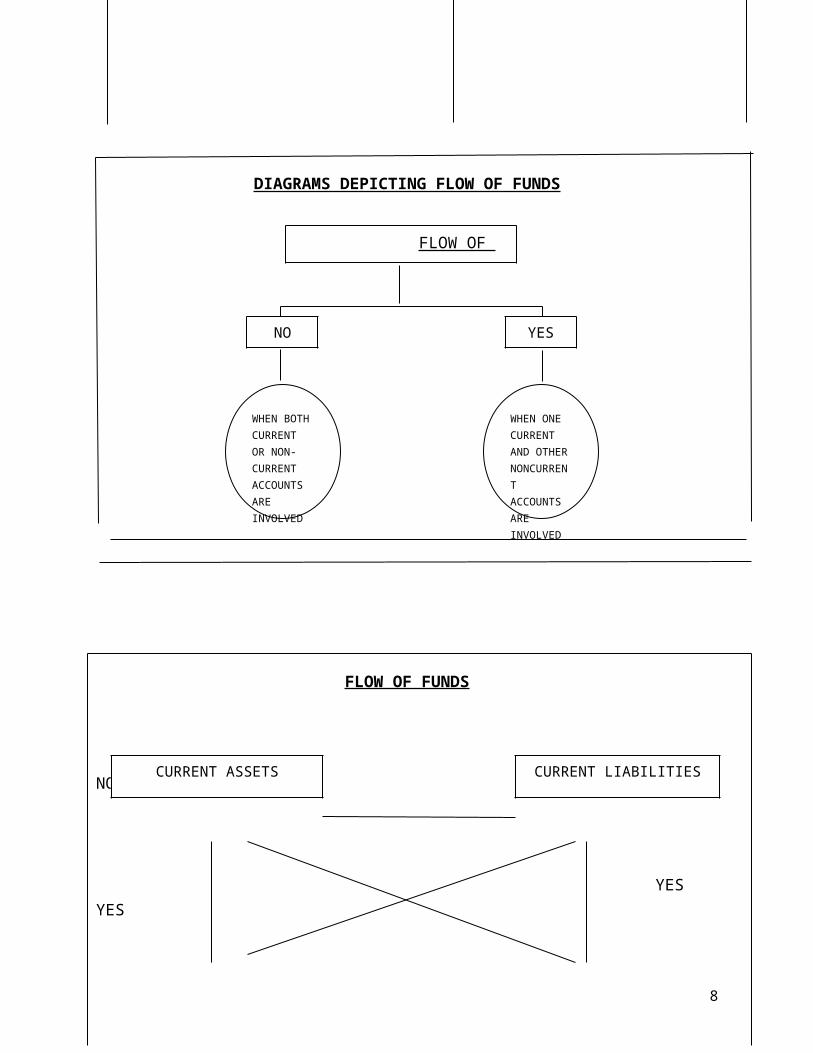

DIAGRAMS DEPICTING FLOW OF FUNDS

FLOW OF FUNDS

NO

YES YES

YES YES

NO

5

FLOW OF FUNDS

NO YES

WHEN BOTH CURRENT OR NON-CURRENT ACCOUNTS ARE INVOLVED

WHEN ONE CURRENT AND OTHER NONCURRENT ACCOUNTS ARE INVOLVED

CURRENT ASSETS CURRENT LIABILITIES

NON-CURRENT ASSETS NON-CURRENT LIABILITIES

IMPORTANCE OF FUNDS:

Funds flow statement helps the financial analyst in having a more detailed analysis

and understanding of changes in the distribution of resources between two balance sheet

dates. In case such study is required regarding the future working capital position of the

company, a projected funds flow statement can be prepared. The uses of a funds flow

statement can be put as follows.

1) It explains the financial consequences of business operations – Funds flow

statement provides a ready answer to so many conflicting situations, such as:

a. Why the liquid position of the business is becoming more and more

unbalanced in spite of business making more and more profits?

b. How was it possible to distribute dividends in excess of current earnings

or in the presence of a net loss for the period?

c. How the business could have good liquid position inspite of business

making losses or acquisition of fixed assets?

d. Where have the profits gone?

Definite answers to these questions will help the financial analyst in

advising his employer/client regarding directing of funds to those

channels which will be most profitable for the business.

2) It answers intricate queries – The financial analyst can find out answer to a

a. What is the overall credit-worthiness of the enterprise?

b. What are the sources of repayments of the loans taken?

c. How much funds are generated through normal business operations?

d. In what way the management has utilized the funds in the past and

what are going to be likely used of funds?

6

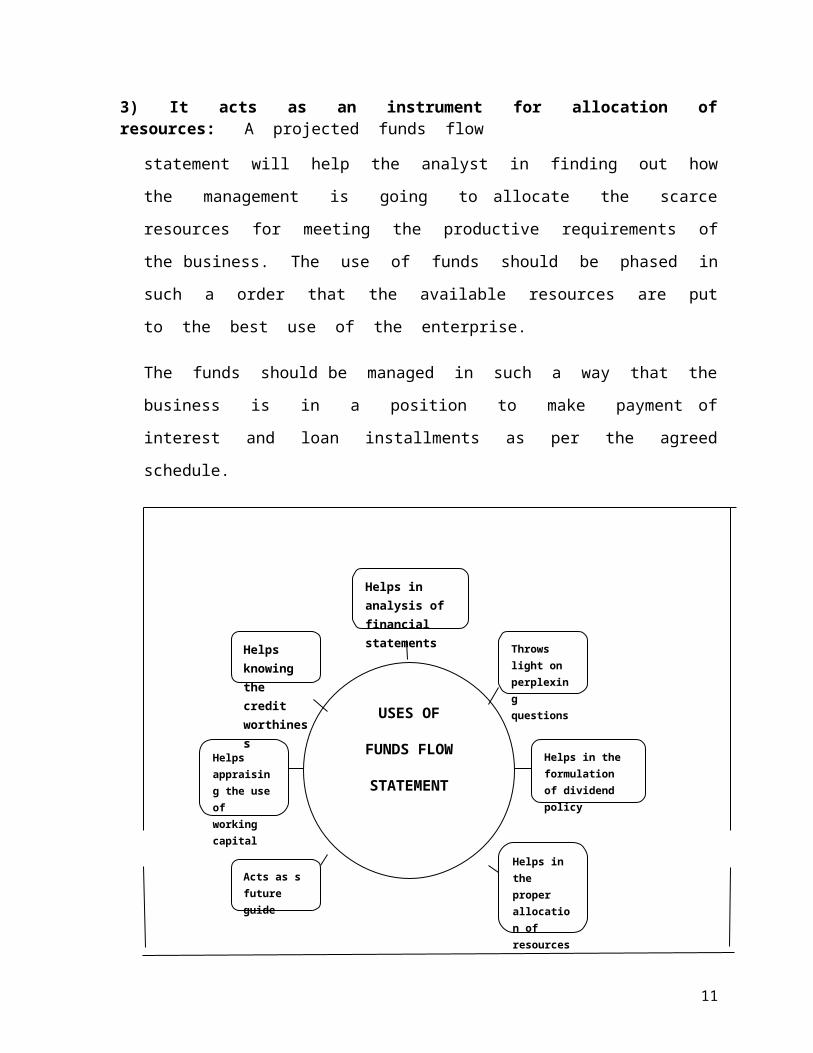

3) It acts as an instrument for allocation of resources: A projected funds flow

statement will help the analyst in finding out how the management is going to

allocate the scarce resources for meeting the productive requirements of the

business. The use of funds should be phased in such a order that the available

resources are put to the best use of the enterprise.

The funds should be managed in such a way that the business is in a position to

make payment of interest and loan installments as per the agreed schedule.

7

USES OF

FUNDS FLOW

STATEMENT

Helps in analysis of financial statements

Throws light on perplexing questions

Helps in the formulation of dividend policy

Helps in the proper allocation of resources

Acts as s future guide

Helps appraising the use of working capital

Helps knowing the credit worthiness

SOURCES OF FUNDS:

The sources of funds can be both internal as well as external.

Internal sources: Funds from operations is the only internal source of funds. However,

following adjustments will be required in the figure of Net Profit for finding out real

funds from operations:

Add the following items as they do not result in outflow of funds:

1) Depreciation on fixed assets.

2) Preliminary expenses or goodwill etc. written off.

3) Contribution to debenture redemption fund, transfer to general reserve etc., if they

have been deducted before arriving at the figure of net profit.

4) Provision for taxation and proposed dividend are usually taken as appropriations

of profits only and not current liabilities for the purposes of Funds Flow

Statement. This is being discussed in detail later.

Non-operating incomes such as dividend received or accrued dividend, refund of

income tax, rent received or accrued rent. These items increase funds but they are non-

operating incomes. They will be shown under separate heads as “sources of funds” in the

Funds Flow Statement.

In case the Profit and Loss Account shows ‘Net Loss’ this should be taken as an

item which decreases the funds.

8

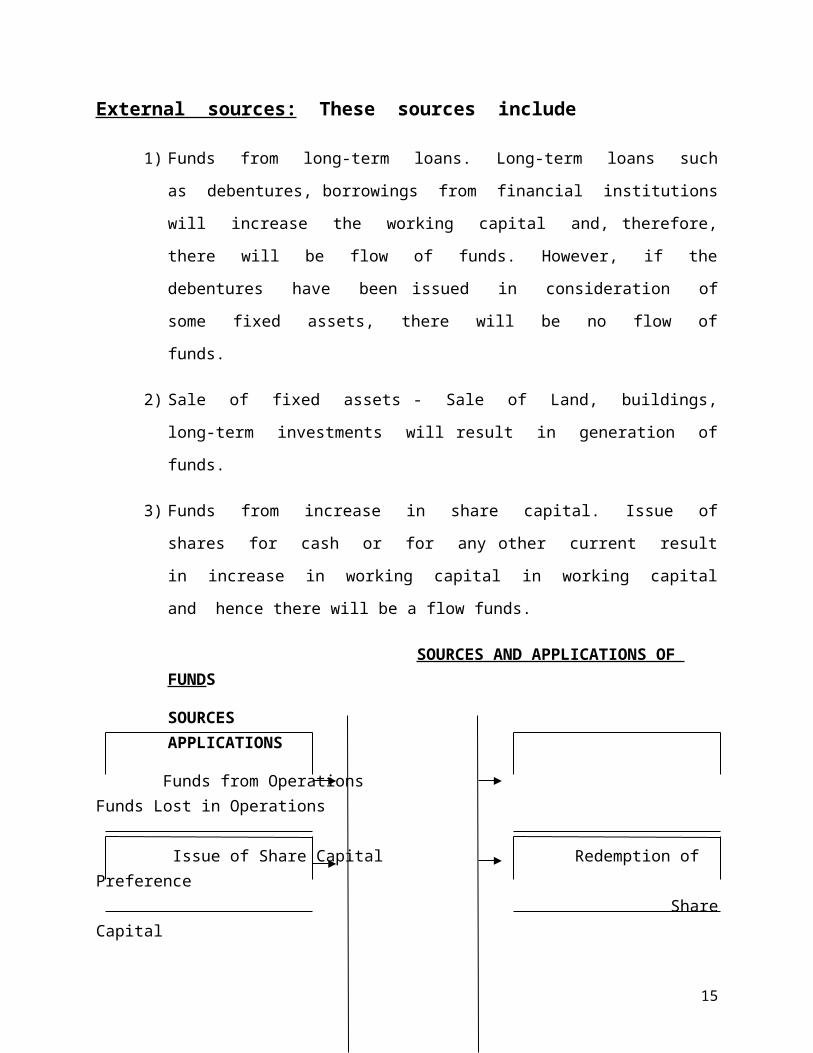

External sources: These sources include

1) Funds from long-term loans. Long-term loans such as debentures, borrowings

from financial institutions will increase the working capital and, therefore, there

will be flow of funds. However, if the debentures have been issued in

consideration of some fixed assets, there will be no flow of funds.

2) Sale of fixed assets - Sale of Land, buildings, long-term investments will result

in generation of funds.

3) Funds from increase in share capital. Issue of shares for cash or for any other

current result in increase in working capital in working capital and hence there

will be a flow funds.

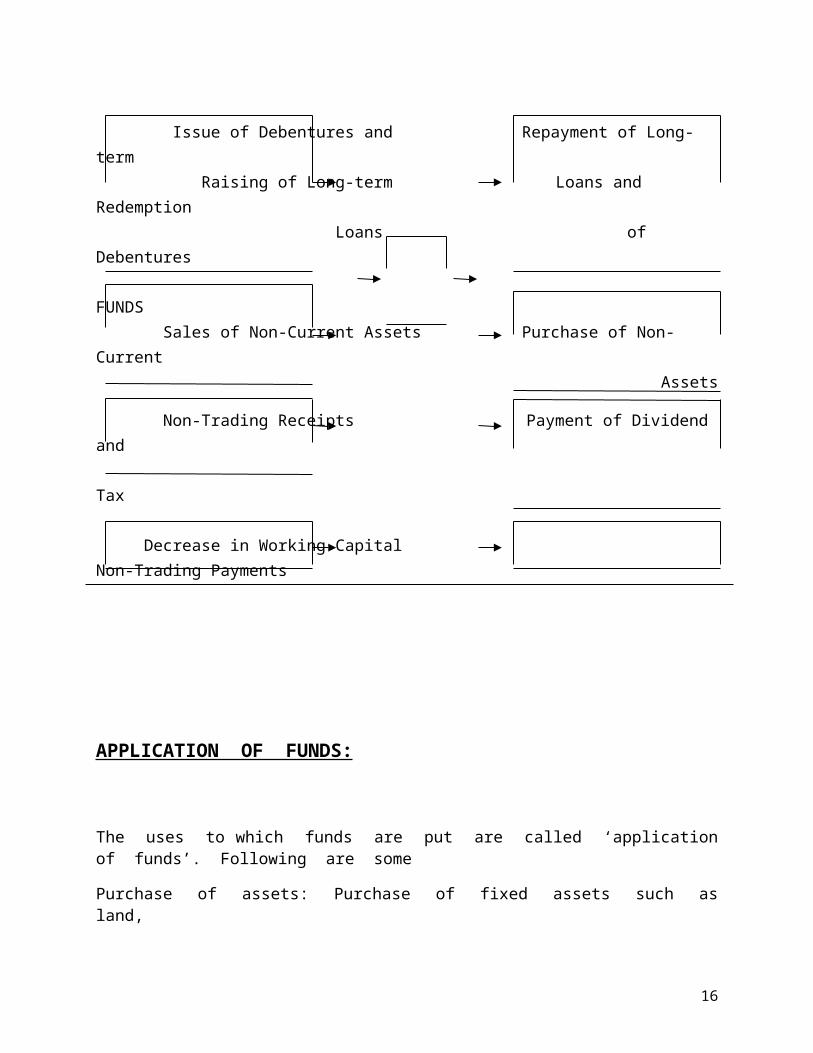

SOURCES AND APPLICATIONS OF FUNDS

SOURCES APPLICATIONS

Funds from Operations Funds Lost in Operations

Issue of Share Capital Redemption of Preference Share Capital Issue of Debentures and Repayment of Long-term Raising of Long-term Loans and Redemption Loans of Debentures FUNDS Sales of Non-Current Assets Purchase of Non-Current

Assets

Non-Trading Receipts Payment of Dividend and Tax

Decrease in Working Capital Non-Trading Payments

9

APPLICATION OF FUNDS:

The uses to which funds are put are called ‘application of funds’. Following are some

Purchase of assets: Purchase of fixed assets such as land,

i. of the purposes for which funds may be used: building, plant, machinery, long-

term investments etc., results in decrease of current assets without any decrease in

current liabilities. Hence, there will be a flow of funds. But in case shares or

debentures are issued for acquisition of fixed assets, there will be flow of funds.

ii. Payment of dividends: Payment of dividends results in decrease of a fixed liability

and therefore, it affects funds. Generally recommendations of directions regarding

declaration of dividend (i.e., proposed dividends) is simply taken as an

appropriation of profits and not as an items affecting the working capital. This

has been explained in detail later.

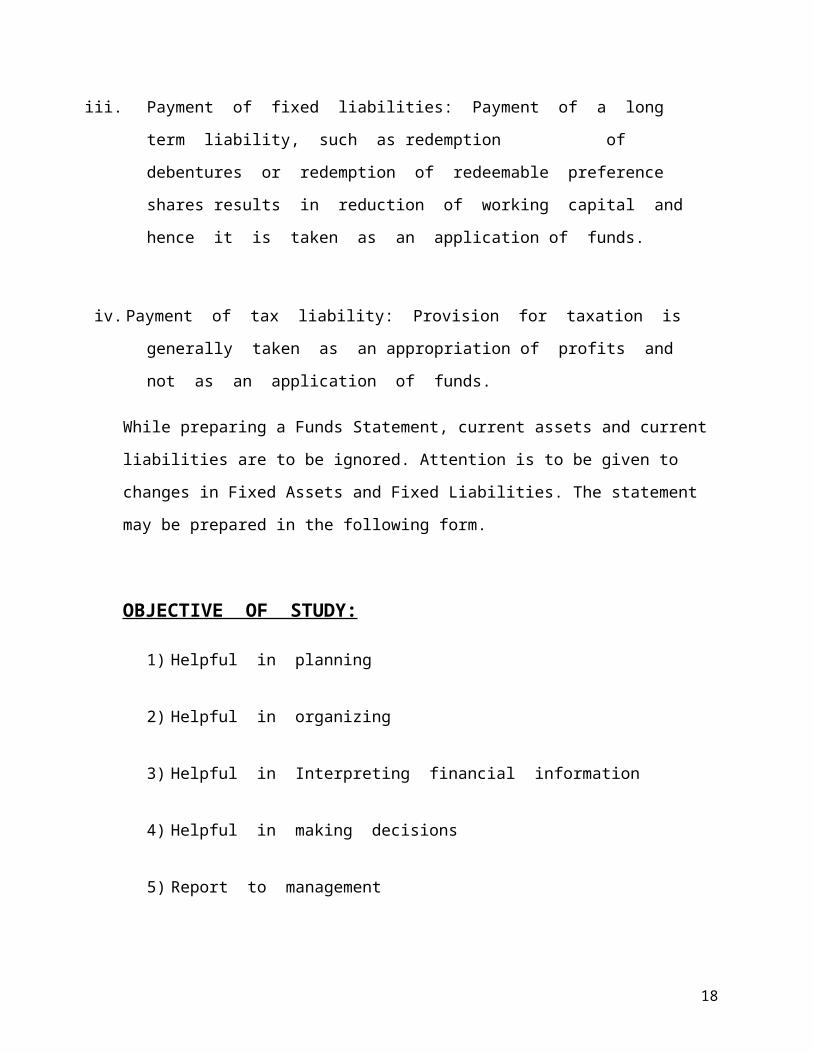

iii. Payment of fixed liabilities: Payment of a long term liability, such as redemption

of debentures or redemption of redeemable preference shares results in reduction

of working capital and hence it is taken as an application of funds.

10

FUNDS

Issue of Shares

Sale of Fixed Assets

Payment of Long

Term Loans

Operational Loss

Payment of Tax/Dividend

Operational Profit

Long Term Borrowings

Redemption of

Pref. Shares

Purchase of

Fixed Assets

iv. Payment of tax liability: Provision for taxation is generally taken as an appropriation

of profits and not as an application of funds.

While preparing a Funds Statement, current assets and current liabilities are to be ignored.

Attention is to be given to changes in Fixed Assets and Fixed Liabilities. The statement may

be prepared in the following form.

OBJECTIVE OF STUDY:

1) Helpful in planning

2) Helpful in organizing

3) Helpful in Interpreting financial information

4) Helpful in making decisions

5) Report to management

11

RESEARCH METHODOLOGY

For the purpose of study 5 years data has been collected from 31-03-2004 to

31-03-2009

1) The data is collected through annual reports i.e the secondary data

2) The collected data has been tabulated and interpreted by using techniques

ration analysis

3) At end meaningful inferences are drawn to reflect the sources and

application of funds of APTDCL and suitable suggestions are offered for

improving the efficiency of working capital sources and application of

APTDCL.

PERIOD & SCOPE OF THE STUDY :

For purpose of study of 5 year data has been collected from 2004 to 2009.

As the data collected is secondary data the study is limited for sources and

application of funds.

12

INTRODUCTION TO APTDC

Introduction:

Tourism was declared as an industry in the state as far back as 1986, duly extending

benefits and concessions to investors. In 1994, special tourist centers were notified and an

incentive subsidy, tax concessions and electricity rebates were offered. The state tourism policy

was document and released in 1994. Despite all this, not too much progress has been made in

attracting tourists and investors. This could be attributed mainly to low initial development,

failure of the state to address the critical areas of kick – starting the tourism development in the

state and poor marketing strategies to attract tourists and potential investors.

The travel and tourism industry is well on its way to becoming one of the most powerful

growth engines in the coming millennium. The govt of Andhra Pradesh is focusing on tourism

for generating greater employment and achieving higher economic growth.

Tourism has a vision of making Andhra Pradesh the destination state of India, given its

attractive diversity, natural endowments and friendly population. Andhra Pradesh has a rich

tourist potential, which is yet to be exploited. “Bring the world to Andhra Pradesh, take Andhra

Pradesh to the world” is the tourism of Andhra Pradesh guiding spirit.

Andhra Pradesh has great potential for tourism with its temple towns, beach resorts,

monuments and other tourist attractions.

About APTDC Ltd:

The Corporation was incorporated during the year 1976 as subsidiary to Andhra Pradesh

State Road Transport Corporation Limited in the name of Travel and Tourism Development

Corporation PVT Ltd with an authorized and paid up share capital of Rs. 100 lakhs and 13 lakhs

respectively. The company became a wholly owned government company in March 1980. The

13

authorized and paid up share capital of the company is Rs. 750 lakhs and 376.12 lakhs

respectively. The name of the company has been changed to Andhra Pradesh Tourism

Development Corporation Limited during the month of October 2000. Now the authorized share

capital of company is Rs.1000 lakhs.

Over the past 4 years, APTDC has added an array of function to its lists of tasks, with a

determination to show commendable performance. From just providing information to tourists, it

has gone into serious business like accommodation, catering and such other services that have

become essential for ensuring tourist infrastructure and service.

The turnover of the corporation in 1998 – 99 was Rs. 328 lakhs and this went on to

become a whopping Rs. 2004 lakhs at the end of the financial year 2001 – 2002, a turn around

that no other tourism corporation in the country would have ever achieved in such a short time.

Keeping this performance in view, the corporation has reset its goal to maintain the tempo and

meet the ever–increasing challenges posed by such rapid development and resultant expectations.

Objective:

The main objective of the company is to develop tourism in the state providing adequate

infrastructure to maintain and sustain tourist interest. Its aim is to take over, develop and manage

the guesthouses, resorts and tourist interest sites for the benefit of the tourists. To run, establish

and manage transport unit and operate tourist buses, cars, coaches and other modes of transport.

Administrative set – up:

The entire administration of APTDC has been reorganized to give it a more effective and

efficient face, matching and expansion of activities. Training of the staff at all levels has been

made a continuous process. At the corporate office overall supervision of activities has been

entrusted to senior officials who report directly to Chairman and Managing Director.

14

Projects & Administration – headed by an Executive Director.

Transport & Conducted tours wing – headed by General Manager (Tours).

Finance wing - headed by a General Manager.

Accommodation and catering wing - headed by two General Managers (Hotels).

Water fleet and Sound & Light shows - headed by a Dy. General Manager.

Legal wing - headed by a Legal Advisor.

Public relations wing – headed by a Manager.

Board of Directors:Board of Directors Designation

Sri. J. Raymond Peter, IAS Chairman & Managing Director

Sri. V. Venkata Rami Reddy Executive Director

Sri. V. Nagi Reddy, IAS Director

Secretary to govt. YAT

Sri. T.S. Appa Rao, IAS Director

Principle secretary (R&E),

Finance department, govt of A.P.

Sri. Y. V. Venkata Naidu Director

Sri. K. Venkateshwara Rao Director

Sri. Vijaya Bhaskar Reddy Director

Vijay Mohan Raj Director

Chairman, travel agents association

Of India Andhra Pradesh Chapter.

Rajiv Narain Director

President, Hotel & Restaurant

Association of A.P.

Activities of Organization:

15

The main activities of the corporation are:

1. Conducted & Package Tours.

2. Accommodation and catering services.

3. Leisure Cruises and Pleasure Boating.

4. Water fleet operations.

5. Sound and Light shows.

6. Eco – Tourism.

7. Adventure Tourism.

8. New Projects Implementation.

1. Conducted and Packaged Tours:

APTDC has given high priority to the second most important

aspect in tourism development, providing

convenient conducted tours. Major expansion and revamping of the transport wing of the

corporation over the past three years have given a major thrust in this area.

At present 63 hi – tech coaches, 29 world famous Volvo

coaches, 8 air conditioned hi – tech coaches, 4 semi –

sleepers, 11 mini vehicles, 1 vintage coach and 10 Qualis

are being operated for conducted & packaged tours from

8 centers of Andhra Pradesh. As many as 54 tour circuits

covered by the corporation encompass all major pilgrim

centers, nature spots, leisure places, hills & valleys in Andhra Pradesh.

a. Other State Package Tour:

16

The tour starting from other than Andhra Pradesh districts comes under other state

packaged tours. The visitors from other states come to different destinations in Andhra Pradesh.

Most of this tour is provided with accommodation.

b. Charted Services:

APTDC can plan & organize leisure time activities for groups, both corporate and

individual. For instance, employees from companies, institutions or those attending as delegates

(and their spouse) at various conferences, boat rides on the launches, and even exclusive dinner

parties on the boat can be arranged.

2. Accommodation and Catering Services:

An important ingredient for development of tourism is provision

of comfortable accommodation for all categories of tourists. With

this in view, the corporation has refurbished its existing

accommodation and have established new hotels/resorts/wayside

amenities at all tourist/pilgrim spots of the state.

Facilities such as swimming pool, conference hall and fitness centre have been created at

many of its hotels and resorts. As of May 2004, there are APTDC’s Punnami

hotels and resorts at 27 locations with a total of 861 rooms and a bad strength of 1910. Revenue

from hotels and catering units has increased from Rs. 361 lakhs in 2000 – 01 to Rs. 1148 lakhs in

2004.

Facilities at Punnami Hotels:

All the hotels/resorts have modern amenities.

Most of the rooms are air – conditioned

Television/telephone in all rooms.

Restaurant, vegetarian in pilgrim centers and multicuisine in others.

Bars in all except in pilgrim centers

Many hotels and resorts have other facilities like fitness centre, swimming pool, souvenir

shop, children play area.

17

Moderately priced.

Professionally managed.

APTDC has its Punnami hotels/resorts at:

Amaravati - Kuppam Resort

Araku Valley resort - Kurnool

Badrachalam - Mahanandi

Basara - Nagarjuna Sagar

Belum Caves - Puttur

Berm Park - Rushikonda

Bhavani Island - Srisailam

Dwaraka Tirumala - Dornala

Ettipotala - Tyda

Horsley Hills, hill resort - Vijayawada

Hyderabad, taramati - Vishakapatnam

Kailasanatha Resort - Warangal

Kesaragutta - Yadagirigutta

18

3. Leisure Cruises and Pleasure Boating:

APTDC has made effective use of rivers and lakes at important places in the state by

strengthening its water fleet and providing pleasure boating and leisure cruise facilities. A

beginning was made with commissioning of two luxury cruises “Bhageerathi” and “Bhagmati”

in the Hussainsagar Lake in Hyderabad.

Apart from strengthening the water fleet at Hussainsagar, Mir Alam Tank and Durgam

Cheruvu in Hyderabad, the corporation has provided shantisri luxury cruiser at Nagarjunasagar

on Krishna River and other mechanized boats that are of great attractions among tourists such as

Agastya, Krishna and Vijayalakshmi. Zaria launch and Chitrangi boat are provided at

Rajahmundry, Vijayasiri twin-deck at Vijayawada.Other boating

units are located at - lower manair at Karimnagar, Nellore tank, Mylaravaram at Kadapa,

Rushikonda beach at Vishakapatnam.

5. Adventure Tourism:

Adventure tourism is at Srisailam, Hyderabad and Vijayawada. Recognizing adventure

tourism as a part of eco-tourism promotion with immense but untapped potential, the corporation

has introduced Parasailing on the inland surface waters of Hussainsagar. To begin with,

consultants are commissioned to explore the possibilities of adventure activities like trekking and

rappelling in the forest tracks of Nallamala and Araku circuits and the scheme will be

commercially launched.

19

6. New Projects under Implementation:

Paryatak Bhavan:

The project work is under progress with the investment of Rs.22 crores, which has been

funded, by the Government of India (GOI) with Rs.500 lakhs, Government of Andhra Pradesh

(GOAP) with Rs.220 lakhs and APTDC/loan Rs.1480 lakhs.

Components of project are:

Reservation counters

Offices for tour operators, hoteliers, travel agents

Central reservation office

Banking

Retail areas

Food courts

Other state tourism offices

Cellar parking for 150 vehicles

Three star hotel

The total build-up area is planned at 1, 30,000 sq.ft. With parking facility for 150 vehicles.

National institute For Tourism & Hospitality Management:

20

Located in Hyderabad with built up area of 3,50,000 s.ft facilitated by administration

block, classroom, lecture hall, laboratories & faculty rooms, library, conference hall &

auditorium, snack bars, medical center, bank, post office, sports room kitchen, dinning rooms &

toilets, hostels & faculty housing. The cost of the project is 20

crores, which includes GOI –Rs. 220 lakhs, GOAP- Rs.228 lakhs, APTDC - Rs.1552 lakhs. The

work is in progress.

Bhavani Island River Resort:

A large island (133 acres) in the river Krishna at Vijayawada is under construction with

an investment of Rs. 220 lakhs and entrance plaza with an investment of Rs.100 lakh. This island

includes 24 cottages, restaurants and a conference hall.

Anantagiri Resorts:

A resort at 4000’ elevation at Anantagiri, Araku, with facilities of 18 cottages,

restaurants, entrance lobby, recreation center, lounge, bar, etc. cost of the project is Rs.200 lakhs.

Konaseema River Project:

21

The backwaters of Vasista and Vynateya are being tapped for houseboat cruises and rural

tourism. Project cost is Rs.135 lakhs,

K. Vijaya Bhaskar Reddy memorial park at Kurnool, project cost: Rs.260 lakhs.

Para ballooning project, at Durgam Cheruvu.

Oravakallu Rock Park situated 21 km from kurnool on NH 18. Project cost: Rs.54 lakhs.

Tourist complex, Bhadrachalam, project cost: Rs.300 lakhs.

Suryalanka beach resort, Bapatla, Guntur dist. Project cost: Rs.100 lakhs

Infrastructure at Tirupati visitor’s zone, Tirupati.

Bapu ghat, Hyderabad. Project cost: Rs.500 lakhs.

Tourist facilities at Kuppam wildlife sanctuary. Project cost: Rs.20.5 lakhs.

Heritage Projects under Implementation:

Sriparvara arama - a Buddhist theme Park at Nagarjunasagar:

A unique theme park on the “life and preachings of Gautama Buddha, life of Acharya

Nagarjuna and Ikshvaku Dynasty”. Components of the project are: entrance plaza, parking areas,

visitor’s amenities, entrance arches & lotus pond, replicas of stupas from different countries.

Project cost is Rs.875 lakhs.

Amaravati Interpretation Center:

The center display art and culture of Satavahana Dynasty. Project includes restaurants,

information center, and souvenir shop. Project cost is Rs.210 lakhs.

22

Proposed New Projects:

Tourist complex, Nellore. Project cost: Rs.100 lakhs.

Sound & light show at thousand-pillar temple, Warangal. Funds from ASI, New

Delhi.

Sea cruise between Visakhapatnam, Port blair & Chennai. Project cost: Rs.2000

lakhs.

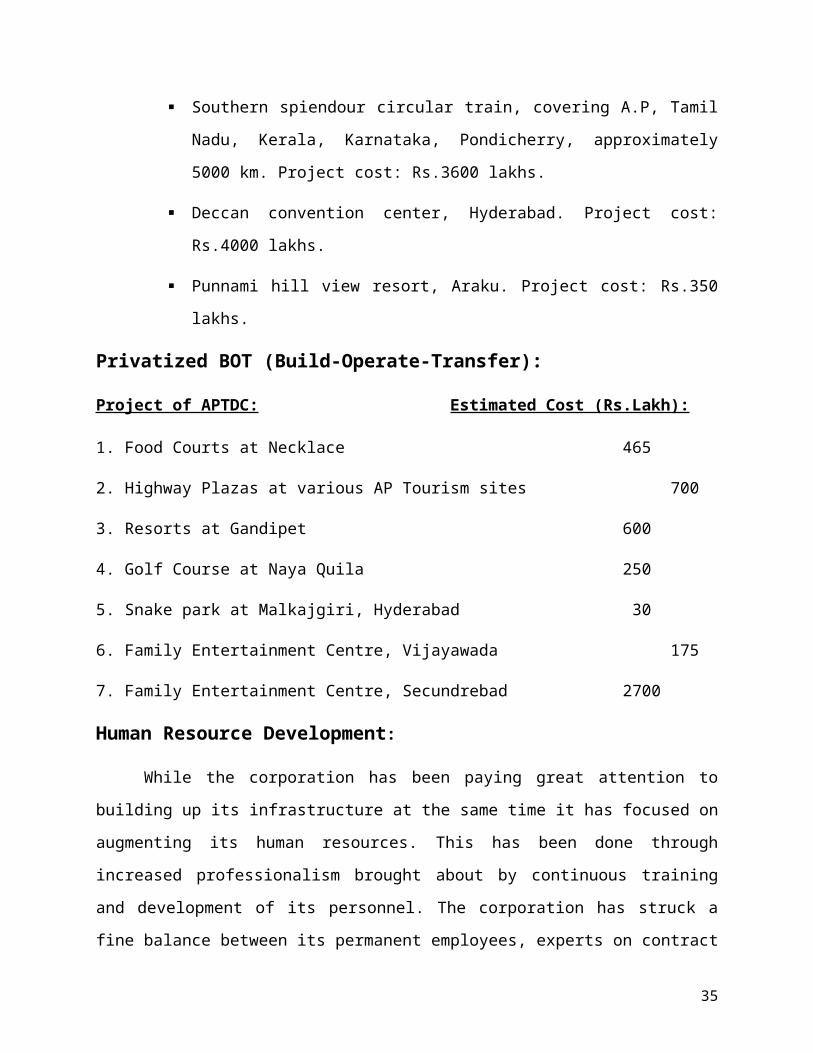

Southern spiendour circular train, covering A.P, Tamil Nadu, Kerala, Karnataka,

Pondicherry, approximately 5000 km. Project cost: Rs.3600 lakhs.

Deccan convention center, Hyderabad. Project cost: Rs.4000 lakhs.

Punnami hill view resort, Araku. Project cost: Rs.350 lakhs.

Privatized BOT (Build-Operate-Transfer):

Project of APTDC: Estimated Cost (Rs.Lakh):

1. Food Courts at Necklace 465

2. Highway Plazas at various AP Tourism sites 700

3. Resorts at Gandipet 600

4. Golf Course at Naya Quila 250

5. Snake park at Malkajgiri, Hyderabad 30

6. Family Entertainment Centre, Vijayawada 175

7. Family Entertainment Centre, Secundrebad 2700

Human Resource Development:

While the corporation has been paying great attention to building up its infrastructure at

the same time it has focused on augmenting its human resources. This has been done through

increased professionalism brought about by continuous training and development of its

personnel. The corporation has struck a fine balance between its permanent employees, experts

23

on contract and employees drawn from other relevant departments. This has prompted a creative

fusion of ideas resulting in the corporation’s spectacular performance with total employee

strength of 1548 as on May 2004. The corporation is highly streamlined with specialized cells

like legal, MIS, project material management, etc.

Accounting and Finance:

Revenues are generated at unit level and remitted into respective banks and transferred to

head office under intimation of controlling office [divisional management]. This is the setup

where operating funds are transferred to divisional office by corporate office on performance of

monthly revenue. In turn divisional office distributes operating funds to units for day-to-day

operation. All units’ officers also submit their expenditure particulars to controlling office and

proper accounts are build-up at divisional office. A monthly trial balance will be submitted to

head office for incorporation. In turn, corporation office consolidates profit & loss account and

balance sheet. Keeping in tune with the growth, several systems have been introduced in regard

to accounting and finance. A computerized accounting system was introduced in 1999. There are

daily collections at large number of points such as accommodation units, catering, water fleet,

Authorized agents, etc. Hence greater control on finance becomes essential. A full proof

coordination and feedback mechanism between the head office and the various units has been

established. Internal audit system has been strengthened

Audit and Accounts:

The audit of accounts has been completed up to 31.03.2005 and the audit of accounts is in

progress for the year 2005-2006. The annual accounts up to the year 2003 -2004 duly audited

and approved by the C&AG were adopted in the Annual General Meeting.

ORGANIZATION STRUCTURE OF A.P.T.D.C.L

AN OVERVIEW OF APTDCL:

24

The Corporation was incorporated during the year 1976 as subsidiary to Andhra

Pradesh State Road Transport Corporation Limited in the name of Travel and Tourism

Development Corporation Pvt. Ltd. with an Authorized and paid up Share capital of

Rs.100 Lakhs and Rs.13 Lakhs respectively. The company became a wholly owned

Government company in March 1980. The authorized and paid up share capital of the

company is Rs.1000.00 Lakhs and Rs.376.23 Lakhs respectively. The name of the

company has been changed to Andhra Pradesh Tourism Development Corporation Limited

during the month of October 2000. The main objective of the company is to develop

Tourism in the state providing adequate infrastructure to maintain and sustain Tourist

interest simultaneously triggering the growth of the economic activity of the region.

The main objective of the company is to take over develop and manage the guesthouses

and tourist interest sites for the benefits of the tourists. To run, establish and manage

transport unit and operate tourist buses cars, coaches and other modes of transport.

Following are the main activities of the corporation.

1. Package Tours

2. Accommodation and Catering Services

3. Water fleet operations

4. Sound and Light shows

5. Eco-Tourism

6. Lease and Privatization of schemes

PREAMBLE:

The entire administration of APTDC has been reorganized to give it a more effective and

efficient face, along with expansion of activities. Training of the staff at all levels has

25

been made a continuous process. At the corporate office overall supervision of activities

has been entrusted to senior officials who report directly to the Managing Director.

1. Projects & Finance – headed by an Executive Director

2. Administration & Leasing headed by Officer on Special Duty

3. Transport & Conducted Tours Wing – headed by General Manager

4. Accommodation and Catering wing headed by 2 General Manager each

5. Water fleet & Sound & Light shows headed by a General Manager

6. Legal wing headed by a Legal Advisor

7. Public Relations headed by Joint Manager.

ACTIVITIES OF ORGANIZATION:

Activities of the organization are divided into 7 divisional officers under their control

units are working. So all units are operated by unit officers and report to respective

divisional managers.

TRANSPORT FLEET:

To make travel hazel free and more comfortable APTDC has designed a number of

Tourist Packages to various destinations covering Temples, Hill Resorts, Beach Resorts,

Heritage sites, Caves both in outside the State through its modern transport fleet of 130

buses. Tours connect major places in the south such as Chennai, Bangalore, Salem,

Coimbatore, Mangalore, Goa, Shirdi.

HOTELS:Under this category the Corporation has built Hotels, Resorts, Wayside amenities,

Accommodation in Forests like Jungle Bells-Tyda, Talakona, Kailasanathkona, Hill resorts

like Horsely Hills and Ananthagiri near Vizag. Prestigious resorts in Hyderabad

26

TARAMATI BARADARI. Mostly all the resorts and Hotels are provided with BARS. In

all there are 54 hotels spread over the whole state with a room capacity of 1100 nos.

SOUND AND LIGHTING:

The sound and lighting show at the Golconda Fort, Hyderabad continues to draw large

groups of tourists every day and is rated one of the best son-et-lumieres in the country.

The sound and lighting show has been introduced at Chandragiri Fort, near Tirupathi, the

last capital of the mighty Vijayanagar kingdom.

WATER FLEET:

The Durgam Cheruvu, popularly know as the ‘Secret Lake’ located beyond Jubilee Hills

has been made into an attractive nature spot. The 63-acre lake and its surrounding land of 21

acres have been developed with wilderness landscaping, promenade for walkers, terraced

lawns for visitors and for parties. This lake has 60 feet water spot in the midst of the

lake and angling facilities are the other attractions. Large number of Water bodies in the

state have enabled APTDC to develop lake and river tourism in Andhra Pradesh. APTDC

has 118 boats of which 62 are mechanized and 46 are non-mechanized. Pleasure cruises

on Hussainsagar lake, River Godavari and Krishna are very popular.

FINANCIAL RESULTS:

Revenues are generated at unit levels and remitted into respective banks and transferred

to head office under intimation to controlling office [divisional management]. This is the

setup of operating funds transferred to divisional office by corporate office on generation

of monthly revenues, in turn divisional office distributes operating funds to units for day-

to-day operation. Keeping in tune with the growth, several systems have been introduced

in regard to accounting and finance. A computerized accounting system was introduced in

1999. There is a daily collection at large number of points such as accommodation units,

catering, water fleet, Authorized agents, etc. Hence greater control on finance becomes

essential.

27

AUDIT AND ACCOUNTS:

The Audit of Accounts has been completed up to 31.03.2008 and the Audit of Accounts

is in progress for the year 2008-2009.The Annual Accounts up to the year 2006-2007

duly audited and approved by the C&AG were adopted in the Annual General Meeting.

Audit of annual Accounts for the year 2006-07 has been completed and ready to be sent

to Accountant General.

ACCOUNTING:

All units’ officers submit their expenditure particulars to controlling office and proper

accounts are prepared at divisional office. A monthly trial balance will be submitted to

head office for incorporation. In turn, corporation office consolidates Profit and Loss

account and Balance Sheet. Keeping in tune with the growth, several systems have been

introduced in regard to accounting & finance.

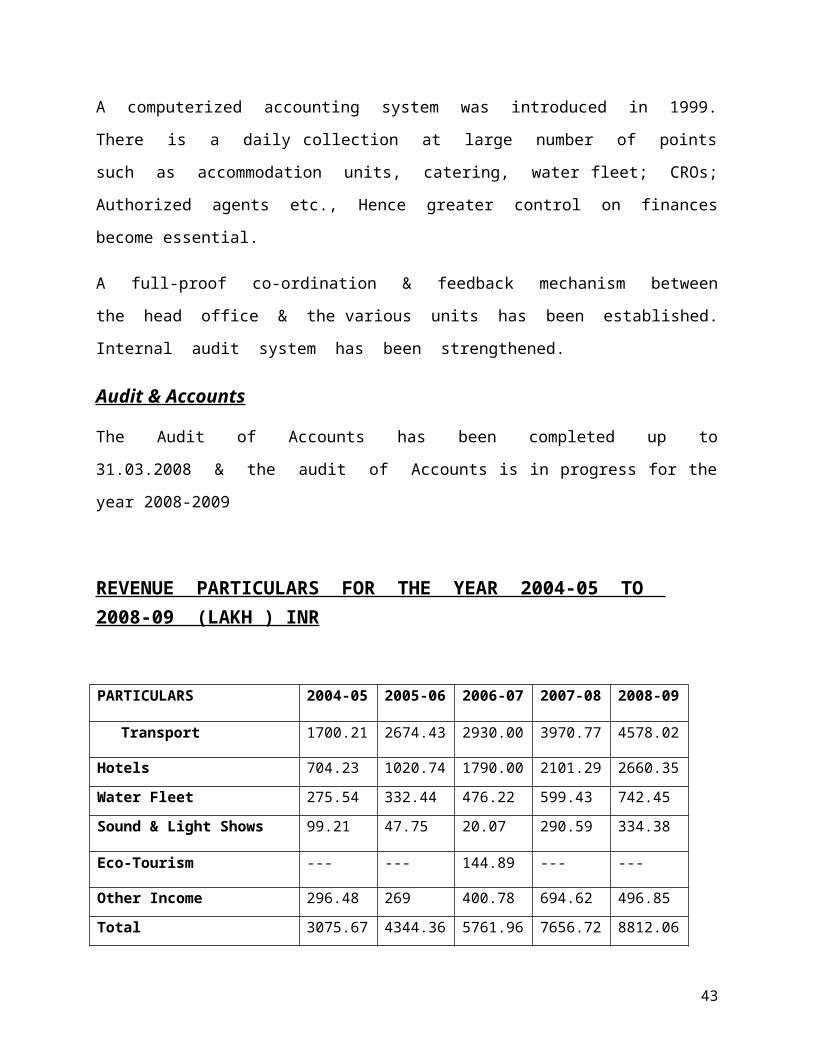

A computerized accounting system was introduced in 1999. There is a daily collection at

large number of points such as accommodation units, catering, water fleet; CROs;

Authorized agents etc., Hence greater control on finances become essential.

A full-proof co-ordination & feedback mechanism between the head office & the various

units has been established. Internal audit system has been strengthened.

Audit & Accounts

The Audit of Accounts has been completed up to 31.03.2008 & the audit of Accounts is

in progress for the year 2008-2009

REVENUE PARTICULARS FOR THE YEAR 2004-05 TO 2008-09 (LAKH ) INR

PARTICULARS 2004-05 2005-06 2006-07 2007-08 2008-09

28

Transport 1700.21 2674.43 2930.00 3970.77 4578.02

Hotels 704.23 1020.74 1790.00 2101.29 2660.35

Water Fleet 275.54 332.44 476.22 599.43 742.45

Sound & Light Shows 99.21 47.75 20.07 290.59 334.38

Eco-Tourism --- --- 144.89 --- ---

Other Income 296.48 269 400.78 694.62 496.85

Total 3075.67 4344.36 5761.96 7656.72 8812.06

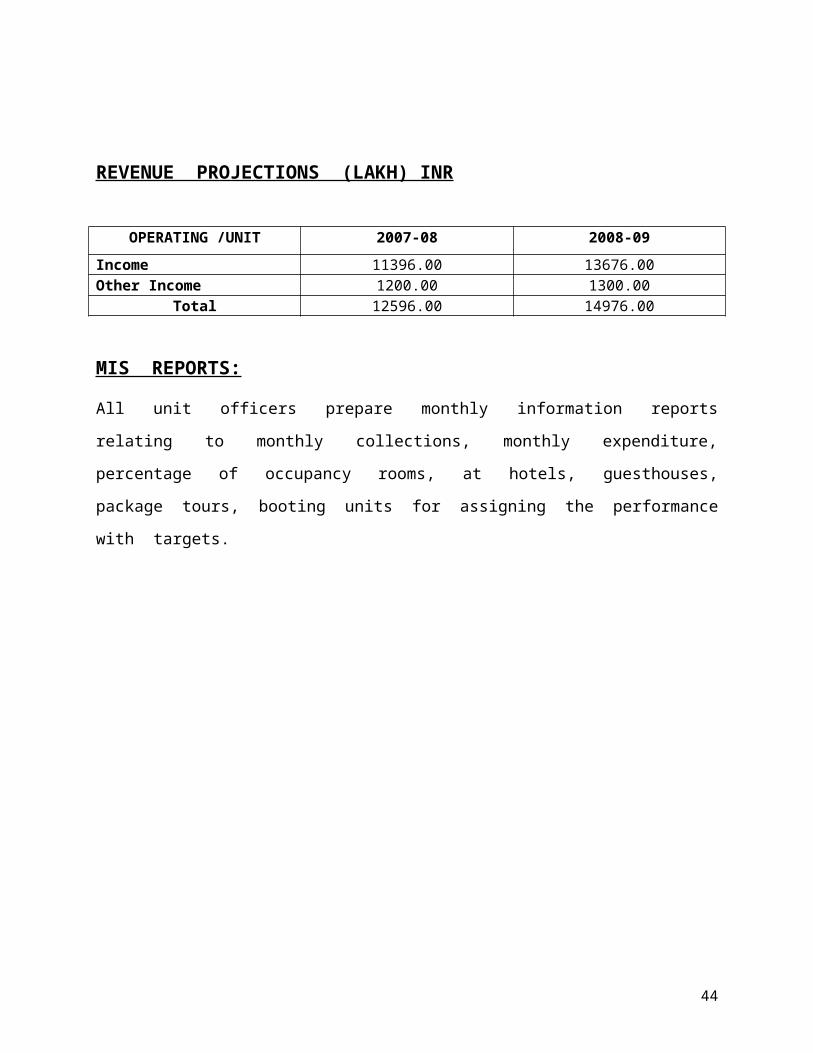

REVENUE PROJECTIONS (LAKH) INR

OPERATING /UNIT 2007-08 2008-09

Income 11396.00 13676.00Other Income 1200.00 1300.00

Total 12596.00 14976.00

MIS REPORTS:

All unit officers prepare monthly information reports relating to monthly collections,

monthly expenditure, percentage of occupancy rooms, at hotels, guesthouses, package

tours, booting units for assigning the performance with targets.

29

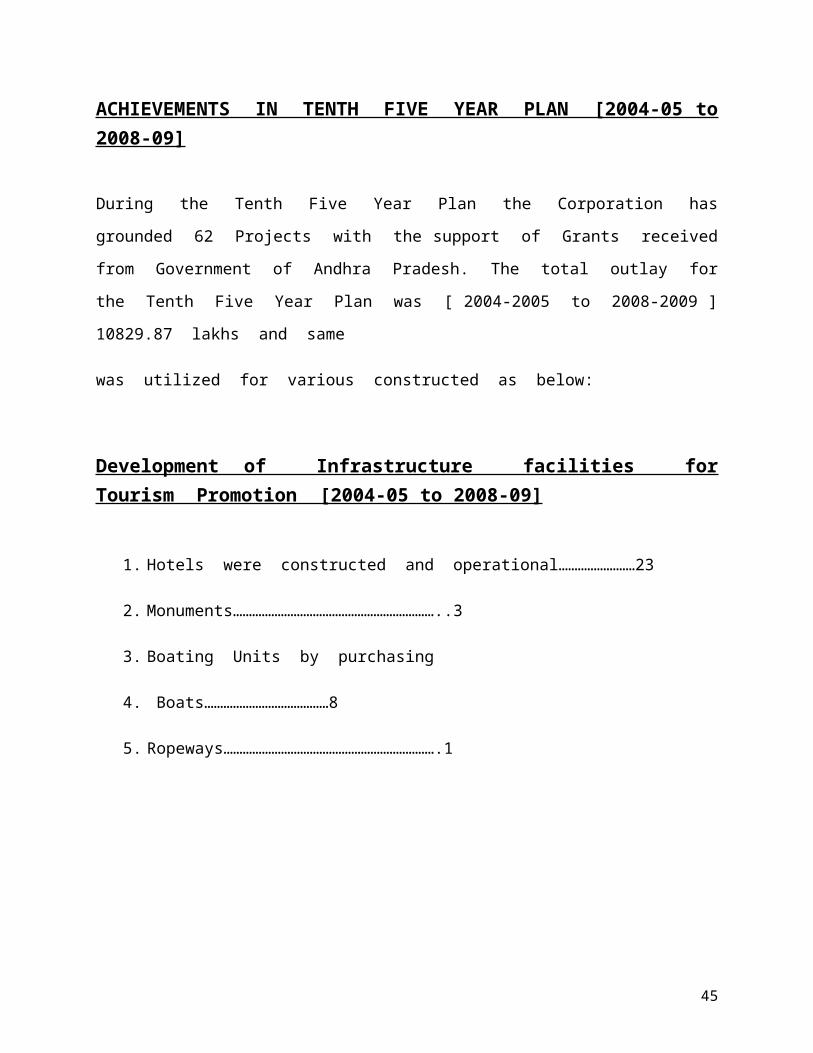

ACHIEVEMENTS IN TENTH FIVE YEAR PLAN [2004-05 to 2008-09]

During the Tenth Five Year Plan the Corporation has grounded 62 Projects with the

support of Grants received from Government of Andhra Pradesh. The total outlay for the

Tenth Five Year Plan was [ 2004-2005 to 2008-2009 ] 10829.87 lakhs and same

was utilized for various constructed as below:

Development of Infrastructure facilities for Tourism Promotion [2004-05 to 2008-09]

1. Hotels were constructed and operational……………………23

2. Monuments………………………………………………………..3

3. Boating Units by purchasing

4. Boats…………………………………8

5. Ropeways………………………………………………………….1

30

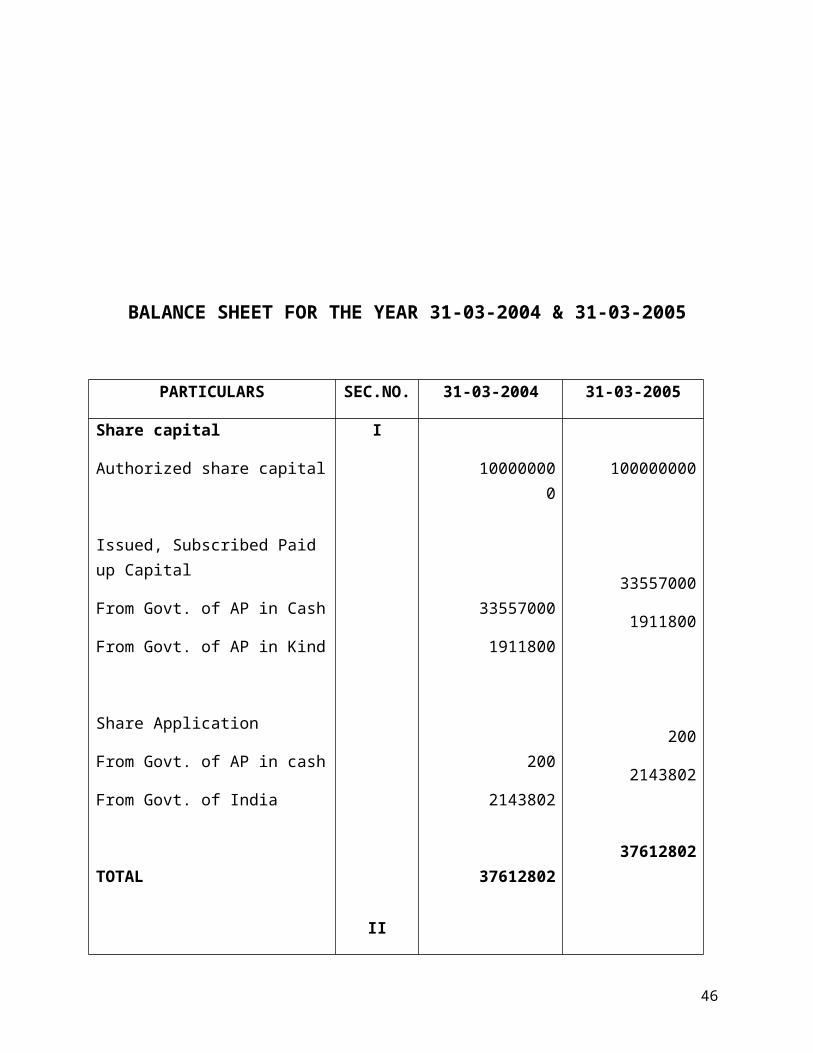

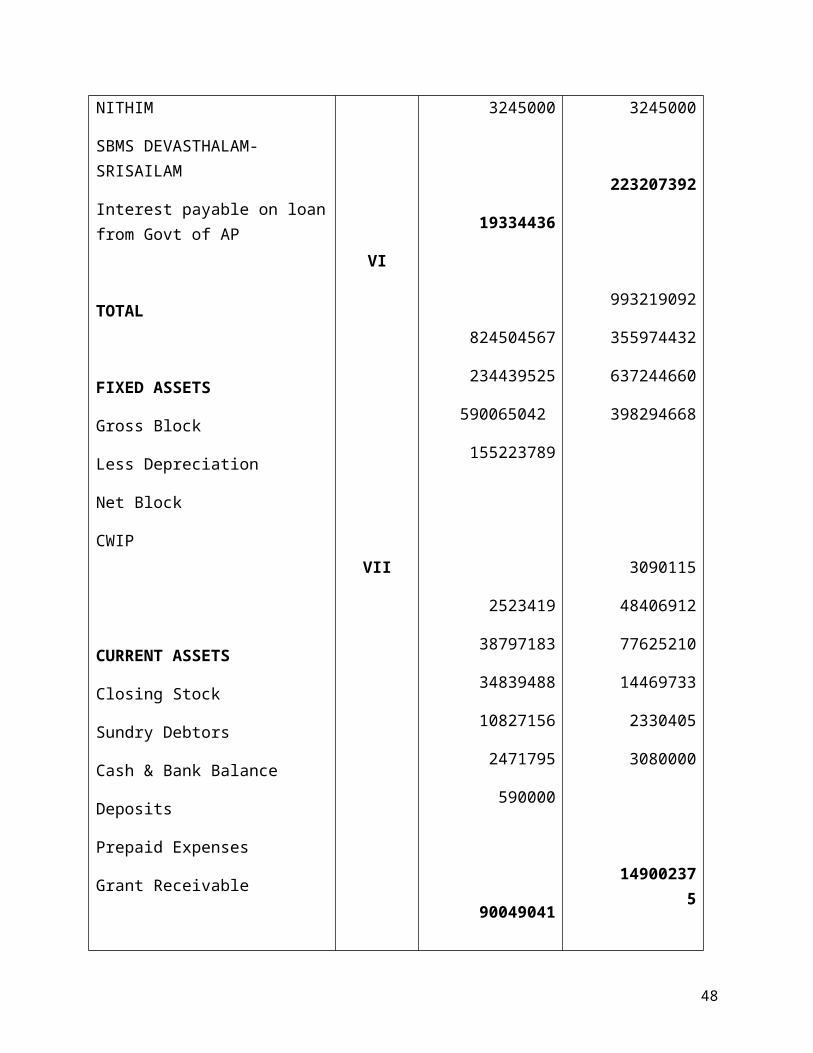

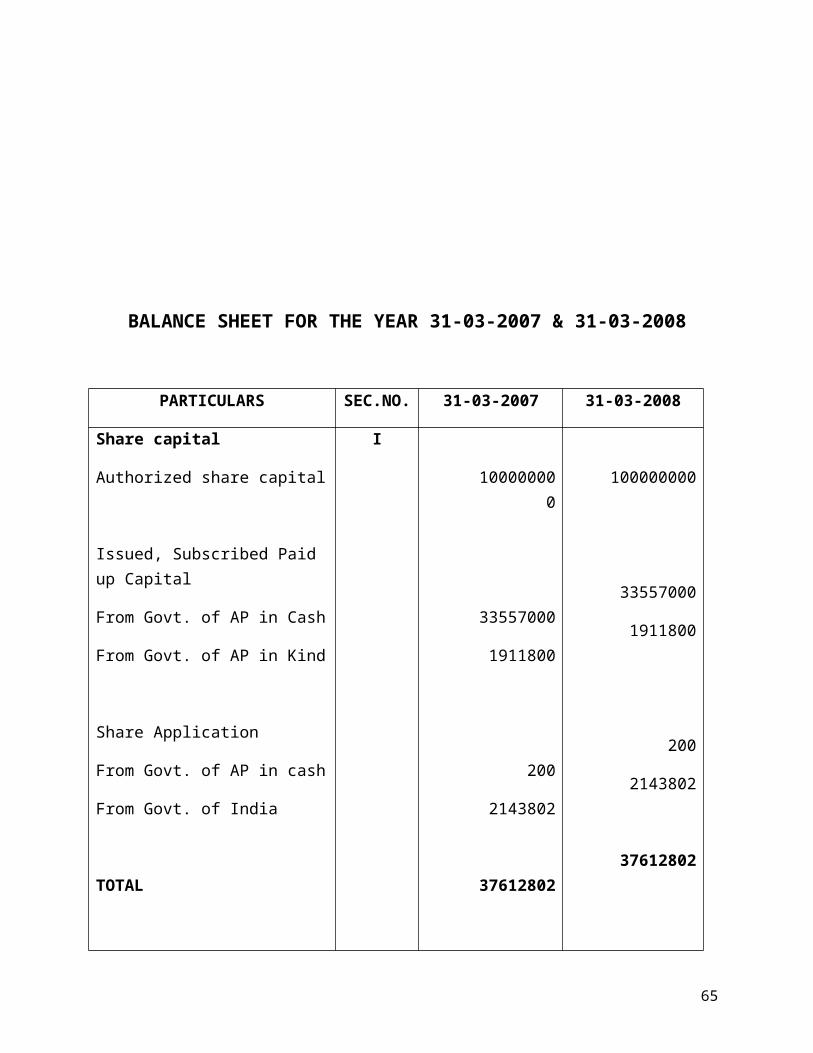

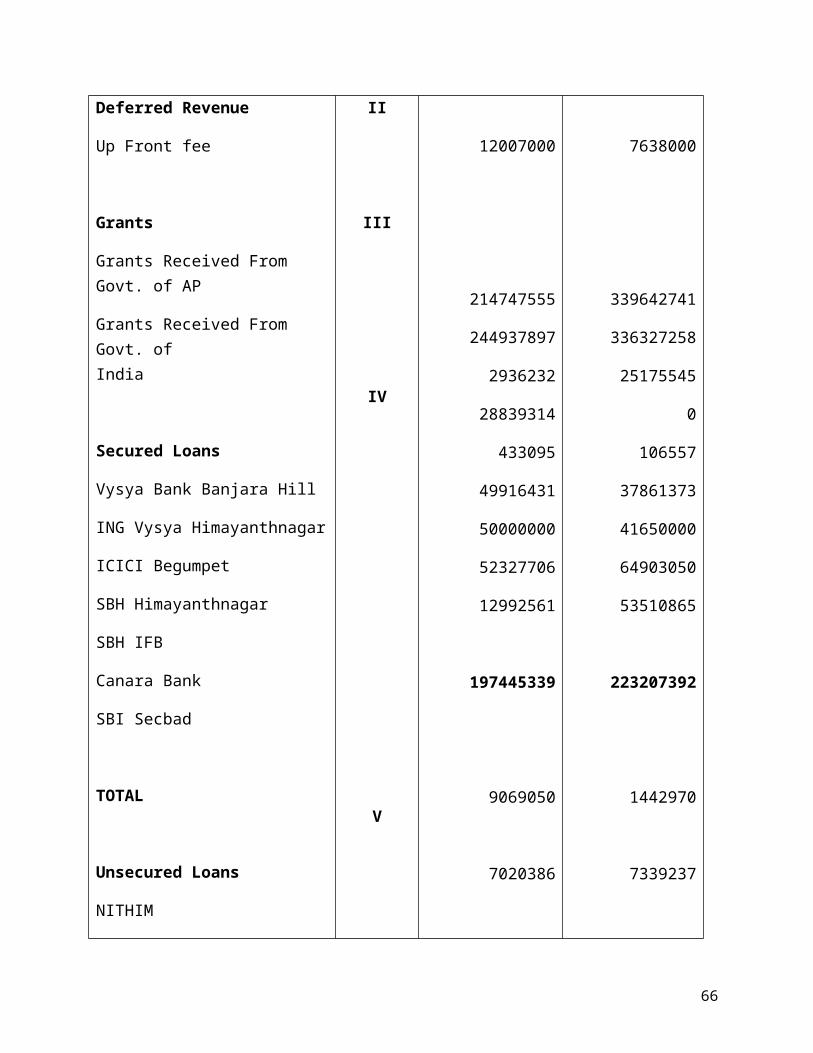

BALANCE SHEET FOR THE YEAR 31-03-2004 & 31-03-2005

PARTICULARS SEC.NO. 31-03-2004 31-03-2005

Share capital

Authorized share capital

Issued, Subscribed Paid up Capital

From Govt. of AP in Cash

From Govt. of AP in Kind

Share Application

From Govt. of AP in cash

From Govt. of India

TOTAL

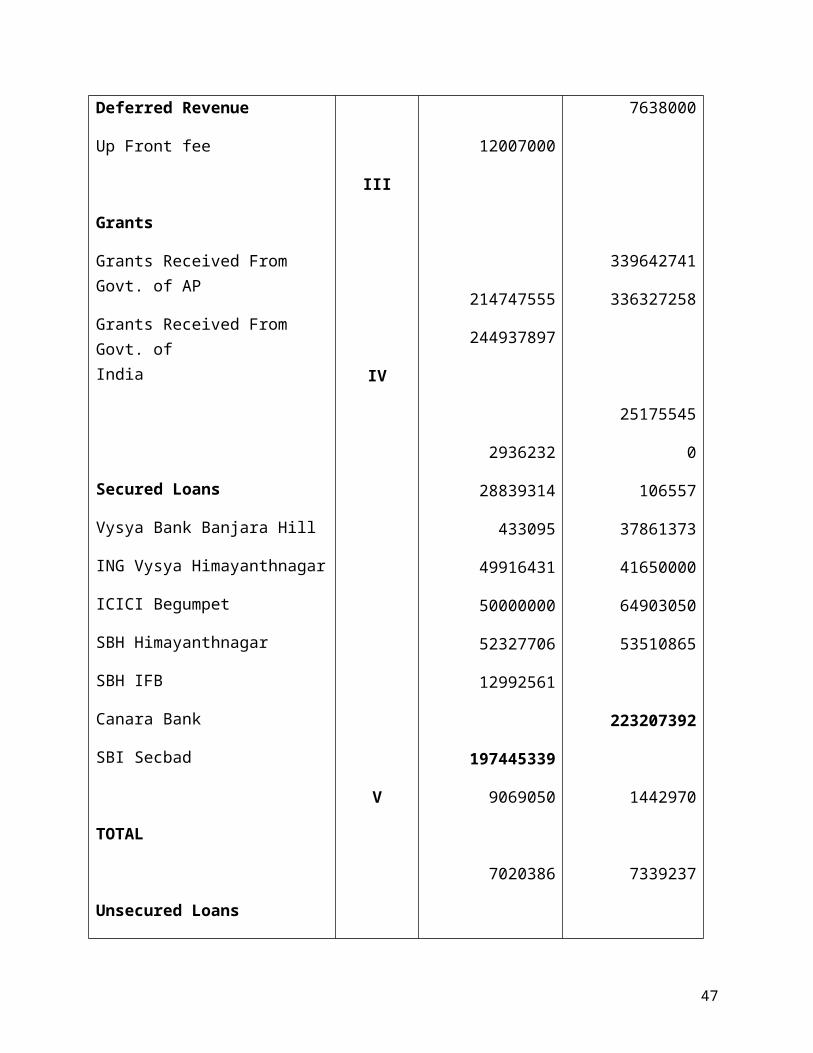

Deferred Revenue

Up Front fee

Grants

Grants Received From Govt. of AP

Grants Received From Govt. of India

I

II

III

100000000

33557000

1911800

200

2143802

37612802

12007000

214747555

244937897

100000000

33557000

1911800

200

2143802

37612802

7638000

339642741

336327258

31

Secured Loans

Vysya Bank Banjara Hill

ING Vysya Himayanthnagar

ICICI Begumpet

SBH Himayanthnagar

SBH IFB

Canara Bank

SBI Secbad

TOTAL

Unsecured Loans

NITHIM

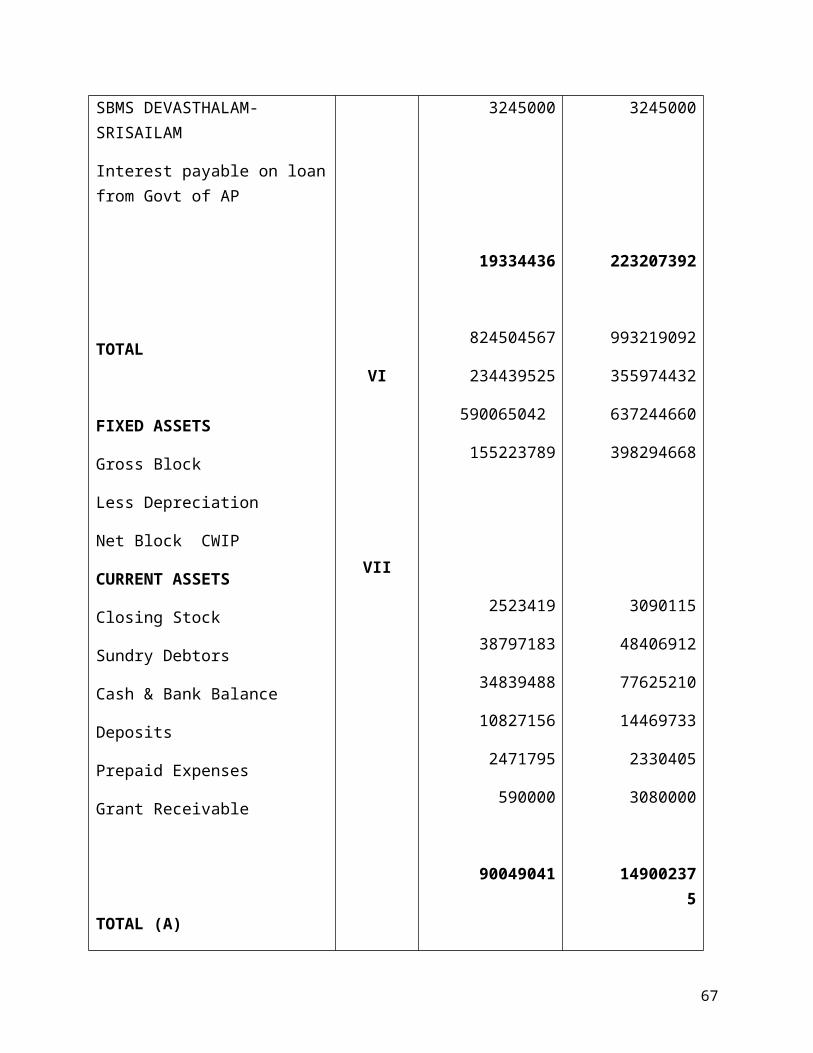

SBMS DEVASTHALAM-SRISAILAM

Interest payable on loan from Govt of AP

TOTAL

FIXED ASSETS

Gross Block

Less Depreciation

Net Block

CWIP

IV

V

VI

2936232

28839314

433095

49916431

50000000

52327706

12992561

197445339

9069050

7020386

3245000

19334436

824504567

234439525

590065042

155223789

25175545

0

106557

37861373

41650000

64903050

53510865

223207392

1442970

7339237

3245000

223207392

993219092

355974432

637244660

398294668

32

CURRENT ASSETS

Closing Stock

Sundry Debtors

Cash & Bank Balance

Deposits

Prepaid Expenses

Grant Receivable

TOTAL (A)

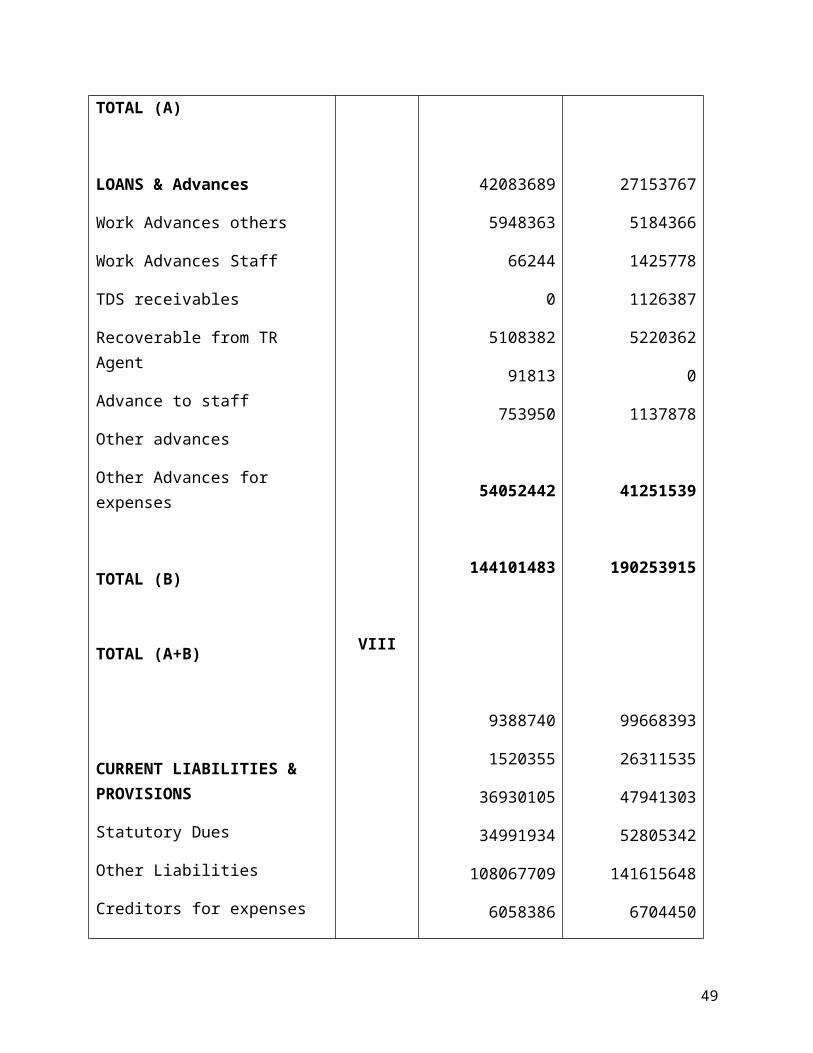

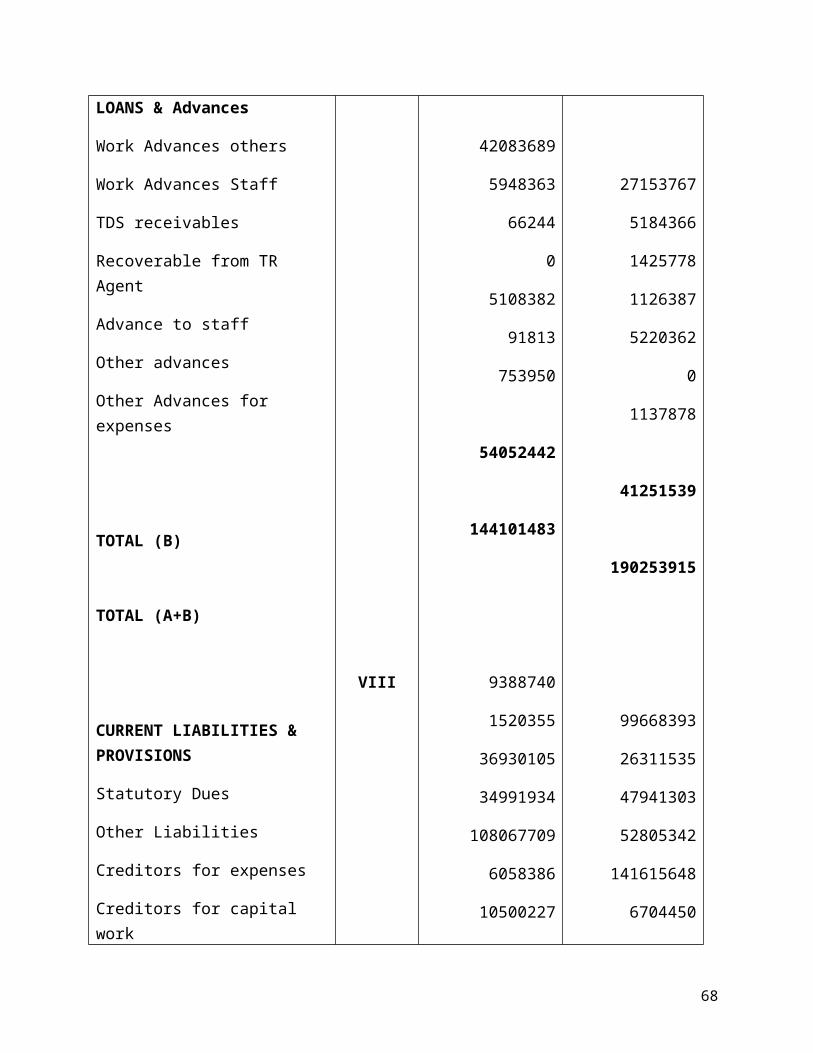

LOANS & Advances

Work Advances others

Work Advances Staff

TDS receivables

Recoverable from TR Agent

Advance to staff

Other advances

Other Advances for expenses

TOTAL (B)

TOTAL (A+B)

VII 2523419

38797183

34839488

10827156

2471795

590000

90049041

42083689

5948363

66244

0

5108382

91813

753950

54052442

144101483

3090115

48406912

77625210

14469733

2330405

3080000

149002375

27153767

5184366

1425778

1126387

5220362

0

1137878

41251539

190253915

33

CURRENT LIABILITIES & PROVISIONS

Statutory Dues

Other Liabilities

Creditors for expenses

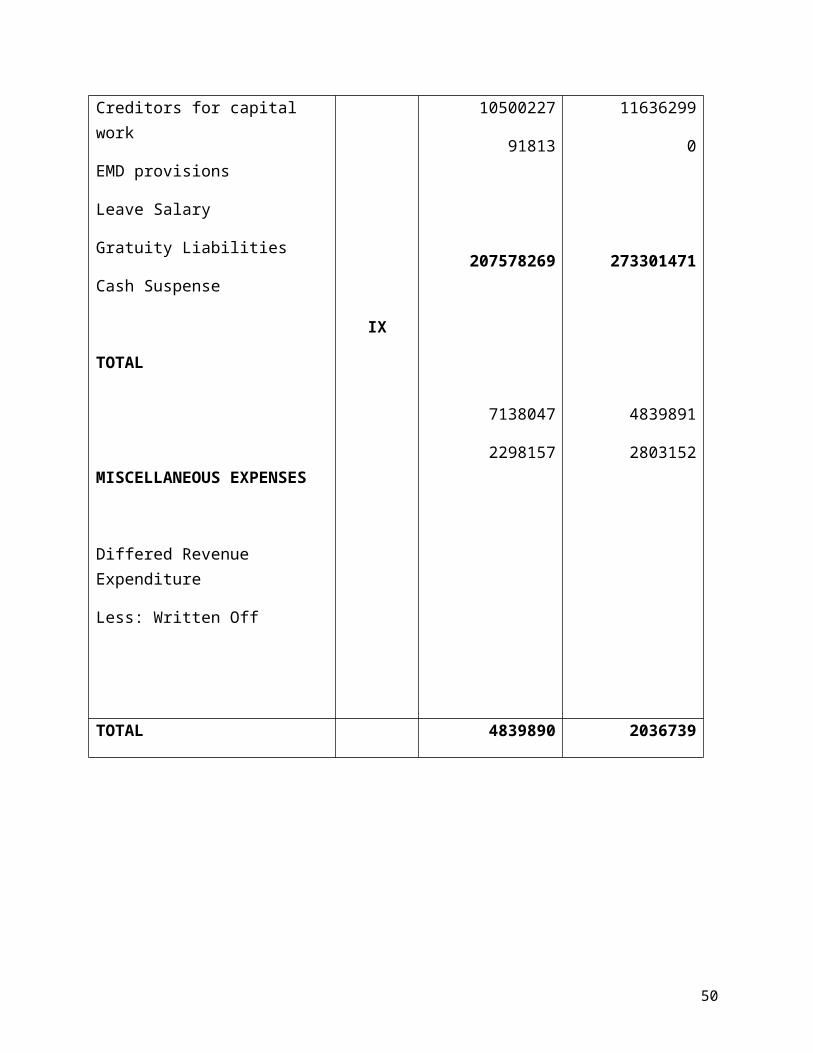

Creditors for capital work

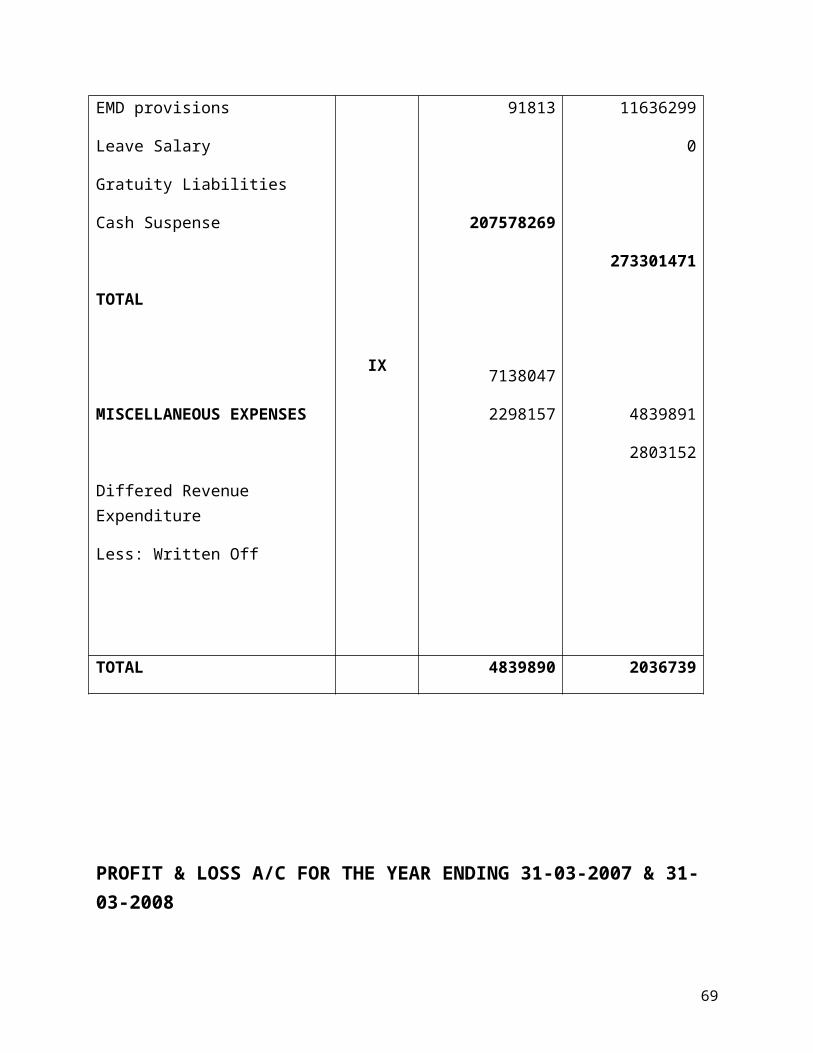

EMD provisions

Leave Salary

Gratuity Liabilities

Cash Suspense

TOTAL

MISCELLANEOUS EXPENSES

Differed Revenue Expenditure

Less: Written Off

VIII

IX

9388740

1520355

36930105

34991934

108067709

6058386

10500227

91813

207578269

7138047

2298157

99668393

26311535

47941303

52805342

141615648

6704450

11636299

0

273301471

4839891

2803152

TOTAL 4839890 2036739

34

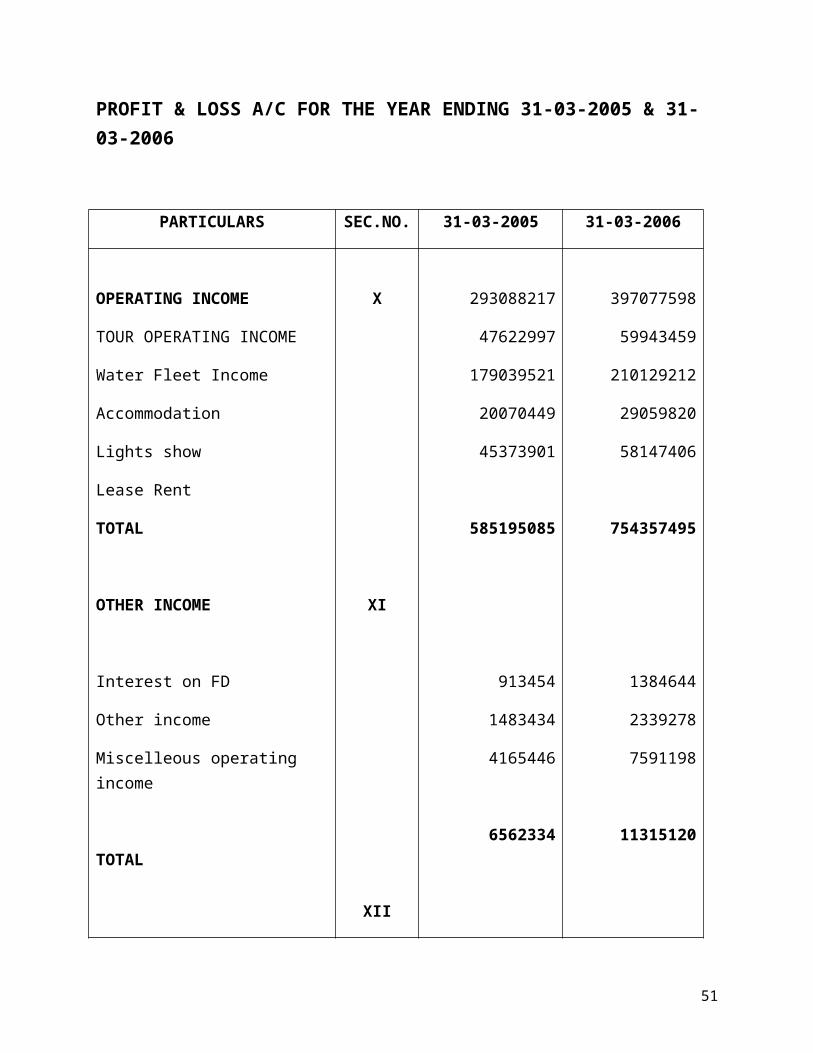

PROFIT & LOSS A/C FOR THE YEAR ENDING 31-03-2005 & 31-03-2006

PARTICULARS SEC.NO. 31-03-2005 31-03-2006

OPERATING INCOME

TOUR OPERATING INCOME

Water Fleet Income

Accommodation

Lights show

Lease Rent

TOTAL

OTHER INCOME

Interest on FD

Other income

Miscelleous operating income

TOTAL

OPERATING EXPENSES

Catering Expenses

X

XI

XII

293088217

47622997

179039521

20070449

45373901

585195085

913454

1483434

4165446

6562334

89014438

397077598

59943459

210129212

29059820

58147406

754357495

1384644

2339278

7591198

11315120

102161948

35

Water Fleet

Sound & Light

Tour Operating Expenses

TOTAL

PERSONAL EXPENSES

Salaries

Other Allowances

Staff welfare Expenses

Gratuity

TOTAL

ADMINISTRATIVE EXPENSES

Rent

Electricity Charges

Insurance

Traveling

Postage

Legal Expenses

XIII

XIV

5164007

149155

166861606

261189206

103964113

9713430

1791919

1792199

117261661

13826003

22293407

8460809

14486793

5451530

2325023

8219928

2267092

247342154

359991122

116257011

116257011

3494488

1731435

131662977

12665694

23753046

6797624

16087790

5712112

1043809

36

Printing Expenses

Other Expenses

Audit fees

TOTAL

PUBLICITY & MARKETING

Advertisement

Publicity & Marketing

Inaugural expenses

Exhibition & Festivals

Entertainment

Fairs & Festivals Abroad

Hospitality

TOTAL

REPAIR & MAINTAINENCE

Rep & Maint. (General)

Rep & Maint. (Furniture

TOTAL

XV

6231775

4334132

165300

77574772

5069686

2855048

717139

4148361

1077914

13156

1000583

14881887

10630402

606792

11237194

6381907

4037139

183750

76662871

0

0

747197

0

0

0

0

747197

11042558

172695

11215253

37

INTEREST & BANK CHARGES

Interest

Interest on Unsecured loans

Bank charges

8503594

0

1189175

12398223

523755

1527129

TOTAL 9692769 14449107

38

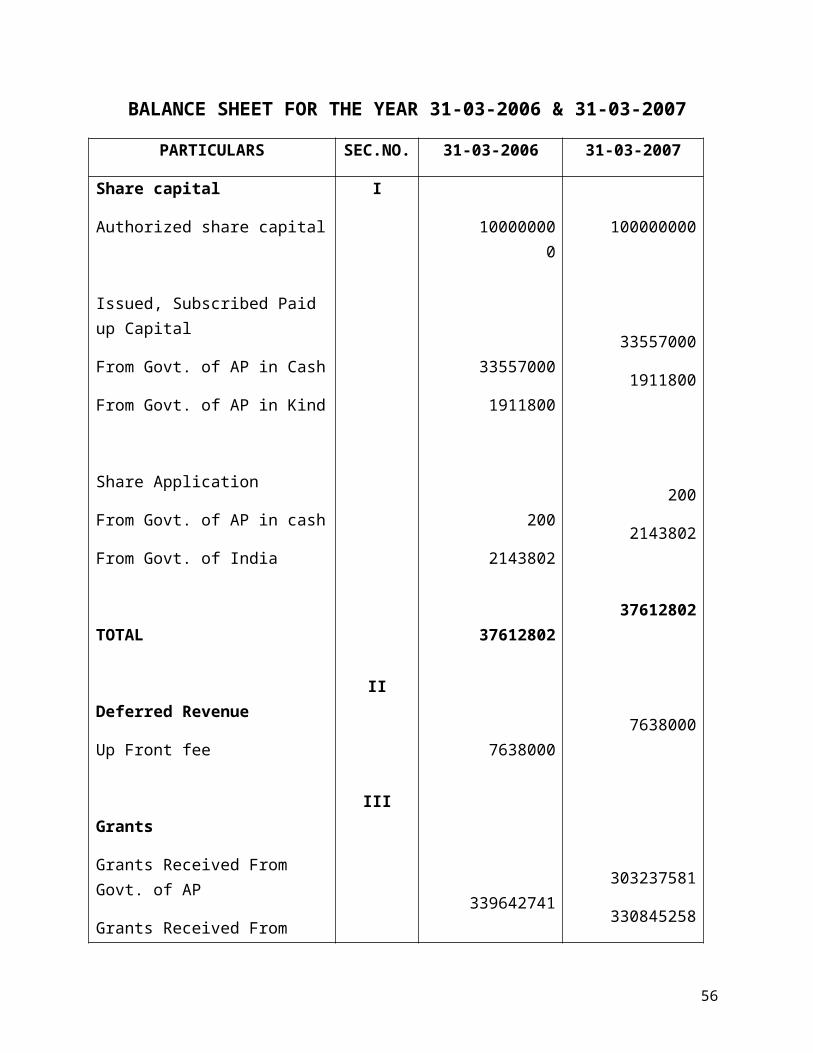

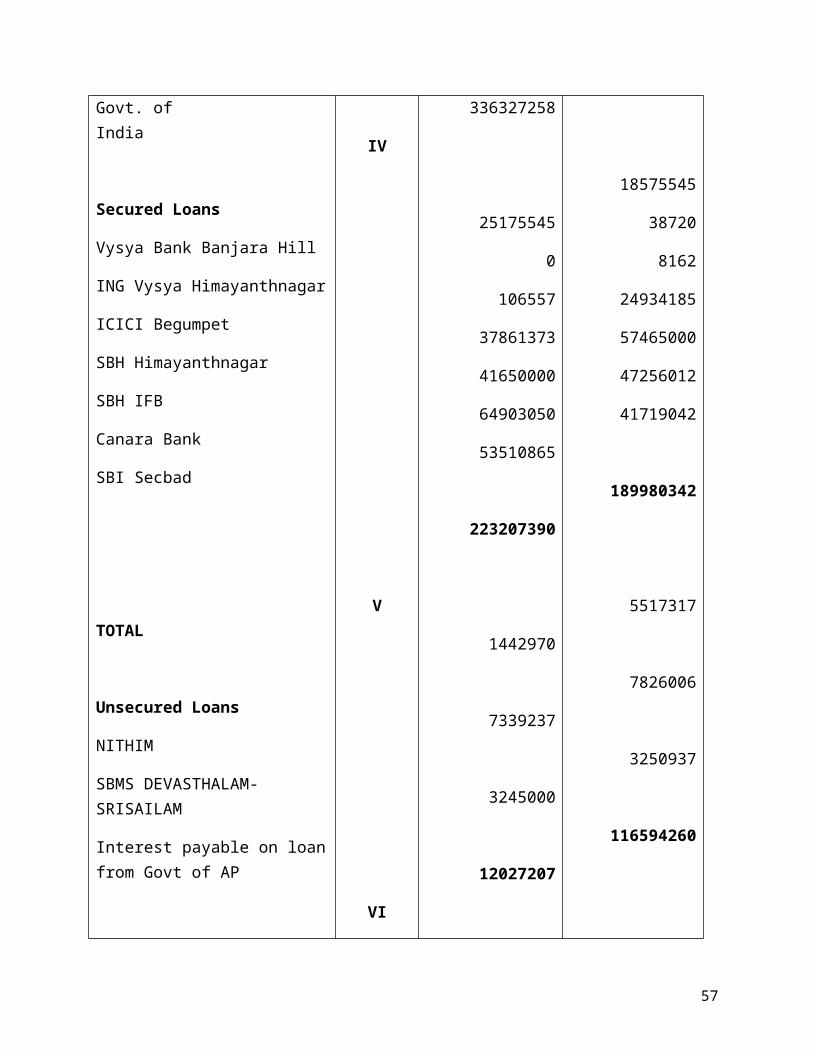

BALANCE SHEET FOR THE YEAR 31-03-2006 & 31-03-2007

PARTICULARS SEC.NO. 31-03-2006 31-03-2007

Share capital

Authorized share capital

Issued, Subscribed Paid up Capital

From Govt. of AP in Cash

From Govt. of AP in Kind

Share Application

From Govt. of AP in cash

From Govt. of India

TOTAL

Deferred Revenue

Up Front fee

Grants

Grants Received From Govt. of AP

Grants Received From Govt. of India

Secured Loans

Vysya Bank Banjara Hill

I

II

III

IV

100000000

33557000

1911800

200

2143802

37612802

7638000

339642741

336327258

100000000

33557000

1911800

200

2143802

37612802

7638000

303237581

330845258

39

ING Vysya Himayanthnagar

ICICI Begumpet

SBH Himayanthnagar

SBH IFB

Canara Bank

SBI Secbad

TOTAL

Unsecured Loans

NITHIM

SBMS DEVASTHALAM-SRISAILAM

Interest payable on loan from Govt of AP

TOTAL

FIXED ASSETS

Gross Block

Less Depreciation

Net Block

CWIP

V

VI

25175545

0

106557

37861373

41650000

64903050

53510865

223207390

1442970

7339237

3245000

12027207

993219090

355974432

637244660

398294336

18575545

38720

8162

24934185

57465000

47256012

41719042

189980342

5517317

7826006

3250937

116594260

120730418

466686967

740617189

288704250

40

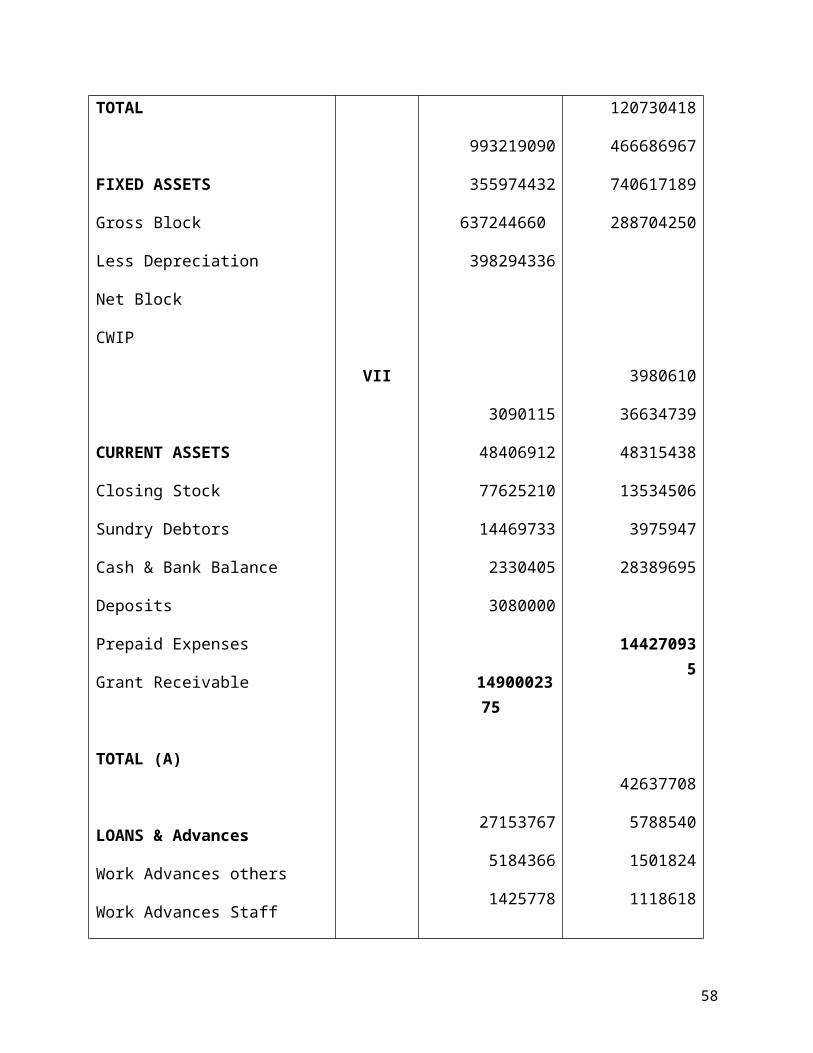

CURRENT ASSETS

Closing Stock

Sundry Debtors

Cash & Bank Balance

Deposits

Prepaid Expenses

Grant Receivable

TOTAL (A)

LOANS & Advances

Work Advances others

Work Advances Staff

TDS receivables

Recoverable from TR Agent

Advance to staff

Other advances

Other Advances for expenses

TOTAL (B)

TOTAL (A+B)

VII 3090115

48406912

77625210

14469733

2330405

3080000

1490002375

27153767

5184366

1425778

1126387

5220362

0

1137878

41251539

190253915

3980610

36634739

48315438

13534506

3975947

28389695

144270935

42637708

5788540

1501824

1118618

5229744

75545

2113848

58465827

202736762

41

CURRENT LIABILITIES & PROVISIONS

Statutory Dues

Other Liabilities

Creditors for expenses

Creditors for capital work

EMD provisions

Leave Salary

Gratuity Liabilities

Cash Suspense

Deferred Tax Liability

TOTAL

MISCELLANEOUS EXPENSES

Differed Revenue Expenditure

Less: Written Off

VIII

IX

99668393

26311535

47941303

52805342

141615648

6704450

11636299

0

0

273301471

4839891

2803152

6126470

3155050

39270811

29972506

147385982

6344168

11609068

0

5777478

23832465

4839891

2803152

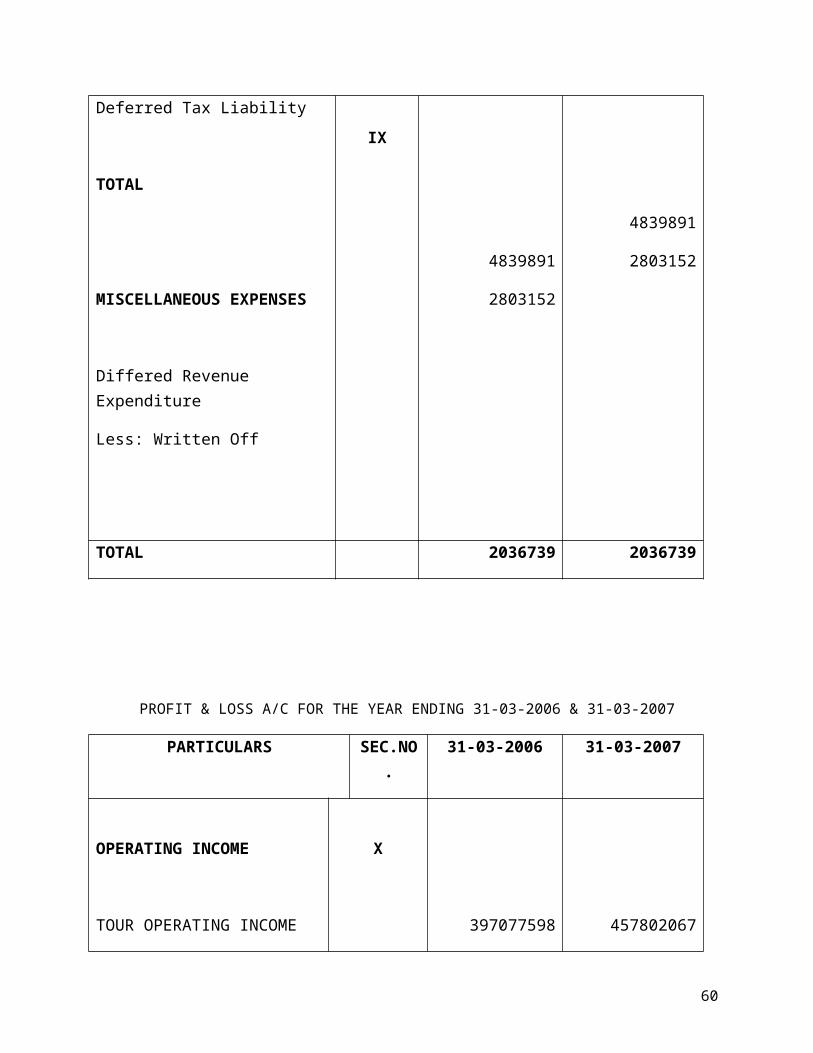

TOTAL 2036739 2036739

42

PROFIT & LOSS A/C FOR THE YEAR ENDING 31-03-2006 & 31-03-2007

PARTICULARS SEC.NO. 31-03-2006 31-03-2007

OPERATING INCOME

TOUR OPERATING INCOME

Water Fleet Income

Accommodation

Lights show

Lease Rent

TOTAL

OTHER INCOME

Interest on FD

Other income

Miscelleous operating income

TOTAL

OPERATING EXPENSES

X

XI

XII

397077598

59943459

210129212

29059820

58147406

754357495

1384644

2339278

7591198

11315120

457802067

74008243

265932949

33438050

42428873

873610182

716007

2027942

1787308

4531257

43

Catering Expenses

Water Fleet

Sound & Light

Tour Operating Expenses

TOTAL

PERSONAL EXPENSES

Salaries

Other Allowances

Staff welfare Expenses

Gratuity

TOTAL

ADMINISTRATIVE EXPENSES

Rent

Electricity Charges

Insurance

Traveling

Postage

XIII

XIV

102161948

8219928

2267092

247342154

359991122

116257011

116257011

3494488

1731435

131662977

12665694

23753046

6797624

16087790

5712112

130612874

4727756

2034291

288795601

426170522

11066202

5585806

681228

388757

117317819

0

25521673

7052131

17227632

5161641

44

Legal Expenses

Printing Expenses

Other Expenses

Audit fees

Hospitality

Security services salaries

TOTAL

PUBLICITY & MARKETING

Advertisement

Publicity & Marketing

Inaugural expenses

Exhibition & Festivals

Entertainment

Fairs & Festivals Abroad

TOTAL

REPAIR & MAINTAINENCE

Rep & Maint. (General)

Rep & Maint. (Furniture

XV

1043809

6381907

4037139

183750

0

0

76662871

0

0

747197

0

0

0

747197

11042558

172695

3215823

5519906

5218605

196224

568869

14587769

84270273

4888687

3465352

472137

886897

665864

47082

10426019

14096849

77638

45

Renovation expenses

Repair & maintenance vehicle

Repair & maint.water fleet

TOTAL

INTEREST & BANK CHARGES

Interest

Interest on Unsecured loans

Bank charges

0

0

0

11215253

12398223

523755

1527129

2034291

20760973

981680

37951431

12398223

523755

1527129

TOTAL 14449107 14449107

46

BALANCE SHEET FOR THE YEAR 31-03-2007 & 31-03-2008

PARTICULARS SEC.NO. 31-03-2007 31-03-2008

Share capital

Authorized share capital

Issued, Subscribed Paid up Capital

From Govt. of AP in Cash

From Govt. of AP in Kind

Share Application

From Govt. of AP in cash

From Govt. of India

TOTAL

Deferred Revenue

Up Front fee

Grants

Grants Received From Govt. of AP

Grants Received From Govt. of India

Secured Loans

I

II

III

IV

100000000

33557000

1911800

200

2143802

37612802

12007000

214747555

244937897

2936232

100000000

33557000

1911800

200

2143802

37612802

7638000

339642741

336327258

25175545

47

Vysya Bank Banjara Hill

ING Vysya Himayanthnagar

ICICI Begumpet

SBH Himayanthnagar

SBH IFB

Canara Bank

SBI Secbad

TOTAL

Unsecured Loans

NITHIM

SBMS DEVASTHALAM-SRISAILAM

Interest payable on loan from Govt of AP

TOTAL

FIXED ASSETS

Gross Block

Less Depreciation

Net Block CWIP

V

VI

28839314

433095

49916431

50000000

52327706

12992561

197445339

9069050

7020386

3245000

19334436

824504567

234439525

590065042

155223789

0

106557

37861373

41650000

64903050

53510865

223207392

1442970

7339237

3245000

223207392

993219092

355974432

637244660

398294668

48

CURRENT ASSETS

Closing Stock

Sundry Debtors

Cash & Bank Balance

Deposits

Prepaid Expenses

Grant Receivable

TOTAL (A)

LOANS & Advances

Work Advances others

Work Advances Staff

TDS receivables

Recoverable from TR Agent

Advance to staff

Other advances

Other Advances for expenses

TOTAL (B)

TOTAL (A+B)

VII

2523419

38797183

34839488

10827156

2471795

590000

90049041

42083689

5948363

66244

0

5108382

91813

753950

54052442

144101483

3090115

48406912

77625210

14469733

2330405

3080000

149002375

27153767

5184366

1425778

1126387

5220362

0

1137878

41251539

190253915

49

CURRENT LIABILITIES & PROVISIONS

Statutory Dues

Other Liabilities

Creditors for expenses

Creditors for capital work

EMD provisions

Leave Salary

Gratuity Liabilities

Cash Suspense

TOTAL

MISCELLANEOUS EXPENSES

Differed Revenue Expenditure

Less: Written Off

VIII

IX

9388740

1520355

36930105

34991934

108067709

6058386

10500227

91813

207578269

7138047

2298157

99668393

26311535

47941303

52805342

141615648

6704450

11636299

0

273301471

4839891

2803152

TOTAL 4839890 2036739

50

PROFIT & LOSS A/C FOR THE YEAR ENDING 31-03-2007 & 31-03-2008

PARTICULARS SEC.NO. 31-03-2007 31-03-2008

OPERATING INCOME

TOUR OPERATING INCOME

Water Fleet Income

Accommodation

Lights show

Lease Rent

TOTAL

OTHER INCOME

Interest on FD

Other income

Miscelleous operating income

TOTAL

X

XI

293088217

47622997

179039521

20070449

45373901

585195085

913454

1483434

4165446

6562334

397077598

59943459

210129212

29059820

58147406

754357495

1384644

2339278

7591198

11315120

51

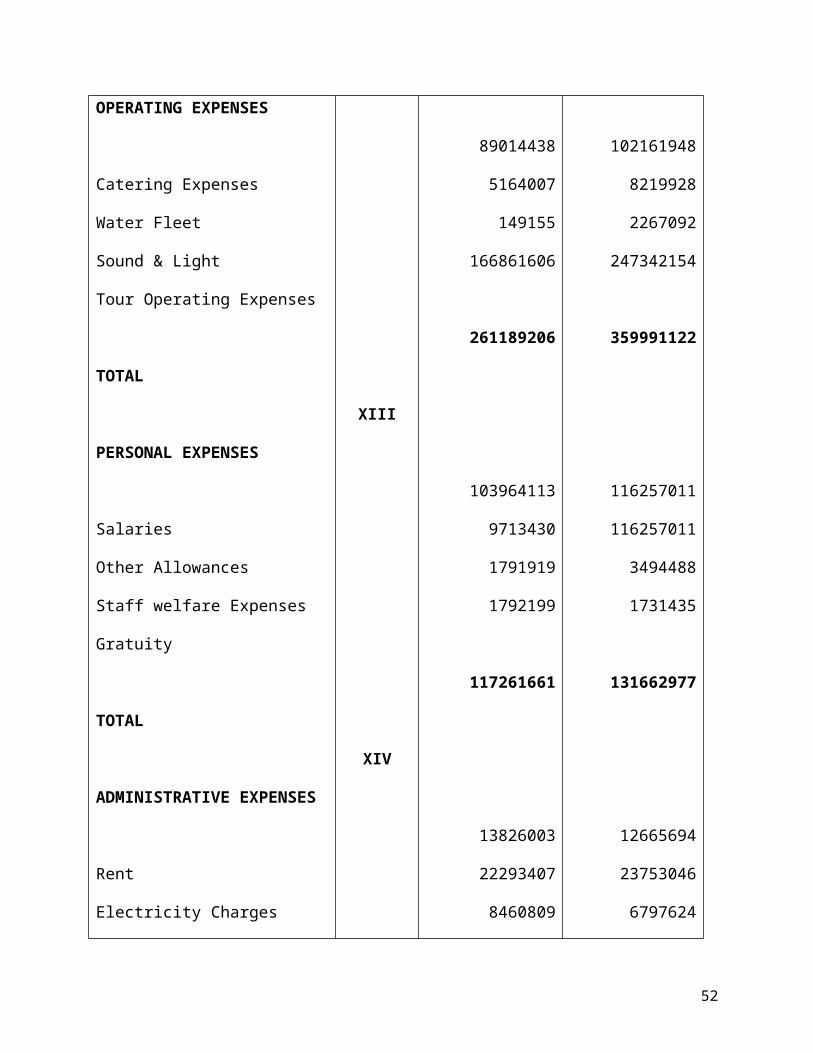

OPERATING EXPENSES

Catering Expenses

Water Fleet

Sound & Light

Tour Operating Expenses

TOTAL

PERSONAL EXPENSES

Salaries

Other Allowances

Staff welfare Expenses

Gratuity

TOTAL

ADMINISTRATIVE EXPENSES

Rent

Electricity Charges

Insurance

Traveling

Postage

Legal Expenses

XII

XIII

XIV

89014438

5164007

149155

166861606

261189206

103964113

9713430

1791919

1792199

117261661

13826003

22293407

8460809

14486793

5451530

2325023

102161948

8219928

2267092

247342154

359991122

116257011

116257011

3494488

1731435

131662977

12665694

23753046

6797624

16087790

5712112

1043809

52

Printing Expenses

Other Expenses

Audit fees

TOTAL

PUBLICITY & MARKETING

Advertisement

Publicity & Marketing

Inaugural expenses

Exhibition & Festivals

Entertainment

Fairs & Festivals Abroad

Hospitality

TOTAL

REPAIR & MAINTAINENCE

Rep & Maint. (General)

Rep & Maint. (Furniture

TOTAL

XV

6231775

4334132

165300

77574772

5069686

2855048

717139

4148361

1077914

13156

1000583

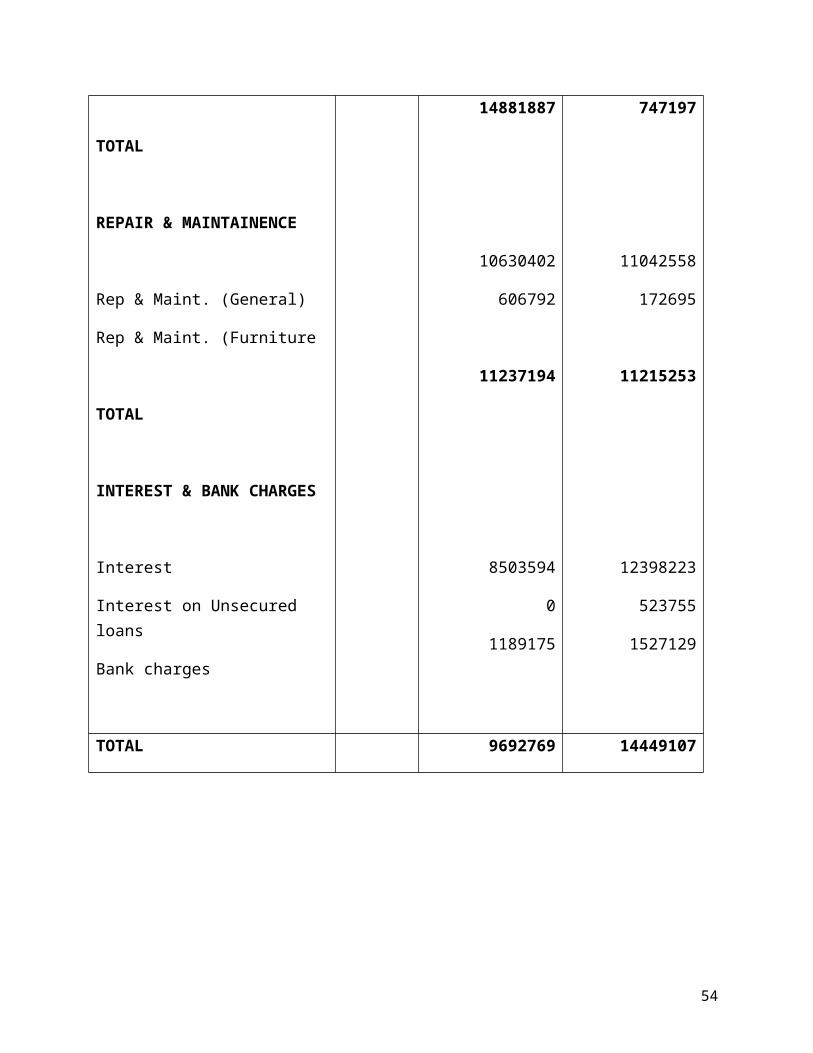

14881887

10630402

606792

11237194

6381907

4037139

183750

76662871

0

0

747197

0

0

0

0

747197

11042558

172695

11215253

53

INTEREST & BANK CHARGES

Interest

Interest on Unsecured loans

Bank charges

8503594

0

1189175

12398223

523755

1527129

TOTAL 9692769 14449107

54

BALANCE SHEET FOR THE YEAR 31-03-2008 & 31-03-2009

PARTICULARS SEC.NO. 31-03-2008 31-03-2009

Share capital

Authorized share capital

Issued, Subscribed Paid up Capital

From Govt. of AP in Cash

From Govt. of AP in Kind

Share Application

From Govt. of AP in cash

From Govt. of India

TOTAL

Deferred Revenue

Up Front fee

Grants

Grants Received From Govt. of AP

Grants Received From Govt. of India

I

II

III

100000000

33557000

1911800

200

2143802

37612802

7638000

339642741

336327258

100000000

33557000

1911800

200

2143802

37612802

7638000

303237581

330845258

55

Secured Loans

Vysya Bank Banjara Hill

ING Vysya Himayanthnagar

ICICI Begumpet

SBH Himayanthnagar

SBH IFB

Canara Bank

SBI Secbad

TOTAL

Unsecured Loans

NITHIM

SBMS DEVASTHALAM-SRISAILAM

Interest payable on loan from Govt of AP

TOTAL

FIXED ASSETS

Gross Block

Less Depreciation

Net Block

CWIP

IV

V

VI

25175545

0

106557

37861373

41650000

64903050

53510865

223207390

1442970

7339237

3245000

12027207

993219090

355974432

637244660

398294336

18575545

38720

8162

24934185

57465000

47256012

41719042

189980342

5517317

7826006

3250937

116594260

120730418

466686967

740617189

288704250

56

CURRENT ASSETS

Closing Stock

Sundry Debtors

Cash & Bank Balance

Deposits

Prepaid Expenses

Grant Receivable

TOTAL (A)

LOANS & Advances

Work Advances others

Work Advances Staff

TDS receivables

Recoverable from TR Agent

Advance to staff

Other advances

Other Advances for expenses

TOTAL (B)

TOTAL (A+B)

VII 3090115

48406912

77625210

14469733

2330405

3080000

1490002375

27153767

5184366

1425778

1126387

5220362

0

1137878

41251539

190253915

3980610

36634739

48315438

13534506

3975947

28389695

144270935

42637708

5788540

1501824

1118618

5229744

75545

2113848

58465827

202736762

57

CURRENT LIABILITIES & PROVISIONS

Statutory Dues

Other Liabilities

Creditors for expenses

Creditors for capital work

EMD provisions

Leave Salary

Gratuity Liabilities

Cash Suspense

Deferred Tax Liability

TOTAL

MISCELLANEOUS EXPENSES

Differed Revenue Expenditure

Less: Written Off

VIII

IX

99668393

26311535

47941303

52805342

141615648

6704450

11636299

0

0

273301471

4839891

2803152

6126470

3155050

39270811

29972506

147385982

6344168

11609068

0

5777478

23832465

4839891

2803152

TOTAL 2036739 2036739

58

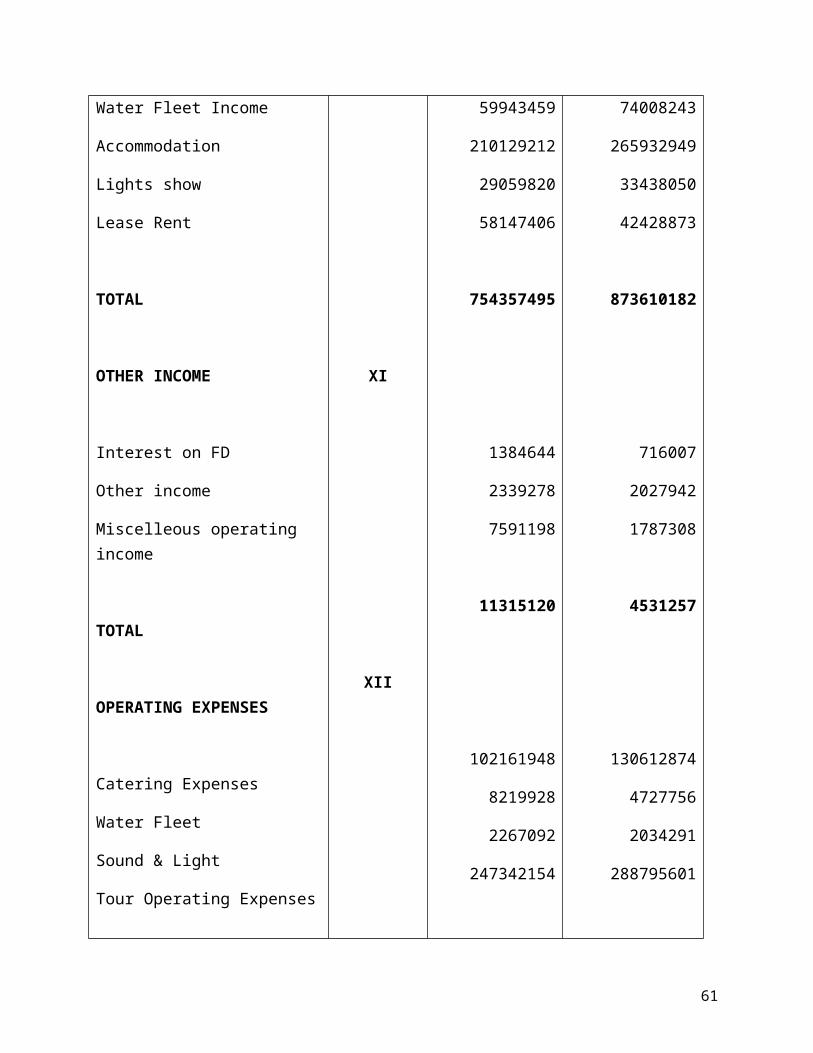

PROFIT & LOSS A/C FOR THE YEAR ENDING 31-03-2008 & 31-03-2009

PARTICULARS SEC.NO. 31-03-2008 31-03-2009

OPERATING INCOME

TOUR OPERATING INCOME

Water Fleet Income

Accommodation

Lights show

Lease Rent

TOTAL

OTHER INCOME

Interest on FD

Other income

Miscelleous operating income

TOTAL

X

XI

397077598

59943459

210129212

29059820

58147406

754357495

1384644

2339278

7591198

11315120

457802067

74008243

265932949

33438050

42428873

873610182

716007

2027942

1787308

4531257

59

OPERATING EXPENSES

Catering Expenses

Water Fleet

Sound & Light

Tour Operating Expenses

TOTAL

PERSONAL EXPENSES

Salaries

Other Allowances

Staff welfare Expenses

Gratuity

TOTAL

ADMINISTRATIVE EXPENSES

Rent

Electricity Charges

Insurance

Traveling

Postage

XII

XIII

XIV

102161948

8219928

2267092

247342154

359991122

116257011

116257011

3494488

1731435

131662977

12665694

23753046

6797624

16087790

5712112

130612874

4727756

2034291

288795601

426170522

11066202

5585806

681228

388757

117317819

0

25521673

7052131

17227632

5161641

60

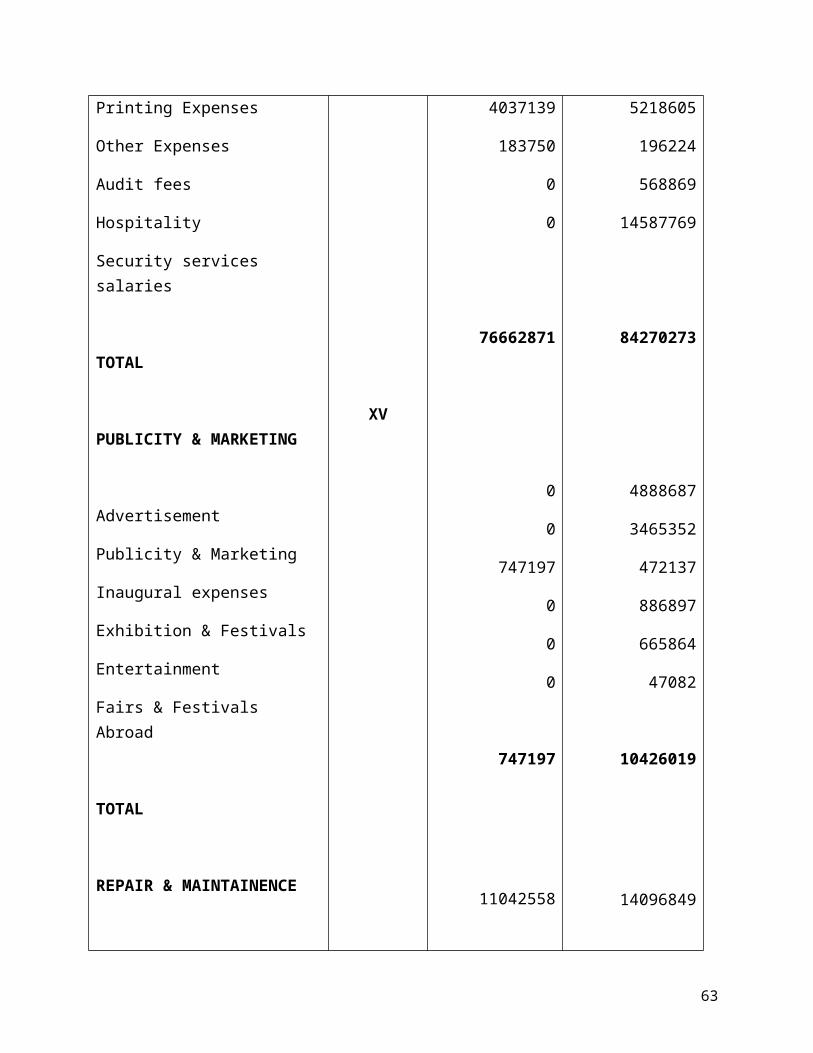

Legal Expenses

Printing Expenses

Other Expenses

Audit fees

Hospitality

Security services salaries

TOTAL

PUBLICITY & MARKETING

Advertisement

Publicity & Marketing

Inaugural expenses

Exhibition & Festivals

Entertainment

Fairs & Festivals Abroad

TOTAL

REPAIR & MAINTAINENCE

Rep & Maint. (General)

Rep & Maint. (Furniture

Renovation expenses

XV

1043809

6381907

4037139

183750

0

0

76662871

0

0

747197

0

0

0

747197

11042558

172695

0

3215823

5519906

5218605

196224

568869

14587769

84270273

4888687

3465352

472137

886897

665864

47082

10426019

14096849

77638

2034291

61

Repair & maintenance vehicle

Repair & maint.water fleet

TOTAL

INTEREST & BANK CHARGES

Interest

Interest on Unsecured loans

Bank charges

0

0

11215253

12398223

523755

1527129

20760973

981680

37951431

12398223

523755

1527129

TOTAL 14449107 14449107

62

ANALYSIS OF SOURCE OF FUNDS OF APTDCL

Here, it is proposed to examine sources of fund of APTDCL by expressing each

sources as percentage of total sources of funds. The following table – I i.e., presents a

relevant data of sources of funds of APTDCL from 2004-2005 to 2008-2009.

TABLE – I : SOURCES OF FUNDS OF APTDCL

Sources of funds 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Share Capital37612802

(5.18)37612802

(3.82)37612802

(5.18)37612802

(3.82)37612802

(4.21)

Deferred Revenue12007000

(1.65)7638000

(0.78)12007000

(1.65)7638000

(0.78)7638000

(0.86)

Grants459685452

(63.31)675969999

(68.59)459685452

(63.31)675969999

(68.59)634082839

(71.1)

Secured Loans197445338

(27.19)223207392

(22.65)197445338

(27.19)223207392

(22.65)189980342

(71.11)

Unsecured Loans19334436

(2.66)12027208

(1.22)19334436

(2.66)12027208

(1.22)16594260

(1.86)

Deferred Tax Liability- 28997310

(2.94)- 28997310

(2.94)5777478

(0.64)

TOTAL726085028

(100.00)985452711

(100.00)726085028

(100.00)985452711

(100.00)891685721

63

THE ANALYSIS OF THE DATA OF THE TABLE

BRINGS OUT THE FOLLOWING

Government grants contributing major amount in every year. The amount of grants

moved between 56.18% to 68.59% during the period under review. This may be an

account of constant encouragement of government towards the tourism development in

the state. However the APTDCL also depending on external sources of fund such as

secured loan and unsecured loans.

With in this two secured loan contributing much more than the unsecured loan in

almost all the years of the Study. The percentage of secured loan varied from 27.19% in

the year 2004-05 to 71.11% in the year 2008-09. Where as unsecured loans moved from

2.66% to 1.86%. The unsecured loans contribution is less in the year 2006-07 and 2005-

06 than the remaining year of the study

The amount of share capital of APTDCL is constant. It indicates that, there is no

increase in the internal sources. Therefore it can be concluded that the APTDCL is

completely depends upon external sources that to only government grants. Thus the

development of APTDCL is completes in the hands of government only.

64

ANALYSIS OF APPLICATION OF FUNDS OF APTDCL

Now, it is proposed to examine application of funds of APTDCL by expressing each

application as percentage of total application of funds.

The following table -- III represents a relevant data of application of funds of

APTDCL from 2004-05 to 2008-09.

TABLE - III : APPLICATION OF FUNDS OF APTDCL

Application of funds

2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Fixed assets gross block

824504567 993219092 824504567 993219092 1207304156

Less Depreciation 234439525 355974432 234439525 355974432 466686967

Net Block 590065042 637244660 590065042 637244660 740617189

Capital work in progress 155223789 398294338 155223789 398294338 288704250

Current assets loan and advance

144101483 190253916 144101483 190253916 182102473

Less Current liabilities provisions 207578269 273301473 207578269 273301473 243876648

Net current assets (63476786) (83047558) (63476786) (83047558) (61774175)

Miscellaneous Expenditure 4839890 2036739 4839890 2036739 243579

Profit & loss account-dr.balance

39433093 30924531 39433093 30924531 -

Total 726085028 985452711 726085028 985452711 967790843

65

THE ANALYSIS OF THE DATA OF THE TABLE BRINGS OUT

THE FOLLOWING INFORMATION

Total fixed assets is increasing APTDCL is progressive increases. The amount of fixed

assets move between 28.22% to 81.26%. It is an intimation A.P. Corporation is

purchasing. It has more invested in purchasing of fixed assets.

In current assets it show the lack of less balances of cash 35.28 to 18.43 it has

having less cash balance. Corporation is not able to get working capital with this two

financial & C.A. we can say that they have much more invested in fixed assets and

capital work in progress in almost all the years of the study. The percentage of fixed

assets varied from 28.22% in the year 2004-2005 to 81.26% in the year 2006-07 and is

a decrease of 64.66% in the year 2008-2009.

The statement of changes in working capital is 22.45% in the year 2004-05 to

40.42 in the year 2006-07. There is relatively decrease in the profit and loss A/c in the

2006-07 when compared with the year 2004-05 and in the current assets it is almost

declaiming from year to year. Miscellaneous expenditure is increasing from 2004-05

where 0.095% to 2006-07 it has 0.206%

0.095% in the year 2004-05 to 0.206% in the year 2008-09

66

CONCLUSIONS

By analyzing the balance sheet of APTDCL it shows that the grants and

secured loans have been raised for acquiring more fixed assets for expanding

their operations in the Andhra Pradesh.

The grants of APTDCL in the year 2004-05 was 459685452 and it increased

UPTO 634082839 in the year 2008-09.

Fixed assets are increased by 824504567 in the year 2007-08 it has reached

to 1207304156. As compared to last year this has been possible by decreasing

in current assets and share capital.

It is a step in the rigid direction because expenses of the business is possible

with increase in fixed assets. Unsecured loans is on lower side so there is a

still force for agreeing for loan for there future expenses for profit activities

can be carriable. It indicates that the amount of loans are not properly

utilized in the year 2004-05 to 2008-09 and current assets are becoming

negative balances from 2004- 05 to 2008-09.

To conclusion corporation is expanding because investment in fixed assets has

increased 81.26% in the year 2006-07 and because of grants are increased it

has expanding their operations.

67

SUGGESTIONS

Since, working capital has been utilized to buy fixed assets which

may lead to working capital shortage and difficulties in paying current

liabilities in the near future.

The company has to control its expenses in the case of its petroleum and

lubricants.

In order to attract he tourist make sure of the best and good advertisement.

Being this corporation is a semi-govt, the government has to provide the

assistance in its development.

68

BIBLIOGRAPHY

Book Title Author Name Publishers

Accounting Theory and S.P. Jain & K.L. Kalyani Publishers

Management Accounting Narang

Financial Management Prasanna Chandra Tata MC Graw Hill

Theory and Practice

Accounting and Finance K. Rajeshwara & Jai Bharat

G. Prasad Publications

Financial Management IM Pandey VIKAS Publishing

69